Embed Size (px)

DESCRIPTION

CHAPTER 18. Cost Behavior & Cost-Volume-Profit Analysis. Cost Behavior. In planning, we must understand how costs behave. For example, do costs change as production activity changes or do they stay the same? - PowerPoint PPT Presentation

Citation preview

CHAPTER 18

Cost Behavior & Cost-Volume-Profit Analysis

Cost Behavior• In planning, we must understand

how costs behave. • For example, do costs change as

production activity changes or do they stay the same?

__________– costs that increase as production activity increases (direct materials, direct labor)

__________– costs that stay the same over a range of activity levels (depreciation, rent) within a given time period.

Variable Costs

Total Variable Cost GraphTo

tal C

osts

$300,000$250,000$200,000$150,000$100,000 $50,000

10 20 300

Unit Variable Cost Graph$20$15$10

$50C

ost p

er U

nit

10 20 30

5,000 $ 50,000 $10 10,000 100,000 10 15,000 150,000 10 20,000 200,000 10 25,000 250,000 10 30,000 300,000 10

Units Total CostProduced Cost per Unit

Units Produced (000)

Units Produced (000)

Fixed Costs

Total Fixed Cost GraphTo

tal C

osts

0

Unit Fixed Cost Graph

Cos

t per

Uni

t

50,000 $75,000 $1.500 100,000 75,000 .750 150,000 75,000 .500 200,000 75,000 .375 250,000 75,000 .300 300,000 75,000 .250

Units Total CostProduced Cost per Unit

$150,000$125,000$100,000$75,000$50,000

$25,000100 200 300

$1.50$1.25$1.00$.75$.50

$.25100 200 3000

Units Produced (000) Units Produced (000)

Relevant Range• Cost relationships remain stable only

over some range of production activity.

• Outside that range the relationships may change.

• __________is the expected range of activity we are interested in. We estimate the cost relationships within

that range. We cannot extrapolate outside the range.

Cost Behavior• __________Costs

include both fixed and variable costs; we separate fixed from variable costs when perform cost-volume profit analysis.

• __________ Costs fixed within a relevant range, but if total

production increases significantly, total costs increase by a lump sum amount

• __________ Costs increase at a non-constant rate as volume

increases.

Mixed Costs• Some costs have a _______ component

and a __________ component.• We can separate mixed costs into the

two components using the ________________.

FC

$

activity

Total costs

Slope = VC/unitEquation of line : y = a + bx

Mixed Costs

Total Mixed Cost GraphTo

tal C

osts

0

Total Machine Hours (000)

$40,000$35,000$30,000$25,000$20,000$15,000$10,000 $5,000

10 20 30 40

Mixed costs are usually separated into their fixed and variable components for management analysis.

Mixed costs are sometimes called semivariable or semifixed costs.

The objective is to classifyall costs as either fixed or variable.

Identifying and MeasuringCost Behavior

Measuring Cost Behavior: Scatter Diagram …

• A __________of past cost behavior may be helpful in analyzing mixed costs.Draw a line through the plotted data points so that about

equal numbers of points fall above and below the line.

Estimated fixed cost = 10,000

0 1 2 3 4

*

Tota

l Cos

t in

1,00

0’s

of D

olla

rs

10

20

0

***

**

* **

*

Activity, 1,000s of Units Produced

Measuring Cost Behavior: Scatter Diagram …

Variable Cost unit = Slope =

Δin costΔin units

0 1 2 3 4

*

Tota

l Cos

t in

1,00

0’s

of D

olla

rs

10

20

0

***

**

* **

*

Activity, 1,000s of Units Produced

Horizontal distance is the change in activity.

Vertical distance

is the change in cost.

Measuring Cost BehaviorHigh/Low Method

• Determine the __________ by finding the slope change in ____ ÷ change in _____ (see prev. slide)

• Determine the __________ component Using the high (or the low) point, plug in

the cost (y), the activity (x), and the slope (VC/unit).

Solve for the y- intercept.• Given the equation of the cost line, we

can now use it to predict cost over some range of activity.

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production TotalUnits Cost

Highest level Lowest level Difference

Production TotalUnits Cost

Highest and lowest levels

Mixed Costs: High-Low Method

Actual costs incurred Production Total

Units CostHighest level 2,100 $61,500Lowest level Difference

Production TotalUnits Cost

Highest and lowest levels

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Mixed Costs: High-Low Method

Actual costs incurred Production Total

Units CostHighest level 2,100 $61,500Lowest level 750 41,250Difference

Production TotalUnits Cost

Highest and lowest levels

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Mixed Costs: High-Low Method

Actual costs incurred Production Total

Units Cost

Variable costper unit

Difference in total costDifference in production

=

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Production TotalUnits Cost

Highest and lowest levels

1

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production Total Units Cost

Variable costper unit

Difference in total costDifference in production

$20,2501,350 units

= = =

Production TotalUnits Cost

Highest and lowest levels

1 $15

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production Total Units Cost

Variable costper unit

Difference in total costDifference in production

$20,2501,350 units

$15= = =

Totalcost

= –Fixedcost

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Production TotalUnits Cost

Highest and lowest levels

Variable costper unit

x Units ofproduction

1

2

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production Total Units Cost

Variable costper unit

Difference in total costDifference in production

$20,2501,350 units

$15= = =

Totalcost

= –Fixedcost

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Production TotalUnits Cost

Highest and lowest levels

Variable costper unit

x Units ofproduction

Highest level: $61,500= – ( $15 x 2,100 ) = $30,000

1

2

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production Total Units Cost

Variable costper unit

Difference in total costDifference in production

$20,2501,350 units

$15= = =

Totalcost

= –Fixedcost

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Production TotalUnits Cost

Highest and lowest levels

Variable costper unit

x Units ofproduction

Highest level: $61,500= – ( $15 x 2,100 ) = $30,000Lowest level: $41,250= – ( $15 x 750 ) = $30,000

1

2

Mixed Costs: High-Low Method

Actual costs incurred

June 1,000 $45,550July 1,500 52,000August 2,100 61,500September 1,800 57,500October 750 41,250

Production Total Units Cost

Variable costper unit

Difference in total costDifference in production

$20,2501,350 units

$15= = =

Totalcost

= –Fixedcost

Highest level 2,100 $61,500Lowest level 750 41,250Difference 1,350 $20,250

Production TotalUnits Cost

Highest and lowest levels

Variable costper unit

x Units ofproduction

Highest level: $61,500= – ( $15 x 2,100 ) = $30,000

Lowest level: $41,250= – ( $15 x 750 ) = $30,000

1

2

Cost-Volume-Profit & Breakeven Analysis

• Given our fixed and variable costs, we can use CVP techniques to help predict our profit at various activity levels.

• We define __________= Sales – VC __________= SP/unit – VC/unit __________= CM/SP

Related Questions• We can use this set of techniques to

answer the following types of questions. How many units do we need to sell to

break even? How much profit will we generate at a

given level of sales? If we want to earn a target profit, how

many units do we need to sell? If we change our sales price, what

happens to our profitability?

Contribution margin is amount by which revenue exceeds the variable costs of producing the revenue.

Total UnitSales Revenue (2,000 units) 200,000$ 100$ Less: Variable costs 140,000 70 Contribution margin 60,000$ 30$ Less: Fixed costs 24,000 Net income 36,000$

Computing Break-Even Point

Total UnitSales Revenue (2,000 units) 200,000$ 100$ Less: Variable costs 140,000 70 Contribution margin 60,000$ 30$ Less: Fixed costs 24,000 Net income 36,000$

How much contribution margin must this company have to cover its fixed costs (break even)?

Answer: $24,000

P2 Computing Break-Even Point

How many units must this company sell to cover its fixed costs (i.e. to break even)?

Total UnitSales Revenue (2,000 units) 200,000$ 100$ Less: Variable costs 140,000 70 Contribution margin 60,000$ 30$ Less: Fixed costs 24,000 Net income 36,000$

Answer: $24,000 ÷ $30 per unit = 800 units

P2 Computing Break-Even Point

Breakeven Sales• Sales = VC + FC + profit or• Profit = Sales – VC – FC• At breakeven, profit = 0

0 = (Sales – VC) – FC 0 = CM - FC CM = FC or (CM/unit)(units) = FC And Breakeven Units = FC/(CM/unit) Or Breakeven in $ = FC/(CM ratio)

Target Net Income• You can use the CVP idea to

determine how much we can sell to earn a desired profit. Profit = Sales – VC – FC Profit + FC = Sales – VC = CM =

CM/unit(units) Target Salesunits = (FC + Profit) /

CM/unit Target Sales$ = (FC + Profit) / CM

ratio

• __________is the amount by which sales can drop before the company incurs a loss.

• Margin of safety may be expressed as a percentage of expected sales.

Margin of SafetyExh. 22-17

Margin of safety Expected sales - Break-even sales percentage Expected sales

=

C3

Breakeven for Multiple Products

• BEunits = FC/(CMcomposite), where

• CMcomposite = [(%A)CMA + (%B) CMB]

The number of units that we get will be a combined unit of A and B together.

You then have to determine the number of A and B each that are actually sold.

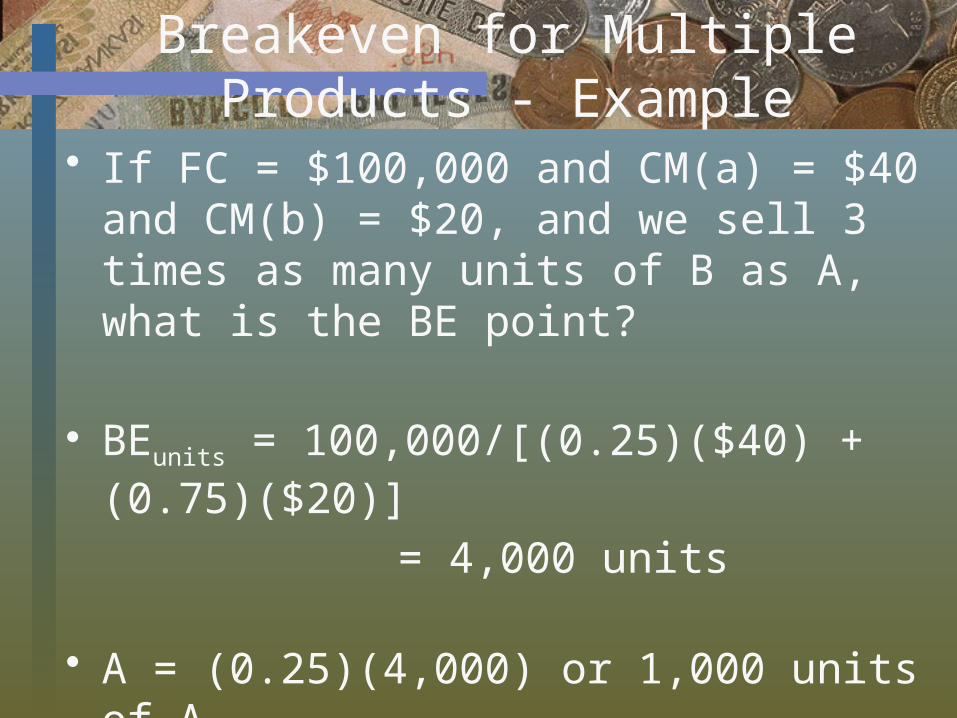

Breakeven for Multiple Products - Example

• If FC = $100,000 and CM(a) = $40 and CM(b) = $20, and we sell 3 times as many units of B as A, what is the BE point?

• BEunits = 100,000/[(0.25)($40) + (0.75)($20)]

= 4,000 units

• A = (0.25)(4,000) or 1,000 units of A • B = (0.75)(4,000) or 3,000 units of B

A measure of the extent to which fixed costs are being used in an organization.

A measure of how a percentage change in sales will affect profits.

Contribution margin Net income

Degree of ____________________=

Operating Leverage

Contribution Margin Reporting

• We can recast the income statement to highlight the contribution margin.

• Sales• - VC• = CM• - FC• = operating income

For Internal Reporting purposes only

The End!!Now, let’s look at the quick studies!