Embed Size (px)

Citation preview

1

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

Chapter 5 aCCruals and deferrals

TABLE OF CONTENTS

Introduction 2

Income Recognition Icon 2

Three Ways to Recognize Current Revenues 5

Recognizing Previously Deferred Revenues 5

Recognizing Revenue When Cash Is Collected 7

Recognizing Revenue Before Cash Is Collected 9

Three Ways to Recognize Current Expenses 11

Recognizing Previously Deferred Expenses 11

Recognizing Expenses When Cash is Paid 13

Recognizing Expenses Before Cash is Paid or Losses are Realized 15

Summary 18

Exercise 5.01 19

Figure 5.01 Gap’s Balance Sheet 25

2

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

INTRODUCTIONMeasuring revenues, expenses, gains, and losses reliably and deciding when to recognize them is often very problematic. Thus, income recognition centers on timing. This chapter introduces two timing concepts that will help you better understand the record keeping and reporting consequences of revenue and expense recognition decisions: deferral and accrual entries. After these concepts are defined, we will use them to create a common structure for recording entries related to revenue and expense recognition.

Accruals and deferrals also explain most of the adjustments that reconcile net income to cash from operations: they are the primary reason that income differs from cash from operations.

Accrual entries are recorded when revenues or expenses are recognized before related cash flow consequences. For example, accrual entries are recorded when revenues are recognized at the time customers are billed.

When revenues are accrued, there is an offsetting increase to an asset such as accounts receivable. By contrast, when expenses are accrued, there is an offsetting increase to a liability or contra asset.

For example, when expenses are accrued to recognize that employees, advertisers, licensors, or others are owed money for resources that helped generate current-period revenues, there is an offsetting increase to an accrued liability.

Deferral entries are recorded when events related to revenues and expenses occur before the revenues and expenses are recognized.

Revenues are deferred when cash or other resources are received from customers before revenue is recognized. For example, deferred revenues are recorded when customers pay for products before they are delivered and the company’s policy is to recognize revenue upon delivery.

Expenses are deferred when resources are acquired that benefit future sales or when goods or services are delivered before revenues are recognized. For example, when PP&E or inventories are acquired, expenses are deferred — the costs of these resources are capitalized rather than expensed immediately.

INCOME RECOGNITION ICONNext we will use seven figures to gradually develop a common structure for understanding the past, present, and future record keeping entries that are related to revenues and expenses recognized during the current reporting period. In particular, this income recognition icon

3

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

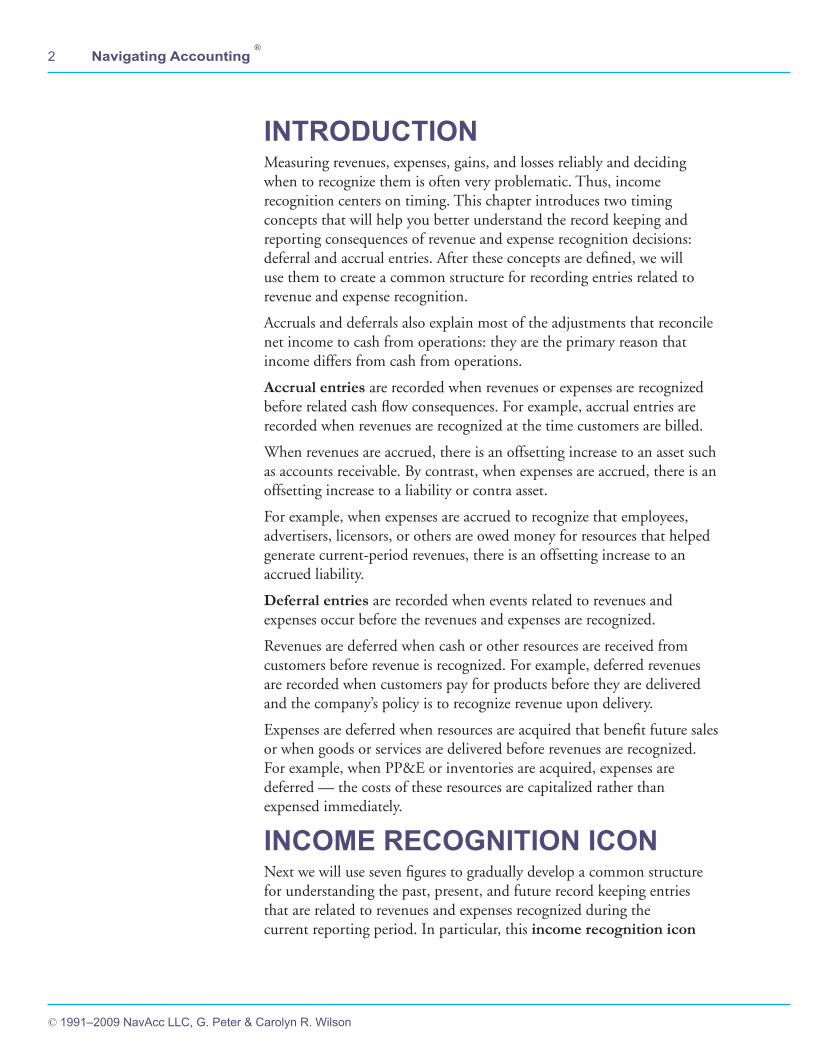

illustrates how accrual and deferral entries relate to revenue and expense recognition. This structure can be generalized rather easily to explain gain and loss recognition. But the icon is busy enough without adding these scenarios.

At the big-picture level, the icon has three parts as indicated below:

• The top part demonstrates that alternative current-period revenue recognition entries can be understood in terms of related past, present, or future entries. The subsequent panels explain these entries.

• The arrow from current period expenses to current period revenues indicates that the relative merits of two principles that largely determine current period expense recognition: the matching and conservative principals discussed in an earlier chapter.

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

CURRENT-PERIOD

EXPENSES

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Matching PrincipalConservative Principal

Valuation Adjustments

4

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

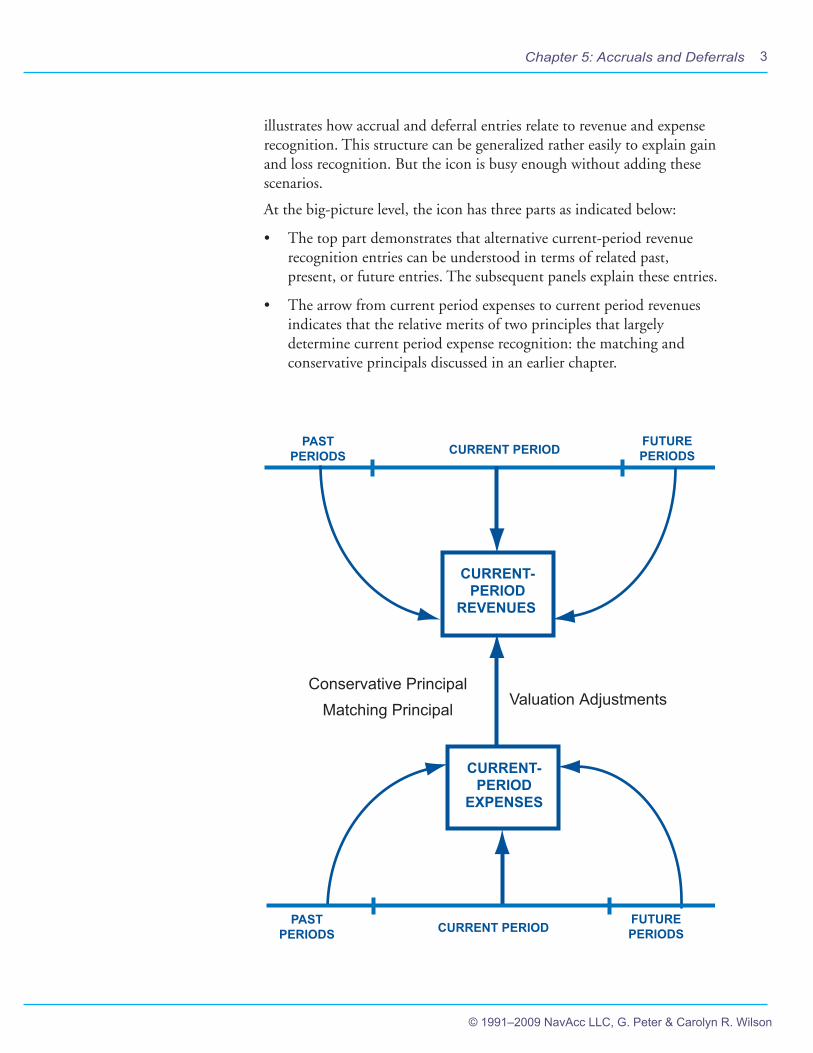

• The bottom part demonstrates that current-period expense recognition entries can be understood in terms of related past, present, or future entries. The subsequent discussion explains many of these entries.

• The center period in the icon is the current reporting period. However, the important aspect of the three periods is their ordering in time. For example, below a special case of the previous figure illustrates how revenues and expenses recognized in year-1 are related to events in years 0, 1 and 2. However, it could easily be modified to illustrate how revenues and expenses in year 2 are related to events in years prior to year 2, year 2, and years after year 2.

YEAR 1YEAR 0 YEAR 2

YEAR-1REVENUES

YEAR-1EXPENSES

Matching PrincipalConservative Principal

Valuation Adjustments

YEAR 1YEAR 0 YEAR 2

5

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

Deferred

earlier

inthe

current period

Deferred

ina

prior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Matching PrincipalConservative Principal Valuation Adjustments

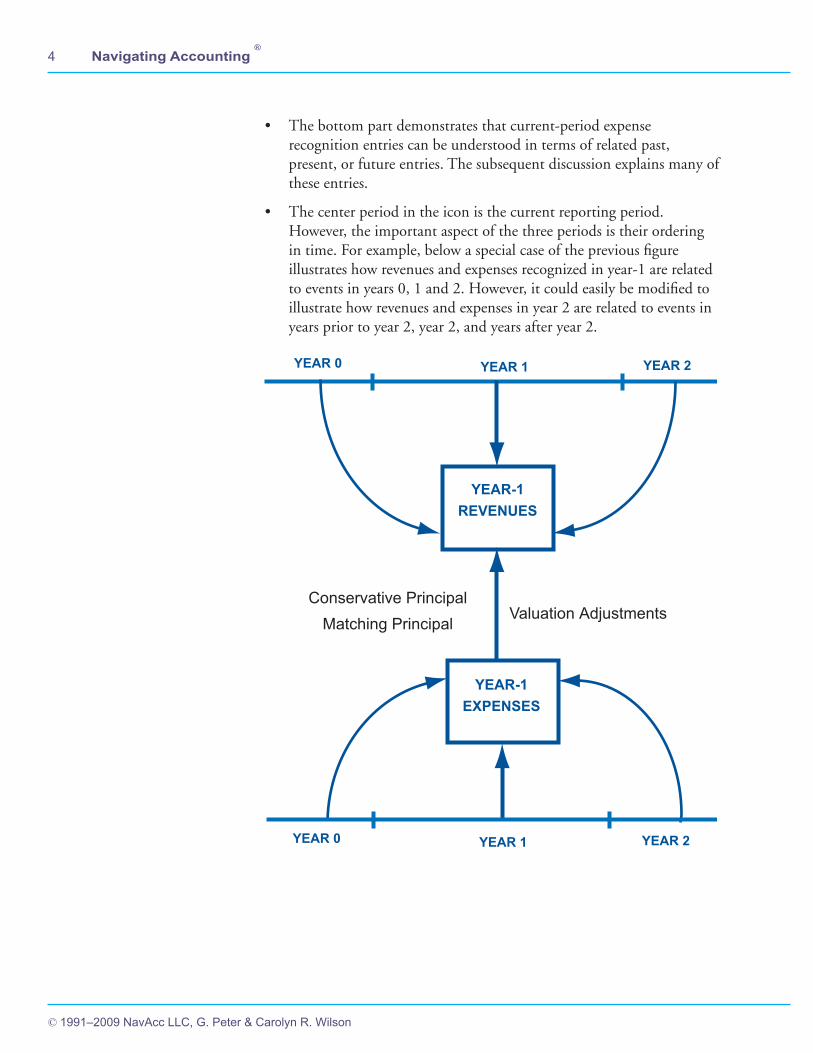

THREE WAYS TO RECOGNIZE CURRENT REVENUESreCognizing previously deferred revenuesThe figure below builds on the previous one by developing the upper left corner of the icon: Revenues recognized in the current period that were deferred in a prior period or earlier in the current period.

6

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

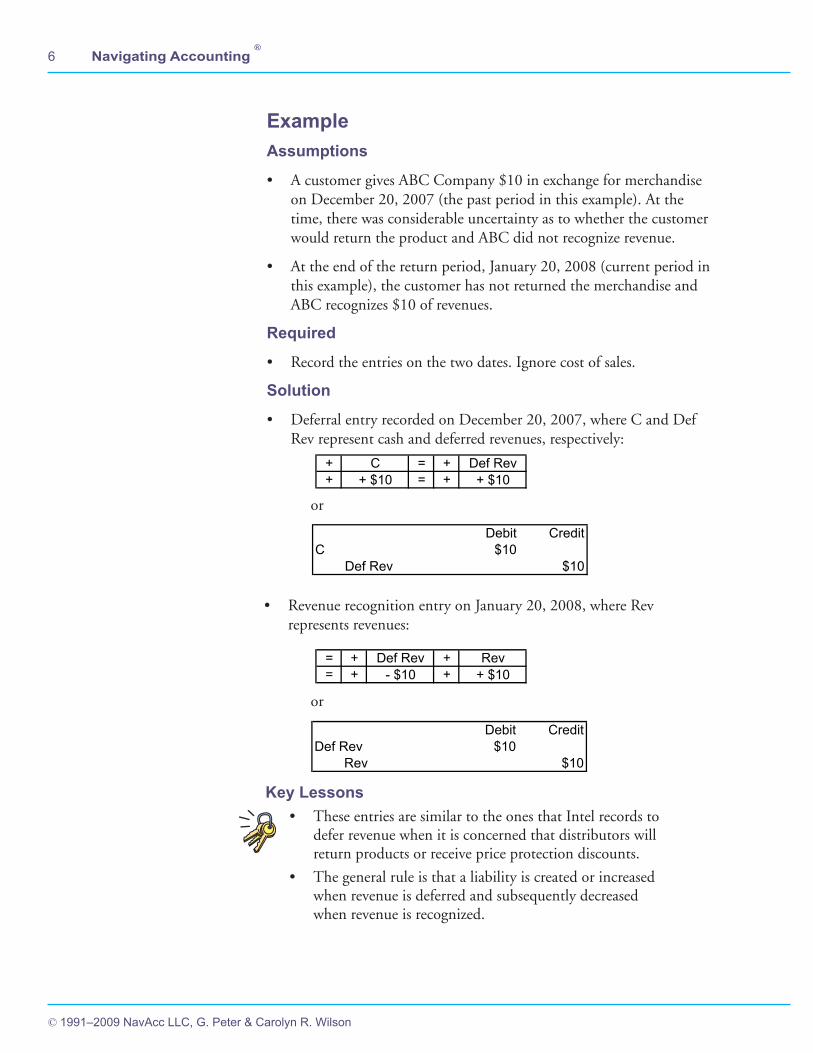

+ C = + Def Rev+ + $10 = + + $10

or

Debit CreditC $10

Def Rev $10

• Revenue recognition entry on January 20, 2008, where Rev represents revenues:

= + Def Rev + Rev= + - $10 + + $10

or

Debit CreditDef Rev $10

Rev $10

Key Lessons• These entries are similar to the ones that Intel records to

defer revenue when it is concerned that distributors will return products or receive price protection discounts.

• The general rule is that a liability is created or increased when revenue is deferred and subsequently decreased when revenue is recognized.

ExampleAssumptions

• A customer gives ABC Company $10 in exchange for merchandise on December 20, 2007 (the past period in this example). At the time, there was considerable uncertainty as to whether the customer would return the product and ABC did not recognize revenue.

• At the end of the return period, January 20, 2008 (current period in this example), the customer has not returned the merchandise and ABC recognizes $10 of revenues.

Required

• Record the entries on the two dates. Ignore cost of sales.

Solution

• Deferral entry recorded on December 20, 2007, where C and Def Rev represent cash and deferred revenues, respectively:

7

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

Deferred

earlier

inthe

current period

Deferred

ina

prior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Current-periodrevenues that are

recognized when cash is collected during the

current period

Matching PrincipalConservative Principal Valuation Adjustments

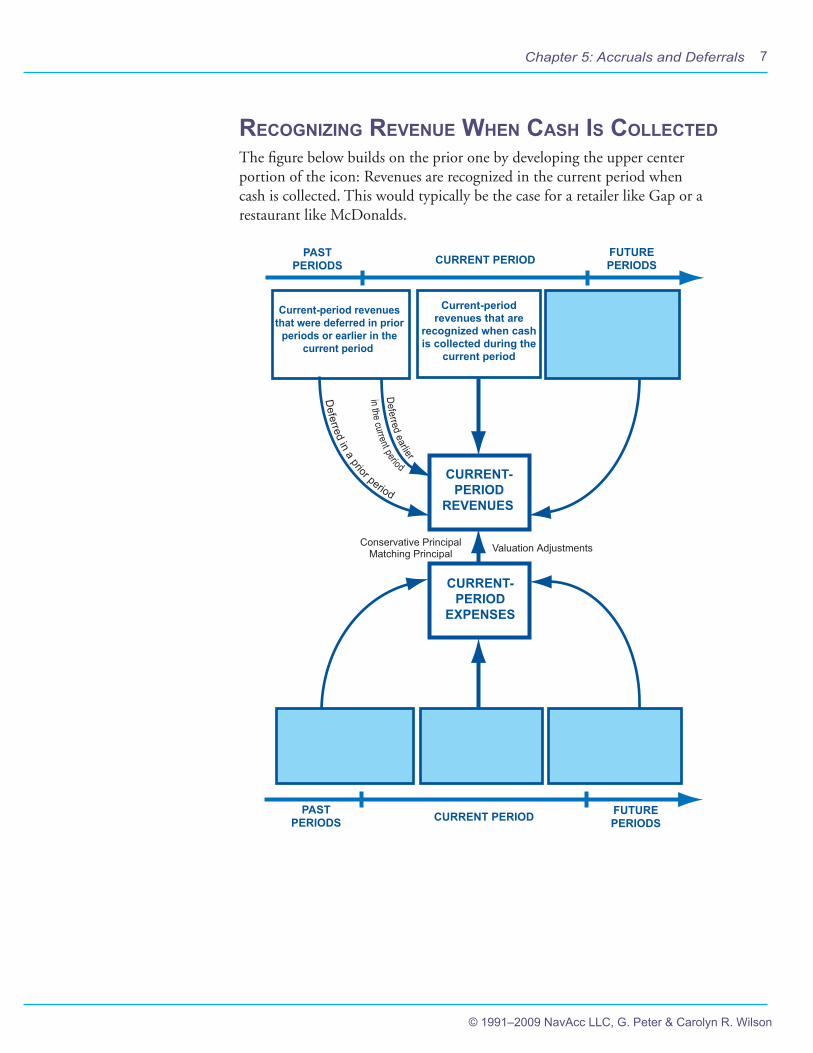

reCognizing revenue When Cash is ColleCtedThe figure below builds on the prior one by developing the upper center portion of the icon: Revenues are recognized in the current period when cash is collected. This would typically be the case for a retailer like Gap or a restaurant like McDonalds.

8

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

or

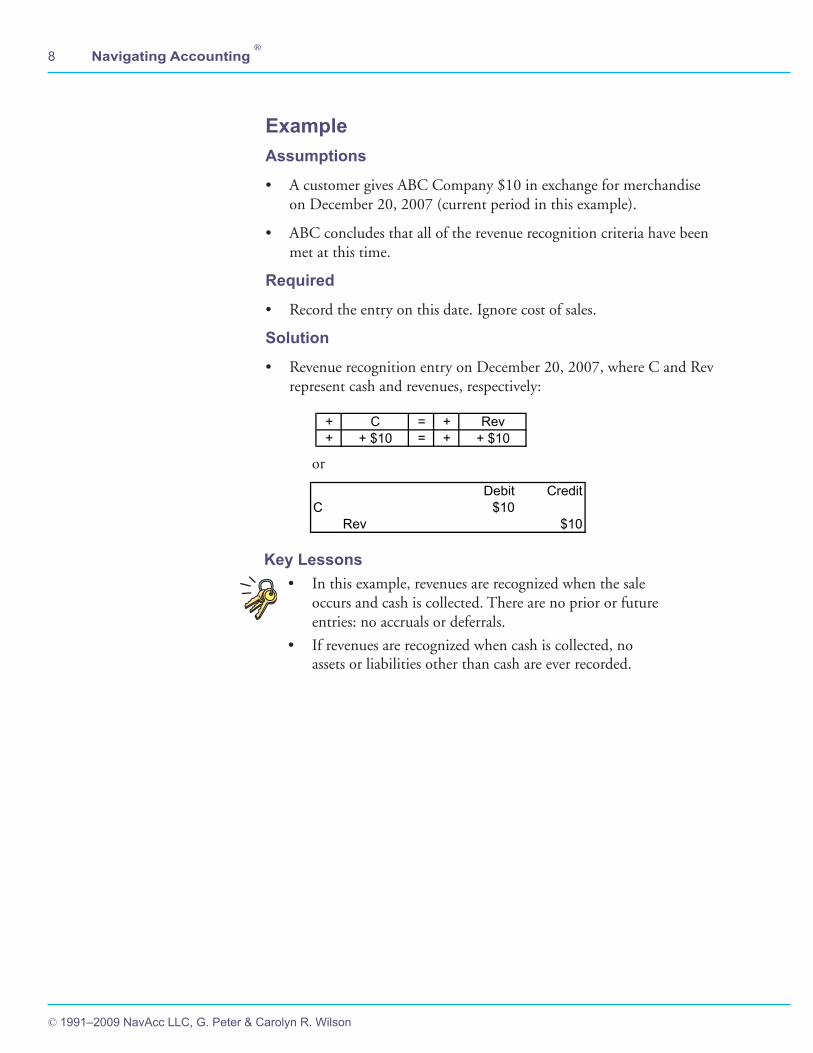

Key Lessons• In this example, revenues are recognized when the sale

occurs and cash is collected. There are no prior or future entries: no accruals or deferrals.

• If revenues are recognized when cash is collected, no assets or liabilities other than cash are ever recorded.

ExampleAssumptions

• A customer gives ABC Company $10 in exchange for merchandise on December 20, 2007 (current period in this example).

• ABC concludes that all of the revenue recognition criteria have been met at this time.

Required

• Record the entry on this date. Ignore cost of sales.

Solution

• Revenue recognition entry on December 20, 2007, where C and Rev represent cash and revenues, respectively:

+ C = + Rev+ + $10 = + + $10

Debit CreditC $10

Rev $10

9

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

Deferred

earlier

inthe

current periodD

eferredin

aprior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Current-periodrevenues that are

recognized when cash is collected during the

current period

Accrue

d and

colle

cted

in thecu

rrent

perio

d

Current-periodrevenues that are

accrued before they are collected in future

periods or later in the current period.

Accrued in the

curren

t period

and collecte

d in afutu

re perio

d

Matching PrincipalConservative Principal Valuation Adjustments

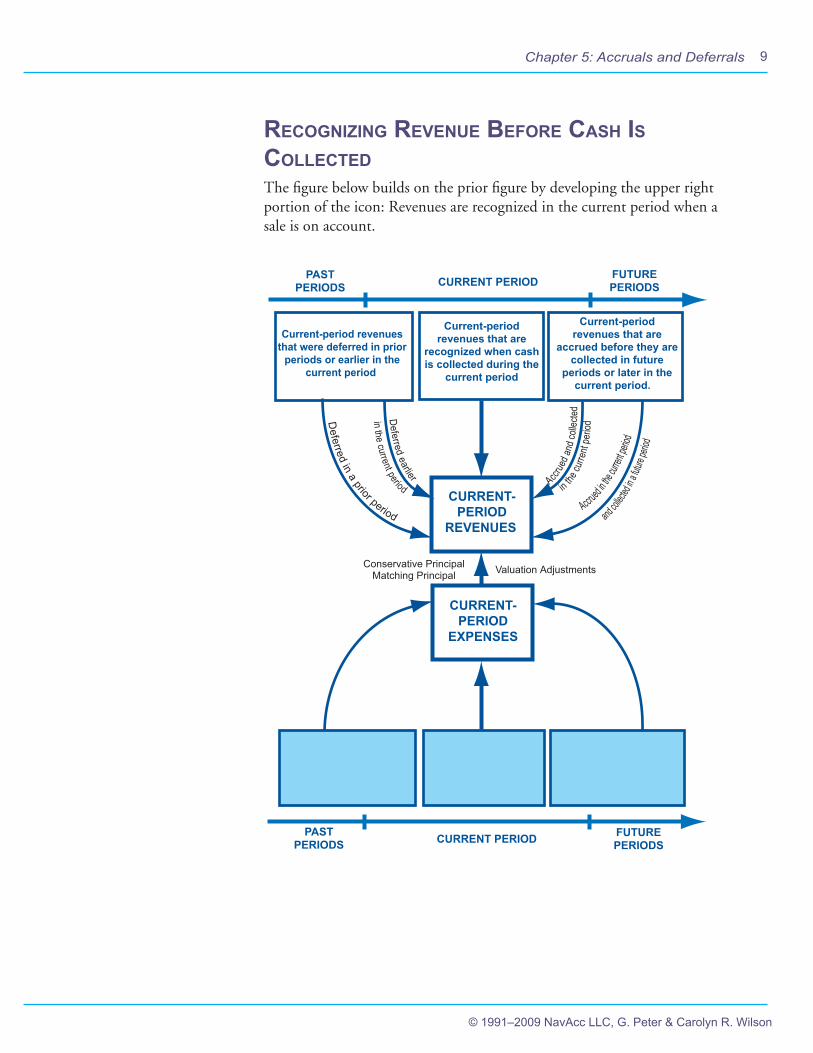

reCognizing revenue Before Cash is ColleCtedThe figure below builds on the prior figure by developing the upper right portion of the icon: Revenues are recognized in the current period when a sale is on account.

10

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

or

• Collection entry on January 20, 2008, where C represents cash:

or

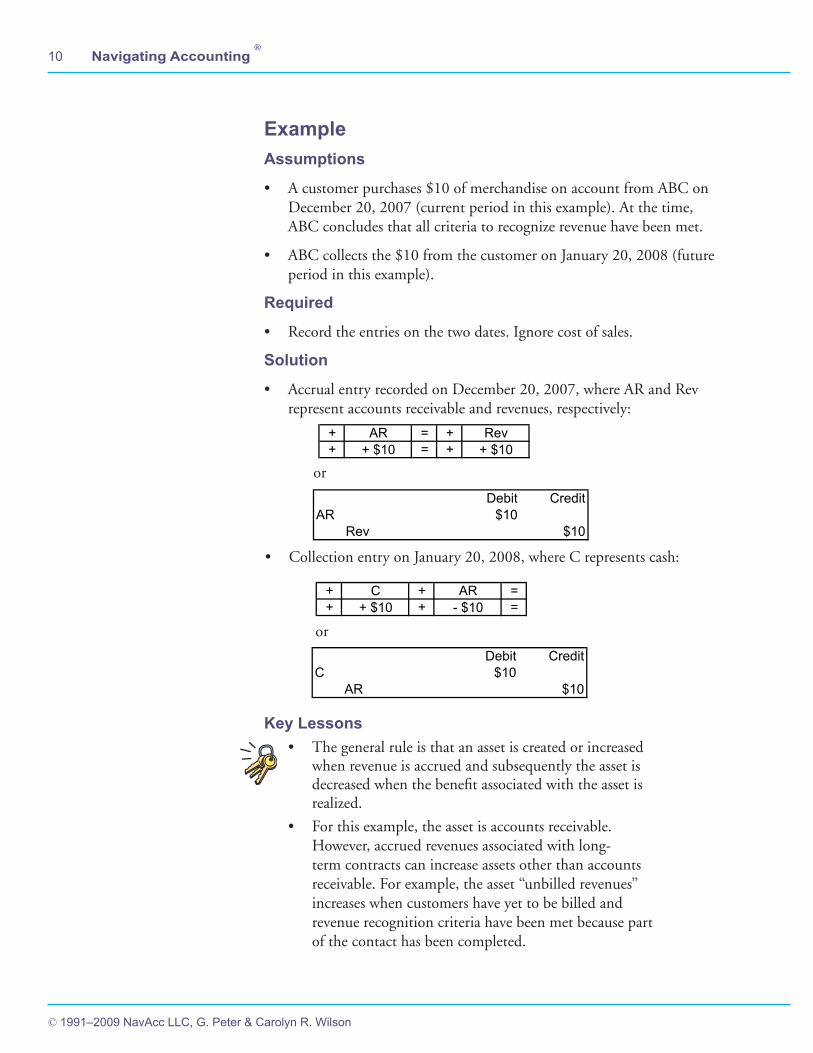

Key Lessons• The general rule is that an asset is created or increased

when revenue is accrued and subsequently the asset is decreased when the benefit associated with the asset is realized.

• For this example, the asset is accounts receivable. However, accrued revenues associated with long-term contracts can increase assets other than accounts receivable. For example, the asset ‘‘unbilled revenues’’ increases when customers have yet to be billed and revenue recognition criteria have been met because part of the contact has been completed.

ExampleAssumptions

• A customer purchases $10 of merchandise on account from ABC on December 20, 2007 (current period in this example). At the time, ABC concludes that all criteria to recognize revenue have been met.

• ABC collects the $10 from the customer on January 20, 2008 (future period in this example).

Required

• Record the entries on the two dates. Ignore cost of sales.

Solution

• Accrual entry recorded on December 20, 2007, where AR and Rev represent accounts receivable and revenues, respectively:

+ AR = + Rev+ + $10 = + + $10

Debit CreditAR $10

Rev $10

+ C + AR =+ + $10 + - $10 =

Debit CreditC $10

AR $10

11

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

Deferred

earlier

inthe

current period

Deferred

ina

prior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Current-periodrevenues that are

recognized when cash is collected during the

current period

Accrue

d and

colle

cted

in thecu

rrent

perio

d

Current-periodrevenues that are

accrued before they are collected in future

periods or later in the current period.

Current-period expenses that were deferred in a

prior period or earlier in the current period

Def

erre

dea

rlier

incu

rren

t per

iod

Accrued in the

curren

t period

Def

erre

din

apr

iorperiod

and collecte

d in afutu

re perio

d

Matching PrincipalConservative Principal Valuation Adjustments

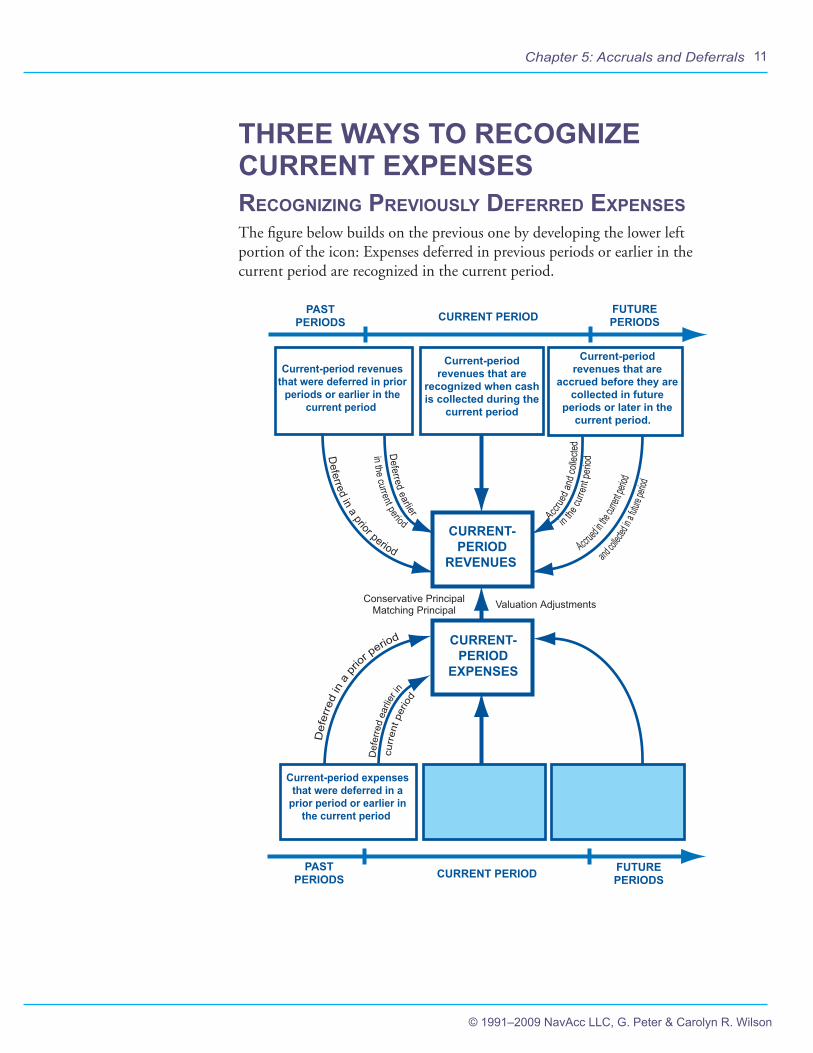

THREE WAYS TO RECOGNIZE CURRENT EXPENSESreCognizing previously deferred expensesThe figure below builds on the previous one by developing the lower left portion of the icon: Expenses deferred in previous periods or earlier in the current period are recognized in the current period.

12

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

or

• Depreciation entry on December 31, 2007, where AccDep and DepExp represent accumulated depreciation and depreciation expense, respectively:

or

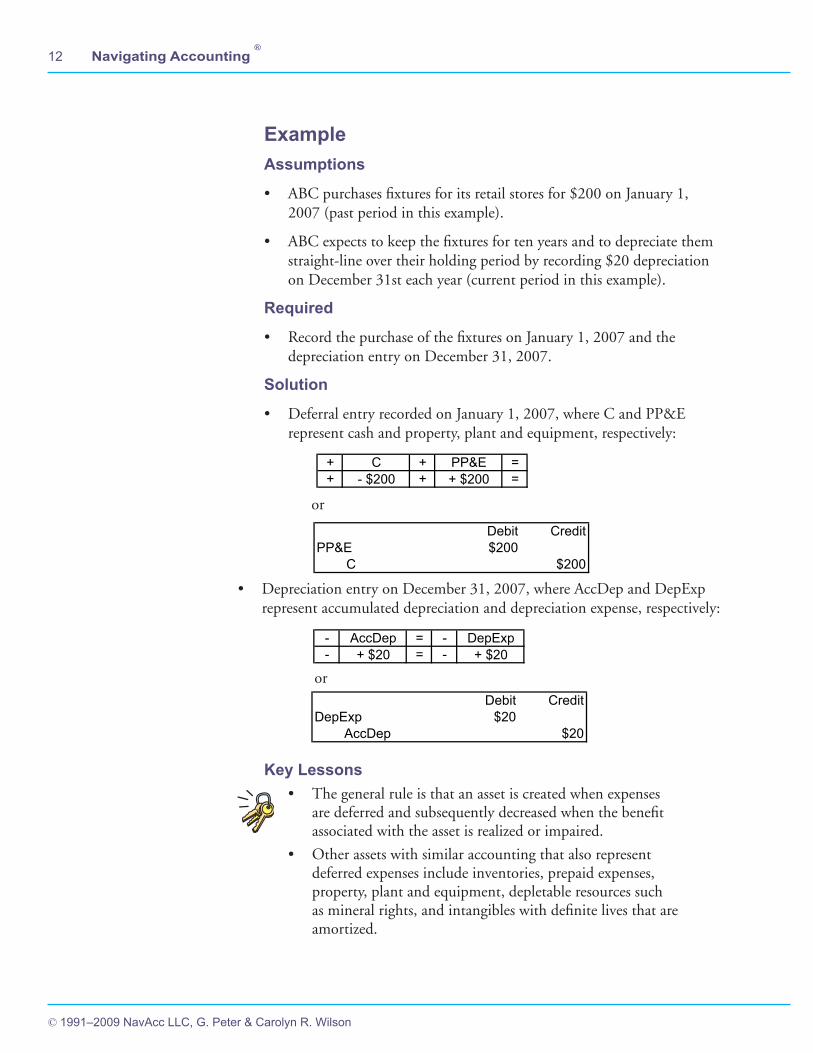

Key Lessons• The general rule is that an asset is created when expenses

are deferred and subsequently decreased when the benefit associated with the asset is realized or impaired.

• Other assets with similar accounting that also represent deferred expenses include inventories, prepaid expenses, property, plant and equipment, depletable resources such as mineral rights, and intangibles with definite lives that are amortized.

ExampleAssumptions

• ABC purchases fixtures for its retail stores for $200 on January 1, 2007 (past period in this example).

• ABC expects to keep the fixtures for ten years and to depreciate them straight-line over their holding period by recording $20 depreciation on December 31st each year (current period in this example).

Required

• Record the purchase of the fixtures on January 1, 2007 and the depreciation entry on December 31, 2007.

Solution

• Deferral entry recorded on January 1, 2007, where C and PP&E represent cash and property, plant and equipment, respectively:

+ C + PP&E =+ - $200 + + $200 =

Debit CreditPP&E $200

C $200

- AccDep = - DepExp- + $20 = - + $20

Debit CreditDepExp $20

AccDep $20

13

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

CURRENT-PERIOD

REVENUES

Deferred

earlier

inthe

current period

Deferred

ina

prior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

CURRENT PERIODPASTPERIODS

FUTUREPERIODS

Current-periodrevenues that are

recognized when cash is collected during the

current period

Accrue

d and

colle

cted

in thecu

rrent

perio

d

Current-periodrevenues that are

accrued before they are collected in future

periods or later in the current period.

Current-period expenses that were deferred in a

prior period or earlier in the current period

Def

erre

dea

rlier

incu

rren

t per

iod

Current-periodexpenses that are recognized when

cash is paid during the current period

Accrued in the

curren

t period

Def

erre

din

apr

iorperiod

and collecte

d in afutu

re perio

d

Matching PrincipalConservative Principal Valuation Adjustments

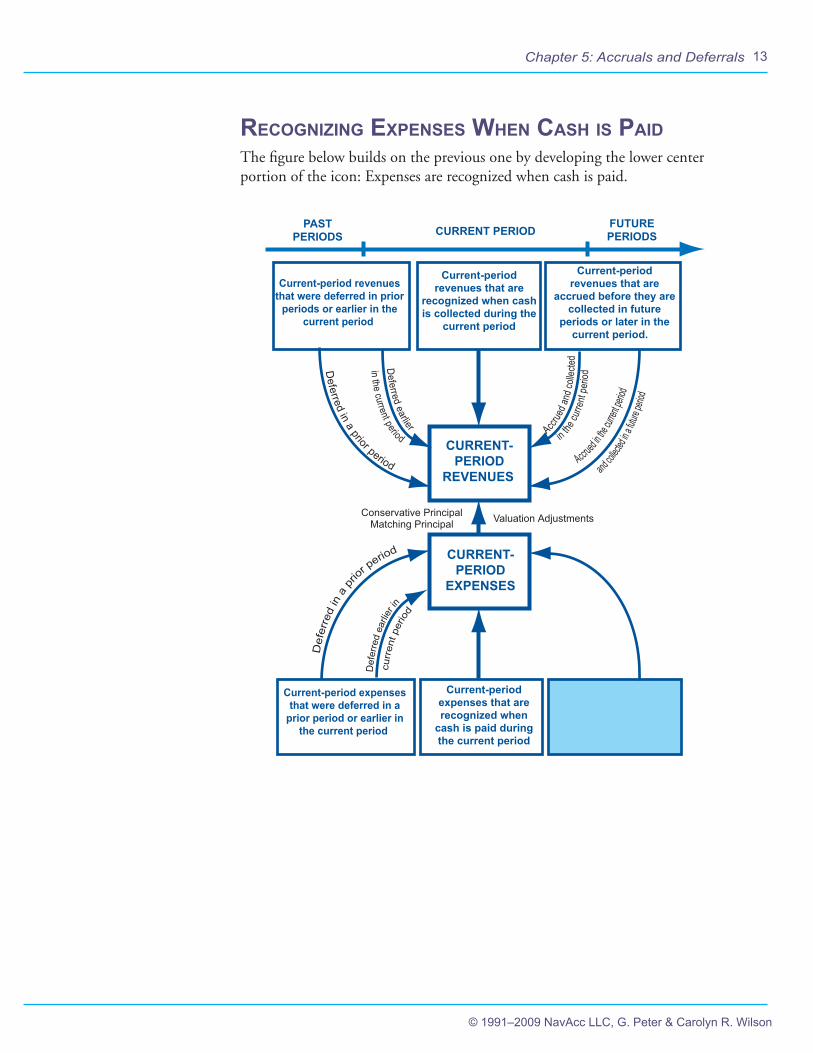

reCognizing expenses When Cash is paidThe figure below builds on the previous one by developing the lower center portion of the icon: Expenses are recognized when cash is paid.

14

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

or

Key Lessons• Expenses that are recognized in the same period that the

related costs are incurred are called period expenses.

• For the central lower part of the income recognition icon, period expenses are recognized when cash is expended. However, period expenses can also be recognized by accruing a liability (lower right part of the icon — studied next).

• Period expenses generally arise in two types of circumstances. First, they arise in situations such as marketing and research and development where the consensus opinion of those that create GAAP is that it is not possible to reliably match current costs to future benefits. In these situations, the conservative principle dominates the matching principle. Second, they arise when costs that might otherwise be capitalized are relatively immaterial or their benefits are realized in the near future and they are stable across reporting periods.

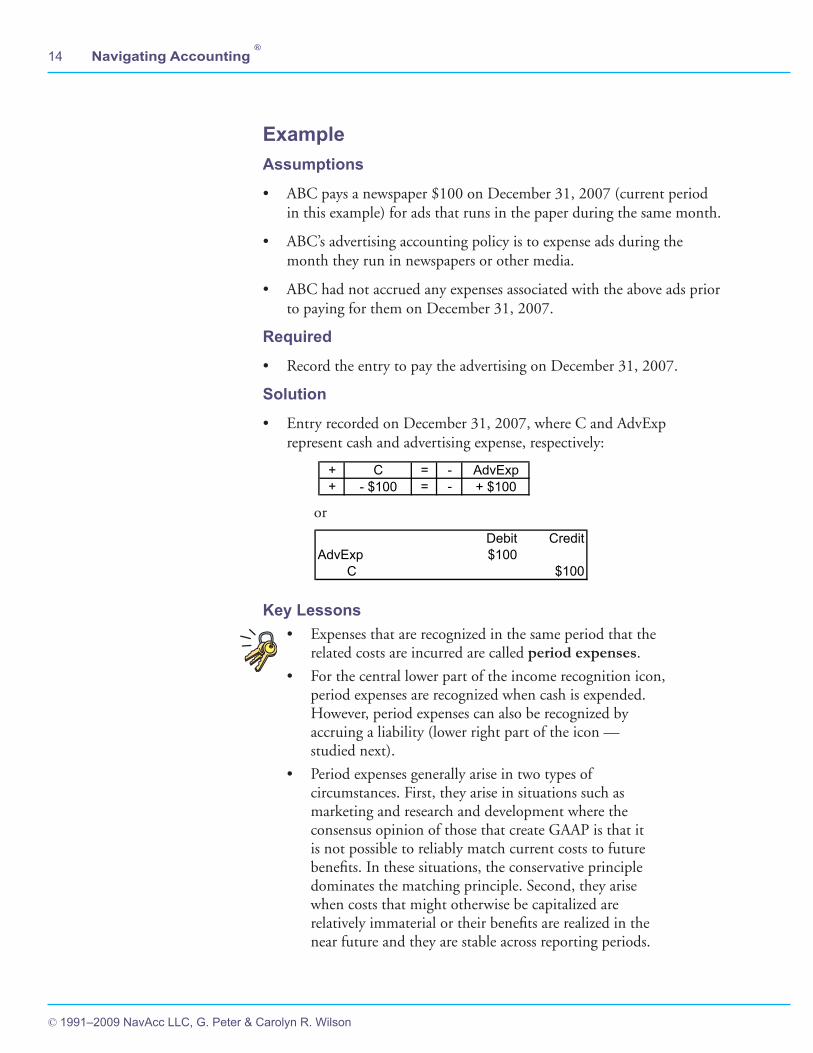

ExampleAssumptions

• ABC pays a newspaper $100 on December 31, 2007 (current period in this example) for ads that runs in the paper during the same month.

• ABC’s advertising accounting policy is to expense ads during the month they run in newspapers or other media.

• ABC had not accrued any expenses associated with the above ads prior to paying for them on December 31, 2007.

Required

• Record the entry to pay the advertising on December 31, 2007.

Solution

• Entry recorded on December 31, 2007, where C and AdvExp represent cash and advertising expense, respectively:

+ C = - AdvExp+ - $100 = - + $100

Debit CreditAdvExp $100

C $100

15

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

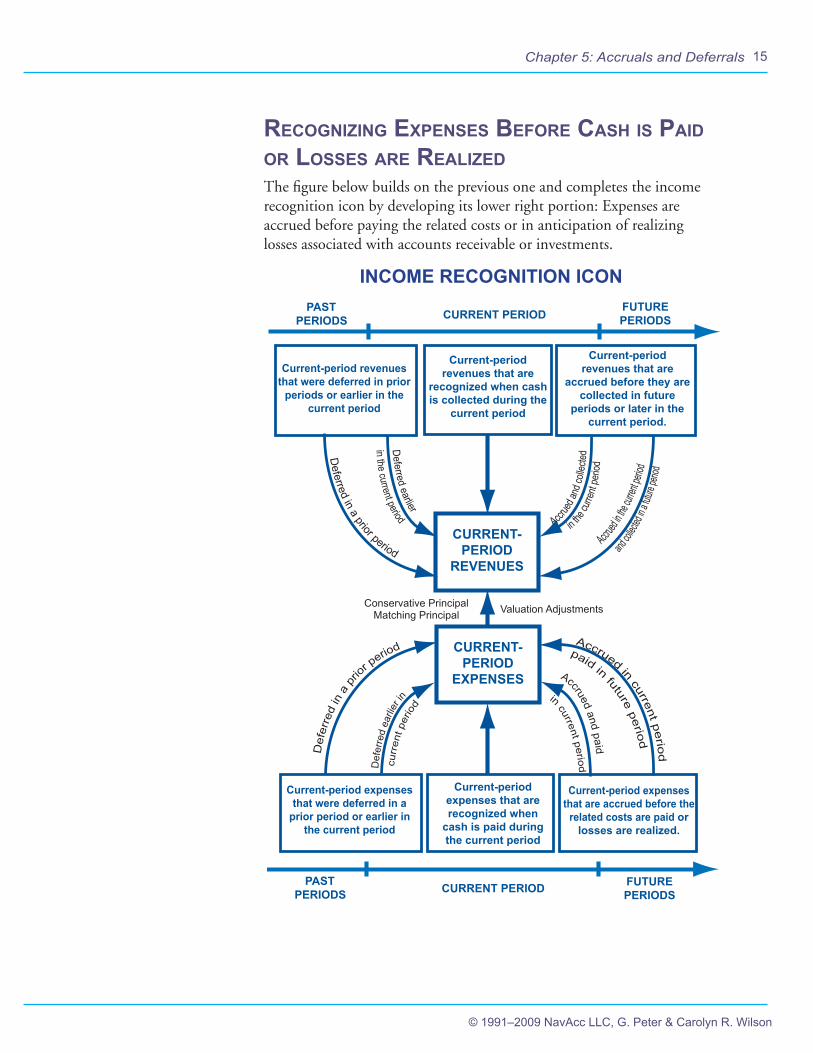

reCognizing expenses Before Cash is paid or losses are realizedThe figure below builds on the previous one and completes the income recognition icon by developing its lower right portion: Expenses are accrued before paying the related costs or in anticipation of realizing losses associated with accounts receivable or investments.

INCOME RECOGNITION ICON

CURRENT PERIOD PAST PERIODS

FUTURE PERIODS

CURRENT-PERIOD

REVENUES

Deferred earlier

in the current period

Deferred in a prior period

CURRENT-PERIOD

EXPENSES

Current-period revenues that were deferred in prior

periods or earlier in the current period

Matching Principal Conservative Principal

CURRENT PERIOD PAST PERIODS

FUTURE PERIODS

Current-period revenues that are

recognized when cash is collected during the

current period

Accrue

d and

colle

cted

in the

curre

nt pe

riod

Current-period revenues that are

accrued before they are collected in future

periods or later in the current period.

Current-period expenses that were deferred in a

prior period or earlier in the current period

Def

erre

d ea

rlier

in

curr

ent p

erio

d

Current-period expenses that are recognized when

cash is paid during the current period

Current-period expenses that are accrued before the

related costs are paid or losses are realized.

Accrued and paid

in current period

Accrued in current perio

d

paid in future period

Accrued i

n the c

urrent p

eriod

Def

erre

d in

a p

rior p

eriod

and col

lected

in a fut

ure pe

riod

Valuation Adjustments

16

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

or

• Interest entry recorded on January 31, 2007, where C represents cash:

or

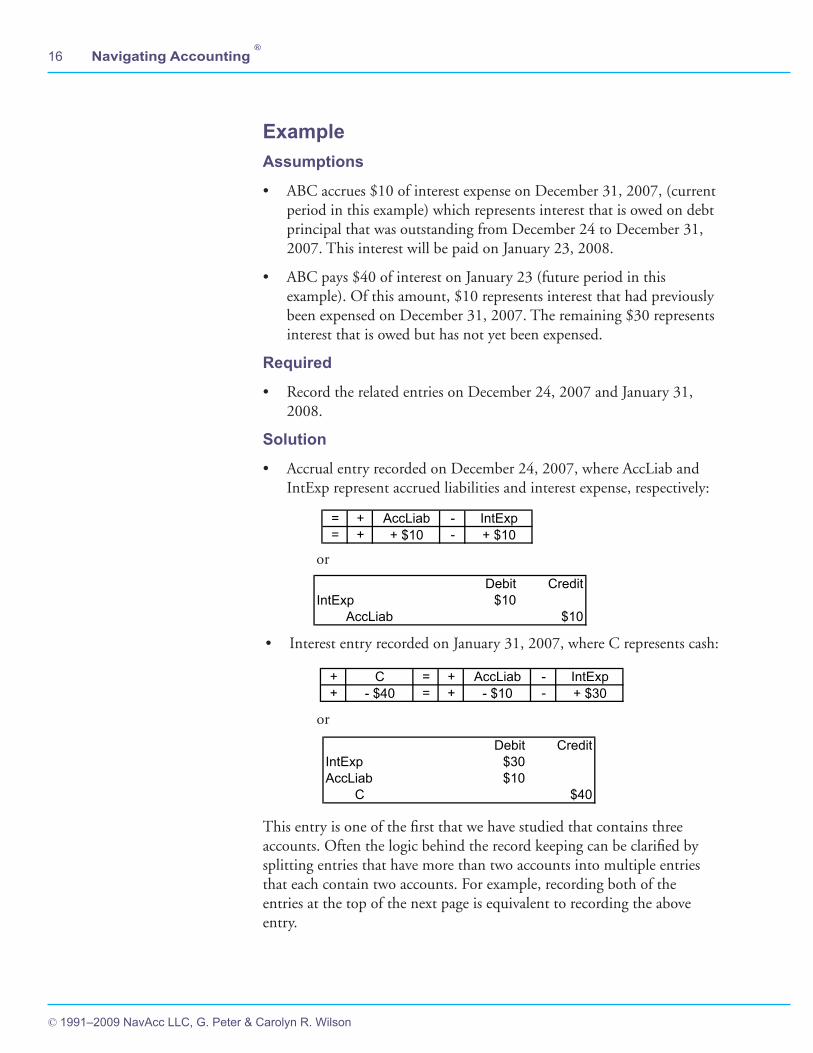

ExampleAssumptions

• ABC accrues $10 of interest expense on December 31, 2007, (current period in this example) which represents interest that is owed on debt principal that was outstanding from December 24 to December 31, 2007. This interest will be paid on January 23, 2008.

• ABC pays $40 of interest on January 23 (future period in this example). Of this amount, $10 represents interest that had previously been expensed on December 31, 2007. The remaining $30 represents interest that is owed but has not yet been expensed.

Required

• Record the related entries on December 24, 2007 and January 31, 2008.

Solution

• Accrual entry recorded on December 24, 2007, where AccLiab and IntExp represent accrued liabilities and interest expense, respectively:

= + AccLiab - IntExp= + + $10 - + $10

Debit CreditIntExp $10

AccLiab $10

+ C = + AccLiab - IntExp+ - $40 = + - $10 - + $30

Debit CreditIntExp $30AccLiab $10

C $40

This entry is one of the first that we have studied that contains three accounts. Often the logic behind the record keeping can be clarified by splitting entries that have more than two accounts into multiple entries that each contain two accounts. For example, recording both of the entries at the top of the next page is equivalent to recording the above entry.

17

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

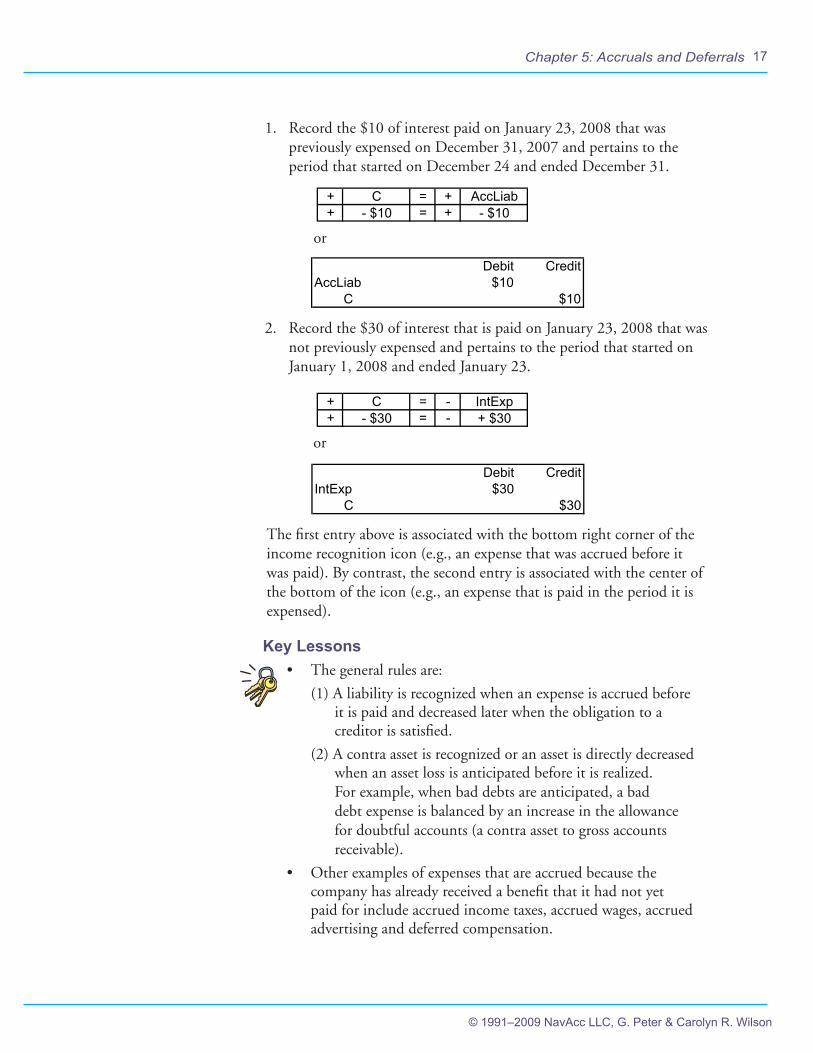

Key Lessons• The general rules are:

(1) A liability is recognized when an expense is accrued before it is paid and decreased later when the obligation to a creditor is satisfied.

(2) A contra asset is recognized or an asset is directly decreased when an asset loss is anticipated before it is realized. For example, when bad debts are anticipated, a bad debt expense is balanced by an increase in the allowance for doubtful accounts (a contra asset to gross accounts receivable).

• Other examples of expenses that are accrued because the company has already received a benefit that it had not yet paid for include accrued income taxes, accrued wages, accrued advertising and deferred compensation.

1. Record the $10 of interest paid on January 23, 2008 that was previously expensed on December 31, 2007 and pertains to the period that started on December 24 and ended December 31.

+ C = + AccLiab+ - $10 = + - $10

or

Debit CreditAccLiab $10

C $10

2. Record the $30 of interest that is paid on January 23, 2008 that was not previously expensed and pertains to the period that started on January 1, 2008 and ended January 23.

+ C = - IntExp+ - $30 = - + $30

or

Debit CreditIntExp $30

C $30

The first entry above is associated with the bottom right corner of the income recognition icon (e.g., an expense that was accrued before it was paid). By contrast, the second entry is associated with the center of the bottom of the icon (e.g., an expense that is paid in the period it is expensed).

18

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

SUMMARY This chapter introduced deferral and accrual entries, which are central to income recognition. Accrual entries are recorded when revenues or expenses are recognized before related cash flow consequences. Examples include accruing revenue before collecting cash from customers and accruing compensation expense before paying employees.

By contrast, deferral entries are recorded when events related to revenues and expenses occur before the revenues and expenses are recognized. Examples include deferring revenue when cash or promised future payment has been received from a customer and deferring expense when property, plant, and equipment has been recognized.

Accrual and deferral entries are always paired with future entries. For example, accruing compensation expense is paired with paying it later and deferring expensing costs associated with purchasing PP&E is paired with future depreciation entries. Similarly, accruing revenues is paired with collecting them later and deferring revenues is paired with recognizing them later.

The Income Recognition icon illustrates that income recognition is determined by four accrual-deferral pairings and two other entries where revenue/gain and expense/loss recognition coincides with cash flows. Importantly, these entry categories in the income recognition icon include most of the investing and operating entries and there are many such entries. Thus, understanding the general structure of the entries for these categories and how these entries affect the financial statements will greatly facilitate your learning.

You can gain this understanding as you work with entries in the exercises at the end of this chapter by asking yourself questions such as the following: How does this entry relate to the income recognition icon, if at all? What is the general structure of entries in this part of the icon? How do these entries affect the balance sheet, income statement, and statement of cash flows?

19

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

Record Keeping and Reporting IconThis exercise helps you meet the insider record keeping and reporting challenge.

Entries

Operating

Investing

Financing

Beg Bal

Tr Bal

Cls IS

Cls RE

End Bal

Zero

Zero

Revenue

Expenses

Gains & Losses

Assets

Liabilities

Owners' Equity

Net IncomeCash change

cash +other assets = liabilities + permanent OE+ temporary OE

Assets = Liabilities + Owners' EquitiesRECORDKEEPING

REPORTING

Adjustments

Operating Cash

Reconciliations

Net Income

Direct Cash Flows Balance Sheets Income Statements

Exercise 5.01BackgroundThis exercise deals with Cardinal’s year-1 non-tax and non-dividend entries. Tax entries are studied in a later chapter and Cardinal does not pay dividends (under the initial assumptions). This builds on Cardinal’s year-0 entries and accounts discussed in an earlier chapter.

Cardinal Accounts needed for Exercise 5.01

The chart below lists the accounts you will need for this exercise. The Accts sheet in the Cardinal model contains these accounts and others. The next few pages describe accounts not discussed in earlier chapters, along with some important concepts.

Abbreviation Account

AR accounts receivable (gross)AcDep accumulated depreciation (PP&E)

C cashMerInv merchandise inventoriesPP&E gross PP&E (at historical cost)Inves investmentsPreEx prepaid expenses

AP accounts payableAcrLiab accrued liabilitiesLTDebt long-term debt (noncurrent portion)STdebt short-term debt

PIC paid-in capital (non-par stock)RetEarn retained earnings

CGS cost of good soldDepEx depreciation expenseIncSum income summary

IntEx interest expenseIntInc interest income

OpLeEx operating lease expenseSalesR sales revenuesOthEx other operating expenses

ASSETS

LIABILITIES

PERMANENT OWNERS' EQUITY

TEMPORARY OWNERS' EQUITY

20

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

Accrued liabilities (AcrLiab) is a liability that records obligations to creditors for resources that are presumed to have helped generate revenues in the current period or past periods.

Interest expense (IntEx) is recognized on debt that is outstanding during the year and on liabilities associated with capital leases. Cardinal makes debt and lease payments on the last day of the year. Part of these payments are interest and part a return of the borrowed principal. The interest is computed by multiplying the outstanding debt at the start of the year by an annual interest rate. The new debt issued during the current year does not accrue interest since it is issued on the last day of the year.

The accounting is simplified by assuming that debt payments are made on the last day of the year. This assumption is relaxed in the MMS model to illustrate the adjusting entry that is made when debt payments do not occur at the end of the reporting period. This is an accrual entry: interest is accrued for the interval from the last payment in the period until the end of the period.

Operating Lease Expense (OpLeExp) is recognized when leases are classified as operating. The expense equals the lease payment.

By contrast, two expenses are recognized for capital leases: depreciation associated with the lease asset and interest expense associated with the lease obligation. The lease depreciation is based on a straight-line computation, meaning it is the same each year. By contrast, the lease interest expense decreases each period as the outstanding obligation decreases (because part of the lease payments are a return of principal).

Thus, the combined expenses (depreciation plus interest) associated with capital leases are large at the start of the lease and decline during the lease life. By contrast, operating lease expenses are constant during the lease life if the lease payments are constant (which is frequently true).

The total expense recognized over the life of a lease will be the same if the lease is classified as capital or operating: it will equal the sum of the lease payments.

However, the pattern of the lease expenses will differ. Capital leases have larger expenses than operating leases early in the lease life and smaller expenses late in the lease life. This pattern can influence the way managers structure leases. In particular, considerable effort is devoted to structuring leases so that they meet the criteria to be classified as operating. This ensures less reported financial leverage (since lease assets and obligations are not recognized) and smaller expenses early in the lease life.

21

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

Other expense (OthEx) includes costs related to new-market launches, holding inventory, building brands, and other miscellaneous sources. Portions of this expense are paid: (1) in the prior year, (2) in the current year, and (3) in the next year. The income recognition icon should help you record this expense.

Cardinal’s Year-1 Non-Tax Entries

Cardinal’s year-1 entries are all assumed to occur on the last day of the year. Here is a brief description of entries.

• Car1.08 — Operating Lease Payment and Expense: See the discussion for the operating lease expense account on the previous page.

• Car1.10 — Other Operating Expenses Paid As Expensed: These expenses belong to the class of expenses in the lower center portion of the income recognition icon.

• Car1.11 — Other Operating Expenses Paid in Prior or Next year: These expenses belong to the classes of expenses in the lower left and right portions of the income recognition icon.

• Car1.12 — Payment of Long-Term Debt Principal and Interest: See the discussion for the interest expense account on the previous page.

The Cardinal model simplifies the long-term debt entries that occur in practice. Generally, companies make an adjusting entry at the end of the period that reclassifies the principal they anticipate paying the next period from long-term debt to the “current portion of long-term debt,” which is a current liability. This informs investors that the companies have short-term obligations. When the payment is made the next period, the current portion account is decreased (rather than long-term debt). These entries are recognized in the MMS model.

• Car1.13 — Payment on Capital Leases: Capital lease payments are similar to long-term debt payments. Part of the lease payment is interest and the other reduces the outstanding principal of the lease obligation. In the model, this entry records $0 when leases are classified as operating. In practice, no entry is made in this situation.

• Car1.14 — Payment of Short-Term Debt Principal and Interest: Initially, the model assumes that Cardinal does not issue short-term debt in year 0 and thus it pays no interest in year 1. However, the model records an entry with $0 recognized for each account. The structure of this entry is identical to the entry for long-term debt

22

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

except the principal portion of the payment decreases short-term debt rather than long-term debt.

• Car1.19 — Sell Investment Securities at Cost: Initially, the model assumes that venture capitalists contribute $8,000,000 at the end of year 0. Cardinal is expected to temporarily invest over $7 million of this cash at the end of year 0 to cover anticipated future shortfalls. At the end of year 1, Cardinal liquidates part of these investments to generate sufficient cash to cover year-1 shortfalls.

Assuming that the securities will be sold at cost is reasonable for a pro-forma model because they are just as likely to increase as decrease in value. However, when Cardinal actually sells investment securities, it will likely record a gain or a loss. Moreover, GAAP requires certain gains and losses to be recognized even when securities are not sold. These issues are built into the MMS model.

Part 1 of Exercise 5.01To answer this question, you will need: (1) the Cardinal model and (2) hard copies of the following Cardinal Excel Workbook sheets: EntryInputs, Accts, IS, BS, SCF, and DCFO.

a) Record Car1.01-Car1.19 manually on paper using the accounts in the Accts sheet and setting up a separate mini-equation for each event.

b) Above in part (a) you recorded the entries using balance-sheet mini-equations. Part (c) you practice recording the entries with debits and credits.

c) Record these entries using journal entries.

d) For each entry, be prepared to explain how the changes in accounts relate to underlying business activity. For example, when inventory is sold, it is no longer controlled by the selling company. Thus, the company no longer has a related future benefit. Accordingly, the financial measure related to this inventory is removed from the inventories account.

e) What line items on Cardinal’s balance sheet, income statement, statement of cash-flows statement (indirect format) and direct cash-flows statement (operating section only) are affected by each of the entries you recorded in part (a)?

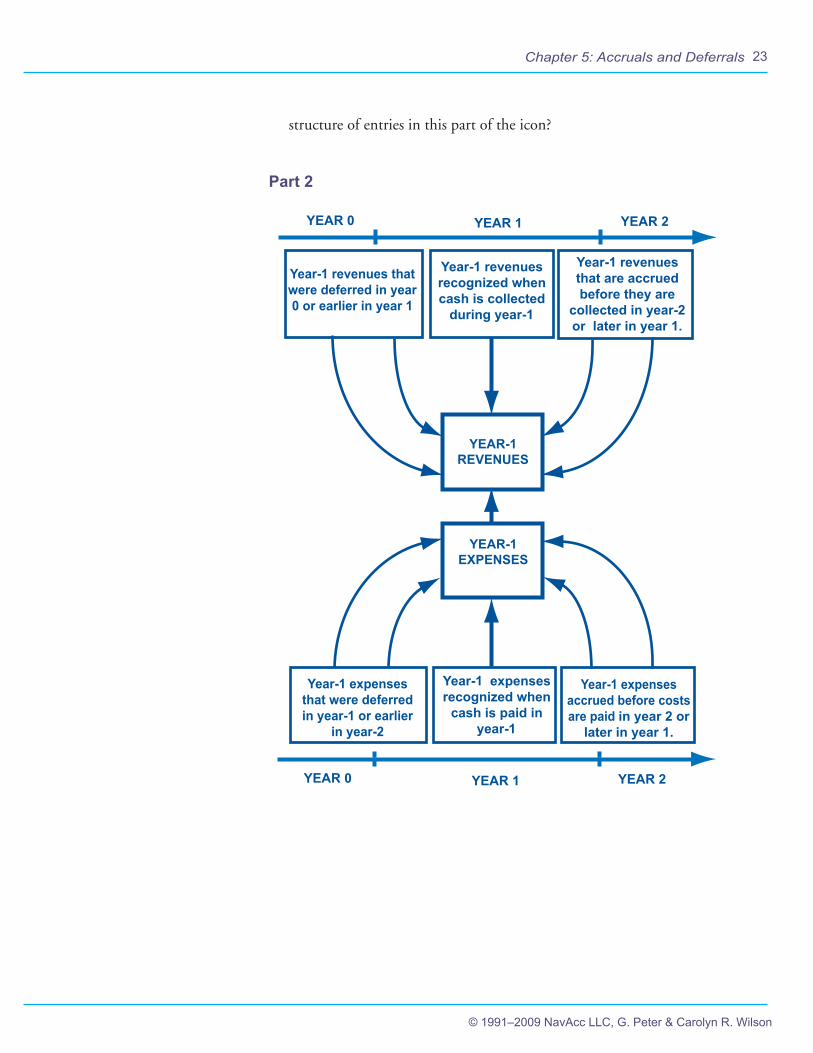

f ) Below is a special case of the income recognition icon where the current year is year 1. Identify all of the year-0 and year-1 Cardinal entries that belong to each of the icon’s six categories (or indicate that none of the entries belong to a category). What is the general

23

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

structure of entries in this part of the icon?

Part 2

YEAR 1YEAR 0 YEAR 2

YEAR-1 REVENUES

YEAR-1 EXPENSES

Year-1 revenues that were deferred in year 0 or earlier in year 1

Year-1 revenues recognized when cash is collected

during year-1

Year-1 revenues that are accrued before they are

collected in year-2 or later in year 1.

Year-1 expenses that were deferred in year-1 or earlier

in year-2

Year-1 expenses recognized when

cash is paid in year-1

Year-1 expenses accrued before costs are paid in year 2 or

later in year 1.

YEAR 1YEAR 0 YEAR 2

24

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Navigating Accounting ®

a) True or False: Gap would record higher interest and depreciation expenses if it were to classify its operating leases as capital leases.

b) Identify items on Gap’s balance sheet that relate to situations where Gap has likely made a payment that has not yet been expensed.

c) Identify items on Gap’s balance sheet that relate to situations where Gap has recognized an expense that has not yet been paid.

Search IconThis exercise requires you to search for information.

Usage IconThis exercise helps you learn how accounting reports are used by investors, creditors, and other stakeholders.

25

© 1991–2009 NavAcc LLC, G. Peter & Carolyn R. Wilson

Chapter 5: Accruals and Deferrals

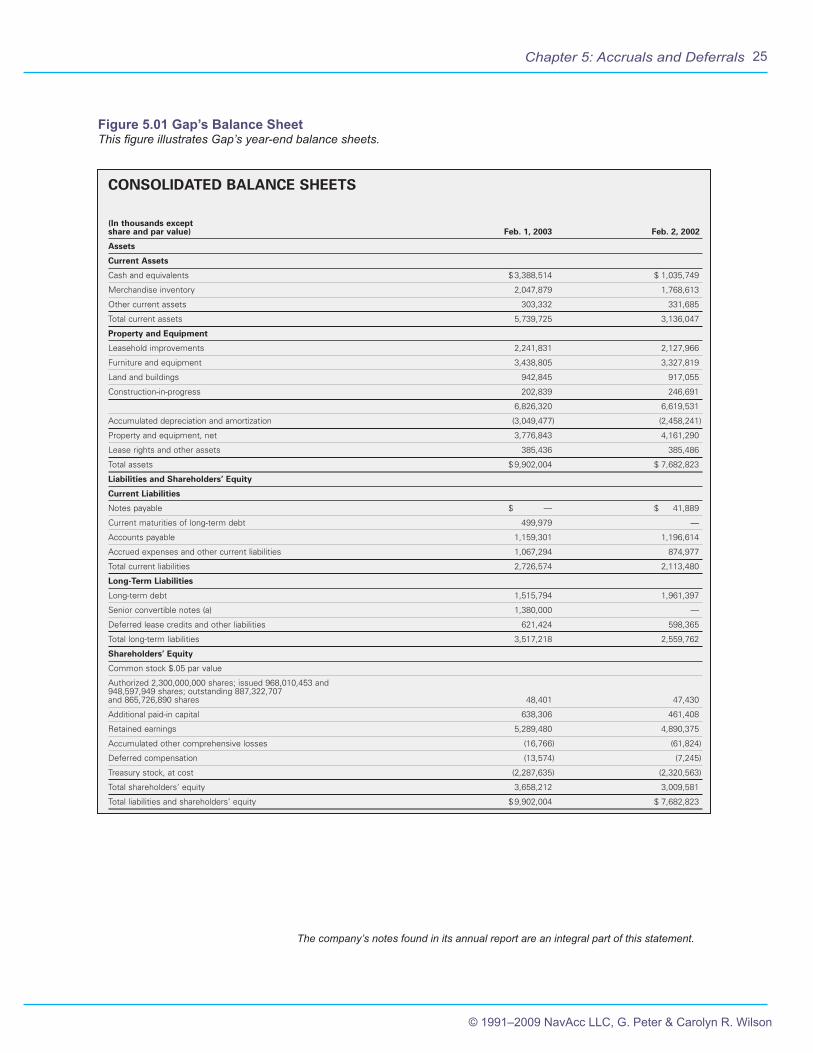

Figure 5.01 Gap’s Balance SheetThis figure illustrates Gap’s year-end balance sheets.

The company’s notes found in its annual report are an integral part of this statement.

CONSOLIDATED BALANCE SHEETS

(In thousands exceptshare and par value) Feb. 1, 2003 Feb. 2, 2002

Assets

Current Assets

Cash and equivalents $ 3,388,514 $ 1,035,749

Merchandise inventory 2,047,879 1,768,613

Other current assets 303,332 331,685

Total current assets 5,739,725 3,136,047

Property and Equipment

Leasehold improvements 2,241,831 2,127,966

Furniture and equipment 3,438,805 3,327,819

Land and buildings 942,845 917,055

Construction-in-progress 202,839 246,691

6,826,320 6,619,531

Accumulated depreciation and amortization (3,049,477) (2,458,241)

Property and equipment, net 3,776,843 4,161,290

Lease rights and other assets 385,436 385,486

Total assets $ 9,902,004 $ 7,682,823

Liabilities and Shareholders’ Equity

Current Liabilities

Notes payable $ — $ 41,889

Current maturities of long-term debt 499,979 —

Accounts payable 1,159,301 1,196,614

Accrued expenses and other current liabilities 1,067,294 874,977

Total current liabilities 2,726,574 2,113,480

Long-Term Liabilities

Long-term debt 1,515,794 1,961,397

Senior convertible notes (a) 1,380,000 —

Deferred lease credits and other liabilities 621,424 598,365

Total long-term liabilities 3,517,218 2,559,762

Shareholders’ Equity

Common stock $.05 par value

Authorized 2,300,000,000 shares; issued 968,010,453 and 948,597,949 shares; outstanding 887,322,707and 865,726,890 shares 48,401 47,430

Additional paid-in capital 638,306 461,408

Retained earnings 5,289,480 4,890,375

Accumulated other comprehensive losses (16,766) (61,824)

Deferred compensation (13,574) (7,245)

Treasury stock, at cost (2,287,635) (2,320,563)

Total shareholders’ equity 3,658,212 3,009,581

Total liabilities and shareholders’ equity $ 9,902,004 $ 7,682,823

See Notes to Consolidated Financial Statements.

(a) See Note B.

34

![CHAPTER 4: ACTUATED CONTROLLER TIMING PROCESSES … · Chapter 4: Actuated Controller Timing Processes 89 [2012.12.19] CHAPTER 4: ACTUATED CONTROLLER TIMING PROCESSES This chapter](https://img.pdfslide.us/doc/110x75/5f68dd109d404110520123b9/chapter-4-actuated-controller-timing-processes-chapter-4-actuated-controller-timing.jpg)

![chapter 3 timing final print - INFLIBNETshodhganga.inflibnet.ac.in/bitstream/10603/9392/3/12. chapter 3.pdf · [62] CHAPTER 3 TIMING OFFSET ESTIMATION iming synchronization is one](https://img.pdfslide.us/doc/110x75/5f7fc8fe18756b64d5250175/chapter-3-timing-final-print-chapter-3pdf-62-chapter-3-timing-offset-estimation.jpg)