Embed Size (px)

Citation preview

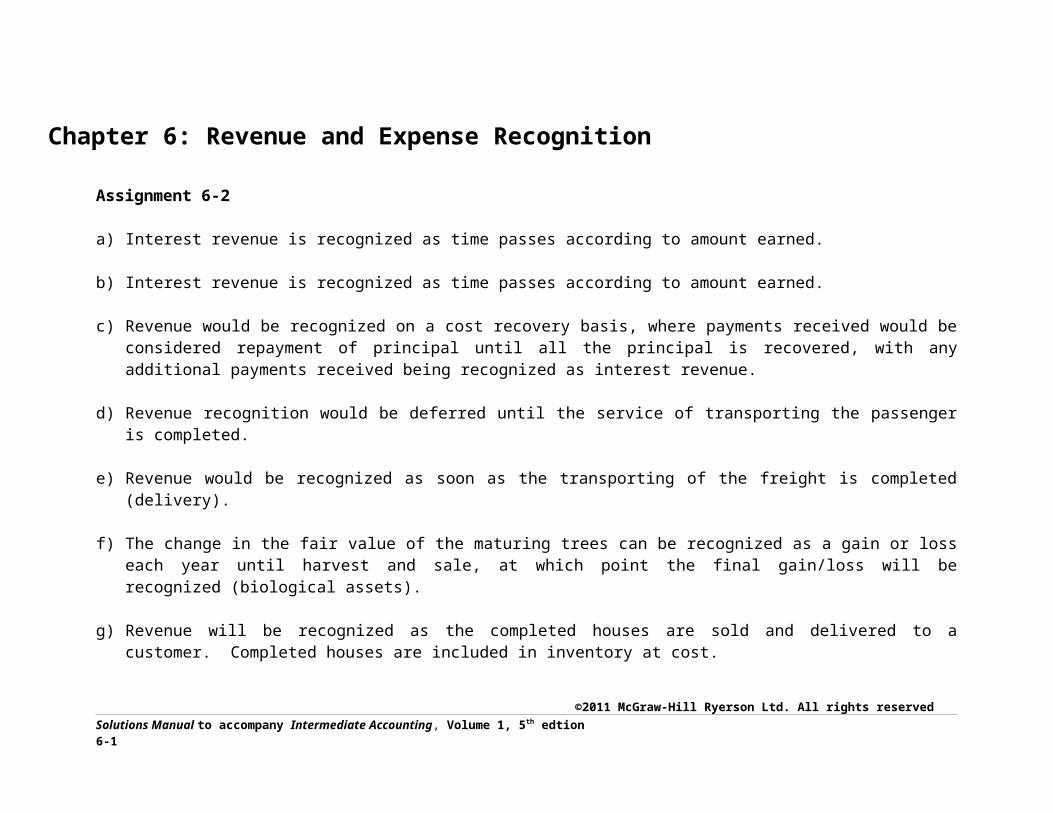

Chapter 6: Revenue and Expense Recognition

Assignment 6-2

a) Interest revenue is recognized as time passes according to amount earned.

b) Interest revenue is recognized as time passes according to amount earned.

c) Revenue would be recognized on a cost recovery basis, where payments received would be considered repayment of principal until all the principal is recovered, with any additional payments received being recognized as interest revenue.

d) Revenue recognition would be deferred until the service of transporting the passenger is completed.

e) Revenue would be recognized as soon as the transporting of the freight is completed (delivery).

f) The change in the fair value of the maturing trees can be recognized as a gain or loss each year until harvest and sale, at which point the final gain/loss will be recognized (biological assets).

g) Revenue will be recognized as the completed houses are sold and delivered to a customer. Completed houses are included in inventory at cost.

h) Revenue could and likely would be recognized on a percentage-of-completion basis, without regard to when payment is received or when the completed houses are delivered to the purchaser.

i) Either the instalment sales method or the cost recovery method would be used to recognize revenue. In this case the more usual treatment is the instalment sales method unless collectibility is in doubt.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-1

j) Revenue would be recognized as it is earned, which in this case will be with the passage of time, i.e., straight-line over 24 months. The large initial payment will be accounted for as a deferred revenue.

k) Because it is not possible to reliably determine the costs for completion and the potential gain or loss on this project, revenue should be recognized only to the extent of costs incurred and expensed.

l) It would be permissible to recognize revenue at fair market value as the silver is produced. Subsequent increases and decreases in market value would be recognized as gains and losses. However, this is permitted under IFRS only if this practice is widely accepted in the industry. If this method is not generally accepted in the industry, revenue would be recognized only when the silver is sold.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-2

Assignment 6-7 (WEB)

Requirement 1(b) Revenue Recognition on

Date (a) Delivery Cash Receipt (c) Preparation 18 July Inventory 456,00

0Inventory 456,00

0Inventory 456,00

0Cash 456,00

0Cash 456,00

0Cash 456,00

024 August Inventory 60,000 Inventory 60,000 Inventory 60,000

Cash 60,000 Cash 60,000 CashInventoryCOS

Sales

196,000

516,000

60,000

712,000

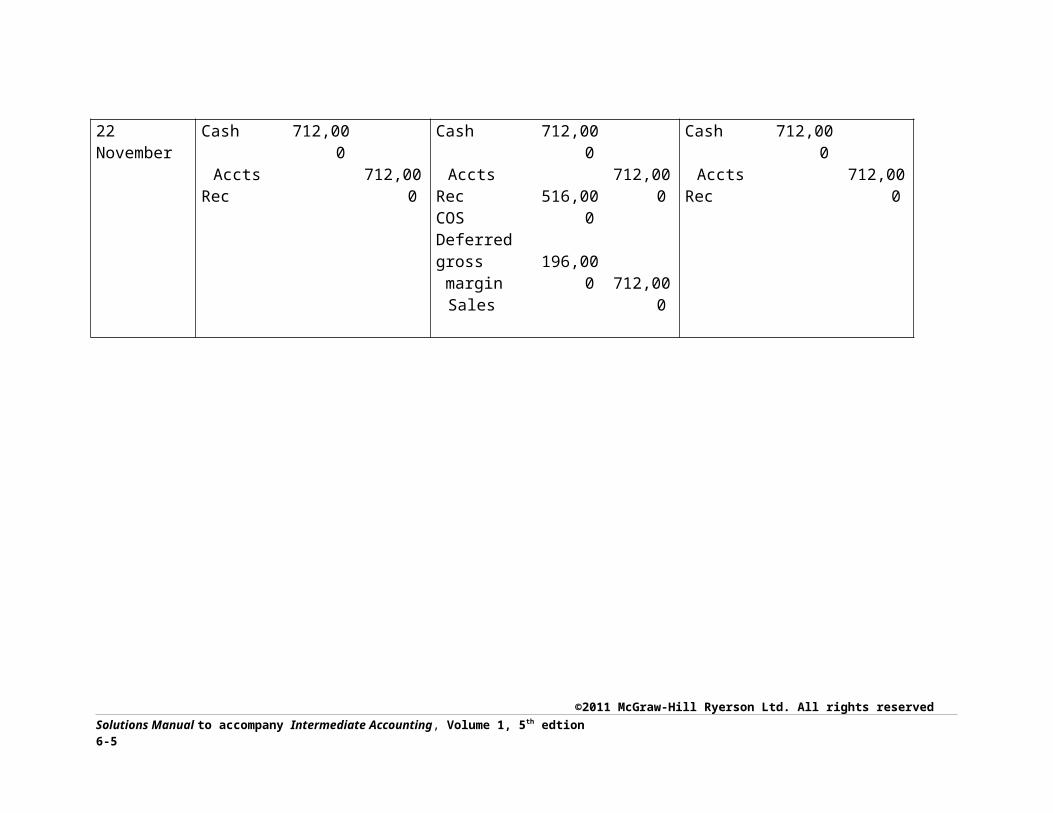

10 September

Accts Rec 712,000

Accts Rec 712,000

Accts Rec 712,000

Sales 712,000

InventoryDeferred gross margin

516,000

196,000

Inventory712,00

0

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-3

COS

Inventory

516,000 516,00

0

22 November

Cash 712,000

Cash 712,000

Cash 712,000

Accts Rec

712,000

Accts RecCOSDeferred gross margin

Sales

516,000

196,000

712,000

712,000

Accts Rec

712,000

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-4

Requirement 2

Delivery is the normal revenue recognition point, based on the presumption that the risks and rewards of ownership pass on this date and that the sales amount is realizable. Revenue recognition on cash receipt is appropriate when the account receivable is considered so doubtful that it fails the realizability test; in these circumstances, revenue cannot be recognized prior to collection. Revenue recognition on production is appropriate only for commodities with stable sales prices and markets where the sales effort and costs are trivial but is not permitted under IFRS except for biological assets and agricultural produce.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion

6-5

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition 6

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition 7

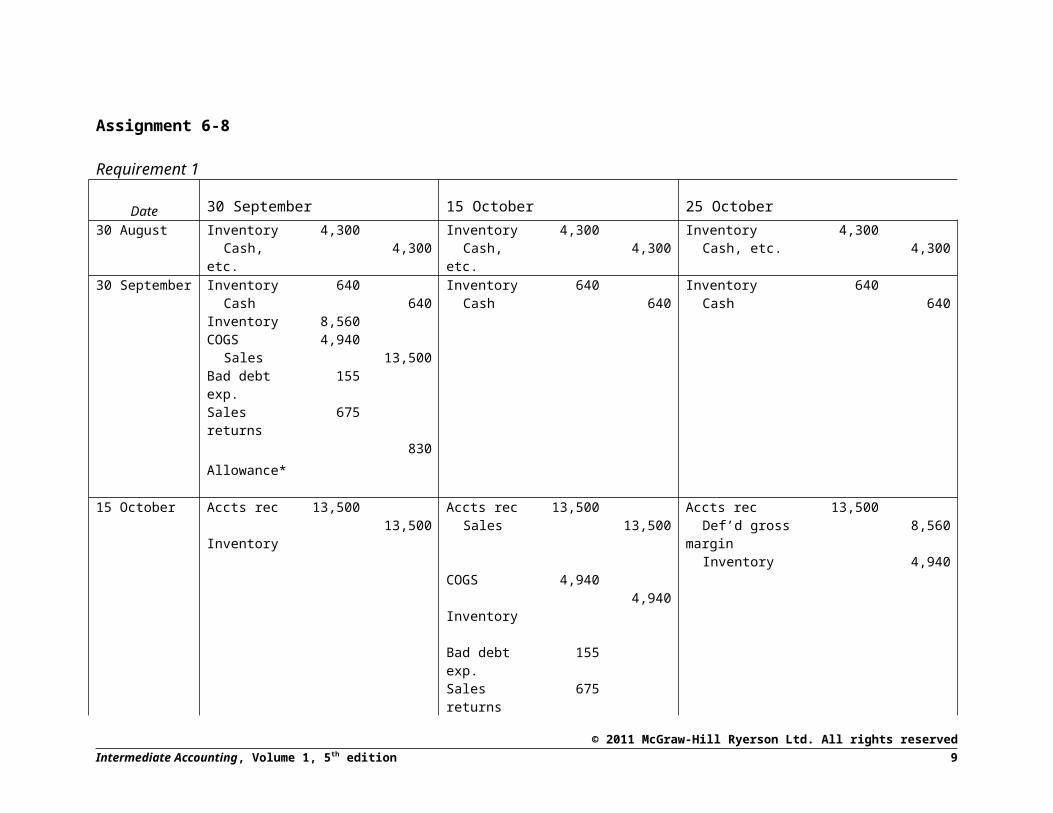

Assignment 6-8

Requirement 1

Date 30 September 15 October 25 October30 August Inventory 4,300 Inventory 4,300 Inventory 4,300

Cash, etc.

4,300 Cash, etc.

4,300 Cash, etc. 4,300

30 September Inventory 640 Inventory 640 Inventory 640Cash 640 Cash 640 Cash 640

Inventory 8,560COGS 4,940

Sales 13,500Bad debt exp.

155

Sales returns

675

Allowance*830

15 October Accts rec 13,500 Accts rec 13,500 Accts rec 13,500Inventory 13,500 Sales 13,500 Def’d gross

margin8,560

Inventory 4,940COGS 4,940

Inventory 4,940

Bad debt exp.

155

Sales returns

675

Allowance830

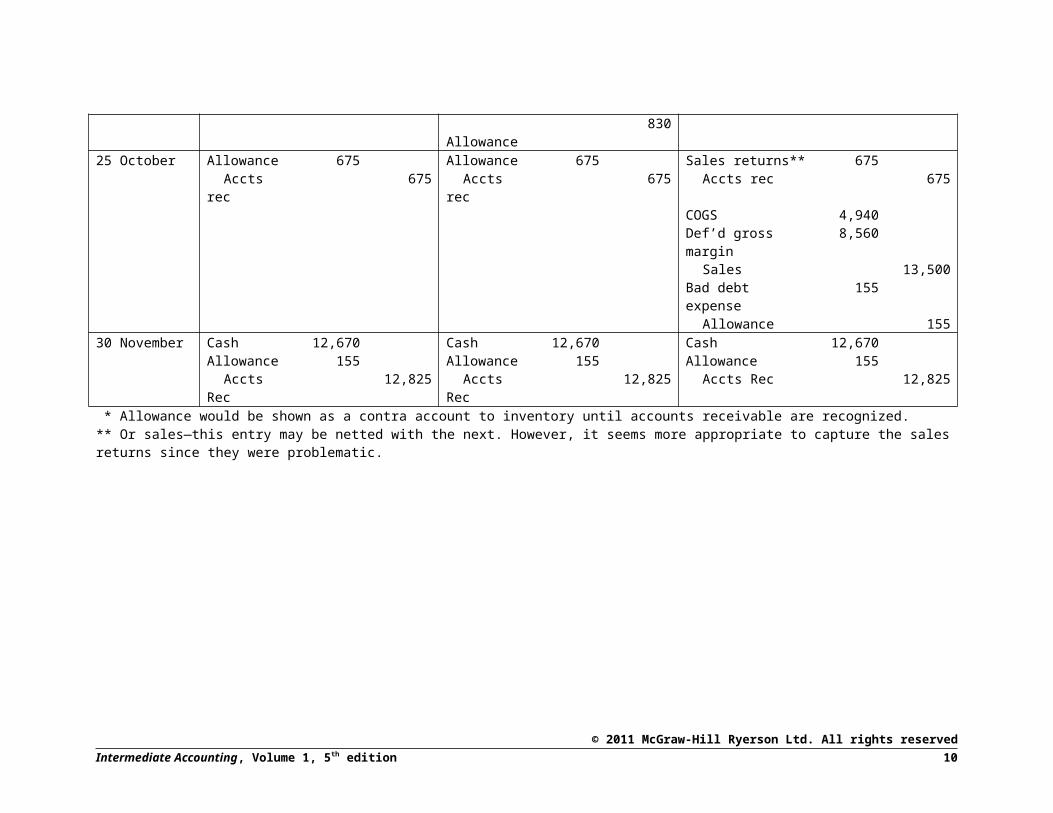

25 October Allowance 675 Allowance 675 Sales returns** 675Accts rec 675 Accts rec 675 Accts rec 675

COGS 4,940Def’d gross 8,560

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition 8

marginSales 13,500

Bad debt expense 155Allowance 155

30 November Cash 12,670 Cash 12,670 Cash 12,670Allowance 155 Allowance 155 Allowance 155

Accts Rec

12,825 Accts Rec

12,825 Accts Rec 12,825

* Allowance would be shown as a contra account to inventory until accounts receivable are recognized.** Or sales—this entry may be netted with the next. However, it seems more appropriate to capture the sales returns since they were problematic.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition 9

Requirement 2

At each critical event, net assets (equity) is affected by the sales and expense accounts. Prior to that point, and after that point, entries affect the distribution within net assets but not the total net amount.

Requirement 3

a. Recognition at production is appropriate for a commodity with an organized market, where sale is trivial, the producer cannot affect price, and also if all costs are known and can be accrued. This point is acceptable under IFRS, but only for biological assets and agricultural produce, and for minerals and mineral products, but then only if this valuation basis is widely used within the industry. Canadian ASPE accepts this revenue recognition point only for biological assets and agricultural produce.

b. Delivery is an appropriate critical event most of the time, as risks and rewards pass to the customer. However, sales amounts have to be realizable and all costs estimable and accrued on this date.

c. Revenue recognition after the right of return has passed is appropriate if returns cannot be predicted.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-10

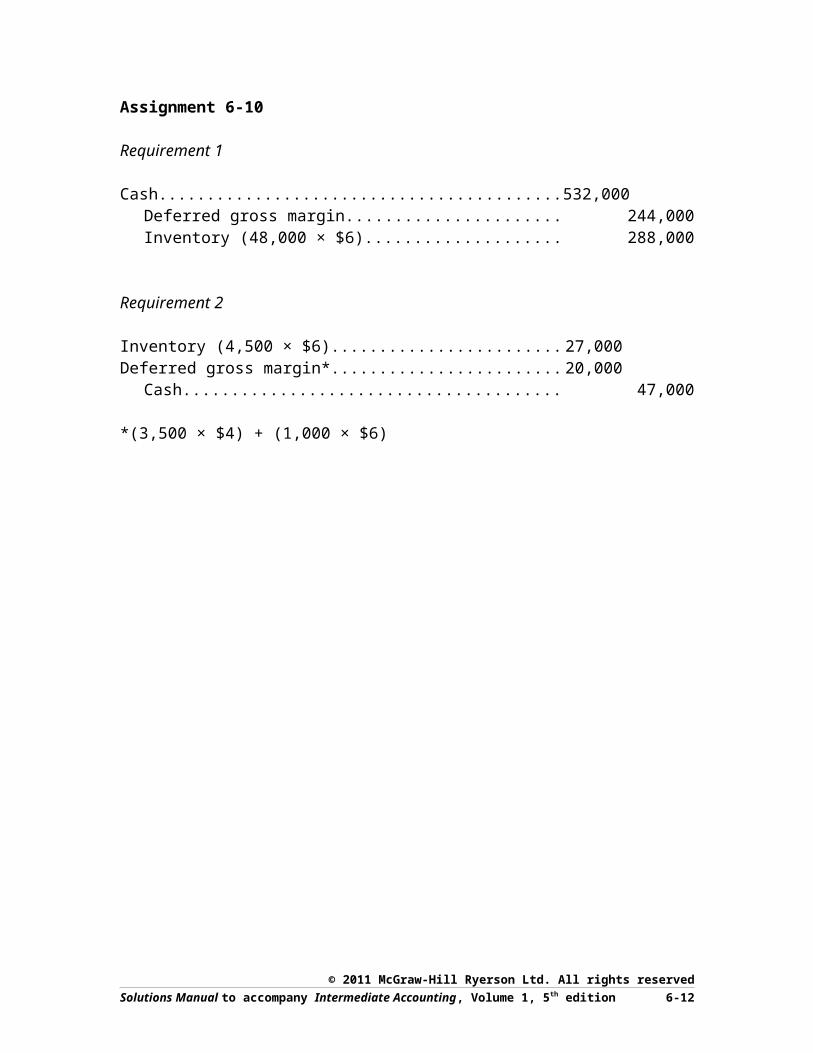

Assignment 6-10

Requirement 1

Cash...............................................................................532,000Deferred gross margin............................................... 244,000Inventory (48,000 × $6)............................................ 288,000

Requirement 2

Inventory (4,500 × $6)................................................... 27,000Deferred gross margin*.................................................. 20,000

Cash........................................................................... 47,000

*(3,500 × $4) + (1,000 × $6)

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-11

Requirement 3

Monthof Sale

UnitsSold

SalesPrice

MonthlySales

Gross UnitsROR

Expired *

Total Units

Returned

Net UnitsROR Expired

†

ROR ExpiredSales

Amount §

September

10,000 $10 $100,000

4,000 2,500 1,500 $15,000

October 12,000 10 120,000 3,600 1,000 2,600 26,000November

15,000 12 180,000 3,000 1,000 2,000 24,000

December

11,000 12 132,00 0

1,10 0

0 1,100 13,200

Totals 48,000 $532,000

11,700

4,500 7,200 $78,200

* Gross number of units sold this month, times 10% times number of months since sale. For example, at 31 December, 20x5, four months have passed since the September sales, thus 4 × 10%, or 40% of the right of return (ROR) has expired; (40% × 10,000 units = 4,000 units).

† Equal to gross units for which ROR expired, less units returned.

§ Equal to Net units for which ROR has expired times sale price per unit for this month sales.

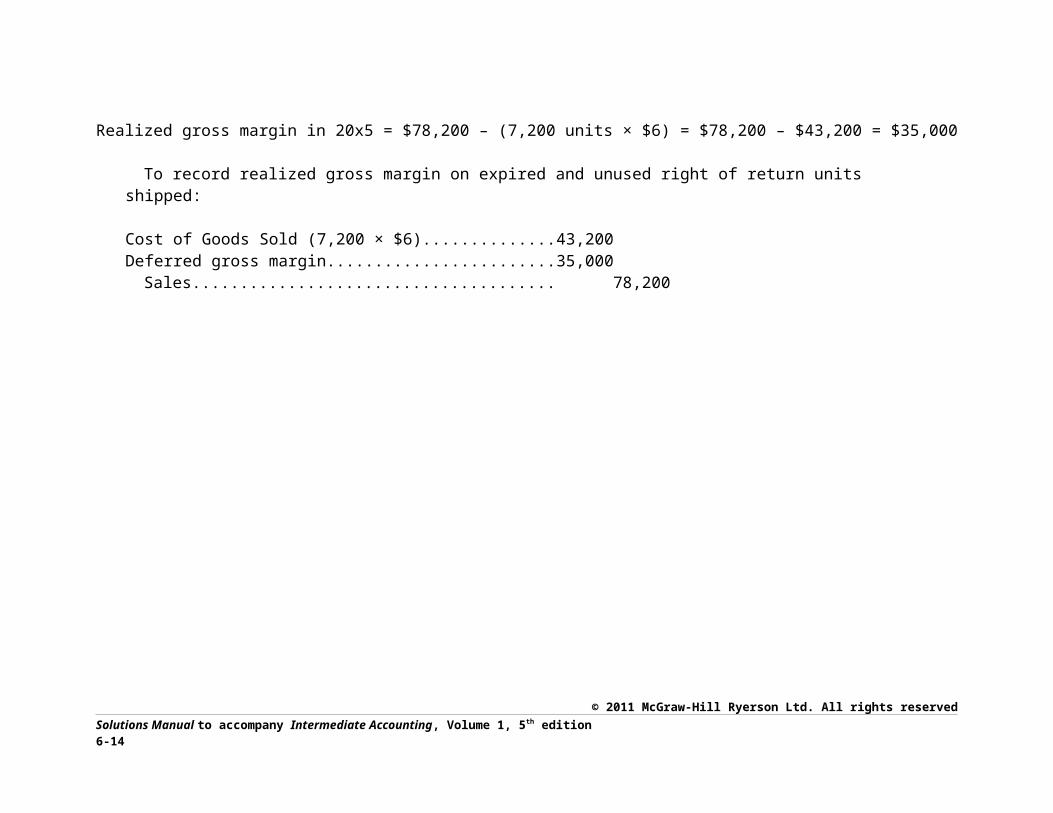

Realized gross margin in 20x5 = $78,200 – (7,200 units × $6) = $78,200 – $43,200 = $35,000

To record realized gross margin on expired and unused right of return unitsshipped:

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-12

Cost of Goods Sold (7,200 × $6)..................................43,200Deferred gross margin.................................................35,000

Sales......................................................................... 78,200

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-13

Requirement 4

Monthof Sale

Units Availablefor Return or

Sale**Units

ReturnedUnits Soldin 20x6 ††

Unit SalePrice

SalesAmount

September

6,000 1,000 5,000 $10 $ 50,000

October 8,400 2,000 6,400 10 64,000November

12,000 2,500 9,500 12 114,000

December

9,900 4,000 5,900 12 70,80 0

9,500 26,800 $298,800

× $6

× $6

Cost of returns $57,000

Costs of units sold $160,800

** Equal to total sold for this month, less those returned or recorded as sold in 20x5 (see Requirement 3).

†† Equal to Units available (column 2) less units returned.

Entry to record returns in 20x6:

Inventory (9,500 units × $6)....................................57,000Deferred gross margin..............................................51,000

Cash...................................................................... 108,000*

*Refund amount on returned units:(1,000 units × $10) + (2,000 units x $10) + ($2,500 units × $12) + (4,000 units × $12) = $108,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

14

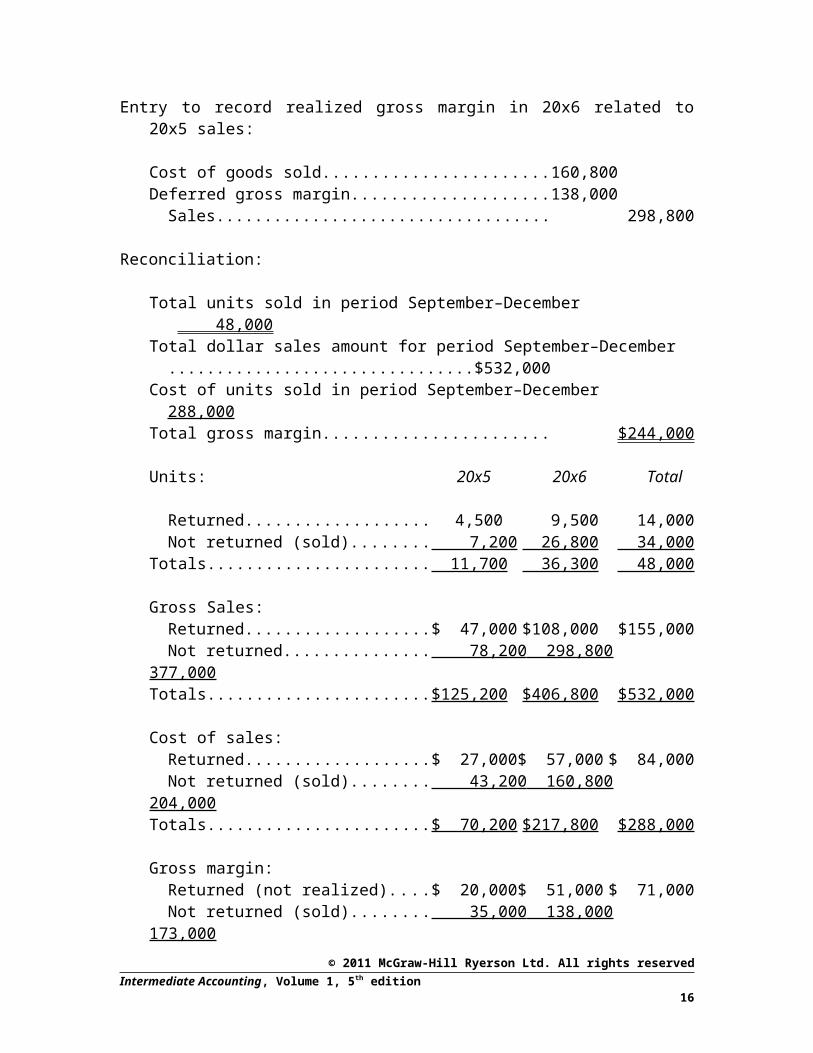

Entry to record realized gross margin in 20x6 related to 20x5 sales:

Cost of goods sold..................................................160,800Deferred gross margin...........................................138,000

Sales................................................................... 298,800

Reconciliation:

Total units sold in period September–December. . . 48,000Total dollar sales amount for period September–December

............................................................$532,000Cost of units sold in period September–December 288,000Total gross margin................................................. $244,000

Units: 20x5 20x6 Total

Returned..................................... 4,500 9,500 14,000Not returned (sold)..................... 7,200 26,800 34,000

Totals.............................................. 11,700 36,300 48,000

Gross Sales:Returned.....................................$ 47,000 $108,000 $155,000Not returned............................... 78,200 298,800 377,000

Totals..............................................$125,200 $406,800 $532,000

Cost of sales:Returned.....................................$ 27,000 $ 57,000 $ 84,000Not returned (sold)..................... 43,200 160,800 204,000

Totals..............................................$ 70,200 $217,800 $288,000

Gross margin:Returned (not realized)...............$ 20,000 $ 51,000 $ 71,000Not returned (sold)..................... 35,000 138,000 173,000

Totals..............................................$ 55,000 $189,000 $244,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

15

Assignment 6-27 a. There is no commercial substance to this transaction, and therefore

the new truck is recorded at the net book value of the old truck plus the cash paid:Truck (new)……………………………………………….

60,000

Accumulated amortization (old)…………………………..

60,000

Truck (old)…………………………………….

100,000

Cash…………………………………………….

20,000

b. This transaction has commercial substance since it enables a new type of operation for Rochester Shipping Company and thereby can be expected to significantly affect the future cash flows of the company. It seems likely that the fair value of the land and building given up is more readily determinable than the fair value of the boat, since it remained unsold for two years and also requires substantial work before it can return to service. Therefore, the boat should be recorded based on the fair value of the land and building.Ferry ……………………………………………………..

1,150,000

Accumulated amortization – building…………………….

210,000

Building………………………………………...

700,000

Land…………………………………………….

300,000

Gain on capital asset disposal………………

360,000

The additional cost for necessary upgrading and maintenance is added to the cost of the boat when the work is done: Ferry…………………………………………………….. 350,000

Cash, accounts payable, etc…………………..

350,000

This brings the recorded ferry value to $1,500,000, which may exceed fair value. Alternatively, the $1,500,000 may be appropriate; it depends on whether the expenditures improve the ferry, or just get it into serviceable shape.The value now assigned to the ferry should be reviewed. It should be reduced if it is more than fair value. If it is reduced, it seems logical

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

16

that the gain on capital asset disposal should be reduced rather than a loss recorded.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

17

Assignment 6-28

Requirement 1

Entry # Effect on net assets1 No change2 No change3 Increase4 Decrease5 Decrease6 No change7 No change8 Decrease9 No change

10 No change

When sales are recognized, inventory is increased. Therefore, the revenue recognition point is production, or inventory acquisition.

Requirement 2

Asset ExplanationInventory Future cash from sale; measured at sales amountPrepaid insurance Future benefits obtained through coverageAccounts receivable Future cash on collectionCash Cash !

Requirement 3

Expense I or D ExplanationCost of goods sold D All expenses are related to normal businessWarranty expense D activities, cause net assets to decline, andCommission expense D have no future benefit past the revenueInsurance expense I recognition point.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

18

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedIntermediate Accounting, Volume 1, 5th edition

19

![2012 FLC100 LED US Druckversion: Sheet.pdf4 FLC121 / FLC131 / FLC141 LED [VN] Floodlight, very narrow beam distribution, symmetric. IP66. Marine-grade die cast aluminum alloy. 5CE](https://img.pdfslide.us/doc/110x75/5e7bd03a68e47a33d44838c0/2012-flc100-led-us-druckversion-sheetpdf-4-flc121-flc131-flc141-led-vn-floodlight.jpg)

![Index [canmedia.mcgrawhill.ca]canmedia.mcgrawhill.ca/college/olcsupport/beechy/6ce/vol2/bee33882... · for exchange rate fluctuations, 788–790 for finance leases, lessee, 1068 for](https://img.pdfslide.us/doc/110x75/5aa0e8767f8b9a89178eb3d2/index-exchange-rate-fluctuations-788790-for-finance-leases-lessee-1068.jpg)