Embed Size (px)

Citation preview

Chapter 14: Taxes and Chapter 14: Taxes and Government Spending Government Spending

Section 1Section 1

Chapter 14, Section 1

Objectives

1. Identify the sources of the government’s authority to tax.

2. Describe types of tax bases and tax structures.

3. List the characteristics of a good tax.

4. Identify who bears the burden of a tax.

Chapter 14, Section 1

Key Terms

tax: a required payment to a local, state, or national government

revenue: the income received by a government from taxes and other nontax sources

progressive tax: a tax for which the percentage of income paid in taxes increases as income increases

proportional tax: a tax for which the percentage of income paid in taxes remains the same at all income levels

regressive tax: a tax for which the percentage of income paid in taxes decreases as income increases

Chapter 14, Section 1

Key Terms, cont.

tax base: the income, property, good, or service that is subject to a tax

individual income tax: a tax based on a person’s earnings

corporate income tax: a tax based on a company’s profits

property tax: a tax based on real estate and other property

sales tax: a tax based on goods or services that are sold

incidence of tax: the final burden of a tax

Chapter 14, Section 1

Introduction

What are the features of a tax system? Fairness Simplicity Efficiency Certainty Balance between tax revenue and tax rates

Chapter 14, Section 1

Government’s Authority to Tax

We authorize the federal government, through the Constitution and our elected representatives in Congress, to raise money in the form of taxes. Taxation is the primary way that the government collects money.

Taxes give the government the money it needs to operate. The first power granted to Congress is the power to tax, which is

the basis of all federal laws.

Chapter 14, Section 1

Limits on the Government

There are also limits on the government’s power to tax. The purpose of a tax must be “for the common defense and

general welfare.” A tax cannot bring in money that goes to individual interests.

Federal taxes must be the same in every state. The government cannot tax exports, only imports.

Chapter 14, Section 1

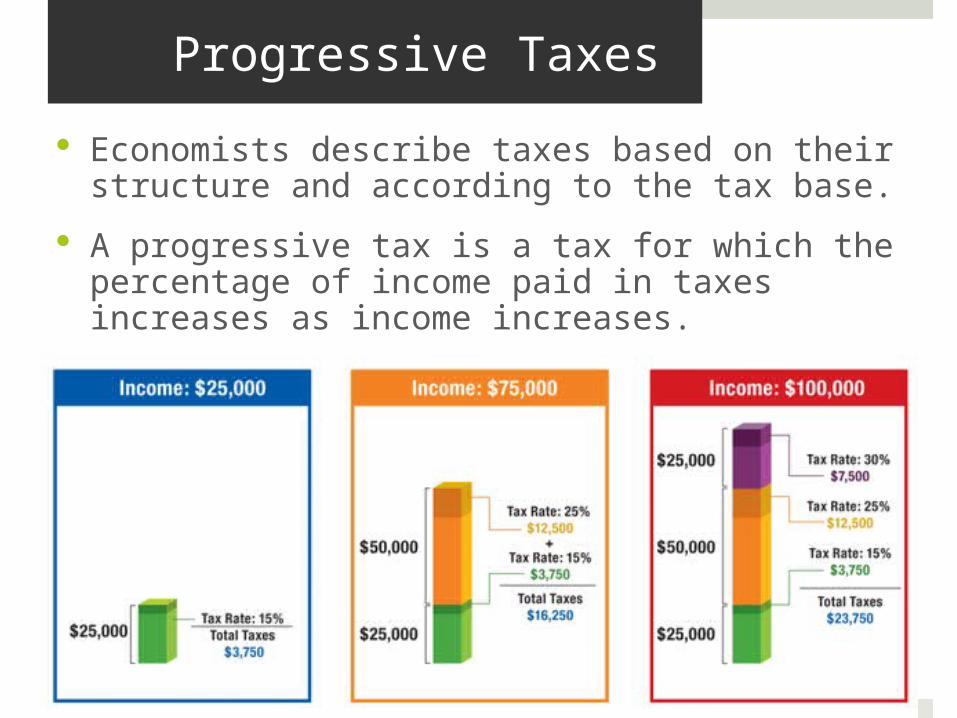

Progressive Taxes

Economists describe taxes based on their structure and according to the tax base.

A progressive tax is a tax for which the percentage of income paid in taxes increases as income increases.

Chapter 14, Section 1

Other Taxes

A proportional tax is a tax for which the percentage of income paid in taxes remains the same at all income levels.

A regressive tax is a tax for which the percentage of income paid in taxes decreases as income increases. A sales tax is regressive because higher income

households spend a lower proportion of their incomes on taxable goods and services.

Checkpoint: Is the federal income tax proportional, progressive, or regressive?

Chapter 14, Section 1

Tax Bases

Different taxes have different tax bases. The individuals income tax is based on a person’s earnings. The corporate income tax is based on a company’s profits. The property tax is based on real estate and other property. The sales tax is based on goods and services that are sold.

Chapter 14, Section 1

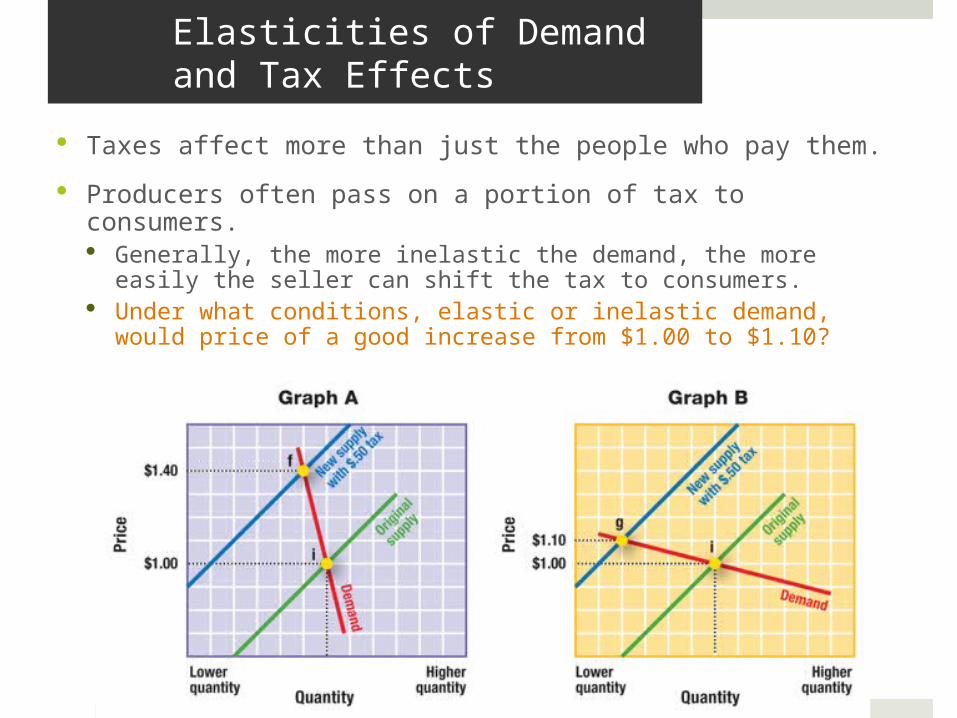

Elasticities of Demand and Tax Effects

Taxes affect more than just the people who pay them.

Producers often pass on a portion of tax to consumers. Generally, the more inelastic the demand, the more easily

the seller can shift the tax to consumers. Under what conditions, elastic or inelastic demand, would

price of a good increase from $1.00 to $1.10?

Chapter 14, Section 1

Chapter 14, Section 1

Characteristics of a Good Tax

Checkpoint: What are the four characteristics of a good tax? Simplicity—tax law should be easy to understand Efficiency—the tax should be able to be collected without

spending too much time or money Certainty—it should be clear when the tax is due, how much is

due, and how to pay the tax Equity—the tax system should ensure that no one bears too much

or too little of the tax

Chapter 14, Section 1

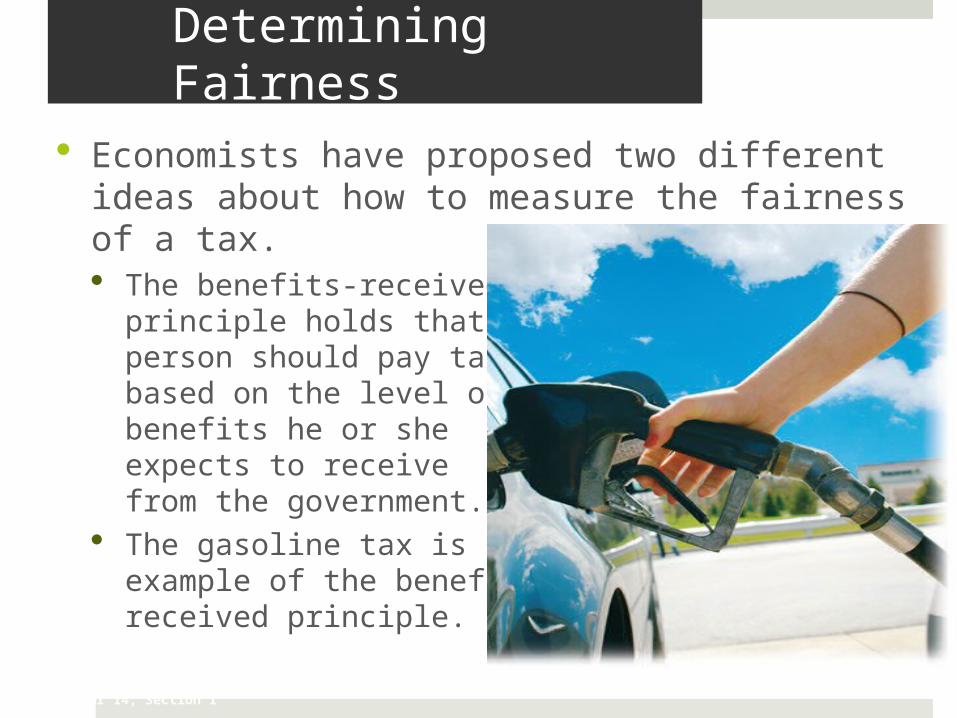

Determining Fairness

Economists have proposed two different ideas about how to measure the fairness of a tax. The benefits-received

principle holds that a person should pay taxes based on the level of benefits he or she expects to receive from the government.

The gasoline tax is an example of the benefits-received principle.

Chapter 14, Section 1

Determining Fairness, cont.

The ability-to-pay principle holds that people should pay taxes according to their ability to pay.

Good taxes generate enough, but not too much, revenue. Citizens needs are met, but not to such an extensive degree that the tax discourages production.

Chapter 14, Section 1

Review

Now that you have learned about the features of a tax system, go back and answer the Chapter Essential Question. How can taxation meet the needs of government and the people?

Chapter 14: Taxes and Chapter 14: Taxes and Government Spending Government Spending

Section 2Section 2

Chapter 14, Section 1

Objectives

1. Describe the process of paying individual income taxes.

2. Identify the basic characteristics of corporate income taxes.

3. Explain the purpose of Social Security, Medicare, and unemployment taxes.

4. Identify other types of taxes.

Chapter 14, Section 1

Key Terms

withholding: taking tax payments out of an employee’s pay before he or she receives it

tax return: a form used to file income taxes

taxable income: the earnings on which tax must be paid; total income minus exemptions and deductions

personal exemption: a set amount that taxpayers may subtract from their gross income for themselves, their spouse, and any dependents

tax deduction: a variable amount that taxpayers may subtract from their gross income

Chapter 14, Section 1

Key Terms, cont.

tax credit: a variable amount that taxpayers may subtract from the total amount of their income tax

estate tax: a tax on the total value of the money and property of a person who has died

gift tax: a tax on the money or property that one living person gives to another

tariff: a tax on imported goods

tax incentive: the use of taxation to discourage or encourage certain types of behavior

Chapter 14, Section 1

Introduction

What taxes does the federal government collect? Individual income taxes Corporate income taxes Social Security, Medicare, and unemployment taxes Excise taxes and tariffs Estate and gift taxes

Chapter 14, Section 1

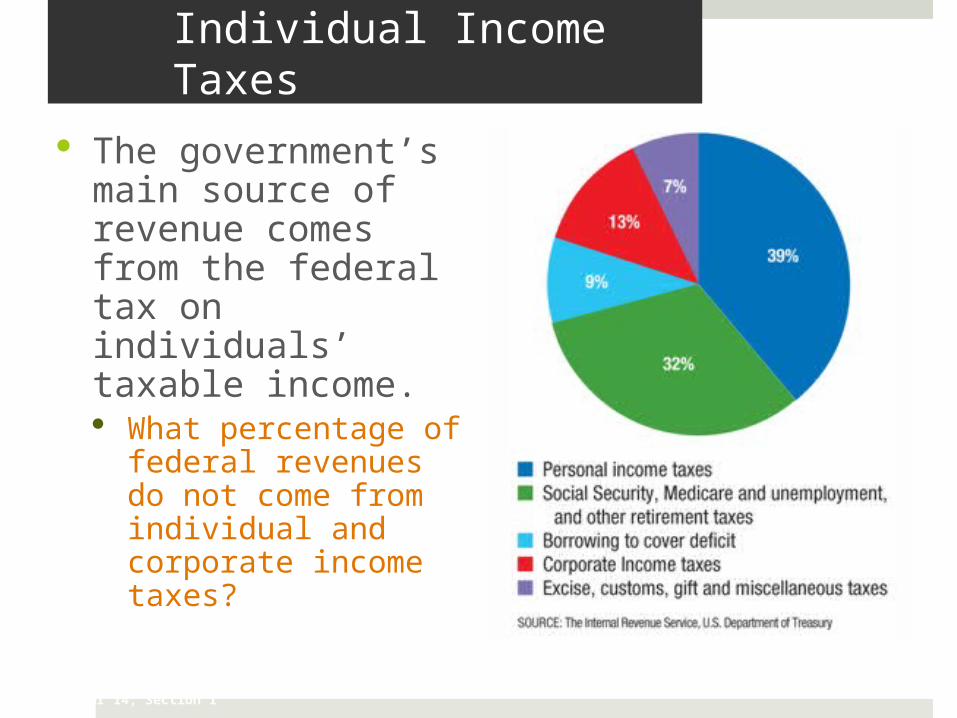

Individual Income Taxes

The government’s main source of revenue comes from the federal tax on individuals’ taxable income. What percentage of

federal revenues do not come from individual and corporate income taxes?

Chapter 14, Section 1

“Pay-As-You-Earn” Taxation

The amount of federal income tax a person owes is determined on an annual basis. To lessen the burden that one large yearly tax would place on an

individual and to make it possible for the government to meet its regular expenses, federal income tax is collected in a “pay-as-you-earn” system. This means that individuals usually pay most of their income

tax throughout the year as they earn income.

Chapter 14, Section 1

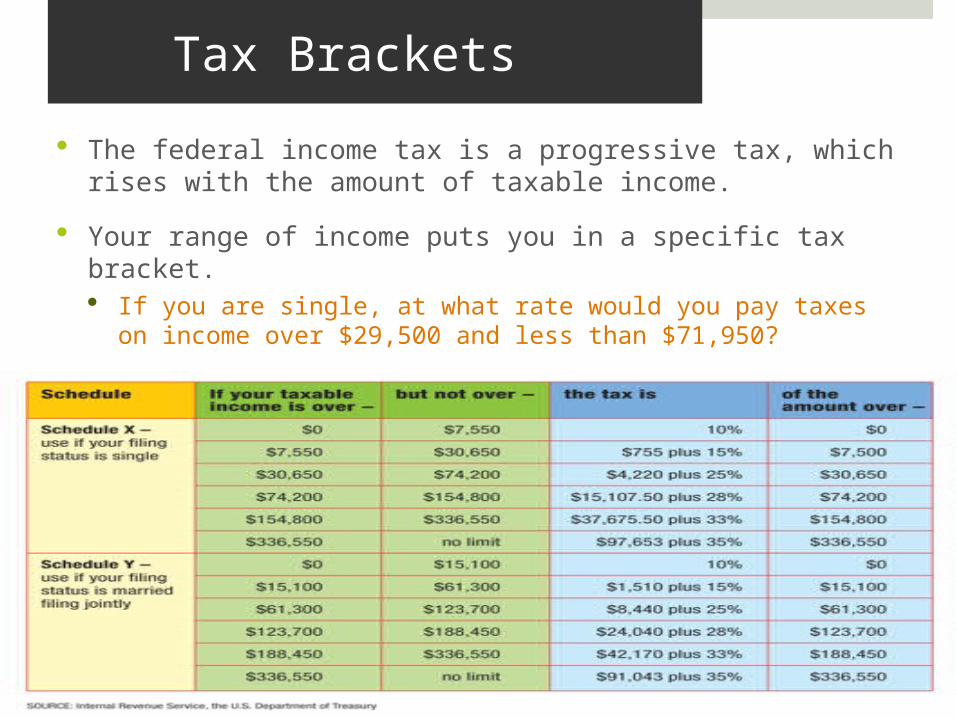

Tax Brackets

The federal income tax is a progressive tax, which rises with the amount of taxable income.

Your range of income puts you in a specific tax bracket. If you are single, at what rate would you pay taxes on

income over $29,500 and less than $71,950?

Chapter 14, Section 1

Withholdings and Tax Returns

Employers help collect taxes by withholding money from your paycheck based on an estimate of how much you will owe in federal income tax for that year.

After the calendar year ends, employers give their employees a report of how much income tax has already been paid. Employees then fill out a tax return to send to the federal

government.

Chapter 14, Section 1

Tax Returns, cont.

On your tax return, you figure out how much of your income is taxable. Taxable income is a

person’s total income minus exemptions and deductions.

Tax returns are due to the Internal Revenue Service by April 15.

Chapter 14, Section 1

Corporate Income Taxes

Like individual income taxes, corporate income taxes are progressive.

Determining corporate income taxes can be more difficult than determining an individual’s because businesses can take many deductions. Companies often deduct the cost of employee’s health

insurance as well as many other costs of doing business. Checkpoint: Why is it difficult to determine a corporation’s

taxable income?

Chapter 14, Section 1

Social Security and Medicare

Employees also withhold money to help fund Social Security, Medicare, and unemployment insurance under the Federal Insurance Coalition Act (FICA). Most of the FICA taxes you pay go to Social Security benefits for

retired people, surviving members of wage earners, and disabled people.

The Medicare tax helps pay for health insurance for people over 65.

Chapter 14, Section 1

Unemployment

The unemployment tax pays for “unemployment compensation” that people can receive when they are laid off.

Chapter 14, Section 1

Other Types of Taxes

Excise taxes—a general revenue tax on the sale or manufacture of a good or service such as gasoline, cigarettes, and other items

Estate taxes—a tax on the total value of the money and property of a person who has died As of 2008, if the total value of an estate is $2 million or less, there

is no federal estate tax.

Chapter 14, Section 1

Other Types of Taxes, cont.

Gift taxes—a tax on the money or property that one living person gives to another The goal of the gift tax is to stop people from avoiding the estate

tax by giving away property before they died.

Import taxes—Tariffs, or import taxes, are taxes placed on imported goods.

Chapter 14, Section 1

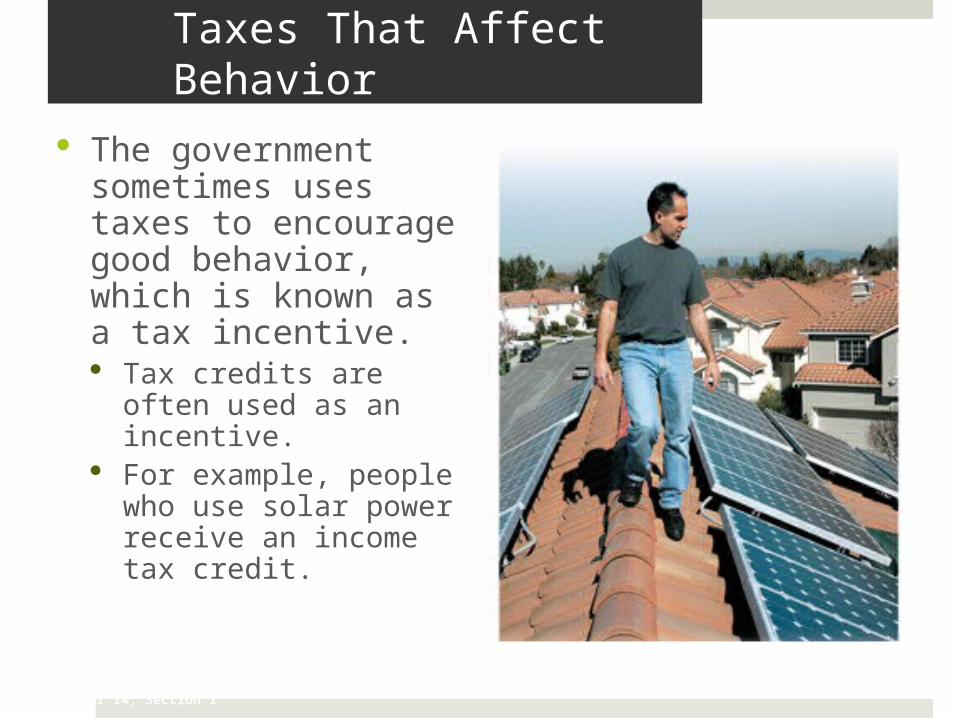

Taxes That Affect Behavior

The government sometimes uses taxes to encourage good behavior, which is known as a tax incentive. Tax credits are often

used as an incentive. For example, people

who use solar power receive an income tax credit.

Chapter 14, Section 1

Review

Now that you have learned about the taxes that the federal government collects, go back and answer the Chapter Essential Question. How can taxation meet the needs of government and the people?

Chapter 14: Taxes and Chapter 14: Taxes and Government Spending Government Spending

Section 3Section 3

Chapter 14, Section 1

Objectives

1. Distinguish between mandatory and discretionary spending.

2. Describe the major entitlement programs.

3. Identify categories of discretionary spending.

4. Explain the impact of federal aid to state and local governments.

Chapter 14, Section 1

Key Terms

mandatory spending: spending that Congress is required by existing law to do

discretionary spending: spending about which Congress is free to make choices

entitlement: social welfare program that people are “entitled to” benefit from if they meet certain eligibility requirements

Chapter 14, Section 1

Introduction

How does the federal government spend its income? Federal spending is divided up into mandatory and discretionary

spending. Mandatory spending pays for Social Security, Medicare,

Medicaid, and other entitlements. Discretionary spending pays for everything else, including

defense, education, law enforcement, environmental cleanup, and disaster aid.

Chapter 14, Section 1

Federal Spending

There are two types of government spending.

Mandatory spending is money that Congress is required by existing law to spend on certain programs or to use for interest payments on the national debt.

Discretionary spending is spending about which lawmakers are free to make choices.

Chapter 14, Section 1

Federal Spending, cont.

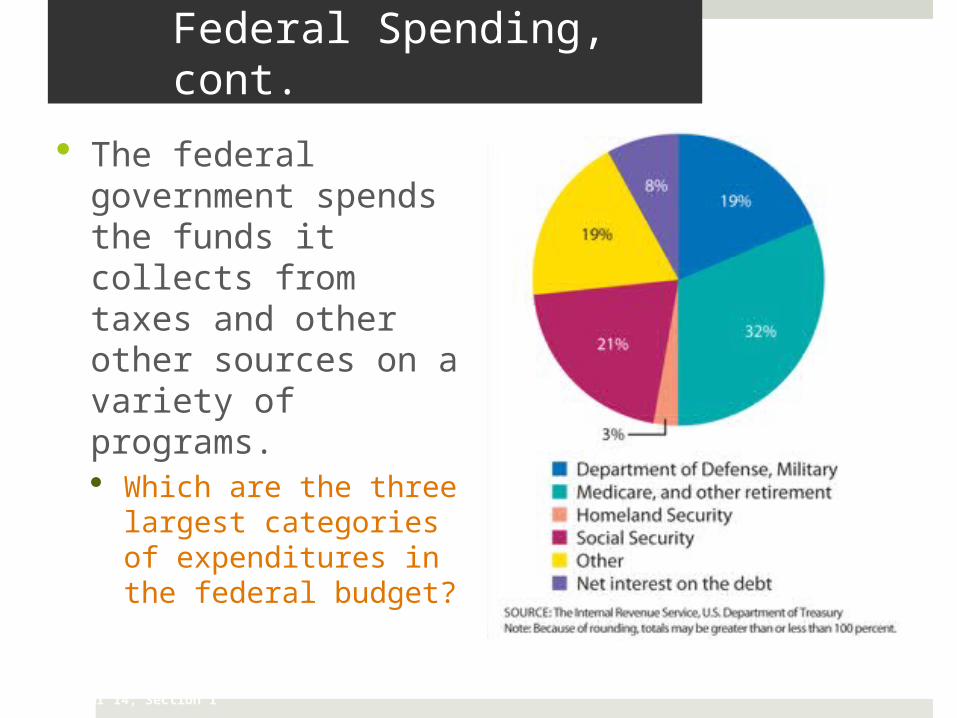

The federal government spends the funds it collects from taxes and other other sources on a variety of programs. Which are the three

largest categories of expenditures in the federal budget?

Chapter 14, Section 1

Entitlement Programs

Most of the mandatory spending items are for entitlement programs, which fund social welfare programs.

The federal government guarantees assistance for all people who quality for such programs.

Entitlements are a largely unchanging part of government spending. Congress can only change the eligibility requirements or

reduce benefits if there is a change in the law.

Chapter 14, Section 1

Social Security

Social Security is a huge portion of federal spending. About 50 million Americans receive monthly benefits from

the Social Security Administration.

The future of Social Security is uncertain. As the millions of baby

boomers—people born after World War II—start to retire, the ratio of existing workers, who pay for Social Security, to retirees will fall.

Chapter 14, Section 1

Medicare and Medicaid

About 42 million people receive Medicare benefits. It pays for hospital care and for the costs of physicians and

medical services. Medicare costs have been

rising as a result of expensive technology and people living longer. It faces the same problem as Social Security.

Medicaid benefits help low-income families pay for their medical expenses The federal government

shares the cost of Medicaid with state governments.

Chapter 14, Section 1

Other Mandatory Programs

Other means-tested entitlements benefit people and families whose incomes fall below a certain level. These entitlements include: Food stamps and child nutrition programs Retirement benefits and insurance for federal workers Veterans’ pensions Unemployment insurance

In recent years, there has been a debate over governmentally funded universal healthcare.

Chapter 14, Section 1

Discretionary Spending

Checkpoint: Approximately how much of the federal government’s discretionary spending goes toward defense? Defense spending accounts

for about half of the government’s discretionary spending.

The Department of Defense uses this money to pay salaries of enlisted men and women as well as its civilian employees.

This money also buys weapons, missiles, ships, tanks, airplanes, and equipment.

Chapter 14, Section 1

Discretionary Spending, cont.

The remaining discretionary funds go to pay for the following: Education and training Scientific research Student loans Law enforcement Environmental cleanup Disaster relief

Chapter 14, Section 1

Federal Aid

Federal taxes are sometimes used to help state and local governments. State and federal governments share the cost of Medicaid,

unemployment insurance, education, lower-income housing, highway construction, and dozens of other programs.

States also rely on federal aid for disaster relief.

Chapter 14, Section 1

Review

Now that you have learned about how the federal government spends its income, go back and answer the Chapter Essential Question. How can taxation meet the needs of government and the people?

Chapter 14: Taxes and Chapter 14: Taxes and Government Spending Government Spending

Section 4Section 4

Chapter 14, Section 1

Objectives

1. Explain how states use a budget to plan their spending.

2. Identify where state taxes are spent.

3. List the major sources of state tax revenue.

4. Describe local government spending and sources of revenue.

Chapter 14, Section 1

Key Terms

budget: an estimate of future revenue and expenses

operating budget: a budget for day-to-day spending needs

capital budget: a budget for spending on major investments

balanced budget: a budget in which revenue and spending are equal

Chapter 14, Section 1

Key Terms, cont.

tax exempt: not subject to taxes

real property: land and any permanent structures on the land to which a person has legal title

personal property: movable possessions or assets

tax assessor: an official who determines the value of property

Chapter 14, Section 1

Introduction

How do local governments manage their money? Local governments manage their money in accordance

with priorities set by elected local government officials. Local governments create budgets and collect taxes just

like the federal government.

Chapter 14, Section 1

State Budgets

Governments plan their spending by creating a budget.

The federal government has one budget while state governments have two budgets. An operating budget is a budget for day-to-day spending

needs. A capital budget is spending on major investments.

Unlike the federal government, 49 states require balanced budgets—budgets in which revenues are equal to spending. Checkpoint: Would the construction of a new courthouse

come out of a state’s operating budget or capital budget?

Chapter 14, Section 1

Where are State Taxes Spent?

Education Every state spends taxpayer money to support at

least one public state university. They also provide financial help to local governments

for public elementary and secondary schools.

Public Safety State police enforce traffic laws and help motorists in

an emergency. State governments build and run corrections

systems.

Public Welfare State funds support hospitals and clinics and

unemployment benefits.

Chapter 14, Section 1

Where are State Taxes Spent?

Highway and Transportation State crews resurface roads and repair bridges. States pay some of the cost of facilities like waterways

and airports.

Arts and Recreation States fund parks, nature reserves, museums, and art

and music programs.

Administration State governments spend money to keep the

government running. Revenues pay for state workers’ salaries.

Chapter 14, Section 1

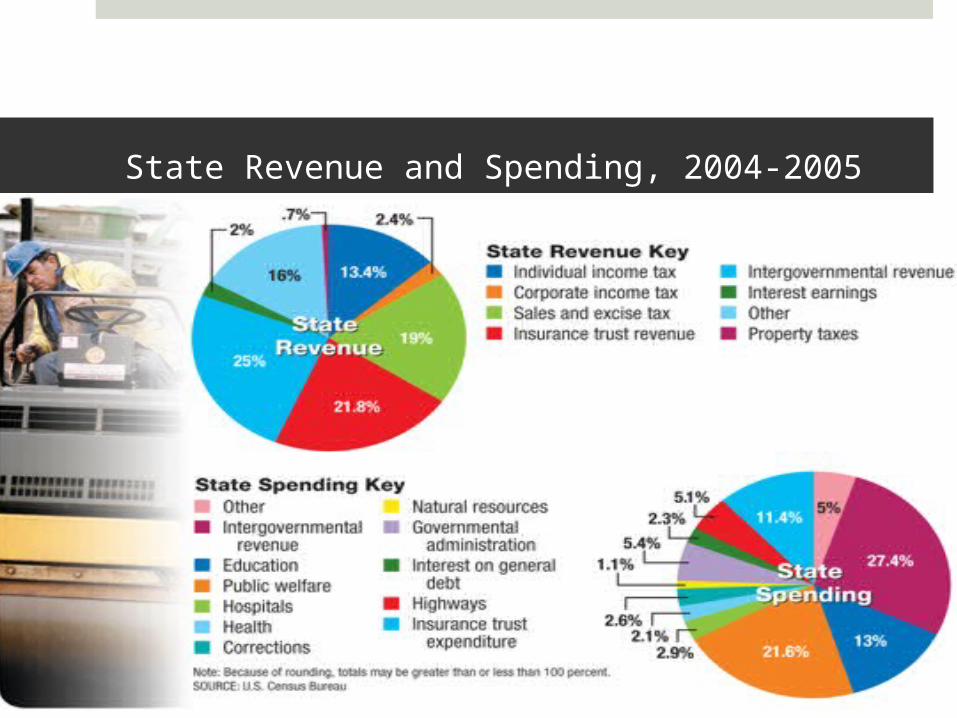

State Revenue and Spending, 2004-2005

Chapter 14, Section 1

State Tax Revenue

States receive most of their revenue through taxes. Sales tax on goods and services is the main source

of state revenue. Some goods, like food and clothing, are tax exempt

in certain states. Even states without a sales tax impose excise taxes

that apply to specific products and activities. Many states also collect an individual income tax,

which is paid in addition to the federal income tax. Some states tax at a flat rate while other have

progressive rates.

Chapter 14, Section 1

State Tax Revenue, cont.

Corporate income tax—Most states collect income taxes from corporations that do business in the state. These taxes make up a small amount of state tax

revenues.

Other state taxes include: Licensing fees on certain businesses Transfer taxes on stock certificates Inheritance taxes Property taxes, including real property and personal

property

Chapter 14, Section 1

Chapter 14, Section 1

Local Government

Local governments, including towns, cities, countries, and school districts, carry major responsibilities in the public school systems, law enforcement, and fire protection. They also manage public facilities, parks, and recreation

facilities. They monitor public health, public transportation,

elections, record keeping, and social services.

Chapter 14, Section 1

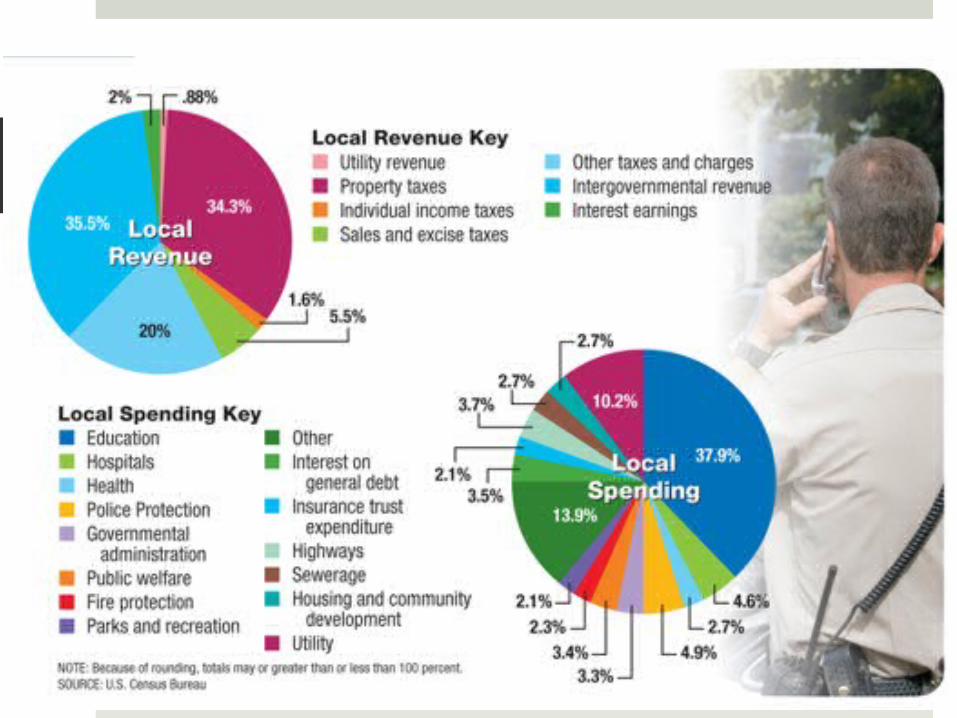

Local Revenue and Spending 2007

Chapter 14, Section 1

Local Government Taxes

Local governments levy property taxes, sales taxes, excise taxes, and income taxes.

Many local taxes affect visitors and are designed to raise revenue from nonresidents. Wall-to-wall traffic

jams, for example, are prompting a few cities to consider a congestion tax.

Chapter 14, Section 1

Review

Now that you have learned about how local governments manage their money, go back and answer the Chapter Essential Question. How can taxation meet the needs of government and the

people?