Embed Size (px)

Citation preview

CHAPTER 2 :

EVOLUTION OF CAPITAL MARKETS IN INDIA :

A HISTORICAL REVIEW

2.1 Introduction

This chapter gives an outline of the pace and pattern in the development of capital

market in India. Historically, some milestones, on which the development of stock

exchange is judged, have been presented in the present chapter in a phased manner. In

itself, this chapter is divided into four important phases. The first phase is from the

inception of the capital markets in India upto the First World War i.e.1875-1919. This

phase brings out initial development in the capital market in India. This studies the

inception of the capital market, limitations for the development at the early stage and

the emergence of various stock exchanges in India. The second phase starts from 1920

i.e. the period when industrial revolution had spread over a large part of globe, but

India, under British Empire, remained underdeveloped country. The phase is restricted

upto 1947 when India got independence. It also highlights the glimpses of

development during the volatile period for the market as well as Indian polity. The

third phase starts with 1947 i.e. independence and it is upto 1990 i.e. announcement of

the New Economic Policy. This was the period when the capital market in India has

shown development in real sense. Quantitatively as well as qualitatively, there was a

remarkable development in capital market during this phase. The final phase starts

from 1991 to the present date. Especially after the adoption of Liberalization -

Privatization - Globalization (LPG) policy, there is huge attention of the global

financial markets on Indian capital market. As India still remains a promising country

for the investors and since now foreign investment is permitted in Indian capital

market, lots of developments have taken place since last two decades.

The chapter also emphasizes on some of the developments which have taken place all

over the world during these phases. Briefly, an account of global developments in

financial markets of different /major countries has been provided herewith.

9

2.2 Inception Phase (upto 1919)

The history of capital market in India dates back to almost 200 years. Indian stock

markets are one of the oldest in Asia. In the early nineteenth century, there are some

signs of existence of capital market in India. Though the records are meager, there are

some evidences of presence of capital market during the first half of the nineteenth

century. During those days, the East India Company was in a dominant position. The

business in its loan securities was transacted even at the close of eighteenth century. In

1830’s business on corporate stocks and shares in bank and cotton presses took place

in Mumbai (the then Bombay). There were only 6 brokers recognized by banks and

merchants during 1840 and 1850. Even after trading list was broadened in 1839, there

was no corresponding growth in the turnover of the markets.1

In the decade of 1850’s, there was a rapid development of commercial enterprise and

brokerage business attracted many people in to the field and by the year 1860, the

number of brokers increased to 60.

In 1860-61 American civil war started. Therefore, cotton supply from the US and

Europe was stopped. Thus, the’ share mania’ began in India. The number of brokers

increased to almost 250. However, at the end of American civil war, a disaster again

took place in 1865. This disaster was so hard that, a share of bank of Bombay which

had touched Rs.2850 could be sold at Rs.87. This was true almost for all securities

traded in the market.

At the end of the American civil war, the brokers who had no place to trade, found the

place in the year 1874. This place was a street in Mumbai where the brokers used to

come and negotiate on a piece of paper which later took the form of share certificate.

The place where the brokers assembled and transacted business regularly, is now

known as Dalal Street and the building which is popularly reckoned as a premier stock

exchange, is now known as ‘Jijibhoy Towers’. In 1887, these brokers formally

established the ‘Native Share and Stock Exchange Association’. It was just an

association of persons which was purely informal. It was not given a separate status as

a corporate or business entity. However, in 1895, the stock exchange acquired a

10

premise in the same street and it was formally inaugurated in 1899. Thus, the stock

exchange of Mumbai (now called as BSE) came into existence.

Next to the city of Mumbai, Ahmedabad gained more importance in this regard. The

cotton business which was a prominent business for both of these cities was a common

feature. Especially after 1880, many textile mills started in Ahmedabad, rapidly surged

and expanded their business. As the new mills were floated, the need for stock

exchange was realized and in 1894, the brokers formed the ‘Ahmedabad Share and

Stock Brokers Association’.

During the same time Calcutta was emerging as a centre for jute industry. Apart from

jute, tea and coal industries were the major industries in and around Calcutta city.

From the experiences of ‘share mania’ in Mumbai during 1861-65, there was a boom

in jute shares in 1870’s. This was further followed by a boom in tea shares in the last

two decades of the nineteenth century i.e. from 1880 to 1900. The similar boom was

also experienced in coal business between 1904 and 1908. The leading brokers of

Calcutta then in June 1908 formed the ‘Calcutta Stock Exchange Association.’

In the nineteenth century, industrial revolution too, was taking place in various parts of

the world. India, under British Empire, was not an industrially emerging country. But

then, since Britishers had an industrial revolution (especially in Europe), the raw

material was mostly supplied from the Indian sub continent and thus, slowly India

became a major supplier of raw materials for the European market which was a

developed market.

Due to this reason, indirectly, in the beginning of the twentieth century, the industrial

revolution was on the way in India. At the same time, ‘Swadeshi Movement’ in India

also got the momentum. In 1907, the Tata Iron And Steel Company Limited was

inaugurated (which is now popularly called as (TISCO). This was an important

development in industrial advancement of Indian enterprises. Further, due to the First

World War some of the Indian industries prospered. These industries included cotton

and jute textiles, steel, sugar, paper, flour mills etc. At that time most of the Indian

11

industries which enjoyed prosperity, were providing the raw material for the

industrially developed European market.

2.3 Umbrella growth (1920-1946)

In 1920 the city of Madras (now Chennai) had a first experience of a stock exchange

functioning in the city. The Madras Stock Exchange was formed with 100 members in

1920. But this exchange had a very short life. When the boom came to an end, the

number of members decreased from 100 to meager 3. Finally, in 1923, the Madras

Stock Exchange went out of existence.

In 1935, the stock market activity again improved, especially in south India. In this

part of the country, there was a huge increase in the number of textile mills and many

plantation companies. In 1937, a stock exchange was again instituted in Madras

which was then called as Madras Stock Exchange Association Pvt. Ltd. Later on, the

name of the stock exchange was changed to Madras Stock Exchange Limited.

In 1934, Lahore Stock Exchange was formed but it had a very short life. It was

merged with the Punjab Stock Exchange Limited which was incorporated in the year

1936 at Ludhiana.

The Second World War broke out in 1939. It had some direct as well as indirect

impact on the Indian industries. Initially, due to the world war, there was a sharp

boom. Immediately, it was followed with a sharp decline due to the fear of extending

period of world war and its ill effects on the economy. After 1943, the situation again

changed and by that India was recognized as a supply base.

On account of restrictive controls on cotton, bullion, seeds and other commodities,

those enterprises dealing in these commodities, were found in the stock exchange as it

provided source of finance for their business. They were interested to join the trade

and their number increased sharply. Many new associations were formed for this

purpose. This led to the emergence of stock exchanges being formed in different parts

of the country.

12

Around this time, some more stock exchanges which came into existence were- the

Uttar Pradesh Stock Exchange Limited (1940), Nagpur Stock Exchange Limited

(1940) and Hyderabad Stock Exchange Limited (1944). In Delhi, around this time two

separate stock exchanges were formed viz. ‘Delhi Stock and Share Broker’s

Association Limited’ and the ‘Delhi Stock and Share Exchange Limited’. During the

World War II, these two exchanges were floated.

2.4 Post independence Growth

During the World War II, there was a fear about its adverse effects on the Indian

industries. But in the post world war period there was a fear of depression which

proved to be true. Most of the stock exchanges suffered almost a sharp fall during the

post world war period. At the same time there was a development on political front

that India got independence. After partition, the Lahore stock exchange was shifted to

Delhi and lateron it merged with Delhi Stock Exchange. In 1947, both of the stock

exchanges in Delhi were amalgamated into the ‘Delhi Stock Exchange Association

Limited’.

In southern India, the Bangalore Stock Exchange was registered in 1957 and it was

recognized in 1963. By this time, only few stock exchanges were recognized by the

Central Government. The first act to regulate and recognize the exchanges came into

force in 1956 i.e. Securities Contracts (Regulation) Act, 1956. The established stock

exchanges of Mumbai, Ahmedabad, Calcutta, Madras, Delhi, Hyderabad and Indore

were recognized under the act. The recognition was given on the condition that

members of other associations were required to be admitted by the recognized stock

exchanges on a concessional basis. But as per the principles of unitary control, all the

‘pseudo stock exchanges’ were refused the recognition by the government and hence

these ‘pseudo’ stock exchanges became defunct. Thus, during the early sixties even

through number of exchanges were incorporated, only 8 ‘recognized’ stock exchanges

were left in India. For nearly twenty years thereafter, the number remained

unchanged. Again after that period, in 1980’s, many more stock exchanges were

established. The stock exchanges which were formed in the 1980’s are listed below.

13

Cochin Stock Exchange (1980)- Kochi ,Kerala

Uttar Pradesh Stock Exchange Association Limited (1982)- Kanpur,U.P.

Pune Stock Exchange Limited (1982)- Pune, Maharashtra.

Ludhiana Stock Exchange Association Limited (1983)- Ludhiana, Punjab.

Gauhati Stock Exchange Limited (1984), Guwadhati, Assam

Kannara Stock Exchange Limited (1985) , Manglalore, Karnataka

Magadh Stock Exchanges Association (1986), Patna, Bihar

Jaipur Stock Exchange Limited (1989) , Jaipur, Rajasthan

Bhubaneshwar Stock Exchange Asso. Limited (1989)- Bhubaneshwar, Orissa

Saurashtra Kutch Stock Exchange Limited (1989) , Rajkot, Gujarat

Vadodara Stock Exchange Limited, (1990), Baroda, Gujarat

Coimbatore Stock Exchange Limited (1990), Coimbatore , Tamilnadu

Meerut Stock Exchange Limited (1990), Meerut , U.P

Thus there were 21 recognized stock exchanges upto the year 1990. The stock

exchanges during this period, not only grew in number, but also the number of listed

companies and capital raised by these companies grew considerably. Especially after

1985, there has been a remarkable growth in the stock exchanges due to the favorable

government policies towards the securities markets. The following table shows the

growth of the stock exchanges during this phase i.e.post independence phase.

Table No.2.1: Growth of Stock Exchanges in Post- Independence Phase14

(Year as on 1st January)

Source: Stock Exchange Official Directory, Vol .2 (a) (iii), BSE

2.5 Post Reform Phase (1991 Onwards)

After independence, there was a steady growth in the stock markets in India. After

1985, the number of stock exchanges increased sharply. But after 1991, there was

really a qualitative development in the Indian market. The uses of technology, variety

of products, investor protection are the areas which emerged during the last two

decades. Eventhough there was quantitative increase in the Indian capital market;

there were some inherent limitations like lack of liquidity, imperfections in the

information, lack of transparency, long settlement periods etc. During this time

benami transactions and some frauds also took place in the Indian stock markets. This

affected the small investors to a great extent. The last decade of the twentieth century 15

1947 1962 1972 1981 1991

No. of stock exchanges 7 7 8 9 20

No. of listed companies 1125 1203 1599 2265 6229

No. of stock issues of

listed companies

1506 2111 2838 3697 8967

Capital of listed

companies (Rs.Cr.)

270 753 1812 3973 32041

Market value of capital of

listed companies (Rs. Cr.)

971 1292 2675 6750 110279

Capital per listed company

(Rs. Lakhs)

24 63 113 175 514

Market value of capital

prelisted company (Rs.

Lakhs)

86 107 167 298 1770

Appreciated value of

capital per listed company

(Rs. Lakhs)

358 176 148 170 344

saw the emergence of two important stock exchanges viz. Over The Counter Exchange

of India (OTCEI) and the National Stock Exchange (NSE)

2.5.1 Over The Counter Exchange Of India (OTCEI)

In 1992 , to provide improved services , the country’s first ring less, scrip less and

electronic stock exchange OTCEI was created by some of the prominent financial

institutions like UTI, ICICI, IDBI , SBI Capital Markets, IFCI, GIC, Canbank

Financial Services. The trading at OTCEI is done over the centres across the country.

The securities traded at OTCEI are classified into listed securities, permitted securities

and initiated debentures. The feature of this exchange is that instead of share

certificate, a counter receipt is generated out at the counter which substitutes the share

certificate and the same is used for all transactions.

2.5.2 National Stock Exchange (NSE)

On the basis of recommendations of the Pherwani Committee,2 the National Stock

Exchange was incorporated in 1992. With the advent of liberalization of the economy,

it was necessary to lift the trading system of Indian stock markets at par with the

international standards. The establishment of NSE was one step forward in this

direction. NSE was incorporated by IDBI, ICICI, IFCI, insurance companies and

selected commercial banks. Trading at NSE is of two broad categories viz. ‘Wholesale

Debt Market’ and ‘Cash Market’. Wholesale Debt Market is segment which is similar

to money market while Cash Segment is a place of normal activity of purchase and

sale of securities.

The National Stock Exchange is a pioneer exchange in introducing screen based

trading mechanism. The use of technology and broad based participation are the key

features of NSE. In its short life so far of less than two decades, it has gone past the

many landmarks of the BSE which is a popular stock exchange in India. NSE gains

vital importance in the Indian capital market as it provides much needed

professionalized service and protection to the small investors.

2.5.3 Inter Connected Stock Exchange (ISE)

16

The formation of NSE changed the way in which the stock exchanges were

functioning. Modern infrastructure, technology, transparency and corporate

governance are now becoming the features in the corporate the world. It also forced

BSE to adopt the new technology and with this, NSE and BSE crossed boundaries and

started functioning, operating throughout India. This affected the functioning of small

and regional exchanges.

This led to the birth of the Inter-connected Stock Exchange of India Ltd. (ISE).

Federation of Indian stock exchanges, in a meeting held in 1996,

constituted a steering committee to evolve an interconnected market system. Thus, 14

regional stock exchanges promoted ISE, which was given recognition by SEBI in

1998 and formal trading was started in 1999. ISE was launched with an objective of

converting small, fragmented and illiquid markets into a large, efficient and liquid

market. But there has not been much success to this exchange and the objectives are

still far from being achieved.

2.6 Contemporary Developments in other Countries

Now a days, since the globalization and liberalization, the prices of securities in the

Indian capital market are influenced by the trends given by stock exchanges abroad.

The major stock exchanges abroad and their brief history are presented herewith.

The history of the earliest stock exchange, the France Stock Exchange, may be traced

back to the 12th century, when transactions occurred in commercial bills of exchange.

To control this activity, Philip, the Fair, created the profession of courtier de change,

which was the predecessor of the French stock broker. At the same time in Bruges

(Europe), merchants began gathering in front of the house of the van der Buerse.

Thereafter, the word bourse comes to signify stock exchange.

More roots of the stock exchanges are found in Industrial Revolution which began in

Europe, more than four centuries ago. This was the time when merchants started to

come together to pool their resources and start new venture. The contributions by each

of these contributors (merchants) later on were called as ‘shares’.

17

Initially, trading in shares began as informal hawking, in the streets of London. As

more and more companies started floating their shares to raise capital, there was a

need for a formal market place. These traders, then started to meet at a coffee house,

which was used as market place and finally, the same coffee house was taken over by

them and this was named as a ‘stock exchange’. Thus in 1773 the London Stock

Exchange was founded while the Wall Street traces back its name back to 1653.

Originally, it was set up as defense and not for commerce. Settlers of Dutch descent

who were always on the lookout for attacks by Native Americans and the British, built

a 12 foot ‘stock a defense’. This now has become a center stage of the whole financial

activity of the globe. The wall lasted till 1685 when it was torn down and a new street

was built. This is now called as the ‘Wall Street’.

Thereafter, in 1790 the place was Philadelphia (America) where the first stock

exchange of the US was established. Two years later, the New York merchants met to

discuss how to command on securities business. This was the way in which the New

York Stock Exchange comes into existence.

Some historical evidences have also been recorded which give us an idea about the

early days of capital market in the world.

During 11th century, in Cairo, the Jewish and the Muslim merchants already had the

notion of trade association and had setup various methods of providing long term

credit. This is in contradiction with the call that the history of the stock market

originates with Italy.

In 12th century, in France, the ‘Courtiers’ de change’ were worried about handling and

regulating debts on bank’s behalf. As these men used to deal with long term debt, they

can also be called as originators of the brokerage business in the history of capital

market.

In 13th century, the traders of Bruges commodity accumulated inside the house of a

native named van der Beurse. These people institutionalized their gathering. This

concept spread rapidly all over the Europe. In the places like Amsterdam, Ghent, its

branches (Beurzen) were opened. At the same time, the bankers of Venice started 18

trading in government securities. The government of Venice outlawed airing bruits

which were intentionally used to lessen the price of government funds.

During 14th century, the bankers from Florence, Verona, and Genoa also started

trading in government securities. Dutch’s were the first in the history to inaugurate the

concept of Joint Stock Exchange. This led people to buy share and become

shareholders in the company. In the year 1602, the Dutch East India Company brought

out first shares in the Stock Exchange of Amsterdam. This was the first stock

exchange to bring out bonds and stocks in the capital market. This is also known as the

first stock exchange in the world to inaugurate continuous trade in stocks and bonds.

2.6.1 New York Stock Exchande (NYSE)

NYSE was established more than 200 years back, at the time of signing of

Buttonwood Agreement by 24 New York City brokers and merchants in the year

1792. NYSE still remains the world’s foremost securities market place. The NYSE got

registered as a national securities market with the US Securities and Exchange

Commission in 1934.

Further, in 1971, the exchange was incorporated as a non-profit corporation. The

prices of securities are determined by demand and supply. With the better use of

technology, all the investors are exposed to a wide range of services by the NYSE.

2.6.2 NASDAQ

National Association of Securities Dealers Automated Quotation System (NASDAQ)

is known for its growth, liquidity, depth of the market and the most powerful, forward

looking technologies. Established in 1971, NASDAQ has steadily outpaced the other

major markets to become the fastest growing stock market in the US. NASDAQ is a

screen based market, operating in an efficient, highly competitive electronic trading

environment. The improved transparency and liquidity are the main features of

NASDAQ.

19

2.6.3 London Stock Exchange

The history of the London stock exchange goes back to 1760 when 150 brokers kicked

out of the Royal Exchange for rowdiness, formed a club at Jonathan’s Coffee House to

buy and sell shares. The services provided by the London Stock Exchange are

classified into company services, trading services, information services etc. The

London Stock Exchange is also known for its successful ‘Share Aware Programme’

launched for the benefits of investors.

2.6.4 Frankfurt Stock Exchange (FSE/FWB ) Germany

The FSE has been operated by Frankfurt Wertpapierborsen AG (FWB). In 1992, the

FWB was renamed as the Deutsche Borse (DB) AG. There are 8 independent stock

exchanges in Germany viz. Frankfurt, Dusseldorf, Munich, Hamburg, Berlin ,

Stuttgart, Hanover and Berman. Now, the stock exchanges of Frankfurt, Dusseldorf,

and Munich extended their cooperation in order to establish uniform pricing

mechanism for the DAX 100 securities. In 1997, FSE introduced a new electronic

system, Xetra which is modern cost efficient, order driven trading system with

automated matching.

2.6.5 Tokyo Stock Exchange (Japan)

The history of Japanese stock market dates back to over 130 years with establishment

of Tokyo Stock Exchange in 1878. Initially, like India, Japanese market had a steady

growth. But during the 1980’s there was substantial deregulation and globalization. In

1999, the TSE launched a new market, ‘Mothors’ to foster new companies. Since

March 2000, when the Hiroshima and Niigata exchanges were merged with the TSE,

there are six stock exchanges which are located in Tokyo, Osaka Nagoya, Kyoto,

Fukoka and Sappora . The TSE is continuous auction markets where buy and sell

orders directly interact with one another. The trading is carried out under the “Zarba

Method” which is similar to open outcry system. Upto 1970’s the Japanese markets

were regulated. But in 1996, Japanese Prime Minister proposed Japanese version of

the ‘Big Bang’ to institute significant financial market reforms and that has made TSE

20

competitive with NYSE and LSE by 2001. Locally, this system is called as ‘Kinyu

biggo ban’.

2.6.6 Malaysia

Malaysia is an emerging market in South-East Asia. The Malaysian government, in

2001, announced various measures to encourage the development of capital market of

the country. The government in the year 2000 announced policy framework for

consolidation of the 62 stock broking companies as a follow up to earlier initiatives to

encourage mergers. The objective of this step was to form a group of well capitalized

universal brokers that will not only provide efficient and cost effective services or

investors, but are strong enough to face the challenges posed by globalization. The

said consolidation of the industry was in the nature of flexible and market driven

system.

2.6.7 Sri Lanka

The capital markets in Sri Lanka do not have a large history. In the first decade of the

present century, the Sri Lankan government started trying to develop the capital

market. In order to deepen the market activities, the government proposed to offer

government stocks in hospitality industry, to make attractive gains for the treasury.

The government still is of the opinion that capital markets will be developed by

eliminating tax on capital gains, reducing dividend taxation, facilitating private

pensioners and introducing the new capital market instruments.

2.6.8 Thailand

Thailand has suffered, in the past from disturbances of unbalanced growth of capital

market. In the year 2001, the government announced its commitments for the reforms

in capital markets. The economy of the country depends largely on tourism. In order to

encourage further the tourism industry, the progress has already been made over the

last few years and these efforts are expected to be continued.

2.6.9 Pakistan

21

Since inception, the capital market in Pakistan has been an important resource for

mobilization of savings. The economic policy of Pakistan has an important aim that

the capital market provides profitable opportunities of investment to small savers.

Efficient capital market is needed for industrial development, which is not a common

feature in Pakistan capital markets.

2.7 Overview of Regulation on the Capital Market in India

The first act which was enacted to regulate the Indian companies was the Joint Stock

Companies Act, 1850. British India during this period legalized formation of joint

stock companies with limited liability. Five Indian companies like East India

Company got registered during 1850’s under this act. These companies were the first

companies of which shares were traded for the first time in Indian capital market.

Then, the Government of Bombay introduced of Bill No. XXVII of 1865 to deal with

the situation arising out of the ‘share mania’ of 1860-65. This attempt failed and

subsequently, the Bill was withdrawn in 1867.

In the 20th century, there was a boom in market. This was particularly the post World

War I effect. Lord Lloyd, the then Governor of Bombay, proposed the formation of a

committee of appeal or control. The committee was to consist of one or two members

of the exchange and outsider experts. But the exchange refused this proposal as it

involved outside representatives. This refusal led to the appointment of the Atlay

Stock Exchange Enquiry Committee3 on September 1923. The committee emphasized

the necessity of framing and maintaining a systematic and settled body of rules and

regulations in the interest of the general investing public and of the trade itself. As per

their recommendations, the Government of Bombay offered a charter to the Bombay

Stock Exchange in 1925. But the exchange turned down this step fearing interference

from the outside in the matters of free trade.

2.7.1 The Bombay Securities Contract Control Act, 1925

The Bombay Legislative Assembly passed a special legislation for the first time to

control stock exchanges when the Bombay Securities Contract Act was passed in

22

October, 1925. The act empowered the government to grant or withdraw the

recognition to a stock exchange. It also provided that the rules of recognized stock

exchange could be made/ amended only by prior approval of government. The

Bombay Stock Exchange and Ahmedabad Stock Exchange were recognized under this

act in 1927 and 1939 respectively, along with their rules and regulations. This act

prevailed till 1956 when Securities Contracts (Regulations) Act was passed by the

Central Government in independent India.

2.7.2 Capital Issues (Control) Act 1947

Capital Issues (Control) Act has now only historical relevance as it has been replaced

by Capital Issues (Control) Repeal Act, 1992. But after independence, Capital Issues

(Control) Act 1947 has played an important part in the functioning of the Indian

capital market for almost 45 years. The provisions of this erstwhile act, have now

become the powers of SEBI. The act was administered by Controller of Capital Issues

(CCI) in the Ministry of Finance, Department of Economic Affairs, and Government

of India. The objectives of this act were- to protect the investing public; to regulate

investment in the marker; to ensure sound capital structure in public interest; to ensure

that there is no undue congestion in the market by public issues; to regulate the

volume, terms and conditions of foreign investment in the market. The act had

empowered the Government of India to regulate the timing of new issues and their

pricing.

2.7.3 Securities Contracts (Regulations) Act ,1956

In the year 1954, on official bill was prepared on the lines of the draft recommended

by the Gorwala Committee. After considering such recommendations, Government of

India decided to pass, enact an act to regulate and control activities of the stock

exchange. The then Finance Minister, Mr. C.D. Deshmukh urged and explained in the

Parliament about the importance of capital market. It was concluded while enacting/

passing the bill in the Parliament that it was absolutely necessary that there should be

an all India legislation to regulate and control the activities of stock exchanges all over

23

the country. A well regulated market, on which investors can safely rely, will

encourage transformation of saving into investment in the country.

2.7.4 The Companies Act , 1956

The financial as well as non-financial aspects of the working of all the companies in

India are governed by the Companies Act, 1956. It aimed at developing an integrated

relationship between promoters, investors and company management. Right from the

formation to the liquidation of company, all the activities are governed and regulated

by the Companies Act, 1956. As far as the financial aspects and capital raising is

concerned, following are some of the matters specially enacted under the act- issue of

capital, capital structure of company, dividend distribution, inter corporate

investments, allotment of shares, etc. The companies act is administered by

Department of Company Affairs and the Company Law Board of the Ministry of Law

, Justice and Company Affairs of the Central Government.

2.7.5 SEBI Act, 1992

As a part of the process of globalization, reforms were inevitable in the Indian

financial system as it was vulnerable to external shocks after liberalization,

privatization, and globalization introduced in the system. In the last decade there was a

need to have an independent body as a vigilant regulatory authority.

Certain powers under certain sections of Securities Contract (Regulation) Act and

Companies Act have now been delegated to the SEBI. The SEBI has its head office in

Mumbai and the organization is under the overall control of the Ministry of Finance,

Central Government. SEBI Act was enacted to avoid the problem of multiple

regulatory bodies. In multiple regulatory structures, there is overlapping of functions

which may cause confusion among the participants of the market. Hence, inception of

SEBI gave way for a single, highly visible and independent organization, backed by a

statute. Primary objective of SEBI Act is to protect the interest of the investor in

securities and to promote the development of and to regulate the securities market. It

also aims at facilitating an efficient mobilization and allocation of resources through

the securities markets.24

SEBI, as regulator has come up with several regulations like -

SEBI (insider Trading) Regulations, 1992;

SEBI (Underwriters) Regulations, 1993;

SEBI (Portfolio Manager) Regulations, 1993;

SEBI (Foreign Institutional Investors) Regulations, 1995;

SEBI (Mutual Funds) Regulations, 1996;

SEBI (Credit Rating Agencies) Regulations, 1999;

SEBI (Issue of Sweat Equity) Regulations, 2002, etc.

2.7.6 Depositories Act, 1996

With the advent of new technology and need for faster settlement, there was a need to

regulate matters in the capital market which arise due to technology adoption. The

Depositories Act provides for the establishment of depositories in securities with the

objective of ensuring free transferability of securities with speed, accuracy and

security. For this purpose, the provisions have been announced for making securities

of public limited companies freely transferable, dematerialization of the securities,

maintaining ownership records in a book entry form. The Act has provided electronic

transfer of securities in the Indian capital market.

2.7.7 RBI ACT (Provisions for NBFCs)

RBI Act, 1934 governs and regulates the entire banking system in India. Though RBI

Act does not directly control or regulate capital markets in India, some of the players

which are participants in the market, are governed by the RBI Act. Non-banking

Financial Corporations in the 1990s had some unethical elements. These NBFCs were

using their surplus and assets in the capital markets. The RBI has initiated adverse

action against such errant NBFCs for various defaults and contraventions of provisions

of RBI Act. Such adverse actions even included prohibition from accepting deposits

and also launching some criminal proceedings against such defaulters.

25

The regulations of the capital markets in India are done through the acts like Securities

Contract (Regulation) Act, SEBI Act and Depositories Act which is monitored by the

Dept. of Company Affairs of the Union Government. Hence all the acts are for the

smooth functioning of the market, but overall control on all the corporate activities is

of the Central Government.

2.8 Evolution of Trading Mechanism in the Capital Market.

There has been huge change in the trading mechanism in the Indian capital market

over the last two decades especially after adoption of the LPG policy. After the

establishment of NSE, the drastic change has taken place in the trading mechanism in

the markets. The uses of technology, faster settlement, variety of instruments are some

of the glimpses which confirm the development of capital market. This move by NSE

has even forced BSE to also enter into the electronic trading mechanism. The

evolution of trading mechanism right from inception till today is presented briefly

herewith.

2.8.1 Types/ Components of the Capital Market

The capital markets are broadly classified into debt and equity markets. Debt markets

are characterized by large institutional involvement with less presence of retail

participation. Debt markets trade in government securities, treasury bills, corporate

bonds, other debt instruments while equity markets deal mainly in equity shares and to

a limited extent in preference shares and company debentures. Recently, futures and

options in indices and equity shares have also become a part of the market.

In the context of equity product, the markets are classified into-

Primary market and Secondary market. Of late, derivatives market has also become a

part of the broader market.

26

In the capital markets, there is large number of participants with variety of products.

The various components of capital market are as follows:-

• Securities :- the term securities include shares, bonds, debentures,

futures, options, mutual funds units

• Intermediaries – intermediaries include brokers, sub-brokers,

custodians, share transfer agents, merchant bankers, and depositories.

• Issuers of securities – companies, body corporate, banks, government,

financial institutions, mutual funds

• Investors – investors include individuals, companies, mutual funds,

financial institutions, foreign institutional investors

• Market regulators – The regulators in the capital markets are SEBI,

RBI (to some extent), Department of Company Affairs, and

Department of Economic Affairs of the Central government.

2.8.2 Market Segments

The entire capital market has two major segments viz. Primary (i.e. new issue) market

and Secondary (i.e. stock) market. The primary market provides the channel for

creation and sale of new securities, while the secondary market deals with those

securities which have been previously issued. The resources are mobilized through

primary market by way of public issue or rights issue or private placement. In public

issue, the shares are to be issued to anybody who subscribes them. In rights issues,

only existing shareholders are eligible to subscribe to share capital, while in private

placement the company identifies few big subscribers to whom the shares can be

issued to raise the capital.

27

The secondary market enables the participants to adjust their holdings in response to

the changes in risk and return.

The securities issued in primary market, are traded in the secondary market. The

secondary market operates through two mediums viz. Over The Counter (OTC) and

Exchange Traded Market. OTC markets are informal markets where trades are

negotiated. Most of the trades in the government securities are in the OTC market. All

the spot trades where securities are traded for immediate delivery and payment, take

place in OTC market. The other option is trade using infrastructure provided by the

stock exchange. There are 19 stock exchanges in India and all of them follow a

systematic settlement period. All the trades taking place over a trading cycle are

settled together after certain time. Now there is T+2 i.e. the securities transactions are

to be settled within two working days of the transaction. Earlier, this settlement cycle

could end till 15 days when we had T+15. The trades are cleared and settled through

clearing corporation which acts as a counter party and guarantee settlement. Now

nearly 100% of the trades in the capital market segment are settled through demat

delivery. A wide range of debt securities, government securities are also traded in a

platform provided by the stock exchange. A part of the secondary market is the

forward market where the securities are traded for further delivery and payment. A

part of the forward market is Futures and Options (F & O) market. Presently, only

NSE and BSE provide trading in F & O.

2.8.3 Evolution of Trading Mechanism

The advent of technology has made the trading in the capital market much simpler and

faster than what it was earlier. In the initial stages, the trading in the capital market

was restricted to a few players. Later on, gradually, the number of participants

increased with increasing importance of the market for the nation.

But to start with, trading on stock exchanges in India used to take place through open

outcry without the use of any kind of technology. There was no immediate matching

of orders or records of trades. The trading was time consuming and inefficient. The

practice of physical trading imposed limits on trading volumes. A person who

28

intended to trade in securities, had to physically go at the exchange or had to send an

agent/ broker on his behalf to perform the transaction. Since there was no order

matching immediately, one had to wait for similar counter order from the other party.

In the floor of a stock exchanges, intending trader had to make gestures, had to shout

and in this way, he could find the counter party. Hence, initially the stock exchange

was like any other “bazar’.

NSE for the first time in India, introduced screen- based trading system. Where a

member can punch into the computer the quantities of the shares and the prices at

which he wants to transact. The transaction is executed as soon as the quote punched

by a trading member finds a matching sale or buy quote from the counter party. In this

system, orders are automatically matched. It helps to cut down time, cost and error as

well as chances of fraud. Screen based trading enables the parties/ traders from a

distant place to trade with each other. This helps to solve the problem of liquidity in

the markets. The high speed with which the transactions are executed and the large

number of participants, who trade simultaneously, allows faster incorporation of

price–sensitive information into prevailing prices. This increases information

efficiency of the markets. It becomes possible for all the participants to see the full

market which helps market to be more transparent and this leads to increase in

investors’ confidence.

This advancement, led by NSE forced BSE as well as other stock exchanges to

introduce screen based trading system. In this wake, most of the regional exchanges

lost their business to NSE. Prior to setting up of NSE, trading on stock exchanges in

India took place without the use of information technology. The trading volumes and

speed were also low. The information –inefficiency gave way to unscrupulous traders

to manipulate the market. This practice “Gala”- of extracting high price of the day for

‘buy’ and low price of the day for ‘sale’ irrespective of exact trading price , was

prevailing in the market.

Under this system, client does not have any method of verifying the actual price. The

electronic order matching has made such manipulation difficult. This has improved

liquidity in the markets. The NSE has its own satellite which helps match the order 29

electronically within a fraction of a second. The NSE has setup a clearing corporation

to provide legal counter party guarantee to each trade thereby eliminating counter

party risk. The National Securities Clearing Corporation Limited (NSCCL)

commenced operations in 1996. Counter party risk is guaranteed through risk

management system an innovative method of online position monitoring and

automatic disablement. In capital market segment now, principle of ‘novation’ has

been applied which means NSCCL is the counter party for every transaction and

therefore, default risk is minimized. To support the assured settlement, a ‘Settlement

Guarantee Fund’ has been created. A large Settlement Guarantee Fund provides a

cushion for any residual risk. As a consequence, despite the fact that daily traded

volume of the NSE run into thousands of crores of rupees, credit risk no longer poses

any problem in the market place. In this system of trading, the depositories also play

an important role. The depositories provide electronic maintenance and transfer of

ownership of dematerialized securities. SEBI administers the rules and regulations for

this system.

The physical movement of paper required a huge time for settlement and it was also a

risky proposition. But now the use of technology has forced to involve the mechanism

for faster settlement. Thus, two depositors NSDL and CDSL work as intermediaries

for faster settlement. Through depositories, the demat accounts are operated and

nowadays more than 99% of turnover of the capital market, is settled in demat form.

This eliminates bad deliveries and associated problems.

30

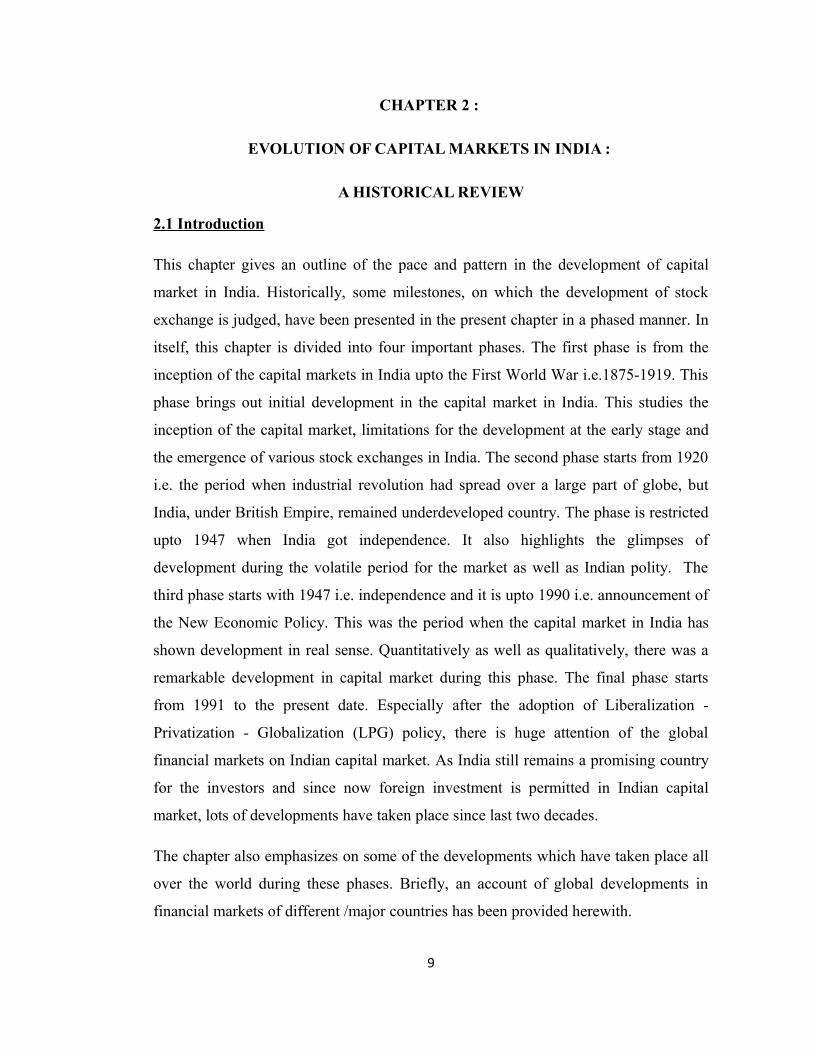

Figure 2.1 Stock Exchanges in India

31

Source: www.mapsofindia.com

32

33

34

1 www.yeahindia.com/c-india1.htm pp.2, 24.09.2003

2Desai Vasant,- “The Indian Financial System and Development”, Himalaya Publishing House, Mumbai,, First Edition, 2005, pp.332-33

3Somaiyya Kirit,- “Scientific Management of Small investors Protection in the New Millennium with reference to India : Challenges and Opportunities (1991-2011)”, Ph.D. Thesis, University of Mumbai, 2005, pp.69

Figure 2.2Institutional Structure of Capital Market in India (Market Players)**

Marketable Securities Non Marketable Securities

Govt. Corporate PSU Mutual Bank Corporate Loans & Post office Securities Securities Bonds Funds Deposits Deposits Advances by Certificate

Banks/FIs and Deposits

Primary market(new Issue market)

Secondary market(Existing securities)

Stock exchanges

Non issuing players

Merchant bankers Collecting bankers

R and T AgentsBrokers

UnderwritersAdvertising Agencies

PrintersSubbrokersSolicitors

Sub-underwriters Mailing agents

BrokersJobbersDealers

Bodla financiersArbitrageurs

Investment advisorsPortfolio managers

Sub-brokersFloor brokers

Promoters and directorsAssociaters and subsidiaries

CollaboratorsEmployees

Financial institutionsBank

Mutural fundsNRIS

Public

Source: The Indian Financial System and Development Vasant Desai, Himalaya Publishing House, Mumbai 1st Edition, 2005, pp. 183

33

Figure 2.3Institutional Structure of Capital Market in India

Demand for capital Supply of capital

Govt. Local Authorities Joint Stock companies Stock Exchange Capital Underwriters

Central State Port Municipal Trusts Trusts Corporation Brokers

Individual Agents Banks Provident Special Investor Funds FI Investment Trusts

Shareholders P.F. Govt. Shareholders and Contributor RBIDepositors WB

SCB

Source: The Institutional Structure of Capital Market in India – K.S. Sharma, Writers and Publishers Corporation, New Delhi, 1st Edition, 1969, p.17.

34