Embed Size (px)

Citation preview

1

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

1) SurveydataandcompanyresultssuggestthatgrowthintheUSbeautymarkethasbeenpolarized,withlower-priceretailersandbeautyspecialiststoreshavingwonshare.

2) Millennials’frugalshoppinghabitsanddesireforqualityexperienceslooktobedrivingthistrend.

3) SurveydatafromProsperInsights&AnalyticssuggestthatWalmartandTargethavegrowntheirbeautyshoppernumbersinrecentyears.SephoraandUltahavegrownfast,too.

4) SurveysshowthatAmazonisthefifth-most-popularretailerforskincareandcosmeticsandthetoponlinedestinationforbeauty.

5) AkeylessonforbeautyretailersisonethatappliesacrossanumberofsectorsinwhichrivalsarecompetingwithAmazon:eithercultivateaconvincingcategoryspecialtyorfocusonlowprices.

Deep Dive: Channel Shifts in US

Beauty Retailing— Sephora, Ulta and

Amazon Carving Greater Share

Deborah Weinswig

Managing Director,

FGRT

US: 917.655.6790

HK: 852.6119.1779

CN: 86.186.1420.3016

2

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

TableofContents

ExecutiveSummary.........................................................................................................................................3Introduction:ChangingShoppingHabits..............................................................................................................4ChartingChannelShifts:SpecialistRetailersOvertakeDepartmentStoresasAmerica’sFavoriteBeautyStores

................................................................................................................................................................................5WhereConsumersShop:Walmart,TargetandAmazonAreHighlyPopular.......................................................6

YoungConsumersOverindexatValueandSpecialistRetailers........................................................................8InFocus:UltaandSephoraDominateSpecialistRetailing.................................................................................11

UltaandSephoraGrowingStrongly................................................................................................................12

WhyConsumersShopatUltaandSephora.....................................................................................................13InFocus:E-CommerceandAmazon...................................................................................................................14

FocusingonAmazon,theMostPopularOnlineDestinationforBeautyandPersonalCareProducts...............16KeyTakeaways...................................................................................................................................................19FurtherReadingfromFGRT................................................................................................................................19

3

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

ExecutiveSummaryIntheUS,youngerconsumersappeartobedrivingshiftsinthebeautyretaillandscape.

• Lower-priceretailerssuchasWalmartandTargethavegrowntheirshareofbeautyshoppers,accordingtosurveysbyProsperInsights&Analytics,andyoungershoppersaremuchmorelikelythanoldergenerationstoshopforbeautyproductsatTarget.

• SpecialistchainsSephoraandUltahavegrownsalesfast,too.Theyareincreasingtheirstorefootprintsandhaveuppedtheirshareofbeautyshoppers—andyoungshopperssignificantlyoverindexatthesechains.

TheseshiftssuggestapolarizationofgrowthintheUSbeautyretailmarket.

AccordingtoProspersurveys,lowerpricesareastrongmotivatorforshoppingforhealthandbeautyproductsatWalmart,TargetandAmazon,andpriceisthemostimportantfactoroverallwhenconsumersaredecidingwheretobuysuchproducts.Bycontrast,thetopthreereasonsconsumersshopforhealthandbeautyitemsatUltaareselection,qualityandpromotionsandthetopreasonstheyshopatSephoraarequality,selectionandbrandsavailable,accordingtoProspersurveys.

ThestrongpriceappealofAmazonsuggeststhatitcould,intime,disruptthegrowthinshoppernumbersthatlower-price,store-basedretailershaveenjoyed.Byshoppernumbers,Amazonisthefifth-most-popularretailerforskincareandcosmeticspurchases,accordingtoProsper,anditisthemostpopularonlineretailerforbeauty,perA.T.Kearney.

Surveydatasuggestthatsomedrugstoresanddepartmentstoresoverindexamongoldershoppers.Toattractyoungershoppers,theseretailerscouldconsiderstrengtheningtheirentry-levelbeautyranges,introducingorbolsteringbeautyloyaltyprogramsand,wherepractical,offeringin-storebeautyservices.

Source:iStockphoto

4

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

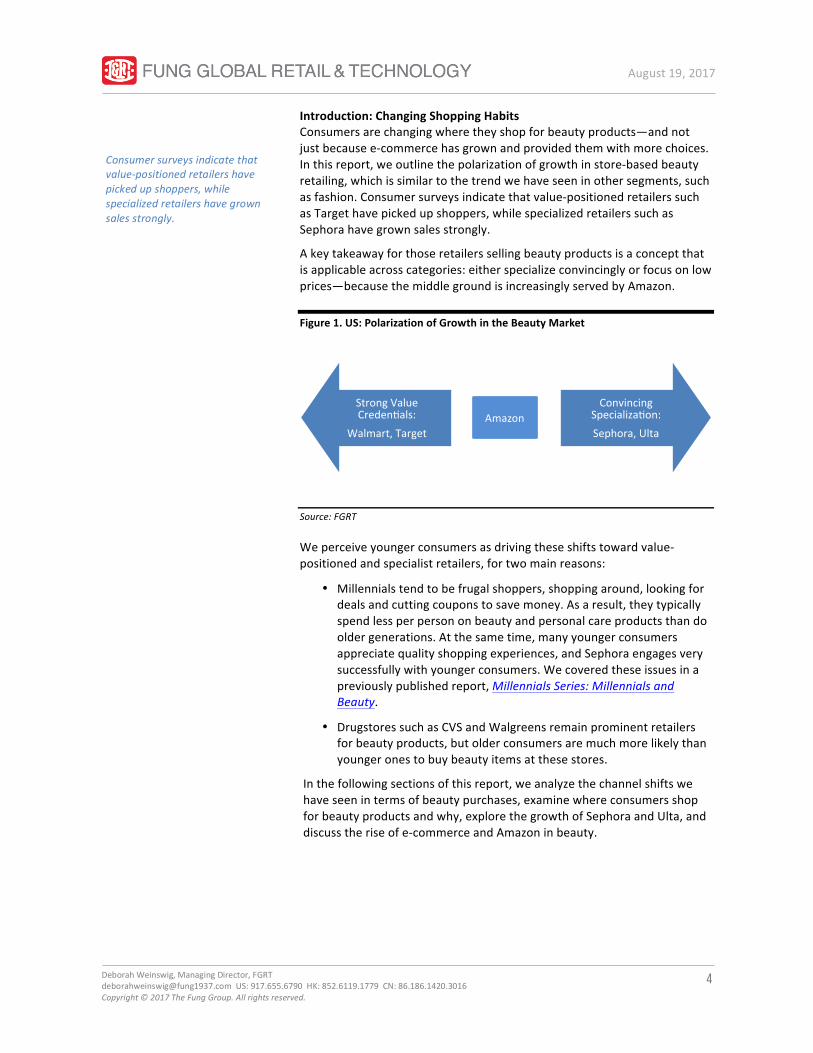

Introduction:ChangingShoppingHabitsConsumersarechangingwheretheyshopforbeautyproducts—andnotjustbecausee-commercehasgrownandprovidedthemwithmorechoices.Inthisreport,weoutlinethepolarizationofgrowthinstore-basedbeautyretailing,whichissimilartothetrendwehaveseeninothersegments,suchasfashion.Consumersurveysindicatethatvalue-positionedretailerssuchasTargethavepickedupshoppers,whilespecializedretailerssuchasSephorahavegrownsalesstrongly.

Akeytakeawayforthoseretailerssellingbeautyproductsisaconceptthatisapplicableacrosscategories:eitherspecializeconvincinglyorfocusonlowprices—becausethemiddlegroundisincreasinglyservedbyAmazon.

Figure1.US:PolarizationofGrowthintheBeautyMarket

Source:FGRT

Weperceiveyoungerconsumersasdrivingtheseshiftstowardvalue-positionedandspecialistretailers,fortwomainreasons:

• Millennialstendtobefrugalshoppers,shoppingaround,lookingfordealsandcuttingcouponstosavemoney.Asaresult,theytypicallyspendlessperpersononbeautyandpersonalcareproductsthandooldergenerations.Atthesametime,manyyoungerconsumersappreciatequalityshoppingexperiences,andSephoraengagesverysuccessfullywithyoungerconsumers.Wecoveredtheseissuesinapreviouslypublishedreport,MillennialsSeries:MillennialsandBeauty.

• DrugstoressuchasCVSandWalgreensremainprominentretailersforbeautyproducts,butolderconsumersaremuchmorelikelythanyoungeronestobuybeautyitemsatthesestores.

Inthefollowingsectionsofthisreport,weanalyzethechannelshiftswehaveseenintermsofbeautypurchases,examinewhereconsumersshopforbeautyproductsandwhy,explorethegrowthofSephoraandUlta,anddiscusstheriseofe-commerceandAmazoninbeauty.

Consumersurveysindicatethatvalue-positionedretailershavepickedupshoppers,whilespecializedretailershavegrownsalesstrongly.

StrongValueCredendals:

Walmart,Target

ConvincingSpecializadon:Sephora,Ulta

Amazon

5

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

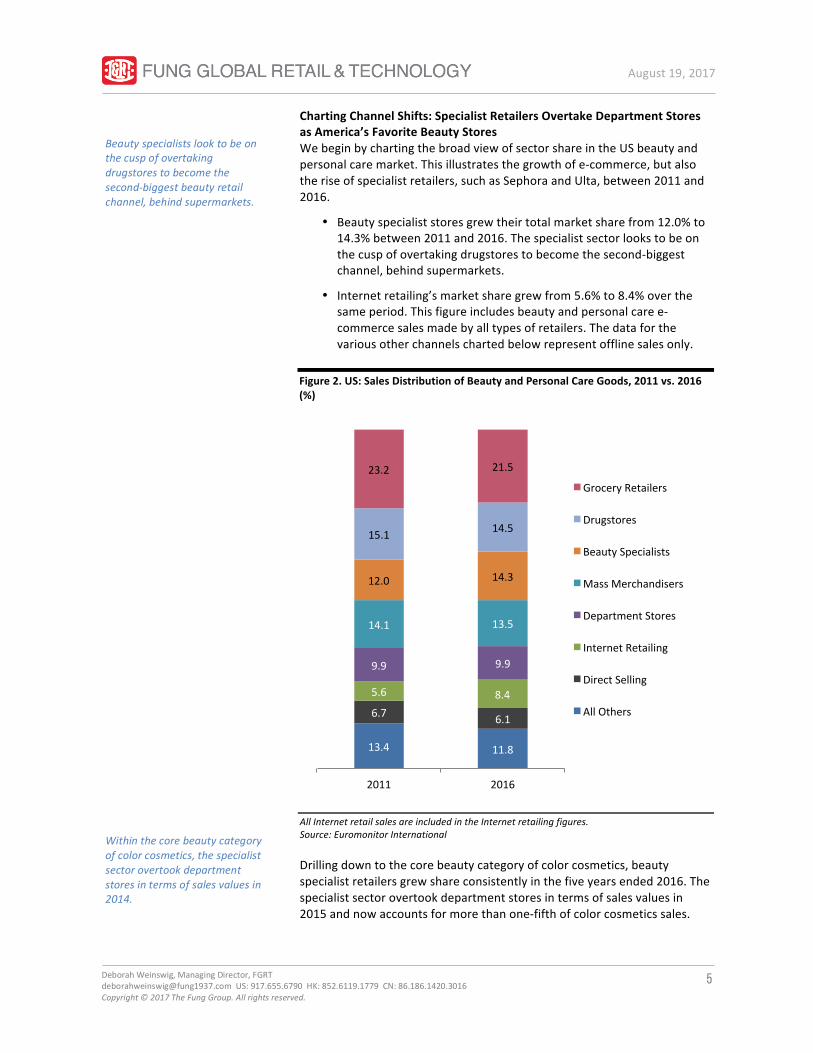

ChartingChannelShifts:SpecialistRetailersOvertakeDepartmentStoresasAmerica’sFavoriteBeautyStoresWebeginbychartingthebroadviewofsectorshareintheUSbeautyandpersonalcaremarket.Thisillustratesthegrowthofe-commerce,butalsotheriseofspecialistretailers,suchasSephoraandUlta,between2011and2016.

• Beautyspecialiststoresgrewtheirtotalmarketsharefrom12.0%to14.3%between2011and2016.Thespecialistsectorlookstobeonthecuspofovertakingdrugstorestobecomethesecond-biggestchannel,behindsupermarkets.

• Internetretailing’smarketsharegrewfrom5.6%to8.4%overthesameperiod.Thisfigureincludesbeautyandpersonalcaree-commercesalesmadebyalltypesofretailers.Thedataforthevariousotherchannelschartedbelowrepresentofflinesalesonly.

Figure2.US:SalesDistributionofBeautyandPersonalCareGoods,2011vs.2016(%)

AllInternetretailsalesareincludedintheInternetretailingfigures.Source:EuromonitorInternational

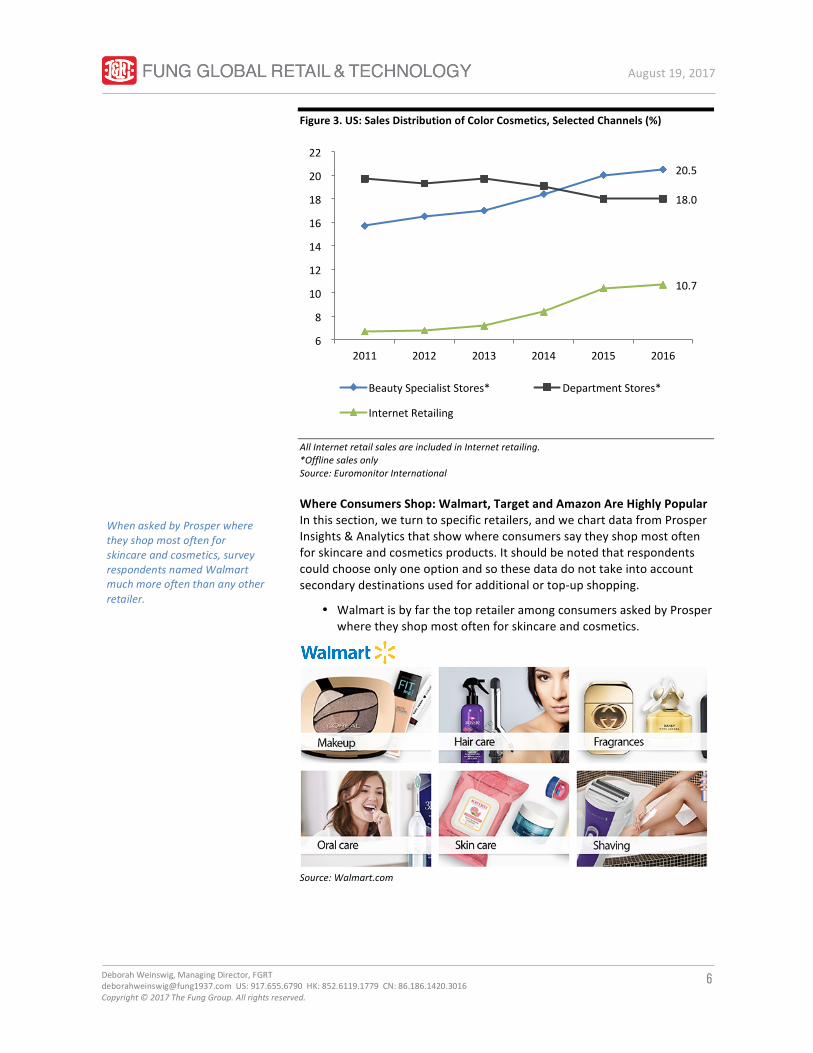

Drillingdowntothecorebeautycategoryofcolorcosmetics,beautyspecialistretailersgrewshareconsistentlyinthefiveyearsended2016.Thespecialistsectorovertookdepartmentstoresintermsofsalesvaluesin2015andnowaccountsformorethanone-fifthofcolorcosmeticssales.

13.4 11.8

6.7 6.1

5.6 8.4

9.9 9.9

14.1 13.5

12.0 14.3

15.1 14.5

23.2 21.5

2011 2016

GroceryRetailers

Drugstores

BeautySpecialists

MassMerchandisers

DepartmentStores

InternetRetailing

DirectSelling

AllOthers

Beautyspecialistslooktobeonthecuspofovertakingdrugstorestobecomethesecond-biggestbeautyretailchannel,behindsupermarkets.

Withinthecorebeautycategoryofcolorcosmetics,thespecialistsectorovertookdepartmentstoresintermsofsalesvaluesin2014.

6

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure3.US:SalesDistributionofColorCosmetics,SelectedChannels(%)

AllInternetretailsalesareincludedinInternetretailing.*OfflinesalesonlySource:EuromonitorInternational

WhereConsumersShop:Walmart,TargetandAmazonAreHighlyPopularInthissection,weturntospecificretailers,andwechartdatafromProsperInsights&Analyticsthatshowwhereconsumerssaytheyshopmostoftenforskincareandcosmeticsproducts.Itshouldbenotedthatrespondentscouldchooseonlyoneoptionandsothesedatadonottakeintoaccountsecondarydestinationsusedforadditionalortop-upshopping.

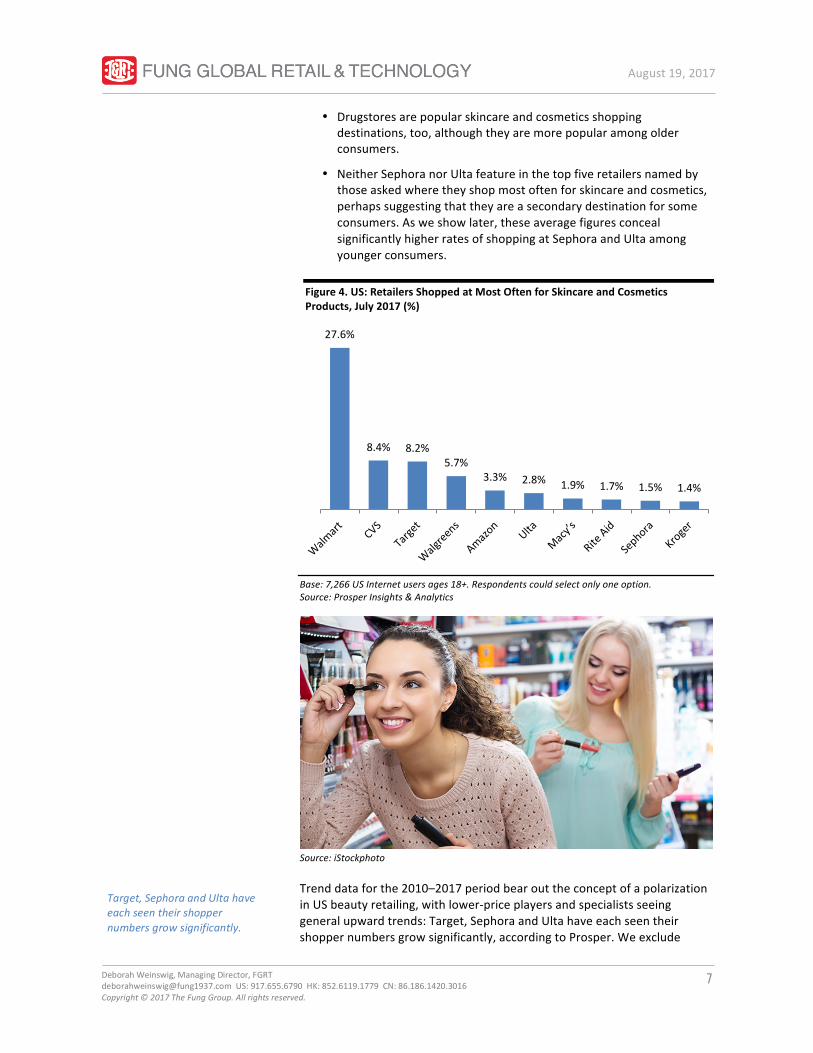

• WalmartisbyfarthetopretaileramongconsumersaskedbyProsperwheretheyshopmostoftenforskincareandcosmetics.

Source:Walmart.com

20.5

18.0

10.7

6

8

10

12

14

16

18

20

22

2011 2012 2013 2014 2015 2016

BeautySpecialistStores* DepartmentStores*

InternetRetailing

WhenaskedbyProsperwheretheyshopmostoftenforskincareandcosmetics,surveyrespondentsnamedWalmartmuchmoreoftenthananyotherretailer.

7

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

• Drugstoresarepopularskincareandcosmeticsshoppingdestinations,too,althoughtheyaremorepopularamongolderconsumers.

• NeitherSephoranorUltafeatureinthetopfiveretailersnamedbythoseaskedwheretheyshopmostoftenforskincareandcosmetics,perhapssuggestingthattheyareasecondarydestinationforsomeconsumers.Asweshowlater,theseaveragefiguresconcealsignificantlyhigherratesofshoppingatSephoraandUltaamongyoungerconsumers.

Figure4.US:RetailersShoppedatMostOftenforSkincareandCosmeticsProducts,July2017(%)

Base:7,266USInternetusersages18+.Respondentscouldselectonlyoneoption.Source:ProsperInsights&Analytics

Source:iStockphoto

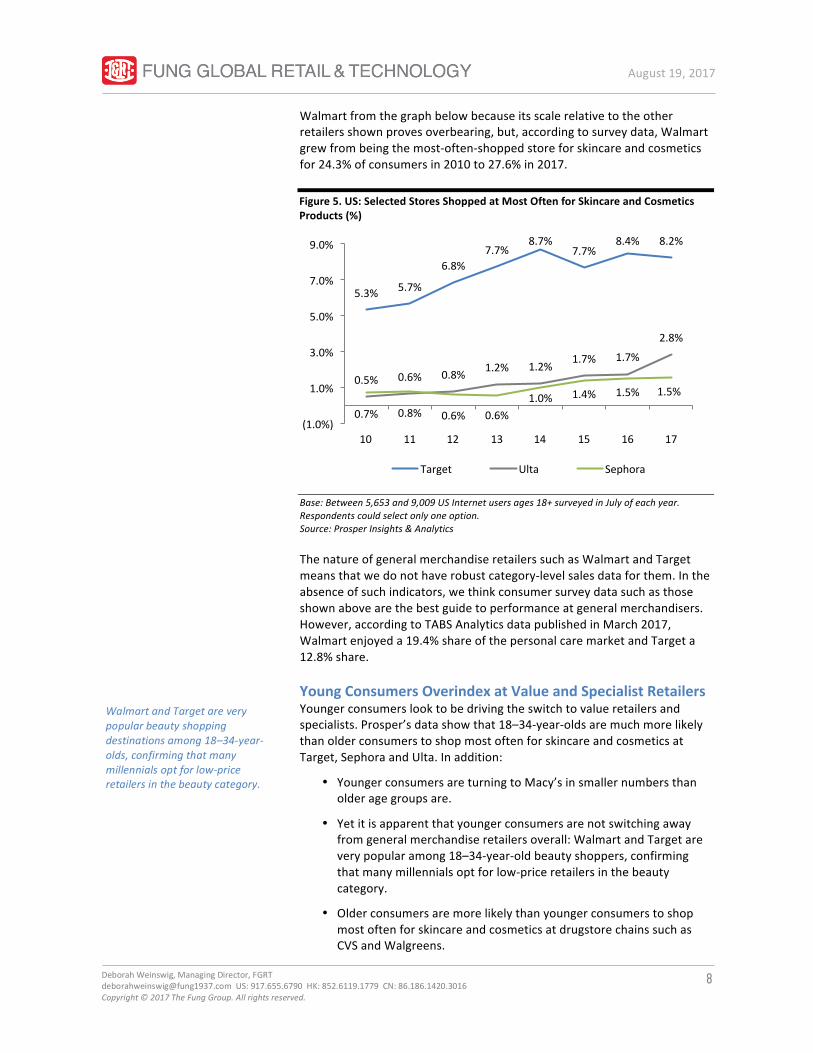

Trenddataforthe2010–2017periodbearouttheconceptofapolarizationinUSbeautyretailing,withlower-priceplayersandspecialistsseeinggeneralupwardtrends:Target,SephoraandUltahaveeachseentheirshoppernumbersgrowsignificantly,accordingtoProsper.Weexclude

27.6%

8.4% 8.2%5.7%

3.3% 2.8% 1.9% 1.7% 1.5% 1.4%

Target,SephoraandUltahaveeachseentheirshoppernumbersgrowsignificantly.

8

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Walmartfromthegraphbelowbecauseitsscalerelativetotheotherretailersshownprovesoverbearing,but,accordingtosurveydata,Walmartgrewfrombeingthemost-often-shoppedstoreforskincareandcosmeticsfor24.3%ofconsumersin2010to27.6%in2017.

Figure5.US:SelectedStoresShoppedatMostOftenforSkincareandCosmeticsProducts(%)

Base:Between5,653and9,009USInternetusersages18+surveyedinJulyofeachyear.Respondentscouldselectonlyoneoption.Source:ProsperInsights&Analytics

ThenatureofgeneralmerchandiseretailerssuchasWalmartandTargetmeansthatwedonothaverobustcategory-levelsalesdataforthem.Intheabsenceofsuchindicators,wethinkconsumersurveydatasuchasthoseshownabovearethebestguidetoperformanceatgeneralmerchandisers.However,accordingtoTABSAnalyticsdatapublishedinMarch2017,Walmartenjoyeda19.4%shareofthepersonalcaremarketandTargeta12.8%share.

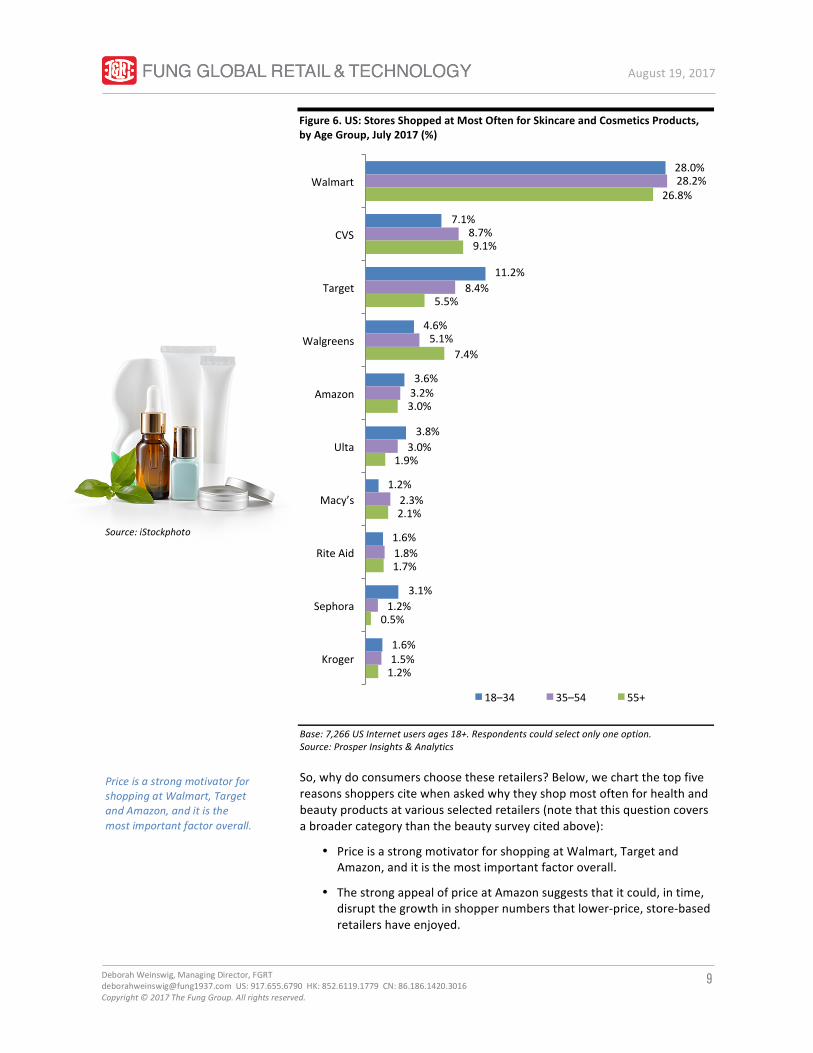

YoungConsumersOverindexatValueandSpecialistRetailersYoungerconsumerslooktobedrivingtheswitchtovalueretailersandspecialists.Prosper’sdatashowthat18–34-year-oldsaremuchmorelikelythanolderconsumerstoshopmostoftenforskincareandcosmeticsatTarget,SephoraandUlta.Inaddition:

• YoungerconsumersareturningtoMacy’sinsmallernumbersthanolderagegroupsare.

• Yetitisapparentthatyoungerconsumersarenotswitchingawayfromgeneralmerchandiseretailersoverall:WalmartandTargetareverypopularamong18–34-year-oldbeautyshoppers,confirmingthatmanymillennialsoptforlow-priceretailersinthebeautycategory.

• OlderconsumersaremorelikelythanyoungerconsumerstoshopmostoftenforskincareandcosmeticsatdrugstorechainssuchasCVSandWalgreens.

5.3% 5.7%

6.8%7.7%

8.7%7.7%

8.4% 8.2%

0.5% 0.6% 0.8% 1.2% 1.2%1.7% 1.7%

2.8%

0.7% 0.8% 0.6% 0.6%1.0% 1.4% 1.5% 1.5%

(1.0%)

1.0%

3.0%

5.0%

7.0%

9.0%

10 11 12 13 14 15 16 17

Target Ulta Sephora

WalmartandTargetareverypopularbeautyshoppingdestinationsamong18–34-year-olds,confirmingthatmanymillennialsoptforlow-priceretailersinthebeautycategory.

9

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure6.US:StoresShoppedatMostOftenforSkincareandCosmeticsProducts,byAgeGroup,July2017(%)

Base:7,266USInternetusersages18+.Respondentscouldselectonlyoneoption.Source:ProsperInsights&Analytics

So,whydoconsumerschoosetheseretailers?Below,wechartthetopfivereasonsshopperscitewhenaskedwhytheyshopmostoftenforhealthandbeautyproductsatvariousselectedretailers(notethatthisquestioncoversabroadercategorythanthebeautysurveycitedabove):

• PriceisastrongmotivatorforshoppingatWalmart,TargetandAmazon,anditisthemostimportantfactoroverall.

• ThestrongappealofpriceatAmazonsuggeststhatitcould,intime,disruptthegrowthinshoppernumbersthatlower-price,store-basedretailershaveenjoyed.

28.0%

7.1%

11.2%

4.6%

3.6%

3.8%

1.2%

1.6%

3.1%

1.6%

28.2%

8.7%

8.4%

5.1%

3.2%

3.0%

2.3%

1.8%

1.2%

1.5%

26.8%

9.1%

5.5%

7.4%

3.0%

1.9%

2.1%

1.7%

0.5%

1.2%

Walmart

CVS

Target

Walgreens

Amazon

Ulta

Macy’s

RiteAid

Sephora

Kroger

18–34 35–54 55+

PriceisastrongmotivatorforshoppingatWalmart,TargetandAmazon,anditisthemostimportantfactoroverall.

Source:iStockphoto

10

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

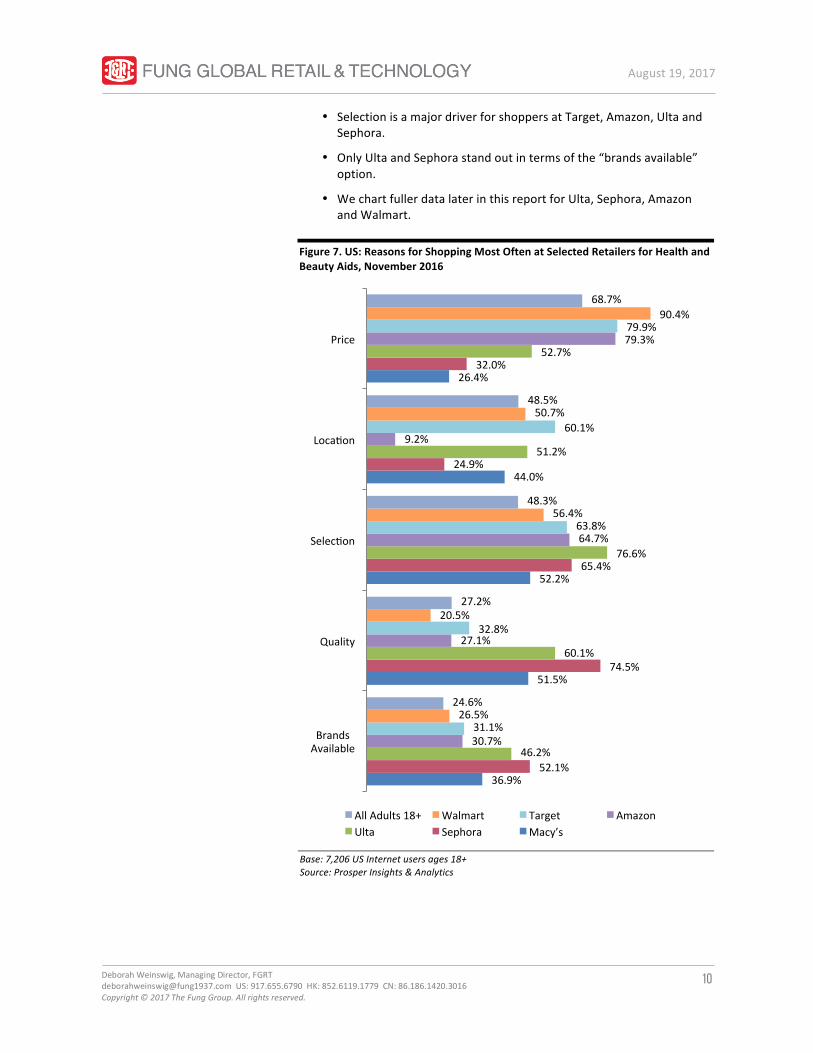

• SelectionisamajordriverforshoppersatTarget,Amazon,UltaandSephora.

• OnlyUltaandSephorastandoutintermsofthe“brandsavailable”option.

• WechartfullerdatalaterinthisreportforUlta,Sephora,AmazonandWalmart.

Figure7.US:ReasonsforShoppingMostOftenatSelectedRetailersforHealthandBeautyAids,November2016

Base:7,206USInternetusersages18+Source:ProsperInsights&Analytics

36.9%

51.5%

52.2%

44.0%

26.4%

52.1%

74.5%

65.4%

24.9%

32.0%

46.2%

60.1%

76.6%

51.2%

52.7%

30.7%

27.1%

64.7%

9.2%

79.3%

31.1%

32.8%

63.8%

60.1%

79.9%

26.5%

20.5%

56.4%

50.7%

90.4%

24.6%

27.2%

48.3%

48.5%

68.7%

BrandsAvailable

Quality

Selecdon

Locadon

Price

AllAdults18+ Walmart Target AmazonUlta Sephora Macy’s

11

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

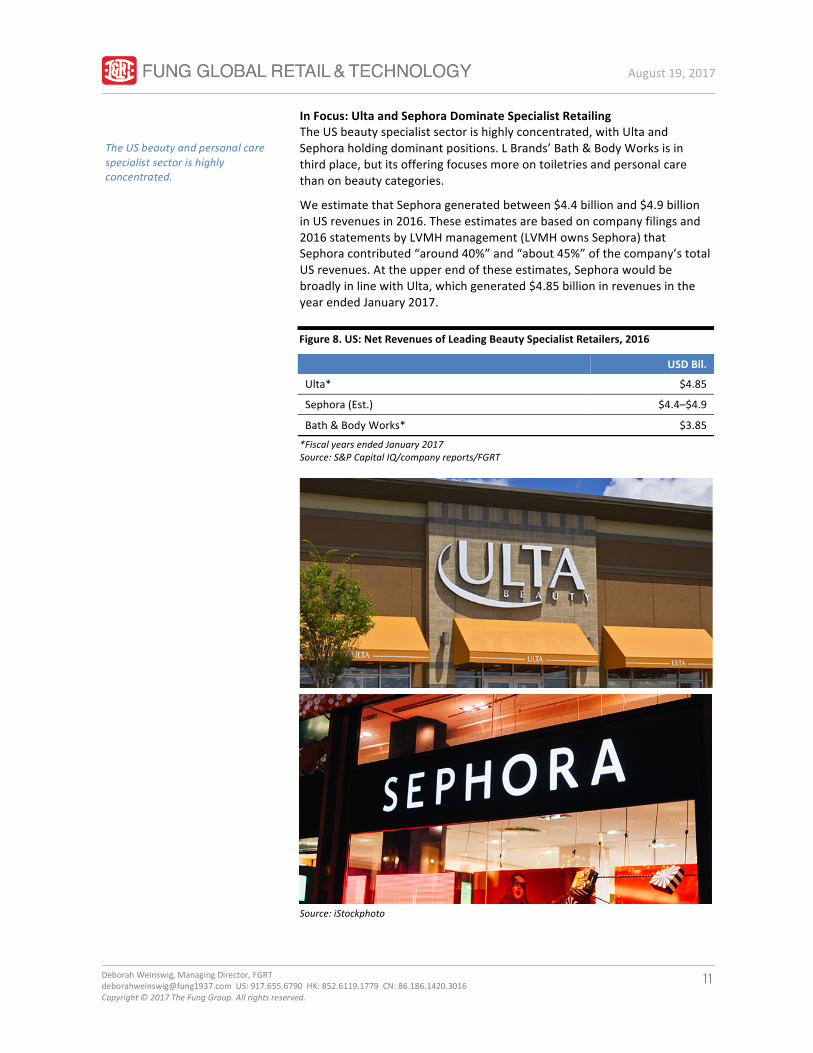

InFocus:UltaandSephoraDominateSpecialistRetailingTheUSbeautyspecialistsectorishighlyconcentrated,withUltaandSephoraholdingdominantpositions.LBrands’Bath&BodyWorksisinthirdplace,butitsofferingfocusesmoreontoiletriesandpersonalcarethanonbeautycategories.

WeestimatethatSephorageneratedbetween$4.4billionand$4.9billioninUSrevenuesin2016.Theseestimatesarebasedoncompanyfilingsand2016statementsbyLVMHmanagement(LVMHownsSephora)thatSephoracontributed“around40%”and“about45%”ofthecompany’stotalUSrevenues.Attheupperendoftheseestimates,SephorawouldbebroadlyinlinewithUlta,whichgenerated$4.85billioninrevenuesintheyearendedJanuary2017.

Figure8.US:NetRevenuesofLeadingBeautySpecialistRetailers,2016

USDBil.

Ulta* $4.85

Sephora(Est.) $4.4–$4.9

Bath&BodyWorks* $3.85

*FiscalyearsendedJanuary2017Source:S&PCapitalIQ/companyreports/FGRT

Source:iStockphoto

TheUSbeautyandpersonalcarespecialistsectorishighlyconcentrated.

12

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

UltaandSephoraGrowingStronglyAswechartbelow,Ultahaspostedveryimpressiverevenuegrowthinrecentyears,withtotalsalesgrowthsupportedbydouble-digitcompsandnewstoreopenings.Thegeneraltrendsinceearly2015hasbeenforrevenuegrowthtostrengthen.

Figure9.Ulta:TotalandComparableSalesGrowth(%)

Source:Companyreports

Banner-leveldisclosureislimitedforLVMH-ownedSephora,butLVMHhassharedthefollowingdetails:

• Initsfirst-half2017earningscall,LVMHmanagementnoteddouble-digitsalesgrowthforSephoraworldwide.

• Inthefirstquarterof2017,LVMHnoted“particularstrength”forSephorainNorthAmerica.

• LVMHpointedtoSephora’s“particularlyremarkableperformance”intheUSin2016.

• Initsfirst-half2016earningscall,LVMHmorespecificallynoteddouble-digitcompsforSephoraintheUSmarket.

SephoraandUltaarebothcapitalizingongrowingdemandtoexpandtheirphysicalpresence:

• Sephorahas357stand-aloneUSstores,accordingtothecompany’swebsite(accessedonJuly28).Inaddition,Sephorahas574shopsinsideJCPenneystores,againperthecompany’swebsite.InApril2017,JCPenneyannouncedplanstoopenafurther70Sephorashopsinitsdepartmentstoresandtoexpand32existingshops-in-shops.

• SephoraopenedaflagshipstoreinBostoninthefirsthalfof2017anditwillopenastoreattheWorldTradeCenterinNewYorkinthesecondhalfoftheyear.

• Ultahad990storesattheendofthefirstquarterof2017(latest);thefigurewasup12%yearoveryear.Across2017,Ultaplanstoopenaround100newstoresandremodel11others.

21.6

19.4

22.121.1

23.7

21.9

24.2 24.622.5

11.410.1

12.8 12.5

15.214.4

16.7 16.6

14.3

10

12

14

16

18

20

22

24

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Total Comps

13

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

WhyConsumersShopatUltaandSephoraEarlier,wediscussedthetopreasonsconsumersciteforshoppingatarangeofbeautyretailers.Inthissection,welookinmoredetailatthereasonstheyshopforhealthandbeautyproductsatSephoraandUlta,usingdatafromtheProspermonthlyconsumersurveyconductedinNovember2016:

• Priceranksrelativelylowasaconsiderationforshoppersateachchain,incontrasttoitbeingthetopconsiderationforhealthandbeautyshoppersoverall.

• UltanarrowlybeatsSephoraonselection,promotionsandprice.Ulta’sstrengthinpromotionsmayreflectitsverypopularloyaltyprogramanditsbonuspointsoffers,whileitsstrengthinpriceislikelydueinparttoitsentry-levelproductofferings.

• Sephoraenjoysaleadintermsofqualityandbrandsavailable—perhapsreflectingdemandforSephora’sownbrand.

Figure10.US:ReasonsforShoppingMostOftenatUltaandSephoraforHealthandBeautyAids,November2016

Samplesize:Sephoracustomers:N=101;Ultacustomers:N=148Source:ProsperInsights&Analytics

18.0%

20.0%

13.2%

16.0%

28.3%

17.4%

32.3%

26.7%

21.0%

52.1%

24.9%

32.0%

32.9%

74.5%

65.4%

11.9%

13.8%

14.4%

16.2%

18.9%

20.0%

23.4%

26.2%

30.6%

46.2%

51.2%

52.7%

58.0%

60.1%

76.6%

StoreExperience

EasytoNavigateWebsite

StoreLayout

KnowledgeableSalesPeople

TrustworthyRetailer

StoreAppearance

Service

UniqueProducts

FrequentShopperCard

BrandsAvailable

Locadon

Price

Promodons

Quality

Selecdon

Ulta

Sephora

UltanarrowlybeatsSephoraforselection,promotionsandprice.

14

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

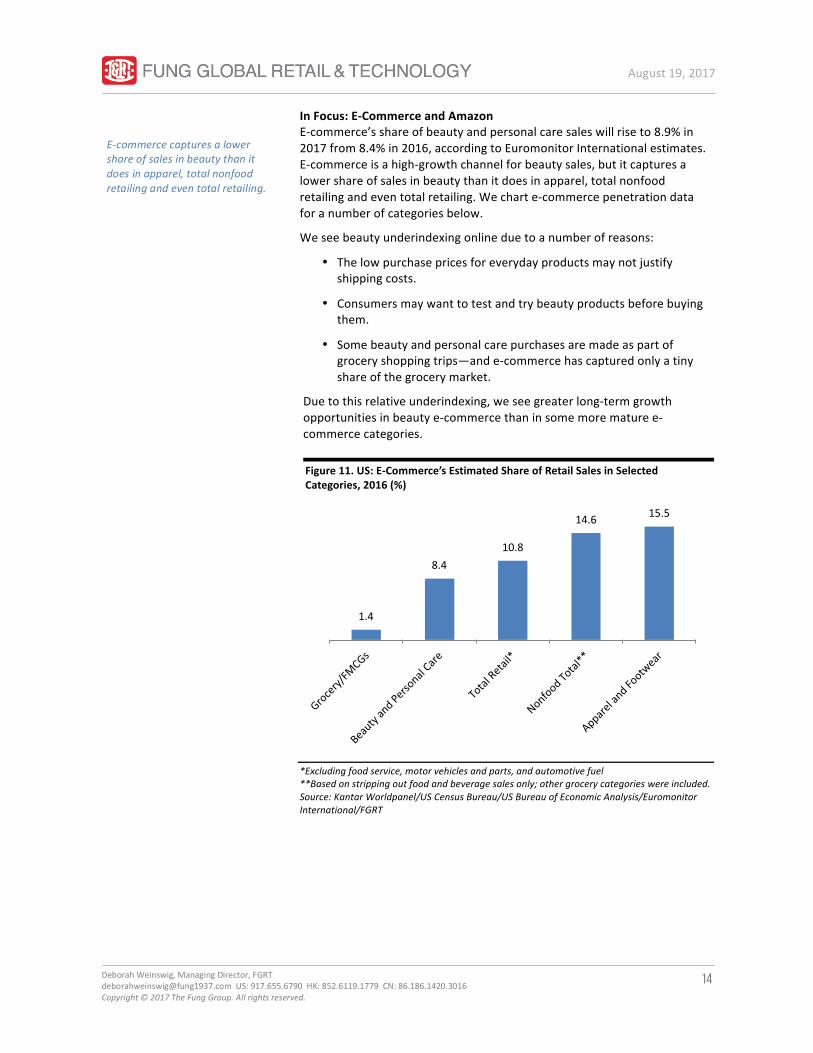

InFocus:E-CommerceandAmazonE-commerce’sshareofbeautyandpersonalcaresaleswillriseto8.9%in2017from8.4%in2016,accordingtoEuromonitorInternationalestimates.E-commerceisahigh-growthchannelforbeautysales,butitcapturesalowershareofsalesinbeautythanitdoesinapparel,totalnonfoodretailingandeventotalretailing.Wecharte-commercepenetrationdataforanumberofcategoriesbelow.

Weseebeautyunderindexingonlineduetoanumberofreasons:

• Thelowpurchasepricesforeverydayproductsmaynotjustifyshippingcosts.

• Consumersmaywanttotestandtrybeautyproductsbeforebuyingthem.

• Somebeautyandpersonalcarepurchasesaremadeaspartofgroceryshoppingtrips—ande-commercehascapturedonlyatinyshareofthegrocerymarket.

Duetothisrelativeunderindexing,weseegreaterlong-termgrowthopportunitiesinbeautye-commercethaninsomemorematuree-commercecategories.

Figure11.US:E-Commerce’sEstimatedShareofRetailSalesinSelectedCategories,2016(%)

*Excludingfoodservice,motorvehiclesandparts,andautomotivefuel**Basedonstrippingoutfoodandbeveragesalesonly;othergrocerycategorieswereincluded.Source:KantarWorldpanel/USCensusBureau/USBureauofEconomicAnalysis/EuromonitorInternational/FGRT

1.4

8.410.8

14.6 15.5

E-commercecapturesalowershareofsalesinbeautythanitdoesinapparel,totalnonfoodretailingandeventotalretailing.

15

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

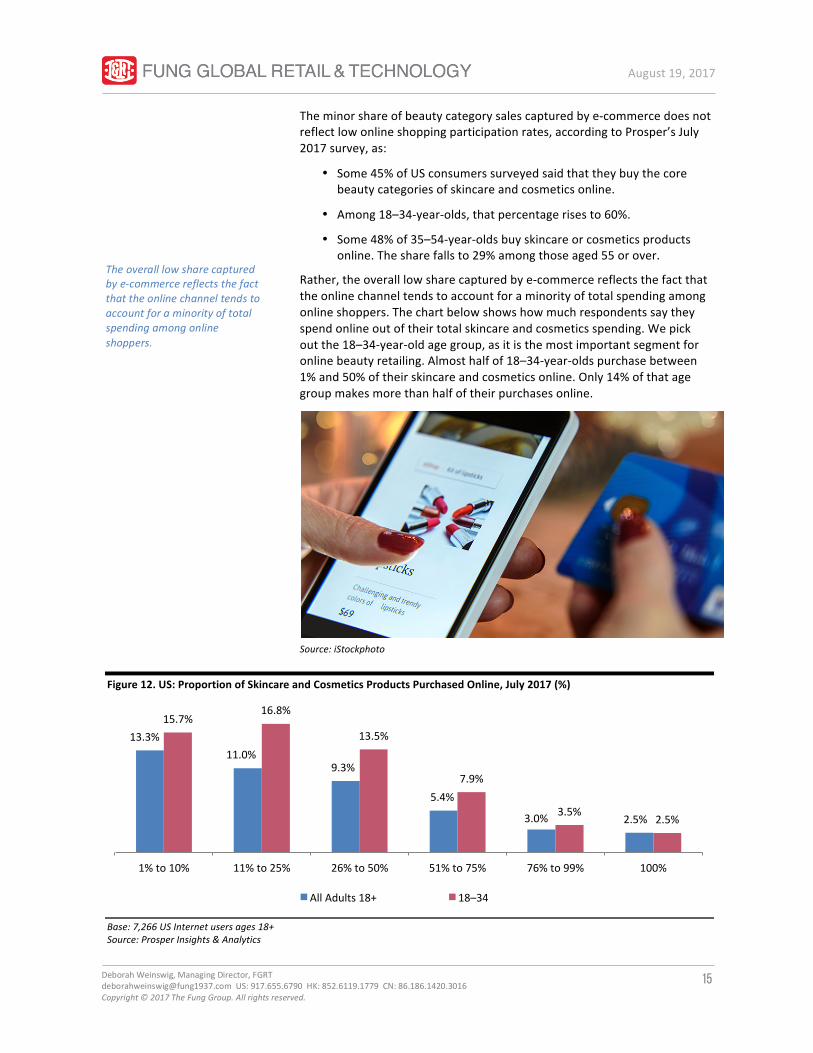

Theminorshareofbeautycategorysalescapturedbye-commercedoesnotreflectlowonlineshoppingparticipationrates,accordingtoProsper’sJuly2017survey,as:

• Some45%ofUSconsumerssurveyedsaidthattheybuythecorebeautycategoriesofskincareandcosmeticsonline.

• Among18–34-year-olds,thatpercentagerisesto60%.

• Some48%of35–54-year-oldsbuyskincareorcosmeticsproductsonline.Thesharefallsto29%amongthoseaged55orover.

Rather,theoveralllowsharecapturedbye-commercereflectsthefactthattheonlinechanneltendstoaccountforaminorityoftotalspendingamongonlineshoppers.Thechartbelowshowshowmuchrespondentssaytheyspendonlineoutoftheirtotalskincareandcosmeticsspending.Wepickoutthe18–34-year-oldagegroup,asitisthemostimportantsegmentforonlinebeautyretailing.Almosthalfof18–34-year-oldspurchasebetween1%and50%oftheirskincareandcosmeticsonline.Only14%ofthatagegroupmakesmorethanhalfoftheirpurchasesonline.

Source:iStockphoto

Figure12.US:ProportionofSkincareandCosmeticsProductsPurchasedOnline,July2017(%)

Base:7,266USInternetusersages18+Source:ProsperInsights&Analytics

Theoveralllowsharecapturedbye-commercereflectsthefactthattheonlinechanneltendstoaccountforaminorityoftotalspendingamongonlineshoppers.

13.3%11.0%

9.3%

5.4%

3.0% 2.5%

15.7%16.8%

13.5%

7.9%

3.5%2.5%

1%to10% 11%to25% 26%to50% 51%to75% 76%to99% 100%

AllAdults18+ 18–34

16

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

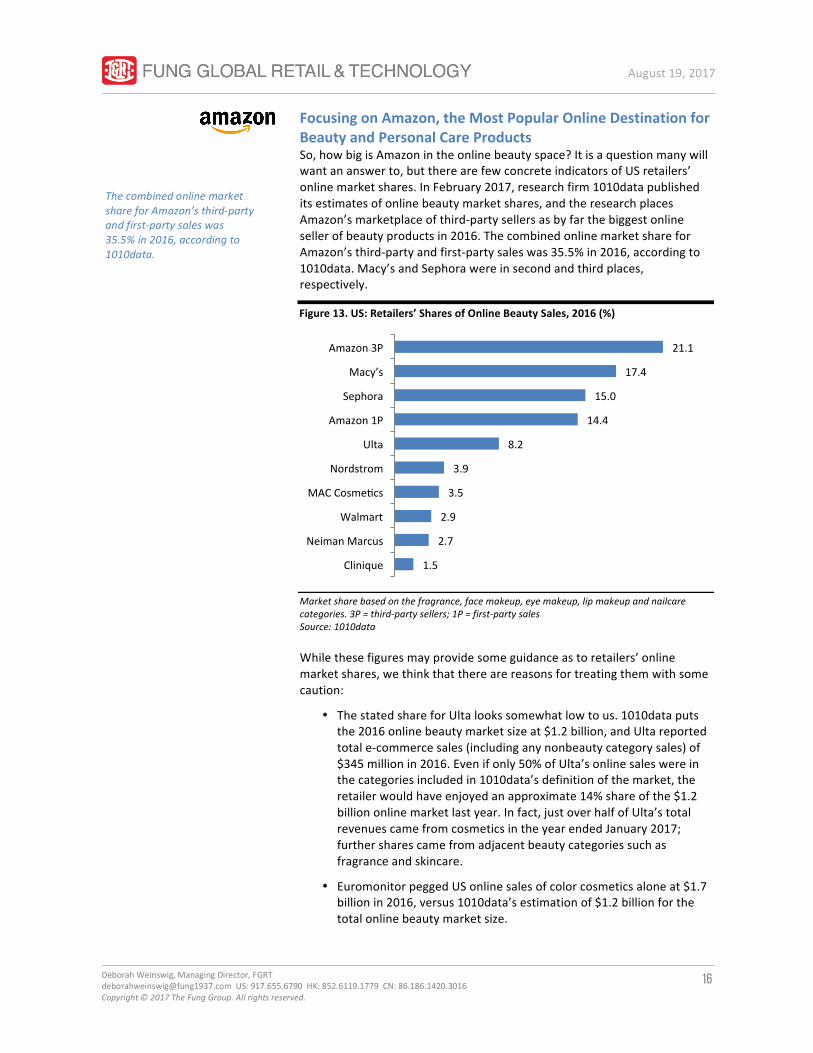

FocusingonAmazon,theMostPopularOnlineDestinationforBeautyandPersonalCareProductsSo,howbigisAmazonintheonlinebeautyspace?Itisaquestionmanywillwantananswerto,buttherearefewconcreteindicatorsofUSretailers’onlinemarketshares.InFebruary2017,researchfirm1010datapublisheditsestimatesofonlinebeautymarketshares,andtheresearchplacesAmazon’smarketplaceofthird-partysellersasbyfarthebiggestonlinesellerofbeautyproductsin2016.ThecombinedonlinemarketshareforAmazon’sthird-partyandfirst-partysaleswas35.5%in2016,accordingto1010data.Macy’sandSephorawereinsecondandthirdplaces,respectively.

Figure13.US:Retailers’SharesofOnlineBeautySales,2016(%)

Marketsharebasedonthefragrance,facemakeup,eyemakeup,lipmakeupandnailcarecategories.3P=third-partysellers;1P=first-partysalesSource:1010data

Whilethesefiguresmayprovidesomeguidanceastoretailers’onlinemarketshares,wethinkthattherearereasonsfortreatingthemwithsomecaution:

• ThestatedshareforUltalookssomewhatlowtous.1010dataputsthe2016onlinebeautymarketsizeat$1.2billion,andUltareportedtotale-commercesales(includinganynonbeautycategorysales)of$345millionin2016.Evenifonly50%ofUlta’sonlinesaleswereinthecategoriesincludedin1010data’sdefinitionofthemarket,theretailerwouldhaveenjoyedanapproximate14%shareofthe$1.2billiononlinemarketlastyear.Infact,justoverhalfofUlta’stotalrevenuescamefromcosmeticsintheyearendedJanuary2017;furthersharescamefromadjacentbeautycategoriessuchasfragranceandskincare.

• EuromonitorpeggedUSonlinesalesofcolorcosmeticsaloneat$1.7billionin2016,versus1010data’sestimationof$1.2billionforthetotalonlinebeautymarketsize.

1.5

2.7

2.9

3.5

3.9

8.2

14.4

15.0

17.4

21.1

Clinique

NeimanMarcus

Walmart

MACCosmedcs

Nordstrom

Ulta

Amazon1P

Sephora

Macy’s

Amazon3P

ThecombinedonlinemarketshareforAmazon’sthird-partyandfirst-partysaleswas35.5%in2016,accordingto1010data.

17

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

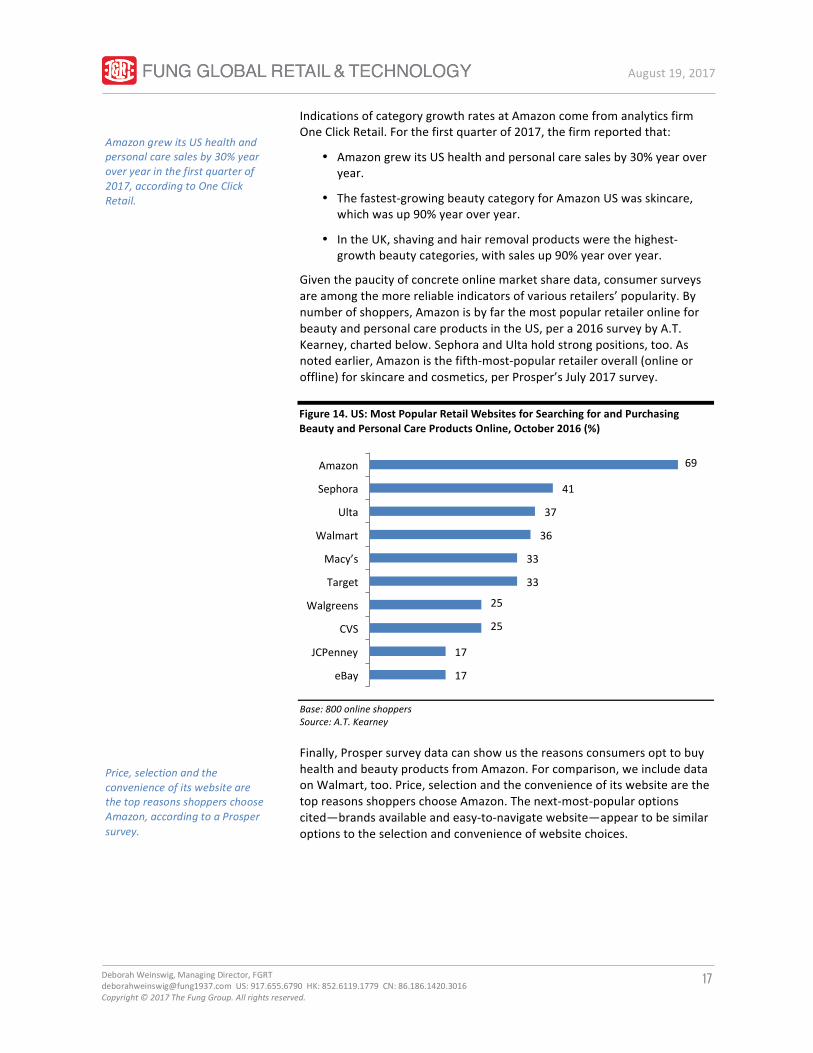

IndicationsofcategorygrowthratesatAmazoncomefromanalyticsfirmOneClickRetail.Forthefirstquarterof2017,thefirmreportedthat:

• AmazongrewitsUShealthandpersonalcaresalesby30%yearoveryear.

• Thefastest-growingbeautycategoryforAmazonUSwasskincare,whichwasup90%yearoveryear.

• IntheUK,shavingandhairremovalproductswerethehighest-growthbeautycategories,withsalesup90%yearoveryear.

Giventhepaucityofconcreteonlinemarketsharedata,consumersurveysareamongthemorereliableindicatorsofvariousretailers’popularity.Bynumberofshoppers,AmazonisbyfarthemostpopularretaileronlineforbeautyandpersonalcareproductsintheUS,pera2016surveybyA.T.Kearney,chartedbelow.SephoraandUltaholdstrongpositions,too.Asnotedearlier,Amazonisthefifth-most-popularretaileroverall(onlineoroffline)forskincareandcosmetics,perProsper’sJuly2017survey.

Figure14.US:MostPopularRetailWebsitesforSearchingforandPurchasingBeautyandPersonalCareProductsOnline,October2016(%)

Base:800onlineshoppersSource:A.T.Kearney

Finally,ProspersurveydatacanshowusthereasonsconsumersopttobuyhealthandbeautyproductsfromAmazon.Forcomparison,weincludedataonWalmart,too.Price,selectionandtheconvenienceofitswebsitearethetopreasonsshopperschooseAmazon.Thenext-most-popularoptionscited—brandsavailableandeasy-to-navigatewebsite—appeartobesimilaroptionstotheselectionandconvenienceofwebsitechoices.

17

17

25

25

33

33

36

37

41

69

eBay

JCPenney

CVS

Walgreens

Target

Macy’s

Walmart

Ulta

Sephora

Amazon

AmazongrewitsUShealthandpersonalcaresalesby30%yearoveryearinthefirstquarterof2017,accordingtoOneClickRetail.

Price,selectionandtheconvenienceofitswebsitearethetopreasonsshopperschooseAmazon,accordingtoaProspersurvey.

18

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

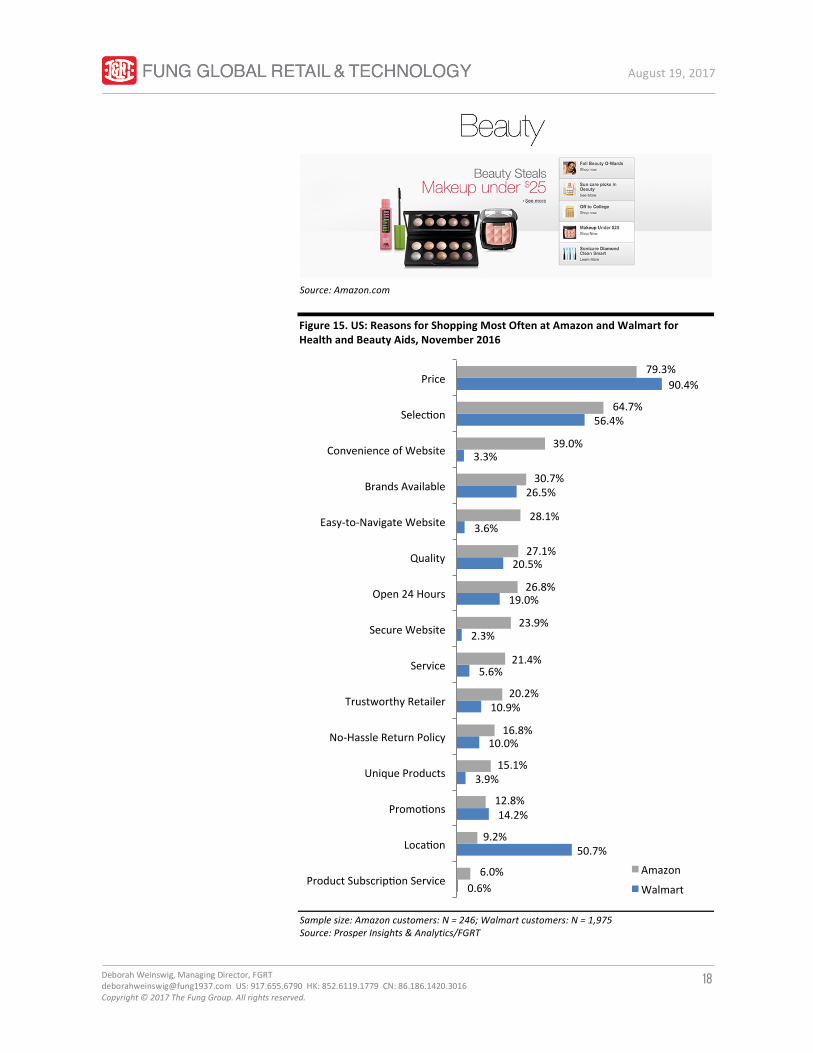

Source:Amazon.com

Figure15.US:ReasonsforShoppingMostOftenatAmazonandWalmartforHealthandBeautyAids,November2016

Samplesize:Amazoncustomers:N=246;Walmartcustomers:N=1,975Source:ProsperInsights&Analytics/FGRT

0.6%

50.7%

14.2%

3.9%

10.0%

10.9%

5.6%

2.3%

19.0%

20.5%

3.6%

26.5%

3.3%

56.4%

90.4%

6.0%

9.2%

12.8%

15.1%

16.8%

20.2%

21.4%

23.9%

26.8%

27.1%

28.1%

30.7%

39.0%

64.7%

79.3%

ProductSubscripdonService

Locadon

Promodons

UniqueProducts

No-HassleReturnPolicy

TrustworthyRetailer

Service

SecureWebsite

Open24Hours

Quality

Easy-to-NavigateWebsite

BrandsAvailable

ConvenienceofWebsite

Selecdon

Price

Amazon

Walmart

19

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

KeyTakeawaysWehaveseenanapparentpolarizationofgrowthinthebeautymarket,withsurveydataandcompanyreportssuggestingthatlow-priceretailersandconvincingbeautyspecialistshavewonshare.Weseemillennials’thriftybehavioranddesireforqualityexperiencesasdrivingthistrend.

Surveydatasuggestthatsomedrugstoresanddepartmentstoresoverindexamongoldershoppers.Ifthesetypesofretailerswanttodrawinmillennials,whatcantheydo?Wesuggestthattheyconsiderstrengtheningtheirentry-levelranges,bolsteringtheirbeautyloyaltyprogramsandintroducing,wherepractical,in-storebeautyservices.

FurtherReadingfromFGRTReadersmayalsobeinterestedinthefollowingreports:

TheMillennialsSeries:MillennialsandBeauty

DeepDive:GenZandBeauty—theSocialMediaSymbiosis

DeepDive:GlobalBeautyE-Commerce—aHighlyAttractiveMarket

DeepDive:ActiveM&AintheBeautySpaceFuelsFutureGrowth

BeautyLoyaltyPrograms:Sephoravs.Ulta

The21st-CenturyDrugstore:USDrugstoresFightingforShareinaShiftingBeautyMarket

Surveydatasuggestthatsomedrugstoresanddepartmentstoresoverindexamongoldershoppers.

20

August19,2017

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFGRTNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

HongKong:2ndFloor,HongKongSpinnersIndustrialBuildingPhase1&2800CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NewYork:1359Broadway,18thFloorNewYork,NY10018Tel:6468397017

FungGlobalRetailTech.com