Embed Size (px)

Citation preview

Chapter 10

The Secondary Mortgage Market

© OnCourse Learning

Chapter 10 Learning Objectives

Understand the workings of the secondary mortgage market

Understand why the secondary mortgage market is important for a more efficient allocation of funds in the real estate market, and what the major secondary mortgage market agencies are

Understand how agency problems and the sub-prime mortgage crisis of 2007 to 2010 affected the major secondary mortgage market entities

© OnCourse Learning 2

Secondary Mortgage Market Market where existing mortgages are bought and sold

Mortgages are used as collateral for mortgage related securities

Reduces reliance on deposits

Agencies and firms that purchase mortgages in the secondary market often raise funds by issuing bonds or other debt instruments, pledging the mortgages as collateral (mortgage-backed securities)

© OnCourse Learning 3

Cash Flows in a Simple Secondary Mortgage Market Transaction

4© OnCourse Learning

Why Does the Secondary Mortgage Market Exist? Until late 1960s:

Difficult for thrifts to sell mortgages as mortgage assets were not homogeneous Potential buyers concerned with default risk Inability to buy and sell mortgages – led to persistent mismatch in supply and

demand for capitalRegional mismatch

Institutional mismatch

• The secondary mortgage market developed to solve the mismatch problem

• The federal government stimulated the development of the secondary mortgage market by overriding state laws hindering its development

5© OnCourse Learning

Characteristics of Mortgage-Backed Securities Have some form of credit enhancement

Implies less default risk than the underlying mortgages serving as collateral

Avoid double taxation Interest revenue from MBSs is passed through to the

investors; Revenues to the issuer and cash flows to the investors are not both taxed

Tailor cash flows of MBS to appeal to investors

6© OnCourse Learning

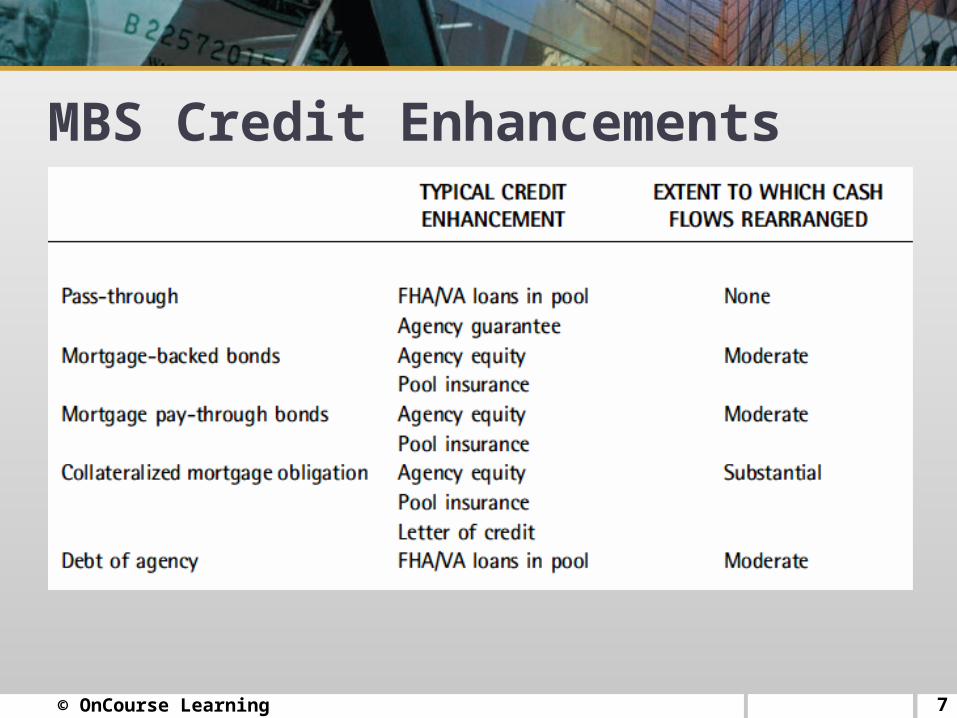

MBS Credit Enhancements

7© OnCourse Learning

Types of Mortgage-Backed Securities There are four principal types of MBS:

Mortgage pass-through securities Mortgage-backed bonds Mortgage pay-through bonds Collateralized mortgage obligations (CMO’s)

© OnCourse Learning 8

Mortgage Pass-Through Securities (MPTs) Fist popular MBS promoted by GNMA The investor has an undivided interest in the pool of

mortgages The investor has an “ownership” position in the mortgages Mortgage principal and interest and any prepayment is

passed-through to the investor on a pro-rata basis Mortgage originators sells the MPT at a slightly lower yield

than the interest rate of the underlying mortgages. The difference is shared by the originator who services the loan

and the agency which provides the credit enhancement9© OnCourse Learning

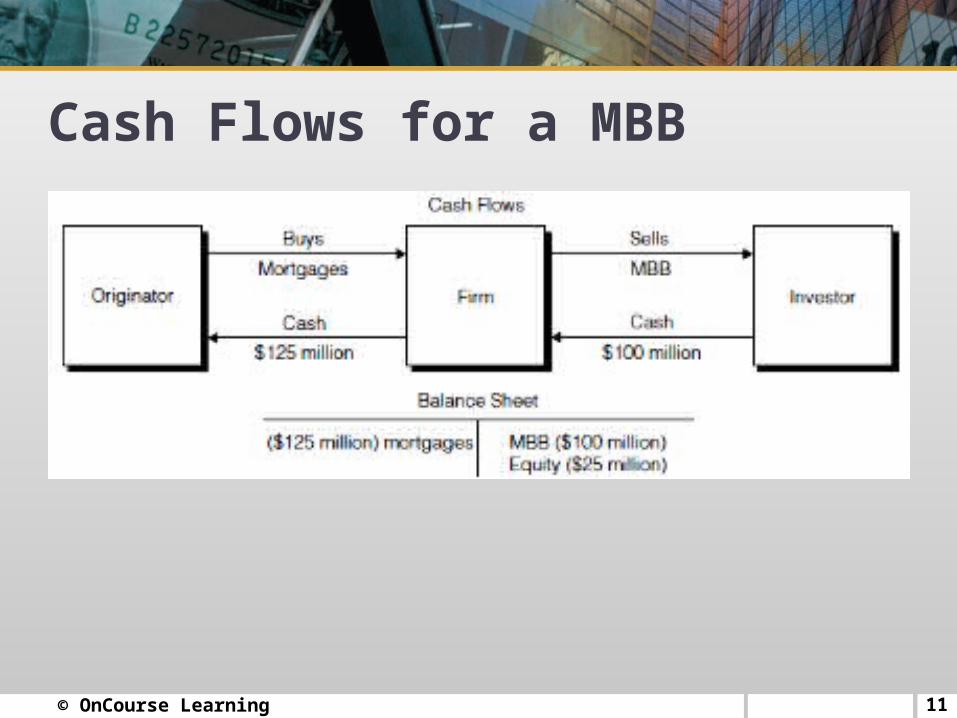

Mortgage-Backed Bonds (MBBs) MBSs that promise payments similar to corporate bonds

Semiannual payments of interest only until maturity Face value due at maturity

Mortgages are owned by the issuer of the MBB Maturity of the bonds is less than that of the underlying mortgages Yield is slightly below that on the mortgages Mortgages are placed with a trustee who marks-to-market any

changes in their value and ensures that the agreed-on overcollateralization is maintained

MBBs rated by rating agencies

10© OnCourse Learning

Cash Flows for a MBB

11© OnCourse Learning

Mortgage Pay-Through Bonds (MPTBs) A cross between pass-throughs and MBBs Issuer retains ownership in the pool and issues MPTB as a

debt obligation Cash flows to the investors are based on the coupon rate of

interest, while principal from amortization and prepayment is passed through as received from the pool

Rated by agencies, based on the same factors associated with MBBs

Less overcollateralization than with MBBs due to passing prepayment risk to the investors

12© OnCourse Learning

Collateralized Mortgage Obligations (CMOs) Rearrange cash flows from the pool of mortgages into

several different bond-like securities with different maturities

Different bond classes called tranches A typical CMO has three or four tranches A residual tranche (Tranche Z) often owned by the

issuer where all residual cash flows accrue Implies equity interest of the issuer in the CMO Cash flows accruing to residual represent return-on-equity.

13© OnCourse Learning

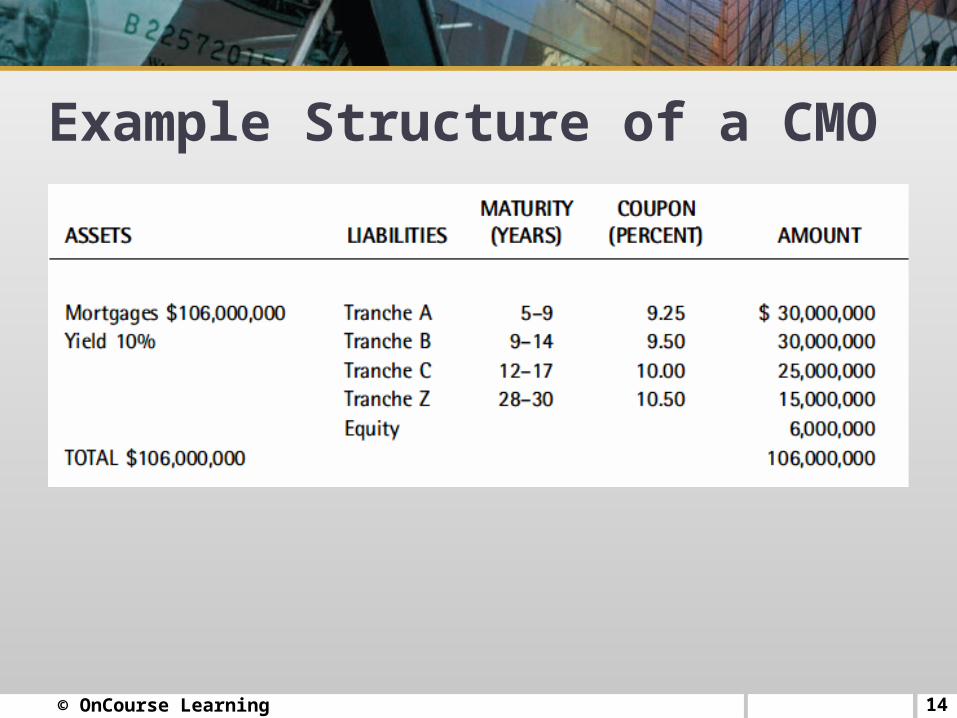

Example Structure of a CMO

14© OnCourse Learning

Swaps A SMM transaction where the lender sells mortgages to

an agency that in turn issues an MBS back to the lender Swaps are attractive due to the liquidity advantage of

MBS over loans Thrifts can use MBS as collateral to borrow funds MBS can be sold quicker than mortgage loans if there is

need for cash Even if they sell the MBS, the lenders are likely to retain

the servicing and receive a servicing fee

15© OnCourse Learning

Real Estate Synthetic Investment Securities (RESIs) Pass all of the credit risk through to the bondholders Rated by agencies Losses from default are passed to the lowest rated

classes first Securities are backed by, primarily, jumbo loans High return – high risk

In 2004 when mortgage rates approx. 6%, 15% yield on lower-grade RESIs

16© OnCourse Learning

Commercial Mortgage Backed Securities Started with S&L crisis of 1980s when RTC packaged commercial loans of

failed thrifts and sold CMBSs

Senior tranche received all principal payments including prepayments

Subordinated tranche bore all losses from defaults

© OnCourse Learning 17

CMBS (Cont.)

Securitization process is same as for CMOs with different tranches

May be backed up by many mortgages on many properties, a single loan on a very large property, or a single loan on many properties

Loans are credit rated and contributed to a REMIC

© OnCourse Learning 18

REMICs An entity that could issue CMOs and not be subject to

double taxation A partnership, trust, or other corporation may elect

REMIC status For tax purposes, income is recorded as received from

the mortgage pool and deductions are allowed for interest paid (on the CMO tranches); The net income can be passed-through to the owner of the residual as income or loss

19© OnCourse Learning

REMICs Can maintain favorable tax status as long as they don't

engage in the following transactions: Receive income from non-qualifying mortgages Receive fees or compensation for services (other than

servicing income from the mortgage portfolio) Buying or selling mortgages out of the pool (except as

the pool is liquidated if all proceeds are disbursed within 90 days)

20© OnCourse Learning

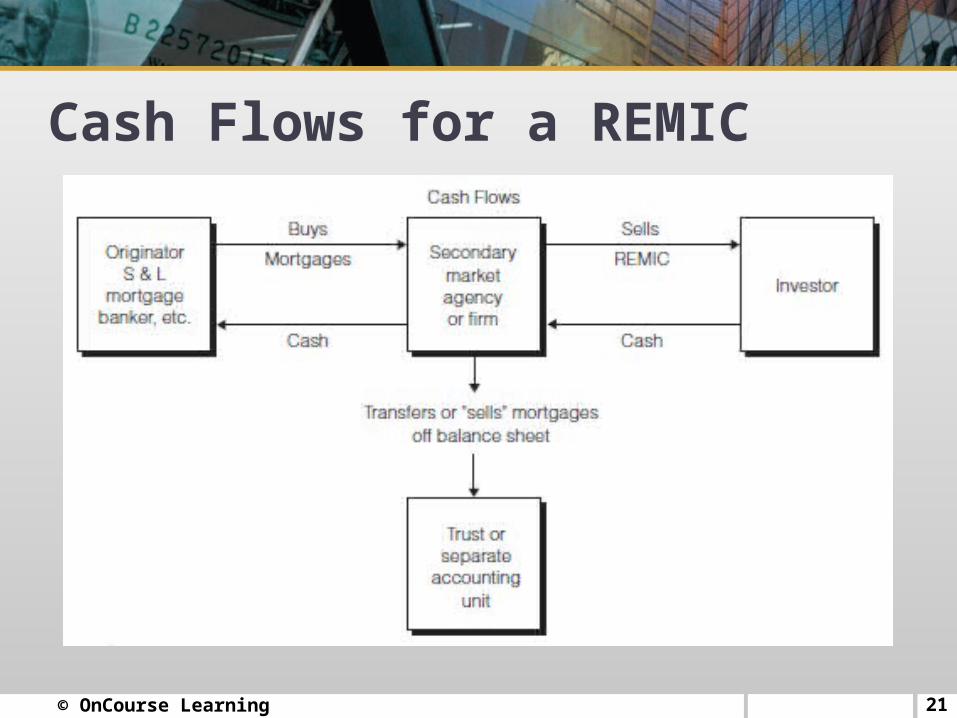

Cash Flows for a REMIC

21© OnCourse Learning

Secondary Mortgage Market Agencies and Firms Federal National Mortgage Association (Fannie Mae, FNMA)

Established in 1938 to buy FHA loans

Re-chartered in 1954 and became a private corporation

As of 1970, allowed to buy FHA,VA, and conventional mortgages

© OnCourse Learning 22

23© OnCourse Learning

Secondary Mortgage Market Agencies and Firms Government National Mortgage Association (Ginnie Mae, GNMA)

Created in 1968 within HUD

Does not purchase mortgages or issue securities

Market focus is to guarantee FHA and VA pass-through securities

Secondary Mortgage Market Agencies and Firms Federal Home Loan Mortgage Corporation (Freddie Mac)

Established in 1970 to create a secondary mortgage market for conventional mortgages

Operates as a private corporation

Currently buys FHA, VA, and conventional mortgages

© OnCourse Learning 24

Federal Home Loan Mortgage Corporation (Freddie Mac) Freddie Mac purchases both newly issued and seasoned (those with some

expired term) mortgages

Freddie Mac will also purchase construction/permanent loans that are FRMs, ARMs, or balloon/reset. These must be new dwellings and not rehabs.

© OnCourse Learning 25

Freddie Mac (Cont.)

Freddie Mac issues a wide variety of securities: Discount Notes and Debentures Mortgage Participation Certificates (Pass-throughs) on FRMs, ARMs, and multifamily Collateralized Mortgage Obligations in several classes or tranches Guaranteed Mortgage Certificates – not sold since 1979

© OnCourse Learning 26

Secondary Mortgage Market

Federal credit agencies that support the primary and secondary mortgage markets: Farm Credit System consolidated three agricultural agencies to make direct loans for

agricultural purposes Federal Agricultural Mortgage Corporation (Farmer Mac) to underwrite pools of farm

mortgages through pass-throughs

© OnCourse Learning 27

Secondary Mortgage Market Agencies and Firms Federal credit agencies that support the primary and secondary mortgage

markets: Rural Housing Service extends loans to rural areas for farms, houses, and community

facilities

Financing Corporation formed in 1987 to recapitalize the FSLIC

© OnCourse Learning 28

Government-Sponsored Enterprises

GSEs are not officially part of the federal government They appear to enjoy the backing of the federal

government Federal government does not guarantee these

agency’s obligations but Congress has shown that federal funds would be used to “bail” them out of financial stress

© OnCourse Learning 29

Government-Sponsored Enterprises

GSEs operate similarly to thrifts in purchasing long-term mortgages

They face interest rate risk, default risk, and management/operating risk

Office of Federal Housing Enterprise and Oversight (OFHEO) oversees the operations of the GSEs

© OnCourse Learning 30