Embed Size (px)

Citation preview

Chapter 7Chapter 7

Accounting Accounting Information Information SystemsSystems

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

7-2

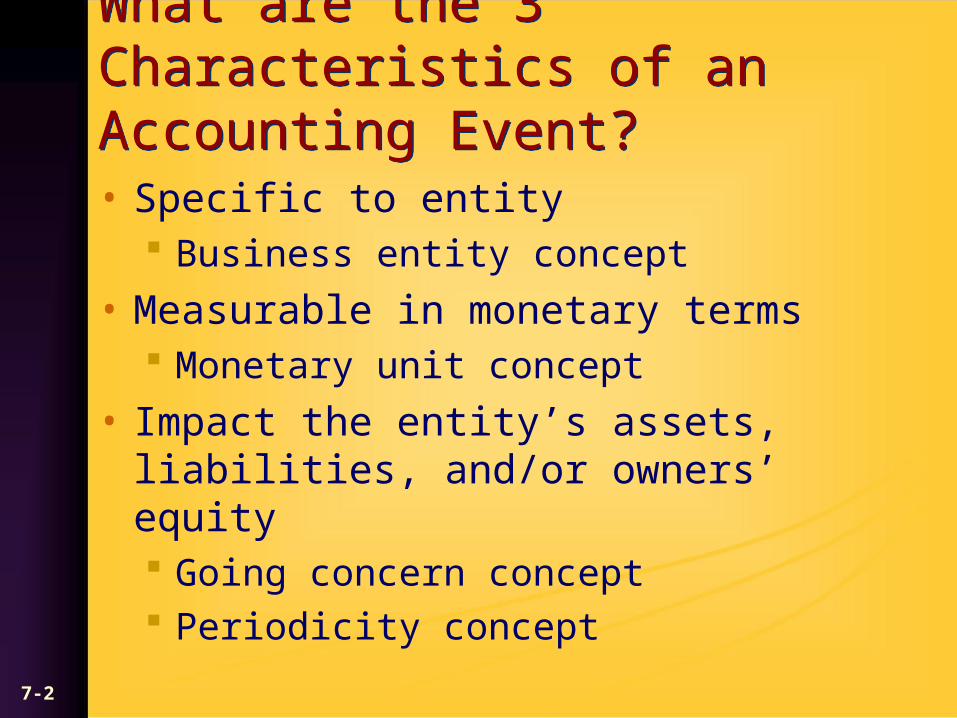

What are the 3 Characteristics of an Accounting Event?What are the 3 Characteristics of an Accounting Event?

• Specific to entity Business entity concept

• Measurable in monetary terms Monetary unit concept

• Impact the entity’s assets, liabilities, and/or owners’ equity Going concern concept Periodicity concept

7-3

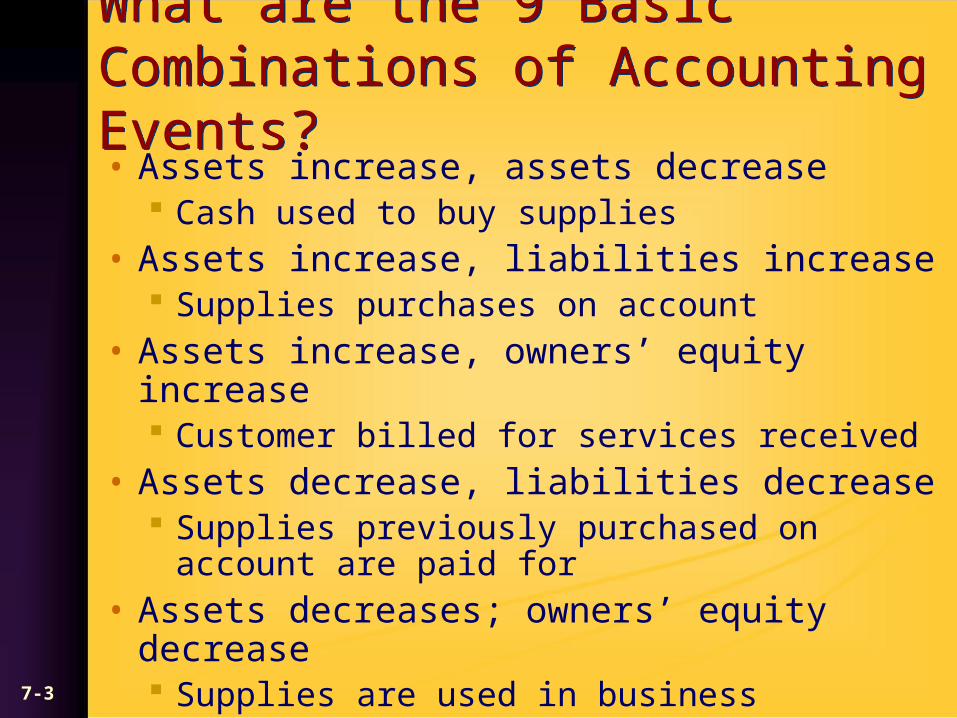

What are the 9 Basic Combinations of Accounting Events?What are the 9 Basic Combinations of Accounting Events?• Assets increase, assets decrease

Cash used to buy supplies• Assets increase, liabilities increase

Supplies purchases on account• Assets increase, owners’ equity increase

Customer billed for services received• Assets decrease, liabilities decrease

Supplies previously purchased on account are paid for

• Assets decreases; owners’ equity decrease Supplies are used in business

7-4

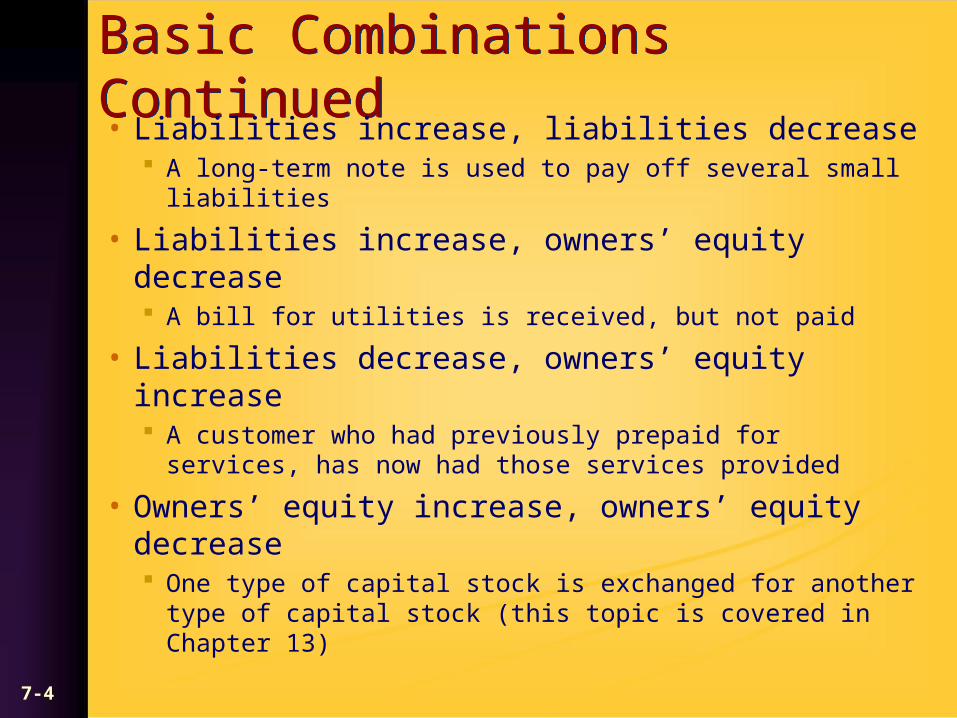

Basic Combinations ContinuedBasic Combinations Continued• Liabilities increase, liabilities decrease

A long-term note is used to pay off several small liabilities

• Liabilities increase, owners’ equity decrease A bill for utilities is received, but not paid

• Liabilities decrease, owners’ equity increase A customer who had previously prepaid for services,

has now had those services provided

• Owners’ equity increase, owners’ equity decrease One type of capital stock is exchanged for another

type of capital stock (this topic is covered in Chapter 13)

7-5

What are Debits and Credits?What are Debits and Credits?

• Debits and credits aren’t good or bad, they’re not happy or sad, rather

• Debit indicates “left” as in the left side of an account

• Credit indicates “right” as in the right side of an account

So What is an Account?So What is an Account?

• A place in the accounting records where the information pertaining to a particular asset, liability, or owners’ equity is maintained.

• An account has a DEBIT side and a CREDIT side and is often represented by a T account:

7-6

Debit Credit

The accounting equation ruleThe accounting equation rule

• Recall: Assets = Liabilities + Owners’ equity

• Then, Assets are on the left; assets increase on the LEFT side of the account—with a DEBIT

• Therefore, Liabilities and Owners’ equity which are on the right; increase on the RIGHT side of the account—with a CREDIT

7-7

7-8

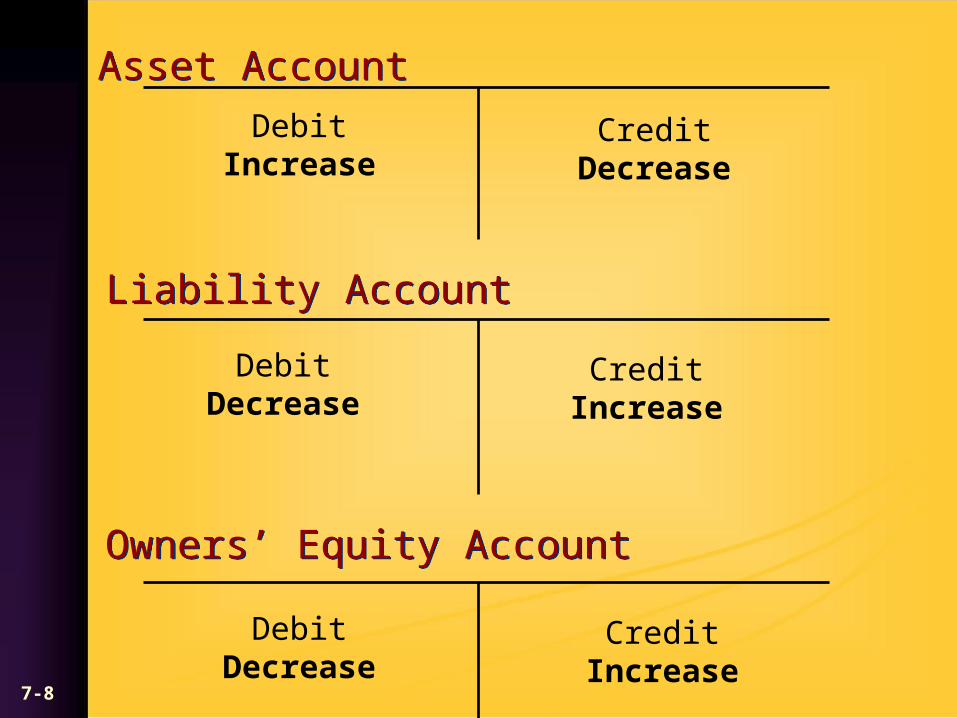

Asset AccountAsset Account

DebitIncrease

CreditDecrease

Liability AccountLiability Account

DebitDecrease

CreditIncrease

Owners’ Equity AccountOwners’ Equity Account

DebitDecrease

CreditIncrease

Revenue and Expense RulesRevenue and Expense Rules• Revenues INCREASE net income; net income

belongs to owners and INCREASES owners’ equity; therefore, revenues increase on the CREDIT side.

• Expenses DECREASE net income; net income belongs to owners and INCREASES owners’ equity; therefore, since an expense reduces net income, it will increase on the DEBIT side.

7-9

DebitDecrease

CreditIncrease

DebitIncrease

CreditDecrease

7-10

How do Debits and Credits Apply to the first 8 Basic Combinations?How do Debits and Credits Apply to the first 8 Basic Combinations?

• Assets increase, assets decrease DR asset account; CR asset account

• Assets increase, liabilities increase DR asset account; CR liability account

• Assets increase, owners’ equity increase DR asset account; CR owners’ equity

account

• Assets decrease, liabilities decrease DR liability account; CR asset account

7-11

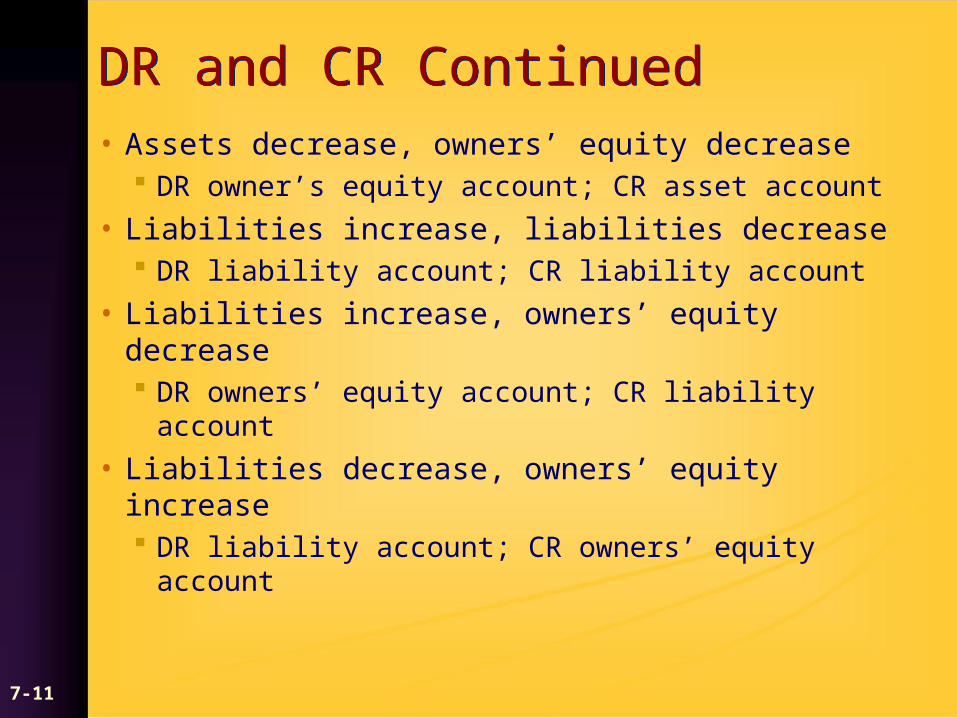

DR and CR ContinuedDR and CR Continued

• Assets decrease, owners’ equity decrease DR owner’s equity account; CR asset account

• Liabilities increase, liabilities decrease DR liability account; CR liability account

• Liabilities increase, owners’ equity decrease DR owners’ equity account; CR liability account

• Liabilities decrease, owners’ equity increase DR liability account; CR owners’ equity account

7-12

What are Adjusting Entries?What are Adjusting Entries?

• Entries made to reflect internal events

• Revenue accrual Increase revenue, increase asset

• Revenue deferral Increase revenue, decrease liability

• Expense accrual Increase expense, increase liability

• Expense deferral Increase expense, decrease asset

7-13

What are Closing Entries?What are Closing Entries?

• Zero-out income statement accounts

• Transfer the balances to owners’ equity Corporation—retained earnings

• Debit each revenue account for the amount of its balance and credit retained earnings

• Credit each expense account for the amount of its balance and debit retained earnings

• The change in retained earnings is the net income (loss) for the period

7-14

What are the Advantages of Computer-Based Transaction Systems?What are the Advantages of Computer-Based Transaction Systems?• Transactions posted quickly—no journalizing

required

• Detailed listing can be printed at any time

• Internal controls

• A wide variety of reports can be generated

What are the Advantages of Database Systems?What are the Advantages of Database Systems?• Business events can be recognized in addition to

accounting events• Reduced operating inefficiencies• Elimination of redundant data throughout the

company

7-15

What is a Business Event?What is a Business Event?

• Any activity that the company wishes to plan and evaluate.

• Includes accounting events and other events

• Which of the Following is a Business, but not an Accounting Event? Determine the need for inventory Receive inventory Pay for inventory Sell inventory

• Answer: determine the need for inventory