Embed Size (px)

DESCRIPTION

notes

Citation preview

Chapter 3

Accrual Accounting

Accrual vs. Cash Basis AccountingACCRUAL ACCOUNTING CASH BASIS

• Records impact of transactions when they occur

• Required by IAS1 – Presentation of Financial Statements

• Records:▫ Revenue when ________▫ Expenses when ________

• Use by virtually all businesses

• Records transactions only if cash is involved▫ Cash receipts▫ Cash payments

• Ignores underlying economic activities

• Used by ________ or ________ operations

Copyright ©2014 Pearson Education2

Learning Objective 1Relate accrual accounting and cash flows

Copyright ©2014 Pearson Education3

Accrual accounting•Records _____ cash and non-cash

transactionsCash transactions Non-cash transactions

Collecting payments from customers

Sales on account

Receiving cash from interest earned

Purchases of inventory on account

Paying salaries, rent, and other expenses

Accrual of expenses incurred but not yet paid

Borrowing money Depreciation expense

Paying off loans Usage of prepaid rent, insurance, and supplies

Issuing shares (for cash) Earning of revenue when cash was collected in advanceCopyright ©2014 Pearson Education

4

Time Period Concept•Accounting information is reported at

regular intervals▫Basic accounting period is ________

•Calendar year▫January 1 – December 31

•Fiscal year▫12-month period ending on a date other

than December 31•Interim periods

▫Month or quarterCopyright ©2014 Pearson Education

5

Learning Objective TwoApply the revenue and matching principles

Copyright ©2014 Pearson Education6

Time-period concept

©2010 Pearson Prentice Hall. All rights reserved.

1-7

Ensures that accounting information is reported at regular intervals

IAS 1 requires an entity to present a complete set of financial statements at least annually.

Companies also prepare financial statements for interim periods of less than a year.

Copyright ©2014 Pearson Education

Revenue Recognition Principle• What is Revenue?

▫ Exchange of __________________• When should revenue be recorded?

▫ Transfer of __________ The entity has transferred to the buyer the significant risks and

rewards of ownership of the goods▫ Transfer of __________

The entity retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold

▫ Amounts _______________ The amount of revenue can be measured reliably

▫ ______________ It is probably that the economic benefits associated with the

transaction will flow to the entity▫ ______________

The costs incurred or to be incurred in respect of the transaction can be measured reliably

8

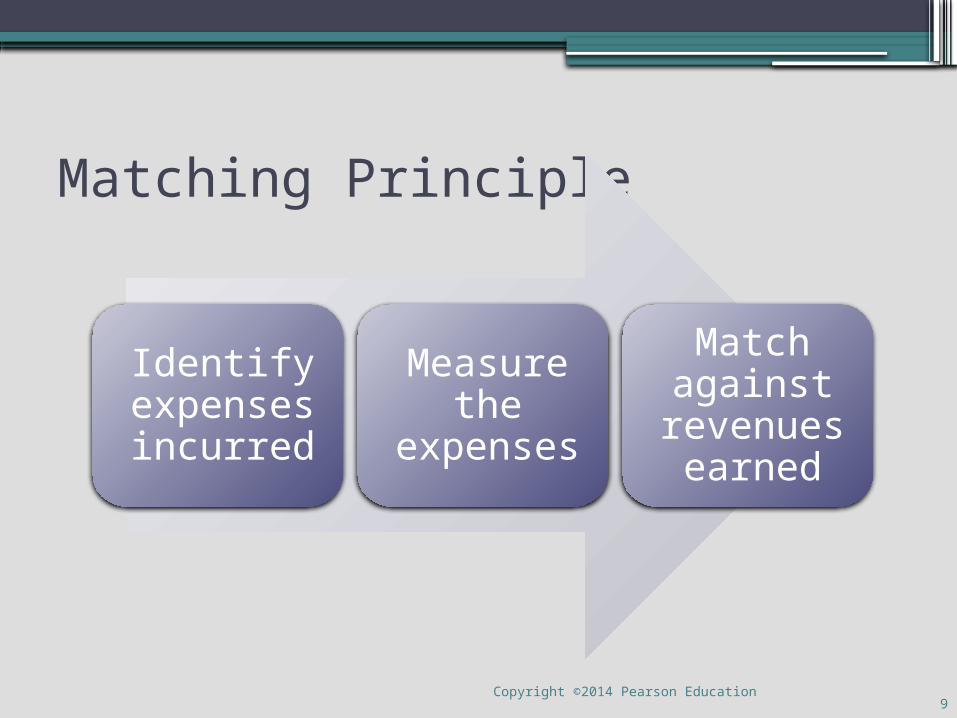

Matching Principle

Identify expenses incurred

Measure the

expenses

Match against

revenues earned

Copyright ©2014 Pearson Education9

Learning Objective ThreeAdjust the accounts

Copyright ©2014 Pearson Education10

Adjusting the Accounts

•Transactions▫In chapter 2, we discussed “transactions”

and accounting when they occur▫Some events do not relate to specific

transactions, so we have to “adjust” for them

•Adjusting Entries▫Financial statements issued at end of

period▫Several accounts on trial balance need to

be brought up-to-date Certain transactions that have not been

recordedCopyright ©2014 Pearson Education

11

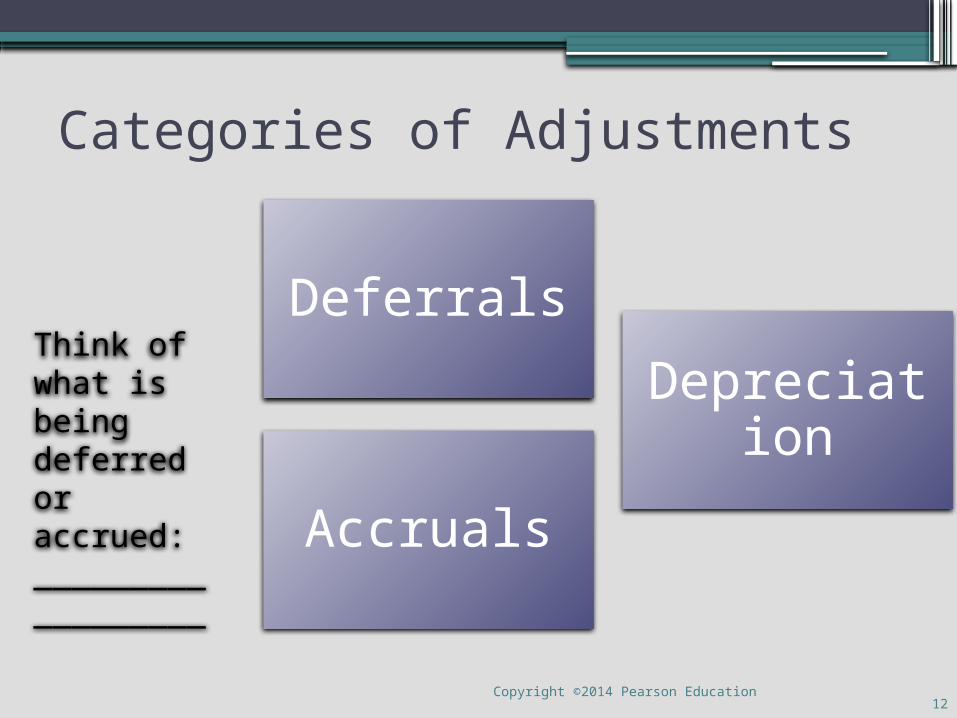

Categories of Adjustments

Deferrals

Depreciation

Accruals

Copyright ©2014 Pearson Education12

Think of what is being deferred or accrued:_________ _________

Deferrals•Business has paid or received cash in

advancePrepaid expense

• Recorded as an _____ when purchased

• _______ when used or expired

Unearned revenue

• Recorded as a ________ when payment is received

• Recorded as ________ when earned

Copyright ©2014 Pearson Education13

Prepaid Expenses•Recorded as assets when purchased

▫Example: On June 1, you prepay 3 months of rent for $3,000

•Expensed when used (or when time passes) JOURNAL

Date Accounts and explanation Debit Credit

Jun 1 _______________ 3,000

Cash 3,000

Paid three months’ rent in advance

Jun 30 Rent expense 1,000

_____________ 1,000

To record rent expenseCopyright ©2014 Pearson Education 14

Prepaid Rent

Prepaid rent

Jun 1 Jun 30

Rent expense

Jun 30

Amount expired

Amount remaining

Balance Sheet

Income Statemen

t

Copyright ©2014 Pearson Education15

Prepaid Expenses•Recorded as assets when purchased•Some pass with time. •Other assets expensed when used

▫Example: Purchase $700 of supplies on Jun 2 JOURNAL

Date Accounts and explanation Debit Credit

Jun 2 Supplies 700

Cash 700

Paid cash for supplies

Jun 30 Supplies expense 300

Supplies 300

To record rent expense

Copyright ©2014 Pearson Education16How do we know this number?

Supplies

Supplies

Jun 2 $700 Jun 30$___

$400

Supplies expense

$___Jun 30

Amount usedAmount on

hand

Balance Sheet

Income Statemen

t

Copyright ©2014 Pearson Education17

Supplies/Inventory _____

Depreciation

•Allocates cost of Property, Plant and Equipment (PPE) to expense over __________▫_______= estimated duration of how long

long-term asset will last▫Depreciation represents wear-and-tear and

obsolescence•Examples of PPE:

▫Buildings▫Equipment▫Furniture

Copyright ©2014 Pearson Education18

Accumulated Depreciation (__)•Depreciation expense (Exp)

▫amount allocated to __________•Accumulated Depreciation (XA)

▫Sum of ____________ expense and increases over plant asset’s life

•______-asset▫Normal credit balance (opposite to the

contra)▫Always has a companion account

•Book value (sometimes called Net Book Value)▫Cost of plant asset less accumulated

depreciation Copyright ©2014 Pearson Education19

Depreciation•Example: Company buys Equipment with

5-year useful life for $24,000 on June 2.▫Assume the asset has no salvage value▫Depreciation = $24,000/60 months =

$400/month

Copyright ©2014 Pearson Education

20

JOURNAL

Date Accounts and explanation Debit Credit

Jun 2 Equipment 24,000

Cash 24,000

Jun 30 Depreciation expense 400

Accumulated depreciation 400

*Note:___________________

DepreciationEquipment

Jun 2 $24,000

Depreciation Expense

$400Jun 30

Balance Sheet Income

Statement

Accumulated Depreciation

Jun 30$400

Copyright ©2014 Pearson Education21

$24,000/60 = $400

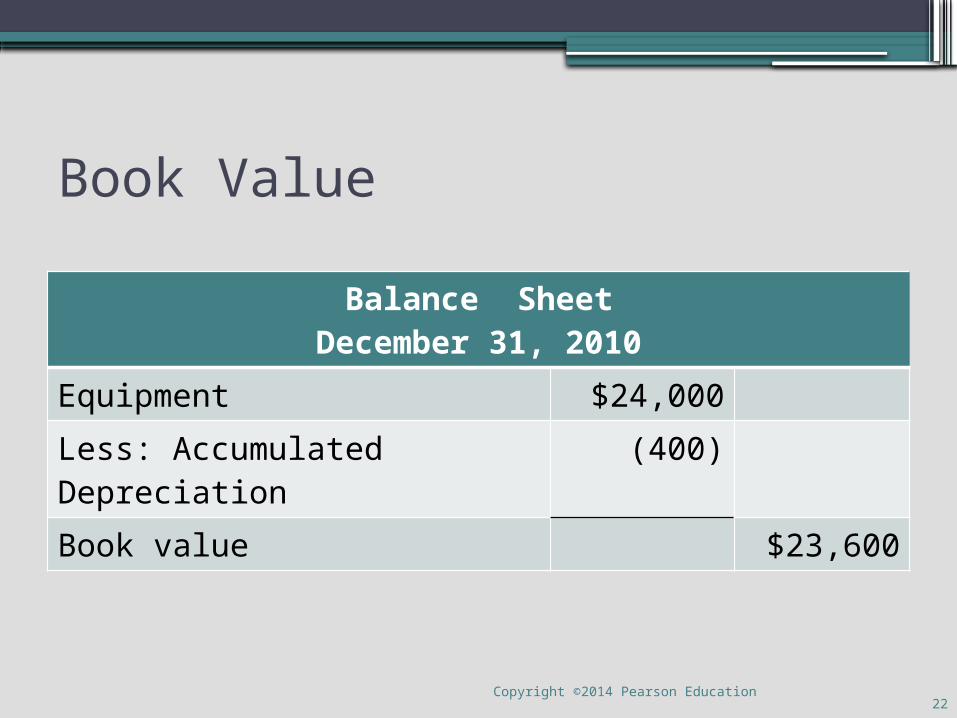

Book Value

Balance SheetDecember 31, 2010

Equipment $24,000

Less: Accumulated Depreciation

(400)

Book value $23,600

Copyright ©2014 Pearson Education22

Unearned Revenue•Sometimes called “Advances from

Customer”•Receive cash before revenue is earned•Creates a liability

▫Business owes customer a good or serviceJOURNAL

Date Accounts and explanation Debit Credit

Jun 1 Cash (A) 400

Unearned service revenue (L) 400

Received cash for revenue in advance.

Copyright ©2014 Pearson Education23

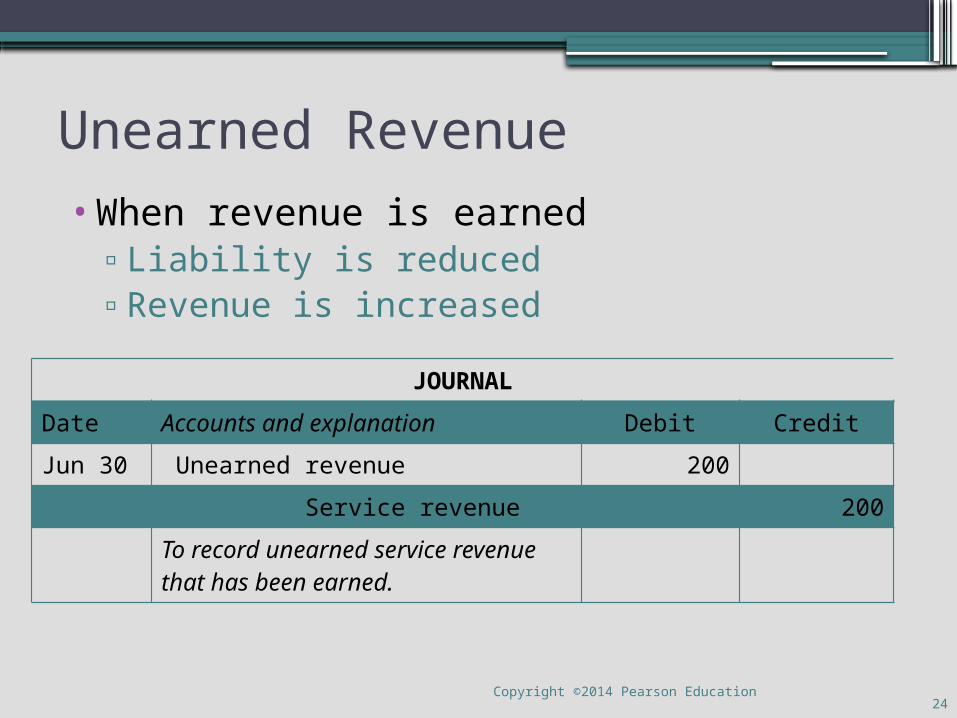

Unearned Revenue•When revenue is earned

▫Liability is reduced▫Revenue is increased

JOURNAL

Date Accounts and explanation Debit Credit

Jun 30 Unearned revenue 200

Service revenue 200

To record unearned service revenue that has been earned.

Copyright ©2014 Pearson Education24

Accruals

Accrued Expenses

• Record expense before paying cash

• Salaries, interest, and income taxes

Accrued Revenues

• Record revenue before collecting cash

• Earned and will collect next period

Copyright ©2014 Pearson Education25

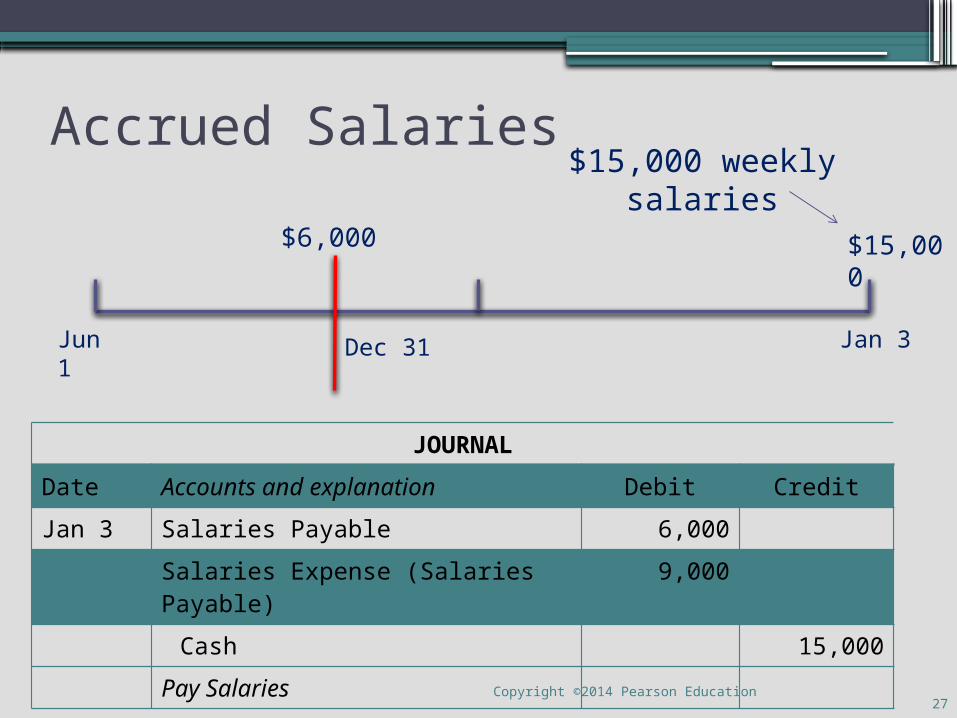

Accrued Salaries

JOURNAL

Date Accounts and explanation Debit Credit

Dec 31 Salaries expense 6,000

Salaries Payable 6,000

To accrue salaries expense

Jan 3 (Fri)Dec 31 (Tues)

$15,000 weekly salaries

$6,000 $15,000

Copyright ©2014 Pearson Education26

2-days accrued

Accrued Salaries

JOURNAL

Date Accounts and explanation Debit Credit

Jan 3 Salaries Payable 6,000

Salaries Expense (Salaries Payable)

9,000

Cash 15,000

Pay Salaries

Jun 1 Jan 3Dec 31

$15,000 weekly salaries

$6,000 $15,000

Copyright ©2014 Pearson Education27

Accrued Revenue

•Revenue earned but not yet received•Assume that a company is hired on June

15 to wash trucks each month for $600 (starting on June 15). The company will be paid on July 15. JOURNAL

Date Accounts and explanation Debit Credit

Jun 30 Accounts receivable ($600 x ½) 300

Service revenue 300

To accrue service revenue.

Copyright ©2014 Pearson Education28

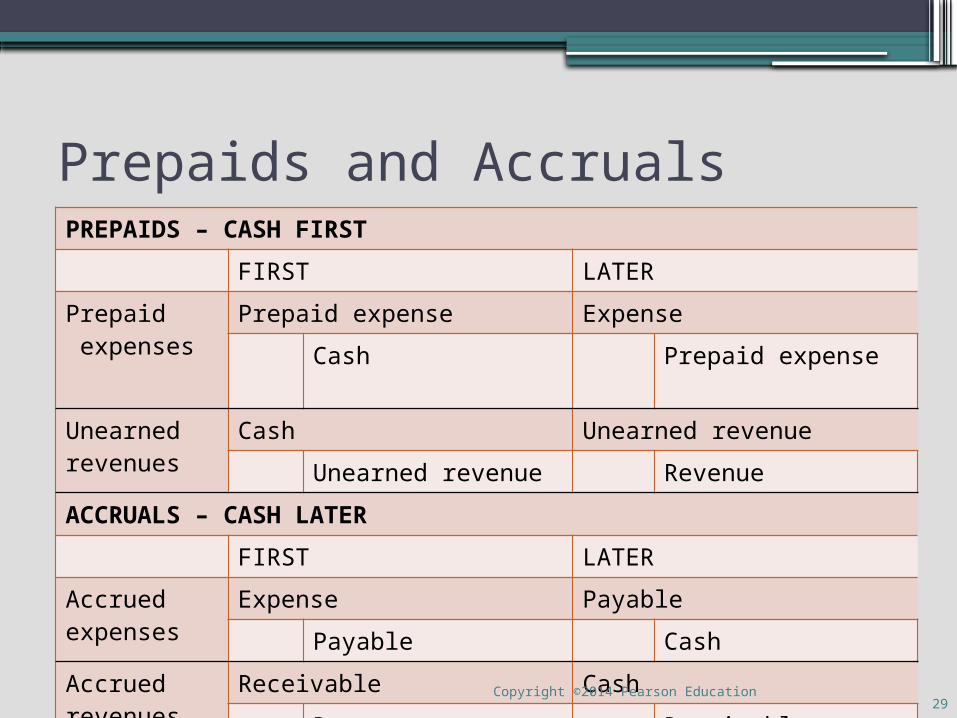

Prepaids and AccrualsPREPAIDS – CASH FIRST

FIRST LATER

Prepaid expenses

Prepaid expense Expense

Cash Prepaid expense

Unearned revenues

Cash Unearned revenue

Unearned revenue Revenue

ACCRUALS – CASH LATER

FIRST LATER

Accrued expenses

Expense Payable

Payable Cash

Accrued revenues

Receivable Cash

Revenue ReceivableCopyright ©2014 Pearson Education

29

Summary of the Adjusting Process•Two purpose of adjusting process

▫Measure (_____) income▫Update balance sheet

•Every adjusting entry affects at least one (of each):▫Revenue or expense▫Asset or liability

Copyright ©2014 Pearson Education30

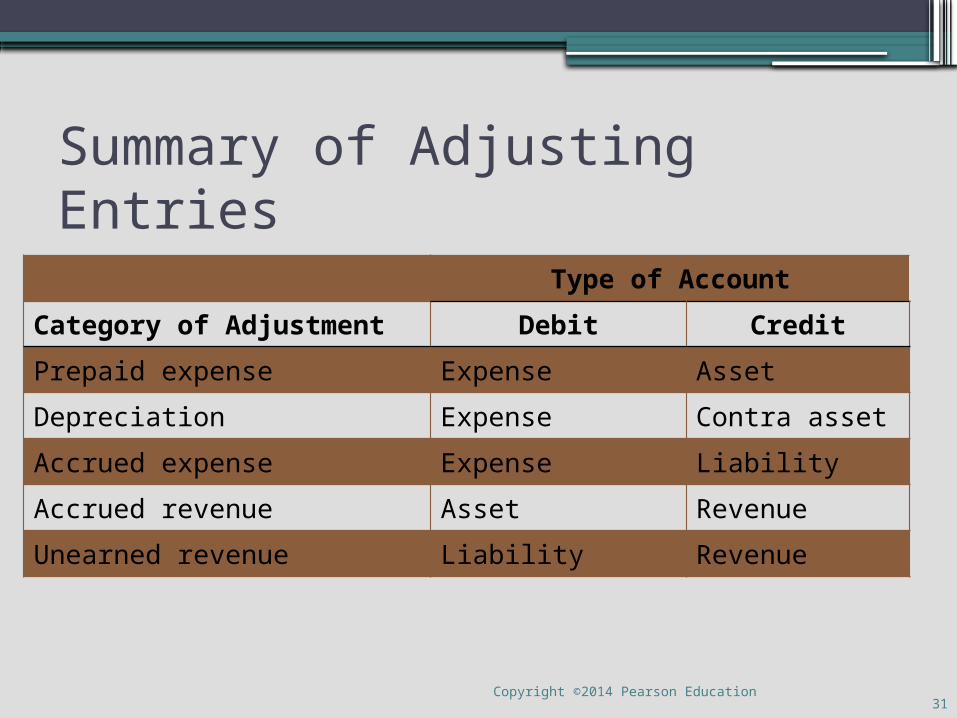

Summary of Adjusting Entries

Type of Account

Category of Adjustment Debit Credit

Prepaid expense Expense Asset

Depreciation Expense Contra asset

Accrued expense Expense Liability

Accrued revenue Asset Revenue

Unearned revenue Liability Revenue

Copyright ©2014 Pearson Education31

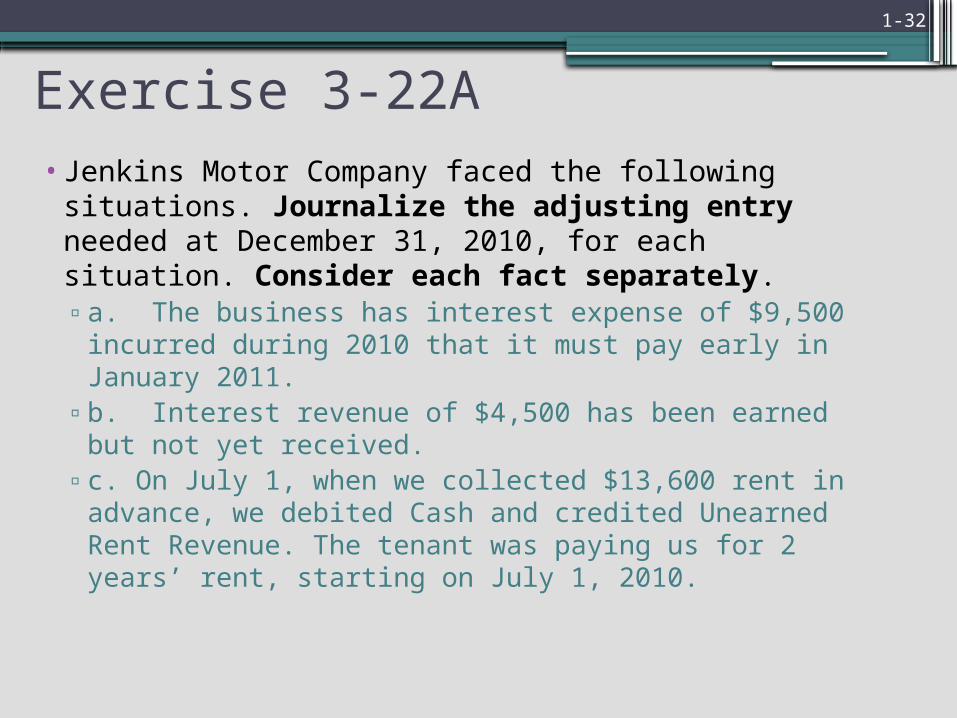

Exercise 3-22A• Jenkins Motor Company faced the following

situations. Journalize the adjusting entry needed at December 31, 2010, for each situation. Consider each fact separately.▫a. The business has interest expense of $9,500

incurred during 2010 that it must pay early in January 2011.

▫b. Interest revenue of $4,500 has been earned but not yet received.

▫c. On July 1, when we collected $13,600 rent in advance, we debited Cash and credited Unearned Rent Revenue. The tenant was paying us for 2 years’ rent, starting on July 1, 2010.

1-32

Exercise 3-22A

JOURNAL

Date Accounts and explanation Debit Credit

(a)

(b)

(c)

Copyright ©2014 Pearson Education33

Exercise 3-22A•d. Salary expense is $1,800 per day—Monday

through Friday—and the business pays employees each Friday. This year, December 31 falls on a Wednesday.

•e. The unadjusted balance of the Supplies account is $3,300. The total cost of supplies on hand is $1,200.

• f. Equipment was purchased at the beginning of this year at a cost of $100,000. The equipment’s useful life is 5 years with no salvage value. ©2010 Pearson Prentice Hall. All rights reserved.

1-34

Exercise 3-22A

JOURNAL

Date Accounts and explanation Debit Credit

(d)

(e)

(f)

Copyright ©2014 Pearson Education35

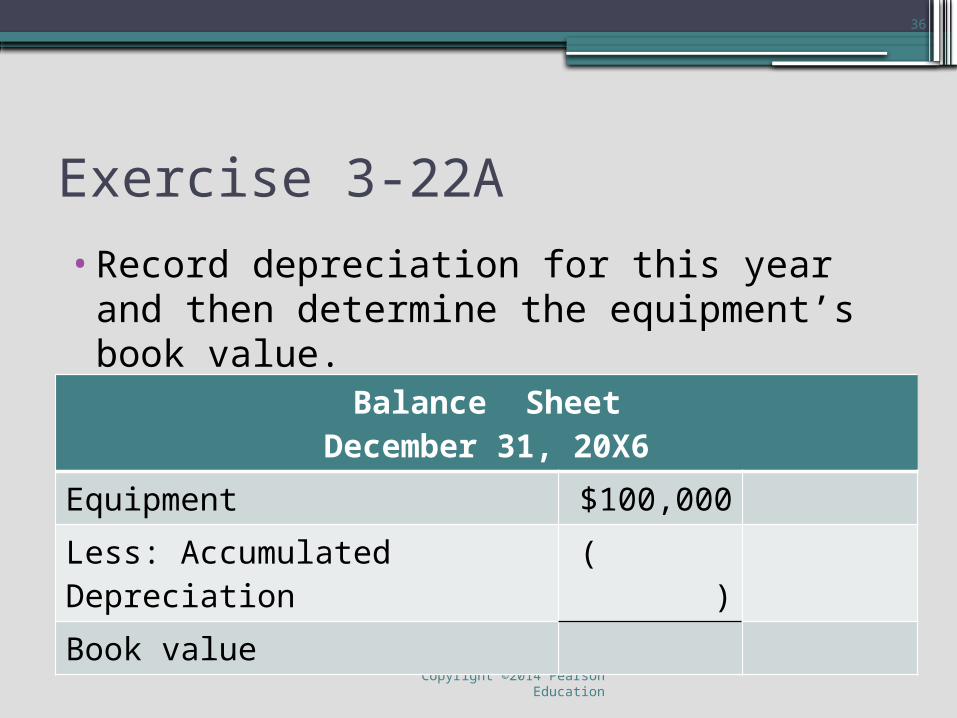

Exercise 3-22A

•Record depreciation for this year and then determine the equipment’s book value.

Copyright ©2014 Pearson Education

36

Balance SheetDecember 31, 20X6

Equipment $100,000

Less: Accumulated Depreciation

( )

Book value

The Adjusted Trial Balance

•Prepared after adjustments are journalized and posted

•Useful step in preparing financial statements

Copyright ©2014 Pearson Education37

Learning Objective FourPrepare the financial statements

Copyright ©2014 Pearson Education38

The Financial Statements

Income Statement• Lists revenues & expenses

Statement of Changes in Equity• Shows changes in components of equity

Balance Sheet• Reports assets, liabilities and

shareholders’ equityCopyright ©2014 Pearson Education

39

Flow of Data in Financial Statements

Income Statement

Revenues $$,$$$

Less: Expenses ($$,$$$)

Net Income $$,$$$

Statement Changes in Equity

Beginning equity balance $$,$$$

Plus: Net income $$,$$$

Less: Dividends ($,$$$)

Ending equity balance $$,$$$

Copyright ©2014 Pearson Education40

Flow of Data in Financial Statements

Statement of Changes in Equity

Beginning equity balance $$,$$$

Plus: Net income $$,$$$

Less: Dividends ($,$$$)

Ending equity balance $$,$$$

Balance Sheet

Current assets $$,$$$ Liabilities $$,$$$

PPE $$,$$$ Share Capital $$,$$$

Other assets $$,$$$ Retained earnings $$,$$$

Total assets$$$,$$

$Total liabilities & shareholders’ equity $$$,$$$

Copyright ©2014 Pearson Education41

Learning Objective FiveClose the books

Copyright ©2014 Pearson Education42

Closing the books

•Prepares the accounts for next period•Temporary accounts are set to zero and

closed into Retained earnings•Permanent accounts are not closed

Copyright ©2014 Pearson Education43

Temporary

• Closed• _______, _______ and _______

Permanent

• Not closed

• Assets, liabilities and equity

Copyright ©2014 Pearson Education44

Closing Entries

©2010 Pearson Prentice Hall. All rights reserved.

Close DividendsDebit Retained earnings Credit Dividends

Close ExpensesDebit Retained earnings Credit each expense

account

Close RevenuesDebit each revenue account Credit Retained earnings

Copyright ©2014 Pearson Education 45

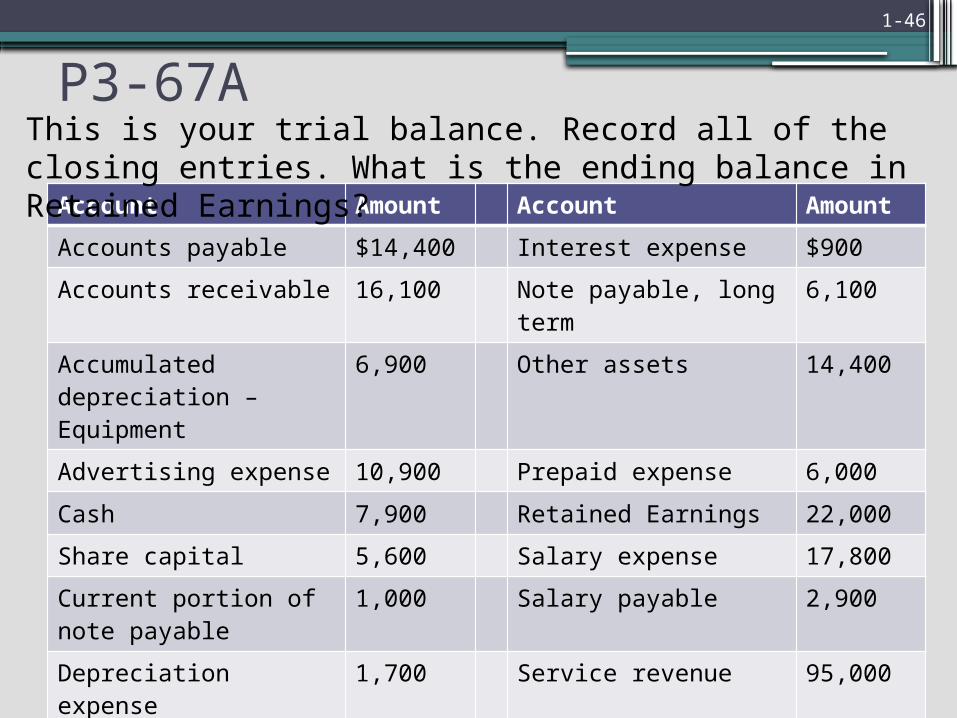

P3-67A

Account Amount Account Amount

Accounts payable $14,400 Interest expense $900

Accounts receivable 16,100 Note payable, long term

6,100

Accumulated depreciation – Equipment

6,900 Other assets 14,400

Advertising expense 10,900 Prepaid expense 6,000

Cash 7,900 Retained Earnings 22,000

Share capital 5,600 Salary expense 17,800

Current portion of note payable

1,000 Salary payable 2,900

Depreciation expense 1,700 Service revenue 95,000

Dividends 31,200 Supplies 3,600

Equipment 41,700 Supplies expense 4,400

Unearned Service Rev

2,700

1-46

This is your trial balance. Record all of the closing entries. What is the ending balance in Retained Earnings?

Problem 3-67AJOURNAL

Date Accounts and explanation Debit Credit

Copyright ©2014 Pearson Education47

Problem 3-67A

Retained Earnings

$Beginning Balance

$ Revenues$

$

Dividends

Expenses

$ Ending Balance

Copyright ©2014 Pearson Education48

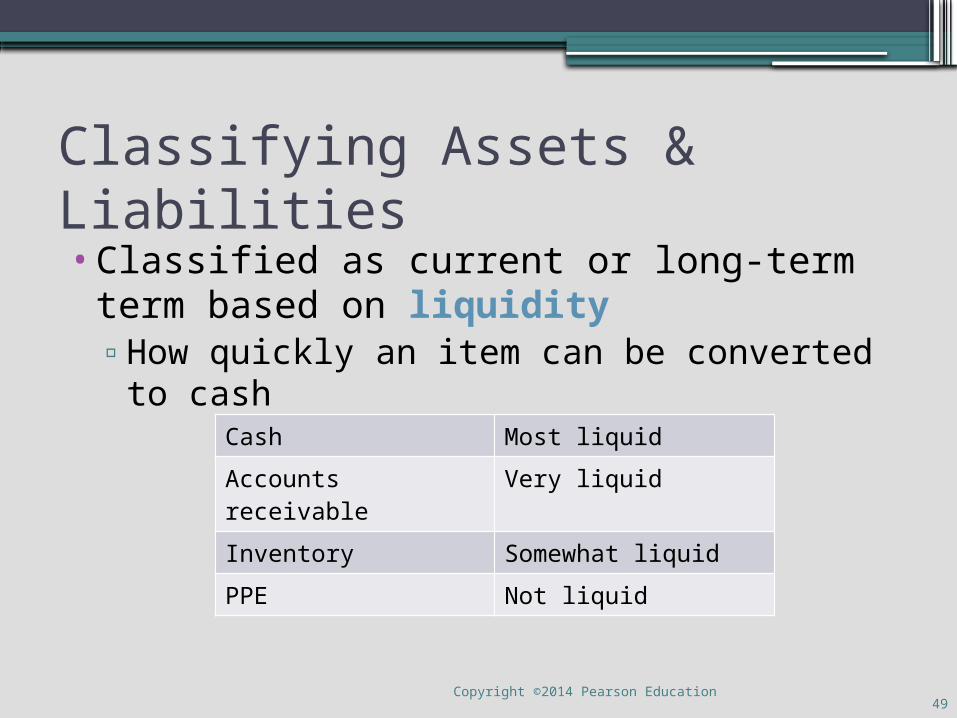

Classifying Assets & Liabilities•Classified as current or long-term term

based on liquidity▫How quickly an item can be converted to

cashCash Most liquid

Accounts receivable Very liquid

Inventory Somewhat liquid

PPE Not liquid

Copyright ©2014 Pearson Education49

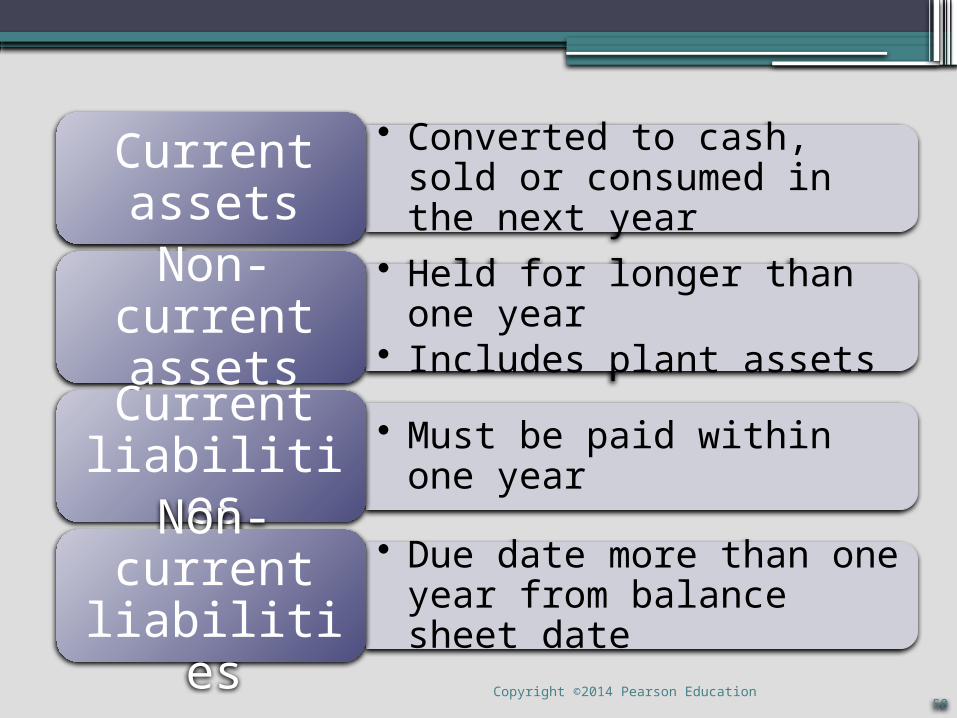

• Converted to cash, sold or consumed in the next year

Current assets

• Held for longer than one year

• Includes plant assets

Non-current assets

• Must be paid within one year

Current liabilities

• Due date more than one year from balance sheet date

Non-current

liabilitiesCopyright ©2014 Pearson Education

50

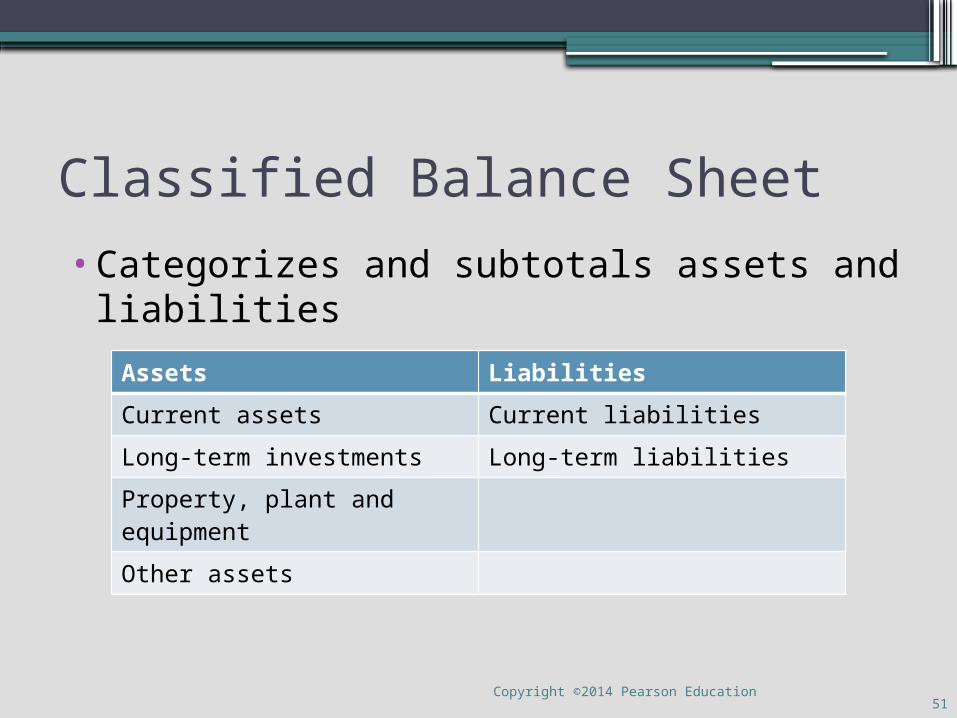

Classified Balance Sheet

•Categorizes and subtotals assets and liabilities

Assets Liabilities

Current assets Current liabilities

Long-term investments Long-term liabilities

Property, plant and equipment

Other assets

Copyright ©2014 Pearson Education51