Embed Size (px)

Citation preview

Chapter 3

Balance Sheet and Owners’ Interests

Chapter 3--Learning Objectives

1. Interpret the conceptual basis for the balance sheet and its

components: assets, liabilities, and owners’ equity

Balance Sheet

Shows financial position

of an enterprise at a particular

point in time

A “snapshot”

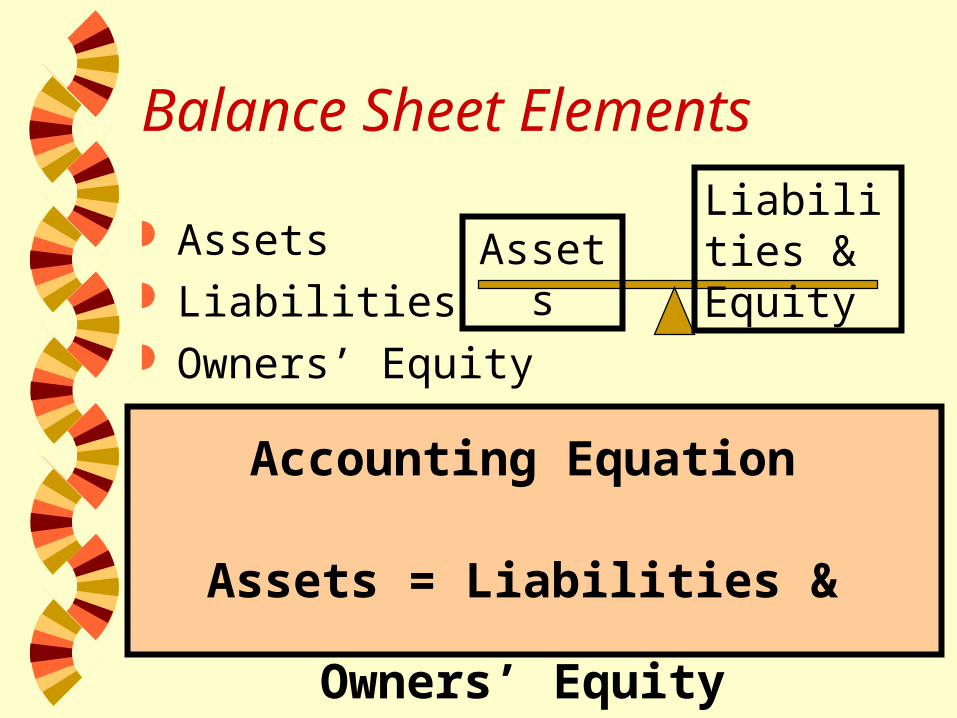

Balance Sheet Elements

Assets Liabilities Owners’ Equity

Accounting Equation

Assets = Liabilities & Owners’ Equity

AssetsLiabilities & Equity

Assets: Definition

Probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events

Assets: Characteristics

Probable Future Benefitwill contribute to future cash flows

Of a Particular Entitythe business that will receive the benefit

Transaction or event giving rise to the benefit has already occurred

Liabilities: Definition

Probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events

Liabilities: Characteristics

Present duty or obligation that entails the probable future transfer or use of assets

Of a Particular Entitythe business that has the duty or obligation

Transaction or event giving rise to the obligation has already occurred

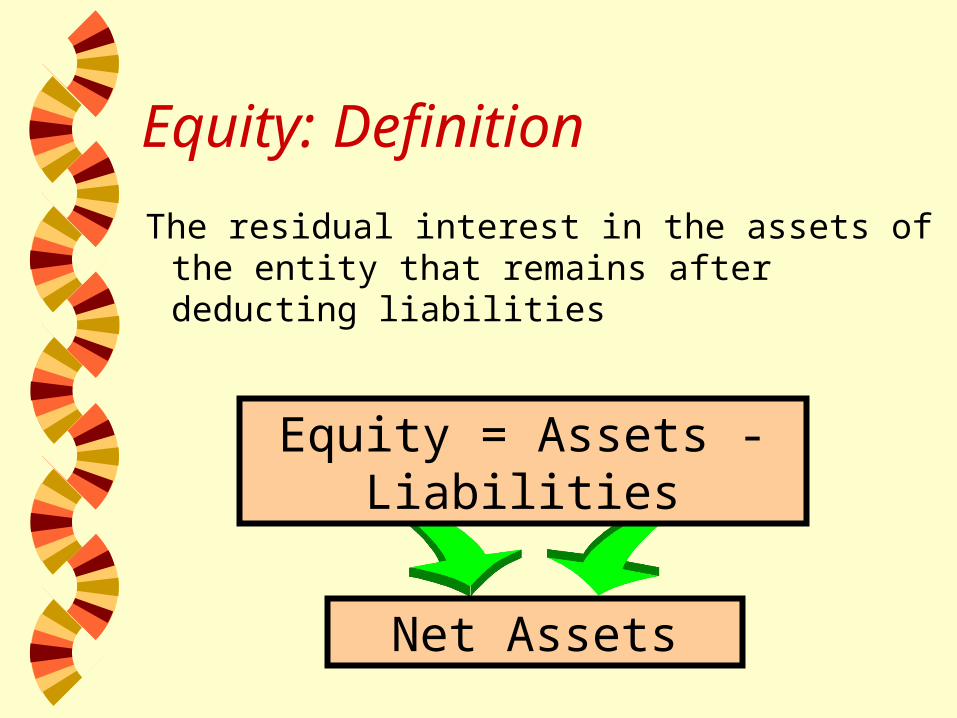

Equity: Definition

The residual interest in the assets of the entity that remains after deducting liabilities

Equity = Assets - Liabilities

Net Assets

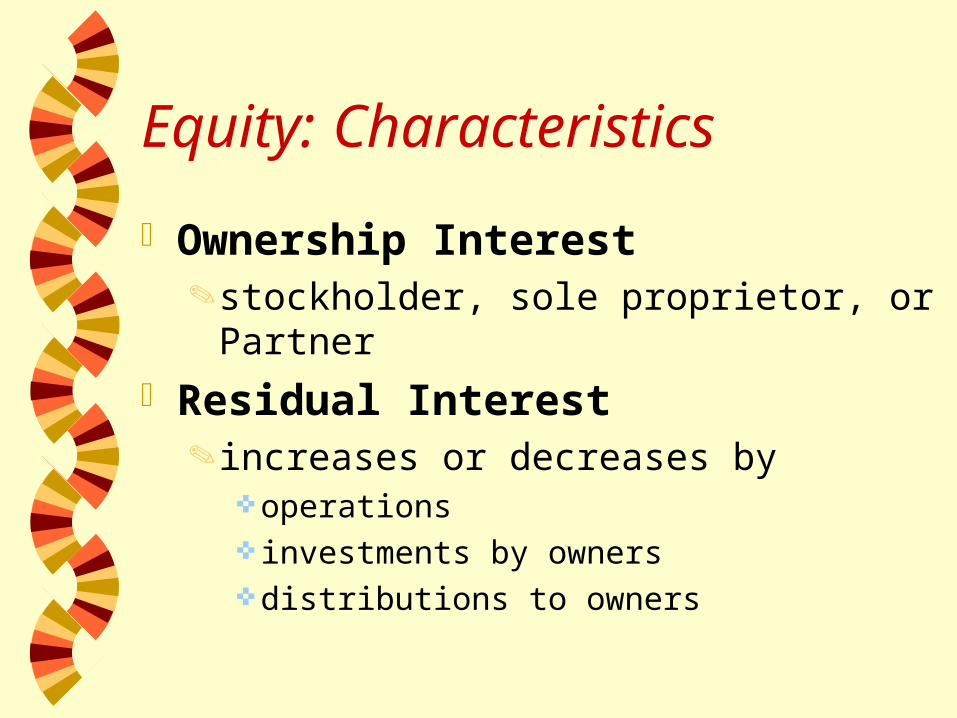

Equity: Characteristics

Ownership Intereststockholder, sole proprietor, or Partner

Residual Interestincreases or decreases by

operations investments by owners distributions to owners

Chapter 3--Learning Objectives

XYZ Company XYZ Company

2. Recognize the various formats and typical account classifications for the balance sheet

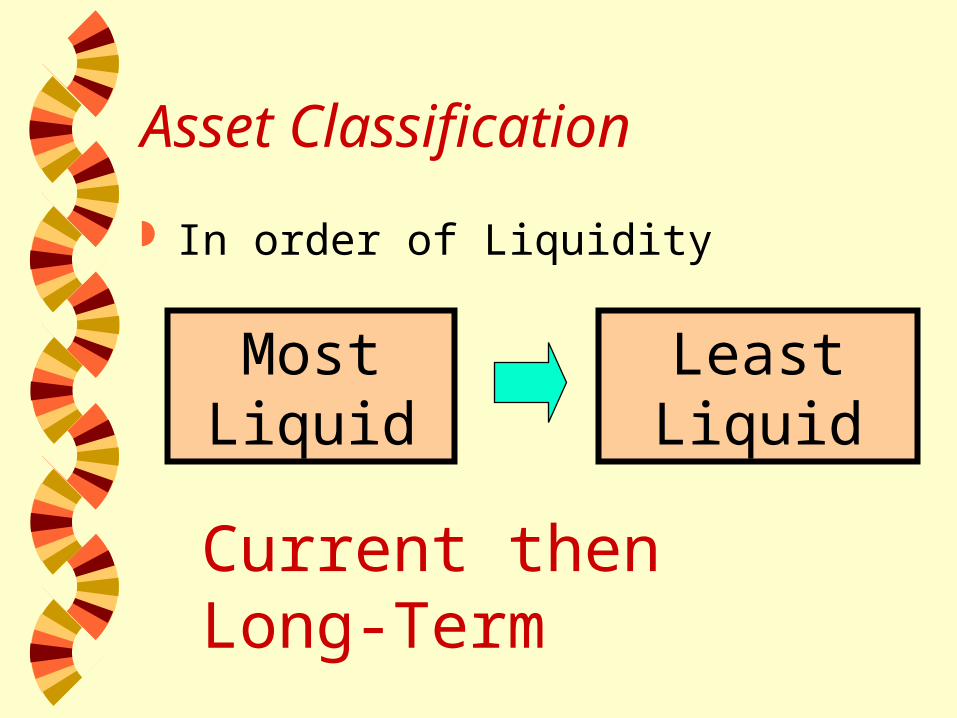

Asset Classification

In order of Liquidity

Current then Long-Term

Most Liquid

Least Liquid

Assets - Order of Classification

Current Assets Investments Property, Plant & Equipment Intangible Assets Other Assets

Chapter 3--Learning Objectives

3. Understand and identify the elements of current assets and current liabilities that comprise an enterprise’s working capital

Working Capital

Current assets

Less: Current liabilities

Equals: Working capital

Definition-Current Asset

Cash and other assets that can reasonably be expected to be converted into cash or consumed within the current operating cycle or one year whichever is longer

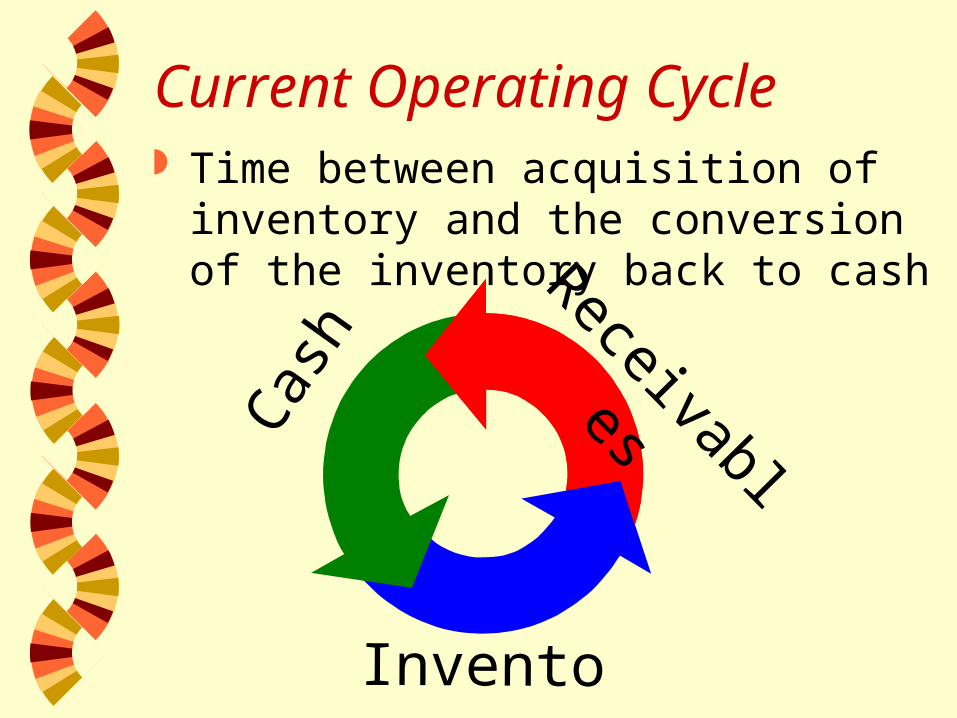

Current Operating Cycle Time between acquisition of inventory and

the conversion of the inventory back to cashCas

hReceivables

Inventory

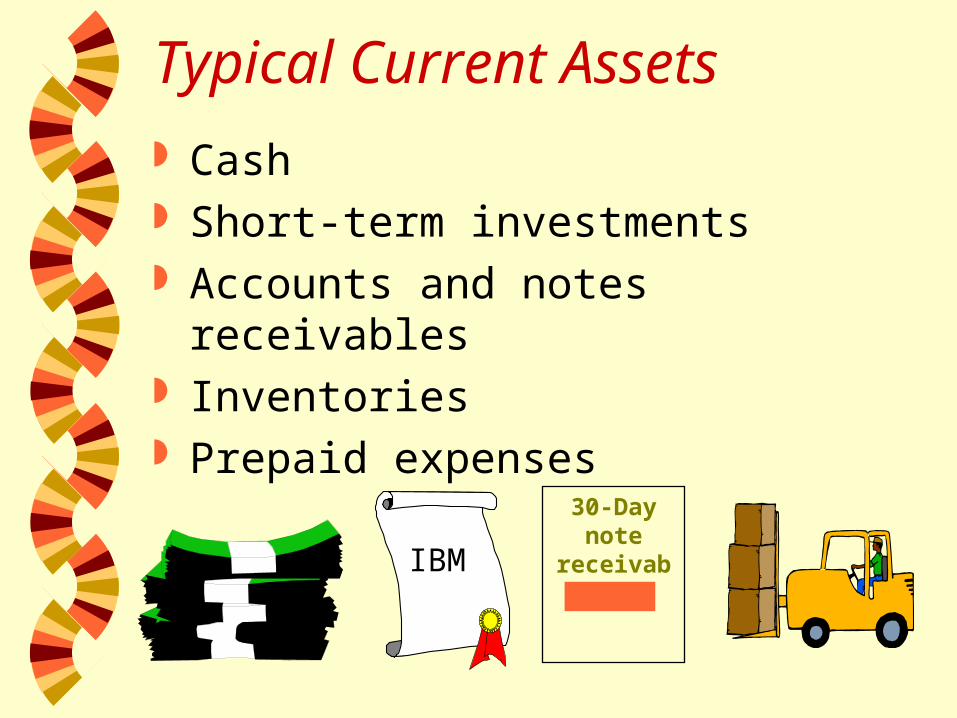

Typical Current Assets

Cash Short-term investments Accounts and notes receivables Inventories Prepaid expenses

30-Daynote

receivableIBM

Cash

All cash on hand and on deposit Readily available for current use Measured in U.S. dollars

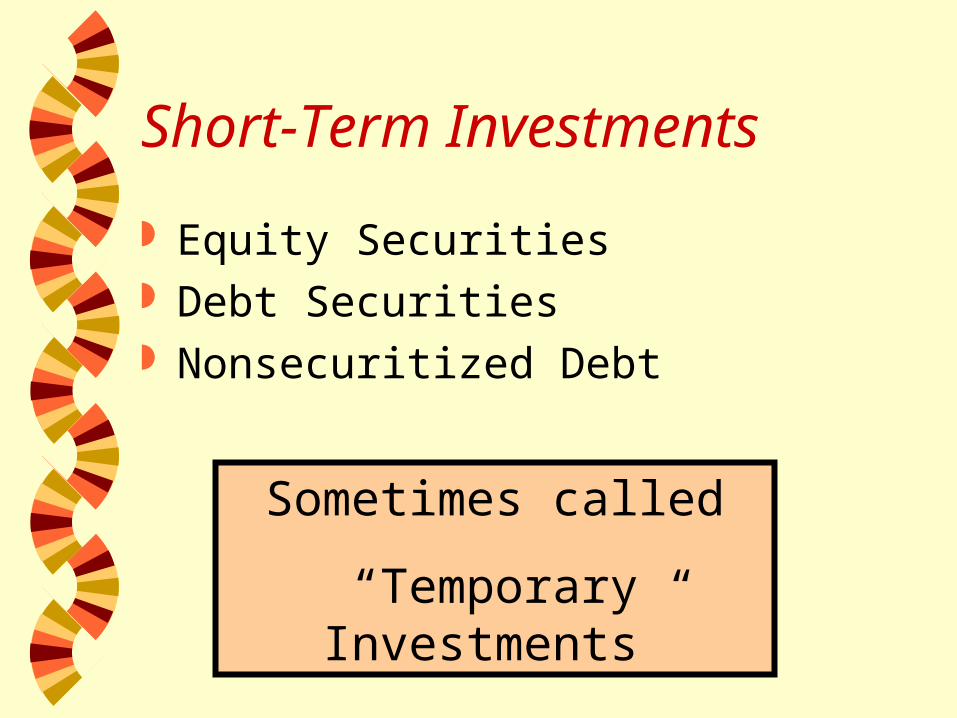

Short-Term Investments

Equity Securities Debt Securities Nonsecuritized Debt

Sometimes called

“Temporary Investments”

SFAS 115

Applies to• Equity securities with readily determinable fair

values• Debt securities

Measurement of Short-term Investments in Equity Securities Fair value

• Equity securities with readily determinable fair values

Cost• all other equity securities

Measurement of Short-Term Investments in Debt Cost

• If management plans to hold to maturity• If nonsecuritized (e.g., notes receivable from

individuals)

Fair value• All other debt securities

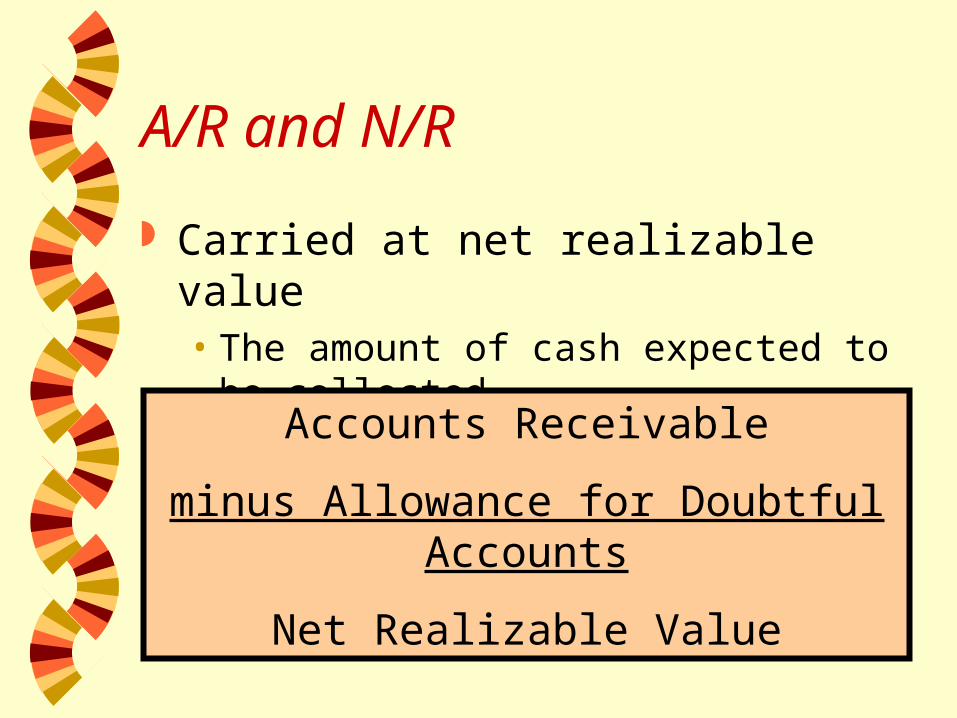

A/R and N/R

Carried at net realizable value• The amount of cash expected to be collected

Accounts Receivable

minus Allowance for Doubtful Accounts

Net Realizable Value

Inventories

Measured at Lower-of-cost-or market Examples:

• Merchandise Inventory• Supplies• Work-in-Process• Raw Materials• Finished Goods

Prepaid Expenses

Measured at historical cost not consumed Examples:

• Prepaid Insurance• Prepaid Taxes• Prepaid Rent

Liability Classifications

Current Liabilities Long-term Liabilities

Current Liabilities

Obligations expected to be eliminated through the use of existing current assets or by the creation of other current liabilities

Typically, those due within one year

Typical current liabilities

Notes Payable Accounts Payable Accrued Expenses Deferred Revenues Current Maturities of Long-term Debt

Notes Payable

Trade and nontrade Report at face value less any discount

Accounts Payable

From purchase of• merchandise• goods• services

Typically reported at invoice amount• ie, not discounted

Accrued Expenses

Typically not discounted Examples:

• Salaries Payable• Interest Payable• Taxes Payable

Deferred Revenues

Obligated to perform services or deliver goods for monies already received

Examples:• Rent received in advance• Magazine subscriptions received• Deposits received

Chapter 3--Learning Objectives

4. Understand and identify the noncurrent elements of a firm’s balance sheet

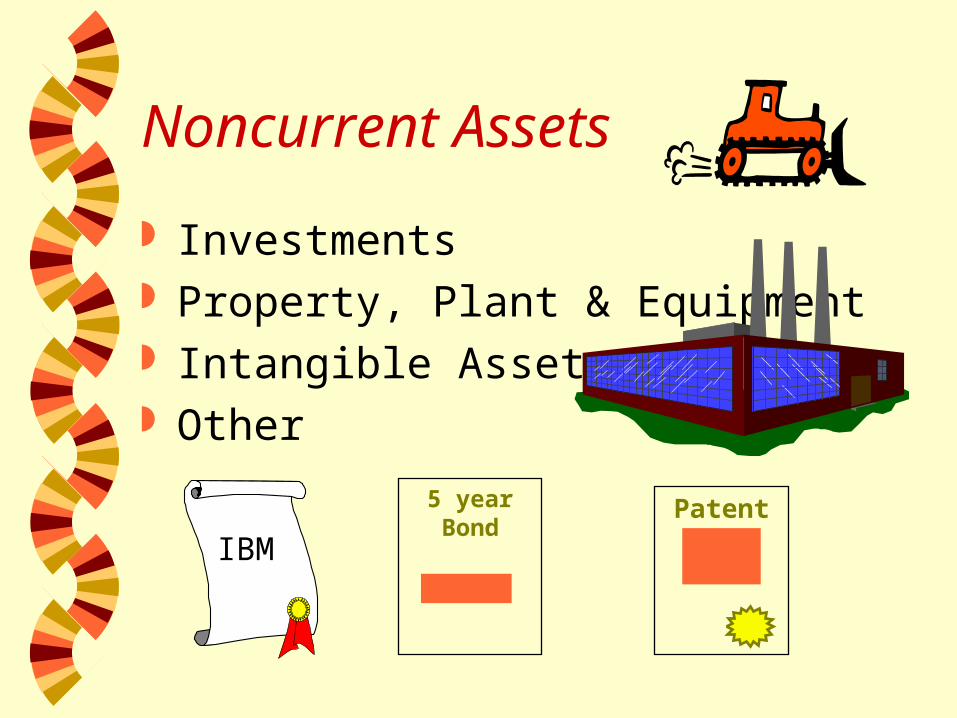

Noncurrent Assets

Investments Property, Plant & Equipment Intangible Assets Other

5 yearBond

IBMPatent

Investments

Special purpose funds (Sinking funds) Long term investments in stock Long term investments in bonds Long term interest-bearing receivables Land held for Speculation

Property, Plant & Equipment

Long-lived tangible assets used in operations Reported at cost less accumulated depreciation Examples:

• Land• Buildings• Equipment• vehicles

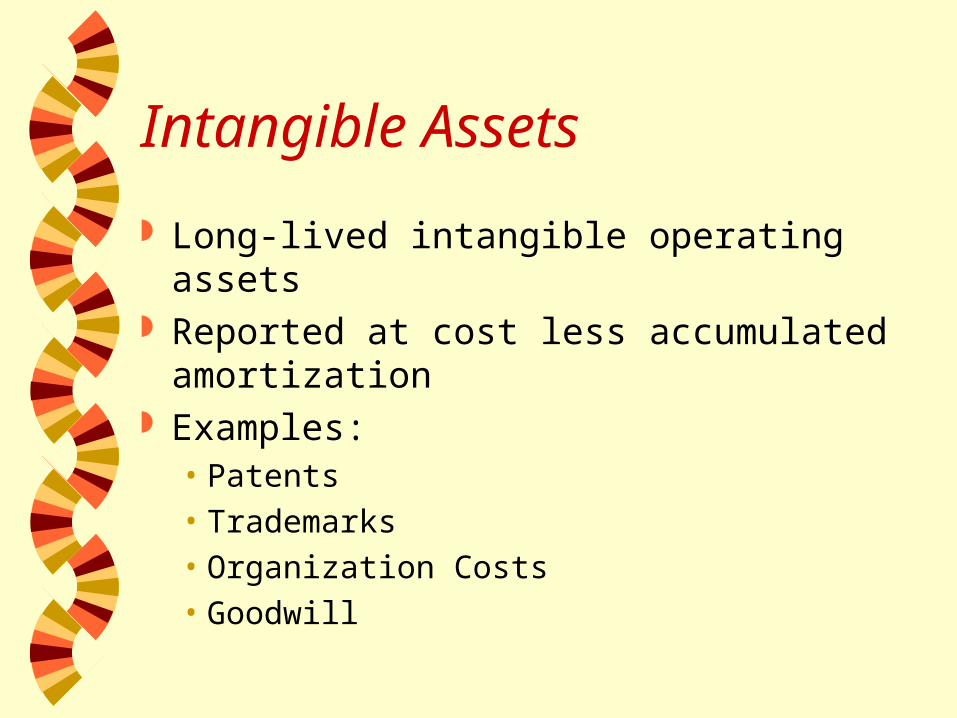

Intangible Assets

Long-lived intangible operating assets Reported at cost less accumulated

amortization Examples:

• Patents• Trademarks• Organization Costs• Goodwill

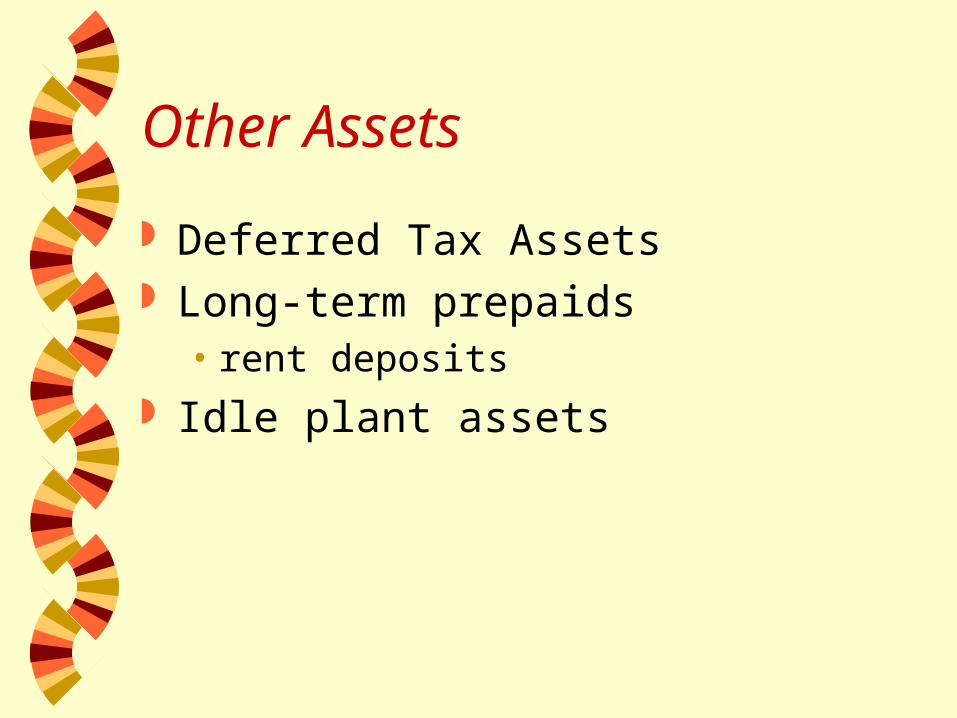

Other Assets

Deferred Tax Assets Long-term prepaids

• rent deposits

Idle plant assets

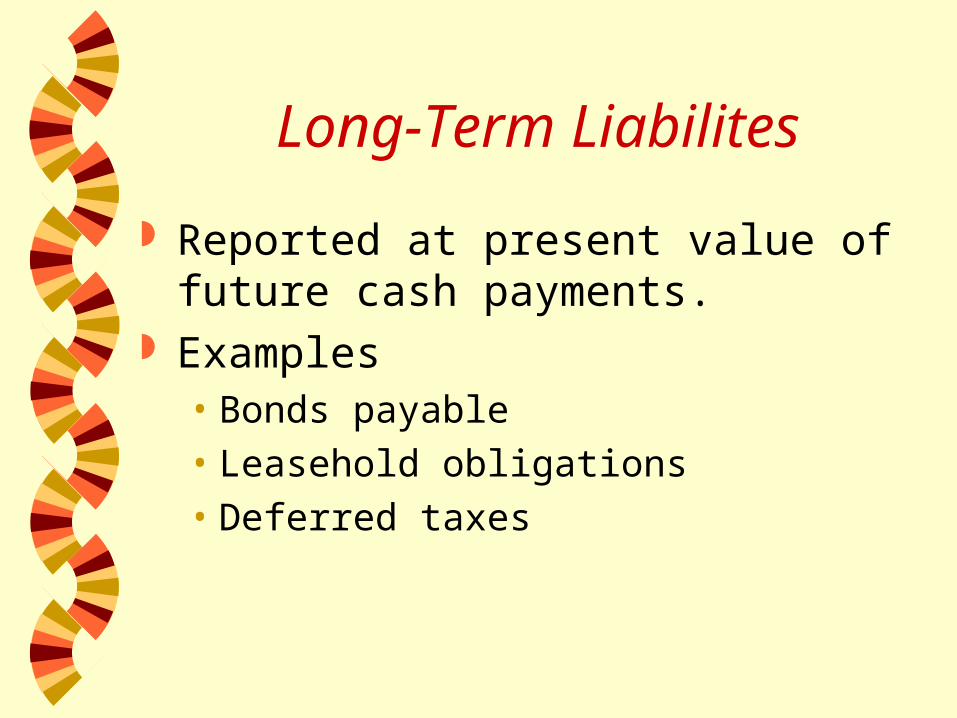

Long-Term Liabilites

Reported at present value of future cash payments.

Examples• Bonds payable• Leasehold obligations• Deferred taxes

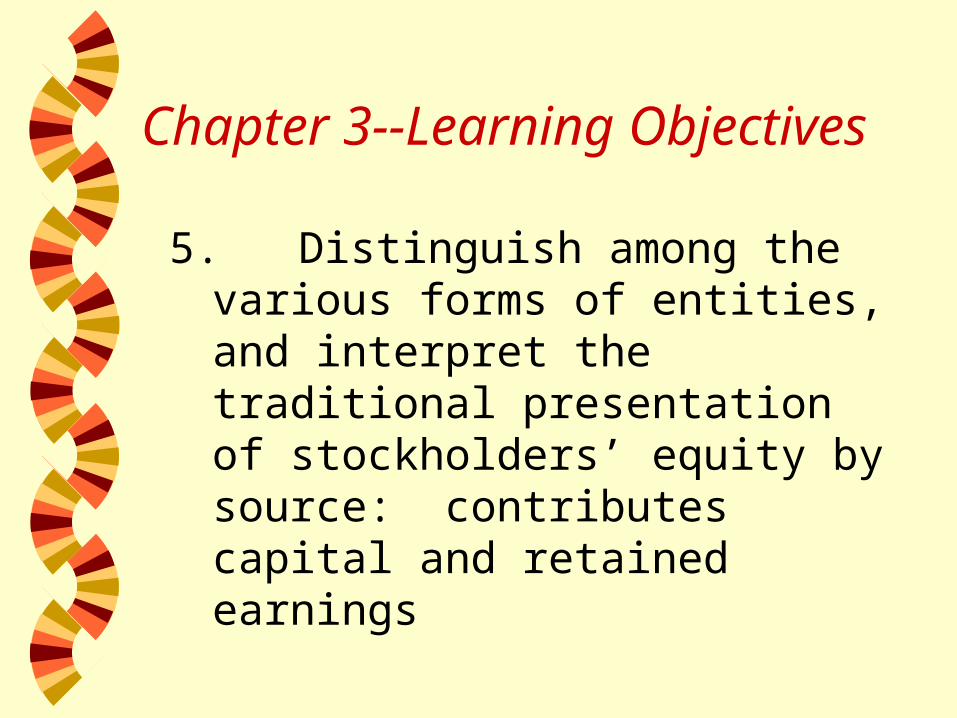

Chapter 3--Learning Objectives

5. Distinguish among the various forms of entities, and interpret the traditional presentation of stockholders’ equity by source: contributes capital and retained earnings

Types of business entity

Proprietorships--Enterprises with a single owner

Partnerships--Unincorporated businesses with two or more owners

Corporations--Separate legal entities established by applicable laws of incorporation

Types of corporations Private companies Stock companies Publicly held Listed companies Unlisted (over-the-counter) Closely held (nonpublic) Nonstock companies Public companies Mutual companies

Advantages of the corporate form of business Potential to accumulate large amounts of

capital Limited liability of owners Relative ease of transferability of

ownership

Disadvantages of the corporate form of business Double taxation Limited control by owners Additional regulatory and reporting

requirements

Owner’s Equity

Paid-in Capital Retained Earnings Accumulated Other Comprehensive Income Treasury Stock

Paid-in Capital

Common Stock Preferred Stock Additional Paid-in Capital

Common Stock & Preferred Stock Par value or stated value Additional paid-in capital

• Investments by owners in excess of par or stated value

Retained Earnings

Accumulated earnings that have not been distributed to owners.

Accumulated Other Comprehensive Earnings Adjustments to assets and liabilities that are

not reported in earnings Examples:

• Unrealized gains/losses on investments in securities under SFAS 115

• Translation Adjustment• Unrealized losses from pension plans

Treasury Stock (at Cost)

The cost of acquiring stock back from stockholders

This is stock that has been reacquired and not retired

A contra equity

Chapter 3--Learning Objectives

6. Identify uses and limitations of traditional balance sheets for financial analysis

Analysis of Liquidity

Liquidity •Ability to pay debts and continue operations

Liquidity measures•Working capital

•Current ratio

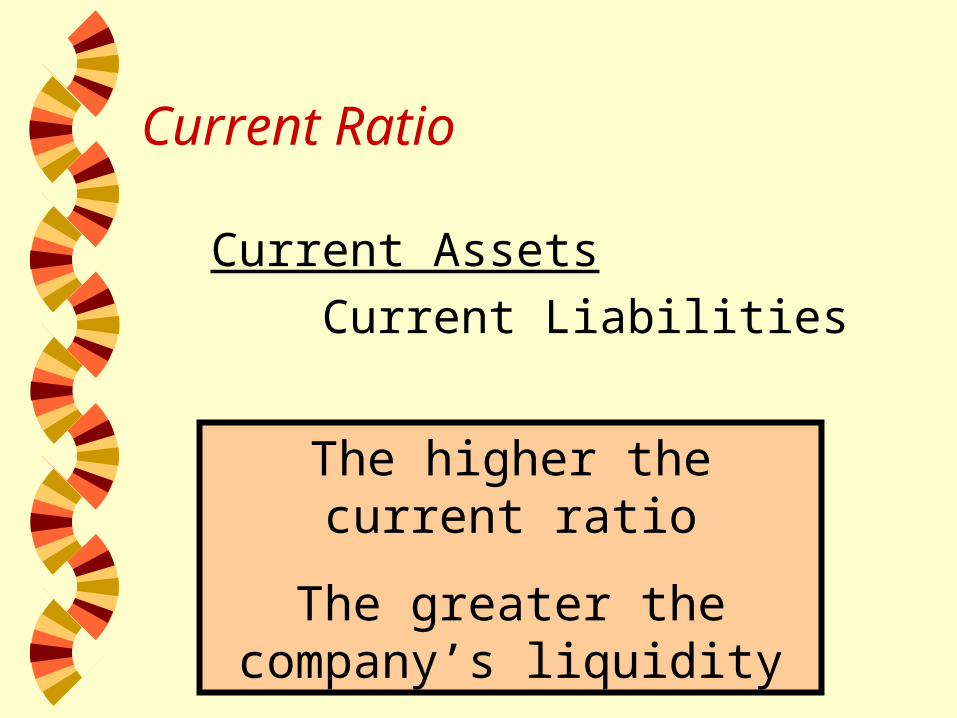

Current Ratio

Current Assets

Current Liabilities

The higher the current ratio

The greater the company’s liquidity

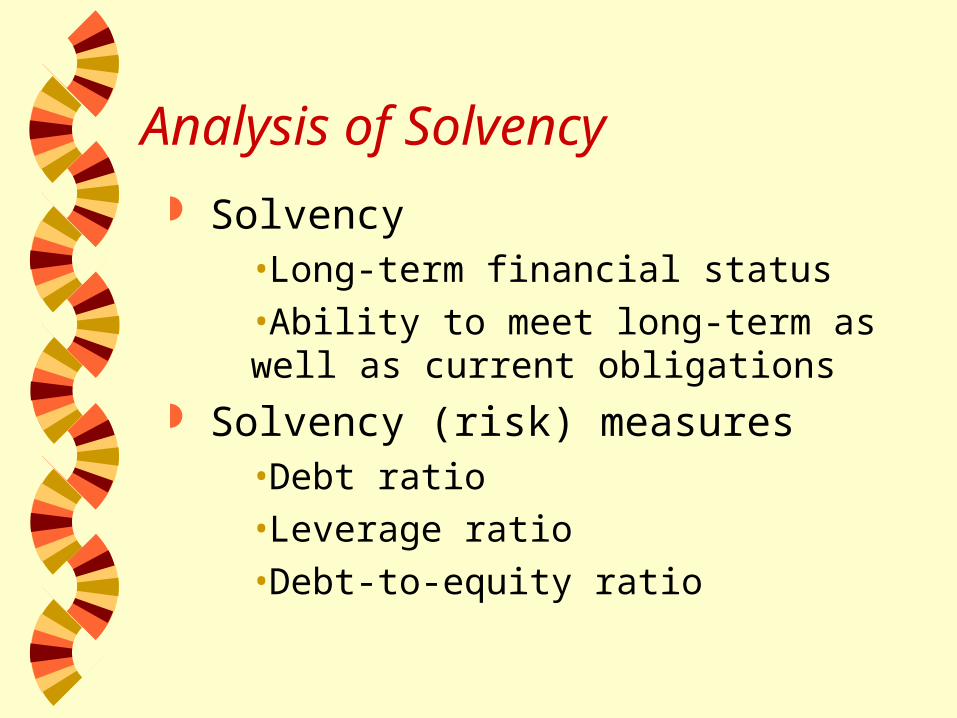

Analysis of Solvency

Solvency•Long-term financial status

•Ability to meet long-term as well as current obligations

Solvency (risk) measures•Debt ratio

•Leverage ratio

•Debt-to-equity ratio

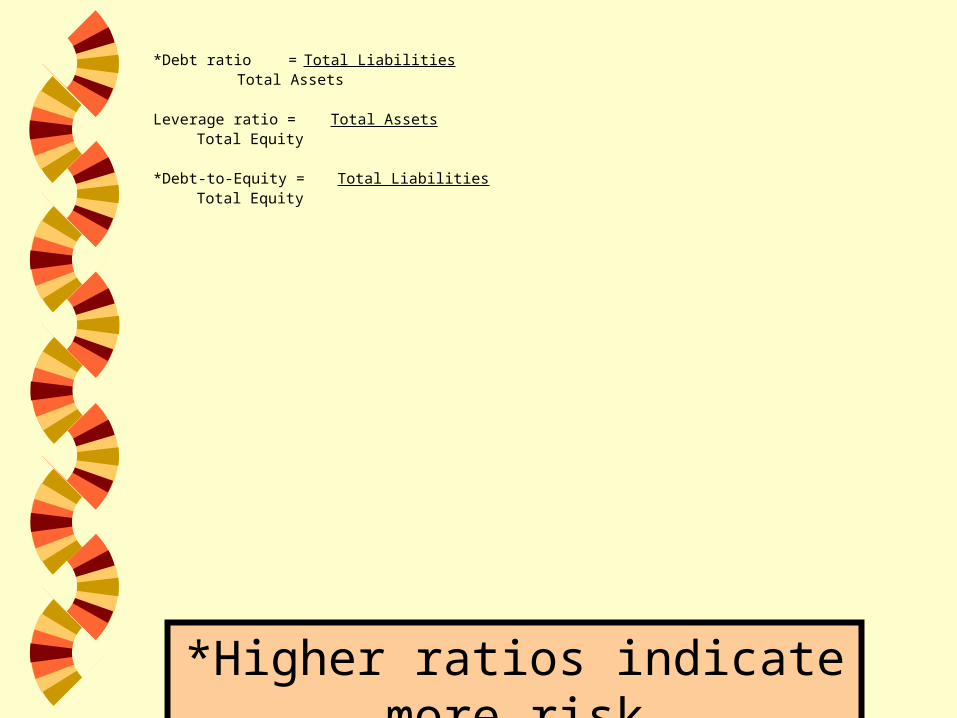

*Debt ratio = Total Liabilities Total Assets

Leverage ratio = Total Assets Total Equity

*Debt-to-Equity = Total Liabilities Total Equity

*Higher ratios indicate more risk

Supplemental Disclosures

Segments Subsequent Events Contingencies

Subsequent events Occur between the end of the reporting period

and the issue date for the financial statements Are not part of the normal operating activities

of the enterprise Two types

1. Originating prior to subsequent period and resolved during it

2. Originating during subsequent period

Subsequent events

Events originating prior to the statement date and resolved during the subsequent period

Requirement: adjust financial statements

Subsequent events

Events originating during the subsequent period

Requirement: disclosure in the notes to the statements

Contingencies

Gain Contingencies• A possible future increase in Cash flows• Generally not recognized in financial

statements

Loss Contingencies• A possible future reduction in Cash flows

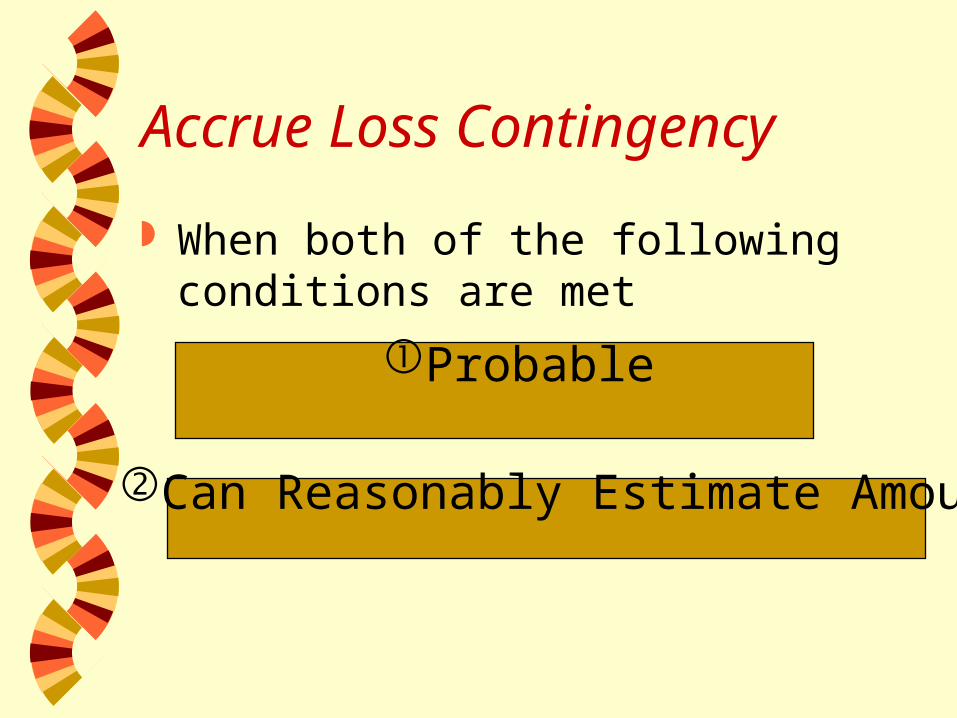

Accrue Loss Contingency

When both of the following conditions are met

Probable

Can Reasonably Estimate Amount

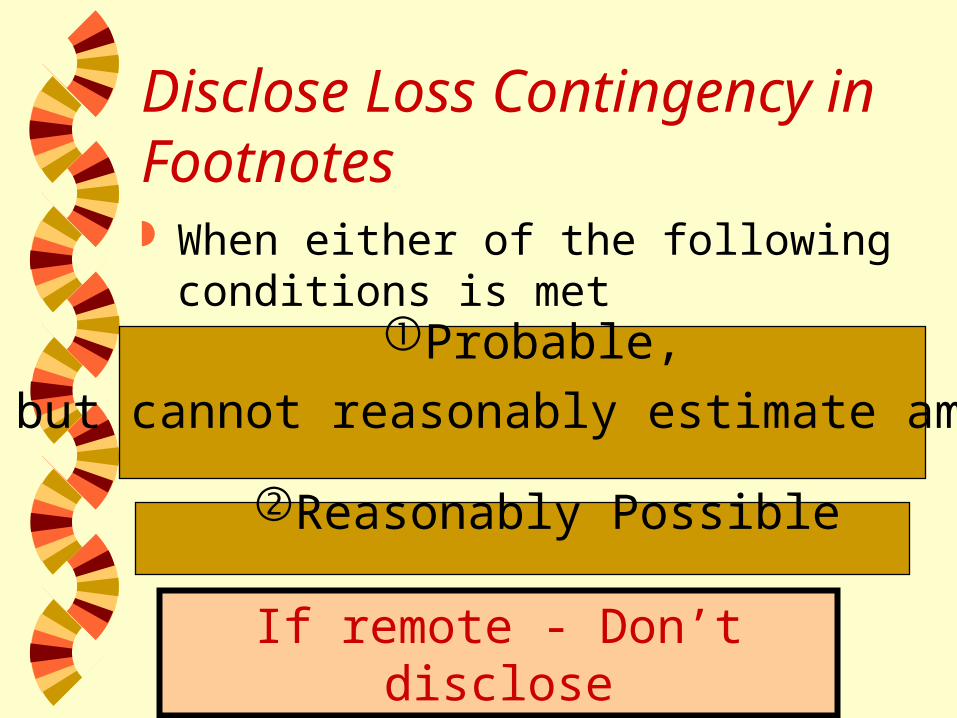

Disclose Loss Contingency in Footnotes When either of the following conditions is

met

If remote - Don’t disclose

Probable,

but cannot reasonably estimate amount

Reasonably Possible

Exercise Determine accounting treatment for

each of the following contingencies

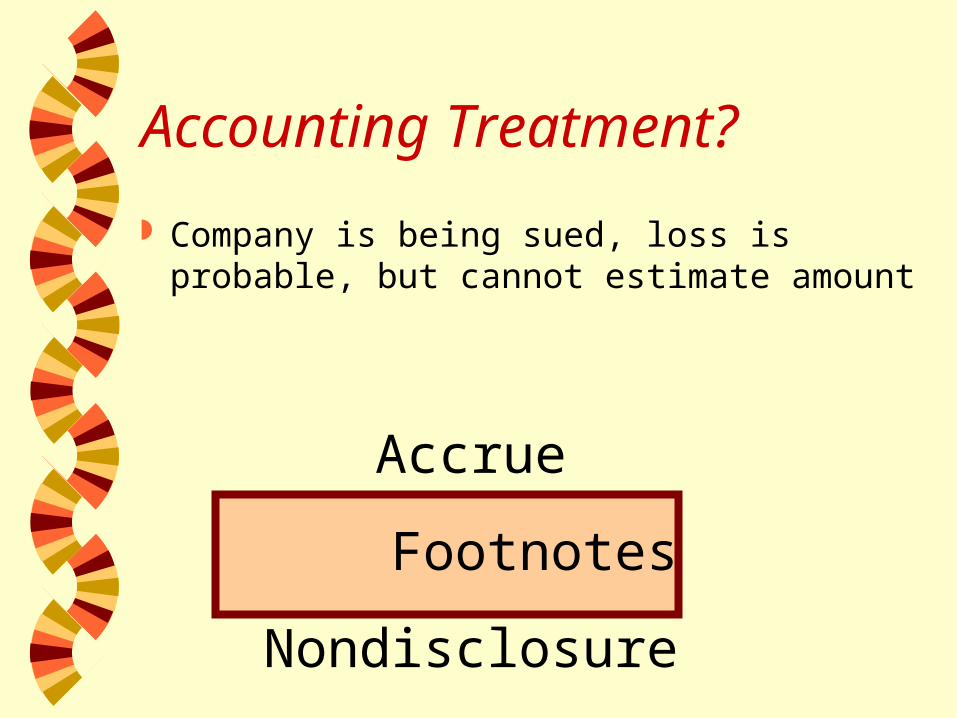

Accounting Treatment?

Company is being sued, loss is probable, but cannot estimate amount

Accrue

Footnotes

Nondisclosure

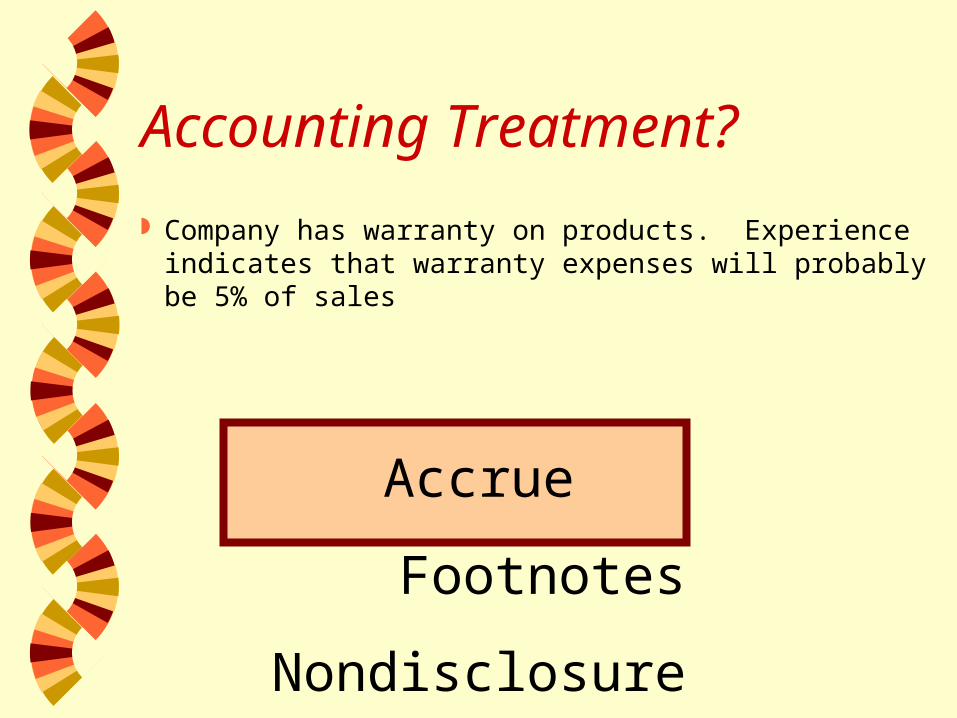

Accounting Treatment?

Company has warranty on products. Experience indicates that warranty expenses will probably be 5% of sales

Accrue

Footnotes

Nondisclosure

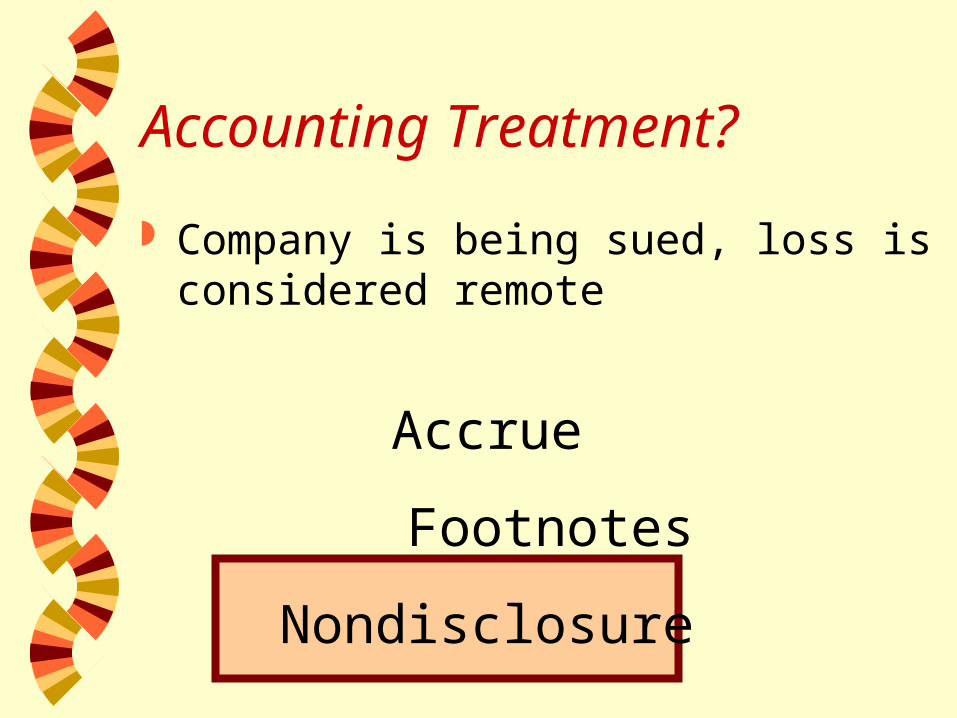

Accounting Treatment?

Company is being sued, loss is considered remote

Accrue

Footnotes

Nondisclosure

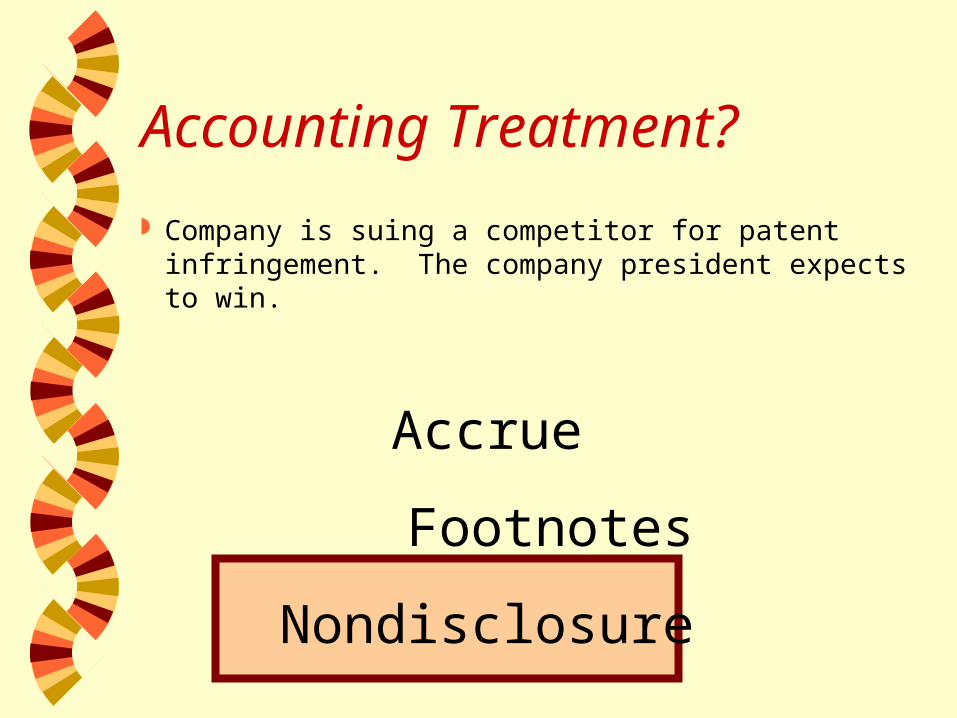

Accounting Treatment?

Company is suing a competitor for patent infringement. The company president expects to win.

Accrue

Footnotes

Nondisclosure

Other disclosures

Significant accounting policies Specific disclosures required by

pronouncements• e.g., pension plan details

Balance sheet limitationsWhat does not appear ?

Human capital

Balance sheet limitationsWhat does not appear ?

Internally generated goodwill

Balance sheet limitationsWhat does not appear ?

Benefits from

research and development activities