Embed Size (px)

Citation preview

Chapter 6

SECURITIZATION, SHADOW-BANKING AND THE VALUE OF FINANCIAL

INNOVATION

Factors that contributed to the financial crisis

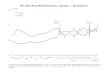

Growth in foreign capitalSurplus balance of payment and increase in savings 1

Low interest ratesLow long term interest rates to stimulate investment 2

Promotion of homeownership by the federal government

Homeownership - investment, source of property tax and stability 3

Deregulatory measures taken by Congress and SEC

Placed some derivatives and firms beyond effective regulation 4

Growth of securitzation and subprime mortgages

Securitization provided capital for on lending and “reduced risks” 5

Overview of the crisis

• Low interest rates as a result of the Federal Reserve Board efforts to keep interest rates low to stimulate investment

• MBS a solution for investors looking for higher interest rates and banks to release funds for on lending

• Sub prime loans developed without a proper regulatory environment

• Housing bubble burst made it difficult for borrowers to repay loans

Low interest rates

Demand for higher rates

Financial innovations

Sub prime loans

Housing bubble burst

Securitization

• Securitization: the process of creating securities backed by pools of loans with similar characteristics

• Mortgage-backed securities (MBS)– the most prevalent type of securitized asset– more liquid than the underlying loans– MBS backed by subprime mortgages played

important role in the recent economic crisis

The securitization process

• Borrowers take out loans from commercial banks or finance companies.

• The lenders sell their loans to the securitizer, a large financial institution.

• The securitizer gathers a large pool of similar loans, e.g. $100 million of subprime mortgages.

• The securitizer issues new securities that entitle their owners to a share of the payments the original borrowers make on the underlying loans.

• The securities are bought by financial institutions and traded in secondary markets.

Fannie and Freddie

• Federal National Mortgage Association (FNMA, or Fannie Mae), created in 1938

• Federal Home Loan Corporation (Freddie Mac), created in 1970

• both created to increase supply of mortgage loans, help more people achieve “the American dream”

• Fannie and Freddie are the largest securitizers of mortgages

Fannie and Freddie

• Fannie and Freddie are government sponsored enterprises (GSEs), private corporations linked to the government.– Perceived to have implicit govt backing, therefore can

borrow funds at lower cost than other financial institutions can.

• Suffered huge losses on subprime mortgages in 2007-2008.

• To prevent bankruptcy, federal government put Fannie and Freddie under conservatorship.

Benefits of securitization

• Homebuyers/borrowers– Easier to get loans, lower interest rates

because securitization increases the pool of funds available for making home loans

• Banks– profit from selling loans for more than they lent, can

use proceeds to make more loans– achieve geographic diversification: sell loans made in

their community, buy MBS backed by loans throughout the country, thus protected from local shocks

Benefits of securitization

• Securitizers– Earn income from securitizing mortgages and

selling MBS• Buyers of MBS

– get assets that are (usually) safe and very liquid

The subprime mortgage fiasco• The housing bubble. House prices…

– rose 71% during 2002-2006– fell 33% during 2006-2009

• Risky lending– Subprime lenders lowered standards regarding

borrowers income, credit– Zero down payment loans, adjustable rate mortgages

with low initial “teaser rates”– Lenders resold loans, so less concerned with default

risk

The subprime mortgage fiasco• The crash

– Falling house prices put many homeowners “underwater” – market value of house less than amount owed on mortgage

– Homeowners couldn’t afford payments, couldn’t borrow more

– Rising delinquencies and foreclosures

12CHAPTER 18 Banking

The subprime mortgage fiasco• Consequences: huge losses for

– Subprime lenders – investment banks and other institutions

holding MBS• Contributed to the worst recession in

decades

The financial innovation led to the formation of non regulated intermediaries acting as banks• Why it is important to define functions, instead of

relying on legal/formal definitions• Tucker’s definition of shadow banking system:

instruments, structures, firms or markets which, alone or in combination, and to a greater or lesser extent, replicate the core features of commercial banks: liquidity services, maturity mismatch and leverage

Definition of Financial innovation

”Financial innovation is the act of creating and then popularizing new financial instruments, as well as new financial technologies, institutions and markets. The innovations are sometimes divided into product or process variants, with product innovations exemplified by new derivative contracts, new corporate securities or new forms of pooled investment products, and process improvements typified byn ew means of distributing securities, processing transactions or pricing transactions. In practice, even this innocuous differentiation is not clear, as process and product innovations are often linked.

Innovation includes the acts of invention and diffusion, although in point of fact these two are related as most financial innovations are evolutionary adaptations of prior products.”

By Source: Lerner, J. & Tufano, P. (2011) The Consequences of Financial Innovation: A Counterfactual Research Agenda. Annual Review of Financial Economics, 3, pp. 6

Shadow Banking system definition

• Buiter definition (2008) : • “The shadow banking sector consists of the many

highly leveraged non-deposit-taking institutions that lend long and illiquid and borrow short in markets that are liquid during normal or orderly times but can become very illiquid when markets become disorderly.

• They are functionally very similar to banks but :• -are barely supervised or regulated. • -hold very little capital, • -are not subject to any meaningful prudential

requirements as regards liquidity, leverage or any other feature of their assets and liabilities.”

Financial Innovation

• Traditional “Old-School” Make & Hold Business Model:

Borrowers SaversCommercial Banks

Cash Cash

Mortgages Bank Deposits

Borrowers

Savers

Investment Banks

Cash

Fixed Income Funds (NAV)

Cash

Mort-gages

CB’sMoney Manag-

ers

CashCash

Pools of Mortgages

SIVs & CDOs

“Elongated” or “New-School” Originate & Distribute Model:

A Basic Balance Sheet with Leverage

• Leverage Factor = Assets / Equity

19

Assets

Debt

Equity

Profit / Loss on A

sset

Priority of R

e-Paym

ent

Mortgage Gives Homeowners 5x’s Leveraged Returns

• Return on Equity = 25%• [(Return on Assets - Interest Expense) / Equity]

= 25%• [($9.00 - $4.00) / $20] = 25%

20

House

$100

Gain on House =

9%

Mortgage Debt $80

Interest Rate =

5%

Equity

$20

Mortgage Securitization Creates “MBS” and Leverage

21

Pool of Mortgage Debts

Equity

D

D

D

D

D

D

D

D

D

D

D

Super Senior

AAA MBS

BB MBS

B MBS

BBB MBS

AA MBS

A MBS

Loss Position

Cre

dit

Ris

k

Yie

ld

FirstLoss

HighRisk

HighYield

LastLoss

LowRisk

LowYield

HOME OWNERS

AAA MBS

Collateralized Debt Obligation (“CDO”)– More Leverage

22

Pool of AA, A, BBB MBS

Equity

MBS

Super-Senior

AAA CDO

AAA CDO

B CDO

Loss Position

Cre

dit

Ris

k

Yie

ld

FirstLoss

HighRisk

HighYield

LastLoss

LowRisk

LowYield

WALL ST BANKS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

MBS

Credit Default Swaps – Infinite Leverage

• Like an insurance contract that pays in the event of default.• FASB requires mark-to-market valuation.• Collateral Call - Protection Buyers can call for partial payment if

default event is likely. Determined by mark-to-market value.

23

Does not usually own reference asset

Going “long”

Benefits when reference asset price INCREASES, max at Par

Tends to own reference asset

Hedging or going “short”

Benefits when reference asset price DECREASES

Protection SellerProtection Buyer

Payment upon Default of Reference Asset

Premium Payments

Reference Asset can be a MBS, CDO, Bond, or Loan

Sub-prime Mortgage 20X’s Leverage

24

House

$100

Mortgage Debt

$95

Equity $5

Homeowner 20X’s

Increasing Leverage

Pooled into MBS – 30X’s Leverage

25

House

$100

Mortgage Debt

$95

Equity $5

Mortgage Debt

$95

MBS

$91.8

Equity $3.2

Homeowner 20X’s

Increasing Leverage

Mort. Securitiz 30X’s

Pooled into CDO – 50X’s Leverage

26

House

$100

Mortgage Debt

$95

Equity $5

MBS

$91.8

CDO

$90.0

Equity $1.8

Mortgage Debt

$95

MBS

$91.8

Equity $3.2

Homeowner 20X’s

Increasing Leverage

Mort. Securitiz 30X’s

CDO Structure 50X’s

CDS on CDO – Infinite Leverage

27

House

$100

Mortgage Debt

$95

Equity $5

MBS

$91.8

CDO

$90.0

Equity $1.8

CDO

$90.0

CDS on CDO

$90.0

Equity $0

Mortgage Debt

$95

MBS

$91.8

Equity $3.2

Homeowner 20X’s

Increasing Leverage

Mort. Securitiz 30X’s

CDO Structure 50X’s

Credit Default Swap ∞

In-Class Exercise: Compare and Contrast the Make & Hold and Originate &

Distribute Models

• You can consider the two types of FI models and their impact on the:

• Speed / velocity of lending• Availability of credit in the economy• Bank’s credit culture• Executive compensation• Role of regulators• Profitability, Riskiness, & Growth of FIs• Future of commercial banking

• Discuss these issues in small groups and report back to the class. 28

Financial Innovation

• forms of financial innovation which are of concern to the prudential regulator are those which have a potential to generate large negative externalities, producing not merely redistribution of an unchanged economic cake but harmful instability in overall patterns of economic growth.

Essential Readings

1.SECURITISATION, SHADOW BANKING AND THE VALUE OF FINA NCIAL INNOVATION by adair turner ,19TH APRIL 2012.

2. Economics of Money ,Banking and Financial Markets, 9th Edn, Chapter 9 by Frederic.S.Mishkin

3. Financial Innovation and the Global Crisis from International Journal of Business and Management by Manuel Sánchez, 11,November 2010.

![Securitization of Loan Oracle FLEXCUBE Universal Banking · Securitization of Loan Oracle FLEXCUBE Universal Banking Release 12.0 [May] [2012] Oracle Part Number E51527-01](https://img.pdfslide.us/doc/110x75/5b2b77d67f8b9abe2a8b4864/securitization-of-loan-oracle-flexcube-universal-banking-securitization-of-loan.jpg)