Embed Size (px)

Citation preview

CHAPTERCHAPTER

1717

INVESTMENTSINVESTMENTS

• In accounting for investments, entries are required to record the:

– Acquisition – Interest/dividends– Disposal

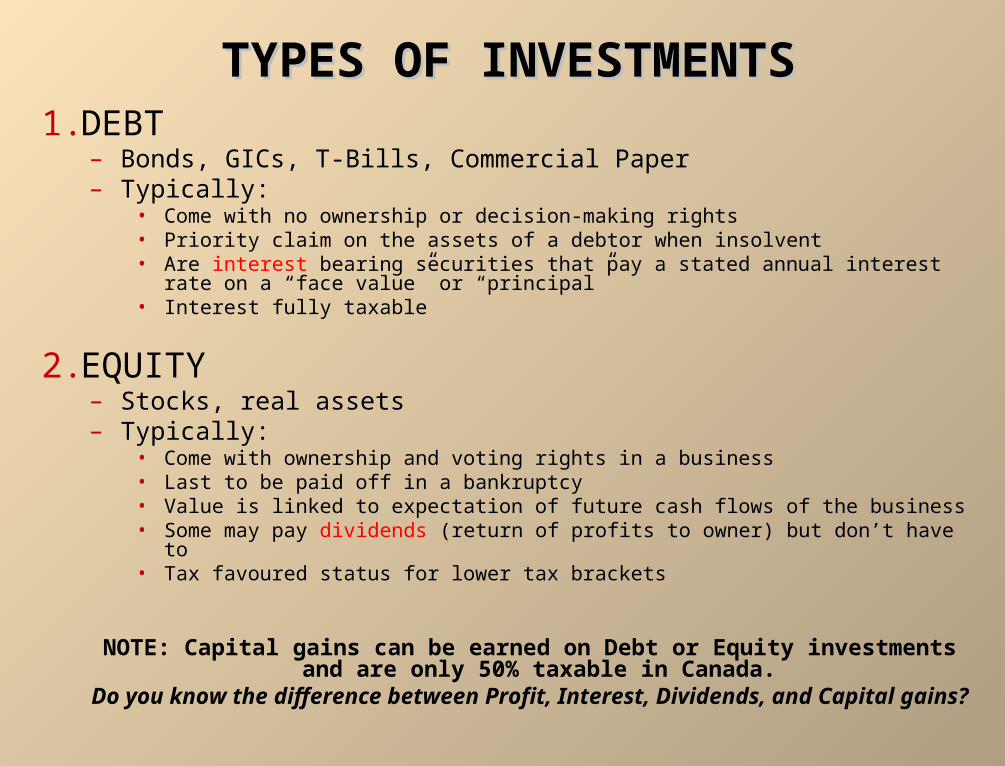

TYPES OF INVESTMENTSTYPES OF INVESTMENTS1. DEBT

– Bonds, GICs, T-Bills, Commercial Paper– Typically:

• Come with no ownership or decision-making rights• Priority claim on the assets of a debtor when insolvent• Are interest bearing securities that pay a stated annual interest rate on a “face value” or

“principal”• Interest fully taxable

2. EQUITY– Stocks, real assets– Typically:

• Come with ownership and voting rights in a business• Last to be paid off in a bankruptcy• Value is linked to expectation of future cash flows of the business• Some may pay dividends (return of profits to owner) but don’t have to• Tax favoured status for lower tax brackets

NOTE: Capital gains can be earned on Debt or Equity investments and are only 50% taxable in Canada.

Do you know the difference between Profit, Interest, Dividends, and Capital gains?

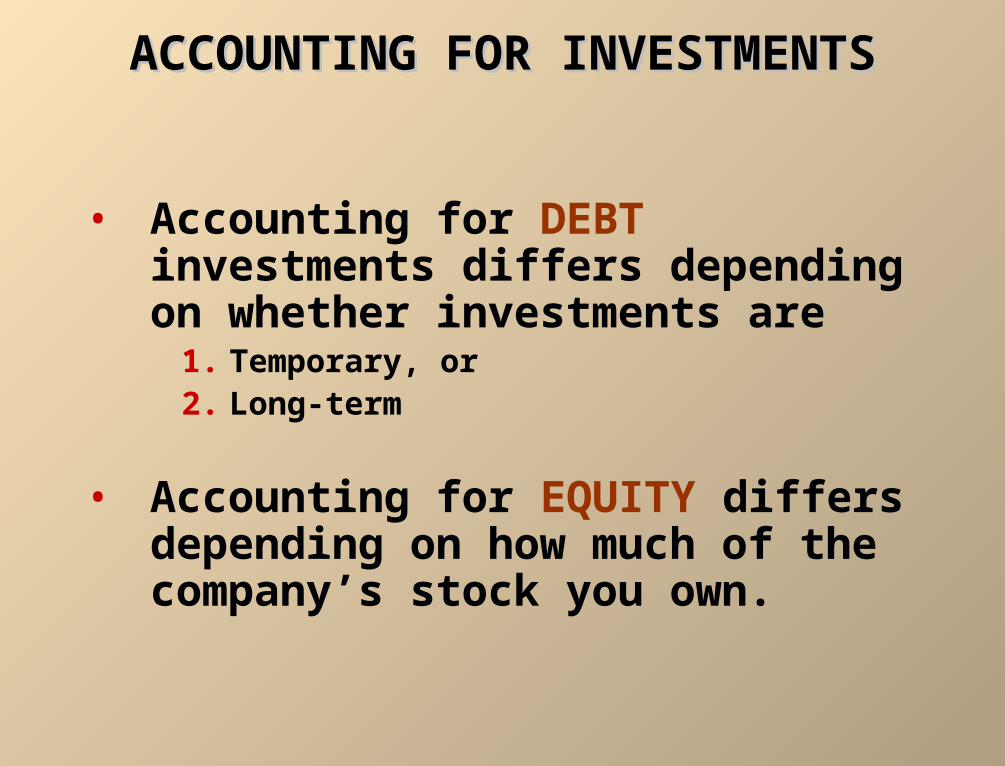

ACCOUNTING FOR INVESTMENTSACCOUNTING FOR INVESTMENTS

• Accounting for DEBT investments differs depending on whether investments are

1. Temporary, or2. Long-term

• Accounting for EQUITY differs depending on how much of the company’s stock you own.

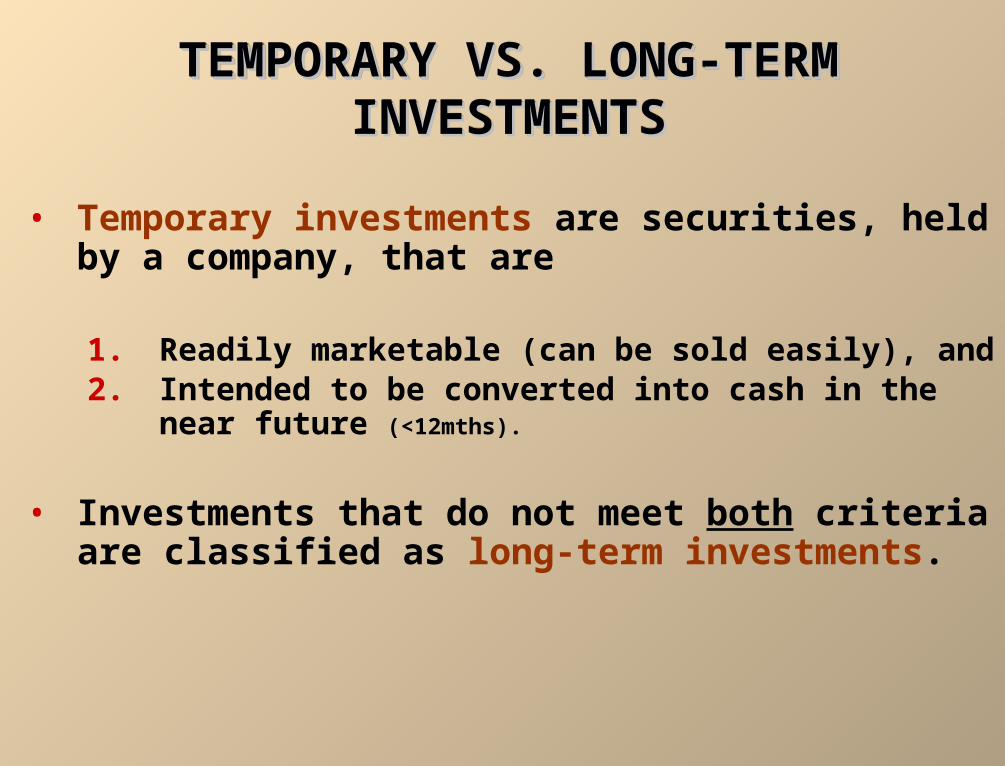

TEMPORARY VS. LONG-TERM TEMPORARY VS. LONG-TERM INVESTMENTSINVESTMENTS

TEMPORARY VS. LONG-TERM TEMPORARY VS. LONG-TERM INVESTMENTSINVESTMENTS

• Temporary investments are securities, held by a company, that are

1. Readily marketable (can be sold easily), and2. Intended to be converted into cash in the near

future (<12mths).

• Investments that do not meet both criteria are classified as long-term investments.

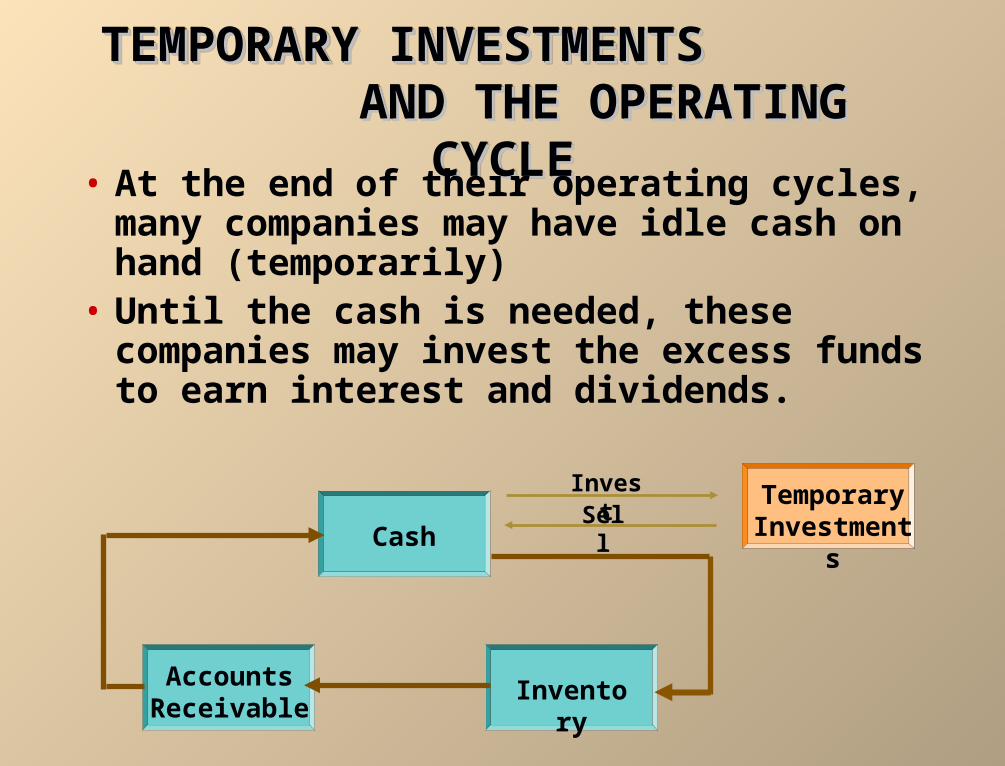

TEMPORARY INVESTMENTS TEMPORARY INVESTMENTS AND THE OPERATING CYCLE AND THE OPERATING CYCLE

TEMPORARY INVESTMENTS TEMPORARY INVESTMENTS AND THE OPERATING CYCLE AND THE OPERATING CYCLE

• At the end of their operating cycles, many companies may have idle cash on hand (temporarily)

• Until the cash is needed, these companies may invest the excess funds to earn interest and dividends.

Cash

Temporary Investments

Accounts Receivable

Inventory

InvestSell

TEMPORARY INVESTMENTS TEMPORARY INVESTMENTS AND THE OPERATING CYCLE AND THE OPERATING CYCLE

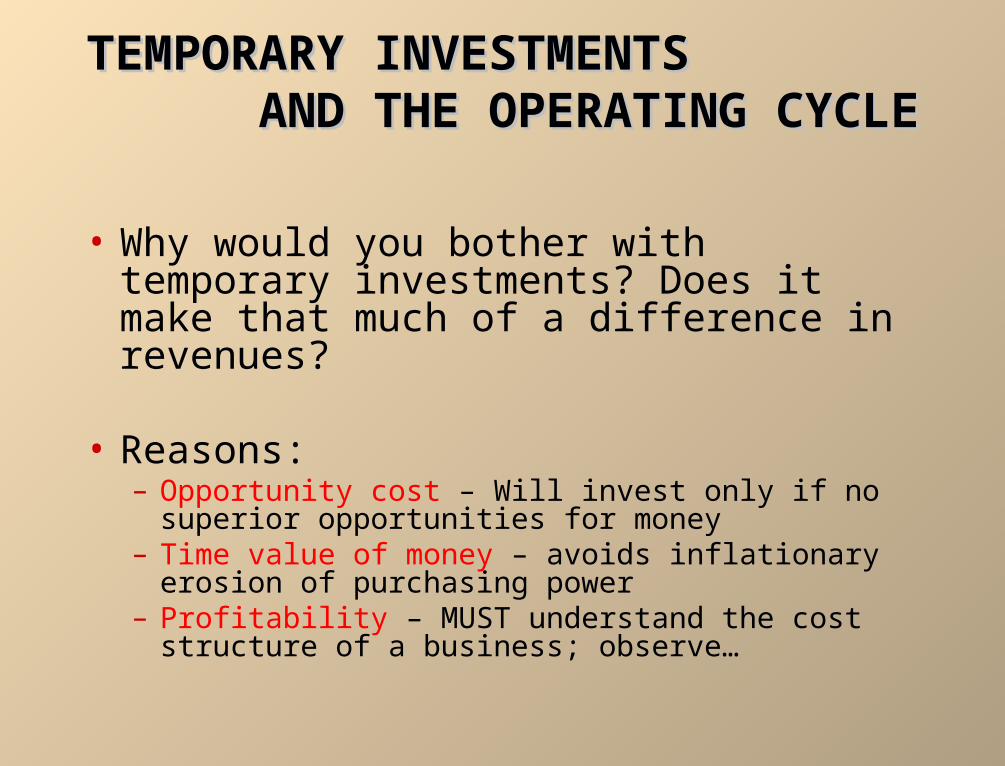

• Why would you bother with temporary investments? Does it make that much of a difference in revenues?

• Reasons:– Opportunity cost – Will invest only if no superior

opportunities for money– Time value of money – avoids inflationary erosion of

purchasing power– Profitability – MUST understand the cost structure of a

business; observe…

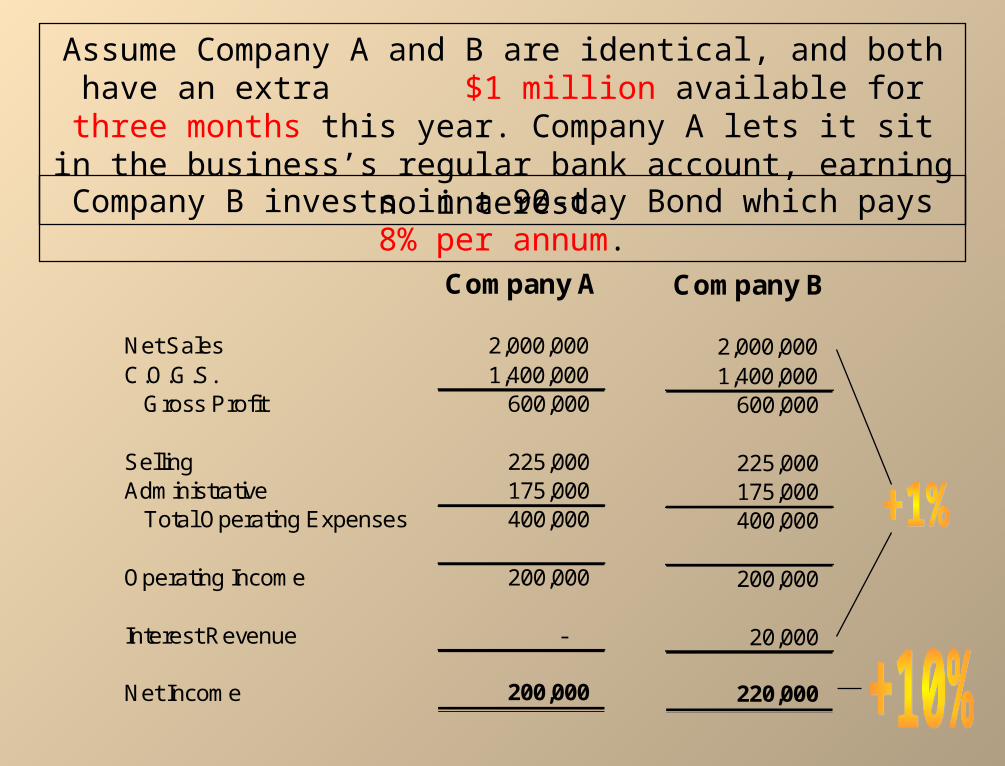

Company A

Net Sales 2,000,000 C.O.G.S. 1,400,000

Gross Profit 600,000

Selling 225,000 Administrative 175,000

Total Operating Expenses 400,000

Operating Income 200,000

Interest Revenue -

Net Income 200,000

Assume Company A and B are identical, and both have an extra $1 million available for three months this year. Company A lets it sit

in the business’s regular bank account, earning no interest.

Company B invests in a 90-day Bond which pays 8% per annum.

Company B

2,000,000 1,400,000

600,000

225,000 175,000 400,000

200,000

20,000

220,000

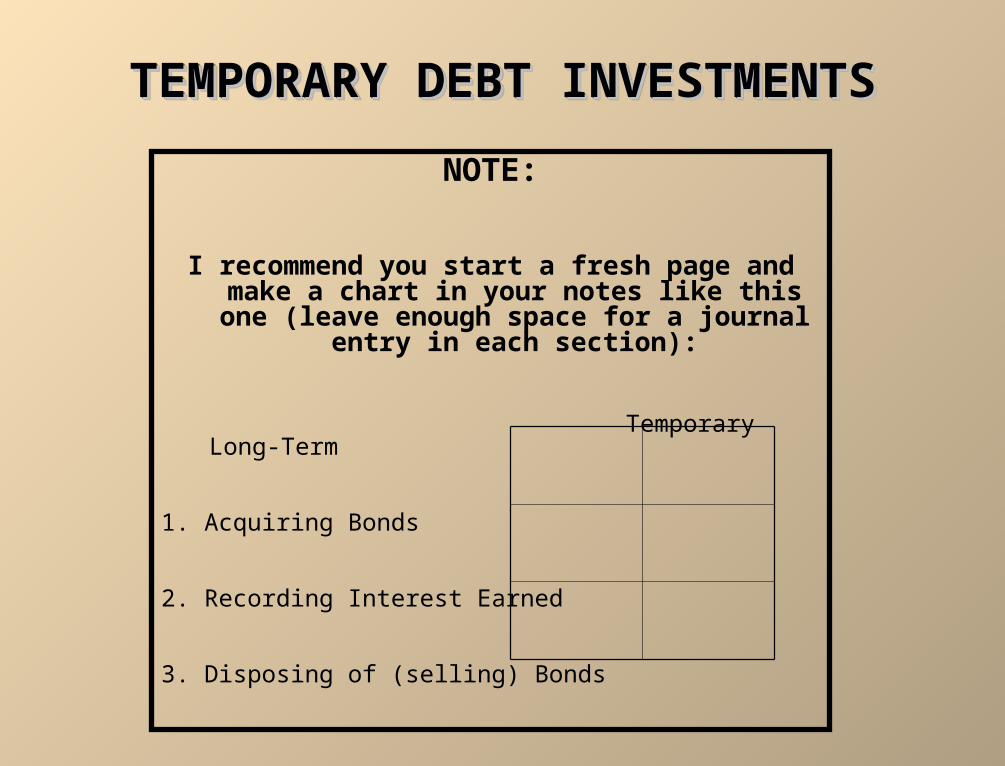

TEMPORARY DEBT INVESTMENTSTEMPORARY DEBT INVESTMENTSTEMPORARY DEBT INVESTMENTSTEMPORARY DEBT INVESTMENTS

NOTE:

I recommend you start a fresh page and make a chart in your notes like this one (leave enough space for a

journal entry in each section):

Temporary Long-Term

1. Acquiring Bonds

2. Recording Interest Earned

3. Disposing of (selling) Bonds

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

1. Acquisition1. Acquisition

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

1. Acquisition1. Acquisition

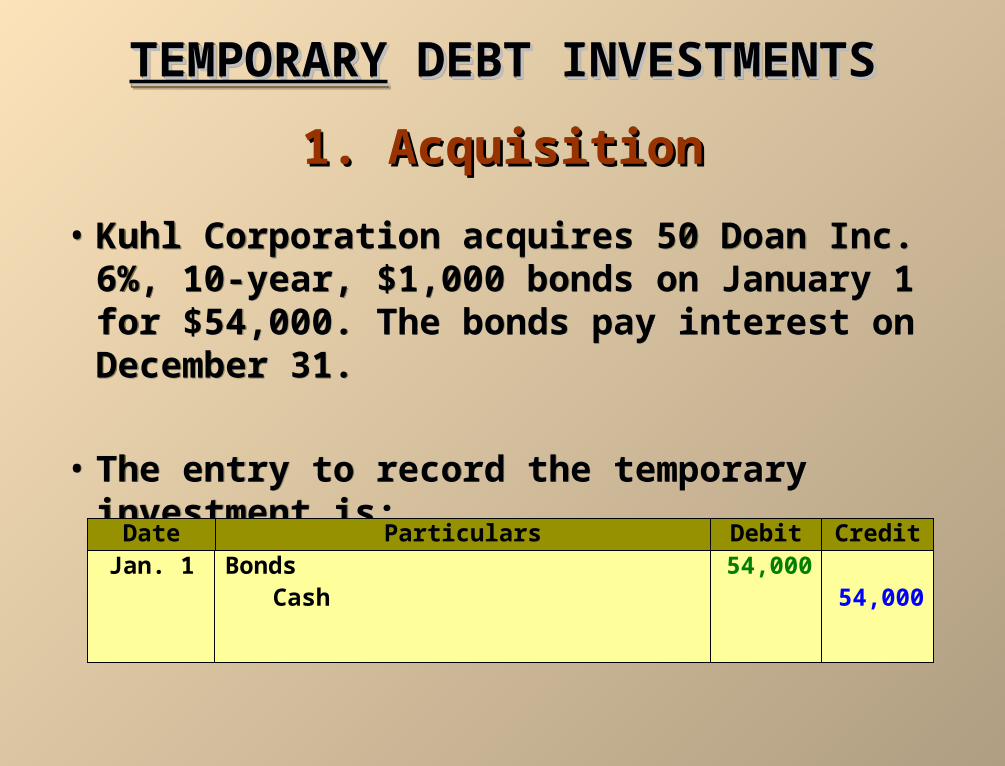

• Kuhl Corporation acquires 50 Doan Inc. 6%, 10-year, $1,000 bonds on January 1 for $54,000. The bonds pay interest on December 31.

• The entry to record the temporary investment is:

• Kuhl Corporation acquires 50 Doan Inc. 6%, 10-year, $1,000 bonds on January 1 for $54,000. The bonds pay interest on December 31.

• The entry to record the temporary investment is:

Date Particulars Debit CreditJan. 1 Bonds 54,000

54,000Cash

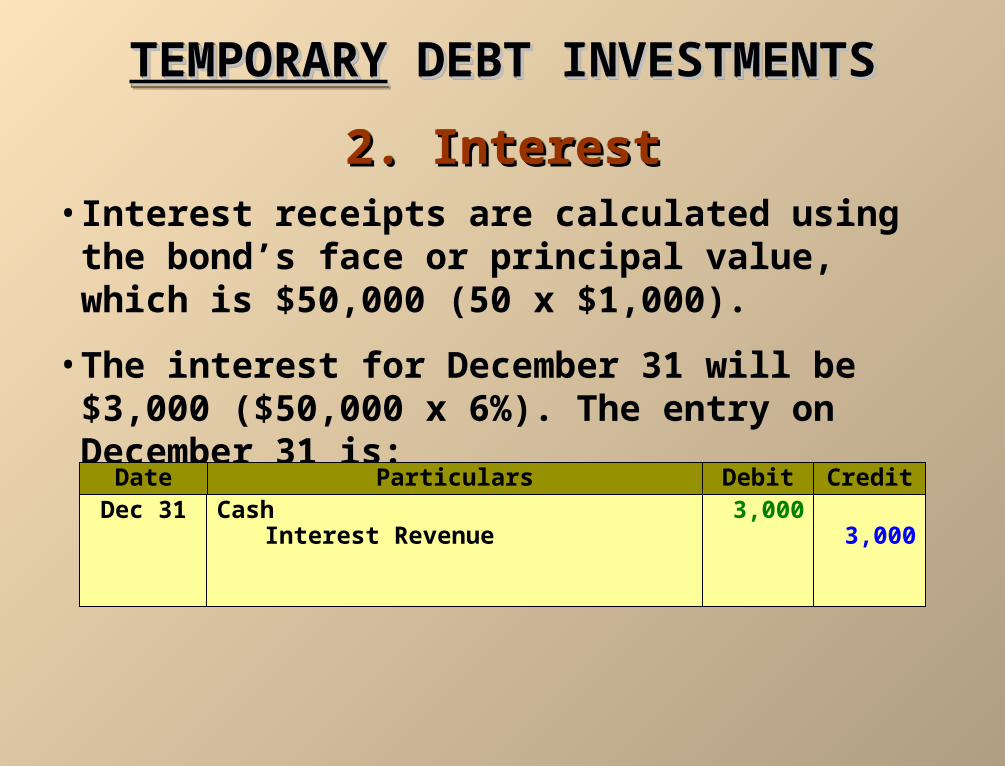

• Interest receipts are calculated using the bond’s face or principal value, which is $50,000 (50 x $1,000).

• The interest for December 31 will be $3,000 ($50,000 x 6%). The entry on December 31 is:

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

2. Interest2. Interest

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

2. Interest2. Interest

Date Particulars Debit CreditDec 31 Cash 3,000

3,000Interest Revenue

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

TEMPORARYTEMPORARY DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

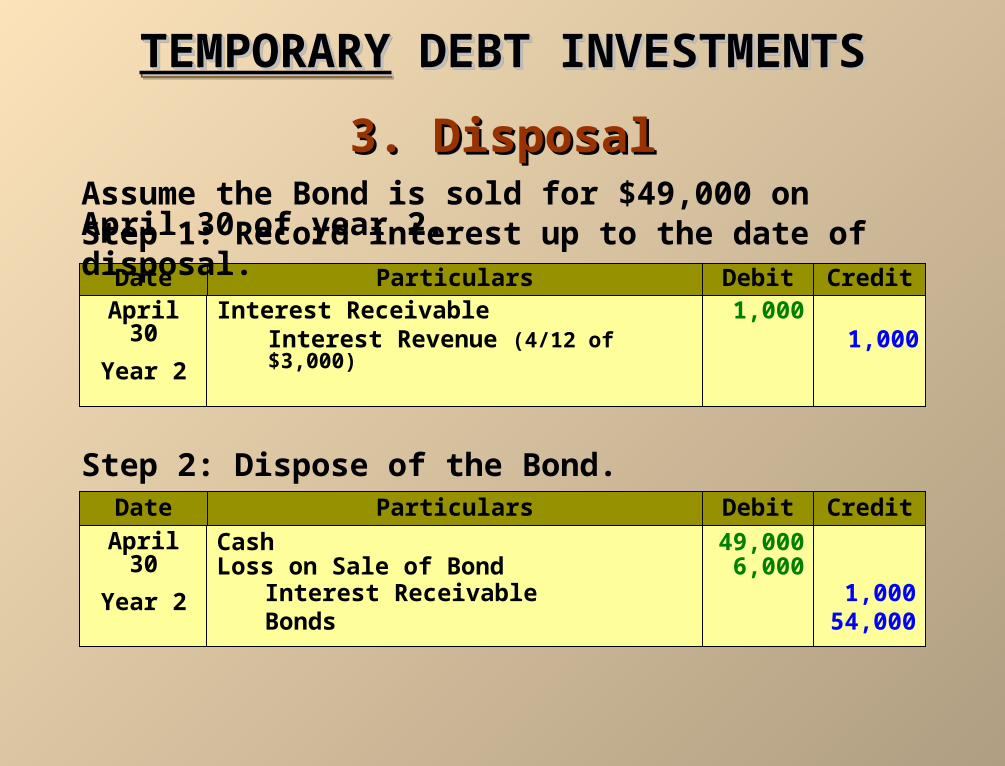

Date Particulars Debit Credit

April 30

Year 2

Cash 49,000

54,000Bonds

Date Particulars Debit CreditApril 30

Year 2

Interest Receivable 1,000

1,000Interest ReceivableLoss on Sale of Bond 6,000

Step 1: Record interest up to the date of disposal.

Step 2: Dispose of the Bond.

Assume the Bond is sold for $49,000 on April 30 of year 2.

1,000Interest Revenue (4/12 of $3,000)

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

1. Acquisition1. Acquisition

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

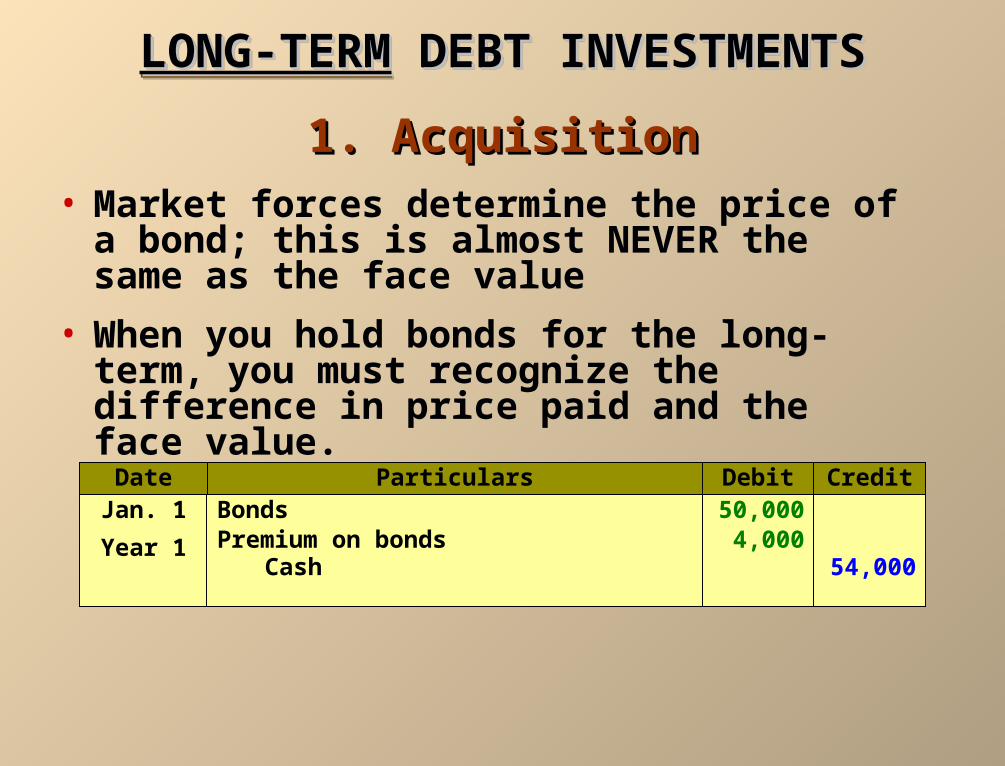

1. Acquisition1. Acquisition• Market forces determine the price of a bond; this

is almost NEVER the same as the face value

• When you hold bonds for the long-term, you must recognize the difference in price paid and the face value.

Date Particulars Debit CreditJan. 1

Year 1

Bonds 50,0004,000Premium on bonds

54,000Cash

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

2. Interest2. Interest

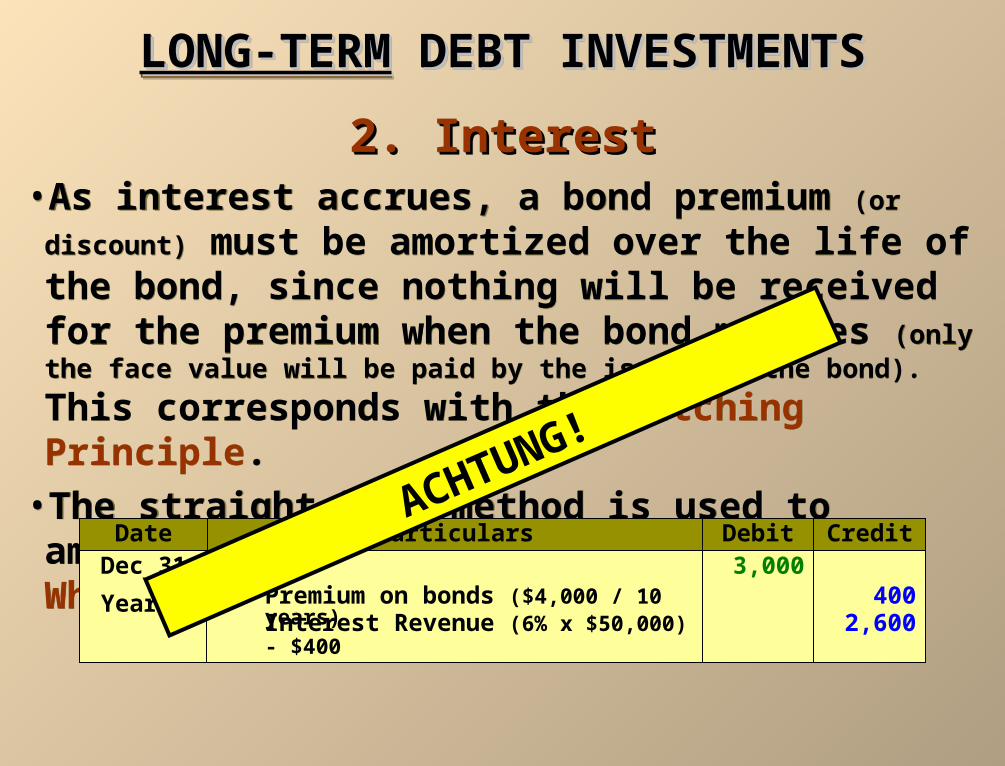

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

2. Interest2. Interest• As interest accrues, a bond premium (or discount) must be amortized over the life of the bond, since nothing will be received for the premium when the bond matures (only the

face value will be paid by the issuer of the bond). This corresponds with the Matching Principle.

• The straight-line method is used to amortize bond premiums and discounts. Why?

• As interest accrues, a bond premium (or discount) must be amortized over the life of the bond, since nothing will be received for the premium when the bond matures (only the

face value will be paid by the issuer of the bond). This corresponds with the Matching Principle.

• The straight-line method is used to amortize bond premiums and discounts. Why?

Date Particulars Debit CreditDec 31

Year 1

Cash 3,000400Premium on bonds ($4,000 / 10 years)

2,600Interest Revenue (6% x $50,000) - $400

ACHTUNG!

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

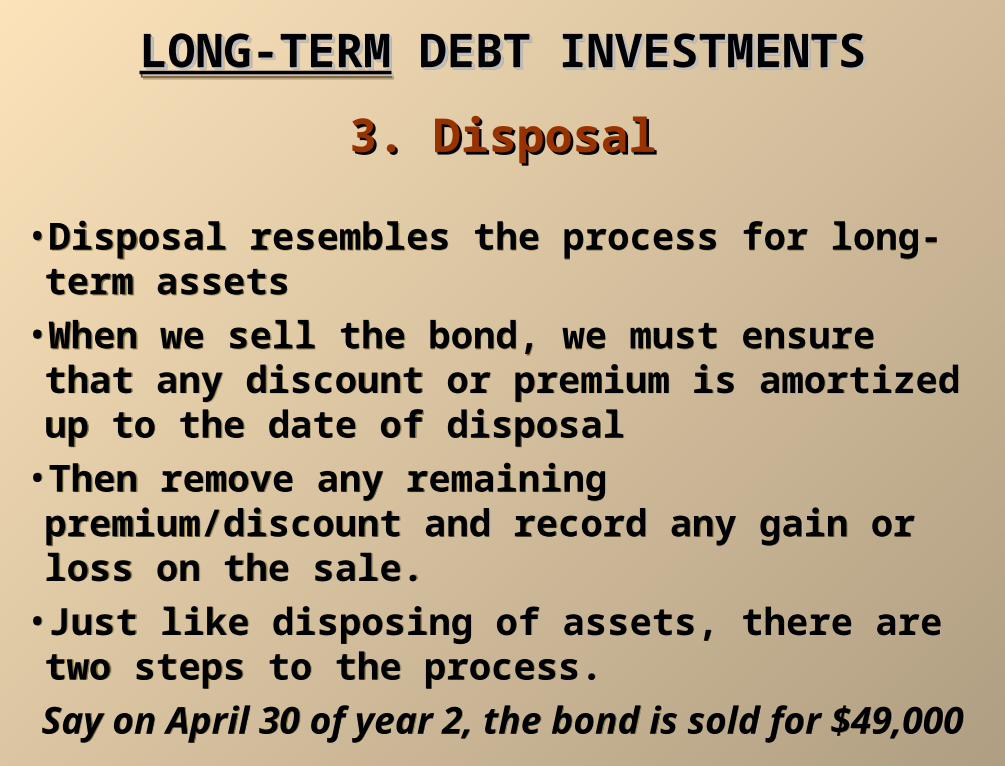

• Disposal resembles the process for long-term assets• When we sell the bond, we must ensure that any discount or premium is amortized up to the date of disposal

• Then remove any remaining premium/discount and record any gain or loss on the sale.

• Just like disposing of assets, there are two steps to the process.

Say on April 30 of year 2, the bond is sold for $49,000

• Disposal resembles the process for long-term assets• When we sell the bond, we must ensure that any discount or premium is amortized up to the date of disposal

• Then remove any remaining premium/discount and record any gain or loss on the sale.

• Just like disposing of assets, there are two steps to the process.

Say on April 30 of year 2, the bond is sold for $49,000

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

LONG-TERMLONG-TERM DEBT INVESTMENTS DEBT INVESTMENTS

3. Disposal3. Disposal

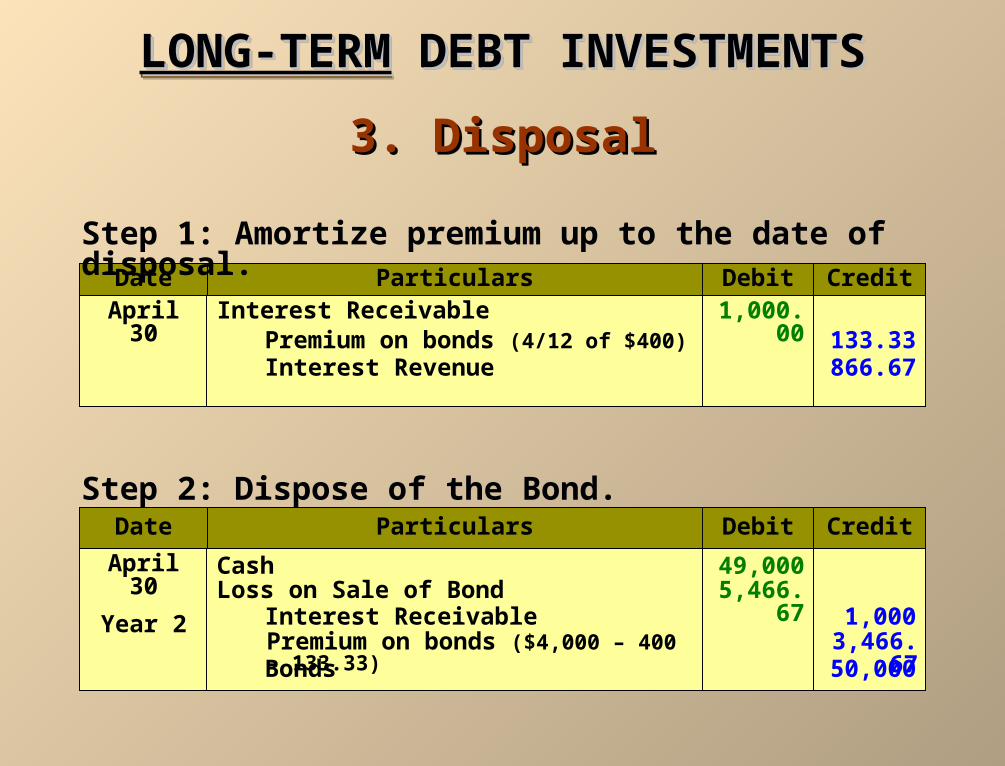

Date Particulars Debit Credit

April 30

Year 2

Cash 49,000

3,466.67Premium on bonds ($4,000 – 400 – 133.33)50,000Bonds

Date Particulars Debit CreditApril 30 Interest Receivable 1,000.00

133.33Premium on bonds (4/12 of $400)866.67Interest Revenue

Loss on Sale of Bond 5,466.67

Step 1: Amortize premium up to the date of disposal.

Step 2: Dispose of the Bond.

1,000Interest Receivable

Do Problems:

BE17-2

P17-1A

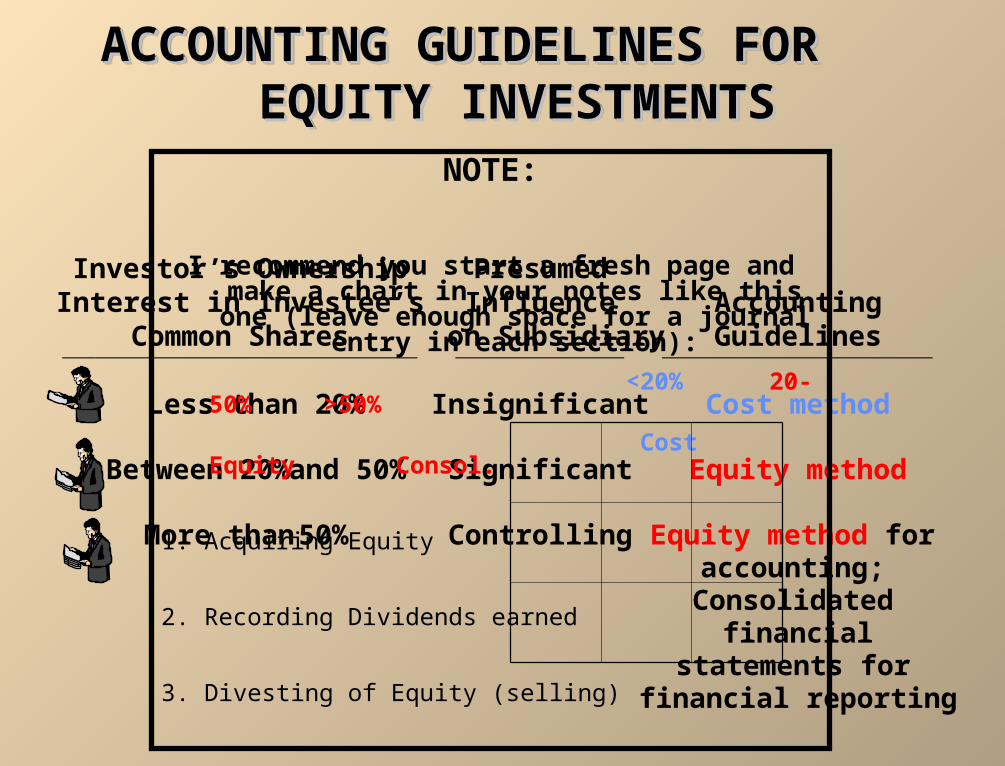

ACCOUNTING GUIDELINES FOR ACCOUNTING GUIDELINES FOR EQUITY INVESTMENTSEQUITY INVESTMENTS

ACCOUNTING GUIDELINES FOR ACCOUNTING GUIDELINES FOR EQUITY INVESTMENTSEQUITY INVESTMENTS

Investor’s Ownership Presumed

Interest in Investee’s Influence Accounting

Common Shares on Subsidiary Guidelines

Less than 20% Insignificant Cost method

Between 20% and 50% Significant Equity method

More than 50% Controlling Equity method for accounting;

Consolidated financial

statements for financial reporting

NOTE:

I recommend you start a fresh page and make a chart in your notes like this one (leave enough space for a

journal entry in each section):

<20% 20-50% >50%

Cost Equity Consol.

1. Acquiring Equity

2. Recording Dividends earned

3. Divesting of Equity (selling)

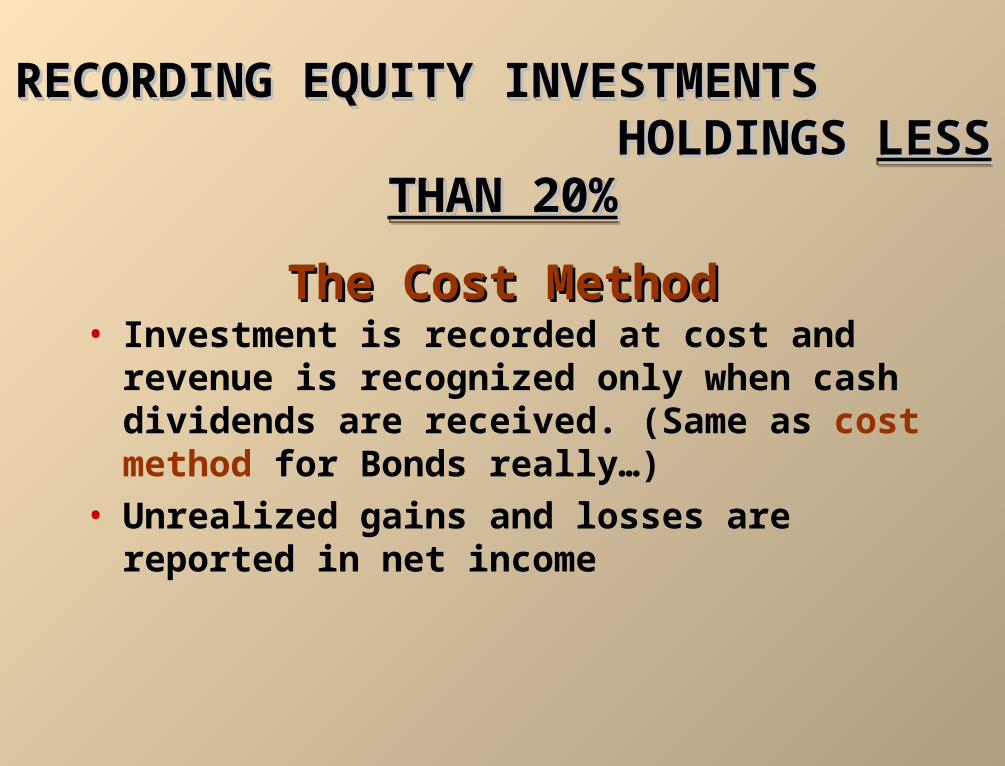

RECORDING EQUITY INVESTMENTS RECORDING EQUITY INVESTMENTS HOLDINGS HOLDINGS LESS THAN 20%LESS THAN 20%

The Cost MethodThe Cost Method

RECORDING EQUITY INVESTMENTS RECORDING EQUITY INVESTMENTS HOLDINGS HOLDINGS LESS THAN 20%LESS THAN 20%

The Cost MethodThe Cost Method

• Investment is recorded at cost and revenue is recognized only when cash dividends are received. (Same as cost method for Bonds really…)

• Unrealized gains and losses are reported in net income

LESS THAN 20%LESS THAN 20%

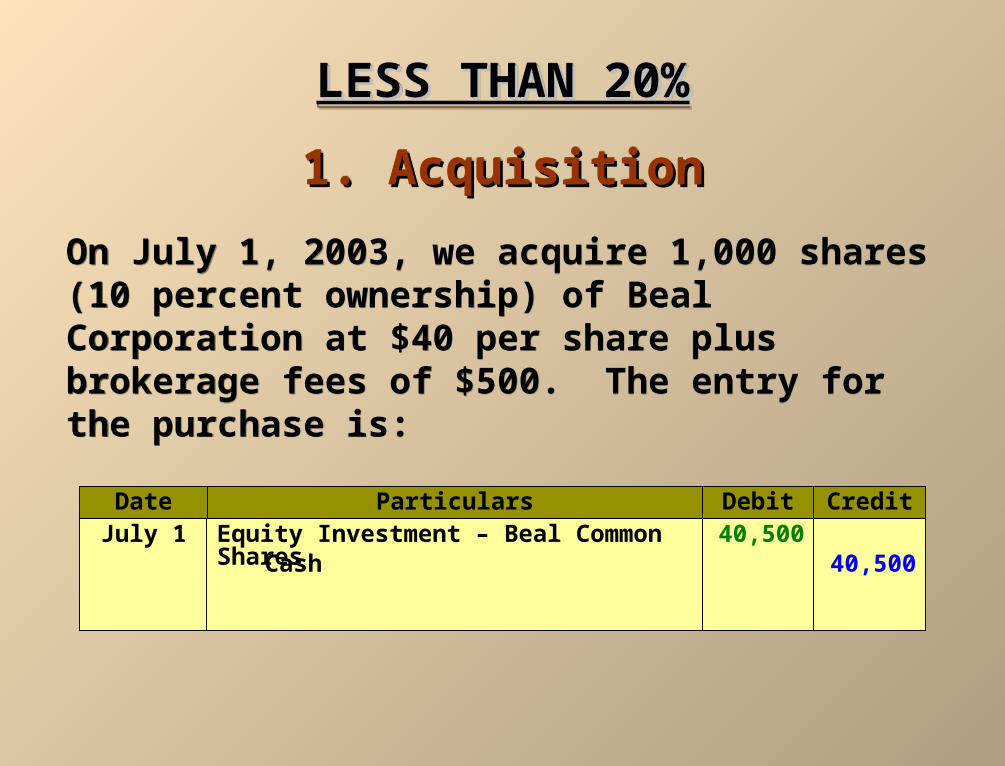

1. Acquisition1. Acquisition

LESS THAN 20%LESS THAN 20%

1. Acquisition1. Acquisition

On July 1, 2003, we acquire 1,000 shares (10 percent ownership) of Beal Corporation at $40 per share plus brokerage fees of $500. The entry for the purchase is:

On July 1, 2003, we acquire 1,000 shares (10 percent ownership) of Beal Corporation at $40 per share plus brokerage fees of $500. The entry for the purchase is:

Date Particulars Debit CreditJuly 1 Equity Investment – Beal Common Shares 40,500

40,500Cash

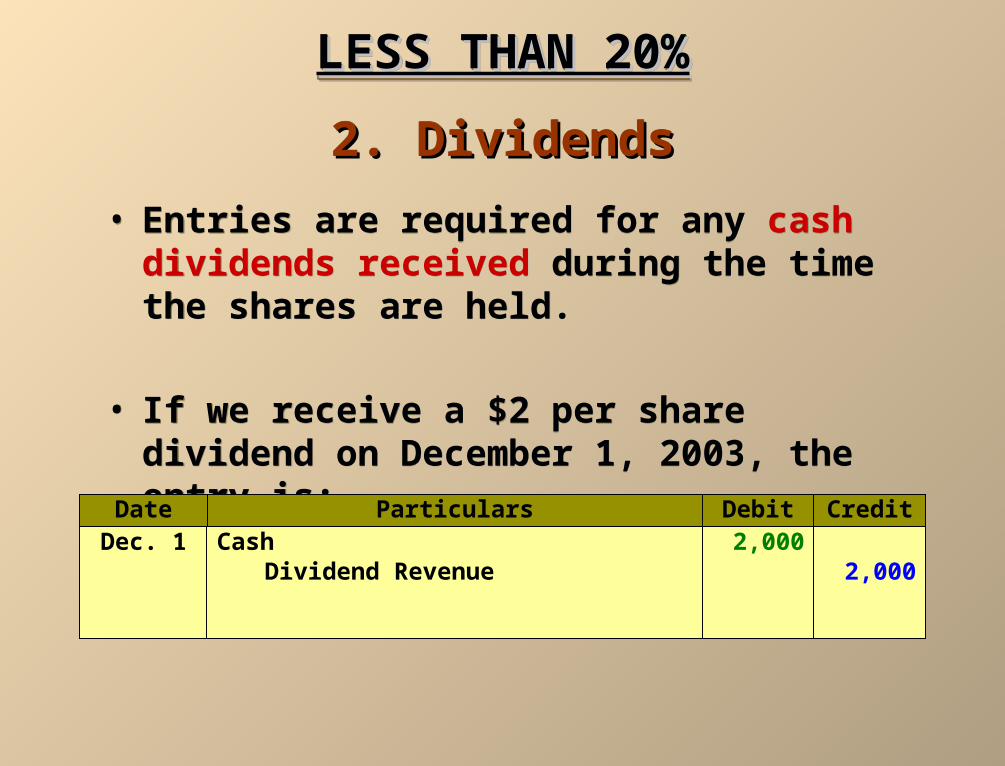

LESS THAN 20%LESS THAN 20%

2. Dividends2. Dividends

LESS THAN 20%LESS THAN 20%

2. Dividends2. Dividends

• Entries are required for any cash dividends received during the time the shares are held.

• If we receive a $2 per share dividend on December 1, 2003, the entry is:

• Entries are required for any cash dividends received during the time the shares are held.

• If we receive a $2 per share dividend on December 1, 2003, the entry is:

Date Particulars Debit CreditDec. 1 Cash 2,000

2,000Dividend Revenue

LESS THAN 20%LESS THAN 20%

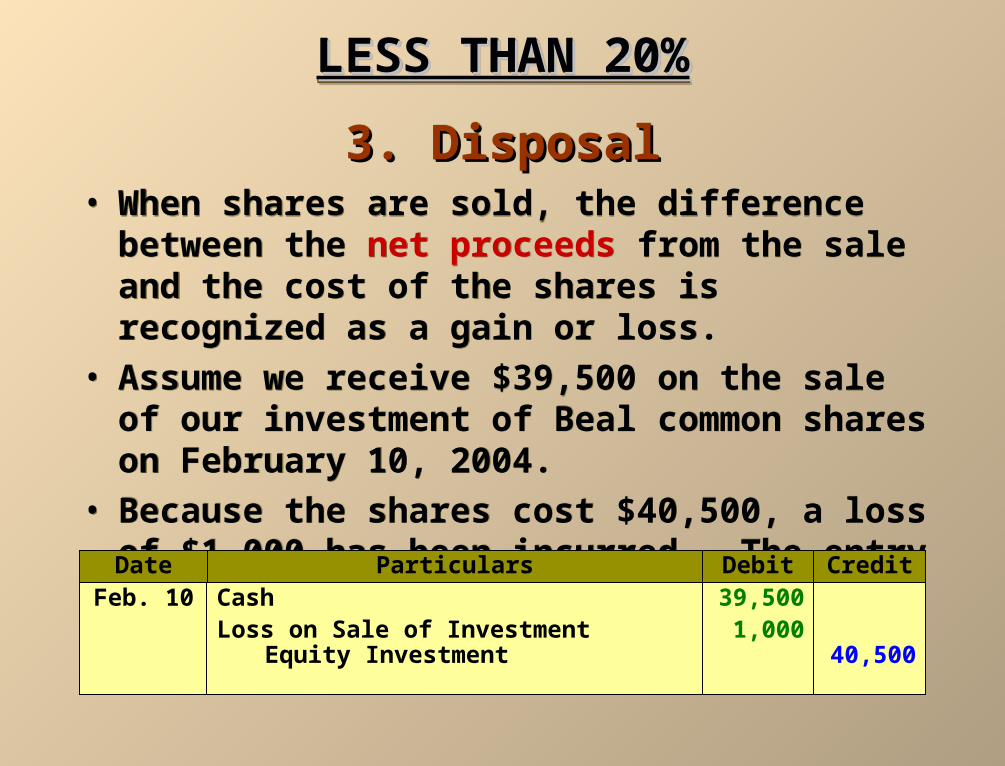

3. Disposal3. Disposal

LESS THAN 20%LESS THAN 20%

3. Disposal3. Disposal• When shares are sold, the difference between the net

proceeds from the sale and the cost of the shares is recognized as a gain or loss.

• Assume we receive $39,500 on the sale of our investment of Beal common shares on February 10, 2004.

• Because the shares cost $40,500, a loss of $1,000 has been incurred. The entry to record the sale is:

• When shares are sold, the difference between the net proceeds from the sale and the cost of the shares is recognized as a gain or loss.

• Assume we receive $39,500 on the sale of our investment of Beal common shares on February 10, 2004.

• Because the shares cost $40,500, a loss of $1,000 has been incurred. The entry to record the sale is:

Date Particulars Debit CreditFeb. 10 Cash 39,500

1,000Loss on Sale of Investment40,500Equity Investment

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

The Equity MethodThe Equity Method

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

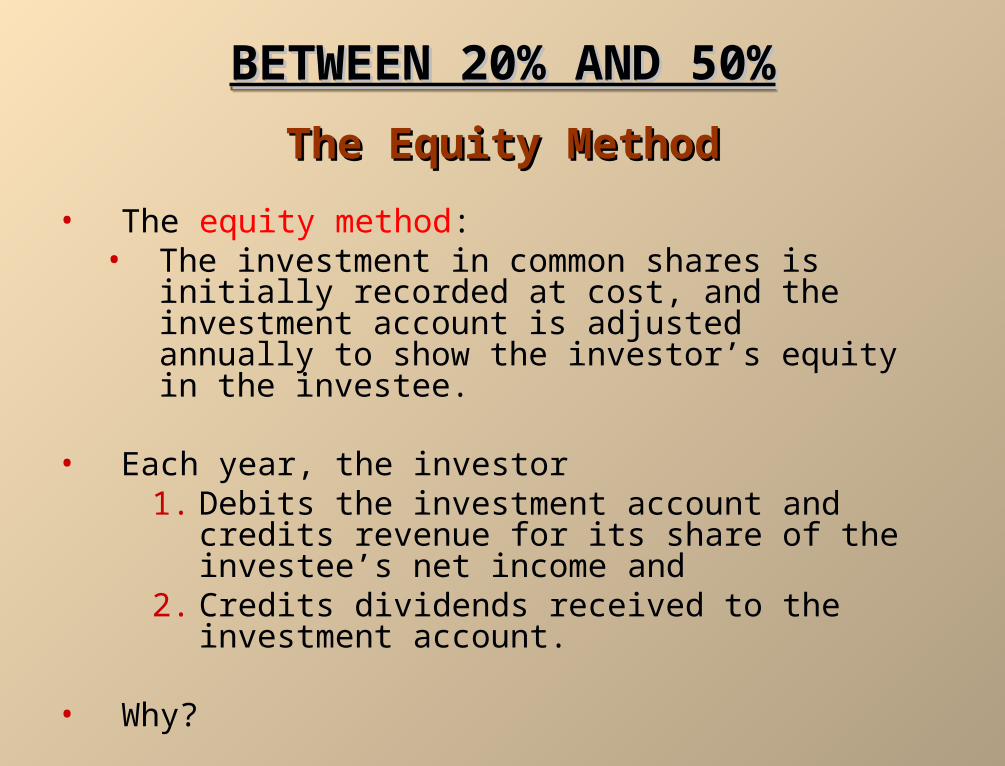

The Equity MethodThe Equity Method

• The equity method:• The investment in common shares is initially

recorded at cost, and the investment account is adjusted annually to show the investor’s equity in the investee.

• Each year, the investor 1. Debits the investment account and credits revenue

for its share of the investee’s net income and2. Credits dividends received to the investment

account.

• Why?

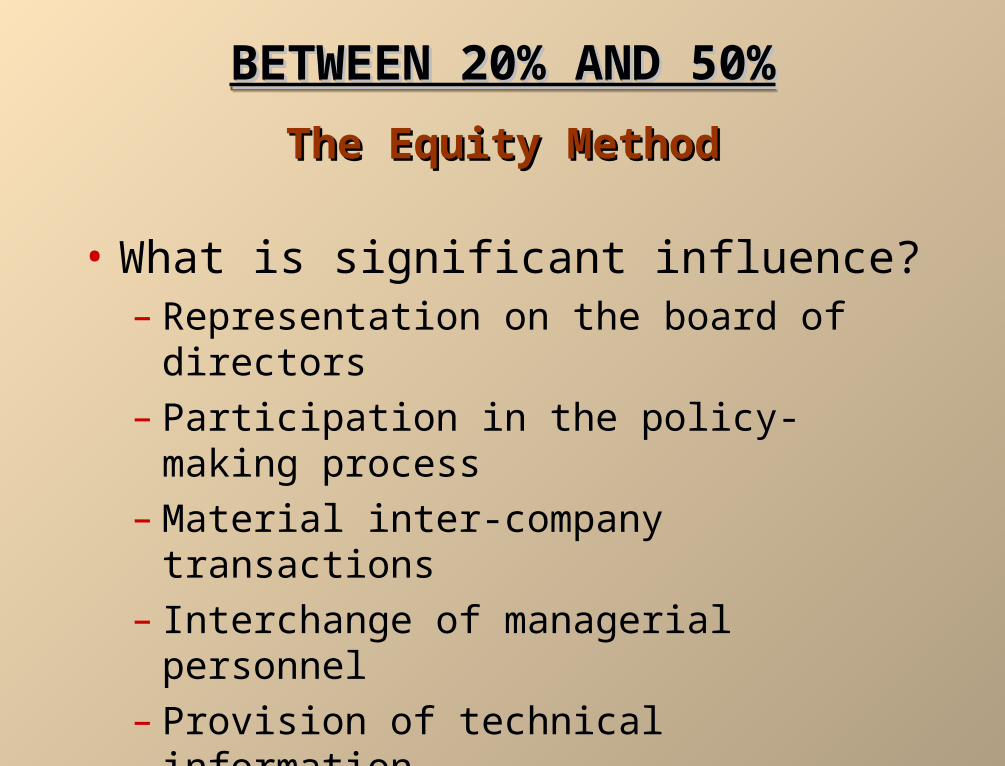

• What is significant influence?– Representation on the board of directors

– Participation in the policy-making process

– Material inter-company transactions

– Interchange of managerial personnel

– Provision of technical information

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

The Equity MethodThe Equity Method

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

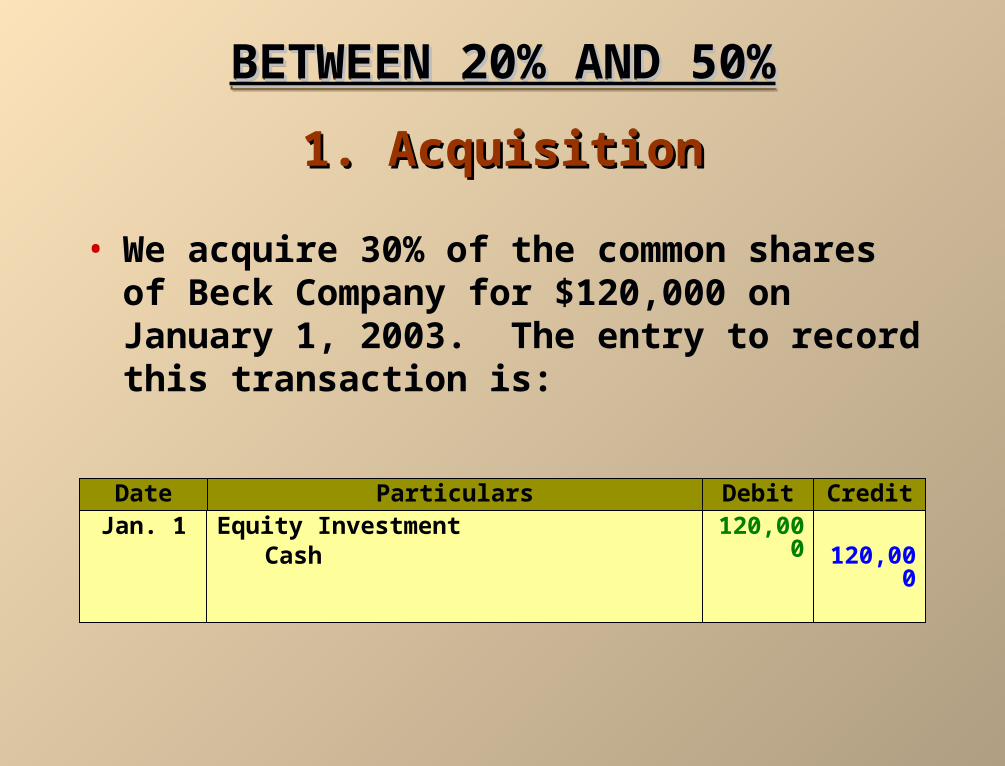

The Equity MethodThe Equity Method

• We acquire 30% of the common shares of Beck Company for $120,000 on January 1, 2003. The entry to record this transaction is:

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

1. Acquisition1. Acquisition

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

1. Acquisition1. Acquisition

Date Particulars Debit CreditJan. 1 Equity Investment 120,000

120,000Cash

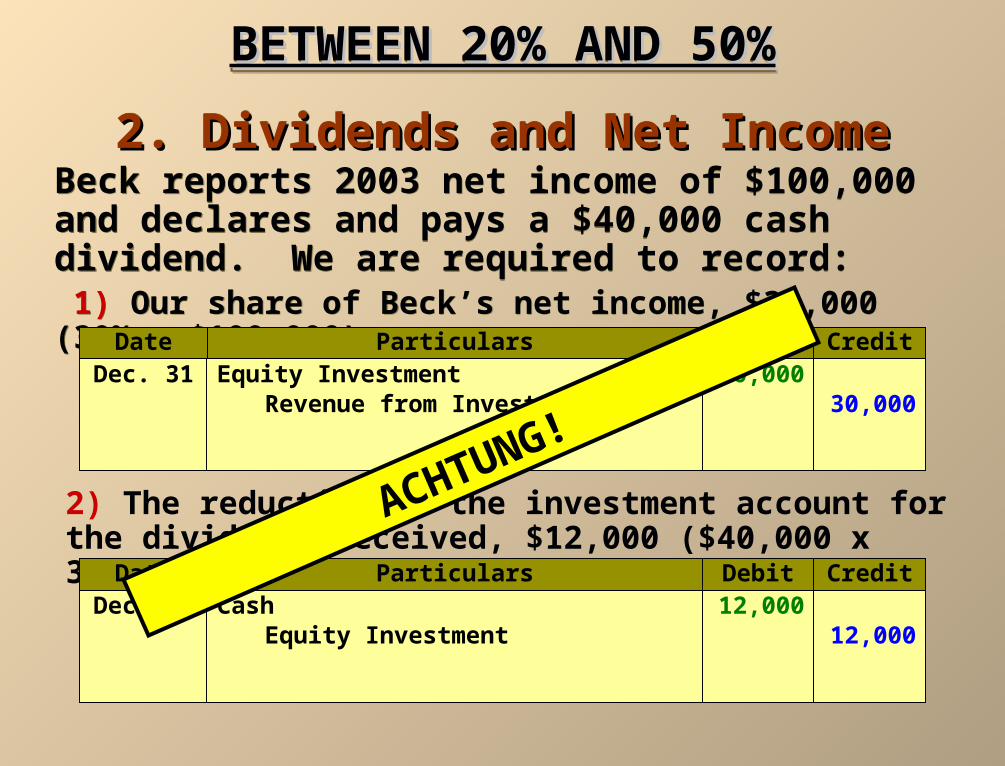

Beck reports 2003 net income of $100,000 and declares and pays a $40,000 cash dividend. We are required to record: 1) Our share of Beck’s net income, $30,000 (30% x $100,000)

Beck reports 2003 net income of $100,000 and declares and pays a $40,000 cash dividend. We are required to record: 1) Our share of Beck’s net income, $30,000 (30% x $100,000)

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

2. Dividends and Net Income2. Dividends and Net Income

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

2. Dividends and Net Income2. Dividends and Net Income

2) The reduction in the investment account for the dividends received, $12,000 ($40,000 x 30%). The entries are:

Date Particulars Debit CreditDec. 31 Equity Investment 30,000

30,000Revenue from Investment

Date Particulars Debit CreditDec. 31 Cash 12,000

12,000Equity Investment

ACHTUNG!

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

3. Disposal3. Disposal

BETWEEN 20% AND 50%BETWEEN 20% AND 50%

3. Disposal3. Disposal

Same as the Cost Method (i.e. same as when holdings are less than 20%)

MORE THAN 50%MORE THAN 50%

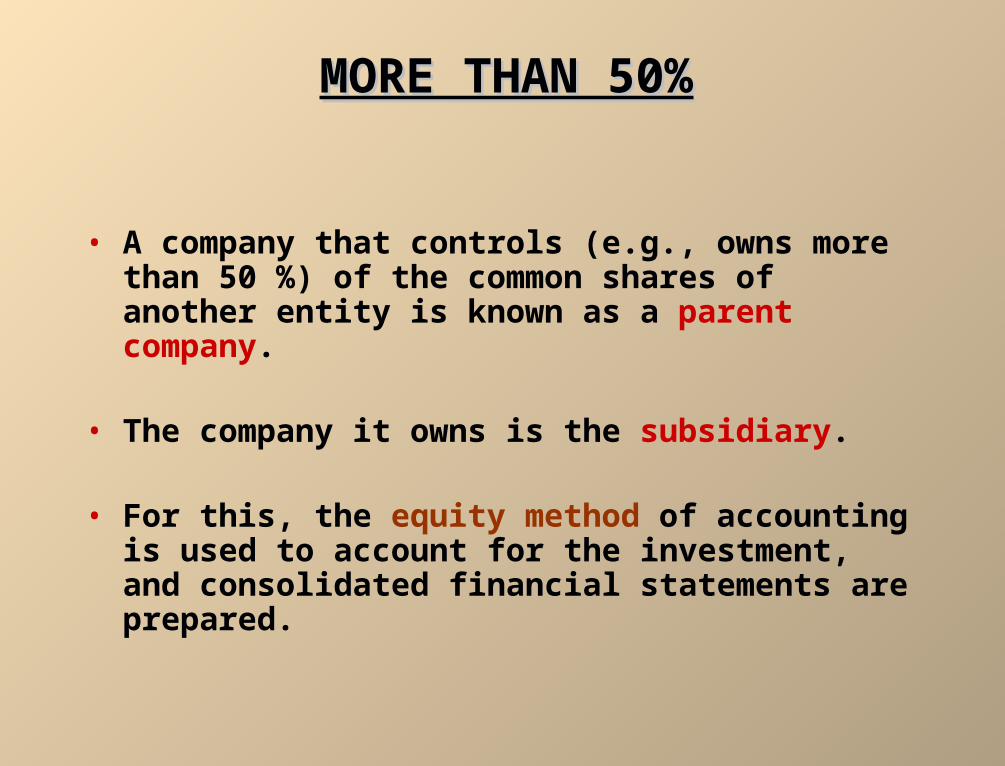

• A company that controls (e.g., owns more than 50 %) of the common shares of another entity is known as a parent company.

• The company it owns is the subsidiary.

• For this, the equity method of accounting is used to account for the investment, and consolidated financial statements are prepared.

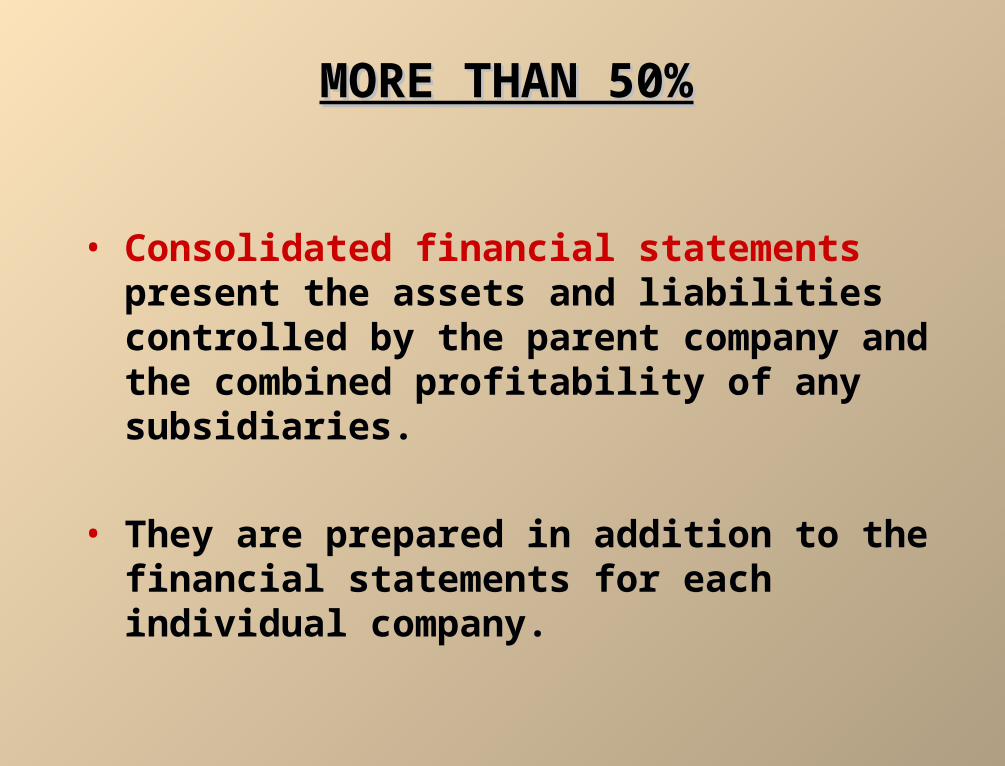

• Consolidated financial statements present the assets and liabilities controlled by the parent company and the combined profitability of any subsidiaries.

• They are prepared in addition to the financial statements for each individual company.

MORE THAN 50%MORE THAN 50%

VALUATION AND REPORTING VALUATION AND REPORTING OF INVESTMENTS OF INVESTMENTS

VALUATION AND REPORTING VALUATION AND REPORTING OF INVESTMENTS OF INVESTMENTS

• The value of debt and equity investments may fluctuate greatly during the time they are held.

• Conservatism principle requires accountants to use the lower of cost and market rule. (When else is this used?)

• Application of the LCM rule varies depending upon whether the investment is temporary or long-term.

VALUATION AND REPORTING OF VALUATION AND REPORTING OF TEMPORARYTEMPORARY INVESTMENTS INVESTMENTS

• The decline in value from cost to market is reported as a loss.

• An Allowance to Reduce Cost to Market Value account is used to record the difference between the cost and market value.

• The Allowance account is a contra asset and is deducted from the cost of the investments

Don’t Panic!

This technique operates just like Allowance for Doubtful

Accounts and Accumulated Depreciation, both of which

YOU ALREADY KNOW!

VALUATION AND REPORTING OF VALUATION AND REPORTING OF LONG-TERMLONG-TERM INVESTMENTS INVESTMENTS

VALUATION AND REPORTING OF VALUATION AND REPORTING OF LONG-TERMLONG-TERM INVESTMENTS INVESTMENTS

• Long-term investments should not be adjusted to reflect temporary fluctuations in market value.

• Only when a drop is NOT due to temporary fluctuations should lower of cost and market be used for long term investments.

• Any write-down to market value is accounted for on the income statement as a permanent loss. No allowance account is used.

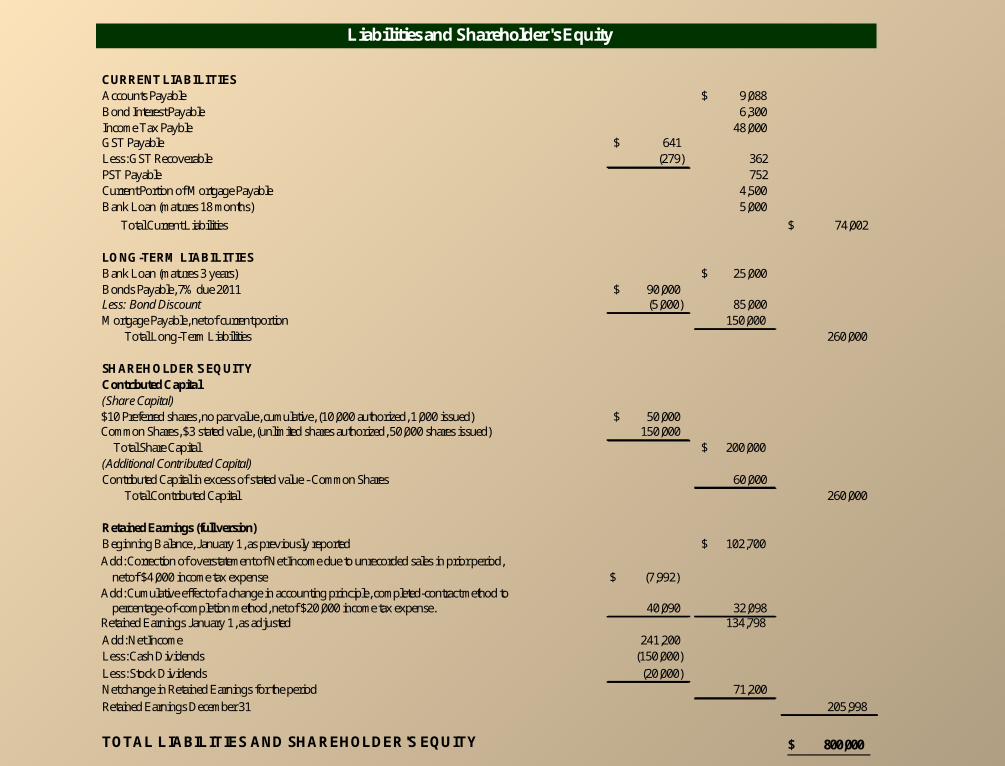

CURRENT ASSETSCash and cash equivalents 1,750$ Temporary Investments (lower of cost and market) 25,000 Accounts Receivable 35,880$ Less: Allowance for Doubtful Accounts (1,600) 34,280 Notes Receivable 30,000 Less: Allowance for Doubtful Notes (2,400) 27,600 Merchandise Inventory 2,500 Supplies 1,350 Prepaid Insurance 1,900 Total Current Assets 94,380$

INVESTMENTSDebt Invstments 100,000$ Equity Investments, at cost 40,000 Equity Investments, at equity 30,000

Total Long-Term Investments 170,000

FIXED ASSETSLand 134,000$ Building 250,000$ Less: Accumulated Amortization (40,000) 210,000 Equipment 85,770 Less: Accumulated Amortization (7,500) 78,270 Patents, net of amortization 80,000 Automobiles 33,350

Total Fixed Assets 535,620

TOTAL ASSETS 800,000$

Assets

COMPREHENSIVE BALANCE SHEETCOMPREHENSIVE BALANCE SHEET

CURRENT LIABILITIESAccounts Payable 9,088$ Bond Interest Payable 6,300 Income Tax Payble 48,000 GST Payable 641$ Less: GST Recoverable (279) 362 PST Payable 752 Current Portion of Mortgage Payable 4,500 Bank Loan (matures 18 months) 5,000

Total Current Liabilities 74,002$

LONG-TERM LIABILITIESBank Loan (matures 3 years) 25,000$ Bonds Payable, 7% due 2011 90,000$ Less: Bond Discount (5,000) 85,000 Mortgage Payable, net of current portion 150,000

Total Long-Term Liabilities 260,000

SHAREHOLDER'S EQUITYContributed Capital(Share Capital)

$10 Preferred shares, no par value, cumulative, (10,000 authorized, 1,000 issued) 50,000$ Common Shares, $3 stated value, (unlimited shares authorized, 50,000 shares issued) 150,000

Total Share Capital 200,000$ (Additional Contributed Capital)Contributed Capital in excess of stated value - Common Shares 60,000

Total Contributed Capital 260,000

Retained Earnings (full version)Beginning Balance, January 1, as previously reported 102,700$

Add: Correction of overstatement of Net Income due to unrecorded sales in prior period, net of $4,000 income tax expense (7,992)$

Add: Cumulative effect of a change in accounting principle, completed-contract method to percentage-of-completion method, net of $20,000 income tax expense. 40,090 32,098

Retained Earnings January 1, as adjusted 134,798

Add: Net Income 241,200 Less: Cash Dividends (150,000)

Less: Stock Dividends (20,000)Net change in Retained Earnings for the period 71,200

Retained Earnings December 31 205,998

TOTAL LIABILITIES AND SHAREHOLDER'S EQUITY 800,000$

Liabilities and Shareholder's Equity

Do Problems:

P17-7A

Homework:

P17-9A

Submit word processed (use excel)