Embed Size (px)

DESCRIPTION

NIL

Citation preview

CHAPTER 3

JOHN DY, Petitioner,

- versus -

PEOPLE OF THE PHILIPPINES and The HONORABLE COURT OF APPEALS, Respondents.

G.R. No. 158312 November 14, 2008

DECISION

QUISUMBING, Acting C.J.:

This appeal prays for the reversal of the Decision[1] dated January 23, 2003 and the Resolution[2] dated May 14, 2003 of the Court of Appeals in CA-G.R. CR No. 23802. The appellate court affirmed with modification the Decision[3] dated November 17, 1999 of the Regional Trial Court (RTC), Branch 82 of Quezon City, which had convicted petitioner John Dy of two counts of estafa in Criminal Cases Nos. Q-93-46711 and Q-93-46713, and two counts of violation of Batas Pambansa Bilang 22[4] (B.P. Blg. 22) in Criminal Cases Nos. Q-93-46712 and Q-93-46714.

The facts are undisputed:

Since 1990, John Dy has been the distributor of W.L. Food Products (W.L. Foods) in Naga City, Bicol, under the business name Dyna Marketing. Dy would pay W.L. Foods in either cash or check upon pick up of stocks of snack foods at the latter’s branch or main office in Quezon City. At times, he would entrust the payment to one of his drivers.

On June 24, 1992, Dy’s driver went to the branch office of W.L. Foods to pick up stocks of snack foods. He introduced himself to the checker, Mary Jane D. Maraca, who upon confirming Dy’s credit with the main office, gave him merchandise worth P106,579.60. In return, the driver handed her a blank Far East Bank and Trust Company (FEBTC) Check with Check No. 553602 postdated July 22, 1992. The check was signed by Dy though it did not indicate a specific amount.

Yet again, on July 1, 1992, the same driver obtained snack foods from Maraca in the amount of P226,794.36 in exchange for a blank FEBTC Check with Check No. 553615 postdated July 31, 1992.

In both instances, the driver was issued an unsigned delivery receipt. The amounts for the purchases were filled in later by Evelyn Ong, accountant of W.L. Foods, based on the value of the goods delivered.

When presented for payment, FEBTC dishonored the checks for insufficiency of funds. Raul D. Gonzales, manager of FEBTC-Naga Branch, notified Atty. Rita Linda Jimeno, counsel of W.L. Foods, of the dishonor. Apparently, Dy only had an available balance of P2,000 as of July 22, 1992 and July 31, 1992.

Later, Gonzales sent Atty. Jimeno another letter[5] advising her that FEBTC Check No. 553602 for P106,579.60 was returned to the drawee bank for the reasons stop payment order and drawn against uncollected deposit (DAUD), and not because it was drawn against insufficient funds as stated in

the first letter. Dy’s savings deposit account ledger reflected a balance of P160,659.39 as of July 22, 1992. This, however, included a regional clearing check for P55,000 which he deposited on July 20, 1992, and which took five (5) banking days to clear. Hence, the inward check was drawn against the yet uncollected deposit.

When William Lim, owner of W.L. Foods, phoned Dy about the matter, the latter explained that he could not pay since he had no funds yet. This prompted the former to send petitioner a demand letter, which the latter ignored.

On July 16, 1993, Lim charged Dy with two counts of estafa under Article 315, paragraph 2(d)[6] of the Revised Penal Code in two Informations, which except for the dates and amounts involved, similarly read as follows:

That on or about the 24th day of June, 1992, in Quezon City, Philippines, the said accused, did then and there [willfully] and feloniously defraud W.L. PRODUCTS, a corporation duly organized and existing under the laws of the Republic of the Philippines with business address at No. 531 Gen. Luis St., Novaliches, this City, in the following manner, to wit: the said accused, by means of false manifestations and fraudulent representation which he made to complainant to the effect that Far East Bank and Trust Co. check No. 553602 dated July 22, 1992 in the amount of P106,579.60, payable to W.L. Products is a good check and will be honored by the bank on its maturity date, and by means of other deceit of similar import, induced and succeeded in inducing the said complainant to receive and accept the aforesaid check in payment of snack foods, the said accused knowing fully well that all his manifestations and representations were false and untrue and were made solely for the purpose of obtaining, as in fact he did obtain the aforesaid snack foods valued at P106,579.60 from said complainant as upon presentation of said check to the bank for payment, the same was dishonored and payment thereof refused for the reason stop payment and the said accused, once in possession of the aforesaid snack foods, with intent to defraud, [willfully], unlawfully and feloniously misapplied, misappropriated and converted the same or the value thereof to his own personal use and benefit, to the damage and prejudice of said W.L. Products, herein represented by RODOLFO BORJAL, in the aforementioned amount of P106,579.60, Philippine Currency.

Contrary to law.[7]

On even date, Lim also charged Dy with two counts of violation of B.P. Blg. 22 in two Informations which likewise save for the dates and amounts involved similarly read as follows:

That on or about the 24th day of June, 1992, the said accused, did then and there [willfully], unlawfully and feloniously make or draw and issue to W.L. FOOD PRODUCTS to apply on account or for value a Far East Bank and Trust Co. Check no. 553602 dated July 22, 1992 payable to W.L. FOOD PRODUCTS in the amount of P106,579.60 Philippine Currency, said accused knowing fully well that at the time of issue he/she/they did not have sufficient funds in or credit with the drawee bank for payment of such check in full upon its presentment, which check when presented 90 days from the date thereof was subsequently dishonored by the drawee bank for the reason “Payment stopped” but the same would have been dishonored for insufficient funds had not the accused without any valid reason, ordered the bank to

stop payment, the said accused despite receipt of notice of such dishonor, failed to pay said W.L. Food Products the amount of said check or to make arrangement for payment in full of the same within five (5) banking days after receiving said notice.

CONTRARY TO LAW.[8]

On November 23, 1994, Dy was arrested in Naga City. On arraignment, he pleaded not guilty to all charges. Thereafter, the cases against him were tried jointly.

On November 17, 1999 the RTC convicted Dy on two counts each of estafa and violation of B.P. Blg. 22. The trial court disposed of the case as follows:

WHEREFORE, accused JOHN JERRY DY ALDEN (JOHN DY) is hereby found GUILTY beyond reasonable doubt of swindling (ESTAFA) as charged in the Informations in Criminal Case No. 93-46711 and in Criminal Case No. Q-93-46713, respectively. Accordingly, after applying the provisions of the Indeterminate Sentence Law and P.D. No. 818, said accused is hereby sentenced to suffer the indeterminate penalty of ten (10) years and one (1) day to twelve (12) years of prision mayor, as minimum, to twenty (20) years of reclusion temporal, as maximum, in Criminal Case No. Q-93-46711 and of ten (10) years and one (1) day to twelve (12) years of prision mayor, as minimum, to thirty (30) years of reclusion perpetua, as maximum, in Criminal Case No. Q-93-46713.

Likewise, said accused is hereby found GUILTY beyond reasonable doubt of Violation of B.P. 22 as charged in the Informations in Criminal Case No. Q-93-46712 and in Criminal Case No. Q-93-46714 and is accordingly sentenced to imprisonment of one (1) year for each of the said offense and to pay a fine in the total amount of P333,373.96, with subsidiary imprisonment in case of insolvency.

FINALLY, judgment is hereby rendered in favor of private complainant, W. L. Food Products, herein represented by Rodolfo Borjal, and against herein accused JOHN JERRY DY ALDEN (JOHN DY), ordering the latter to pay to the former the total sum of P333,373.96 plus interest thereon at the rate of 12% per annum from September 28, 1992 until fully paid; and, (2) the costs of this suit.

SO ORDERED.[9]

Dy brought the case to the Court of Appeals. In the assailed Decision of January 23, 2003, the appellate court affirmed the RTC. It, however, modified the sentence and deleted the payment of interests in this wise:

WHEREFORE, in view of the foregoing, the decision appealed from is hereby AFFIRMED with MODIFICATION. In Criminal Case No. Q-93-46711 (for estafa), the accused-appellant JOHN JERRY DY ALDEN (JOHN DY) is hereby sentenced to suffer an indeterminate penalty of imprisonment ranging from six (6) years and one (1) day of prision mayor as minimum to twenty (20) years ofreclusion temporal as maximum plus eight (8) years in excess of [P]22,000.00. In Criminal Case No. Q-93-46712 (for violation of BP 22), accused-appellant is sentenced to suffer an imprisonment of one (1) year and to indemnify W.L. Food Products, represented by Rodolfo Borjal, the amount of ONE HUNDRED SIX THOUSAND FIVE HUNDRED SEVENTY NINE PESOS and 60/100 ([P]106,579.60). In Criminal Case No. Q-93-46713 (for

estafa), accused-appellant is hereby sentenced to suffer an indeterminate penalty of imprisonment ranging from eight (8) years and one (1) day ofprision mayor as minimum to thirty (30) years as maximum. Finally, in Criminal Case No. Q-93-46714 (for violation of BP 22), accused-appellant is sentenced to suffer an imprisonment of one (1) year and to indemnify W.L. Food Products, represented by Rodolfo Borjal, the amount of TWO HUNDRED TWENTY SIX THOUSAND SEVEN HUNDRED NINETY FOUR PESOS AND 36/100 ([P]226,794.36).

SO ORDERED.[10]

Dy moved for reconsideration, but his motion was denied in the Resolution dated May 14, 2003.

Hence, this petition which raises the following issues:

I.

WHETHER OR NOT THE HONORABLE COURT OF APPEALS GRAVELY ERRED IN FINDING THAT THE PROSECUTION HAS PROVEN THE GUILT OF ACCUSED BEYOND REASONABLE DOUBT OF ESTAFA ON TWO (2) COUNTS?

II.

WHETHER OR NOT THE HONORABLE COURT OF APPEALS GRAVELY ERRED IN FINDING THAT THE PROSECUTION HAS PROVEN THE GUILT OF ACCUSED BEYOND REASONABLE DOUBT OF VIOLATION OF BP 22 ON TWO (2) COUNTS?

III.

WHETHER OR NOT THE HONORABLE COURT OF APPEALS GRAVELY ERRED IN AWARDING DAMAGES TO PRIVATE COMPLAINANT, W.L. FOOD PRODUCTS, THE TOTAL SUM OF [P]333,373.96? [11]

Essentially, the issue is whether John Dy is liable for estafa and for violation of B.P. Blg. 22.

First, is petitioner guilty of estafa?

Mainly, petitioner contends that the checks were ineffectively issued. He stresses that not only were the checks blank, but also that W.L. Foods’ accountant had no authority to fill the amounts. Dy also claims failure of consideration to negate any obligation to W.L. Foods. Ultimately, petitioner denies having deceived Lim inasmuch as only the two checks bounced since he began dealing with him. He maintains that it was his long established business relationship with Lim that enabled him to obtain the goods, and not the checks issued in payment for them. Petitioner renounces personal liability on the checks since he was absent when the goods were delivered.

The Office of the Solicitor General (OSG), for the State, avers that the delivery of the checks by Dy’s driver to Maraca, constituted valid issuance. The OSG sustains Ong’s prima facie authority to fill the checks based on the value of goods taken. It observes that nothing in the records showed that W.L. Foods’ accountant filled up the checks in violation of Dy’s instructions or their previous

agreement. Finally, the OSG challenges the present petition as an inappropriate remedy to review the factual findings of the trial court.

We find that the petition is partly meritorious.

Before an accused can be held liable for estafa under Article 315, paragraph 2(d) of the Revised Penal Code, as amended by Republic Act No. 4885,[12] the following elements must concur: (1) postdating or issuance of a check in payment of an obligation contracted at the time the check was issued; (2) insufficiency of funds to cover the check; and (3) damage to the payee thereof. [13] These elements are present in the instant case.

Section 191 of the Negotiable Instruments Law[14] defines “issue” as the first delivery of an instrument, complete in form, to a person who takes it as a holder. Significantly, delivery is the final act essential to the negotiability of an instrument. Delivery denotes physical transfer of the instrument by the maker or drawer coupled with an intention to convey title to the payee and recognize him as a holder. [15] It means more than handing over to another; it imports such transfer of the instrument to another as to enable the latter to hold it for himself.[16]

In this case, even if the checks were given to W.L. Foods in blank, this alone did not make its issuance invalid. When the checks were delivered to Lim, through his employee, he became a holder with prima facie authority to fill the blanks. This was, in fact, accomplished by Lim’s accountant.

The pertinent provisions of Section 14 of the Negotiable Instruments Law are instructive:

SEC. 14. Blanks; when may be filled.–Where the instrument is wanting in any material particular, the person in possession thereof has a prima facie authority to complete it by filling up the blanks therein. And a signature on a blank paper delivered by the person making the signature in order that the paper may be converted into a negotiable instrument operates as a prima facie authority to fill it up as such for any amount. …. (Emphasis supplied.)

Hence, the law merely requires that the instrument be in the possession of a person other than the drawer or maker. From such possession, together with the fact that the instrument is wanting in a material particular, the law presumes agency to fill up the blanks.[17] Because of this, the burden of proving want of authority or that the authority granted was exceeded, is placed on the person questioning such authority.[18] Petitioner failed to fulfill this requirement.

Next, petitioner claims failure of consideration. Nevertheless, in a letter[19] dated November 10, 1992, he expressed willingness to pay W.L. Foods, or to replace the dishonored checks. This was a clear acknowledgment of receipt of the goods, which gave rise to his duty to maintain or deposit sufficient funds to cover the amount of the checks.

More significantly, we are not swayed by petitioner’s arguments that the single incident of dishonor and his absence when the checks were delivered belie fraud. Indeed damage and deceit are essential

elements of the offense and must be established with satisfactory proof to warrant conviction. [20] Deceit as an element of estafa is a specie of fraud. It is actual fraud which consists in any misrepresentation or contrivance where a person deludes another, to his hurt. There is deceit when one is misled -- by guile, trickery or by other means -- to believe as true what is really false. [21]

Prima facie evidence of deceit was established against petitioner with regard to FEBTC Check No. 553615 which was dishonored for insufficiency of funds. The letter[22]of petitioner’s counsel dated November 10, 1992 shows beyond reasonable doubt that petitioner received notice of the dishonor of the said check for insufficiency of funds. Petitioner, however, failed to deposit the amounts necessary to cover his check within three banking days from receipt of the notice of dishonor. Hence, as provided for by law,[23] the presence of deceit was sufficiently proven.

Petitioner failed to overcome the said proof of deceit. The trial court found no pre-existing obligation between the parties. The existence of prior transactions between Lim and Dy alone did not rule out deceit because each transaction was separate, and had a different consideration from the others. Even as petitioner was absent when the goods were delivered, by the principle of agency, delivery of the checks by his driver was deemed as his act as the employer. The evidence shows that as a matter of course, Dy, or his employee, would pay W.L. Foods in either cash or check upon pick up of the stocks of snack foods at the latter’s branch or main office. Despite their two-year standing business relations prior to the issuance of the subject check, W.L Foods employees would not have parted with the stocks were it not for the simultaneous delivery of the check issued by petitioner. [24] Aside from the existing business relations between petitioner and W.L. Foods, the primary inducement for the latter to part with its stocks of snack foods was the issuance of the check in payment of the value of the said stocks.

In a number of cases,[25] the Court has considered good faith as a defense to a charge of estafa by postdating a check. This good faith may be manifested by making arrangements for payment with the creditor and exerting best efforts to make good the value of the checks. In the instant case petitioner presented no proof of good faith. Noticeably absent from the records is sufficient proof of sincere and best efforts on the part of petitioner for the payment of the value of the check that would constitute good faith and negate deceit.

With the foregoing circumstances established, we find petitioner guilty of estafa with regard to FEBTC Check No. 553615 for P226,794.36.

The same, however, does not hold true with respect to FEBTC Check No. 553602 for P106,579.60. This check was dishonored for the reason that it was drawn against uncollected deposit. Petitioner had P160,659.39 in his savings deposit account ledger as of July 22, 1992. We disagree with the conclusion of the RTC that since the balance included a regional clearing check worth P55,000 deposited on July 20, 1992, which cleared only five (5) days later, then petitioner had inadequate funds in this instance. Since petitioner technically and retroactively had sufficient funds at the time Check No. 553602 was presented for payment then the second element (insufficiency of funds to cover the check) of the crime is absent. Also there is no prima facie evidence of deceit in this instance because the check was not dishonored for lack or insufficiency of funds. Uncollected deposits are not the same as

insufficient funds. The prima facie presumption of deceit arises only when a check has been dishonored for lack or insufficiency of funds. Notably, the law speaks of insufficiency of funds but not of uncollected deposits. Jurisprudence teaches that criminal laws are strictly construed against the Government and liberally in favor of the accused.[26] Hence, in the instant case, the law cannot be interpreted or applied in such a way as to expand its provision to encompass the situation of uncollected deposits because it would make the law more onerous on the part of the accused.

Clearly, the estafa punished under Article 315, paragraph 2(d) of the Revised Penal Code is committed when a check is dishonored for being drawn against insufficient funds or closed account, and not against uncollected deposit.[27] Corollarily, the issuer of the check is not liable for estafa if the remaining balance and the uncollected deposit, which was duly collected, could satisfy the amount of the check when presented for payment.

Second, did petitioner violate B.P. Blg. 22?

Petitioner argues that the blank checks were not valid orders for the bank to pay the holder of such checks. He reiterates lack of knowledge of the insufficiency of funds and reasons that the checks could not have been issued to apply on account or for value as he did not obtain delivery of the goods.

The OSG maintains that the guilt of petitioner has been proven beyond reasonable doubt. It cites pieces of evidence that point to Dy’s culpability: Maraca’s acknowledgment that the checks were issued to W.L. Foods as consideration for the snacks; Lim’s testimony proving that Dy received a copy of the demand letter; the bank manager’s confirmation that petitioner had insufficient balance to cover the checks; and Dy’s failure to settle his obligation within five (5) days from dishonor of the checks.

Once again, we find the petition to be meritorious in part.

The elements of the offense penalized under B.P. Blg. 22 are as follows: (1) the making, drawing and issuance of any check to apply to account or for value; (2) the knowledge of the maker, drawer or issuer that at the time of issue he does not have sufficient funds in or credit with the drawee bank for the payment of such check in full upon its presentment; and (3) subsequent dishonor of the check by the drawee bank for insufficiency of funds or credit or dishonor for the same reason had not the drawer, without any valid cause, ordered the bank to stop payment.[28] The case at bar satisfies all these elements.

During the joint pre-trial conference of this case, Dy admitted that he issued the checks, and that the signatures appearing on them were his.[29] The facts reveal that the checks were issued in blank because of the uncertainty of the volume of products to be retrieved, the discount that can be availed of, and the deduction for bad orders. Nevertheless, we must stress that what the law punishes is simply the issuance of a bouncing check and not the purpose for which it was issued nor the terms and conditions relating thereto.[30] If inquiry into the reason for which the checks are issued, or the terms and conditions of their issuance is required, the public’s faith in the stability and commercial value of checks as currency substitutes will certainly erode.[31]

Moreover, the gravamen of the offense under B.P. Blg. 22 is the act of making or issuing a worthless check or a check that is dishonored upon presentment for payment. The act effectively declares the offense to be one of malum prohibitum. The only valid query, then, is whether the law has been breached, i.e., by the mere act of issuing a bad check, without so much regard as to the criminal intent of the issuer.[32] Indeed, non-fulfillment of the obligation is immaterial. Thus, petitioner’s defense of failure of consideration must likewise fall. This is especially so since as stated above, Dy has acknowledged receipt of the goods.

On the second element, petitioner disputes notice of insufficiency of funds on the basis of the check being issued in blank. He relies on Dingle v. Intermediate Appellate Court[33] and Lao v. Court of Appeals[34] as his authorities. In both actions, however, the accused were co-signatories, who were neither apprised of the particular transactions on which the blank checks were issued, nor given notice of their dishonor. In the latter case, Lao signed the checks without knowledge of the insufficiency of funds, knowledge she was not expected or obliged to possess under the organizational structure of the corporation.[35] Lao was only a minor employee who had nothing to do with the issuance, funding and delivery of checks.[36] In contrast, petitioner was the proprietor of Dyna Marketing and the sole signatory of the checks who received notice of their dishonor.

Significantly, under Section 2[37] of B.P. Blg. 22, petitioner was prima facie presumed to know of the inadequacy of his funds with the bank when he did not pay the value of the goods or make arrangements for their payment in full within five (5) banking days upon notice. His letter dated November 10, 1992 to Lim fortified such presumption.

Undoubtedly, Dy violated B.P. Blg. 22 for issuing FEBTC Check No. 553615. When said check was dishonored for insufficient funds and stop payment order, petitioner did not pay or make arrangements with the bank for its payment in full within five (5) banking days.

Petitioner should be exonerated, however, for issuing FEBTC Check No. 553602, which was dishonored for the reason DAUD or drawn against uncollected deposit. When the check was presented for payment, it was dishonored by the bank because the check deposit made by petitioner, which would make petitioner’s bank account balance more than enough to cover the face value of the subject check, had not been collected by the bank.

In Tan v. People,[38] this Court acquitted the petitioner therein who was indicted under B.P. Blg. 22, upon a check which was dishonored for the reason DAUD, among others. We observed that:

In the second place, even without relying on the credit line, petitioner’s bank account covered the check she issued because even though there were some deposits that were still uncollected the deposits became “good” and the bank certified that the check was “funded.”[39]

To be liable under Section 1[40] of B.P. Blg. 22, the check must be dishonored by the drawee bank for insufficiency of funds or credit or dishonored for the same reason had not the drawer, without any valid cause, ordered the bank to stop payment.

In the instant case, even though the check which petitioner deposited on July 20, 1992 became good only five (5) days later, he was considered by the bank to retroactively have had P160,659.39 in his account on July 22, 1992. This was more than enough to cover the check he issued to respondent in the amount of P106,579.60. Under the circumstance obtaining in this case, we find the petitioner had issued the check, with full ability to abide by his commitment[41] to pay his purchases.

Significantly, like Article 315 of the Revised Penal Code, B.P. Blg. 22 also speaks only of insufficiency of funds and does not treat of uncollected deposits. To repeat, we cannot interpret the law in such a way as to expand its provision to encompass the situation of uncollected deposits because it would make the law more onerous on the part of the accused. Again, criminal statutes are strictly construed against the Government and liberally in favor of the accused.[42]

As regards petitioner’s civil liability, this Court has previously ruled that an accused may be held civilly liable where the facts established by the evidence so warrant. [43] The rationale for this is simple. The criminal and civil liabilities of an accused are separate and distinct from each other. One is meant to punish the offender while the other is intended to repair the damage suffered by the aggrieved party. So, for the purpose of indemnifying the latter, the offense need not be proved beyond reasonable doubt but only by preponderance of evidence.[44]

We therefore sustain the appellate court’s award of damages to W.L. Foods in the total amount of P333,373.96, representing the sum of the checks petitioner issued for goods admittedly delivered to his company.

As to the appropriate penalty, petitioner was charged with estafa under Article 315, paragraph 2(d) of the Revised Penal Code, as amended by Presidential Decree No. 818[45] (P.D. No. 818).

Under Section 1[46] of P.D. No. 818, if the amount of the fraud exceeds P22,000, the penalty of reclusión temporal is imposed in its maximum period, adding one year for each additional P10,000 but the total penalty shall not exceed thirty (30) years, which shall be termed reclusión perpetua.[47] Reclusión perpetua is not the prescribed penalty for the offense, but merely describes the penalty actually imposed on account of the amount of the fraud involved.

WHEREFORE, the petition is PARTLY GRANTED. John Dy is hereby ACQUITTED in Criminal Case No. Q-93-46711 for estafa, and Criminal Case No. Q-93-46712 for violation of B.P. Blg. 22, but he is ORDERED to pay W.L. Foods the amount of P106,579.60 for goods delivered to his company.

In Criminal Case No. Q-93-46713 for estafa, the Decision of the Court of Appeals is AFFIRMED with MODIFICATION. Petitioner is sentenced to suffer an indeterminate penalty of twelve (12) years of prisión mayor, as minimum, to thirty (30) years of reclusión perpetua, as maximum.

In Criminal Case No. Q-93-46714 for violation of B.P. Blg. 22, the Decision of the Court of Appeals is AFFIRMED, and John Dy is hereby sentenced to one (1) year imprisonment and ordered to indemnify W.L. Foods in the amount of P226,794.36.

SO ORDERED.

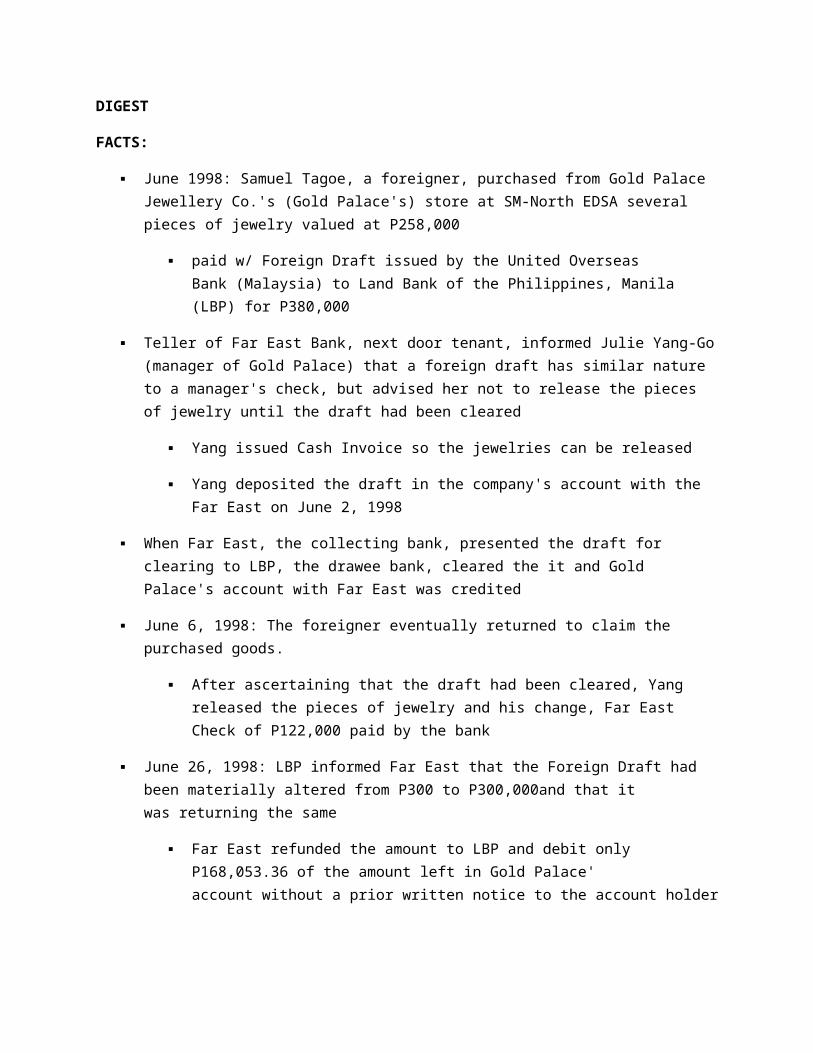

DIGEST

FACTS:

Since 1990, John Dy under the business name Dyna MarketinG has been the distributor of W.L. Food Products (W.L. Foods)

Dy would pay W.L. Foods in either cash or check upon pick up of stocks of snack foods

At times, he would entrust the payment to one of his drivers.

June 24, 1992: Dy's driver went to the branch office of W.L. Foods to pick up stocks of snack foods.

He introduced himself to the checker, Mary Jane D. Maraca, who upon confirming Dy's credit with the main office, gave him merchandise worth P106,579.60

In return, the driver handed her a blank Far East Bank and Trust Company (FEBTC) Check postdated July 22, 1992 signed by Dy

July 1, 1992: the driver obtained snack foods worth P226,794.36 in exchange for a blank FEBTC Check postdated July 31, 1992

In both instances, the driver was issued an unsigned delivery receipt.

When presented for payment, FEBTC dishonored the checks for insufficiency of funds.

Later, Gonzales sent Atty. Jimeno another letter advising her that FEBTC Check for P106,579.60 was returned to the drawee bank for the reasons stop payment order and drawn against uncollected deposit (DAUD), and not because it was drawn against insufficient funds as stated in the first letter.

Dy's savings deposit account ledger reflected a balance of P160,659.39 as of July 22, 1992. This, however, included a regional clearing check for P55,000 which he deposited on July 20, 1992, and which took 5 banking days to clear.

When William Lim, owner of W.L. Foods, phoned Dy about the matter, the latter explained that he could not pay since he had no funds yet.

This prompted the former to send petitioner a demand letter, which the latter ignored.

July 16, 1993: Lim charged Dy with 2 counts of estafa under Article 315, paragraph 2(d) of RPC and 2 counts of violation of B.P. Blg. 22

RTC convicted Dy on two counts each of estafa and violation of B.P. Blg. 22.

CA: affirmed

Dy contends that the checks were ineffectively issued

W.L. Foods' accountant had no authority to fill the amounts

ISSUE:

W/N Dy is liable for estafa and in violation of BP 22. Acquitted for the criminal cases in relation to the first check.

HELD:

YES but only for the 2nd check.

Estafa under Article 315, paragraph 2(d) of the Revised Penal Code, as amended by Republic Act No. 4885 elements postdating or issuance of a check in payment of an obligation contracted at the time the check was issued insufficiency of funds to cover the check - including the uncollected deposit he had more than enough funds to cover the first check damage to the payee

Section 191 of the Negotiable Instruments Law

"issue" - first delivery of an instrument, complete in form, to a person who takes it as a holder

Significantly, delivery is the final act essential to the negotiability of an instrument. Delivery denotes physical transfer of the instrument by the maker or drawer coupled with an intention to convey title to the payee and recognize him as a holder. It means more than handing over to another; it imports such transfer of the instrument to another as to enable the latter to hold it for himself

Even if the checks were given to W.L. Foods in blank, this alone did not make its issuance invalid.

When the checks were delivered to Lim, through his employee, he became a holder with prima facie authority to fill the blanks

SEC. 14. Blanks; when may be filled.-Where the instrument is wanting in any material particular,the person in possession thereof has a prima facie authority to complete it by filling up the blanks therein. And a signature on a blank paper delivered by the person making the signature in order that the paper may be converted into a negotiable instrument operates as aprima facie authority to fill it up as such for any amount.

The law merely requires that the instrument be in the possession of a person other than the drawer or maker

From such possession, together with the fact that the instrument is wanting in a material particular, the law presumes agency to fill up the blanks burden of proving want of authority or that the authority granted was exceeded, is placed on the person questioning such authority - Dy didn't fulfill this estafa punished under Article 315, paragraph 2(d) of the Revised Penal Code is committed when a check is dishonored for being drawn against insufficient funds or closed account, and not against uncollected deposit. Corollarily, the issuer of the check is not liable for estafa if the remaining balance and the

uncollected deposit, which was duly collected, could satisfy the amount of the check when presented for payment.

B.P. Blg. 22 elements = malum prohibitum

the making, drawing and issuance of any check to apply to account or for value the knowledge of the maker, drawer or issuer that at the time of issue he does not have sufficient funds in or credit with the drawee bank for the payment of such check in full upon its presentment subsequent dishonor of the check by the drawee bank for insufficiency of funds or credit or dishonor for the same reason had not the drawer, without any valid cause, ordered the bank to stop payment - considered by the bank to retroactively have had P160,659.39 in his account on July 22, 1992 which was more than enough to cover the first check. Dy admitted that he issued the checks, and that the signatures appearing on them were his Section 2 of B.P. Blg. 22, petitioner was prima facie presumed to know of the inadequacy of his funds with the bank when he did not pay the value of the goods or make arrangements for their payment in full within 5 banking days upon notice

G.R. No. 111190 June 27, 1995

LORETO D. DE LA VICTORIA, as City Fiscal of Mandaue City and in his personal capacity as garnishee, petitioner, vs.HON. JOSE P. BURGOS, Presiding Judge, RTC, Br. XVII, Cebu City, and RAUL H. SESBREÑO, respondents.

BELLOSILLO, J.:

RAUL H. SESBREÑO filed a complaint for damages against Assistant City Fiscals Bienvenido N. Mabanto, Jr., and Dario D. Rama, Jr., before the Regional Trial Court of Cebu City. After trial judgment was rendered ordering the defendants to pay P11,000.00 to the plaintiff, private respondent herein. The decision having become final and executory, on motion of the latter, the trial court ordered its execution. This order was questioned by the defendants before the Court of Appeals. However, on 15 January 1992 a writ of execution was issued.

On 4 February 1992 a notice of garnishment was served on petitioner Loreto D. de la Victoria as City Fiscal of Mandaue City where defendant Mabanto, Jr., was then detailed. The notice directed petitioner not to disburse, transfer, release or convey to any other person except to the deputy sheriff concerned the salary checks or other checks, monies, or cash due or belonging to Mabanto, Jr., under penalty of law. 1 On 10 March 1992 private respondent filed a motion before the trial court for examination of the garnishees.

On 25 May 1992 the petition pending before the Court of Appeals was dismissed. Thus the trial court, finding no more legal obstacle to act on the motion for examination of the garnishees, directed petitioner on 4 November 1992 to submit his report showing the amount of the garnished salaries of Mabanto, Jr., within fifteen (15) days from receipt 2 taking into consideration the provisions of Sec. 12, pars. (f) and (i), Rule 39 of the Rules of Court.

On 24 November 1992 private respondent filed a motion to require petitioner to explain why he should not be cited in contempt of court for failing to comply with the order of 4 November 1992.

On the other hand, on 19 January 1993 petitioner moved to quash the notice of garnishment claiming that he was not in possession of any money, funds, credit, property or anything of value belonging to Mabanto, Jr., except his salary and RATA checks, but that said checks were not yet properties of Mabanto, Jr., until delivered to him. He further claimed that, as such, they were still public funds which could not be subject to garnishment.

On 9 March 1993 the trial court denied both motions and ordered petitioner to immediately comply with its order of 4 November 1992. 3 It opined that the checks of Mabanto, Jr., had already been released through petitioner by the Department of Justice duly signed by the officer concerned. Upon service of the writ of garnishment, petitioner as custodian of the checks was under obligation to hold them for the judgment creditor. Petitioner became a virtual party to, or a forced intervenor in, the case and the trial court thereby acquired jurisdiction to bind him to its orders and processes with a view to

the complete satisfaction of the judgment. Additionally, there was no sufficient reason for petitioner to hold the checks because they were no longer government funds and presumably delivered to the payee, conformably with the last sentence of Sec. 16 of the Negotiable Instruments Law.

With regard to the contempt charge, the trial court was not morally convinced of petitioner's guilt. For, while his explanation suffered from procedural infirmities nevertheless he took pains in enlightening the court by sending a written explanation dated 22 July 1992 requesting for the lifting of the notice of garnishment on the ground that the notice should have been sent to the Finance Officer of the Department of Justice. Petitioner insists that he had no authority to segregate a portion of the salary of Mabanto, Jr. The explanation however was not submitted to the trial court for action since the stenographic reporter failed to attach it to the record. 4

On 20 April 1993 the motion for reconsideration was denied. The trial court explained that it was not the duty of the garnishee to inquire or judge for himself whether the issuance of the order of execution, writ of execution and notice of garnishment was justified. His only duty was to turn over the garnished checks to the trial court which issued the order of execution. 5

Petitioner raises the following relevant issues: (1) whether a check still in the hands of the maker or its duly authorized representative is owned by the payee before physical delivery to the latter: and, (2) whether the salary check of a government official or employee funded with public funds can be subject to garnishment.

Petitioner reiterates his position that the salary checks were not owned by Mabanto, Jr., because they were not yet delivered to him, and that petitioner as garnishee has no legal obligation to hold and deliver them to the trial court to be applied to Mabanto, Jr.'s judgment debt. The thesis of petitioner is that the salary checks still formed part of public funds and therefore beyond the reach of garnishment proceedings.

Petitioner has well argued his case.

Garnishment is considered as a species of attachment for reaching credits belonging to the judgment debtor owing to him from a stranger to the litigation. 6 Emphasis is laid on the phrase "belonging to the judgment debtor" since it is the focal point in resolving the issues raised.

As Assistant City Fiscal, the source of the salary of Mabanto, Jr., is public funds. He receives his compensation in the form of checks from the Department of Justice through petitioner as City Fiscal of Mandaue City and head of office. Under Sec. 16 of the Negotiable Instruments Law, every contract on a negotiable instrument is incomplete and revocable until deliveryof the instrument for the purpose of giving effect thereto. As ordinarily understood, delivery means the transfer of the possession of the instrument by the maker or drawer with intent to transfer title to the payee and recognize him as the holder thereof. 7

According to the trial court, the checks of Mabanto, Jr., were already released by the Department of Justice duly signed by the officer concerned through petitioner and upon service of the writ of

garnishment by the sheriff petitioner was under obligation to hold them for the judgment creditor. It recognized the role of petitioner as custodian of the checks. At the same time however it considered the checks as no longer government funds and presumed delivered to the payee based on the last sentence of Sec. 16 of the Negotiable Instruments Law which states: "And where the instrument is no longer in the possession of a party whose signature appears thereon, a valid and intentional delivery by him is presumed." Yet, the presumption is not conclusive because the last portion of the provision says "until the contrary is proved." However this phrase was deleted by the trial court for no apparent reason. Proof to the contrary is its own finding that the checks were in the custody of petitioner. Inasmuch as said checks had not yet been delivered to Mabanto, Jr., they did not belong to himand still had the character of public funds. In Tiro v. Hontanosas 8 we ruled that —

The salary check of a government officer or employee such as a teacher does not belong to him before it is physically delivered to him. Until that time the check belongs to the government. Accordingly, before there is actual delivery of the check, the payee has no power over it; he cannot assign it without the consent of the Government.

As a necessary consequence of being public fund, the checks may not be garnished to satisfy the judgment. 9 The rationale behind this doctrine is obvious consideration of public policy. The Court succinctly stated in Commissioner of Public Highways v. San Diego 10 that —

The functions and public services rendered by the State cannot be allowed to be paralyzed or disrupted by the diversion of public funds from their legitimate and specific objects, as appropriated by law.

In denying petitioner's motion for reconsideration, the trial court expressed the additional ratiocination that it was not the duty of the garnishee to inquire or judge for himself whether the issuance of the order of execution, the writ of execution, and the notice of garnishment was justified, citing our ruling in Philippine Commercial Industrial Bank v. Court of Appeals.11 Our precise ruling in that case was that "[I]t is not incumbent upon the garnishee to inquire or to judge for itself whether or not the order for the advance execution of a judgment is valid." But that is invoking only the general rule. We have also established therein the compelling reasons, as exceptions thereto, which were not taken into account by the trial court, e.g., a defect on the face of the writ or actual knowledge by the garnishee of lack of entitlement on the part of the garnisher. It is worth to note that the ruling referred to the validity of advance execution of judgments, but a careful scrutiny of that case and similar cases reveals that it was applicable to a notice of garnishment as well. In the case at bench, it was incumbent upon petitioner to inquire into the validity of the notice of garnishment as he had actual knowledge of the non-entitlement of private respondent to the checks in question. Consequently, we find no difficulty concluding that the trial court exceeded its jurisdiction in issuing the notice of garnishment concerning the salary checks of Mabanto, Jr., in the possession of petitioner.

WHEREFORE, the petition is GRANTED. The orders of 9 March 1993 and 20 April 1993 of the Regional Trial Court of Cebu City, Br. 17, subject of the petition are SET ASIDE. The notice of garnishment served on petitioner dated 3 February 1992 is ordered DISCHARGED.

SO ORDERED.

Quiason and Kapunan, JJ., concur.

Separate Opinions

DAVIDE, JR., J., concurring and dissenting:

This Court may take judicial notice of the fact that checks for salaries of employees of various Departments all over the country are prepared in Manila not at the end of the payroll period, but days before it to ensure that they reach the employees concerned not later than the end of the payroll period. As to the employees in the provinces or cities, the checks are sent through the heads of the corresponding offices of the Departments. Thus, in the case of Prosecutors and Assistant Prosecutors of the Department of Justice, the checks are sent through the Provincial Prosecutors or City Prosecutors, as the case may be, who shall then deliver the checks to the payees.

Involved in the instant case are the salary and RATA checks of then Assistant City Fiscal Bienvenido Mabanto, Jr., who was detailed in the Office of the City Fiscal (now Prosecutor) of Mandaue City. Conformably with the aforesaid practice, these checks were sent to Mabanto thru the petitioner who was then the City Fiscal of Mandaue City.

The ponencia failed to indicate the payroll period covered by the salary check and the month to which the RATA check corresponds.

I respectfully submit that if these salary and RATA checks corresponded, respectively, to a payroll period and to a month which had already lapsed at the time the notice of garnishment was served, the garnishment would be valid, as the checks would then cease to be property of the Government and would become property of Mabanto. Upon the expiration of such period and month, the sums indicated therein were deemed automatically segregated from the budgetary allocations for the Department of Justice under the General Appropriations Act.

It must be recalled that the public policy against execution, attachment, or garnishment is directed to public funds.

Thus, in the case of Director of the Bureau of Commerce and Industry vs. Concepcion 1 where the core issue was whether or not the salary due from the Government to a public officer or employee can, by garnishment, be seized before being paid to him and appropriated to the payment of his judgment debts, this Court held:

A rule, which has never been seriously questioned, is that money in the hands of public officers, although it may be due government employees, is not liable to the creditors of these employees in the process of garnishment. One reason is, that the State, by virtue of its sovereignty, may not be sued in its own courts except by express authorization by the Legislature, and to subject its officers to garnishment would be to permit indirectly what is prohibited directly. Another reason is that moneys sought to be garnished, as long as they remain in the hands of the disbursing officer of the Government, belong to the latter, although the defendant in garnishment may be entitled to a specific portion thereof. And still another reason which covers both of the foregoing is that every consideration of public policy forbids it.

The United States Supreme Court, in the leading case of Buchanan vs. Alexander ([1846], 4 How., 19), in speaking of the right of creditors of seamen, by process of attachment, to divert the public money from its legitimate and appropriate object, said:

To state such a principle is to refute it. No government can sanction it. At all times it would be found embarrassing, and under some circumstances it might be fatal to the public service. . . .So long as money remains in the hands of a disbursing officer, it is as much the money of the United States, as if it had not been drawn from the treasury. Until paid over by the agent of the government to the person entitled to it, the fund cannot, in any legal sense, be considered a part of his effects." (See, further, 12 R.C.L., p. 841; Keene vs. Smith [1904], 44 Ore., 525; Wild vs. Ferguson [1871], 23 La. Ann., 752; Bank of Tennessee vs. Dibrell [1855], 3 Sneed [Tenn.], 379). (emphasis supplied)

The authorities cited in the ponencia are inapplicable. Garnished or levied on therein were public funds, to wit: (a) the pump irrigation trust fund deposited with the Philippine National Bank (PNB) in the account of the Irrigation Service Unit inRepublic vs. Palacio; 2 (b) the deposits of the National Media Production Center in Traders Royal Bank vs. Intermediate Appellate Court; 3 and (c) the deposits of the Bureau of Public Highways with the PNB under a current account, which may be expended only for their legitimate object as authorized by the corresponding legislative appropriation in Commissioner of Public Highways vs. Diego. 4

Neither is Tiro vs. Hontanosas 5 squarely in point. The said case involved the validity of Circular No. 21, series of 1969, issued by the Director of Public Schools which directed that "henceforth no cashier or disbursing officer shall pay to attorneys-in-fact or other persons who may be authorized under a power of attorney or other forms of authority to collect the salary of an employee, except when the persons so designated and authorized is an immediate member of the family of the employee concerned, and in all other cases except upon proper authorization of the Assistant Executive Secretary for Legal and Administrative Matters, with the recommendation of the Financial Assistant." Private respondent Zafra Financing Enterprise, which had extended loans to public school teachers in Cebu City and obtained from the latter promissory notes and special powers of attorney authorizing it to take and collect their salary checks from the Division Office in Cebu City of the Bureau of Public Schools, sought, inter alia, to nullify the Circular. It is clear that the teachers had in fact assigned to or waived in favor of Zafra their future salaries which were still public funds. That assignment or waiver was contrary to public policy.

I would therefore vote to grant the petition only if the salary and RATA checks garnished corresponds to an unexpired payroll period and RATA month, respectively.

Padilla, J., concurs.

Separate Opinions

DAVIDE, JR., J., concurring and dissenting:

This Court may take judicial notice of the fact that checks for salaries of employees of various Departments all over the country are prepared in Manila not at the end of the payroll period, but days

before it to ensure that they reach the employees concerned not later than the end of the payroll period. As to the employees in the provinces or cities, the checks are sent through the heads of the corresponding offices of the Departments. Thus, in the case of Prosecutors and Assistant Prosecutors of the Department of Justice, the checks are sent through the Provincial Prosecutors or City Prosecutors, as the case may be, who shall then deliver the checks to the payees.

Involved in the instant case are the salary and RATA checks of then Assistant City Fiscal Bienvenido Mabanto, Jr., who was detailed in the Office of the City Fiscal (now Prosecutor) of Mandaue City. Conformably with the aforesaid practice, these checks were sent to Mabanto thru the petitioner who was then the City Fiscal of Mandaue City.

The ponencia failed to indicate the payroll period covered by the salary check and the month to which the RATA check corresponds.

I respectfully submit that if these salary and RATA checks corresponded, respectively, to a payroll period and to a month which had already lapsed at the time the notice of garnishment was served, the garnishment would be valid, as the checks would then cease to be property of the Government and would become property of Mabanto. Upon the expiration of such period and month, the sums indicated therein were deemed automatically segregated from the budgetary allocations for the Department of Justice under the General Appropriations Act.

It must be recalled that the public policy against execution, attachment, or garnishment is directed to public funds.

Thus, in the case of Director of the Bureau of Commerce and Industry vs. Concepcion 1 where the core issue was whether or not the salary due from the Government to a public officer or employee can, by garnishment, be seized before being paid to him and appropriated to the payment of his judgment debts, this Court held:

A rule, which has never been seriously questioned, is that money in the hands of public officers, although it may be due government employees, is not liable to the creditors of these employees in the process of garnishment. One reason is, that the State, by virtue of its sovereignty, may not be sued in its own courts except by express authorization by the Legislature, and to subject its officers to garnishment would be to permit indirectly what is prohibited directly. Another reason is that moneys sought to be garnished, as long as they remain in the hands of the disbursing officer of the Government, belong to the latter, although the defendant in garnishment may be entitled to a specific portion thereof. And still another reason which covers both of the foregoing is that every consideration of public policy forbids it.

The United States Supreme Court, in the leading case of Buchanan vs. Alexander ([1846], 4 How., 19), in speaking of the right of creditors of seamen, by process of attachment, to divert the public money from its legitimate and appropriate object, said:

To state such a principle is to refute it. No government can sanction it. At all times it would be found embarrassing, and under some circumstances it might be fatal to the public service. . . .So long as money

remains in the hands of a disbursing officer, it is as much the money of the United States, as if it had not been drawn from the treasury. Until paid over by the agent of the government to the person entitled to it, the fund cannot, in any legal sense, be considered a part of his effects." (See, further, 12 R.C.L., p. 841; Keene vs. Smith [1904], 44 Ore., 525; Wild vs. Ferguson [1871], 23 La. Ann., 752; Bank of Tennessee vs. Dibrell [1855], 3 Sneed [Tenn.], 379). (emphasis supplied)

The authorities cited in the ponencia are inapplicable. Garnished or levied on therein were public funds, to wit: (a) the pump irrigation trust fund deposited with the Philippine National Bank (PNB) in the account of the Irrigation Service Unit inRepublic vs. Palacio; 2 (b) the deposits of the National Media Production Center in Traders Royal Bank vs. Intermediate Appellate Court; 3 and (c) the deposits of the Bureau of Public Highways with the PNB under a current account, which may be expended only for their legitimate object as authorized by the corresponding legislative appropriation in Commissioner of Public Highways vs. Diego. 4

Neither is Tiro vs. Hontanosas 5 squarely in point. The said case involved the validity of Circular No. 21, series of 1969, issued by the Director of Public Schools which directed that "henceforth no cashier or disbursing officer shall pay to attorneys-in-fact or other persons who may be authorized under a power of attorney or other forms of authority to collect the salary of an employee, except when the persons so designated and authorized is an immediate member of the family of the employee concerned, and in all other cases except upon proper authorization of the Assistant Executive Secretary for Legal and Administrative Matters, with the recommendation of the Financial Assistant." Private respondent Zafra Financing Enterprise, which had extended loans to public school teachers in Cebu City and obtained from the latter promissory notes and special powers of attorney authorizing it to take and collect their salary checks from the Division Office in Cebu City of the Bureau of Public Schools, sought, inter alia, to nullify the Circular. It is clear that the teachers had in fact assigned to or waived in favor of Zafra their future salaries which were still public funds. That assignment or waiver was contrary to public policy.

I would therefore vote to grant the petition only if the salary and RATA checks garnished corresponds to an unexpired payroll period and RATA month, respectively.

DIGEST

FACTS:

Assistant City Fiscal Bienvenido N. Mabanto was ordered to pay herein private respondent Raul Sesbreño P11,000.00 as damages. A notice of garnishment was served on herein petitioner Loreto D. de la Victoria as City Fiscal of Mandaue City where Mabanto was detailed. V was directed not to disburse, transfer, release or convey to any other person except to the deputy sheriff concerned the salary checks or other checks, monies, or cash due or belonging to Mabanto, Jr., under penalty of law. Later, V was directed to submit his report showing the amount of the garnished salaries. V moved to quash the notice of garnishment claiming that he was not in possession of any money, funds, credit, property or anything of value belonging to Mabanto, Jr., except his salary and RATA checks, but that said checks were not yet properties of Mabanto, Jr., until delivered to him. He further claimed that, as such, they were still public funds which could not be subject to garnishment.

ISSUE:

W/N a check still in the hands of the maker or its duly authorized representative is owned by the payee before physical delivery to the latter.

RULING:

As Assistant City Fiscal, the source of the salary of Mabanto, Jr., is public funds. He receives his compensation in the form of checks from the DOJ through V as City Fiscal of Mandaue City and head of office. Under Sec. 16 of the Negotiable Instruments Law, every contract on a negotiable instrument is incomplete and revocable until delivery of the instrument for the purpose of giving effect thereto. As ordinarily understood, delivery means the transfer of the possession of the instrument by the maker or drawer with intent to transfer title to the payee and recognize him as the holder thereof.

Inasmuch as said checks had not yet been delivered to Mabanto, Jr., they did not belong to him and still had the character of public funds. The salary check of a government officer or employee does not belong to him before it is physically delivered to him. Until that time the check belongs to the government. Accordingly, before there is actual delivery of the check, the payee has no power over it; he cannot assign it without the consent of the Government. Being public fund, the checks may not be garnished to satisfy the judgment in consideration of public policy.

BANK OF THE PHILIPPINE ISLANDS, Petitioner,

-versus-

GREGORIO C. ROXAS, Respondent.

G.R. No. 157833October 15, 2007

DECISION

SANDOVAL-GUTIERREZ, J.:

For our resolution is the instant Petition for Review on Certiorari assailing the Decision[1] of the Court of Appeals (Fourth Division) dated February 13, 2003 in CA-G.R. CV No. 67980.

The facts of the case, as found by the trial court and affirmed by the Court of Appeals, are:

Gregorio C. Roxas, respondent, is a trader. Sometime in March 1993, he delivered stocks of vegetable oil to spouses Rodrigo and Marissa Cawili. As payment therefor, spouses Cawili issued a personal check in the amount of P348,805.50. However, when respondent tried to encash the check, it was dishonored by the drawee bank. Spouses Cawili then assured him that they would replace the bounced check with a cashier’s check from the Bank of the Philippine Islands (BPI), petitioner.

On March 31, 1993, respondent and Rodrigo Cawili went to petitioner’s branch at Shaw Boulevard, Mandaluyong City where Elma Capistrano, the branch manager, personally attended to them. Upon Elma’s instructions, Lita Sagun, the bank teller, prepared BPI Cashier’s Check No. 14428 in the amount of P348,805.50, drawn against the account of Marissa Cawili, payable to respondent. Rodrigo then handed the check to respondent in the presence of Elma.

The following day, April 1, 1993, respondent returned to petitioner’s branch at Shaw Boulevard to encash the cashier’s check but it was dishonored. Elma informed him that Marissa’s account was closed on that date.

Despite respondent’s insistence, the bank officers refused to encash the check and tried to retrieve it from respondent. He then called his lawyer who advised him to deposit the check in his (respondent’s) account at Citytrust, Ortigas Avenue. However, the check was dishonored on the ground “Account Closed.”

On September 23, 1993, respondent filed with the Regional Trial Court, Branch 263, Pasig City a complaint for sum of money against petitioner, docketed as Civil Case No. 63663. Respondent prayed that petitioner be ordered to pay the amount of the check, damages and cost of the suit.

In its answer, petitioner specifically denied the allegations in the complaint, claiming that it issued the check by mistake in good faith; that its dishonor was due to lack of consideration; and that respondent’s remedy was to sue Rodrigo Cawili who purchased the check. As a counterclaim, petitioner prayed that respondent be ordered to pay attorney’s fees and expenses of litigation.

Petitioner filed a third-party complaint against spouses Cawili. They were later declared in default for their failure to file their answer.

After trial, the RTC rendered a Decision, the dispositive portion of which reads:

WHEREFORE, in view of the foregoing premises, this Court hereby renders judgment in favor of herein plaintiff and orders the defendant, Bank of the Philippine Islands, to pay Gerardo C. Roxas:

1) The sum of P348,805.50, the face value of the cashier’s check, with legal interest thereon computed from April 1, 1993 until the amount is fully paid;

2) The sum of P50,000.00 for moral damages;

3) The sum of P50,000.00 as exemplary damages to serve as an example for the public good;

4) The sum of P25,000.00 for and as attorney’s fees; and the

5) Costs of suit.

As to the third-party complaint, third-party defendants Spouses Rodrigo and Marissa Cawili are hereby ordered to indemnify defendant Bank of the Philippine Islands such amount(s) adjudged and actually paid by it to herein plaintiff Gregorio C. Roxas, including the costs of suit.

SO ORDERED.

On appeal, the Court of Appeals, in its Decision, affirmed the trial court’s judgment.

Hence, this petition.

Petitioner ascribes to the Court of Appeals the following errors: (1) in finding that respondent is a holder in due course; and (2) in holding that it (petitioner) is liable to respondent for the amount of the cashier’s check.

Section 52 of the Negotiable Instruments Law provides:

SEC. 52. What constitutes a holder in due course. – A holder in due course is a holder who has taken the instrument under the following conditions:

(a) That it is complete and regular upon its face;

(b) That he became the holder of it before it was overdue and without notice that it had been previously dishonored, if such was the fact;

(c) That he took it in good faith and for value;

(d) That at the time it was negotiated to him, he had no notice of any infirmity in the instrument or defect in the title of person negotiating it.

As a general rule, under the above provision, every holder is presumed prima facie to be a holder in due course. One who claims otherwise has the onus probandi to prove that one or more of the conditions required to constitute a holder in due course are lacking. In this case, petitioner contends that the element of “value” is not present, therefore, respondent could not be a holder in due course.

Petitioner’s contention lacks merit. Section 25 of the same law states:

SEC. 25. Value, what constitutes. – Value is any consideration sufficient to support a simple contract. An antecedent or pre-existing debt constitutes value; and is deemed as such whether the instrument is payable on demand or at a future time.

In Walker Rubber Corp. v. Nederlandsch Indische & Handelsbank, N.V. and South Sea Surety & Insurance Co., Inc.,[2] this Court ruled that value “in general terms may be some right, interest, profit or benefit to the party who makes the contract or some forbearance, detriment, loan, responsibility, etc. on the other side.” Here, there is no dispute that respondent received Rodrigo Cawili’s cashier’s check as payment for the former’s vegetable oil. The fact that it was Rodrigo who purchased the cashier’s check frompetitioner will not affect respondent’s status as a holder for value since the check was delivered to him as payment for the vegetable oil he sold to spouses Cawili. Verily, the Court of Appeals did not err in concluding that respondent is a holder in due course of the cashier’s check.

Furthermore, it bears emphasis that the disputed check is a cashier’s check. In International Corporate Bank v. Spouses Gueco,[3] this Court held that a cashier’s check is really the bank’s own check and may be treated as a promissory note with the bank as the maker. The check becomes the primary obligation of the bank which issues it and constitutes a written promise to pay upon demand. In New Pacific Timber & Supply Co. Inc. v. Señeris,[4] this Court took judicial notice of the “well-known and accepted practice in the business sector that a cashier’s check is deemed as cash.” This is because the mere issuance of a cashier’s check is considered acceptance thereof.

In view of the above pronouncements, petitioner bank became liable to respondent from the moment it issued the cashier’s check. Having been accepted by respondent, subject to no condition whatsoever, petitioner should have paid the same upon presentment by the former.

WHEREFORE, the petition is DENIED. The assailed Decision of the Court of Appeals (Fourth Division) in CA-G.R. CV No. 67980 is AFFIRMED. Costs against petitioner.

SO ORDERED.

DIGEST

FACTS:

Gregorio Roxas, as trader, delivered stocks of vegetable oil to Spouses Rodrigo and MarissaCawili. As payment, they issued a personal check amounting to PHP348,805.50 which wasdishonored by the drawee bank when respondent tried to encash.The Spouses Cawili replaced the check with a cashier's check from Bank of the Philippine Island(Petitioner). The cashier's check was drawn against the account of Marissa Cawili. The Cashier Checkwas wanded to respondent by Rodrigo Cawili.When respondent tried to encash the Cashier Check, it was dishonored on the ground that theaccount of Marissa was closed on the same date that respondent tried to encash. Respondentthereafter filed a complaint with the Regional Trial Court for a sum of money praying that petitioner payhim the amount of the chack, damages and cost of the suit.The RTC in its decision held that Petitioner is liable to pay the face value of the cashier's checkamounting to PHP 384, 805.50. On appeal, the CA affirmed the decision of the RTC. Hence, the filingof the Petition for Certiorari by the petitioner.

LAW INVOLVED: Sec 50 and Sec. 25 of NIL

ISSUE:

(1) Whether or not the respondent is a holder in due course?

(2) Whether or not petitioner is liable to respondent for the amount of the cashier’s check?

HELD

:The petition is DENIED. The assailed Decision of the Court of Appeals (Fourth Division) is AFFIRMED. Held [1]:

Petitioner contends that the element of "value" is not present, therefore, respondent could notbe a holder in due course.There is no dispute that respondent received Rodrigo Cawili’s cashier’s check as payment for the former’s vegetable oil. The fact that it was Rodrigo who purchased the cashier’s check frompetitioner will not affect respondent’s status as a holder for value since the check was delivered to himas payment for the vegetable oil he sold to spouses Cawili. Verily, the Court of Appeals did not err in

G.R. No. 93073 December 21, 1992

REPUBLIC PLANTERS BANK, petitioner, vs.COURT OF APPEALS and FERMIN CANLAS, respondents.

CAMPOS, JR., J.:

This is an appeal by way of a Petition for Review on Certiorari from the decision * of the Court of Appeals in CA G.R. CV No. 07302, entitled "Republic Planters Bank.Plaintiff-Appellee vs. Pinch Manufacturing Corporation, et al., Defendants, and Fermin Canlas, Defendant-Appellant", which affirmed the decision ** in Civil Case No. 82-5448 except that it completely absolved Fermin Canlas from liability under the promissory notes and reduced the award for damages and attorney's fees. The RTC decision, rendered on June 20, 1985, is quoted hereunder:

WHEREFORE, premises considered, judgment is hereby rendered in favor of the plaintiff Republic Planters Bank, ordering defendant Pinch Manufacturing Corporation (formerly Worldwide Garment Manufacturing, Inc.) and defendants Shozo Yamaguchi and Fermin Canlas to pay, jointly and severally, the plaintiff bank the following sums with interest thereon at 16% per annum from the dates indicated, to wit:

Under the promissory note (Exhibit "A"), the sum of P300,000.00 with interest from January 29, 1981 until fully paid; under promissory note (Exhibit "B"), the sum of P40,000.00 with interest from November 27, 1980; under the promissory note (Exhibit "C"), the sum of P166,466.00 which interest from January 29, 1981; under the promissory note (Exhibit "E"), the sum of P86,130.31 with interest from January 29, 1981; under the promissory note (Exhibit "G"), the sum of P12,703.70 with interest from November 27, 1980; under the promissory note (Exhibit "H"), the sum of P281,875.91 with interest from January 29, 1981; and under the promissory note (Exhibit "I"), the sum of P200,000.00 with interest from January 29, 1981.

Under the promissory note (Exhibit "D") defendants Pinch Manufacturing Corporation (formerly named Worldwide Garment Manufacturing, Inc.), and Shozo Yamaguchi are ordered to pay jointly and severally, the plaintiff bank the sum of P367,000.00 with interest of 16% per annum from January 29, 1980 until fully paid

Under the promissory note (Exhibit "F") defendant corporation Pinch (formerly Worldwide) is ordered to pay the plaintiff bank the sum of P140,000.00 with interest at 16% per annum from November 27, 1980 until fully paid.

Defendant Pinch (formely Worldwide) is hereby ordered to pay the plaintiff the sum of P231,120.81 with interest at 12% per annum from July 1, 1981, until fully paid and the sum of P331,870.97 with interest from March 28, 1981, until fully paid.

All the defendants are also ordered to pay, jointly and severally, the plaintiff the sum of P100,000.00 as and for reasonable attorney's fee and the further sum equivalent to 3% per annum of the respective principal sums from the dates above stated as penalty charge until fully paid, plus one percent (1%) of the principal sums as service charge.

With costs against the defendants.

SO ORDERED. 1

From the above decision only defendant Fermin Canlas appealed to the then Intermediate Court (now the Court Appeals). His contention was that inasmuch as he signed the promissory notes in his capacity as officer of the defunct Worldwide Garment Manufacturing, Inc, he should not be held personally liable for such authorized corporate acts that he performed. It is now the contention of the petitioner Republic Planters Bank that having unconditionally signed the nine (9) promissory notes with Shozo Yamaguchi, jointly and severally, defendant Fermin Canlas is solidarity liable with Shozo Yamaguchi on each of the nine notes.

We find merit in this appeal.

From the records, these facts are established: Defendant Shozo Yamaguchi and private respondent Fermin Canlas were President/Chief Operating Officer and Treasurer respectively, of Worldwide Garment Manufacturing, Inc.. By virtue of Board Resolution No.1 dated August 1, 1979, defendant Shozo Yamaguchi and private respondent Fermin Canlas were authorized to apply for credit facilities with the petitioner Republic Planters Bank in the forms of export advances and letters of credit/trust receipts accommodations. Petitioner bank issued nine promissory notes, marked as Exhibits A to I inclusive, each of which were uniformly worded in the following manner:

___________, after date, for value received, I/we, jointly and severaIly promise to pay to the ORDER of the REPUBLIC PLANTERS BANK, at its office in Manila, Philippines, the sum of ___________ PESOS(....) Philippine Currency...

On the right bottom margin of the promissory notes appeared the signatures of Shozo Yamaguchi and Fermin Canlas above their printed names with the phrase "and (in) his personal capacity" typewritten below. At the bottom of the promissory notes appeared: "Please credit proceeds of this note to:

________ Savings Account ______XX Current Account

No. 1372-00257-6

of WORLDWIDE GARMENT MFG. CORP.

These entries were separated from the text of the notes with a bold line which ran horizontally across the pages.

In the promissory notes marked as Exhibits C, D and F, the name Worldwide Garment Manufacturing, Inc. was apparently rubber stamped above the signatures of defendant and private respondent.

On December 20, 1982, Worldwide Garment Manufacturing, Inc. noted to change its corporate name to Pinch Manufacturing Corporation.

On February 5, 1982, petitioner bank filed a complaint for the recovery of sums of money covered among others, by the nine promissory notes with interest thereon, plus attorney's fees and penalty charges. The complainant was originally brought against Worldwide Garment Manufacturing, Inc. inter alia, but it was later amended to drop Worldwide Manufacturing, Inc. as defendant and substitute Pinch Manufacturing Corporation it its place. Defendants Pinch Manufacturing Corporation and Shozo Yamaguchi did not file an Amended Answer and failed to appear at the scheduled pre-trial conference despite due notice. Only private respondent Fermin Canlas filed an Amended Answer wherein he, denied having issued the promissory notes in question since according to him, he was not an officer of Pinch Manufacturing Corporation, but instead of Worldwide Garment Manufacturing, Inc., and that when he issued said promissory notes in behalf of Worldwide Garment Manufacturing, Inc., the same were in blank, the typewritten entries not appearing therein prior to the time he affixed his signature.

In the mind of this Court, the only issue material to the resolution of this appeal is whether private respondent Fermin Canlas is solidarily liable with the other defendants, namely Pinch Manufacturing Corporation and Shozo Yamaguchi, on the nine promissory notes.

We hold that private respondent Fermin Canlas is solidarily liable on each of the promissory notes bearing his signature for the following reasons:

The promissory motes are negotiable instruments and must be governed by the Negotiable Instruments Law. 2

Under the Negotiable lnstruments Law, persons who write their names on the face of promissory notes are makers and are liable as such. 3 By signing the notes, the maker promises to pay to the order of the payee or any holder 4 according to the tenor thereof. 5 Based on the above provisions of law, there is no denying that private respondent Fermin Canlas is one of the co-makers of the promissory notes. As such, he cannot escape liability arising therefrom.

Where an instrument containing the words "I promise to pay" is signed by two or more persons, they are deemed to be jointly and severally liable thereon. 6 An instrument which begins" with "I" ,We" , or "Either of us" promise to, pay, when signed by two or more persons, makes them solidarily liable. 7 The fact that the singular pronoun is used indicates that the promise is individual as to each other; meaning that each of the co-signers is deemed to have made an independent singular promise to pay the notes in full.

In the case at bar, the solidary liability of private respondent Fermin Canlas is made clearer and certain, without reason for ambiguity, by the presence of the phrase "joint and several" as describing the unconditional promise to pay to the order of Republic Planters Bank. A joint and several note is one in which the makers bind themselves both jointly and individually to the payee so that all may be sued together for its enforcement, or the creditor may select one or more as the object of the suit. 8 A joint and several obligation in common law corresponds to a civil law solidary obligation; that is, one of

several debtors bound in such wise that each is liable for the entire amount, and not merely for his proportionate share. 9 By making a joint and several promise to pay to the order of Republic Planters Bank, private respondent Fermin Canlas assumed the solidary liability of a debtor and the payee may choose to enforce the notes against him alone or jointly with Yamaguchi and Pinch Manufacturing Corporation as solidary debtors.

As to whether the interpolation of the phrase "and (in) his personal capacity" below the signatures of the makers in the notes will affect the liability of the makers, We do not find it necessary to resolve and decide, because it is immaterial and will not affect to the liability of private respondent Fermin Canlas as a joint and several debtor of the notes. With or without the presence of said phrase, private respondent Fermin Canlas is primarily liable as a co-maker of each of the notes and his liability is that of a solidary debtor.

Finally, the respondent Court made a grave error in holding that an amendment in a corporation's Articles of Incorporation effecting a change of corporate name, in this case from Worldwide Garment manufacturing Inc to Pinch Manufacturing Corporation extinguished the personality of the original corporation.

The corporation, upon such change in its name, is in no sense a new corporation, nor the successor of the original corporation. It is the same corporation with a different name, and its character is in no respect changed. 10

A change in the corporate name does not make a new corporation, and whether effected by special act or under a general law, has no affect on the identity of the corporation, or on its property, rights, or liabilities. 11

The corporation continues, as before, responsible in its new name for all debts or other liabilities which it had previously contracted or incurred. 12

As a general rule, officers or directors under the old corporate name bear no personal liability for acts done or contracts entered into by officers of the corporation, if duly authorized. Inasmuch as such officers acted in their capacity as agent of the old corporation and the change of name meant only the continuation of the old juridical entity, the corporation bearing the same name is still bound by the acts of its agents if authorized by the Board. Under the Negotiable Instruments Law, the liability of a person signing as an agent is specifically provided for as follows: