Embed Size (px)

Citation preview

Chapter 12

Preparing Payroll Records

In Chapter 12

You will learn:• Define accounting terms related to payroll records.

• Identify accounting practices related to payroll records.

• Complete a payroll time card.

• Calculate payroll taxes.

• Complete a payroll register and an employee earnings record.

• Prepare payroll checks.

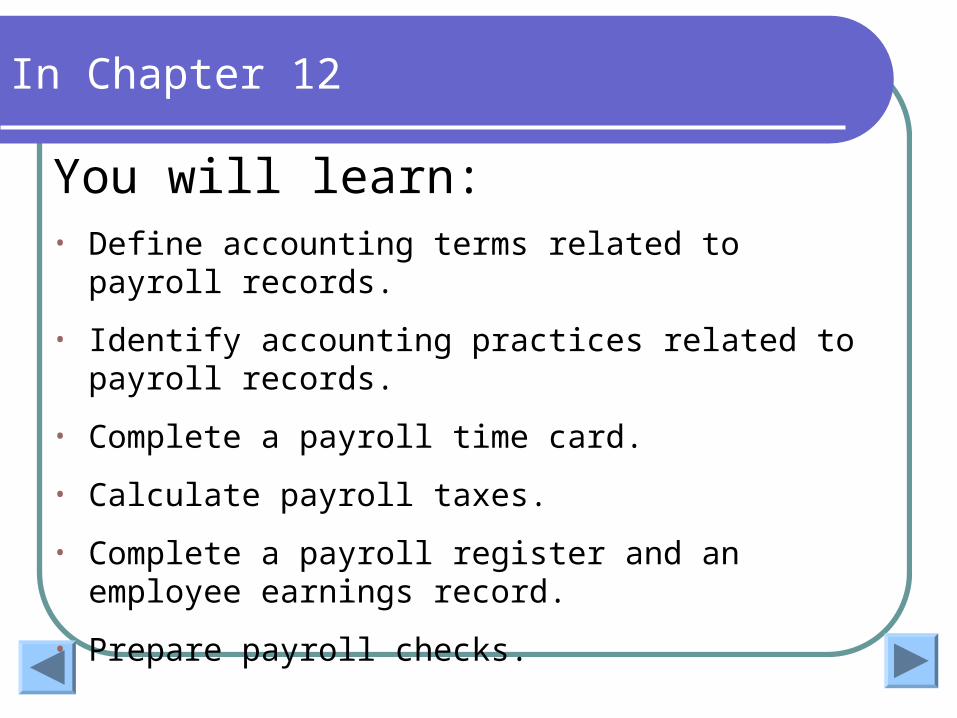

Reporting Current and Non-Current Liabilities

Current Liabilities are debts that will be

settled within the next year

Long-term Liabilities are debts that will NOT be settled

within the next year

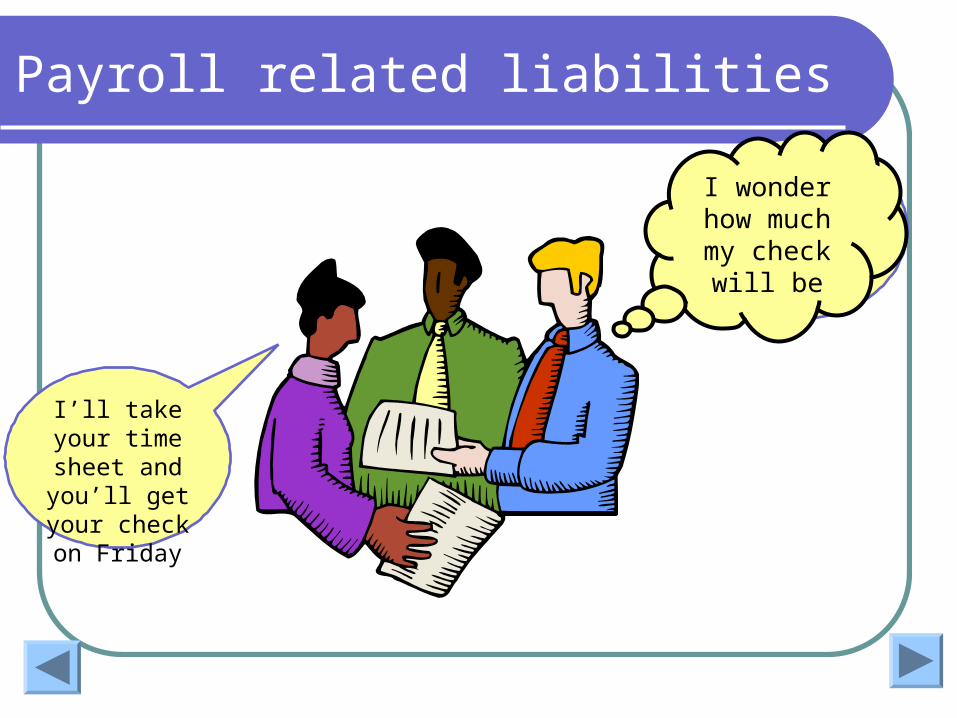

Payroll related liabilities

I worked 40 hours this week. My hourly rate

is $12.50.

I’ll take your time sheet and you’ll get your

check on Friday

I wonder how much my

check will be

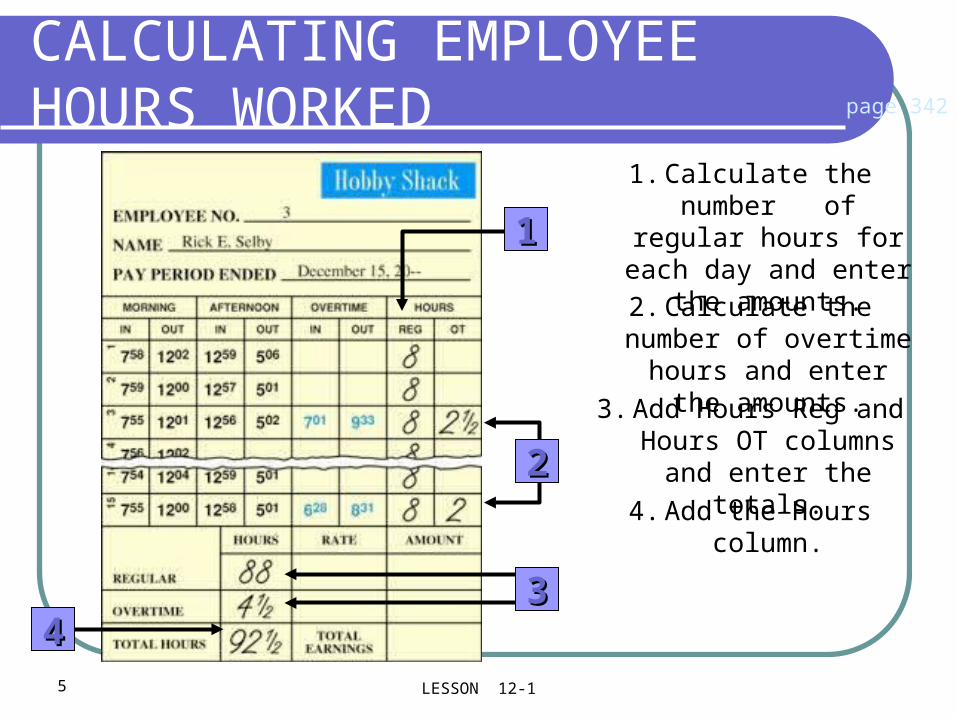

5 LESSON 12-1

4. Add the Hours column.

CALCULATING EMPLOYEE HOURS WORKED page 342

11

22

3344

3. Add Hours Reg and Hours OT columns and

enter the totals.

2. Calculate the number of overtime hours and enter the amounts.

1. Calculate the number of regular hours for each

day and enter the amounts.

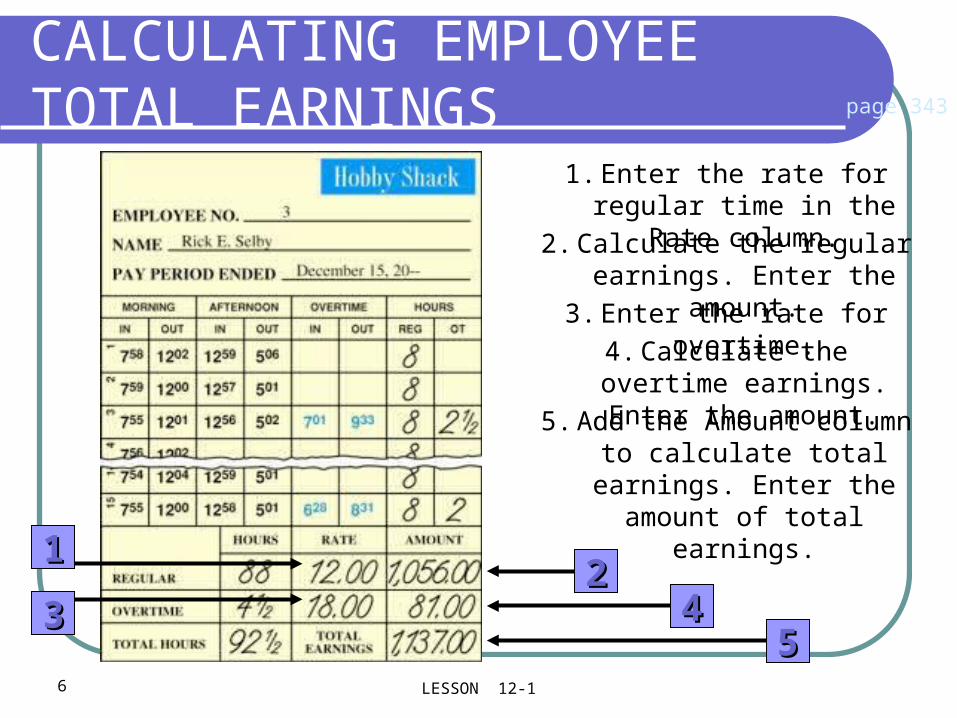

6 LESSON 12-1

CALCULATING EMPLOYEE TOTAL EARNINGS page 343

33

1122

4455

1. Enter the rate for regular time in the Rate column.

2. Calculate the regular earnings. Enter the amount.

3. Enter the rate for overtime.

4. Calculate the overtime earnings. Enter the amount.

5. Add the Amount column to calculate total earnings. Enter the amount of total

earnings.

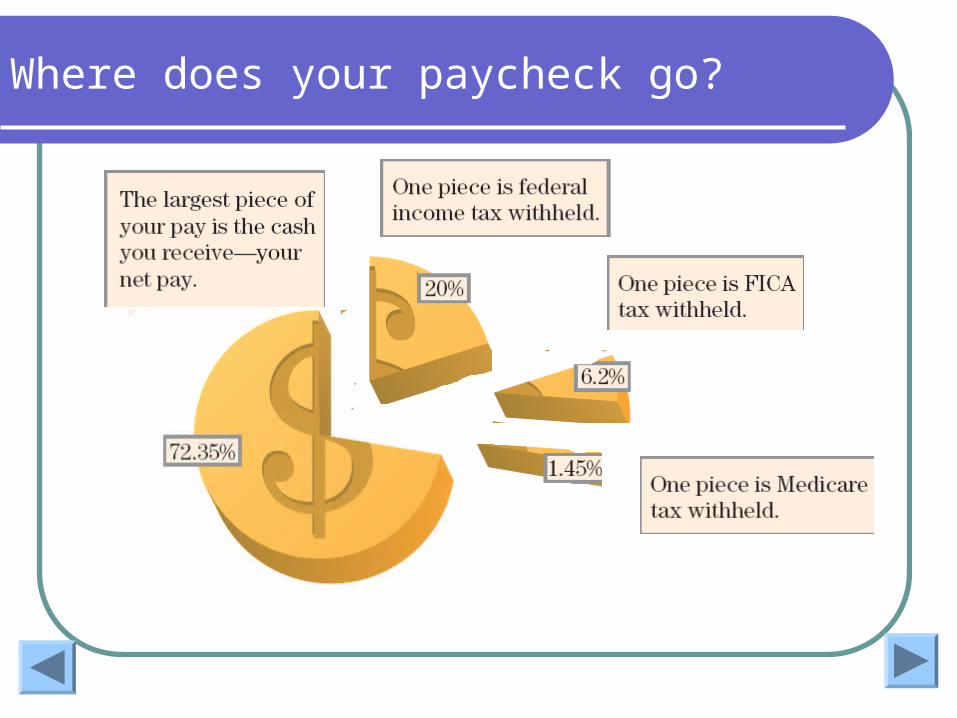

Gross Pay

Where does your paycheck go?

8 LESSON 12-2

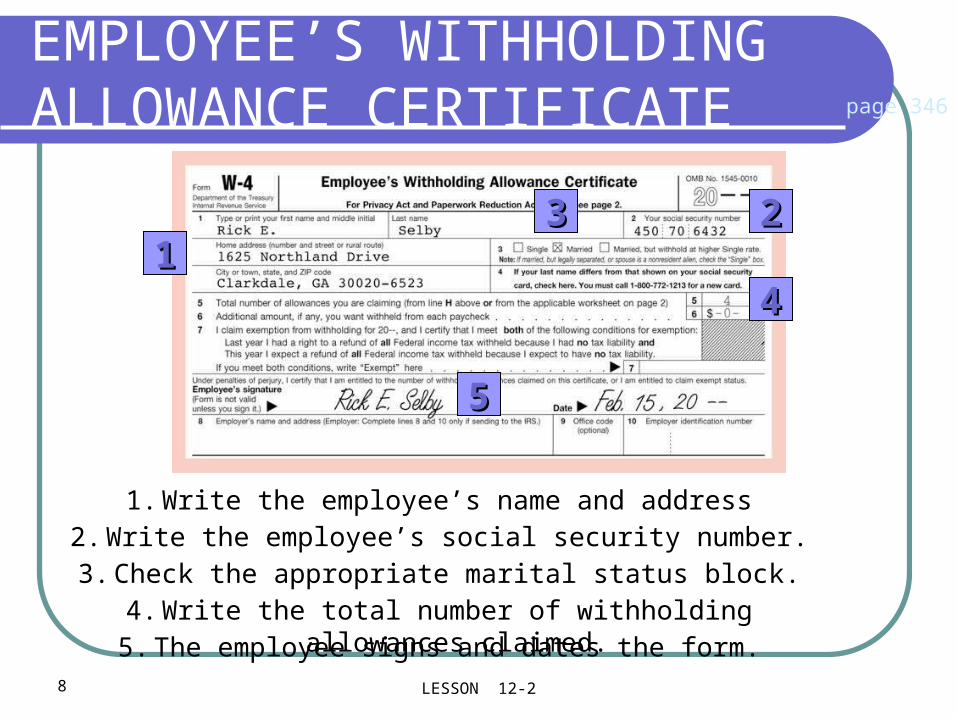

EMPLOYEE’S WITHHOLDING ALLOWANCE CERTIFICATE

112233

44

55

page 346

1. Write the employee’s name and address2. Write the employee’s social security number.3. Check the appropriate marital status block.

4. Write the total number of withholding allowances claimed.5. The employee signs and dates the form.

9 LESSON 12-2

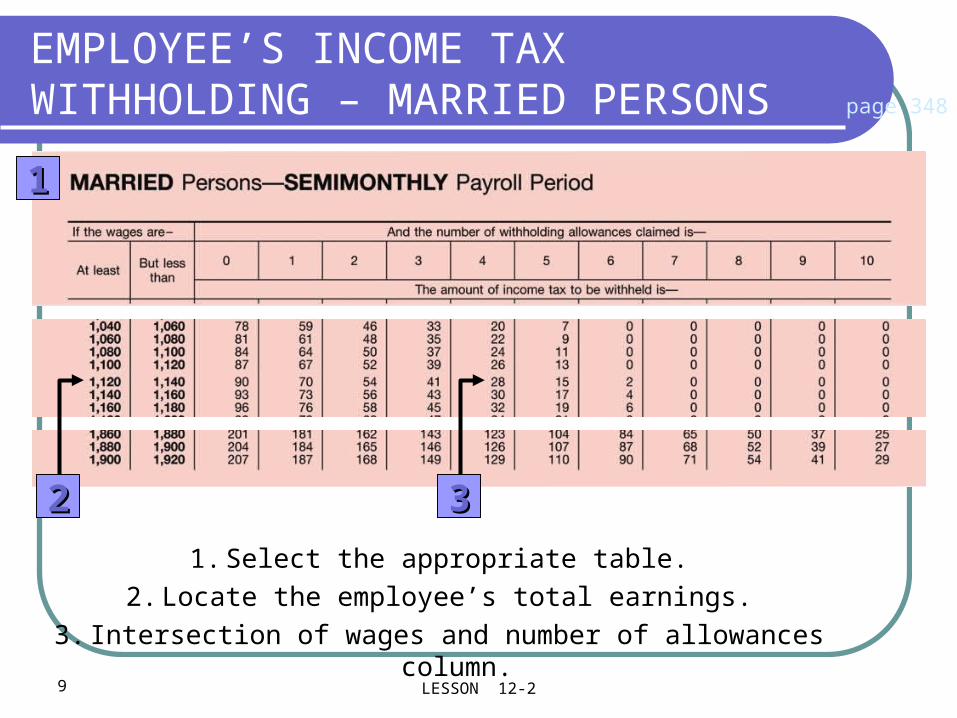

EMPLOYEE’S INCOME TAX WITHHOLDING – MARRIED PERSONS page 348

11

22 33

1. Select the appropriate table.

2. Locate the employee’s total earnings.

3. Intersection of wages and number of allowances column.

Payday!

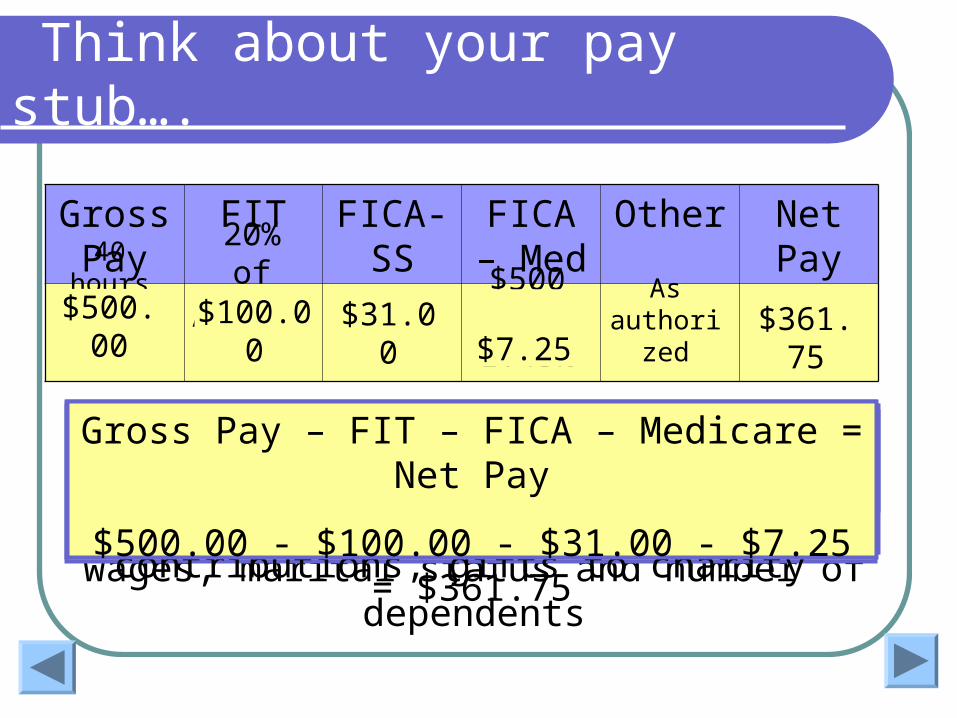

Think about your pay stub….

Gross Pay

FIT FICA-SS

FICA – Med

Other Net Pay

Gross Pay = # of hours worked at hourly rate

40 hours @ $12.50$500.00

FIT = Federal Income Tax Withholding The amount is determined based on the employee’s wages,

marital status and number of dependents

Assume 20%

20% of $500 =$100.00

FICA (SS) = Social Security Taxes withheld. This amount is 6.2% of gross wages

$500 * 6.2%$31.00

FICA (Med) = Medicare Taxes withheld. This amount is 1.45% of gross wages

$500 * 1.45%$7.25

As authorized

Other Employee-Authorized deductions to include: Health Insurance, Union Dues, 401k contributions,

gifts to charity

Gross Pay – FIT – FICA – Medicare = Net Pay

$500.00 - $100.00 - $31.00 - $7.25 = $361.75

$361.75

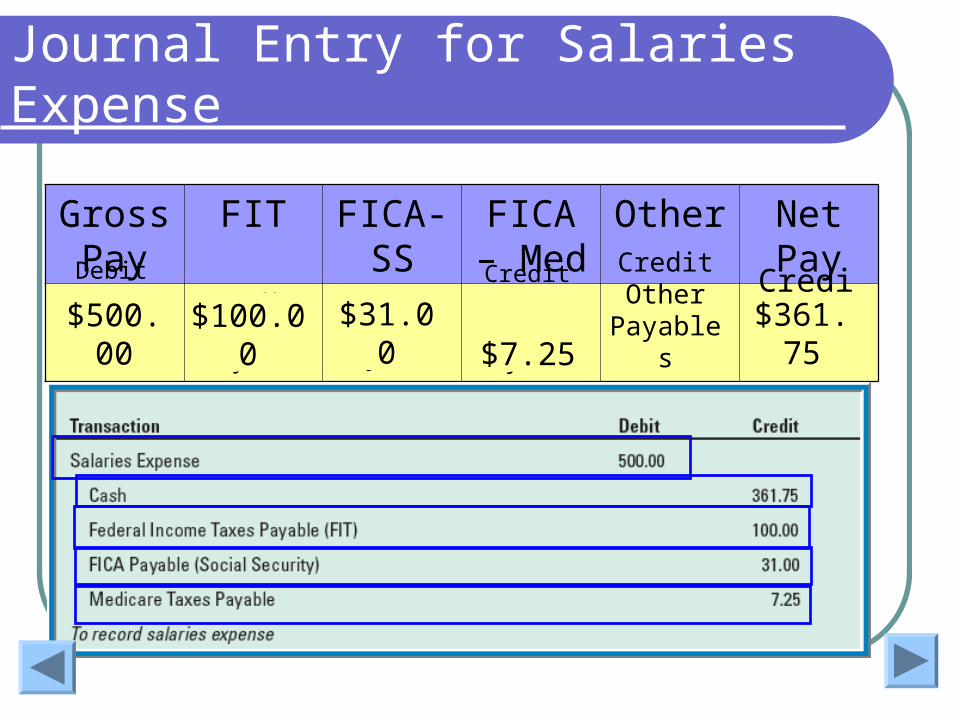

Journal Entry for Salaries Expense

Gross Pay

FIT FICA-SS

FICA – Med

Other Net Pay

Debit Salaries Expense$500.00

Credit FIT Payable$100.00

Credit FICA

Payable$31.00

Credit Medicare Payable$7.25

Credit Other

Payables

Credit Cash$361.75

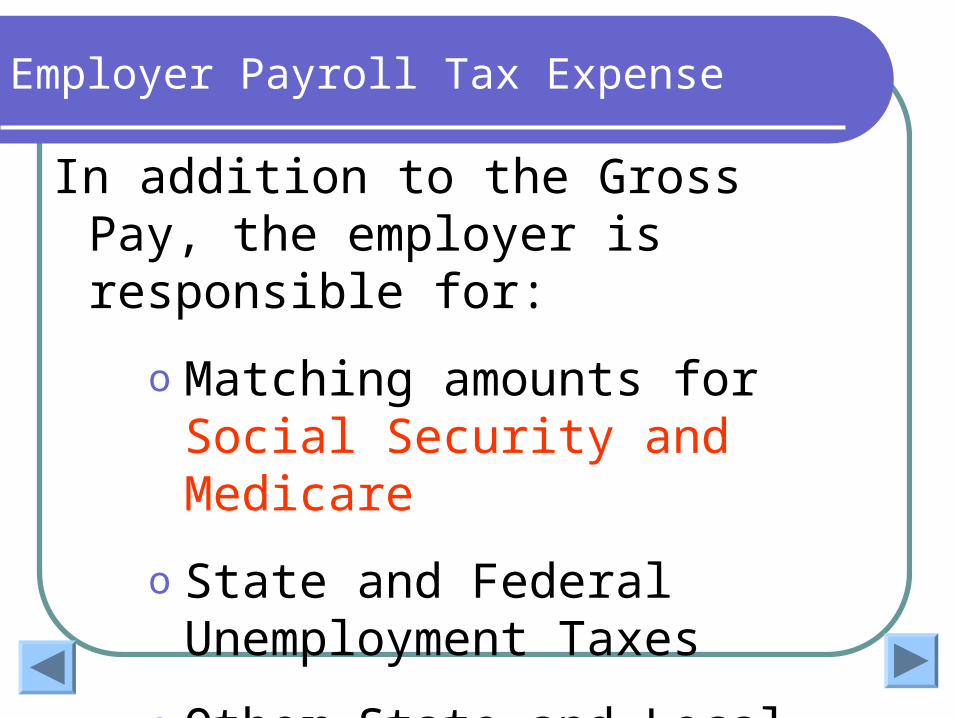

Employer Payroll Tax Expense

In addition to the Gross Pay, the employer is responsible for:

o Matching amounts for Social Security and Medicare

o State and Federal Unemployment Taxes

o Other State and Local taxes

$7.25

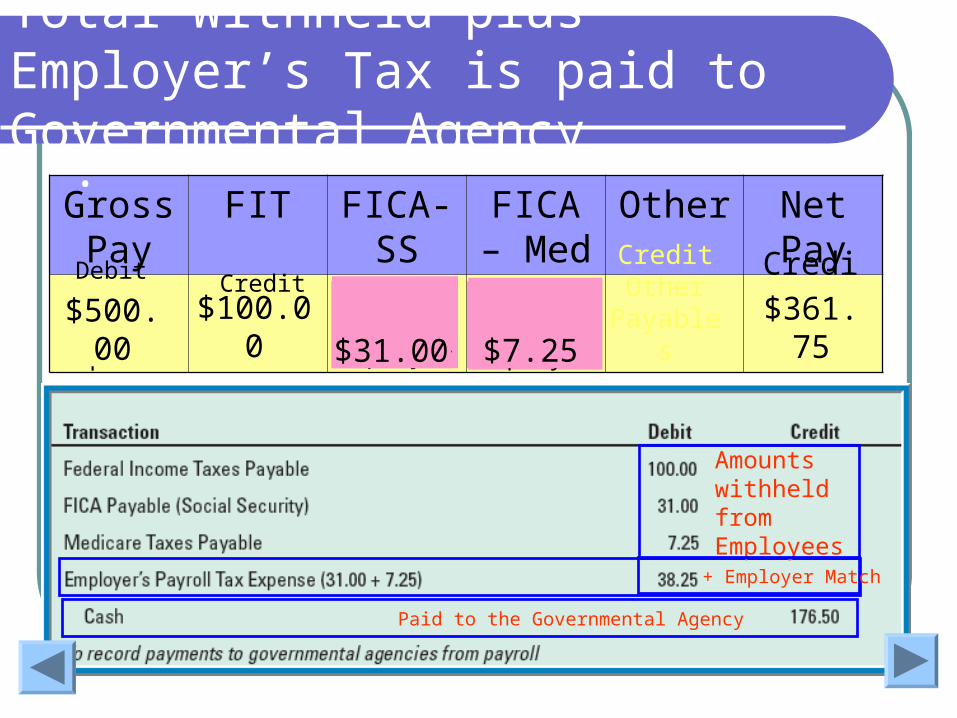

Employer’s Payroll Tax Expense

Gross Pay

FIT FICA-SS

FICA – Med

Other Net Pay

Debit Salaries Expense$500.00

Credit FIT Payable$100.00

Credit Other

Payables

Credit Cash$361.75$31.00

Amounts withheld from Employees

$7.25Matched by Employer$31.00

Matched by Employer$7.25

Paid to the Governmental Agency

Total Withheld .Total Withheld plus Employer’s Tax is paid to Governmental Agency

+ Employer Match

15 LESSON 12-3

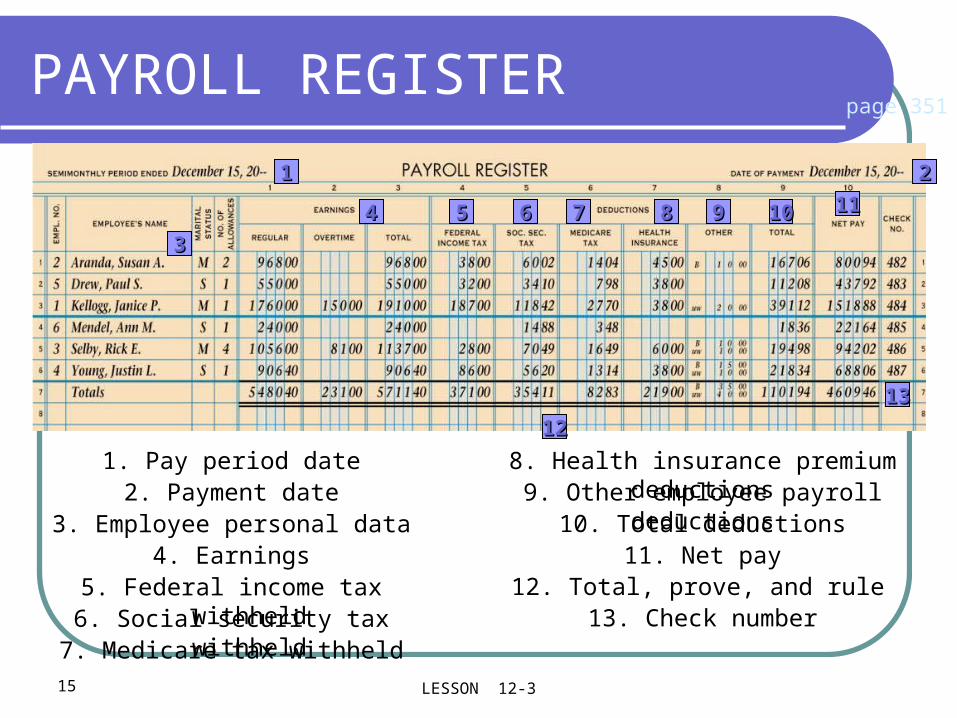

PAYROLL REGISTER

77 88 99 1010 1111

1212

page 351

11 22

33

44 55 66

1313

8. Health insurance premium deductions2. Payment date

3. Employee personal data9. Other employee payroll deductions

4. Earnings10. Total deductions

5. Federal income tax withheld11. Net pay

6. Social security tax withheld12. Total, prove, and rule

7. Medicare tax withheld13. Check number

1. Pay period date

16 LESSON 12-3

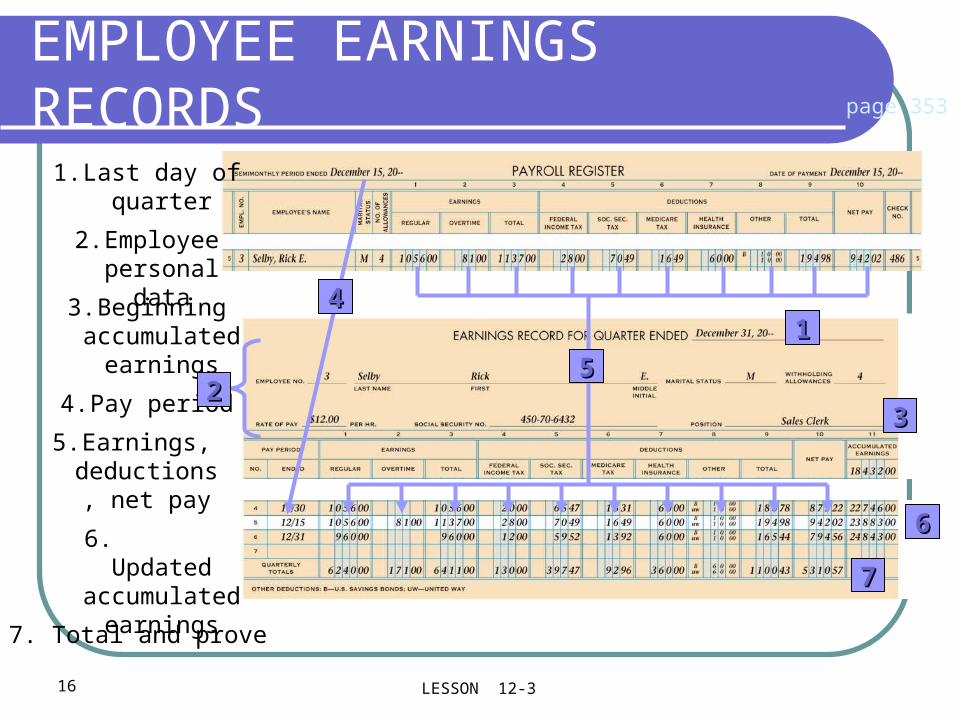

EMPLOYEE EARNINGS RECORDS page 353

7. Total and prove

5. Earnings, deductions,

net pay

2. Employee personal data

11

1. Last day of quarter

4. Pay period

3. Beginning accumulated

earnings

6. Updated accumulated

earnings

44

22

77

66

33

55

17 LESSON 12-4

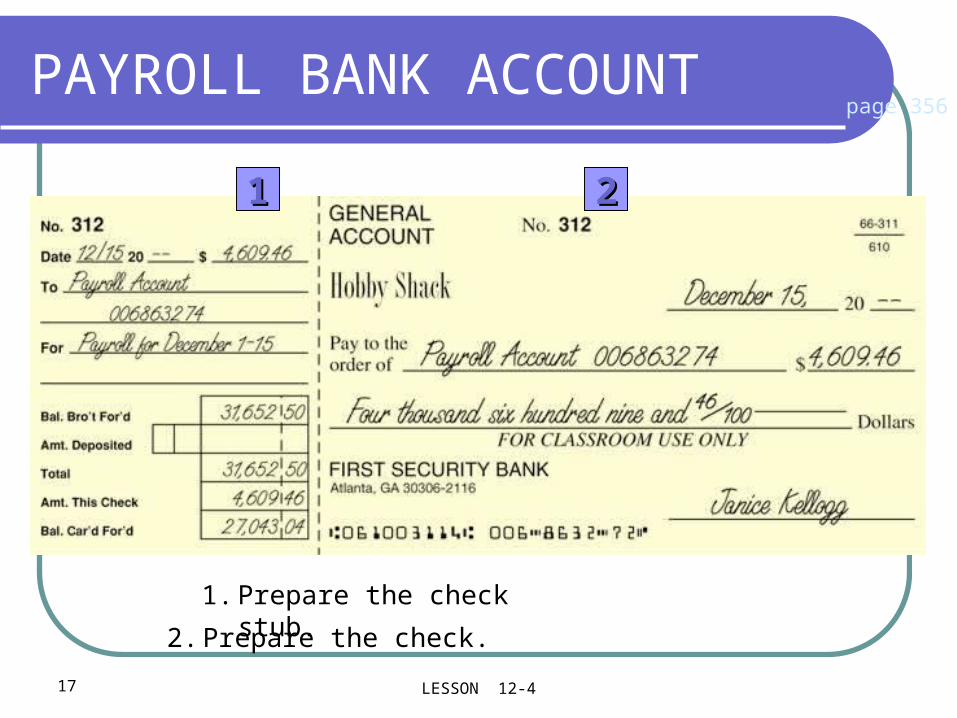

PAYROLL BANK ACCOUNT

1. Prepare the check stub.

page 356

2. Prepare the check.

11 22

18 LESSON 12-4

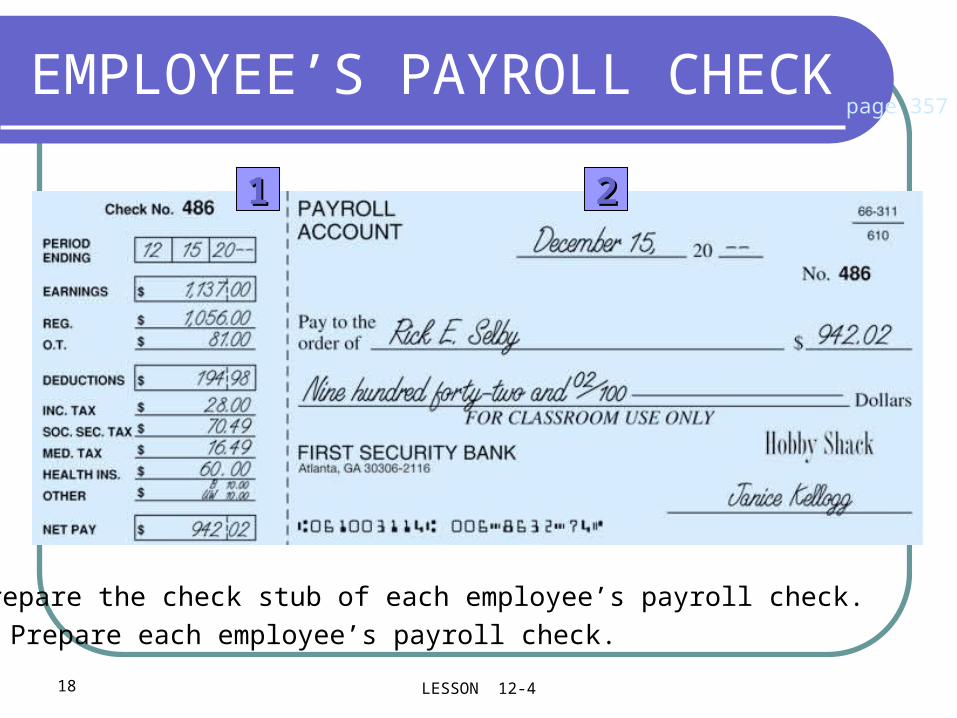

EMPLOYEE’S PAYROLL CHECK page 357

1. Prepare the check stub of each employee’s payroll check.

2. Prepare each employee’s payroll check.

2211

End – Chapter 12

Chapter 13

Payroll Accounting, Taxes and Reports

21 LESSON 13-1

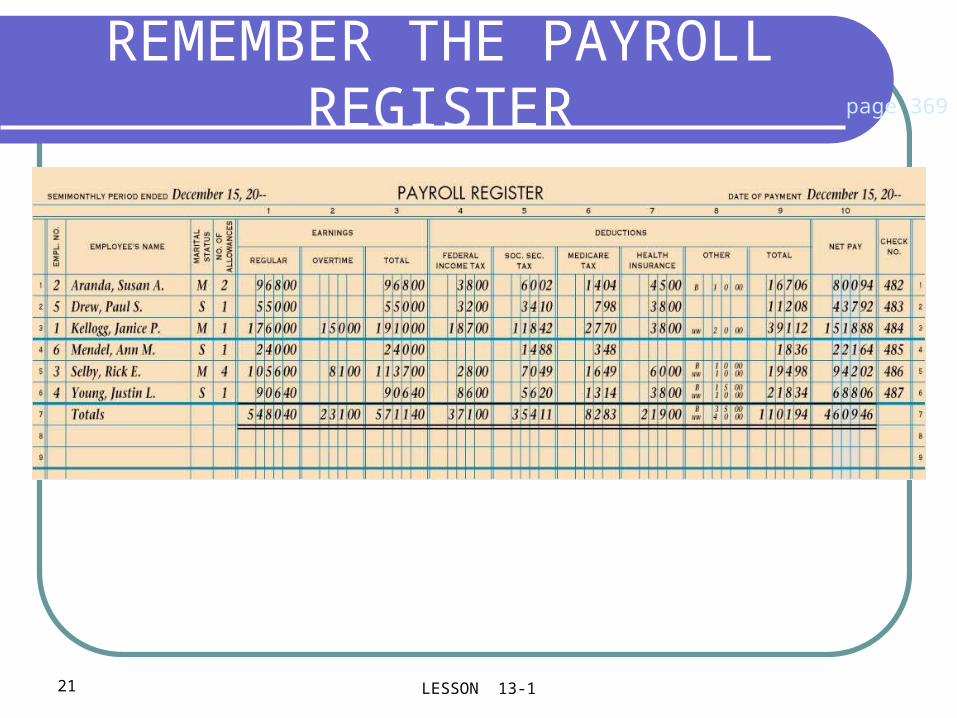

REMEMBER THE PAYROLL REGISTER page 369

22 LESSON 13-1

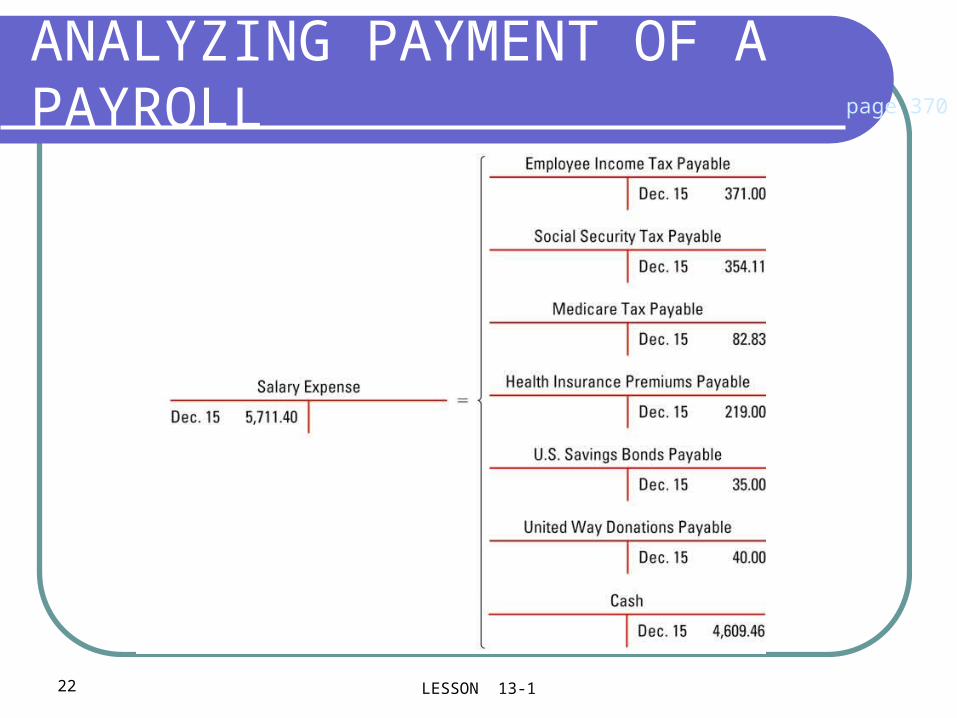

ANALYZING PAYMENT OF A PAYROLL page 370

23 LESSON 13-1

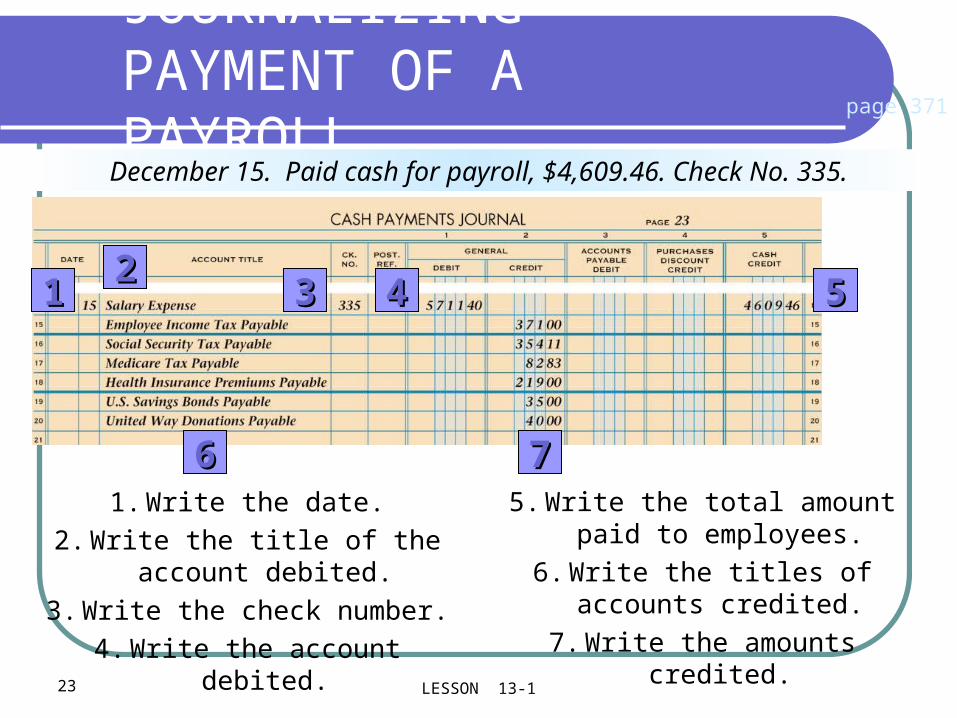

6. Write the titles of accounts credited.

JOURNALIZING PAYMENT OF A PAYROLL

1122

33 44 55

66

page 371

December 15. Paid cash for payroll, $4,609.46. Check No. 335.

771. Write the date.

2. Write the title of the account debited.

3. Write the check number.

4. Write the account debited. 7. Write the amounts credited.

5. Write the total amount paid to employees.

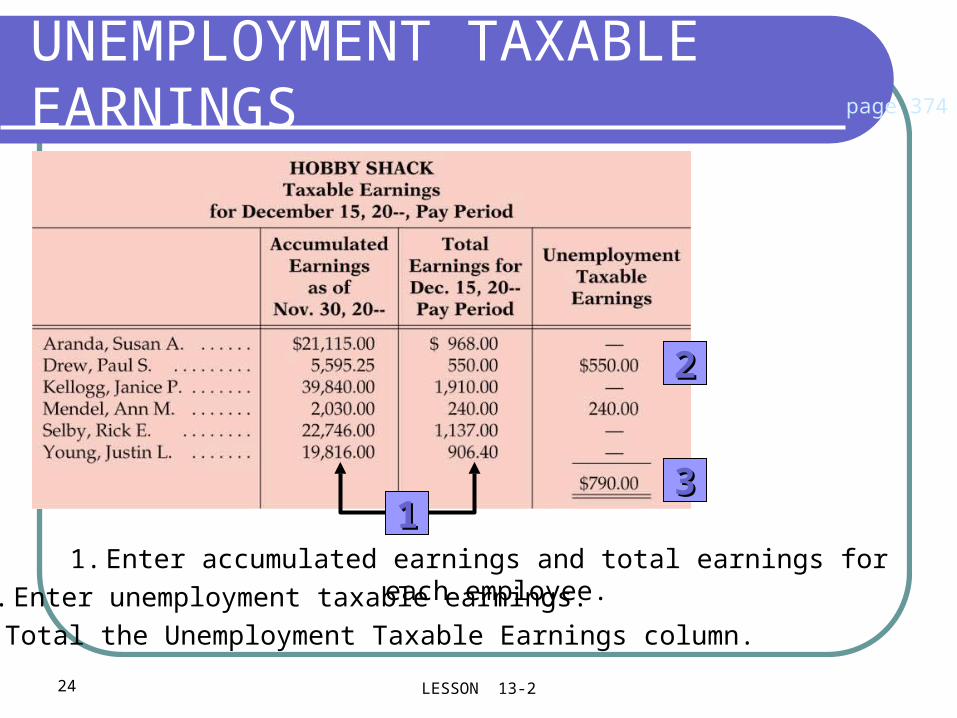

24 LESSON 13-2

UNEMPLOYMENT TAXABLE EARNINGS

22

33

page 374

111. Enter accumulated earnings and total earnings for each employee.

2. Enter unemployment taxable earnings.

3. Total the Unemployment Taxable Earnings column.

25

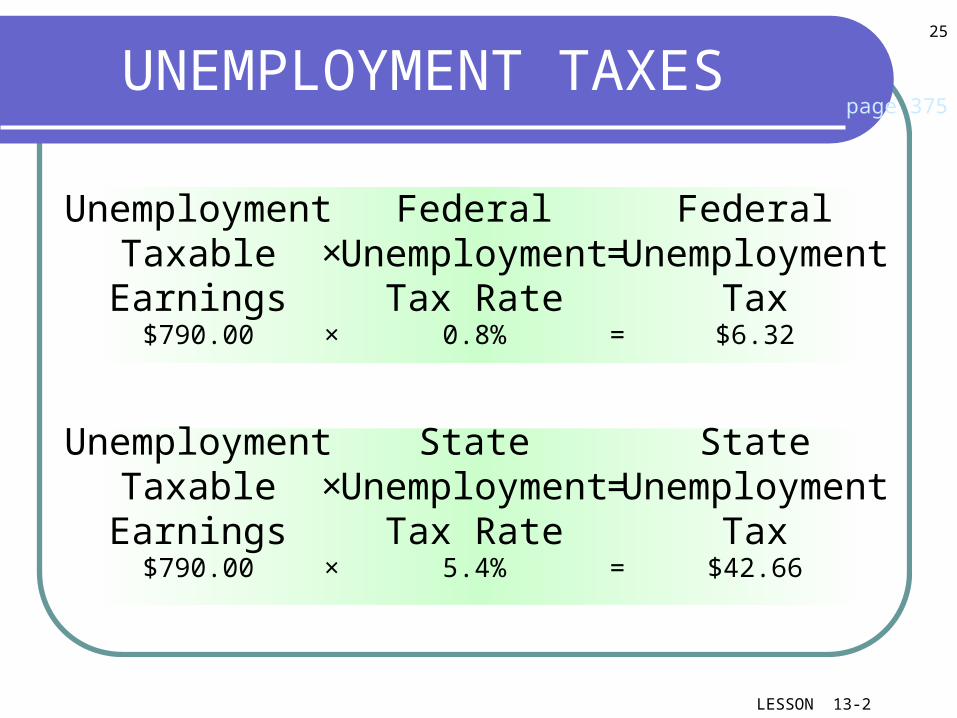

LESSON 13-2

FederalUnemployment

Tax=

FederalUnemployment

Tax Rate×

UnemploymentTaxableEarnings

StateUnemployment

Tax=

StateUnemployment

Tax Rate×

UnemploymentTaxableEarnings

UNEMPLOYMENT TAXESpage 375

$6.32=0.8%×$790.00

$42.66=5.4%×$790.00

26 LESSON 13-2

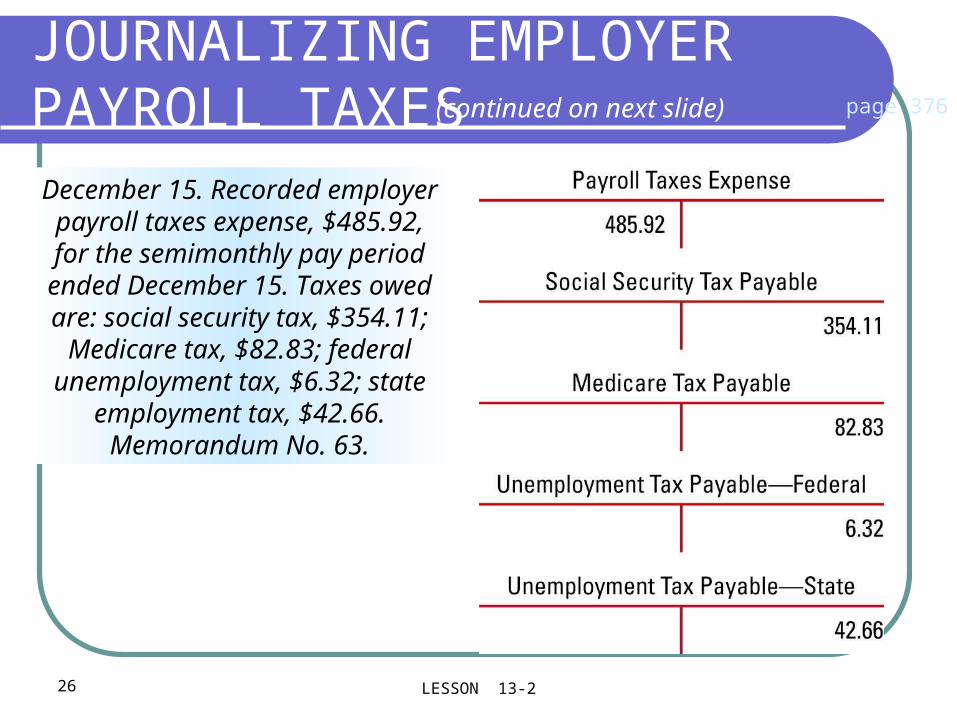

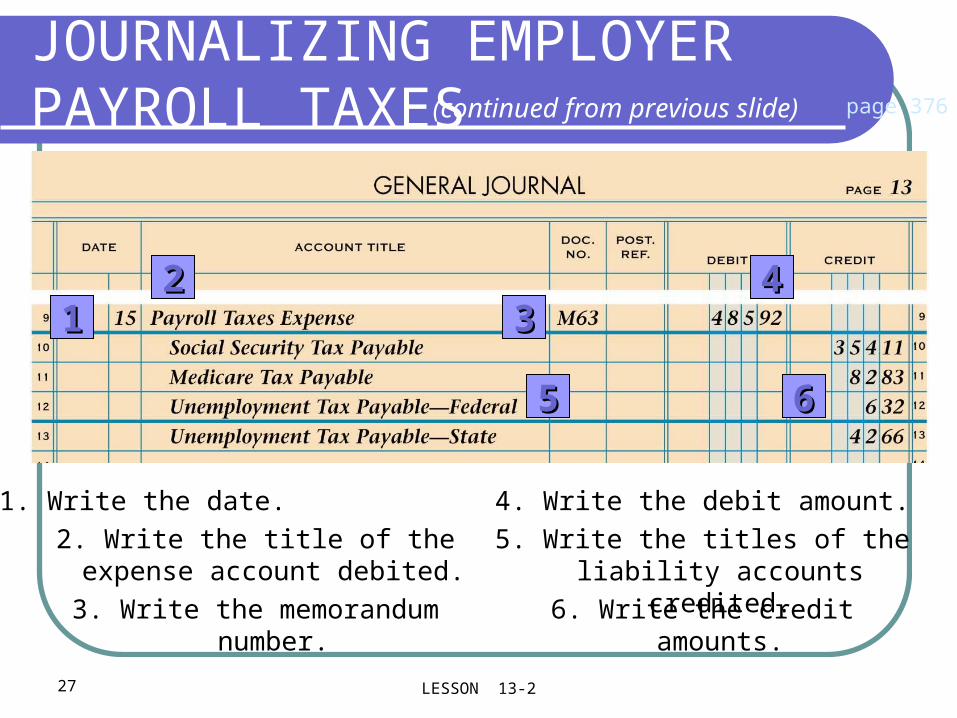

JOURNALIZING EMPLOYER PAYROLL TAXES page 376

December 15. Recorded employer payroll taxes expense, $485.92, for the semimonthly pay

period ended December 15. Taxes owed are: social security

tax, $354.11; Medicare tax, $82.83; federal unemployment

tax, $6.32; state employment tax, $42.66. Memorandum No. 63.

(continued on next slide)

27 LESSON 13-2

JOURNALIZING EMPLOYER PAYROLL TAXES

1122

33

55

44

66

page 376

4. Write the debit amount.1. Write the date.

5. Write the titles of the liability accounts credited.

2. Write the title of the expense account debited.

6. Write the credit amounts.3. Write the memorandum number.

(continued from previous slide)

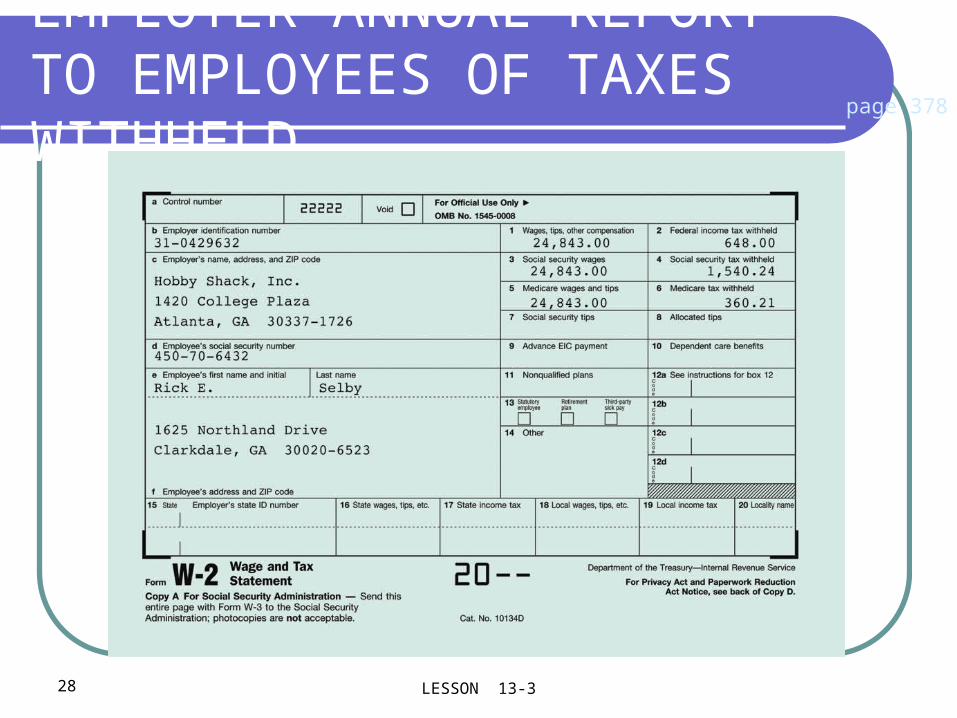

28 LESSON 13-3

EMPLOYER ANNUAL REPORT TO EMPLOYEES OF TAXES WITHHELD

page 378

29 LESSON 13-3

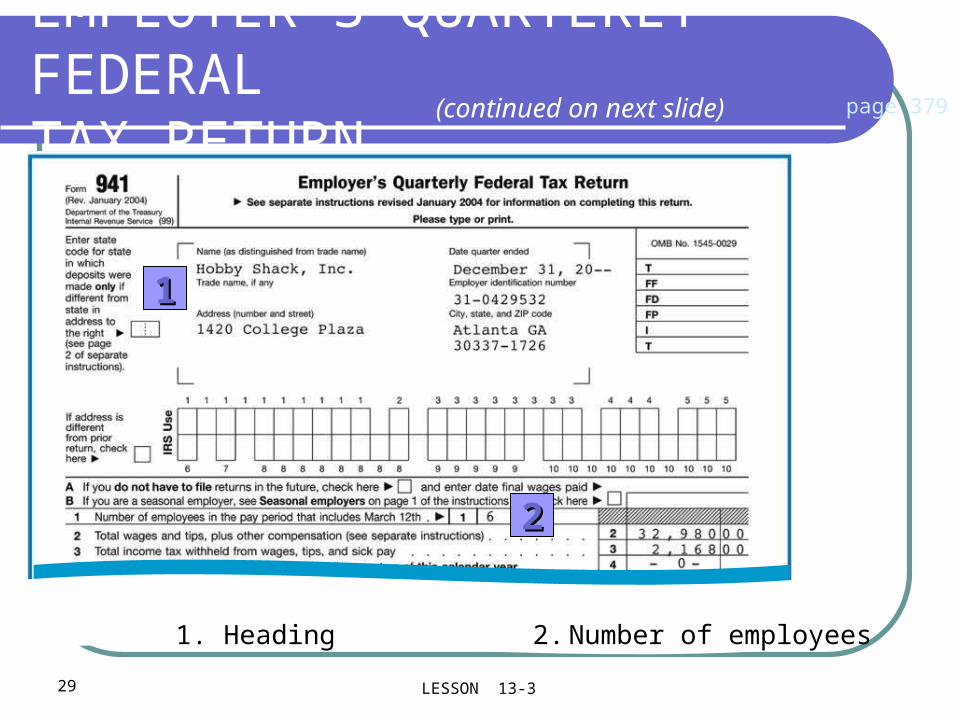

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN

page 379(continued on next slide)

11

22

1. Heading 2. Number of employees

30 LESSON 13-3

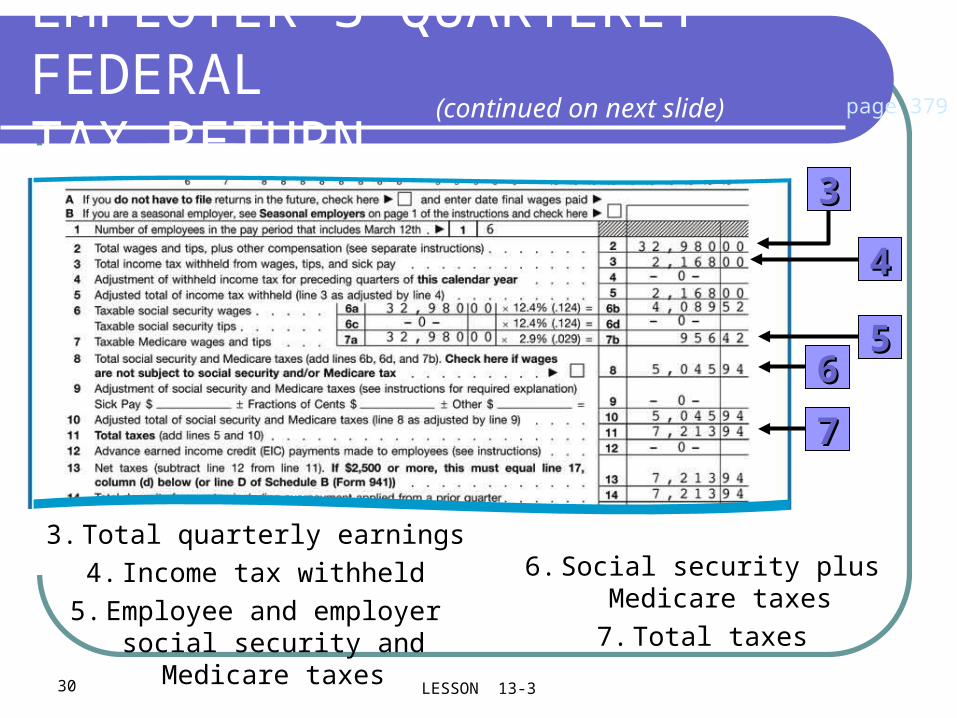

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN

page 379(continued on next slide)

3. Total quarterly earnings

4. Income tax withheld

5. Employee and employer social security and Medicare taxes 7. Total taxes

6. Social security plus Medicare taxes

44

55

33

66

77

31 LESSON 13-3

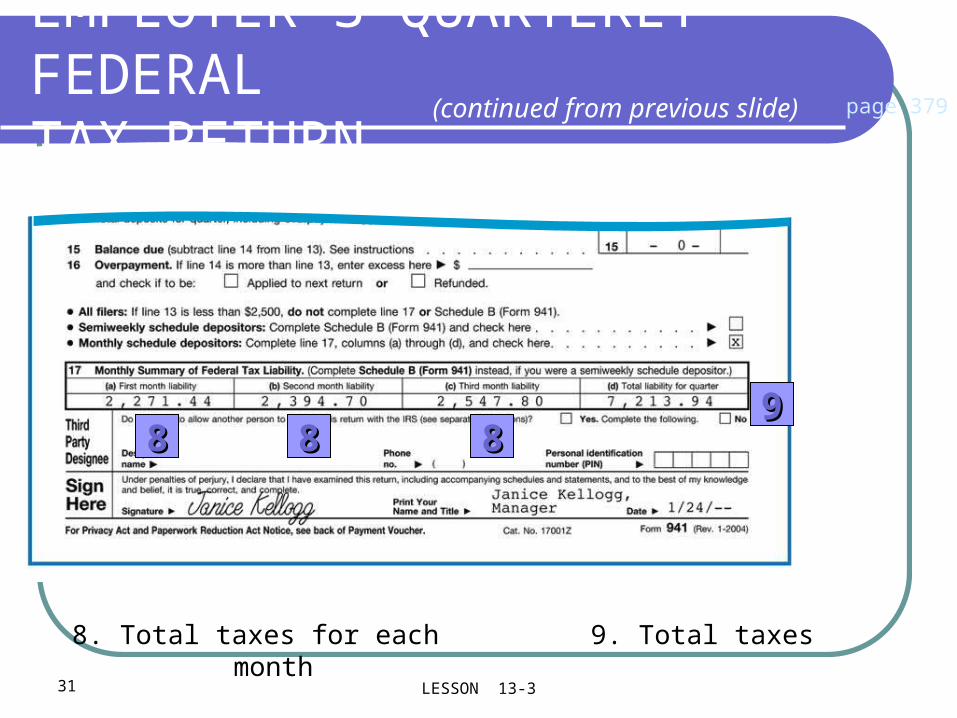

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN

page 379(continued from previous slide)

88 88 8899

8. Total taxes for each month 9. Total taxes

32 LESSON 13-3

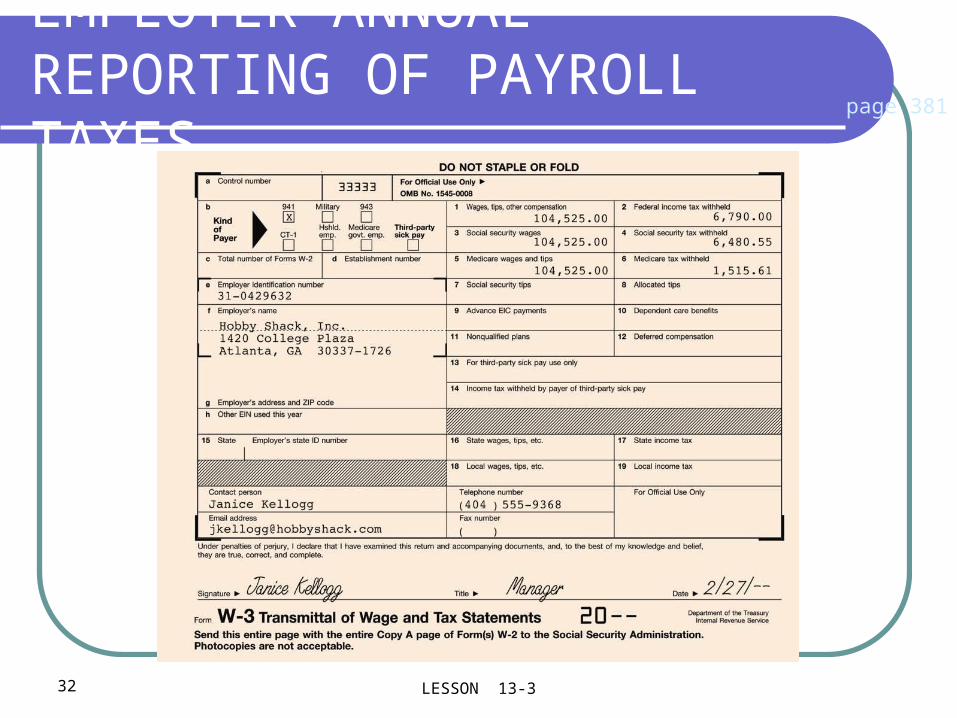

EMPLOYER ANNUAL REPORTING OF PAYROLL TAXES

page 381

33 LESSON 13-4

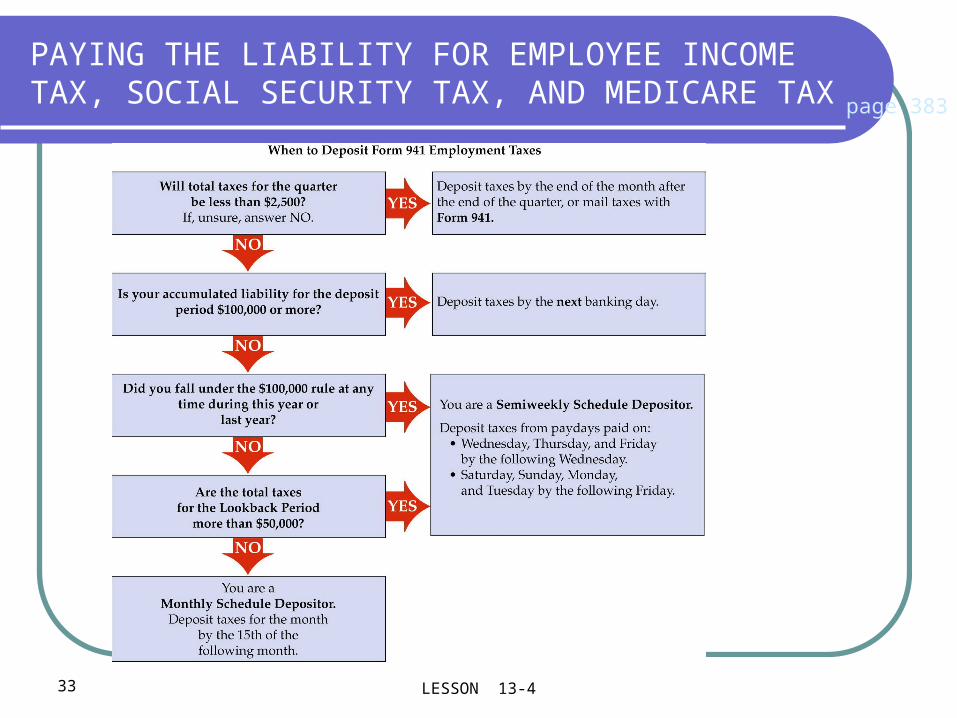

PAYING THE LIABILITY FOR EMPLOYEE INCOME TAX, SOCIAL SECURITY TAX, AND MEDICARE TAX page 383

34 LESSON 13-4

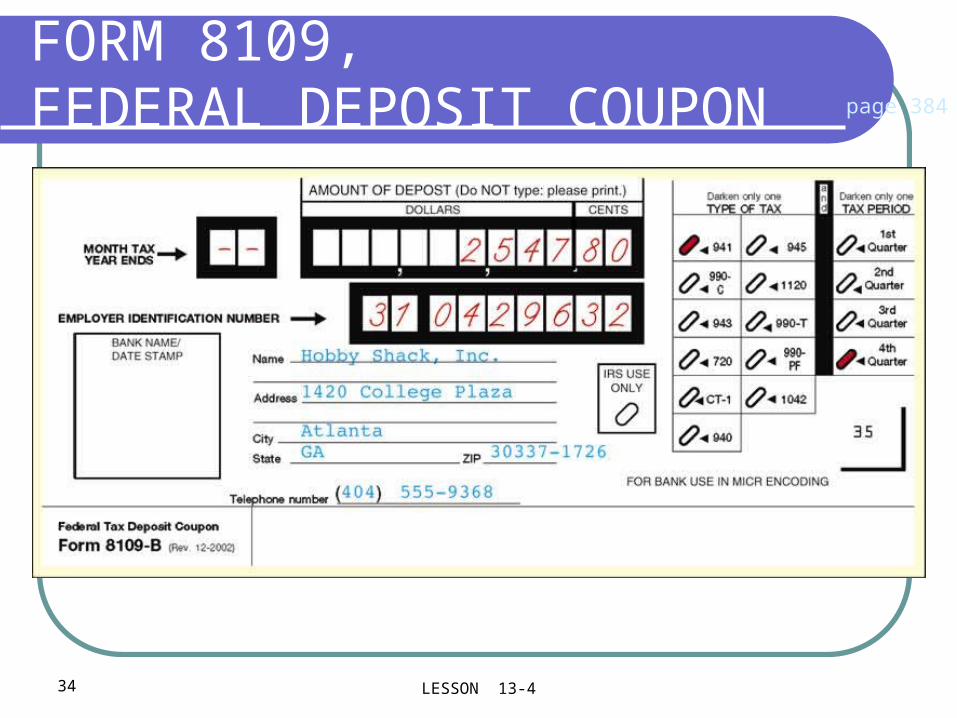

FORM 8109, FEDERAL DEPOSIT COUPON page 384

35 LESSON 13-4

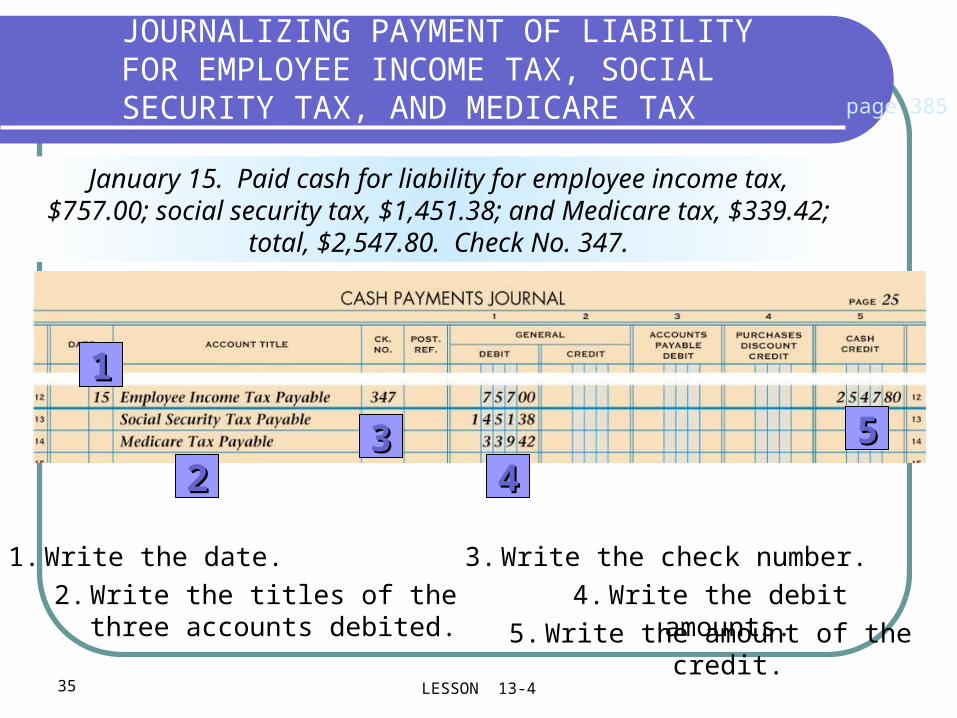

JOURNALIZING PAYMENT OF LIABILITY FOR EMPLOYEE INCOME TAX, SOCIAL SECURITY TAX, AND MEDICARE TAX

11

2233

4455

page 385

January 15. Paid cash for liability for employee income tax, $757.00; social security tax, $1,451.38; and Medicare tax, $339.42;

total, $2,547.80. Check No. 347.

1. Write the date.

2. Write the titles of the three accounts debited.

3. Write the check number.

4. Write the debit amounts.

5. Write the amount of the credit.

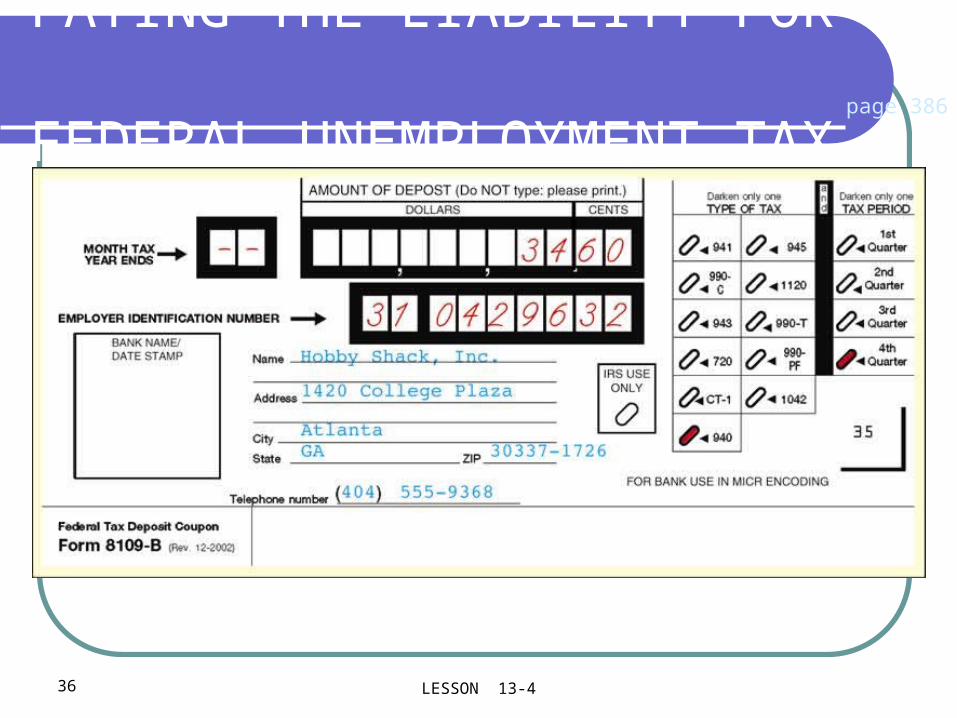

36 LESSON 13-4

PAYING THE LIABILITY FOR FEDERAL UNEMPLOYMENT TAX

page 386

37 LESSON 13-4

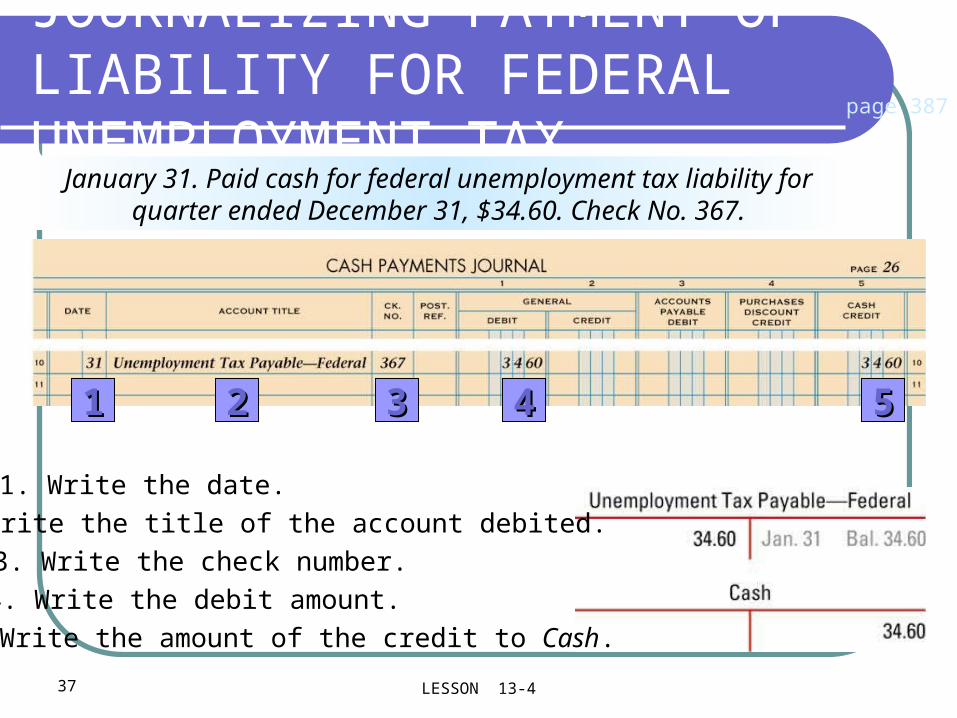

JOURNALIZING PAYMENT OF LIABILITY FOR FEDERAL UNEMPLOYMENT TAX

11 22 33 44 55

page 387

January 31. Paid cash for federal unemployment tax liability for quarter ended December 31, $34.60. Check No. 367.

1. Write the date.

5. Write the amount of the credit to Cash.

4. Write the debit amount.

3. Write the check number.

2. Write the title of the account debited.

38 LESSON 13-4

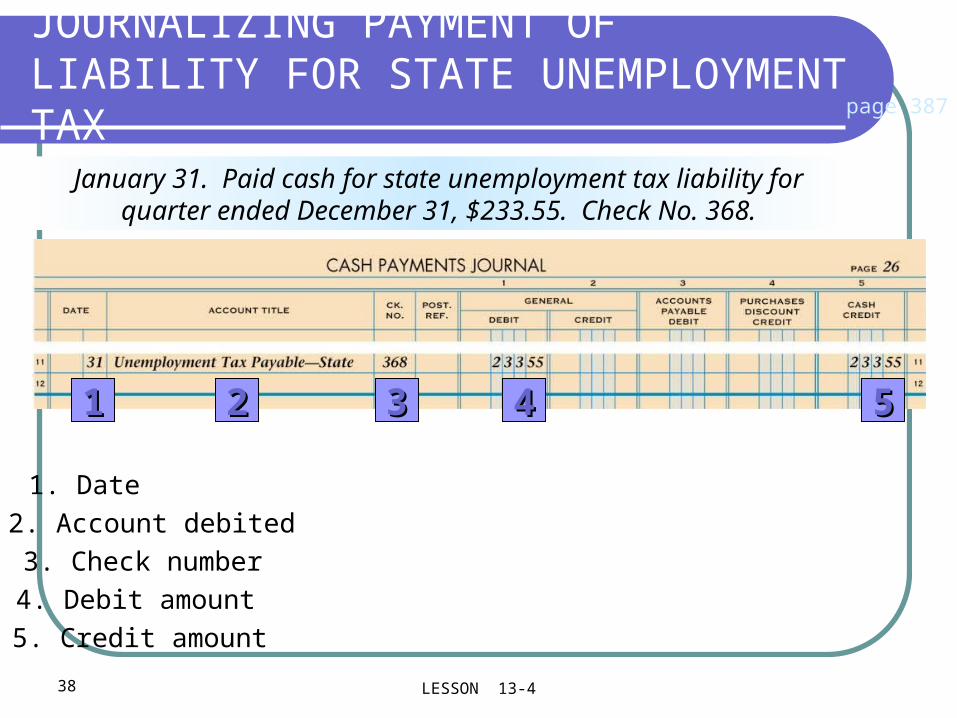

JOURNALIZING PAYMENT OF LIABILITY FOR STATE UNEMPLOYMENT TAX page 387

January 31. Paid cash for state unemployment tax liability for quarter ended December 31, $233.55. Check No. 368.

1. Date

5. Credit amount

4. Debit amount

3. Check number

2. Account debited

11 22 33 44 55