Embed Size (px)

Citation preview

Chapter 24Principles of

Corporate FinanceTenth Edition

The Many Different Kinds of Debt

Slides by

Matthew Will

McGraw-Hill/Irwin Copyright © 2011 by the McGraw-Hill Companies, Inc. All rights reserved.

24-2

Topics Covered

Domestic Bonds, Foreign Bonds and Euro Bonds

The Bond ContractSecurity and SeniorityRepayment ProvisionsDebt CovenantsConvertible Bonds and WarrantsPrivate Placements and Project FinanceInnovation in the Bond Market

24-3

Bond Terminology

Foreign bonds - bonds that are sold to local investors in another country's bond market

Yankee bond- a bond sold publicly by a foreign company in the United States

Samurai - a bond sold by a foreign firm in Japan Eurobond market - when European and American

multinationals are forced to tap into international markets for capital

Global Bonds - very large bond issues that are marketed both internationally (that is, in the eurobond market) and in individual domestic markets

24-4

Bond Terminology

Indenture or trust deed - the bond agreement between the borrower and a trust company

Registered bond - a bond in which the Company's records show ownership and interest and principal are paid directly to each owner

Bearer bonds - the bond holder must send in coupons to claim interest and must send a certificate to claim the final payment of principal

Accrued interest - the amount of accumulated interest since the last coupon payment

Coupon – the annual or semiannual interest paid on a bond LIBOR - London interbank offered rate - the rate at which

international banks lend to one another

24-5

Bond Contract

Trustee Bank of America National Trust and Savings Association

Rights of defaultThe trustee or 25% of debenture holders may declare the principle due and payable

Registered Fully registeredDenomination $1,000 Amount issued $250 millionIssue Date 26-Aug-1992

OfferedIssued at a price of 99.489% plus accrued interest (proceeds to company 98.614%) through First Boston Corporation

Interest At a rate of 8.25% per annum, payable February 15 and August 15Seniority Ranks pari passu with other unsecured unsubordinated debt

Security

Not secured. Company will not permit to have any lien on its property or assets without equally and ratably securing the debt securities

Maturity 15-Aug-2022

Sinking fundAnnually from August 15, 2003, sufficient to redeem $12.5 million principal amount, plus an optional sinking fund of up to $25 million

Callable

At whole or in part on or after August 15, 2002, at the option of the company with at least 30 days, but not more than 60 days notice to each August 14 as follows: schedule inserted here

Moody's rating B

Summary of terms of 8.25% sinking fund debenture 2022 issued by J.C. Penney

24-6

Bond Terminology

Debentures - long-term unsecured issues on debt

Mortgage bonds - long-term secured debt often containing a claim against a specific building or property

Collateral trust bonds - Bonds secured by common stocks or other securities that are owned by the borrower

Equipment trust certificate - Form of secured debt generally used to finance railroad equipment. The trustee retains ownership of the equipment until the debt is repaid.

24-7

Recovery Rates

Ultimate Percentage Recovery Rates on Defaulting Debt (1987 – 2006)

Rec

over

y P

erce

ntag

e

24-8

Bond Terminology

Asset backed securities (ABS) - the sale of cash flows derived directly from a specific set of bundled assets

Mortgage pass through certificates - ABS backed by a package of mortgage pass-throughs

24-9

Bond Terminology

Sinking fund - a fund established to retired debt before maturity

Callable bond - a bond that may be repurchased by a the firm before maturity at a specified call price

Defeasance - a method of retiring corporate debt involving the creation of a trust funded with treasury bonds

24-10

Bond Terminology

Restrictive covenants - Limitations set by bondholders on the actions of the Corporation

Negative Pledge Clause - the processing of giving unsecured debentures equal protection and when assets are mortgaged

Poison Put - a clause that obliges the borrower to repay the bond if a large quantity of stock is bought by single investor, which causes the firms bonds to beat down rated

24-11

Bond Terminology

Pay in kind (PIK) - a bond that makes regular interest payments, but in the early years of the bonds life the issuer can choose to pay interest in the form of either cash or more bonds with an equivalent face value

Puttable bond – A provision that allows the bondholder to demand immediate payment. This is the central feature in loan guarantees issued by the government.

24-12

Straight Bond vs. Callable Bond

24-13

Covenants

Debt ratios:– Senior debt limits senior borrowing– Junior debt limits senior & junior borrowing

Security:– Negative pledge

Dividends Event risk Positive covenants:

– Working capital– Net worth

24-14

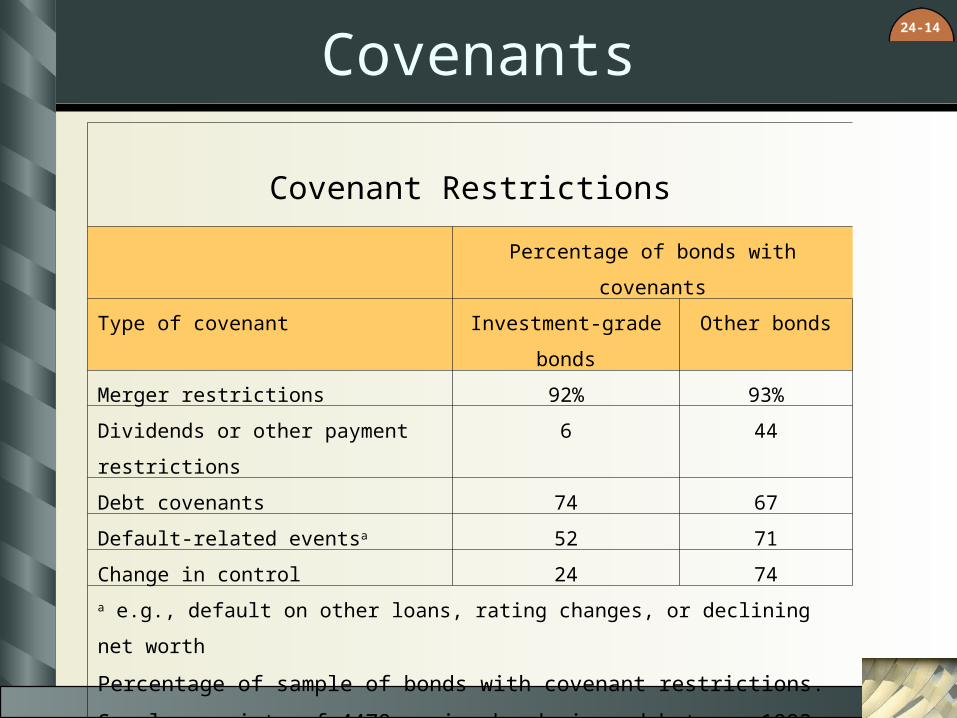

Covenants

Covenant Restrictions

Percentage of bonds with covenants

Type of covenant Investment-grade bonds Other bonds

Merger restrictions 92% 93%

Dividends or other payment restrictions 6 44

Debt covenants 74 67

Default-related eventsa 52 71

Change in control 24 74

a e.g., default on other loans, rating changes, or declining net worth

Percentage of sample of bonds with covenant restrictions. Sample consists of 4478

senior bonds issued between 1993 and 2007. Source: S. Chava, P. Kumar, and A.

Warga, “Managerial Agency and Bond Covenants,” Review of Financial Studies

24-15

Event Risk: An Example

October 1993 Marriott spun off its hotel management business worth 80% of its value.

Before the spin-off, Marriott’s long-term book debt ratio was 2891/3644 = 79%. Almost all the debt remained with the parent (renamed Host Marriott), whose debt ratio therefore rose to 93%.

Marriott’s stock price rose 13.8% and its bond prices declined by up to 30%.

Bondholders sued and Marriott modified its spinoff plan.

24-16

What is a Convertible Bond?

Chiquita Brands– 4.25% Convertible 2016

– Convertible into 44.5524 shares

– Conversion ratio 44.5524

– Conversion price = 1000/44.5524 = $22.45

Lower bound of value – Bond value

– Conversion value = conversion ratio x share price

24-17

Convertible Bond Valuation Issues

Dividends Dilution Changing bond values

24-18

What is a Convertible Bond?

How bond value varies with firm value at maturity

0

1

2

3

0 1 2 3 4 5

Value of firm ($ million)

default

bond repaid in full

Bond value ($ thousands)

24-19

What is a Convertible Bond?

How conversion value at maturity varies with firm value

0

1

2

3

0 0.5 1 1.5 2 2.5 3 3.5 4

Value of firm ($ million)

Conversion value ($ thousands)

24-20

What is a Convertible Bond? How value of convertible at maturity varies with firm value

0

1

2

3

0 1 2 3 4

Value of firm ($ million)

default

bond repaid in full

convert

Value of convertible ($ thousands)

24-21

Bond Warrant Package

Bond and Option– Warrants are usually issued privately– Warrants can be detached– Warrants are exercised for cash– A package of bonds and warrants may be taxed

differently– Warrants may be issued on their own

24-22

Project Finance

1. Project is set up as a separate company.

2. A major proportion of equity is held by project manager or contractor, so provision of finance and management are linked.

3. The company is highly levered.

24-23

Parties In Project Finance

Contractor Supplier(s)

Equity investors

Government Projectcompany

Equity sponsor

Lenders

Purchaser(s)

24-24

Risk Allocation

Risk Shifted to: Contract

Completion/ continuing management

Sponsor Management contract/ completion gtees / working capital maintenance

Construction cost Contractor Turnkey contract/ fixed price/ delay penalties

Raw materials Supplier(s) Long-term contract/ indexed prices/ supply or pay

Revenues Purchaser(s) Long-term contract/ indexed to costs/ take or pay/ throughput agreements/ tolling contract

Concession/regulation Government Concession agreement/ provision of supporting infrastructure

Currency convertibility

Government Gtees or comfort letters/ hard currency paid to offshore escrow account

24-25

Bond Innovations

Liquid yield option notes (LYONS) Puttable, callable, convertible zero coupon debt

Floating-price (death spiral) convertibles

Convertible debt where the bondholder can convert into a fixed value of shares

Asset backed securities Many small loans are packaged together and resold as a bond

Catastrophe (CAT) bonds Payments are reduced in the event of a specific natural disaster

Reverse floaters (yield curve notes)

Floating rate bonds that pay a higher rate of interest when other interest rates fall and a lower rate when other rates rise

Equity linked bonds Payments are linked to the performance of a stock market index

Pay-in-kind bonds (PIKs)

Issuer can choose to make interest payments either in cash or in more bonds with an equivalent face value

Rate sensitive bonds Coupon rate changes as company's credit rating changes

Mortality BondsBonds whoe payments are reduced or eliminated if there is a jump in mortality rates

24-26

Bond Innovations

Motives for creating new bonds

1.Investor choice

2.Government regulation and taxes

3.Reducing agency costs

24-27

Web Resources

Click to access web sitesClick to access web sites

Internet connection requiredInternet connection required

www.investinginbonds.com/

www.hbs.edu/projfinportal