Embed Size (px)

Citation preview

Chapter 12 Auditing the

Human Resource Management

Process

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Overview of the Human Resource

Management Process

The human resource process starts with the

establishment of sound policies for hiring, training,

evaluating, counseling, promoting, compensating,

and taking remedial actions for employees.

The main concern of the auditor involves payroll

transactions once an employee has been hired.

LO# 1

12-2

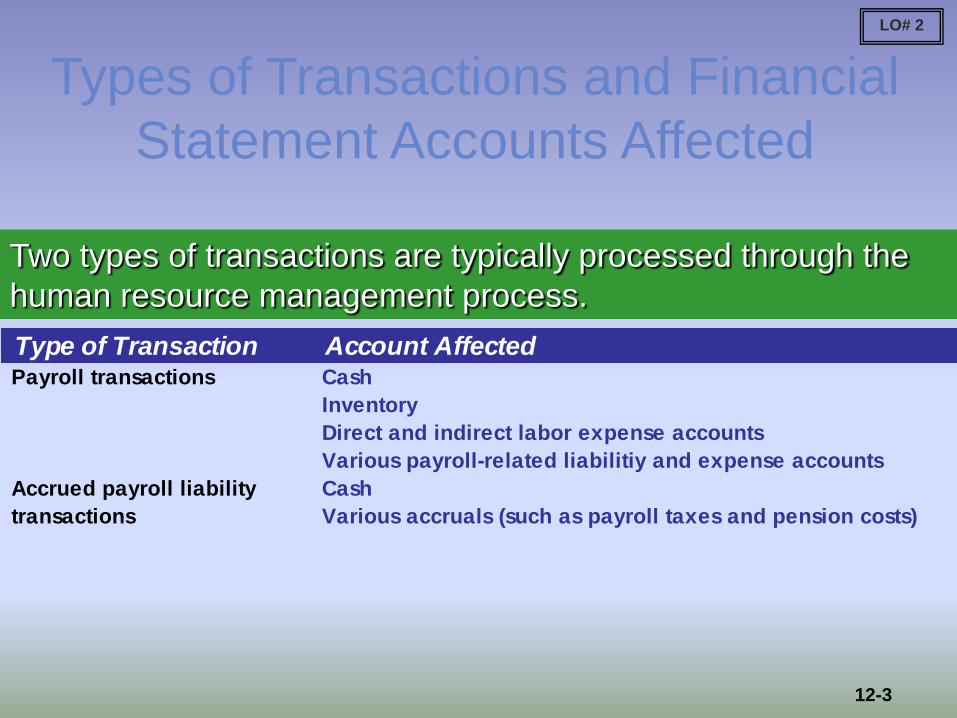

Type of Transaction Account AffectedPayroll transactions Cash

Inventory

Direct and indirect labor expense accounts

Various payroll-related liabilitiy and expense accounts

Accrued payroll liability Cash

transactions Various accruals (such as payroll taxes and pension costs)

LO# 2

Types of Transactions and Financial

Statement Accounts Affected

12-3

Two types of transactions are typically processed through the

human resource management process.

Types of Documents and Records

▪Personnel records, including wage-rate or salary authorizations.

▪W-4 and other deduction authorization forms.

▪Time card/time sheet.

▪Payroll check/direct deposit records.

▪Payroll register.

▪Payroll master file.

▪Payroll master file changes report.

▪Periodic payroll reports.

▪Various tax reports and forms.

LO# 3

12-4

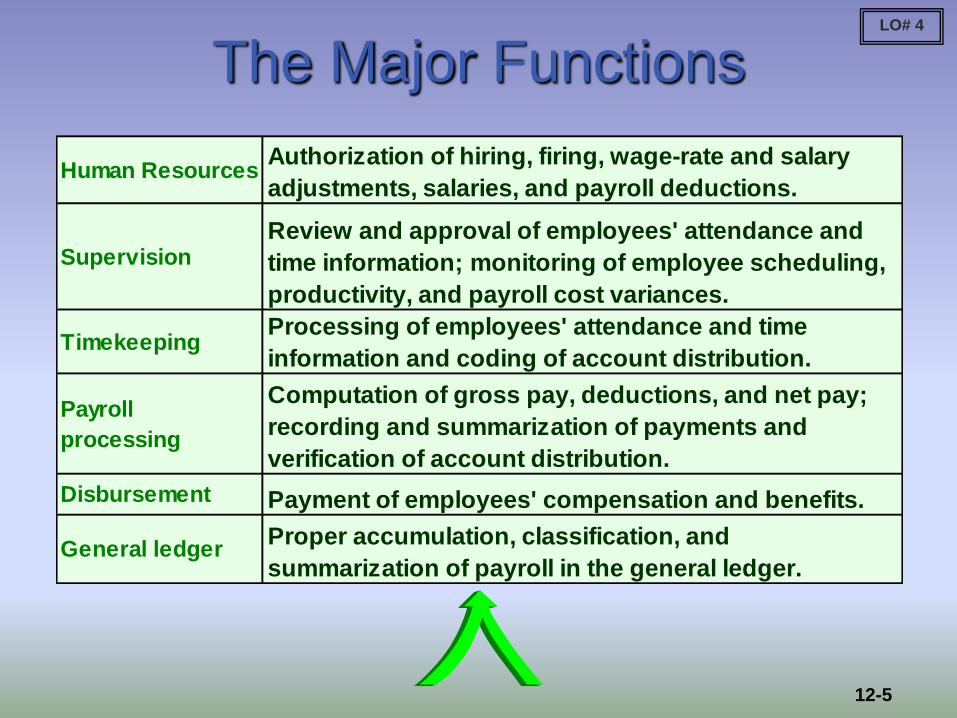

The Major Functions

Human ResourcesAuthorization of hiring, firing, wage-rate and salary

adjustments, salaries, and payroll deductions.

SupervisionReview and approval of employees' attendance and

time information; monitoring of employee scheduling,

productivity, and payroll cost variances.

TimekeepingProcessing of employees' attendance and time

information and coding of account distribution.

Payroll

processing

Computation of gross pay, deductions, and net pay;

recording and summarization of payments and

verification of account distribution.

Disbursement Payment of employees' compensation and benefits.

General ledgerProper accumulation, classification, and

summarization of payroll in the general ledger.

LO# 4

12-5

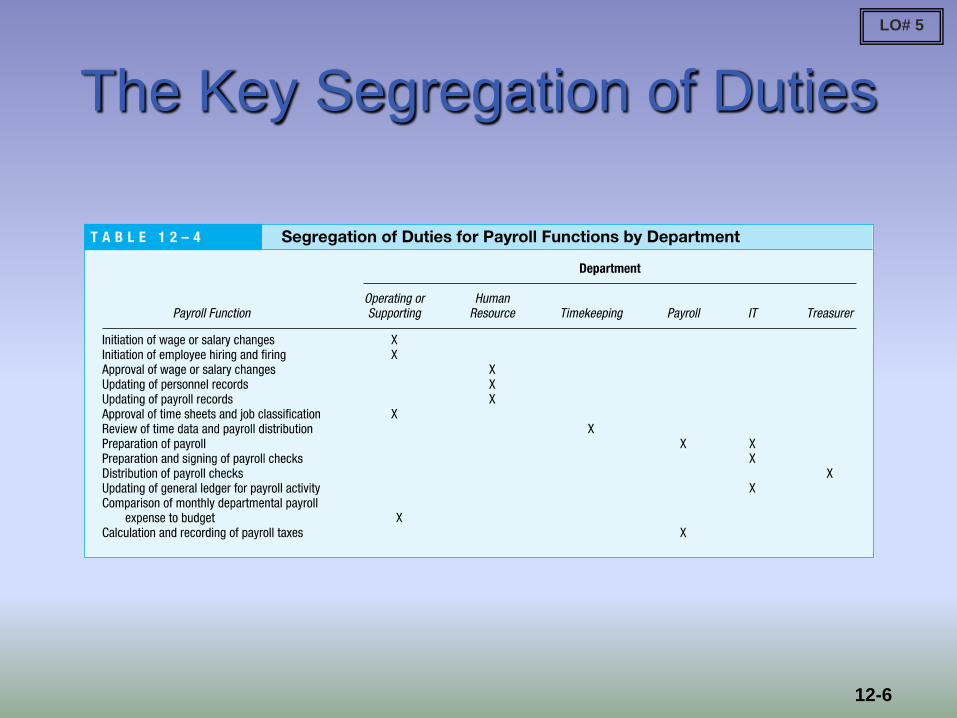

The Key Segregation of Duties

LO# 5

12-6

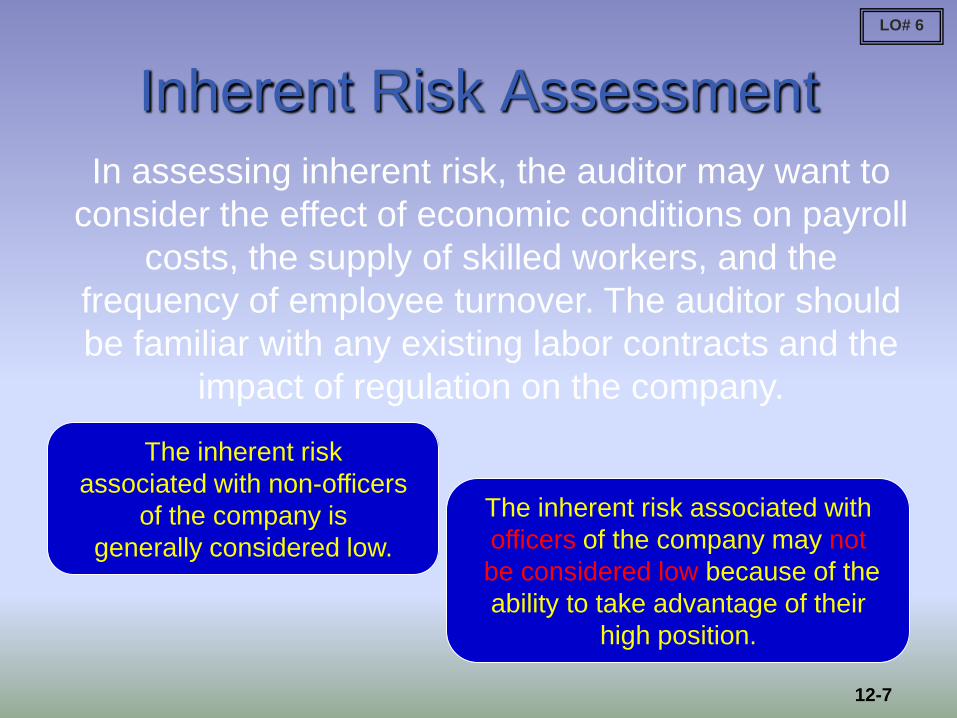

Inherent Risk Assessment

In assessing inherent risk, the auditor may want to

consider the effect of economic conditions on payroll

costs, the supply of skilled workers, and the

frequency of employee turnover. The auditor should

be familiar with any existing labor contracts and the

impact of regulation on the company.

The inherent risk

associated with non-officers

of the company is

generally considered low.

The inherent risk associated with

officers of the company may not

be considered low because of the

ability to take advantage of their

high position.

LO# 6

12-7

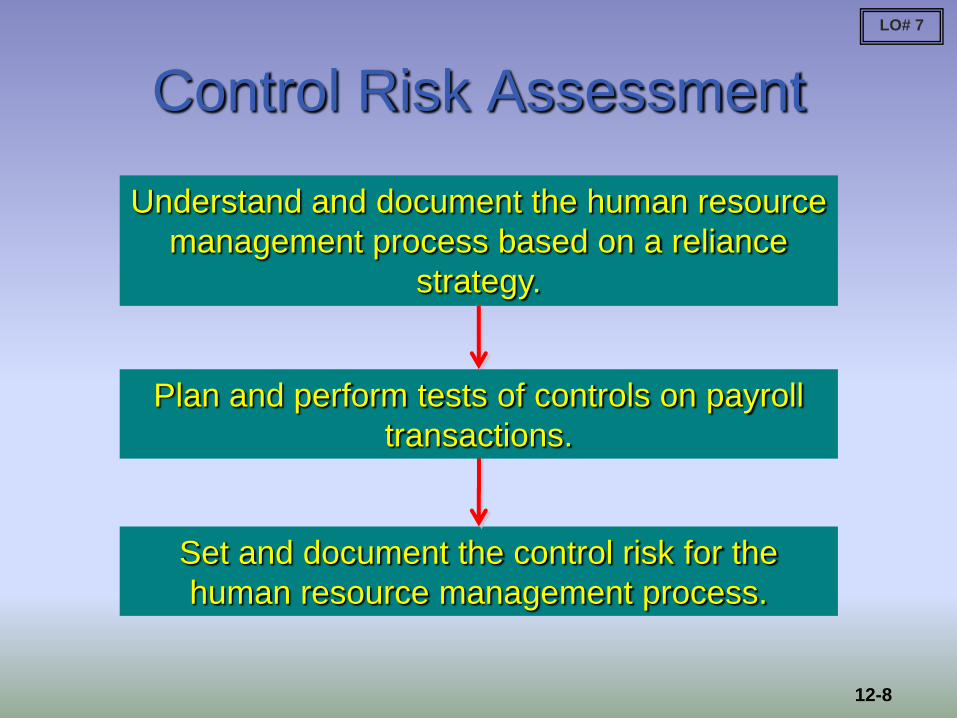

Control Risk Assessment

Understand and document the human resource

management process based on a reliance

strategy.

Set and document the control risk for the

human resource management process.

Plan and perform tests of controls on payroll

transactions.

LO# 7

12-8

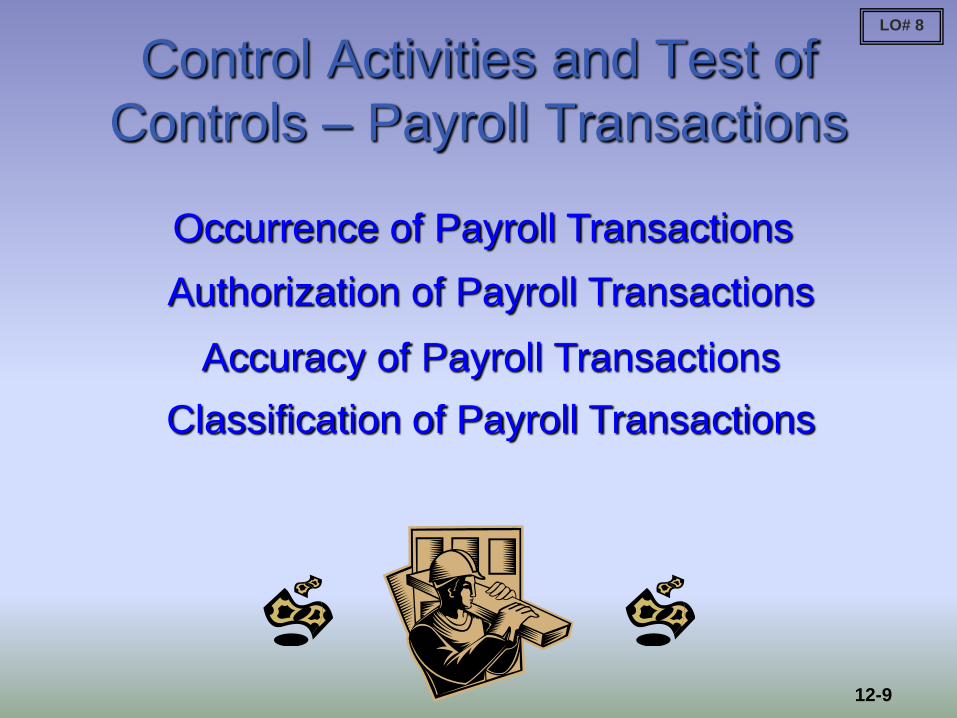

Control Activities and Test of

Controls – Payroll Transactions

Occurrence of Payroll Transactions

LO# 8

12-9

Authorization of Payroll Transactions

Accuracy of Payroll Transactions

Classification of Payroll Transactions

Relating the Assessed Level of Control

Risk to Substantive Procedures

If the results of the tests of controls for the payroll

system support the planned level of control risk, the

auditor conducts substantive procedures of payroll-

related accounts at the assessed level. If the tests

do not support the level of control risk, the nature

and extent of substantive testing will be increased.

LO# 9

12-10

Auditing Payroll-Related

Accounts

Substantive Analytical Procedures

Payroll Expense Accounts:

Compare current-year with prior years' payroll expense accounts

Compare current and prior years' payroll costs as percent of sales and industry data

Compare labor utilization rates and statistics with industry data

Compare budgeted payroll expenses with actual payroll expenses

Estimate sales commissions with formulas and recorded sales

Payroll-Related Accrual Accounts:

Compare current and prior years' balances in payroll related accounts

Test reasonableness of accrual balances

LO# 10

12-11

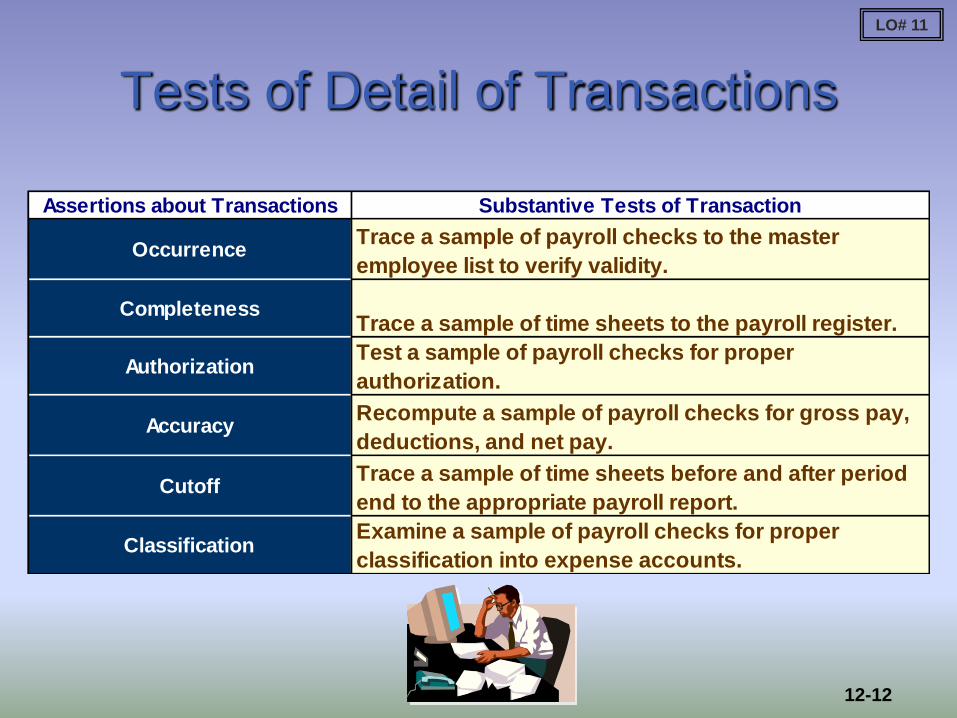

Tests of Detail of Transactions

Assertions about Transactions Substantive Tests of Transaction

OccurrenceTrace a sample of payroll checks to the master

employee list to verify validity.

CompletenessTrace a sample of time sheets to the payroll register.

AuthorizationTest a sample of payroll checks for proper

authorization.

AccuracyRecompute a sample of payroll checks for gross pay,

deductions, and net pay.

CutoffTrace a sample of time sheets before and after period

end to the appropriate payroll report.

ClassificationExamine a sample of payroll checks for proper

classification into expense accounts.

LO# 11

12-12

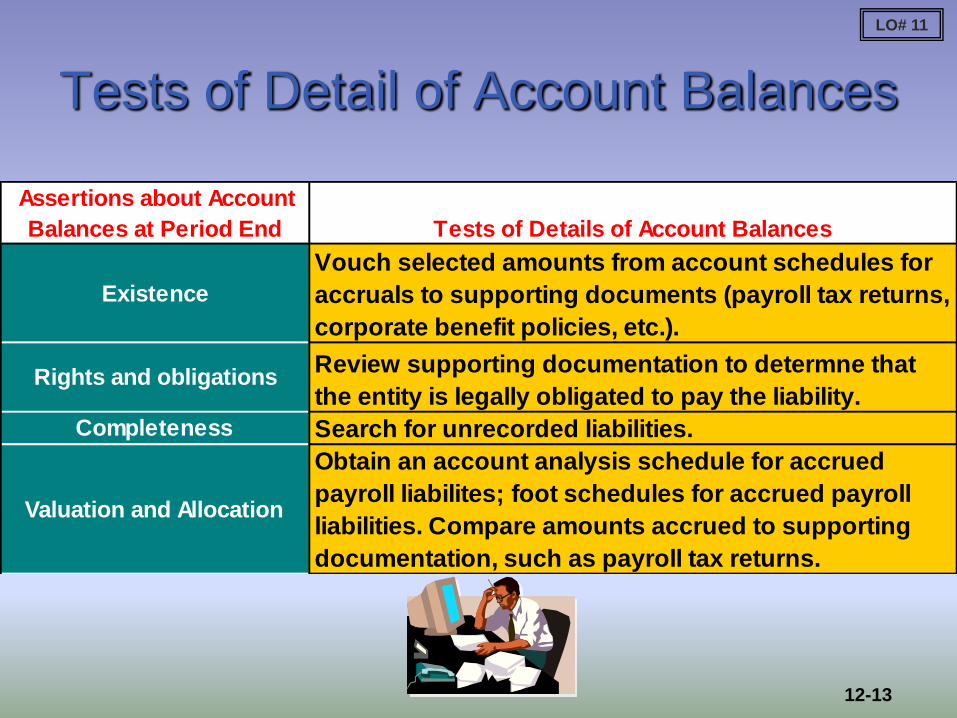

Tests of Detail of Account Balances

Assertions about Account

Balances at Period End Tests of Details of Account Balances

Existence

Vouch selected amounts from account schedules for

accruals to supporting documents (payroll tax returns,

corporate benefit policies, etc.).

Rights and obligationsReview supporting documentation to determne that

the entity is legally obligated to pay the liability.

Completeness Search for unrecorded liabilities.

Valuation and Allocation

Obtain an account analysis schedule for accrued

payroll liabilites; foot schedules for accrued payroll

liabilities. Compare amounts accrued to supporting

documentation, such as payroll tax returns.

LO# 11

12-13

Tests of Detail of Disclosures

Assertions about

Presentation and

Disclosure Tests of Details of Disclosures

Occurrence, and rights and

obligations

Inquire about accruals to ensure that they are properly

disclosed.

Completeness

Complete financial reporting checklist to ensure that

all financial statement disclosures related to payroll

expense have been made.

Classification and

understandability

Review accrued payroll liabilities for proper short-

term/long-term classification.

Accuracy and valuation

Review benefit contracts for proper disclosure of

pension and postretirement benefits. Read footnotes

and other information to ensure that the information is

accurate and properly presented at the appropriate

amounts.

LO# 11

12-14

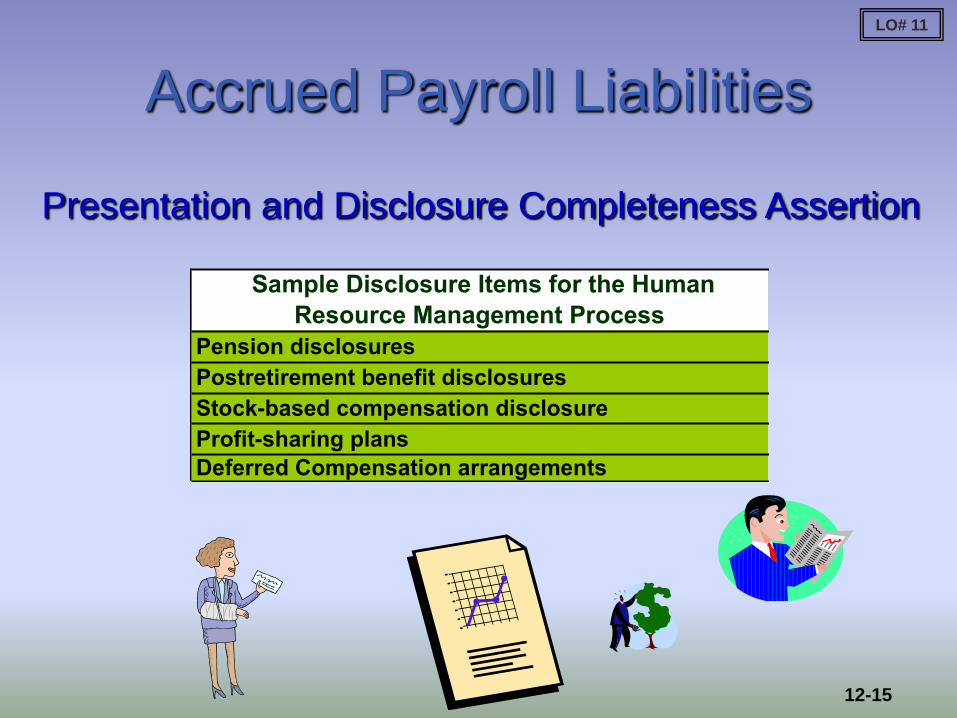

Accrued Payroll Liabilities

Presentation and Disclosure Completeness Assertion

Sample Disclosure Items for the Human

Resource Management Process

Pension disclosures

Postretirement benefit disclosures

Stock-based compensation disclosure

Profit-sharing plans

Deferred Compensation arrangements

LO# 11

12-15

Evaluating the Audit Findings –

Payroll-Related Accounts

If the likely misstatement is less than the tolerable

misstatement, the auditor may accept

the accounts as fairly presented.

If the likely misstatement is greater than the

tolerable misstatement, the auditor must

conclude that the accounts are not fairly presented.

LO# 12

12-16

End of Chapter 12

12-17