Embed Size (px)

Citation preview

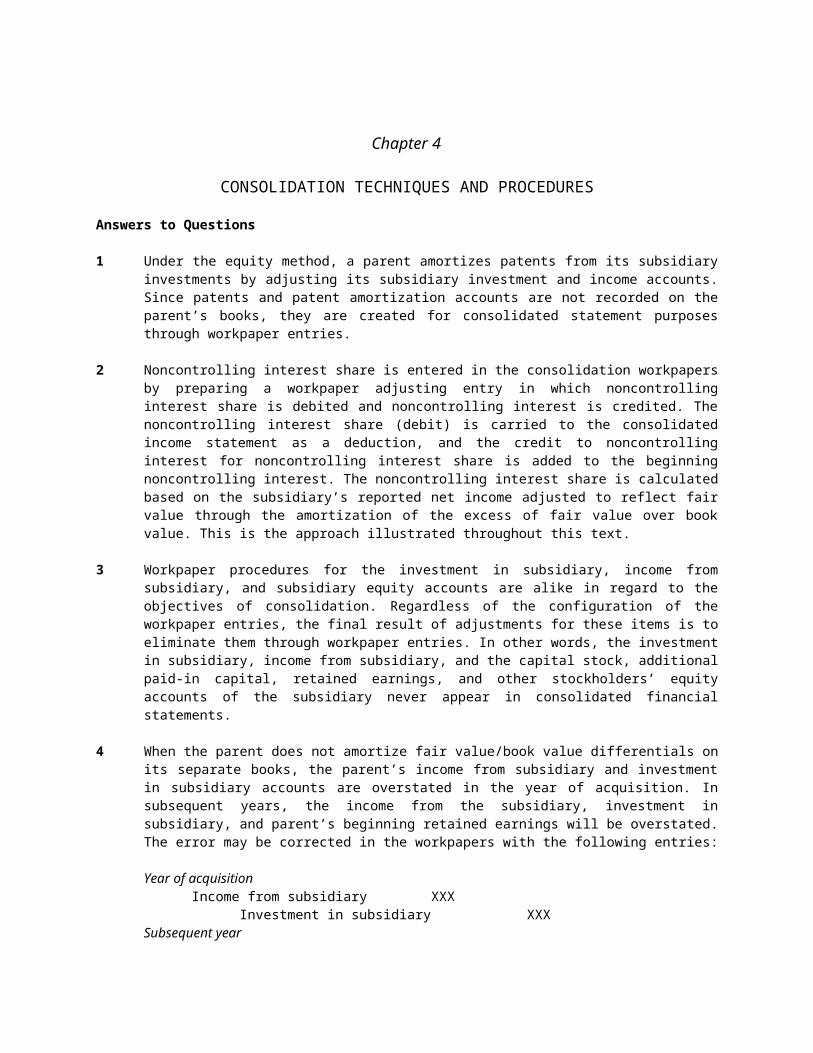

Chapter 4

CONSOLIDATION TECHNIQUES AND PROCEDURES

Answers to Questions

1 Under the equity method, a parent amortizes patents from its subsidiary investments by adjusting its subsidiary investment and income accounts. Since patents and patent amortization accounts are not recorded on the parent’s books, they are created for consolidated statement purposes through workpaper entries.

2 Noncontrolling interest share is entered in the consolidation workpapers by preparing a workpaper adjusting entry in which noncontrolling interest share is debited and noncontrolling interest is credited. The noncontrolling interest share (debit) is carried to the consolidated income statement as a deduction, and the credit to noncontrolling interest for noncontrolling interest share is added to the beginning noncontrolling interest. The noncontrolling interest share is calculated based on the subsidiary’s reported net income adjusted to reflect fair value through the amortization of the excess of fair value over book value. This is the approach illustrated throughout this text.

3 Workpaper procedures for the investment in subsidiary, income from subsidiary, and subsidiary equity accounts are alike in regard to the objectives of consolidation. Regardless of the configuration of the workpaper entries, the final result of adjustments for these items is to eliminate them through workpaper entries. In other words, the investment in subsidiary, income from subsidiary, and the capital stock, additional paid-in capital, retained earnings, and other stockholders’ equity accounts of the subsidiary never appear in consolidated financial statements.

4 When the parent does not amortize fair value/book value differentials on its separate books, the parent’s income from subsidiary and investment in subsidiary accounts are overstated in the year of acquisition. In subsequent years, the income from the subsidiary, investment in subsidiary, and parent’s beginning retained earnings will be overstated. The error may be corrected in the workpapers with the following entries:

Year of acquisitionIncome from subsidiary XXX

Investment in subsidiary XXXSubsequent year

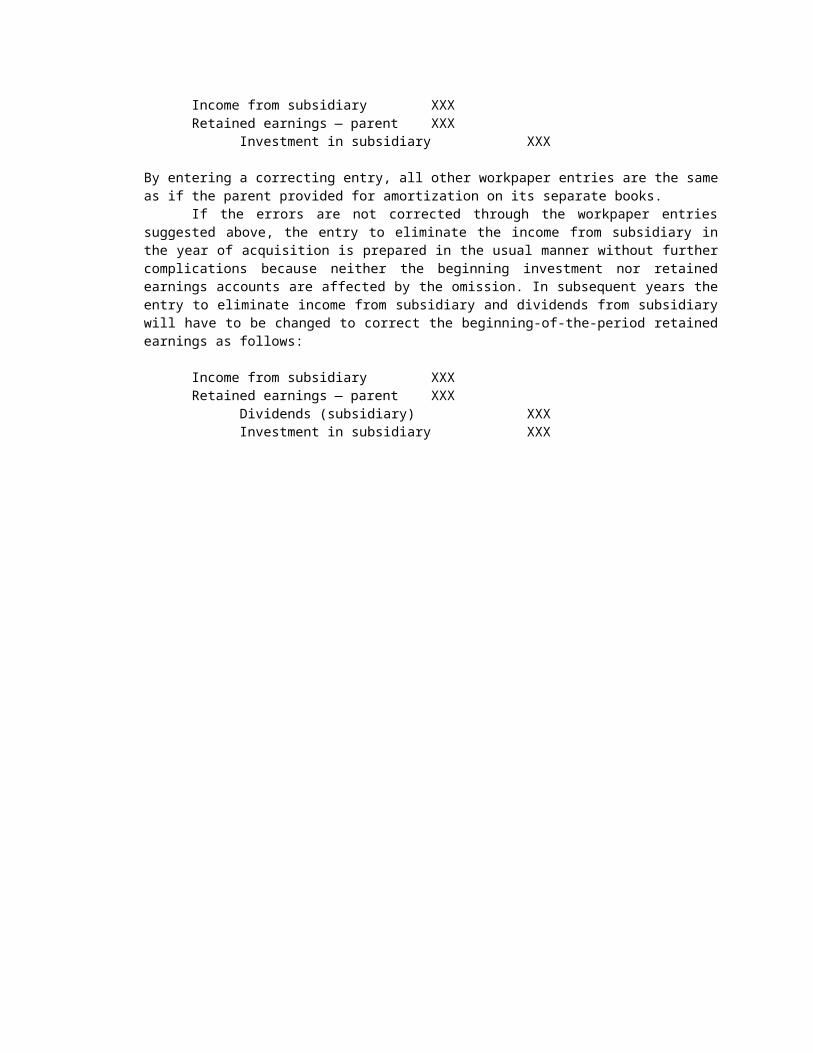

Income from subsidiary XXXRetained earnings — parent XXX

Investment in subsidiary XXX

By entering a correcting entry, all other workpaper entries are the same as if the parent provided for amortization on its separate books.

If the errors are not corrected through the workpaper entries suggested above, the entry to eliminate the income from subsidiary in the year of acquisition is prepared in the usual manner without further complications because neither the beginning investment nor retained earnings accounts are affected by the omission. In subsequent years the entry to eliminate income from subsidiary and dividends from subsidiary will have to be changed to correct the beginning-of-the-period retained earnings as follows:

Income from subsidiary XXXRetained earnings — parent XXX

Dividends (subsidiary) XXXInvestment in subsidiary XXX

5 Workpaper adjustments are not normally entered in the general ledger of the parent or any other entity. They are used in the preparation of consolidated financial statements for a conceptual entity for which there are no formal accounting records. An exception occurs when the adjusting entries involve the correction of an error. For example, if a parent does not record a dividend from a subsidiary. Then the workpaper entry is recorded in the parent’s separate books.

6 Workpapers are tools of the accountant that facilitate the consolidation of parent and subsidiary financial statements. Given the tools available, the accountant should select those that are most convenient in the circumstances. If financial statements are to be consolidated, the financial statement approach is the appropriate tool. The trial balance approach is most convenient when the data are presented in the form of a trial balance. The accountant needs to be familiar with both approaches to perform the work as efficiently as possible.

7 Workpaper adjustment and elimination entries as illustrated in this text are exactly the same when the trial balance approach is used as when the financial statement approach is used.

8 The retained earnings of the parent will equal consolidated retained earnings if the equity method of accounting has been correctly applied. In consolidating the financial statements of affiliated companies, the beginning retained earnings of the parent are used as beginning consolidated retained earnings. If the equity method has not been correctly applied, parent beginning retained earnings will not equal beginning consolidated retained earnings. In this case, retained earnings of the parent are adjusted to a correct equity basis in order to establish the correct amount of beginning consolidated retained earnings. Thus, workpaper adjustments to beginning retained earnings of the parent are needed whenever the beginning retained earnings of the parent do not correctly reflect the equity method.

9 The noncontroling interest that appears in the consolidated balance sheet can be checked by first adjusting the equity of the subsidiary on the consolidated balance sheet date to fair value (i.e., adjusting for any unamortized excess of fair value over book value) and then multiplying by the noncontrolling interest percentage. Consolidated retained earnings at a balance sheet date can be checked by comparing the amount with the parent’s retained earnings on the same date. If consolidated retained earnings and parent retained earnings are not equal, either consolidated retained earnings have been computed incorrectly, or parent retained earnings do not reflect a correct equity method of accounting.

10 Consolidated assets and liabilities are reported for all equity holders—noncontrolling as well as controlling. Therefore, the change in net cash from operations for a period results from noncontrolling interest share and controlling interest share.

11 No. It relates to all interests in the consolidated entity. This difference is one of many inconsistencies in the concepts underlying consolidated financial statements. Consider, for example, the error that could result from dividing cash provided by operations by outstanding parent shares to compute cash flow per share.

SOLUTIONS TO EXERCISES

Solution E4-11 d 6 d2 c 7 b3 a 8 b4 d 9 a5 b 10 b

Solution E4-2Preliminary computations (in thousands)Investment cost January 2 $1,200Implied total fair value of Sal ($1,200 / 80%) $1,500Less: Book value (1,000)

Excess fair value over book value $ 500Excess allocated to:Inventory $ 50Remainder to goodwill 450

Excess fair value over book value $500

1 Income from SalSal’s reported net income $280Less: Excess allocated to inventory (sold in 2011) (50)Sal adjusted income $230Pan’s 80% share $184

2 Noncontrolling interest shareSal’s adjusted income $230 ´ 20% noncontrolling interest $ 46

3 Noncontrolling interest December 31Sal’s equity book value $1,040Add: Unamortized excess (Goodwill) 450Sal’s equity fair value $1,49020% noncontrolling interest $ 298

4 Investment in Sal December 31Investment cost January 2 $1,200Add: Income from Sal (given)* 200Less: Dividends ($120 ´ 80%) (192)

Investment in Sal December 31 $1,208* Assumes this is based on Sal’s adjusted income

5 Noncontrolling interest shareControlling interest share equals Parent NI under equity method.Consolidated net income

$ 50

720.8$770.8

Investment income is given as $200,000 = $250,000 x 80%Noncontrolling interest share is $250,000 x 20% = $50,000

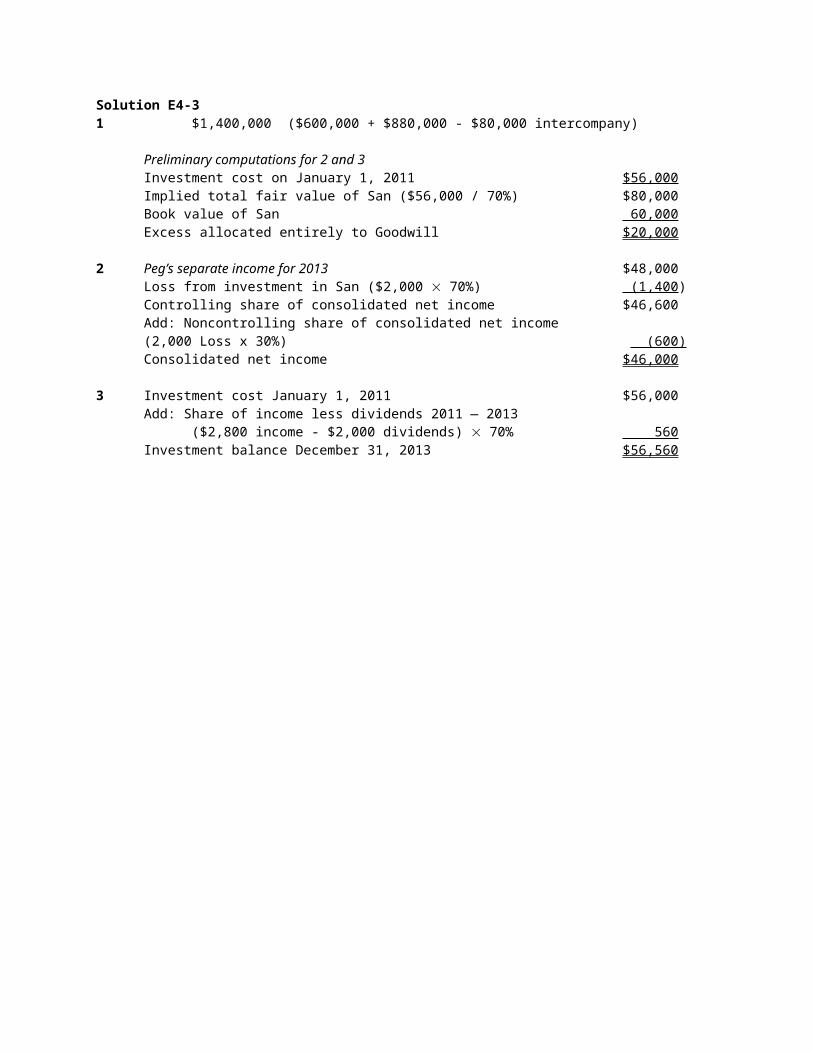

Solution E4-31 $1,400,000 ($600,000 + $880,000 - $80,000 intercompany)

Preliminary computations for 2 and 3Investment cost on January 1, 2011 $56,000Implied total fair value of San ($56,000 / 70%) $80,000Book value of San 60,000Excess allocated entirely to Goodwill $20,000

2 Peg’s separate income for 2013 $48,000Loss from investment in San ($2,000 ´ 70%) (1,400)Controlling share of consolidated net income $46,600Add: Noncontrolling share of consolidated net income (2,000 Loss x 30%) (600)Consolidated net income $46,000

3 Investment cost January 1, 2011 $56,000Add: Share of income less dividends 2011 — 2013

($2,800 income - $2,000 dividends) ´ 70% 560Investment balance December 31, 2013 $56,560

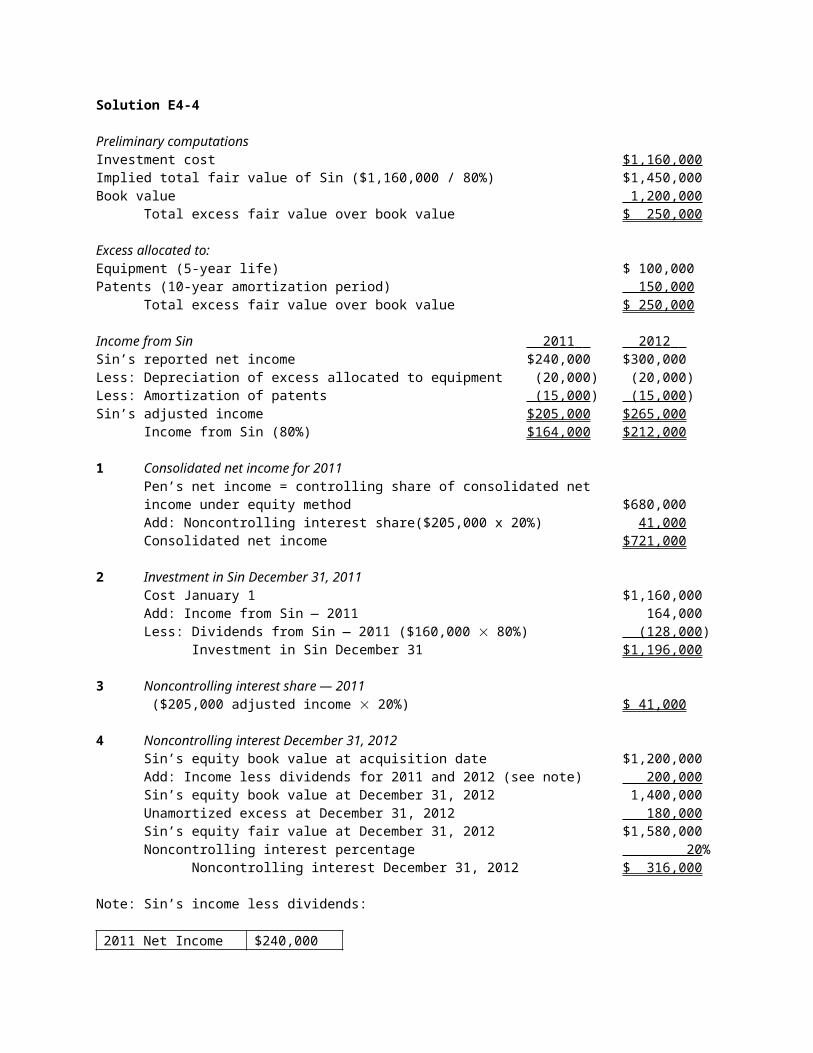

Solution E4-4

Preliminary computationsInvestment cost $1,160,000Implied total fair value of Sin ($1,160,000 / 80%) $1,450,000Book value 1,200,000

Total excess fair value over book value $ 250,000

Excess allocated to:Equipment (5-year life) $ 100,000Patents (10-year amortization period) 150,000

Total excess fair value over book value $ 250,000

Income from Sin 2011 2012 Sin’s reported net income $240,000 $300,000Less: Depreciation of excess allocated to equipment (20,000) (20,000)Less: Amortization of patents (15,000) (15,000)Sin’s adjusted income $205,000 $265,000

Income from Sin (80%) $164,000 $212,000

1 Consolidated net income for 2011Pen’s net income = controlling share of consolidated net income under equity method $680,000Add: Noncontrolling interest share($205,000 x 20%) 41,000Consolidated net income $721,000

2 Investment in Sin December 31, 2011Cost January 1 $1,160,000Add: Income from Sin — 2011 164,000Less: Dividends from Sin — 2011 ($160,000 ´ 80%) (128,000)

Investment in Sin December 31 $1,196,000

3 Noncontrolling interest share — 2011 ($205,000 adjusted income ´ 20%) $ 41,000

4 Noncontrolling interest December 31, 2012Sin’s equity book value at acquisition date $1,200,000Add: Income less dividends for 2011 and 2012 (see note) 200,000Sin’s equity book value at December 31, 2012 1,400,000Unamortized excess at December 31, 2012 180,000Sin’s equity fair value at December 31, 2012 $1,580,000Noncontrolling interest percentage 20%

Noncontrolling interest December 31, 2012 $ 316,000

Note: Sin’s income less dividends:

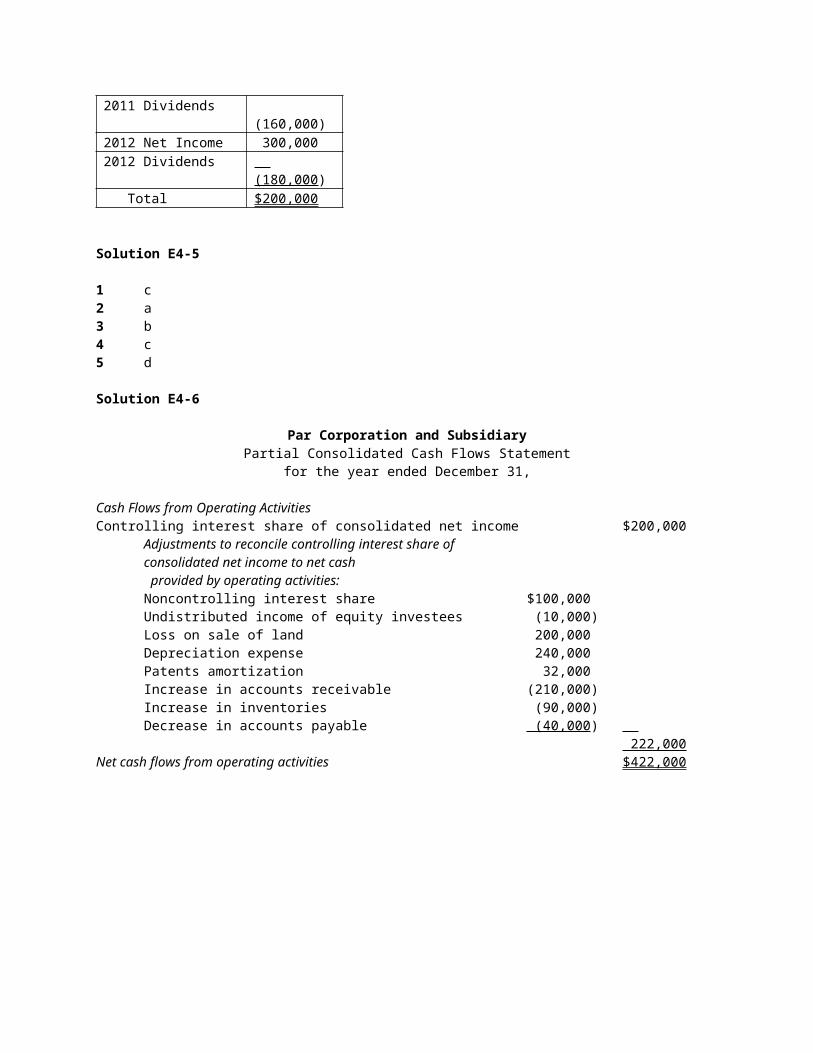

2011 Net Income $240,0002011 Dividends

(160,000)2012 Net Income 300,0002012 Dividends

(180,000) Total $200,000

Solution E4-5

1 c2 a3 b4 c5 d

Solution E4-6

Par Corporation and SubsidiaryPartial Consolidated Cash Flows Statement

for the year ended December 31,

Cash Flows from Operating ActivitiesControlling interest share of consolidated net income $200,000

Adjustments to reconcile controlling interest share of consolidated net income to net cash provided by operating activities:Noncontrolling interest share $100,000Undistributed income of equity investees (10,000)Loss on sale of land 200,000Depreciation expense 240,000Patents amortization 32,000Increase in accounts receivable (210,000)Increase in inventories (90,000)Decrease in accounts payable (40,000)

222,000Net cash flows from operating activities $422,000

Solution E4-7Pro Corporation and Subsidiary

Partial Consolidated Cash Flows Statementfor the year ended December 31,

Cash Flows from Operating ActivitiesCash received from customers $645,000Dividends received from equity investees 14,000

Less: Cash paid to suppliers $365,000Cash paid to employees 54,000Cash paid for other operating items 47,000Cash paid for interest expense 24,000 490,000

Net cash flows from operating activities $169,000

Solutions to Problems

Solution P4-1 (in thousands of $)

Preliminary computationsInvestment in Sen (75%) January 1, 2011 $4,800Implied fair value of Sen ($4,800 / 75%) $6,400Book value of Sen (4,800)

Total excess of fair value over book value $1,600Excess allocated:10% to inventories (sold in 2011) $ 16040% to plant assets (use life 8 years) 64050% to goodwill 800

Total excess of fair value over book value $1,600

1 Goodwill at December 31, 2015 (not amortized) $ 800

2 Noncontrolling interest share for 2015Net income ($2,000 sales - $1,200 expenses) $ 800Less: Amortization of excess Plant assets ($640 / 8 yrs.) (80)Adjusted Sen income $ 72025% Share $ 180

3 Consolidated retained earnings December 31, 2014Equal to Pea’s December 31, 2014 retained earningsSince this a trial balance, reported retained earnings equals beginning of 2015 retained earnings. $3,340

4 Consolidated retained earnings December 31, 2015Pea’s retained earnings December 31, 2014 $3,340Add: Pea’s net income for 2015 2,170Less: Pea’s dividends for 2015 (1,000)Consolidated retained earnings December 31 $4,510

5 Consolidated net income for 2015Consolidated sales $10,000Less: Consolidated expenses ($7,570 + $80 depreciation) (7,650)Total consolidated income 2,350Less: Noncontrolling interest share (180)Controlling share of consolidated net income for 2015 $ 2,170

6 Noncontrolling interest December 31, 2014Sen’s stockholders’ equity at book value $4,800 Unamortized excess after four years: Inventory 0 Plant assets ($640 - $320) 320 Goodwill 800Sen’s stockholders’ equity at fair value $5,92025% Sen’s stockholders’ equity at fair value $1,480

Solution P4-1 (continued)

7 Noncontrolling interest December 31, 2015Sen’s stockholders’ equity at book value $5,200 Unamortized excess after five years: Inventory 0 Plant assets ($640 - $400) 240 Goodwill 800Sen’s stockholders’ equity at fair value $6,24025% Sen’s stockholders’ equity at fair value $1,560

Solution P4-2

1 Pal Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011(in thousands)

Pal80%Sal

Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $1,240 $ 400 $1,640

Income from Sal 42 a 42

Cost of goods sold 800* 260* 1,060*

Operating expenses 308* 80* 388*

Consolidated NI $ 192

Noncontrol. share($60,000´ 30%) c 18 18*

Controlling share $ 174 $ 60 $ 174

Retained EarningsRetained earnings — Pal $ 260 $ 260

Retained earnings — Sal $ 44 b 44

Controlling Share of net income

174 60 174

Dividends 120* 40* a 28

c 12 120*

Retained earnings

December 31 $ 314 $ 64 $ 314

Balance SheetCash $ 182 $ 60 $ 242

Receiv. — net 240 120 360

Inventories 96 80 176

PP&E — net 480 140 620

Investment in Sal 196______ _____

a 14b 182

$1,194 $ 400 $1,398

Accounts payable $ 120 $ 72 $ 192

Other liabilities 80 48 128

Capital stock 600 200 b 200 600

Other paid-in capital 80 16 b 16 80

Retained earnings 314 64 314

$1,194 $ 400

Noncontrolling interest January 1 b 78

Noncontrolling interest December 31 __________ c 6 84

320 320 $1,398* Deduct

Workpaper entriesa To eliminate income from Sal and dividends received from Sal and adjust the

investment in Sal account to its beginning of the period balance.b To eliminate reciprocal investment in Sal and equity amounts of Sal and to

enter beginning noncontrolling interest.c To enter noncontrolling interest share of subsidiary income and dividends.

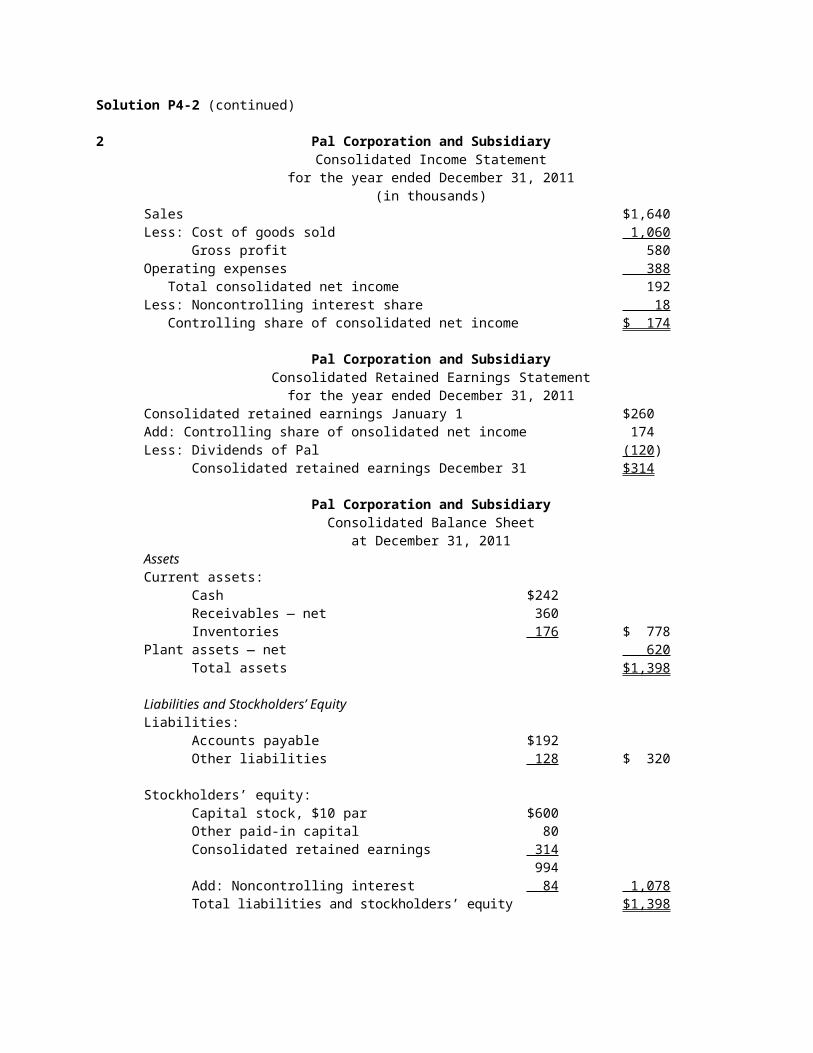

Solution P4-2 (continued)

2 Pal Corporation and SubsidiaryConsolidated Income Statement

for the year ended December 31, 2011(in thousands)

Sales $1,640Less: Cost of goods sold 1,060

Gross profit 580Operating expenses 388 Total consolidated net income 192Less: Noncontrolling interest share 18 Controlling share of consolidated net income $ 174

Pal Corporation and SubsidiaryConsolidated Retained Earnings Statementfor the year ended December 31, 2011

Consolidated retained earnings January 1 $260Add: Controlling share of onsolidated net income 174Less: Dividends of Pal (120)

Consolidated retained earnings December 31 $314

Pal Corporation and SubsidiaryConsolidated Balance Sheet

at December 31, 2011AssetsCurrent assets:

Cash $242Receivables — net 360Inventories 176 $ 778

Plant assets — net 620Total assets $1,398

Liabilities and Stockholders’ EquityLiabilities:

Accounts payable $192Other liabilities 128 $ 320

Stockholders’ equity:Capital stock, $10 par $600Other paid-in capital 80Consolidated retained earnings 314

994Add: Noncontrolling interest 84 1,078Total liabilities and stockholders’ equity $1,398

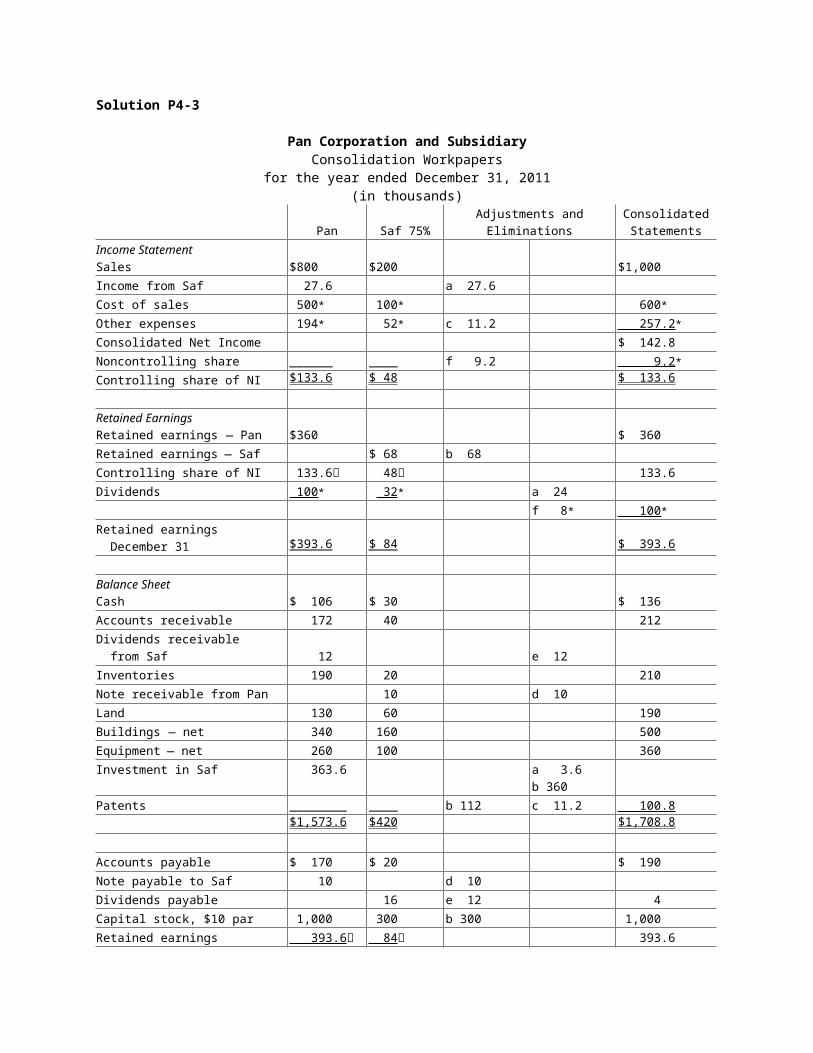

Solution P4-3

Pan Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011(in thousands)

Pan Saf 75%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $800 $200 $1,000Income from Saf 27.6 a 27.6Cost of sales 500* 100* 600*Other expenses 194* 52* c 11.2 257.2*Consolidated Net Income $ 142.8Noncontrolling share ______ ____ f 9.2 9.2*Controlling share of NI $133.6 $ 48 $ 133.6

Retained EarningsRetained earnings — Pan $360 $ 360

Retained earnings — Saf $ 68 b 68

Controlling share of NI 133.6 48 133.6

Dividends 100* 32* a 24f 8* 100*

Retained earnings December 31 $393.6 $ 84 $ 393.6

Balance SheetCash $ 106 $ 30 $ 136Accounts receivable 172 40 212Dividends receivable from Saf 12 e 12Inventories 190 20 210Note receivable from Pan 10 d 10Land 130 60 190

Buildings — net 340 160 500

Equipment — net 260 100 360

Investment in Saf 363.6 a 3.6b 360

Patents ________ ____ b 112 c 11.2 100.8$1,573.6 $420 $1,708.8

Accounts payable $ 170 $ 20 $ 190Note payable to Saf 10 d 10Dividends payable 16 e 12 4Capital stock, $10 par 1,000 300 b 300 1,000Retained earnings 393.6 84 393.6

$1,573.6 $420

Noncontrolling interest January 1 b 120Noncontrolling interest December 31 _____ f 1.2 121.2

550 550 $1,708.8*Deduct

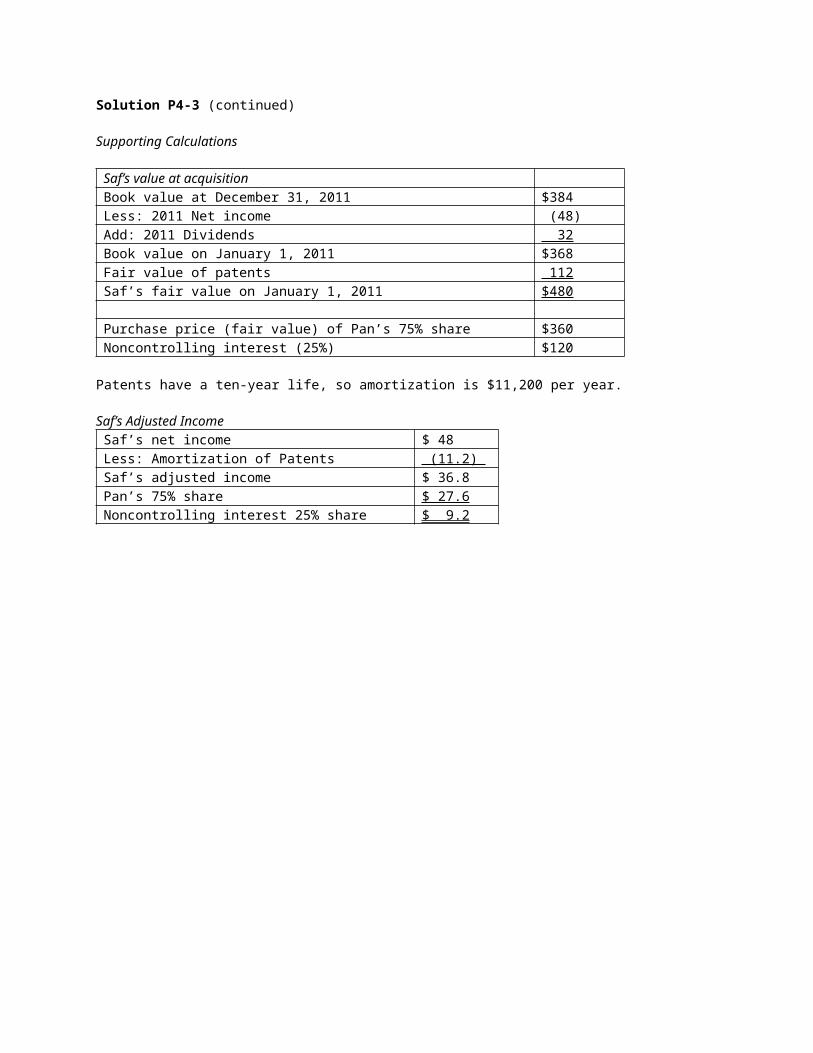

Solution P4-3 (continued)

Supporting Calculations

Saf’s value at acquisitionBook value at December 31, 2011 $384Less: 2011 Net income (48)Add: 2011 Dividends 32Book value on January 1, 2011 $368Fair value of patents 112Saf’s fair value on January 1, 2011 $480

Purchase price (fair value) of Pan’s 75% share $360Noncontrolling interest (25%) $120

Patents have a ten-year life, so amortization is $11,200 per year.

Saf’s Adjusted IncomeSaf’s net income $ 48Less: Amortization of Patents (11.2) Saf’s adjusted income $ 36.8Pan’s 75% share $ 27.6Noncontrolling interest 25% share $ 9.2

Solution P4-4

Pal Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011(in thousands)

Pal Sun 75%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $1,600 $400 $2,000

Income from Sun 72 a 72

Cost of sales 1,000* 200* 1,200*

Other expenses 388* 104* 492*

Consolidated NI $ 308

Noncontrolling share c 24 24*

Controlling share of NI $ 284 $ 96 $ 284

Retained EarningsRetained earnings — Pal $ 720 $720

Retained earnings — Sun $136 b 136

Controlling share of NI 284 96 284

Dividends 200* 64* a 48

c 16 200*

Retained earnings – Dec 31 $ 804 $168 $804

Balance SheetCash $ 236 $ 60 $ 296

Accounts receivable 320 80 400

Dividends receivable from Sun 24 e 24

Inventories 380 40 420

Note receivable from Pal 20 d 20

Land 260 120 380

Buildings — net 680 320 1,000

Equipment — net 520 200 720

Investment in Sun 744 a 24b 720

Goodwill ______ ____ b 224 224

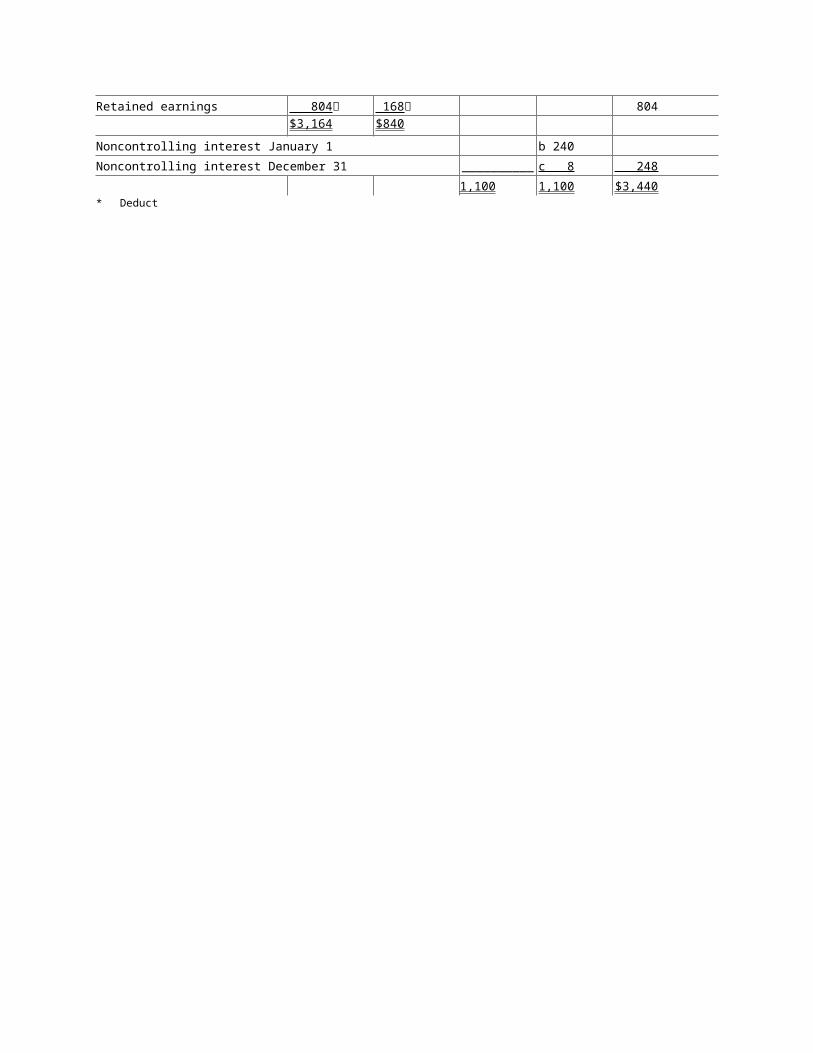

$3,164 $840 $3,440

Accounts payable $ 340 $ 40 $ 380

Note payable to Sun 20 d 20

Dividends payable 32 e 24 8

Capital stock, $10 par 2,000 600 b 600 2,000

Retained earnings 804 168 804

$3,164 $840

Noncontrolling interest January 1 b 240

Noncontrolling interest December 31 __________ c 8 248

1,100 1,100 $3,440* Deduct

Solution P4-4(continued)

Supporting CalculationsSun’s value at acquisition:Book value at December 31, 2011 $768Less: 2011 Net income (96)Add: 2011 Dividends 64Book value on January 1, 2011 $736

Purchase price of Pal’s 75% share $720Implied fair value of Sun ($720 / 75%) $960Sun’s book value 736Excess allocated to Goodwill $224Noncontrolling interest (25% x $960) $240

Sun’s Adjusted IncomeSun’s net income $96Less: Amortization of Goodwill (0) Sun’s adjusted income $96Pal’s 75% share $72Noncontrolling interest 25% share $24

Solution P4-5

Preliminary computations

Allocation of excess fair value over book valueCost of 70% interest January 1 $ 980,000Implied fair value of Sul ($980,000 / 70%) $1,400,000Book value of Sul (1,200,000)

Excess fair value over book value $ 200,000Noncontrolling interest – 30% of fair value at acquisition $ 420,000

Excess allocatedUndervalued inventory items sold in 2011 $ 10,000Undervalued buildings (7 year life) 28,000Undervalued equipment (3 year life) 42,000Trademark 80,000

Remainder to Goodwill 40,000Excess fair value over book value $200,000

Calculation of income from SulSul’s net income $200,000Less: Undervalued inventories sold in 2011 (10,000)Less: Additional Depreciation on building ($28,000/7 years) (4,000)Less: Additional Depreciation on equipment ($42,000/3 years) (14,000)Less: Trademark amortization ($80,000/40 years) (2,000)Sul’s adjusted income $170,000Par’s 70% controlling interest share $119,000Noncontrolling interest’s 30% share $ 51,000

Solution P4-5 (continued)

Workpaper entries for 2011

a Income from Sul 119,000Dividends (Sul) 70,000Investment in Sul 49,000

b Capital stock (Sul) 1,000,000Retained earnings (Sul) January 1 200,000Unamortized excess 200,000

Investment in Sul 980,000Noncontrolling interest January 1 420,000

c Cost of sales (for inventory items) 10,000Buildings — net 28,000Equipment — net 42,000Trademarks 80,000Goodwill 40,000

Unamortized excess 200,000

d Depreciation expense 4,000Buildings — net 4,000

e Depreciation expense 14,000Equipment — net 14,000

f Other expenses 2,000Trademarks 2,000

g Accounts payable 20,000Accounts receivable 20,000

h Dividends payable 28,000Dividends receivable 28,000

i Noncontrolling Interest Share 51,000Dividends — Sul 30,000Noncontrolling Interest 21,000

Solution P4-5 (continued)Par Corporation and Subsidiary

Consolidation Workpapersfor the year ended December 31, 2011

(in thousands)

Par Sul 70%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 1,600 $1,400 $3,000

Income from Sul 119 a 119

Cost of sales 600* 800* c 10 1,410*

Depreciation expense 308* 120* d 4e 14

446*

Other expenses 320* 280* f 2 602*

Consolidated NI $ 542

Noncontrolling share i 51 51*

Controlling share of NI $ 491 $ 200 $ 491

Retained EarningsRetained earnings — Par $ 600 $ 600

Retained earnings — Sul $ 200 b 200

Net income 491 200 491

Dividends 400* 100* a 70

i 30 400*

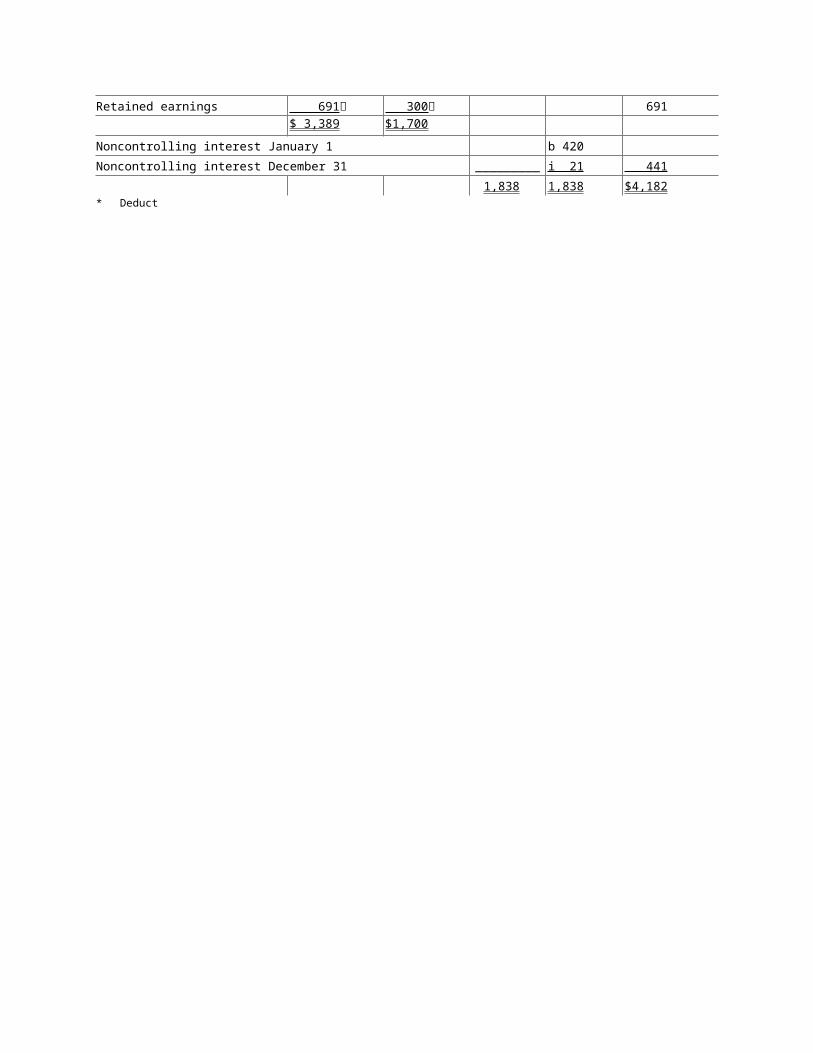

Retained earnings – Dec 31 $ 691 $ 300 $ 691

Balance SheetCash $ 172 $ 120 $ 292

Accounts receivable 200 140 g 20 320

Dividends receivable 28 h 28

Inventories 300 200 500

Other current assets 140 60 200

Land 100 200 300

Buildings — net 280 320 c 28 d 4 624

Equipment — net 1,140 660 c 42 e 14 1,828

Investment in Sul 1,029 a 49b 980

Trademarks c 80 f 2 78

Goodwill c 40 40

Unamortized excess _______ ______ b 200 c 200 ______

$ 3,389 $1,700 $4,182

Accounts payable $ 400 $ 170 g 20 $ 550

Dividends payable 200 40 h 28 212

Other liabilities 98 190 288

Capital stock, $10 par 2,000 1,000 b 1,000 2,000

Retained earnings 691 300 691

$ 3,389 $1,700

Noncontrolling interest January 1 b 420

Noncontrolling interest December 31 _________ i 21 441

1,838 1,838 $4,182* Deduct

Solution P4-6

Supporting computations

Ownership percentage 13,500/15,000 shares = 90%

Investment cost (13,500 shares ´ $30) $405,000Implied fair value of Syn ($405,000 / 90%) $450,000Book value of Syn 330,000

Excess fair value over book value $120,000

Excess allocated toLand $ 40,000Remainder to patents 80,000

Excess fair value over book value $120,000

Income from SynSyn’s reported net income $ 48,000Less: Patent amortization (8,000)Syn’s adjusted income $ 40,000

Pen’s share of Syn’s income (90%) $ 36,000Noncontrolling interest share (10%) $ 4,000

Investment in Syn December 31, 2012Cost January 1, 2011 $405,000Pen’s share of the change in Syn’s retained earnings ($84,000 - $30,000) ´ 90% 48,600Less: Pen’s share (90%) of Patent amortization for 2 years (14,400)

Investment in Syn December 31 $439,200

Solution P4-6 (continued)

Pen Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2012(in thousands)

Pen 90% SynAdjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 800 $ 200 $1,000

Income from Syn 36 a 36

Cost of sales 500* 100* 600*

Other expenses 201.2* 52* c 8 261.2*

Consolidated NI $ 138.8

Noncontrolling share g 4 4 *

Controlling share of NI $ 134.8 $ 48 $ 134.8

Retained EarningsRetained earnings — Pen $ 354 $ 354

Retained earnings — Syn $ 68 b 68

Net income 134.8 48 134.8

Dividends 100* 32* a 28.8

g 3.2 100*

Retained earnings – Dec 31 $ 388.8 $ 84 $ 388.8

Balance SheetCash $ 36 $ 30 $ 66

Accounts receivable 160 40 f 10 190

Dividends receivable 14.4 d 14.4

Inventories 190 20 210

Note receivable — Pen 10 e 10

Investment in Syn 439.2 a 7.2b 432

Land 130 60 b 40 230

Buildings — net 340 160 500

Equipment — net 260 100 360

Patents ________ _____ b 72 c 8 64

$1,569.6 $ 420 $1,620

Accounts payable $ 170.8 $ 20 f 10 $ 180.8

Note payable to Syn 10 e 10

Dividends payable 16 d 14.4 1.6

Capital stock 1,000 300 b 300 1,000

Retained earnings 388.8 84 388.8

$1,569.6 $ 420

Noncontrolling interest January 1 b 48

Noncontrolling interest December 31 _________ g .8 48.8

562.4 562.4 $1,620* Deduct

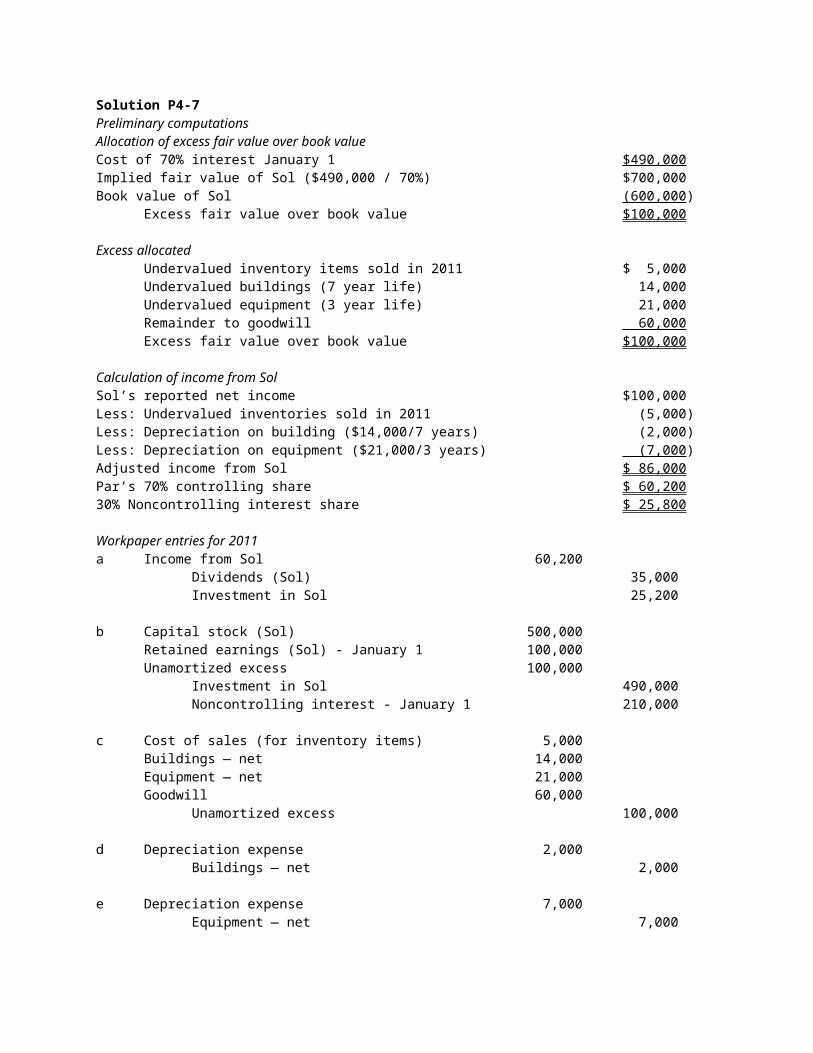

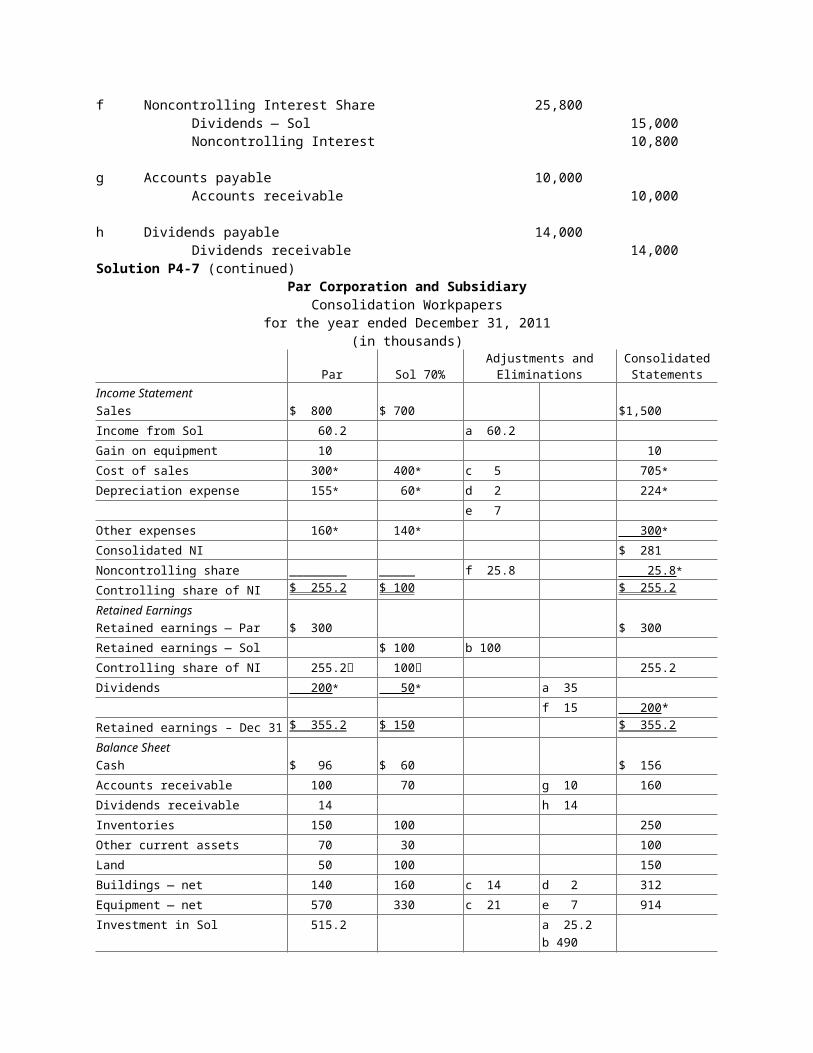

Solution P4-7Preliminary computationsAllocation of excess fair value over book valueCost of 70% interest January 1 $490,000Implied fair value of Sol ($490,000 / 70%) $700,000Book value of Sol (600,000)

Excess fair value over book value $100,000

Excess allocatedUndervalued inventory items sold in 2011 $ 5,000Undervalued buildings (7 year life) 14,000Undervalued equipment (3 year life) 21,000Remainder to goodwill 60,000Excess fair value over book value $100,000

Calculation of income from SolSol’s reported net income $100,000Less: Undervalued inventories sold in 2011 (5,000)Less: Depreciation on building ($14,000/7 years) (2,000)Less: Depreciation on equipment ($21,000/3 years) (7,000)Adjusted income from Sol $ 86,000Par’s 70% controlling share $ 60,20030% Noncontrolling interest share $ 25,800

Workpaper entries for 2011a Income from Sol 60,200

Dividends (Sol) 35,000Investment in Sol 25,200

b Capital stock (Sol) 500,000Retained earnings (Sol) - January 1 100,000Unamortized excess 100,000

Investment in Sol 490,000Noncontrolling interest - January 1 210,000

c Cost of sales (for inventory items) 5,000Buildings — net 14,000Equipment — net 21,000Goodwill 60,000

Unamortized excess 100,000

d Depreciation expense 2,000Buildings — net 2,000

e Depreciation expense 7,000Equipment — net 7,000

f Noncontrolling Interest Share 25,800Dividends — Sol 15,000Noncontrolling Interest 10,800

g Accounts payable 10,000Accounts receivable 10,000

h Dividends payable 14,000Dividends receivable 14,000

Solution P4-7 (continued)Par Corporation and Subsidiary

Consolidation Workpapersfor the year ended December 31, 2011

(in thousands)

Par Sol 70%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 800 $ 700 $1,500

Income from Sol 60.2 a 60.2

Gain on equipment 10 10

Cost of sales 300* 400* c 5 705*

Depreciation expense 155* 60* d 2 224*

e 7

Other expenses 160* 140* 300*

Consolidated NI $ 281

Noncontrolling share ________ _____ f 25.8 25.8*

Controlling share of NI $ 255.2 $ 100 $ 255.2

Retained EarningsRetained earnings — Par $ 300 $ 300

Retained earnings — Sol $ 100 b 100

Controlling share of NI 255.2 100 255.2

Dividends 200* 50* a 35

f 15 200*

Retained earnings – Dec 31 $ 355.2 $ 150 $ 355.2

Balance SheetCash $ 96 $ 60 $ 156

Accounts receivable 100 70 g 10 160

Dividends receivable 14 h 14

Inventories 150 100 250

Other current assets 70 30 100

Land 50 100 150

Buildings — net 140 160 c 14 d 2 312

Equipment — net 570 330 c 21 e 7 914

Investment in Sol 515.2 a 25.2b 490

Goodwill c 60 60

Unamortized excess ________ _____ b 100 c 100 ______

$1,705.2 $ 850 $2,102

Accounts payable $ 200 $ 85 g 10 $ 275

Dividends payable 100 20 h 14 106

Other liabilities 50 95 145

Capital stock, $10 par 1,000 500 b 500 1,000

Retained earnings 355.2 150 355.2

$1,705.2 $ 850

Noncontrolling interest January 1 b 210

Noncontrolling interest December 31 _________ f 10.8 220.8

919 919 $2,102* Deduct

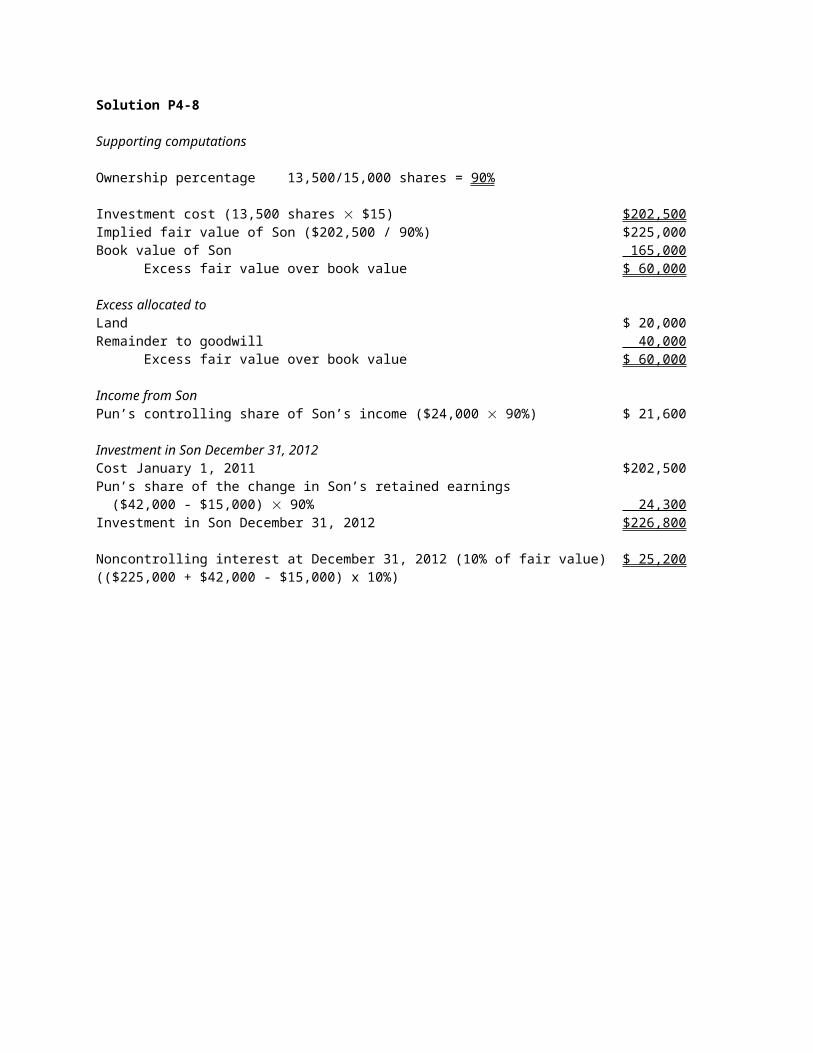

Solution P4-8

Supporting computations

Ownership percentage 13,500/15,000 shares = 90%

Investment cost (13,500 shares ´ $15) $202,500Implied fair value of Son ($202,500 / 90%) $225,000Book value of Son 165,000

Excess fair value over book value $ 60,000

Excess allocated toLand $ 20,000Remainder to goodwill 40,000

Excess fair value over book value $ 60,000

Income from SonPun’s controlling share of Son’s income ($24,000 ´ 90%) $ 21,600

Investment in Son December 31, 2012Cost January 1, 2011 $202,500Pun’s share of the change in Son’s retained earnings ($42,000 - $15,000) ´ 90% 24,300Investment in Son December 31, 2012 $226,800

Noncontrolling interest at December 31, 2012 (10% of fair value)(($225,000 + $42,000 - $15,000) x 10%)

$ 25,200

Solution P4-8 (continued)

Pun Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2012(in thousands)

Pun 90% SonAdjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 400 $ 100 $ 500

Income from Son 21.6 a 21.6

Cost of sales 250* 50* 300*

Expenses 100.6* 26* 126.6*

Consolidated NI $ 73.4

Noncontrolling share c 2.4 2.4*

Controlling share of NI $ 71 $ 24 $ 71

Retained EarningsRetained earnings — Pun $ 181 $ 181

Retained earnings — Son $ 34 b 34

Controlling share of NI 71 24 71

Dividends 50* 16* a 14.4

c 1.6 50*

Retained earnings – Dec 31 $ 202 $ 42 $ 202

Balance SheetCash $ 18 $ 15 $ 33

Accounts receivable 80 20 f 5 95

Dividends receivable 7.2 d 7.2

Inventories 95 10 105

Note receivable — Pun 5 e 5

Investment in Son 226.8 a 7.2b 219.6

Land 65 30 b 20 115

Buildings — net 170 80 250

Equipment — net 130 50 180

Goodwill _____ _____ b 40 40

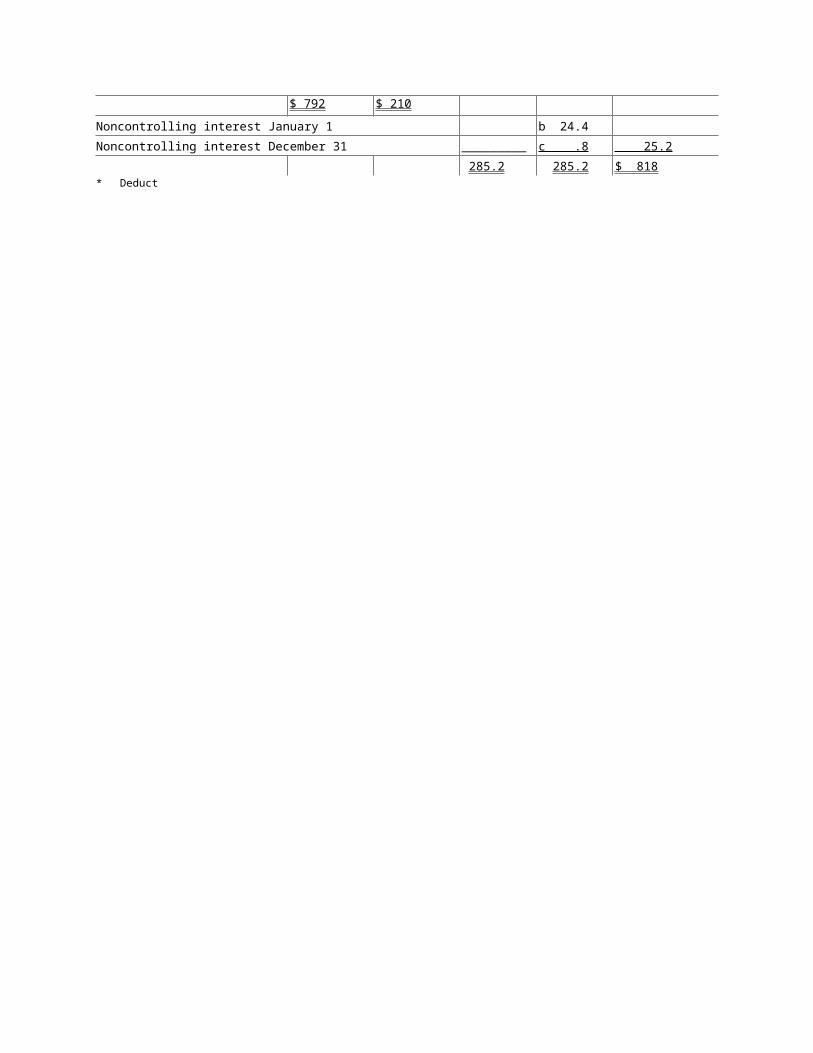

$ 792 $ 210 $ 818

Accounts payable $ 85 $ 10 f 5 $ 90

Note payable to Son 5 e 5

Dividends payable 8 d 7.2 .8

Capital stock 500 150 b 150 500

Retained earnings 202 42 202

$ 792 $ 210

Noncontrolling interest January 1 b 24.4

Noncontrolling interest December 31 _________ c .8 25.2

285.2 285.2 $ 818* Deduct

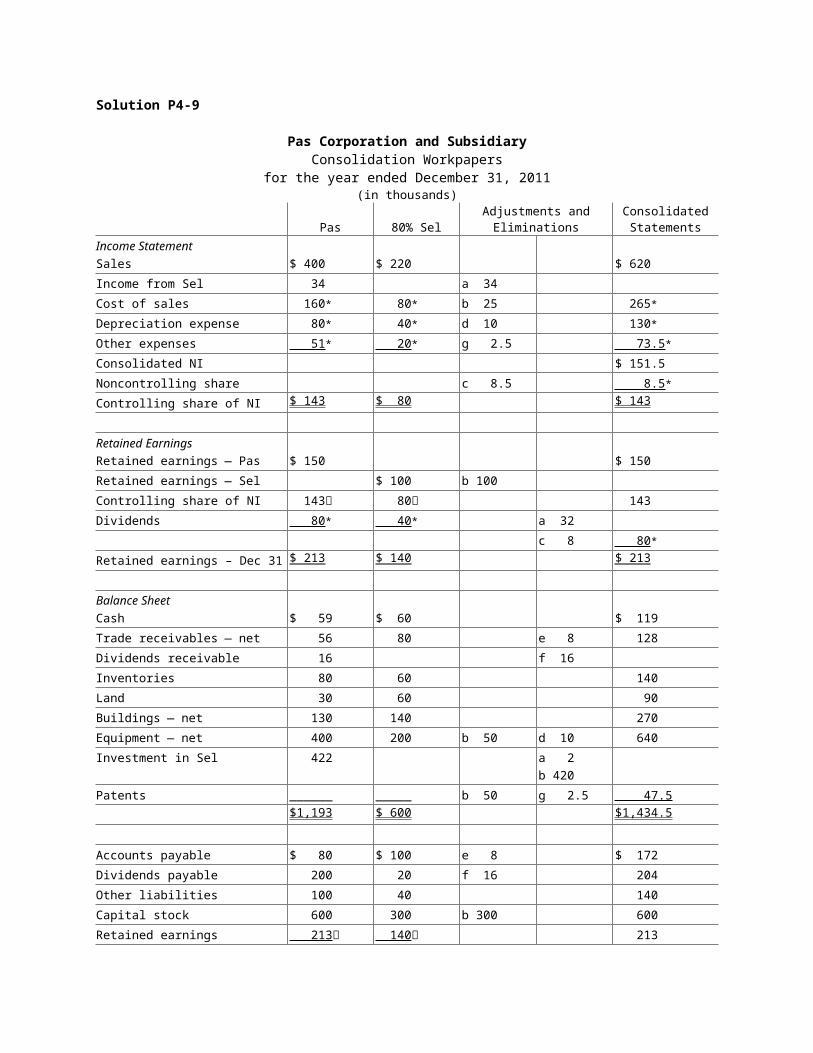

Solution P4-9

Pas Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011(in thousands)

Pas 80% SelAdjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 400 $ 220 $ 620

Income from Sel 34 a 34

Cost of sales 160* 80* b 25 265*

Depreciation expense 80* 40* d 10 130*

Other expenses 51* 20* g 2.5 73.5*

Consolidated NI $ 151.5

Noncontrolling share c 8.5 8.5*

Controlling share of NI $ 143 $ 80 $ 143

Retained EarningsRetained earnings — Pas $ 150 $ 150

Retained earnings — Sel $ 100 b 100

Controlling share of NI 143 80 143

Dividends 80* 40* a 32

c 8 80*

Retained earnings – Dec 31 $ 213 $ 140 $ 213

Balance SheetCash $ 59 $ 60 $ 119

Trade receivables — net 56 80 e 8 128

Dividends receivable 16 f 16

Inventories 80 60 140

Land 30 60 90

Buildings — net 130 140 270

Equipment — net 400 200 b 50 d 10 640

Investment in Sel 422 a 2b 420

Patents ______ _____ b 50 g 2.5 47.5

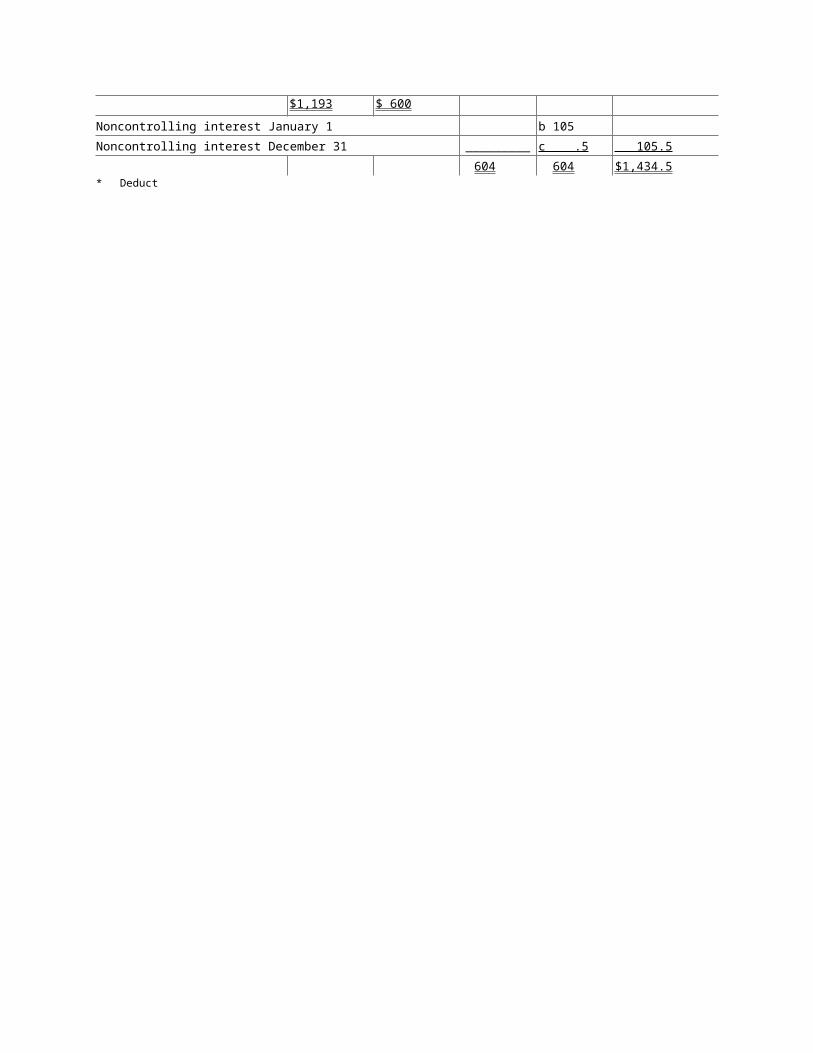

$1,193 $ 600 $1,434.5

Accounts payable $ 80 $ 100 e 8 $ 172

Dividends payable 200 20 f 16 204

Other liabilities 100 40 140

Capital stock 600 300 b 300 600

Retained earnings 213 140 213

$1,193 $ 600

Noncontrolling interest January 1 b 105

Noncontrolling interest December 31 _________ c .5 105.5

604 604 $1,434.5* Deduct

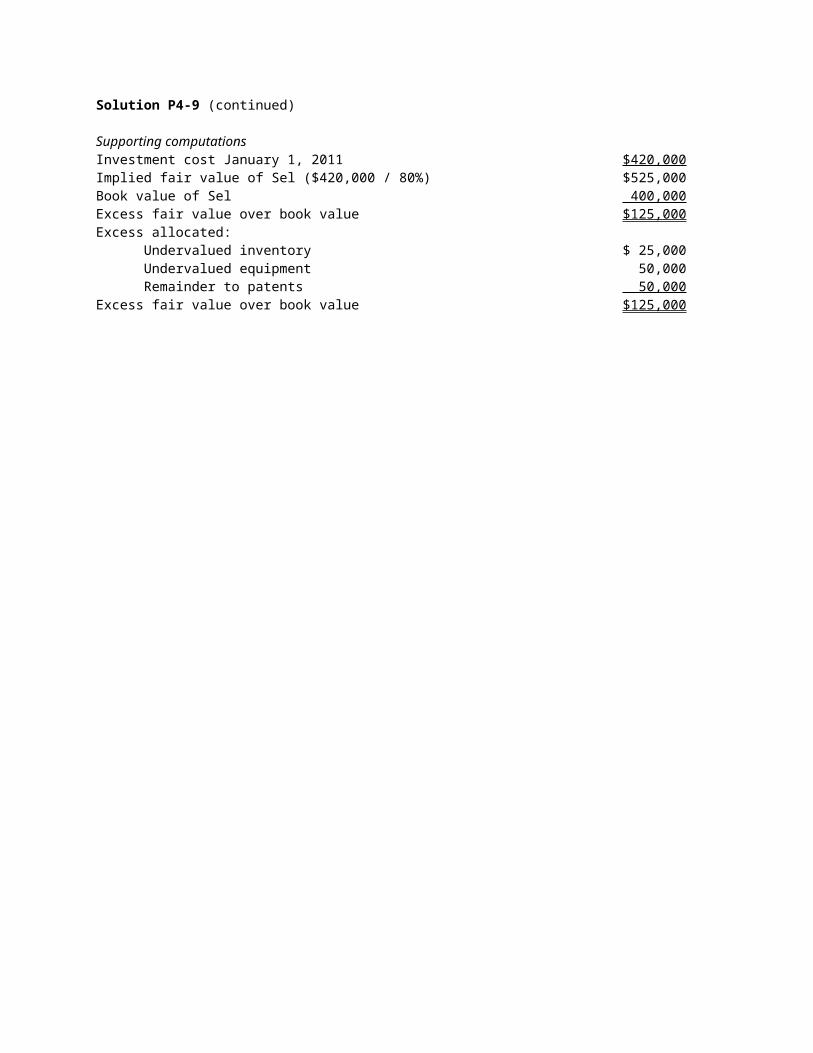

Solution P4-9 (continued)

Supporting computationsInvestment cost January 1, 2011 $420,000Implied fair value of Sel ($420,000 / 80%) $525,000Book value of Sel 400,000Excess fair value over book value $125,000Excess allocated:

Undervalued inventory $ 25,000Undervalued equipment 50,000Remainder to patents 50,000

Excess fair value over book value $125,000

Solution P4-10

Pik Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011(in thousands)

Pik80%Sel

Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 400 $ 220 $ 620

Income from Sel 36 a 36

Cost of sales 160* 80* b 25 265*

Depreciation expense 80* 40* d 10 130*

Other expenses 51* 20* 71*

Consolidated NI $ 154

Noncontrolling share _____ _____ c 9 9*

Controlling share of NI $ 145 $ 80 $ 145

Retained EarningsRetained earnings — Pik $ 150 $ 150

Retained earnings — Sel $ 100 b 100

Controlling share of NI 145 80 145

Dividends 80* 40* a 32

c 8 80*

Retained earnings – Dec 31 $ 215 $ 140 $ 215

Balance SheetCash $ 59 $ 60 $ 119

Trade receivables — net 56 80 e 8 128

Dividends receivable 16 f 16

Inventories 80 60 140

Land 30 60 90

Buildings — net 130 140 270

Equipment — net 400 200 b 50 d 10 640

Investment in Sel 424 a 4b 420

Goodwill ______ _____ b 50 50

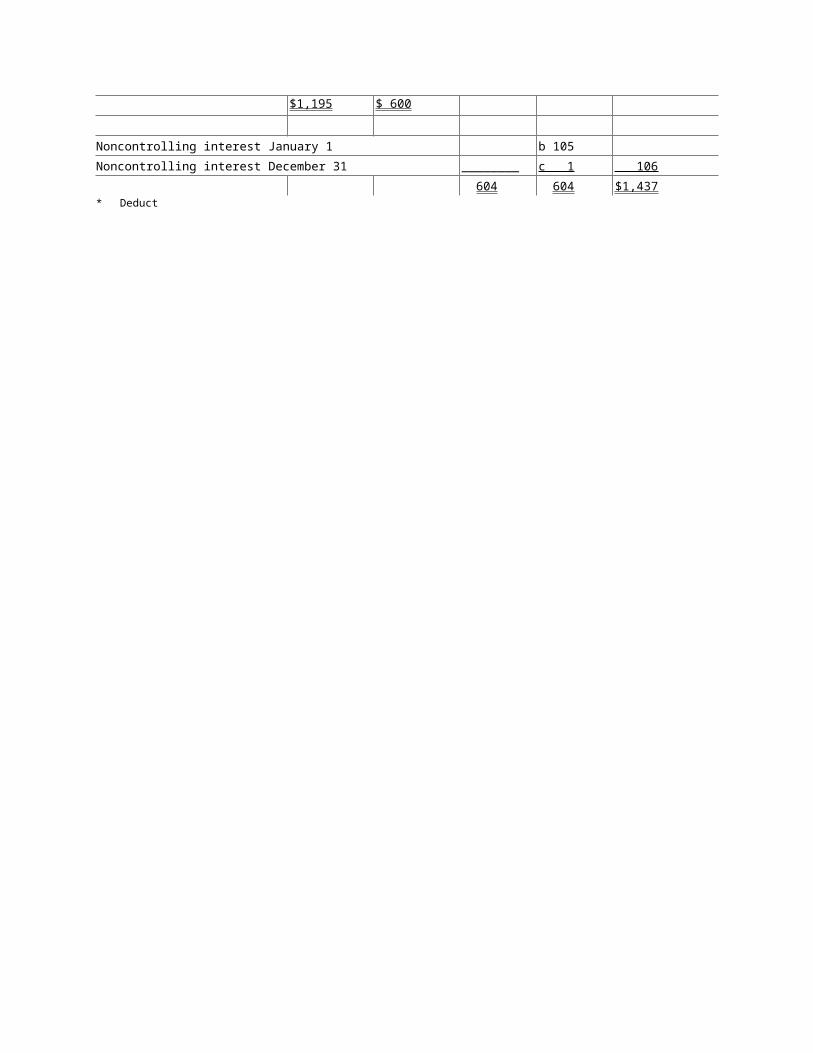

$1,195 $ 600 $1,437

Accounts payable $ 80 $ 100 e 8 $ 172

Dividends payable 200 20 f 16 204

Other liabilities 100 40 140

Capital stock 600 300 b 300 600

Retained earnings 215 140 215

$1,195 $ 600

Noncontrolling interest January 1 b 105

Noncontrolling interest December 31 ________ c 1 106

604 604 $1,437* Deduct

Solution P4-10 (continued)

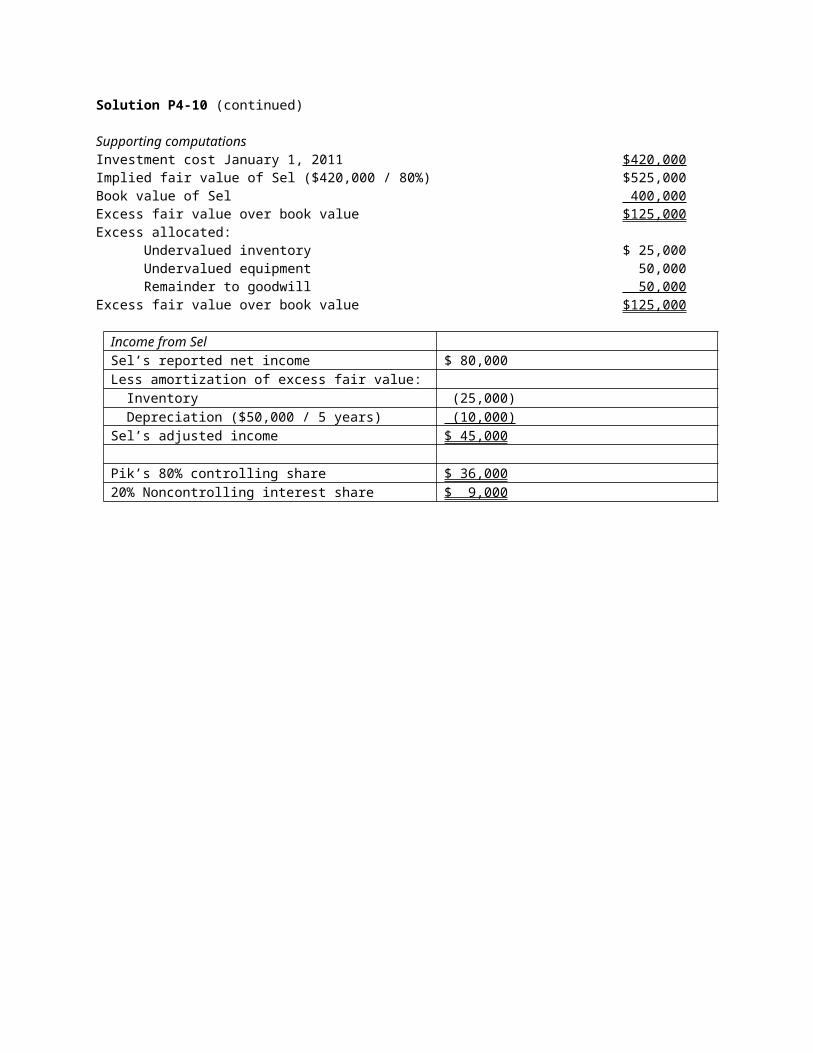

Supporting computationsInvestment cost January 1, 2011 $420,000Implied fair value of Sel ($420,000 / 80%) $525,000Book value of Sel 400,000Excess fair value over book value $125,000Excess allocated:

Undervalued inventory $ 25,000Undervalued equipment 50,000Remainder to goodwill 50,000

Excess fair value over book value $125,000

Income from SelSel’s reported net income $ 80,000Less amortization of excess fair value: Inventory (25,000) Depreciation ($50,000 / 5 years) (10,000)Sel’s adjusted income $ 45,000

Pik’s 80% controlling share $ 36,00020% Noncontrolling interest share $ 9,000

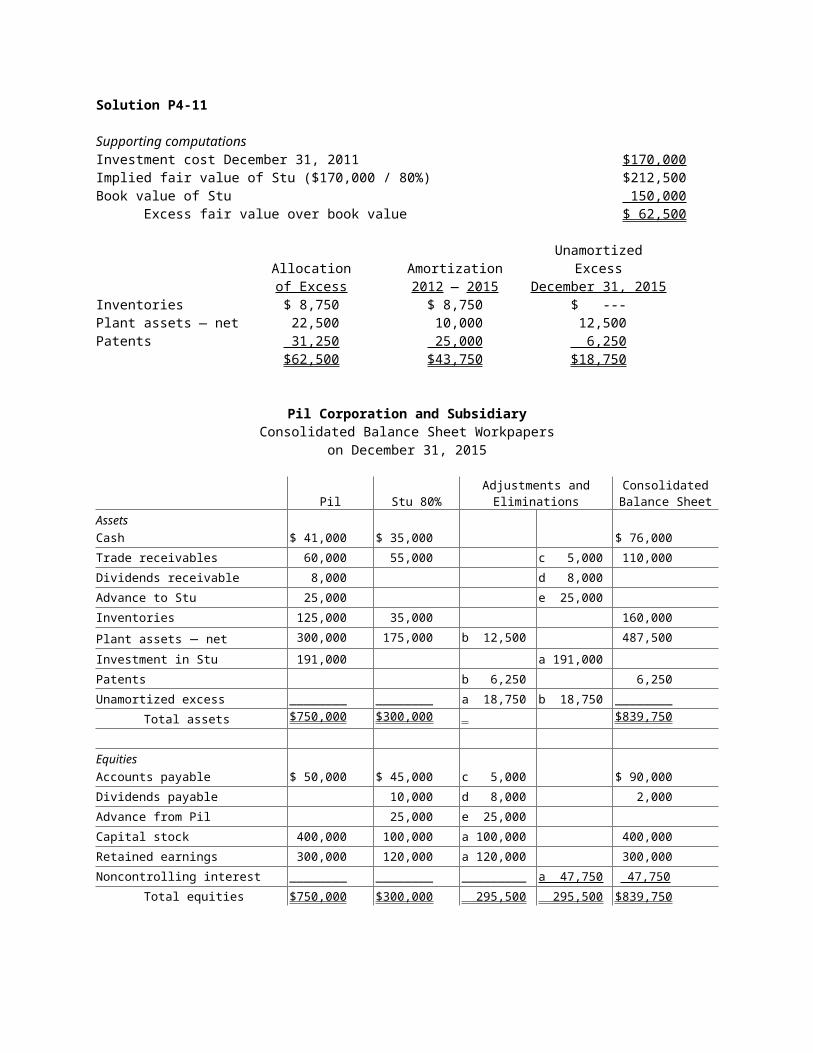

Solution P4-11

Supporting computationsInvestment cost December 31, 2011 $170,000Implied fair value of Stu ($170,000 / 80%) $212,500Book value of Stu 150,000

Excess fair value over book value $ 62,500

Allocationof Excess

Amortization2012 — 2015

UnamortizedExcess

December 31, 2015Inventories $ 8,750 $ 8,750 $ ---Plant assets — net 22,500 10,000 12,500Patents 31,250 25,000 6,250

$62,500 $43,750 $18,750

Pil Corporation and SubsidiaryConsolidated Balance Sheet Workpapers

on December 31, 2015

Pil Stu 80%Adjustments andEliminations

ConsolidatedBalance Sheet

AssetsCash $ 41,000 $ 35,000 $ 76,000

Trade receivables 60,000 55,000 c 5,000 110,000

Dividends receivable 8,000 d 8,000

Advance to Stu 25,000 e 25,000

Inventories 125,000 35,000 160,000

Plant assets — net 300,000 175,000 b 12,500 487,500

Investment in Stu 191,000 a 191,000

Patents b 6,250 6,250

Unamortized excess ________ ________ a 18,750 b 18,750 ________

Total assets $750,000 $300,000 $839,750

EquitiesAccounts payable $ 50,000 $ 45,000 c 5,000 $ 90,000

Dividends payable 10,000 d 8,000 2,000

Advance from Pil 25,000 e 25,000

Capital stock 400,000 100,000 a 100,000 400,000

Retained earnings 300,000 120,000 a 120,000 300,000

Noncontrolling interest ________ ________ _________ a 47,750 47,750

Total equities $750,000 $300,000 295,500 295,500 $839,750

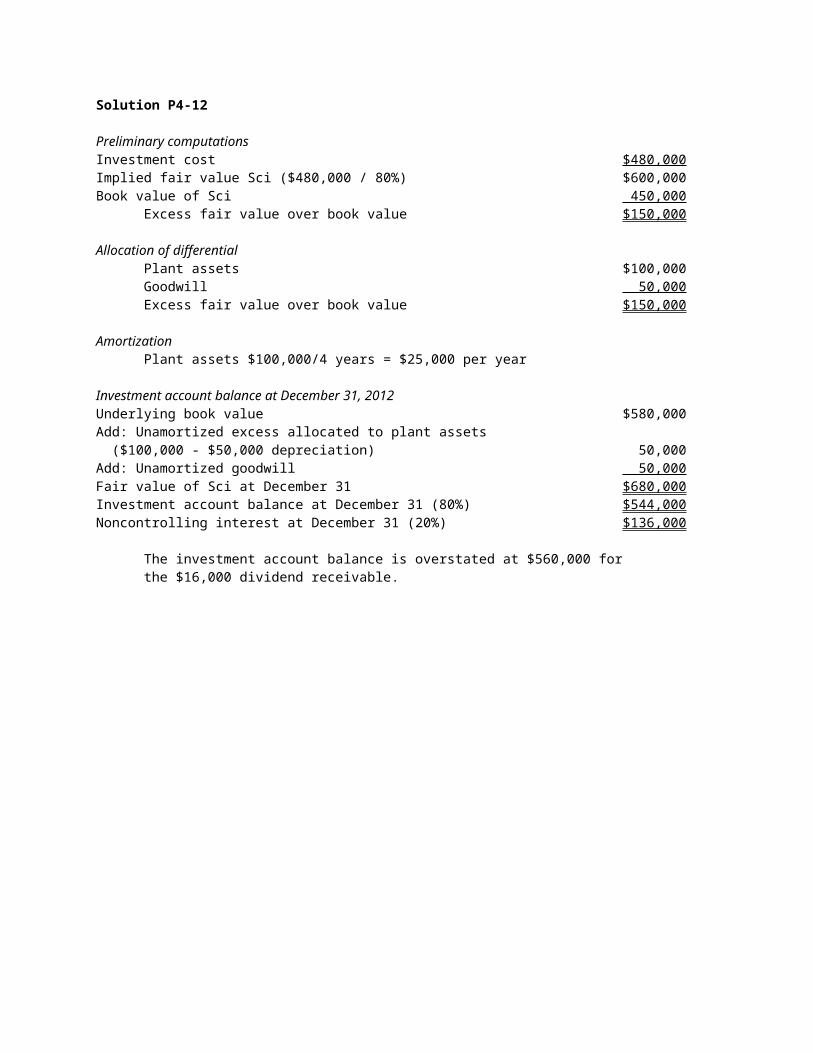

Solution P4-12

Preliminary computationsInvestment cost $480,000Implied fair value Sci ($480,000 / 80%) $600,000Book value of Sci 450,000

Excess fair value over book value $150,000

Allocation of differentialPlant assets $100,000Goodwill 50,000Excess fair value over book value $150,000

AmortizationPlant assets $100,000/4 years = $25,000 per year

Investment account balance at December 31, 2012Underlying book value $580,000Add: Unamortized excess allocated to plant assets ($100,000 - $50,000 depreciation) 50,000Add: Unamortized goodwill 50,000Fair value of Sci at December 31 $680,000Investment account balance at December 31 (80%) $544,000Noncontrolling interest at December 31 (20%) $136,000

The investment account balance is overstated at $560,000 forthe $16,000 dividend receivable.

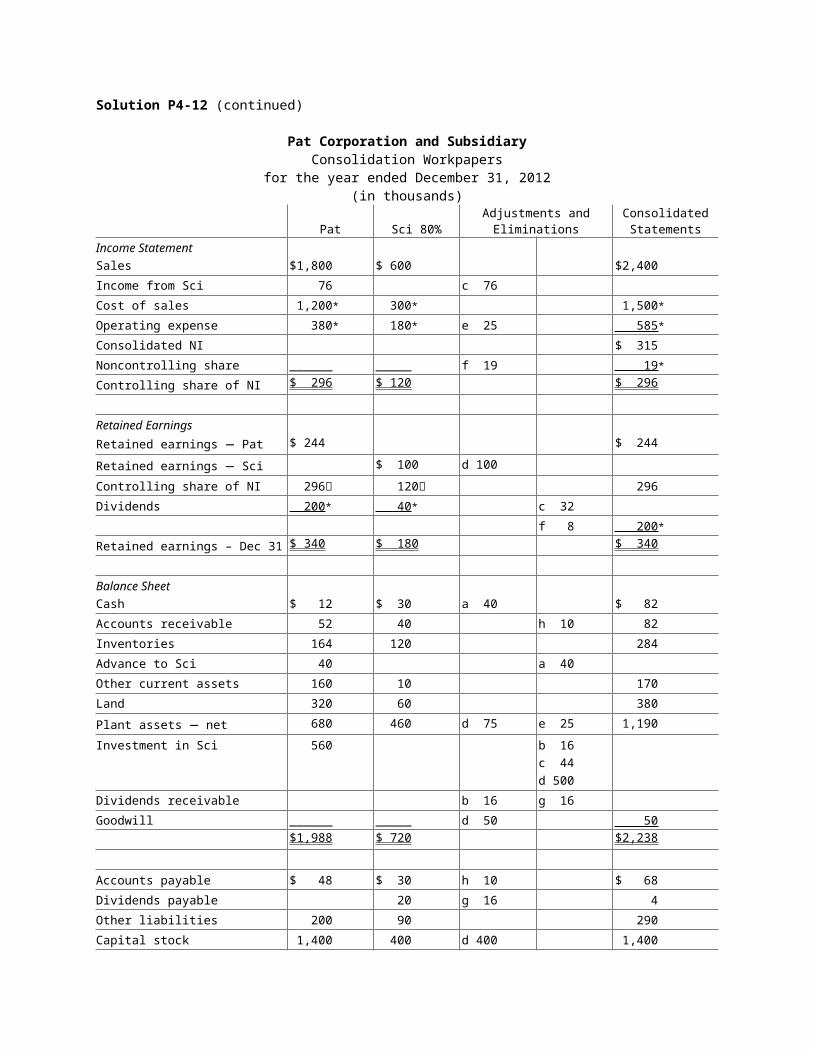

Solution P4-12 (continued)

Pat Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2012(in thousands)

Pat Sci 80%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $1,800 $ 600 $2,400

Income from Sci 76 c 76

Cost of sales 1,200* 300* 1,500*

Operating expense 380* 180* e 25 585*

Consolidated NI $ 315

Noncontrolling share ______ _____ f 19 19*

Controlling share of NI $ 296 $ 120 $ 296

Retained Earnings

Retained earnings — Pat $ 244 $ 244

Retained earnings — Sci $ 100 d 100

Controlling share of NI 296 120 296

Dividends 200* 40* c 32

f 8 200*

Retained earnings – Dec 31 $ 340 $ 180 $ 340

Balance SheetCash $ 12 $ 30 a 40 $ 82

Accounts receivable 52 40 h 10 82

Inventories 164 120 284

Advance to Sci 40 a 40

Other current assets 160 10 170

Land 320 60 380

Plant assets — net 680 460 d 75 e 25 1,190

Investment in Sci 560 b 16c 44d 500

Dividends receivable b 16 g 16

Goodwill ______ _____ d 50 50

$1,988 $ 720 $2,238

Accounts payable $ 48 $ 30 h 10 $ 68

Dividends payable 20 g 16 4

Other liabilities 200 90 290

Capital stock 1,400 400 d 400 1,400

Retained earnings 340 180 340

$1,988 $ 720

Noncontrolling interest January 1 d 125

Noncontrolling interest December 31 _______ f 11 136

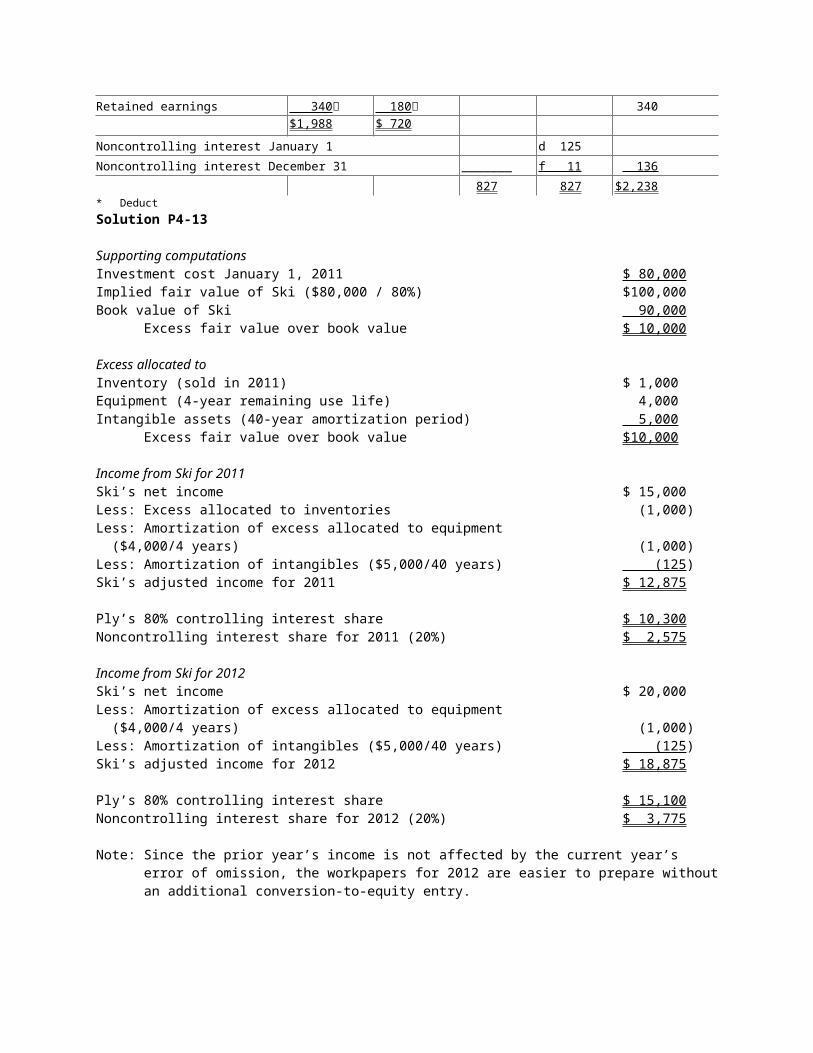

827 827 $2,238* DeductSolution P4-13

Supporting computationsInvestment cost January 1, 2011 $ 80,000Implied fair value of Ski ($80,000 / 80%) $100,000Book value of Ski 90,000

Excess fair value over book value $ 10,000

Excess allocated toInventory (sold in 2011) $ 1,000Equipment (4-year remaining use life) 4,000Intangible assets (40-year amortization period) 5,000

Excess fair value over book value $10,000

Income from Ski for 2011Ski’s net income $ 15,000Less: Excess allocated to inventories (1,000)Less: Amortization of excess allocated to equipment ($4,000/4 years) (1,000)Less: Amortization of intangibles ($5,000/40 years) (125)Ski’s adjusted income for 2011 $ 12,875

Ply’s 80% controlling interest share $ 10,300Noncontrolling interest share for 2011 (20%) $ 2,575

Income from Ski for 2012Ski’s net income $ 20,000Less: Amortization of excess allocated to equipment ($4,000/4 years) (1,000)Less: Amortization of intangibles ($5,000/40 years) (125)Ski’s adjusted income for 2012 $ 18,875

Ply’s 80% controlling interest share $ 15,100Noncontrolling interest share for 2012 (20%) $ 3,775

Note: Since the prior year’s income is not affected by the current year’s error of omission, the workpapers for 2012 are easier to prepare without an additional conversion-to-equity entry.

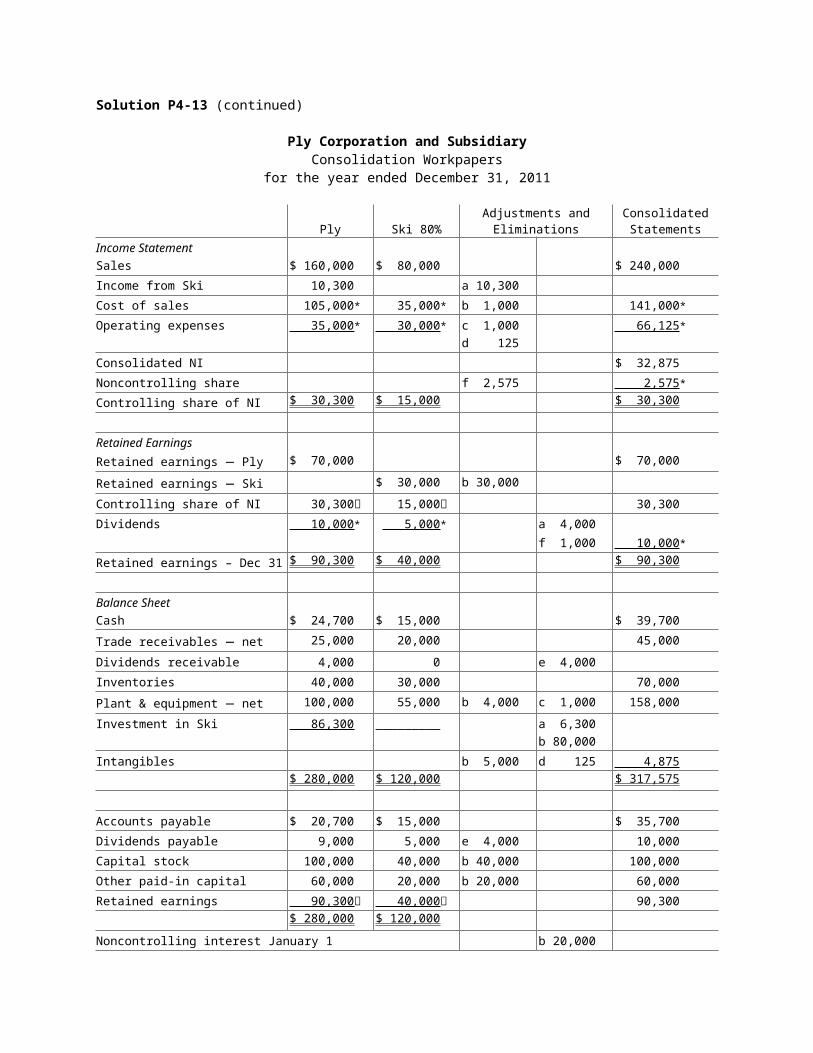

Solution P4-13 (continued)

Ply Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011

Ply Ski 80%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 160,000 $ 80,000 $ 240,000

Income from Ski 10,300 a 10,300

Cost of sales 105,000* 35,000* b 1,000 141,000*

Operating expenses 35,000* 30,000* c 1,000d 125

66,125*

Consolidated NI $ 32,875

Noncontrolling share f 2,575 2,575*

Controlling share of NI $ 30,300 $ 15,000 $ 30,300

Retained Earnings

Retained earnings — Ply $ 70,000 $ 70,000

Retained earnings — Ski $ 30,000 b 30,000

Controlling share of NI 30,300 15,000 30,300

Dividends 10,000* 5,000* a 4,000f 1,000 10,000*

Retained earnings – Dec 31 $ 90,300 $ 40,000 $ 90,300

Balance SheetCash $ 24,700 $ 15,000 $ 39,700

Trade receivables — net 25,000 20,000 45,000

Dividends receivable 4,000 0 e 4,000

Inventories 40,000 30,000 70,000

Plant & equipment — net 100,000 55,000 b 4,000 c 1,000 158,000

Investment in Ski 86,300 _________ a 6,300b 80,000

Intangibles b 5,000 d 125 4,875

$ 280,000 $ 120,000 $ 317,575

Accounts payable $ 20,700 $ 15,000 $ 35,700

Dividends payable 9,000 5,000 e 4,000 10,000

Capital stock 100,000 40,000 b 40,000 100,000

Other paid-in capital 60,000 20,000 b 20,000 60,000

Retained earnings 90,300 40,000 90,300

$ 280,000 $ 120,000

Noncontrolling interest January 1 b 20,000

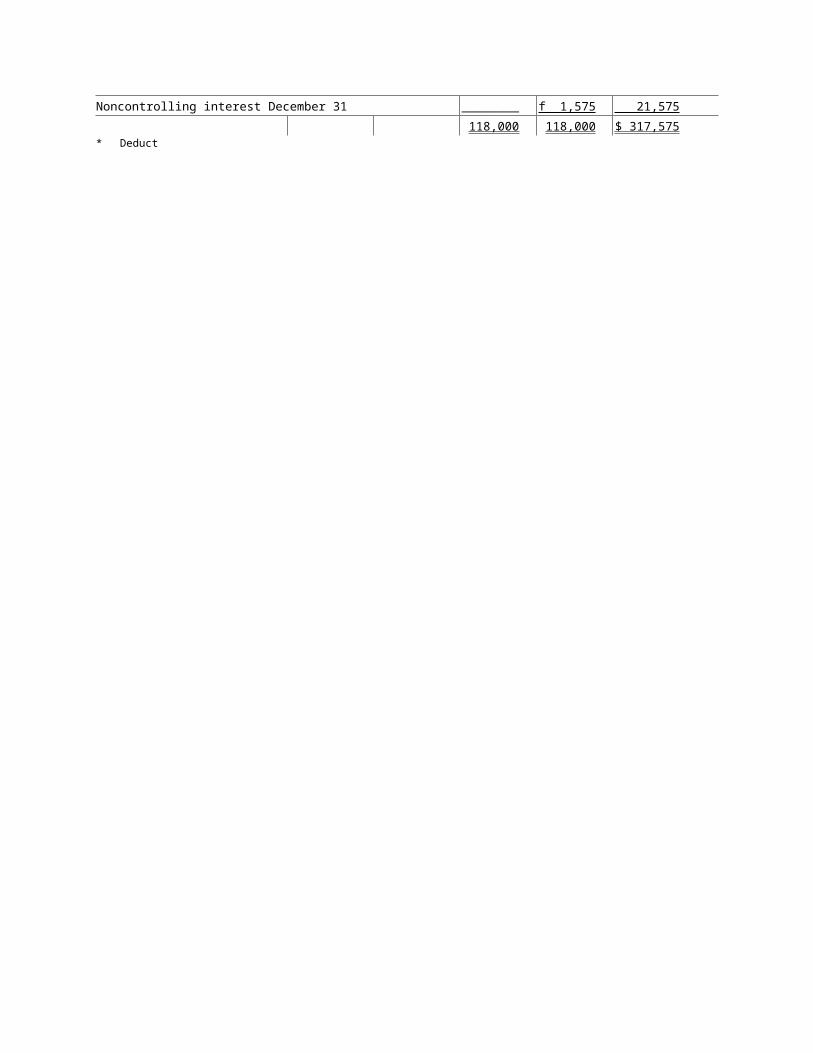

Noncontrolling interest December 31 ________ f 1,575 21,575

118,000 118,000 $ 317,575* Deduct

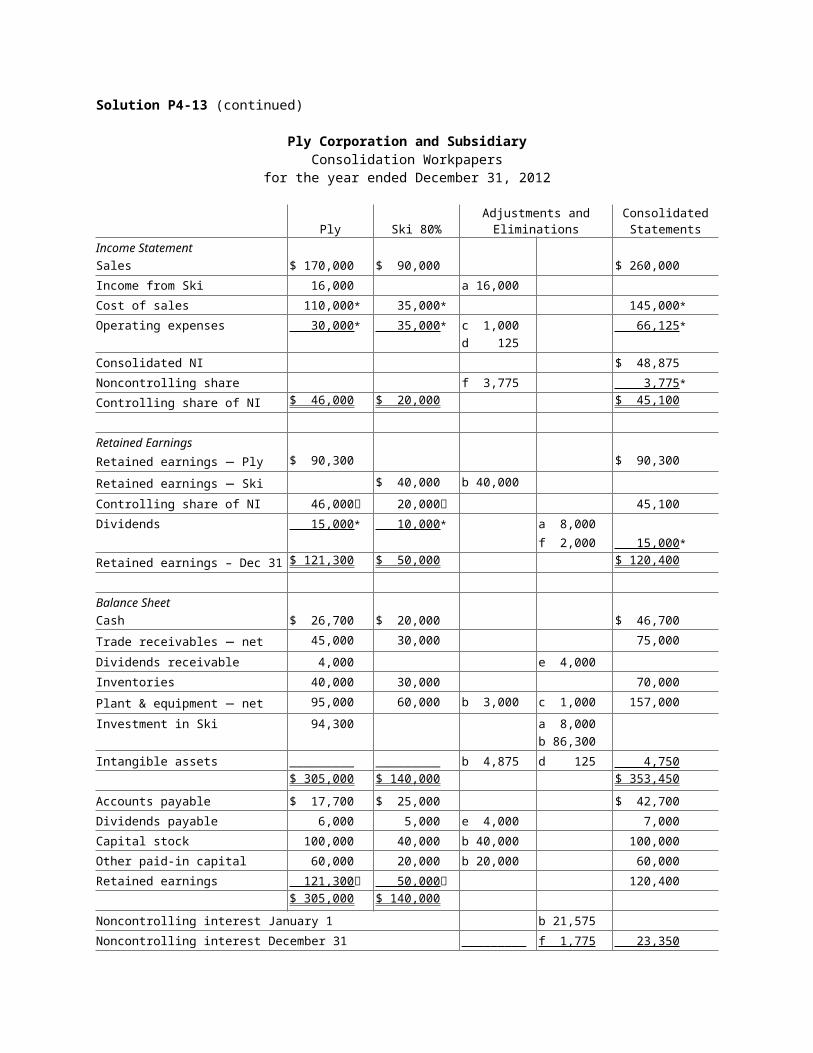

Solution P4-13 (continued)

Ply Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2012

Ply Ski 80%Adjustments andEliminations

ConsolidatedStatements

Income StatementSales $ 170,000 $ 90,000 $ 260,000

Income from Ski 16,000 a 16,000

Cost of sales 110,000* 35,000* 145,000*

Operating expenses 30,000* 35,000* c 1,000d 125

66,125*

Consolidated NI $ 48,875

Noncontrolling share f 3,775 3,775*

Controlling share of NI $ 46,000 $ 20,000 $ 45,100

Retained Earnings

Retained earnings — Ply $ 90,300 $ 90,300

Retained earnings — Ski $ 40,000 b 40,000

Controlling share of NI 46,000 20,000 45,100

Dividends 15,000* 10,000* a 8,000f 2,000 15,000*

Retained earnings – Dec 31 $ 121,300 $ 50,000 $ 120,400

Balance SheetCash $ 26,700 $ 20,000 $ 46,700

Trade receivables — net 45,000 30,000 75,000

Dividends receivable 4,000 e 4,000

Inventories 40,000 30,000 70,000

Plant & equipment — net 95,000 60,000 b 3,000 c 1,000 157,000

Investment in Ski 94,300 a 8,000b 86,300

Intangible assets _________ _________ b 4,875 d 125 4,750

$ 305,000 $ 140,000 $ 353,450

Accounts payable $ 17,700 $ 25,000 $ 42,700

Dividends payable 6,000 5,000 e 4,000 7,000

Capital stock 100,000 40,000 b 40,000 100,000

Other paid-in capital 60,000 20,000 b 20,000 60,000

Retained earnings 121,300 50,000 120,400

$ 305,000 $ 140,000

Noncontrolling interest January 1 b 21,575

Noncontrolling interest December 31 _________ f 1,775 23,350

132,775 132,775 $ 353,450* Deduct

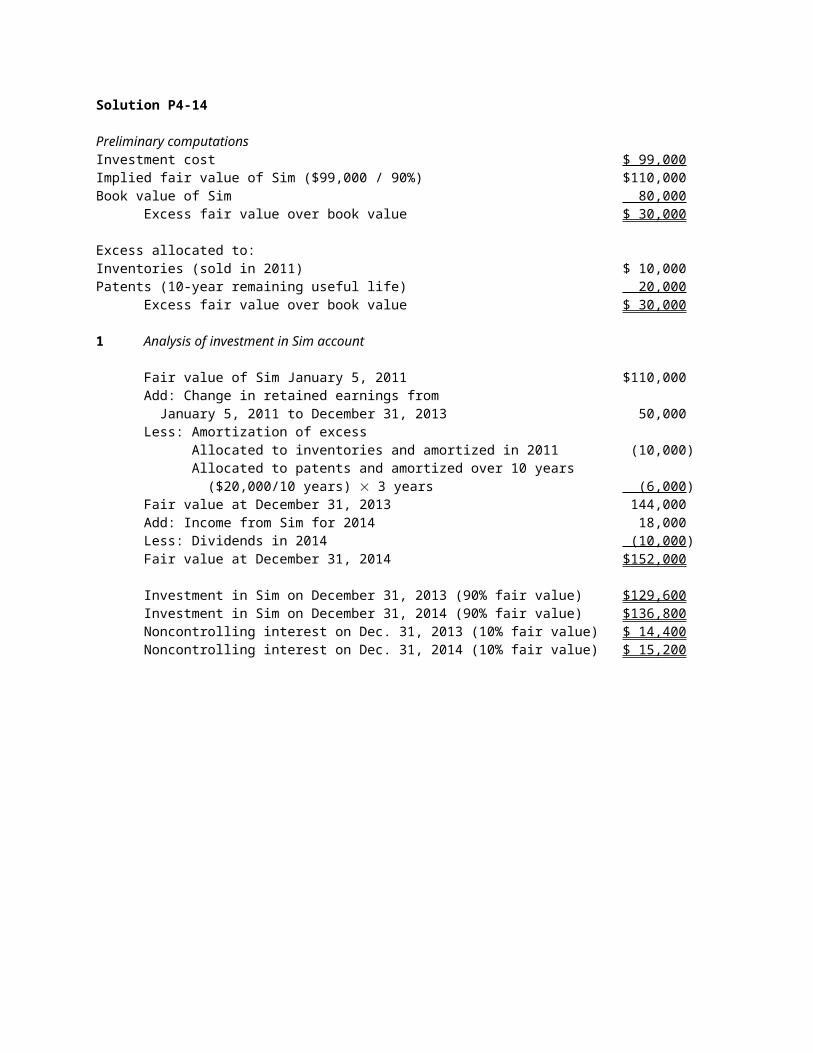

Solution P4-14

Preliminary computationsInvestment cost $ 99,000Implied fair value of Sim ($99,000 / 90%) $110,000Book value of Sim 80,000

Excess fair value over book value $ 30,000

Excess allocated to:Inventories (sold in 2011) $ 10,000Patents (10-year remaining useful life) 20,000

Excess fair value over book value $ 30,000

1 Analysis of investment in Sim account

Fair value of Sim January 5, 2011 $110,000Add: Change in retained earnings from January 5, 2011 to December 31, 2013 50,000Less: Amortization of excess

Allocated to inventories and amortized in 2011 (10,000)Allocated to patents and amortized over 10 years ($20,000/10 years) ´ 3 years (6,000)

Fair value at December 31, 2013 144,000Add: Income from Sim for 2014 18,000Less: Dividends in 2014 (10,000)Fair value at December 31, 2014 $152,000

Investment in Sim on December 31, 2013 (90% fair value) $129,600Investment in Sim on December 31, 2014 (90% fair value) $136,800Noncontrolling interest on Dec. 31, 2013 (10% fair value) $ 14,400Noncontrolling interest on Dec. 31, 2014 (10% fair value) $ 15,200

Solution P4-14 (continued)

Pep Company and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2014

Pep SimAdjustments andEliminations

IncomeStatement

RetainedEarnings

BalanceSheet

DebitsCash $ 11,000 $ 15,000 $ 26,000

Accounts receivable 15,000 25,000 40,000

Plant assets 220,000 180,000 400,000

Investment in Sim 136,800

a 7,200b 129,600

Patents b 14,000 c 2,000 12,000

Cost of goods sold 50,000 30,000 $ 80,000*

Operating expenses 25,000 40,000 c 2,000 67,000*

Dividends 20,000 10,000 a 9,000 $ 20,000*

d 1,000 ________

$477,800 $300,000 $478,000

CreditsAccumulated depreciation $ 90,000 $ 50,000 140,000

Liabilities 80,000 30,000 110,000

Capital stock 100,000 60,000 b 60,000 100,000

Paid-in-excess 20,000 20,000

Retained earnings 71,600 70,000 b 70,000 71,600

Sales 100,000 90,000 190,000

Income from Sim 16,200 ________ a 16,200

$477,800 $300,000

Noncontrolling interest Dec 31, 2013 b 14,400

Noncontrolling interest share($18,000 adj. inc. x 10%) d 1,800 1,800*

Controlling share of NI $ 41,200 41,200

Consolidated retained earnings $ 92,800 92,800

Noncontrolling interest Dec 31, 2014 ________ d 800 15,200

164,000 164,000 $478,000* Deduct

a To eliminate income from subsidiary and dividends received and reduce the investment account to its beginning-of-the-period balance.

b To eliminate reciprocal investment and subsidiary equity amounts, establish beginning noncontrolling interest, and adjust patents for the unamortized excess as of the beginning of the period.

c To amortize excess allocated to patents for 2014.d To enter noncontrolling interest share of subsidiary income and dividends.

Solution P4-15

1 Journal entries on Peg’s books

January 1, 2011Investment in Sup (90%) 36,000

Cash 36,000To record purchase of 90% of Sup’s stock for cash.

July 1, 2011Investment in Ell (25%) 14,000

Cash 14,000To record purchase of 25% of Ell’s stock for cash.

November 2011Cash 5,400

Investment in Sup (90%) 5,400To record receipt of 90% of Sup’s $6,000 dividends.

November 2011Cash 2,500

Investment in Ell (25%) 2,500To record receipt of 25% of Ell’s $10,000 dividends.

December 31, 2011Investment in Sup (90%) 9,000

Income from Sup 9,000To record Share of Sup’s reported income ($56,000 - $46,000) ´ 90%

December 31, 2011Investment in Ell (25%) 1,400

Income from Ell 1,400To record investment income from Ell for 2011 computed as:Share of Ell’s reported income $ 1,500($60,000-$48,000)´1/2 year ´ 25%Less: Amortization of excess [$14,000 – ($48,000 ´ 25%)] ¸ 10 years ´ 1/2 year (100)

$ 1,400

Solution P4-15 (continued)

2 Peg’s separate company financial statements

Peg CorporationIncome Statement

for the year ended December 31, 2011

RevenuesSales $200,000Income from Sup 9,000Income from Ell 1,400

Total revenue $210,400Costs and expenses

Cost of sales $120,000Other expenses 50,000

Total costs and expenses 170,000Net income $ 40,400

Peg CorporationRetained Earnings Statement

for the year ended December 31, 2011

Retained earnings January 1 $ 40,000Add: Net income 40,400Deduct: Dividends (20,000)

Retained earnings December 31 $ 60,400

Peg CorporationBalance Sheet

at December 31, 2011

AssetsCurrent assets:

Cash $ 37,900Other current assets 80,000 $117,900

Plant assets — net 240,000Investments:

Investment in Sup (90%) $ 39,600Investment in Ell (25%) 12,900 52,500

Total assets $410,400

Liabilities and stockholders’ equityCurrent liabilities $ 50,000Stockholders’ equity:Capital stock $300,000Retained earnings December 31 60,400 360,400

Total liabilities and stockholders’ equity $410,400

Solution P4-15 (continued)

3 Consolidation workpapers — trial balance format

Peg Corporation and SubsidiaryConsolidation Workpapers

for the year ended December 31, 2011

Peg90%Sup

Adjustments andEliminations

IncomeStatement

RetainedEarnings

BalanceSheet

DebitsCash $ 37,900 $ 8,000 $ 45,900

Other current assets 80,000 22,000 102,000

Plant assets — net 240,000 28,000 268,000

Investment in Sup 39,600

a 3,600b 36,000

Investment in Ell 12,900 12,900

Cost of sales 120,000 32,000 $152,000*

Other expenses 50,000 14,000 64,000*

Dividends 20,000 6,000 a 5,400 $ 20,000*d 600* ________

Total debits $600,400 $110,000 $428,800

CreditsCurrent liabilities $ 50,000 $ 14,000 $ 64,000

Capital stock 300,000 36,000 b 36,000 300,000

Retained earnings 40,000 4,000 b 4,000 40,000

Sales 200,000 56,000 256,000

Income from Sup 9,000 a 9,000

Income from Ell 1,400 ________ 1,400

Total credits $600,400 $110,000

Noncontrolling interest - January 1 b 4,000

Noncontrolling interest share $10,000 ´ 10% d 1,000 1,000*

Controlling share of NI $ 40,400 40,400

Consolidated retained earnings $ 60,400 60,400

Noncontrolling interest December 31 ________ d 400 4,400

50,000 50,000 $428,800

Solution P4-15 (continued)

4 Consolidated financial statementsPeg Corporation and SubsidiaryConsolidated Income Statement

for the year ended December 31, 2011Revenues

Sales $256,000Income from Ell (equity method) 1,400

Total revenues $257,400Costs and expenses

Cost of sales $152,000Other expenses 64,000

Total costs and expenses 216,000Total consolidated income 41,400Less: Noncontrolling interest share 1,000

Controlling share of NI $ 40,400

Peg Corporation and SubsidiaryConsolidated Retained Earnings Statementfor the year ended December 31, 2011

Consolidated retained earnings January 1 $ 40,000Add: Controlling share of NI 40,400Deduct: Dividends (20,000)

Consolidated retained earnings December 31 $ 60,400

Peg Corporation and SubsidiaryConsolidated Balance Sheet

at December 31, 2011Assets

Current assets:Cash $ 45,900Other current assets 102,000 $147,900

Plant assets — net 268,000Investments and other assets:

Investment in Ell 12,900Total assets $428,800Liabilities and stockholders’ equity

Current liabilities $ 64,000Stockholders’ equity:Capital stock $300,000Consolidated retained earnings 60,400Noncontrolling interest 4,400 364,800

Total liabilities and stockholders’ equity $428,800

Solution P4-16

Partial consolidated statement of cash flows using the direct methodPil Corporation and Subsidiaries

Partial Consolidated Statement of Cash Flowsfor the current year

Cash Flows from Operating ActivitiesCash received from customers $3,200,000Dividends from equity investees 80,000Interest received from short-term loan 10,000Cash paid for other expenses (900,000)Cash paid to suppliers (1,260,000) Net cash flow from operating activities $1,130,000

Solution P4-17

Direct Method

Pes Corporation and SubsidiaryConsolidated Statement of Cash Flowsfor the year ended December 31, 2011

Cash Flows from Operating ActivitiesCash received from customers $1,340,000Cash paid to suppliers $696,000Cash paid for operating expenses 315,000 (1,011,000)Net cash flows from operating activities 329,000

Cash Flows from Investing ActivitiesPurchase of equipment (250,000)Net cash flows from investing activities (250,000)

Cash Flows from Financing ActivitiesPayment of cash dividends — controlling (72,000)Payment of cash dividends — noncontrolling (4,000)Payment of long-term liabilities (22,000)Net cash flows from financing activities (98,000)

Decrease in cash for the year (19,000)Cash on January 1 130,000Cash on December 31 $ 111,000

Reconciliation of controlling share of consolidated net income to net cash provided by operating activities

Controlling share of NI $260,000Adjustments to reconcile controlling share of consolidated net income to net cash provided by operating activities:

Noncontrolling interest share $ 10,000Depreciation expense 102,000Patents amortization 1,000Increase in accounts payable 44,000Increase in accounts receivable (10,000)Increase in inventories (40,000)Increase in other current assets (38,000) 69,000Net cash flows from operating activities $329,000

Solution P4-17 (continued)

Indirect Method

Pes Corporation and SubsidiaryConsolidated Statement of Cash Flowsfor the year ended December 31, 2011

Cash Flows from Operating ActivitiesControlling share of NI $260,000

Adjustments to reconcile controlling share of consolidated net income to net cash provided by operating activities:

Noncontrolling interest share 10,000Depreciation $102,000Patents amortization 1,000Increase in accounts receivable (10,000)Increase in inventories (40,000)Increase in other current assets (38,000)Increase in accounts payable 44,000

69,000Net cash flows from operating activities 329,000

Cash Flows from Investing ActivitiesPurchase of equipment (250,000)Net cash flows from investing activities (250,000)

Cash Flows from Financing ActivitiesPayment of cash dividends — controlling (72,000)Payment of cash dividends — noncontrolling (4,000)Payment of long-term liabilities (22,000)Net cash flows from financing activities (98,000)

Decrease in cash for the year (19,000)Cash on January 1 130,000Cash on December 31 $111,000

Note: The cash flows from investing activities and cash flows from financing activities sections of the statement of cash flows are the same under the direct and indirect method.

Solution P4-18 [AICPA]

Indirect Method

Puh, Inc. and SubsidiaryStatement of Cash Flows (Indirect Method)

for the year ended December 31, 2011

Cash Flows from Operating ActivitiesControlling share of NI $ 198,000Adjustments to reconcile controlling share of consolidated net income to net cash provided by operating activities:

Noncontrolling interest share $ 33,000Depreciation expense 82,000Patents amortization 3,000Decrease in accounts receivable 22,000Increase in accounts and accrued payables 121,000Increase in deferred income taxes 12,000Increase in inventories (70,000)Gain on marketable equity securities (11,000)Gain on sale of equipment (6,000) 186,000

Net cash flows from operating activities 384,000Cash Flows from Investing Activities

Purchase of equipment $(127,000)Proceeds from sale of equipment 40,000

Net cash flows from investing activities (87,000)Cash Flows from Financing Activities

Cash received from sale of treasury stock 44,000Payment of cash dividends — controlling (58,000)Payment of cash dividends — noncontrolling (15,000)Payment on long-term note (150,000)

Net cash flows from financing activities (179,000)Increase in cash for the year 118,000Cash on January 1 195,000Cash on December 31 $ 313,000

Listing of non-cash investing and financing activities:

Issued common stock in exchange for land with a fair value of $215,000.

Solution P4-18 (continued)

Indirect Method

Puh, Inc. and SubsidiaryWorkpapers for the Statement of Cash Flows (Indirect Method)

for the year ended December 31, 2011

Cash Flow Cash Flow Cash Flow Year’s Reconciling Items From Investing FinancingChange Debit Credit Operations Activities Activities

Asset ChangesCash 118,000Allowance to reduce MES 11,000 e 11,000

Accounts receivable — net (22,000) f 22,000

Inventories 70,000 g 70,000Land* 215,000 h 215,000Plant and equipment 65,000 k 62,000 j 127,000Accumulated depreciation (54,000) l 82,000 k 28,000

Patents — net (3,000) m 3,000

Total asset changes 400,000

Changes in EquitiesAccounts & accrued payable 121,000 n 121,000Note payable long-term (150,000) o 150,000Deferred income taxes 12,000 p 12,000Noncontrolling interest in Sto

18,000 b 33,000 d 15,000

Common stock, $10 par* 100,000 h 100,000Additional paid-in capital 123,000 h 115,000

i 8,000Retained earnings 140,000 a 198,000 c 58,000Treasury stock at cost 36,000 i 36,000

Total changes in equities 400,000

Controlling share of NI a 198,000 198,000Noncontrolling interest share b 33,000 33,000Gain on MES e 11,000 (11,000)Purchase of plant and equipment j 127,000 (127,000)Sale of equipment k 40,000 40,000Gain on equipment k 6,000 (6,000)Depreciation expense l 82,000 82,000Payment on long-term note o 150,000 (150,000)Amortization of patents m 3,000 3,000Decrease in receivables f 22,000 22,000Increase in inventories g 70,000 (70,000)Increase in accounts and accrued payables

n 121,000 121,000

Increase in deferred income taxes p 12,000 12,000Proceeds from treasury stock i 44,000 44,000

Payment of dividends — controlling c 58,000 (58,000)

Payment of dividends — noncontrolling d 15,000 (15,000)

1,229,000 1,229,000384,000 (87,000) (179,000)

Cash increase for the year = $384,000 – $87,000 – $179,000 = $118,000.* Non-cash item: Purchased $215,000 land through common stock issuance.

Solution P4-19

Indirect Method

Pil Corporation and SubsidiaryConsolidated Statement of Cash Flowsfor the year ended December 31, 2011

Cash Flows from Operating ActivitiesControlling share of NI $1,000,000

Adjustments to reconcile controlling share of consolidated net income to net cash provided by operating activities:

Noncontrolling interest share $ 80,000Depreciation expense 400,000Patents amortization 20,000Increase in accounts payable 34,000

Income less dividends — equity investee (60,000)

Increase in accounts receivable (420,000) 54,000Net cash flows from operating activities 1,054,000Cash Flows from Investing Activities

Purchase of equipment $(1,000,000)Net cash flows from investing activities (1,000,000)Cash Flows from Financing Activities

Cash received from long-term note $ 400,000

Payment of cash dividends — controlling (274,000)

Payment of cash dividends — noncontrolling (40,000)

Net cash flows from financing activities 86,000Increase in cash for the year 140,000Cash on January 1 720,000Cash on December 31 $ 860,000

Solution P4-19 (continued)

Indirect MethodPil Corporation and Subsidiary

Workpapers for the Statement of Cash Flows (Indirect Method)for the year ended December 31, 2011

Cash Flows Cash Flows Cash FlowsYear’s Reconciling Items From Investing FinancingChange Debit Credit Operations Activities Activities

Asset ChangesCash $ 140,000

Accounts receivable — net 420,000 e 420,000

Inventories 0

Plant & equipment — net 600,000 F 400,000 g 1,000,000

Equity investments 60,000 l 60,000 m 120,000Patents (20,000) h 20,000

Total asset changes $1,200,000

Changes in EquitiesAccounts payable $ 34,000 i 34,000Dividends payable 26,000 k 26,000Long-term note payable 400,000 j 400,000Common stock 0Other paid-in capital 0Retained earnings 700,000 a 1,000,000 c 300,000Noncontrol. interest 20% 40,000 b 80,000 d 40,000

Changes in equities $1,200,000

Controlling share of NI a 1,000,000 $1,000,000Noncontrolling interest share b 80,000 80,000Purchase of plant & equipment g 1,000,000 $(1,000,000)

Depreciation — plant & equipment f 400,000 400,000

Amortization of patents h 20,000 20,000Increase in accounts receivable e 420,000 (420,000)Income less dividends from Investees m 120,000 l 60,000 (60,000)Increase in accounts payable i 34,000 34,000Received cash from long-term note J 400,000 0 $ 400,000

Payment of dividends — controlling c 300,000 k 26,000 (274,000)

Payment of dividends — noncontrolling d 40,000 __ _ (40,000)

3,900,000 3,900,000 $1,054,000 $(1,000,000) $ 86,000

Cash increase for the year = $1,054,000 - $1,000,000 + $86,000 = $140,000

Solution P4-19 (continued)

Direct Method

Pil Corporation and SubsidiaryConsolidated Statement of Cash Flowsfor the year ended December 31, 2011

(in thousands)

Cash Flows from Operating ActivitiesCash received from customers $4,780Cash received from equity investees 60Cash paid to suppliers $ 2,866Cash paid for other operating expenses 920 (3,786)

Net cash flows from operating activities 1,054Cash Flows from Investing Activities

Purchase of equipment $(1,000)Net cash flows from investing activities (1,000)Cash Flows from Financing Activities

Cash received from long-term note $ 400

Payment of cash dividends — controlling (274)

Payment of cash dividends — noncontrolling (40)

Net cash flows from financing activities 86Increase in cash for the year 140Cash on January 1 720Cash on December 31 $ 860

Reconciliation of controlling share of consolidated net income to net cash provided by operating activitiesControlling share of NI $1,000Adjustments to reconcile controlling share of consolidated net income to net cash provided by operating activities:

Noncontrolling interest share $ 80

Income less dividends — equity investee (60)

Depreciation expense 400Patents amortization 20Increase in accounts payable 34Increase in accounts receivable (420) 54

Net cash flows from operating activities $1,054

Solution P4-19 (continued)

Direct Method

Pil Corporation and SubsidiaryWorkpapers for the Statement of Cash Flows (Direct Method)

for the year ended December 31, 2011(in thousands)

Cash Flow Cash Flow Cash Flow Year’s Reconciling Items From Investing FinancingChange Debit Credit Operations Activities Activities

Asset ChangesCash $ 140Accounts receivable — net 420 a 420Inventories 0Plant & equipment — net 600 b 400 c 1,000Equity investments 60 d 60Patents (20) e 20 Total asset changes $1,200Changes in EquitiesAccounts payable $ 34 f 34Dividends payable 26 g 26Long-term note payable 400 h 400Retained earnings* 700Noncontrol.interest 20% 40 i 80 j 40 Changes in equities $1,200Ret. earnings change*Sales $5,200 a 420 $4,780Income from equity investees 120 d 60 60Cost of goods sold (2,900) f 34 (2,866)Depreciation expense (400) b 400 0Other operating expenses (940) e 20 (920)Noncontrolling interest share (80) i 80 0

Dividends declared — Pil (300) g 26

k 274Retained earnings ______ change $ 700Received cash from long-term note h 400 $ 400

Payment of dividends — controlling k 274 (274)

Payment of dividends — noncontrolling j 40 (40)

Purchase of equipment c 1,000 $(1,000) __ 2,754 2,754 $1,054 $(1,000) $ 86

* Retained earnings changes replace the retained earnings account for reconciling purposes.

Cash increase for the year = $1,054 - $1,000 + $86 = $140.