Embed Size (px)

Citation preview

OrthoIndex™

Chicago, Illinois

OrthoIndex™

Chicago, Illinois

Challenges of Integrating Physicians

John Cherf MD, MPH, MBA Chief of Orthopedics, Advocate IMMC President, OrthoIndex CMO, PinpointCare

Kevin McCune, MD CMO, Advocate Medical Group Senior Medical Director, Advocate at Home

Physicians Legal Issues Conference Chicago, IL

June 9-10, 2016

At a Time When The Market Is Demanding Integration

OrthoIndex™ 2 OrthoIndex™ 2

I do not have any relevant financial relationships to disclose.

OrthoIndex™ OrthoIndex™

Review of Healthcare Reform Impact of New Payment Model’s on Physicians Preparing for the Future

Agenda

1996BRA, HIPAA

OrthoIndex™ 4 OrthoIndex™ 4

History of Healthcare Reform

Medicare (Part A and B) and Medicaid incorporated under Social Security Act 1965

Medicare introduces Diagnostic Related

groups (DRGs) 1983

Medicare Drug, Improvement, and Modernization Act

2003

1996 EMTALA, COBRA,

HIPAA

Deficit Reduction Act, Tax Relief and Health Care Act 2005

2006 Medicare Part D

1977 Health Care Financing Administration (HCFA) established within the Department of Health,

Education and Welfare (HEW)

1997 Balanced Budget Act

2015

Medicare Access and CHIP Reauthorization Act

(MACRA)

PPACA and HCERA (ACA) 2010

Source: OrthoIndex Analysis, 2015.

1996BRA, HIPAA

OrthoIndex™ 5 OrthoIndex™ 5

ACA: Key Components

PL 111-148, The Patient Protection and Affordable Care Act (PPACA), signed into law on March 23, 2010 Health Care and Education Reconciliation

Act (HCERA) of 2010, signed into law on March 30, 2010 Focus is largely on expansion of coverage

and insurance regulation Supports pilots and demonstrations

designed to control cost and reform care delivery (new payment models) and funds the Innovation Center Lays the foundation for more regulation

and oversight (MACRA)

MACRA = Medicare Access and CHIP (Children’s Health Insurance Program) Reauthorization Act.

1996BRA, HIPAA

OrthoIndex™ 6 OrthoIndex™ 6

New Payment Models Are About Managing Risk To A Budget

Lower Risk/ Value Potential

Higher Risk/ Value Potential

Fee-for-Service

Traditional Prospective Capitation

Risk-Sharing/ ACOs

Bundled Payments

Risk to Provider

Moving from a Fee-For-Service to a Value-Based Payment System

1996BRA, HIPAA

OrthoIndex™ 7 OrthoIndex™ 7

Transformation to a More Collaborative Healthcare Economy

IP

Lab

PAC

Home Imaging OP

Office

MD

IP = Inpatient, OP = Outpatient, PAC = post acute care..

1996BRA, HIPAA

OrthoIndex™ 8 OrthoIndex™ 8

2014

… efficient, coordinated and high quality care

A Commitment to Value and Quality

2016 2018 2011

68%

>80% 85% 90%

~20% 0%

30% 50%

Historical Performance HSS Goals

HSS = The Department of Health and Human Services; APM = Alternative Payment Model; FFS = fee-for-service. Source: CMS, 2015.

APMs (ACOs, Bundled Payments, etc.) FFS linked to quality All Medicare FFS

1996BRA, HIPAA

OrthoIndex™ 9 OrthoIndex™ 9

Medicare Access and CHIP Reauthorization Act of 2015 (MACRA)

Eliminates the SGR formula (and avoids a 21% cut) and provides new updates the Medicare Physician Fee Schedule (MPFS) Shifts MPFS to two new value-based physician payment tracks Merit-Based Incentive Payment System (MIPS) Alternative Payment Models (APM)

Encourages providers taking risk (two-sided) Bipartisan support suggest longevity beyond 2016 Provides clarity for future provider payments Continues the evolution of bundled payments

The SGR Repeal Law: Key Points

CHIP = Children’s Health Insurance Program; SGR = sustainable growth rate. Source: OrthoIndex Analysis, 2015.

Bundled Payments: Connecting the Unconnected

1996BRA, HIPAA

OrthoIndex™ 10 OrthoIndex™ 10

Sustainable Growth Rate (SGR)

Repeals the Sustainable Growth Rate (SGR) Formula Changes the way Medicare

pays clinicians Streamlines multiple quality

reporting programs in to 1 new system (MIPS) Provides bonus payments for

participation in eligible alternative payment models (APMs)

Quality Payment Program (QPP)

Implements the Quality Payment Program (QPP) Establishes a new framework to

reward value over volume Immense and complex Favors primary care over

specialists and large over small physician practices Increases provider costs

required for compliance

MACRA

1996BRA, HIPAA

OrthoIndex™ 11 OrthoIndex™ 11

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 and later

Physician Fee

schedule updates (%)

+0.5 +0.5 +0.5 +0.5 0 0 0 0 0 0 +0.75 QAPMCF*

+0.25 N-QAPMCF**

MIPS (%)

PQRS, Value Modifier, EHR Incentives +/- 4 +/- 5 +/- 7 +/- 9

Eligible

APMs (%)

Physician Value-Based Payment Timeline

Excluded from MIPS

*Qualifying APM conversion factor; **Non-qualifying APM conversion factor. MIPS = merit-based incentive payment system; PQRS = physician quality reporting system; EHR = electronic health record; APM = alternative payment model. Source: CMS; OrthoIndex Analysis, 2016.

+/- 9%

+5% Incentive Payment

1996BRA, HIPAA

OrthoIndex™ 12 OrthoIndex™ 12

Not in APM In non-Advanced APM QP in Advanced APM

Some clinicians may be in Advanced APMs but

not have enough payments or patients through the advanced

APM to be a QP.

In Advanced APM, but not a QP

Most Practitioners Will Be Subject to MIPS

Subject to MIPS (90%) Qualify for APM (10%)

MIPS = Merit-Based Incentive Payment System; APM = Alternative Payment Model; QP = qualified provider.

1996BRA, HIPAA

OrthoIndex™ 13 OrthoIndex™ 13

Practice Size Clinicians Negative

Adjustment

Average Negative

Adjustment

Positive Adjustment

Average Positive

Adjustment

No Adjustment

1 102,788 14% 87.0% $2,919 12.9% $1,022 ˂0.1%

2-9 123,695 16% 69.9% $2,256 29.8% $2,385 ˂0.1%

10-24 81,207 11% 59.4% $1,244 40.3% $2,020 ˂0.1%

25-99 147,976 19% 44.9% $642 54.5% $1,554 ˂0.2%

≥100 305,676 40% 18.3% $186 81.3% $1,763 ˂0.2%

Overall 761,342 100% 45.5% $1,094 54.1% $1,751 ˂0.4%

Size Matters

The QPP favors: Primary care more than specialists Large groups more than small groups

1996BRA, HIPAA

OrthoIndex™ 14 OrthoIndex™ 14

Collaboration Can Be Achieved Through a Spectrum of Options

Degree of Alignment Independent Full Integration

Low

High

System Resources

Required

Physician Employment

Joint Venture

Under Arrangement

Voluntary Medical Staff

Access to Resources & Capital Investment

Directorships

Gainsharing Paying for Call

Co-marketing

Relocation Support/Income Guarantee

Physician Ownership

Bundled Payment

ACO/Shared Savings

IPA

Co-management PHO

1996BRA, HIPAA

OrthoIndex™ 15 OrthoIndex™ 15

The Past 10 Years

0%

10%

20%

30%

40%

50%

2004 2006 2008 2010 2012 2014

PP - SoloPP - GroupPP - MSGAcademic - SalaryHospital Employed

Orthopedic Practice Settings Are Changing Again

PP = private practice; MSG = multispecialty group. Source: AAOS Orthopaedic Practice in the U.S., January 2015.

_______________

~ 90% of Respondents

1996BRA, HIPAA

OrthoIndex™ 16 OrthoIndex™ 16

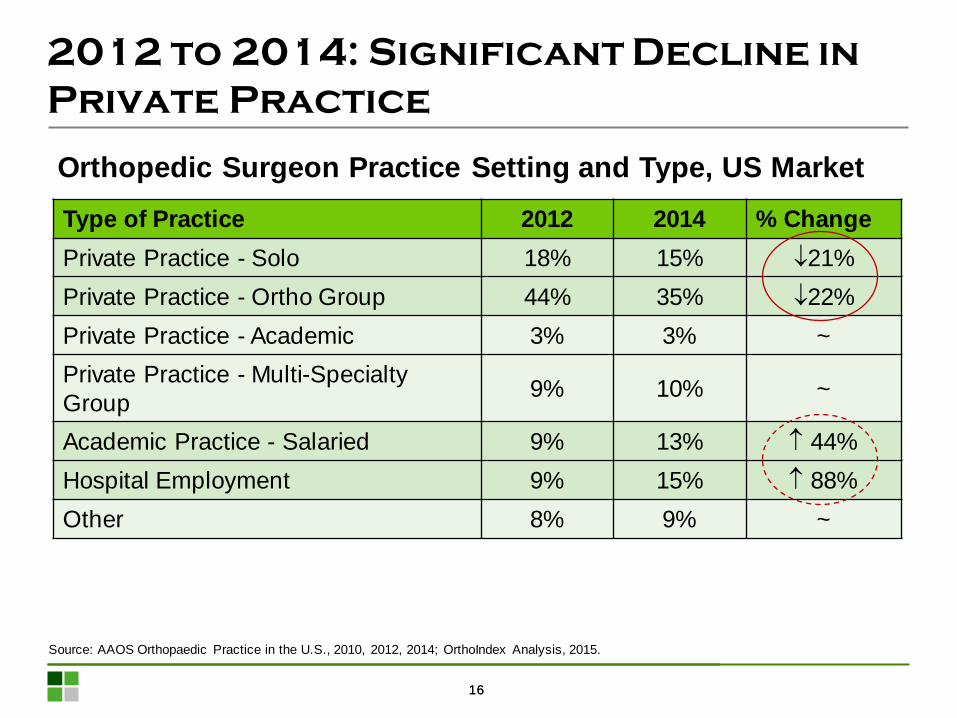

2012 to 2014: Significant Decline in Private Practice

Orthopedic Surgeon Practice Setting and Type, US Market Type of Practice 2012 2014 % Change Private Practice - Solo 18% 15% ↓21% Private Practice - Ortho Group 44% 35% ↓22% Private Practice - Academic 3% 3% ~ Private Practice - Multi-Specialty Group 9% 10% ~

Academic Practice - Salaried 9% 13% ↑ 44% Hospital Employment 9% 15% ↑ 88% Other 8% 9% ~

Source: AAOS Orthopaedic Practice in the U.S., 2010, 2012, 2014; OrthoIndex Analysis, 2015.

1996BRA, HIPAA

OrthoIndex™ 17 OrthoIndex™ 17

0%10%20%30%40%50%60%70%80%90%

100%

2004 2006 2008 2010 2012 2014 2016 2018

AIMMC AHC National

What is the Future of the Private Practice Workforce?

PP = private practice. Source: AAOS Orthopaedic Practice in the U.S., January 2015; OrthoIndex Analysis, 2015.

?

Single Specialty Orthopedic Private Practice, US Market

1996BRA, HIPAA

OrthoIndex™ 18 OrthoIndex™ 18

Preparing For Our New Customer

B2B Providers sell their services to the government, insurers and

employers who make decisions on behalf of

individuals and their families “wholesale”

B2C Providers sell their services

to consumers who make decisions on benefits,

providers and course of care

“retail”

Other Peoples Money

Your Money

B2B = business to business; B2C = business to consumer.

1996BRA, HIPAA

OrthoIndex™ 19 OrthoIndex™ 19

“The Patient Will See You Now”

Patients most frequently request pricing for obstetric services, imaging and outpatient surgery.

Insurance card

Procedure type

Treatment location

Verbal or written estimate within 2 business days

Consumer Driven Health Care

1996BRA, HIPAA

OrthoIndex™ 20 OrthoIndex™ 20

Our Market is Undergoing Transformational Change

Providers

Source: OrthoIndex Analysis, 2015.

Patient And Healthcare Asset Managers

1996BRA, HIPAA

OrthoIndex™ 21 OrthoIndex™ 21

Higher education, banking, healthcare …

The New “Cost Of Doing Business”

1996BRA, HIPAA

OrthoIndex™ 22 OrthoIndex™ 22

1996BRA, HIPAA

OrthoIndex™

Chicago, Illinois

OrthoIndex™

Chicago, Illinois

Thank You

John Cherf MD, MPH, MBA M: 312.339.4925 [email protected] 321 North Clark Street, Suite 1301 Chicago, Illinois 60654