Embed Size (px)

Citation preview

Chapter 10A Monetary Intertemporal Model: Money, Banking, Prices, and Monetary Policy

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-2

Chapter 10 Topics

• What is money?

• Monetary Intertemporal Model

• Demand for Money – Banks and alternative means of payment.

• Real and nominal interest rates

• Neutrality of money

• Monetary policy: targets and rules

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-3

What is Money?

• Medium of exchange

• Store of value

• Unit of account

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-4

Measures of Money

• Monetary Base (outside money): currency in circulation plus bank reserves (reserves essentially zero in Canada)

• M1: currency in circulation plus transactions deposits at some financial institutions.

• M2: M1 + savings deposits at some financial institutions.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-5

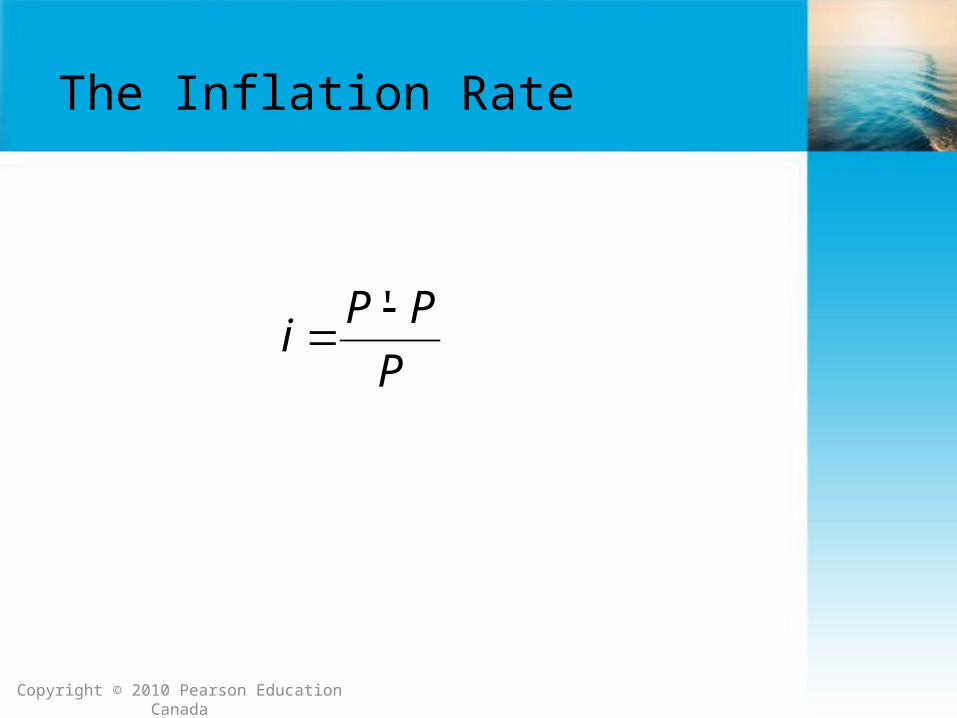

The Inflation Rate

P

PPi

'

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-6

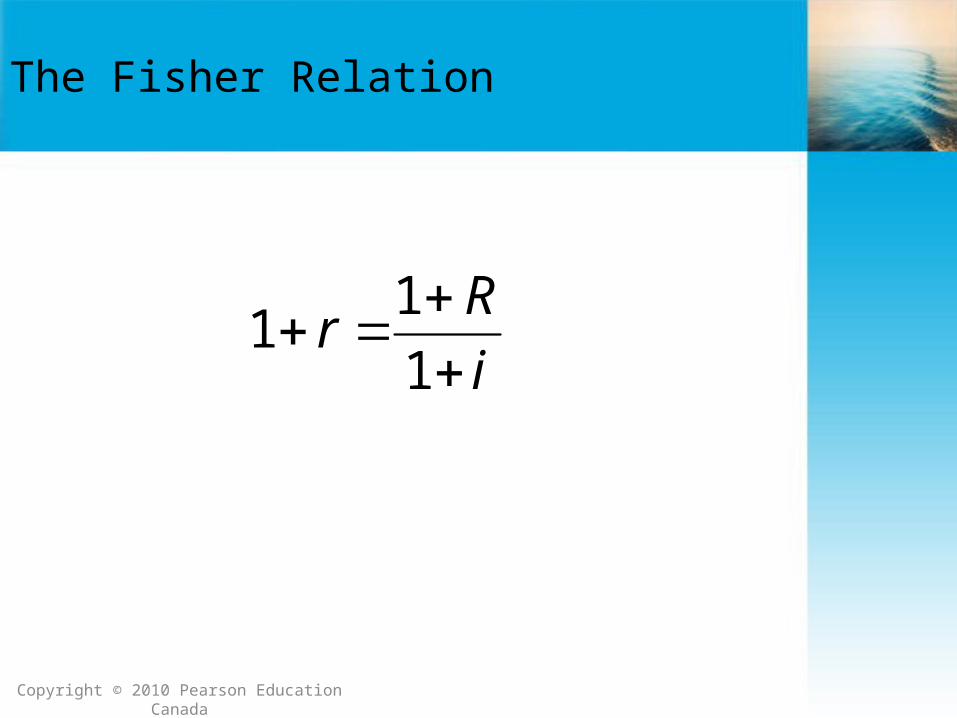

The Fisher Relation

i

Rr

1

11

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-7

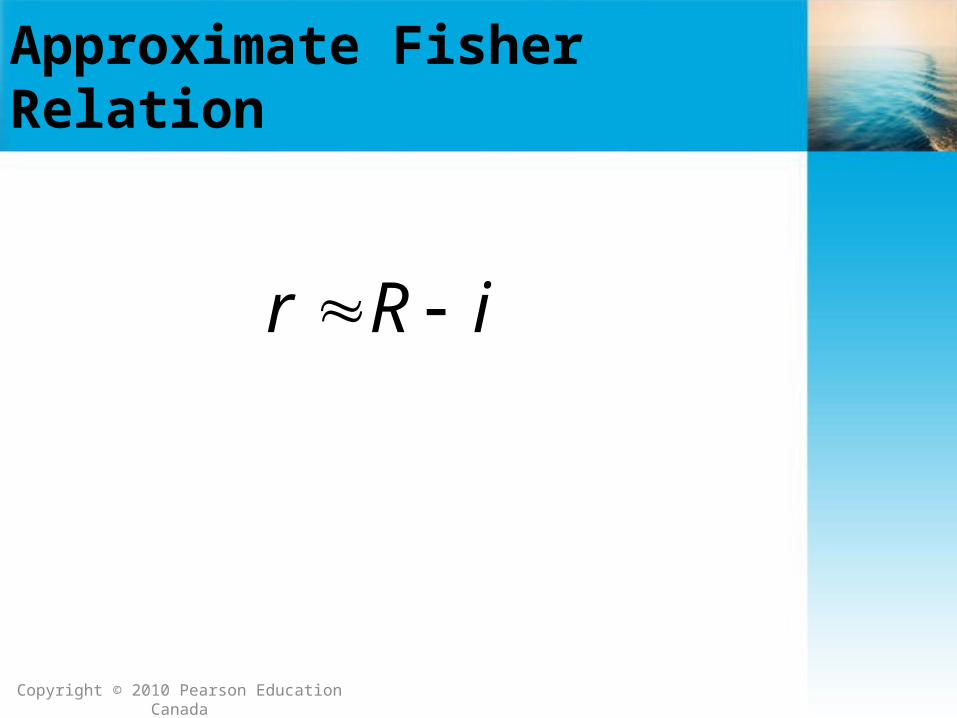

Approximate Fisher Relation

iRr

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-8

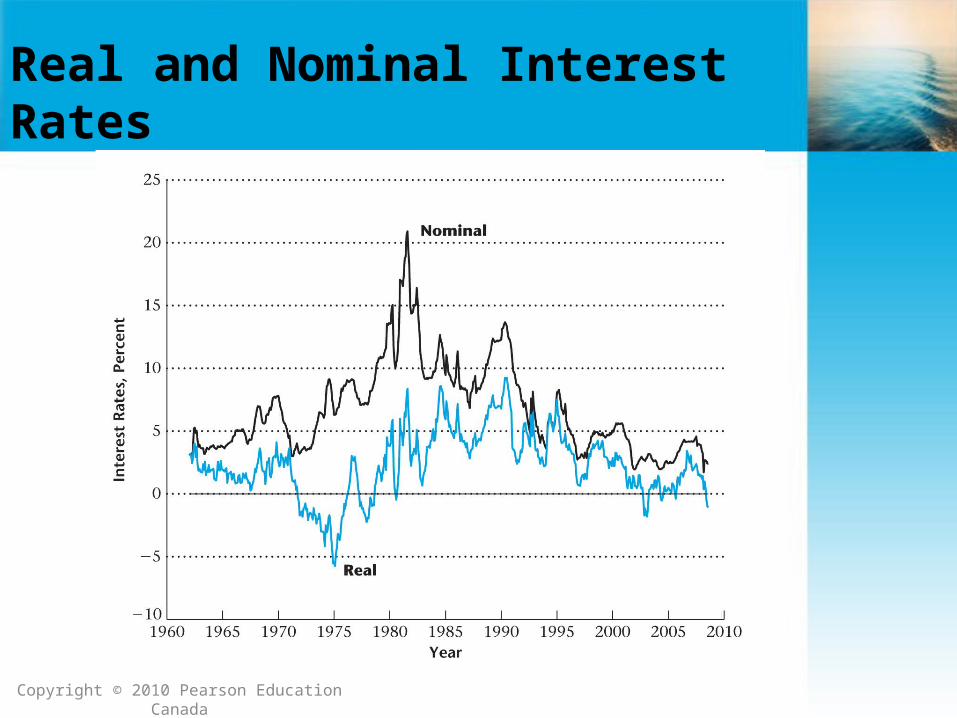

Real and Nominal Interest Rates

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-9

Monetary Intertemporal Model

• Type of cash-in-advance model.

• Representative consumer, representative firm, banks, and government.

• Consumers and firms require cash on hand to purchase goods, or can use “credit cards,” which involves obtaining credit from the bank.

• The quantity of credit card balances is determined by the supply (from banks) and the demand (consumers and firms).Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-10

Banks

• Assets are money, credit card balances (credit extended to firms and consumers), and nominal government bonds.

• Liabilities are transactions deposits and time deposits.

• Essentially 2 separate businesses – money and credit card balances back transactions deposits, bonds back time deposits.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-11

Transactions Deposits, Time Deposits, Credit Card Balances

• Transactions deposits – can be withdrawn as currency at the beginning of the period. No interest within the period.

• Time deposits – held until the following period, earning nominal interest rate R.

• Credit card balances – cost to the bank of q per unit (in real terms) to issue credit.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-12

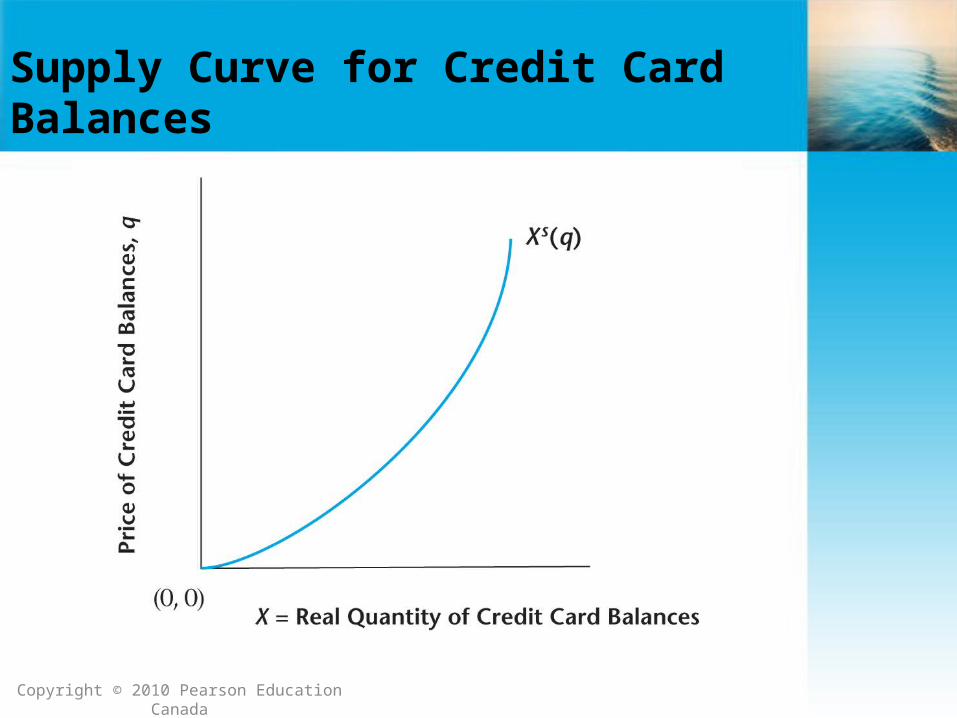

Supply Curve for Credit Card Balances

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-13

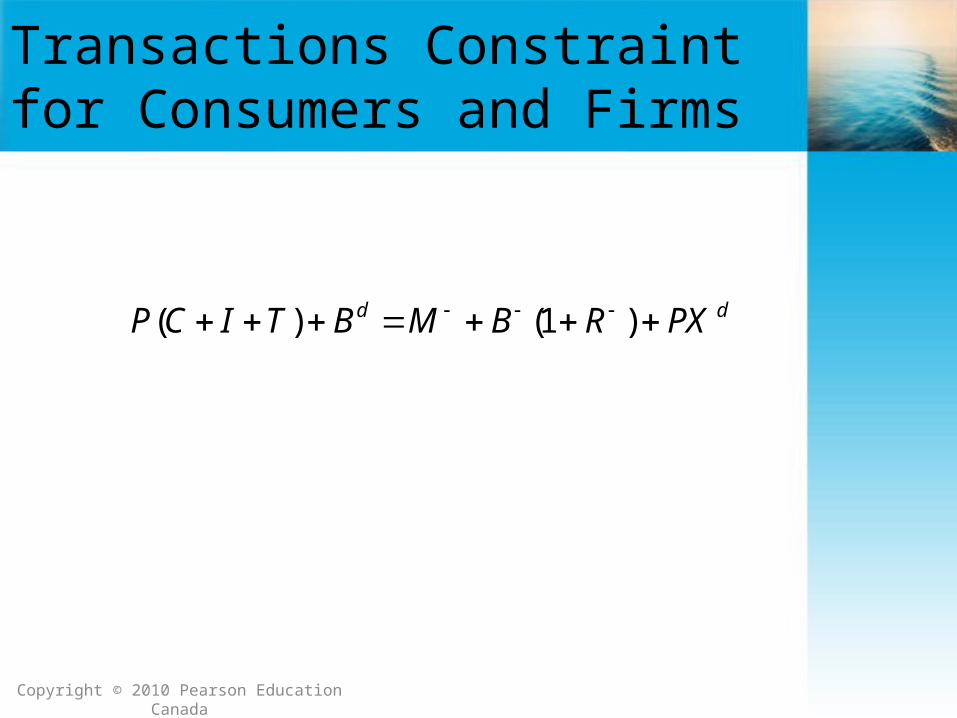

Transactions Constraint for Consumers and Firms

dd PXRBMBTICP )1()(

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-14

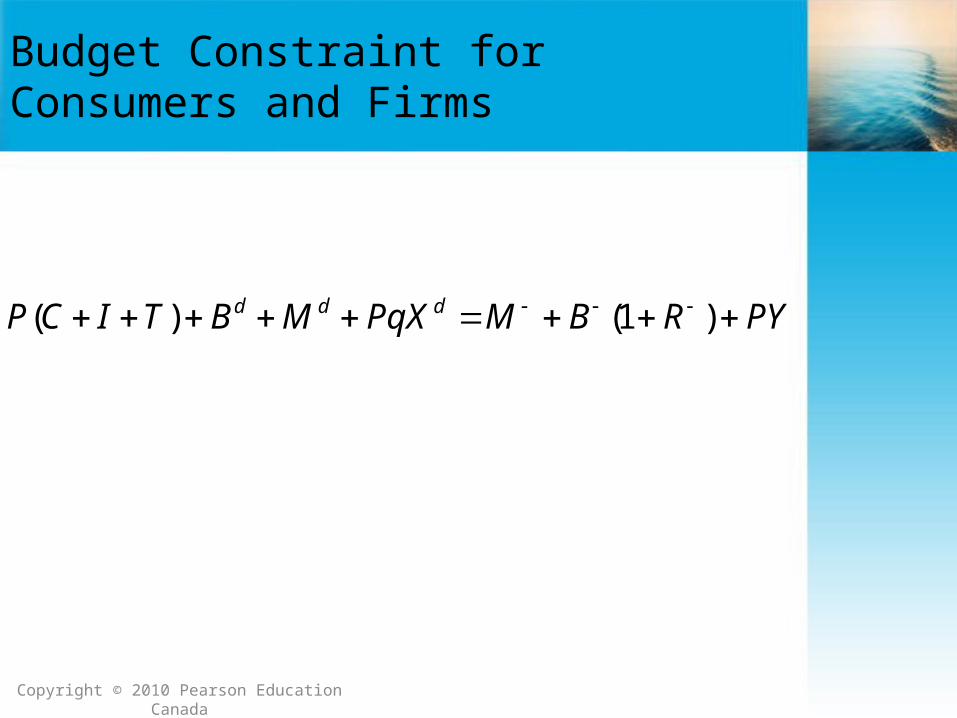

Budget Constraint for Consumers and Firms

PYRBMPqXMBTICP ddd )1()(

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-15

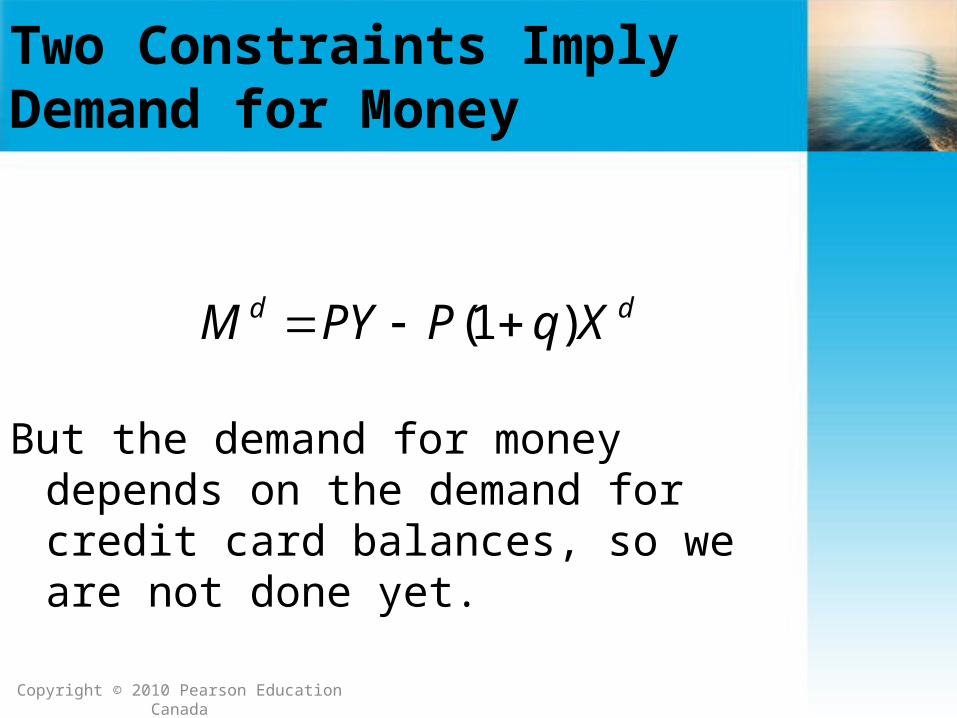

Two Constraints Imply Demand for Money

dd XqPPYM )1(

But the demand for money depends on the demand for credit card balances, so we are not done yet.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-16

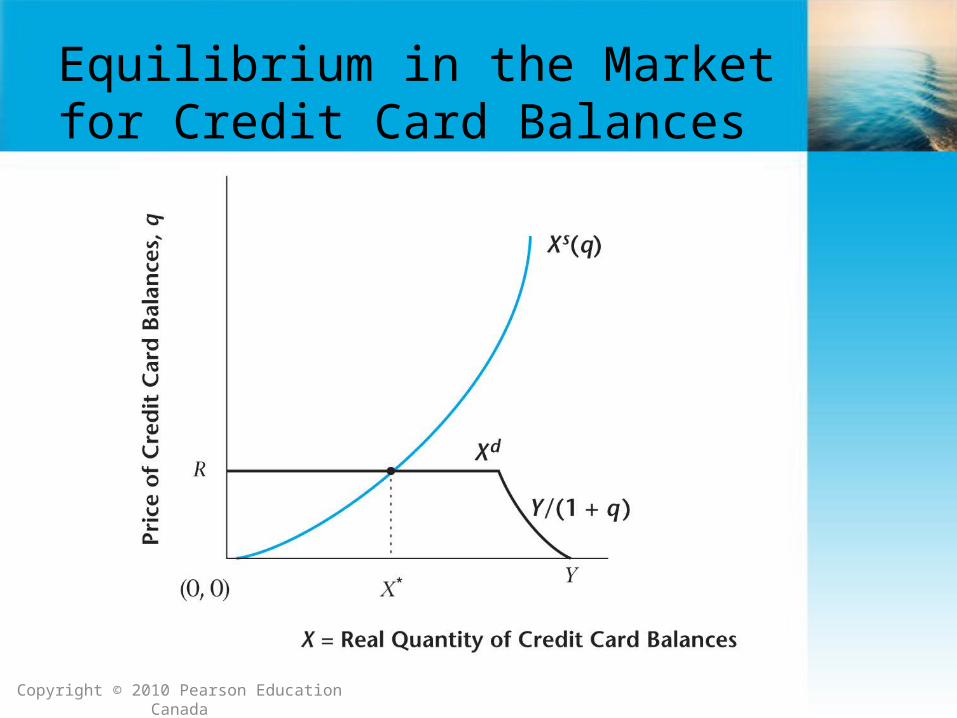

Equilibrium in the Market for Credit Card Balances

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-17

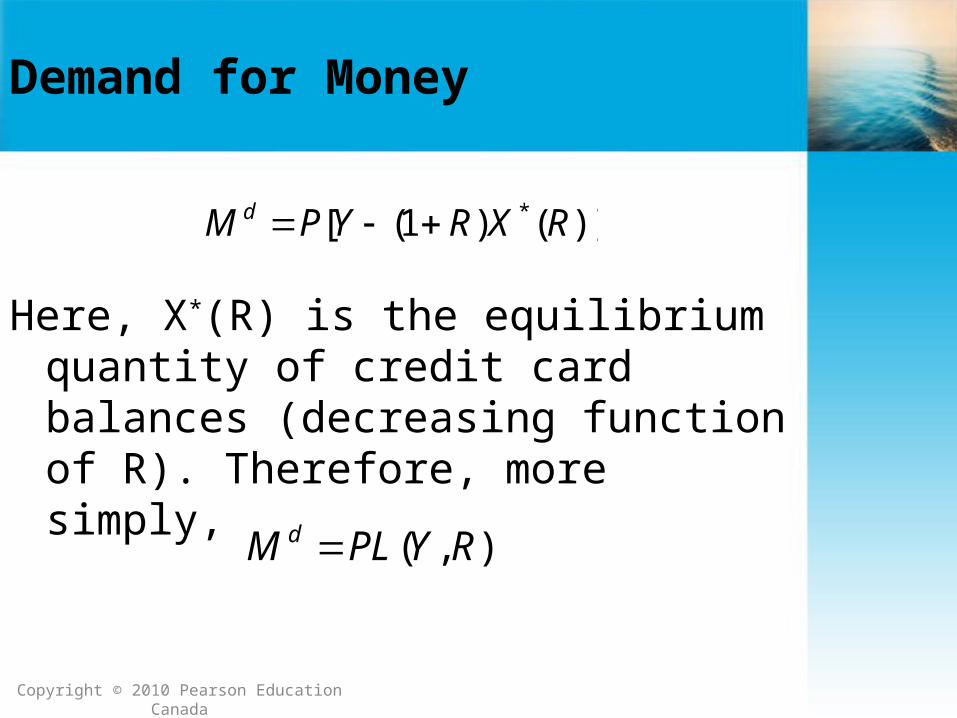

Demand for Money

)]()1([ * RXRYPM d

),( RYPLM d

Here, X*(R) is the equilibrium quantity of credit card balances (decreasing function of R). Therefore, more simply,

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-18

Demand for Money

• Increasing in real income – more currency required as volume of transactions increases.

• Decreasing in the nominal interest rate. The nominal interest rate is the opportunity cost of using currency in transactions – higher R implies greater use of credit in transactions, and less use of currency.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-19

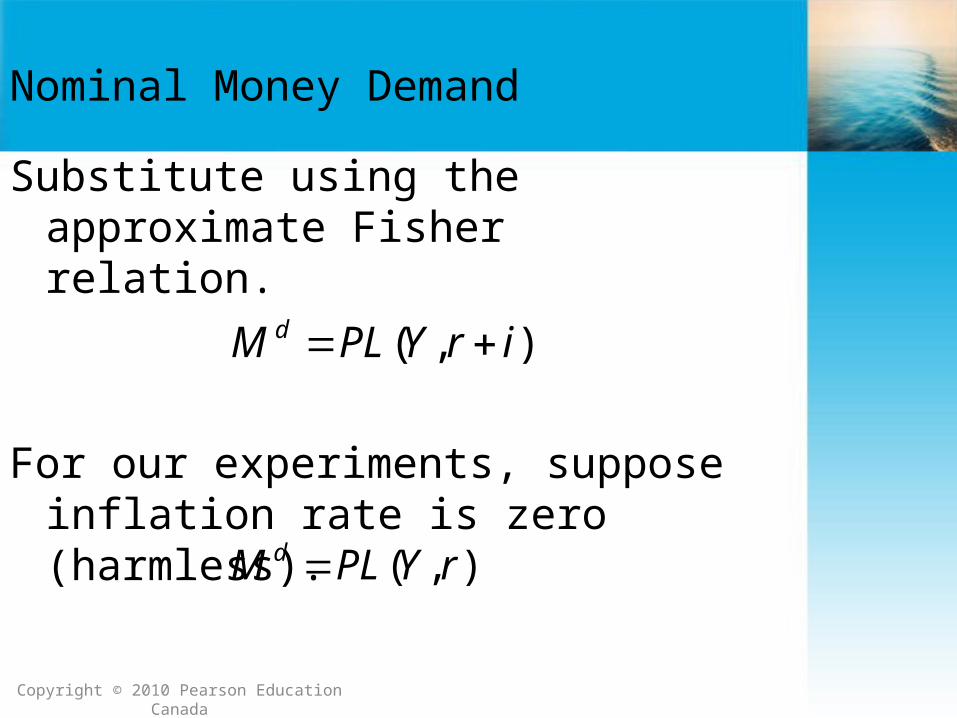

Nominal Money Demand

Substitute using the approximate Fisher relation.

For our experiments, suppose inflation rate is zero (harmless).

),( irYPLM d

),( rYPLM d

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-20

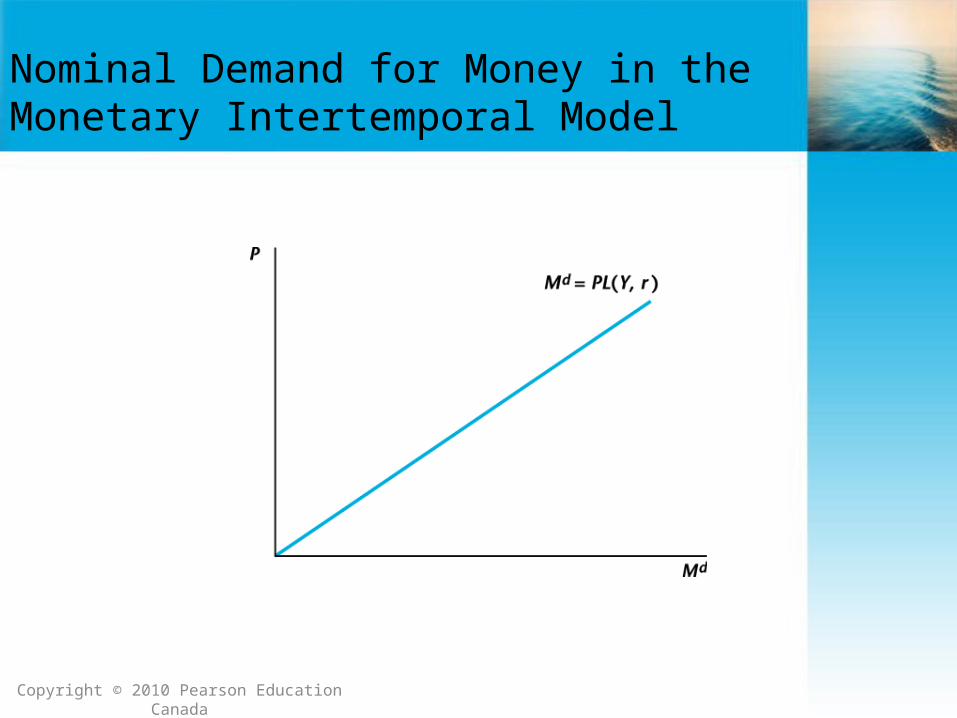

Nominal Demand for Money in the Monetary Intertemporal Model

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-21

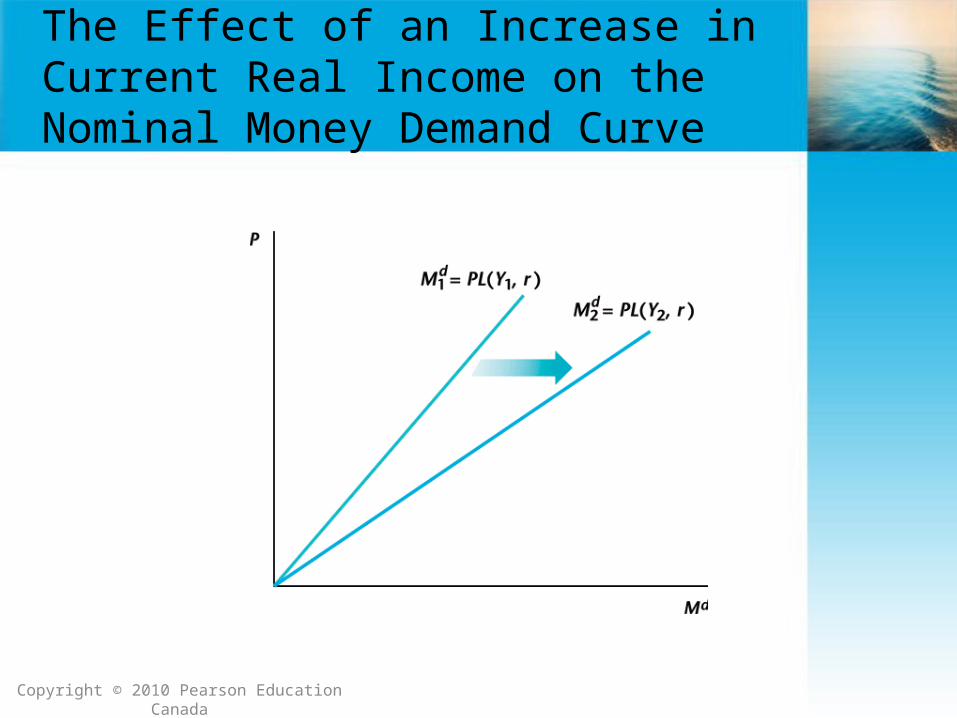

The Effect of an Increase in Current Real Income on the Nominal Money Demand Curve

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-22

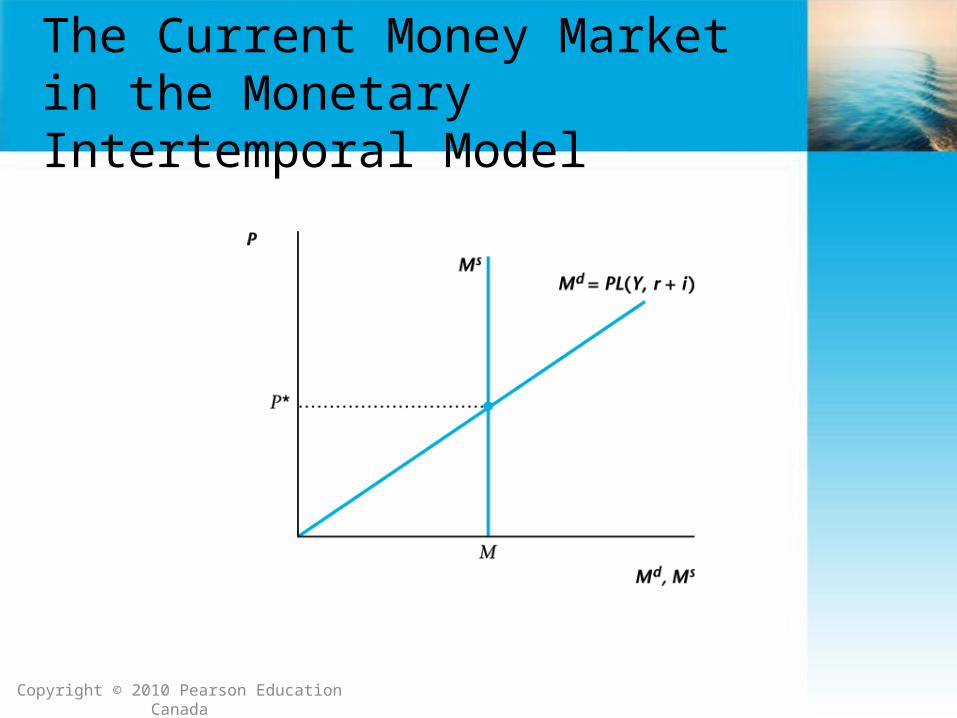

The Current Money Market in the Monetary Intertemporal Model

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-23

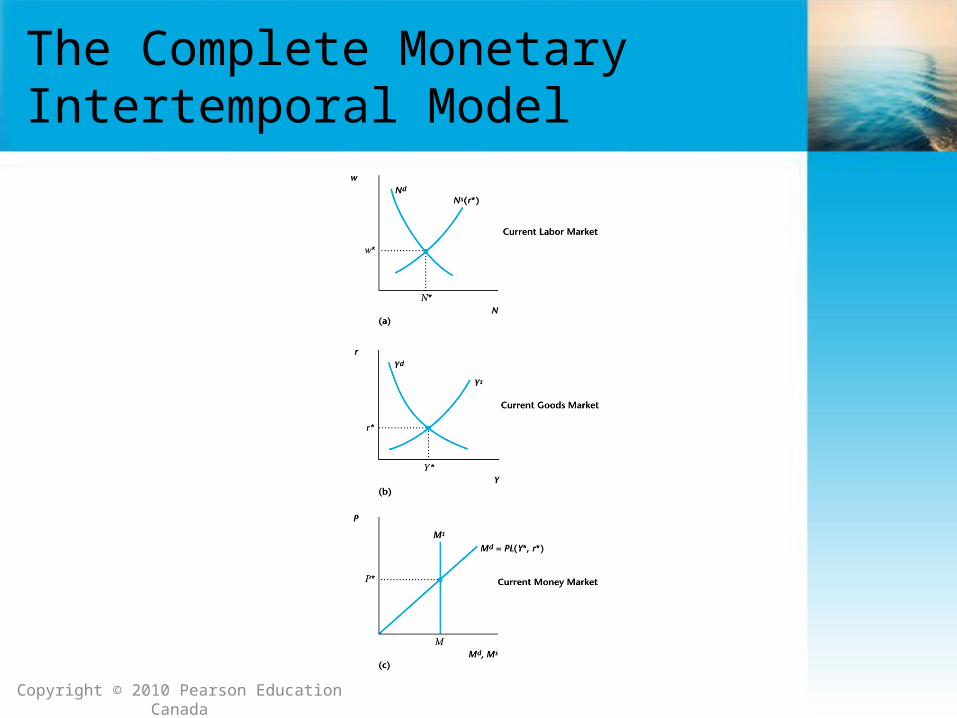

The Complete Monetary Intertemporal Model

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-24

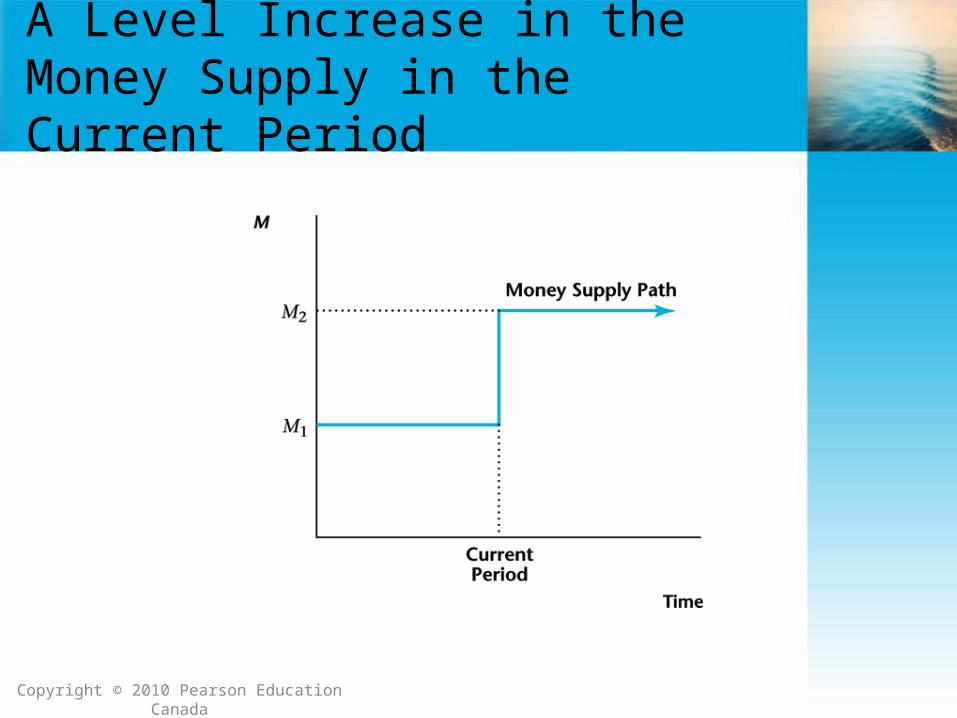

A Level Increase in the Money Supply in the Current Period

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-25

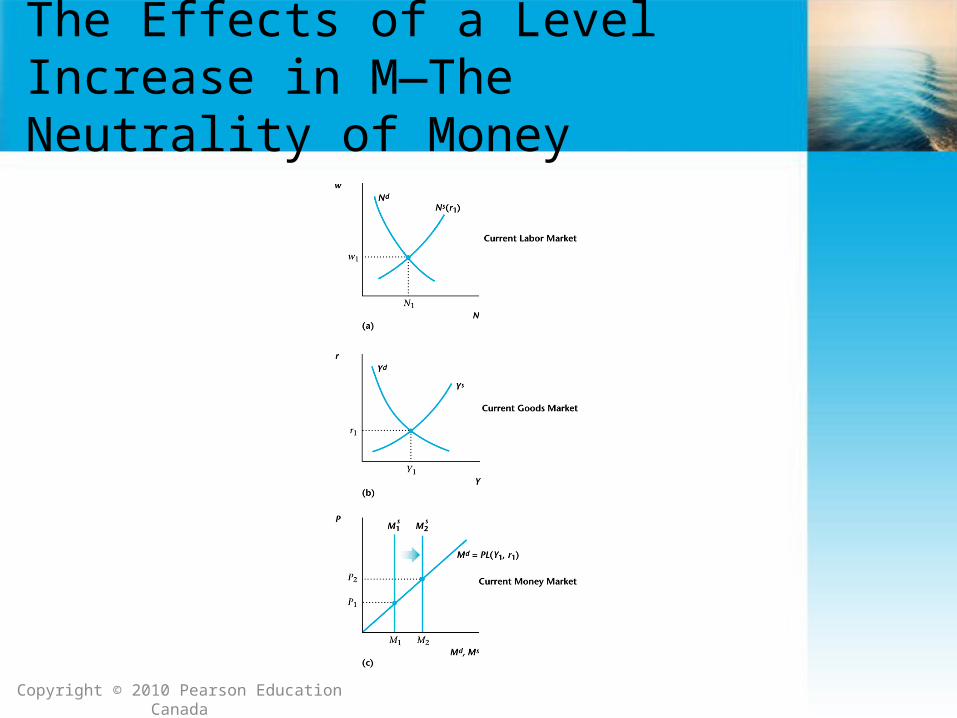

The Neutrality of Money

In the monetary intertemporal model, a level increase in the money supply increases the price level and the nominal wage in proportion to the money supply increase, but has no effect on any real macroeconomic variable.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-26

The Effects of a Level Increase in M—The Neutrality of Money

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-27

Increase in Total Factor Productivity

If z increases, this increases money demand (Y increases and r falls), which causes the price level to fall.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-28

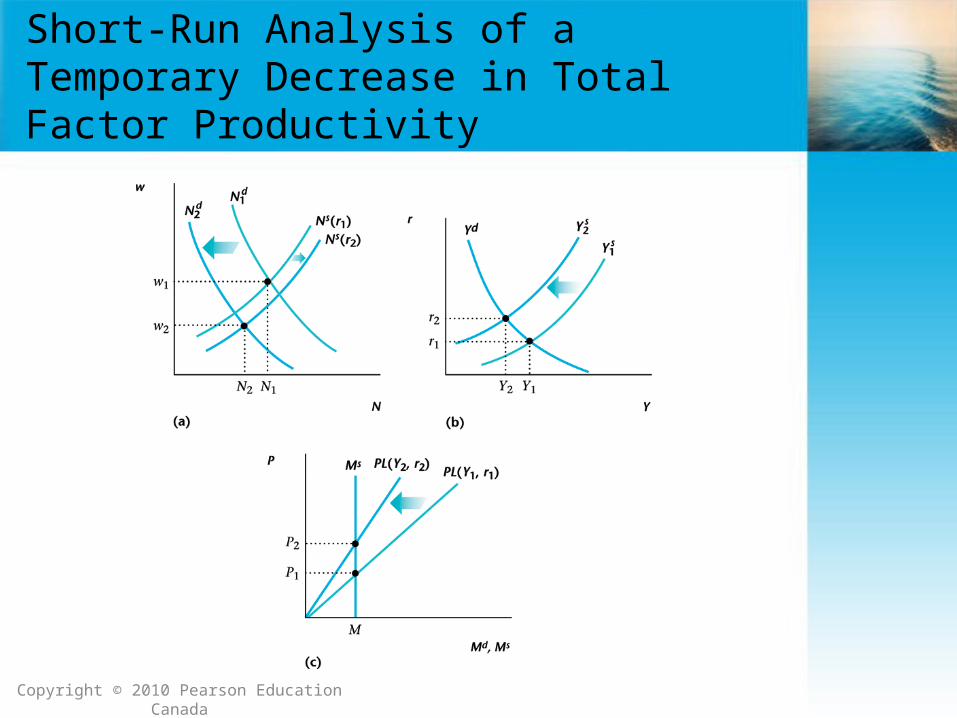

Short-Run Analysis of a Temporary Decrease in Total Factor Productivity

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-29

Shifts in the Demand for Money

• These shifts are important for how monetary policy should be conducted.

• Shifts in the demand for money that occur within a day, week or month (the very short run) are a critical for the central bank.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-30

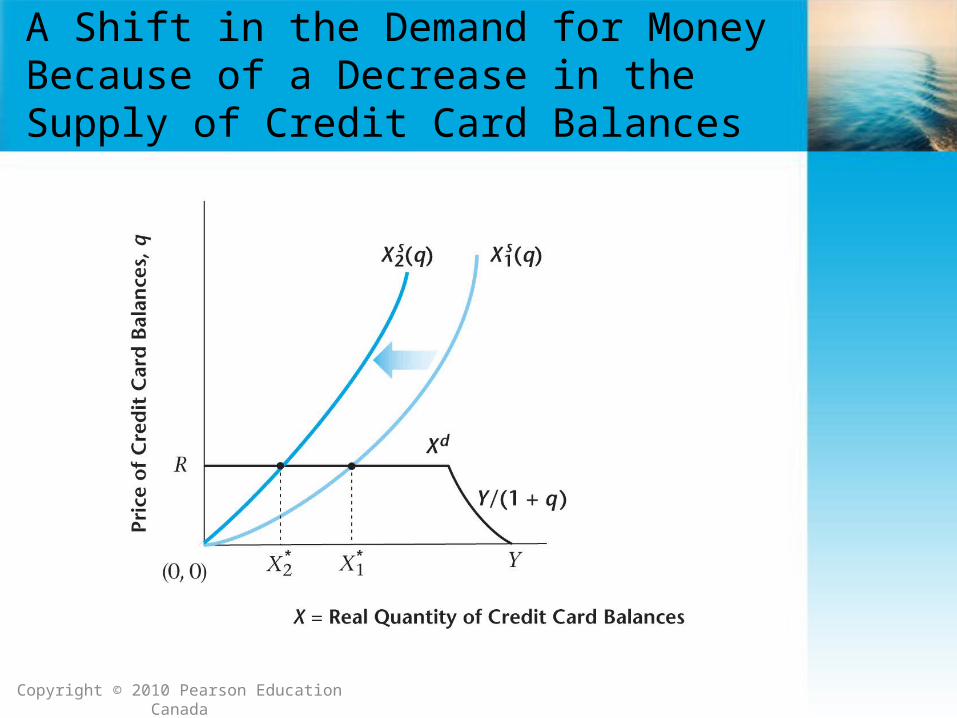

A Shift in the Demand for Money Because of a Decrease in the Supply of Credit Card Balances

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-31

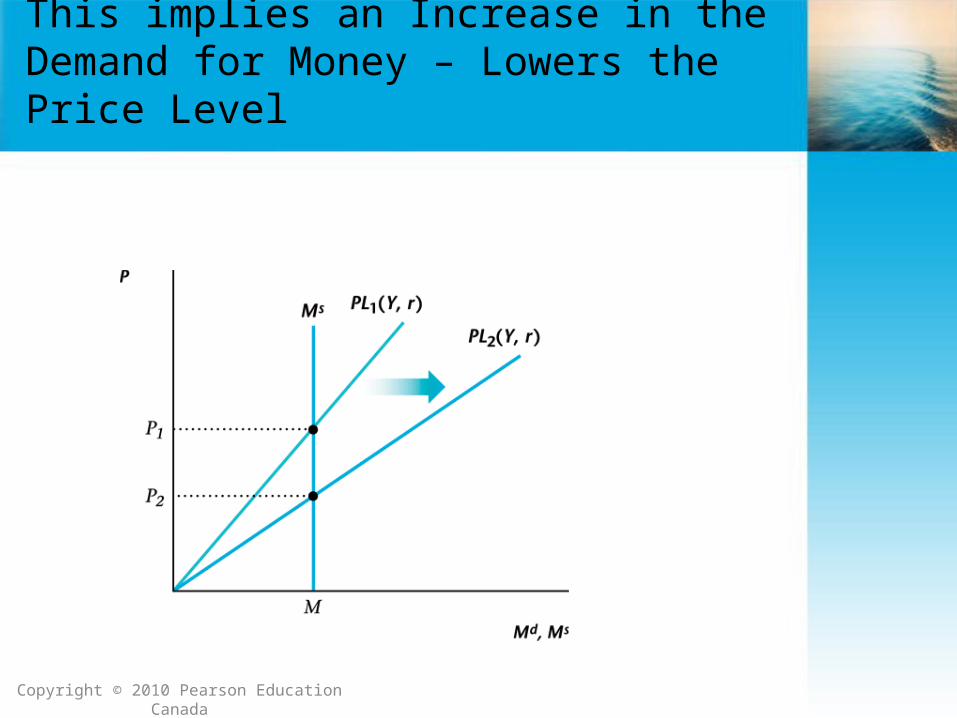

This implies an Increase in the Demand for Money – Lowers the Price Level

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-32

Monetary Policy – Targets and Policy Rules

• Shocks that the central bank is concerned with (in our model): shifts in money demand, output demand, output supply.

• Two alternative policy rules which central banks have adopted: money supply targeting, interest rate targeting.

• Key problem for the central bank: it cannot observe the shocks directly, and does not have timely information on all economic variables.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-33

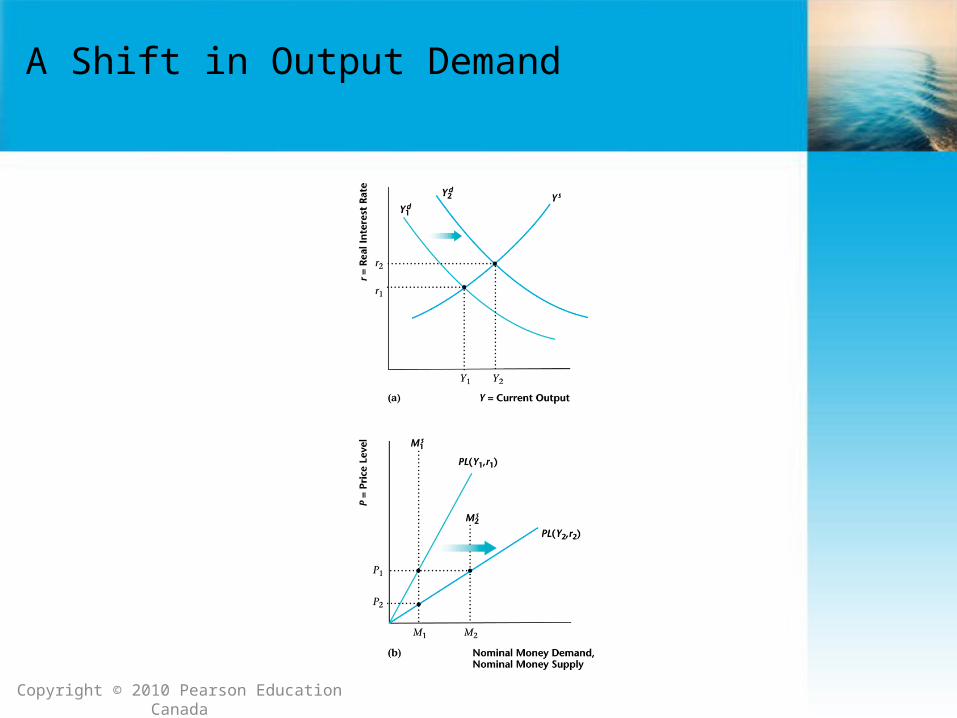

A Shift in Output Demand

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-34

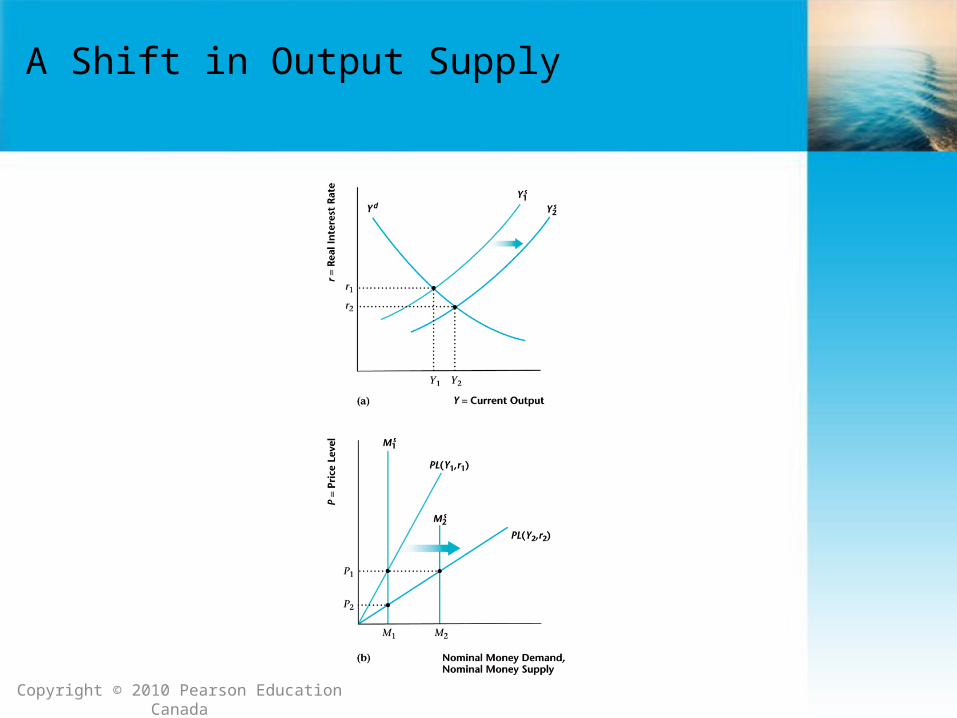

A Shift in Output Supply

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-35

Objective for the Central Bank

• Suppose that the central bank wishes to stabilize the price level – has an inflation target of zero. Our analysis would be the same for any inflation rate target.

• Bank of Canada has an explicit inflation rate target.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-36

Does Money Supply Targeting Achieve Price Stability in the Face of Shocks?

No, with a money demand shock, an output demand shock, or an output supply shock, the price level will change if the money supply is held constant. This is because money demand changes in each case.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-37

Does Interest Rate Targeting Achieve Price Stability in the Face of Shocks?

• Money demand shocks – yes. When money demand increases, money supply increases to accommodate the demand increase. Price level and interest rate remain constant.

• Output demand shocks – no. Interest rate targeting not consistent with price stability.

• Output supply shocks – no. For same reason as for output demand shocks.

Copyright © 2010 Pearson Education Canada

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 5-38

Bank of Canada Policy

• Current Bank of Canada policy procedure: set a target interest rate, and revise this target about every 6 weeks.

• Why does this work? Important shocks within a 6-week horizon tend to be money demand shocks. Output demand and supply shocks are slower to develop. When these shocks occur, this requires changing the target rate.

• Money supply targeting popular in the 1970s and 1980s – generally failed.

Copyright © 2010 Pearson Education Canada