Embed Size (px)

Citation preview

CHALLENGING ISSUES

IN M&A TRANSACTIONS

Noah Fisette, Senior Corporate Counsel at Evonik Corporation

Caryn Groce, VP & Associate GC, Corporate Transactions at Viacom, Inc.

Joseph Napoli, Assistant GC at U.S. Steel Corporation

Chris Abbinante, Partner, Sidley Austin LLP

Moderator: Brian Fahrney, Partner, Sidley Austin LLP

Agenda

• M&A Market Overview and Observations

• Seller-Friendly Deal Environment

• Role of In-House Counsel in M&A

• Earnouts and Purchase Price Adjustments

• M&A Due Diligence Hot Buttons

• Common Issues in Corporate Carveouts

• Shareholder Activism Relating to M&A

• Lessons Learned from Recent M&A Litigation

• Allocating Antitrust Risk in M&A Deals

2

M&A Market

Overview and Observations

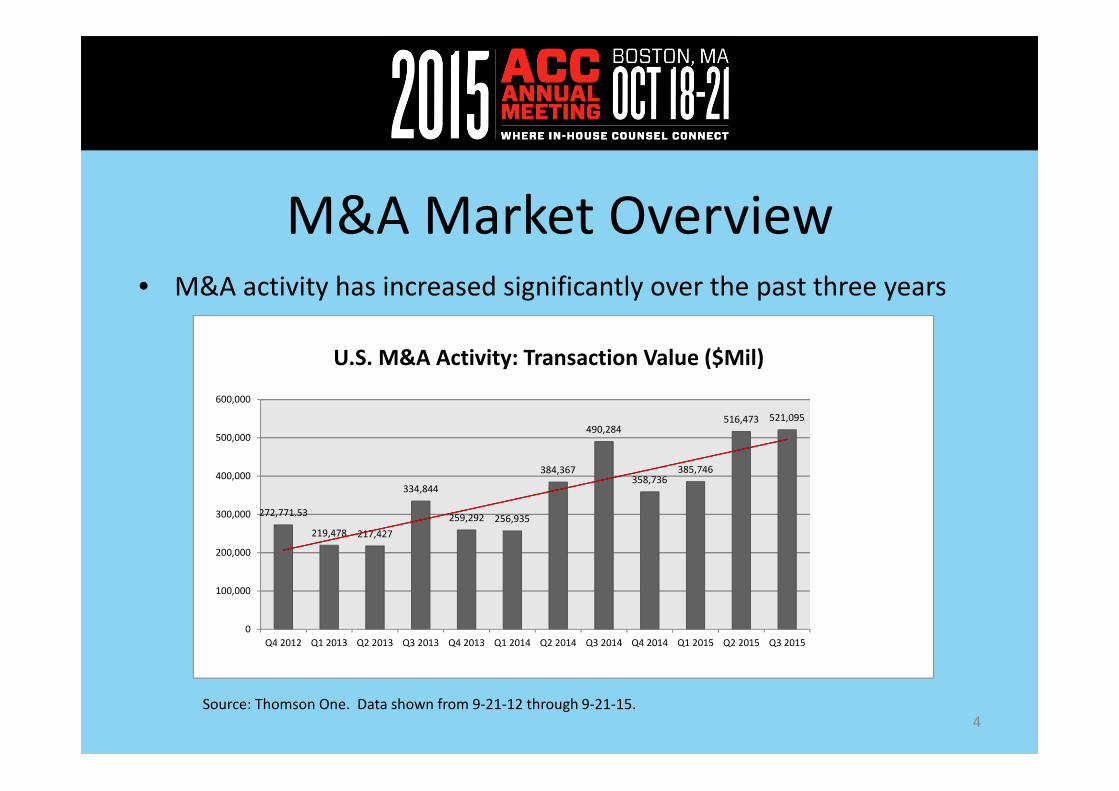

M&A Market Overview• M&A activity has increased significantly over the past three years

4

272,771.53

219,478 217,427

334,844

259,292 256,935

384,367

490,284

358,736385,746

516,473 521,095

0

100,000

200,000

300,000

400,000

500,000

600,000

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

U.S. M&A Activity: Transaction Value ($Mil)

Source: Thomson One. Data shown from 9-21-12 through 9-21-15.

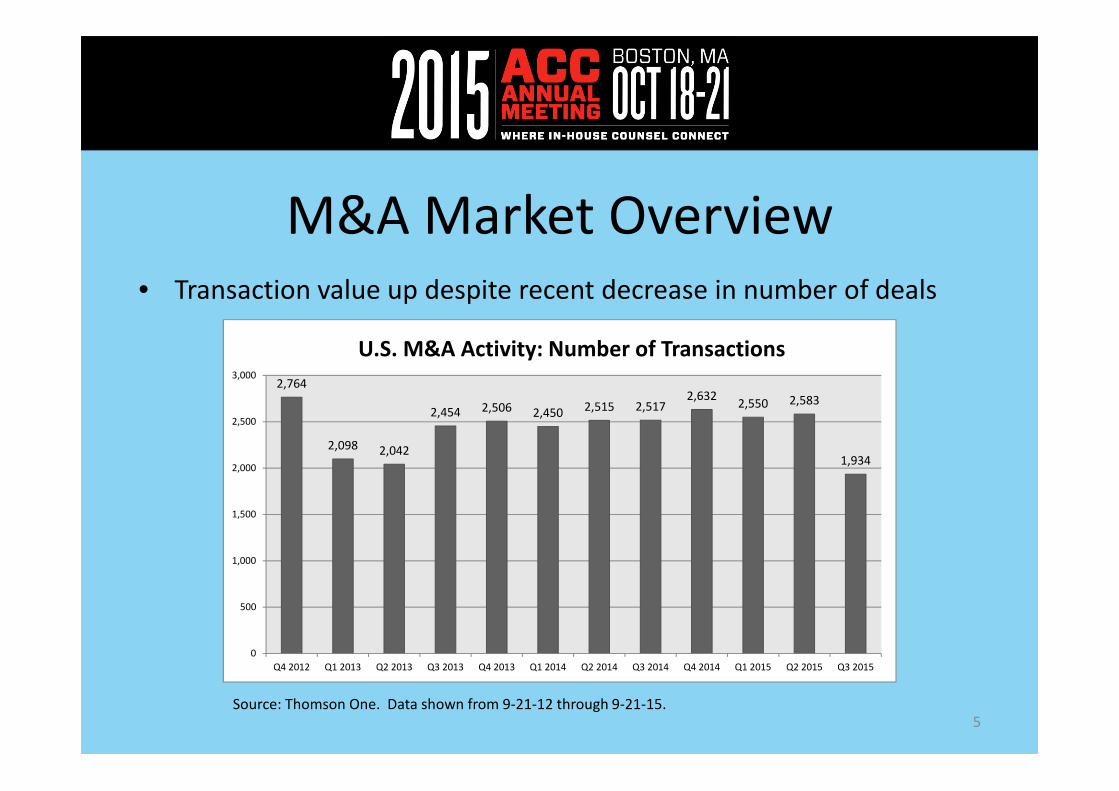

M&A Market Overview• Transaction value up despite recent decrease in number of deals

5Source: Thomson One. Data shown from 9-21-12 through 9-21-15.

2,764

2,098 2,042

2,454 2,506 2,450 2,515 2,5172,632

2,550 2,583

1,934

0

500

1,000

1,500

2,000

2,500

3,000

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

U.S. M&A Activity: Number of Transactions

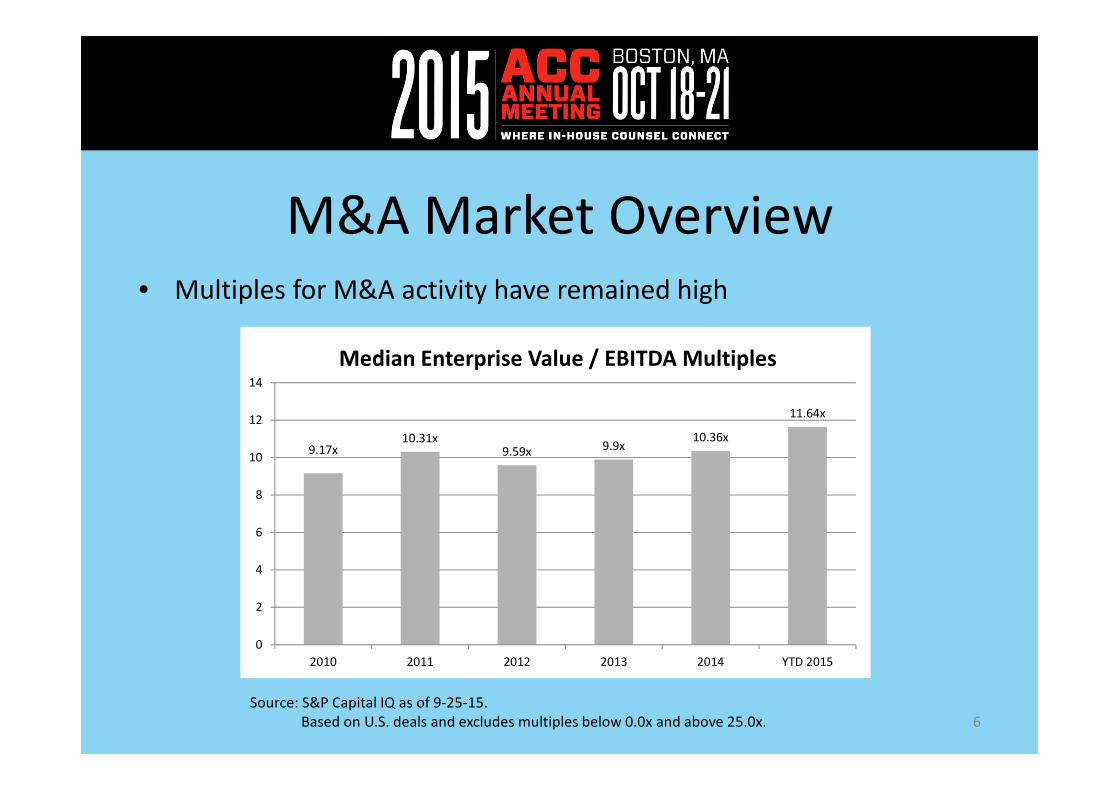

M&A Market Overview• Multiples for M&A activity have remained high

6

Source: S&P Capital IQ as of 9-25-15.

Based on U.S. deals and excludes multiples below 0.0x and above 25.0x.

9.17x10.31x

9.59x 9.9x10.36x

11.64x

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 YTD 2015

Median Enterprise Value / EBITDA Multiples

M&A Market Observations• Seller-friendly market

– Sellers getting full value for desirable assets

• Delayed diligence

– Bankers letting more bidders into second round

– Result is increased time between winning bidder selected and

signing

– If seller pushes for quick signing, buyer must decide if it can

live with less diligence

• Joint ventures / minority investments more common

• Fewer club deals

7

M&A Market Observations• More strategic buyers

– Strategics may find it cheaper to acquire than organically grow

– Lots of cash on balance sheet

• More tender offers

– 251(h) popular

– Eliminates the need for dual track merger or messy top-up

options

• Increased hostile activity

• Increased appraisal arbitrage

8

Seller-Friendly

Deal Environment

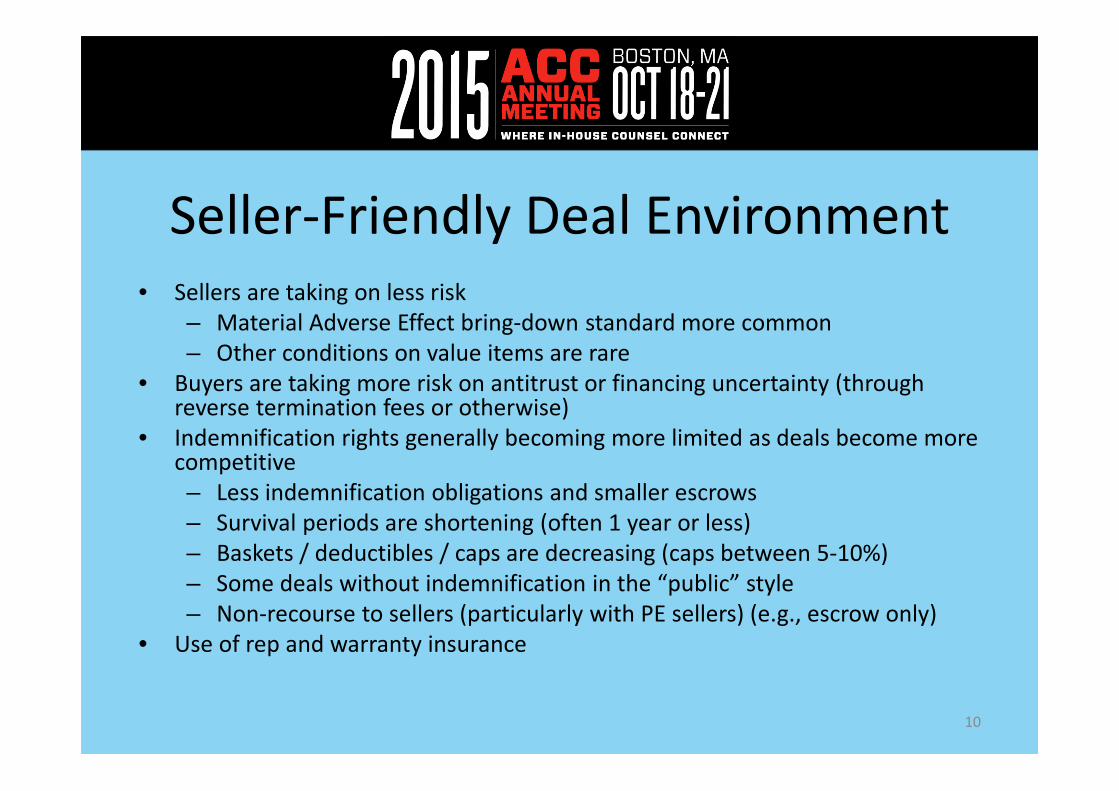

Seller-Friendly Deal Environment• Sellers are taking on less risk

– Material Adverse Effect bring-down standard more common

– Other conditions on value items are rare

• Buyers are taking more risk on antitrust or financing uncertainty (through reverse termination fees or otherwise)

• Indemnification rights generally becoming more limited as deals become more competitive

– Less indemnification obligations and smaller escrows

– Survival periods are shortening (often 1 year or less)

– Baskets / deductibles / caps are decreasing (caps between 5-10%)

– Some deals without indemnification in the “public” style

– Non-recourse to sellers (particularly with PE sellers) (e.g., escrow only)

• Use of rep and warranty insurance

10

Rep and Warranty Insurance• Works for deals as small as $15 million

• Premiums currently range from 2-5% of policy limits (one-time)

• Deductibles typically run between 1-3% of deal price

• Can be purchased by buyer or seller

– But better for buyer to purchase it

– Because covers seller’s fraud

• Stapled insurance

• Timing considerations

– 1 week to get bids

– 7-10 days to secure once insurer has been selected

• Other specific coverages (e.g., taxes, environmental)11

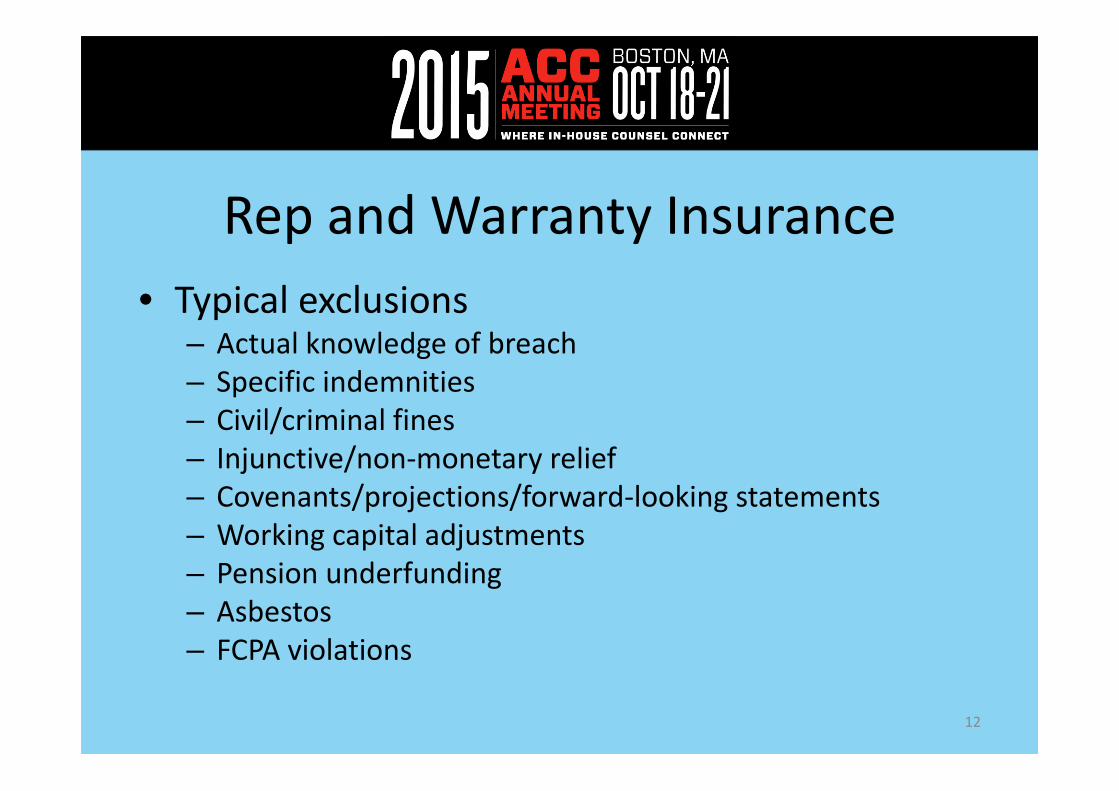

Rep and Warranty Insurance

• Typical exclusions– Actual knowledge of breach

– Specific indemnities

– Civil/criminal fines

– Injunctive/non-monetary relief

– Covenants/projections/forward-looking statements

– Working capital adjustments

– Pension underfunding

– Asbestos

– FCPA violations

12

Role of In-House

Counsel in M&A

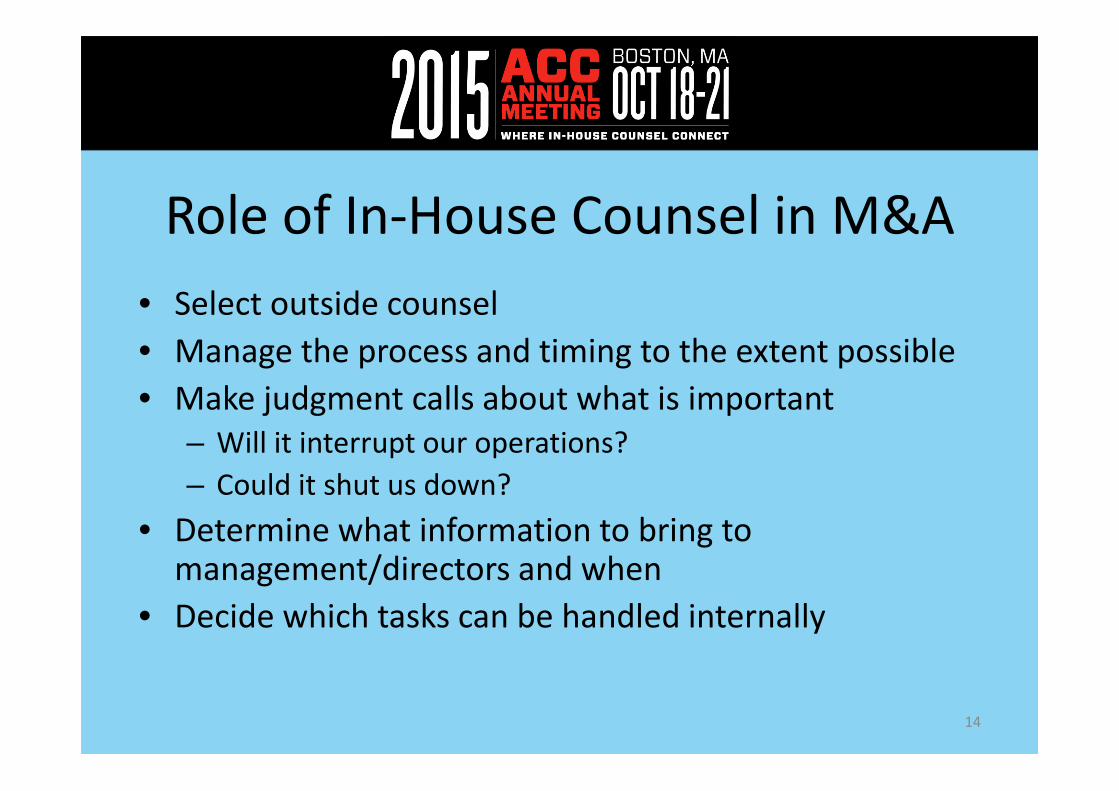

Role of In-House Counsel in M&A

• Select outside counsel

• Manage the process and timing to the extent possible

• Make judgment calls about what is important

– Will it interrupt our operations?

– Could it shut us down?

• Determine what information to bring to management/directors and when

• Decide which tasks can be handled internally

14

Earnouts and

Purchase Price Adjustments

Earnouts Generally• Why do an earnout?

• Earnout structure– Contingent consideration payable to seller based on the post-closing

performance of the target business

– May be based on: • Mere passage of time (really just deferred purchase price)

• Revenue or earnings / EBITDA metric

• Milestones; extrinsic events

• Accompanying covenants– Maintain books and records consistent with past practice; hold

business separate

– No change to management / key employees

– No fundamental change in business, divestitures

16

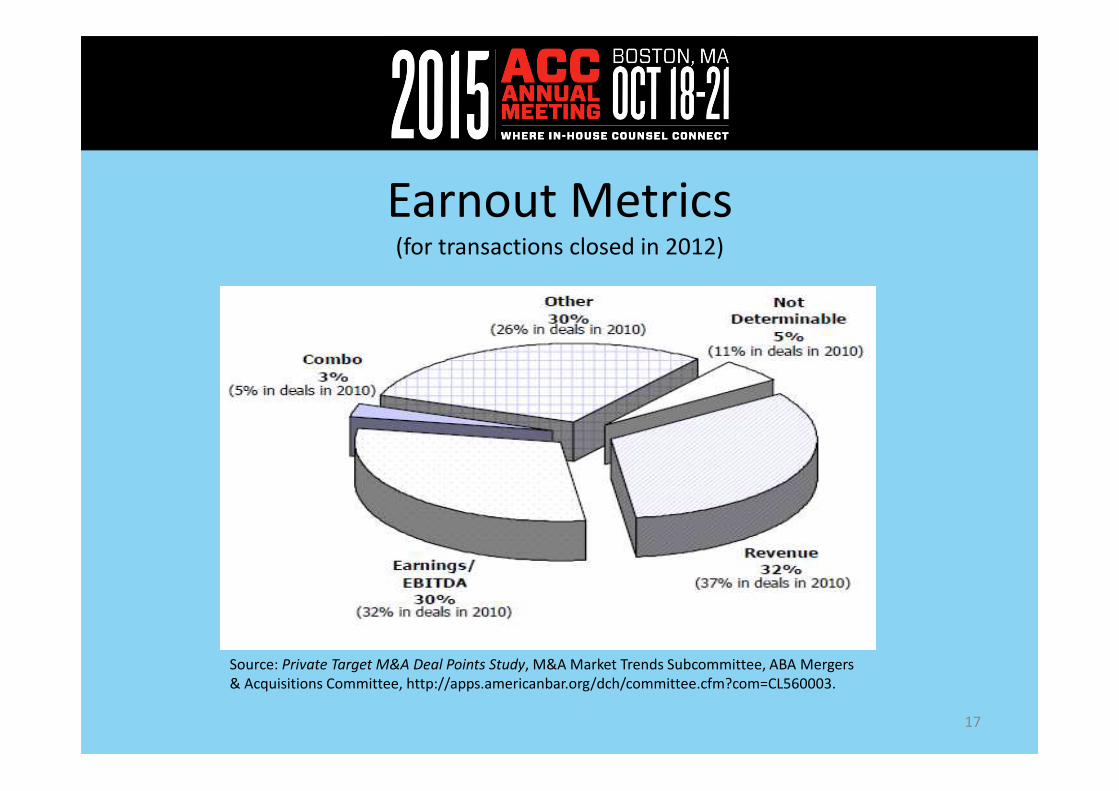

Earnout Metrics(for transactions closed in 2012)

17

Source: Private Target M&A Deal Points Study, M&A Market Trends Subcommittee, ABA Mergers

& Acquisitions Committee, http://apps.americanbar.org/dch/committee.cfm?com=CL560003.

Common Earnout Disputes• Whether earnout metric has been satisfied / calculation of

the earnout amount– Definitional issues relating to earnout metric

• Overhead, intercompany transactions, etc.

• Failure to invest and/or support the business; cap ex / marketing spend

• Whether buyer complied with post-closing covenants with respect to the operation of the target business and/or accounting for the business

• How earnout should be treated if buyer disposes of the target business, acquires a similar business or experiences a change of control during earnout period

18

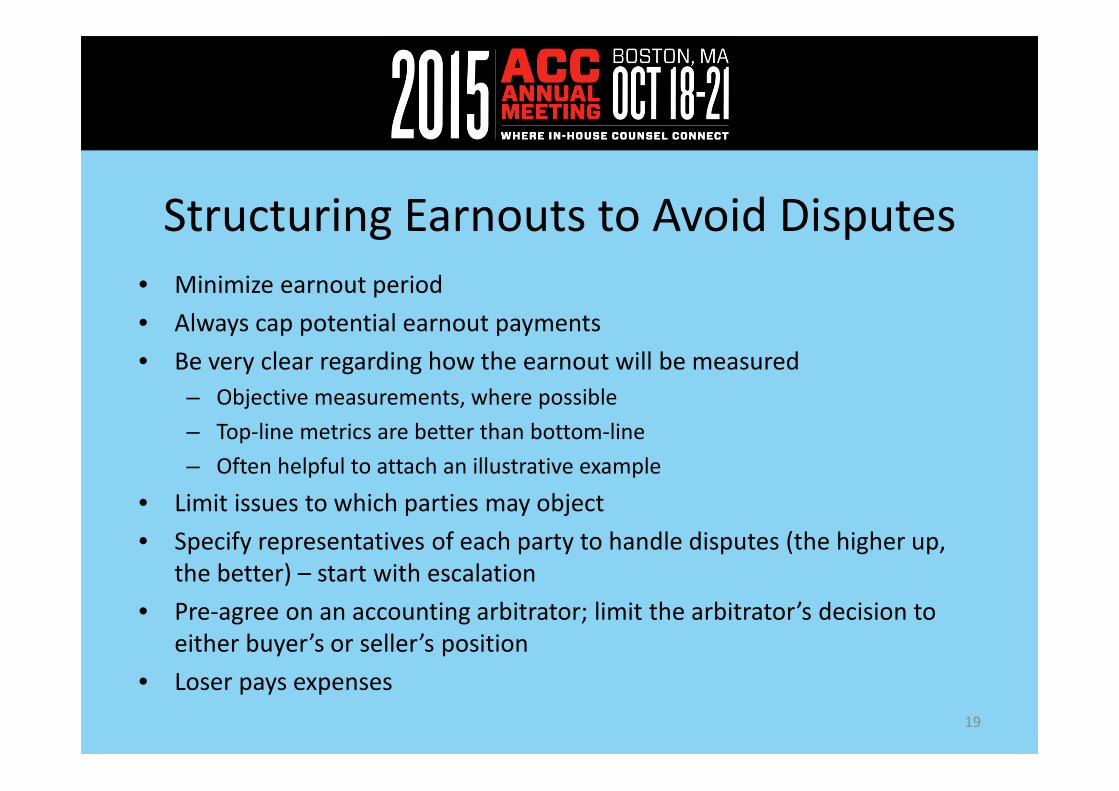

Structuring Earnouts to Avoid Disputes

• Minimize earnout period

• Always cap potential earnout payments

• Be very clear regarding how the earnout will be measured

– Objective measurements, where possible

– Top-line metrics are better than bottom-line

– Often helpful to attach an illustrative example

• Limit issues to which parties may object

• Specify representatives of each party to handle disputes (the higher up,

the better) – start with escalation

• Pre-agree on an accounting arbitrator; limit the arbitrator’s decision to

either buyer’s or seller’s position

• Loser pays expenses

19

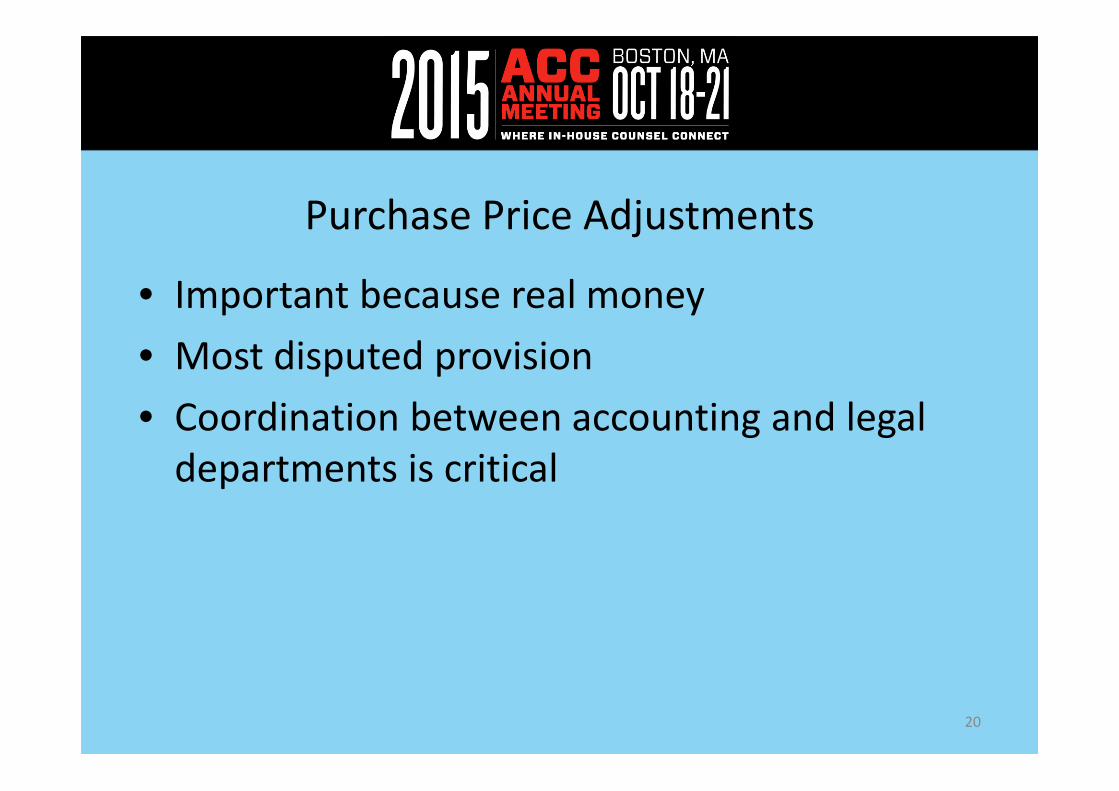

Purchase Price Adjustments

• Important because real money

• Most disputed provision

• Coordination between accounting and legal

departments is critical

20

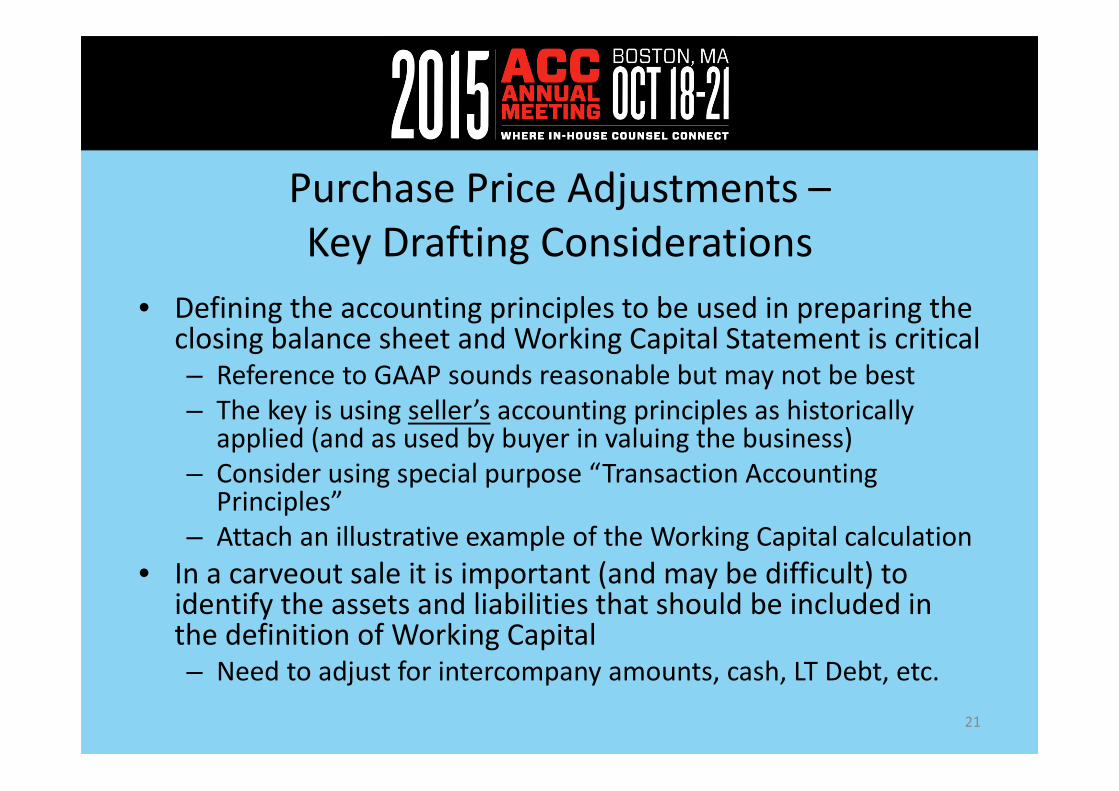

Purchase Price Adjustments –

Key Drafting Considerations

• Defining the accounting principles to be used in preparing the closing balance sheet and Working Capital Statement is critical – Reference to GAAP sounds reasonable but may not be best

– The key is using seller’s accounting principles as historically applied (and as used by buyer in valuing the business)

– Consider using special purpose “Transaction Accounting Principles”

– Attach an illustrative example of the Working Capital calculation

• In a carveout sale it is important (and may be difficult) to identify the assets and liabilities that should be included in the definition of Working Capital– Need to adjust for intercompany amounts, cash, LT Debt, etc.

21

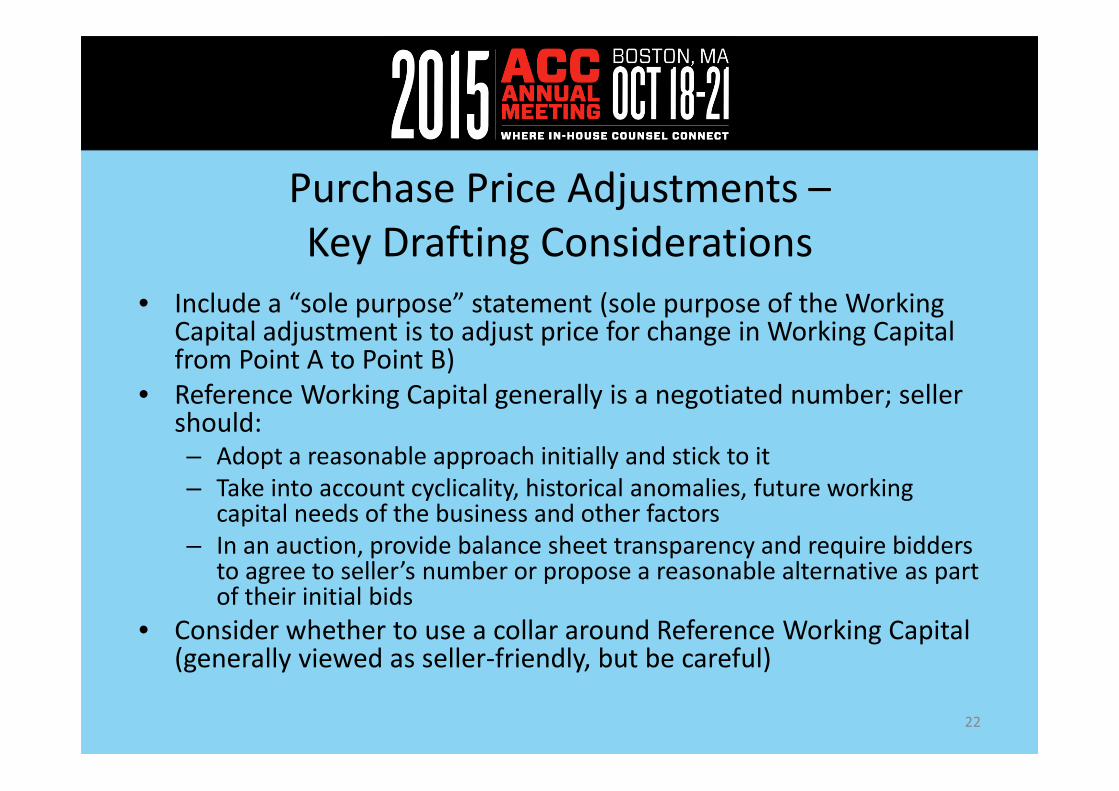

Purchase Price Adjustments –

Key Drafting Considerations

• Include a “sole purpose” statement (sole purpose of the Working Capital adjustment is to adjust price for change in Working Capital from Point A to Point B)

• Reference Working Capital generally is a negotiated number; seller should: – Adopt a reasonable approach initially and stick to it

– Take into account cyclicality, historical anomalies, future working capital needs of the business and other factors

– In an auction, provide balance sheet transparency and require bidders to agree to seller’s number or propose a reasonable alternative as part of their initial bids

• Consider whether to use a collar around Reference Working Capital (generally viewed as seller-friendly, but be careful)

22

Purchase Price Adjustments –

Key Drafting Considerations

• Include estoppel language – resolution of a disputed matter in the Working Capital true-up precludes an indemnity claim on a similar or related matter (no “double-dipping”)

• Estimate of Working Capital should not be subject to buyer approval (can create closing complications, delay)

• Mechanical issues around the “true-up” procedures:– Who prepares initial Working Capital Statement

– Access provisions

– Choice of arbitrator, scope of arbitration, arbitration rules

– “Loser pays” provisions

– Requirement of a “reasoned decision”

23

Purchase Price Adjustments –

Process Tips (Front End)

• Accounting and legal functions must work closely together in preparing reference Balance Sheet and (if applicable) Transaction Accounting Principles

• If the accounting staff for the business is going with the business, recognize their interests may at some point diverge from seller’s – Involvement of seller’s accounting staff or a third party advisor is

important for post-closing continuity

• Certain buyers (e.g., private equity) will not want to pay for cash –make certain that if credit is not given in the Working Capital calculation for cash it can be swept at closing– Particular problem if cash is trapped in non-U.S. subsidiaries

24

Purchase Price Adjustments –

Process Tips (Back End)

• Obtain input from arbitration specialists at time initial Working Capital Statement (or Notice of Disagreement) is prepared – Legal

– Forensic accountant

• Consider having physical inventory completed at or about time of closing (w/ access given to buyer’s accounting staff)

• Comply with all technical timing requirements in the purchase agreement and establish record of good faith / fair dealing

• Use care in negotiating arbitrator’s engagement letter

• Recognize that an accounting arbitrator is likely to take a different approach from a judge – More focus on facts and GAAP, less on legal principles

25

Purchase Price Adjustments: Lesson Learned

• Case Study – Seller planned to sell $5.6 million facility

• After signing, Buyer asked Seller not to sell facility

• Seller agreed

– Buyer had surprise for Seller during working capital adjustment

• Seller had included $5.6 million facility as current asset, because held for sale

• Buyer classified as long-term asset at closing, because no longer held for sale

• Seller lost $5.6 million in purchase price

• Lesson: When making post-signing changes, consider impacts on other parts of the deal

26

M&A Due Diligence

Hot Buttons

M&A Due Diligence Hot Buttons

• Time to update your M&A due diligence checklist

• Increased globalization coupled with a spike in

enforcement activity has made effective due

diligence of certain topics critical

– Foreign Corrupt Practices Act (FCPA)

– Office of Foreign Assets Control (OFAC)

– Cyber Risk

28

FCPA Enforcement in the M&A Context

• Expectation by SEC / DOJ that companies perform FCPA due

diligence in M&A context

• Several settlements involve FCPA violations discovered in the

course of pre-acquisition due diligence and voluntarily

disclosed as a condition of deal – Collapse of Lockheed Martin’s proposed $1.6 billion acquisition of Titan

– Deferred prosecution agreement entered into by Invision Technologies, Inc.

prior to acquisition by GE

– SEC / DOJ settlements by Syncor, Inc. prior to acquisition by Cardinal Health

– ABB, Ltd. and ABB Vetco settlement involving $10.5 million criminal fine and

$5.9 million disgorgement

29

FCPA Enforcement in the M&A Context

• Risk of successor liability for target’s prior FCPA violations

• Significant factors in determining whether government will

pursue a prosecution under a successor liability theory:

– The extent of the due diligence conducted to identify and

address potential issues

– The extent and effectiveness of safeguards adopted upon

acquisition to prevent reimbursement by the acquirer of

improper actions and to prevent them in the future

– Whether the company self-reported the problem

30

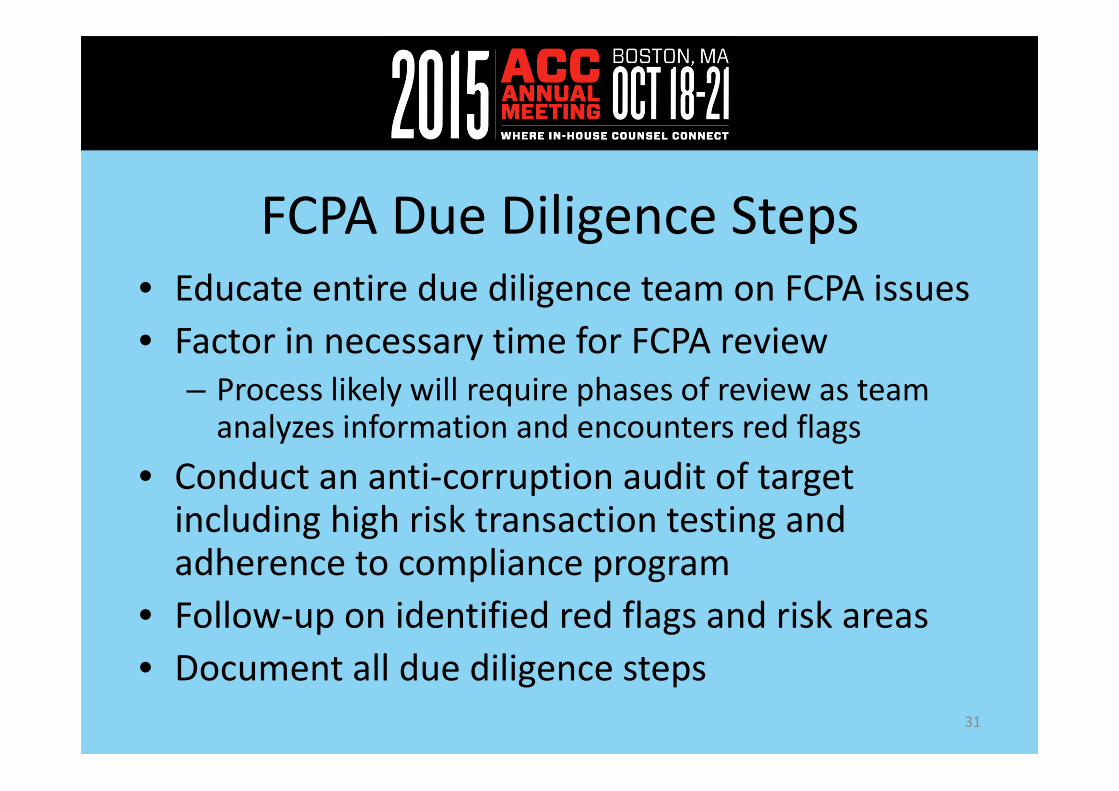

FCPA Due Diligence Steps• Educate entire due diligence team on FCPA issues

• Factor in necessary time for FCPA review

– Process likely will require phases of review as team analyzes information and encounters red flags

• Conduct an anti-corruption audit of target including high risk transaction testing and adherence to compliance program

• Follow-up on identified red flags and risk areas

• Document all due diligence steps

31

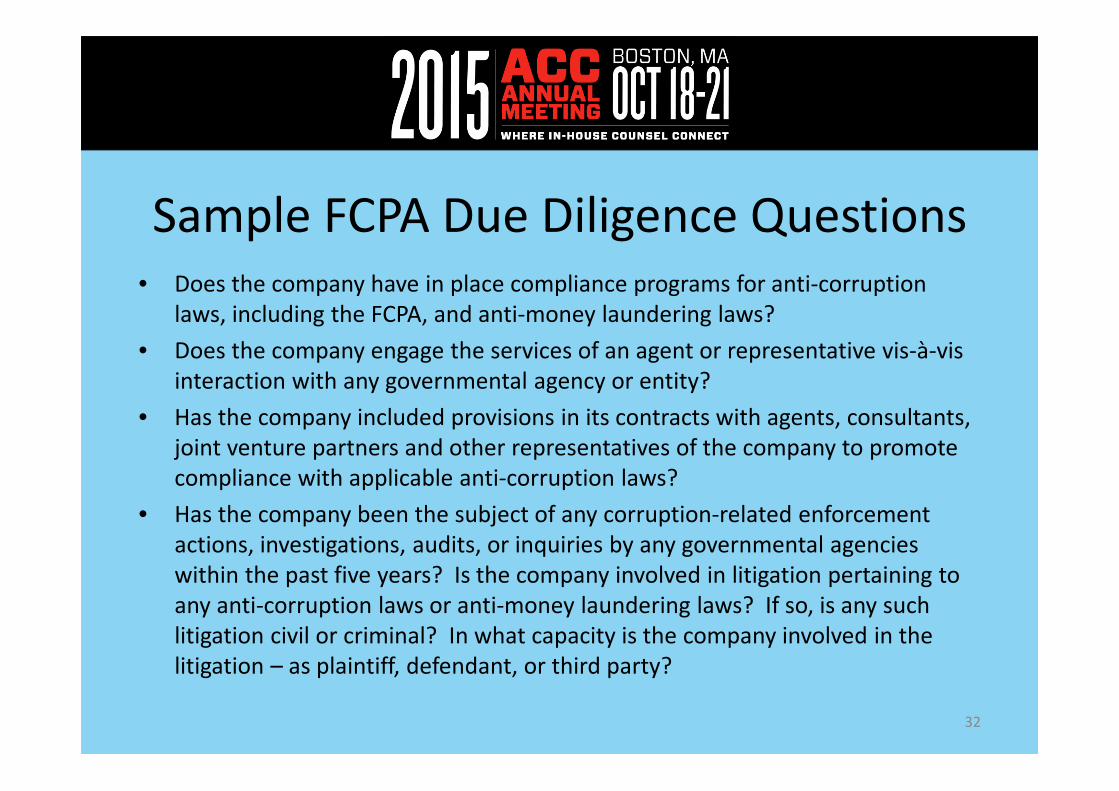

Sample FCPA Due Diligence Questions• Does the company have in place compliance programs for anti-corruption

laws, including the FCPA, and anti-money laundering laws?

• Does the company engage the services of an agent or representative vis-à-vis

interaction with any governmental agency or entity?

• Has the company included provisions in its contracts with agents, consultants,

joint venture partners and other representatives of the company to promote

compliance with applicable anti-corruption laws?

• Has the company been the subject of any corruption-related enforcement

actions, investigations, audits, or inquiries by any governmental agencies

within the past five years? Is the company involved in litigation pertaining to

any anti-corruption laws or anti-money laundering laws? If so, is any such

litigation civil or criminal? In what capacity is the company involved in the

litigation – as plaintiff, defendant, or third party?

32

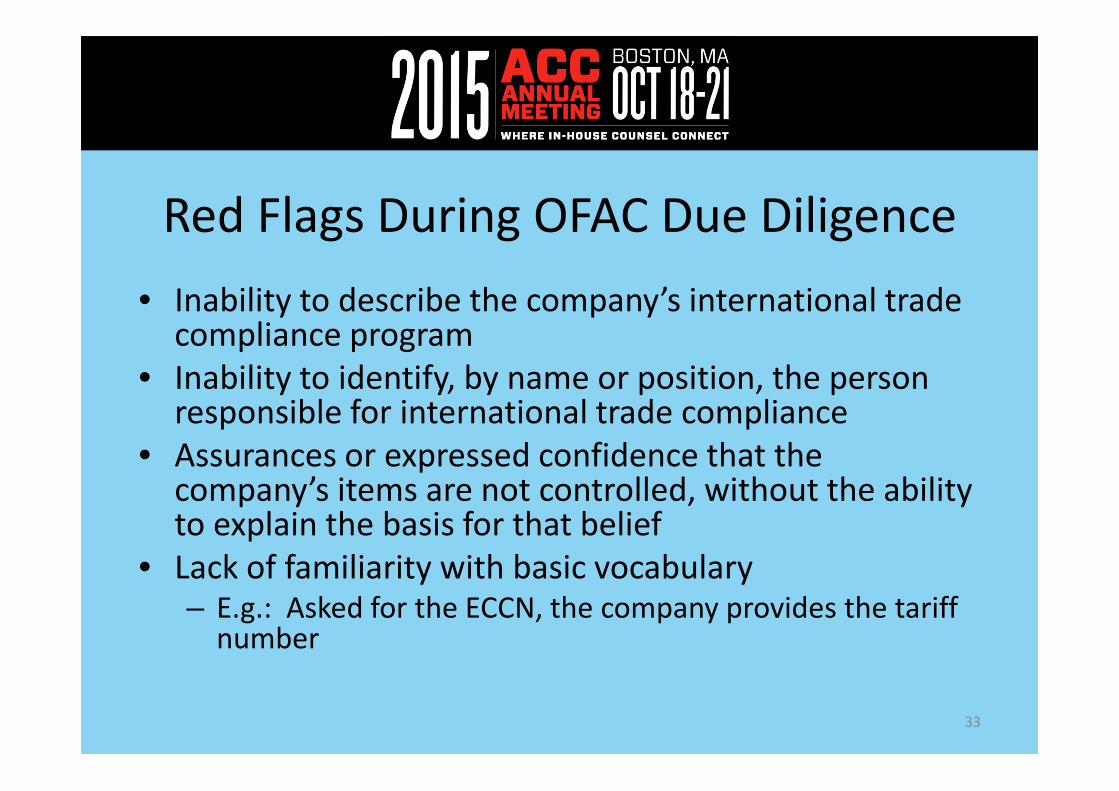

Red Flags During OFAC Due Diligence

• Inability to describe the company’s international trade compliance program

• Inability to identify, by name or position, the person responsible for international trade compliance

• Assurances or expressed confidence that the company’s items are not controlled, without the ability to explain the basis for that belief

• Lack of familiarity with basic vocabulary– E.g.: Asked for the ECCN, the company provides the tariff

number

33

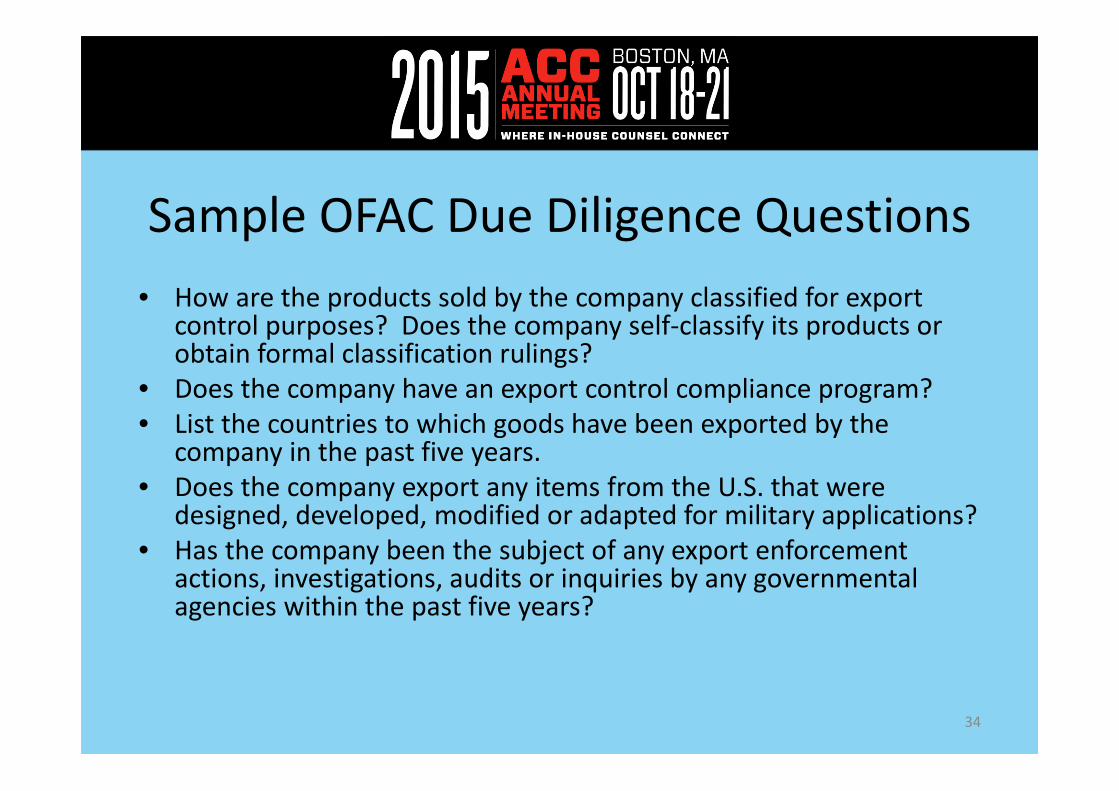

Sample OFAC Due Diligence Questions

• How are the products sold by the company classified for export control purposes? Does the company self-classify its products or obtain formal classification rulings?

• Does the company have an export control compliance program?

• List the countries to which goods have been exported by the company in the past five years.

• Does the company export any items from the U.S. that were designed, developed, modified or adapted for military applications?

• Has the company been the subject of any export enforcement actions, investigations, audits or inquiries by any governmental agencies within the past five years?

34

Reasons to Conduct Diligence on Cyber Risk

• Value of a deal can drop if there was a prior breach or a breach is discovered post-closing – Buyer should discuss cyber insurance rider with broker

• Helps to evaluate whether target is properly securing key assets and information (R&D, IP, trade secrets, systems, etc.)

• Helps to evaluate the capital (human and financial) that would be needed to implement sufficient controls

• Absence of controls could cause significant financial and reputational harm

• Absence of controls could lead to litigation (class actions) / government enforcement / fines

35

Cyber Risk Due Diligence Steps

• No one-size fits all approach– Depends on the nature of the company and sensitivity

of its information

• Combination of document requests, interviews and review of actual processes, procedures and controls/systems

• Prioritize more important issues– Identify the most sensitive information; determine

where it is stored and if those systems are protected

36

Cyber Risk Due Diligence Steps

• Types of documents to request:– Defined privacy policies

– Information Security (passwords, user access, firewalls, etc.)

– Incident Response Plan

– IS Test / Audits / Assessments – internal or external re: technology or security

– Retailers accepting credit cards – PCI / Annual Report on Compliance

– Training materials on basic cyber procedures, policies, and risks (e.g., password, phishing scams, access, etc.)

– Diligence regarding third parties or provisions in third party contracts

– Cyberinsurance policies

37

Cyber Risk Due Diligence Steps

• Questions to ask:– What controls are in place?

– How do they assess security and how often?

– Any prior breaches? If so, how handled and resolved?

– Any government inquiries or enforcement issues? Litigation?

– Any violations of the policies above?

– What privacy-related practices are in place?

38

Common Issues in

Corporate Carveouts

Considerations in Corporate Carveouts

• Assess shared assets, personnel, IP, contracts

• Sufficiency of assets rep critical

• Insurance regime / self-insurance

• Capital expenditures

• Deep diligence on transition services

40

Common Issues in Corporate Carveouts• Identifying the business to be sold

– Is this really a “business” or a portfolio of assets?

– What assets, people or services are needed to operate the business post-closing?

• Financial statements and projections – Will you need an independent audit?

– Determine an appropriate level of baseline working capital

– Review and update projections with management

• Contract review / legal preparation– Advance review of key agreements and leases for anti-assignment and change of

control provisions

– Review intercompany agreements

• HR matters– Identify early the key employees that would “go with the business”

– Execute retention agreements as appropriate

– Understand benefits platform of transferred employees

– Consider WARN Act issues

41

Shareholder Activism

Relating to M&A

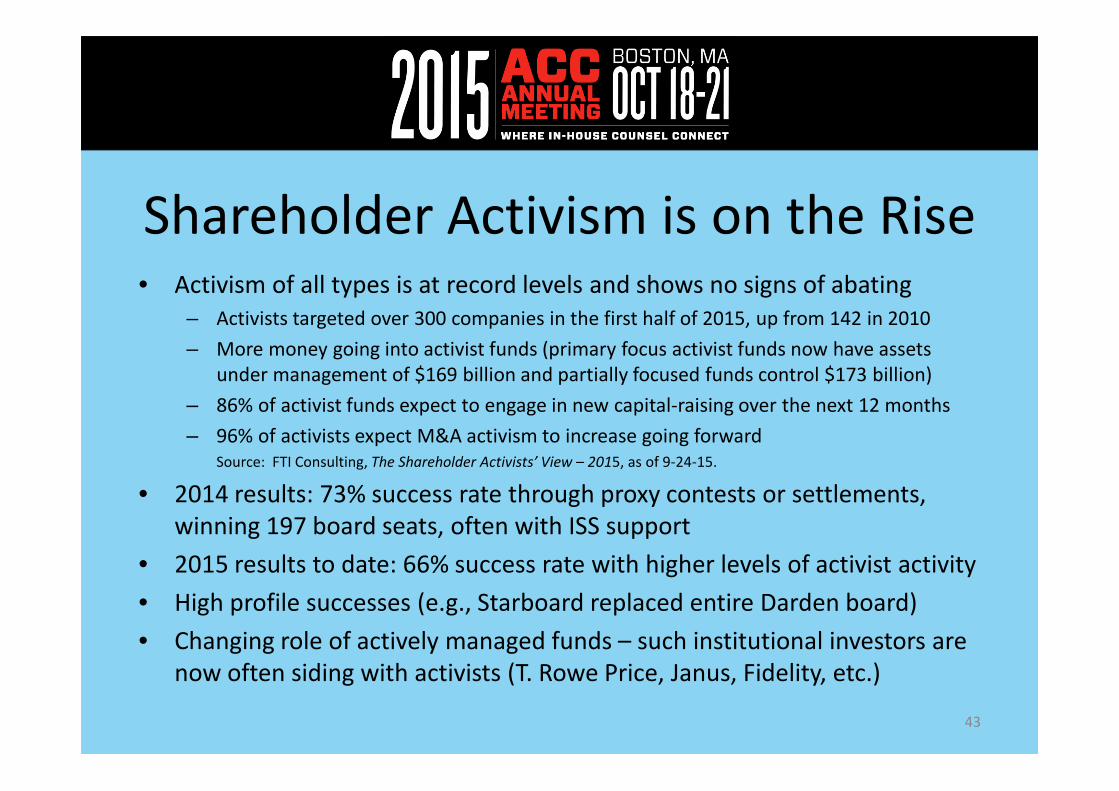

Shareholder Activism is on the Rise• Activism of all types is at record levels and shows no signs of abating

– Activists targeted over 300 companies in the first half of 2015, up from 142 in 2010

– More money going into activist funds (primary focus activist funds now have assets

under management of $169 billion and partially focused funds control $173 billion)

– 86% of activist funds expect to engage in new capital-raising over the next 12 months

– 96% of activists expect M&A activism to increase going forward Source: FTI Consulting, The Shareholder Activists’ View – 2015, as of 9-24-15.

• 2014 results: 73% success rate through proxy contests or settlements,

winning 197 board seats, often with ISS support

• 2015 results to date: 66% success rate with higher levels of activist activity

• High profile successes (e.g., Starboard replaced entire Darden board)

• Changing role of actively managed funds – such institutional investors are

now often siding with activists (T. Rowe Price, Janus, Fidelity, etc.)

43

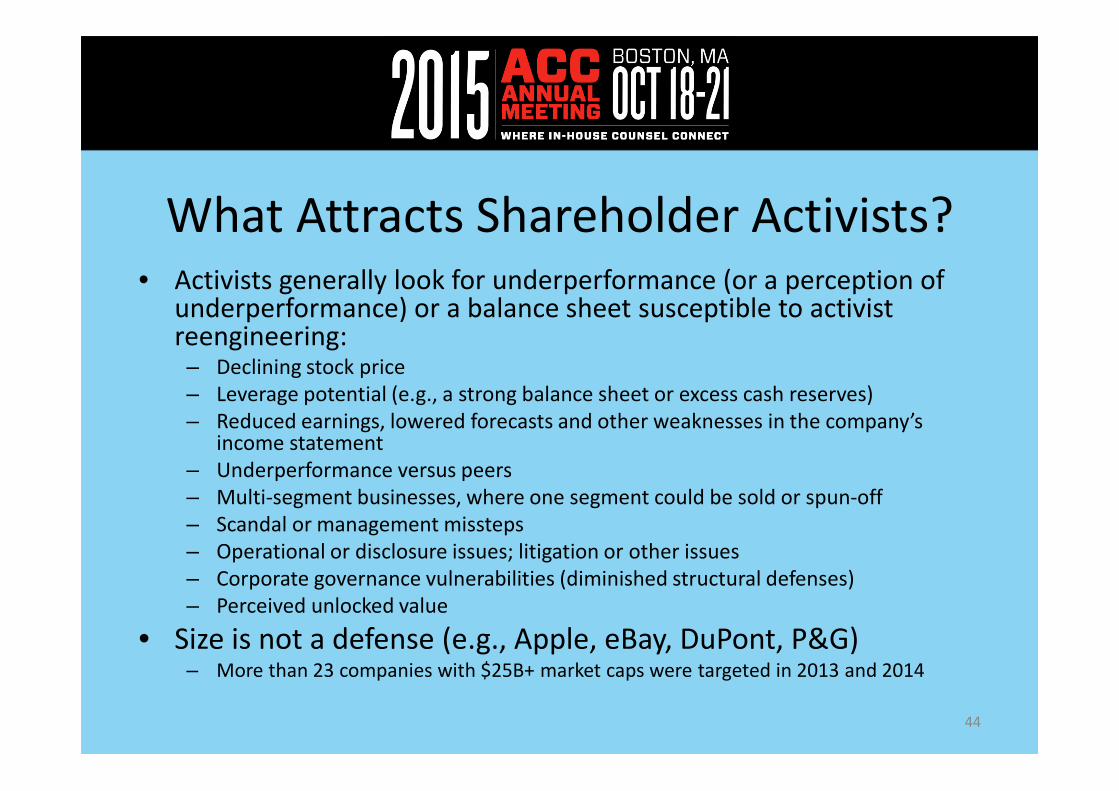

What Attracts Shareholder Activists?• Activists generally look for underperformance (or a perception of

underperformance) or a balance sheet susceptible to activist reengineering:– Declining stock price

– Leverage potential (e.g., a strong balance sheet or excess cash reserves)

– Reduced earnings, lowered forecasts and other weaknesses in the company’s income statement

– Underperformance versus peers

– Multi-segment businesses, where one segment could be sold or spun-off

– Scandal or management missteps

– Operational or disclosure issues; litigation or other issues

– Corporate governance vulnerabilities (diminished structural defenses)

– Perceived unlocked value

• Size is not a defense (e.g., Apple, eBay, DuPont, P&G)– More than 23 companies with $25B+ market caps were targeted in 2013 and 2014

44

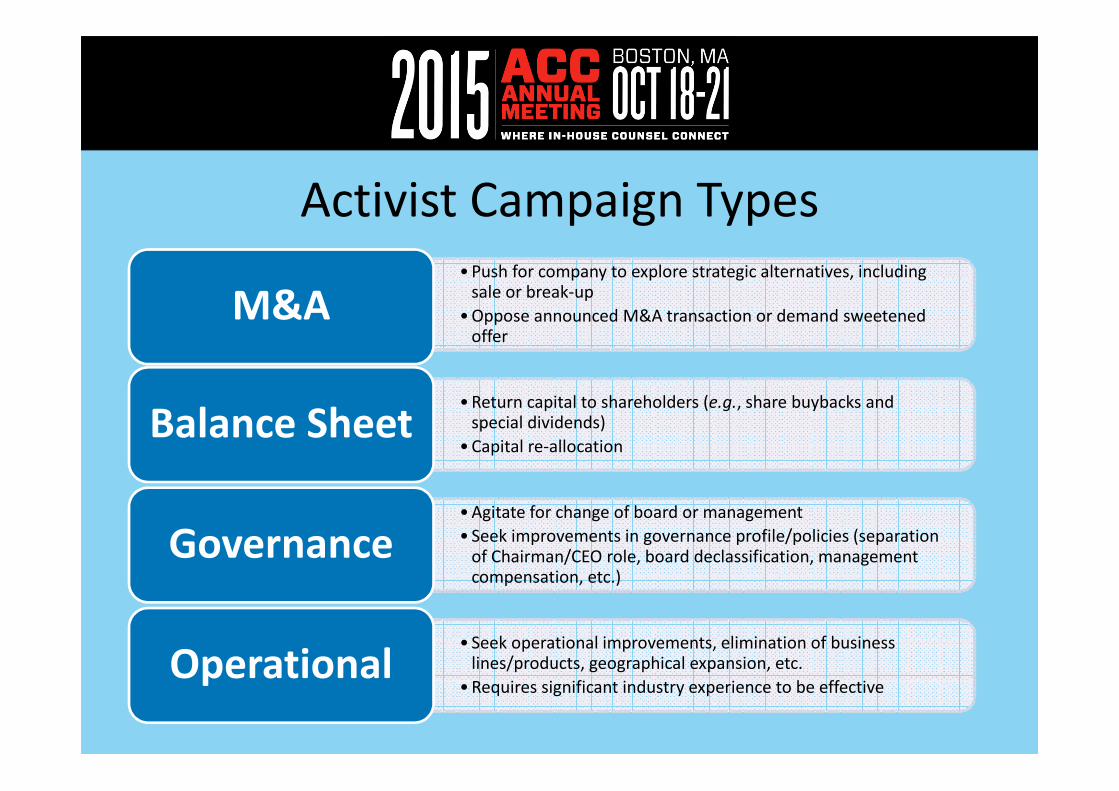

Activist Campaign Types• Push for company to explore strategic alternatives, including

sale or break-up

• Oppose announced M&A transaction or demand sweetened offer

M&A

• Return capital to shareholders (e.g., share buybacks and special dividends)

• Capital re-allocationBalance Sheet

• Agitate for change of board or management

• Seek improvements in governance profile/policies (separation of Chairman/CEO role, board declassification, management compensation, etc.)

Governance

• Seek operational improvements, elimination of business lines/products, geographical expansion, etc.

• Requires significant industry experience to be effectiveOperational

46

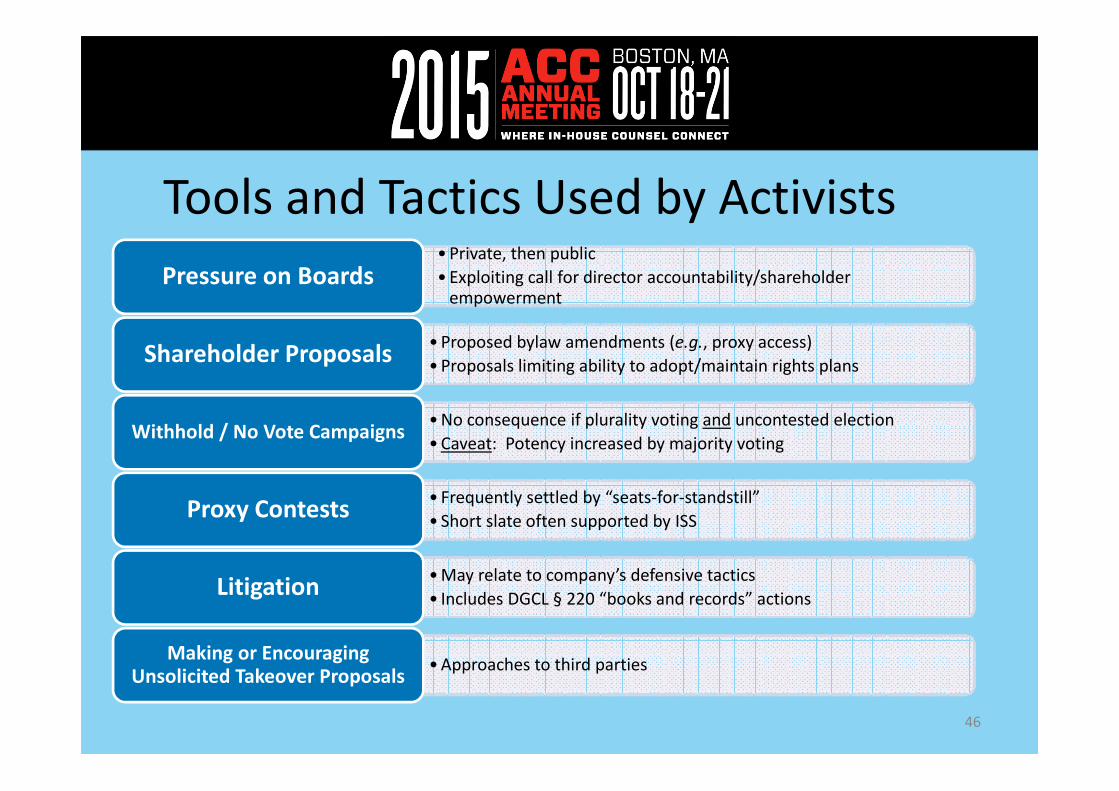

• Private, then public

• Exploiting call for director accountability/shareholder empowerment

Pressure on Boards

• Proposed bylaw amendments (e.g., proxy access)

• Proposals limiting ability to adopt/maintain rights plansShareholder Proposals

• No consequence if plurality voting and uncontested election

• Caveat: Potency increased by majority votingWithhold / No Vote Campaigns

• Frequently settled by “seats-for-standstill”

• Short slate often supported by ISSProxy Contests

• May relate to company’s defensive tactics

• Includes DGCL § 220 “books and records” actionsLitigation

• Approaches to third partiesMaking or Encouraging

Unsolicited Takeover Proposals

Tools and Tactics Used by Activists

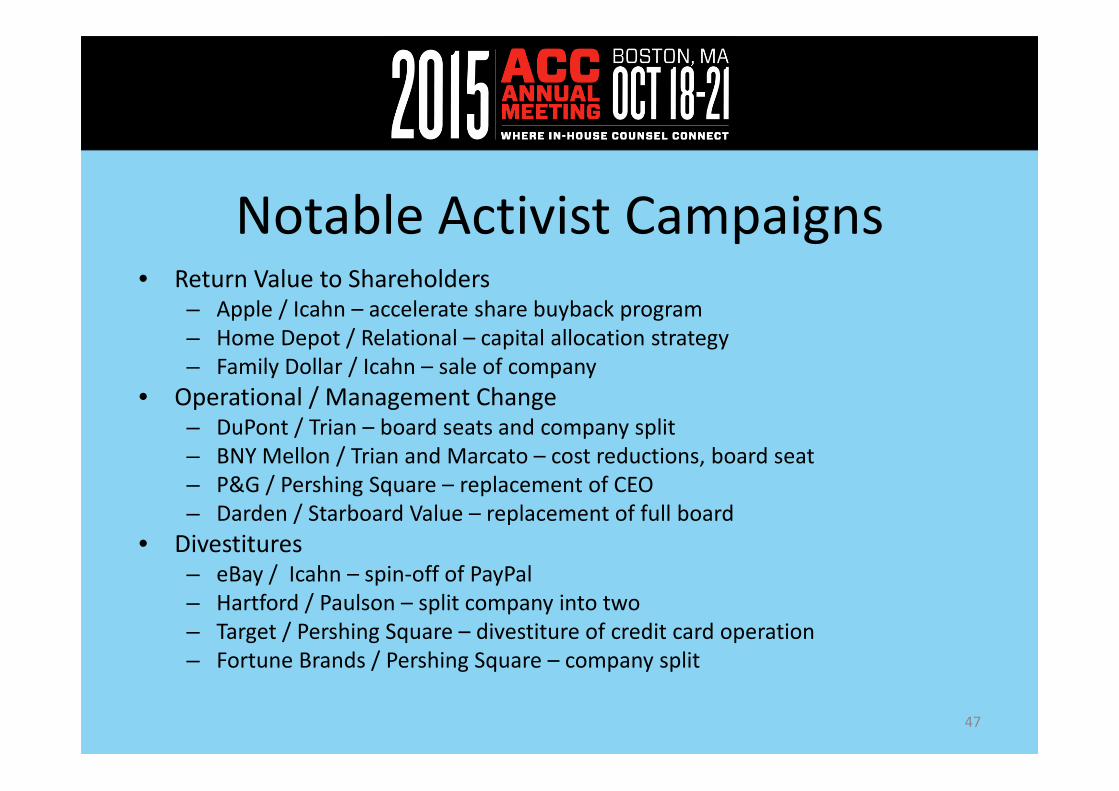

Notable Activist Campaigns• Return Value to Shareholders

– Apple / Icahn – accelerate share buyback program

– Home Depot / Relational – capital allocation strategy

– Family Dollar / Icahn – sale of company

• Operational / Management Change– DuPont / Trian – board seats and company split

– BNY Mellon / Trian and Marcato – cost reductions, board seat

– P&G / Pershing Square – replacement of CEO

– Darden / Starboard Value – replacement of full board

• Divestitures– eBay / Icahn – spin-off of PayPal

– Hartford / Paulson – split company into two

– Target / Pershing Square – divestiture of credit card operation

– Fortune Brands / Pershing Square – company split

47

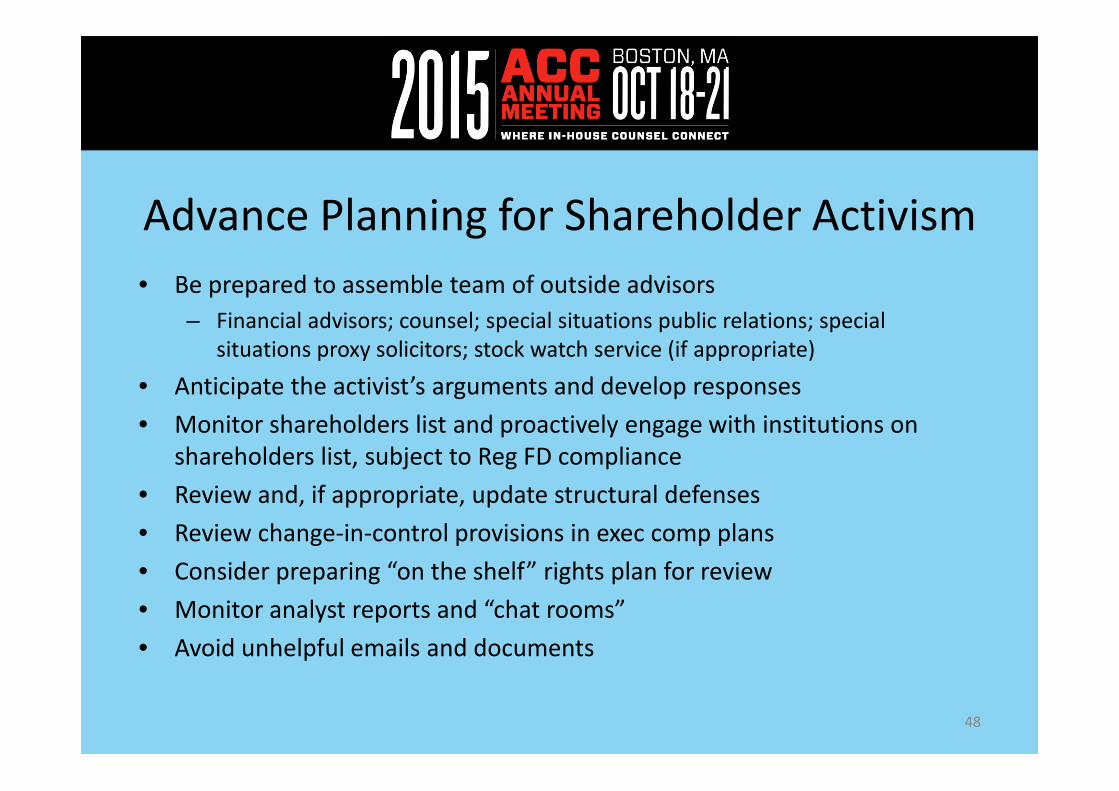

Advance Planning for Shareholder Activism

• Be prepared to assemble team of outside advisors

– Financial advisors; counsel; special situations public relations; special

situations proxy solicitors; stock watch service (if appropriate)

• Anticipate the activist’s arguments and develop responses

• Monitor shareholders list and proactively engage with institutions on

shareholders list, subject to Reg FD compliance

• Review and, if appropriate, update structural defenses

• Review change-in-control provisions in exec comp plans

• Consider preparing “on the shelf” rights plan for review

• Monitor analyst reports and “chat rooms”

• Avoid unhelpful emails and documents

48

Lessons Learned from

Recent M&A Litigation

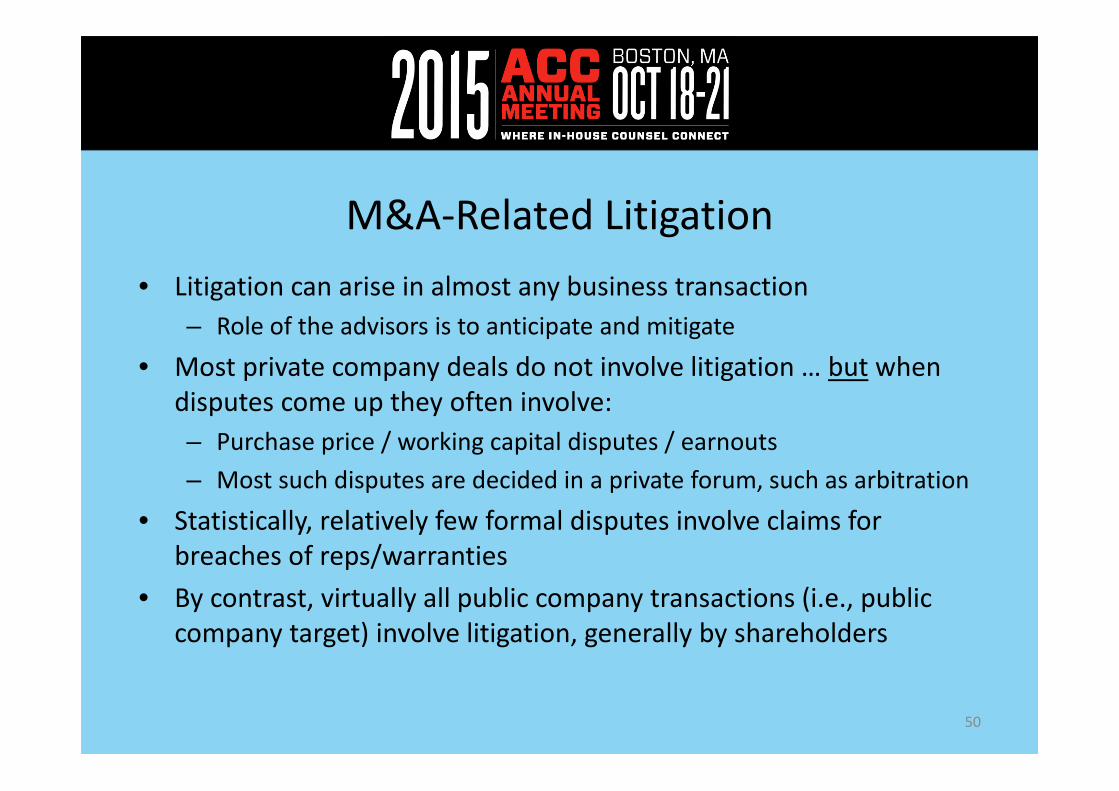

M&A-Related Litigation

• Litigation can arise in almost any business transaction

– Role of the advisors is to anticipate and mitigate

• Most private company deals do not involve litigation … but when

disputes come up they often involve:

– Purchase price / working capital disputes / earnouts

– Most such disputes are decided in a private forum, such as arbitration

• Statistically, relatively few formal disputes involve claims for

breaches of reps/warranties

• By contrast, virtually all public company transactions (i.e., public

company target) involve litigation, generally by shareholders

50

M&A-Related Litigation

• Virtually every public company merger in the U.S. will result in

shareholder litigation

• Shareholder litigation generally names board members of target

company (among others) and alleges state law breach of

fiduciary duties and federal proxy law violations

• In practice, most suits settle for nominal (and fairly predictable)

amounts (but increased scrutiny of settlements recently)

• But cases involving bad facts and/or bad process can result in

significant liability exposure for the directors and others

participants (including financial advisors) and potentially

jeopardize the transaction

51

Lessons Learned from Recent M&A Litigation

• Recent rulings indicate that the Delaware Chancery Court is

becoming less willing to approve disclosure-only M&A

settlements (Aeroflex, Riverbed Technologies)

– “Peppercorn” of consideration (e.g., disclosures and fees for plaintiffs’

attorneys) may no longer be sufficient to support an “intergalactic”

release of claims

– May cause plaintiffs’ attorneys to file claims outside of Delaware

– Even for companies with Delaware exclusive forum bylaws, plaintiffs

may pursue federal disclosure claims in a different jurisdiction

52

Importance of Good Process

• Be vigilant for conflicts (among board, management and advisors)

• Brief board on duties and importance of process early

• Understand management team’s incentives and ensure appropriate procedural safeguards are in place

• Use care in preparing materials for the board, planning meetings and documenting the minutes

• Take proactive measures where conflicts exist:

– Conflicted persons abstain from key deliberations / votes

– Potentially form special committee of independent directors (but must be properly formed and independent in fact)

• Active, informed participation by directors on key decisions

53

Use of Financial Advisors

• An important protection for directors is to obtain the advice of an independent financial advisor (and if appropriate a fairness opinion)

• There can be judicial scrutiny of the financial advisor’s activities / independence (Rural Metro, Del Monte, El Paso)

• Thus, financial advisors should be thoroughly screened for subject matter competence and independence

• Engagement letter safeguards (e.g., reps) may be useful

• Board involvement in screening process and terms of banker engagement is appropriate

• Common potential conflicts: (i) lending or advisory relationships with potential bidders; (ii) equity ownership in potential bidders; (iii) buyside or “staple” financing

54

Appraisal Arbitrage

• Recently hedge funds have shown an increased interest in appraisal rights

– Significant uptick in claims in Delaware: from 10 in 2010 to 33 in 2014

– Since 2010, Delaware courts have granted increases between 8.5% and 149% of merger price in 7 of 9 cases decided

• Statutory interest provides good incentive

– 5% plus federal funds rate (versus current low interest rate environment)

– Can be awarded even if court ultimately awards merger price

• But note pending amendments to DGCL Section 262

– Would permit surviving corporations to limit the accrual of statutory interest on appraisal awards, thereby reducing economic incentive

55

Appraisal Rights – Avoiding Pitfalls

• Delaware Chancery Court permitted a claim to be brought under Delaware’s

appraisal statute even though petitioner purchased shares after public

announcement of merger solely to bring an appraisal lawsuit and could not prove

that shares had not been voted in favor of the deal (Merion Capital, Jan. 2015)

• Be aware of the state of jurisdiction (outside Delaware the risks of an unfavorable

outcome may be greater)

• Be aware of when appraisal rights trigger

– Not just all-cash mergers – can include asset sales, recaps, cash/stock mergers and

extraordinary dividends

• Merger documentation:

– Get waiver of appraisal rights in voting agreements from key shareholders

– Enforce waivers of appraisal rights in shareholder agreements, if applicable

– Cooperation provisions in merger agreement

– Closing condition in merger agreement

56

Reducing the Threat of M&A Litigation

• Leo E. Strine, Jr., Chief Justice of the Delaware Supreme Court, recently published an article* highlighting actions that directors and legal and financial advisors can take in an M&A process to:

– Promote making better decisions

– Reduce conflicts of interests and address those that exist more effectively

– Accurately record what happened so that advisors and their clients will be able to recount events in approximately the same way

– As a result, reduce the target zone for plaintiffs’ lawyers

57

Reducing the Threat of M&A Litigation -

Documenting the Deal

• Important to record in the minutes the advice received from financial advisers regarding, and Board's reason for making, critical decisions– How conflicts were handled

– How many potential buyers, and what kind, to solicit

– When to narrow the field or allow bidders to club

– When to allow discussions with management

– When to revise projections and why assumptions were changed

– Whether some valuation methods are more or less important than others

• Document the range of factors considered in connection with each major decision

• Identify clearly what the Board decided and why

58

Reducing the Threat of M&A Litigation -

Documenting the Deal

• Consider how to reflect advice of counsel– Reliance on counsel can help in defense

– Requires partial waiver of privilege

• Changes to investment banker board books– Where possible, prepare blacklines

– In any event, include summary of what changed and why

– Plaintiffs' lawyers will try to exploit changes that make the transaction appear more fair

• Provide materials to directors in advance so they can review them before the meeting

59

Allocating Antitrust

Risk in M&A Deals

Antitrust Risk in M&A Deals• Significant execution risks from antitrust inquiry by:

– DOJ or FTC (U.S.)

– EU or other ex-U.S. governmental entity

• Heightened scrutiny from DOJ and FTC activity under the Obama administration

• Ex-U.S. jurisdictions also can pose risk and delay (e.g., PRC)

• Potential governmental responses (in order of severity):– Verbal inquiries / customer calls

– Pull and re-file

– Formal second request / investigation

– Forced (or agreed) divestitures or other remedies

– Injunction

61

Allocating Antitrust Risk in M&A Deals

• Bottom line: What is the point beyond which any

divestitures are commercially unacceptable?

• Buyer’s objectives when proposing antitrust risk

allocation provisions:

– Show seller that buyer is accepting some risks but cap them

– Avoid giving regulators a “road map” or undercutting

negotiating power with regulators

– Make obligations clear to avoid potentially costly disputes

62

Antitrust Risk – Contract Terms• “Best efforts” and cooperation clauses

• Agreement to litigate, comply with second request

• Divestiture requirements: – Specific assets (but “road map” problem)

– MAE / “material divestitures” / express $ cap

– “Hell or high water” provision (unusual)

• Covenant not to engage in other transactions

• Reverse termination fee:– No obligation to divest

– But buyer pays fee (typically “x% of deal equity value”) if clearances not obtained

63

Variations on Reverse Termination Fees• May or may not be seller’s sole and exclusive remedy

• Ticking fee: Fee increases at certain intervals if merger is not closed (or terminated) before a specified date

• Option to either comply with a governmental divestiture request or terminate agreement and pay fee

• Fee payable if agreement is terminated due to a final non-appealable injunction under the antitrust laws that permanently prevents the merger from closing as long as certain other closing conditions are satisfied

• Average fee of 5.18% (median fee of 4.76%) of total deal value based on sample of 64 deals that closed since April 2011

Source: Practical Law, What’s Market: Reverse Break-Up Fees for Antitrust Failure.

64

Antitrust Risk – Avoiding Litigation• Both parties must exercise care in due diligence (e.g., clean team

arrangements) to avoid perceived improper sharing of competitively sensitive information

• Antitrust counsel should engage in early discussions regarding potential overlaps and remedies

• Principal agreement should be clear as to which jurisdictions will require filings / clearances (important for seller)

• More clarity on degree of “efforts” is preferable than naked “best efforts” provision

• But remember … governmental authorities will read the agreement (“road map” issue)

65

Questions?