Embed Size (px)

Citation preview

Chapter 1

AppendixTime Value of

Money:The Basics

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

• Answers the questions:– “If I deposit $10,000 today, how much will I

have for a down payment on a house in 5 years?”

– “Will $2,000 saved each year give me enough money when I retire?”

– “How much must I save today to have enough for my children’s education?”

Time Value of Money

App 1-2

Time Value of Money

Basic Principles– A dollar received today is worth more than

a dollar received a year from today

– A dollar that will be received in the future is worth less than a dollar today

– Why?• A dollar today could be saved or invested

• A dollar in the future is uncertain

App 1-3

Time Value of Money

• Definitions• Solving TVM Problems

– Types of Problems• Interest rate basics - Simple interest• Future value - Single amount & Annuity• Present value - Single amount & Annuity• Calculating Loan payments

– Solutions Methods• Formulas• TVM Tables• Financial Calculator• Excel Functions

App 1-4

Basic TVM Definitions

• Future Value (FV)– The increased value of money from interest

earned– The amount to which a current sum will grow

given a certain interest rate and time period– “Compounding”

• Present Value (PV)– The current value of a future amount given a

certain interest rate and time period– “Discounting”

App 1-5

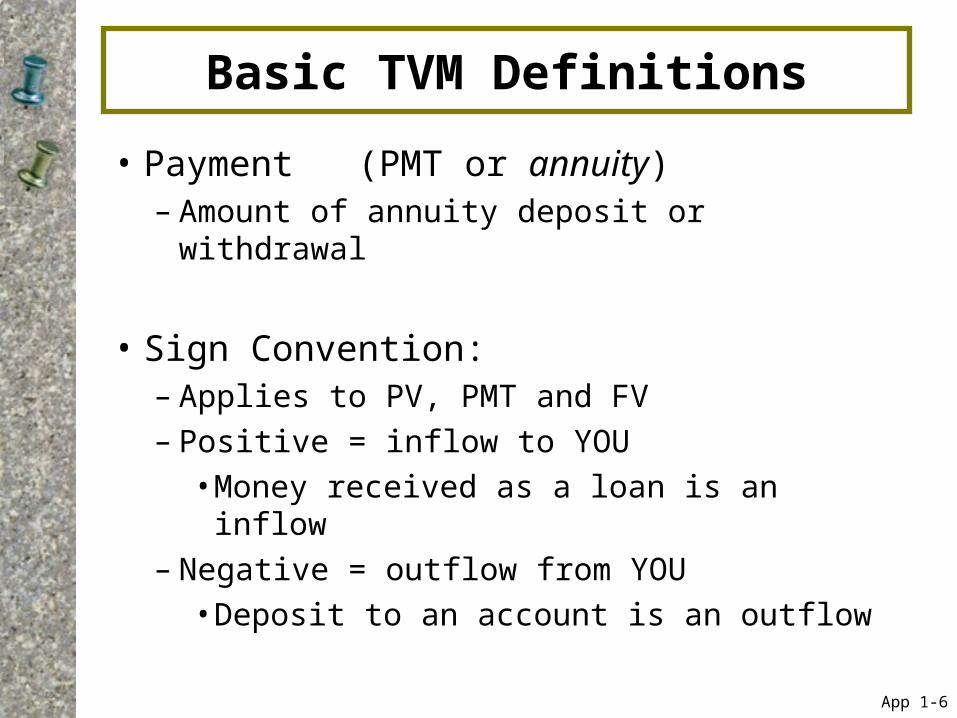

Basic TVM Definitions

• Payment (PMT or annuity)– Amount of annuity deposit or withdrawal

• Sign Convention:– Applies to PV, PMT and FV– Positive = inflow to YOU

• Money received as a loan is an inflow– Negative = outflow from YOU

• Deposit to an account is an outflow

App 1-6

Basic TVM Definitions

• Interest rate (i or I/Y)– Stated as a percent per year– Also called “discount rate”– 12% =

• “0.12” in formulas & in Excel• “12” in financial calculators

App 1-7

Basic TVM Definitions

• Time Periods (n or t)– Expressed in years

• 3 months = “0.25” years• 2 ½ years = “2.5” years

– Interest rate and time period must match• Annual periods annual rate• Monthly periods monthly rate

App 1-8

Single Amount & Annuities

• Single Amount:– A single payment made or received at one

time– Calculator: PMT=0

• Annuity:– Finite series of equal payments that occur at

regular intervals– PMT key used– Sign convention is important

App 1-9

Basic TVM Formulas

Simple Interest: Principal x Rate x Time

Future Value:

Single Amount FV = PV(1 + i)n

Annuity

Present Value

Single Amount

Annuity

i

iPMT n 1)1(

nn iFVPV

i

FVPV

)1(

)1(

ii

PMTn)1(

11

App 1-10

TVM Calculator SolutionsTexas Instruments BA-II Plus

• FV = future value

• PV = present value

• PMT = periodic payment

• I/Y = interest rate

• N = number of periods

One of these MUST be negative

N I/Y PV PMT FV

App 1-11

Texas Instruments BA-II Plus

• I/Y = period interest rate (i)– P/Y must = 1 – Interest is entered as a percent, not a

decimal• 5% interest = “5”, not “0.05”

• Clear the registers before each problem– [2nd] [CLR TVM]– Or reenter each field

App 1-12

TVM with Excel Spreadsheet Functions

=FV(Rate,Nper,Pmt,PV)

=PV(Rate,Nper,Pmt,FV)

=RATE(Nper,Pmt,PV,FV)

=NPER(Rate,Pmt,PV,FV)

=PMT(Rate,Nper,PV,FV)

• Use the formula icon (ƒx)

when you can’t remember

the exact formula

• Calculating interest earned:– Principal = dollar amount of savings– Annual rate of interest – Length of time money on deposit (in years)

• Simple interest:

Time Value of MoneyInterest Rate Basics

Amt in Svgs X

Annual Interest

Rate

Time Period InterestX =

App 1-14

You borrow $1,000 at 5% annual interest for 1 year:

Principal = $1,000

Interest rate = 5% = .05

Time period = 1

Interest Rate BasicsExample A

$50$1,000 X .05 1X =

App 1-15

You deposit $750 at 8% per year for 9 months:

Principal = $750Interest rate = 8%Time period = 9/12 = .75

Interest Rate BasicsExample B

$45$750 X .08 0.75X =

App 1-16

Principal = $750

Interest rate = 8%

Time period = 9/12 = .75

Interest Rate BasicsExample B – Calculator*

Calculator Solution Keystrokes .75 N 8 I/Y -750 PV 0 PMT CPT FV = 794.56 – 750 = 44.56 ≈ 45

*Calculator solutions match the TI Business Analyst II+. Keystroke adjustments may need to be made for other financial calculators

App 1-17

Interest Rate BasicsExample B – Calculator

Calculator Solution .75 N 8 I/Y -750 PV ** 0 PMT CPT FV = 794.56 – 750 = 44.56 ≈ 45

** Remember: when using a financial calculator, either PV or FV must be negative.

• Outflows (from you) are negative• Inflows (to you) are positive• Depositing money in an account is an outflow

App 1-18

Future Value of a Single Amount

• Amount to which current savings will increase• = Original amount + compounded interest• = Compounding

• Formula Solution:

• Table Solution:

• Calculator Solution: N I/Y PV PMT CPT FV

• Excel Function: FV(Rate,Nper,Pmt,PV )

niPVFV )1(

Factor) Table(PVFV

App 1-19

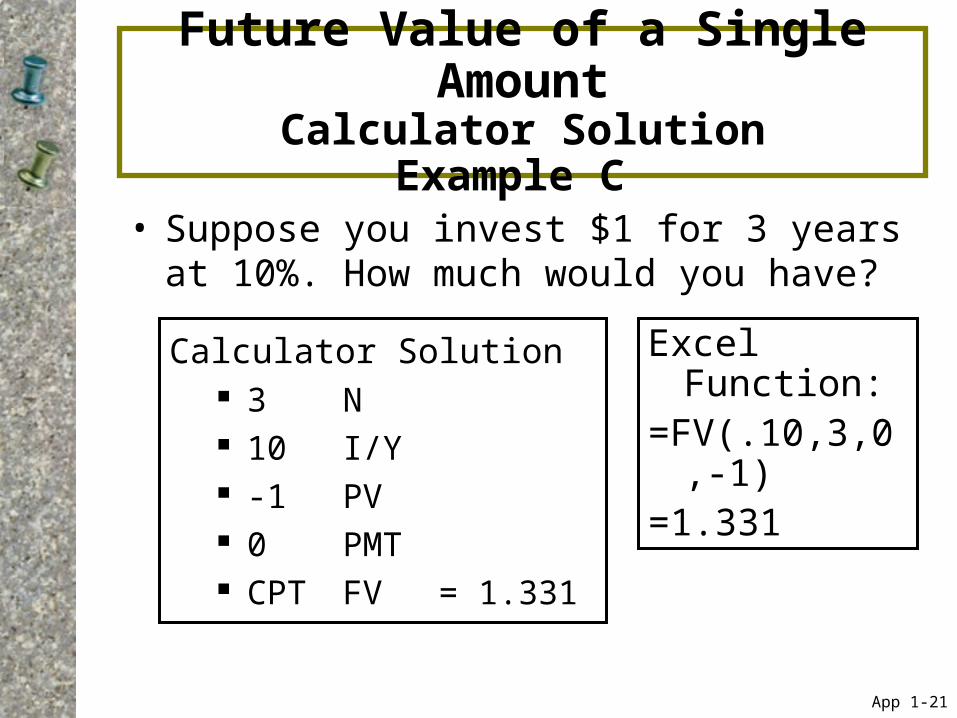

Future Value of a Single AmountFormula & TVM Table Solutions

Example C

• Suppose you invest $1 for 3 years at 10%• How much would you have?

Formula Solution:

FV =PV(1+i)n

=1(1.10)3

=1(1.331)

=1.331

TVM Tables Solution:

Exhibit 1-A

Periods = 3

Rate = 10%

Factor = 1.331

FV = PV(Factor)

FV = 1(1.331)

FV = 1.331App 1-20

Future Value of a Single Amount

Calculator SolutionExample C

• Suppose you invest $1 for 3 years at 10%. How much would you have?

Calculator Solution 3 N 10 I/Y -1 PV 0 PMT CPT FV = 1.331

App 1-21

Excel Function:=FV(.10,3,0,-1)=1.331

Future Value of a Single AmountFormula & TVM Tables

Example D

• Your savings of $400 earns 12% compounded monthly (=1% per month)

• How much would you have after 18 months?• Table Hint: Use 1% and 18 periods

Formula Solution:

FV=PV(1+i)n

=400(1.01)18

=400(1.196)

=478.46

TVM Tables Solution:

Exhibit 1-A

Periods = 18

Rate = 1%

Factor = 1.196

FV = 400(1.196)

FV = 478.40

App 1-22

Future Value of a Single Amount

Calculator SolutionExample D

• Suppose you invest $400 for 18 months at 12% compounded monthly. How much would you have?

Calculator Solution 18 N 1 I/Y -400 PV 0 PMT CPT FV = 478.46

App 1-23

Excel Function:=FV(.01,18,0,-400)=478.46

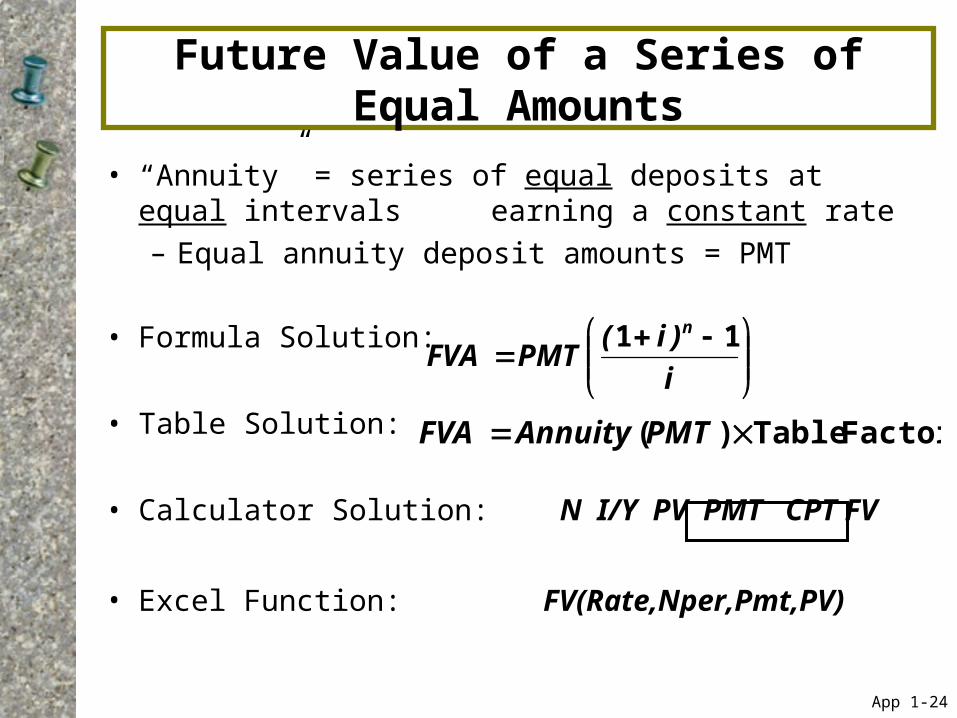

Future Value of a Series of Equal Amounts

• “Annuity” = series of equal deposits at equal intervals earning a constant rate

– Equal annuity deposit amounts = PMT

• Formula Solution:

• Table Solution:

• Calculator Solution: N I/Y PV PMT CPT FV

• Excel Function: FV(Rate,Nper,Pmt,PV)

i

)i(PMTFVA

n 11

Factor Table)( PMTAnnuityFVA

App 1-24

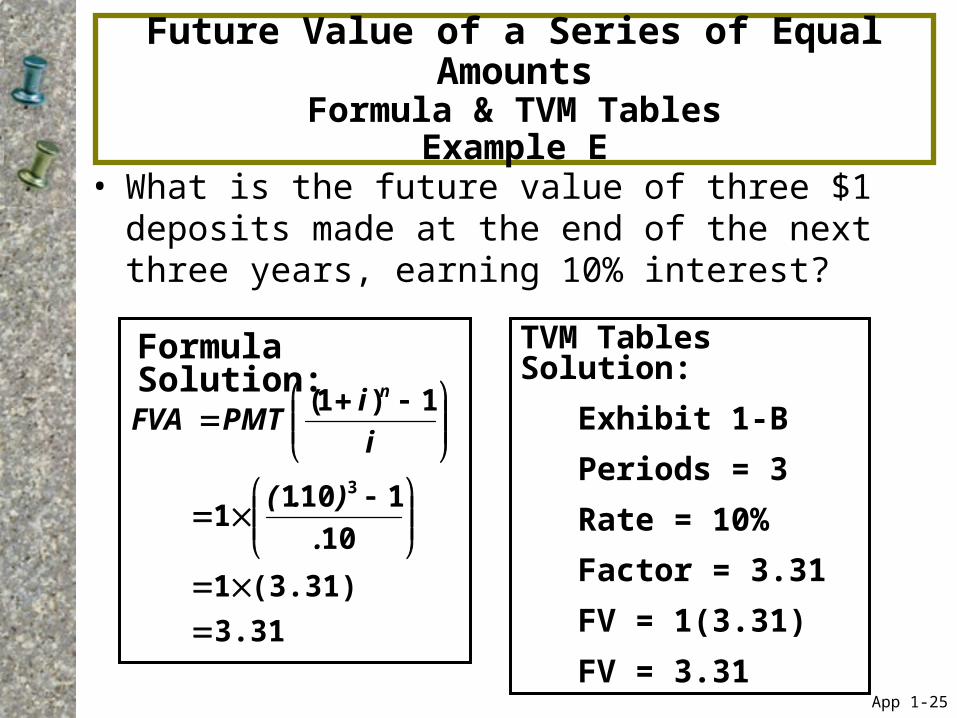

Future Value of a Series of Equal Amounts

Formula & TVM TablesExample E

• What is the future value of three $1 deposits made at the end of the next three years, earning 10% interest?

Formula Solution:

TVM Tables Solution:

Exhibit 1-B

Periods = 3

Rate = 10%

Factor = 3.31

FV = 1(3.31)

FV = 3.313.31

(3.31)1

10

11011

1)1(

3

.

).(

i

iPMTFVA

n

App 1-25

Future Value of a Series of Equal Amounts

Calculator SolutionExample E

Calculator Solution 3 N 10 I/Y 0 PV -1 PMT* CPT FV = 3.31

* Note that the PMT value is negative since it is an outflow/deposit.

App 1-26

Excel Function:=FV(.10,3,-1,0)=3.31

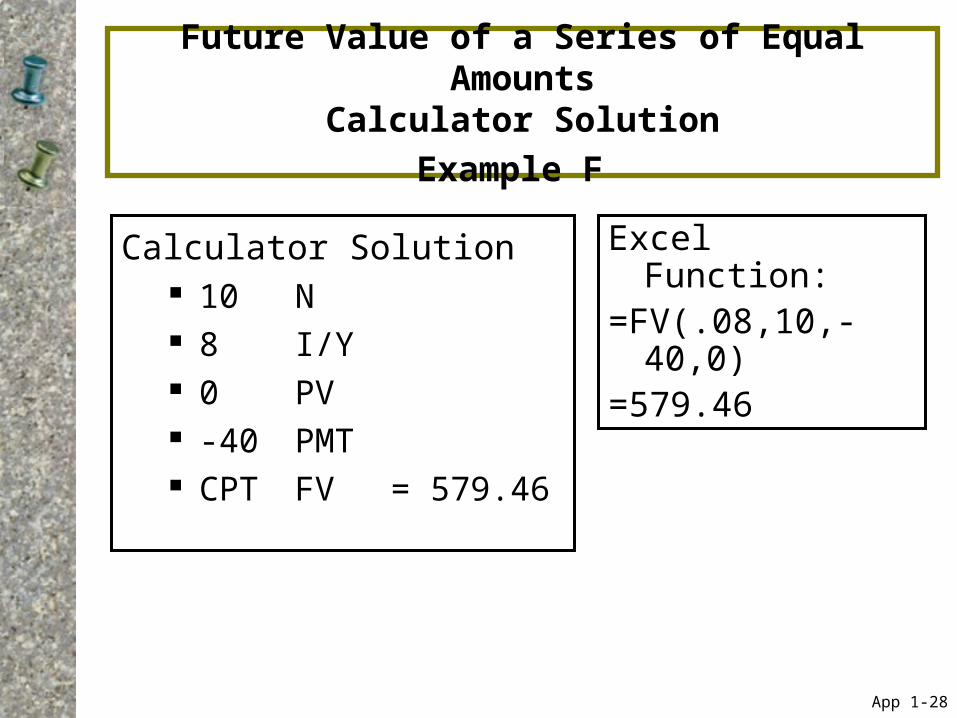

Future Value of a Series of Equal AmountsFormula & TVM Tables

Example F

• What is the future value of ten $40 deposits earning 8% compounded annually?

Formula Solution:

TVM Tables Solution:

Exhibit 1-B

Periods = 10

Rate = 8%

Factor = 14.487

FV = 40(14.487)

FV = 579.48579.46

(14.487)40

08

108140

1)1(

10

.

).(

i

iPMTFVA

n

App 1-27

Future Value of a Series of Equal Amounts

Calculator SolutionExample F

Calculator Solution 10 N 8 I/Y 0 PV -40 PMT CPT FV = 579.46

App 1-28

Excel Function:=FV(.08,10,-40,0)=579.46

Present ValueSingle Amount - Basic Equation

FV = PV(1 + i)n

• Rearrange to solve for PV

• “Discounting” = finding the present value of one or more future amounts

n

n

)i(FVPV

)i(

FVPV

1

1

App 1-29

Present Value of a Single Amount

• Formula Solution:

• Table Solution:

• Calculator Solution: N I/Y PMT FV CPT PV

• Excel Function: =PV(Rate,Nper,Pmt,FV)

ni)(1

FV

)1(

niFVPV

Factor) Table(FVPV

App 1-30

Present Value of a Single AmountFormula & TVM Tables Example

Example G

• What is the present value of $1 to be received in 3 years at a 10% interest rate?

Formula Solution:

PV =FV/(1+i)n

=1/(1.10)3

=1*(.7513)

=0.7513

TVM Tables Solution:

Exhibit 1-C

Periods = 3

Rate = 10%

Factor = .751

PV = FV*(Factor)

PV = 1*(0.751)

PV = 0.751

App 1-31

Present Value of a Single Amount

Example GFormula Solution: PV =FV/(1+i)n

=1/(1.10)3=1*(0.7513)=0.7513

TVM Tables Solution:

Exhibit 1-C

Periods = 3 (down left column)

Rate = 10% (across top)

Factor = .751

PV = FV(Factor)

PV = 1(0.751)

PV = 0.751

Calculator Solution 3 N 10 I/Y CPT PV = -.7513 0 PMT 1 FV

App 1-32

Excel Function:=PV(.10,3,0,1)= -0.75

Present Value of a Single Amount

Example H

Formula Solution: PV=FV/(1+i)n

=300/(1.05)14

=300/(1.9799)=151.52

TVM Tables Solution:

Exhibit 1-C

Periods = 14 (down left column)

Rate = 5% (across top)

Factor = .505

PV = FV(Factor)

PV = 300 x (0.505)

PV = $151.50

Calculator Solution 14 N 5 I/Y CPT PV = -151.52 0 PMT 300 FV

You want to have $300 seven years from now. Your savings earns 10% compounded semiannually. How much must you deposit today?

App 1-33

Excel Function:=PV(.05,14,0,300) = -151.52

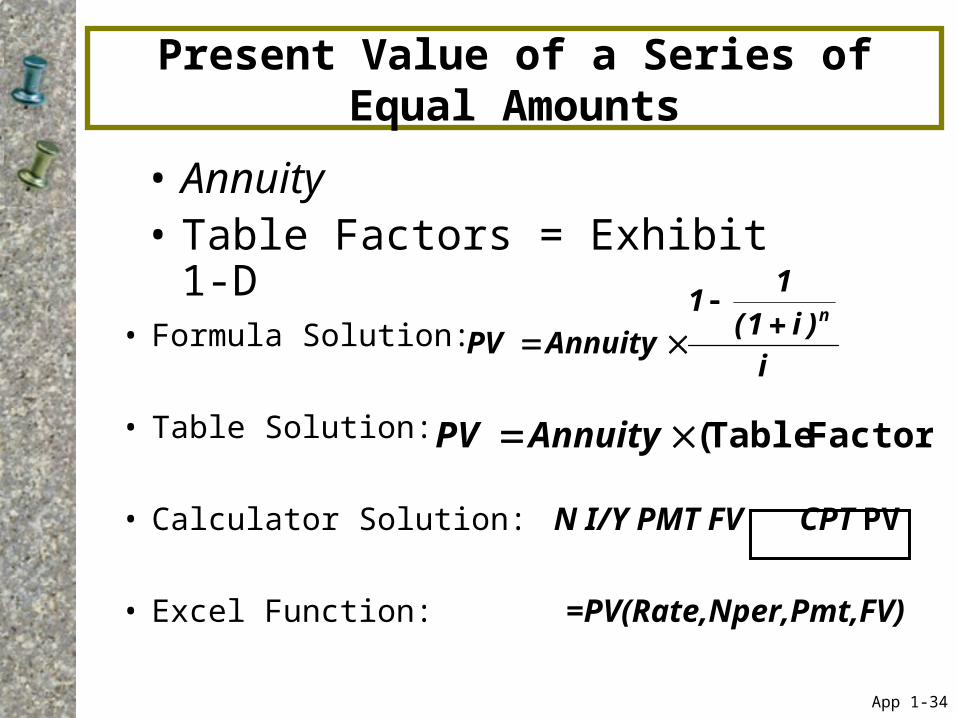

Present Value of a Series of Equal Amounts

• Formula Solution:

• Table Solution:

• Calculator Solution: N I/Y PMT FV CPT PV

• Excel Function: =PV(Rate,Nper,Pmt,FV)

i)i1(

11

AnnuityPVn

Factor) Table(AnnuityPV

• Annuity• Table Factors = Exhibit 1-D

App 1-34

Present Value of an AnnuityExample I

• You wish to withdraw $1 at the end of each of the next 3 years. (= an Inflow)

• The account earns 10% compounded annually.• How much do you need to deposit today to be able to

make these withdrawals?

49.2$10.

)10.1(1

11

3

PV

3 N; 10 I/Y; 1 PMT; CPT PV = -2.48685FV 0

Exhibit 1-D: Row 3, column 10%

Factor = 2.487

PV = PMT*(Factor) = 1*(2.487)

PV = $2.49

App 1-35

Excel Function:=PV(.10,3,1,0) = -2.49

Present Value of an AnnuityExample J

• You wish to withdraw $100 at the end of each of the next 10 years. (Inflow)

• The account earns 14% compounded annually.• How much do you need to deposit today to be able to

make these withdrawals?

61.521$14.

)14.1(1

11

10

PV

10 N; 14 I/Y; 100 PMT; CPT PV = -521.61FV 0

Exhibit 1-D:

Factor = 5.216

PV = PMT*(Factor) = 100*(5.216)

PV = $521.60App 1-36

Excel Function:=PV(.14,10,100,0) = -521.61

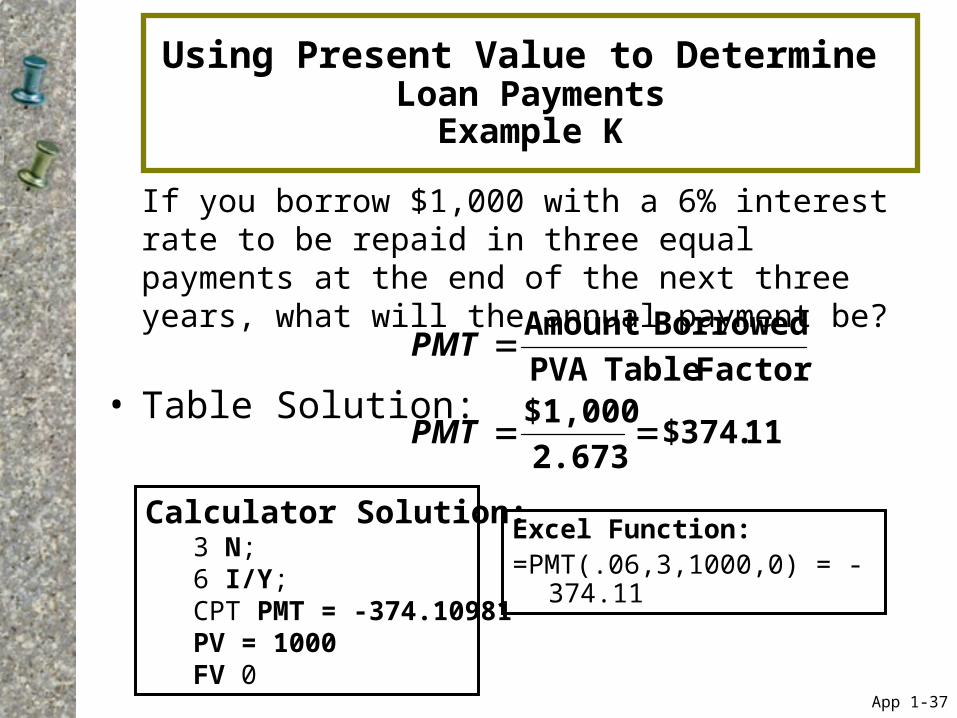

Using Present Value to Determine Loan Payments

Example K

If you borrow $1,000 with a 6% interest rate to be repaid in three equal payments at the end of the next three years, what will the annual payment be?

• Table Solution:

11.374$2.673

$1,000Factor TablePVA

BorrowedAmount

PMT

PMT

Calculator Solution:3 N; 6 I/Y; CPT PMT = -374.10981 PV = 1000FV 0

App 1-37

Excel Function:=PMT(.06,3,1000,0) = -374.11