Embed Size (px)

Citation preview

Changing Regional Midstream andChanging Regional Midstream and Transportation Developments

Terry McGillEnergy Summit 2009Energy Market Challenges & OpportunitiesLSU Center for Energy StudiesOctober 28, 2009

1

LEGAL NOTICE

Certain information during this presentation will constitute forward-l ki t t t Th ill i l d b t t il li it dlooking statements. These will include, but are not necessarily limited to, throughput volumes, financial projections, expansion or acquisition projects, external economics and competitive factors. These statements are based on certain assumptions made by managementstatements are based on certain assumptions made by management. Accordingly, actual results may differ materially from current estimates. You are referred to the Enbridge Energy Partners' SEC filings, including the annual Form 10-K, for a more detailed discussionfilings, including the annual Form 10 K, for a more detailed discussion of risk factors.

2#2

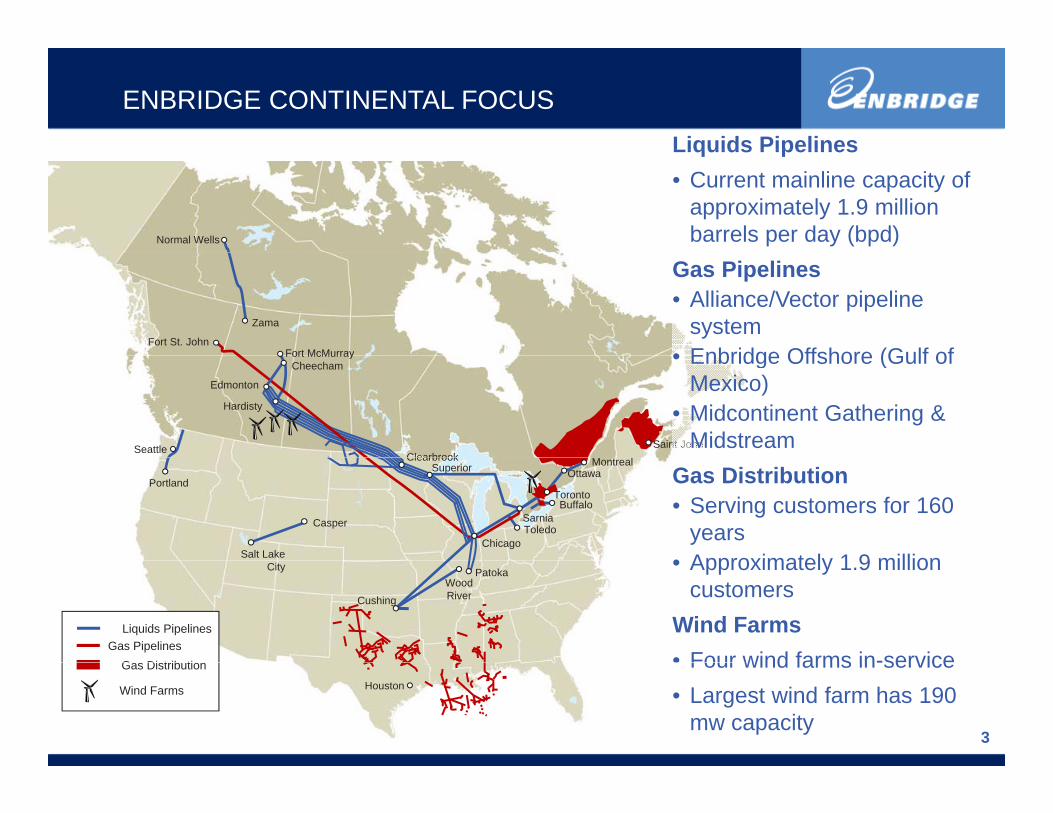

Liquids Pipelines

ENBRIDGE CONTINENTAL FOCUS

Normal Wells

Liquids Pipelines• Current mainline capacity of

approximately 1.9 million barrels per day (bpd)

Zama

Fort McMurrayFort St. John

Gas Pipelines• Alliance/Vector pipeline

system• Enbridge Offshore (Gulf ofFort McMurray

Seattle Saint John

M t lClearbrook

Edmonton

Hardisty

Cheecham • Enbridge Offshore (Gulf of Mexico)

• Midcontinent Gathering & Midstream

Saint JoPortland

Casper

Montreal

Salt Lake

Toledo

Buffalo

Ottawa

Sarnia

SuperiorClearbrook

Chicago

TorontoGas Distribution• Serving customers for 160

years• Approximately 1 9 millionCity Patoka

CushingWood River

Gas Distrib tion

Liquids PipelinesGas Pipelines

• Approximately 1.9 million customers

Wind Farms• Four wind farms in-service

3

Houston

Gas Distribution

Wind Farms

Four wind farms in service• Largest wind farm has 190

mw capacity

Fundamentals that direct midstreamInfrastructure

• Supply – Where are the producers in esting and de eloping?investing and developing?

• Demand – Where is the market for theDemand Where is the market for the gas?

P i Wh th d bt i• Price – Where can the producer obtain the best cost margins for production and market price for the gas?and market price for the gas?

4

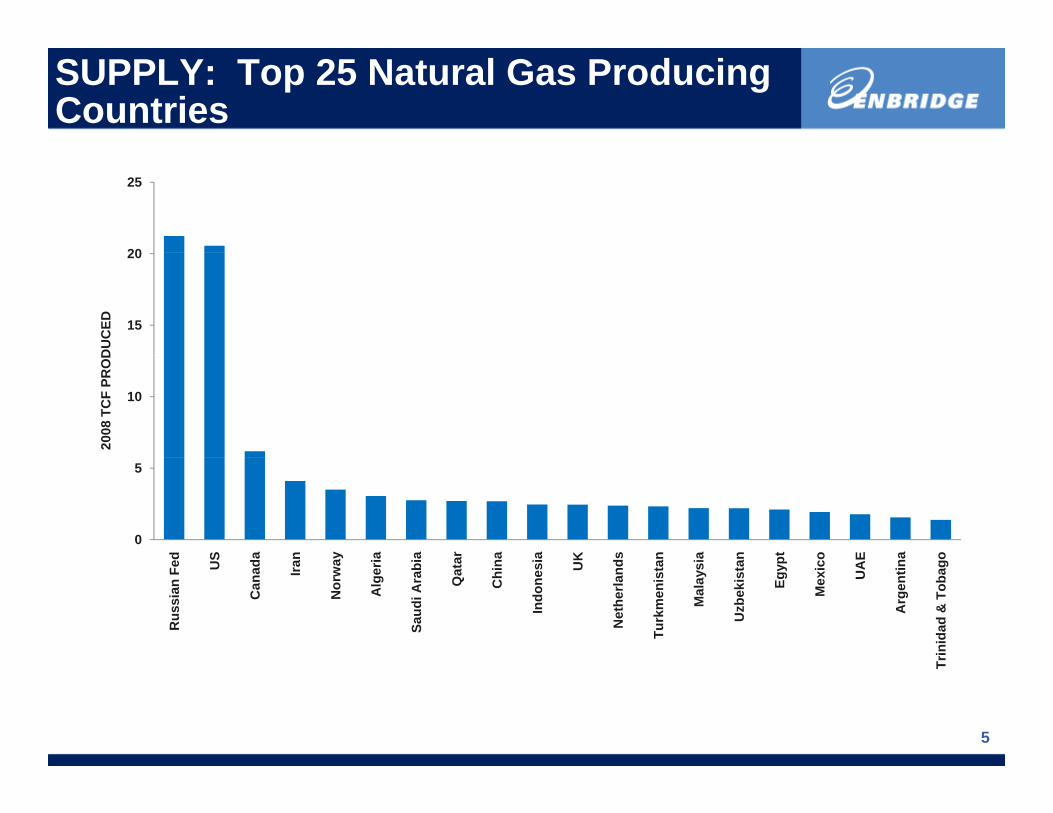

SUPPLY: Top 25 Natural Gas Producing Countries

20

25

15

20

DU

CED

10

2008

TC

F PR

OD

0

5

ed S da an ay ia ia ar na ia K ds an ia an pt co AE na o

Rus

sian

Fe U

Can

a d Ira

Nor

wa

Alg

eri

Saud

i Ara

bi

Qat

a

Chi

n

Indo

nesi U

Net

herla

n d

Turk

men

ista

Mal

aysi

Uzb

ekis

ta

Egyp

Mex

ic UA

Arg

entin

Trin

idad

& T

obag

5

T

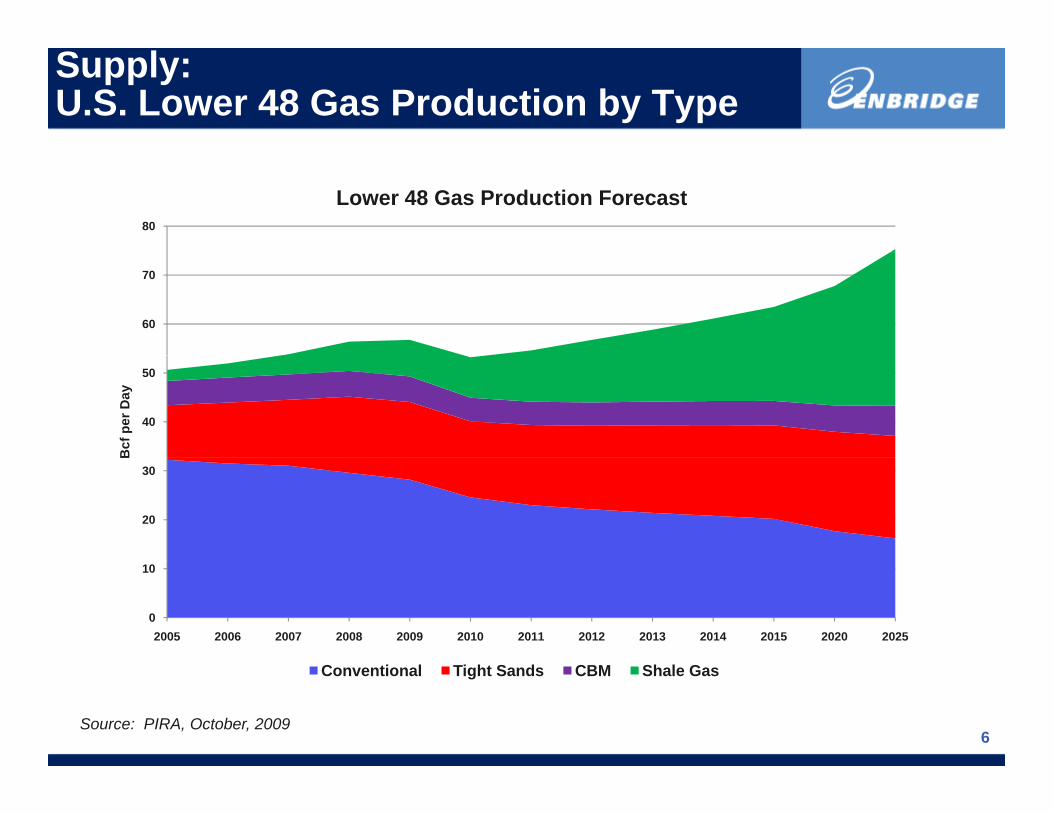

Supply:U.S. Lower 48 Gas Production by Type

80

Lower 48 Gas Production Forecast

60

70

40

50

Bcf

per

Day

20

30

0

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2020 2025

6

Conventional Tight Sands CBM Shale Gas

Source: PIRA, October, 2009

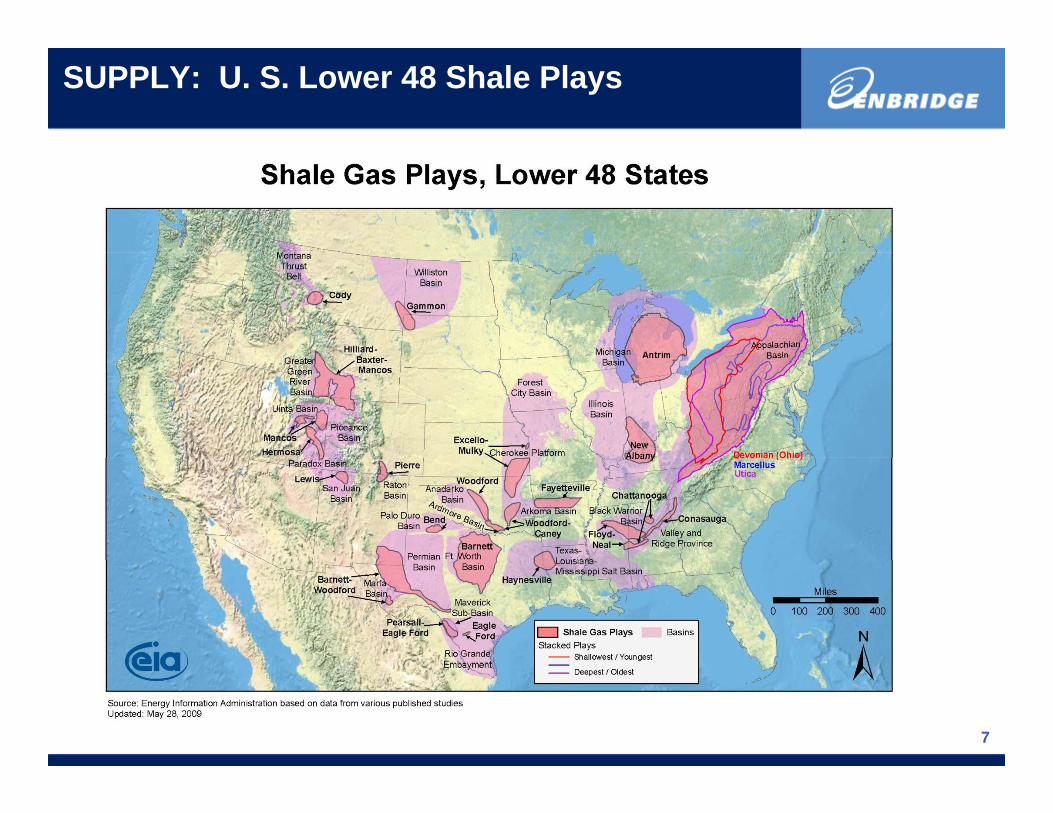

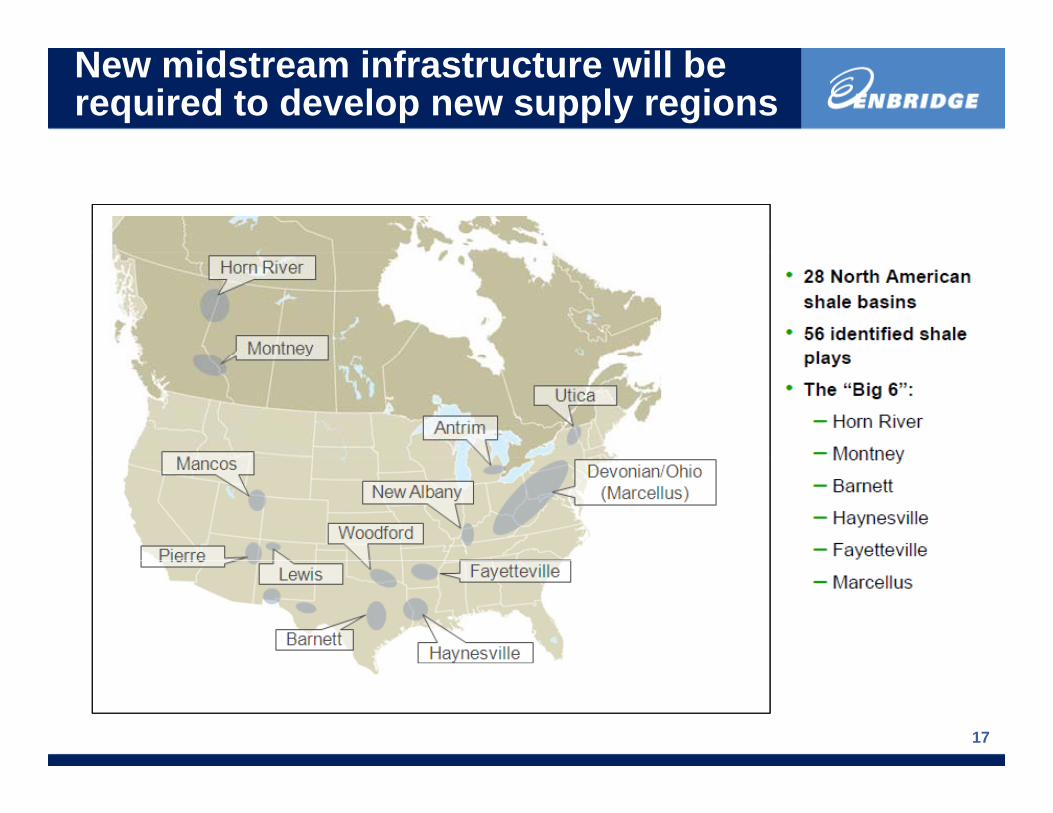

SUPPLY: U. S. Lower 48 Shale Plays

7

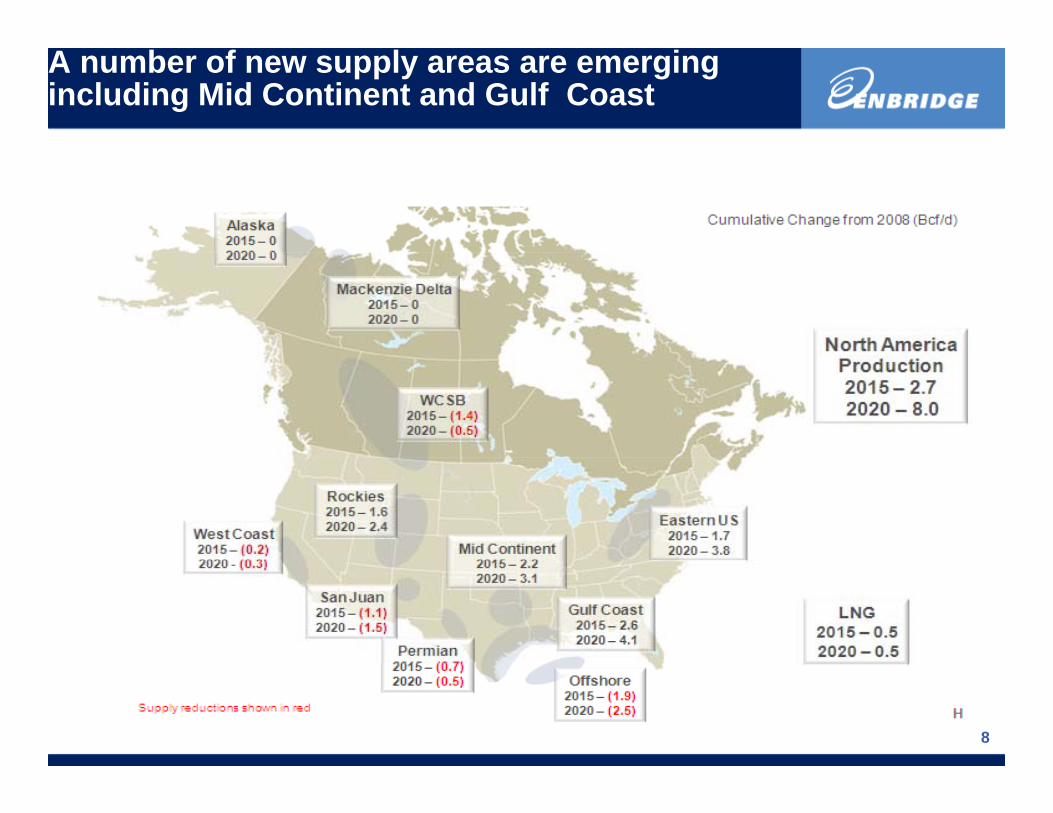

A number of new supply areas are emerging including Mid Continent and Gulf Coast

8

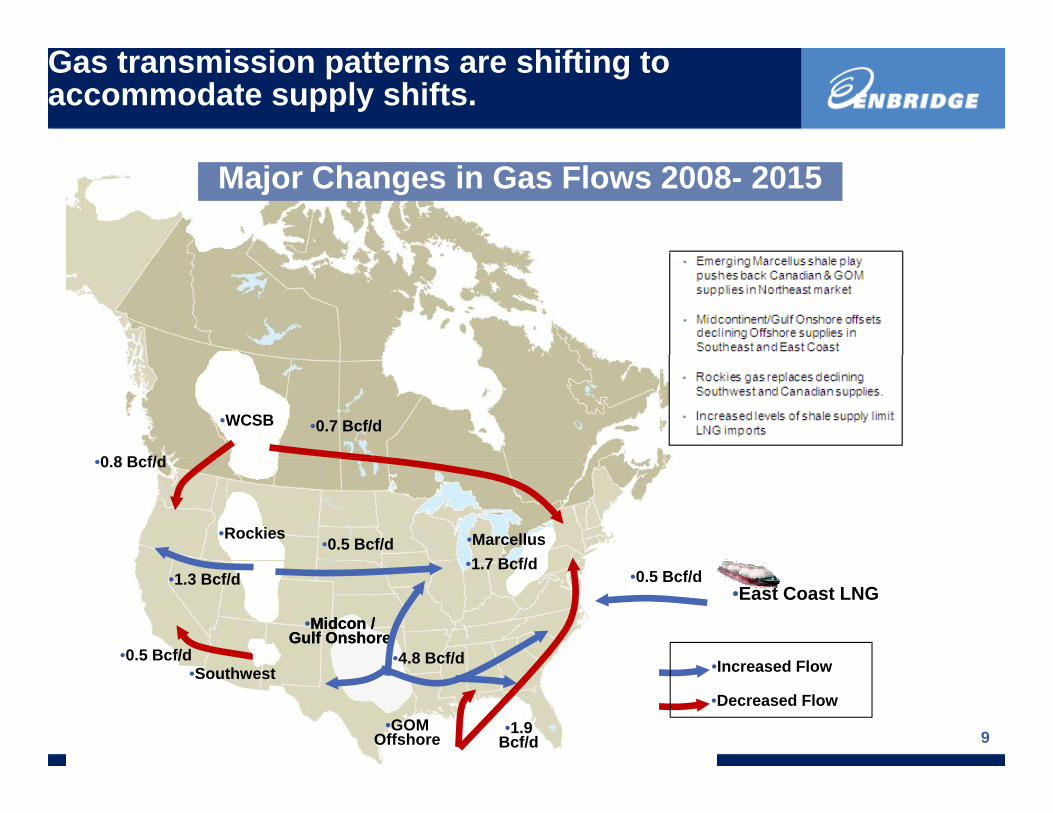

Gas transmission patterns are shifting to accommodate supply shifts.

Major Changes in Gas Flows 2008- 2015

•WCSB

0 8 B f/d

•0.7 Bcf/d

•Rockies•0.5 Bcf/d

•0.8 Bcf/d

•Marcellus1 7 B f/d

•Midcon / Gulf Onshore

•Midcon / Gulf Onshore

I d Fl

•1.3 Bcf/d

•4.8 Bcf/d•0.5 Bcf/d

•East Coast LNG•0.5 Bcf/d

•1.7 Bcf/d

9

•Increased Flow

•Decreased Flow

4.8 Bcf/d

•1.9 Bcf/d

•Southwest

•GOM Offshore

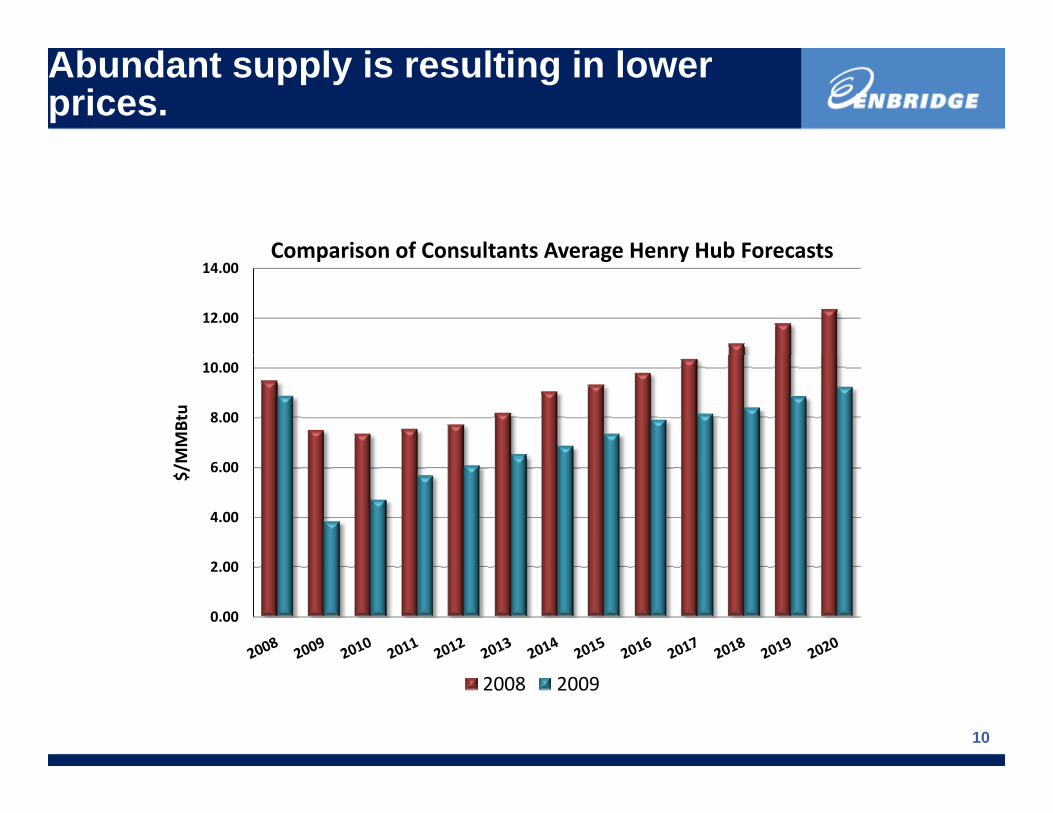

Abundant supply is resulting in lower prices.

Comparison of Consultants Average Henry Hub Forecasts

12.00

14.00Comparison of Consultants Average Henry Hub Forecasts

8.00

10.00

MMBtu

4.00

6.00$/M

0.00

2.00

10

2008 2009

Natural Gas Supply and Demand Imbalance

• U.S. is supply long at rate of 1.7 Bcf/d

• Storage is at record levels• Storage is at record levels.

• Rig count has fallen by 48% since October 2008 but production fell by only 2% in same period.

• Drilling in Haynesville is up 25%.HOWEVER

• Drilling in Marcellus is up 59%.

11

Producers drill where cost margins allow for best return on investment.

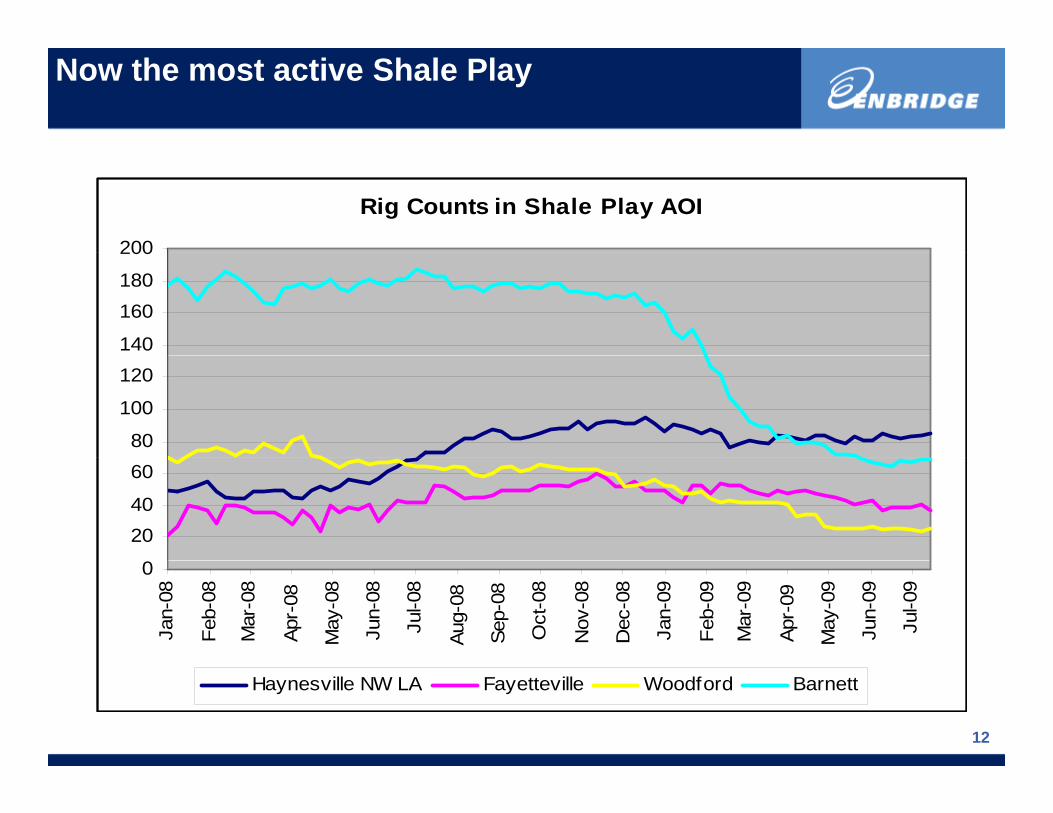

Now the most active Shale Play

Rig Counts in Shale Play AOI

200

140

160180

200

80

100

120

2040

60

0

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr-

09

May

-09

Jun-

09

Jul-0

9

12

Haynesville NW LA Fayetteville Woodford Barnett

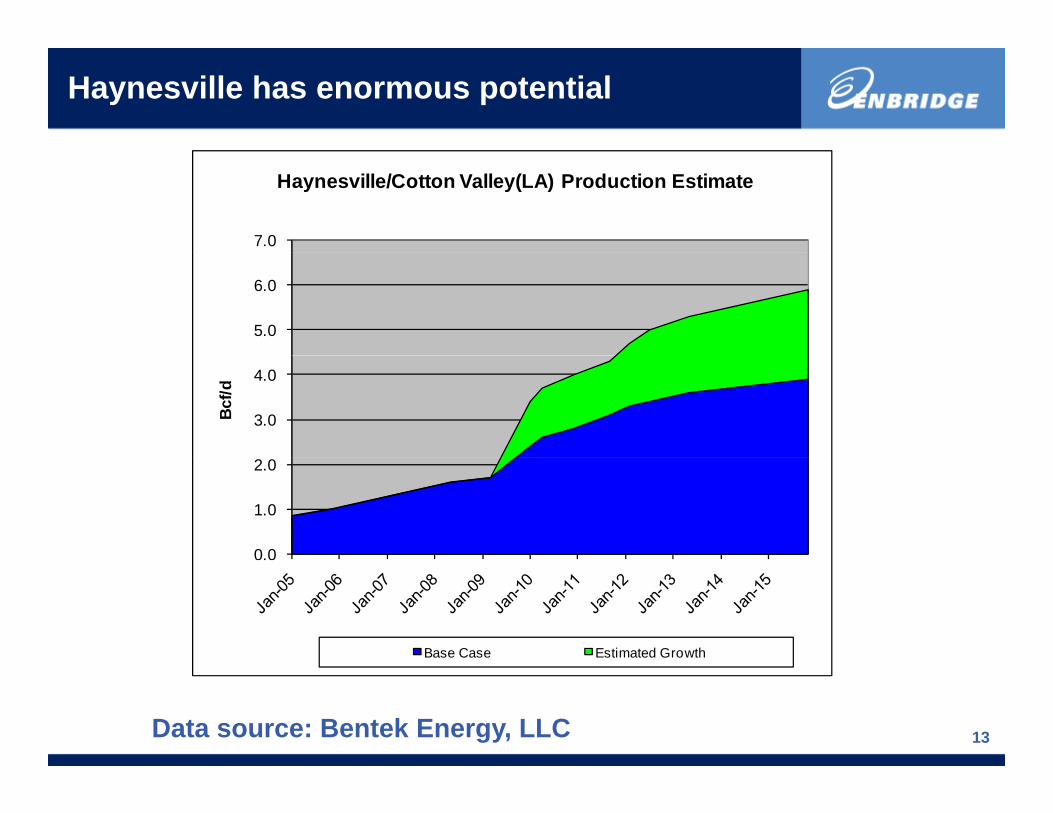

Haynesville has enormous potential

7.0

Haynesville/Cotton Valley(LA) Production Estimate

5.0

6.0

3.0

4.0

Bcf

/d

0.0

1.0

2.0

Base Case Estimated Growth

13Data source: Bentek Energy, LLC

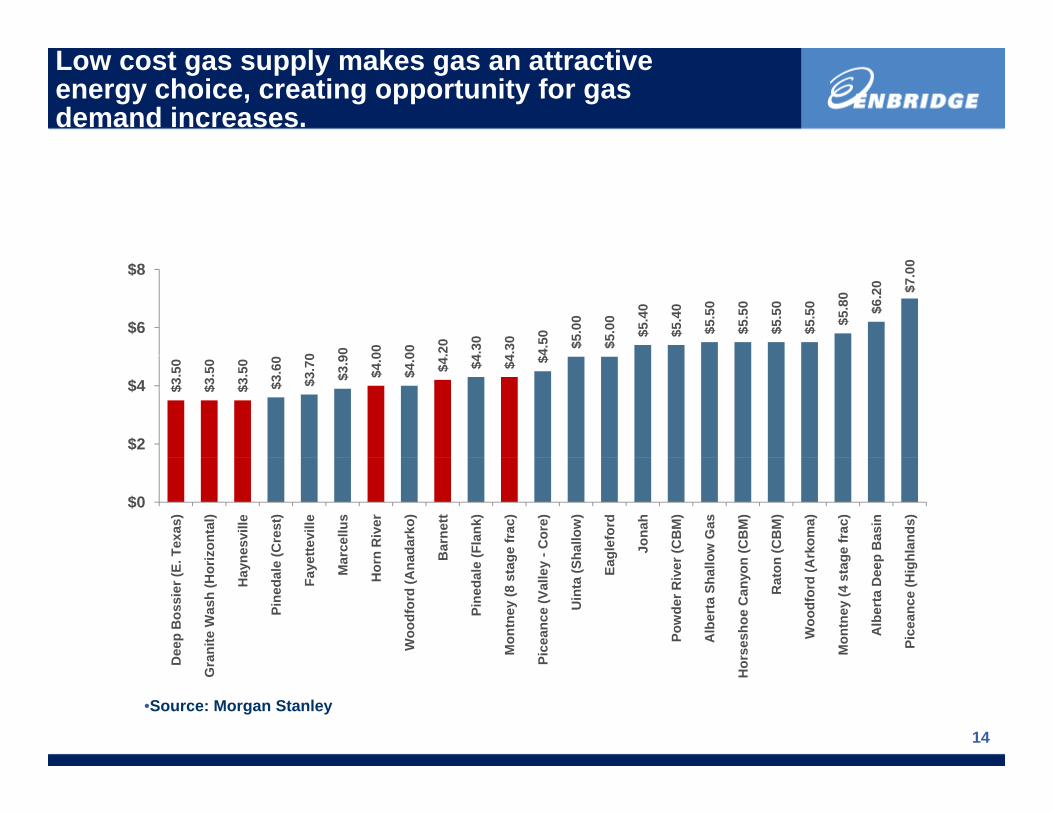

Low cost gas supply makes gas an attractiveenergy choice, creating opportunity for gas demand increases.

0 90 00 00 .20

4.30

4.30 4.50 $5

.00

$5.0

0

$5.4

0

$5.4

0

$5.5

0

$5.5

0

$5.5

0

$5.5

0

$5.8

0

$6.2

0 $7.0

0

$6

$8

$3.5

0

$3.5

0

$3.5

0

$3.6

0

$3.7

0

$3.9

$4.0

$4.0 $4.

$4 $4 $4

$2

$4

$0

Tex

as)

rizon

tal)

nesv

ille

(Cre

st)

ette

ville

arce

llus

rn R

iver

adar

ko)

Bar

nett

(Fla

nk)

ge fr

ac)

-Cor

e)

hallo

w)

agle

ford

Jona

h

r (C

BM

)

ow G

as

n (C

BM

)

n (C

BM

)

Ark

oma)

ge fr

ac)

p B

asin

hlan

ds)

Dee

p B

ossi

er (E

.

rani

te W

ash

(Hor

Hay

n

Pine

dale

Faye Ma

Hor

Woo

dfor

d (A

na

Pine

dale

Mon

tney

(8 s

tag

Pice

ance

(Val

ley

Uin

ta (S Ea

Pow

der R

iver

Alb

erta

Sha

llo

orse

shoe

Can

yon

Rat

on

Woo

dfor

d (A

Mon

tney

(4 s

tag

Alb

erta

Dee

p

Pice

ance

(Hig

h

14

D

Gr P

Ho

•Source: Morgan Stanley

Regional Supply Areas could provide economic stimulus to Gulf Coast Industry

• Natural Gas provides low cost feedstock.

• Lower U.S. dollar value makes U.S.

t dexport goods attractive.

• Gas Supply such as Haynesville Shale

id lHouston Chronicle, October 18, 2009 provides a close source and long term supply to industrial

15

supply to industrial consumers.

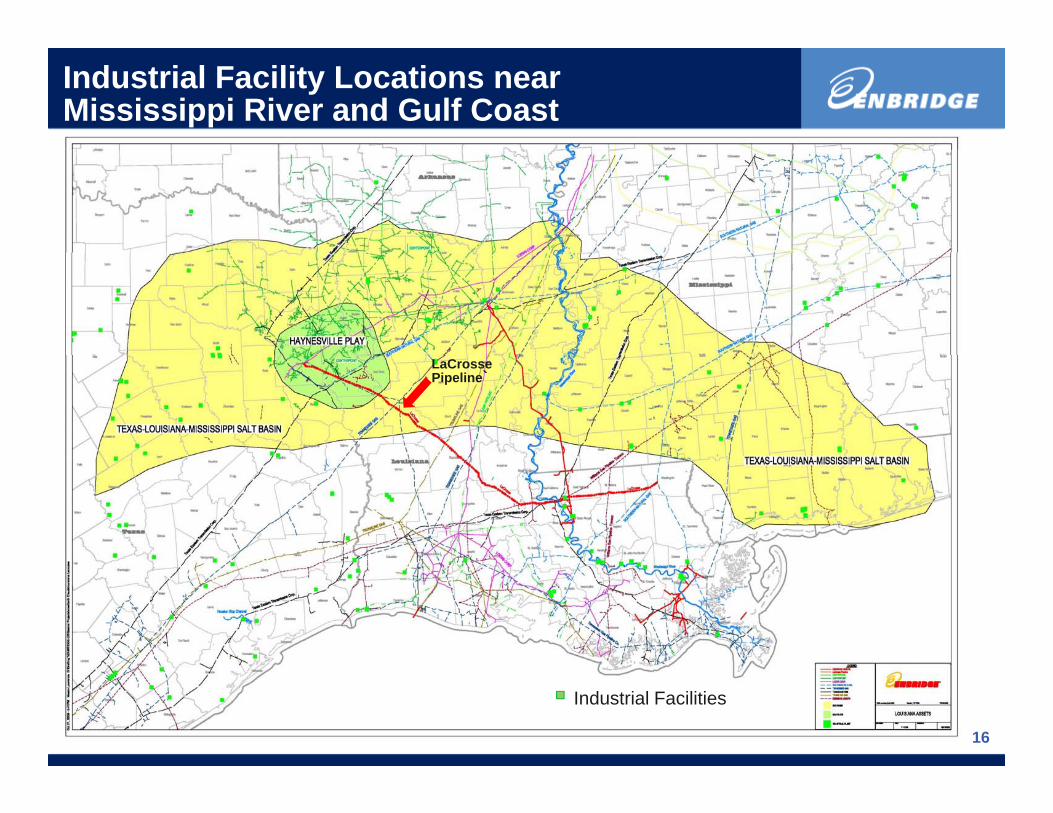

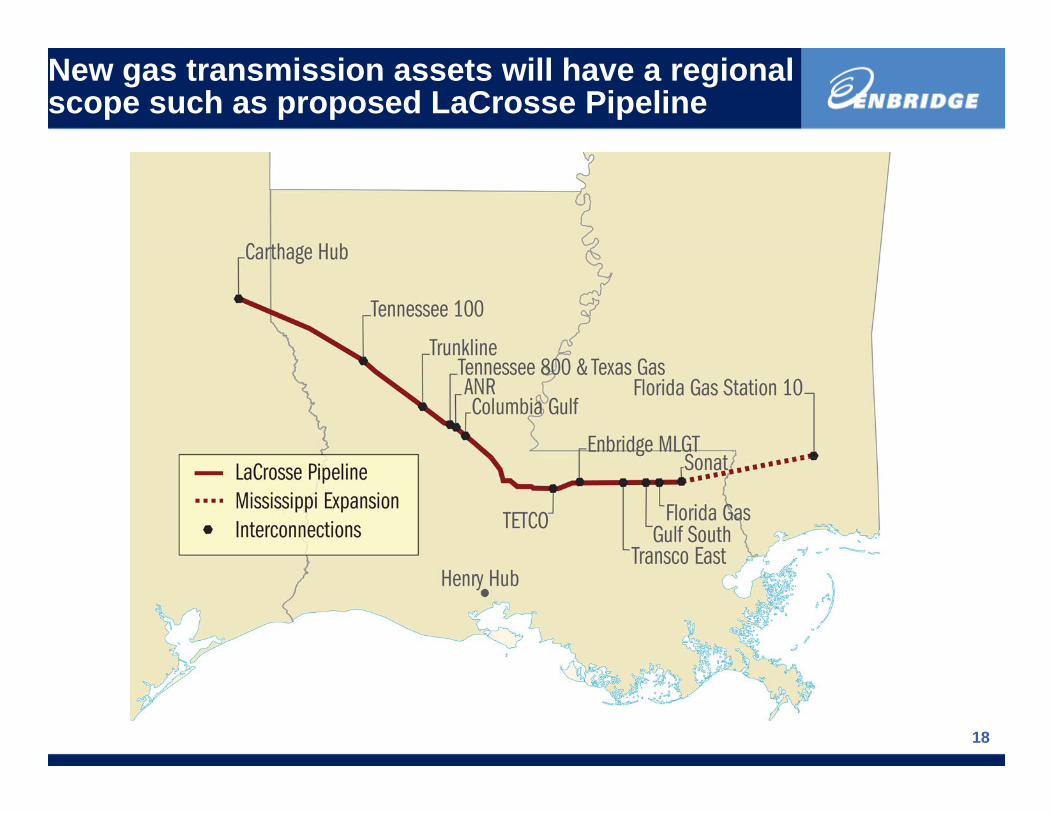

Industrial Facility Locations near Mississippi River and Gulf Coast

LaCrosse Pipeline`

16

Industrial Facilities

New midstream infrastructure will be required to develop new supply regions

17

New gas transmission assets will have a regional scope such as proposed LaCrosse Pipeline

18

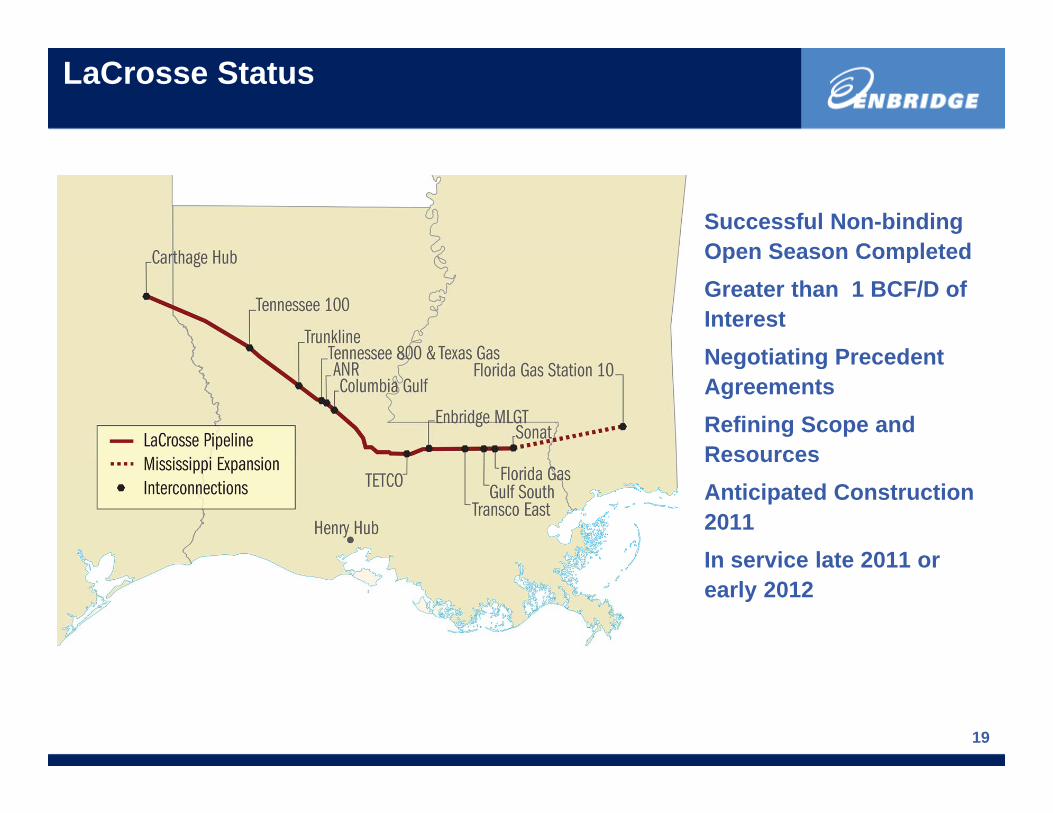

LaCrosse Status

• Successful Non-binding Open Season CompletedOpen Season Completed

• Greater than 1 BCF/D of Interest

• Negotiating Precedent• Negotiating Precedent Agreements

• Refining Scope and ResourcesResources

• Anticipated Construction 2011

• In service late 2011 or• In service late 2011 or early 2012

19

New Supply Areas will need other midstream components based on gas composition.

• Gathering lines to transport pproduction to transmission lines

• Gas treating, processing and p gdehydration facilities

• Compressor stations

20

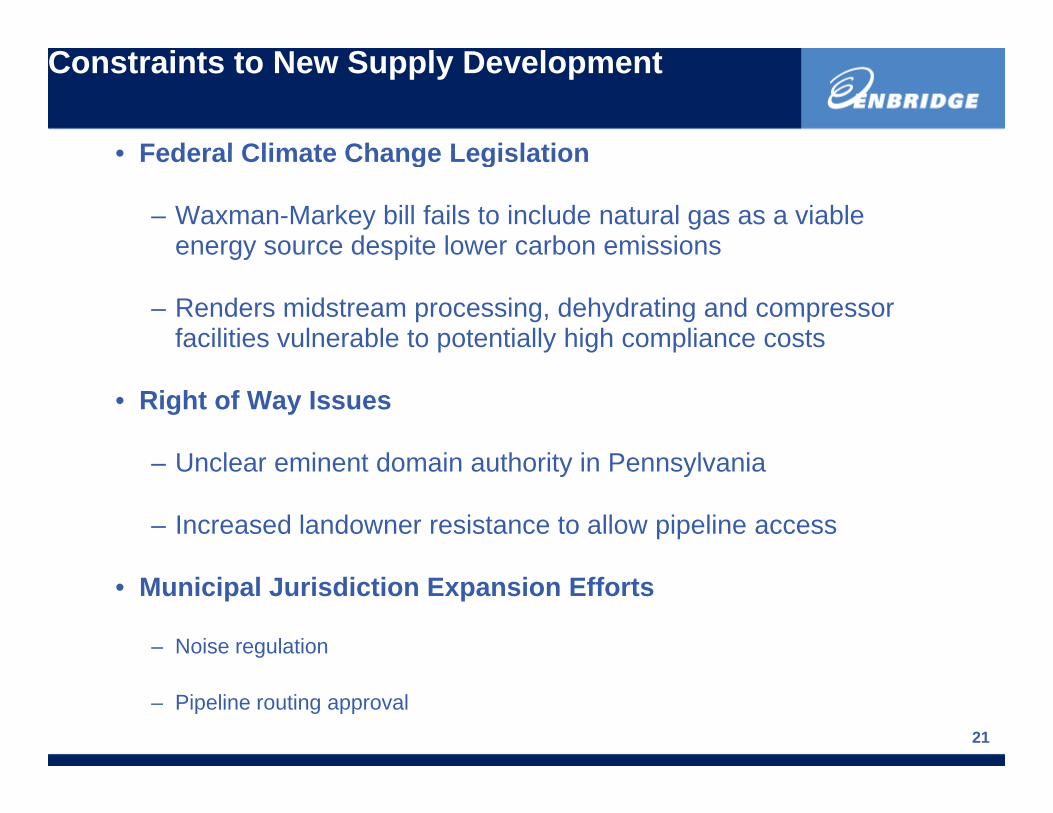

Constraints to New Supply Development

• Federal Climate Change Legislation• Federal Climate Change Legislation

– Waxman-Markey bill fails to include natural gas as a viable energy source despite lower carbon emissionsenergy source despite lower carbon emissions

– Renders midstream processing, dehydrating and compressor facilities vulnerable to potentially high compliance costs

• Right of Way Issues

Unclear eminent domain authority in Pennsylvania– Unclear eminent domain authority in Pennsylvania

– Increased landowner resistance to allow pipeline access

• Municipal Jurisdiction Expansion Efforts

– Noise regulation

21

– Pipeline routing approval

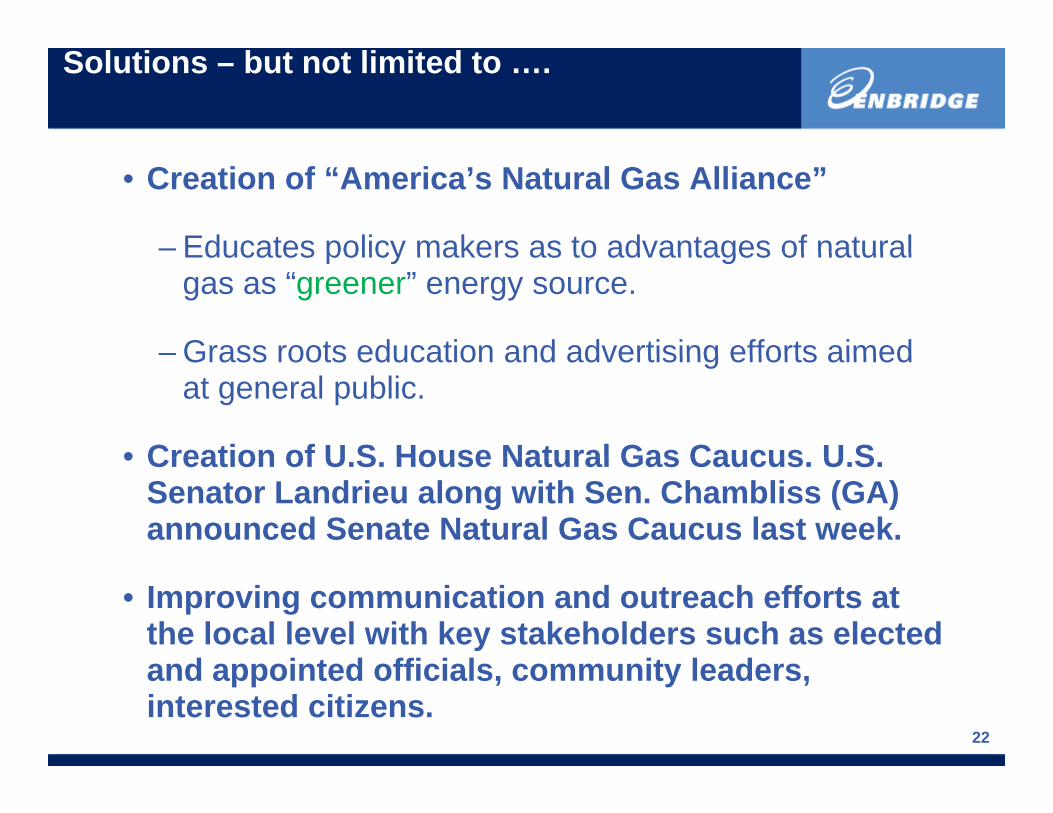

Solutions – but not limited to ….

• Creation of “America’s Natural Gas Alliance”

– Educates policy makers as to advantages of naturalEducates policy makers as to advantages of natural gas as “greener” energy source.

– Grass roots education and advertising efforts aimedGrass roots education and advertising efforts aimed at general public.

• Creation of U S House Natural Gas Caucus U S• Creation of U.S. House Natural Gas Caucus. U.S. Senator Landrieu along with Sen. Chambliss (GA) announced Senate Natural Gas Caucus last week.

• Improving communication and outreach efforts at the local level with key stakeholders such as elected

d i t d ffi i l it l d

22

and appointed officials, community leaders, interested citizens.

QUESTIONS?QUESTIONS?

23