Embed Size (px)

DESCRIPTION

Commercial Bank

Citation preview

Chapter Eleven

Liquidity and Reserves Management: Strategies and Policies

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Key Topics

•Sources of Demand for and Supply of Liquidity

•Why Financial Firms Have Liquidity Problems •Liquidity Management Strategies •Estimating Liquidity Needs •The Impact of Market Discipline •Legal Reserves and Money Management

11-2

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Introduction

• One of the most important tasks the management of any financial institution faces is ensuring adequate liquidity at all times

• A financial firm is considered to be “liquid” if it has ready access to immediately spendable funds at reasonable cost at precisely the time those funds are needed

• This suggests that a liquid financial firm either has▫ The right amount of immediately spendable funds on hand when they

are required▫ They can raise liquid funds in timely fashion by borrowing or selling

assets• Lack of adequate liquidity can be one of the first signs that a

financial institution is in trouble• A financial firm can be closed if it cannot raise sufficient

liquidity even though, technically, it may still be solvent

11-3

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

The Demand for and Supply of Liquidity

• Demands for Liquidity▫Customer deposit withdrawals▫Credit requests from quality loan customers▫Repayment of nondeposit borrowings▫Operating expenses and taxes▫ Payment of stockholder dividends

• Supplies of Liquid Funds▫ Incoming customer deposits▫Revenues from the sale of nondeposit services▫Customer loan repayments▫ Sales of bank assets ▫ Borrowings from the money market

11-4

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

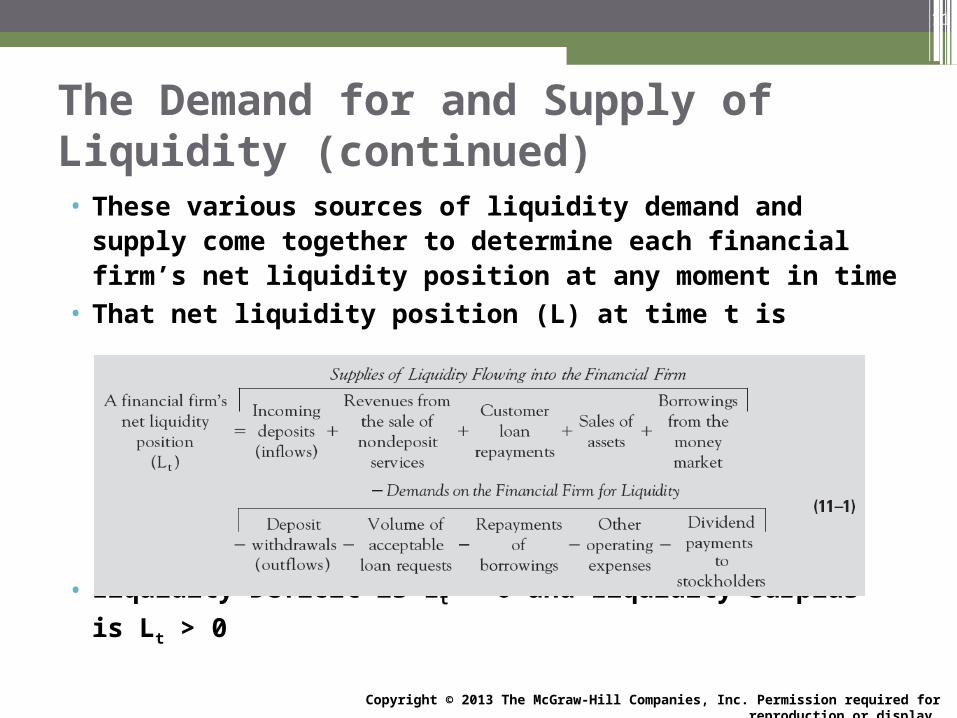

The Demand for and Supply of Liquidity (continued)• These various sources of liquidity demand and supply come

together to determine each financial firm’s net liquidity position at any moment in time

• That net liquidity position (L) at time t is

• Liquidity Deficit is Lt < 0 and Liquidity Surplus is Lt > 0

11-5

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

The Demand for and Supply of Liquidity (continued) • The essence of liquidity management problems for

financial institutions1. Rarely are demands for liquidity equal to the supply of

liquidity at any particular moment in time▫The financial firm must continually deal with either a

liquidity deficit or a liquidity surplus. 2. There is a trade-off between liquidity and profitability▫The more resources are tied up in readiness to meet

demands for liquidity, the lower is that financial firm’s expected profitability (other factors held constant)

11-6

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Why Financial Firms Often Face Significant Liquidity Problems• Imbalances between maturity dates of their assets and

liabilities• High proportion of liabilities (especially demand deposits

and money market borrowings) are subject to immediate repayment

• Sensitivity to changes in interest rates▫May affect customer demand for deposits▫May affect customer demand for loans

• Central role in the payment process, reputation and public confidence in the system

11-7

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Strategies for Liquidity Managers

• Think about what is a liquid asset?▫ Liquid assets have a ready market, stable price and are

reversible• Identify strategies for liquidity management▫ Asset Liquidity Management or Asset Conversion Strategy▫ This strategy calls for storing liquidity in the form of liquid assets (T-

bills, fed funds loans, CDs, etc.) and selling them when liquidity is needed

▫ Borrowed Liquidity or Liability Management Strategy▫ This strategy calls for the bank to purchase or borrow from the

money market to cover all of its liquidity needs▫ Balanced Liquidity Strategy▫ The combined use of liquid asset holdings (Asset Management) and

borrowed liquidity (Liability Management) to meet liquidity needs

11-8

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Strategies for Liquidity Managers (continued)

• Guidelines for Liquidity Managers▫Keep track of all fund-using and fund-raising departments▫Know in advance withdrawals by the biggest credit or

deposit customers▫Priorities and objectives for liquidity management should

be clear▫Liquidity needs must be evaluated on a continuing basis

11-9

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs

•Sources and Uses of Funds Approach•Structure of Funds Approach•Liquidity Indicator Approach•The Ultimate Standard for Assessing Liquidity

Needs: Signals from the Marketplace

11-10

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

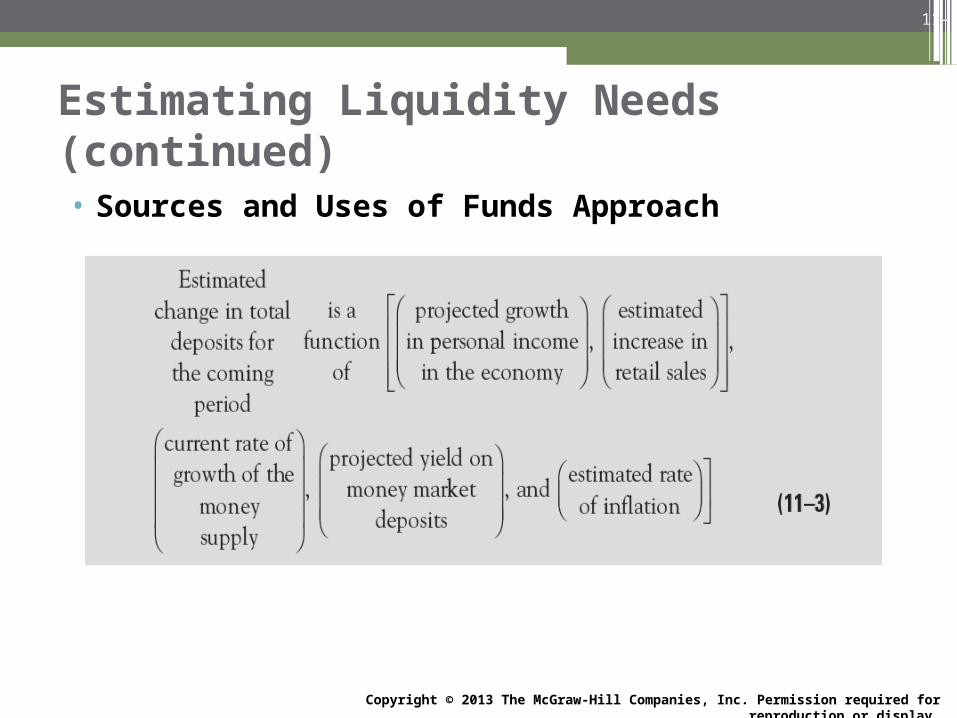

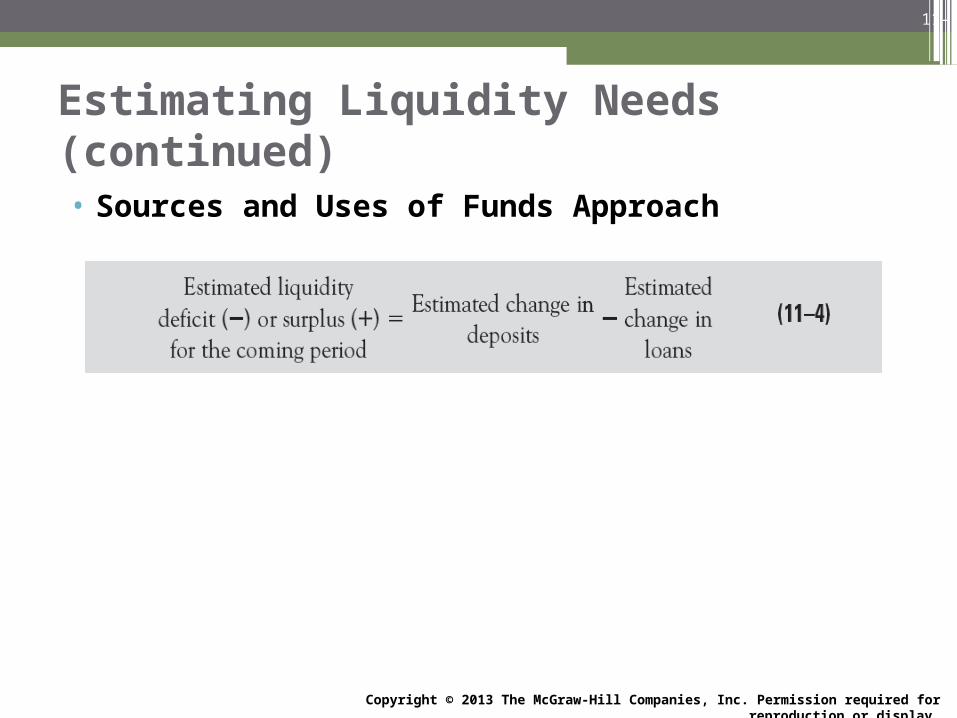

Estimating Liquidity Needs (continued)

• Sources and Uses of Funds Approach▫ Loans and deposits must be forecast for a given liquidity

planning period▫ The estimated change in loans and deposits must be calculated

for the same planning period▫ The liquidity manager must estimate the bank’s net liquid funds

by comparing the estimated change in loans to the estimated change in deposits

11-11

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

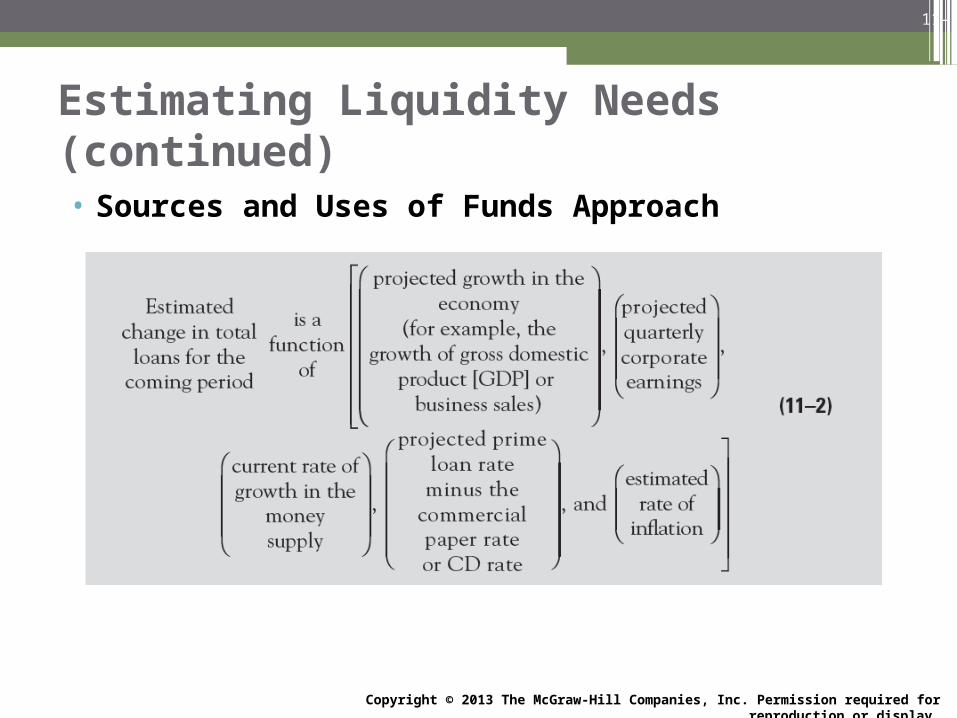

Estimating Liquidity Needs (continued)

• Sources and Uses of Funds Approach

11-12

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs (continued)

• Sources and Uses of Funds Approach

11-13

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs (continued)

• Sources and Uses of Funds Approach

11-14

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs (continued)

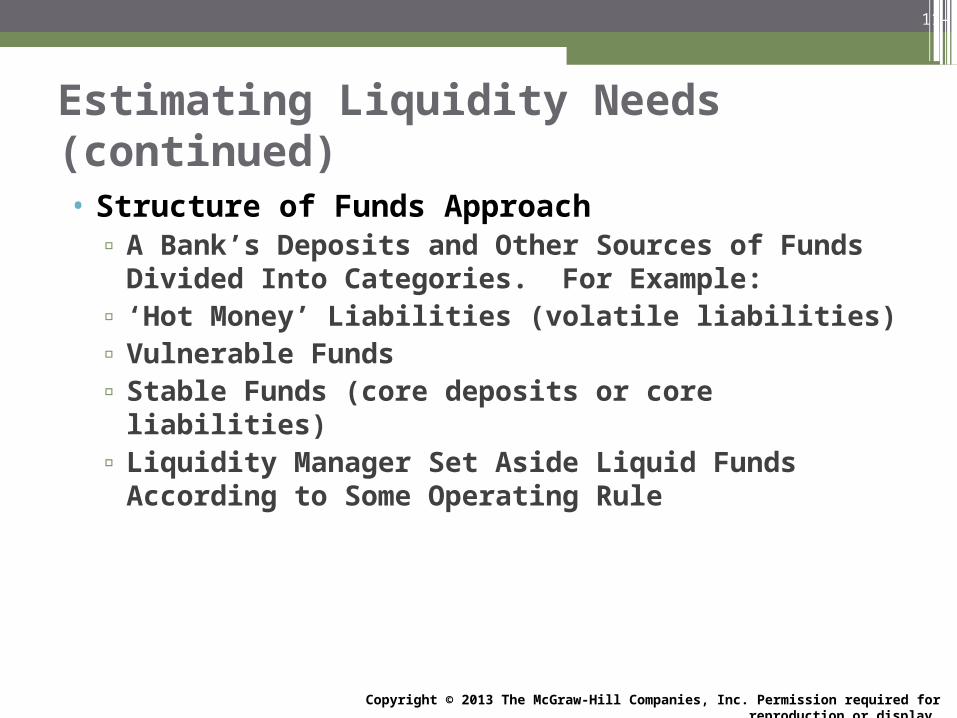

• Structure of Funds Approach▫ A Bank’s Deposits and Other Sources of Funds Divided Into

Categories. For Example:▫ ‘Hot Money’ Liabilities (volatile liabilities)▫ Vulnerable Funds▫ Stable Funds (core deposits or core liabilities) ▫ Liquidity Manager Set Aside Liquid Funds According to Some

Operating Rule

11-15

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs (continued)

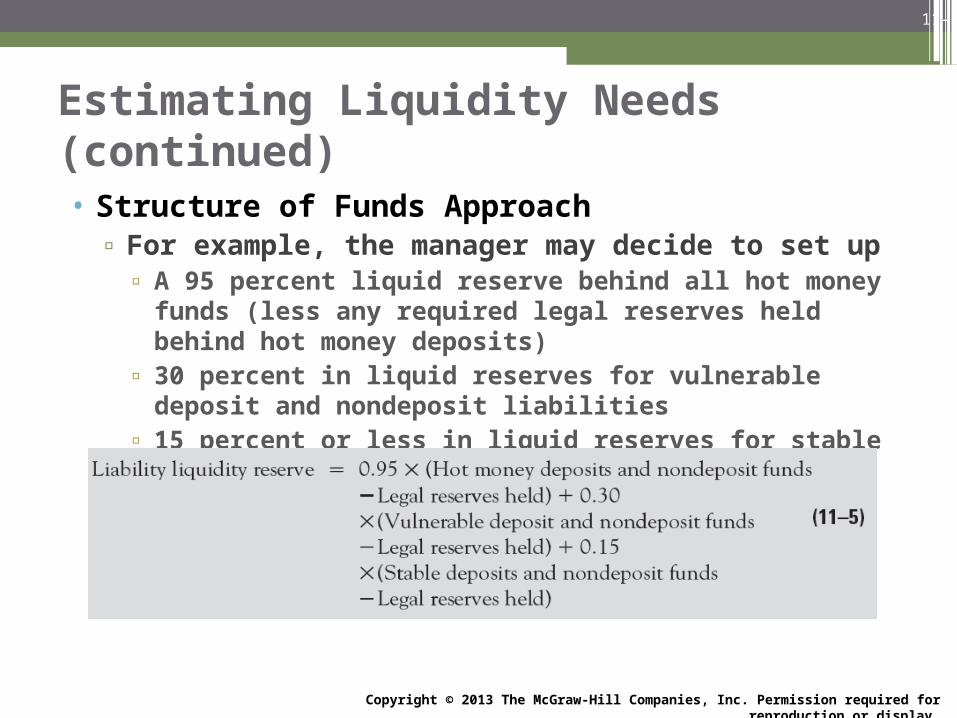

• Structure of Funds Approach▫ For example, the manager may decide to set up▫ A 95 percent liquid reserve behind all hot money funds (less any

required legal reserves held behind hot money deposits)▫ 30 percent in liquid reserves for vulnerable deposit and nondeposit

liabilities▫ 15 percent or less in liquid reserves for stable (core) funds sources

11-16

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Estimating Liquidity Needs (continued)

• Structure of Funds Approach▫ Combining both loan and deposit liquidity requirements, this

institution’s total liquidity requirement would be

11-17

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

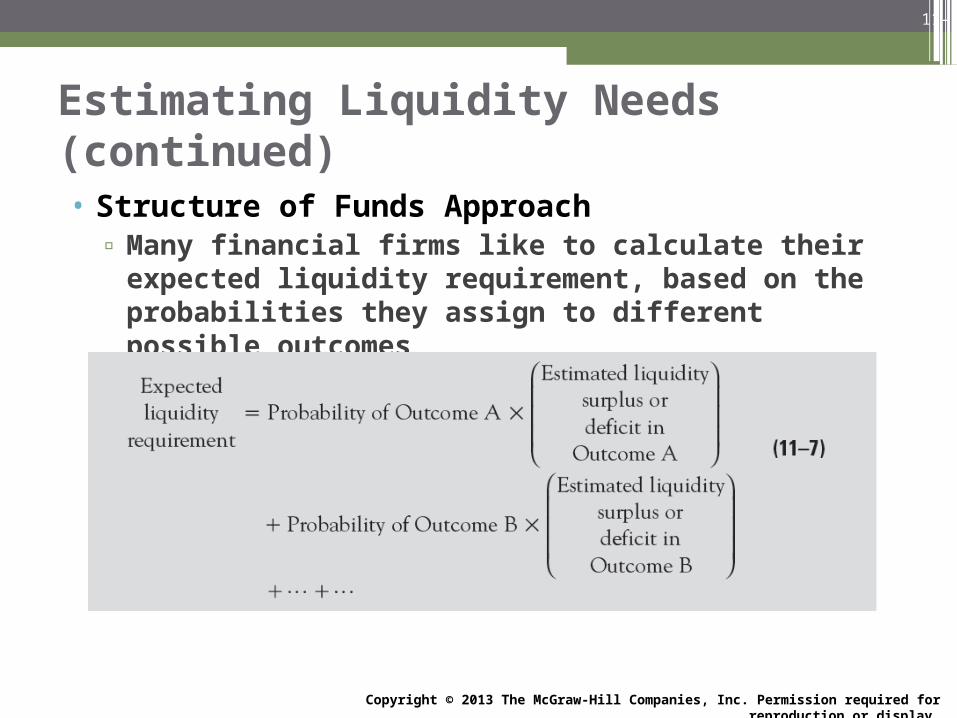

Estimating Liquidity Needs (continued)

• Structure of Funds Approach▫ Many financial firms like to calculate their expected liquidity

requirement, based on the probabilities they assign to different possible outcomes

11-18

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

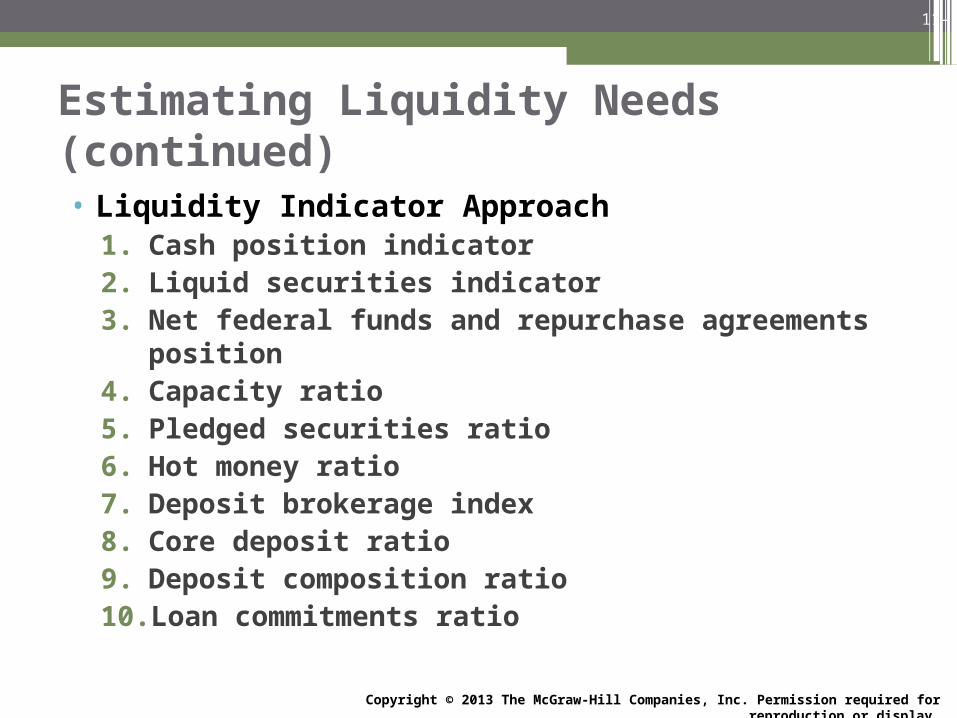

Estimating Liquidity Needs (continued)

• Liquidity Indicator Approach1. Cash position indicator2. Liquid securities indicator3. Net federal funds and repurchase agreements position4. Capacity ratio5. Pledged securities ratio6. Hot money ratio7. Deposit brokerage index8. Core deposit ratio9. Deposit composition ratio 10. Loan commitments ratio

11-19

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

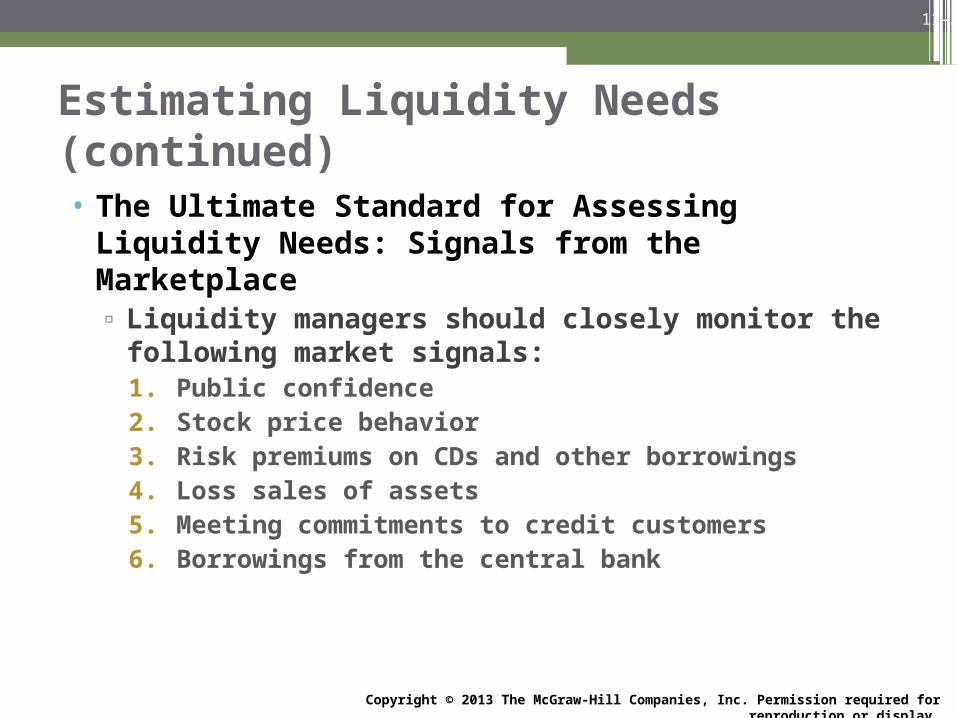

Estimating Liquidity Needs (continued)

• The Ultimate Standard for Assessing Liquidity Needs: Signals from the Marketplace▫ Liquidity managers should closely monitor the following market

signals:1. Public confidence2. Stock price behavior 3. Risk premiums on CDs and other borrowings 4. Loss sales of assets 5. Meeting commitments to credit customers6. Borrowings from the central bank

11-20

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

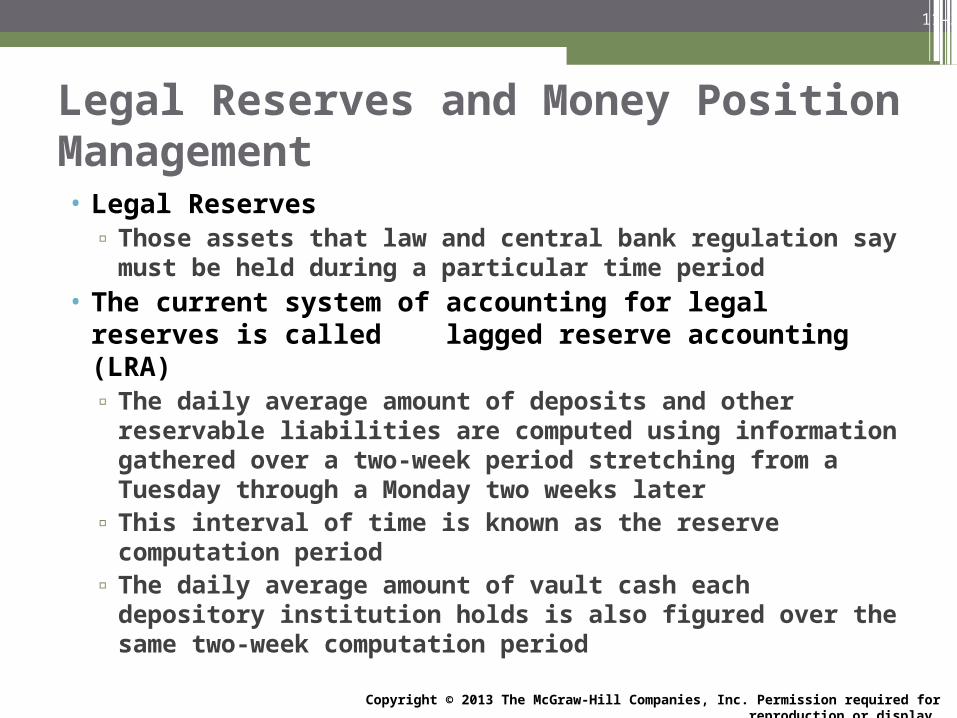

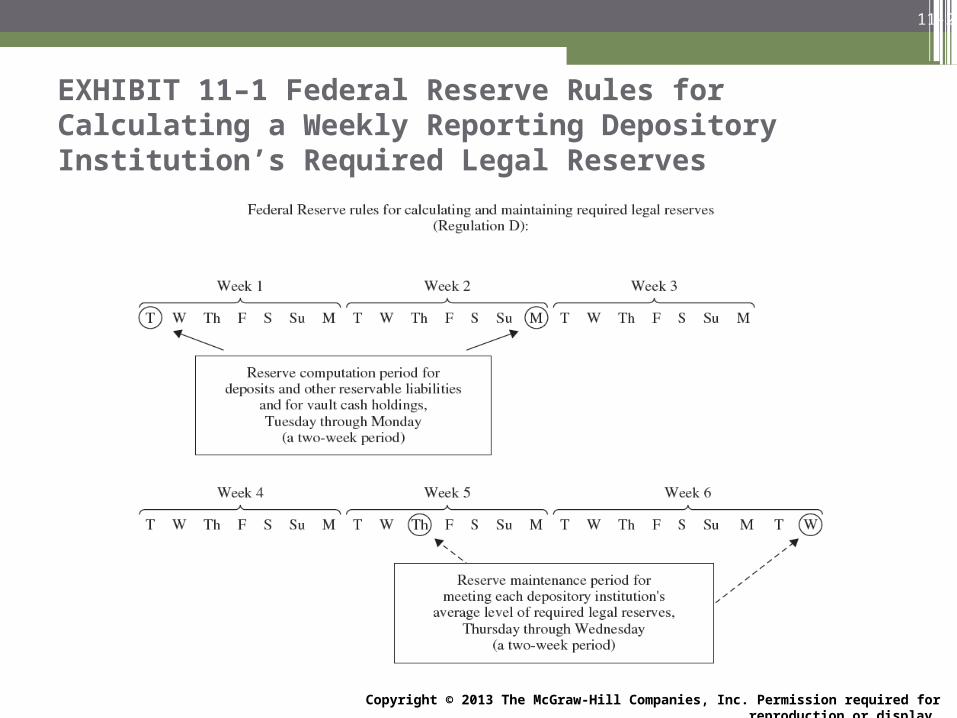

Legal Reserves and Money Position Management • Legal Reserves▫ Those assets that law and central bank regulation say must be

held during a particular time period• The current system of accounting for legal reserves is called

lagged reserve accounting (LRA)▫ The daily average amount of deposits and other reservable

liabilities are computed using information gathered over a two-week period stretching from a Tuesday through a Monday two weeks later

▫ This interval of time is known as the reserve computation period▫ The daily average amount of vault cash each depository

institution holds is also figured over the same two-week computation period

11-21

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

EXHIBIT 11–1 Federal Reserve Rules for Calculating a Weekly Reporting Depository Institution’s Required Legal Reserves

11-22

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Legal Reserves and Money Position Management (continued)• Legal Reserves

▫ Only two kinds of assets can be used for this purpose1. Cash in the vault2. Deposits held in a reserve account with the regional Fed

▫ The reserve requirement in 2010 was 3 percent of the end-of-the-day daily average amount held over a two-week period, from $10.7 million up to $58.8 million▫ The first $10.7 million have zero legal reserves

▫ The $58.8 million figure is known as the reserve tranche and changes every year based on deposit growth

▫ Transaction deposits over $58.8 million held by the same depository institution carried a 10 percent legal reserve requirement

▫ This annual legal reserve adjustment is designed to offset inflation

11-23

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

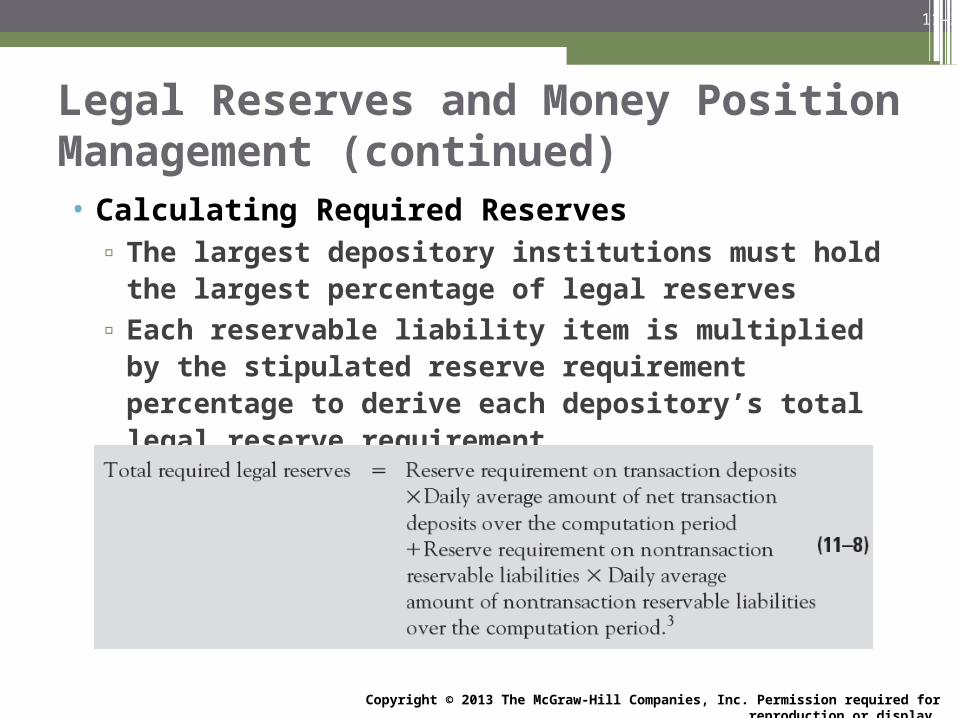

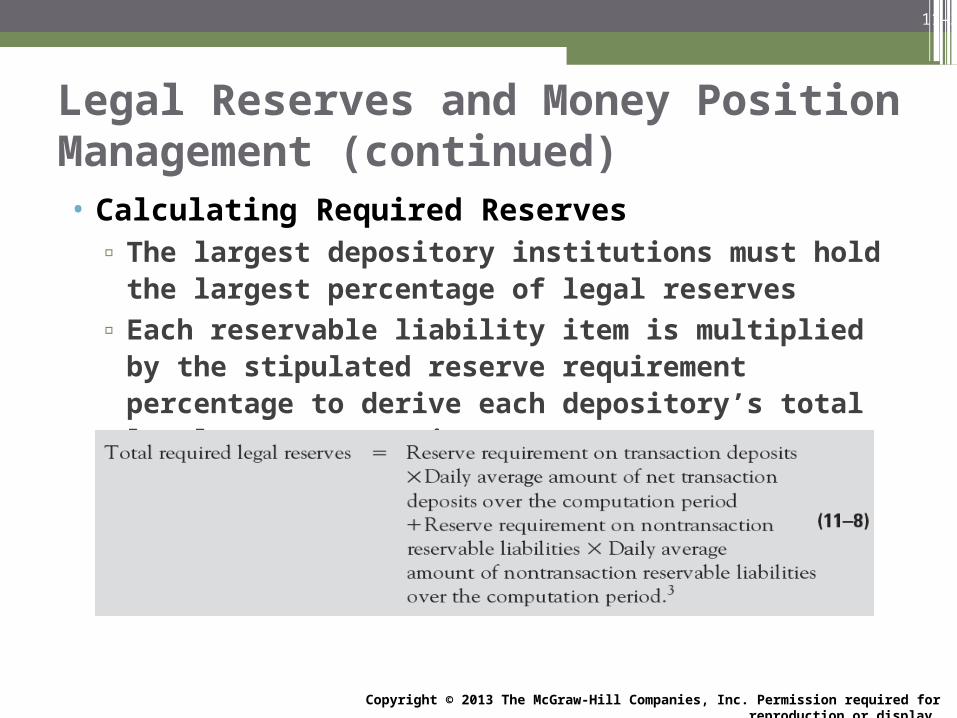

Legal Reserves and Money Position Management (continued)• Calculating Required Reserves ▫ The largest depository institutions must hold the largest

percentage of legal reserves▫ Each reservable liability item is multiplied by the stipulated

reserve requirement percentage to derive each depository’s total legal reserve requirement

11-24

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Legal Reserves and Money Position Management (continued)• Calculating Required Reserves ▫ The largest depository institutions must hold the largest

percentage of legal reserves▫ Each reservable liability item is multiplied by the stipulated

reserve requirement percentage to derive each depository’s total legal reserve requirement

11-25

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

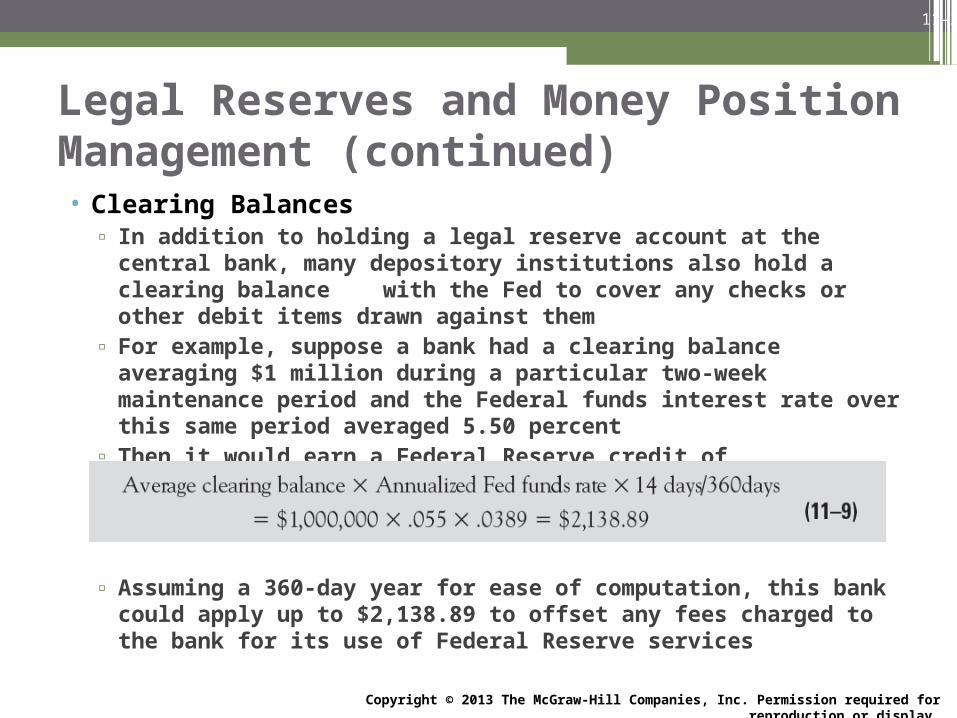

Legal Reserves and Money Position Management (continued)• Clearing Balances

▫ In addition to holding a legal reserve account at the central bank, many depository institutions also hold a clearing balance with the Fed to cover any checks or other debit items drawn against them

▫ For example, suppose a bank had a clearing balance averaging $1 million during a particular two-week maintenance period and the Federal funds interest rate over this same period averaged 5.50 percent

▫ Then it would earn a Federal Reserve credit of

▫ Assuming a 360-day year for ease of computation, this bank could apply up to $2,138.89 to offset any fees charged to the bank for its use of Federal Reserve services

11-26

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

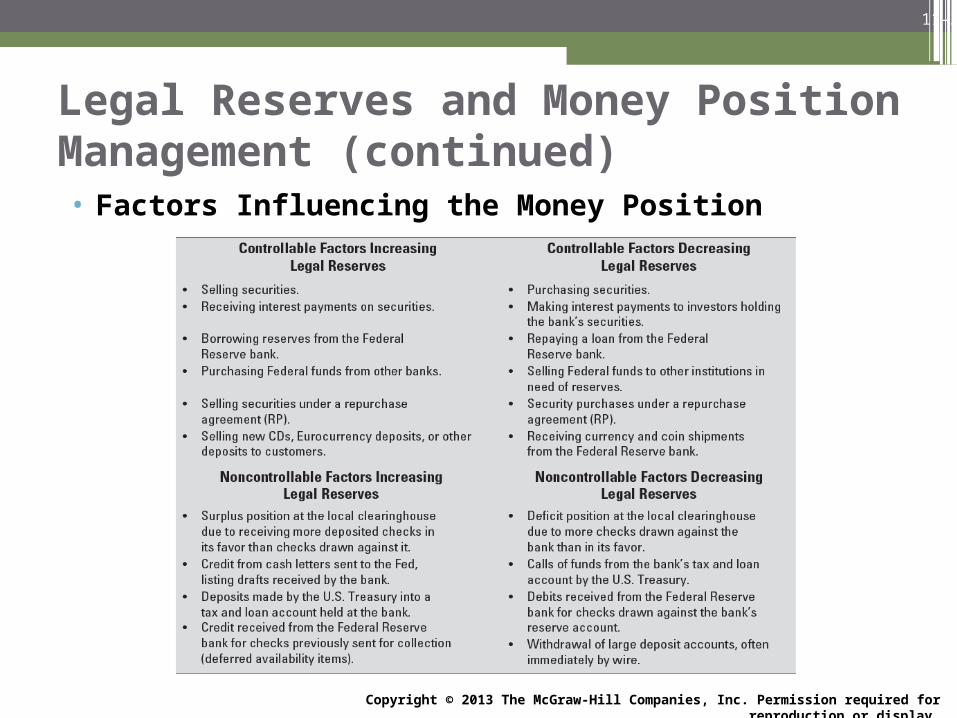

Legal Reserves and Money Position Management (continued)• Factors Influencing the Money Position

11-27

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Legal Reserves and Money Position Management (continued)• Sweep Accounts ▫ Volume of legal reserves held at the Fed has declined in recent years

largely due to sweep accounts▫ A contractual account between a bank and a customer that permits

the bank to move funds out of a customer’s checking account overnight in order to generate higher returns for the customer and lower reserve requirements for the bank▫ Retail Sweep▫ Business Sweep

▫ The sweeps market is likely to change in form and importance due to the recent passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2009

11-28

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Legal Reserves and Money Position Management (continued)• Other Factors to Influence Legal Reserves▫ Use of Fed Funds Market▫ The cheapest source▫ But very volatile▫ Managers rely on the Fed funds target rate (the most volatile on the

settlement date)▫ Other Options▫ Sell liquid securities▫ Draw upon excess correspondent balances▫ Enter into repurchase agreements for temporary borrowings▫ Sell new time deposits▫ Borrow in the Eurocurrency market

11-29

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

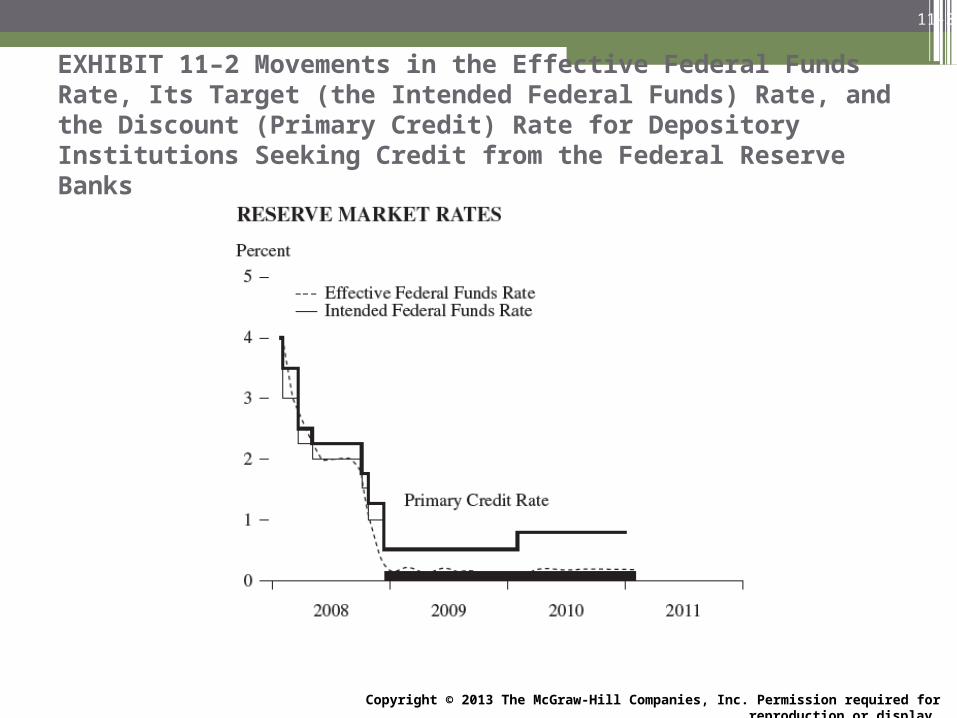

EXHIBIT 11–2 Movements in the Effective Federal Funds Rate, Its Target (the Intended Federal Funds) Rate, and the Discount (Primary Credit) Rate for Depository Institutions Seeking Credit from the Federal Reserve Banks

11-30

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

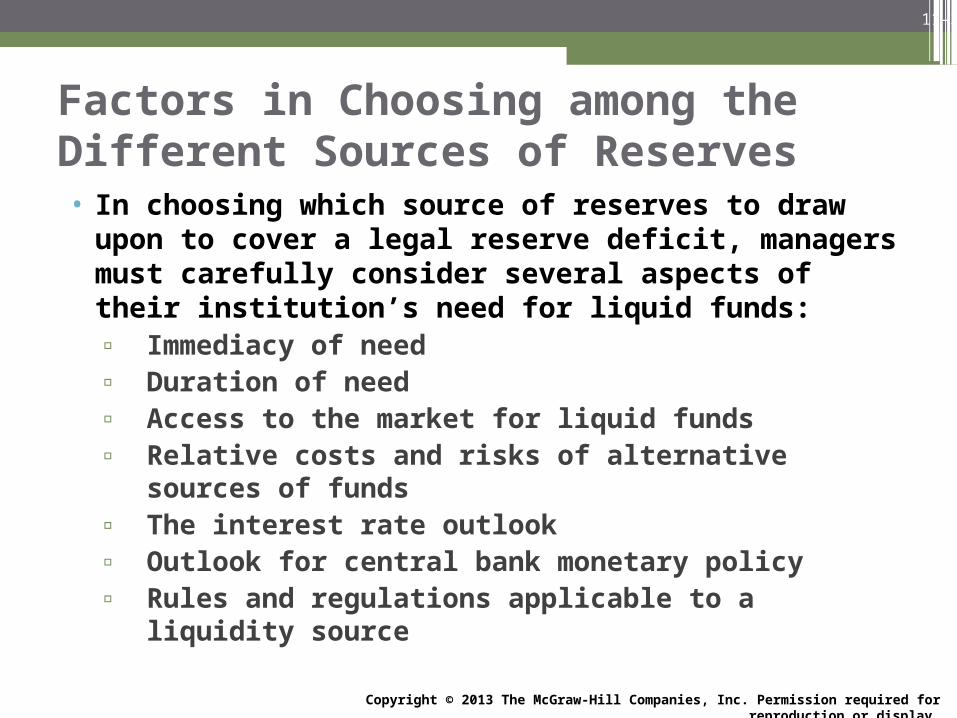

Factors in Choosing among the Different Sources of Reserves• In choosing which source of reserves to draw upon to cover a

legal reserve deficit, managers must carefully consider several aspects of their institution’s need for liquid funds:▫ Immediacy of need▫ Duration of need▫ Access to the market for liquid funds▫ Relative costs and risks of alternative sources of funds▫ The interest rate outlook▫ Outlook for central bank monetary policy▫ Rules and regulations applicable to a liquidity source

11-31

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

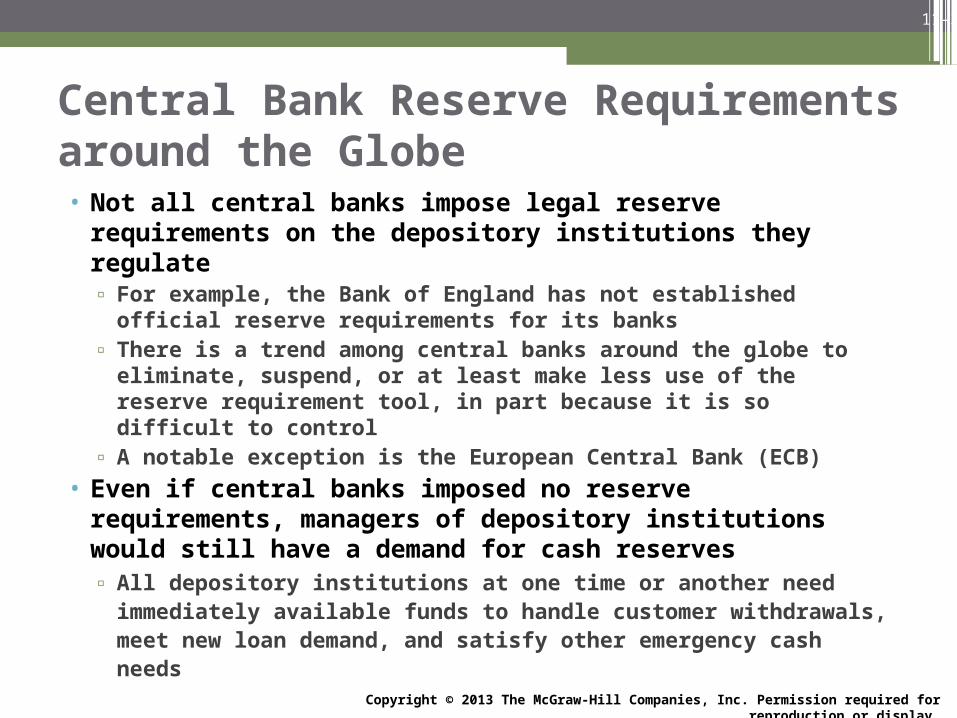

Central Bank Reserve Requirements around the Globe• Not all central banks impose legal reserve requirements on the

depository institutions they regulate▫ For example, the Bank of England has not established official reserve

requirements for its banks▫ There is a trend among central banks around the globe to eliminate,

suspend, or at least make less use of the reserve requirement tool, in part because it is so difficult to control

▫ A notable exception is the European Central Bank (ECB)• Even if central banks imposed no reserve requirements,

managers of depository institutions would still have a demand for cash reserves▫ All depository institutions at one time or another need immediately

available funds to handle customer withdrawals, meet new loan demand, and satisfy other emergency cash needs

11-32

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

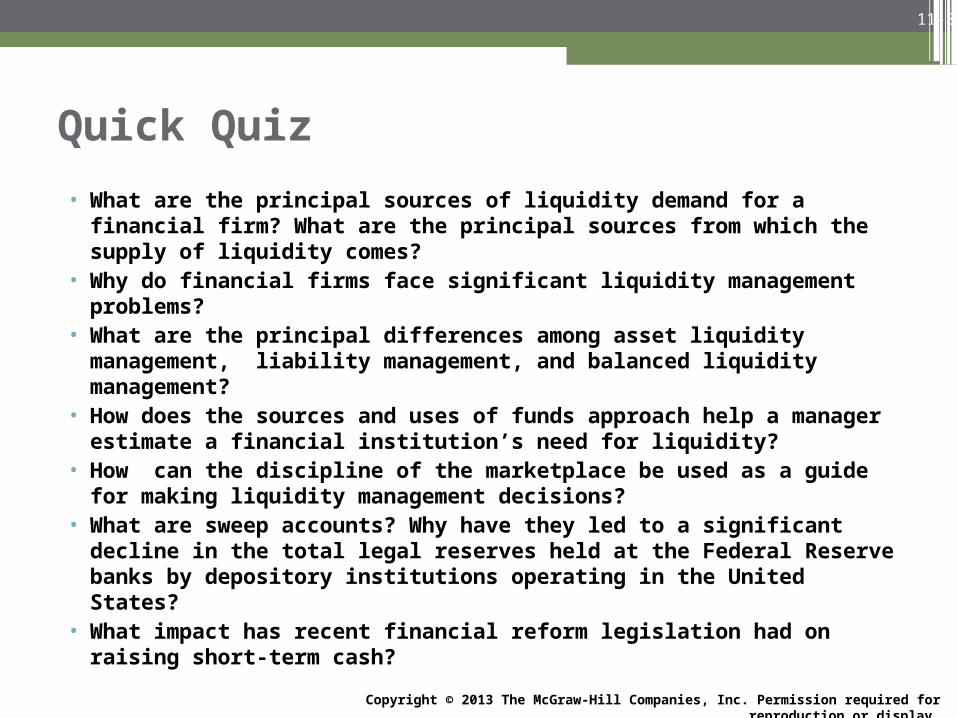

Quick Quiz• What are the principal sources of liquidity demand for a financial firm?

What are the principal sources from which the supply of liquidity comes?• Why do financial firms face significant liquidity management problems?• What are the principal differences among asset liquidity management,

liability management, and balanced liquidity management?• How does the sources and uses of funds approach help a manager estimate

a financial institution’s need for liquidity?• How can the discipline of the marketplace be used as a guide for making

liquidity management decisions?• What are sweep accounts? Why have they led to a significant decline in

the total legal reserves held at the Federal Reserve banks by depository institutions operating in the United States?

• What impact has recent financial reform legislation had on raising short-term cash?

11-33

Copyright © 2013 The McGraw-Hill Companies, Inc. Permission required for reproduction or display.