Embed Size (px)

Citation preview

Chapter 15 Organization and Operation of Corporations

Questions

1. The board of directors of a corporation is responsible for directing the corporation’s affairs.

2. Organization costs are incurred in creating a corporation. Examples include: legal fees, promoters’ fees, accountants’ fees, costs of printing share certificates, and fees paid to the provincial legal jurisdiction to obtain a corporate charter.

3. Organization costs are intangible assets, if material. If not, can be expensed.4. The general rights of common shareholders include: (1) the right to vote in shareholders’

meetings, (2) the right to sell or otherwise dispose of shares, (3) the preemptive right, (4) the right to share proportionately in dividends, and (5) the right to share proportionately in assets remaining after the creditors are paid if the corporation is liquidated. In addition, shareholders have the right to receive timely and useful financial reports that describe the corporation’s financial position and the results of its activities.

5. The preemptive right of common shareholders is the right to maintain their relative ownership interests in the corporation by having the first opportunity to purchase their proportionate share of any additional common shares issued by the corporation.

6. The call price is the amount that a corporation must pay if it exercises the option to buy back and retire callable shares.

7. Convertible preferred shares are attractive because they offer the safety of a regular return as well as the opportunity to share in the increased value of the issuer’s common shares.

8. According to Note 7(b), WestJet Airlines had 129,575,099 common and variable shares issued and outstanding at December 31, 2005 for a total of $429,613,000. The average issue price at December 31, 2005 is $429,613,000/129,575,099 = $3.32 per common share.

9. According to the statement of retained earnings, Danier Leather declared and paid dividends of $1,620,000 during the year ended June 25, 2005.

Copyright © 2007 by McGraw-Hill Ryerson Limited. All rights reserved.Solutions Manual for Chapter 15 180

QUICK STUDY

Quick Study 15-1 (10 minutes)a, d

Quick Study 15-2 (10 minutes)2011Jan.

1Organization Costs....................... 56,000

Cash........................................ 50,000 Common Shares....................... 6,000 To record payment of organization costs and issuance of shares as part consideration.

Dec. 31

Amortization Expense, Organization Costs...........................................

11,200

Accumulated Amort., Organization Costs.......................

11,200

To record accumulated amortization, organization costs; 56,000/5 = 11,200.

Quick Study 15-3 (10 minutes)

LUDWIG LTD.Income Statement

For Year Ended October 31, 2011Sales................................ $

982,000Cost of goods sold............. 420,00

0Gross profit....................... $

562,000Operating expenses.......... 162,00

0Income from operations..... $

400,000Other revenues and expenses: Gain on sale of capital assets...............................

$ 4,000

Copyright © 2007 by McGraw-Hill Ryerson Limited. All rights reserved.181 Fundamental Accounting Principles, Twelfth Canadian Edition

Interest expense........... (6,200) (2,200 )Income before tax............. $

397,800Income tax expense.......... 99,45

0Net income....................... $

298,350

Quick Study 15-4 (5 minutes)X Cash CC Preferred sharesCC Common shares RE Retained earningsX Common dividend

payableX Preferred dividend

payableRE Deficit CC Preferred shares,

$5 noncumulative

Quick Study 15-5 (20 minutes)FORM OF BUSINESS ORGANIZATION

Transaction Sole Proprietorship CorporationJan. 1, 2011:The owner(s) invested $10,000into the new business

Cash.................10,000 Ian Smith, Capital........................10,000

Cash............10,000 Common Shares.........10,000

During 2011:Revenues of $50,000 were earned; all cash

Cash.................50,000 Revenues...................50,000

Cash............50,000 Revenues. 50,000

During 2011:Expenses of $30,000 were incurred; all cash

Expenses..........30,000 Cash..........................30,000

Expenses......30,000 Cash........ 30,000

Copyright © 2007 by McGraw-Hill Ryerson Limited. All rights reserved.Solutions Manual for Chapter 15 182

Dec. 15, 2011:$15,000 cash was distributed to the owner(s)

Ian Smith, Withdrawals 15,000 Cash..........................15,000

Cash Dividends 15,000 (or R/E) Cash......... 15,000

Dec. 31, 2011, Year End:All temporary accounts were closed—Close Revenue account

Revenues.........50,000 Income Summary............. 50,000

Revenues.....50,000 Income Summary.........50,000

—Close Expense account

Income Summary..............30,000 Expenses...................30,000

Income Summary 30,000 Expenses. 30,000

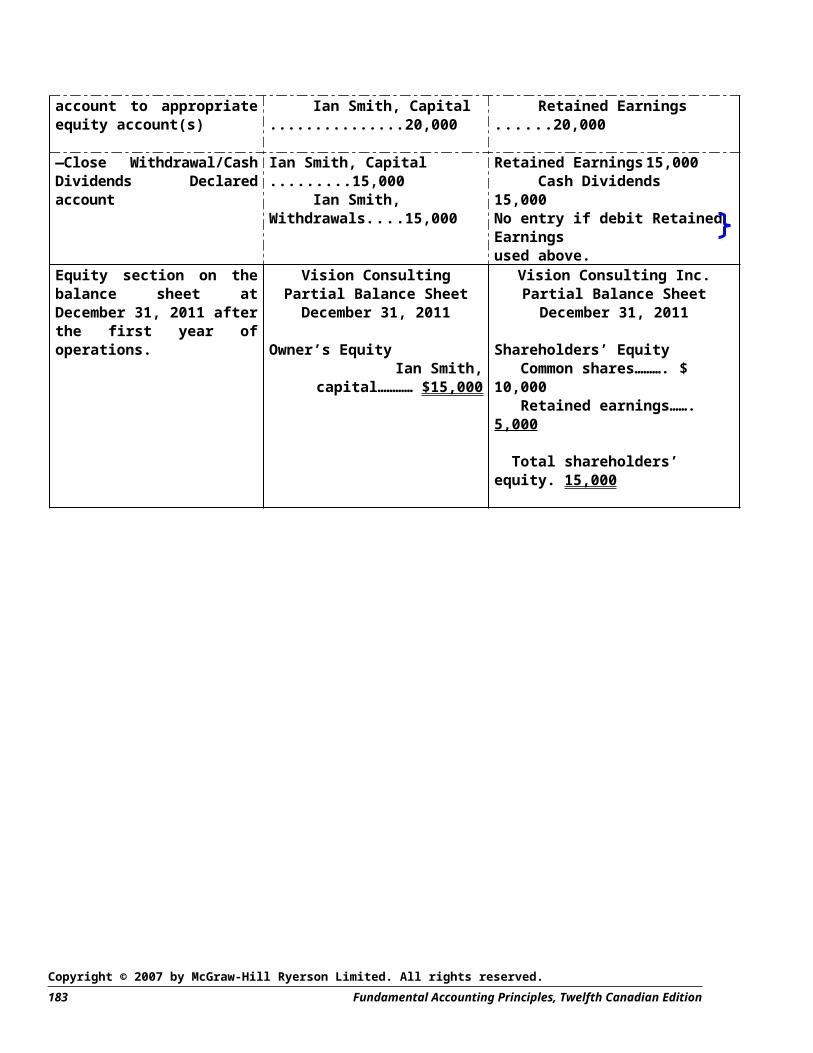

—Close Income Summary account to appropriate equity account(s)

Income Summary..............20,000 Ian Smith, Capital........................20,000

Income Summary 20,000 Retained Earnings.........20,000

—Close Withdrawal/Cash Dividends Declared account

Ian Smith, Capital..............15,000 Ian Smith, Withdrawals.....15,000

Retained Earnings15,000 Cash Dividends 15,000No entry if debit Retained Earnings used above.

Equity section on the balance sheet at December 31, 2011 after the first year of operations.

Vision ConsultingPartial Balance SheetDecember 31, 2011

Owner’s Equity Ian Smith,

capital………… $15,000

Vision Consulting Inc.Partial Balance SheetDecember 31, 2011

Shareholders’ Equity Common shares……….$ 10,000 Retained earnings…….

Copyright © 2007 by McGraw-Hill Ryerson Limited. All rights reserved.183 Fundamental Accounting Principles, Twelfth Canadian Edition

5,000

Total shareholders’ equity. 15,000

Copyright © 2007 by McGraw-Hill Ryerson Limited. All rights reserved.Solutions Manual for Chapter 15 184

Quick Study 15-6 (10 minutes)$48,000 + $146,000 – $47,000 – $15,000 = $132,000

OR

Retained Earnings 48,000

Bal. Dec. 31/11

146,000

Net income, 2012

Dividends, 2012

47,000

Net loss, 2013

15,000

132,000

Bal. Dec. 31/13

Quick Study 15-7 (5 minutes)1. 300,000 – 120,000 + 50,000 = 230,0002. Net income 3. Dividends

Quick Study 15-8 (10 minutes)Feb. 1............................................Cash 252,440

Common shares ................ 252,440 Issued shares for cash.

Feb. 12............................................Cash 340,750 Common shares ................ 340,750

Issued shares for cash; 47,000 x $7.25.

The average issue price is $7.02 calculated as:

($252,440 + $340,750) ÷ (37,500 + 47,000).

Quick Study 15-9 (10 minutes)a. Sold common shares for cash.b. Issued common shares to pay organization costs.

c. Issued common shares for inventory and machinery, and assumed a note payable.

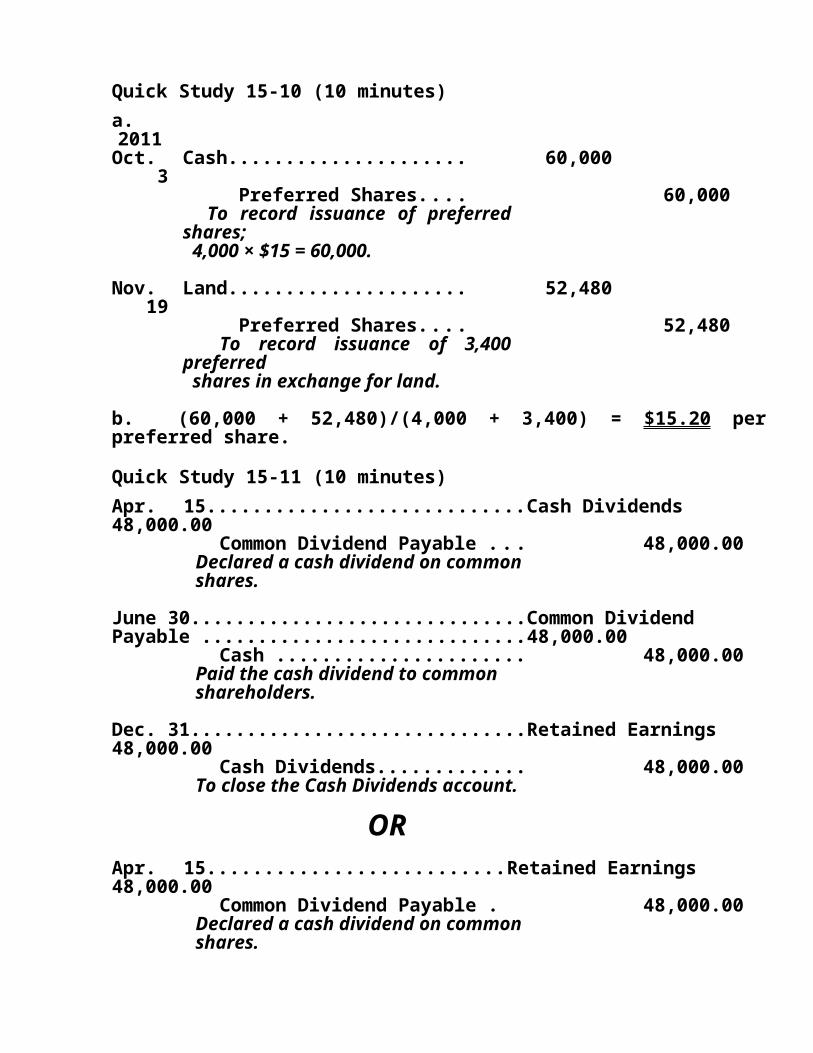

Quick Study 15-10 (10 minutes)a.2011Oct.

3Cash................................. 60,000

Preferred Shares.......... 60,000 To record issuance of preferred shares; 4,000 × $15 = 60,000.

Nov. 19

Land................................. 52,480

Preferred Shares.......... 52,480 To record issuance of 3,400 preferred shares in exchange for land.

b. (60,000 + 52,480)/(4,000 + 3,400) = $15.20 per preferred share.

Quick Study 15-11 (10 minutes)Apr. 15...............................................Cash Dividends48,000.00

Common Dividend Payable . . 48,000.00 Declared a cash dividend on common shares.

June 30...............................................Common Dividend Payable ..............................................48,000.00

Cash ................................... 48,000.00 Paid the cash dividend to common shareholders.

Dec. 31...............................................Retained Earnings 48,000.00

Cash Dividends.................... 48,000.00 To close the Cash Dividends account.

OR

Apr. 15............................................Retained Earnings 48,000.00

Common Dividend Payable 48,000.00 Declared a cash dividend on common shares.

June30.............................................Common Dividend Payable ........................................... 48,000.00

Cash ................................ 48,000.00 Paid the cash dividend to common shareholders.

Dec. 31 No entry required.

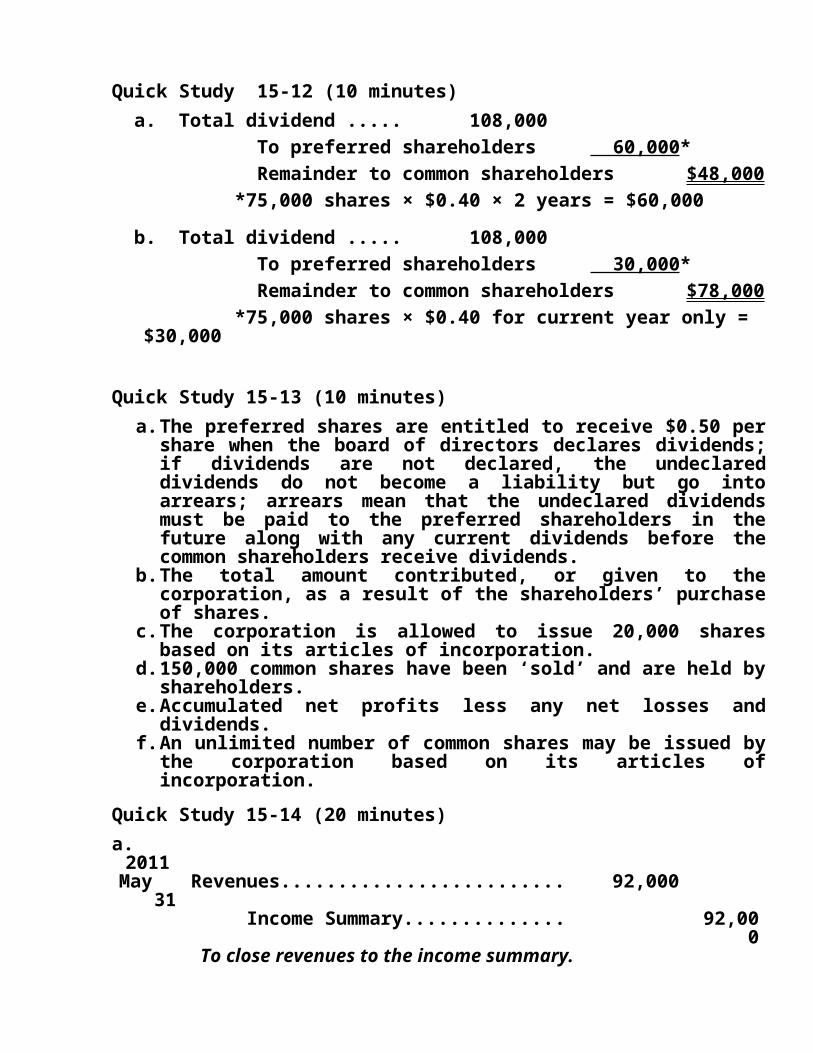

Quick Study 15-12 (10 minutes) a. Total dividend ............... 108,000 To preferred shareholders 60,000* Remainder to common shareholders $48,000 *75,000 shares × $0.40 × 2 years = $60,000

b. Total dividend ............... 108,000 To preferred shareholders 30,000* Remainder to common shareholders $78,000 *75,000 shares × $0.40 for current year only =

$30,000

Quick Study 15-13 (10 minutes)a. The preferred shares are entitled to receive $0.50 per

share when the board of directors declares dividends; if dividends are not declared, the undeclared dividends do not become a liability but go into arrears; arrears mean that the undeclared dividends must be paid to the preferred shareholders in the future along with any current dividends before the common shareholders receive dividends.

b. The total amount contributed, or given to the corporation, as a result of the shareholders’ purchase of shares.

c. The corporation is allowed to issue 20,000 shares based on its articles of incorporation.

d. 150,000 common shares have been ‘sold’ and are held by shareholders.

e. Accumulated net profits less any net losses and dividends.

f. An unlimited number of common shares may be issued by the corporation based on its articles of incorporation.

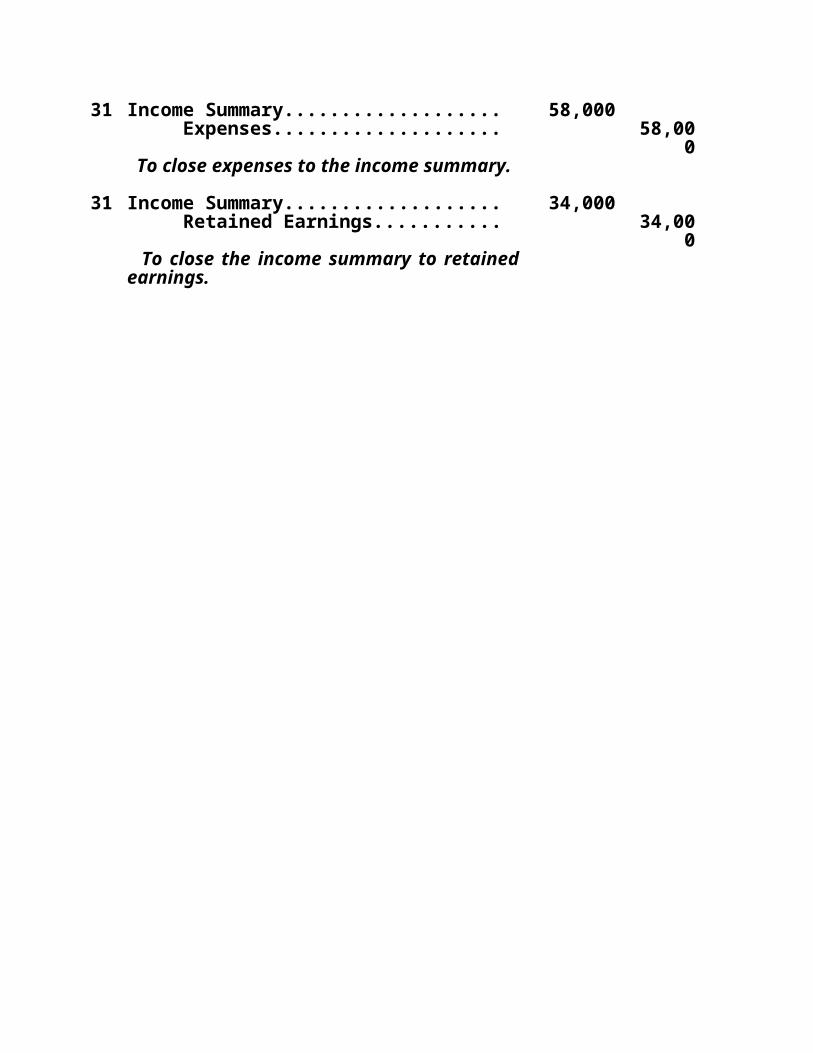

Quick Study 15-14 (20 minutes)a.2011May

31Revenues...................................... 92,000

Income Summary...................... 92,000

To close revenues to the income summary.

31 Income Summary........................... 58,000 Expenses.................................. 58,00

0 To close expenses to the income summary.

31 Income Summary........................... 34,000 Retained Earnings..................... 34,00

0 To close the income summary to retained earnings.

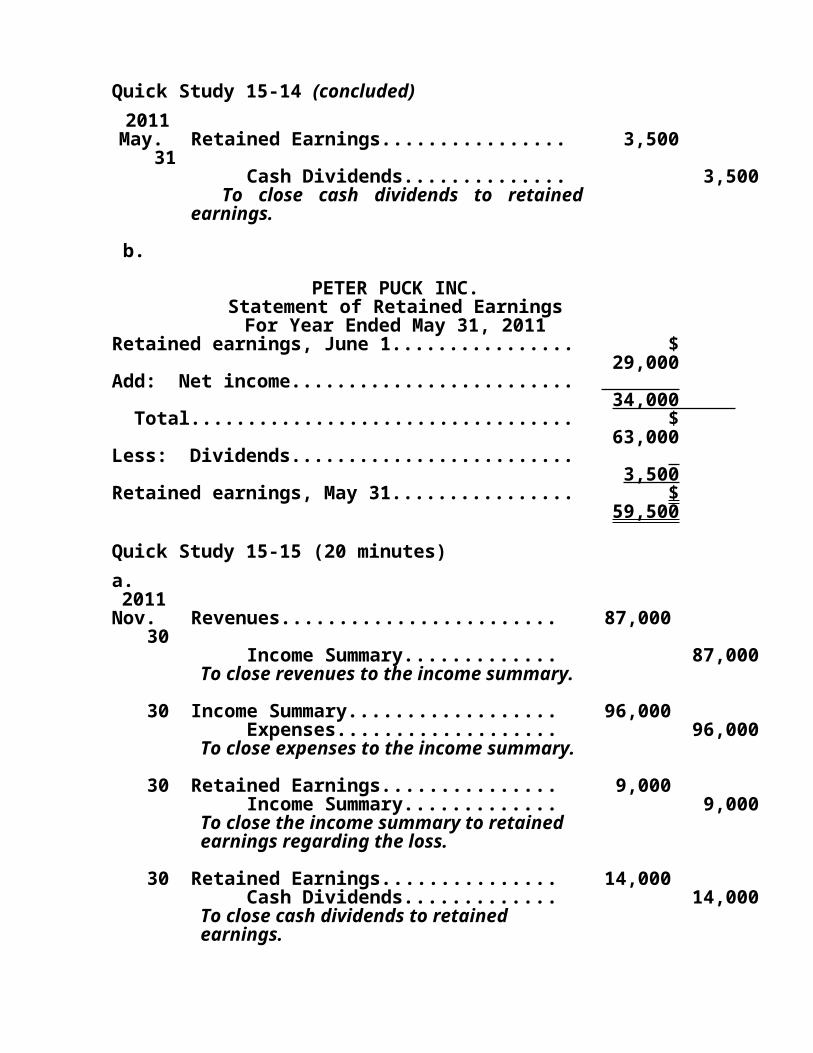

Quick Study 15-14 (concluded)2011May.

31Retained Earnings.......................... 3,500

Cash Dividends......................... 3,500 To close cash dividends to retained earnings.

b.

PETER PUCK INC.Statement of Retained Earnings

For Year Ended May 31, 2011Retained earnings, June 1........................... $

29,000Add: Net income........................................ 34,

000 Total........................................................ $

63,000Less: Dividends......................................... 3,

500Retained earnings, May 31......................... $

59,500

Quick Study 15-15 (20 minutes)a.2011

Nov. 30

Revenues..................................... 87,000

Income Summary..................... 87,000 To close revenues to the income summary.

30 Income Summary.......................... 96,000 Expenses................................. 96,000 To close expenses to the income summary.

30 Retained Earnings........................ 9,000 Income Summary..................... 9,000 To close the income summary to retained earnings regarding the loss.

30 Retained Earnings........................ 14,000 Cash Dividends........................ 14,000

To close cash dividends to retained earnings.

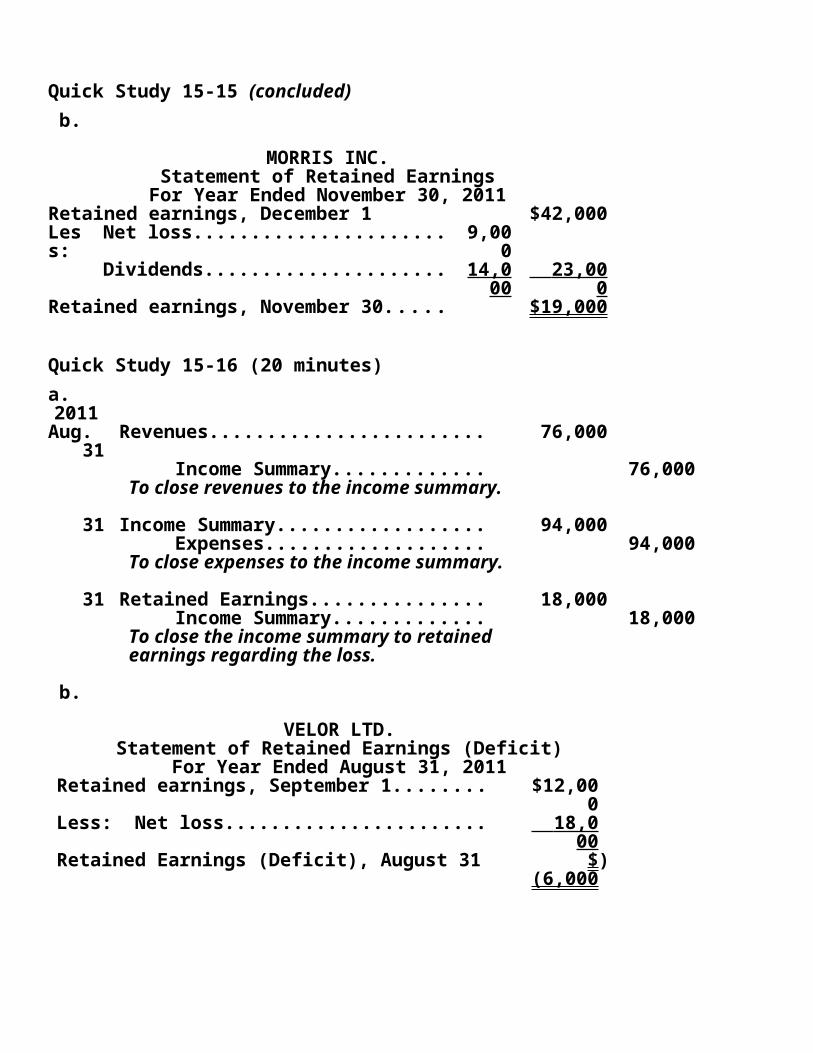

Quick Study 15-15 (concluded) b.

MORRIS INC.Statement of Retained Earnings

For Year Ended November 30, 2011Retained earnings, December 1 $42,00

0Less:

Net loss.................................... 9,000

Dividends.................................. 14,000

23,00 0

Retained earnings, November 30....... $19,000

Quick Study 15-16 (20 minutes)a.2011Aug.

31Revenues..................................... 76,000

Income Summary..................... 76,000 To close revenues to the income summary.

31 Income Summary.......................... 94,000 Expenses................................. 94,000 To close expenses to the income summary.

31 Retained Earnings........................ 18,000 Income Summary..................... 18,000 To close the income summary to retained earnings regarding the loss.

b.

VELOR LTD.Statement of Retained Earnings (Deficit)

For Year Ended August 31, 2011Retained earnings, September 1............ $12,0

00Less: Net loss....................................... 18,0

00Retained Earnings (Deficit), August 31. . . $ )

(6,000

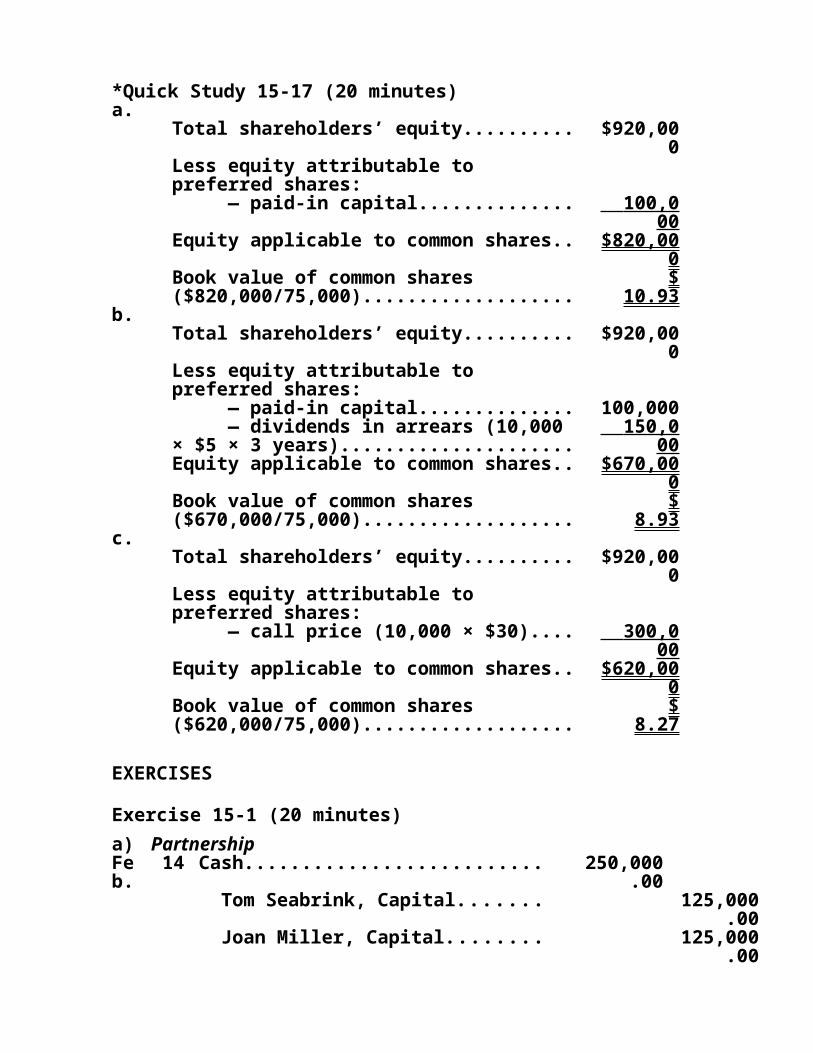

*Quick Study 15-17 (20 minutes)a.

Total shareholders’ equity................. $920,000

Less equity attributable to preferred shares: — paid-in capital........................... 100,0

00Equity applicable to common shares... $820,0

00Book value of common shares ($820,000/75,000).............................

$ 10.93

b.Total shareholders’ equity................. $920,0

00Less equity attributable to preferred shares: — paid-in capital........................... 100,00

0 — dividends in arrears (10,000 × $5 × 3 years).........................................

150,0 00

Equity applicable to common shares... $670,000

Book value of common shares ($670,000/75,000).............................

$ 8.93

c.Total shareholders’ equity................. $920,0

00Less equity attributable to preferred shares: — call price (10,000 × $30)............ 300,0

00Equity applicable to common shares... $620,0

00Book value of common shares ($620,000/75,000).............................

$ 8.27

EXERCISES

Exercise 15-1 (20 minutes)a) PartnershipFeb.

14

Cash......................................... 250,000.00

Tom Seabrink, Capital.......... 125,000.00

Joan Miller, Capital............... 125,00

0.00 To record investment into business by partners.

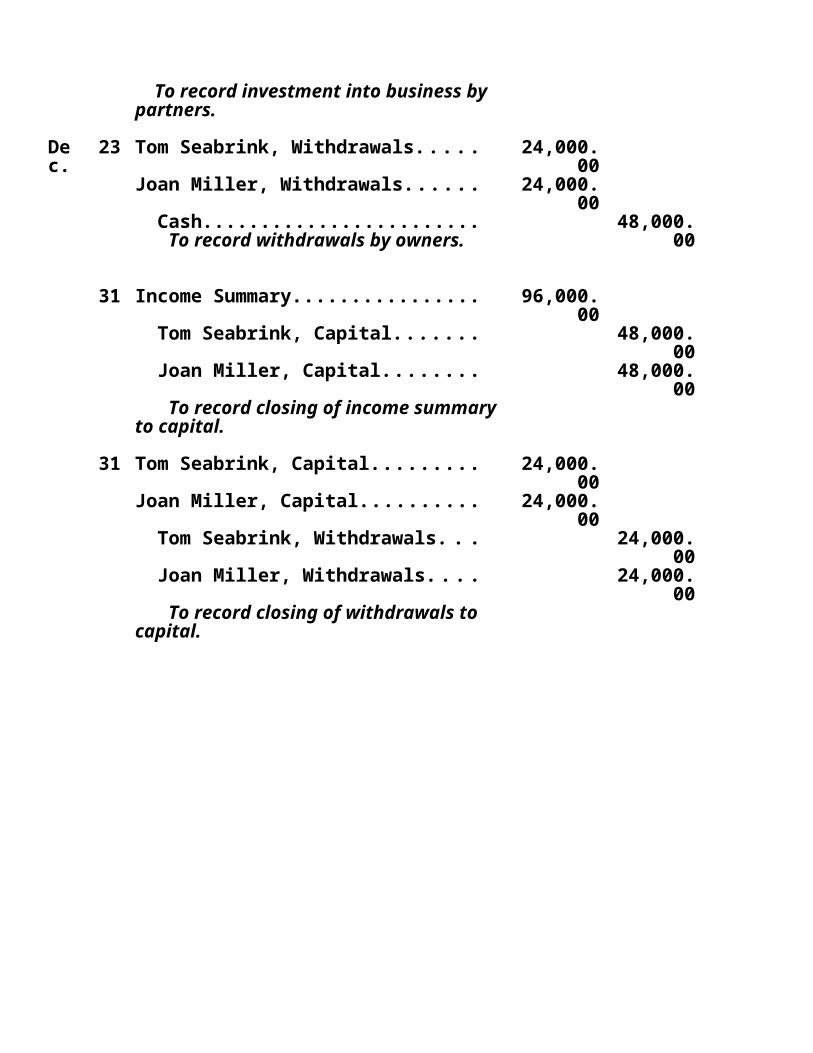

Dec.

23

Tom Seabrink, Withdrawals....... 24,000.00

Joan Miller, Withdrawals............ 24,000.00

Cash.................................... To record withdrawals by owners.

48,000.00

31

Income Summary....................... 96,000.00

Tom Seabrink, Capital.......... 48,000.00

Joan Miller, Capital............... 48,000.00

To record closing of income summary to capital.

31

Tom Seabrink, Capital................ 24,000.00

Joan Miller, Capital.................... 24,000.00

Tom Seabrink, Withdrawals. . 24,000.00

Joan Miller, Withdrawals....... 24,000.00

To record closing of withdrawals to capital.

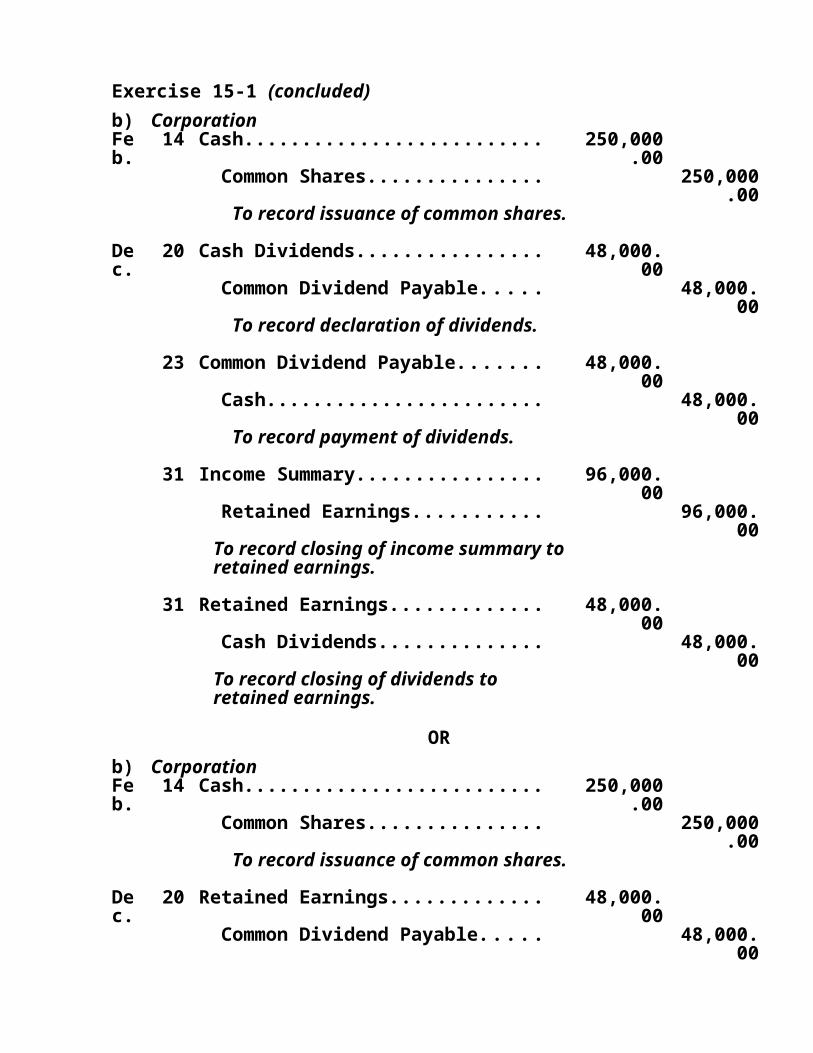

Exercise 15-1 (concluded)b) CorporationFeb.

14

Cash......................................... 250,000.00

Common Shares................... 250,000.00

To record issuance of common shares.

Dec.

20

Cash Dividends.......................... 48,000.00

Common Dividend Payable. . . 48,000.00

To record declaration of dividends.

23

Common Dividend Payable......... 48,000.00

Cash.................................... 48,000.00

To record payment of dividends.

31

Income Summary....................... 96,000.00

Retained Earnings................ 96,000.00

To record closing of income summary to retained earnings.

31

Retained Earnings..................... 48,000.00

Cash Dividends.................... 48,000.00

To record closing of dividends to retained earnings.

ORb) CorporationFeb.

14

Cash......................................... 250,000.00

Common Shares................... 250,000.00

To record issuance of common shares.

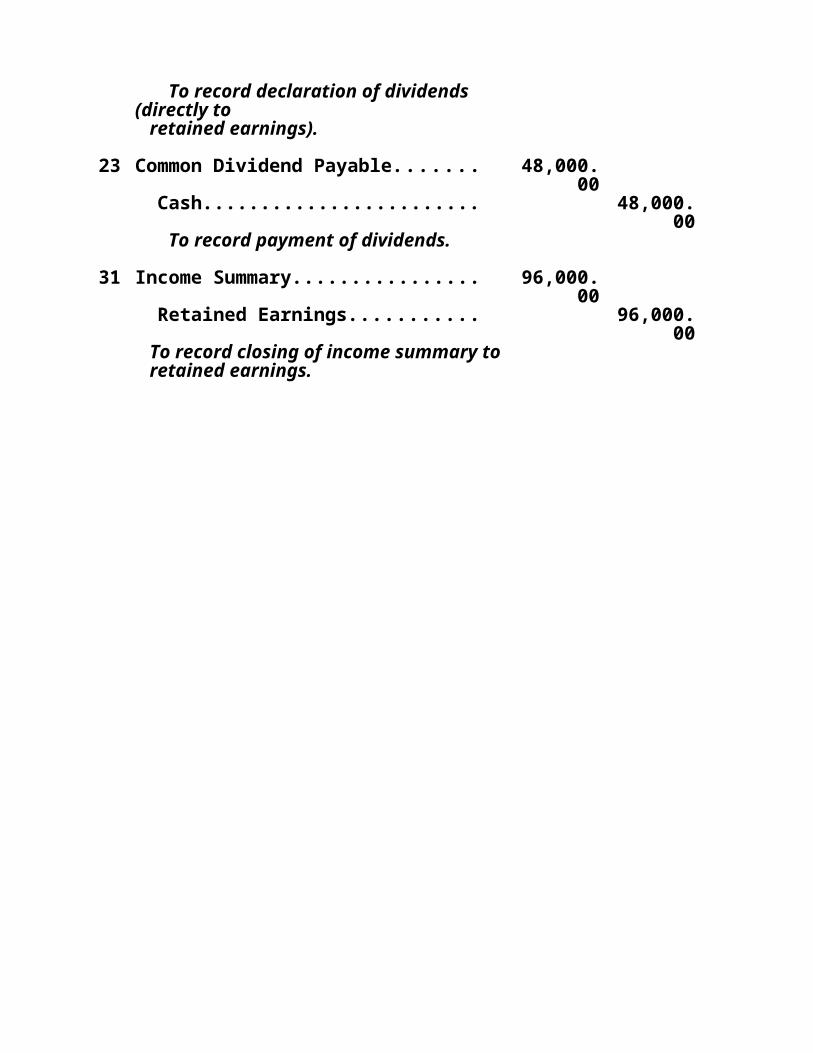

De 2 Retained Earnings..................... 48,000.

c. 0 00 Common Dividend Payable. . . 48,000.

00 To record declaration of dividends (directly to retained earnings).

23

Common Dividend Payable......... 48,000.00

Cash.................................... 48,000.00

To record payment of dividends.

31

Income Summary....................... 96,000.00

Retained Earnings................ 96,000.00

To record closing of income summary to retained earnings.

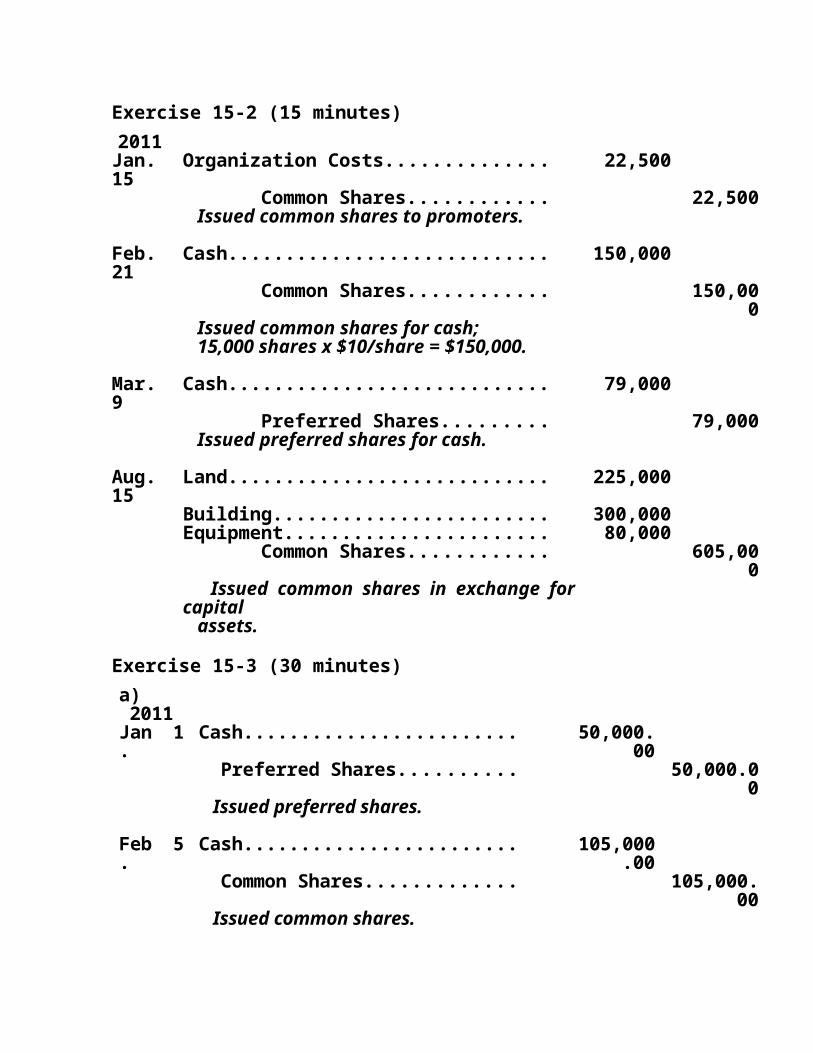

Exercise 15-2 (15 minutes)2011Jan. 15

Organization Costs....................... 22,500

Common Shares..................... 22,500 Issued common shares to promoters.

Feb. 21

Cash............................................ 150,000

Common Shares..................... 150,000

Issued common shares for cash; 15,000 shares x $10/share = $150,000.

Mar. 9

Cash............................................ 79,000

Preferred Shares.................... 79,000 Issued preferred shares for cash.

Aug. 15

Land............................................ 225,000

Building....................................... 300,000

Equipment.................................... 80,000 Common Shares..................... 605,00

0 Issued common shares in exchange for capital assets.

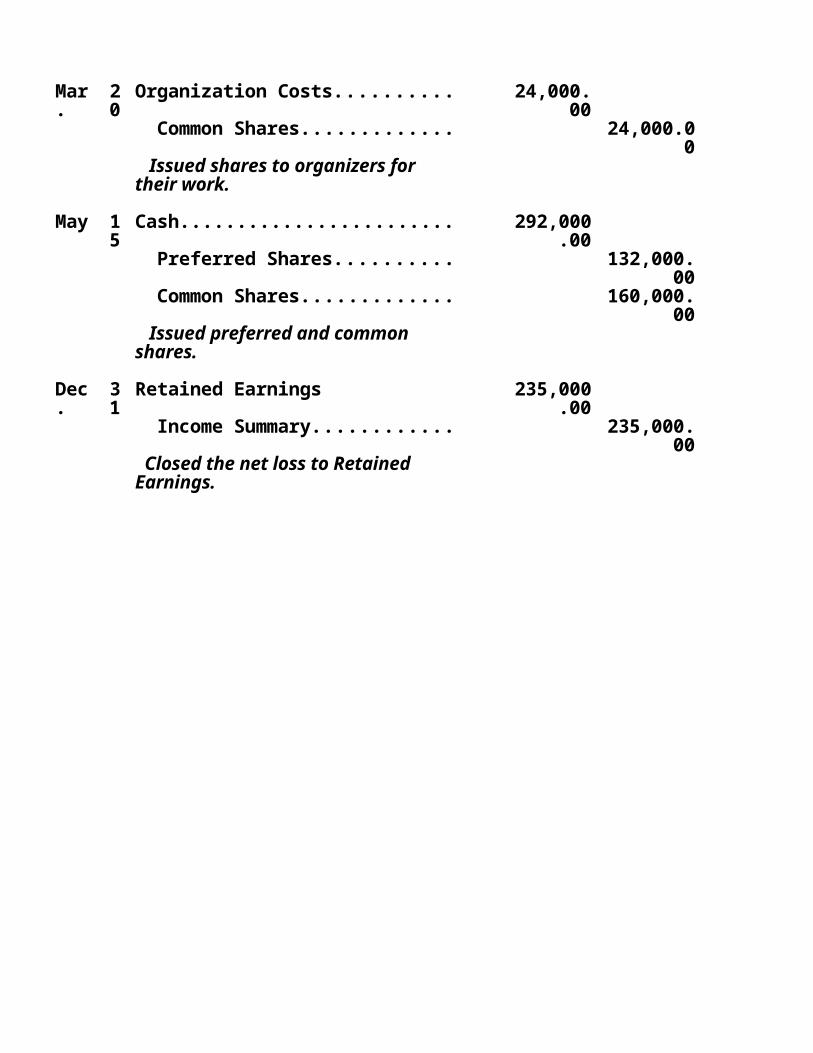

Exercise 15-3 (30 minutes)a)2011

Jan.

1 Cash...................................... 50,000.00

Preferred Shares............... 50,000.00

Issued preferred shares.

Feb.

5 Cash...................................... 105,000.00

Common Shares................ 105,000.00

Issued common shares.

Mar.

20

Organization Costs................. 24,000.00

Common Shares................ 24,000.00

Issued shares to organizers for their work.

May

15

Cash...................................... 292,000.00

Preferred Shares............... 132,000.00

Common Shares................ 160,000.00

Issued preferred and common shares.

Dec.

31

Retained Earnings 235,000.00

Income Summary.............. 235,000.00

Closed the net loss to Retained Earnings.

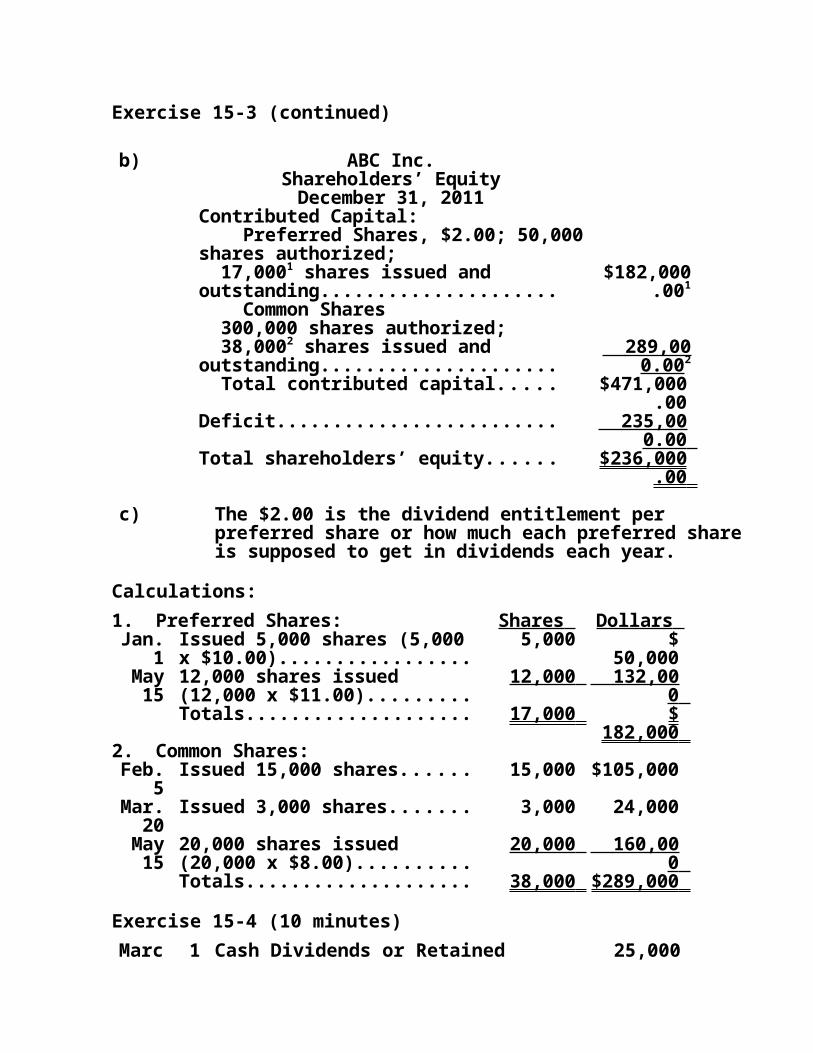

Exercise 15-3 (continued)

b) ABC Inc.Shareholders’ EquityDecember 31, 2011

Contributed Capital: Preferred Shares, $2.00; 50,000 shares authorized; 17,0001 shares issued and outstanding.................................

$182,000.001

Common Shares 300,000 shares authorized; 38,0002 shares issued and outstanding.................................

289,00 0.002

Total contributed capital........... $471,000.00

Deficit......................................... 235,00 0.00

Total shareholders’ equity............ $236,000.00

c) The $2.00 is the dividend entitlement per preferred share or how much each preferred share is supposed to get in dividends each year.

Calculations:1. Preferred Shares: Shares Dollars

Jan. 1

Issued 5,000 shares (5,000 x $10.00)...........................

5,000 $ 50,000

May 15

12,000 shares issued (12,000 x $11.00)...............

12,000 132,00 0

Totals................................ 17,000 $ 182,000

2. Common Shares:Feb.

5Issued 15,000 shares.......... 15,000 $105,00

0Mar.

20Issued 3,000 shares............ 3,000 24,000

May 15

20,000 shares issued (20,000 x $8.00).................

20,000 160,00 0

Totals................................ 38,000 $289,000

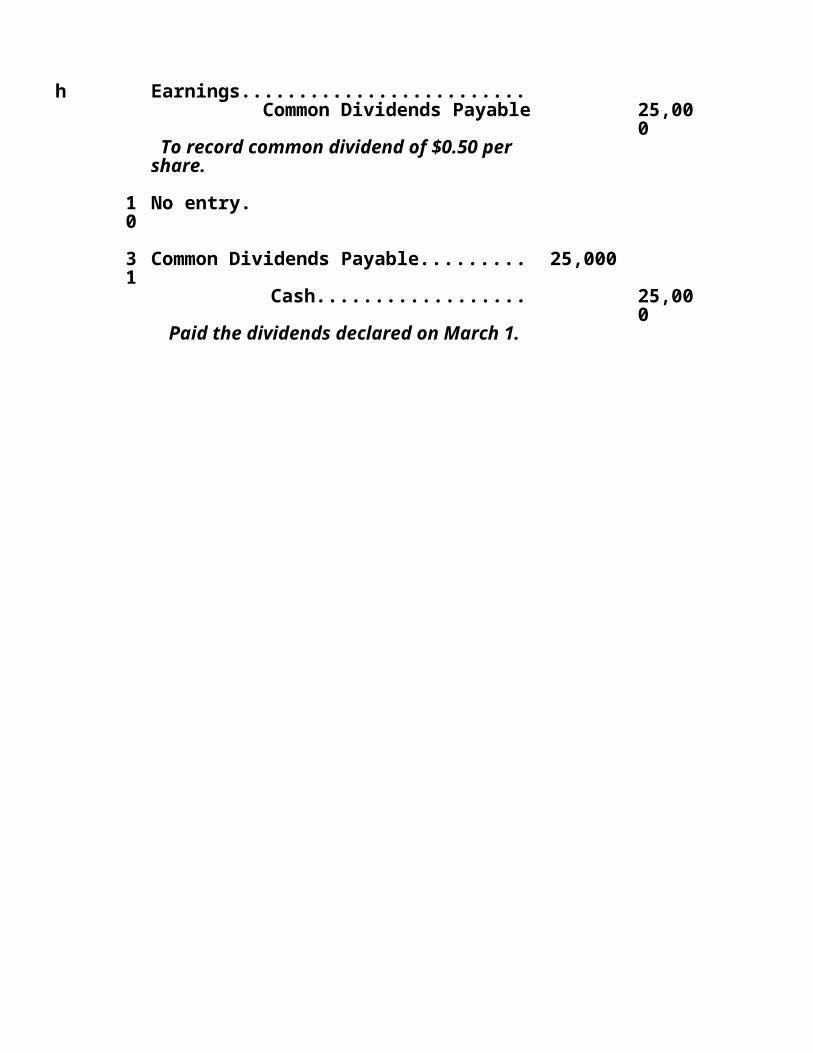

Exercise 15-4 (10 minutes)March

1 Cash Dividends or Retained Earnings........................................

25,000

Common Dividends Payable. . 25,000

To record common dividend of $0.50 per share.

10

No entry.

31

Common Dividends Payable........... 25,000

Cash................................... 25,000

Paid the dividends declared on March 1.

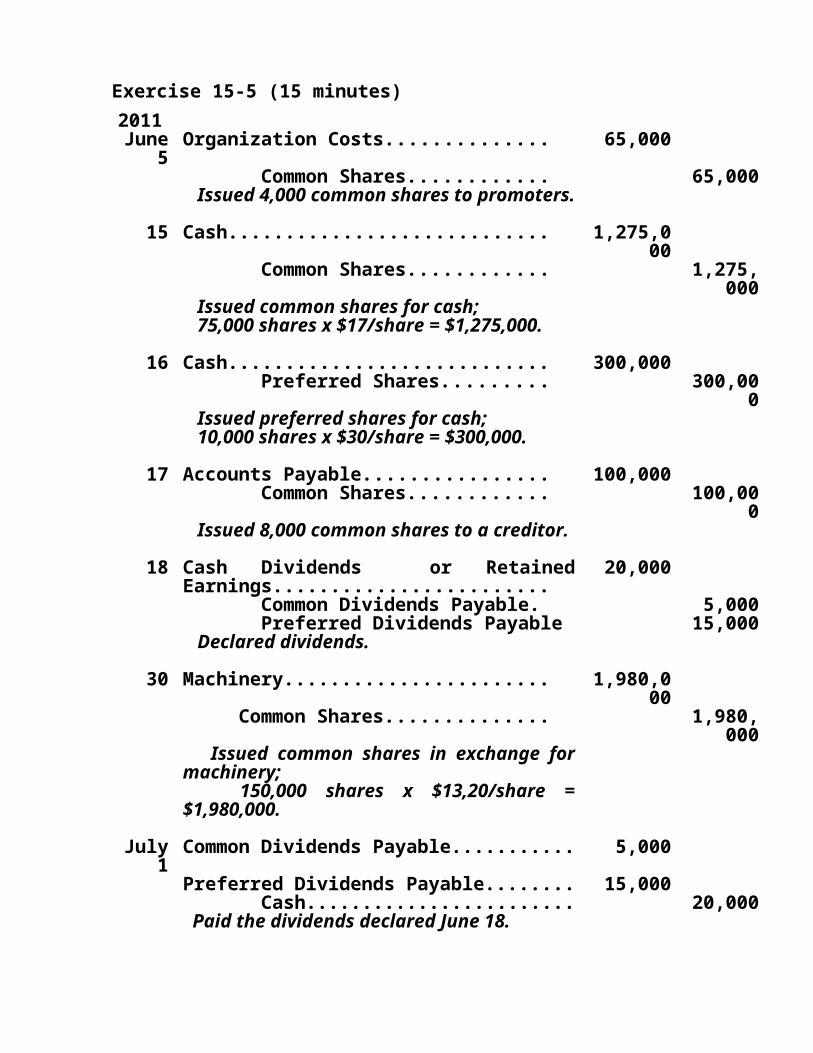

Exercise 15-5 (15 minutes)2011June

5Organization Costs....................... 65,000

Common Shares..................... 65,000 Issued 4,000 common shares to promoters.

15 Cash............................................ 1,275,000

Common Shares..................... 1,275,000

Issued common shares for cash; 75,000 shares x $17/share = $1,275,000.

16 Cash............................................ 300,000

Preferred Shares.................... 300,000

Issued preferred shares for cash; 10,000 shares x $30/share = $300,000.

17 Accounts Payable......................... 100,000

Common Shares..................... 100,000

Issued 8,000 common shares to a creditor.

18 Cash Dividends or Retained Earnings.......................................

20,000

Common Dividends Payable.... 5,000 Preferred Dividends Payable... 15,000 Declared dividends.

30 Machinery.................................... 1,980,000

Common Shares....................... 1,980,000

Issued common shares in exchange for machinery; 150,000 shares x $13,20/share = $1,980,000.

July Common Dividends Payable.............. 5,000

1Preferred Dividends Payable............. 15,000 Cash.......................................... 20,000 Paid the dividends declared June 18.

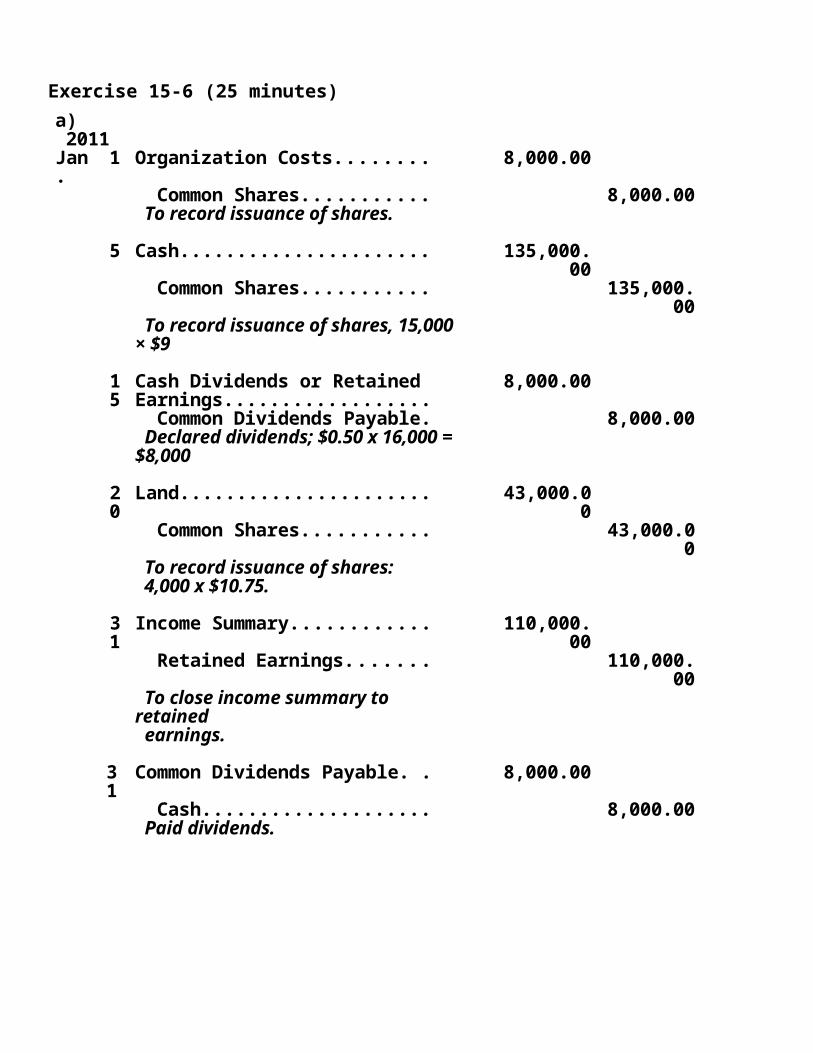

Exercise 15-6 (25 minutes)a)2011

Jan.

1 Organization Costs.............. 8,000.00

Common Shares............. 8,000.00

To record issuance of shares.

5 Cash.................................. 135,000.00

Common Shares............. 135,000.00

To record issuance of shares, 15,000 × $9

15

Cash Dividends or Retained Earnings.............................

8,000.00

Common Dividends Payable..............................

8,000.00

Declared dividends; $0.50 x 16,000 = $8,000

20

Land.................................. 43,000.00

Common Shares............. 43,000.00

To record issuance of shares: 4,000 x $10.75.

31

Income Summary................ 110,000.00

Retained Earnings.......... 110,000.00

To close income summary to retained earnings.

31

Common Dividends Payable. 8,000.00

Cash............................. 8,000.00

Paid dividends.

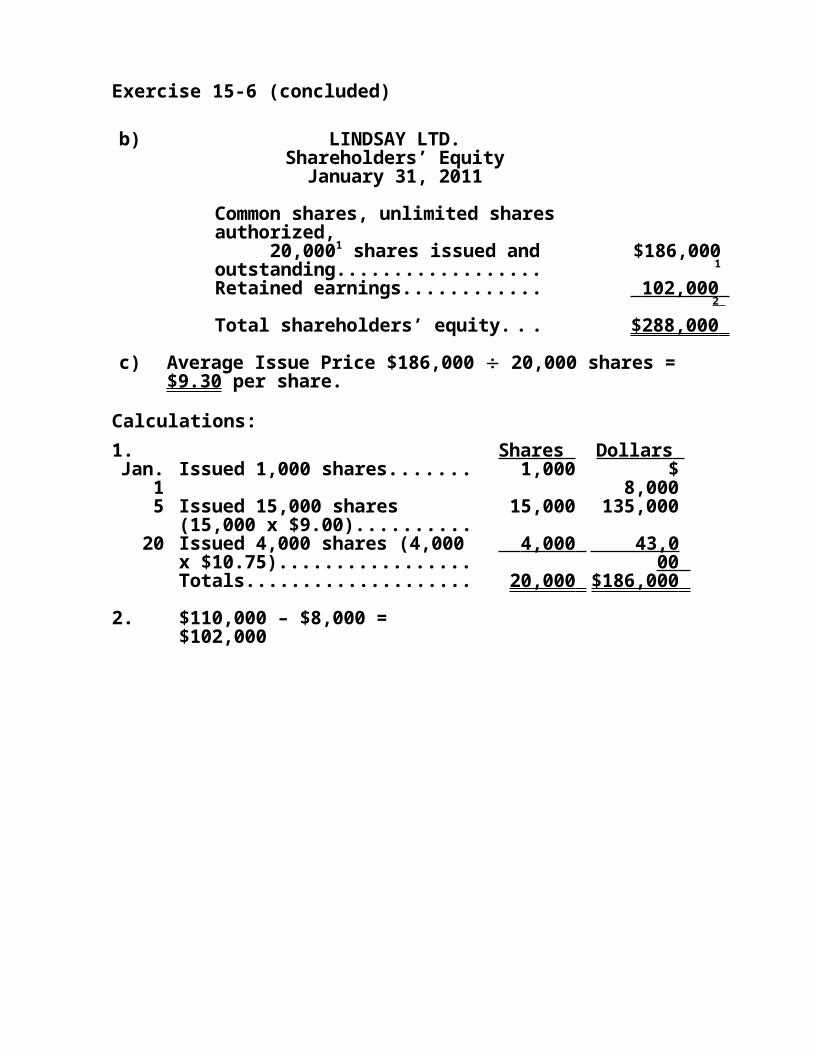

Exercise 15-6 (concluded)

b) LINDSAY LTD.Shareholders’ Equity

January 31, 2011

Common shares, unlimited shares authorized, 20,0001 shares issued and outstanding............................

$186,0001

Retained earnings................... 102,00 0 2

Total shareholders’ equity....... $288,000

c) Average Issue Price $186,000 20,000 shares = $9.30 per share.

Calculations:1. Shares Dollars

Jan. 1

Issued 1,000 shares............ 1,000 $ 8,000

5 Issued 15,000 shares (15,000 x $9.00).................

15,000 135,000

20 Issued 4,000 shares (4,000 x $10.75)...........................

4,000 43,00 0

Totals................................ 20,000 $186,000

2. $110,000 – $8,000 = $102,000

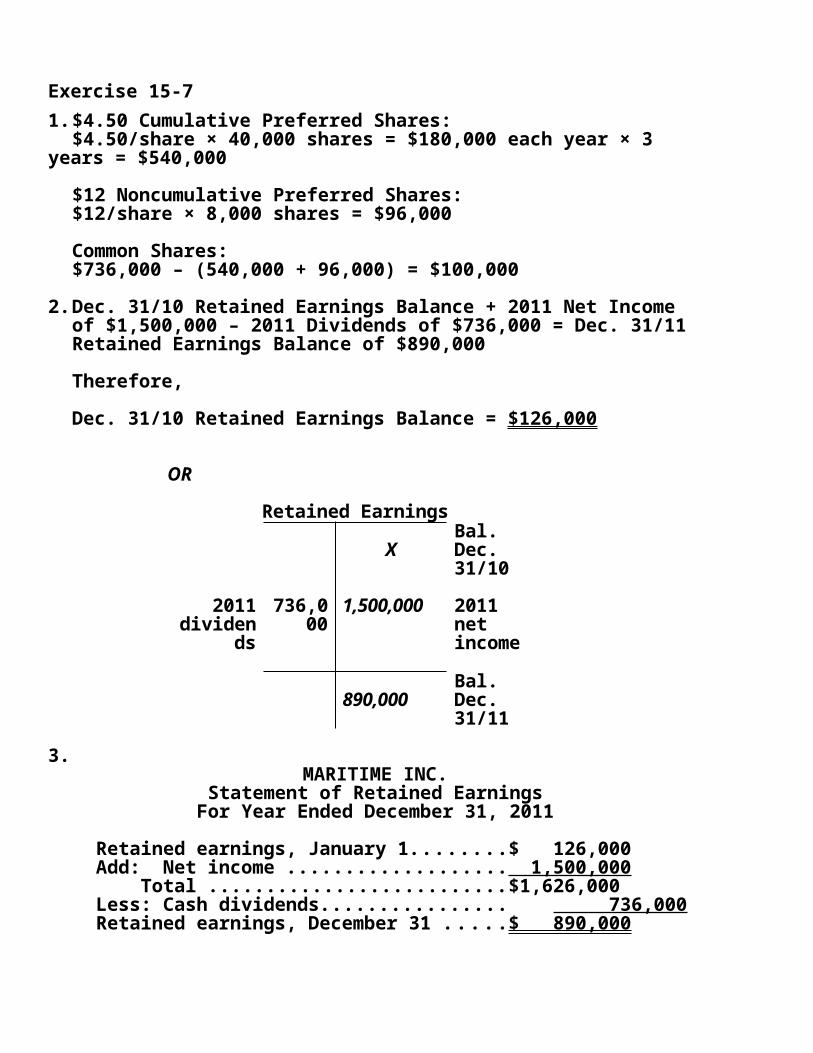

Exercise 15-71. $4.50 Cumulative Preferred Shares:

$4.50/share × 40,000 shares = $180,000 each year × 3 years = $540,000

$12 Noncumulative Preferred Shares:$12/share × 8,000 shares = $96,000

Common Shares:$736,000 – (540,000 + 96,000) = $100,000

2. Dec. 31/10 Retained Earnings Balance + 2011 Net Income of $1,500,000 – 2011 Dividends of $736,000 = Dec. 31/11 Retained Earnings Balance of $890,000

Therefore,

Dec. 31/10 Retained Earnings Balance = $126,000

OR

Retained Earnings

XBal. Dec. 31/10

2011 dividen

ds

736,000

1,500,000

2011 net income

890,000Bal.Dec. 31/11

3.MARITIME INC.

Statement of Retained EarningsFor Year Ended December 31, 2011

Retained earnings, January 1...............$ 126,000Add: Net income ............................... 1,500,000 Total ..............................................$1,626,000Less: Cash dividends........................... 736,000Retained earnings, December 31 ........$ 890,000

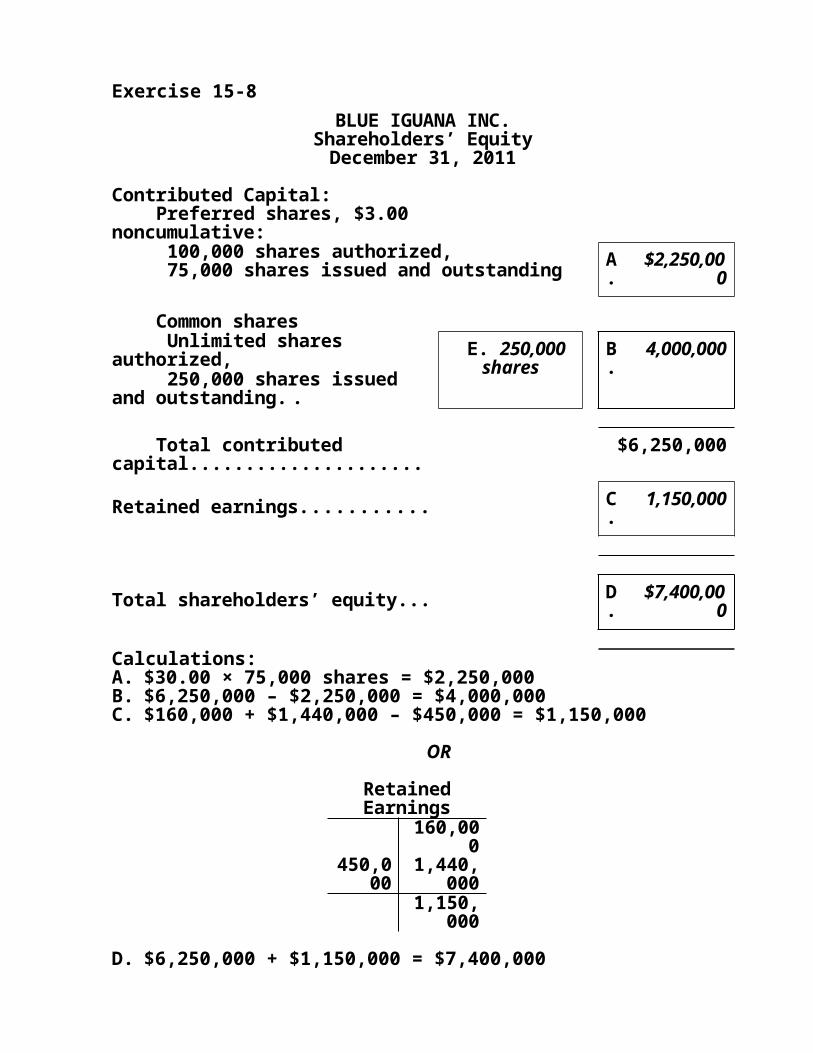

Exercise 15-8BLUE IGUANA INC.

Shareholders’ EquityDecember 31, 2011

Contributed Capital: Preferred shares, $3.00 noncumulative: 100,000 shares authorized, 75,000 shares issued and outstanding A

.$2,250,

000

Common shares Unlimited shares authorized, E. 250,000

sharesB.

4,000,000 250,000 shares issued

and outstanding...

Total contributed capital.... $6,250,000

Retained earnings.................. C.

1,150,000

Total shareholders’ equity...... D.

$7,400,000

Calculations:A. $30.00 × 75,000 shares = $2,250,000B. $6,250,000 – $2,250,000 = $4,000,000C. $160,000 + $1,440,000 – $450,000 = $1,150,000

OR

Retained Earnings

160,000

450,000

1,440,000

1,150,000

D. $6,250,000 + $1,150,000 = $7,400,000E. $4,000,000 $16.00 = 250,000 shares

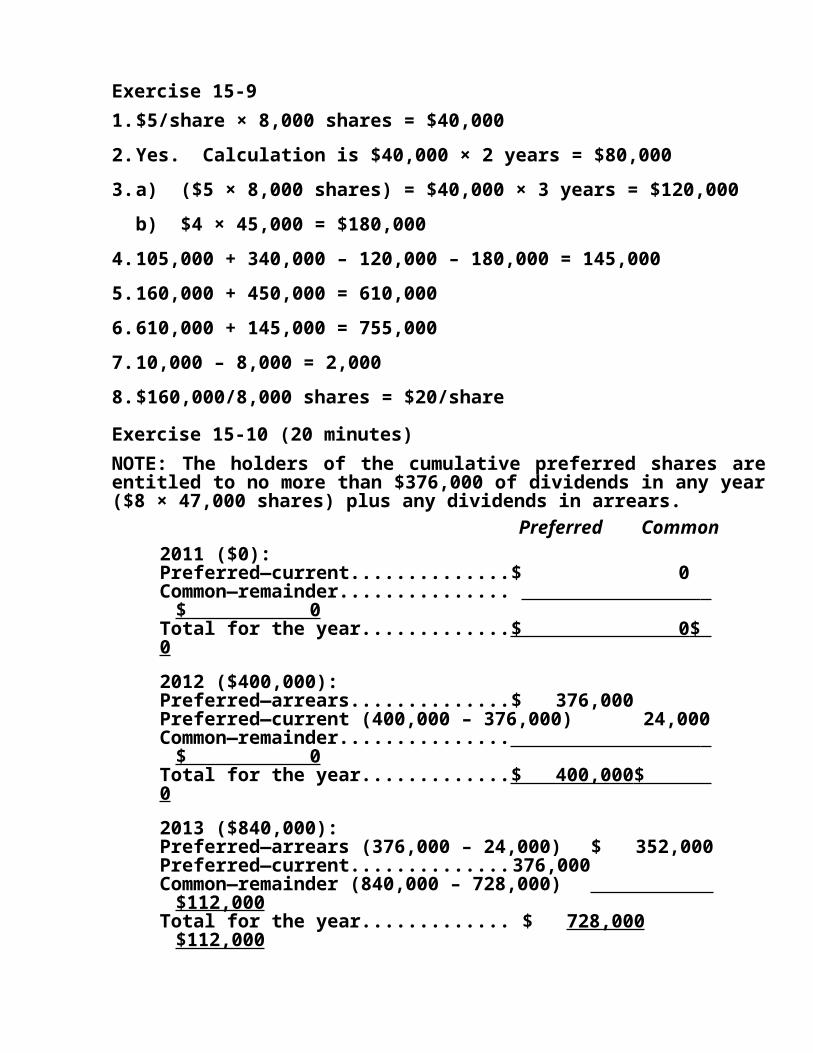

Exercise 15-91. $5/share × 8,000 shares = $40,0002. Yes. Calculation is $40,000 × 2 years = $80,0003. a) ($5 × 8,000 shares) = $40,000 × 3 years = $120,000

b) $4 × 45,000 = $180,0004. 105,000 + 340,000 – 120,000 – 180,000 = 145,0005. 160,000 + 450,000 = 610,0006. 610,000 + 145,000 = 755,0007. 10,000 – 8,000 = 2,0008. $160,000/8,000 shares = $20/share

Exercise 15-10 (20 minutes)NOTE: The holders of the cumulative preferred shares are entitled to no more than $376,000 of dividends in any year ($8 × 47,000 shares) plus any dividends in arrears.

Preferred Common2011 ($0):Preferred—current.....................$ 0Common—remainder.................. $ 0Total for the year.......................$ 0$ 02012 ($400,000):Preferred—arrears......................$ 376,000Preferred—current (400,000 – 376,000) 24,000Common—remainder.................. $ 0Total for the year.......................$ 400,000$ 02013 ($840,000):Preferred—arrears (376,000 – 24,000) $ 352,000Preferred—current.....................376,000Common—remainder (840,000 – 728,000)

.................$112,000Total for the year....................... $ 728,000

$112,000

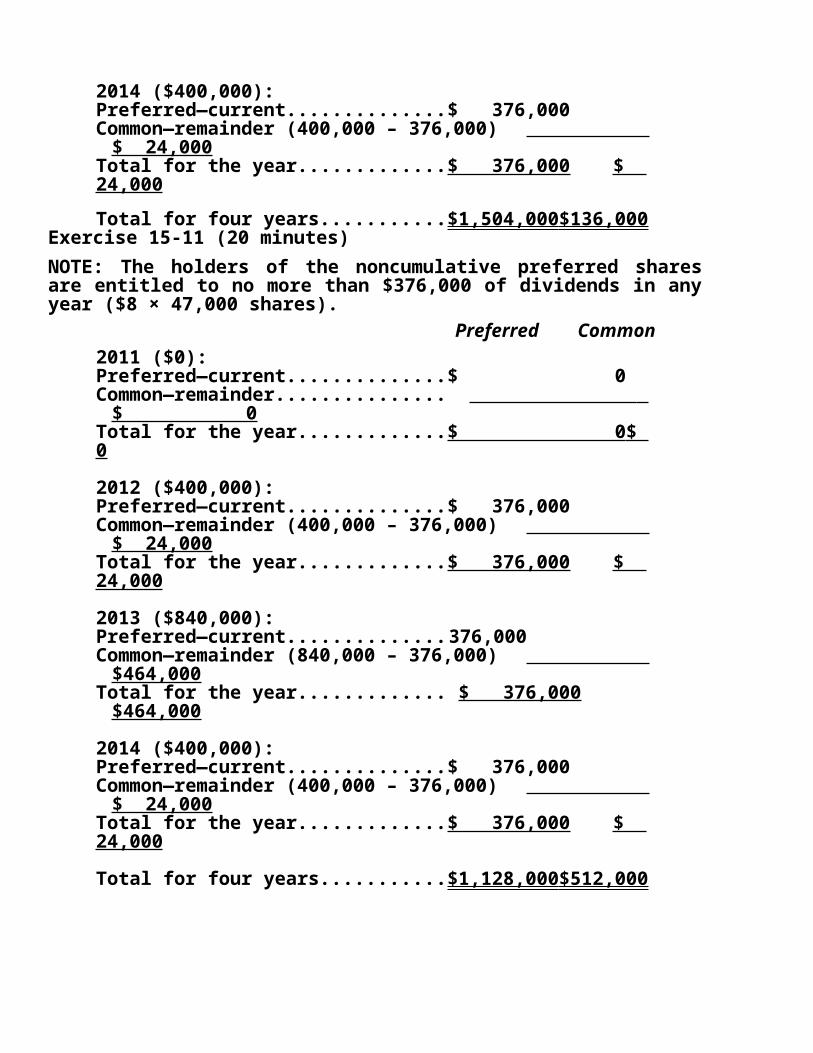

2014 ($400,000):Preferred—current.....................$ 376,000Common—remainder (400,000 – 376,000)

..................$ 24,000Total for the year.......................$ 376,000 $ 24,000Total for four years....................$1,504,000

$136,000Exercise 15-11 (20 minutes)NOTE: The holders of the noncumulative preferred shares are entitled to no more than $376,000 of dividends in any year ($8 × 47,000 shares).

Preferred Common2011 ($0):Preferred—current.....................$ 0Common—remainder.................. $ 0Total for the year.......................$ 0$ 0

2012 ($400,000):Preferred—current.....................$ 376,000Common—remainder (400,000 – 376,000)

..................$ 24,000Total for the year.......................$ 376,000 $ 24,000

2013 ($840,000):Preferred—current.....................376,000Common—remainder (840,000 – 376,000)

..................$464,000Total for the year....................... $ 376,000

$464,000

2014 ($400,000):Preferred—current.....................$ 376,000Common—remainder (400,000 – 376,000)

..................$ 24,000Total for the year.......................$ 376,000 $ 24,000

Total for four years....................$1,128,000$512,000

Exercise 15-12 (10 minutes)

1. B2. A3. F4. E5. D6. C

Exercise 15-131. (15,000 shares × $4.50/share) × 2 years = $135,000

2. $150,000 Total dividends – $135,000 paid to preferred shareholders = $15,000 to common shareholders

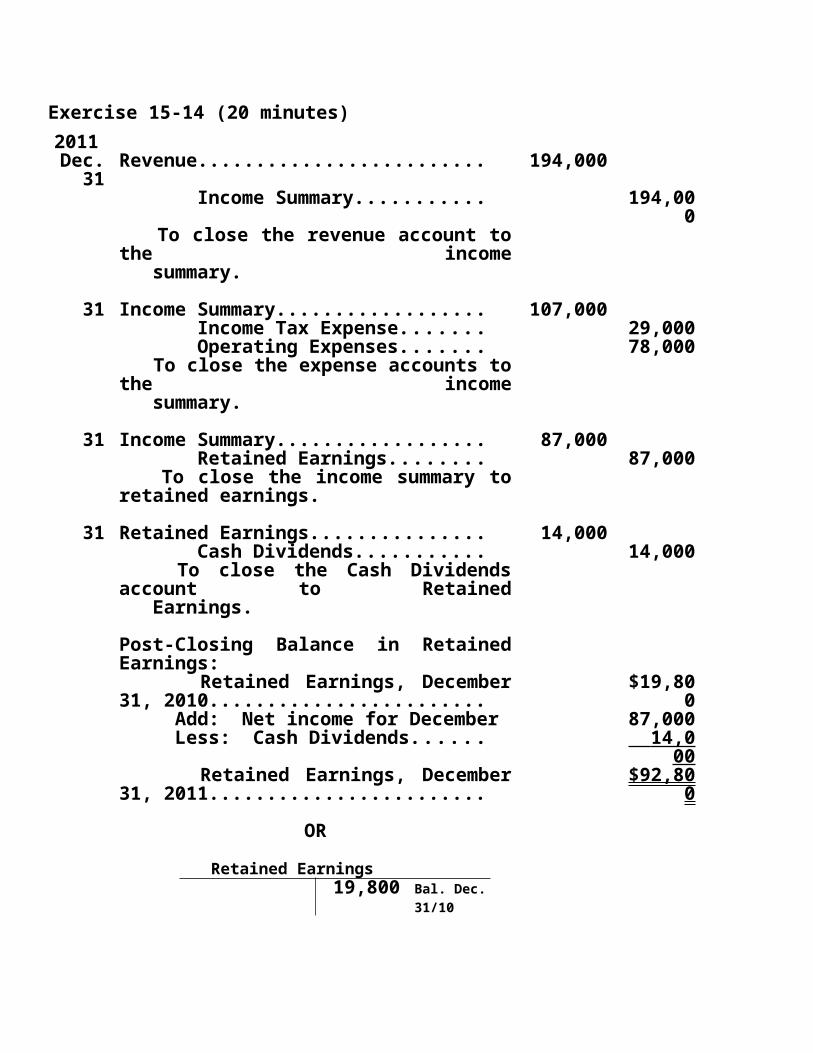

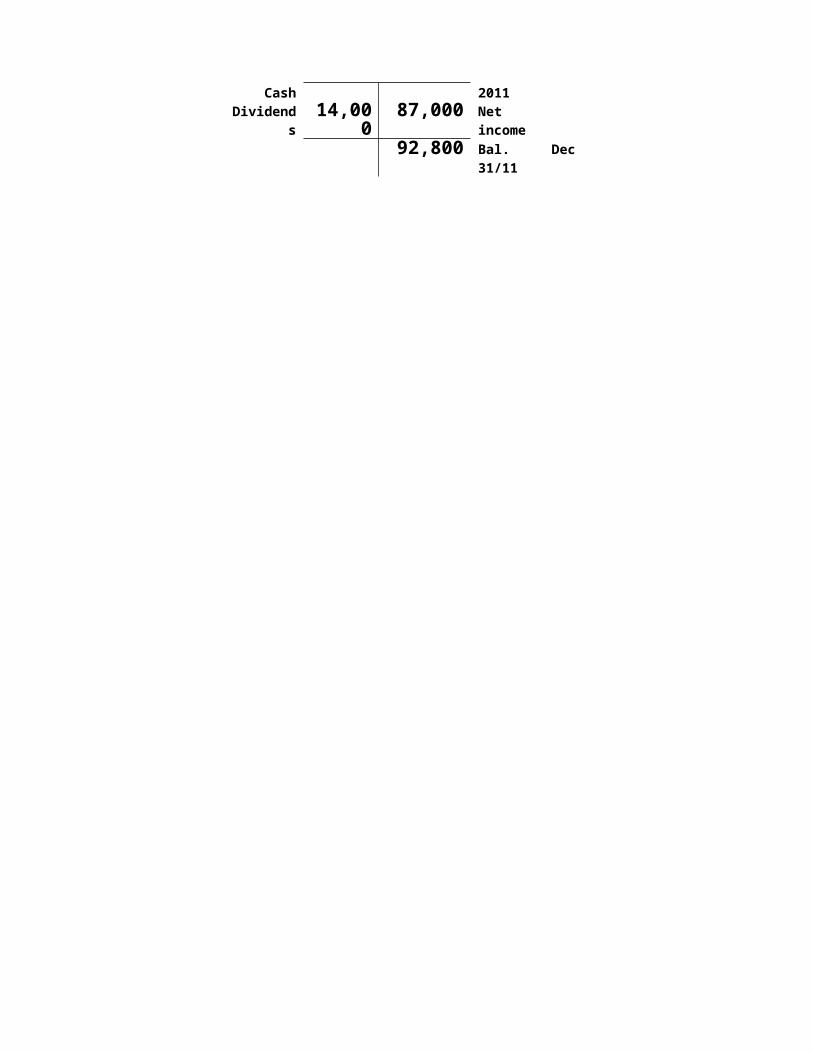

Exercise 15-14 (20 minutes)2011Dec.

31Revenue....................................... 194,00

0 Income Summary................... 194,00

0 To close the revenue account to the income summary.

31 Income Summary.......................... 107,000

Income Tax Expense............... 29,000 Operating Expenses............... 78,000 To close the expense accounts to the income summary.

31 Income Summary.......................... 87,000 Retained Earnings.................. 87,000 To close the income summary to retained earnings.

31 Retained Earnings........................ 14,000 Cash Dividends...................... 14,000 To close the Cash Dividends account to Retained Earnings.

Post-Closing Balance in Retained Earnings: Retained Earnings, December 31, 2010............................................

$19,800

Add: Net income for December 87,000 Less: Cash Dividends............... 14,00

0 Retained Earnings, December 31, 2011............................................

$92,800

OR

Retained Earnings19,800 Bal. Dec.

31/10

Cash Dividend

s14,00

087,000

2011Net income

92,800 Bal. Dec 31/11

Exercise 15-15 (30 minutes)Gildan Corp.

Balance SheetDecember 31, 2011

Assets Current assets: Cash.................................. $ 6,000 Accounts receivable........... 28,000 Total current assets......... $34,00

0 Property, plant and equipment: Land................................. $84,000 Warehouse........................ $92,0

00 Less: Accumulated amortization...............................

15, 200

76,800

Equipment......................... $56,000

Less: Accumulated amortization...............................

7,6 00

48,400

Total property, plant and equipment..................................

209,200

Total assets................................ $243,200

Liabilities Current liabilities : Accounts payable.............. $ 18,400 Long-term liabilities: Long term note payable, due in 2014................................

24,000

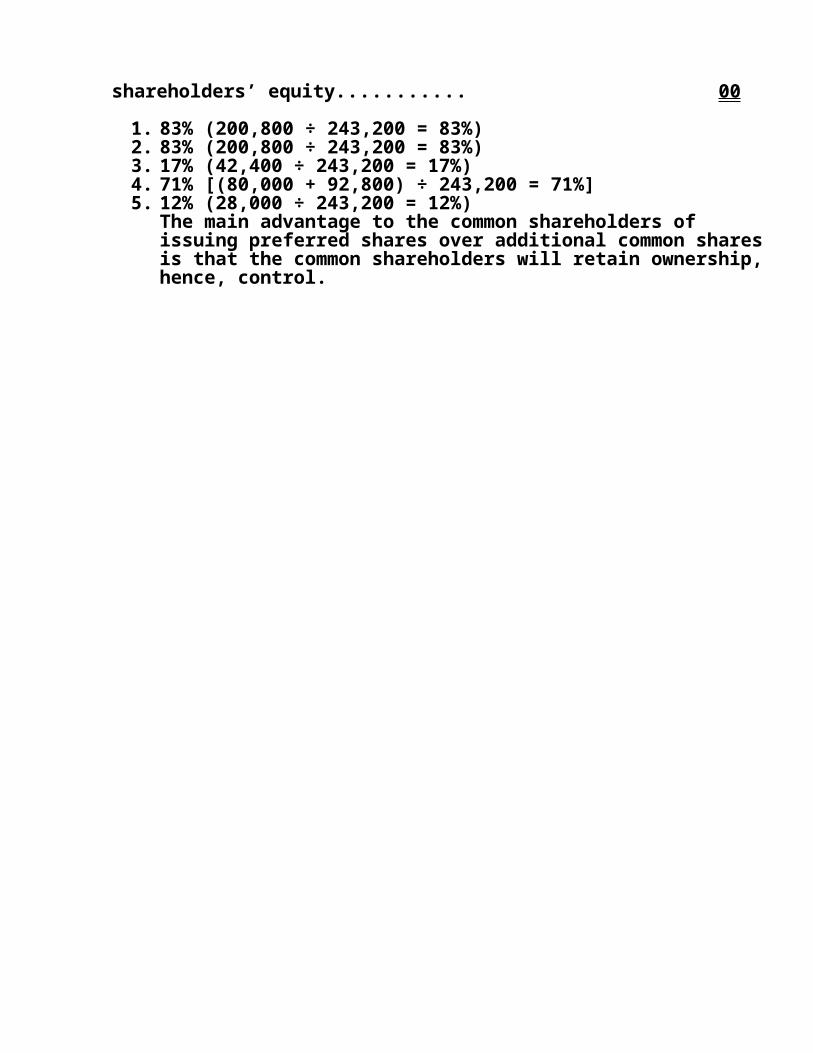

Total liabilities............................ $ 42,400

Shareholders’ Equity Contributed Capital: Preferred shares..................................................................

$28,000

Common shares................. 80,000 Total contributed capital. . $108,00

0 Retained earnings.................. 92,800 Total shareholders’ equity........... 200,80

0Total liabilities and shareholders’ $243,2

equity........................................ 00

1. 83% (200,800 ÷ 243,200 = 83%)2. 83% (200,800 ÷ 243,200 = 83%)3. 17% (42,400 ÷ 243,200 = 17%)4. 71% [(80,000 + 92,800) ÷ 243,200 = 71%]5. 12% (28,000 ÷ 243,200 = 12%)

The main advantage to the common shareholders of issuing preferred shares over additional common shares is that the common shareholders will retain ownership, hence, control.

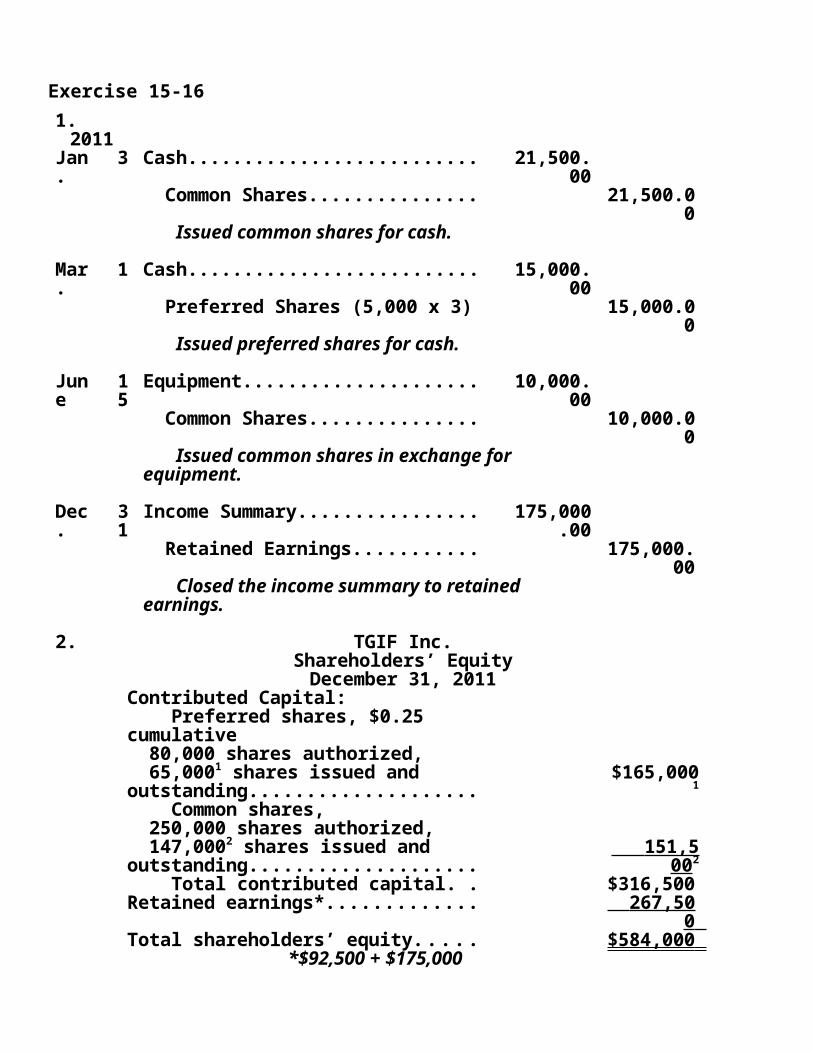

Exercise 15-161.2011

Jan. 3 Cash........................................ 21,500.00

Common Shares.................. 21,500.00

Issued common shares for cash.

Mar .

1 Cash........................................ 15,000.00

Preferred Shares (5,000 x 3) 15,000.00

Issued preferred shares for cash.

June

15

Equipment............................... 10,000.00

Common Shares.................. 10,000.00

Issued common shares in exchange for equipment.

Dec.

31

Income Summary...................... 175,000.00

Retained Earnings............... 175,000.00

Closed the income summary to retained earnings.

2. TGIF Inc.Shareholders’ EquityDecember 31, 2011

Contributed Capital: Preferred shares, $0.25 cumulative 80,000 shares authorized, 65,0001 shares issued and outstanding................................

$165,0001

Common shares, 250,000 shares authorized, 147,0002 shares issued and outstanding................................

151,50 02

Total contributed capital.......... $316,500

Retained earnings*..................... 267,50 0

Total shareholders’ equity........... $584,000

*$92,500 + $175,0003.

15,000

4.

103,000

Exercise 15-16 (concluded)

Calculations:1. Preferred Shares: Shares Dollars

Jan. 1

Balance brought forward..... 60,000 $150,000

Mar. 1

Issued 5,000 shares (5,000 x $3.00).............................

5,000 15,00 0

Totals................................ 65,000 $165,000

2. Common Shares: Shares Dollars Jan.

1Balance brought forward..... 120,000 $120,00

03 20,000 shares issued.......... 20,000 21,500

Jun. 15

Issued 7,000 shares............ 7,000 10,00 0

Totals................................ 147,000 $151,500

Exercise 15-17Part A

2011

Oct. 1

Cash.............................................. 4,000

Preferred Shares....................... 4,000 Issued preferred shares; 1,000 shares × $4.00/share.

10 Cash.............................................. 150,000

Common Shares........................ 150,000

Issued common shares; 50,000 shares × $3.00/share.

12 Organization Costs......................... 11,250 Preferred Shares....................... 11,250 Issued preferred shares in exchange for organization efforts; 2,500 shares × $4.50/share.

15 Land.............................................. 155,000

Cash......................................... 55,000 Notes Payable........................... 100,00

0 Purchased land in exchange for cash and a note.

20 Cash.............................................. 70,500 Preferred Shares....................... 70,500 Issued preferred shares for cash.

24 Cash Dividends (or Retained Earnings).......................................

31,650

Common Dividends Payable....... 22,400 Preferred Dividends Payable...... 9,250 Declared dividends; 18,500 preferred shares × $0.50 = $9,250.

31 Cash.............................................. 750,000

Revenues.................................. 750,000

To record revenues.

31 Expenses....................................... 250,000

Cash......................................... 250,000

To record expenses.

31 Income Summary........................... 500,000

Retained Earnings..................... 500,000

To record closing of income summary to retained earnings.

31 Retained Earnings*........................ 31,650 Cash Dividends......................... 31,650 To record closing of dividends to retained earnings(*or no entry if on Oct. 24 it was debited to Retained Earnings).

Exercise 15-17 (concluded)Part B

ABC INC.Balance Sheet

October 31, 2011Assets Current assets: Cash.......................................... $669,

500 Property, plant and equipment: Land......................................... 155,0

00 Intangible assets: Organization costs.................... 11,

250Total assets........................................ $835,

750

Liabilities Current liabilities Dividends payable..................... $

31,650

Long term liabilities: Long term note payable............. 100,0

00Total liabilities.................................... $131,

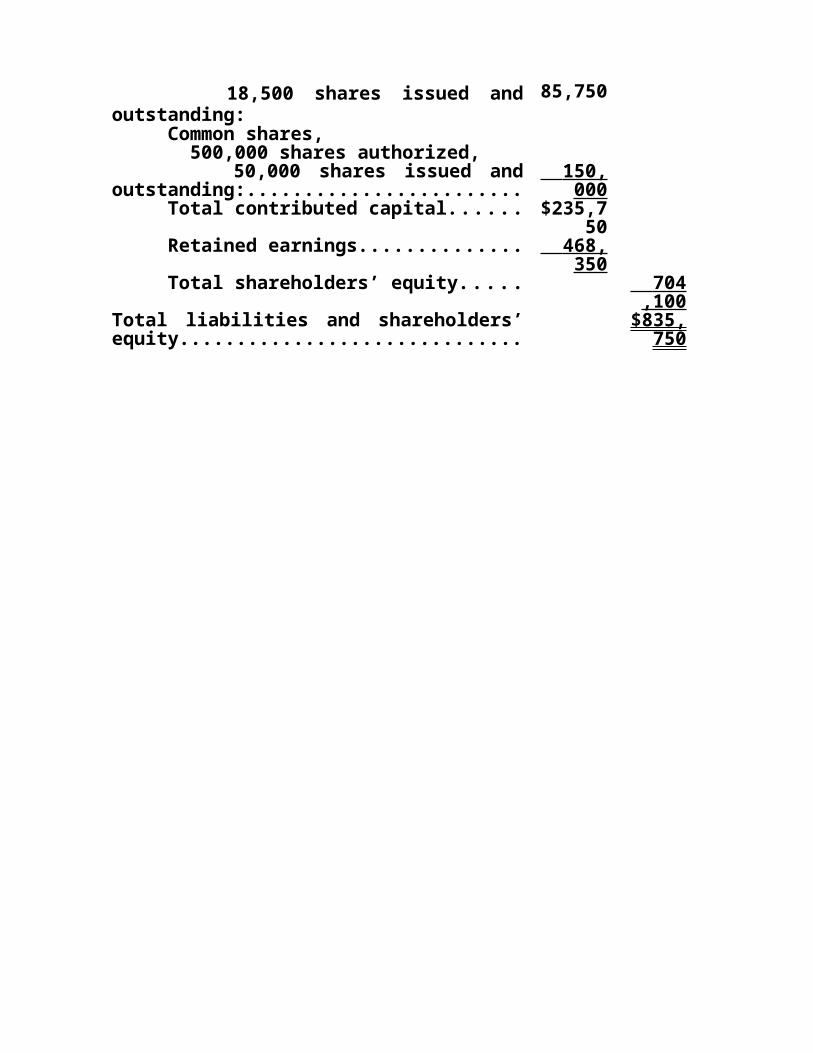

650

Shareholders’ EquityContributed Capital: Preferred shares, $0.50 cumulative, 100,000 shares authorized, 18,500 shares issued and outstanding:

$ 85,75

0 Common shares, 500,000 shares authorized, 50,000 shares issued and outstanding:.......................................

150, 000

Total contributed capital................ $235,750

Retained earnings.......................... 468, 350

Total shareholders’ equity.............. 704, 100

Total liabilities and shareholders’ equity................................................

$835,750

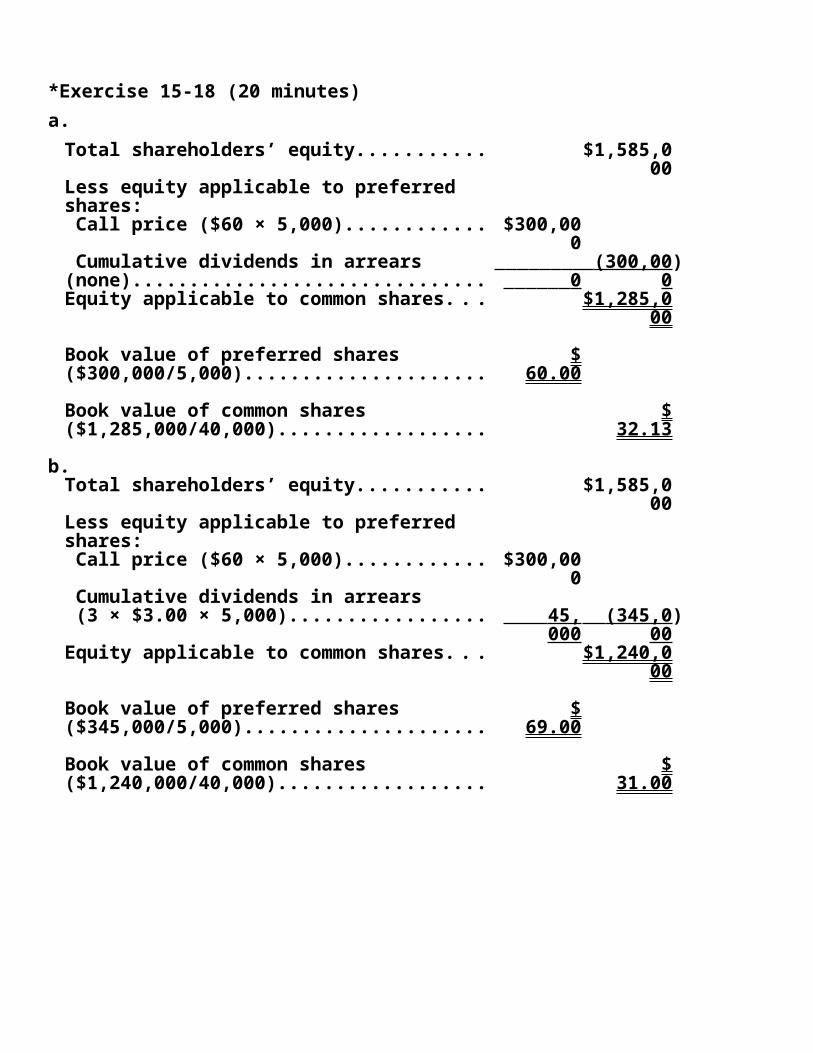

*Exercise 15-18 (20 minutes)a.

Total shareholders’ equity.................... $1,585,000

Less equity applicable to preferred shares: Call price ($60 × 5,000)...................... $300,00

0 Cumulative dividends in arrears (none)

0 (300,00

0)

Equity applicable to common shares..... $1,285,000

Book value of preferred shares ($300,000/5,000)..................................

$ 60.00

Book value of common shares ($1,285,000/40,000).............................

$ 32.13

b.Total shareholders’ equity.................... $1,585,

000Less equity applicable to preferred shares: Call price ($60 × 5,000)...................... $300,00

0 Cumulative dividends in arrears (3 × $3.00 × 5,000)............................ 45,00

0 (345,0

00)

Equity applicable to common shares..... $1,240,000

Book value of preferred shares ($345,000/5,000)..................................

$ 69.00

Book value of common shares ($1,240,000/40,000).............................

$ 31.00

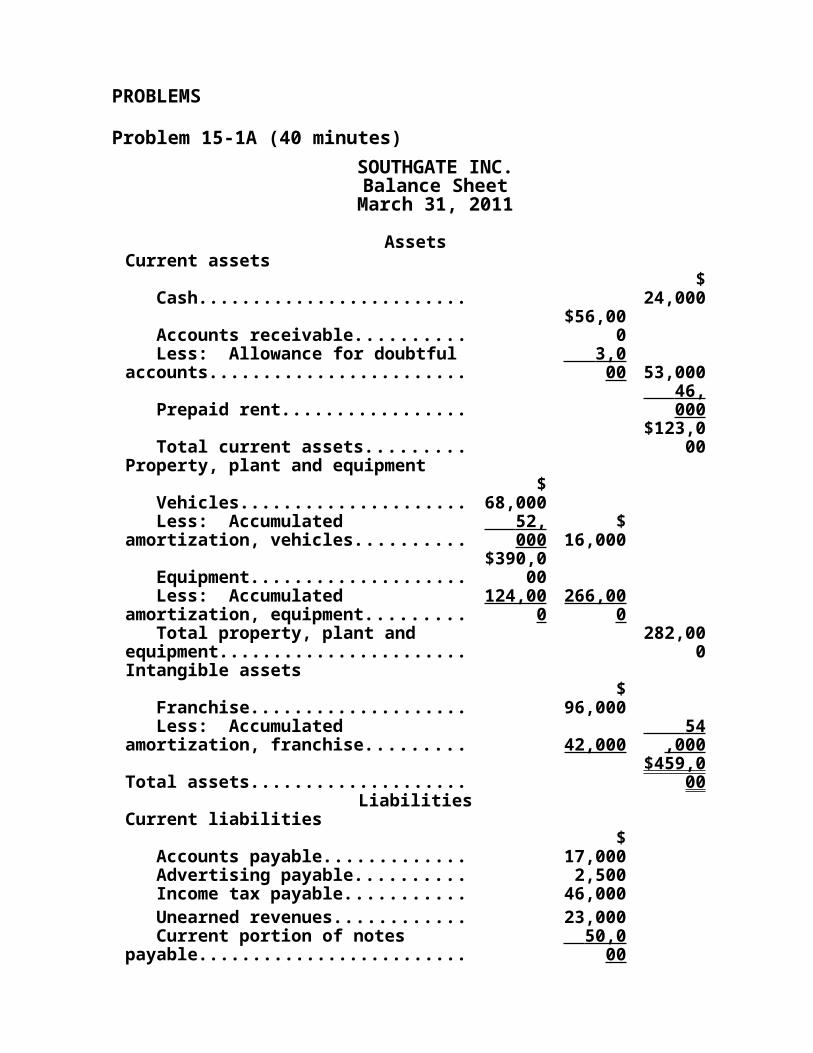

PROBLEMS

Problem 15-1A (40 minutes)SOUTHGATE INC.

Balance SheetMarch 31, 2011

AssetsCurrent assets

Cash..........................................

$ 24,00

0

Accounts receivable...................$56,0

00 Less: Allowance for doubtful accounts......................................

3,00 0

53,000

Prepaid rent.............................. 46,0

00

Total current assets...................$123,

000Property, plant and equipment

Vehicles....................................

$ 68,00

0

Less: Accumulated amortization, vehicles...................

52,0 00

$ 16,00

0

Equipment.................................$390,

000 Less: Accumulated amortization, equipment...............

124,000

266,000

Total property, plant and equipment....................................

282,000

Intangible assets

Franchise..................................

$ 96,00

0 Less: Accumulated amortization, franchise.................

42,000

54, 000

Total assets..................................$459,

000Liabilities

Current liabilities

Accounts payable.......................

$ 17,00

0

Advertising payable................... 2,500

Income tax payable....................46,00

0

Unearned revenues....................23,00

0

Current portion of notes payable 50,0

00

Total current liabilities...............

$ 138,5

00Long-term liabilities Notes payable, less $50,000 current portion.............................

70,0 00

Total liabilities.............................208,5

00Shareholders' equity

Contributed capital Common shares, 100,000 shares authorized,

25,000 shares issued............$200,

000

Retained earnings...................... 50,5

00

Total shareholders' equity.......... 250,

500Total liabilities and shareholders' equity..........................................

$459,000

Problem 15-1A (concluded)

Analysis component:1. 45.42% (208,500/459,000 × 100)2. 54.58% (100 – 45.42)3. Assuming that 37% of Southgate’s

assets were financed by debt at March 31, 2010, the balance sheet has not been strengthened over the current year.

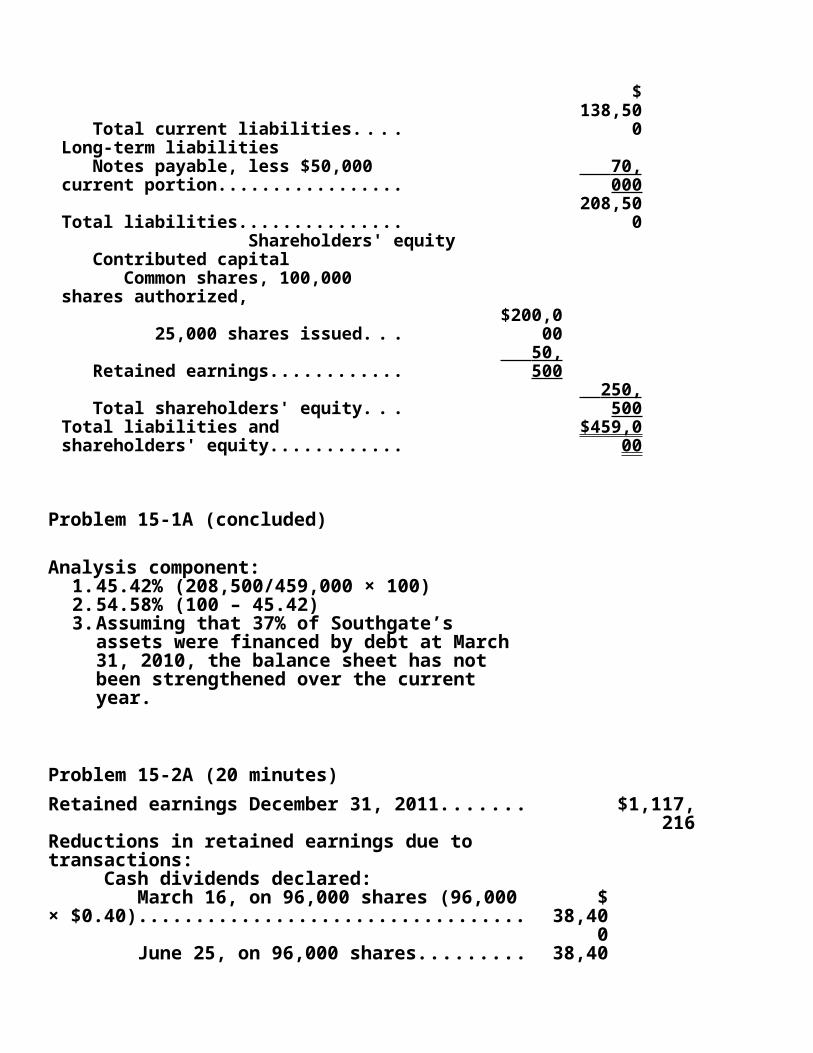

Problem 15-2A (20 minutes)Retained earnings December 31, 2011.......... $1,117,

216

Reductions in retained earnings due to transactions: Cash dividends declared: March 16, on 96,000 shares (96,000 × $0.40)..........................................................

$ 38,40

0 June 25, on 96,000 shares..................... 38,40

0 Sept. 25, on 96,000 shares.................... 38,40

0 Nov. 22, on 115,200 shares (115,200 × $0.40)

46,0 80

161,280

Less: Retained earnings December 31, 2012. 919,2 00

Net loss....................................................... $ 36,736

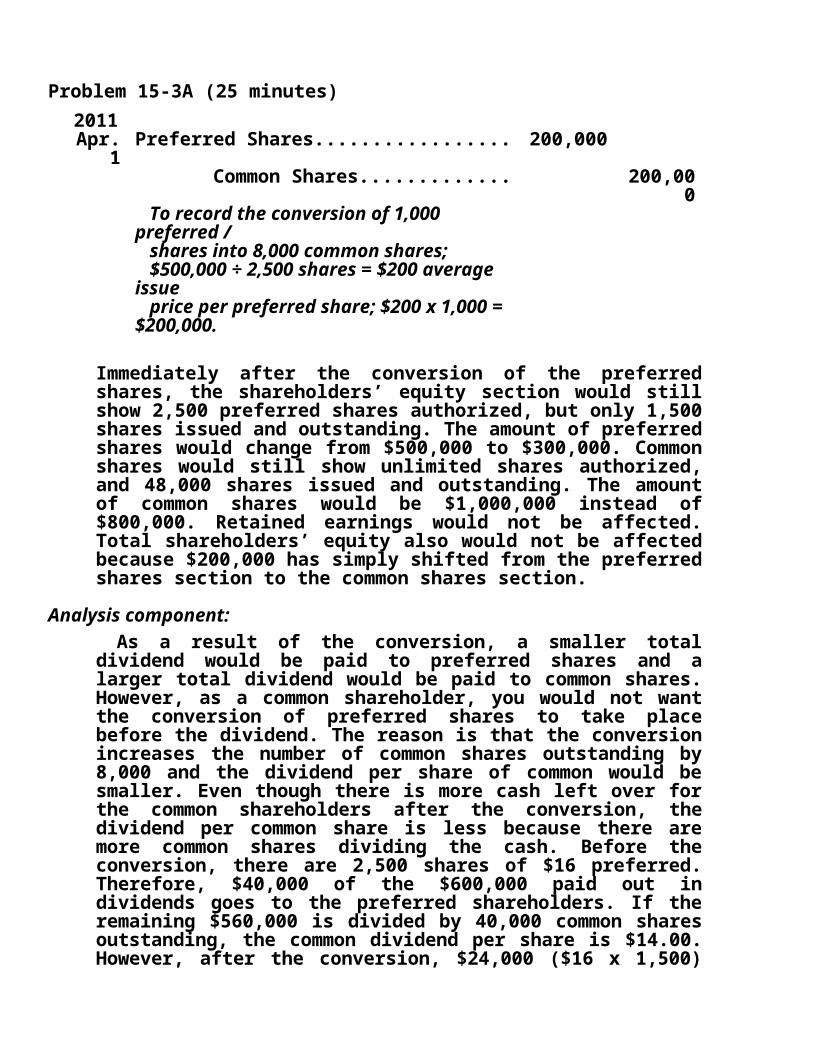

Problem 15-3A (25 minutes)201

1Apr.

1Preferred Shares............................ 200,00

0 Common Shares...................... 200,00

0 To record the conversion of 1,000 preferred / shares into 8,000 common shares; $500,000 ÷ 2,500 shares = $200 average issue price per preferred share; $200 x 1,000 = $200,000.

Immediately after the conversion of the preferred shares, the shareholders’ equity section would still show 2,500 preferred shares authorized, but only 1,500 shares issued and outstanding. The amount of preferred shares would change from $500,000 to $300,000. Common shares would still show unlimited shares authorized, and 48,000 shares issued and outstanding. The amount of common shares would be $1,000,000 instead of $800,000. Retained earnings would not be affected. Total shareholders’ equity also would not be affected because $200,000 has simply shifted from the preferred shares section to the common shares section.

Analysis component: As a result of the conversion, a smaller total dividend would be paid to preferred shares and a larger total dividend would be paid to common shares. However, as a common shareholder, you would not want the conversion of preferred shares to take place before the dividend. The reason is that the conversion increases the number of common shares outstanding by 8,000 and the dividend per share of common would be smaller. Even though there is more cash left over for the common shareholders after the conversion, the dividend per common share is less because there are more common shares dividing the cash. Before the conversion, there are 2,500 shares of $16 preferred. Therefore, $40,000 of the $600,000 paid out in dividends goes to the preferred shareholders. If the remaining $560,000 is divided by 40,000 common shares outstanding, the common dividend per share is $14.00. However, after the conversion, $24,000 ($16 x

1,500) of the $600,000 paid out in dividends goes to the 1,500 shares of $16 preferred, and the remaining $576,000 is divided between the 48,000 common shares outstanding. This reduces the dividend per share to $12.00.

Problem 15-4A (25 minutes)1. $450,000/$15 per share = 30,000 shares2. 325,000 shares × $8 per share = $2,600,0003. 450,000 + 2,600,000 = 3,050,000

4. $3,050,000 – $2,890,000 = $160,000 Deficit

5. 2,890,000 – 3,050,000 = 160,000 Deficit; 320,000 + 160,000 = 480,000 Net Loss

6. a) $2.50/share × 30,000 shares = $75,000 to preferred shareholdersb)$100,000 – $75,000 paid to preferred shareholders =

$25,000 to common shareholders7. a) $75,000/30,000 shares = $2.50/share

b)$25,000/325,000 shares = $.0769/share8. No, because the preferred shares are non-cumulative.9. Retained Earnings result when cumulative net earnings are

greater than cumulative losses + dividends. A deficit results when cumulative earnings are less than cumulative losses and dividends.

10. Dividends in arrears represent undeclared dividends that must be paid to preferred shareholders before any dividends are given to common shareholders but only if dividends are declared. Dividends payable, in contrast, are dividends that have been declared but not yet paid.

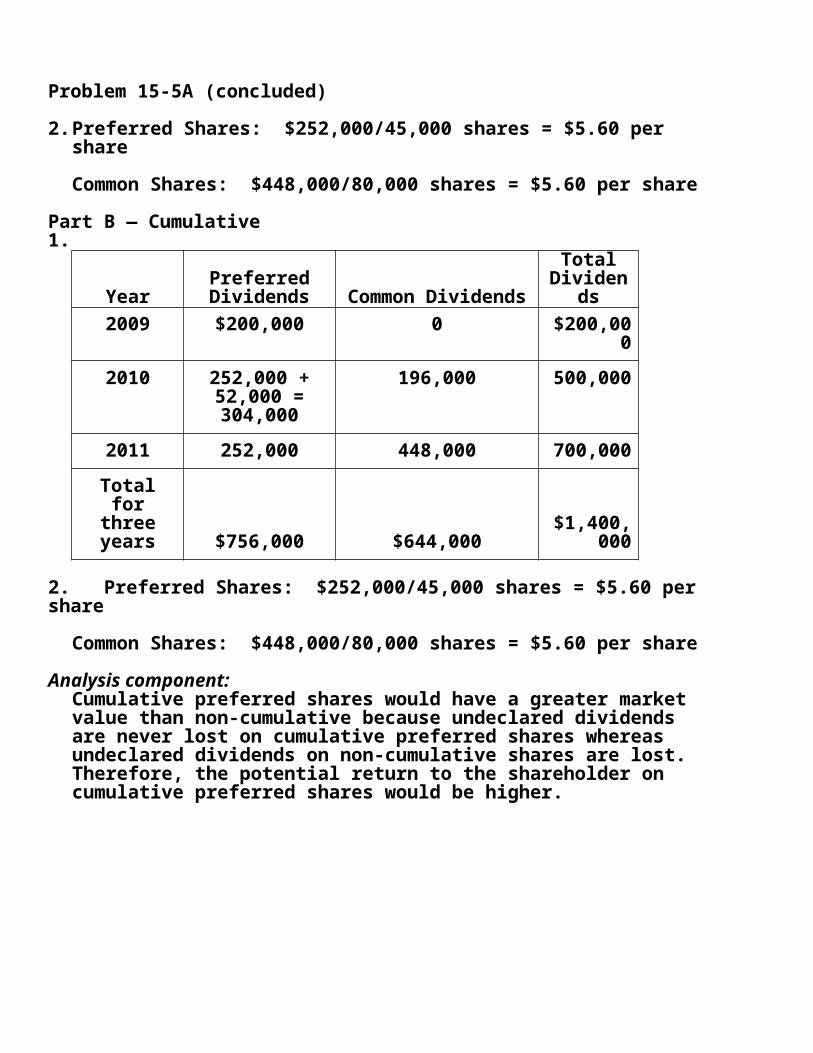

Problem 15-5A (20 minutes)Part A – Non-cumulative (maximum annual dividend: 45,000 x $5.60 = $252,000)1.

YearPreferred Dividends

Common Dividends

Total Dividen

ds2009 $200,000 0 $200,00

02010 252,000 248,000 500,000

2011 252,000 448,000 700,000Total for

three years $704,000 $696,000

$1,400,000

Problem 15-5A (concluded)

2. Preferred Shares: $252,000/45,000 shares = $5.60 per share

Common Shares: $448,000/80,000 shares = $5.60 per share

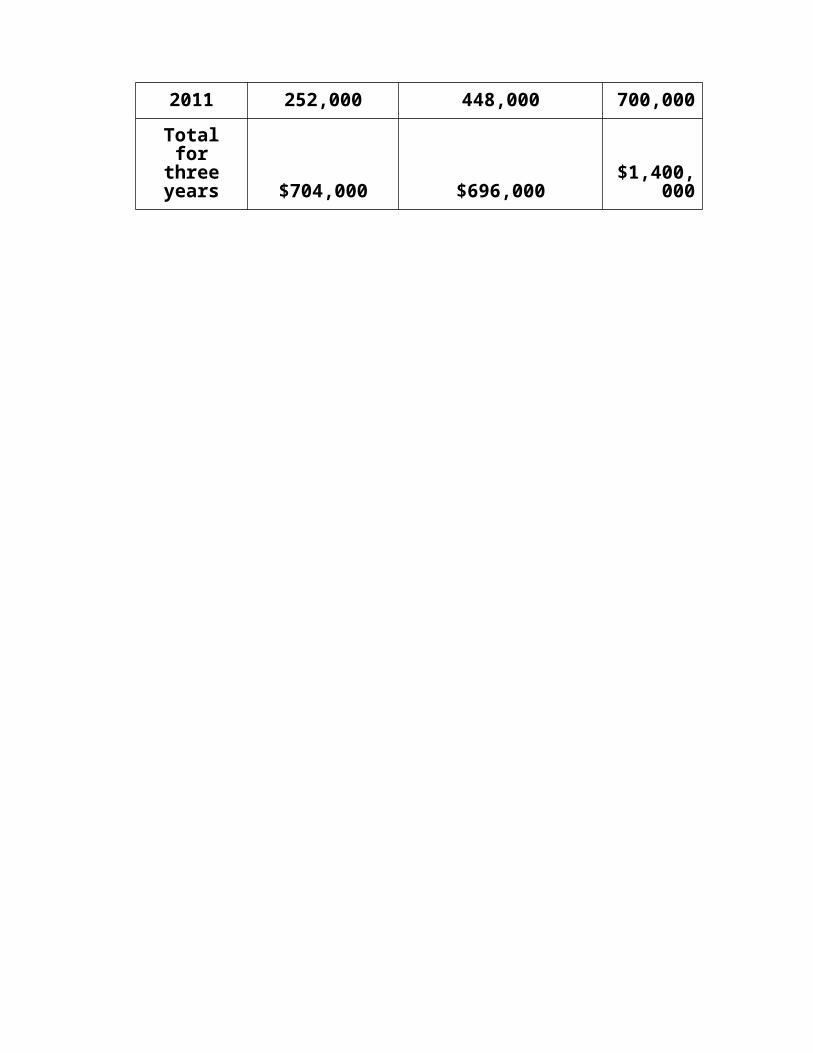

Part B — Cumulative1.

YearPreferred Dividends

Common Dividends

Total Dividen

ds2009 $200,000 0 $200,00

02010 252,000 +

52,000 = 304,000

196,000 500,000

2011 252,000 448,000 700,000Total for

three years $756,000 $644,000

$1,400,000

2. Preferred Shares: $252,000/45,000 shares = $5.60 per share

Common Shares: $448,000/80,000 shares = $5.60 per share

Analysis component:Cumulative preferred shares would have a greater market value than non-cumulative because undeclared dividends are never lost on cumulative preferred shares whereas undeclared dividends on non-cumulative shares are lost. Therefore, the potential return to the shareholder on cumulative preferred shares would be higher.

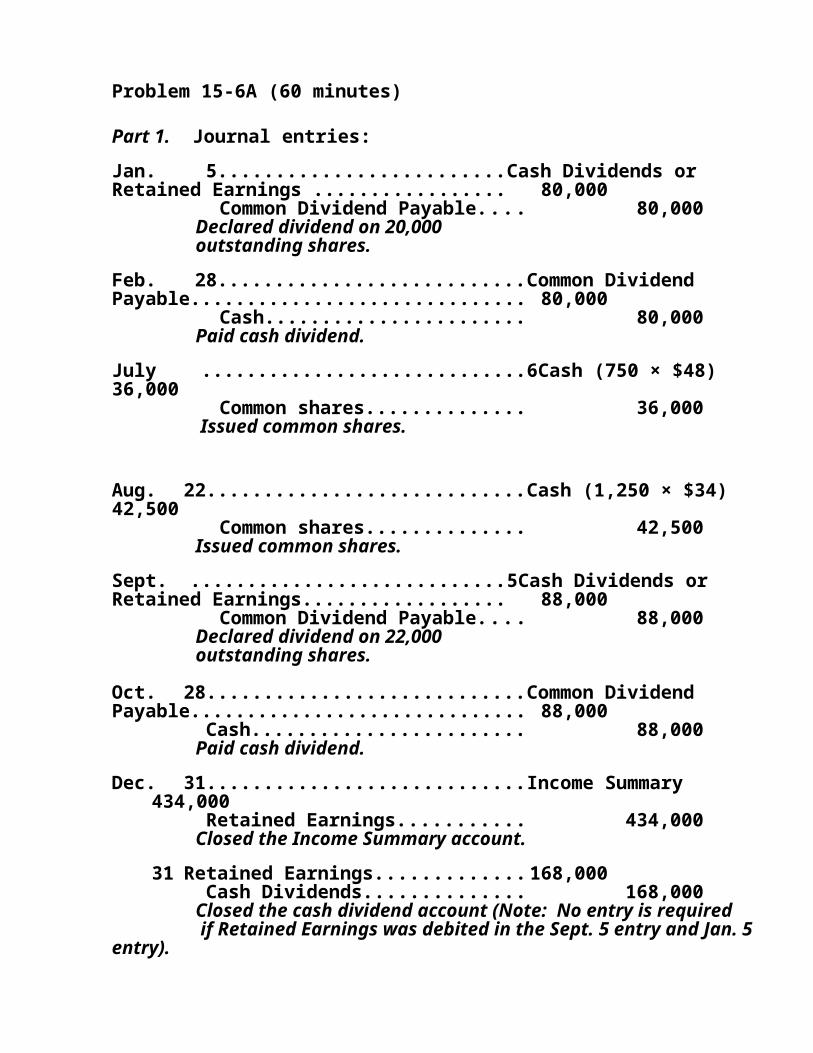

Problem 15-6A (60 minutes)

Part 1. Journal entries:Jan. 5............................................Cash Dividends or Retained Earnings ........................... 80,000

Common Dividend Payable. . . 80,000 Declared dividend on 20,000 outstanding shares.

Feb. 28..............................................Common Dividend Payable............................................... 80,000

Cash.................................... 80,000 Paid cash dividend.

July 6..............................................Cash (750 × $48)36,000

Common shares................... 36,000 Issued common shares.

Aug. 22...............................................Cash (1,250 × $34)42,500

Common shares................... 42,500 Issued common shares.

Sept. 5............................................Cash Dividends or Retained Earnings............................ 88,000

Common Dividend Payable. . . 88,000 Declared dividend on 22,000 outstanding shares.

Oct. 28.............................................Common Dividend Payable............................................... 88,000

Cash.................................... 88,000 Paid cash dividend.

Dec. 31.............................................Income Summary434,000

Retained Earnings................ 434,000 Closed the Income Summary account.

31 Retained Earnings.....................168,000 Cash Dividends.................... 168,000 Closed the cash dividend account (Note: No entry is

required

if Retained Earnings was debited in the Sept. 5 entry and Jan. 5 entry).

Problem 15-6A (concluded)

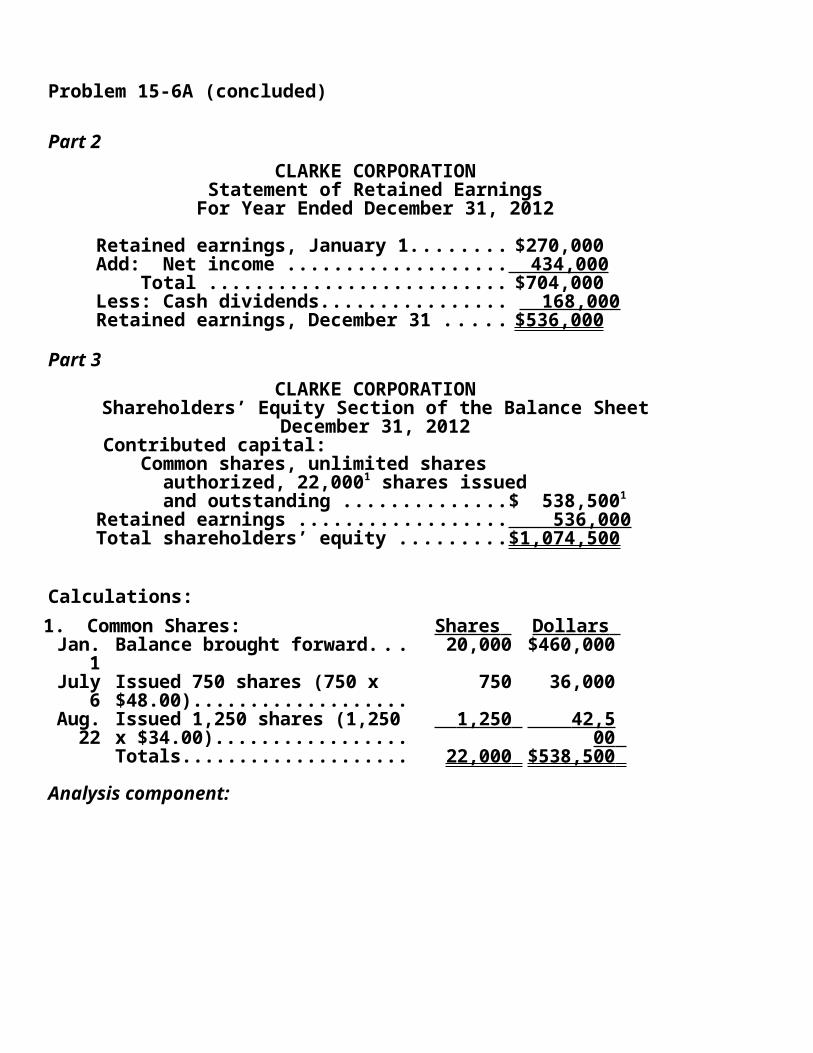

Part 2CLARKE CORPORATION

Statement of Retained EarningsFor Year Ended December 31, 2012

Retained earnings, January 1...............$270,000Add: Net income ............................... 434,000 Total ..............................................$704,000Less: Cash dividends........................... 168,000Retained earnings, December 31 ........$536,000

Part 3CLARKE CORPORATION

Shareholders’ Equity Section of the Balance SheetDecember 31, 2012

Contributed capital: Common shares, unlimited shares authorized, 22,0001 shares issued and outstanding ...........................$ 538,5001

Retained earnings .............................. 536,000Total shareholders’ equity ..................$1,074,500

Calculations:1. Common Shares: Shares Dollars

Jan. 1

Balance brought forward..... 20,000 $460,000

July 6

Issued 750 shares (750 x $48.00)..............................

750 36,000

Aug. 22

Issued 1,250 shares (1,250 x $34.00)...........................

1,250 42,50 0

Totals................................ 22,000 $538,500

Analysis component:

The relationship between assets and retained earnings is that retained earnings represents how much of the assets are financed by the accumulated profits less losses less distributions of dividends. In other words, retained earnings is a component of equity and we know that assets are financed in part by equity. Using the information in Part (3) above for Clarke Corporation, we know that $536,00000 of the assets are financed by retained earnings as at December 31, 2012.

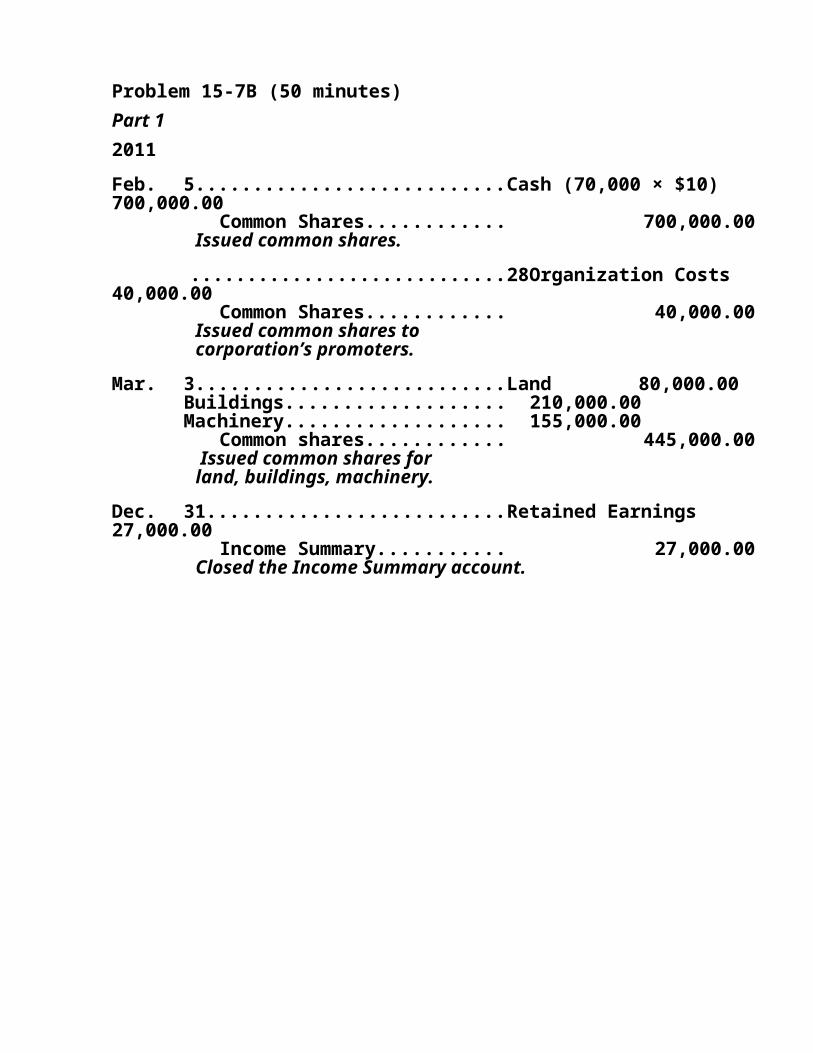

Problem 15-7A (50 minutes)Part 12011Jan. 1

2Cash............................................... 160,00

0 Common Shares............................ 160,00

0 To record issuance of shares.

20

Organization Costs.......................... 30,000

Common Shares............................ 30,000 To record issuance of shares in exchange for organization efforts.

31

Land............................................... 300,000

Building.......................................... 400,000

Equipment...................................... 40,000 Common Shares............................ 740,00

0 To record exchange of shares for capital assets.

Mar.

4 Equipment...................................... 6,800

Cash............................................ 6,800 To record purchase of equipment.

Dec.

31

Retained Earnings........................... 80,000

Income Summary.......................... To record closing of income summary to retained earnings.

80,000

2012Jan. 4 Cash............................................... 300,00

0 Preferred Shares.......................... 300,00

0 To record issuance of preferred shares.

Dec 3 Income Summary............................. 180,00

. 1 0 Retained Earnings......................... 180,00

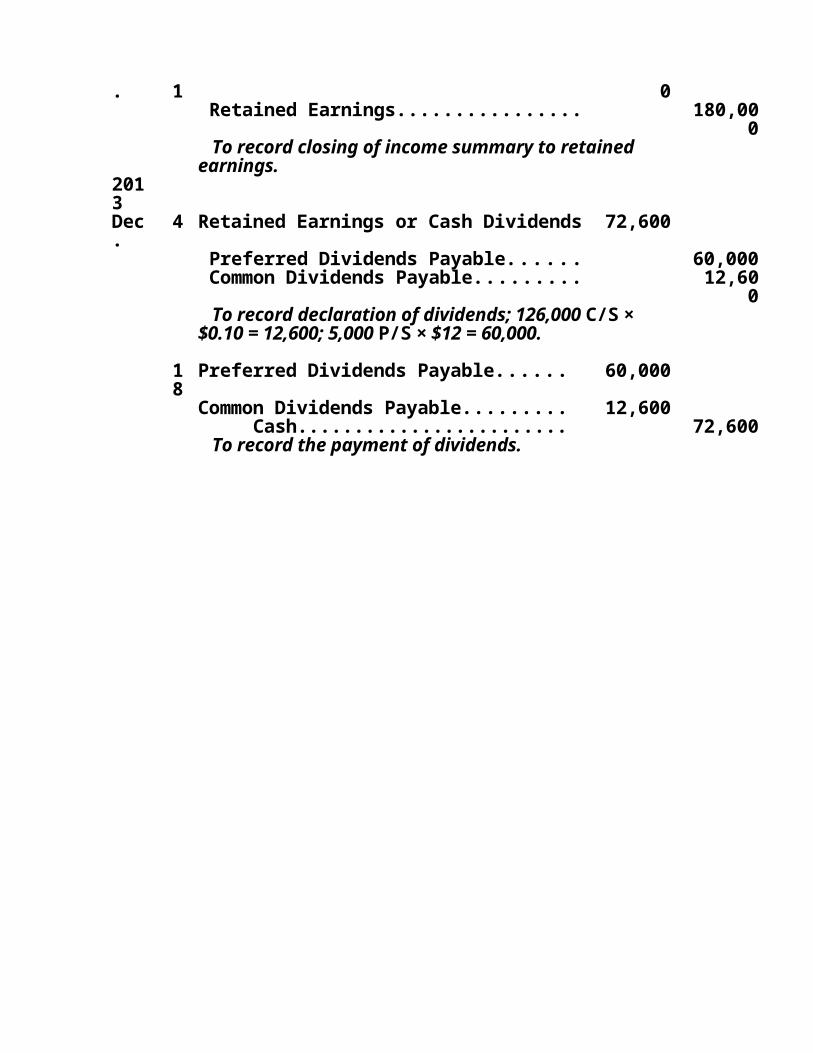

0 To record closing of income summary to retained earnings.

2013Dec.

4 Retained Earnings or Cash Dividends 72,600

Preferred Dividends Payable.......... 60,000 Common Dividends Payable........... 12,60

0 To record declaration of dividends; 126,000 C/S × $0.10 = 12,600; 5,000 P/S × $12 = 60,000.

18

Preferred Dividends Payable.......... 60,000

Common Dividends Payable........... 12,600 Cash........................................ 72,600 To record the payment of dividends.

Problem 15-7A (continued)

31

Retained Earnings......................... 72,600

Cash Dividends......................... 72,600 To close the cash dividends account (assuming the Cash Dividends account was debited on December 4).

31

Income Summary........................... 160,000

Retained Earnings................... 160,000

To close the income summary account.

Part 2WRIGHTSON CORP.

Statement of Retained EarningsFor Year Ended December 31, 2013

Retained earnings, January 1......................... $ 100,000Add: Net income........................................... 160,000 Total.......................................................... $260,000Less: Cash dividends.................................... 72,600Retained earnings, December 31.................... $ 187,400

Part 3WRIGHTSON CORP.

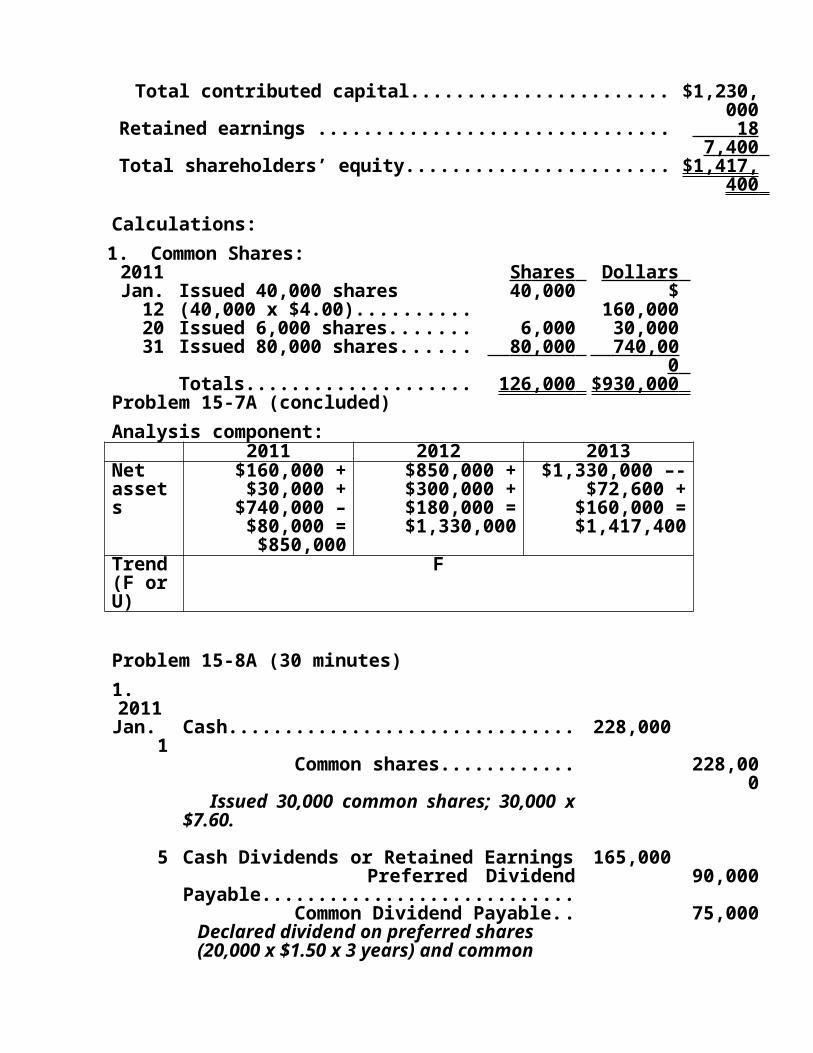

Shareholders’ Equity December 31, 2013

Contributed Capital:Preferred shares, $12 noncumulative, 100,000 shares authorized, 5,000 shares issued & outstanding.... $

300,000

Common shares, unlimited shares authorized, 126,0001 shares issued and outstanding..........................................................

930, 0001

Total contributed capital....................................... $1,230,000

Retained earnings .................................................. 187, 400

Total shareholders’ equity....................................... $1,417,400

Calculations:1. Common Shares:2011 Shares Dollars Jan.

12Issued 40,000 shares (40,000 x $4.00).................

40,000 $ 160,000

20 Issued 6,000 shares............ 6,000 30,00031 Issued 80,000 shares.......... 80,000 740,00

0 Totals................................ 126,000 $930,00

0 Problem 15-7A (concluded)Analysis component:

2011 2012 2013Net assets

$160,000 + $30,000 +

$740,000 – $80,000 = $850,000

$850,000 + $300,000 + $180,000 = $1,330,000

$1,330,000 –- $72,600 +

$160,000 = $1,417,400

Trend (F or U)

F

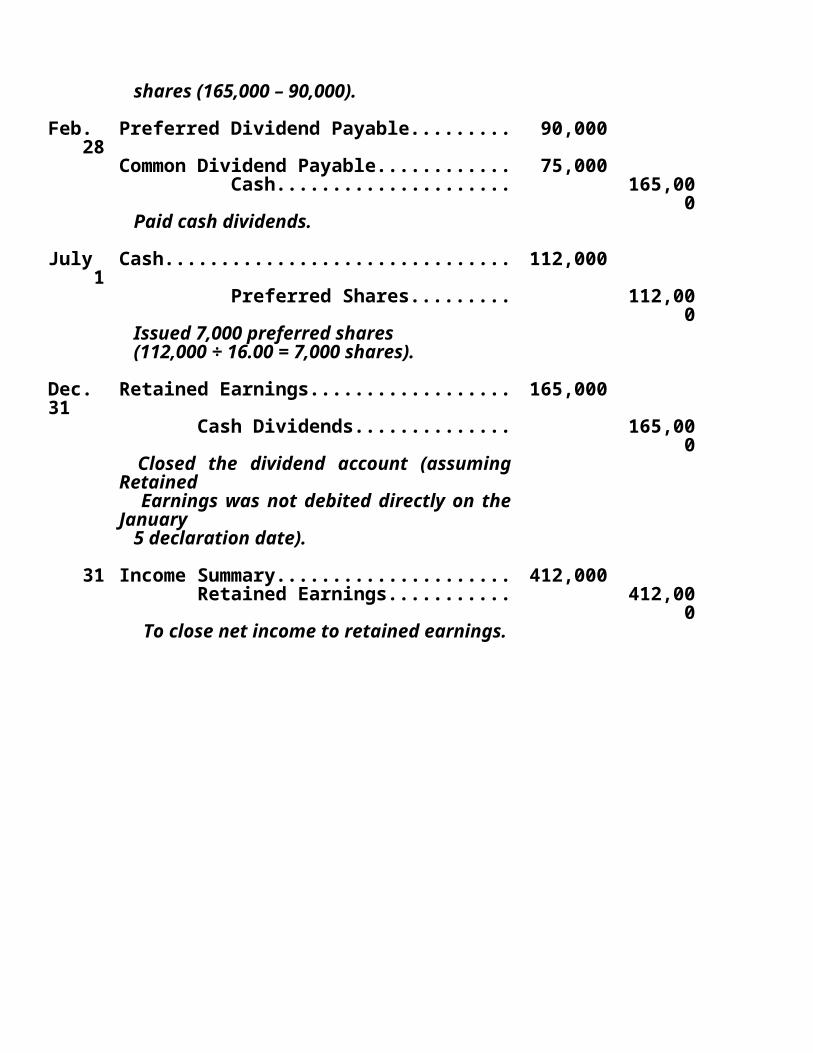

Problem 15-8A (30 minutes)1.2011Jan.

1Cash................................................ 228,00

0 Common shares...................... 228,00

0 Issued 30,000 common shares; 30,000 x $7.60.

5 Cash Dividends or Retained Earnings 165,000

Preferred Dividend Payable..... 90,000 Common Dividend Payable...... 75,000 Declared dividend on preferred shares (20,000 x $1.50 x 3 years) and

common shares (165,000 – 90,000).

Feb. 28

Preferred Dividend Payable.............. 90,000

Common Dividend Payable............... 75,000 Cash....................................... 165,00

0 Paid cash dividends.

July 1

Cash................................................ 112,000

Preferred Shares..................... 112,000

Issued 7,000 preferred shares (112,000 ÷ 16.00 = 7,000 shares).

Dec. 31

Retained Earnings............................ 165,000

Cash Dividends.......................... 165,000

Closed the dividend account (assuming Retained Earnings was not debited directly on the January 5 declaration date).

31 Income Summary............................. 412,000

Retained Earnings..................... 412,000

To close net income to retained earnings.

Problem 15-8A (continued)

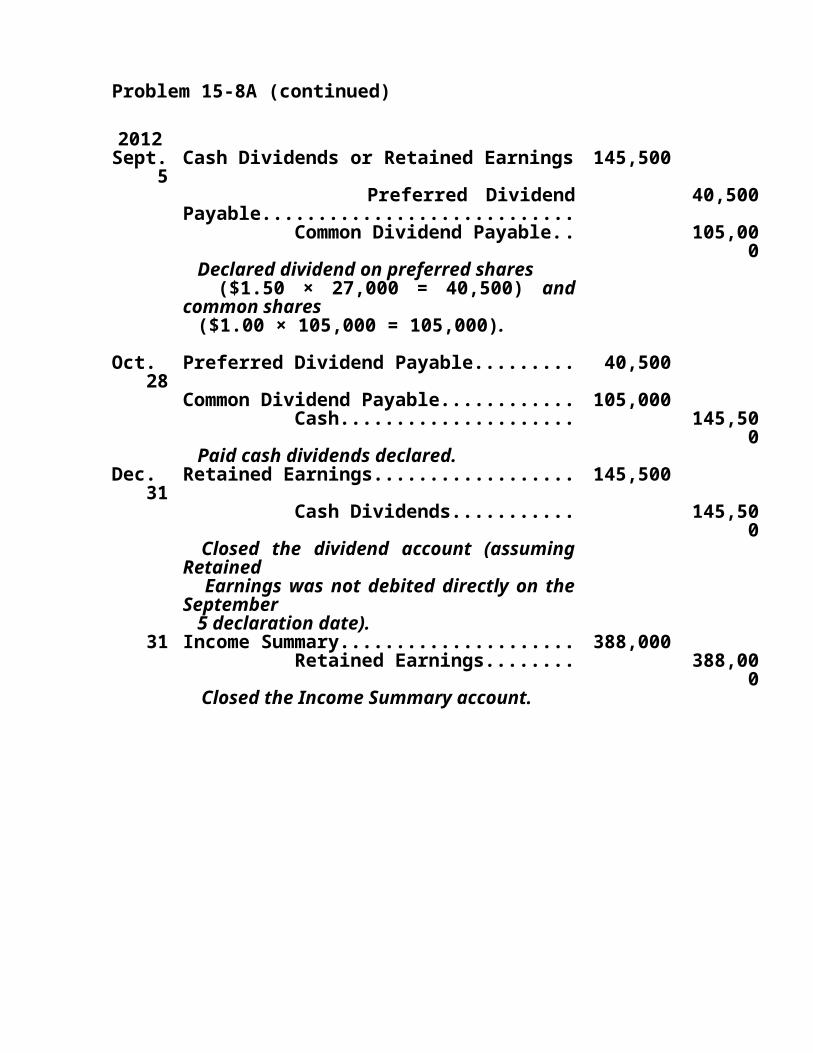

2012Sept.

5Cash Dividends or Retained Earnings 145,50

0 Preferred Dividend Payable..... 40,500 Common Dividend Payable...... 105,00

0 Declared dividend on preferred shares ($1.50 × 27,000 = 40,500) and common shares ($1.00 × 105,000 = 105,000).

Oct. 28

Preferred Dividend Payable.............. 40,500

Common Dividend Payable............... 105,000

Cash....................................... 145,500

Paid cash dividends declared.Dec.

31Retained Earnings............................ 145,50

0 Cash Dividends....................... 145,50

0 Closed the dividend account (assuming Retained Earnings was not debited directly on the September 5 declaration date).

31 Income Summary............................. 388,000

Retained Earnings................... 388,000

Closed the Income Summary account.

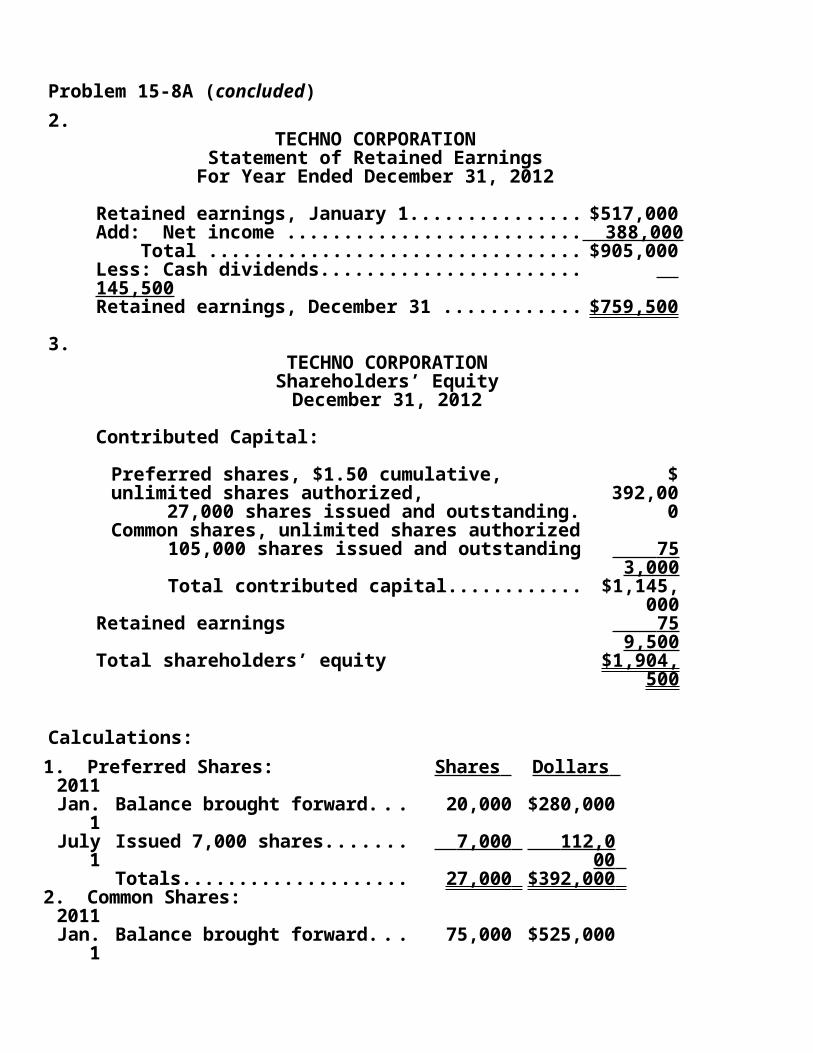

Problem 15-8A (concluded)2.

TECHNO CORPORATIONStatement of Retained Earnings

For Year Ended December 31, 2012

Retained earnings, January 1.........................$517,000Add: Net income .......................................... 388,000 Total ........................................................$905,000Less: Cash dividends..................................... 145,500Retained earnings, December 31 ...................$759,500

3.TECHNO CORPORATIONShareholders’ EquityDecember 31, 2012

Contributed Capital:

Preferred shares, $1.50 cumulative, unlimited shares authorized, 27,000 shares issued and outstanding.....

$ 392,00

0Common shares, unlimited shares authorized 105,000 shares issued and outstanding... 753,

000 Total contributed capital......................... $1,145,

000Retained earnings 759,

500Total shareholders’ equity $1,904,

500

Calculations:1. Preferred Shares: Shares Dollars 2011Jan.

1Balance brought forward..... 20,000 $280,00

0July

1Issued 7,000 shares............ 7,000 112,0

00 Totals................................ 27,000 $392,00

0 2. Common Shares:2011Jan.

1Balance brought forward..... 75,000 $525,00

0

Jan. 1

Issued 30,000 shares (30,000 x $7.60).................

30,000 228,00 0

Totals................................ 105,000 $753,000

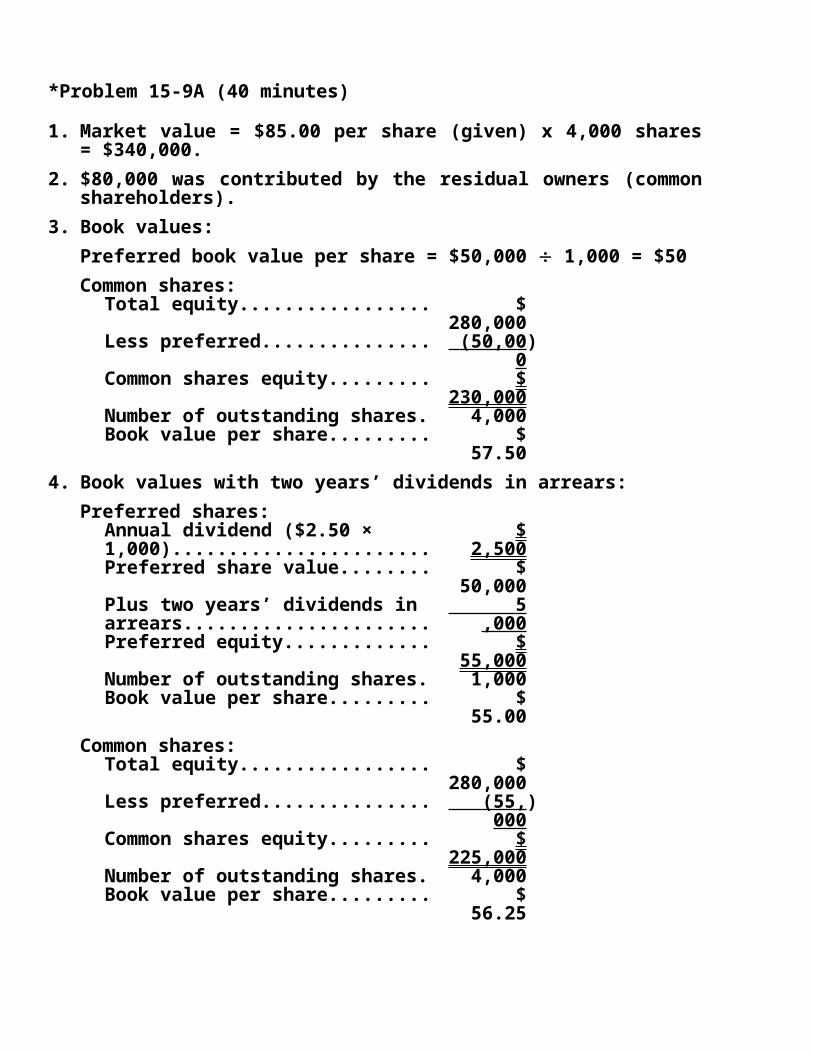

*Problem 15-9A (40 minutes)

1. Market value = $85.00 per share (given) x 4,000 shares = $340,000.

2. $80,000 was contributed by the residual owners (common shareholders).

3. Book values:Preferred book value per share = $50,000 1,000 = $50Common shares:

Total equity............................ $ 280,00

0Less preferred........................ (50,00

0)

Common shares equity............ $ 230,00

0Number of outstanding shares 4,000Book value per share.............. $

57.504. Book values with two years’ dividends in arrears:

Preferred shares:Annual dividend ($2.50 × 1,000) $

2,500Preferred share value............. $

50,000Plus two years’ dividends in arrears...................................

5,0 00

Preferred equity..................... $ 55,000

Number of outstanding shares 1,000Book value per share.............. $

55.00Common shares:

Total equity............................ $ 280,00

0Less preferred........................ (55,0

00)

Common shares equity............ $ 225,00

0Number of outstanding shares 4,000

Book value per share.............. $ 56.25

5. Book values with call price and two years’ dividends in arrears:Preferred shares:

Annual dividend...................... $ 2,500

Preferred shares call price (1,000 × $55)..........................

$ 55,000

Plus two years’ dividends in arrears...................................

5,00 0

Preferred equity..................... $ 60,000

Number of outstanding shares 1,000Book value per share.............. $

60.00Common shares:

Total equity............................ $ 280,00

0Less preferred........................ (60,00

0)

Common shares equity............ $ 220,00

0Number of outstanding shares 4,000Book value per share.............. $

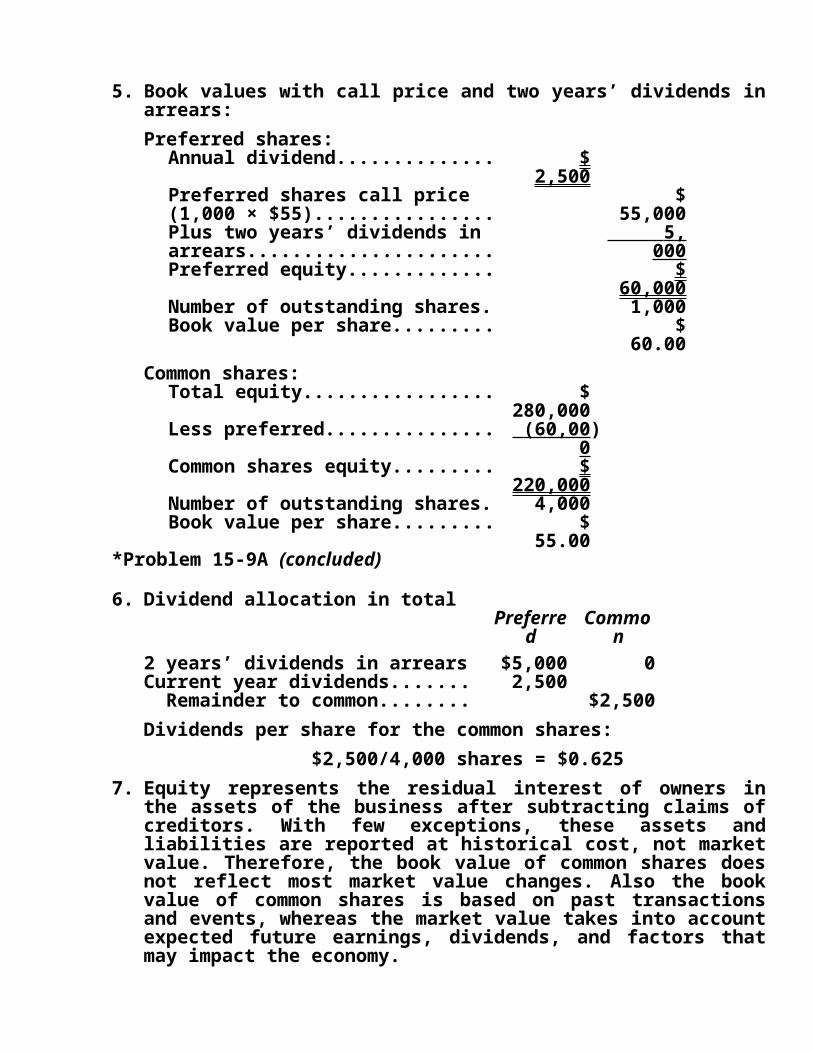

55.00*Problem 15-9A (concluded)

6. Dividend allocation in totalPrefer

redComm

on2 years’ dividends in arrears... $5,000 0Current year dividends............ 2,500 Remainder to common....... $2,500Dividends per share for the common shares:

$2,500/4,000 shares = $0.6257. Equity represents the residual interest of owners in the

assets of the business after subtracting claims of creditors. With few exceptions, these assets and liabilities are reported at historical cost, not market value. Therefore, the book value of common shares does not

reflect most market value changes. Also the book value of common shares is based on past transactions and events, whereas the market value takes into account expected future earnings, dividends, and factors that may impact the economy.

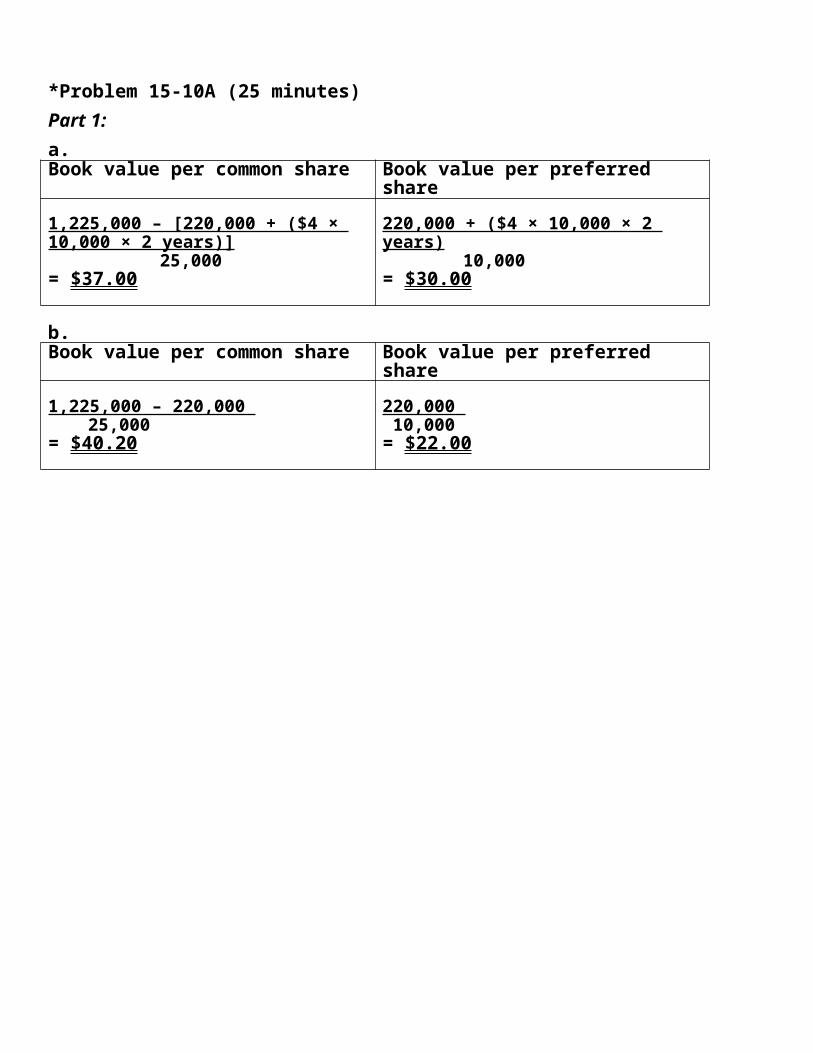

*Problem 15-10A (25 minutes)Part 1:a.Book value per common share Book value per preferred

share1,225,000 – [220,000 + ($4 × 10,000 × 2 years)]

220,000 + ($4 × 10,000 × 2 years)

25,000 10,000= $37.00 = $30.00

b.Book value per common share Book value per preferred

share1,225,000 – 220,000 220,000

25,000 10,000= $40.20 = $22.00

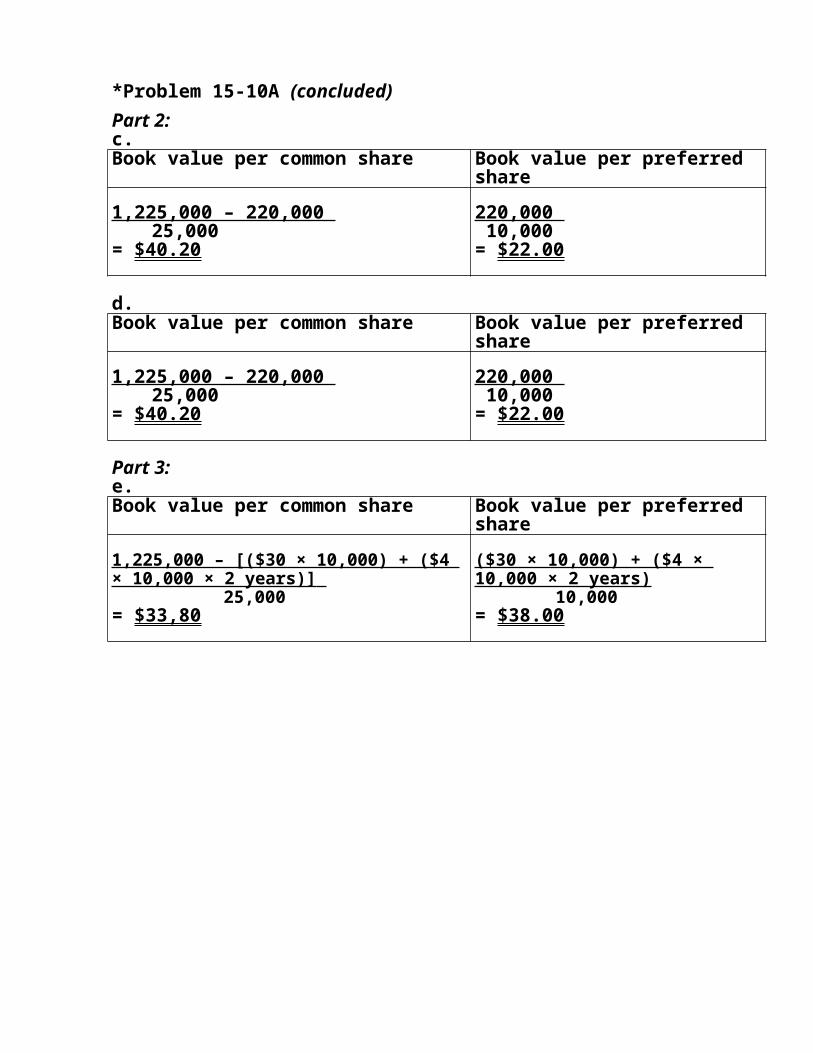

*Problem 15-10A (concluded)Part 2:c.Book value per common share Book value per preferred

share1,225,000 – 220,000 220,000

25,000 10,000= $40.20 = $22.00

d.Book value per common share Book value per preferred

share1,225,000 – 220,000 220,000

25,000 10,000= $40.20 = $22.00

Part 3:e.Book value per common share Book value per preferred

share1,225,000 – [($30 × 10,000) + ($4 × 10,000 × 2 years)]

($30 × 10,000) + ($4 × 10,000 × 2 years)

25,000 10,000= $33,80 = $38.00

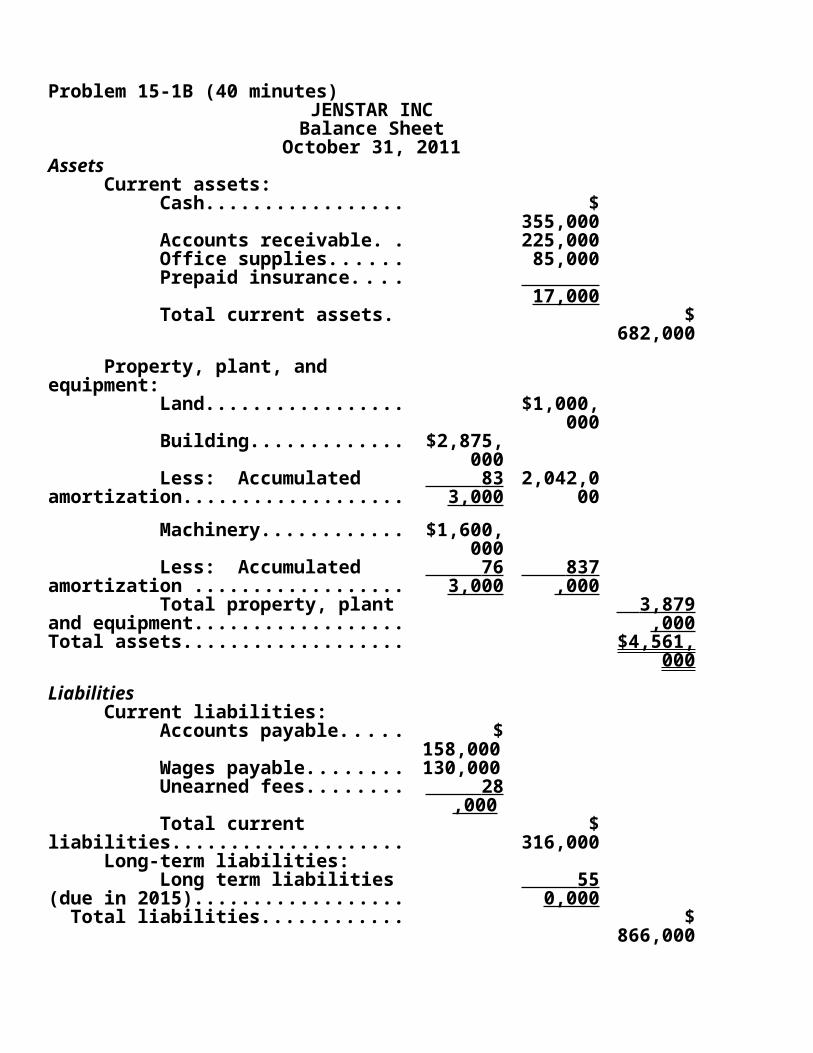

Problem 15-1B (40 minutes)JENSTAR INC

Balance SheetOctober 31, 2011

Assets Current assets: Cash.................................. $

355,000

Accounts receivable........... 225,000

Office supplies................... 85,000 Prepaid insurance.............. 17,

000 Total current assets........... $

682,000

Property, plant, and equipment: Land.................................. $1,000,

000 Building............................. $2,875,

000 Less: Accumulated amortization...............................

833, 000

2,042,000

Machinery......................... $1,600,000

Less: Accumulated amortization ..............................

763, 000

837, 000

Total property, plant and equipment..................................

3,879, 000

Total assets................................ $4,561,000

Liabilities Current liabilities: Accounts payable............... $

158,000

Wages payable.................. 130,000

Unearned fees................... 28,0 00

Total current liabilities....... $ 316,00

0

Long-term liabilities: Long term liabilities (due in 2015)..........................................

550, 000

Total liabilities.......................... $ 866,00

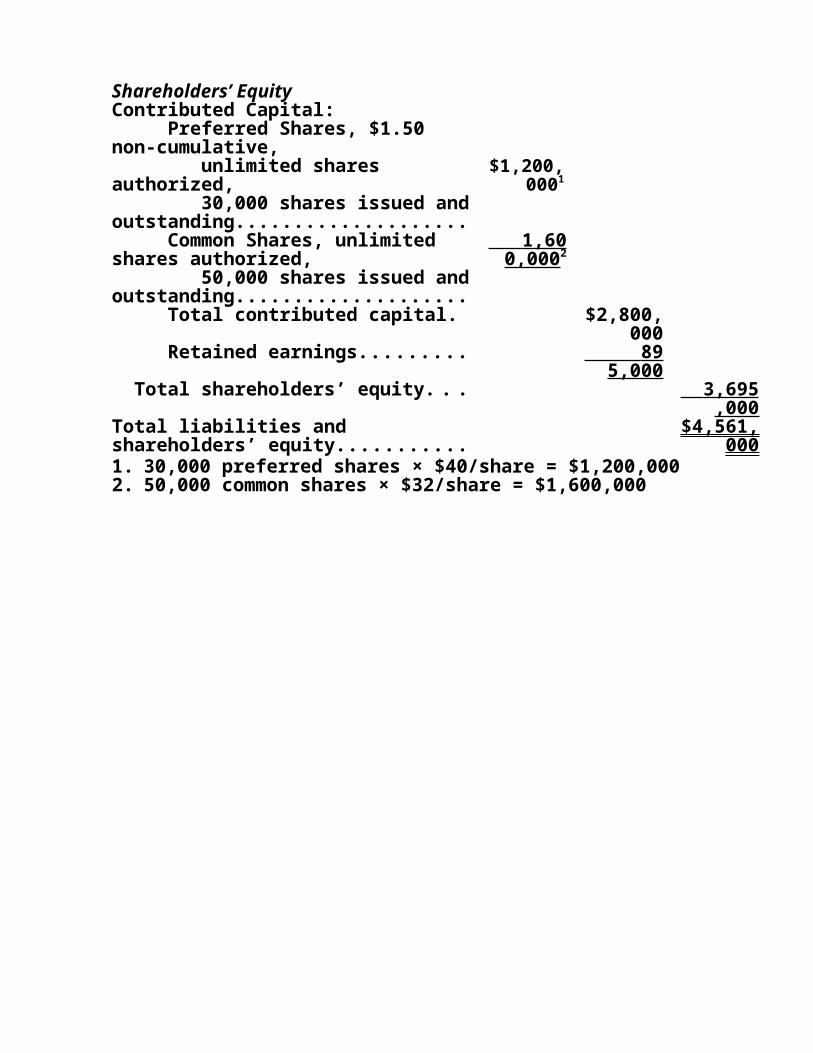

0Shareholders’ EquityContributed Capital: Preferred Shares, $1.50 non-cumulative, unlimited shares authorized, 30,000 shares issued and outstanding................................

$1,200,0001

Common Shares, unlimited shares authorized, 50,000 shares issued and outstanding................................

1,600 ,0002

Total contributed capital......... $2,800,000

Retained earnings.................. 895, 000

Total shareholders’ equity......... 3,695, 000

Total liabilities and shareholders’ equity.........................................

$4,561,000

1. 30,000 preferred shares × $40/share = $1,200,0002. 50,000 common shares × $32/share = $1,600,000

Problem 15-2B (20 minutes)Retained earnings December 31, 2011......... $1,960

,720Reductions in retained earnings due to transactions: Cash dividends declared: Feb. 11, on 350,000 shares (350,000 × $0.25)......................................................

$ 87,50

0 May 24, on 350,000 shares................. 87,50

0 Aug. 13, on 365,000 shares (365,000 × $0.25)......................................................

91,250

Dec. 12, on 385,000 shares (385,000 × $0.25)......................................................

96,2 50

362,500

Less: Retained earnings December 31, 2012 2,200 ,500

Net income.................................................. $ 602,28

0

Problem 15-3B (25 minutes)a.

2011

Dec. 1

Preferred Shares............................ 100,000

Common Shares...................... 100,000

To record the conversion of 1,000 preferred shares into 8,000 common shares; $200,000 ÷ 2,000 shares = $100 average issue price per preferred share; $100 x 1,000 = $100,000.

Immediately after the conversion of preferred shares, the shareholders’ equity section would still show 2,000 shares of preferred shares authorized, but only 1,000 shares issued and outstanding. The amount of preferred shares would change from $200,000 to $100,000. Common shares would still show unlimited shares authorized, and 68,000 shares issued. The amount of common shares would be $700,000 instead of $600,000.

Retained earnings would not be affected. Total shareholders’ equity also would not be affected because $100,000 has simply shifted from the preferred share section to the common share section.

b. As a common shareholder, you would not want the conversion of preferred shares to take place. As a result of the conversion, a smaller total dividend would be paid to preferred shares and a larger total dividend would be paid to common shares. However, the dividend per common share is less because there are more common shares dividing the cash. Before the conversion, there are 2,000 shares of $11 preferred. Therefore, $22,000 of the $487,000 paid out in dividends goes to the preferred shareholders. If the remaining $465,000 is divided by 60,000 shares of common shares outstanding, the common dividend per share is $7.75. However, after the conversion, $11,000 of the $487,000 paid out in dividends goes to the 1,000 shares of $11 preferred, and the remaining $476,000 is divided between the 68,000 common shares outstanding. This reduces the dividend per share to $7.00.

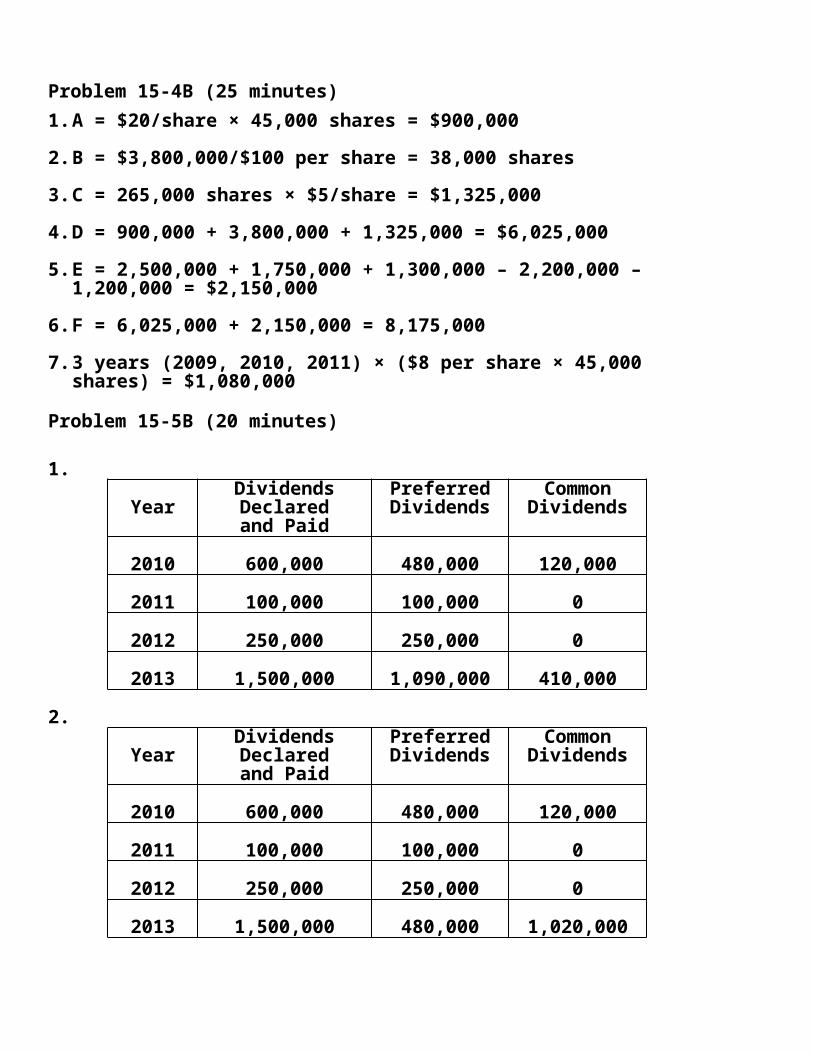

Problem 15-4B (25 minutes)1. A = $20/share × 45,000 shares = $900,000

2. B = $3,800,000/$100 per share = 38,000 shares

3. C = 265,000 shares × $5/share = $1,325,000

4. D = 900,000 + 3,800,000 + 1,325,000 = $6,025,000

5. E = 2,500,000 + 1,750,000 + 1,300,000 – 2,200,000 – 1,200,000 = $2,150,000

6. F = 6,025,000 + 2,150,000 = 8,175,000

7. 3 years (2009, 2010, 2011) × ($8 per share × 45,000 shares) = $1,080,000

Problem 15-5B (20 minutes)

1.

YearDividends Declared and Paid

PreferredDividends

CommonDividends

2010 600,000 480,000 120,000

2011 100,000 100,000 0

2012 250,000 250,000 0

2013 1,500,000 1,090,000 410,000

2.

YearDividends Declared and Paid

PreferredDividends

CommonDividends

2010 600,000 480,000 120,000

2011 100,000 100,000 0

2012 250,000 250,000 0

2013 1,500,000 480,000 1,020,000

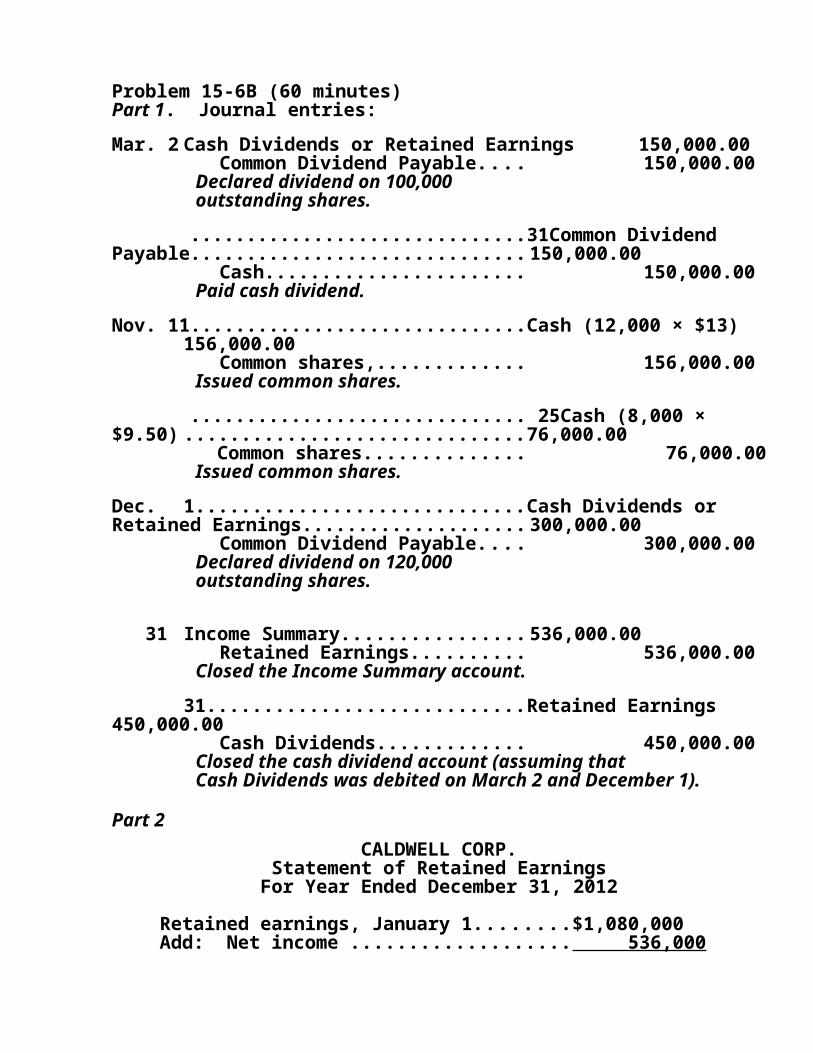

Problem 15-6B (60 minutes)Part 1. Journal entries:Mar. 2 Cash Dividends or Retained Earnings 150,000.00

Common Dividend Payable. . . 150,000.00 Declared dividend on 100,000 outstanding shares.

31Common Dividend Payable........150,000.00 Cash.................................... 150,000.00

Paid cash dividend.Nov. 11...............................................Cash (12,000 × $13)

156,000.00 Common shares,.................. 156,000.00

Issued common shares. 25...............................................Cash (8,000 × $9.50)

76,000.00 Common shares...................... 76,000.00Issued common shares.

Dec. 1 Cash Dividends or Retained Earnings 300,000.00 Common Dividend Payable. . . 300,000.00

Declared dividend on 120,000 outstanding shares.

31 Income Summary......................536,000.00 Retained Earnings................ 536,000.00

Closed the Income Summary account.

31 Retained Earnings.....................450,000.00 Cash Dividends.................... 450,000.00

Closed the cash dividend account (assuming that Cash Dividends was debited on March 2 and

December 1).

Part 2CALDWELL CORP.

Statement of Retained EarningsFor Year Ended December 31, 2012

Retained earnings, January 1...............$1,080,000Add: Net income ............................... 536,000 Total ..............................................$1,616,000

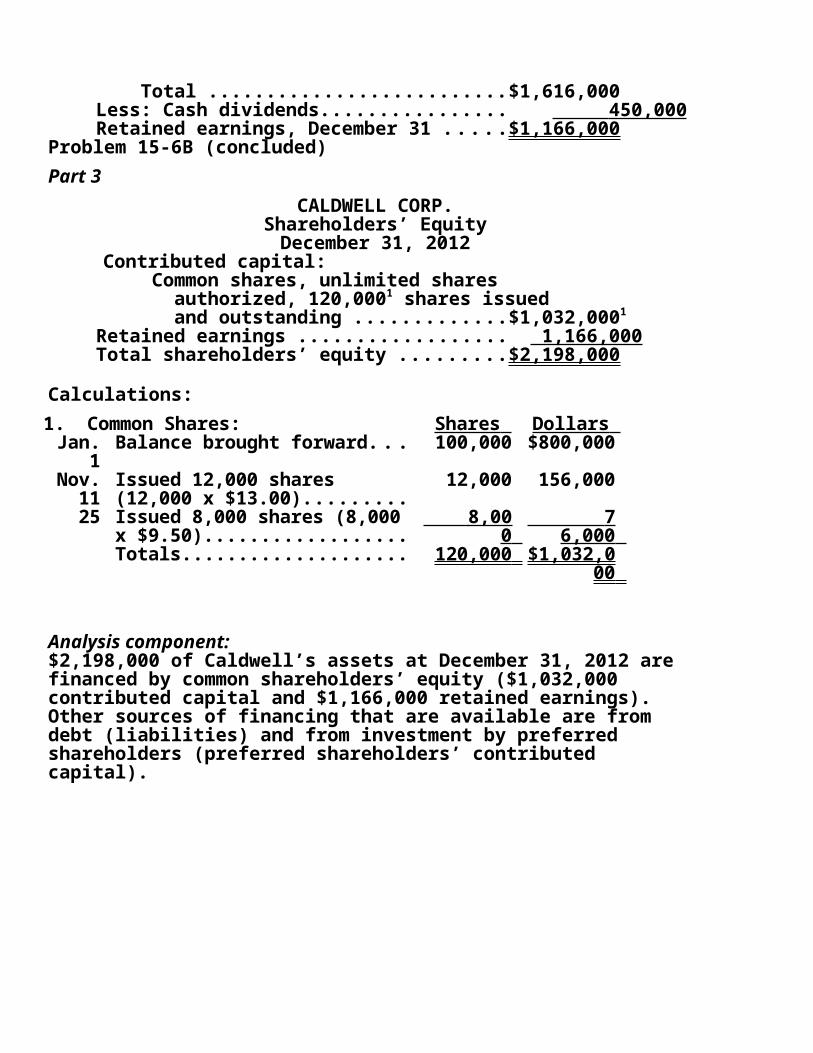

Less: Cash dividends........................... 450,000 Retained earnings, December 31 ........$1,166,000

Problem 15-6B (concluded)Part 3

CALDWELL CORP.Shareholders’ EquityDecember 31, 2012

Contributed capital: Common shares, unlimited shares authorized, 120,0001 shares issued and outstanding ..........................$1,032,0001

Retained earnings .............................. 1,166,000Total shareholders’ equity ..................$2,198,000

Calculations:1. Common Shares: Shares Dollars

Jan. 1

Balance brought forward..... 100,000 $800,000

Nov. 11

Issued 12,000 shares (12,000 x $13.00)...............

12,000 156,000

25 Issued 8,000 shares (8,000 x $9.50).............................

8,000 76, 000

Totals................................ 120,000 $1,032,000

Analysis component:$2,198,000 of Caldwell’s assets at December 31, 2012 are financed by common shareholders’ equity ($1,032,000 contributed capital and $1,166,000 retained earnings). Other sources of financing that are available are from debt (liabilities) and from investment by preferred shareholders (preferred shareholders’ contributed capital).

Problem 15-7B (50 minutes)Part 12011 Feb. 5 Cash (70,000 × $10)............... 700,000.00

Common Shares................ 700,000.00 Issued common shares.

28Organization Costs................. 40,000.00 Common Shares................ 40,000.00

Issued common shares to corporation’s promoters.

Mar. 3 Land...................................... 80,000.00Buildings................................ 210,000.00 Machinery.............................. 155,000.00

Common shares................ 445,000.00 Issued common shares for

land, buildings, machinery.Dec. 31............................................Retained Earnings27,000.00

Income Summary.............. 27,000.00 Closed the Income Summary account.

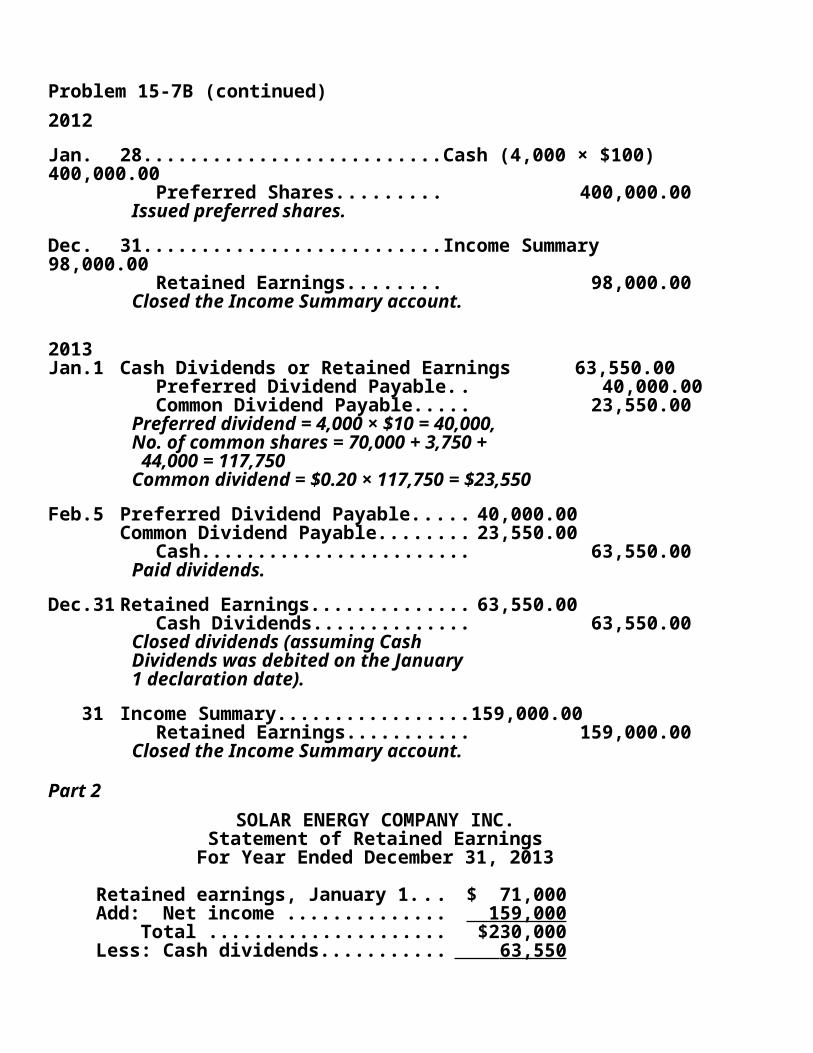

Problem 15-7B (continued)2012Jan. 28.............................................Cash (4,000 × $100)400,000.00

Preferred Shares............... 400,000.00 Issued preferred shares.

Dec. 31............................................Income Summary98,000.00

Retained Earnings............. 98,000.00 Closed the Income Summary account.

2013Jan.1 Cash Dividends or Retained Earnings 63,550.00

Preferred Dividend Payable... 40,000.00Common Dividend Payable... . 23,550.00

Preferred dividend = 4,000 × $10 = 40,000,No. of common shares = 70,000 + 3,750 + 44,000 = 117,750Common dividend = $0.20 × 117,750 = $23,550

Feb.5 Preferred Dividend Payable........40,000.00Common Dividend Payable..........23,550.00

Cash..................................... 63,550.00 Paid dividends.

Dec.31.................................................Retained Earnings63,550.00

Cash Dividends..................... 63,550.00 Closed dividends (assuming Cash Dividends was debited on the January 1 declaration date).

31 Income Summary........................159,000.00 Retained Earnings................. 159,000.00

Closed the Income Summary account.

Part 2SOLAR ENERGY COMPANY INC.

Statement of Retained EarningsFor Year Ended December 31, 2013

Retained earnings, January 1...... $ 71,000

Add: Net income ....................... 159,000 Total ..................................... $230,000Less: Cash dividends.................. 63,550 Retained earnings, December 31 $166,450

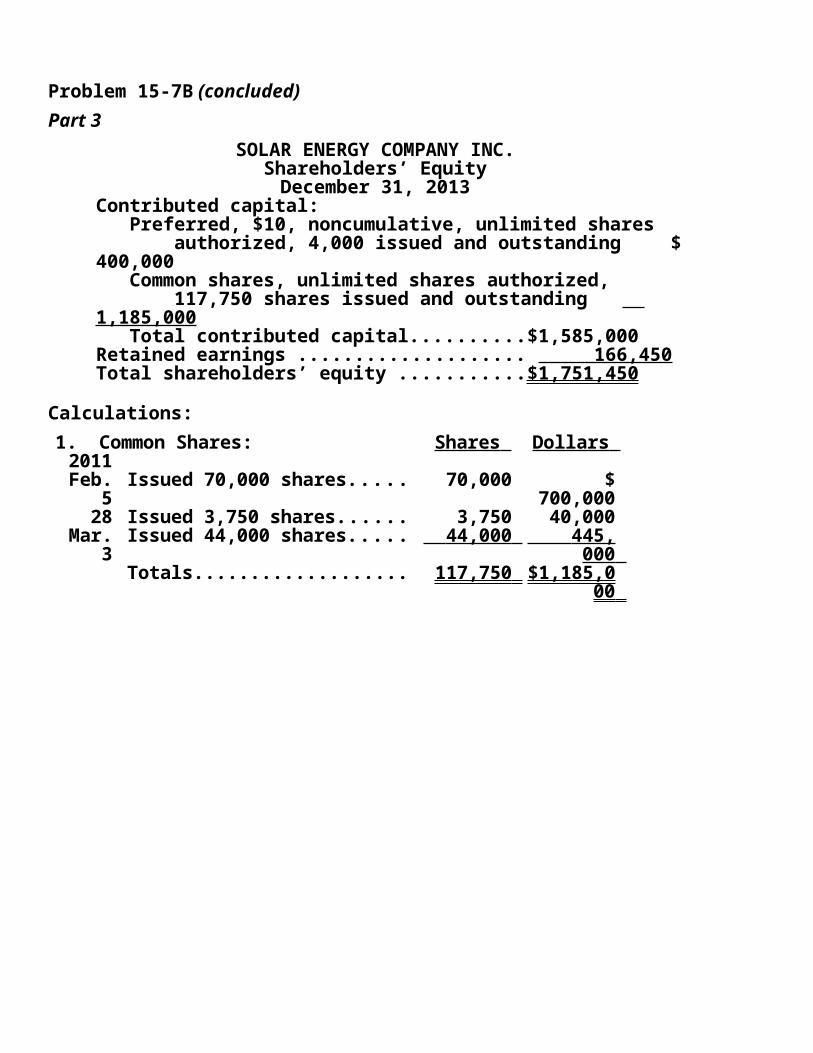

Problem 15-7B (concluded) Part 3

SOLAR ENERGY COMPANY INC.Shareholders’ EquityDecember 31, 2013

Contributed capital: Preferred, $10, noncumulative, unlimited shares authorized, 4,000 issued and outstanding $ 400,000 Common shares, unlimited shares authorized, 117,750 shares issued and outstanding 1,185,000 Total contributed capital.....................$1,585,000Retained earnings ................................ 166,450Total shareholders’ equity ....................$1,751,450

Calculations:1. Common Shares: Shares Dollars 2011Feb.

5Issued 70,000 shares........ 70,000 $

700,00028 Issued 3,750 shares.......... 3,750 40,000

Mar. 3

Issued 44,000 shares........ 44,000 445,0 00

Totals.............................. 117,750 $1,185,000

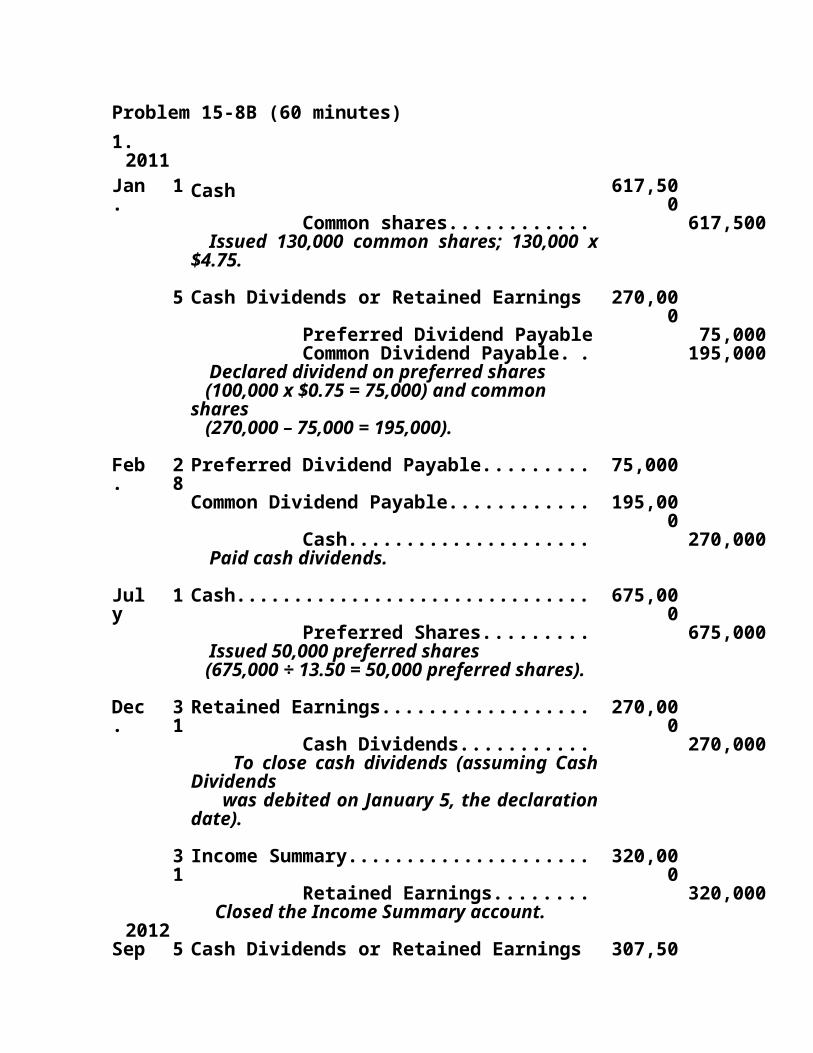

Problem 15-8B (60 minutes)1.2011

Jan. 1 Cash 617,500

Common shares....................... 617,500

Issued 130,000 common shares; 130,000 x $4.75.

5 Cash Dividends or Retained Earnings. 270,000

Preferred Dividend Payable...... 75,000 Common Dividend Payable....... 195,00

0 Declared dividend on preferred shares (100,000 x $0.75 = 75,000) and common shares (270,000 – 75,000 = 195,000).

Feb.

28

Preferred Dividend Payable............... 75,000

Common Dividend Payable................ 195,000

Cash........................................ 270,000

Paid cash dividends.

July 1 Cash................................................. 675,000

Preferred Shares...................... 675,000

Issued 50,000 preferred shares (675,000 ÷ 13.50 = 50,000 preferred shares).

Dec.

31

Retained Earnings............................. 270,000

Cash Dividends........................ 270,000

To close cash dividends (assuming Cash Dividends was debited on January 5, the declaration date).

31

Income Summary.............................. 320,000

Retained Earnings.................... 320,000

Closed the Income Summary account.

2012Sept.

5 Cash Dividends or Retained Earnings. 307,500

Preferred Dividend Payable ($0.75 × 150,000).............................

112,500

Common Dividend Payable ($0.25 × 780,000).............................

195,000

Declared dividend on preferred and common shares.

Oct. 28

Preferred Dividend Payable............... 112,500

Common Dividend Payable................. 195,000

Cash.................................. 307,500

Paid cash dividends declared.

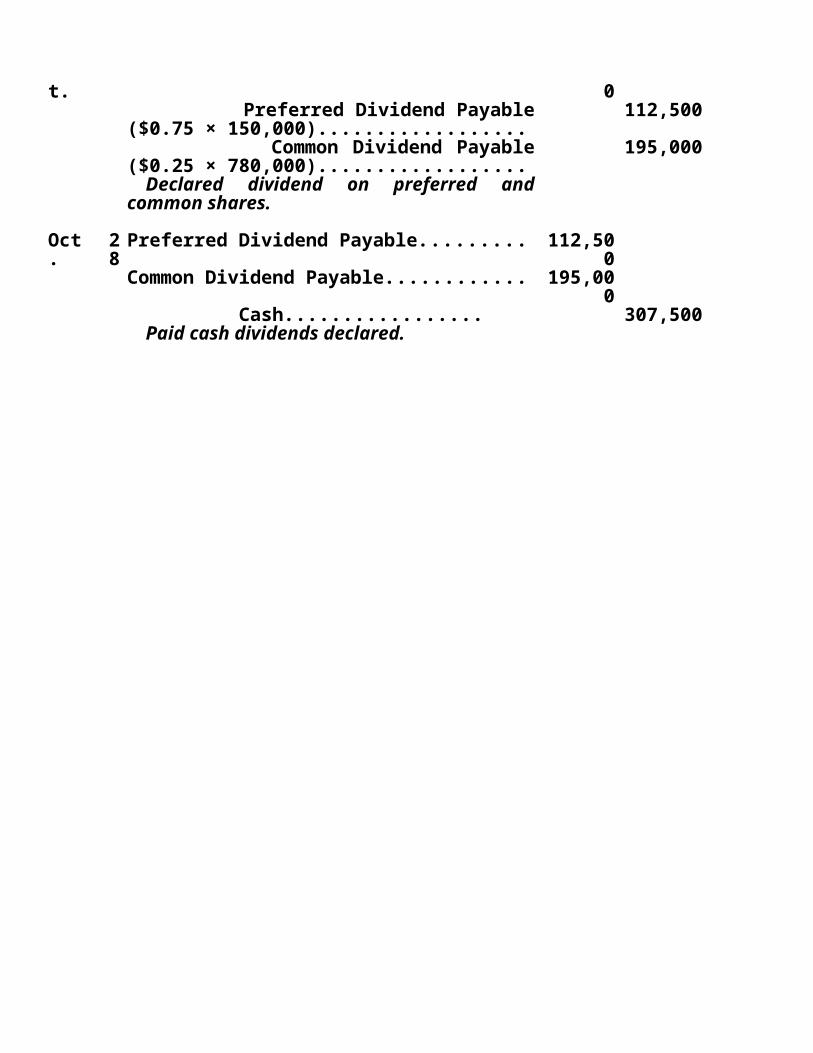

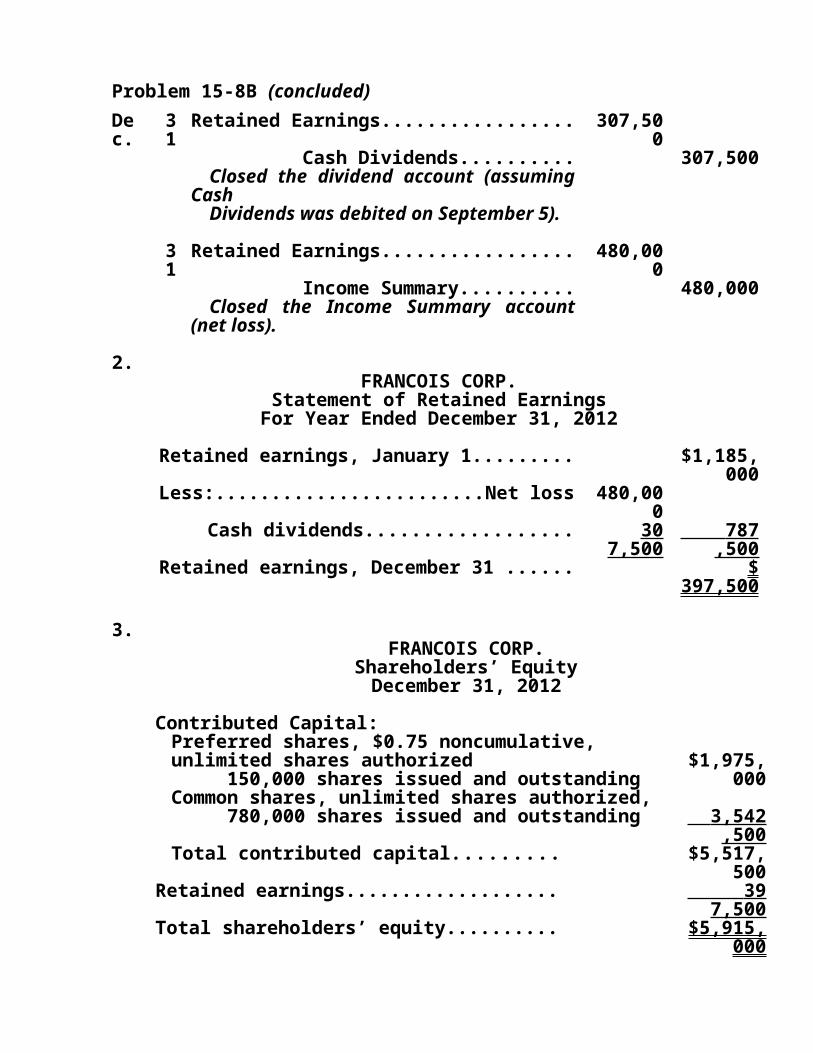

Problem 15-8B (concluded)Dec.

31

Retained Earnings........................... 307,500

Cash Dividends...................... 307,500

Closed the dividend account (assuming Cash Dividends was debited on September 5).

31

Retained Earnings........................... 480,000

Income Summary................... 480,000

Closed the Income Summary account (net loss).

2.FRANCOIS CORP.

Statement of Retained EarningsFor Year Ended December 31, 2012

Retained earnings, January 1............... $1,185,000

Less:.......................................Net loss 480,000

Cash dividends............................. 307,500

787, 500

Retained earnings, December 31 ......... $ 397,50

0

3.FRANCOIS CORP.

Shareholders’ EquityDecember 31, 2012

Contributed Capital:Preferred shares, $0.75 noncumulative, unlimited shares authorized 150,000 shares issued and outstanding

$1,975,000

Common shares, unlimited shares authorized, 780,000 shares issued and outstanding 3,542,

500Total contributed capital.................. $5,517,

500

Retained earnings............................. 397, 500

Total shareholders’ equity................. $5,915,000

Calculations:1. Preferred Shares: Shares Dollars

Jan. 1

Balance brought forward..... 100,000 $1,300,000

July 1

Issued 50,000 shares.......... 50,000 675, 000

Totals................................ 150,000 $1,975,000

1. Common Shares: Shares Dollars Jan.

1Balance brought forward..... 650,000 $2,925,

0001 Issued 130,000 shares

(130,000 x $4.75)...............130,000 617,5

00 Totals................................ 780,000 $3,542,

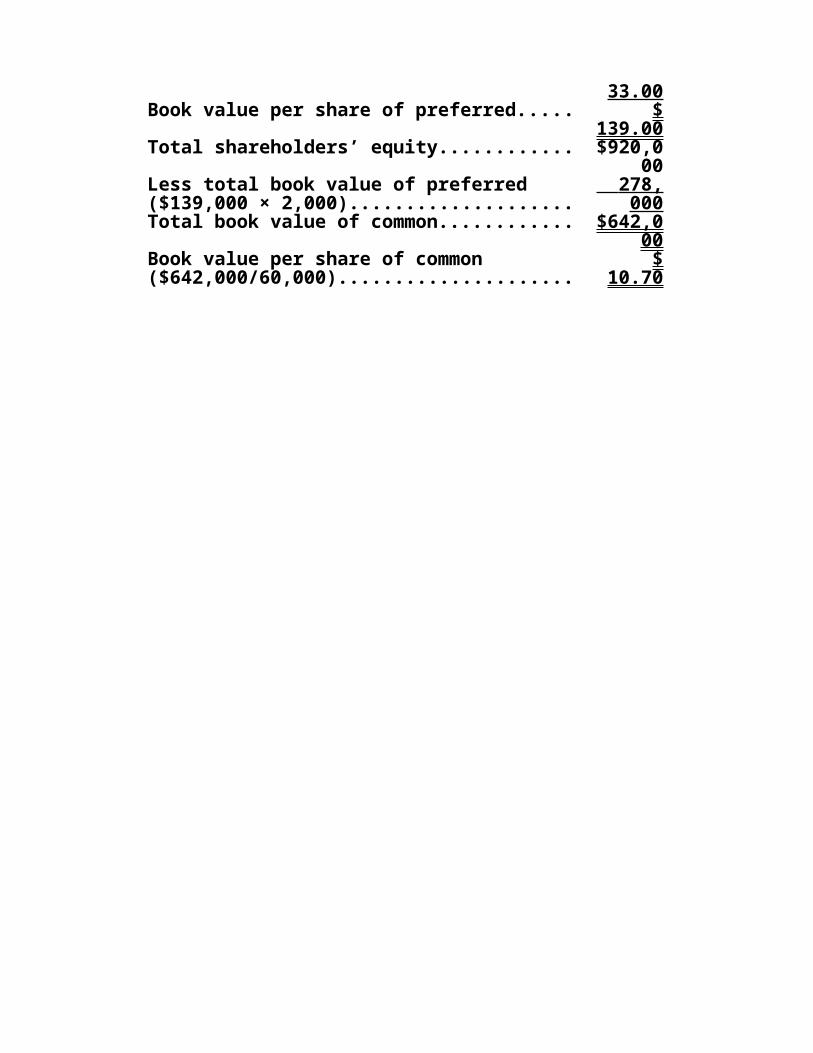

500 *Problem 15-9B (25 minutes)a. Book value per share of preferred is call

price.....................................................$

106.00Total shareholders’ equity..................... $920,0

00Less total book value of preferred ($106 × 2,000)...............................................

212,0 00

Total book value of common.................. $708,000

Book value per share of common ($708,000/60,000).................................

$ 11.80

b. Call price.............................................. $ 106.00

Dividends in arrears.............................. 11. 00

Book value per share of preferred.......... $ 117.00

Total shareholders’ equity..................... $920,000

Less total book value of preferred ($117 × 2,000)...............................................

234,0 00

Total book value of common.................. $686,000

Book value per share of common $

($686,000/60,000)................................. 11.43

c. Call price.............................................. $ 106.00

Dividends in arrears ($11 × 3)............... 33. 00

Book value per share of preferred.......... $ 139.00

Total shareholders’ equity..................... $920,000

Less total book value of preferred ($139,000 × 2,000)...............................

278,0 00

Total book value of common.................. $642,000

Book value per share of common ($642,000/60,000).................................

$ 10.70

*Problem 15-10B (25 minutes)Part 1:a.Book value per common share Book value per preferred

share1,800,000 – [400,000 + ($0.75 × 50,000 × 2 years)]

400,000 + ($0.75 × 50,000 × 2 years)

125,000 50,000= $10.60 = $9.50

b.Book value per common share Book value per preferred

share1,800,000 – 400,000 400,000

125,000 50,000= $11.20 = $8.00

Part 2:c.Book value per common share Book value per preferred

share1,800,000 – (400,000 + 25,000*) 400,000 + 25,000

125,000 50,000= $11.00* $0.75 × 50,000 × 2 years = $75,000;$75,000 – $50,000 dividends paid =

$25,000 arrears

= $8.50

d.Book value per common share Book value per preferred

share1,800,000 – 400,000 400,000

125,000 50,000= $11.20 = $8.00 Part 3:e.

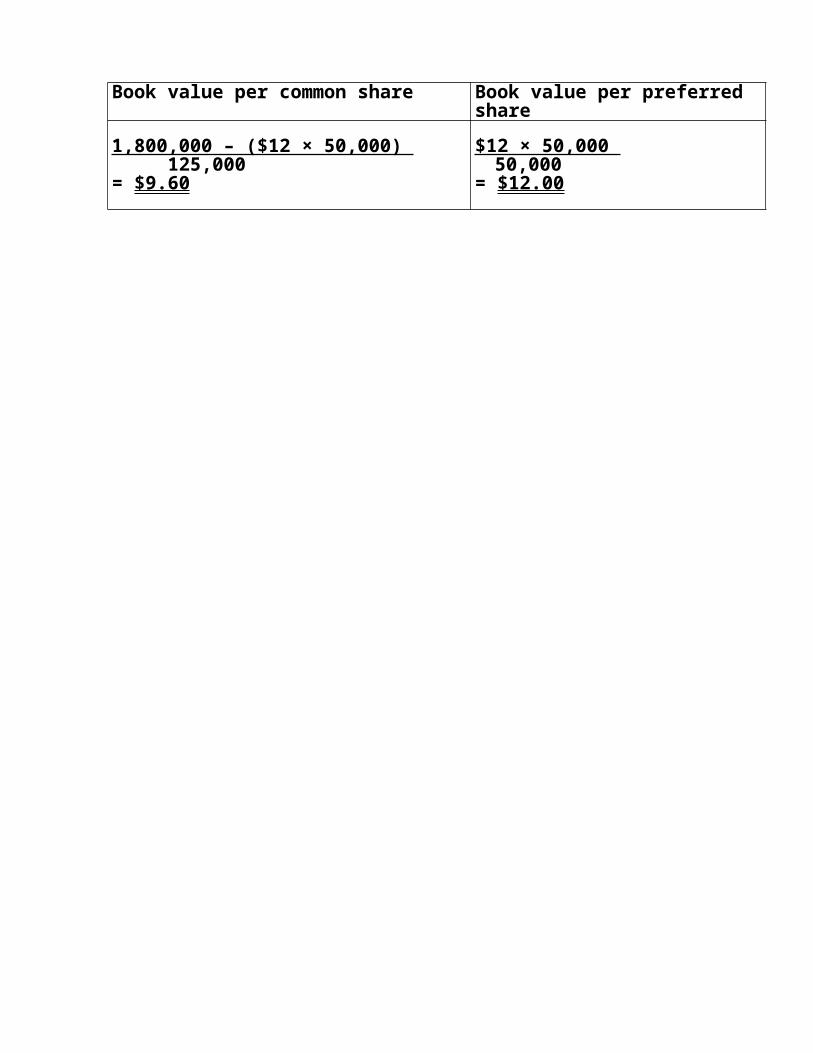

Book value per common share Book value per preferred share

1,800,000 – ($12 × 50,000) $12 × 50,000 125,000 50,000

= $9.60 = $12.00

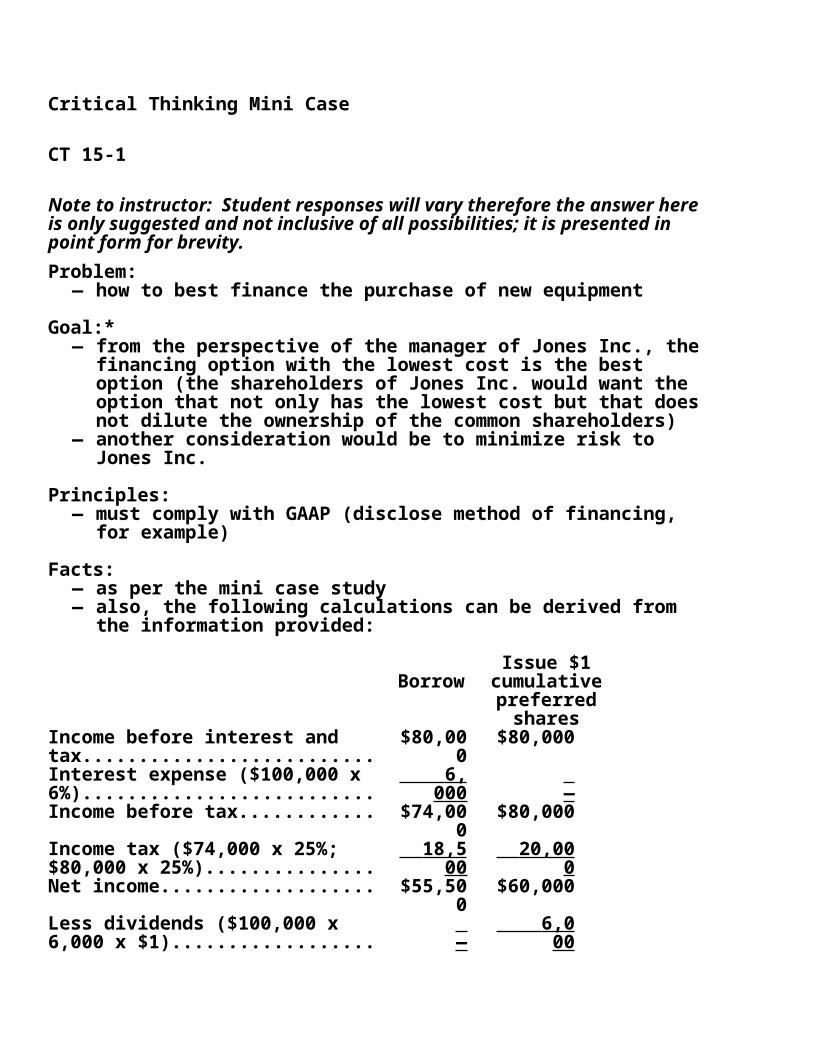

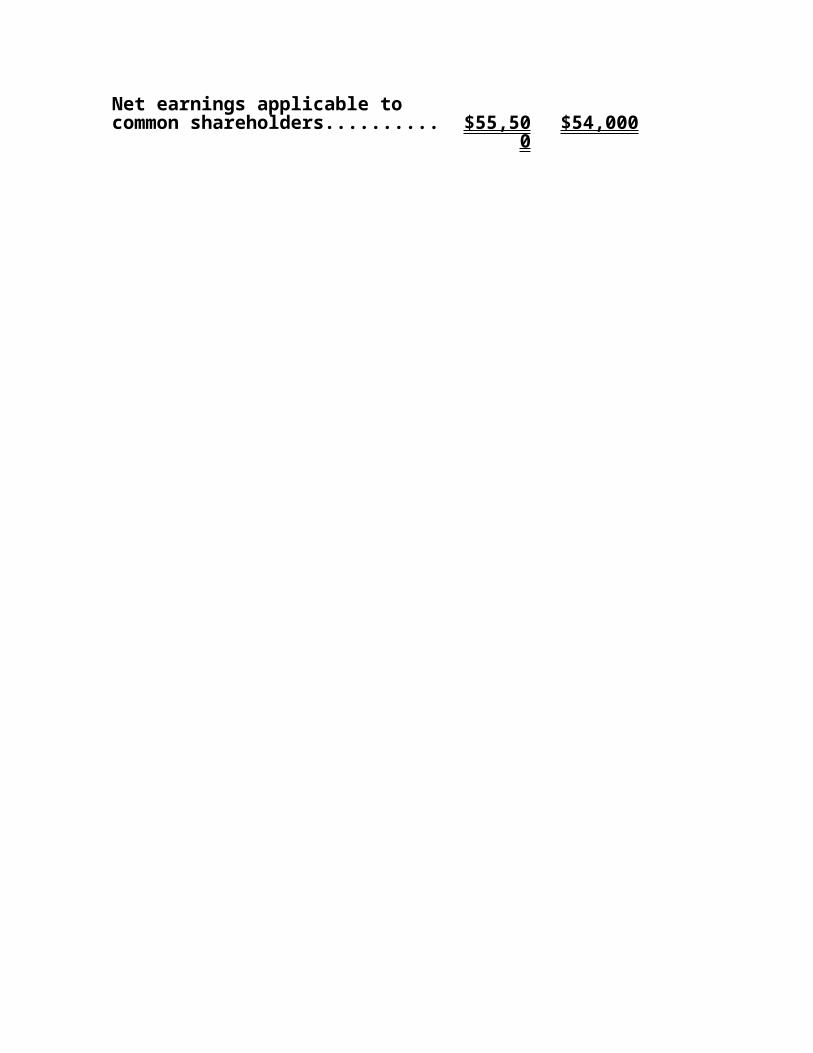

ANALYTICAL & REVIEW PROBLEMSA&R Problem 15-1

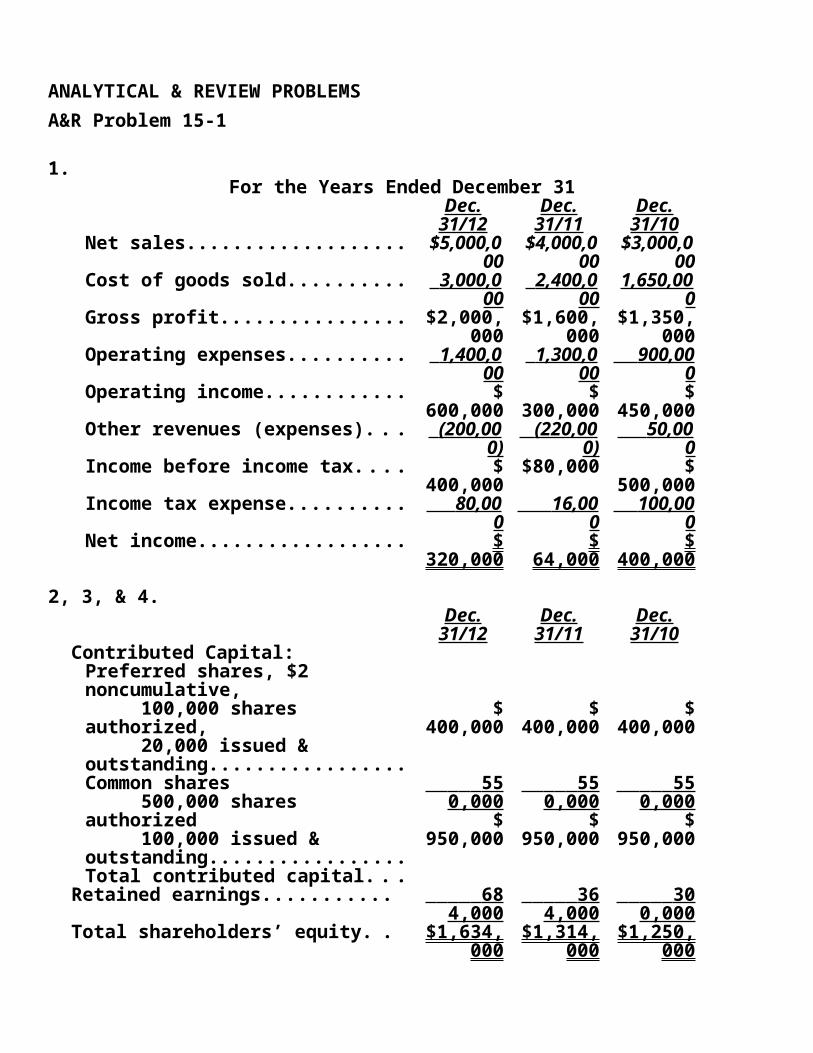

1.For the Years Ended December 31

Dec. 31/12

Dec. 31/11

Dec. 31/10

Net sales............................... $5,000,000

$4,000,000

$3,000,000

Cost of goods sold.................. 3,000, 000

2,400, 000

1,650,000

Gross profit............................ $2,000,000

$1,600,000

$1,350,000

Operating expenses............... 1,400, 000

1,300, 000

900, 000

Operating income................... $ 600,00

0

$ 300,00

0

$ 450,00

0Other revenues (expenses)..... (200,0

00) (220,

000) 50,

000Income before income tax...... $

400,000

$80,000

$ 500,00

0Income tax expense............... 80,

000 16,

000 100,

000Net income............................ $

320,000

$ 64,000

$ 400,00

0

2, 3, & 4.Dec. 31/12

Dec. 31/11

Dec. 31/10

Contributed Capital:Preferred shares, $2 noncumulative, 100,000 shares authorized, 20,000 issued & outstanding...........................Common shares 500,000 shares authorized 100,000 issued & outstanding...........................Total contributed capital........

$ 400,00

0

550, 000

$ 950,00

0

$ 400,00

0

550, 000

$ 950,00

0

$ 400,00

0

550, 000

$ 950,00

0Retained earnings.................. 684, 364, 300,

000 000 000Total shareholders’ equity...... $1,634,

000$1,314,

000$1,250,

000

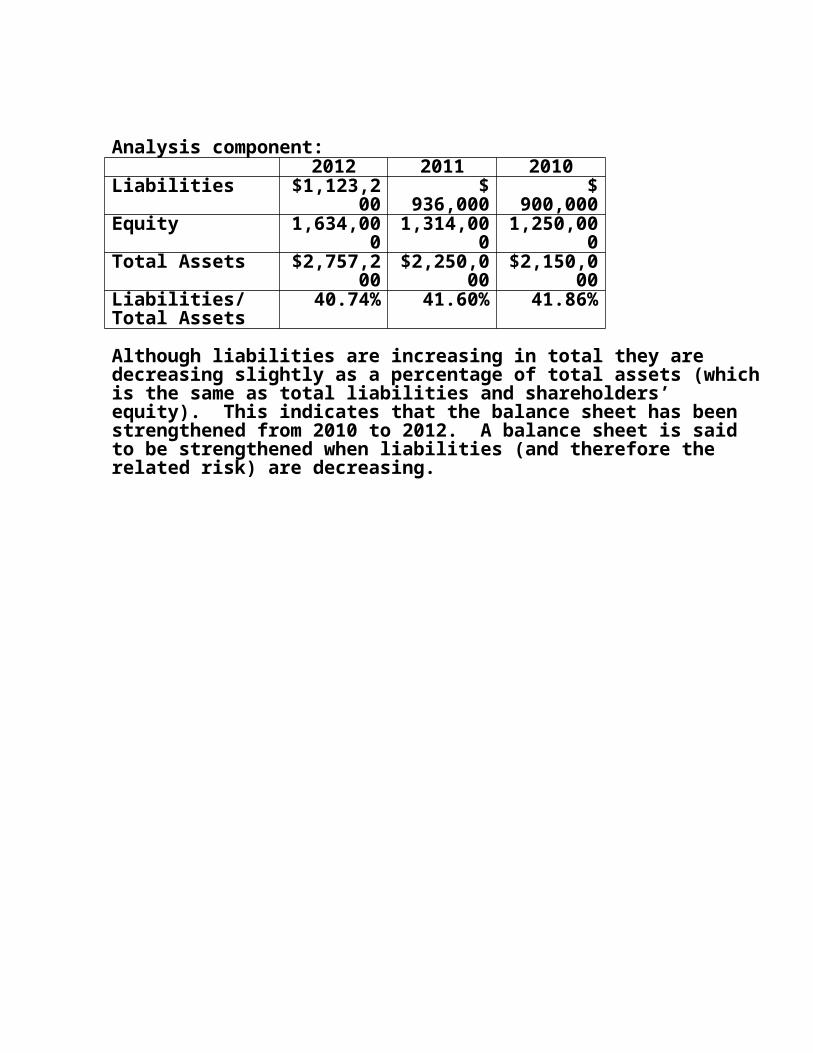

Analysis component:2012 2011 2010

Liabilities $1,123,200

$ 936,000

$ 900,000

Equity 1,634,000

1,314,000

1,250,000

Total Assets $2,757,200

$2,250,000

$2,150,000

Liabilities/Total Assets

40.74% 41.60% 41.86%

Although liabilities are increasing in total they are decreasing slightly as a percentage of total assets (which is the same as total liabilities and shareholders’ equity). This indicates that the balance sheet has been strengthened from 2010 to 2012. A balance sheet is said to be strengthened when liabilities (and therefore the related risk) are decreasing.

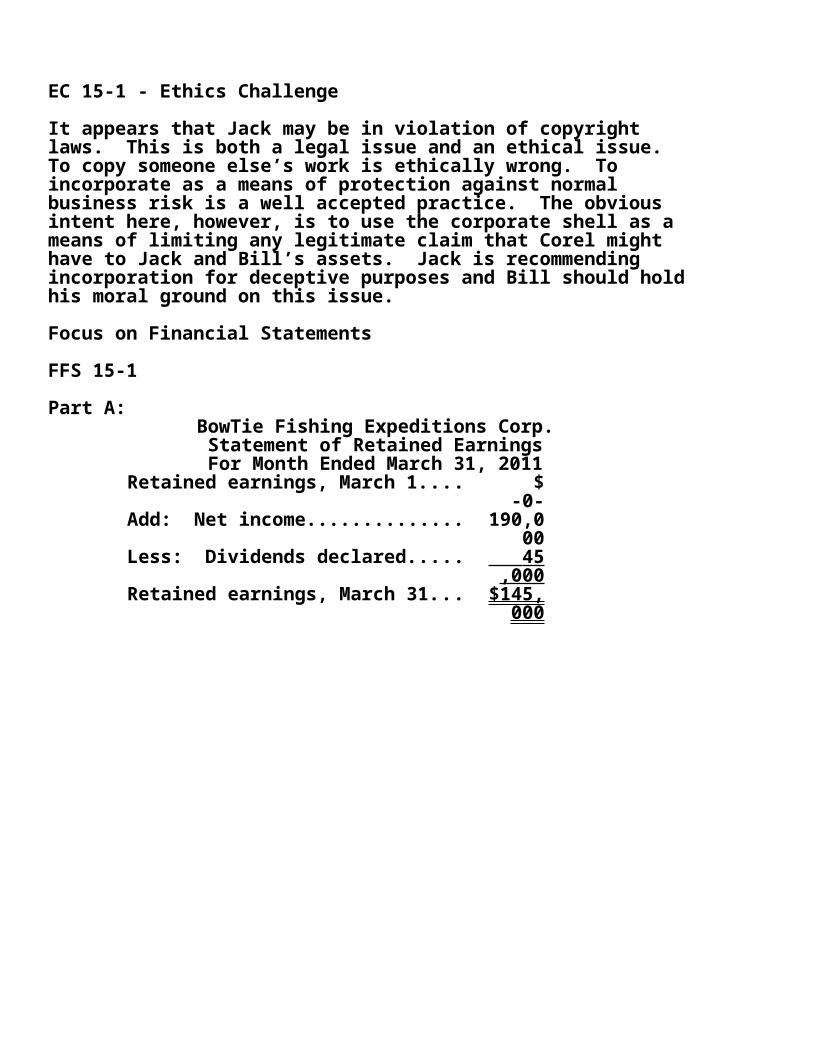

EC 15-1 - Ethics Challenge

It appears that Jack may be in violation of copyright laws. This is both a legal issue and an ethical issue. To copy someone else’s work is ethically wrong. To incorporate as a means of protection against normal business risk is a well accepted practice. The obvious intent here, however, is to use the corporate shell as a means of limiting any legitimate claim that Corel might have to Jack and Bill’s assets. Jack is recommending incorporation for deceptive purposes and Bill should hold his moral ground on this issue.

Focus on Financial Statements

FFS 15-1

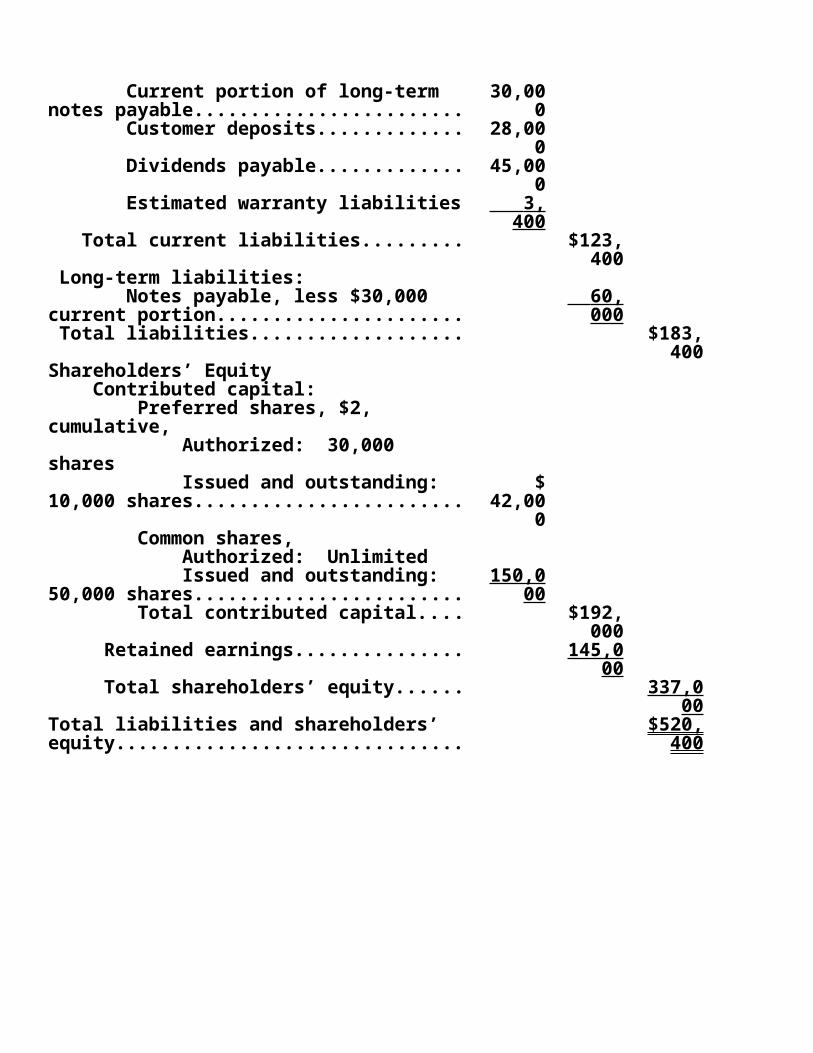

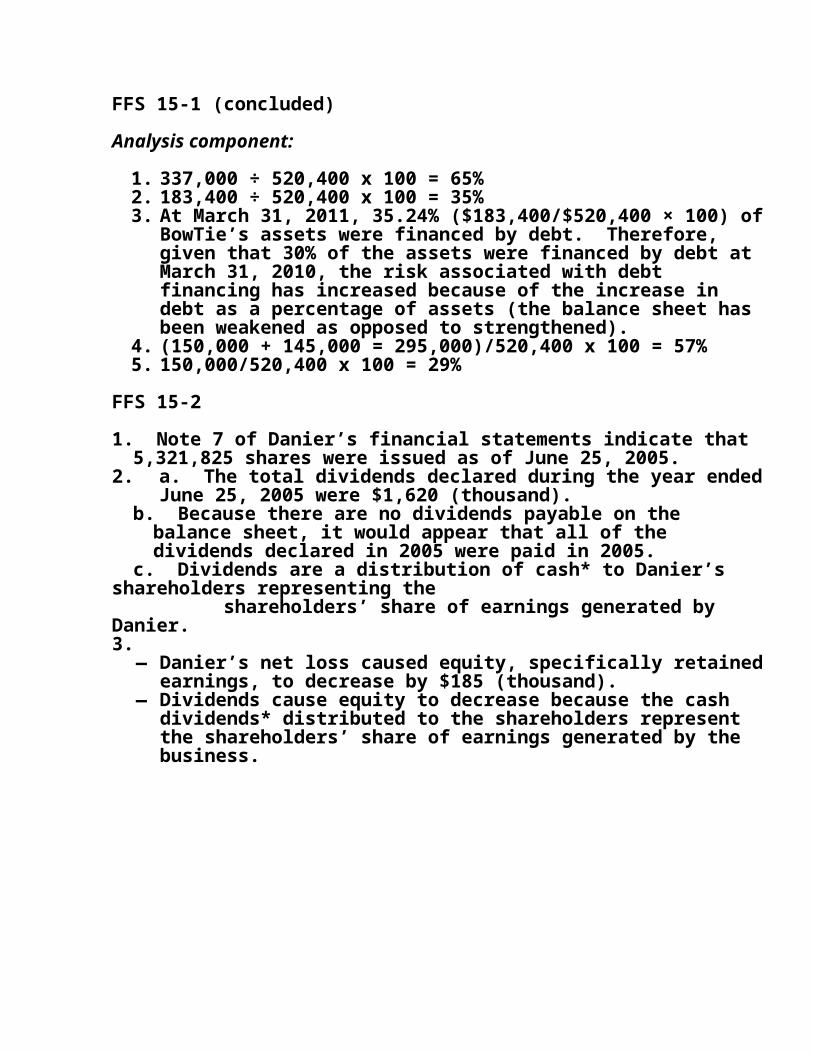

Part A:BowTie Fishing Expeditions Corp.Statement of Retained EarningsFor Month Ended March 31, 2011

Retained earnings, March 1...... $ -0-

Add: Net income...................... 190,000

Less: Dividends declared......... 45,0 00

Retained earnings, March 31... . $145,000

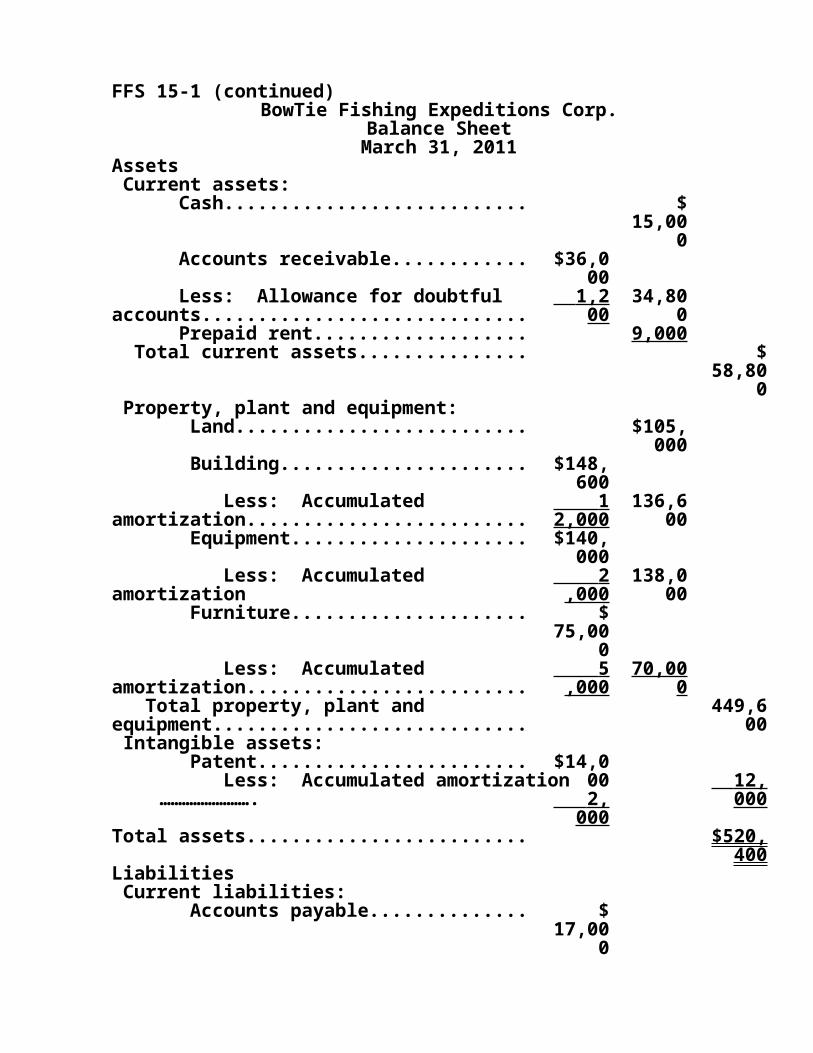

FFS 15-1 (continued)BowTie Fishing Expeditions Corp.

Balance SheetMarch 31, 2011

Assets Current assets: Cash.............................................. $

15,000

Accounts receivable....................... $36,000