Embed Size (px)

Citation preview

Accounting for Merchandising

Businesses

Chapter 4 T.Haya Alajaji

Nature of Businesses .

Special terms of Merchandising businesses .

Analysis of merchandising transactions.

Multiple-Step Income Statement

Objectives :

Ch4

Merchandising businesses

Service businesses

compute Net income

Selas Revenues Cost of goods Sold

Gross Profit

Merchandising Inventory

Analyze Merchandising

transactions

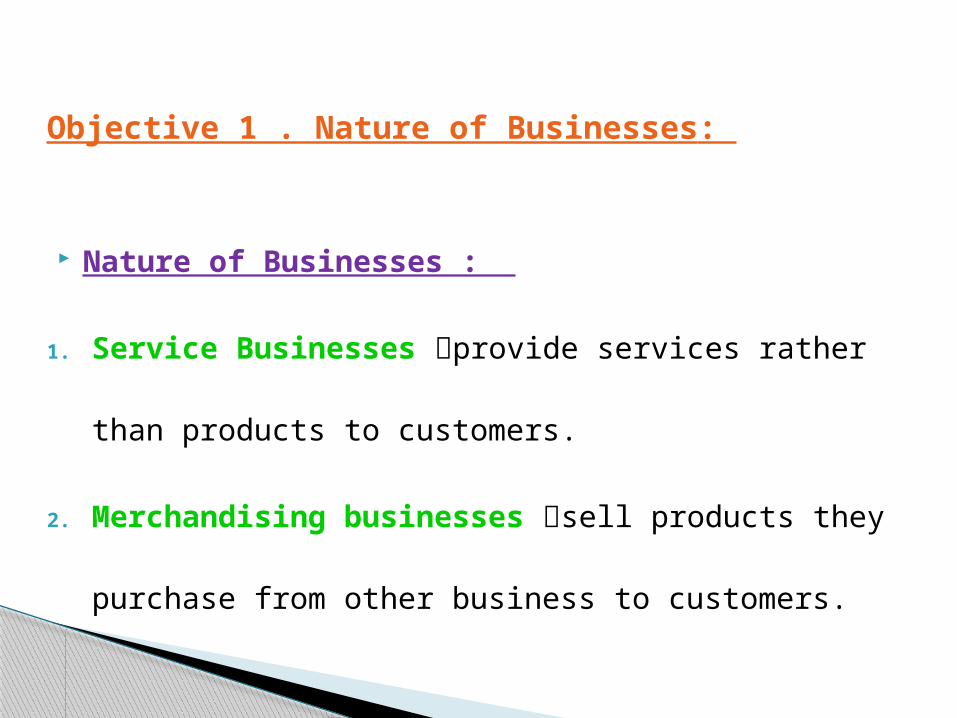

Nature of Businesses :

1. Service Businesses provide services rather

than products to customers.

2. Merchandising businesses sell products they

purchase from other business to customers.

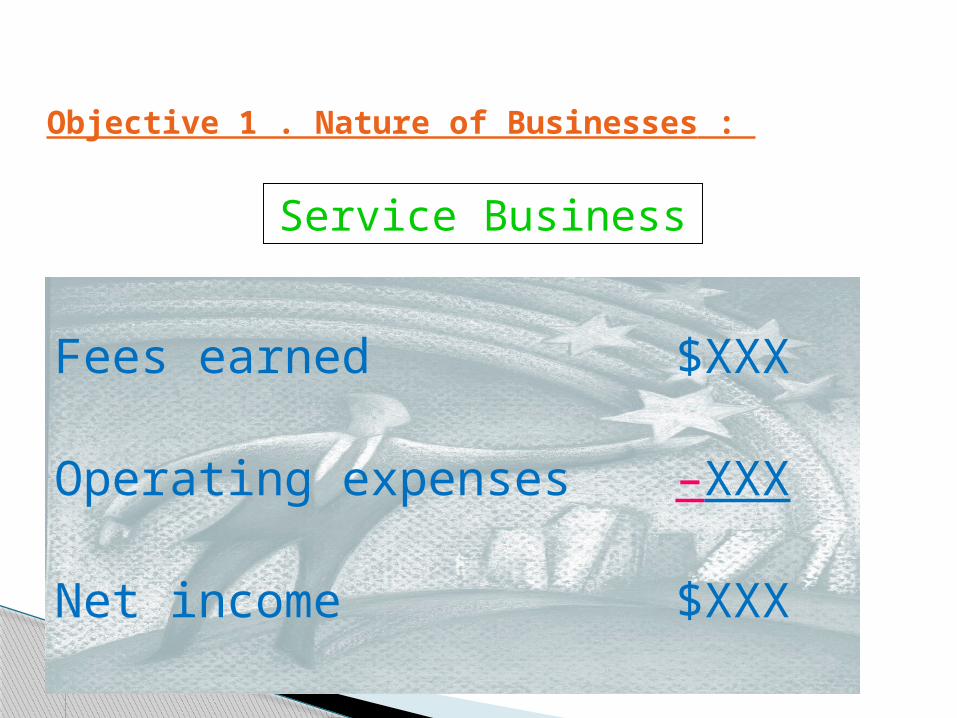

: Objective 1 . Nature of Businesses

Service Business

Fees earned $XXX

Operating expenses –XXX

Net income $XXX

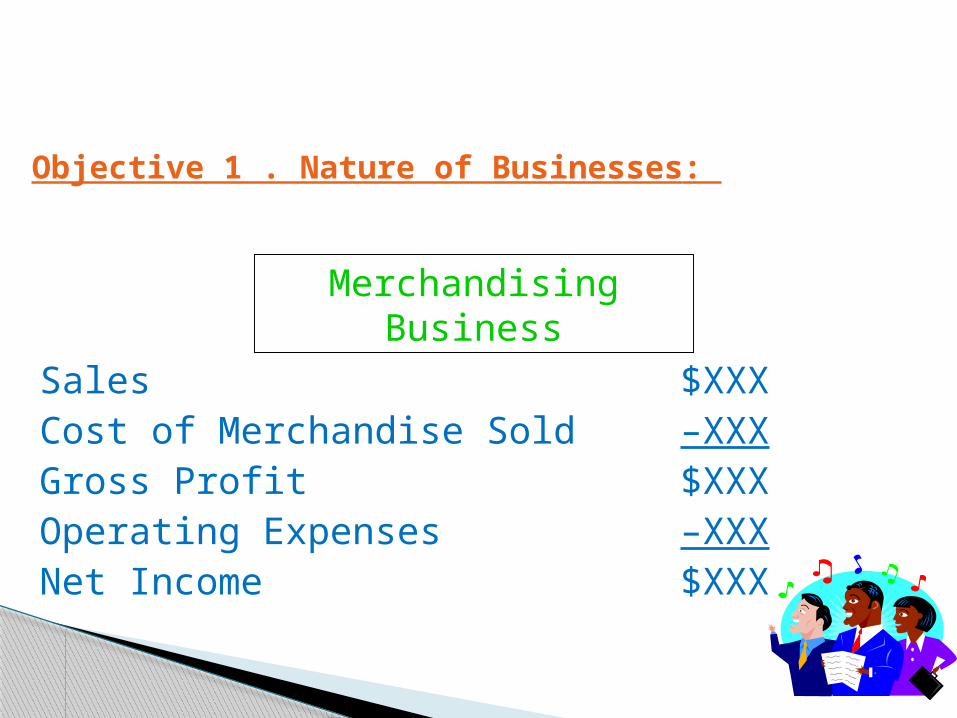

: Objective 1 . Nature of Businesses

Merchandising Business

Sales $XXXCost of Merchandise Sold –XXXGross Profit $XXXOperating Expenses –XXXNet Income $XXX

: Objective 1 . Nature of Businesses

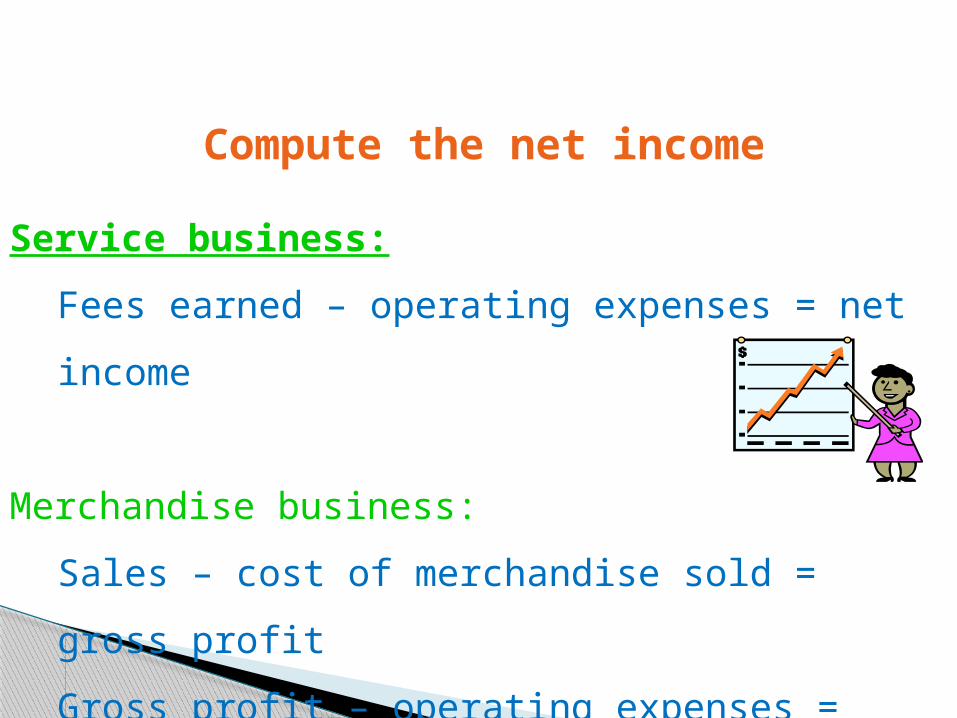

Service business:

Fees earned – operating expenses = net

income

Merchandise business:

Sales – cost of merchandise sold = gross

profit

Gross profit – operating expenses = net

income

Compute the net income

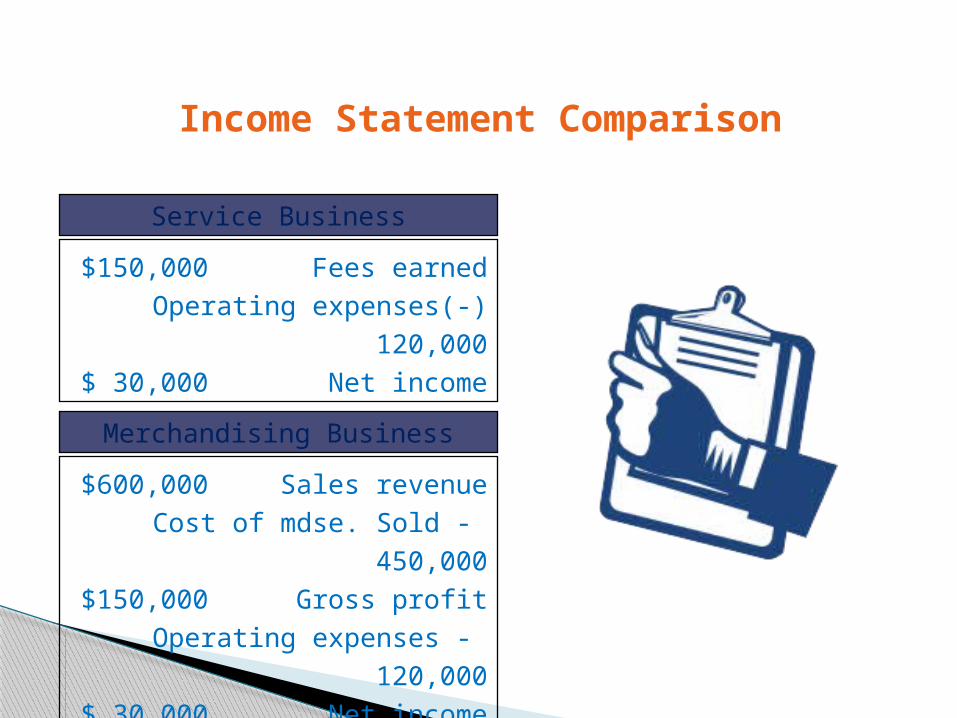

Income Statement Comparison

Fees earned$150,000Operating expenses(-)120,000

Net income$ 30,000

Service Business

Sales revenue$600,000Cost of mdse. Sold - 450,000

Gross profit$150,000Operating expenses - 120,000

Net income$ 30,000

Merchandising Business

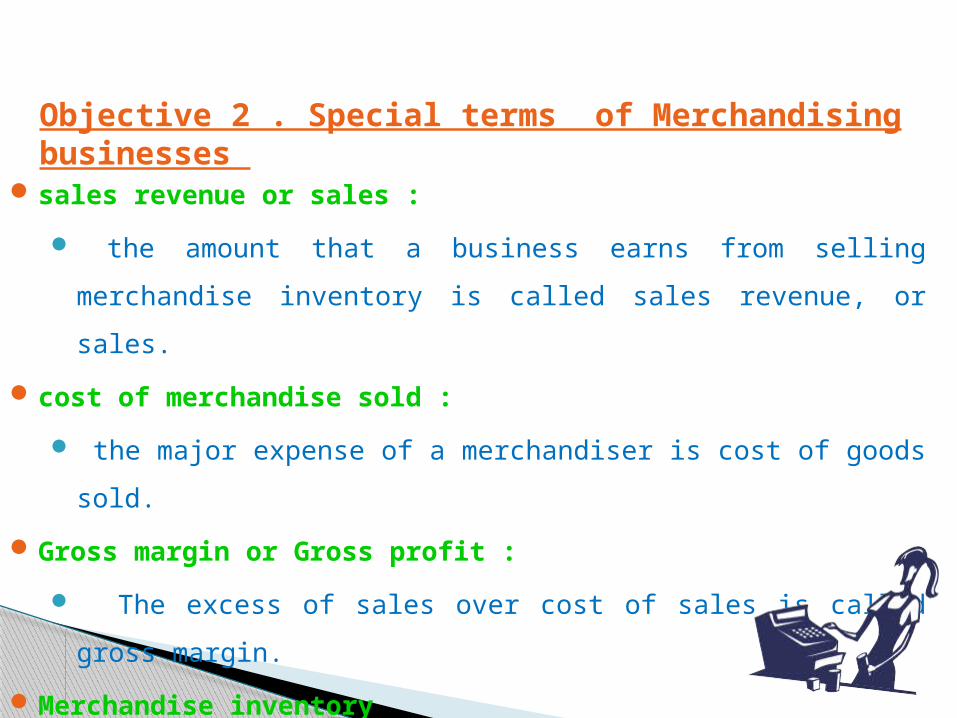

Objective 2 . Special terms of Merchandising businesses

sales revenue or sales :

the amount that a business earns from selling merchandise

inventory is called sales revenue, or sales.

cost of merchandise sold :

the major expense of a merchandiser is cost of goods sold.

Gross margin or Gross profit :

The excess of sales over cost of sales is called gross margin.

Merchandise inventory

Merchandise on hand at the end of an account period

Objective 3 Analyze Merchandising

transactions

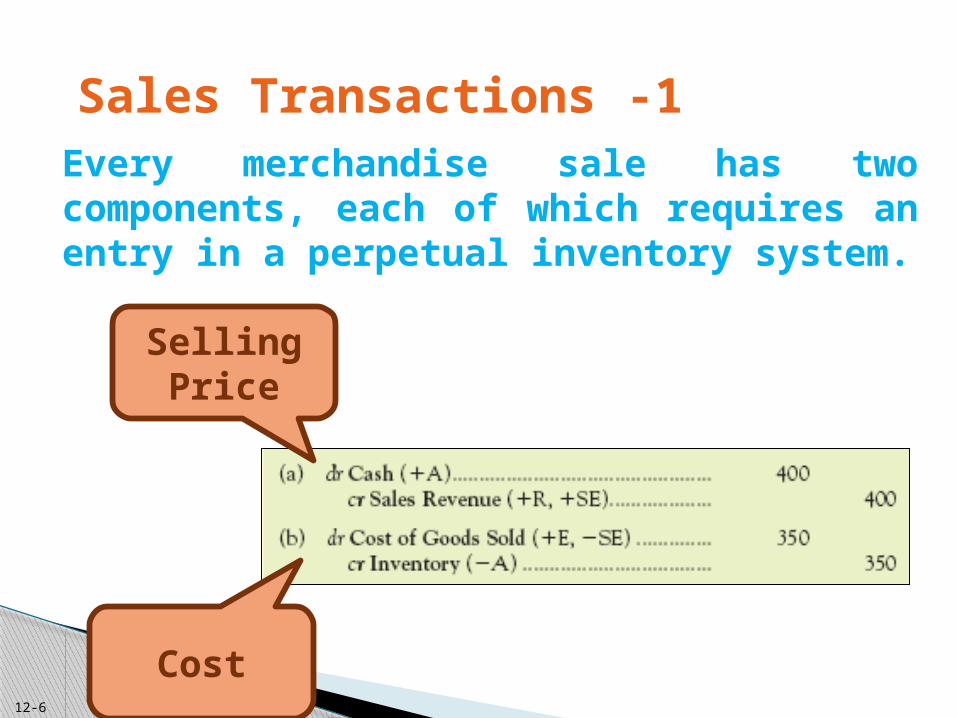

1 -Sales TransactionsEvery merchandise sale has two components, each of which requires an entry in a perpetual inventory system.

Selling Price

Cost6-12

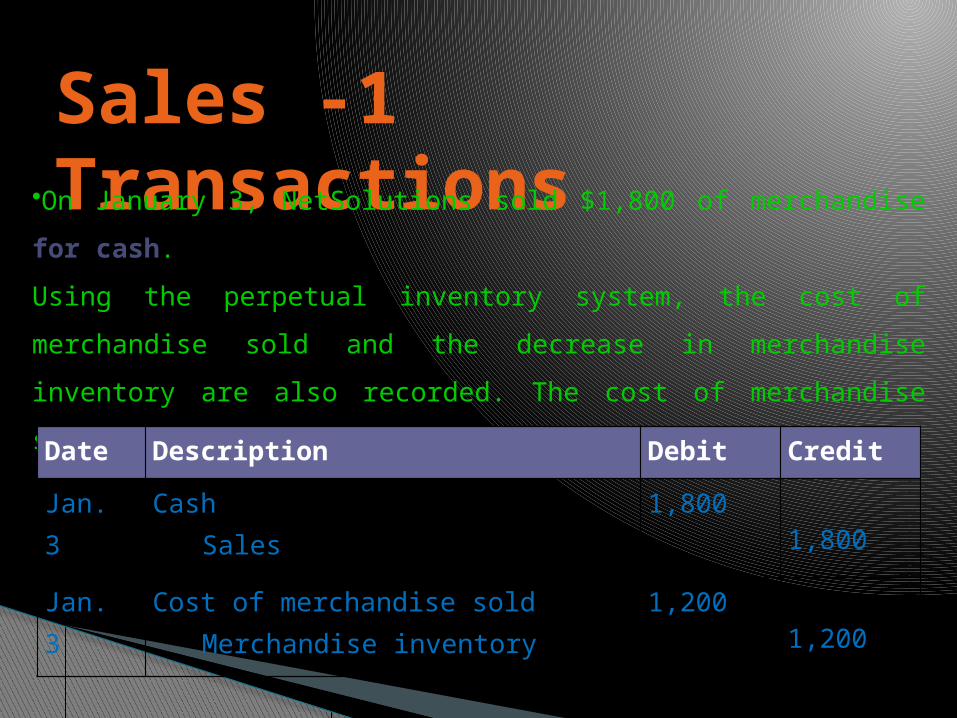

1 -Sales Transactions•On January 3, NetSolutions sold $1,800 of merchandise for cash.

Using the perpetual inventory system, the cost of merchandise

sold and the decrease in merchandise inventory are also recorded.

The cost of merchandise sold on January 3 is $1,200

Date Description Debit Credit

Jan. 3 CashSales

1,8001,800

Jan. 3 Cost of merchandise soldMerchandise inventory

1,2001,200

1 -Sales Transactions

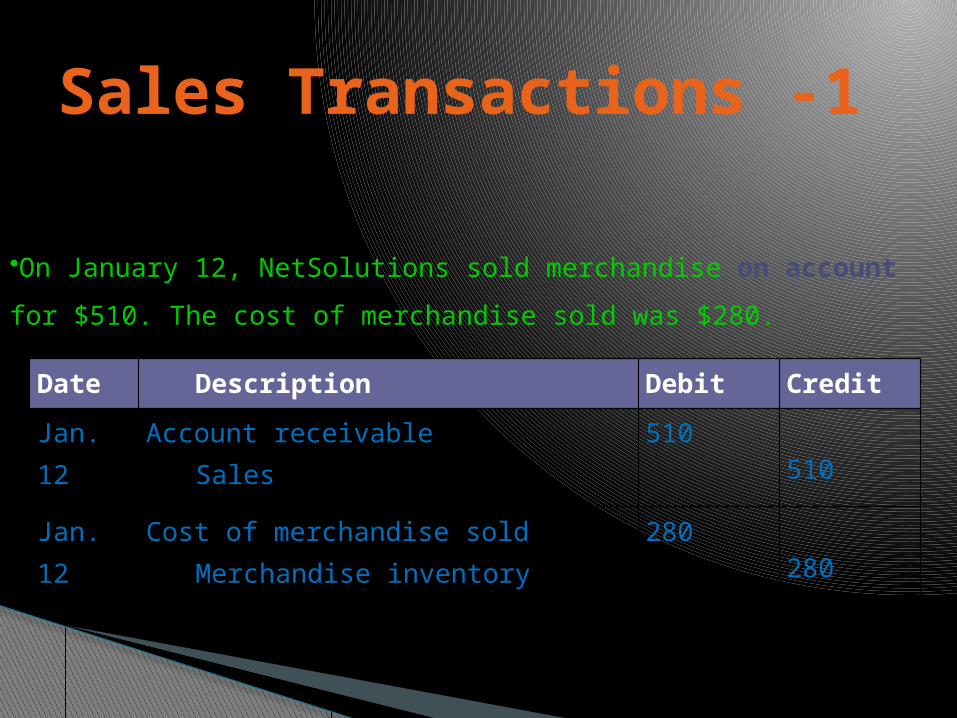

•On January 12, NetSolutions sold merchandise on account for $510.

The cost of merchandise sold was $280.

Date Description Debit Credit

Jan. 12 Account receivableSales

510510

Jan. 12 Cost of merchandise soldMerchandise inventory

280280

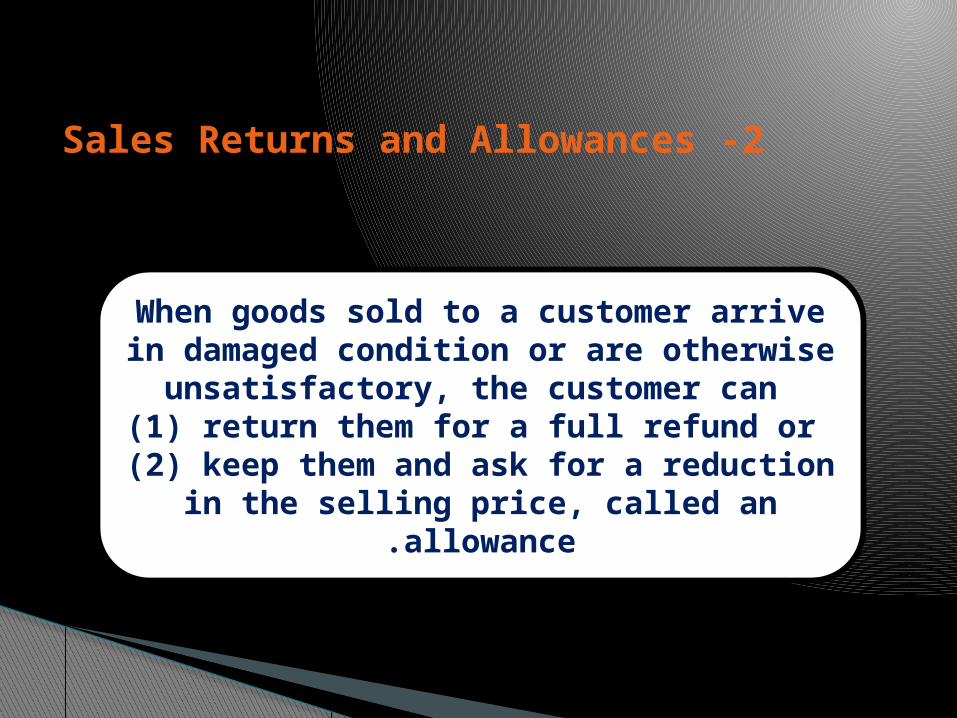

2 -Sales Returns and Allowances

When goods sold to a customer arrive in damaged condition or are otherwise

unsatisfactory, the customer can (1) return them for a full refund or

(2) keep them and ask for a reduction in the selling price, called an

allowance.

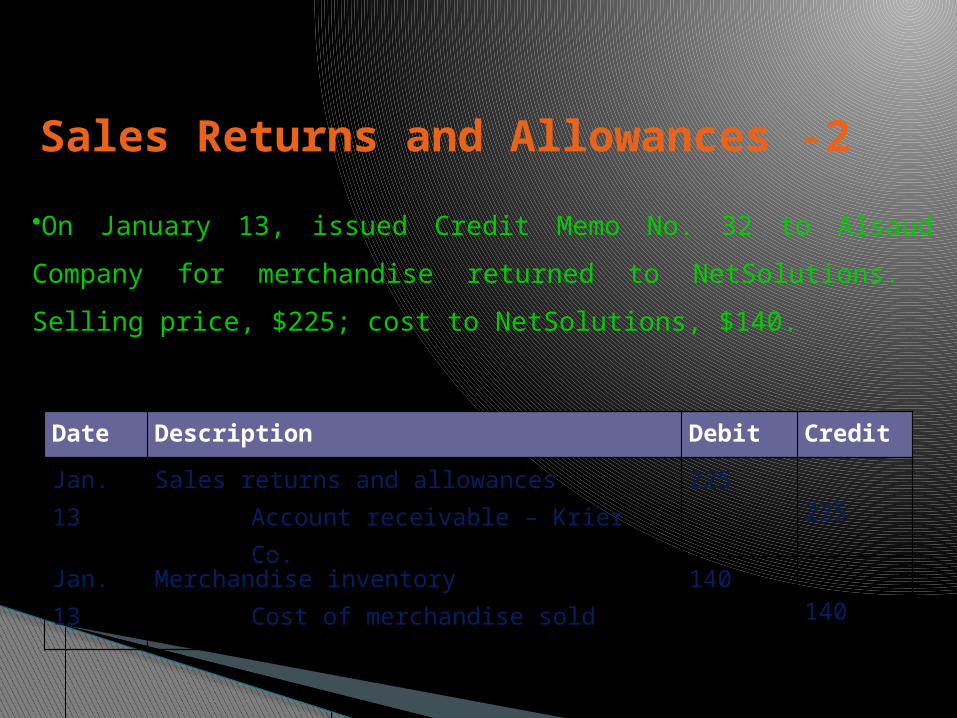

2 -Sales Returns and Allowances

•On January 13, issued Credit Memo No. 32 to Alsaud Company for

merchandise returned to NetSolutions. Selling price, $225; cost to

NetSolutions, $140.

Date Description Debit Credit

Jan. 13 Sales returns and allowancesAccount receivable – Krier Co.

225225

Jan. 13 Merchandise inventoryCost of merchandise sold

140140

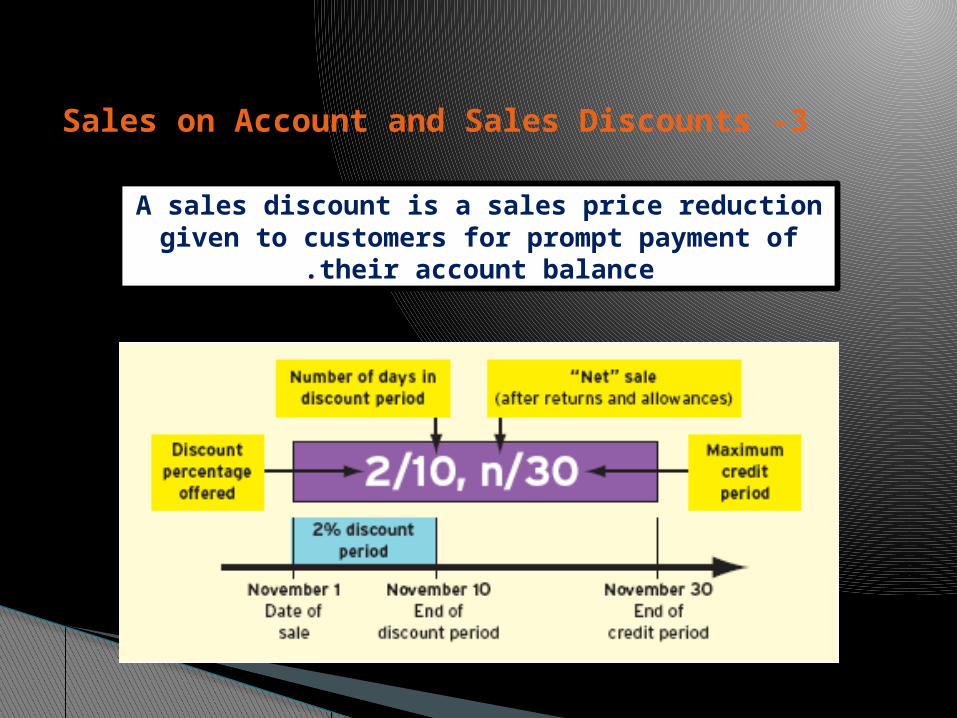

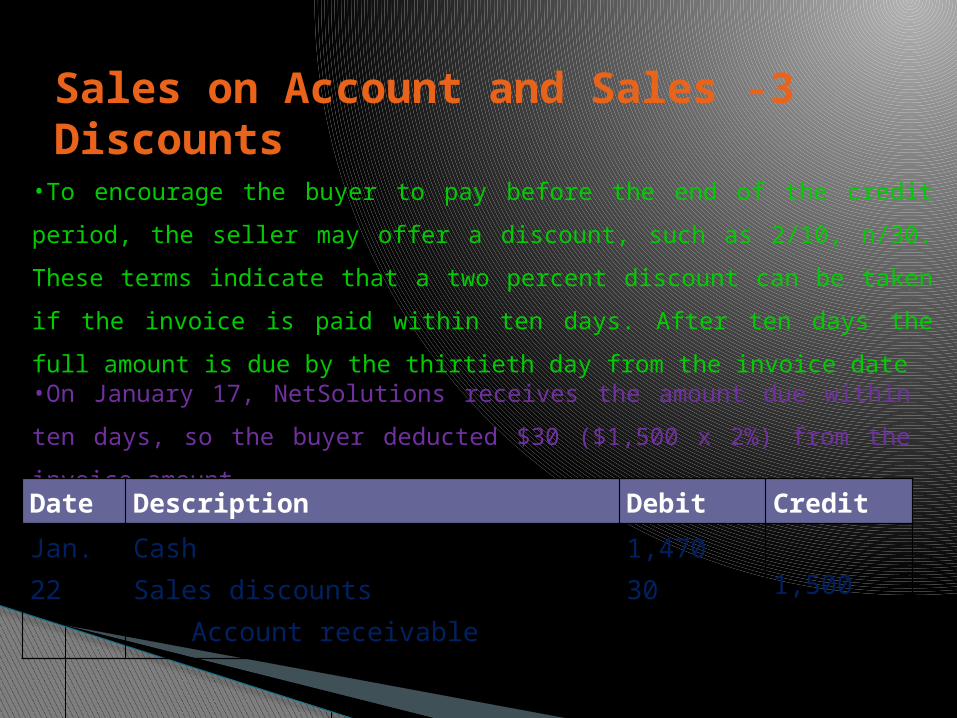

3 -Sales on Account and Sales Discounts

A sales discount is a sales price reduction given to customers for prompt payment of

their account balance.

3 -Sales on Account and Sales Discounts

•To encourage the buyer to pay before the end of the credit period, the

seller may offer a discount, such as 2/10, n/30. These terms indicate that

a two percent discount can be taken if the invoice is paid within ten days.

After ten days the full amount is due by the thirtieth day from the invoice

date•On January 17, NetSolutions receives the amount due within ten days,

so the buyer deducted $30 ($1,500 x 2%) from the invoice amount

Date Description Debit Credit

Jan. 22

Cash Sales discounts

Account receivable

1,47030 1,500

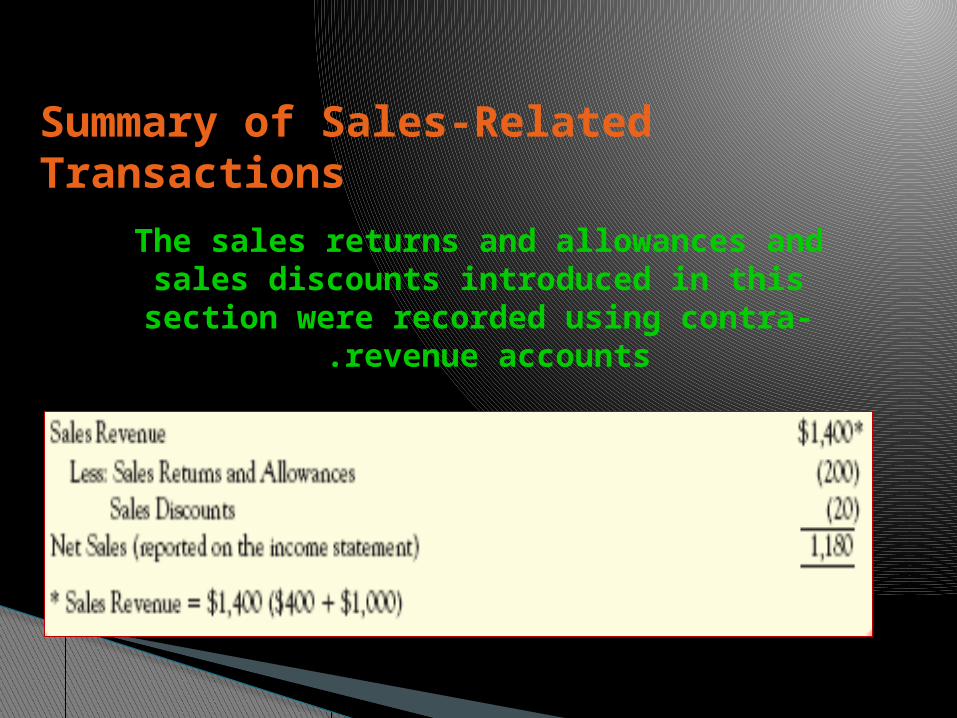

Summary of Sales-Related Transactions

The sales returns and allowances and sales discounts introduced in this section

were recorded using contra-revenue accounts .

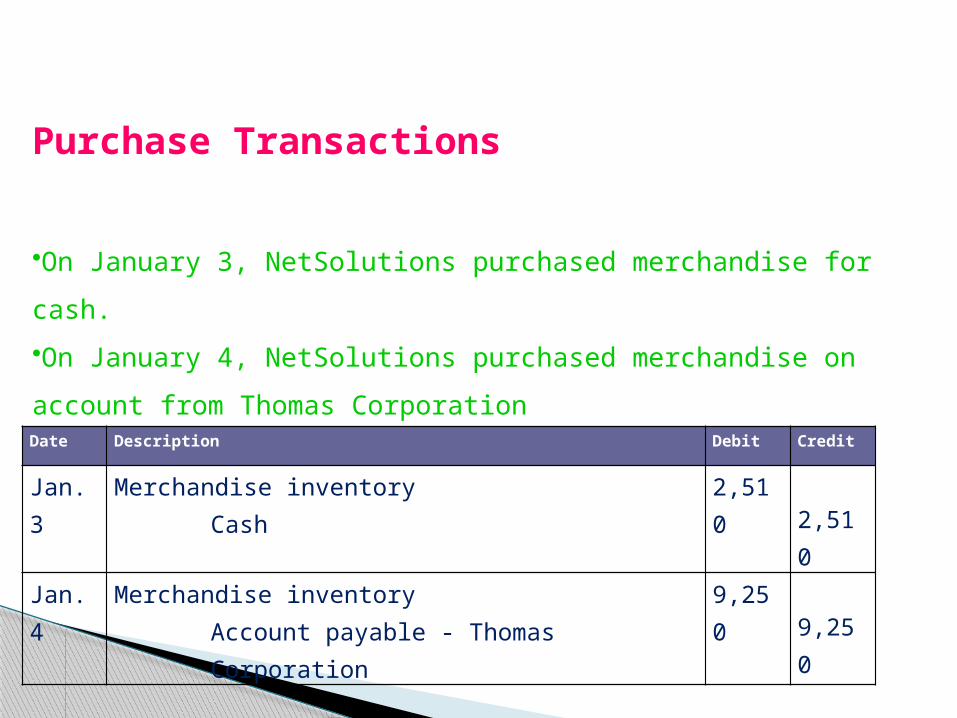

Date Description Debit Credit

Jan. 3 Merchandise inventoryCash

2,5102,510

Jan. 4 Merchandise inventoryAccount payable - Thomas Corporation

9,2509,250

Purchase Transactions

•On January 3, NetSolutions purchased merchandise for cash.

•On January 4, NetSolutions purchased merchandise on account

from Thomas Corporation

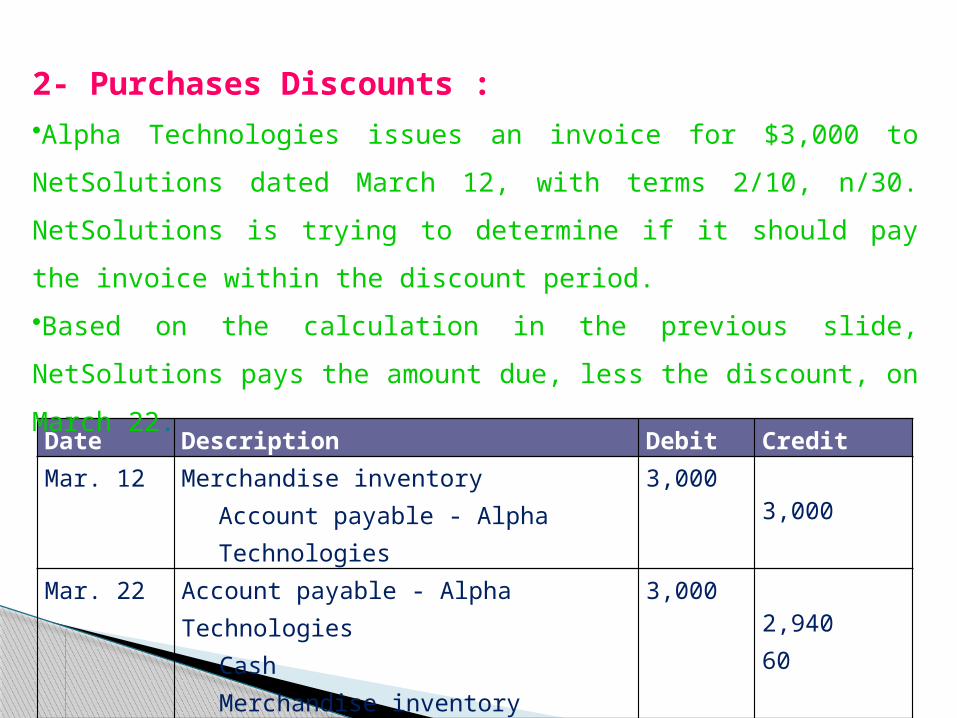

Date Description Debit CreditMar. 12 Merchandise inventory

Account payable - Alpha Technologies

3,0003,000

Mar. 22 Account payable - Alpha Technologies

CashMerchandise inventory

3,0002,94060

2- Purchases Discounts :•Alpha Technologies issues an invoice for $3,000 to NetSolutions

dated March 12, with terms 2/10, n/30. NetSolutions is trying to

determine if it should pay the invoice within the discount period.

•Based on the calculation in the previous slide, NetSolutions pays

the amount due, less the discount, on March 22.

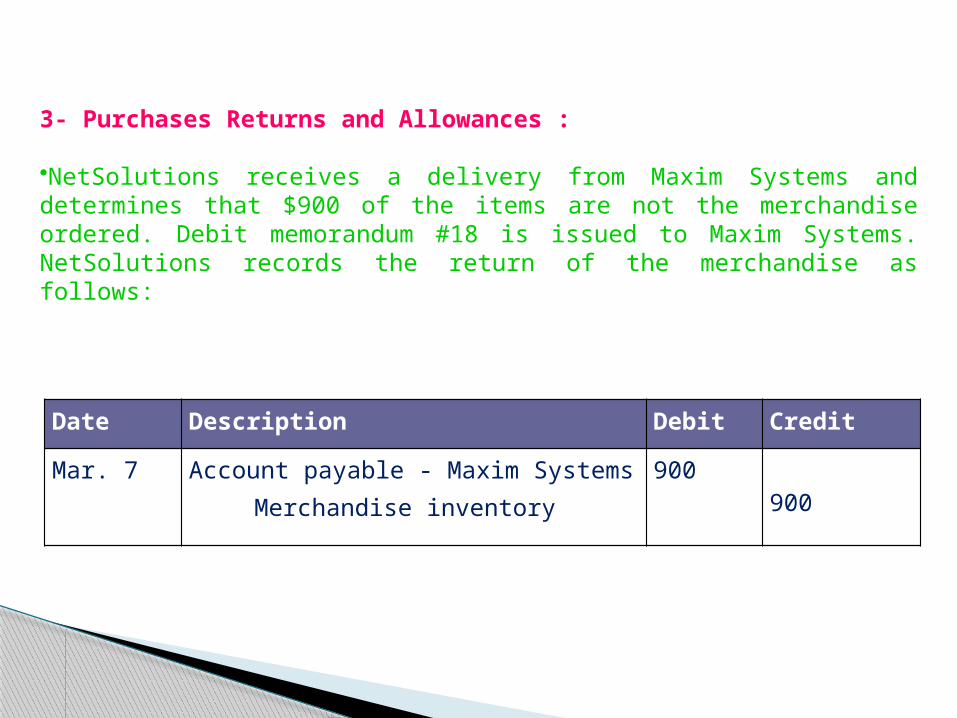

Date Description Debit Credit

Mar. 7 Account payable - Maxim SystemsMerchandise inventory

900900

3- Purchases Returns and Allowances :

•NetSolutions receives a delivery from Maxim Systems and determines that $900 of the items are not the merchandise ordered. Debit memorandum #18 is issued to Maxim Systems. NetSolutions records the return of the merchandise as follows:

Multiple-Step Income Statement

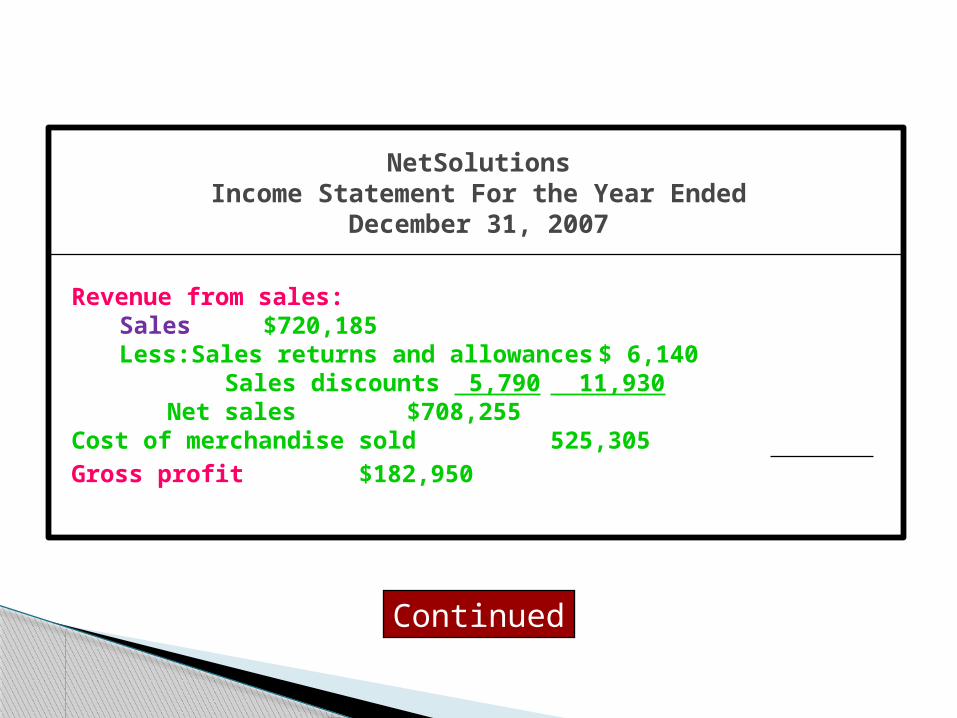

Revenue from sales:Sales $720,185Less:Sales returns and allowances $ 6,140

Sales discounts 5,790 11,930Net sales $708,255

Cost of merchandise sold 525,305Gross profit $182,950

NetSolutionsIncome Statement For the Year

Ended December 31, 2007

Continued

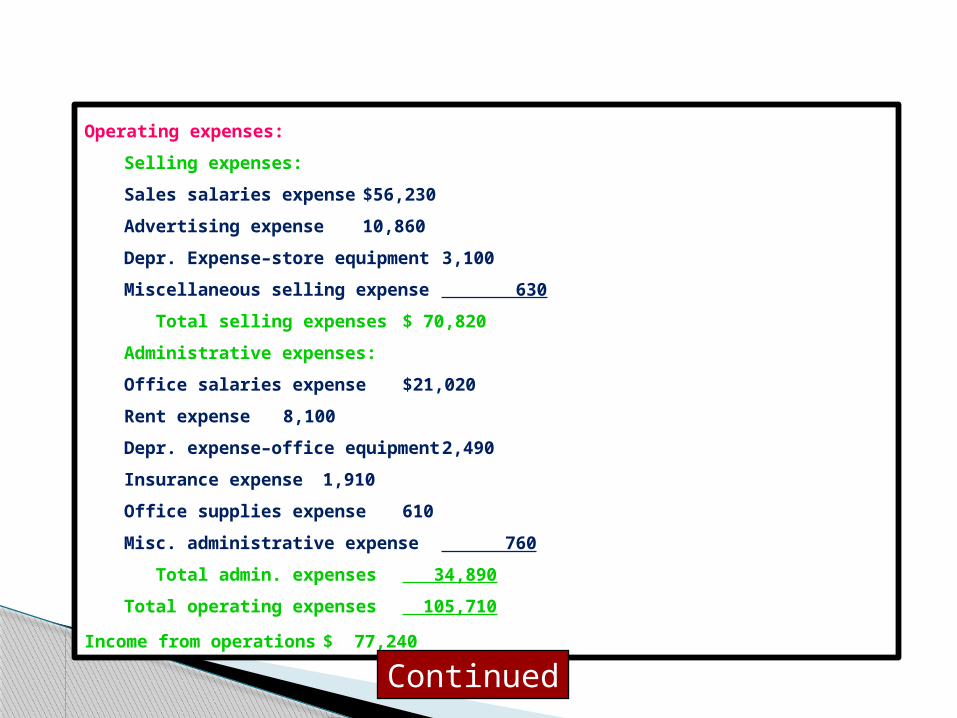

Operating expenses:

Selling expenses:

Sales salaries expense $56,230

Advertising expense 10,860

Depr. Expense–store equipment 3,100

Miscellaneous selling expense 630

Total selling expenses $ 70,820

Administrative expenses:

Office salaries expense $21,020

Rent expense 8,100

Depr. expense–office equipment2,490

Insurance expense 1,910

Office supplies expense 610

Misc. administrative expense 760

Total admin. expenses 34,890

Total operating expenses 105,710

Income from operations $ 77,240Continued

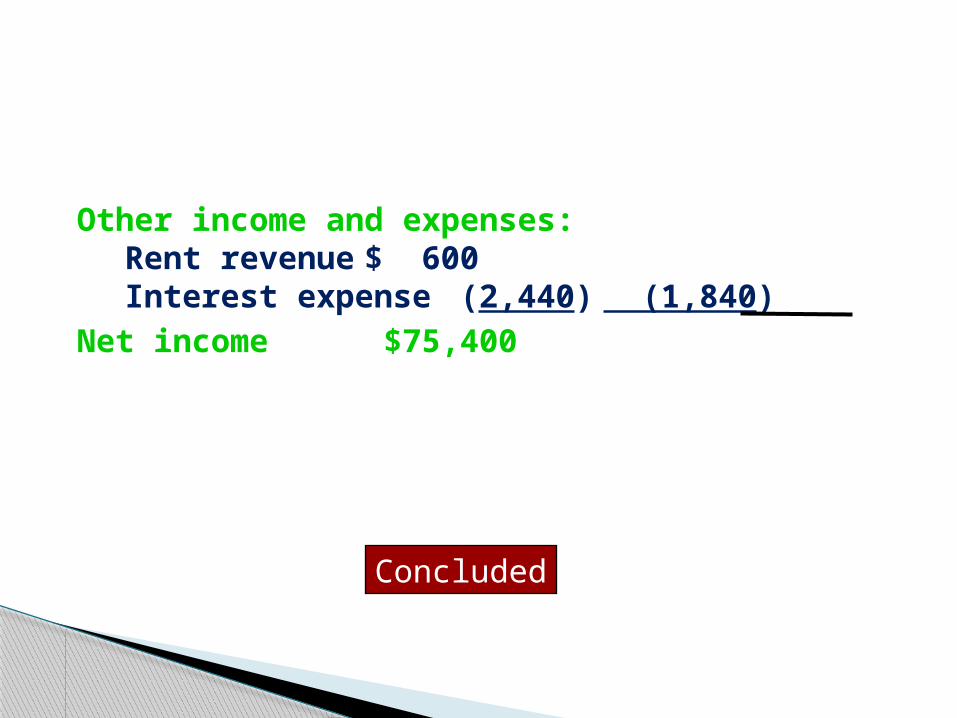

Other income and expenses:Rent revenue $ 600Interest expense (2,440)

(1,840)Net income $75,400

Concluded

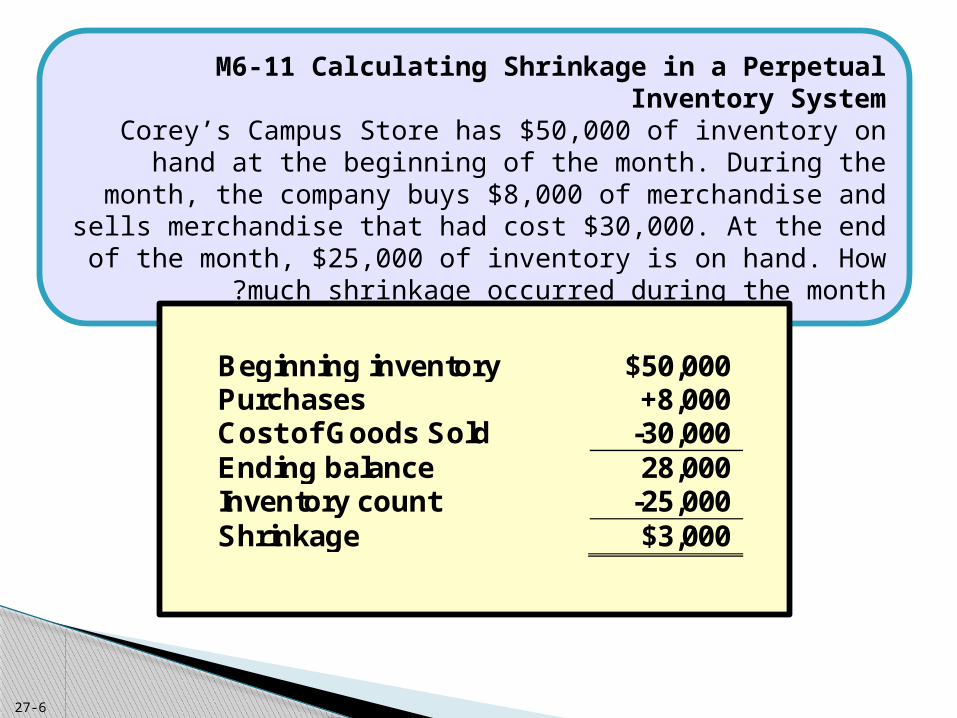

M6-11 Calculating Shrinkage in a Perpetual Inventory System

Corey’s Campus Store has $50,000 of inventory on hand at the beginning of the month. During the month, the company buys $8,000 of merchandise and sells merchandise that had cost $30,000. At the end of the month, $25,000 of inventory is on hand. How much shrinkage occurred during the month?

Beginning inventory $50,000 Purchases +8,000 Cost of Goods Sold -30,000 Ending balance 28,000 Inventory count -25,000 Shrinkage $3,000

6-27