Embed Size (px)

Citation preview

Chapter 10

Georgia Real Estate An Introduction to the Profession

Eighth Edition

Chapter 10

Lending Practices

Key Terms• amortized loan• balloon loan• conventional loans• equity• FHA• impound or reserve

account• loan origination fee• loan-to-value ratio

• maturity• PITI payment• PMI• point• principal• UFMIP• VA

© 2015 OnCourse Learning

Term Loans

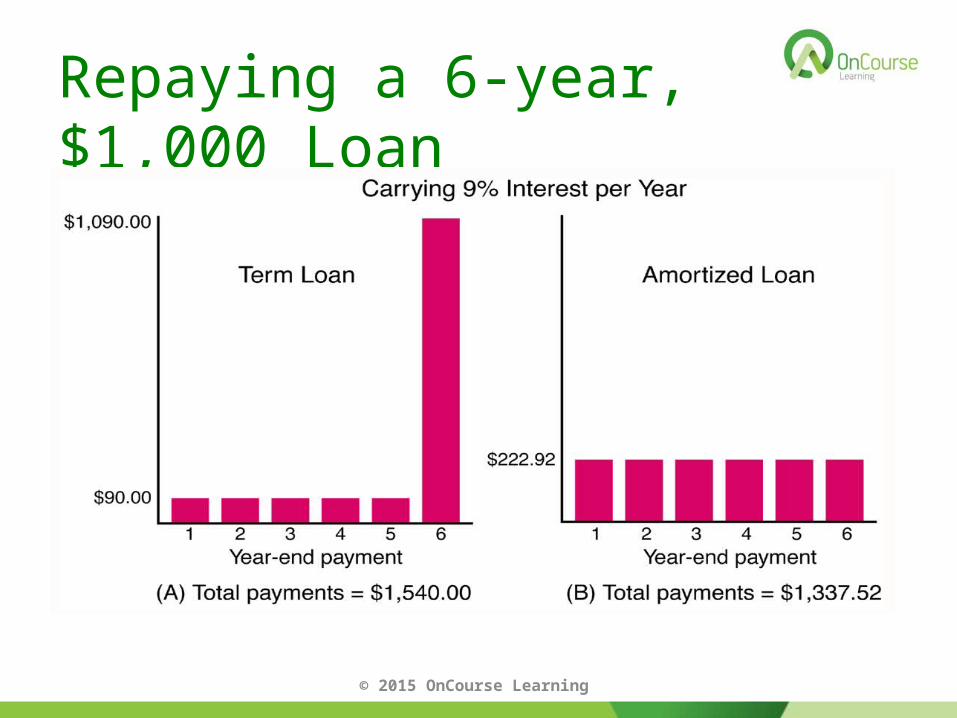

A loan that requires only interest payments until the last day of its life is called a term loan.

The borrower is required to pay the entire amount of the loan upon maturity (end of the life of the loan).

© 2015 OnCourse Learning

Amortized Loans

An amortized loan is a loan requiring periodic payments that include both interest and partial repayment of principal.

It is the accepted method of loan repayment.

© 2015 OnCourse Learning

Repayment Methods

An amortized loan requires regular and equal payments during the life of the loan.

The principal due at the end of an amortized loan is $0.00

© 2015 OnCourse Learning

9% Interest per Year of the Loan

© 2015 OnCourse Learning

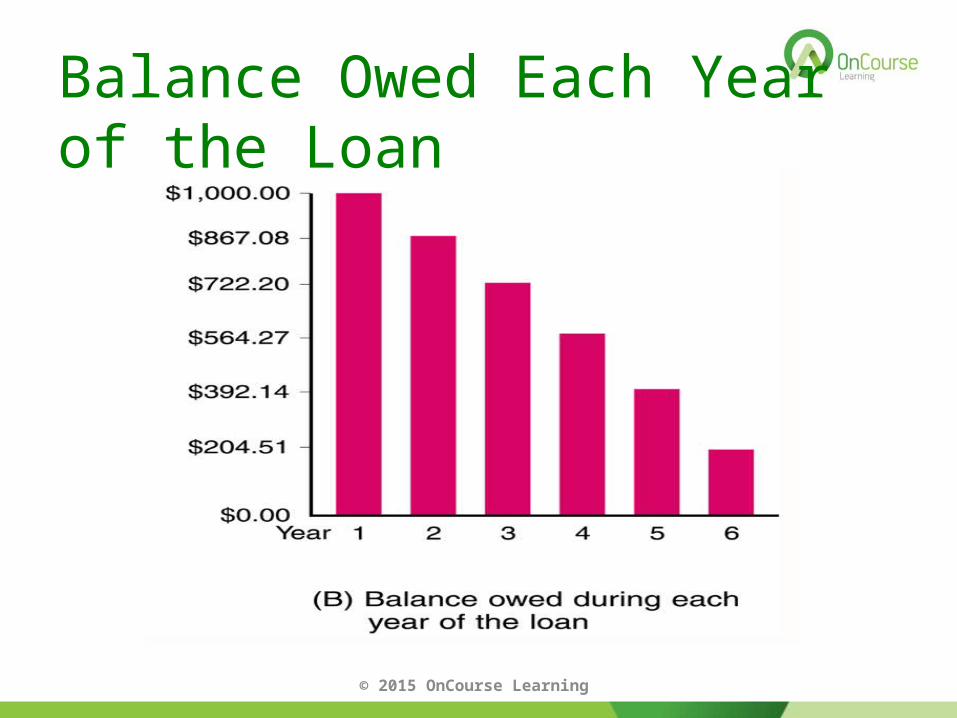

Balance Owed Each Year of the Loan

© 2015 OnCourse Learning

Repaying a 6-year, $1,000 Loan

© 2015 OnCourse Learning

Monthly Payments

Amortization tables can be used to calculate the monthly payments per $1,000 of loan for interest rates from 5 to 40 years for periods ranging from 5 to 40 years.

© 2015 OnCourse Learning

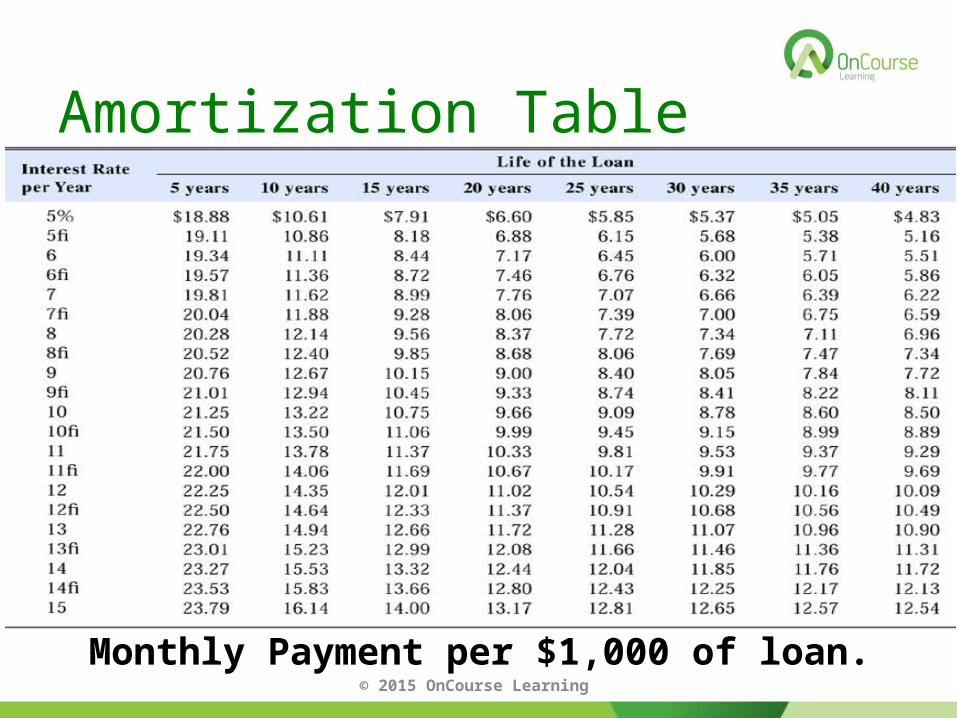

Amortization Table

© 2015 OnCourse Learning

Monthly Payment per $1,000 of loan.

Budget MortgageA budget mortgage collects principal, interest, one-twelfth of the estimated cost of the annual property taxes and hazard insurance on the mortgaged property.

The money for tax and insurance payments is placed in an escrow account also known as an impound account.

© 2015 OnCourse Learning

Budget Mortgage

When taxes and insurance payments are due, the lender pays them from the funds in the escrow account.

The principal, interest, taxes and insurance payment is often referred to as PITI.

© 2015 OnCourse Learning

Budget Mortgage

All VA loans, all FHA loans and most conventional loans above 80% of the value of the property are budget mortgages.

© 2015 OnCourse Learning

Balloon Mortgage

A balloon loan has a final payment larger than any of the previous payments on the loan.

In tight money markets, balloon loans increase considerably.

© 2015 OnCourse Learning

Partially Amortized Loan

A partially amortized loan has a series of amortized payments followed by a balloon payment at maturity.

© 2015 OnCourse Learning

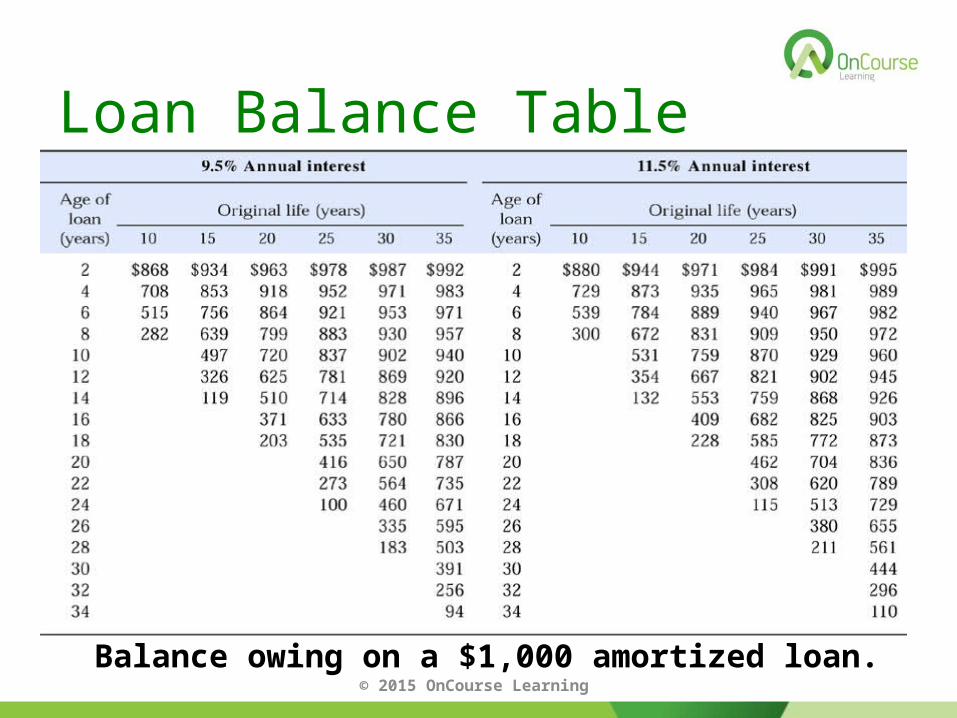

Loan Balance Table

© 2015 OnCourse Learning

Balance owing on a $1,000 amortized loan.

15-Year Loan

A lender is usually willing to offer a 15-year loan at a lower rate of interest than a 30-year loan.

© 2015 OnCourse Learning

Bi-Weekly PaymentsInstead of paying once a month, the borrower makes one-half of the monthly payment every two weeks.

Biweekly payment results in 26 half-payments being made per year versus 12 whole payments. This can have significant savings over the life of the loan.

© 2015 OnCourse Learning

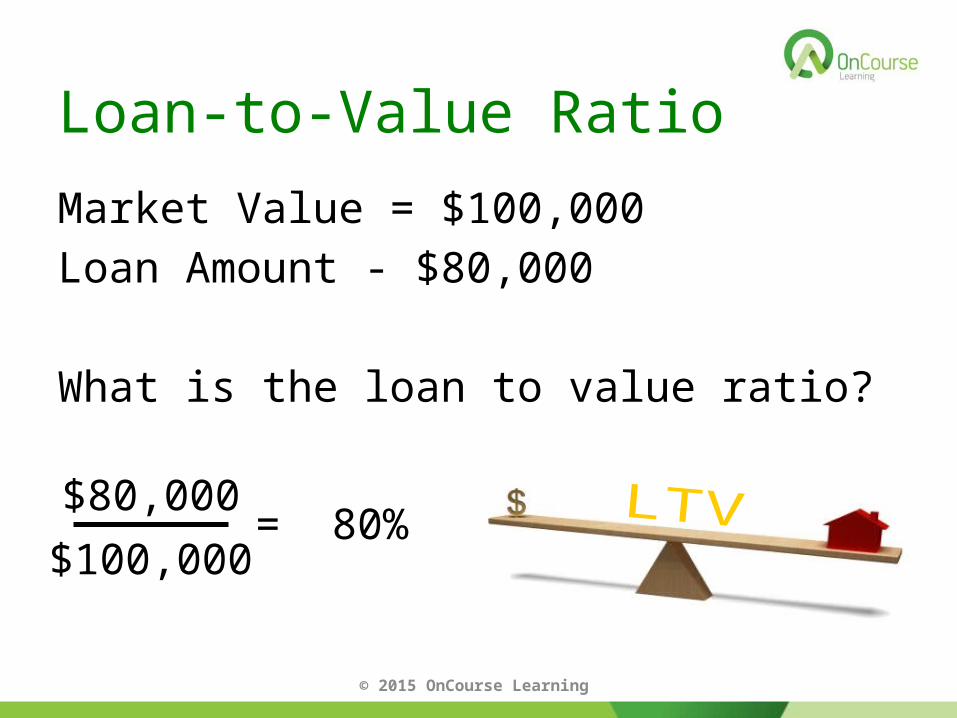

Loan-to-Value RatioThe relationship between the amount of money a lender is willing to loan and the lender’s estimate of the market value of the property that will serve as security is called the loan-to-value ratio.

The lender will loan the sales price or the appraised value, whichever is lower.

© 2015 OnCourse Learning

Loan-to-Value Ratio

Market Value = $100,000Loan Amount - $80,000

What is the loan to value ratio?

© 2015 OnCourse Learning

$80,000

$100,000= 80%

Equity

The difference between the market value of a property and the debt owed against it is called the owner’s equity.

© 2015 OnCourse Learning

Loan Points

In finance, a point is 1% of the loan amount.

On a $100,000 loan, one point is $1,000.

On an $80,000 loan, three points is $2,400.

© 2015 OnCourse Learning

Origination Fee

The loan origination fee is what the borrower pays to get the loan.

It is generally 1% of the loan amount.

© 2015 OnCourse Learning

Discount PointsPoints charged to raise the lender’s return on a loan are known as discount points.

A discount point is a yield to the lender.

Each discount point raises the yield by 1/8 of 1%.

© 2015 OnCourse Learning

Discount Points

Four discount points would raise the yield by 0.5%.

Discount points are most often charged during periods of tight money.

© 2015 OnCourse Learning

FHA Insurance Programs

The Federal Housing Administration (FHA) insures lenders against losses due to non-repayment on loans on both new and existing homes.

© 2015 OnCourse Learning

Current FHA Coverage

As of 2014, the maximum loan amount in Georgia for single-family residential is $320,850.

Current limits can be researched at www.hud.gov.

© 2015 OnCourse Learning

Current FHA Coverage

Private investors are banned from the FHA single-family program.

No single-family loans can be assumed by investors.

© 2015 OnCourse Learning

Assumability

The FHA requires the creditworthiness approval prior to the conveyance of title on all assumption loans.

If the borrower assumes a mortgage loan, the lender cannot refuse to release the original borrower from liability on the loan.

© 2015 OnCourse Learning

Mortgage InsuranceThe FHA charges a one-time up-front mortgage insurance premium (UPMIP) that is paid when the loan is made. Currently it is 1.75% of the loan amount.

As of January 2015, the annual premium was lowered to 0.85% of the annual loan balance.

© 2015 OnCourse Learning

Mortgage Insurance

The annual MIP is collected for the life of the loan on all loans originated after April 1, 2013.

© 2015 OnCourse Learning

Floating Interest Rates

Fixed-rate FHA loans are negotiable and float with the market. The seller has a choice in how many points to contribute toward the borrower’s loan.

© 2015 OnCourse Learning

Construction Regulations

FHA has its own minimum construction requirements.

If a building is defective, the borrower is more likely to default on the loan and create an insurance claim against the FHA.

© 2015 OnCourse Learning

Construction Regulations

The FHA is an insurance agency. The loan itself is obtained from a savings and loan, bank, mortgage company or similar lender.

It is an FHA-insured loan, not a loan from the FHA.

© 2015 OnCourse Learning

Department of Veteran Affairs

The Department of Veteran Affairs is commonly known as the VA.

The VA guarantees loans made to veterans.

© 2015 OnCourse Learning

No Down Payment

In 2014, the Freddie Mac conforming loan limit was $417,000. Since lenders will typically loan up to four times the amount of the VA guarantee, the current loan limit with no money down is $417,000.

© 2015 OnCourse Learning

No Down PaymentThe guarantee entitlement for an honorably discharged veteran is good until used. If not remarried, the spouse of a veteran who died as a result of service can also obtain a housing guarantee.

Eligibility requirements for veterans vary according to years served. Active duty personnel also qualify.

© 2015 OnCourse Learning

VA CertificatesA veteran should make application to the Department of Veterans Affairs for a certificate of eligibility. This shows whether the veteran is qualified and the amount of the guarantee available.

© 2015 OnCourse Learning

VA Certificates

When the veteran applies for a VA guarantee, the property is appraised and the VA issues a certificate of reasonable value.

The veteran must agree to occupy the property.

© 2015 OnCourse Learning

VA Certificates

The VA guarantees fixed-rate loans for as long as 30 years on homes.

No prepayment penalty is charged if the borrower wishes to pay sooner.

© 2015 OnCourse Learning

VA CertificatesThere is no due-on-sale clause that requires the loan to be repaid if the property is sold.

The VA guarantees loans for the purchase of townhouses and condominiums, to build or improve a home, and to buy a mobile home as a residence.

© 2015 OnCourse Learning

Financial LiabilityIn the event of default and subsequent foreclosure, they are required eventually to make good any losses suffered by the VA on the loan.

A veteran is permitted a full new guarantee entitlement if complete repayment of a previous VA-guaranteed loan has been made.

© 2015 OnCourse Learning

Funding FeeThe funding fee for an active duty personnel or veteran putting $0 down is currently 2.15%

VA funding fees vary according to the down payment amount, active duty versus National Guard and Reservists, and first-time use of a VA loan versus subsequent use of a VA loan.

© 2015 OnCourse Learning

Interest Rates

Interest rates and discount points agreed on by the veteran and the lender..

VA does not set interest rates.

© 2015 OnCourse Learning

Assumption Requirements

VA LOANS ARE NOT ASSUMABLE WITHOUT THE PRIOR APPROVAL OF THE DEPARTMENT OF THE VETERANS AFFAIRS.

© 2015 OnCourse Learning

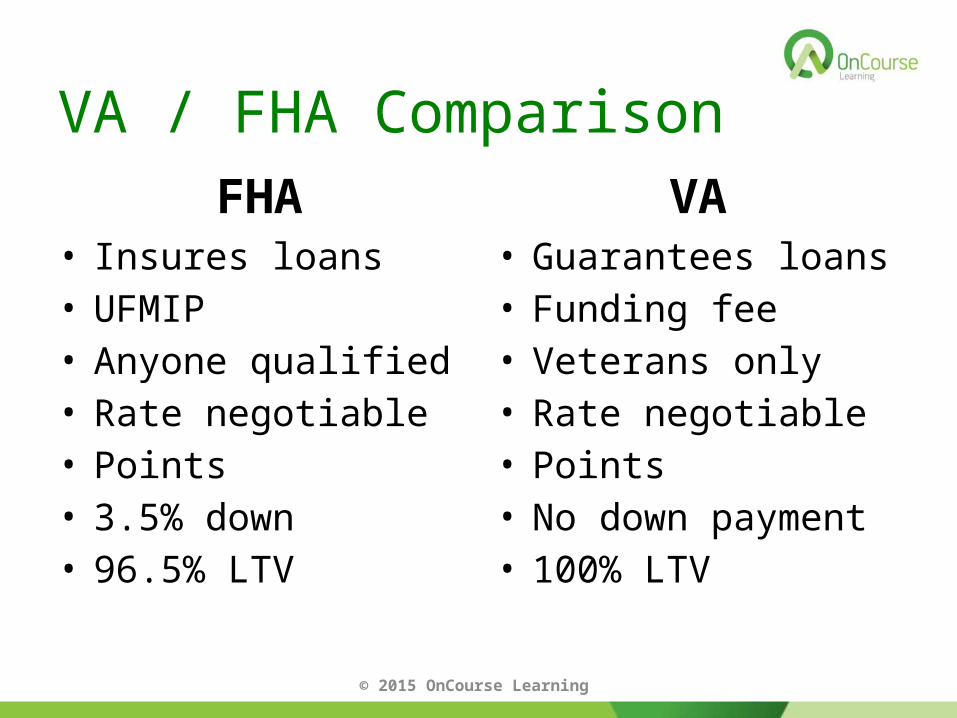

VA / FHA ComparisonFHA

• Insures loans• UFMIP• Anyone qualified• Rate negotiable• Points• 3.5% down• 96.5% LTV

VA• Guarantees loans• Funding fee• Veterans only• Rate negotiable• Points• No down payment• 100% LTV

© 2015 OnCourse Learning

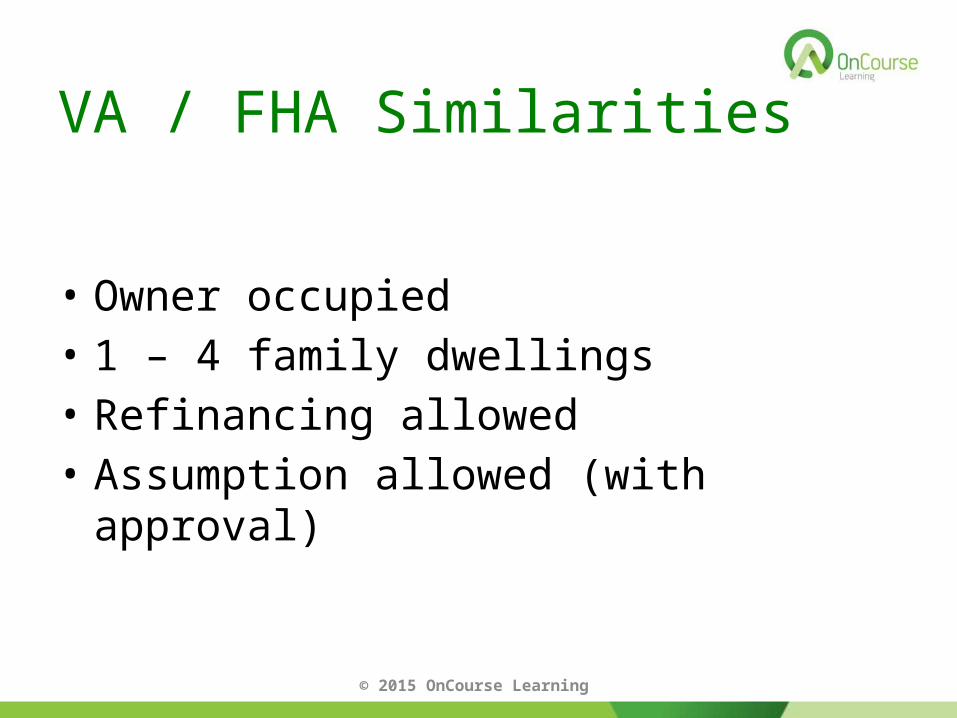

VA / FHA Similarities

• Owner occupied• 1 – 4 family dwellings• Refinancing allowed• Assumption allowed (with approval)

© 2015 OnCourse Learning

Private Mortgage Insurance

The object of private mortgage insurance (PMI) is to insure lenders against foreclosure losses.

PMI insures only the top 20% to 25% of a loan, not the whole loan.

© 2015 OnCourse Learning

Private Mortgage Insurance

The Homeowner’s Protection Act (HPA) requires servicers to automatically cancel PMI once a loan reaches 78% of the property’s original value.

© 2015 OnCourse Learning