Embed Size (px)

Citation preview

Chapter 4

Accounting Entries in General Journal and General Ledger – Merchandising Business

1

Merchandising Operation

2

Merchandising Companies

Buy and Sell Goods

Wholesaler Retailer Consumer

Merchandising Operation

3

The operating

cycle of a

merchandising

company

ordinarily is

longer than that

of a service

company.

Operating

Cycles

Merchandising Operation

4

Income Measurement Statement of Profit or Loss

Sales 1000

Less Costs of goods sold (COGS) (300)

Gross Profit 700

Less Operating Expense (250)Net Income (Loss) 450

5

See Cost of Goods Sold Worksheet

Merchandising Operation

6

Cost Measurement

1. Periodic Inventory System

• Do not keep detailed records of the goods on hand.

• Cost of goods sold determined by count at the end of the accounting period.

2. Perpetual Inventory System

• Maintain detailed records of the cost of each inventory purchase and sale.

• Records continuously show inventory that should be on hand.

• Company determines cost of goods sold each time a sale occurs.

Periodic Inventory System

7

Cost of Goods Sold (COGS)

Periodic Inventory System

8

Cost of Goods Sold (COGS)

Freight

9

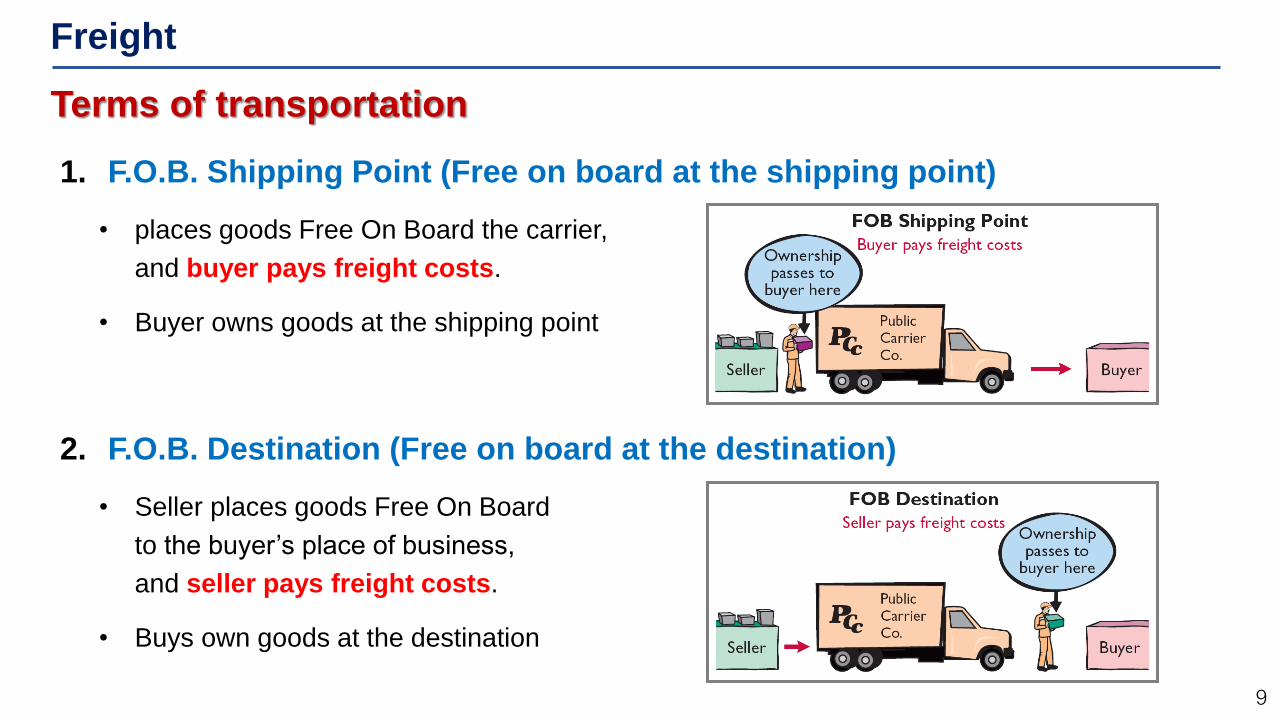

Terms of transportation

1. F.O.B. Shipping Point (Free on board at the shipping point)

• places goods Free On Board the carrier,

and buyer pays freight costs.

• Buyer owns goods at the shipping point

2. F.O.B. Destination (Free on board at the destination)

• Seller places goods Free On Board

to the buyer’s place of business,

and seller pays freight costs.

• Buys own goods at the destination

Discounts

10

1. Trade Discount

• Discount immediately when purchase/sell goods

• E.g. At department store, buy shoes 800 Baht discount 10% pay only 720 Baht

• No accounting record for cash discounts

• Record purchase and sales accounts after deducting cash discounts

2. Cash Discount

• Discount only when the buyers or sellers pay for goods within credit term

• If buyers or sellers pay within credit term, cash collected is less than invoice amount

• Record “Purchase Discounts” or “Sales Discounts”

• Record full amount of purchase and sales

Cash discount (Credit terms)

11

n/30 Pay within 30 days after purchasing

n/60 Pay within 60 days after purchasing

3/10, n/30 3% discount if paid within 10 days. If not, the full amount is due within 30 days

5/20, n/45 5% discount if paid within 20 days. If not, the full amount is due within 45 days

n/EOM Pay within “end of month” (e.g. buy 15th –> must pay within 30th)

3/10, EOM 3% discount if paid within 10 days. If not, the full amount is due at the end of month

Question:

On January 1st, 2017, the company buys goods 1,000 baht on credit. The cash discount

term is 5/10, n/60. How much the company has to pay to the seller if the company;

1. Pay on January 9th, 2017

……………………………………………………………………………………………..

2. Pay on January 20th, 2017

……………………………………………………………………………………………..

Questions

12

1. The statement for a merchandiser shows each of the

following features except:

a. gross profit.

b. cost of goods sold.

c. a sales revenue section.

d. investing activities section.

Questions

13

2. What is the difference between income of service business and income of merchandising

business?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

3. What is the difference between expenses of service business and expenses of

merchandising business?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

Questions

14

4. How is “inventory” account shown on statement of financial position when a

merchandising company applying periodic or perpetual inventory system?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

5. How is “inventory” account shown on statement of profit or loss when a merchandising

company applying periodic or perpetual inventory system?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

Questions

15

6. What is the difference of accounting records for purchase transactions between periodic and

perpetual inventory system?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

7. What is the difference of accounting records for sales transactions between periodic and

perpetual inventory system?

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

...............................................................................................................................................

Questions

16

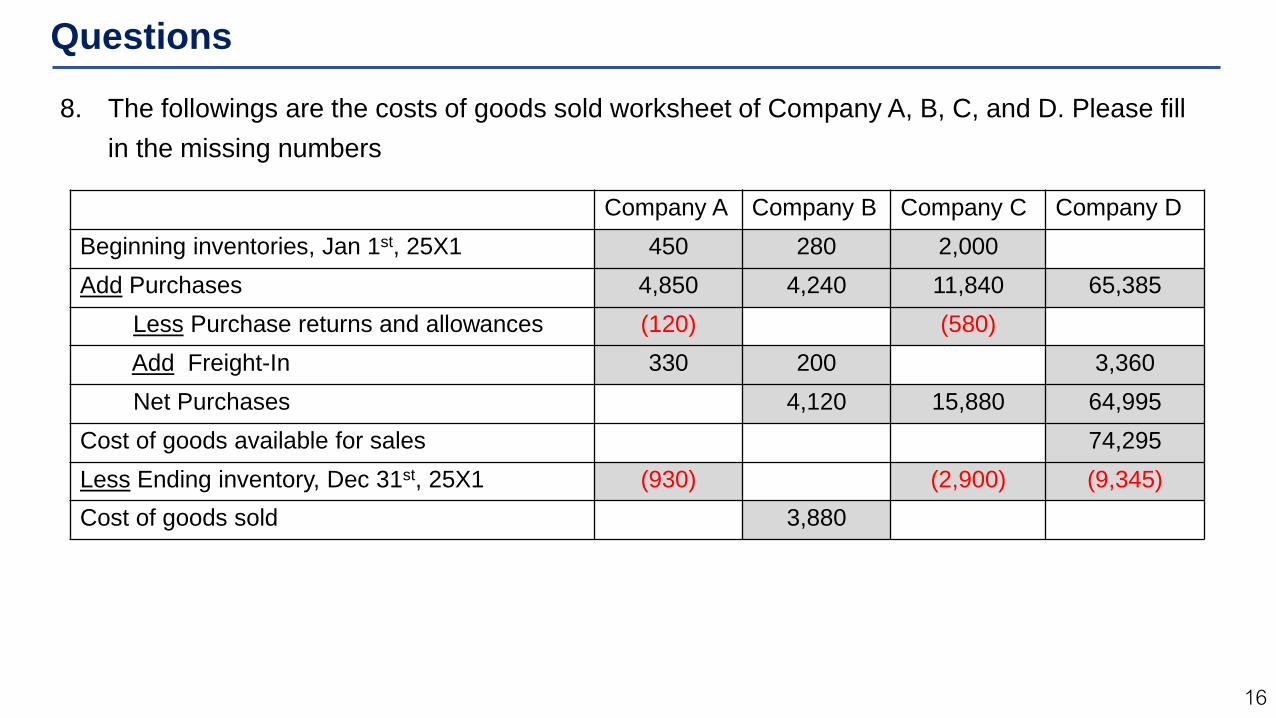

8. The followings are the costs of goods sold worksheet of Company A, B, C, and D. Please fill

in the missing numbers

Company A Company B Company C Company D

Beginning inventories, Jan 1st, 25X1 450 280 2,000

Add Purchases 4,850 4,240 11,840 65,385

Less Purchase returns and allowances (120) (580)

Add Freight-In 330 200 3,360

Net Purchases 4,120 15,880 64,995

Cost of goods available for sales 74,295

Less Ending inventory, Dec 31st, 25X1 (930) (2,900) (9,345)

Cost of goods sold 3,880

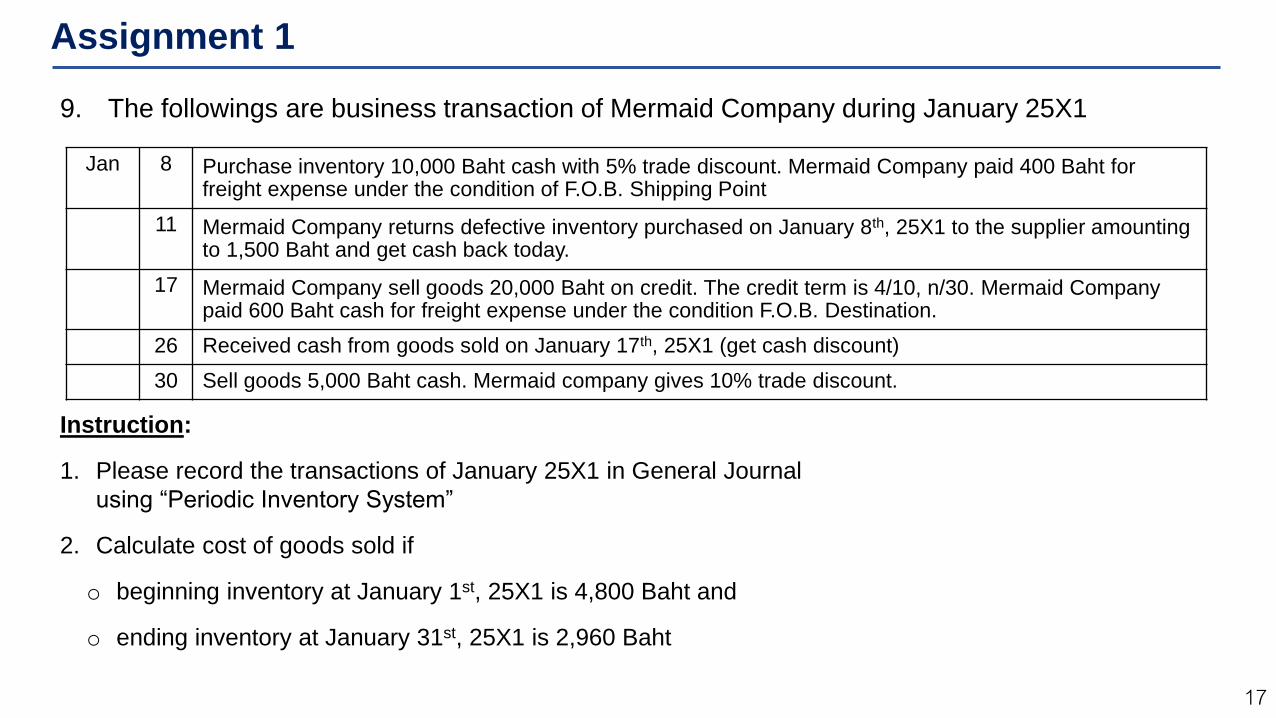

Assignment 1

17

9. The followings are business transaction of Mermaid Company during January 25X1

Instruction:

1. Please record the transactions of January 25X1 in General Journal

using “Periodic Inventory System”

2. Calculate cost of goods sold if

o beginning inventory at January 1st, 25X1 is 4,800 Baht and

o ending inventory at January 31st, 25X1 is 2,960 Baht

Jan 8 Purchase inventory 10,000 Baht cash with 5% trade discount. Mermaid Company paid 400 Baht for freight expense under the condition of F.O.B. Shipping Point

11 Mermaid Company returns defective inventory purchased on January 8th, 25X1 to the supplier amounting to 1,500 Baht and get cash back today.

17 Mermaid Company sell goods 20,000 Baht on credit. The credit term is 4/10, n/30. Mermaid Company paid 600 Baht cash for freight expense under the condition F.O.B. Destination.

26 Received cash from goods sold on January 17th, 25X1 (get cash discount)

30 Sell goods 5,000 Baht cash. Mermaid company gives 10% trade discount.

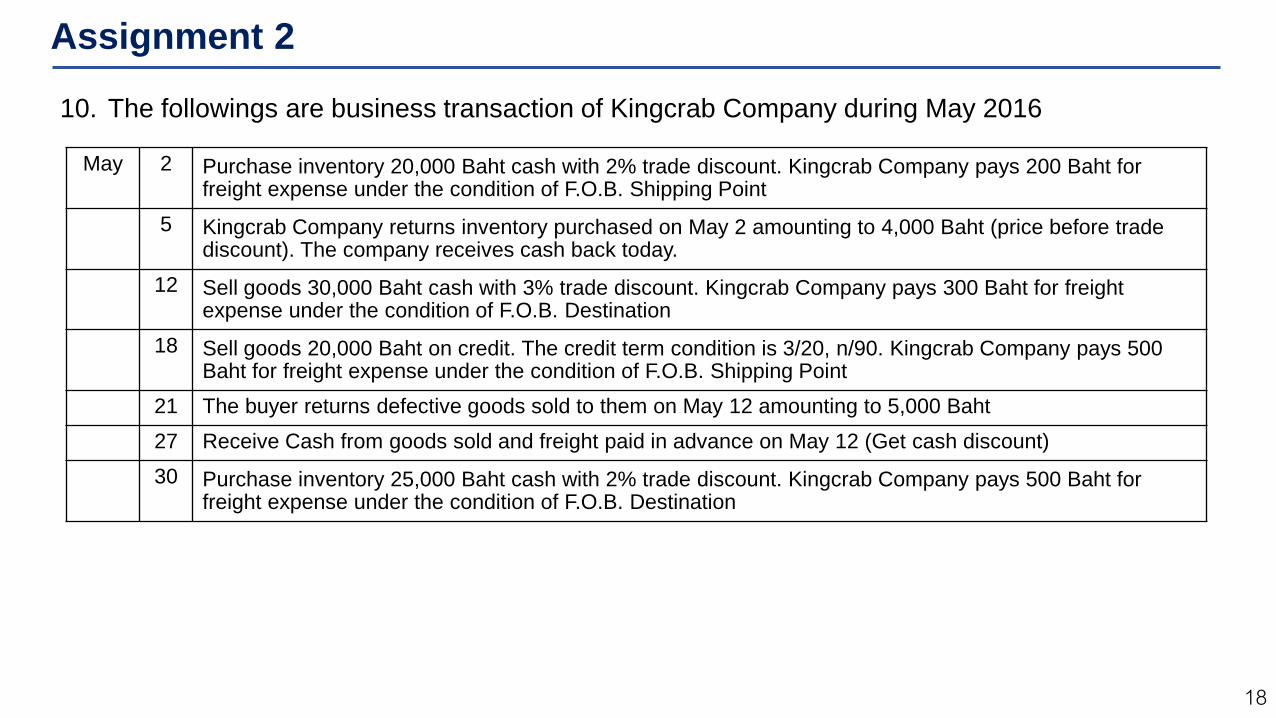

Assignment 2

18

10. The followings are business transaction of Kingcrab Company during May 2016

May 2 Purchase inventory 20,000 Baht cash with 2% trade discount. Kingcrab Company pays 200 Baht for freight expense under the condition of F.O.B. Shipping Point

5 Kingcrab Company returns inventory purchased on May 2 amounting to 4,000 Baht (price before trade discount). The company receives cash back today.

12 Sell goods 30,000 Baht cash with 3% trade discount. Kingcrab Company pays 300 Baht for freight expense under the condition of F.O.B. Destination

18 Sell goods 20,000 Baht on credit. The credit term condition is 3/20, n/90. Kingcrab Company pays 500 Baht for freight expense under the condition of F.O.B. Shipping Point

21 The buyer returns defective goods sold to them on May 12 amounting to 5,000 Baht

27 Receive Cash from goods sold and freight paid in advance on May 12 (Get cash discount)

30 Purchase inventory 25,000 Baht cash with 2% trade discount. Kingcrab Company pays 500 Baht for freight expense under the condition of F.O.B. Destination

Assignment 2

19

Instructions

1. Please record the transactions of May 2016 in General Journal

using “Periodic Inventory System”

2. Calculate cost of goods sold if

Beginning inventory at May 1st, 2016 is 40,120 Baht

Ending inventory at May 31st, 2016 is 30,500 Baht