Embed Size (px)

Citation preview

Chapter 14

Georgia Real Estate An Introduction to the Profession

Eighth Edition

Chapter 14

Taxes and Assessments

Key Terms• ad valorem taxes• amount realized• assessed value• assessment appeal

board• basis

• documentary tax• installment method• mill rate• tax certificate• tax lien

© 2015 OnCourse Learning

Property Taxes

The largest single source of income in the United States for local government programs and services is the property tax. Schools, fire and police departments, libraries, parks and more are mainly supported by property taxes.

© 2015 OnCourse Learning

Property Taxes

Property taxes are ad valorem taxes. They are levied according to the value of one’s property.

© 2015 OnCourse Learning

Budget and Appropriation

Each taxing body prepares its budget for the coming year. Each budget is enacted into law through the appropriation process.

© 2015 OnCourse Learning

Budget and Appropriation

Estimated sales taxes, business licenses and other taxes are subtracted from the budget. The balance must come from property taxes.

© 2015 OnCourse Learning

Appraisal and Assessment

The valuation of the taxable property within each district must be determined. The assessor’s office appraises each taxable parcel of land.

© 2015 OnCourse Learning

Appraisal and Assessment

The appraised value is converted into an assessed value upon which the taxes are based.

© 2015 OnCourse Learning

Appraisal and Assessment

In Georgia, the assessed value is 40% of the market value.

© 2015 OnCourse Learning

Tax Rate Calculation

The assessed values of all properties subject to property taxation are added together to calculate the tax rate.

For example: the district requires $8 million from property taxes and the assessed value of property within the district is $200 million.

© 2015 OnCourse Learning

Tax Rate Calculation

By dividing $8 million by $200 million, we discover the district must collect a tax of 4% or $4.00 per thousand dollars of assessed valuation.

© 2015 OnCourse Learning

Tax Rate Calculation

This levy can be expressed three ways:• as a mill rate• as dollars per hundred• as dollars per thousand

© 2015 OnCourse Learning

Tax Rate Calculation

Mill rate is the property tax rate that is expressed in tenths of a cent per dollar of assessed value.

As a mill rate, this tax is usually expressed as dollars per thousand.

© 2015 OnCourse Learning

Applying the Rate

Apply the mill rate to a home by multiplying the mills by the assessed valuation.

Assessed value of $200,000 with a tax rate of 80 mills ($80.00 per thousand dollars of assessed value)

200 x 80 = $16,000

© 2015 OnCourse Learning

Applying the Rate

To ensure collection, a tax lien for this amount is placed against the property. It is removed when the tax is paid.

Property tax liens are superior to other types of liens. A mortgage foreclosure does not clear property tax liens; they still must be paid.

© 2015 OnCourse Learning

Applying the Rate

Property tax years are assessed and collected on a calendar year basis, January 1 through December 31.

© 2015 OnCourse Learning

Unpaid Property Taxes

If you own real estate and you fail to pay the property taxes, you will lose the property.

© 2015 OnCourse Learning

Unpaid Property Taxes

A redemption period follows during which the owner can redeem the property by paying back taxes and penalties.

© 2015 OnCourse Learning

Unpaid Property Taxes

If redemption does not occur, the property is sold at a publicly announced auction and the highest bidder receives a tax deed.

© 2015 OnCourse Learning

Unpaid Property Taxes

At the sale, a tax certificate in the amount of the unpaid taxes is sold.

The purchaser is entitled to a deed to the property provided the delinquent taxpayer does not step forward and redeem it during the redemption period.

© 2015 OnCourse Learning

Unpaid Property Taxes

The redemption period for a tax sale in Georgia is one year.

A lienholder is allowed to redeem a property if the property taxes are not paid because the lienholder's creditor rights in the property are cut off due to the superiority of the tax lien.

© 2015 OnCourse Learning

Assessment Appeal

Property owners can compare the assessed value of their property with values on similar properties. An owner who feels over-assessed can file an appeal before an assessment appeal board or a board of equalization.

© 2015 OnCourse Learning

Property Tax Exemptions

More than half the land in many cities and counties is exempt from real property taxes because governments and their agencies do not tax themselves or each other.

© 2015 OnCourse Learning

Property Tax Exemptions

Most properties owned by religious and charitable organizations are also exempt.

© 2015 OnCourse Learning

Property Tax Exemptions

Georgia grants an assessment reduction known as homestead exemption. This reduces the amount of taxes owed on property used as a primary residence.

© 2015 OnCourse Learning

Property Tax Variations

The amount and type of taxable property in a community affects local tax rates.

© 2015 OnCourse Learning

Special Assessments

Local municipal improvements that will benefit property owners within a limited area are financed through special assessments on property.

The property receiving the benefit of an improvement in the area bears the cost of the improvement.

© 2015 OnCourse Learning

Calculating a Home’s Basis

Income taxes are due if you sell your personal residence for more than you paid.

The first step in determining the amount of taxable gain upon the sale of a residence is to calculate the home’s basis.

© 2015 OnCourse Learning

Calculating a Home’s Basis

The basis is the price originally paid for the home, plus any fees paid for closing services and legal counsel, and any fee or commission paid to help find the property.

© 2015 OnCourse Learning

Calculating a Home’s Basis

Improvements made by the seller are added to the original cost of the home.

Adding a bedroom, installing a new roof, paving a new driveway are classed as improvements and are added to the home’s basis.

© 2015 OnCourse Learning

Calculating a Home’s Basis

Maintenance and repairs are not added, as they only maintain the property in ordinary operating condition.

© 2015 OnCourse Learning

Calculating the Amount RealizedThe amount realized is the selling price of the home, less selling expenses.

Selling expenses include brokerage commissions, advertising, legal fees, title services, closing fees and mortgage points paid by the seller.

© 2015 OnCourse Learning

Calculating Gain on the Sale

The gain on the sale is the difference between the amount realized and the basis.

This is the amount to be reported as gain on the seller’s annual income tax forms.

© 2015 OnCourse Learning

Calculating Gain on the Sale

© 2015 OnCourse Learning

$90,000 Purchase price + $500 closing costs Basis $ 90,500

$3,500 landscaping and fencing Basis $ 94,000

$15,000 Bedroom and bathroom Basis $109,000

$125,000 Sales Price

$8,000 commissions and closing costs

Amt. realized $117,000

Amt. realized $117,000

Less basis -$109,000

Equals gain $ 8,000

Income Tax Exclusion

A taxpayer can exclude $250,000 of gain from the sale of the taxpayer’s principal residence.

If the taxpayer is married, there is a $500,000 exclusion for married individuals filing jointly.

© 2015 OnCourse Learning

Income Tax Exclusion

The taxpayer must have lived in the home for two of the last five years.

This exclusion cannot be taken more frequently than once every two years.

© 2015 OnCourse Learning

Capital GainsCapital gains tax is a tax levied on an investment.

Stocks, bonds, precious metals, real estate or anything else purchased with the hopes of making a profit.

© 2015 OnCourse Learning

Capital Gains Tax Rate

© 2015 OnCourse Learning

Tax Bracket 1/1/01 – 5/5/03

5/6/03 –12/31/07

2008 2009

10% & 15% 8% / 10% 5% 0% 10%

25% & up 20% 15% 15% 20%

Installment Method

When a gain cannot be excluded, a popular method of deferring income taxes is to use the installment method of reporting the gain.

If you sell for all cash, you are required to pay all the income taxes due on that gain in the year of the sale.

© 2015 OnCourse Learning

Installment Method

A solution is to sell to the buyer on terms rather than to send the buyer to a lender to obtain a loan.

The gain would then be taxed at the income tax rates at the time the installment is received.

© 2015 OnCourse Learning

Property Tax and Interest Deductions

A homeowner can deduct real property taxes and personal property taxes from other income when calculating income taxes.

This applies to single-family residences, condos, and cooperatives.

© 2015 OnCourse Learning

Property Tax and Interest Deductions

Interest paid to finance the purchase of a home is deductible against a homeowner’s other income.

© 2015 OnCourse Learning

Interest Deduction Limitations

All of the interest is deductible on a loan to purchase a first or second home.

The ability to deduct property taxes and mortgage interest becomes more valuable in higher tax brackets.

© 2015 OnCourse Learning

Agent’s Liability for Tax Advice

A real estate agent is liable for tax advice (or lack of it) if the advice is material to the transaction and to give such advice is common in the brokerage business.

© 2015 OnCourse Learning

Agent’s Liability for Tax Advice

An agent should have enough general knowledge of real estate tax laws to be able to answer basic questions accurately, and to warn clients and recommend tax counsel if the questions posed by the transaction are beyond the agent’s knowledge.

© 2015 OnCourse Learning

Agent’s Liability for Tax Advice

An agent is responsible for the quality and accuracy of tax information given out by the agent.

© 2015 OnCourse Learning

Transfer Tax

Georgia requires a conveyance tax more commonly referred to as a transfer tax when the deed is recorded.

The rate is $0.10 per $100 on the adjusted sales price.

© 2015 OnCourse Learning

Transfer Tax

The adjusted sales price is the sales price minus any assumed loan.

These fees are paid to the county recorder prior to recording and are in addition to the fee for recording itself.

© 2015 OnCourse Learning

Intangibles Tax

Georgia also charges a separate tax on the value of any mortgage debt created by the transaction.

The intangibles tax is paid at a rate of $1.50 per $500 (or any part of $500) of any new recorded loan.

© 2015 OnCourse Learning

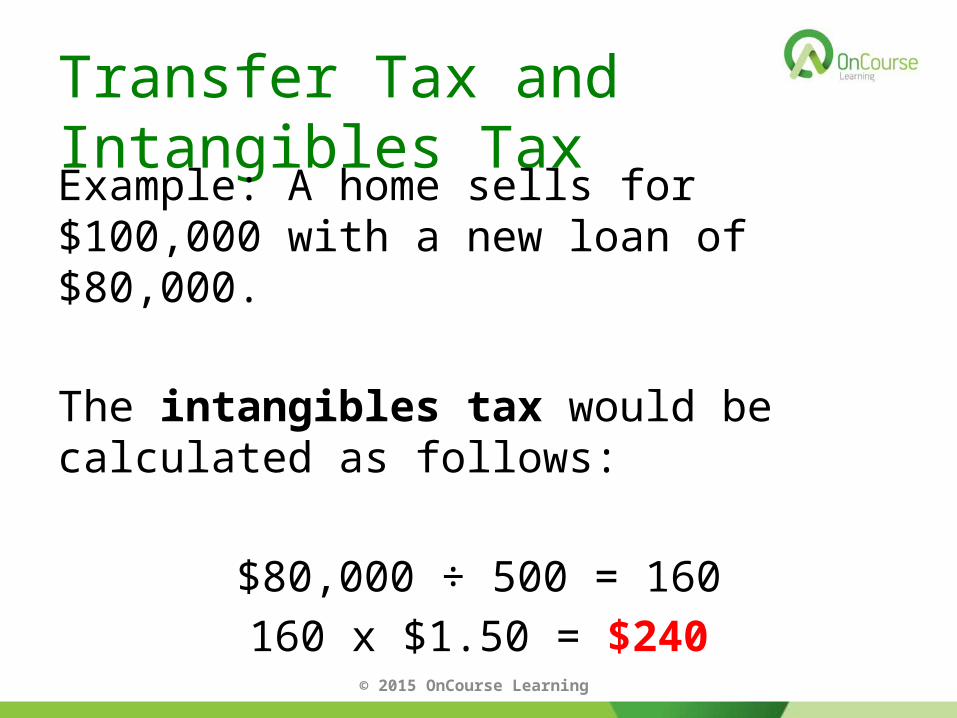

Transfer Tax and Intangibles TaxExample: A home sells for $100,000 with a new loan of $80,000.

The transfer tax would be calculated as follows:

$100,000 ÷ 100 = 1,000 1,000 x $0.10 = $100.00

© 2015 OnCourse Learning

Transfer Tax and Intangibles TaxExample: A home sells for $100,000 with a new loan of $80,000.

The intangibles tax would be calculated as follows:

$80,000 ÷ 500 = 160160 x $1.50 = $240

© 2015 OnCourse Learning

Transfer Tax and Intangibles TaxWhen calculating transfer tax and intangibles tax, remember to round up your calculations.

Transfer tax is always divisible by $0.10.

Intangibles tax is always divisible by $1.50.

If there are pennies in your answer, you didn’t round up.© 2015 OnCourse Learning

Transfer Tax and Intangibles TaxExample: A home sells for $344,050 with a new loan of $309,600.

Transfer tax would be calculated as follows:

$344,050 ÷ 100 = 3,441 (round up) 3,441 x $0.10 = $344.10

© 2015 OnCourse Learning

Transfer Tax and Intangibles TaxExample: A home sells for $344,050 with a new loan of $309,600.

Intangibles tax would be calculated as follows:

$309,600 ÷ 500 = 620 (round up)620 x $1.50 = $930.00

© 2015 OnCourse Learning

Transfer Tax and Intangibles TaxExample: A home sells for $132,400 with an assumed loan of $51,000.

Transfer tax would be calculated as follows:

$132,000 - $51,000 = $81,400$81,400 ÷ 100 = 814

814 x $0.10 = $81.40© 2015 OnCourse Learning

Transfer Tax and Intangibles Tax

A home sells for $250,000 for cash.

There would be no intangibles tax because there is no loan.

© 2015 OnCourse Learning

Transfer Tax and Intangibles Tax

Transfer tax is usually paid by the seller, but it is negotiable.

Intangibles tax is usually paid by the borrower, but it is negotiable.

© 2015 OnCourse Learning