-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

1/34

MARKET STRUCTURE

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

2/34

Objectives

How Firms in Market Operate.

What are different Market Structures.

How price and quantity is determined.

What is profit maximizing output.

Supply curve of a perfectly competitive firm.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

3/34

Market Structures

Market structure is influenced by howa firm behaves:

Pricing ( how they decide the price)

Supply (how much they supply)

Barriers to Entry ( high or low)

Efficiency ( allocative efficiency)

Competition ( high or low)

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

4/34

How do we know about market structure?

To determine structure of anyparticular market, we begin by

askingHow many buyers and sellers are there in the

market? Is each seller offering a homogenous product?

Are there any barriers to entry or exit, or canoutsiders easily

enter and leave this market?

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

5/34

Different Market Structure

Perfect competition.

Imperfect competition

MonopolyOligopoly

Monopolistic

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

6/34

Perfect Competition

Assumptions of Perfectly competitive market

Large Number of Buyers and Sellers

Homogenous Products

Full information

Each firm produces a small fraction of total output of an

industry

Firms are price taker: decision is only about quantity

Free entry and free exit

No government intervention

6

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

7/34

Perfect Competition

Each Firm Has Zero Market Power.

Market Power: the power an individual firm has to

influence the price in the market.

Price is fixed by the market ( not by the firm)

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

8/34

Perfect Competition

Demand curve of the firm andindustry in Perfect Competition?

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

9/34

Perfect Competition

Q

P

Market Supply

pe

p1

Market Demand

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

10/34

Perfect Competition

MarketSupply

MarketDemand

Q

P

Firms Demand Curve

P

P* P*

Qf

Firms demand

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

11/34

Figure 1: The Competitive Industry and Firm

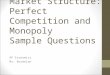

11

quantity

Price perOunce

D

$400

S

Market

DemandCurve Facing

the Firm

$400

Firm

1. The intersection of the market supplyand the market demand

curve

3. The typical firm can sell all itwants at the market price

quantity

Price perOunce

2. determine the equilibriummarket price

4. so it faces a horizontaldemand curve

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

12/34

The Firms Decisions in Perfect Competition

The competitive firm makes two decisions in the short run:1.

Whether to produce or to shut down?

2. If the decision is to produce, what quantity to produce?

A firms long-run decisions are1. Whether to increase or decrease

its plant size?

2. Whether to stay in the industry or leave it?

A perfectly competitive firm chooses the output thatmaximizes

its economic profit.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

13/34

Profit maximization: Twoapproaches

Total revenue and total cost approach.

Marginal revenue and marginal costapproach.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

14/34

Total Revenue and Total costapproach

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

15/34

Minimizing Short-Run Losses

15

$4.003.00

2.50

0 5 10 15

Marginal cost

Average total cost

d= Marginal revenue

= average revenue

Average variable costeLoss

Bushels of wheat per day

Dollarsper

bushel

b) Marginal Cost Equals Marginal Revenue

$40

30

15

0 5 10 15

Total costTotal revenue(= $3 q)

Minimum economicloss = $10

Bushels of wheat per day

(a) Total Cost and Total Revenue

TotaldollarsIn panel (a), Total revenue is lower

because of the lower priceTotal revenue now lies below thetotal

cost curve at all output rates. The

vertical distance between the twocurves measures the loss at

each rateof outputThe vertical distance is minimized atan output

rate of 10 bushels where theloss is $10 per daySame result in panel

bFirm will produce rather than shut

down if MR= MCat a rate of outputwhere price equals or exceeds

averagevariable costAt point e, output is 10 bushels perday and the

price of $3 exceeds theaverage variable cost of $2.50 Totaleconomic

loss shown by shaded area

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

16/34

Marginal Revenue and Marginal cost

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

17/34

Short run profits and losses

Maximum profit is not always a positive economic profit.

To determine whether a firm is earning an economic

profit or incurring an economic loss, we compare thefirms

average total cost, ATC, at the profit-

maximizing output with the market price.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

18/34

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

19/34

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

20/34

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

21/34

Short run supply curve

A perfectly competitive firms short-run supply curveshows how

the firms profit-maximizing output variesas the market price

varies, other things remaining thesame.

Because the firm produces the output at which marginalcost

equals marginal revenue, and because marginalrevenue equals price,

the firms supply curve is linkedto its marginal cost curve.

But there is a price below which the firm producesnothing and

shuts down temporarily.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

22/34

Short run supply curve

The shutdown point is the output and price atwhich the firm just

covers its total variable cost.

This point is where average variable cost is at

its minimum. It is also the point at which themarginal cost

curve crosses the averagevariable cost curve.

If the price exceeds minimum average variablecost, the firm

produces the quantity at whichmarginal cost equals price. Price

exceedsaverage variable cost, and the firm covers all itsvariable

cost and at least part of its fixed cost.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

23/34

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

24/34

Short run supply curve of the firm

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

25/34

Summary of Short-Run Output Decisions

25

q

1

0

Quantity per period

d1

A C

A VC

4

1

Marginal cost

p1

Shutdownpoint

2

q

2

p2 d

2

q

3

3p3 d

3

Break-evenpoint

q

4

p4 d

4

q

5

p5 5 d

5

Dollarsperunit

At p1, the firm will shutdown rather thanoperate because price

isbelow average variablecost at all output rates.If the price is

p3, thefirm will produce q3 to

minimize its loss while atp4, the firm will produceq4 to earn

just a normalprofit: break-even pointAt p2, the firm isindifferent:

shutdownpoint

If the price rises to p5,the firm will earn a short-run economic

profit byproducing q5

The short-run supply curve is theupward-sloping portion of

the

marginal cost curve beginning atpoint 2.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

26/34

Long run Adjustments

In short-run equilibrium, a firm may make aneconomic profit,

make normal profit, or incur aneconomic loss.

Which of these states exists determines the furtherdecisions the

firm makes in the long run.

In the long run, the firm may:

Enter or exit an industry

Change its plant size

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

27/34

Effects of entry

As new firms enter anindustry, industry supplyincreases. The

industrysupply curve shifts

rightward.

The price falls, the

quantity increases, andthe economic profit ofeach firm

decreases.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

28/34

Effects of exit

As firms exit anindustry, industry supplydecreases. The

industry

supply curve shiftsleftward.

The price rises, thequantity decreases, andthe economic profit

ofeach firm increases.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

29/34

Changes in plant size

Firms change their plant size whenever doing sois

profitable.

If average total cost exceeds the minimum long-

run average cost, firms change their plant sizeto lower costs

and increase profits.

If the firms earn zero economic profit with the

current plant and the LRACcurve slopesdownward at the current

output, the firm canincrease profit by expanding the plant. As

theplant size increases, short-run supplyincreases, the price

falls.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

30/34

Long-run equilibrium occurs when the firm is producingat the

minimum long-run average cost and earning zeroeconomic profit.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

31/34

Long run equilibrium

Long-run equilibrium occurs in a competitiveindustry when:

(1) Economic profit is zero, so firms neither enternor exit the

industry.

(2) Long-run average cost is at its minimum, sofirms dont change

their plant size.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

32/34

Why Do Competitive Firms Stay inBusiness If They Make Zero

Profit?

Remember that accounting (nominal)profit is positive even if

economicprofit is zero.

The firm making zero economic profitmeans the firm is doing the

best it canand there is no other alternative thatwill give better

profit. If there was,current economic profit would benegative.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

33/34

Allocative Efficiency of perfect competition

Efficient allocation of resources ( no otherallocation that

would allow someone to bemade better off while no one was made

worse off).Consumers & producers surplus.

Allocative efficiency: Sum of consumer

surplus and producers surplus is maximum.

-

8/2/2019 Chapter-6 Market Structure and Perfect Competition

34/34