Embed Size (px)

Citation preview

Chapter 08 - Process-Costing Systems

Chapter 08

Process-Costing Systems

True / False Questions

1. In processcosting, material costs are not traced to individual units of output, as in job costing. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 1

2. Companies that produce products in continuousflow production, such as paint and cereals use processcosting. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 1

3. Processcosting is used to help set selling prices, but is not used to determine inventory values for financial accounting. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 2

8-1

Chapter 08 - Process-Costing Systems

4. Conversion costs of resources used by processes generally occur at the unitlevel of output. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 2

8-2

Chapter 08 - Process-Costing Systems

5. Conversion costs of resources used by processes can apply to all levels of the cost hierarchy. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 2

6. Temporary labor is normally a batchlevel conversion cost. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 2

7. In process costing, material costs are traced to individual units of output. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

8. The first step in the process costing system is to compute the number of equivalent units produced. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

8-3

Chapter 08 - Process-Costing Systems

9. The first step in the process costing system is to summarize the physical flow of units. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

10. The basic cost flow model to help account for units processed during the period is beginning inventory plus transfers in minus transfers out equals ending inventory. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

11. Equivalent units represent the amount of physical units transferred to finished goods. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

12. Equivalent units represent the amount of work actually accomplished, expressed as the number of units that could have been fully completed. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

8-4

Chapter 08 - Process-Costing Systems

13. In process costing, two halffinished units equal one equivalent unit. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 3

14. Cost per equivalent unit is calculated by dividing the number of equivalent units by the total cost. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3

15. Weightedaverage costing combines the cost in beginning inventory with costs incurred during the period to compute unit costs. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 4

16. For weightedaverage costing, it is not necessary to know which of the finished units werefrom the beginning inventory in order to compute the number of finished equivalent units. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

8-5

Chapter 08 - Process-Costing Systems

17. Weightedaverage process costing provides detailed information to management to assess worker productivity for the current period. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

18. Overstating the percentage of completion of the ending inventory under weightedaverage processcosting will result in overstated profits for the period. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 4

19. Under weightedaverage processcosting, all costs of material and conversion are averaged together in determining cost per finished equivalent unit. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

20. If the degree of completion of the ending inventory is underestimated, a company's profitswill be overstated for the period. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 4

8-6

Chapter 08 - Process-Costing Systems

21. Prior department costs should be excluded from a department's costs for purposes of performance evaluations. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 5

22. In a multiple department process, the costs of units transferred out of one department and into another are called prior department costs. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 5

23. Prior department process costs are always assigned an equivalent unit percent complete of 0%. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 5

24. The cost of normal spoilage should be written off as an expense account during the accounting period. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

8-7

Chapter 08 - Process-Costing Systems

25. The cost of abnormal spoilage should be written off as a cost of the period rather than added to inventory. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 6

26. Companies that have a zero defect policy might treat all spoilage as abnormal. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

27. The entry to account for abnormal spoilage consists of a debit to workinprocess inventory and a credit to an expense account. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

28. Lost units are goods that evaporate or otherwise disappear during a production process. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 6

8-8

Chapter 08 - Process-Costing Systems

29. All lost units should be written off as an expense for the period. FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

30. Total costs to be accounted for are the same for both the weightedaverage and FIFO methods. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 8

31. The weightedaverage method is usually more accurate in matching actual costs to the period of production. (Appendix) FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

32. Only the weightedaverage method is allowed for external financial reporting. (Appendix) FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 8

8-9

Chapter 08 - Process-Costing Systems

33. If both the number of physical units in the beginning and ending inventory and their degrees of completion are equal, then the number of units started will equal the number of units transferred out. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 8

34. If there are no units in beginning inventory, weightedaverage and FIFO will result in the same number of finished equivalent units. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

35. If there are no units in ending inventory, weightedaverage and FIFO will result in the same number of finished equivalent units. (Appendix) FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

36. If materials are added at the end of the process and assuming no spoilage, under FIFO process costing, the equivalent units will always be equal to the number of units transferred out during the period. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-10

Chapter 08 - Process-Costing Systems

37. The FIFO method differs from the weightedaverage method in that the FIFO method allocates costs based on whole units whereas the weightedaverage method uses equivalent units. (Appendix) FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

38. The weightedaverage method differs from the FIFO method in that the weightedaverage method does not consider the degree of completion for the beginning workinprocess inventory whereas FIFO does. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

39. Prior process costs are always assigned an equivalent unit percent complete of 100% under both the FIFO and weightedaverage methods. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 8

40. In computing the cost per equivalent unit, the weightedaveragemethod considers current costs only, while the FIFO Method considers prior period costs and current costs. (Appendix) FALSE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

8-11

Chapter 08 - Process-Costing Systems

41. Under FIFO processcosting, if materials are added at the end of the process, the materialsportion of the ending inventory of workinprocess will always be assigned a cost of zero. TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

42. In operation costing, direct materials for each work order or batch passing through a particular operation are different, while conversion costs are the same. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 9

43. A company using operation costing typically uses different materials for products that pass through the same operations. (Appendix) TRUE

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 9

Multiple Choice Questions

Use the following to answer questions 4445:Diamond Company has a process costing system using the weightedaverage cost flow method. All materials are introduced at the beginning of the process in Department 1. The following information is available for the month of January:

8-12

Chapter 08 - Process-Costing Systems

8-13

Chapter 08 - Process-Costing Systems

44. The number of equivalent units of production for material costs for the month of January is: A. 28,000b. 23,200c. 24,000d. 22,000

Units finished (22,000) + Ending WIP (6,000) = 28,000

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

45. The number of equivalent units of production for conversion costs for the month of January is: a. 21,600b. 24,000c. 22,000D. 23,200

Units finished (22,000) + Ending WIP (6,000 x .2) = (22,000 + 1,200) = 23,200

AACSB: Reflective ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

46. Under what conditions will the FIFO method produce the same cost of goods manufactured as the weightedaverage method? (Appendix) a. When there is no ending inventoryb. When the beginning and ending inventories are both 50% completeC. When there is no beginning inventoryd. When the beginning and ending inventories are equal

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: EasyLearning Objective: 8

8-14

Chapter 08 - Process-Costing Systems

8-15

Chapter 08 - Process-Costing Systems

Use the following to answer questions 4750:Carlton Manufacturing Company has the following information available for its processcosting system for the month of May in the finishing department. The finishing department is the second of a multipledepartment manufacturing plant. Materials are added at the end of the process in finishing.

Beginning inventory is 30% complete as to conversion costs; ending inventory is 80% complete as to conversion costs.

47. The number of units transferred out of the finishing department is: A. 250,000b. 50,000c. 300,000d. 100,000

Beginning inventory + Transferredin = Transferred Out + Ending inventory

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 4Learning Objective: 5

48. The number of finished equivalent units of materials under weightedaverage is: a. 300,000B. 250,000c. 200,000d. 50,000

Units finished: 250,000 FEU; Ending inventory is 0% complete for materials

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4Learning Objective: 5

8-16

Chapter 08 - Process-Costing Systems

8-17

Chapter 08 - Process-Costing Systems

49. The cost per finished equivalent unit for materials under weightedaverage is: a. $0.75b. $2.00C. $0.90d. $0.94

$225,000/250,000 FEU = $0.90

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

50. The value assigned to the materials portion of ending inventory under weightedaverage is: a. $140,000b. $100,000c. $45,000D. $0

$0 (Materials are added at the end of the process; therefore, ending inventory has no material)

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

51. The total cost of the units transferred out under weightedaverage is: a. $225,000B. $1,190,500c. $1,365,000d. $174,500

Finished equivalent units: Materials Conversion Prior Department

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

8-18

Chapter 08 - Process-Costing Systems

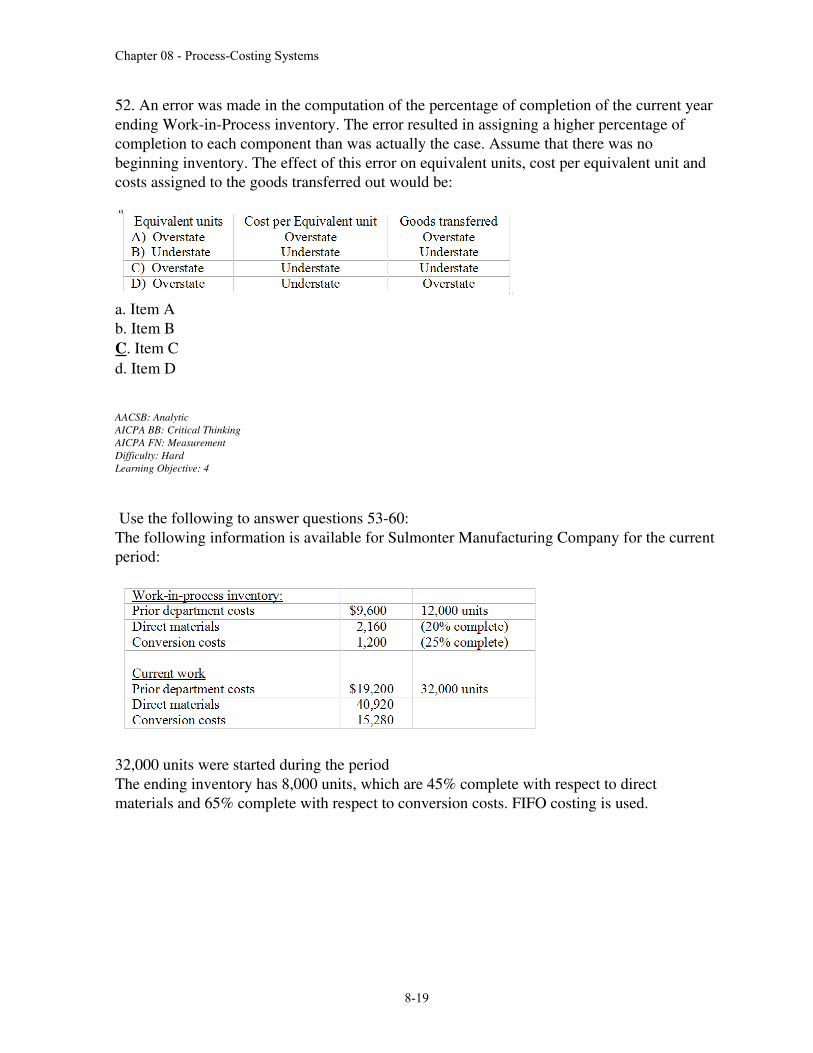

52. An error was made in the computation of the percentage of completion of the current year ending WorkinProcess inventory. The error resulted in assigning a higher percentage of completion to each component than was actually the case. Assume that there was no beginning inventory. The effect of this error on equivalent units, cost per equivalent unit and costs assigned to the goods transferred out would be:

a. Item Ab. Item BC. Item Cd. Item D

AACSB: AnalyticAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 4

Use the following to answer questions 5360:The following information is available for Sulmonter Manufacturing Company for the currentperiod:

32,000 units were started during the periodThe ending inventory has 8,000 units, which are 45% complete with respect to direct materials and 65% complete with respect to conversion costs. FIFO costing is used.

8-19

Chapter 08 - Process-Costing Systems

53. What are the total units to be accounted for? (Appendix A) a. 32,000b. 40,000C. 44,000d. 52,000

12,000 + 32,000 = 44,000

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 7

54. How many units were started and completed during the current period? (Appendix A) a. 20,000B. 24,000c. 32,000d. 40,000

Units completed less units in beginning inventory (36,000 12,000)

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

55. What are the equivalent units produced for materials using FIFO? (Appendix A) a. 29,200b. 30,000C. 37,200d. 38,000

Beginning inventory (12,000 x .8) 9,600

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-20

Chapter 08 - Process-Costing Systems

56. What are the equivalent units produced for conversion costs using FIFO Costing? (Appendix A) a. 32,200b. 35,800c. 36,000D. 38,200

Beginning inventory (12,000 x .75) 9,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

57. What is the prior department cost per equivalent unit, using FIFO costing (rounded to the nearest cent?) (Appendix A) A. $0.60b. $0.80c. $0.655d. $0.50

Current period cost $19,200

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 5Learning Objective: 7

58. What is the material cost per equivalent unit using FIFO costing? (Appendix A) a. $1.16B. $1.10c. $1.35d. $1.09

Current period cost $40,920

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-21

Chapter 08 - Process-Costing Systems

8-22

Chapter 08 - Process-Costing Systems

59. What is the total cost of the units transferred out under FIFO? (Appendix A) a. $88,360B. $77,520c. $50,400d. $67,566

Beginning inventory prior cost $12,960

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

60. What is the total cost of the ending inventory under FIFO? (Appendix A) A. $10,840b. $11,212c. $12,720d. $6,412

(3,600 x $1.10) + (5,200 x $0.40) + (8,000 x $0.60) = $10,840

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

Use the following to answer questions 6162:Vassel Company has a processcosting system using the WeightedAverage cost flow method.All materials are introduced at the beginning of the process in Department 1. The following information is available for the month of December.

8-23

Chapter 08 - Process-Costing Systems

61. The number of equivalent units of production for materials for the month of December is: a. 8,000b. 7,500C. 9,000d. 7,800

Units finished (7,500) + Ending inventory (1,500 x 100%) = 9,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

62. The number of equivalent units of production for conversion costs for the month of December is: a. 8,000b. 7,500c. 9,000D. 7,800

Units finished (7,500) + Ending inventory (1,500 x .20) = 7,800

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

63. In computing the cost per equivalent unit, the FIFO method considers: (Appendix A) a. Current costs less costs in beginning WorkinProcess InventoryB. Current costs onlyc. Current costs plus costs in beginning WorkinProcess Inventoryd. Current costs plus costs of ending WorkinProcess Inventory

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-24

Chapter 08 - Process-Costing Systems

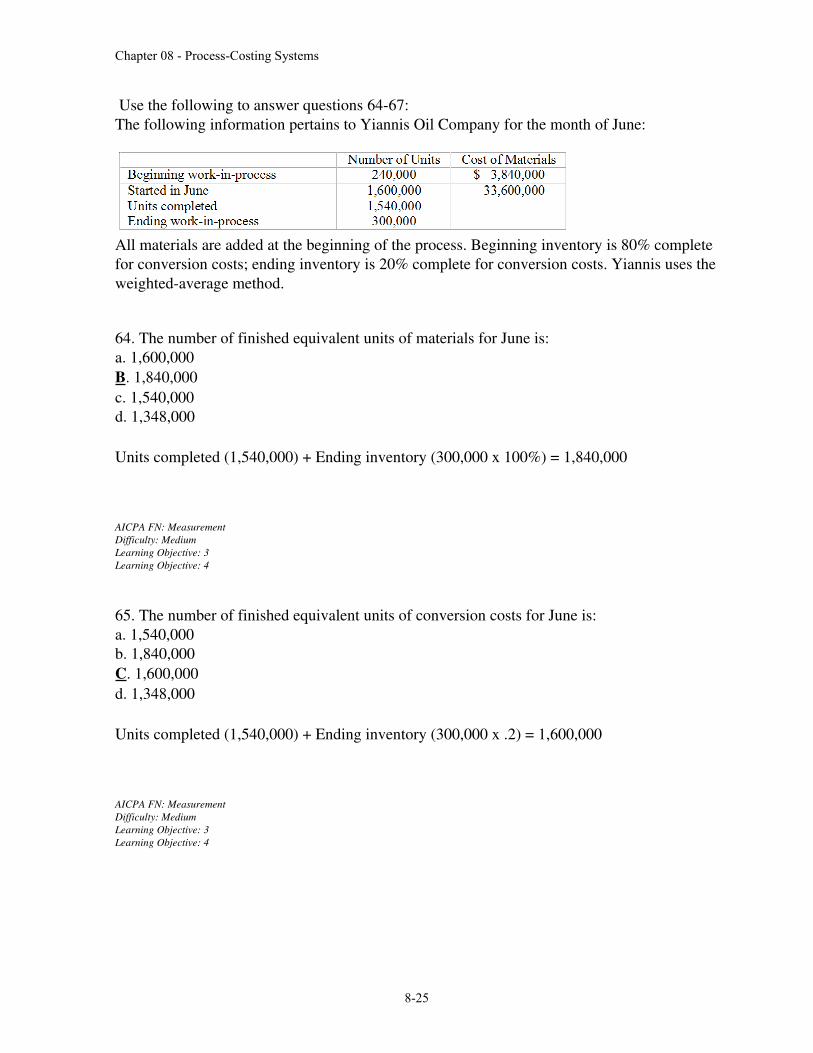

Use the following to answer questions 6467:The following information pertains to Yiannis Oil Company for the month of June:

All materials are added at the beginning of the process. Beginning inventory is 80% complete for conversion costs; ending inventory is 20% complete for conversion costs. Yiannis uses theweightedaverage method.

64. The number of finished equivalent units of materials for June is: a. 1,600,000B. 1,840,000c. 1,540,000d. 1,348,000

Units completed (1,540,000) + Ending inventory (300,000 x 100%) = 1,840,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

65. The number of finished equivalent units of conversion costs for June is: a. 1,540,000b. 1,840,000C. 1,600,000d. 1,348,000

Units completed (1,540,000) + Ending inventory (300,000 x .2) = 1,600,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

8-25

Chapter 08 - Process-Costing Systems

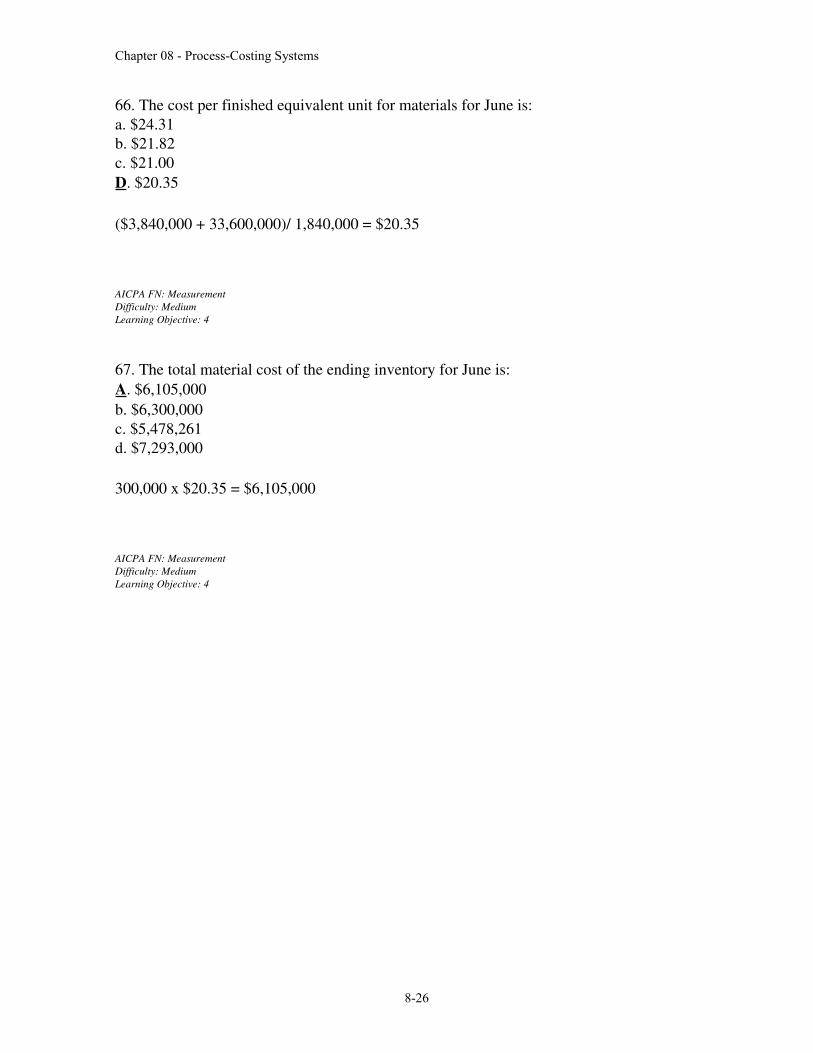

66. The cost per finished equivalent unit for materials for June is: a. $24.31b. $21.82c. $21.00D. $20.35

($3,840,000 + 33,600,000)/ 1,840,000 = $20.35

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

67. The total material cost of the ending inventory for June is: A. $6,105,000b. $6,300,000c. $5,478,261d. $7,293,000

300,000 x $20.35 = $6,105,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

8-26

Chapter 08 - Process-Costing Systems

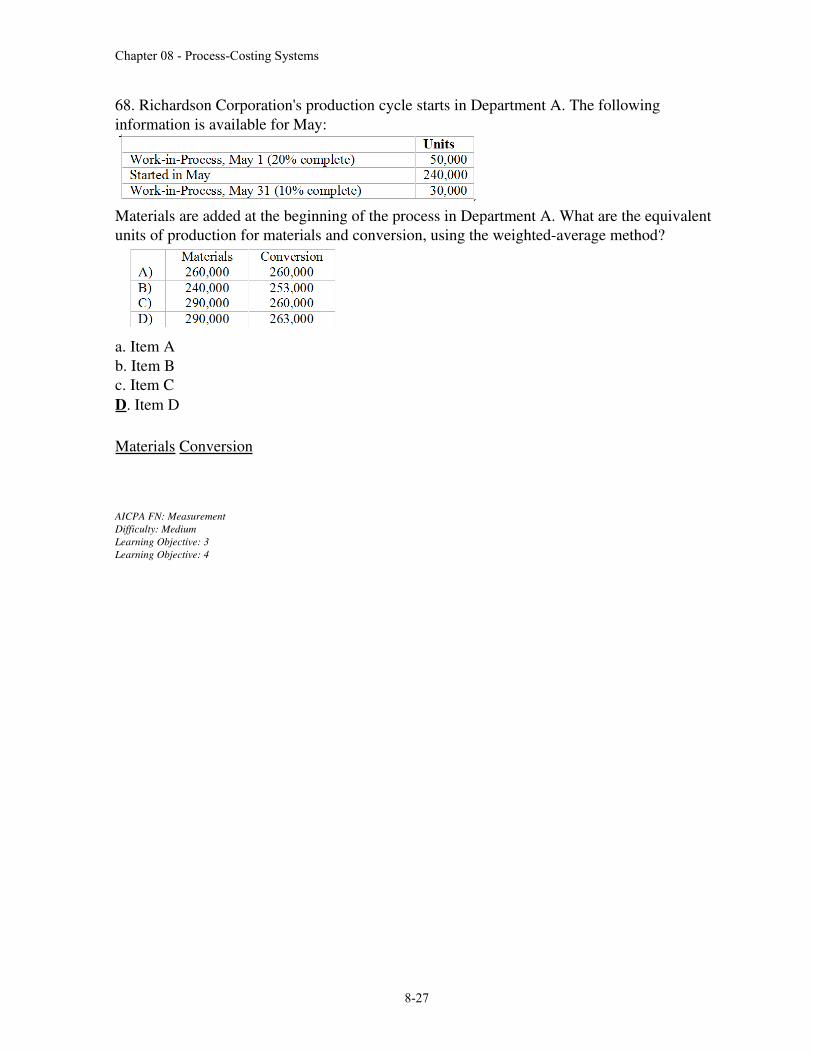

68. Richardson Corporation's production cycle starts in Department A. The following information is available for May:

Materials are added at the beginning of the process in Department A. What are the equivalent units of production for materials and conversion, using the weightedaverage method?

a. Item Ab. Item Bc. Item CD. Item D

Materials Conversion

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

8-27

Chapter 08 - Process-Costing Systems

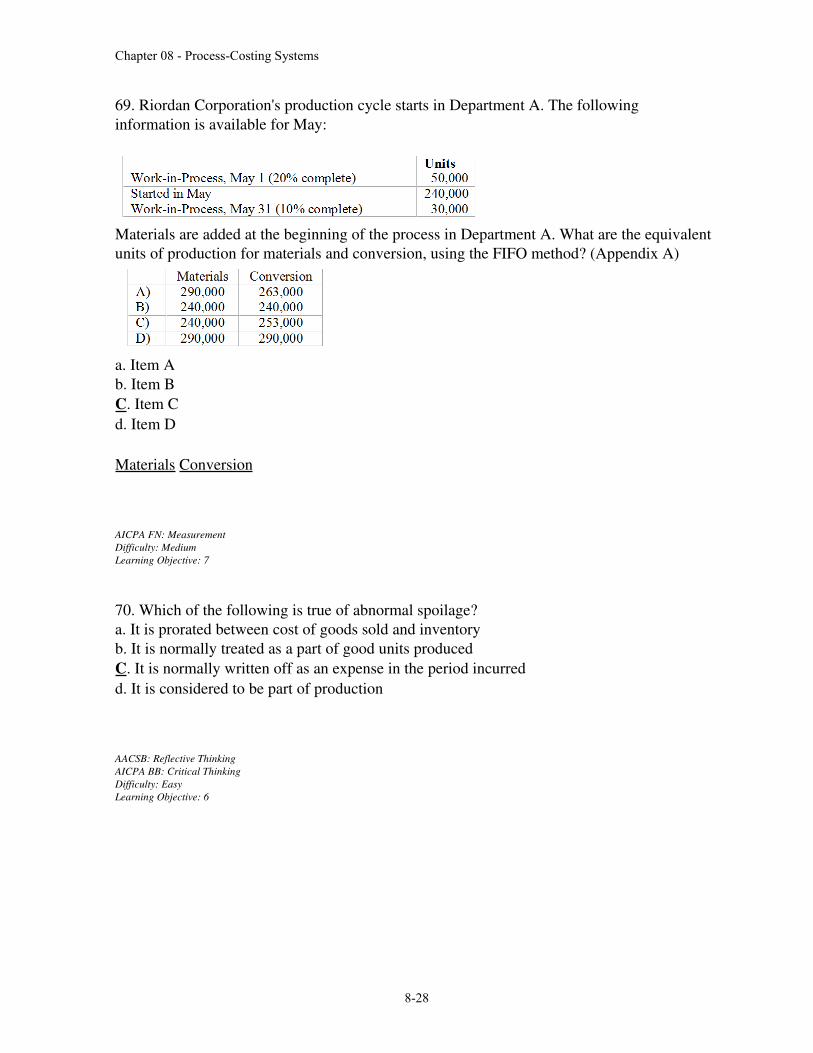

69. Riordan Corporation's production cycle starts in Department A. The following information is available for May:

Materials are added at the beginning of the process in Department A. What are the equivalent units of production for materials and conversion, using the FIFO method? (Appendix A)

a. Item Ab. Item BC. Item Cd. Item D

Materials Conversion

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

70. Which of the following is true of abnormal spoilage? a. It is prorated between cost of goods sold and inventoryb. It is normally treated as a part of good units producedC. It is normally written off as an expense in the period incurredd. It is considered to be part of production

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: EasyLearning Objective: 6

8-28

Chapter 08 - Process-Costing Systems

71. Which of the following statements is false about normal or tolerated spoilage? a. It is expected as a natural outcome of an imperfect process and counted as a normal cost of good units producedb. With wide acceptance of quality improvement initiatives, the idea is now in disfavorC. For external financial reporting purposes, it is normally reported as a separate line item in the income statementd. Regardless of the treatment and computation, it is usually desirable to internally report spoilage costs as a separate item for management purposes

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: EasyLearning Objective: 6

Use the following to answer questions 7278:Winchester Salad Dressing had beginning workinprocess in July of $248,320 consisting of $101,640 of materials and $146,680 of conversion costs. There were 16,000 units (one unit equals one case of salad dressing) in beginning workinprocess, 40% complete as to conversion costs. Materials are added at the beginning of the process. During November, 34,000 were transferred out; 1,000 were spoiled and 9,000 remained in ending inventory. The spoiled units were 60% complete for conversion cost. The ending workinprocess was 70% complete for conversion cost. Costs during the period amounted to $781,200 for direct materials and $1,009,280 for conversion. Winchester uses the weightedaveragemethod and identifies all spoilage costs separately.

72. The number of units started during July was: a. 35,000b. 53,000C. 28,000d. 34,000

16,000 + X = 34,000 + 1,000 + 9,000

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 3

8-29

Chapter 08 - Process-Costing Systems

73. The number of finished equivalent units under weightedaverage for materials is: A. 44,000b. 43,000c. 39,600d. 39,400

Units Finished 34,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4Learning Objective: 6

74. The number of finished equivalent units under weightedaverage for conversions costs is: a. 44,000b. 34,000c. 40,300D. 40,900

Units Finished 34,000

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4Learning Objective: 6

75. The cost per finished equivalent unit for materials under weightedaverage is: a. $17.75B. $20.06c. $20.53d. $21.69

($101,640 +$781,200) /44,000 = $20.06

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

8-30

Chapter 08 - Process-Costing Systems

76. The cost per finished equivalent unit for conversion costs under weightedaverage is: a. $24.68b. $26.27c. $28.68D. $28.26

($146,680 + $1,009,280)/40,900 = $28.26

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 4Learning Objective: 6

77. The total cost of units transferred out assuming spoilage is written off as an expense underweightedaverage was: a. $1,680,000b. $1,394,665C. $1,642,880d. $2,038,579

34,000 x $48.32 = $1,642,880

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

78. The total cost assigned to spoiled units under weightedaverage is: a. $48,320b. $20,060C. $37,016d. $28,260

(1,000 x $20.06) +(600 x $28.26) = $37,016

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 6

8-31

Chapter 08 - Process-Costing Systems

Use the following to answer questions 7985:Oliver Corporation's Department 2 had 1,600 units in the beginning inventory (60% complete for conversion costs). During July, 14,000 units were started into production; 14,400 good units were transferred to Department 3 and 400 units were left in the ending inventory, which were 40% complete for conversion costs. All materials are added at the end of the process in Department 2. Units are inspected at the completion of the process, at which point spoiled units are identified and disposed of. The cost of spoiled units is written off as an abnormal expense during the period. The following costs were assigned to Department 2 during the period:

79. The number of units spoiled during July was: a. 400B. 800c. 1,200d. 0

1,600 + 14,000 = 14,400 + 400 + X; X = 800

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 3Learning Objective: 6

8-32

Chapter 08 - Process-Costing Systems

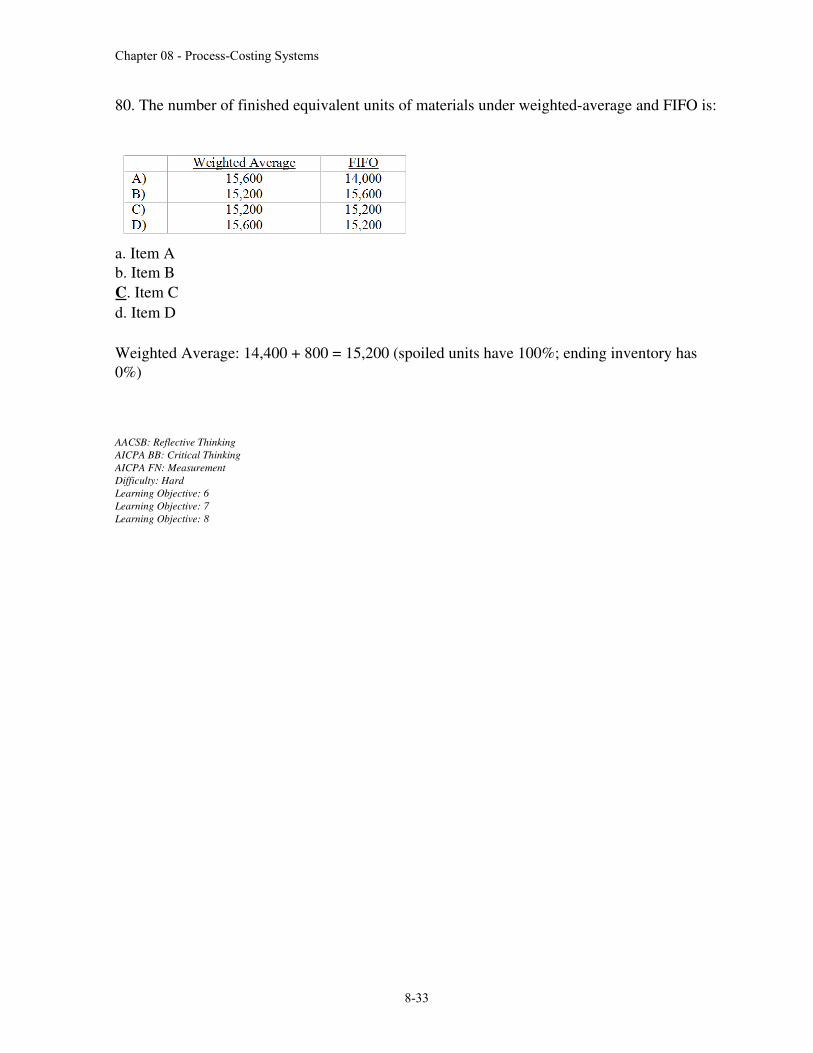

80. The number of finished equivalent units of materials under weightedaverage and FIFO is:

a. Item Ab. Item BC. Item Cd. Item D

Weighted Average: 14,400 + 800 = 15,200 (spoiled units have 100%; ending inventory has 0%)

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 6Learning Objective: 7Learning Objective: 8

8-33

Chapter 08 - Process-Costing Systems

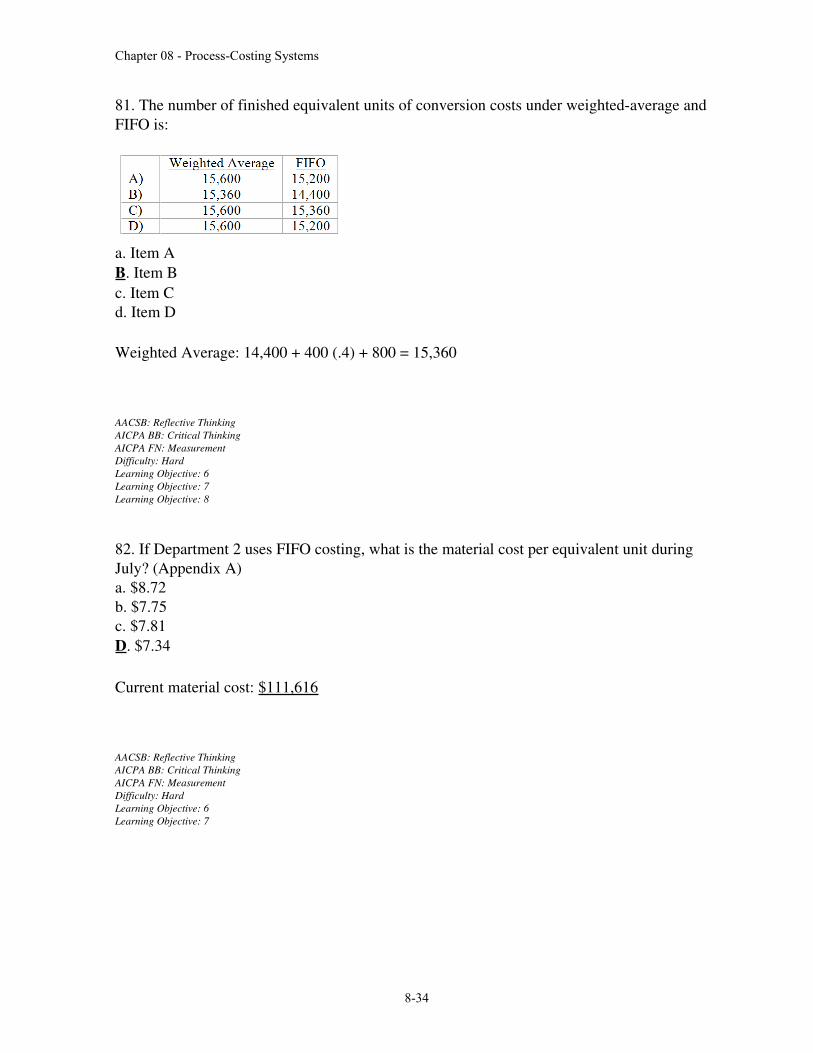

81. The number of finished equivalent units of conversion costs under weightedaverage and FIFO is:

a. Item AB. Item Bc. Item Cd. Item D

Weighted Average: 14,400 + 400 (.4) + 800 = 15,360

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 6Learning Objective: 7Learning Objective: 8

82. If Department 2 uses FIFO costing, what is the material cost per equivalent unit during July? (Appendix A) a. $8.72b. $7.75c. $7.81D. $7.34

Current material cost: $111,616

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 6Learning Objective: 7

8-34

Chapter 08 - Process-Costing Systems

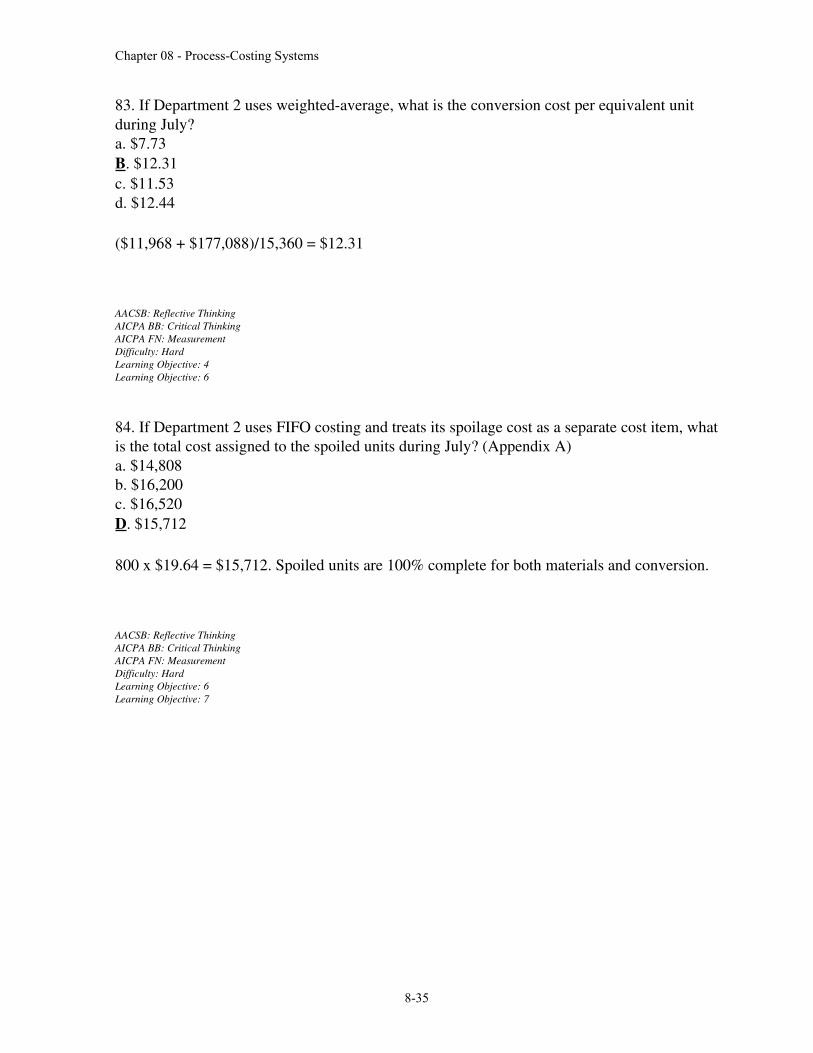

83. If Department 2 uses weightedaverage, what is the conversion cost per equivalent unit during July? a. $7.73B. $12.31c. $11.53d. $12.44

($11,968 + $177,088)/15,360 = $12.31

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 4Learning Objective: 6

84. If Department 2 uses FIFO costing and treats its spoilage cost as a separate cost item, whatis the total cost assigned to the spoiled units during July? (Appendix A) a. $14,808b. $16,200c. $16,520D. $15,712

800 x $19.64 = $15,712. Spoiled units are 100% complete for both materials and conversion.

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 6Learning Objective: 7

8-35

Chapter 08 - Process-Costing Systems

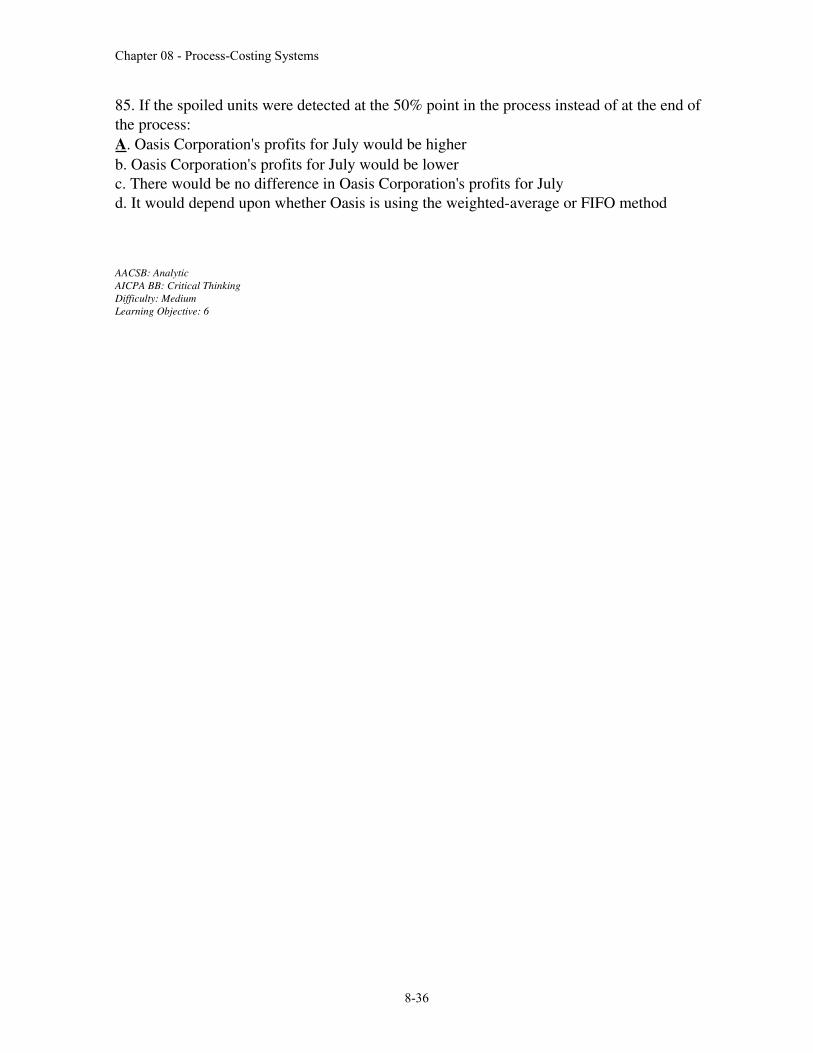

85. If the spoiled units were detected at the 50% point in the process instead of at the end of the process: A. Oasis Corporation's profits for July would be higherb. Oasis Corporation's profits for July would be lowerc. There would be no difference in Oasis Corporation's profits for Julyd. It would depend upon whether Oasis is using the weightedaverage or FIFO method

AACSB: AnalyticAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 6

8-36

Chapter 08 - Process-Costing Systems

86. Which of the following companies would most likely use a process costing system? a. A large computer manufacturer where each computer is made to customer specificationsb. A luxury home builderc. A law firmD. A manufacturer of cereals

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 1

87. If the FIFO costing method is used and materials are added at the beginning of the period, the total equivalent units for materials will equal the number of units: (Appendix A) a. Started into the process plus the units in the ending inventoryb. Started and completed during the periodc. Transferred out during the periodD. Started into the process during the period

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 7

88. Which of the following companies is most likely to use operation costing? (Appendix B) a. A large oil refinerb. A paint manufacturerc. A shipbuilderD. A shoe manufacturer

AICPA FN: MeasurementDifficulty: EasyLearning Objective: 8

8-37

Chapter 08 - Process-Costing Systems

89. Which of the following statements regarding operation costing is true? (Appendix B) a. Costs of conversion are accounted for separately, while all products have the same materials costb. It is ideal in mass production of units in continuous processesC. Direct materials for each batch passing through a particular operation are different, while conversion costs are the samed. It is best used in companies that make customized products

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 8

Use the following to answer questions 9093:Preston Manufacturing Company has the following information available for its process costing system for the month of May in the finishing department. The finishing department is the second of a multipledepartment manufacturing plant. Materials are added at the end of the process in finishing.

Beginning inventory is 30% complete as to conversion costs; ending inventory is 80% complete as to conversion costs.

8-38

Chapter 08 - Process-Costing Systems

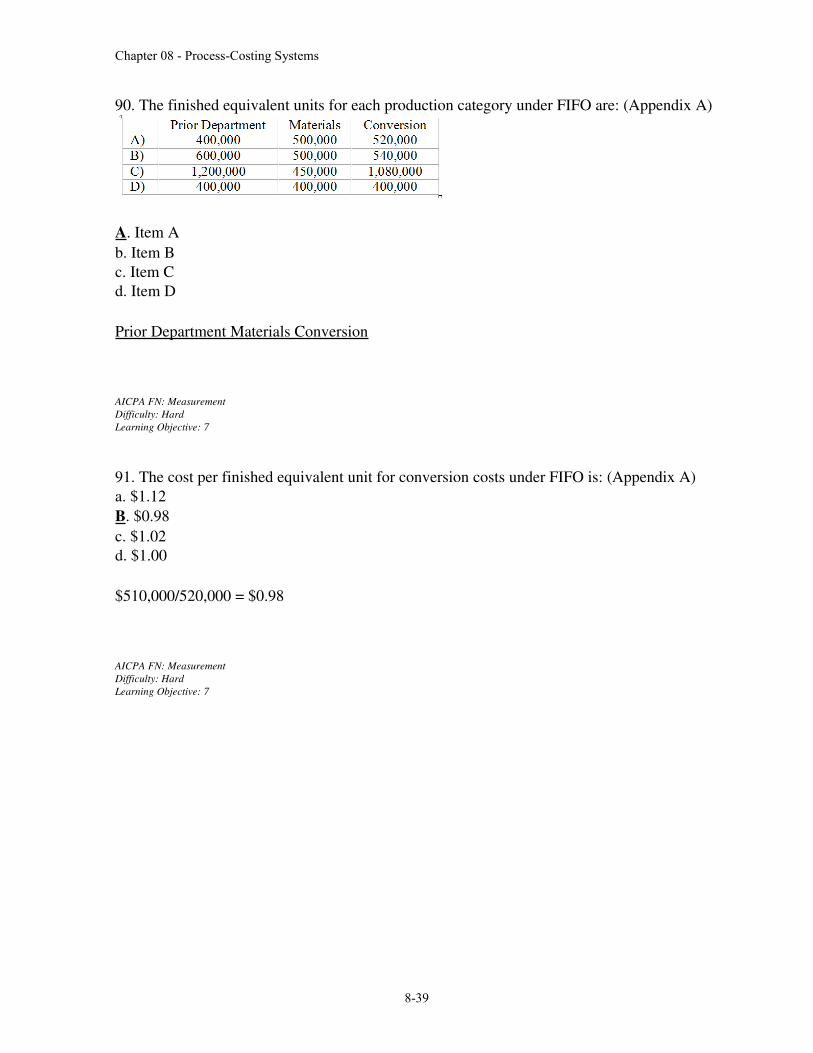

90. The finished equivalent units for each production category under FIFO are: (Appendix A)

A. Item Ab. Item Bc. Item Cd. Item D

Prior Department Materials Conversion

AICPA FN: MeasurementDifficulty: HardLearning Objective: 7

91. The cost per finished equivalent unit for conversion costs under FIFO is: (Appendix A) a. $1.12B. $0.98c. $1.02d. $1.00

$510,000/520,000 = $0.98

AICPA FN: MeasurementDifficulty: HardLearning Objective: 7

8-39

Chapter 08 - Process-Costing Systems

92. The total cost of units transferred out under FIFO is: (Appendix A) a. $1,402,500b. $841,500C. $1,148,700d. $921,500

Beginning inventory $80,000

AICPA FN: MeasurementDifficulty: HardLearning Objective: 7

8-40

Chapter 08 - Process-Costing Systems

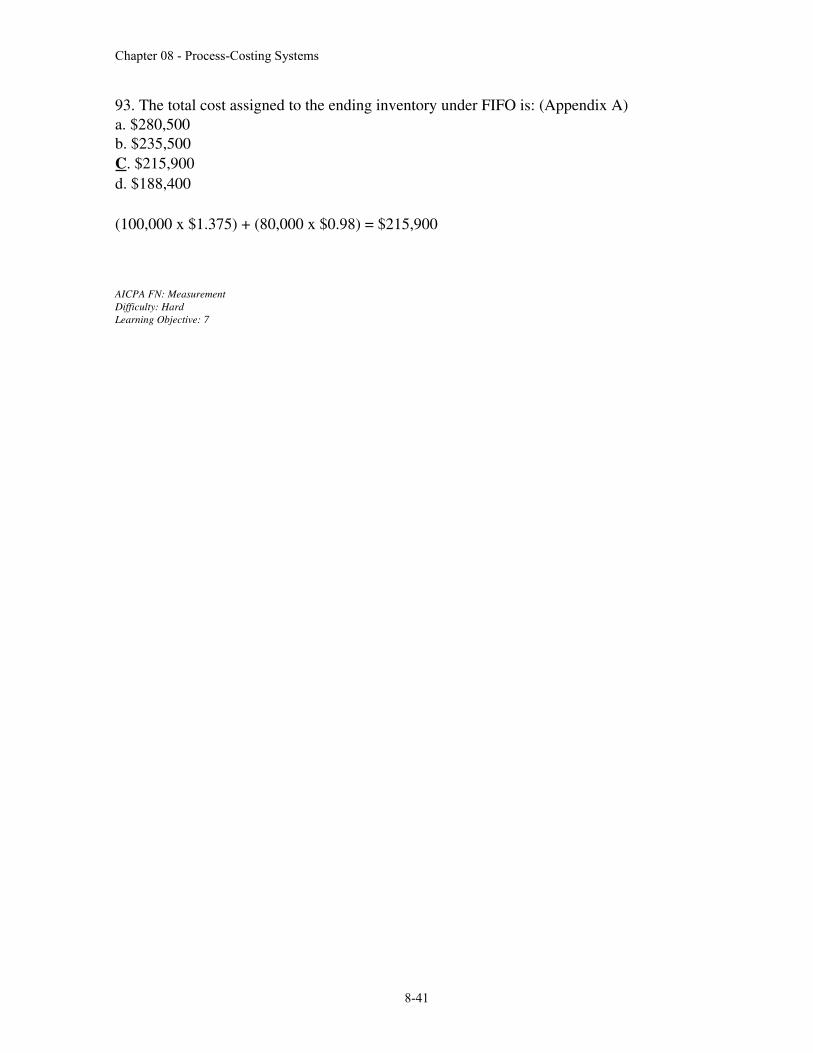

93. The total cost assigned to the ending inventory under FIFO is: (Appendix A) a. $280,500b. $235,500C. $215,900d. $188,400

(100,000 x $1.375) + (80,000 x $0.98) = $215,900

AICPA FN: MeasurementDifficulty: HardLearning Objective: 7

8-41

Chapter 08 - Process-Costing Systems

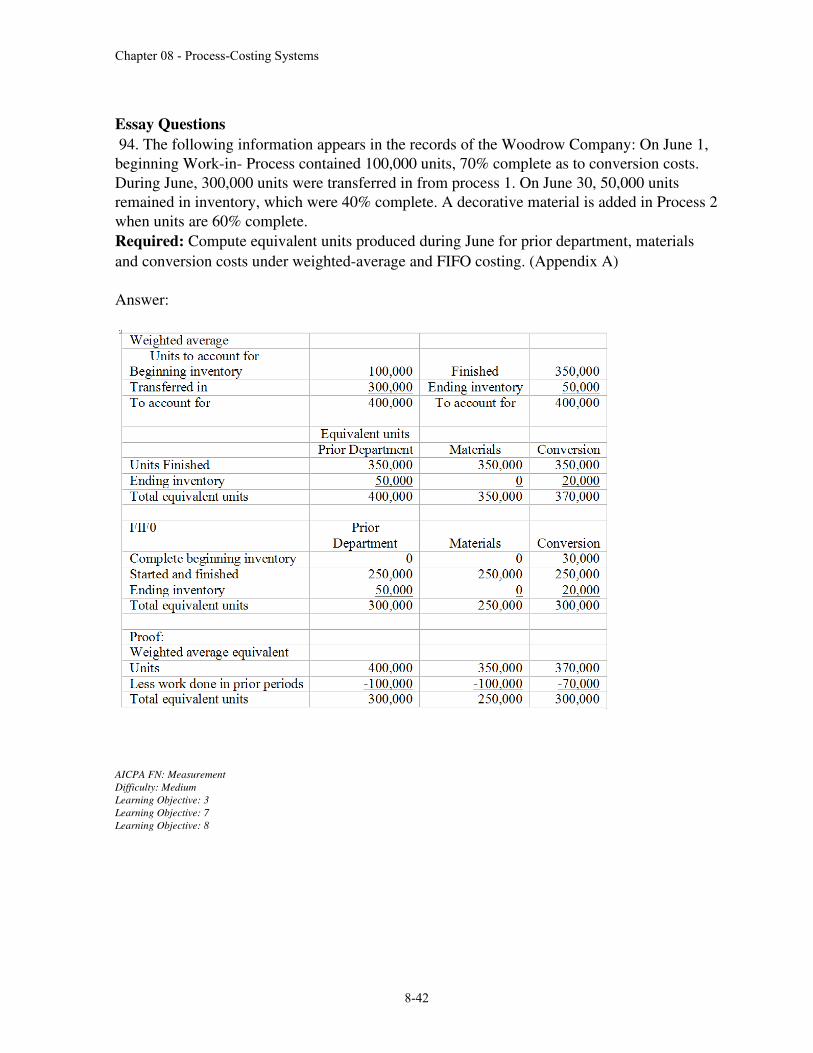

Essay Questions 94. The following information appears in the records of the Woodrow Company: On June 1, beginning Workin Process contained 100,000 units, 70% complete as to conversion costs. During June, 300,000 units were transferred in from process 1. On June 30, 50,000 units remained in inventory, which were 40% complete. A decorative material is added in Process 2when units are 60% complete. Required: Compute equivalent units produced during June for prior department, materials and conversion costs under weightedaverage and FIFO costing. (Appendix A)

Answer:

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 7Learning Objective: 8

8-42

Chapter 08 - Process-Costing Systems

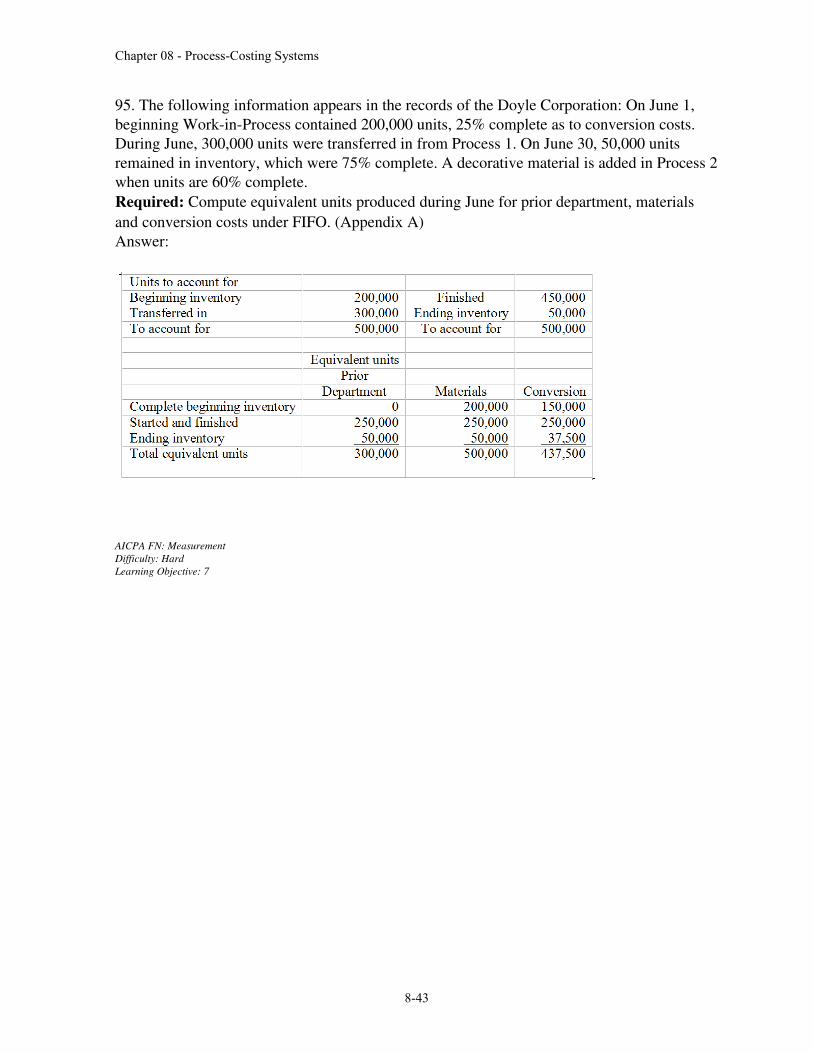

95. The following information appears in the records of the Doyle Corporation: On June 1, beginning WorkinProcess contained 200,000 units, 25% complete as to conversion costs. During June, 300,000 units were transferred in from Process 1. On June 30, 50,000 units remained in inventory, which were 75% complete. A decorative material is added in Process 2when units are 60% complete. Required: Compute equivalent units produced during June for prior department, materials and conversion costs under FIFO. (Appendix A) Answer:

AICPA FN: MeasurementDifficulty: HardLearning Objective: 7

8-43

Chapter 08 - Process-Costing Systems

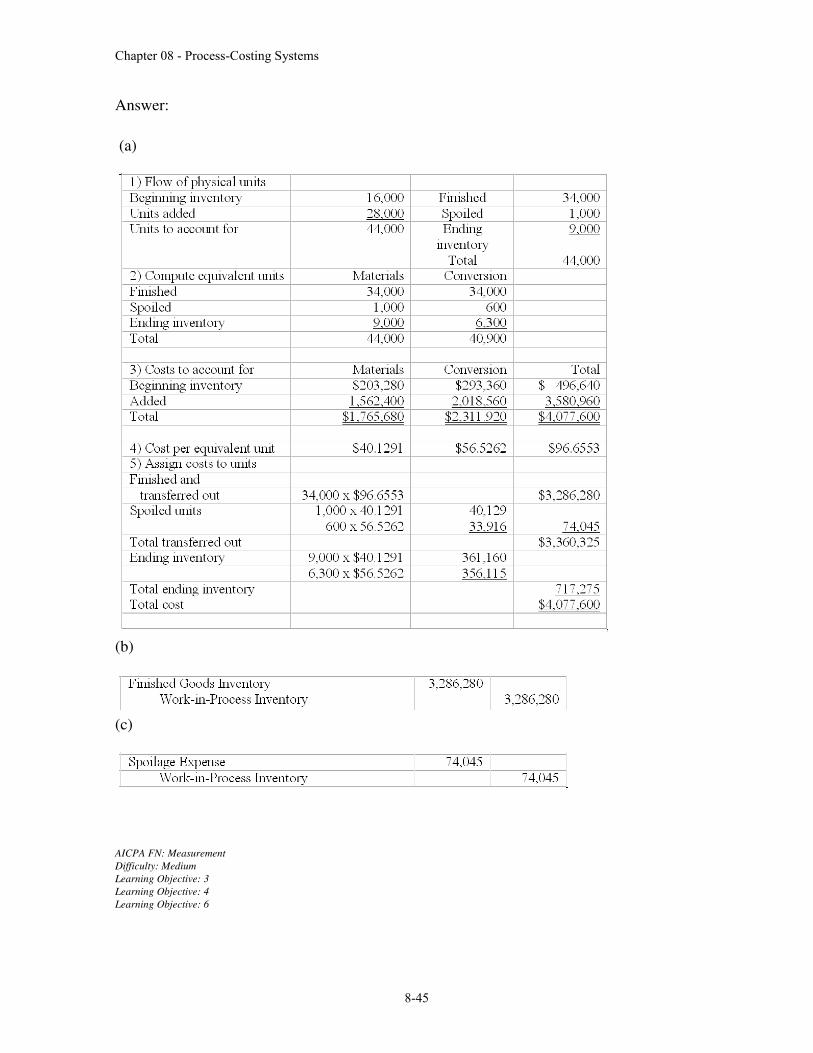

96. Celia's Salad Dressings had beginning workinprocess of $496,640 consisting of $203,280 of materials and $293,360 of conversion costs. There were 16,000 units (one unit equals one case) in beginning inventory, 40% complete as to conversion costs. Materials are added at the beginning of the process. During November, 34,000 units were transferred out, 1,000 were spoiled and 9,000 remained in ending inventory. The spoiled units were 60% complete for conversion costs. The ending workinprocess was 70% complete for conversioncosts. Costs during the period amounted to $1,562,400 for materials and $2,018,560 for conversion. Celia's accounts for spoiled units separately and does not spread their cost over good units produced. Required:(a) Prepare a process costing report for November using the weightedaverage method. Use the five step costing method to assign costs to products. Round costs to four decimal points.(b) Prepare the journal entry required to transfer units to finished goods inventory.(c) Prepare the journal entry required to dispose of spoiled units.

8-44

Chapter 08 - Process-Costing Systems

Answer:

(a)

(b)

(c)

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4Learning Objective: 6

8-45

Chapter 08 - Process-Costing Systems

8-46

Chapter 08 - Process-Costing Systems

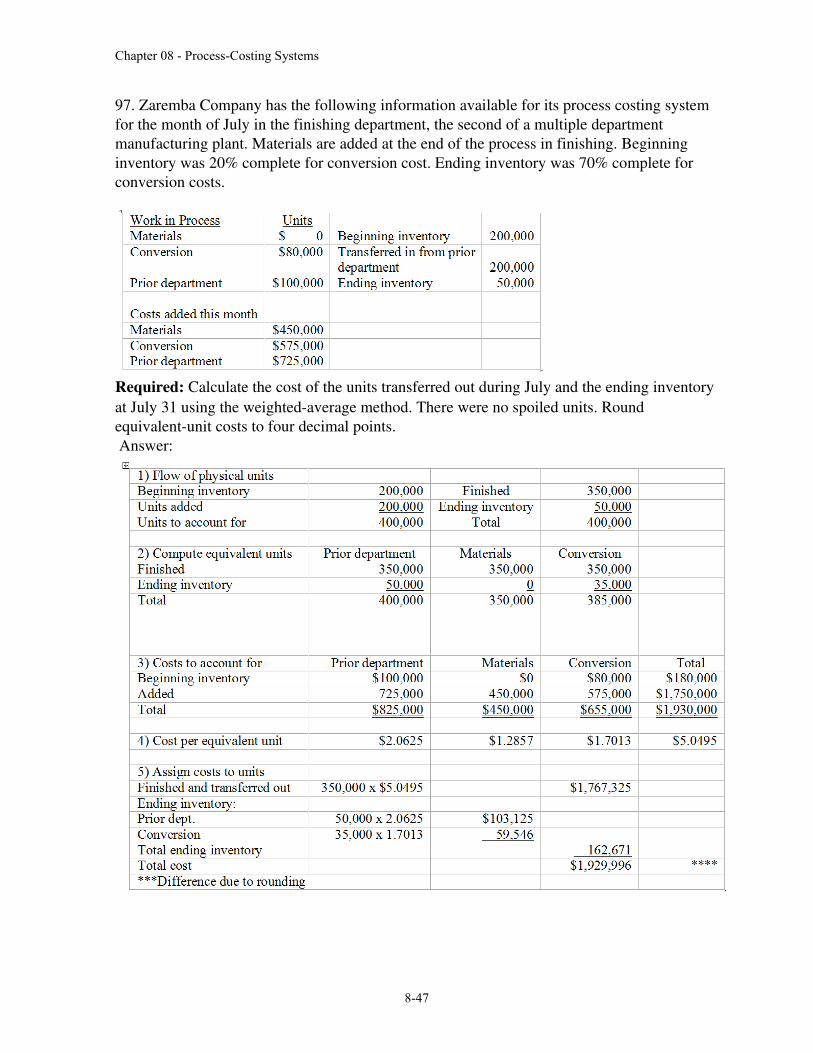

97. Zaremba Company has the following information available for its process costing system for the month of July in the finishing department, the second of a multiple department manufacturing plant. Materials are added at the end of the process in finishing. Beginning inventory was 20% complete for conversion cost. Ending inventory was 70% complete for conversion costs.

Required: Calculate the cost of the units transferred out during July and the ending inventory at July 31 using the weightedaverage method. There were no spoiled units. Round equivalentunit costs to four decimal points. Answer:

8-47

Chapter 08 - Process-Costing Systems

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4Learning Objective: 5

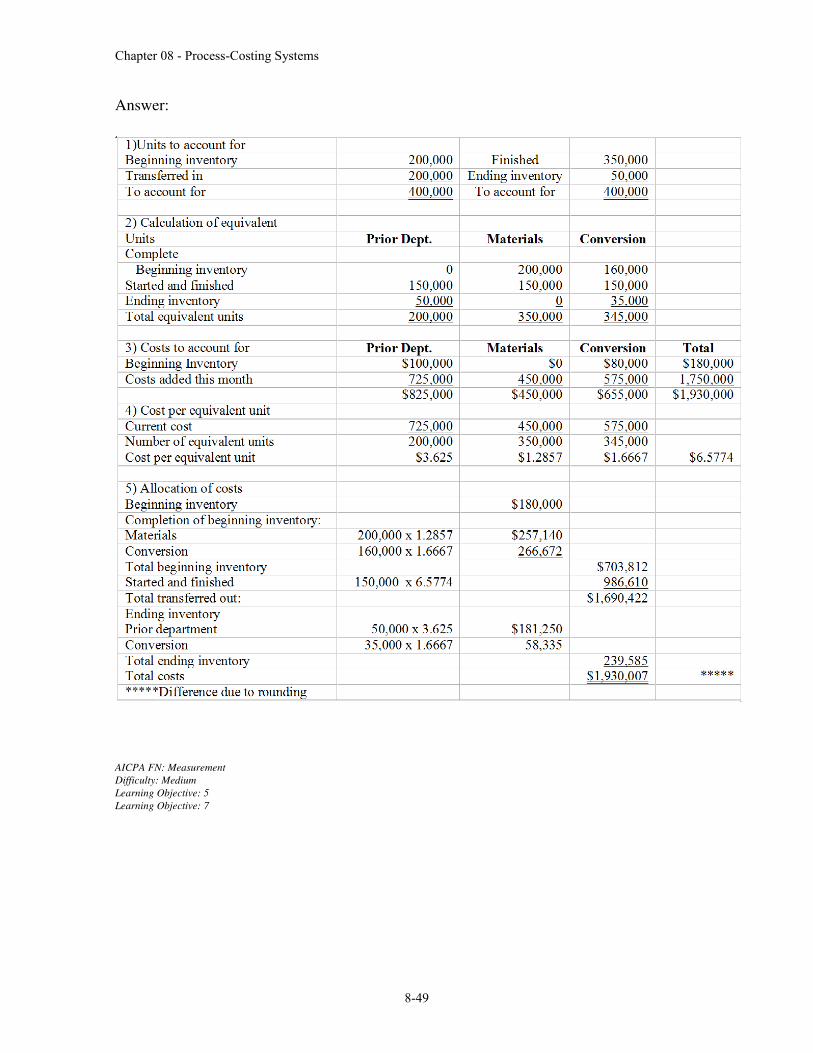

98. Wax Company has the following information available for its process costing system for the month of July in the finishing department, the second of a multiple department manufacturing plant. Materials are added at the end of the process in finishing. Beginning inventory was 20% complete for conversion cost. Ending inventory was 70% complete for conversion costs.

Costs added this month: Materials: $450,000; Conversion: $575,000; Prior department: $725,000Required: Calculate the cost of the units transferred out during July and the ending inventory at July 31 using the FIFO method. There were no spoiled units. Round equivalentunit costs tofour decimal points. (Appendix A)

8-48

Chapter 08 - Process-Costing Systems

Answer:

AICPA FN: MeasurementDifficulty: MediumLearning Objective: 5Learning Objective: 7

8-49

Chapter 08 - Process-Costing Systems

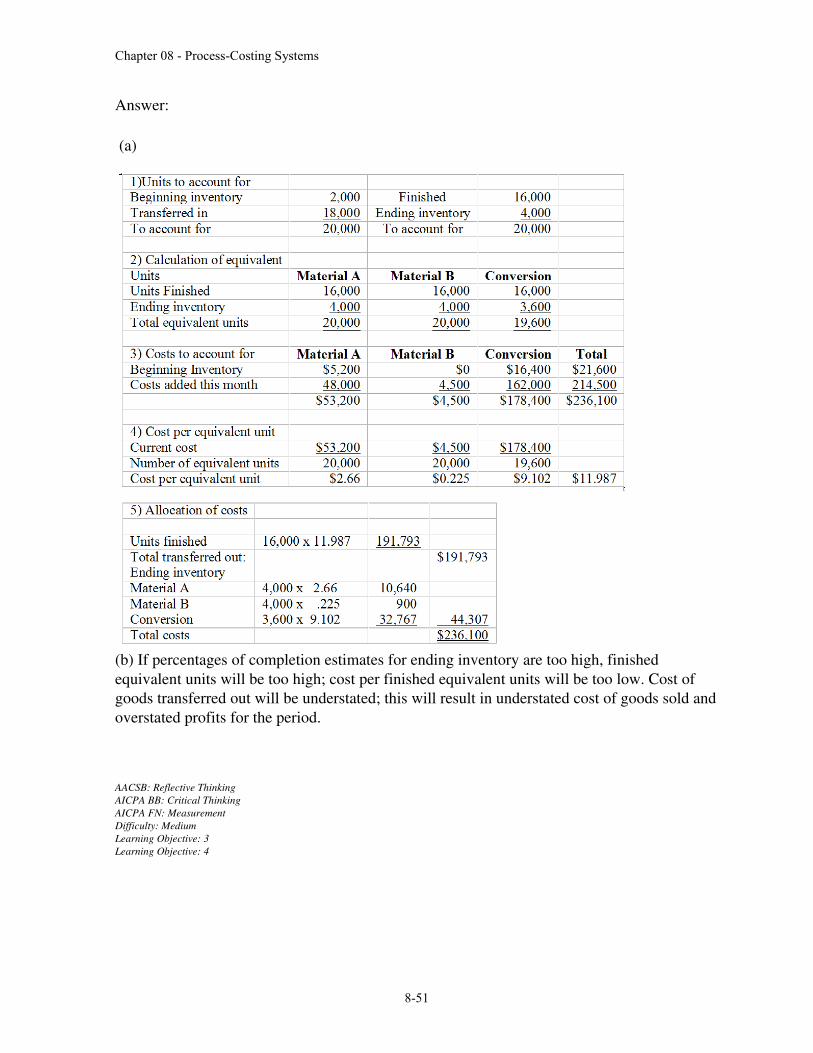

99. Crazy Cool Colas prepares specialtyflavored sodas for large grocery chains and bakeries. The company employs a processcosting system. Most of the basic ingredients, labeled Material Group A, are added at the beginning of the mixing process. However, to give the sodas the special "sizzle" they are named for, the company adds a special ingredient when units are 80% complete, which is labeled Material Group B. Information regarding the mixingdepartment in a recent month reveals the following: Beginning inventory: 2,000 Cases (60% complete for conversion)Cases started: 18,000Cases finished: 16,000The ending inventory is 90% complete as to conversion costsCost information:Beginning WorkinProcess: $21,600 consisting of $5,200 of Material Group A, $0 ofMaterial Group B and $16,400 of conversion costsAdded during the month: $48,000 of Material Group A, $4,500 of Material Group B and$162,000 of conversion costsRequired: a) Prepare a cost report using the weightedaverage method. Round all numbers to four decimal points.b) During the annual audit, the company's auditors discover that management's estimates of percentage of completion for the ending inventory were too high. Discuss how this error will affect the company's ending inventory and profits for the period.

8-50

Chapter 08 - Process-Costing Systems

Answer:

(a)

(b) If percentages of completion estimates for ending inventory are too high, finished equivalent units will be too high; cost per finished equivalent units will be too low. Cost of goods transferred out will be understated; this will result in understated cost of goods sold andoverstated profits for the period.

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 3Learning Objective: 4

8-51

Chapter 08 - Process-Costing Systems

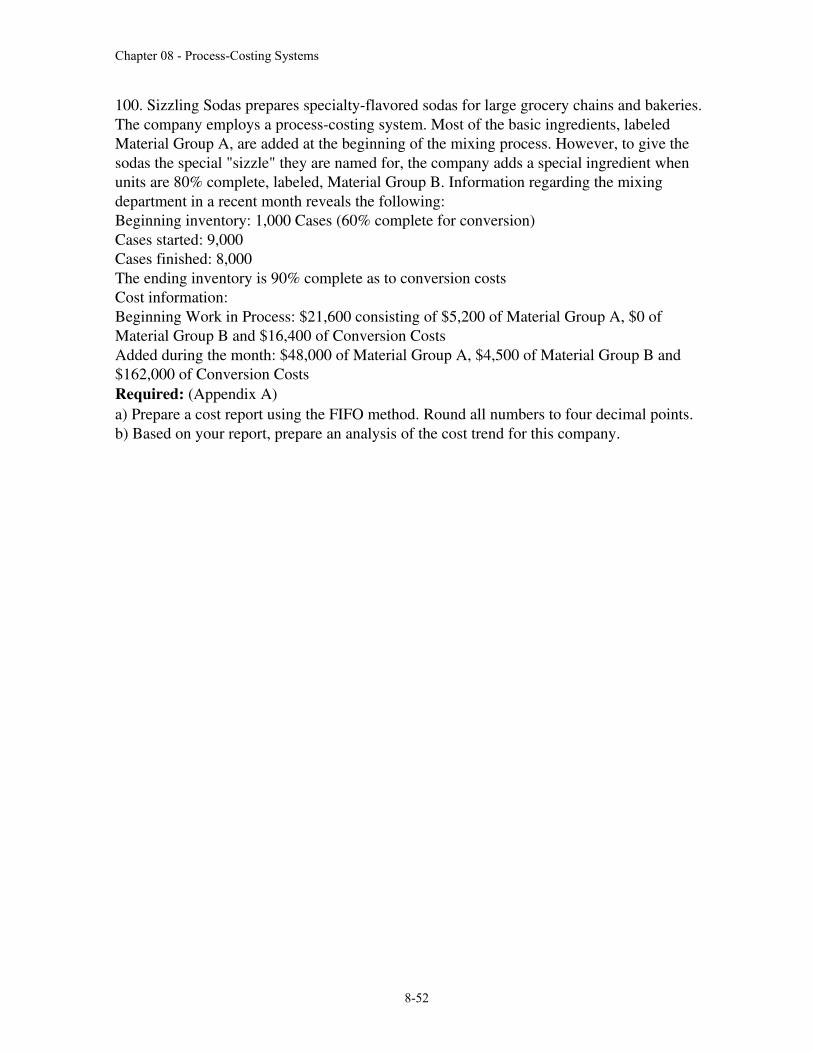

100. Sizzling Sodas prepares specialtyflavored sodas for large grocery chains and bakeries. The company employs a processcosting system. Most of the basic ingredients, labeled Material Group A, are added at the beginning of the mixing process. However, to give the sodas the special "sizzle" they are named for, the company adds a special ingredient when units are 80% complete, labeled, Material Group B. Information regarding the mixing department in a recent month reveals the following: Beginning inventory: 1,000 Cases (60% complete for conversion)Cases started: 9,000Cases finished: 8,000The ending inventory is 90% complete as to conversion costsCost information:Beginning Work in Process: $21,600 consisting of $5,200 of Material Group A, $0 of Material Group B and $16,400 of Conversion CostsAdded during the month: $48,000 of Material Group A, $4,500 of Material Group B and $162,000 of Conversion CostsRequired: (Appendix A)a) Prepare a cost report using the FIFO method. Round all numbers to four decimal points.b) Based on your report, prepare an analysis of the cost trend for this company.

8-52

Chapter 08 - Process-Costing Systems

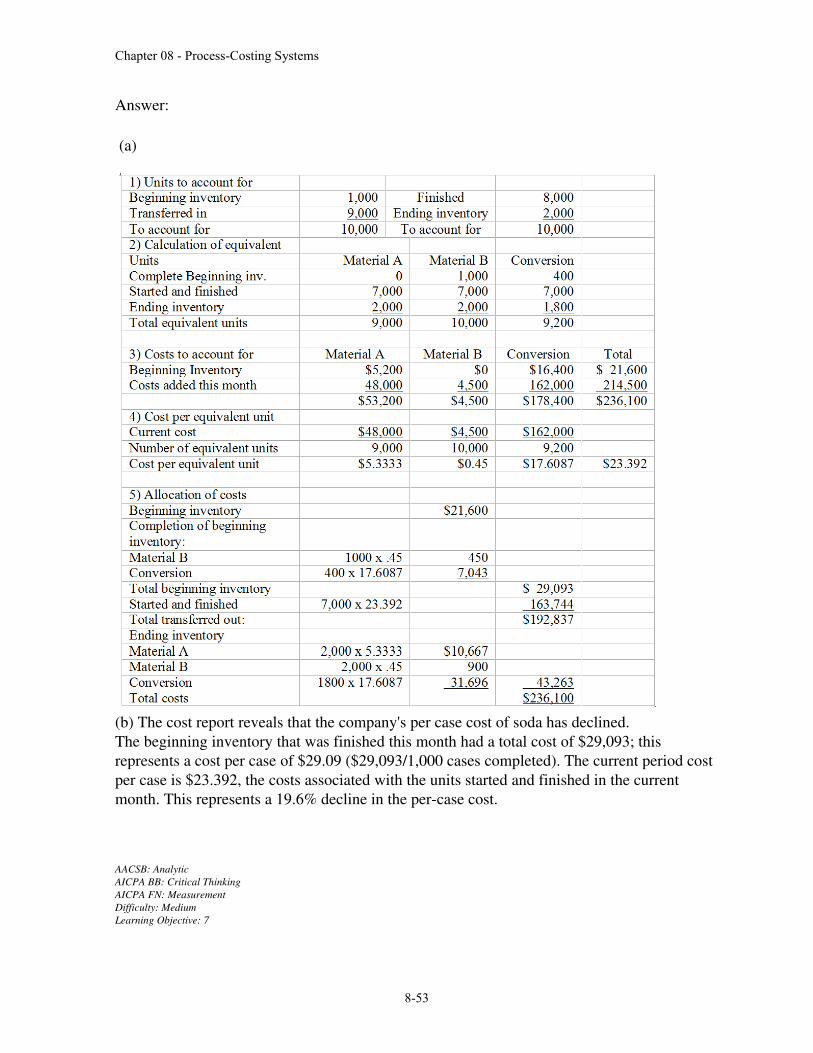

Answer:

(a)

(b) The cost report reveals that the company's per case cost of soda has declined.The beginning inventory that was finished this month had a total cost of $29,093; this represents a cost per case of $29.09 ($29,093/1,000 cases completed). The current period cost per case is $23.392, the costs associated with the units started and finished in the current month. This represents a 19.6% decline in the percase cost.

AACSB: AnalyticAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-53

Chapter 08 - Process-Costing Systems

8-54

Chapter 08 - Process-Costing Systems

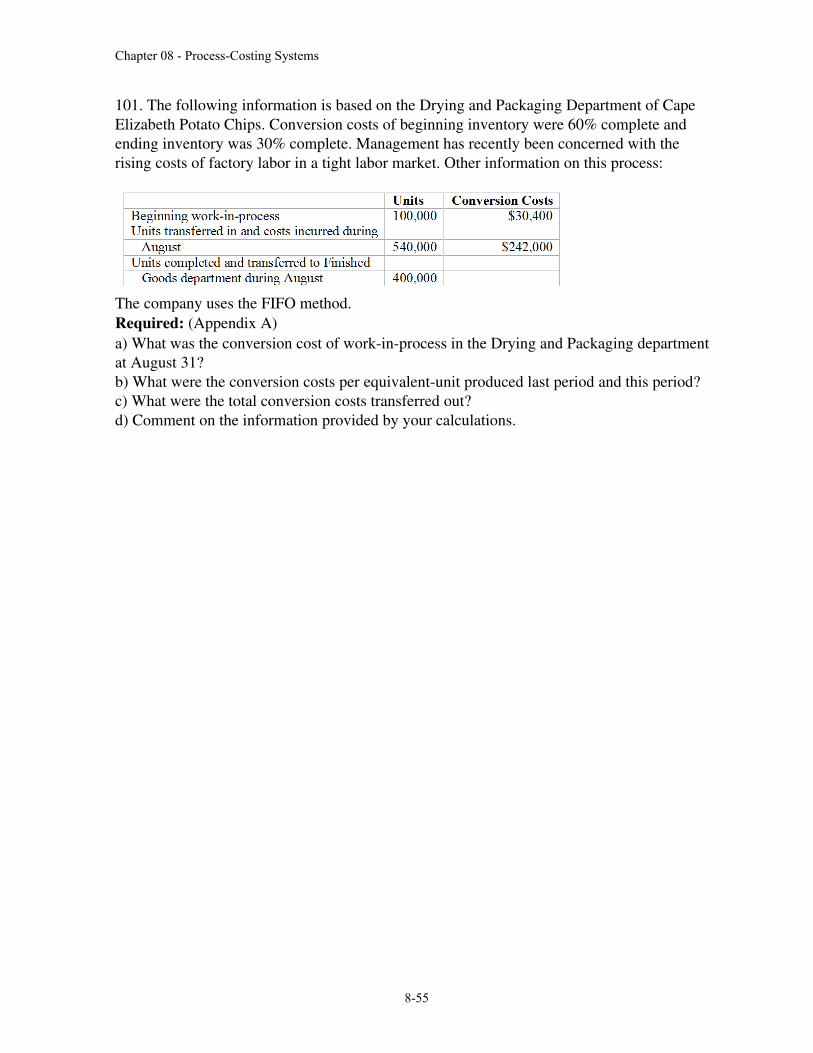

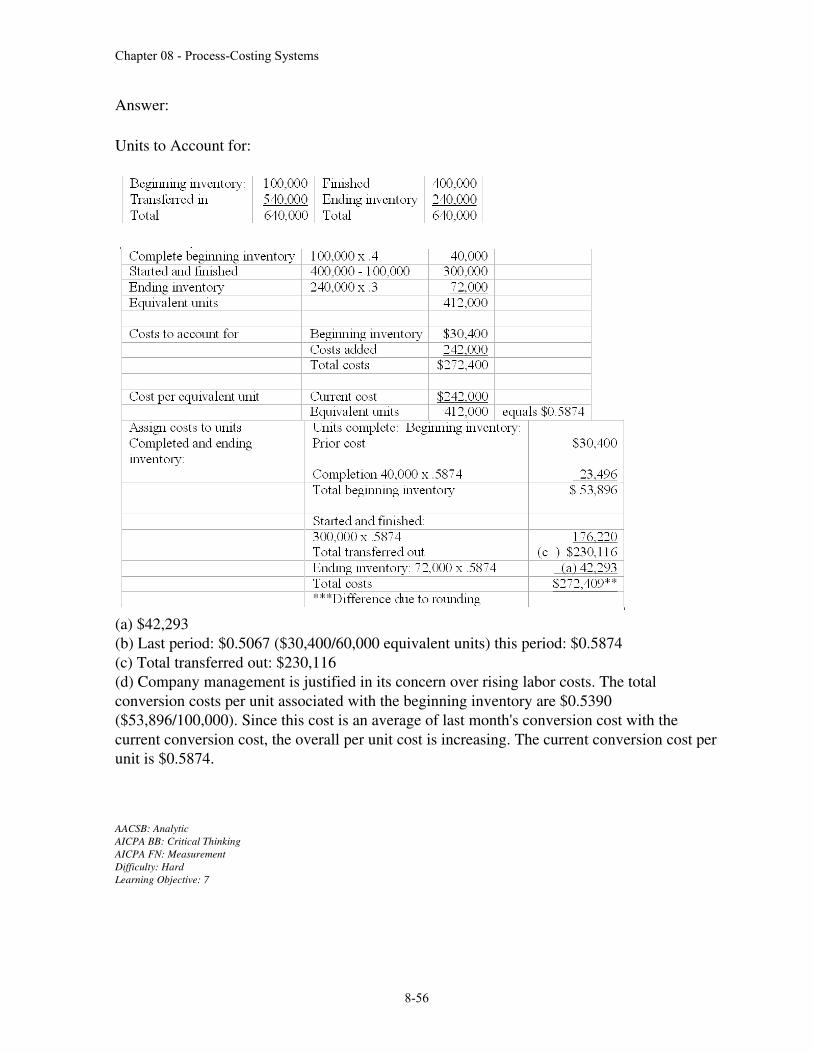

101. The following information is based on the Drying and Packaging Department of Cape Elizabeth Potato Chips. Conversion costs of beginning inventory were 60% complete and ending inventory was 30% complete. Management has recently been concerned with the rising costs of factory labor in a tight labor market. Other information on this process:

The company uses the FIFO method.Required: (Appendix A)a) What was the conversion cost of workinprocess in the Drying and Packaging department at August 31?b) What were the conversion costs per equivalentunit produced last period and this period?c) What were the total conversion costs transferred out?d) Comment on the information provided by your calculations.

8-55

Chapter 08 - Process-Costing Systems

Answer:

Units to Account for:

(a) $42,293(b) Last period: $0.5067 ($30,400/60,000 equivalent units) this period: $0.5874(c) Total transferred out: $230,116(d) Company management is justified in its concern over rising labor costs. The total conversion costs per unit associated with the beginning inventory are $0.5390 ($53,896/100,000). Since this cost is an average of last month's conversion cost with the current conversion cost, the overall per unit cost is increasing. The current conversion cost perunit is $0.5874.

AACSB: AnalyticAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 7

8-56

Chapter 08 - Process-Costing Systems

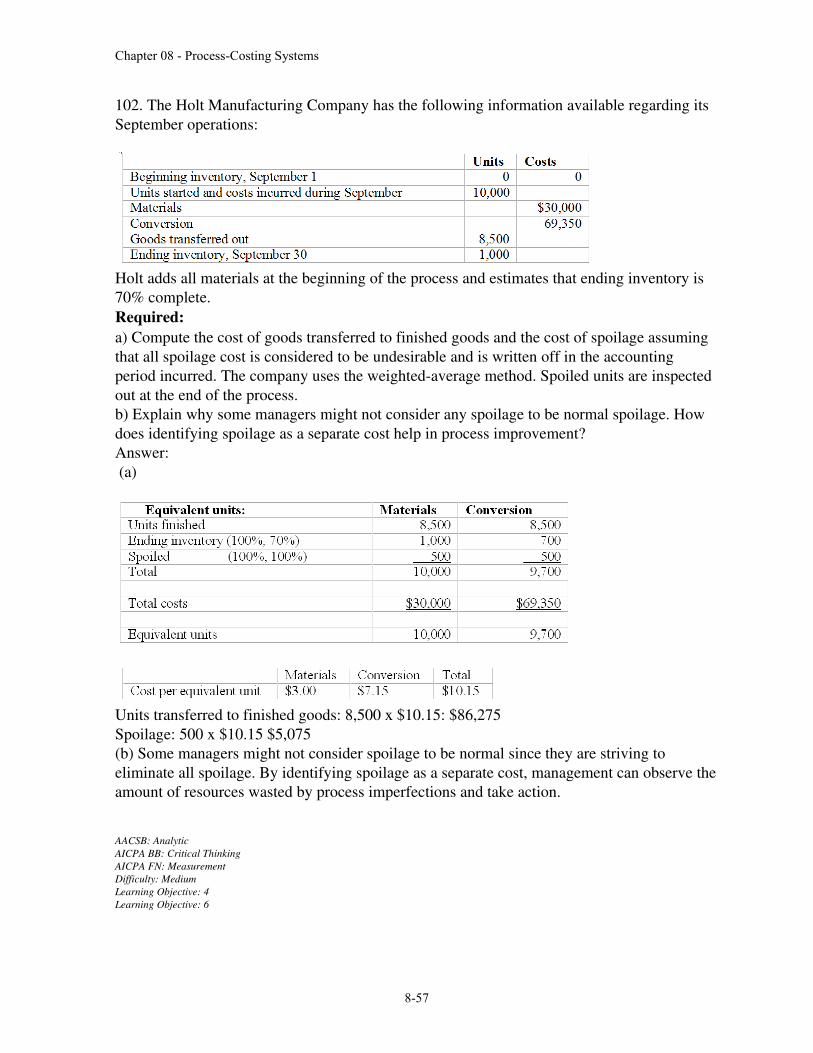

102. The Holt Manufacturing Company has the following information available regarding its September operations:

Holt adds all materials at the beginning of the process and estimates that ending inventory is 70% complete.Required:a) Compute the cost of goods transferred to finished goods and the cost of spoilage assuming that all spoilage cost is considered to be undesirable and is written off in the accounting period incurred. The company uses the weightedaverage method. Spoiled units are inspected out at the end of the process.b) Explain why some managers might not consider any spoilage to be normal spoilage. How does identifying spoilage as a separate cost help in process improvement? Answer: (a)

Units transferred to finished goods: 8,500 x $10.15: $86,275Spoilage: 500 x $10.15 $5,075(b) Some managers might not consider spoilage to be normal since they are striving to eliminate all spoilage. By identifying spoilage as a separate cost, management can observe theamount of resources wasted by process imperfections and take action.

AACSB: AnalyticAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4Learning Objective: 6

8-57

Chapter 08 - Process-Costing Systems

8-58

Chapter 08 - Process-Costing Systems

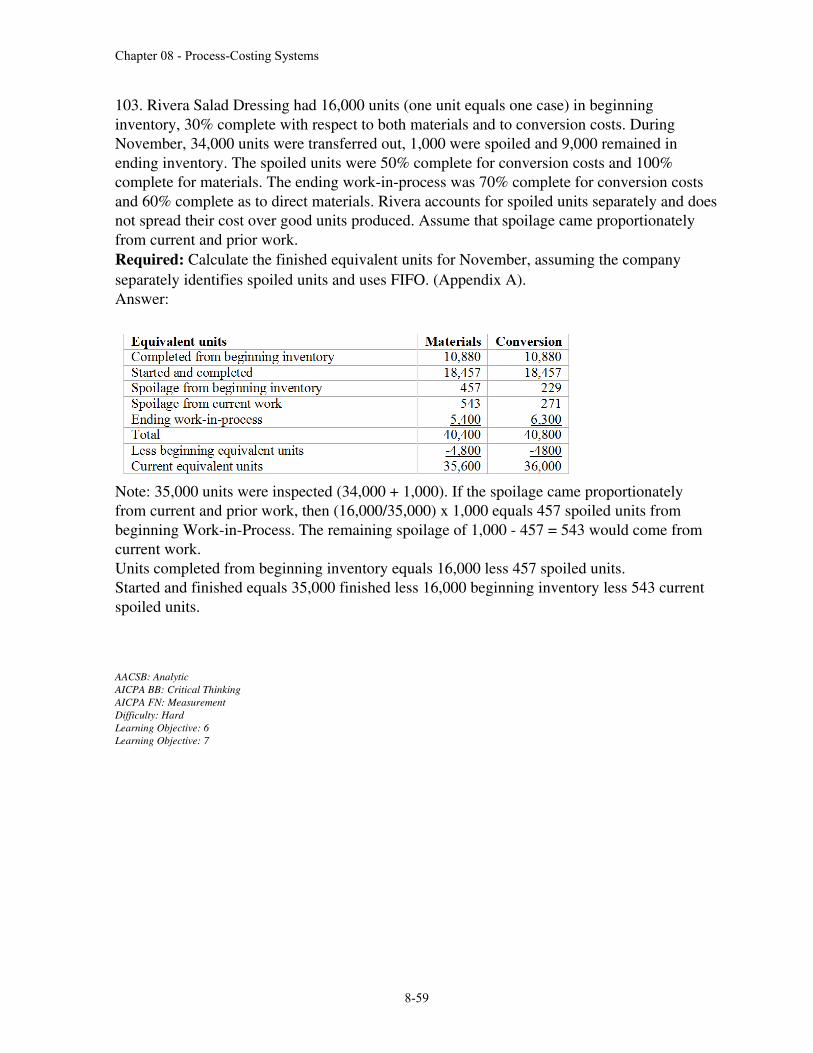

103. Rivera Salad Dressing had 16,000 units (one unit equals one case) in beginning inventory, 30% complete with respect to both materials and to conversion costs. During November, 34,000 units were transferred out, 1,000 were spoiled and 9,000 remained in ending inventory. The spoiled units were 50% complete for conversion costs and 100% complete for materials. The ending workinprocess was 70% complete for conversion costs and 60% complete as to direct materials. Rivera accounts for spoiled units separately and doesnot spread their cost over good units produced. Assume that spoilage came proportionately from current and prior work. Required: Calculate the finished equivalent units for November, assuming the company separately identifies spoiled units and uses FIFO. (Appendix A). Answer:

Note: 35,000 units were inspected (34,000 + 1,000). If the spoilage came proportionately from current and prior work, then (16,000/35,000) x 1,000 equals 457 spoiled units from beginning WorkinProcess. The remaining spoilage of 1,000 457 = 543 would come from current work.Units completed from beginning inventory equals 16,000 less 457 spoiled units.Started and finished equals 35,000 finished less 16,000 beginning inventory less 543 current spoiled units.

AACSB: AnalyticAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: HardLearning Objective: 6Learning Objective: 7

8-59

Chapter 08 - Process-Costing Systems

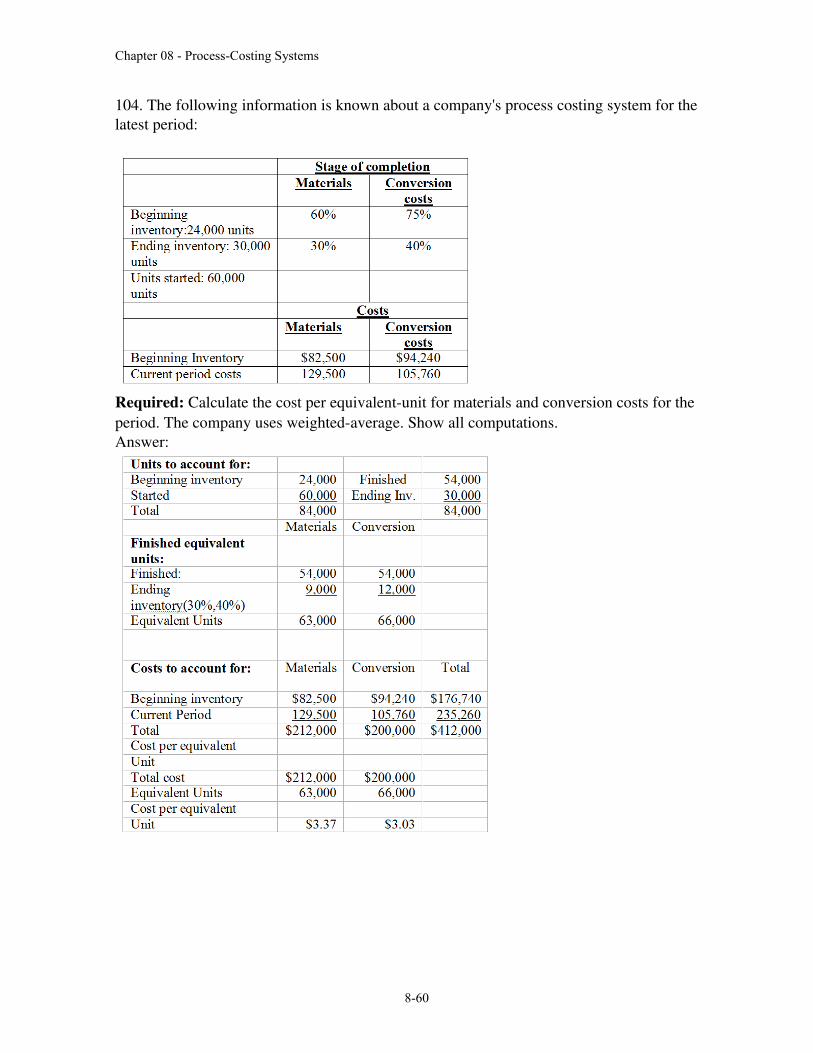

104. The following information is known about a company's process costing system for the latest period:

Required: Calculate the cost per equivalentunit for materials and conversion costs for the period. The company uses weightedaverage. Show all computations. Answer:

8-60

Chapter 08 - Process-Costing Systems

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

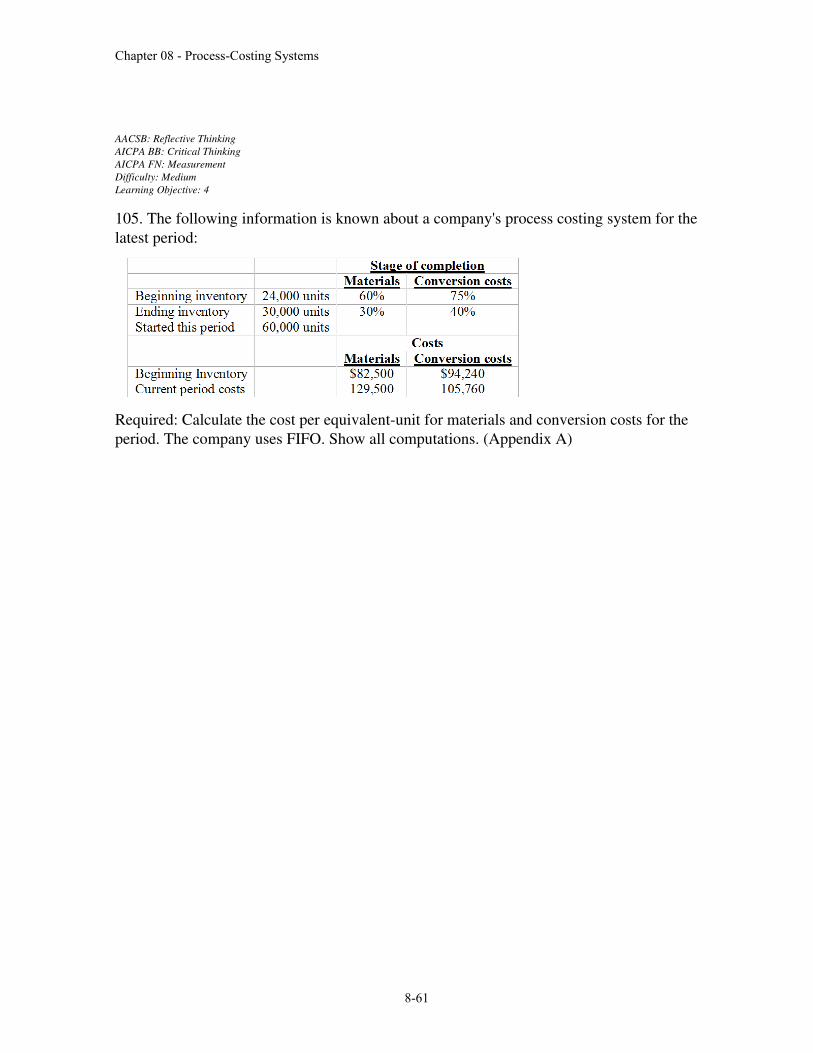

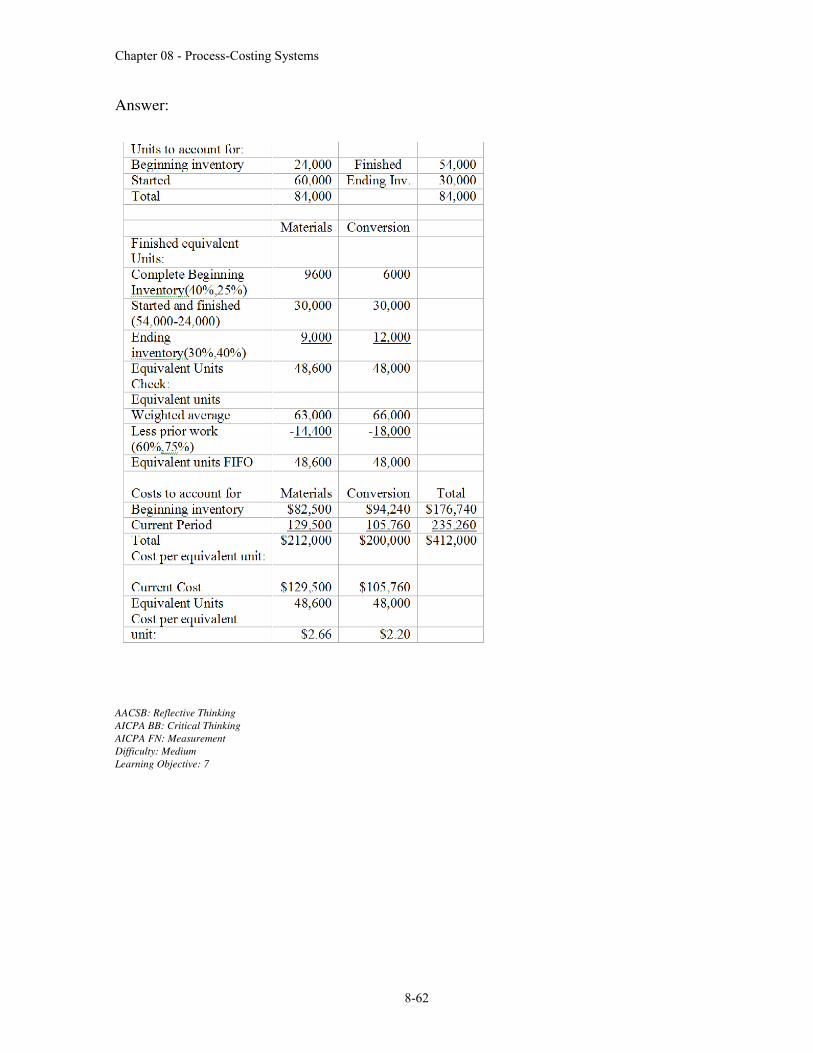

105. The following information is known about a company's process costing system for the latest period:

Required: Calculate the cost per equivalentunit for materials and conversion costs for the period. The company uses FIFO. Show all computations. (Appendix A)

8-61

Chapter 08 - Process-Costing Systems

Answer:

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 7

8-62

Chapter 08 - Process-Costing Systems

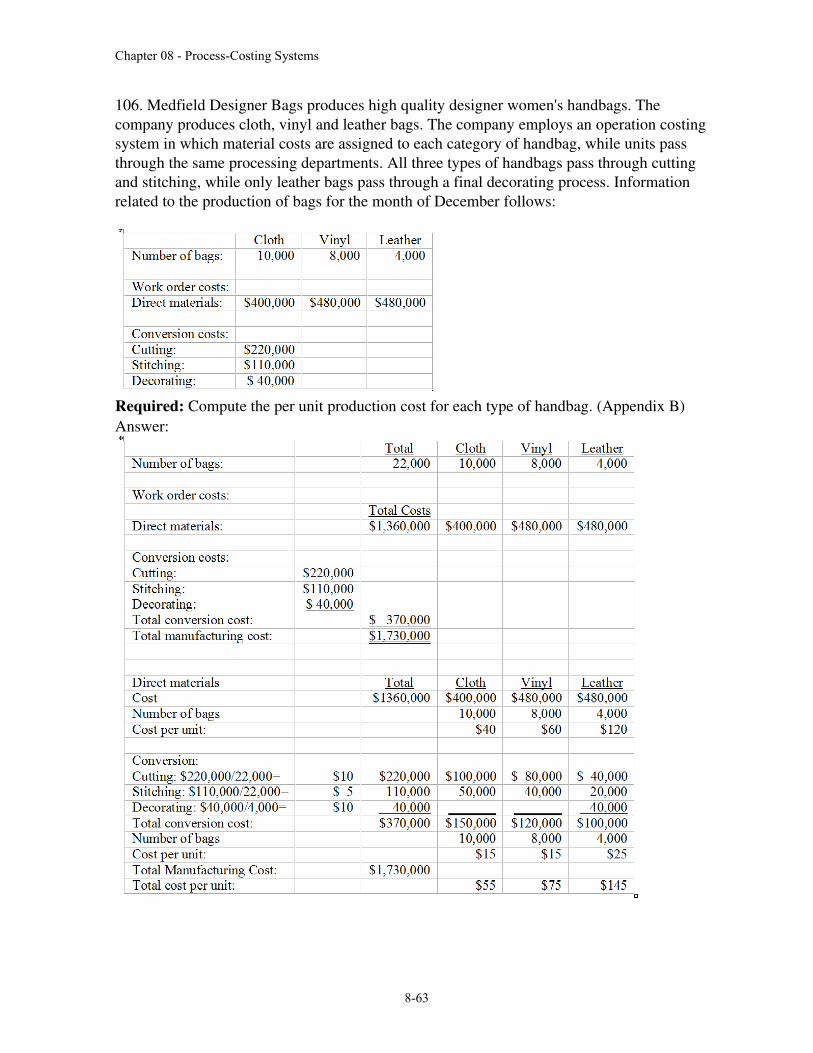

106. Medfield Designer Bags produces high quality designer women's handbags. The company produces cloth, vinyl and leather bags. The company employs an operation costing system in which material costs are assigned to each category of handbag, while units pass through the same processing departments. All three types of handbags pass through cutting and stitching, while only leather bags pass through a final decorating process. Information related to the production of bags for the month of December follows:

Required: Compute the per unit production cost for each type of handbag. (Appendix B) Answer:

8-63

Chapter 08 - Process-Costing Systems

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 9

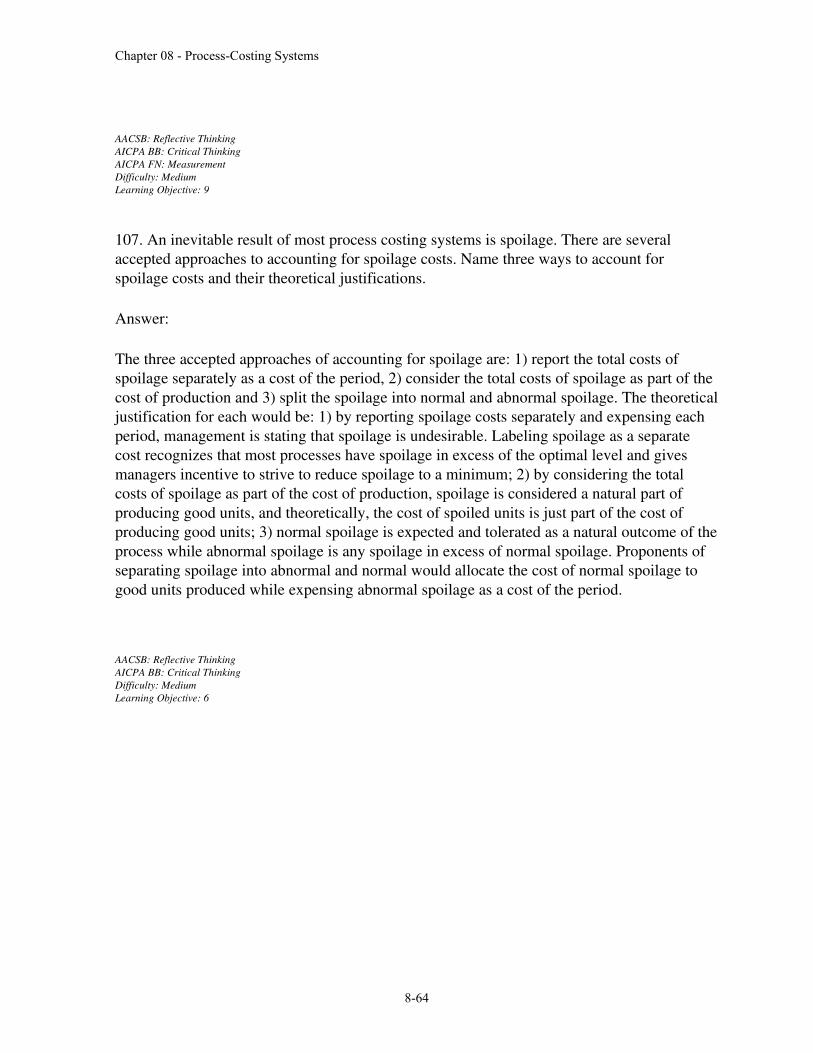

107. An inevitable result of most process costing systems is spoilage. There are several accepted approaches to accounting for spoilage costs. Name three ways to account for spoilage costs and their theoretical justifications.

Answer:

The three accepted approaches of accounting for spoilage are: 1) report the total costs of spoilage separately as a cost of the period, 2) consider the total costs of spoilage as part of the cost of production and 3) split the spoilage into normal and abnormal spoilage. The theoreticaljustification for each would be: 1) by reporting spoilage costs separately and expensing each period, management is stating that spoilage is undesirable. Labeling spoilage as a separate cost recognizes that most processes have spoilage in excess of the optimal level and gives managers incentive to strive to reduce spoilage to a minimum; 2) by considering the total costs of spoilage as part of the cost of production, spoilage is considered a natural part of producing good units, and theoretically, the cost of spoiled units is just part of the cost of producing good units; 3) normal spoilage is expected and tolerated as a natural outcome of theprocess while abnormal spoilage is any spoilage in excess of normal spoilage. Proponents of separating spoilage into abnormal and normal would allocate the cost of normal spoilage to good units produced while expensing abnormal spoilage as a cost of the period.

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 6

8-64

Chapter 08 - Process-Costing Systems

108. What is the advantage of using a FIFO processcosting system over a Weighted average system? Are there any situations where FIFO and Weighted average will give the same per unit cost? (Appendix) Answer:

FIFO separates the current period's production and costs from the prior period's production and costs. In situations where cost control is critical, this is an important advantage. Managerswill be able to compare the specific current per unit costs of manufacturing with those of the prior period. Managers have a structured way to help control costs. The FIFO and Weightedaverage will result in the same per unit cost if there is no beginning inventory. All costs and all effort will be associated with the same units, with no costs or effort carried over from priorperiods.

AACSB: AnalyticAICPA BB: Critical ThinkingDifficulty: MediumLearning Objective: 8

109. Explain how earnings of a period can be manipulated by misstating the degrees of completion of finished equivalents units to result in higher profit. Can this practice be continued indefinitely?

Answer:

To overstate profits, the company would want to understate the cost of each unit produced andsold. Since the cost per unit is determined by the number of equivalent units, overstating the percent complete in the ending inventory will understate the cost per equivalent unit, understate the cost of units transferred out and ultimately understate the cost of goods sold associated with those units. The ending workinprocess inventory will contain more cost thanit would have otherwise, since less cost is being transferred out to Finished Goods. To continue to understate cost of goods sold, increasingly higher percentages would have to be applied to the degree of completion of the ending inventory. Since the highest possible degreeof completion is 100%, an audit of the units in inventory would reveal the fact that their percentage of completion is being overstated. It is unlikely that such a plan would succeed beyond a few accounting periods.

AACSB: AnalyticAACSB: EthicsAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

8-65

Chapter 08 - Process-Costing Systems

8-66

Chapter 08 - Process-Costing Systems

110. What is operation costing? Briefly explain how operation costing is similar to and differsfrom processcosting. What type of company would most likely use operation costing? How is operating costing like joborder costing? (Appendix) Answer:

Operation costing is a hybrid method that combines features of joborder and processcosting.It is used when goods or services are semi customized but the basic units and conversion processes are similar. Typically, a company that uses a variety of materials which can differ greatly in cost might use operation costing. Direct materials costs can be traced to specific units as in joborder costing, while the cost of conversion may be similar to a traditional process costing system. Examples would be an auto manufacturer where the basic model is produced on a line with other models, but interior seats and other accessories are customized or a computer manufacturer where the customer orders specific items to go into a standard "box."

AACSB: Reflective ThinkingAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 9

111. How would a company manipulate the degrees of completion to understate profits, resulting in lower income taxes? Can this practice be continued indefinitely?

Answer: To understate profits, the company would overstate the cost of each unit produced and sold. Since cost per unit is determined by the number of equivalent units, understating the percent complete in the ending inventory will overstate the cost per equivalent unit, overstate the cost of units transferred out and ultimately overstate the cost of goods sold associated with those units. The ending workinprocess will contain relatively less cost than it would have otherwise, since more cost is being transferred out to Finished Goods. To continue to overstate cost of goods sold, increasingly lower percentages would have to be applied to the degree of completion of the ending inventory. Since the lowest possible degree of completion is 0% or no inventory, an audit of the units in inventory would reveal the fact that their percentage of completion is being understated. It is unlikely that such a plan would succeed beyond a few accounting periods.

AACSB: AnalyticAACSB: EthicsAICPA BB: Critical ThinkingAICPA FN: MeasurementDifficulty: MediumLearning Objective: 4

8-67