Embed Size (px)

Citation preview

Challenges in the Governance of Extractive Industries in theExtractive Industries in the

Philippines

Elisea “Bebet” G. GozunMay 16, 2014

Philippines –Rich in Mineral Resources

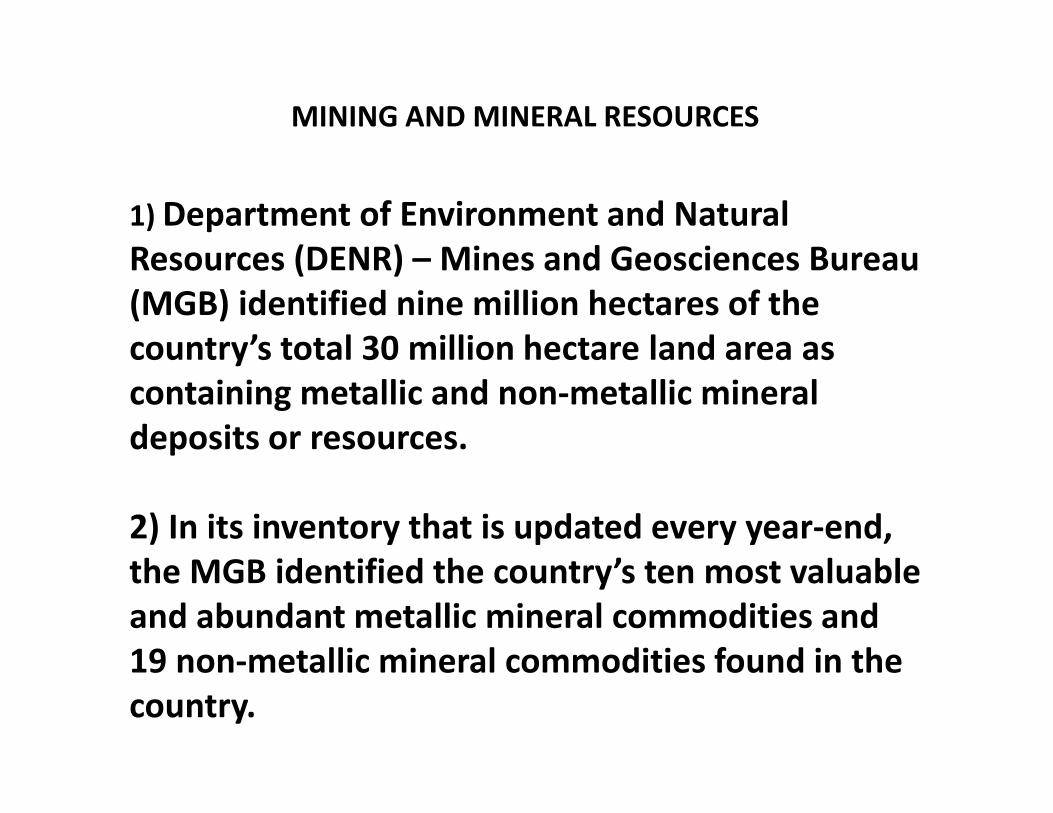

MINING AND MINERAL RESOURCES

1) Department of Environment and Natural Resources (DENR) Mines and Geosciences BureauResources (DENR) – Mines and Geosciences Bureau (MGB) identified nine million hectares of the country’s total 30 million hectare land area ascountry s total 30 million hectare land area as containing metallic and non‐metallic mineral deposits or resources.

2) In its inventory that is updated every year‐end, h MGB id ifi d h ’ l blthe MGB identified the country’s ten most valuable and abundant metallic mineral commodities and 19 non‐metallic mineral commodities found in the19 non‐metallic mineral commodities found in the country.

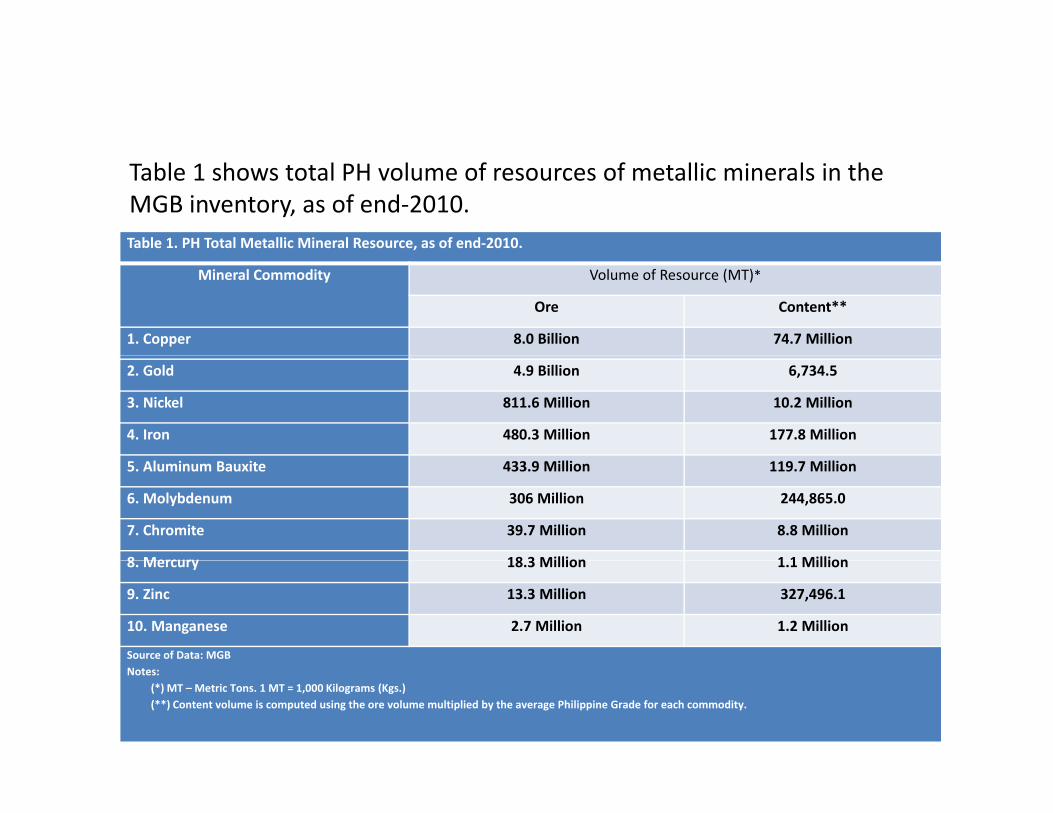

Table 1 shows total PH volume of resources of metallic minerals in the MGB inventory, as of end‐2010.Table 1. PH Total Metallic Mineral Resource, as of end‐2010.

Mineral Commodity Volume of Resource (MT)*

Ore Content**

1. Copper 8.0 Billion 74.7 Million

2. Gold 4.9 Billion 6,734.5

3. Nickel 811.6 Million 10.2 Million

4. Iron 480.3 Million 177.8 Million

5. Aluminum Bauxite 433.9 Million 119.7 Million

6. Molybdenum 306 Million 244,865.0

7. Chromite 39.7 Million 8.8 Million

8 Mercury 18 3 Million 1 1 Million8. Mercury 18.3 Million 1.1 Million

9. Zinc 13.3 Million 327,496.1

10. Manganese 2.7 Million 1.2 Million

Source of Data: MGBNotes:

(*) MT – Metric Tons. 1 MT = 1,000 Kilograms (Kgs.)(**) Content volume is computed using the ore volume multiplied by the average Philippine Grade for each commodity.

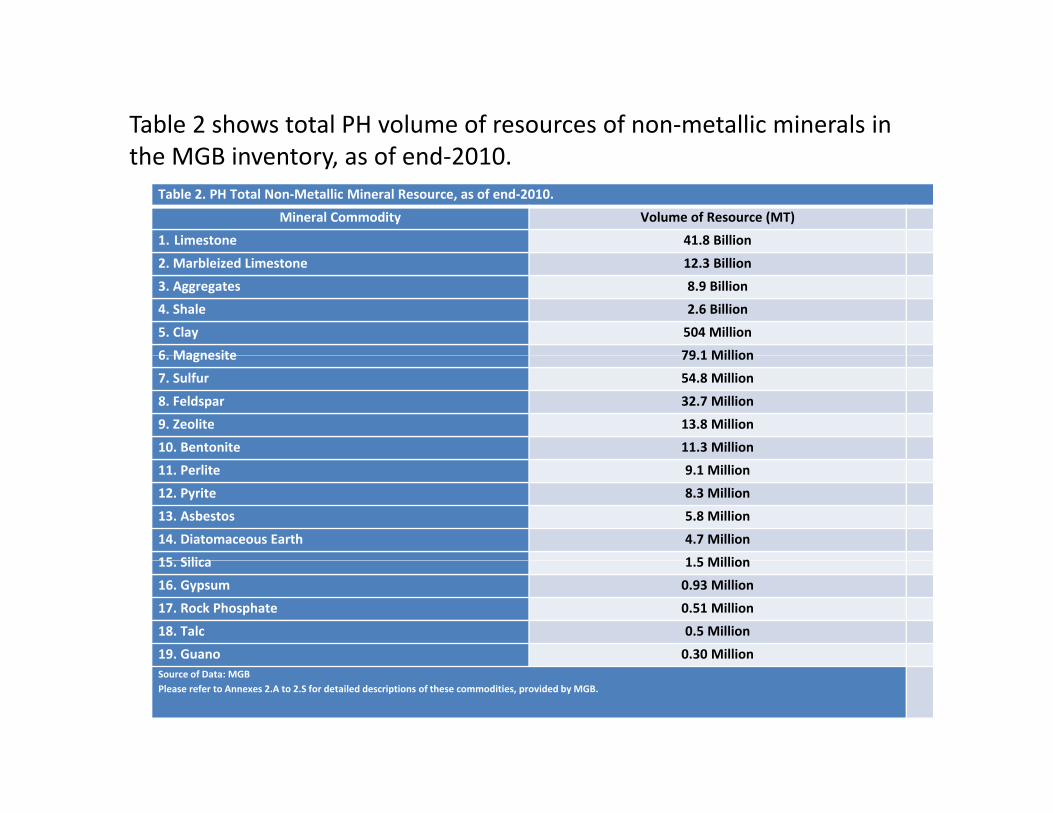

Table 2 shows total PH volume of resources of non‐metallic minerals in th MGB i t f d 2010the MGB inventory, as of end‐2010.

Table 2. PH Total Non‐Metallic Mineral Resource, as of end‐2010.

Mineral Commodity Volume of Resource (MT)

1. Limestone 41.8 Billion

2. Marbleized Limestone 12.3 Billion

3. Aggregates 8.9 Billion

4. Shale 2.6 Billion

5. Clay 504 Million

6 Magnesite 79 1 Million6. Magnesite 79.1 Million

7. Sulfur 54.8 Million

8. Feldspar 32.7 Million

9. Zeolite 13.8 Million

10. Bentonite 11.3 Million

11. Perlite 9.1 Million

12. Pyrite 8.3 Million

13. Asbestos 5.8 Million

14. Diatomaceous Earth 4.7 Million

15 Silica 1 5 Million15. Silica 1.5 Million

16. Gypsum 0.93 Million

17. Rock Phosphate 0.51 Million

18. Talc 0.5 Million

19. Guano 0.30 MillionSource of Data: MGBPlease refer to Annexes 2.A to 2.S for detailed descriptions of these commodities, provided by MGB.

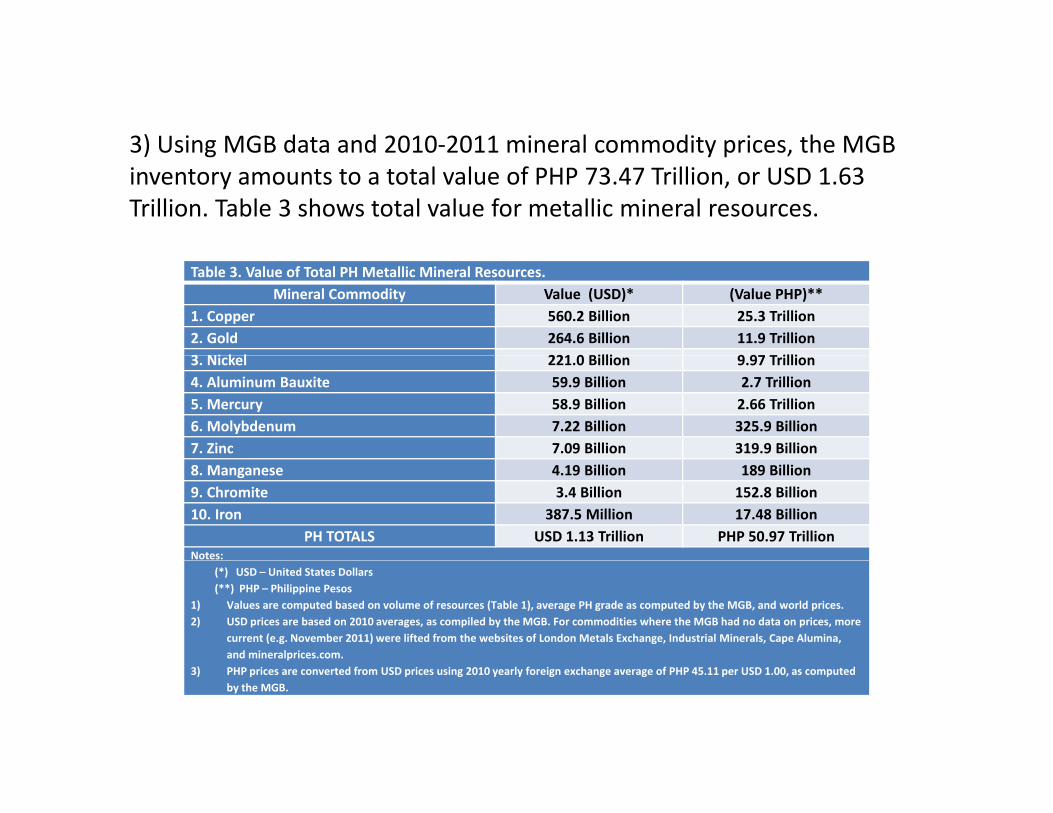

3) Using MGB data and 2010‐2011 mineral commodity prices, the MGB3) Using MGB data and 2010 2011 mineral commodity prices, the MGB inventory amounts to a total value of PHP 73.47 Trillion, or USD 1.63 Trillion. Table 3 shows total value for metallic mineral resources.

Table 3. Value of Total PH Metallic Mineral Resources. Mineral Commodity Value (USD)* (Value PHP)**

1. Copper 560.2 Billion 25.3 Trillion2. Gold 264.6 Billion 11.9 Trillion3 Ni k l 221 0 Billi 9 97 T illi3. Nickel 221.0 Billion 9.97 Trillion4. Aluminum Bauxite 59.9 Billion 2.7 Trillion5. Mercury 58.9 Billion 2.66 Trillion6. Molybdenum 7.22 Billion 325.9 Billion7. Zinc 7.09 Billion 319.9 Billion8. Manganese 4.19 Billion 189 Billion9. Chromite 3.4 Billion 152.8 Billion10. Iron 387.5 Million 17.48 Billion

PH TOTALS USD 1.13 Trillion PHP 50.97 TrillionNotes:

(*) USD – United States Dollars(**) PHP – Philippine Pesos

1) Values are computed based on volume of resources (Table 1), average PH grade as computed by the MGB, and world prices.2) USD prices are based on 2010 averages, as compiled by the MGB. For commodities where the MGB had no data on prices, more

current (e.g. November 2011) were lifted from the websites of London Metals Exchange, Industrial Minerals, Cape Alumina, and mineralprices.com.

3) PHP prices are converted from USD prices using 2010 yearly foreign exchange average of PHP 45.11 per USD 1.00, as computed by the MGB.

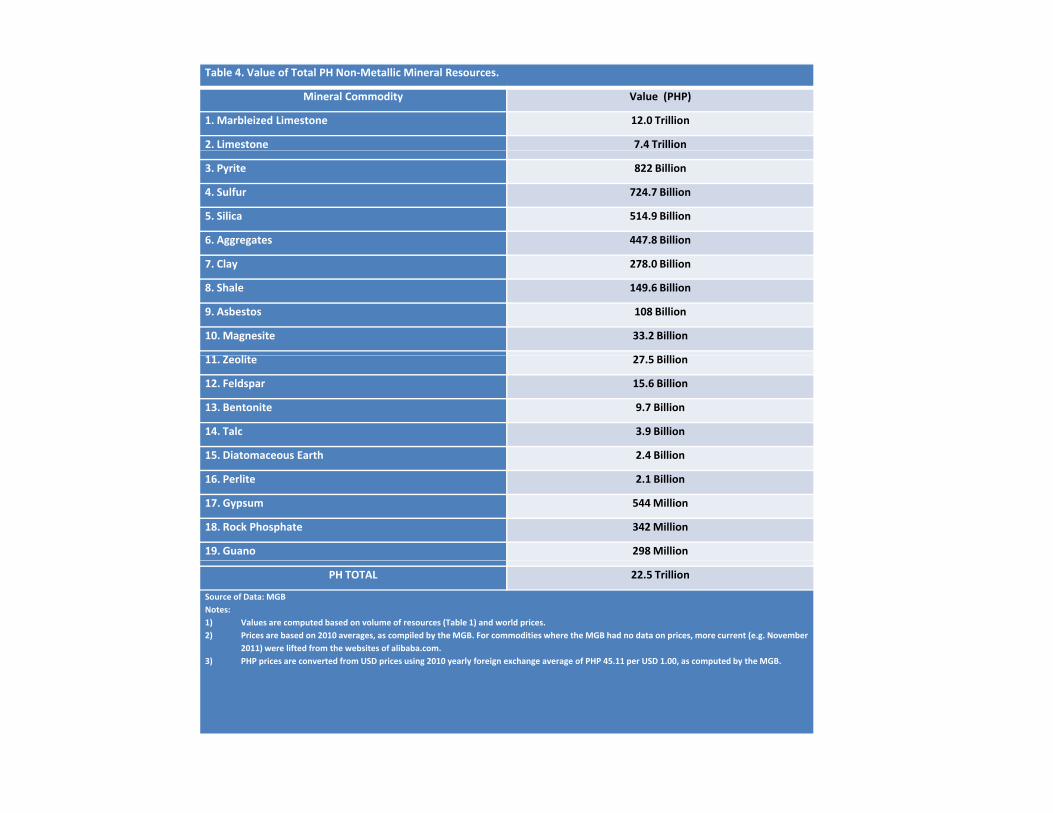

Table 4. Value of Total PH Non‐Metallic Mineral Resources.

Mineral Commodity Value (PHP)

1. Marbleized Limestone 12.0 Trillion

2. Limestone 7.4 Trillion

3. Pyrite 822 Billion

4. Sulfur 724.7 Billion

5. Silica 514.9 Billion

6. Aggregates 447.8 Billion

7. Clay 278.0 Billion

8. Shale 149.6 Billion

9. Asbestos 108 Billion

10. Magnesite 33.2 Billion

li illi11. Zeolite 27.5 Billion

12. Feldspar 15.6 Billion

13. Bentonite 9.7 Billion

14. Talc 3.9 Billion

15. Diatomaceous Earth 2.4 Billion15. Diatomaceous Earth 2.4 Billion

16. Perlite 2.1 Billion

17. Gypsum 544 Million

18. Rock Phosphate 342 Million

19. Guano 298 Million

PH TOTAL 22.5 Trillion

Source of Data: MGBNotes: 1) Values are computed based on volume of resources (Table 1) and world prices.2) Prices are based on 2010 averages, as compiled by the MGB. For commodities where the MGB had no data on prices, more current (e.g. November

2011) were lifted from the websites of alibaba.com.3) PHP prices are converted from USD prices using 2010 yearly foreign exchange average of PHP 45.11 per USD 1.00, as computed by the MGB.3) PHP prices are converted from USD prices using 2010 yearly foreign exchange average of PHP 45.11 per USD 1.00, as computed by the MGB.

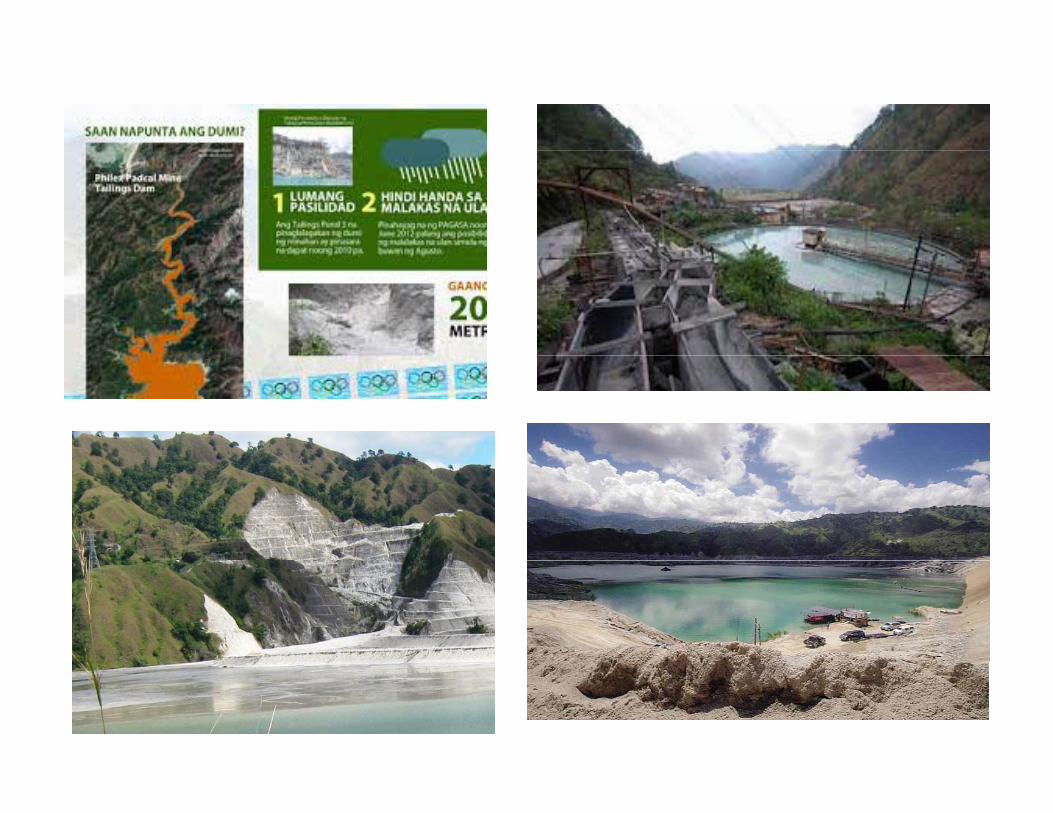

In terms of geographic areas, metallic and non‐metallicminerals can be found in all regions in the country This canminerals can be found in all regions in the country. This canbe best illustrated by the number of mining explorationpermits and permit applications that practically cover theentire country, and over thirty operating large‐scale mines,all of which are regulated and monitored by the DENRthrough the MGB and its other bureaus.g

In addition to this are the numerous small‐scale miningareas operations and quarrying concessions permitted byareas, operations, and quarrying concessions permitted byalmost all local governments throughout the country.

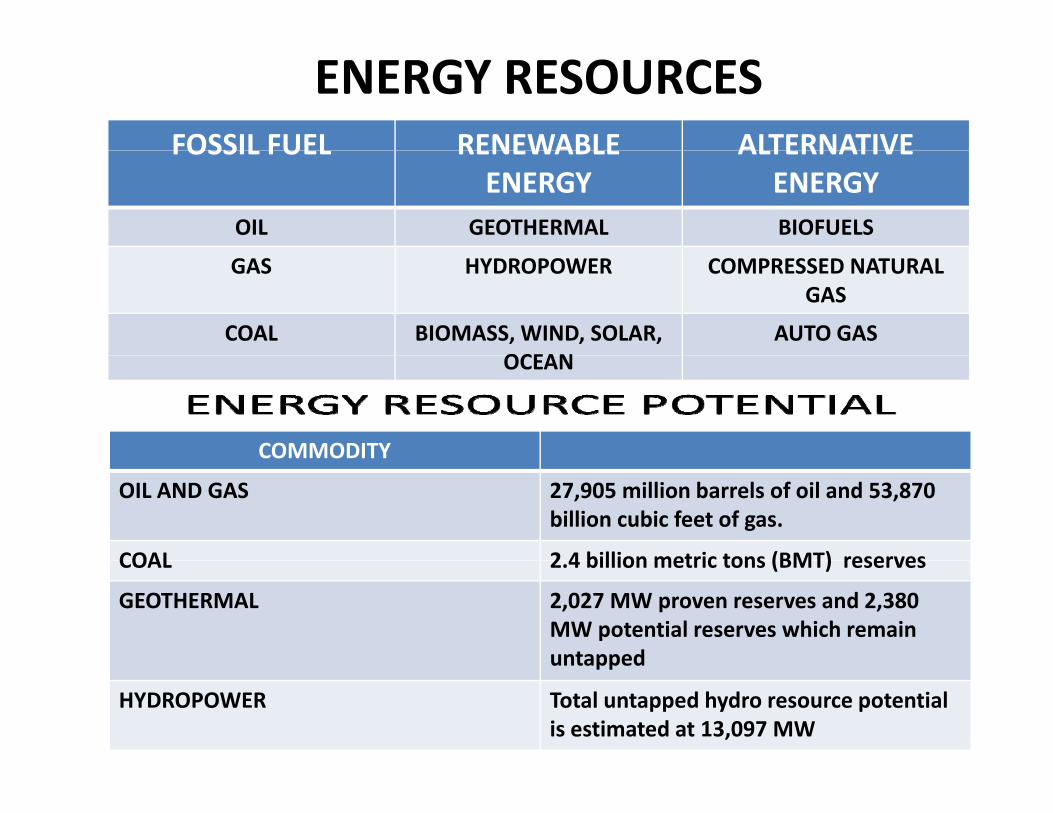

ENERGY RESOURCESFOSSIL FUEL RENEWABLE ALTERNATIVEFOSSIL FUEL RENEWABLE

ENERGYALTERNATIVE

ENERGYOIL GEOTHERMAL BIOFUELS

GAS HYDROPOWER COMPRESSED NATURAL GAS

COAL BIOMASS, WIND, SOLAR, OCEAN

AUTO GASOCEAN

COMMODITYCOMMODITY

OIL AND GAS 27,905 million barrels of oil and 53,870 billion cubic feet of gas.

COAL 2 4 billion metric tons (BMT) reservesCOAL 2.4 billion metric tons (BMT) reserves

GEOTHERMAL 2,027 MW proven reserves and 2,380 MW potential reserves which remain untappeduntapped

HYDROPOWER Total untapped hydro resource potential is estimated at 13,097 MW

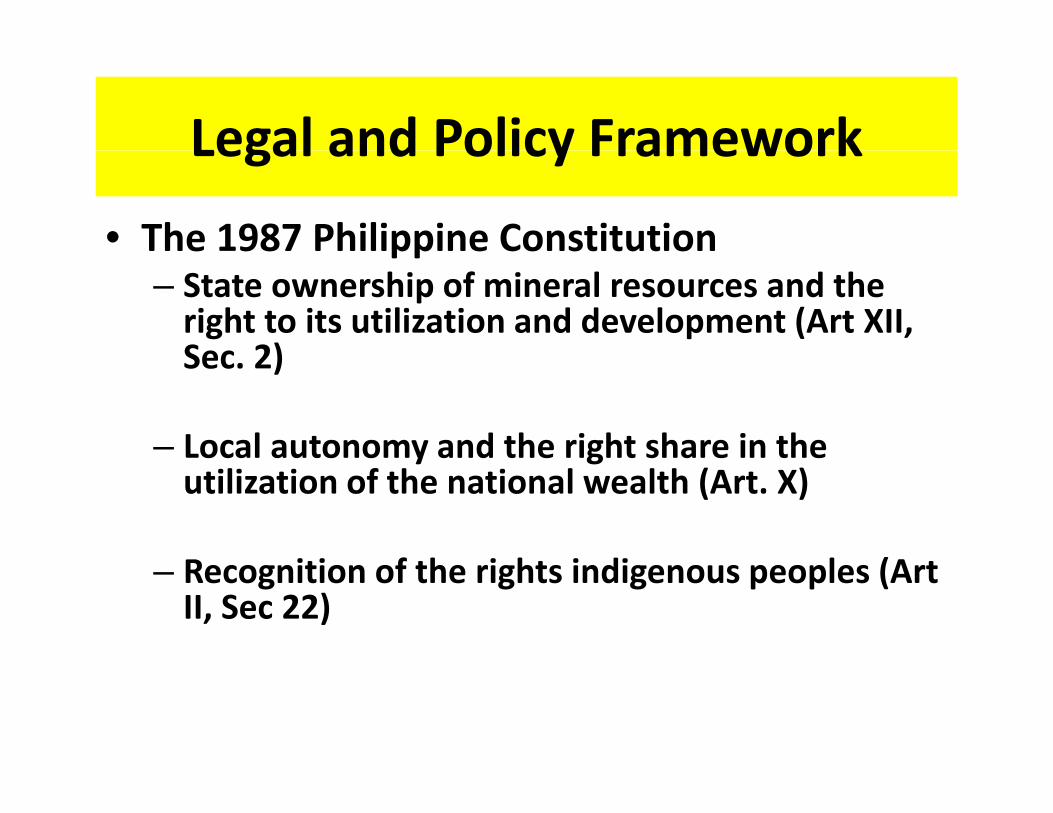

Legal and Policy FrameworkLegal and Policy Framework

• The 1987 Philippine Constitutionpp– State ownership of mineral resources and the right to its utilization and development (Art XII, Sec 2)Sec. 2)

– Local autonomy and the right share in the oca auto o y a d t e g t s a e t eutilization of the national wealth (Art. X)

R i i f h i h i di l (A– Recognition of the rights indigenous peoples (Art II, Sec 22)

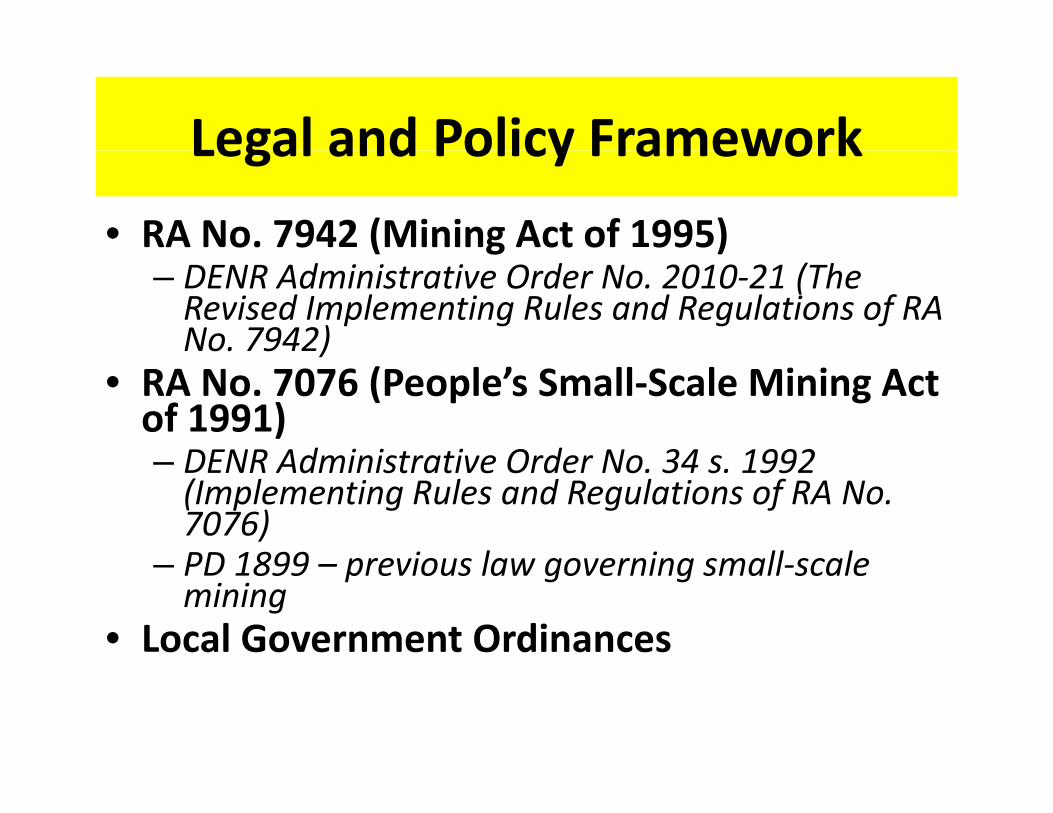

Legal and Policy FrameworkLegal and Policy Framework • RA No. 7942 (Mining Act of 1995)( g )

– DENR Administrative Order No. 2010‐21 (The Revised Implementing Rules and Regulations of RA No. 7942))

• RA No. 7076 (People’s Small‐Scale Mining Act of 1991)

DENR Administrative Order No 34 s 1992– DENR Administrative Order No. 34 s. 1992 (Implementing Rules and Regulations of RA No. 7076)PD 1899 previous law governing small scale– PD 1899 – previous law governing small‐scale mining

• Local Government Ordinances

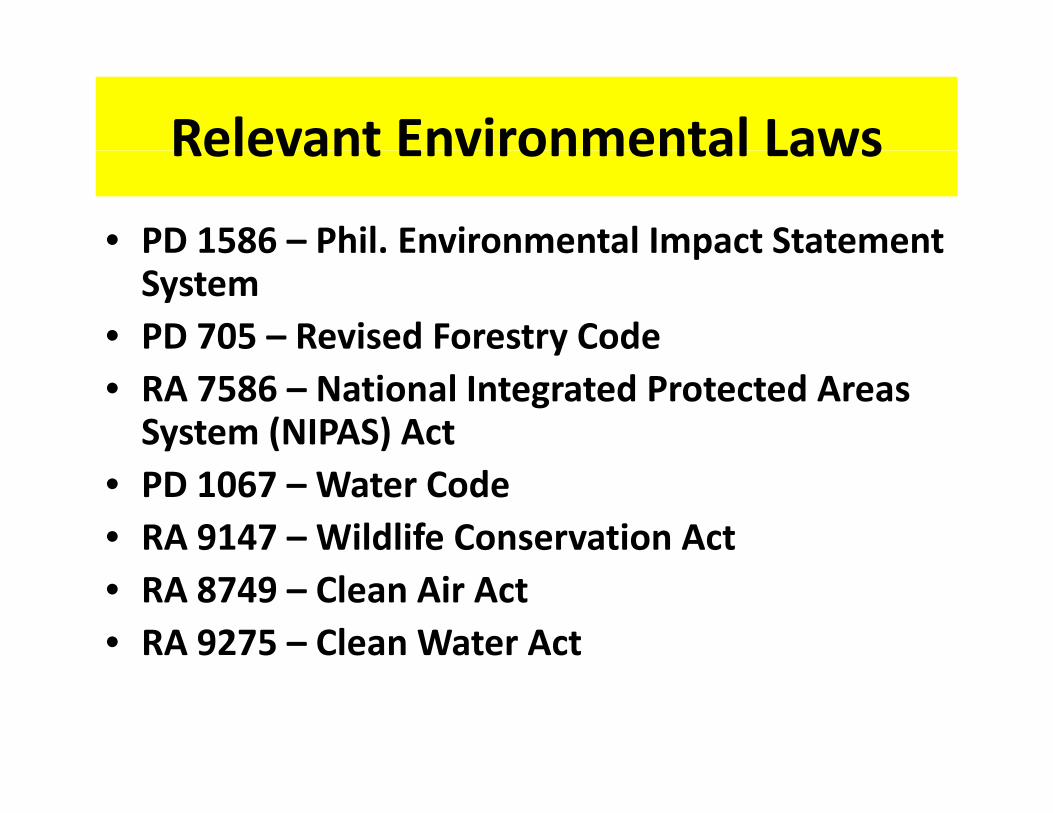

Relevant Environmental LawsRelevant Environmental Laws

• PD 1586 – Phil. Environmental Impact Statement 586 . o e ta pact State e tSystem

• PD 705 – Revised Forestry Code y• RA 7586 – National Integrated Protected Areas System (NIPAS) Act

• PD 1067 – Water Code• RA 9147 – Wildlife Conservation Act • RA 8749 – Clean Air Act • RA 9275 – Clean Water Act

Mining Industry StakeholdersMining Industry Stakeholders

• Stakeholders includeStakeholders include1. The government regulators2 The private sector/mining industry2. The private sector/mining industry 3. Civil society and non‐government

organizations/ The Catholic Churchorganizations/ The Catholic Church 4. Indigenous Peoples5 Local Government Units5. Local Government Units

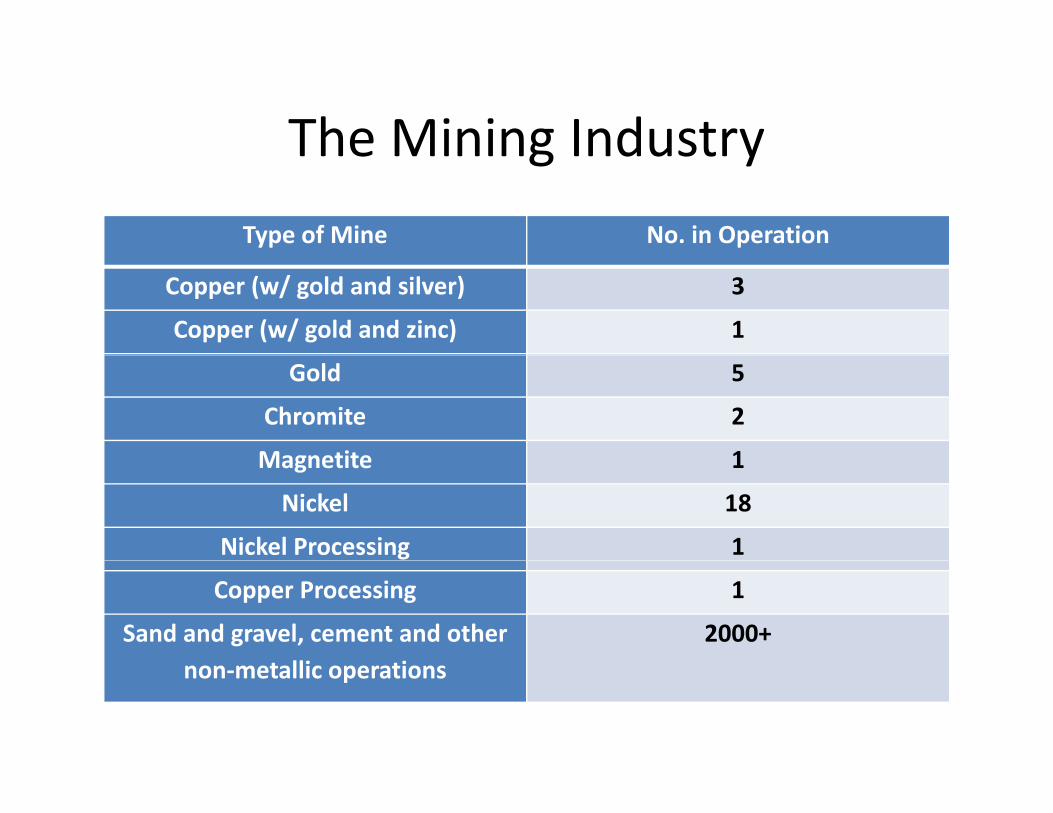

The Mining IndustryThe Mining Industry Type of Mine No. in Operation

Copper (w/ gold and silver) 3

Copper (w/ gold and zinc) 1

Gold 5

Chromite 2

Magnetite 1Magnetite 1

Nickel 18

Nickel Processing 1

Copper Processing 1

Sand and gravel, cement and other t lli ti

2000+non‐metallic operations

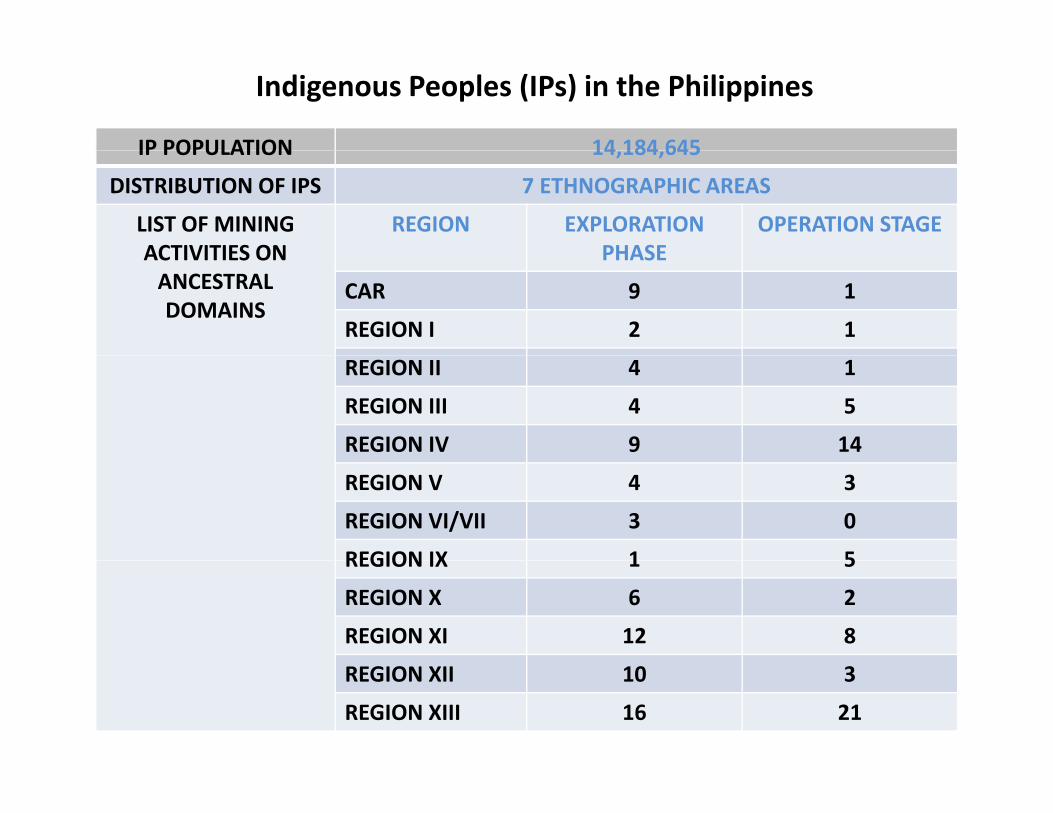

Indigenous Peoples (IPs) in the Philippines

IP POPULATION 14 184 645IP POPULATION 14,184,645

DISTRIBUTION OF IPS 7 ETHNOGRAPHIC AREAS

LIST OF MINING ACTIVITIES ON

REGION EXPLORATIONPHASE

OPERATION STAGEACTIVITIES ON ANCESTRAL DOMAINS

PHASE

CAR 9 1

REGION I 2 1

REGION II 4 1

REGION III 4 5

REGION IV 9 14

REGION V 4 3

REGION VI/VII 3 0

REGION IX 1 5REGION IX 1 5

REGION X 6 2

REGION XI 12 8

REGION XII 10 3

REGION XIII 16 21

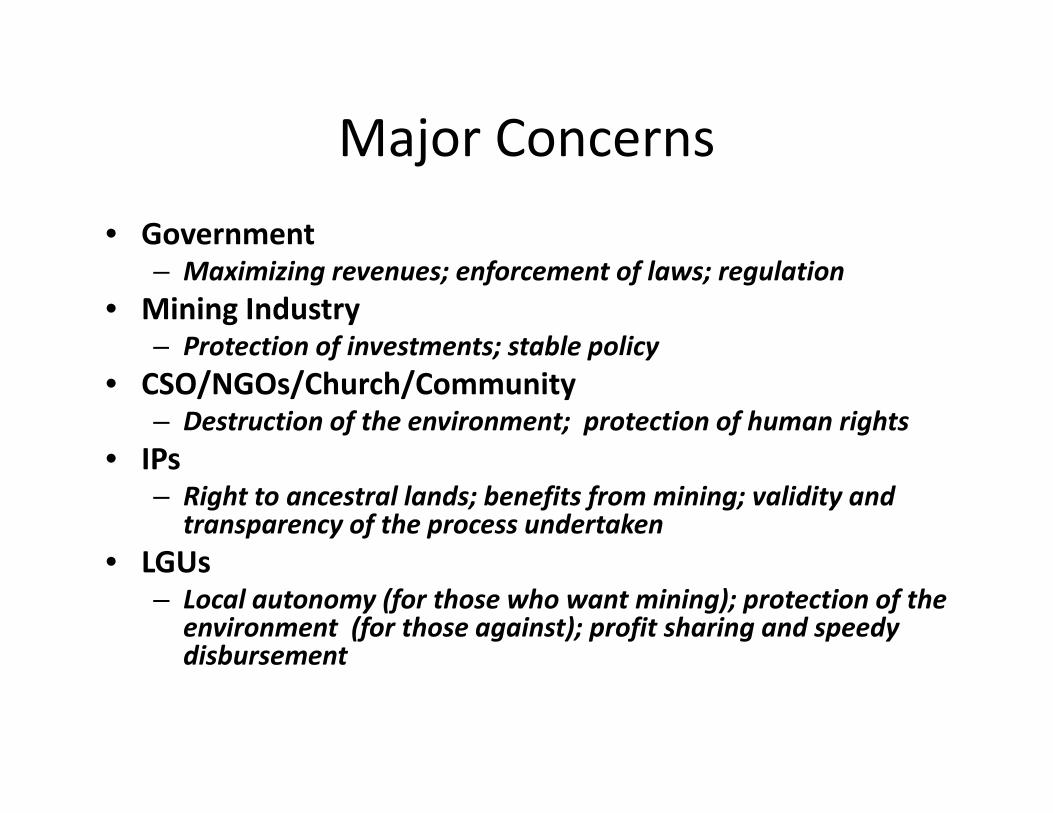

Major ConcernsMajor Concerns • Government

– Maximizing revenues; enforcement of laws; regulation • Mining Industry

– Protection of investments; stable policy otect o of est e ts; stab e po cy• CSO/NGOs/Church/Community

– Destruction of the environment; protection of human rights• IPs• IPs

– Right to ancestral lands; benefits from mining; validity and transparency of the process undertaken

• LGUs• LGUs– Local autonomy (for those who want mining); protection of the

environment (for those against); profit sharing and speedy disbursementdisbursement

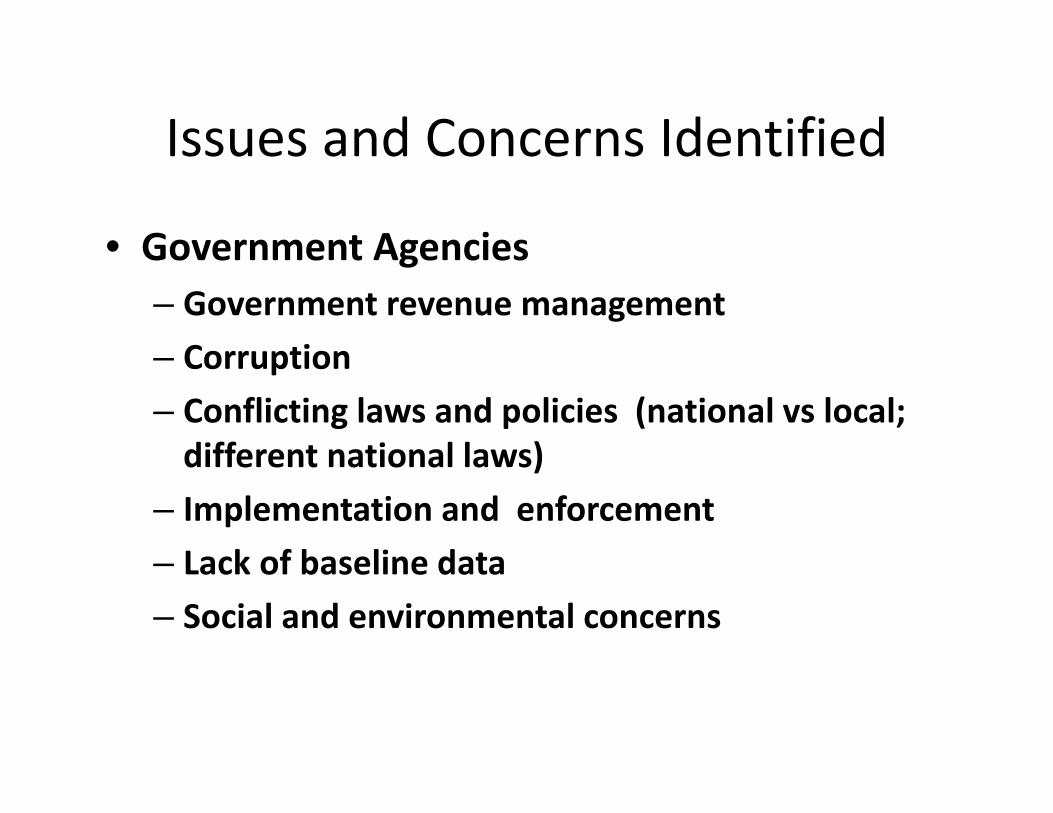

Issues and Concerns IdentifiedIssues and Concerns Identified

• Government AgenciesGovernment Agencies – Government revenue management Corruption– Corruption

– Conflicting laws and policies (national vs local; different national laws)different national laws)

– Implementation and enforcementLack of baseline data– Lack of baseline data

– Social and environmental concerns

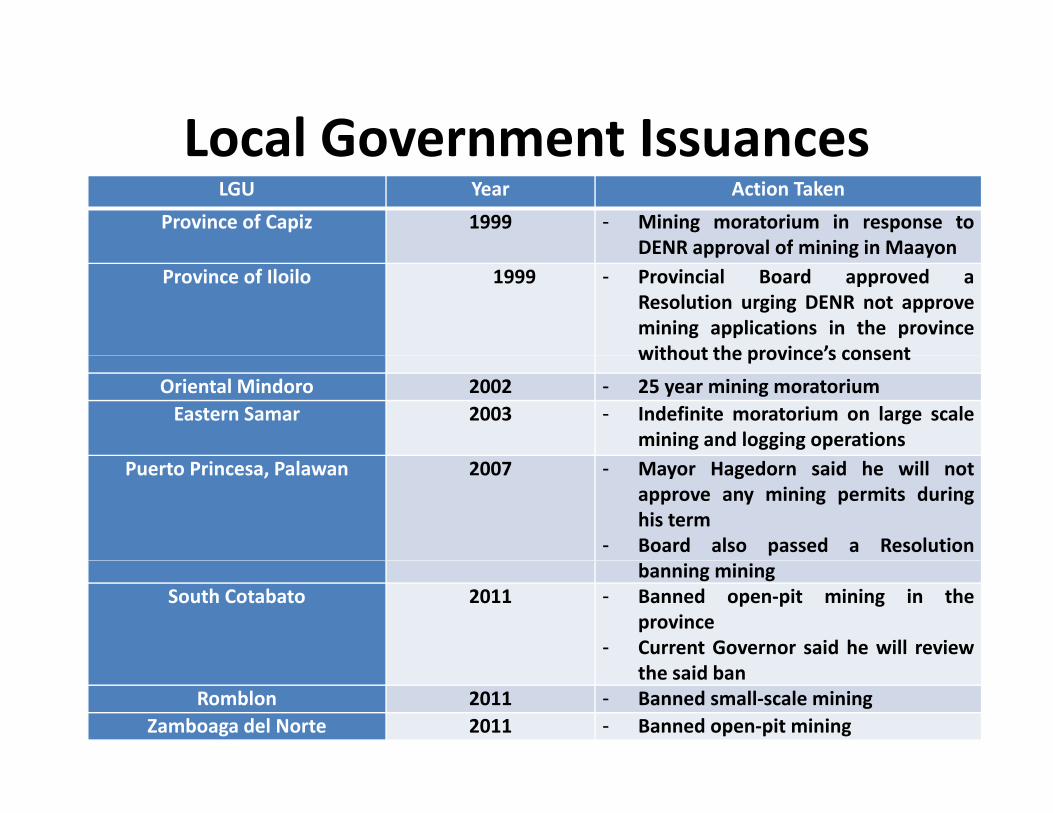

Local Government IssuancesLocal Government IssuancesLGU Year Action Taken

Province of Capiz 1999 - Mining moratorium in response toDENR approval of mining in MaayonDENR approval of mining in Maayon

Province of Iloilo 1999 - Provincial Board approved aResolution urging DENR not approvemining applications in the provincewithout the province’s consentwithout the province s consent

Oriental Mindoro 2002 - 25 year mining moratoriumEastern Samar 2003 - Indefinite moratorium on large scale

mining and logging operationsPuerto Princesa, Palawan 2007 - Mayor Hagedorn said he will not

approve any mining permits duringhis term

- Board also passed a Resolutionbanning mining

South Cotabato 2011 - Banned open‐pit mining in theprovince

- Current Governor said he will reviewthe said ban

Romblon 2011 - Banned small‐scale miningZamboaga del Norte 2011 - Banned open‐pit mining

Issues and Concerns IdentifiedIssues and Concerns Identified

• Mining IndustryMining Industry – Conflicting laws and policies Security of physical investments– Security of physical investments

– Enforcement and implementation of laws S i l d i t l– Social and environmental concerns

– Disunity within the industry S i f b i i– Security of business interests

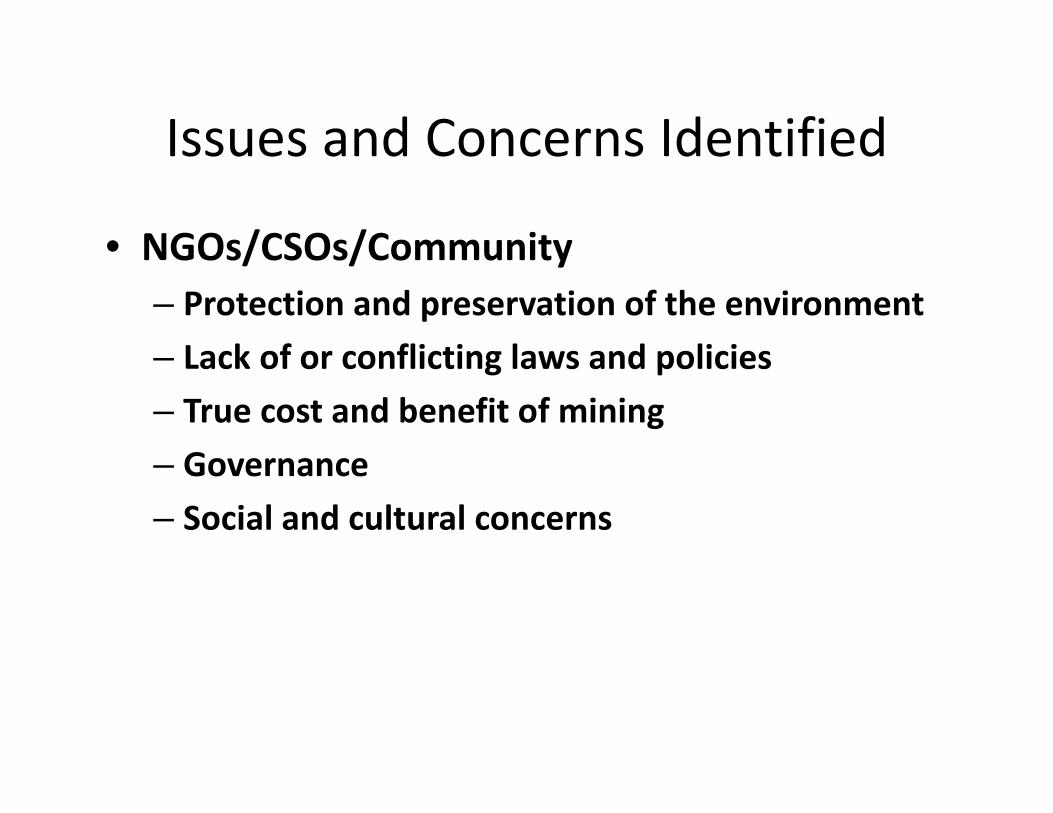

Issues and Concerns IdentifiedIssues and Concerns Identified

• NGOs/CSOs/CommunityNGOs/CSOs/Community – Protection and preservation of the environment Lack of or conflicting laws and policies– Lack of or conflicting laws and policies

– True cost and benefit of mining G– Governance

– Social and cultural concerns

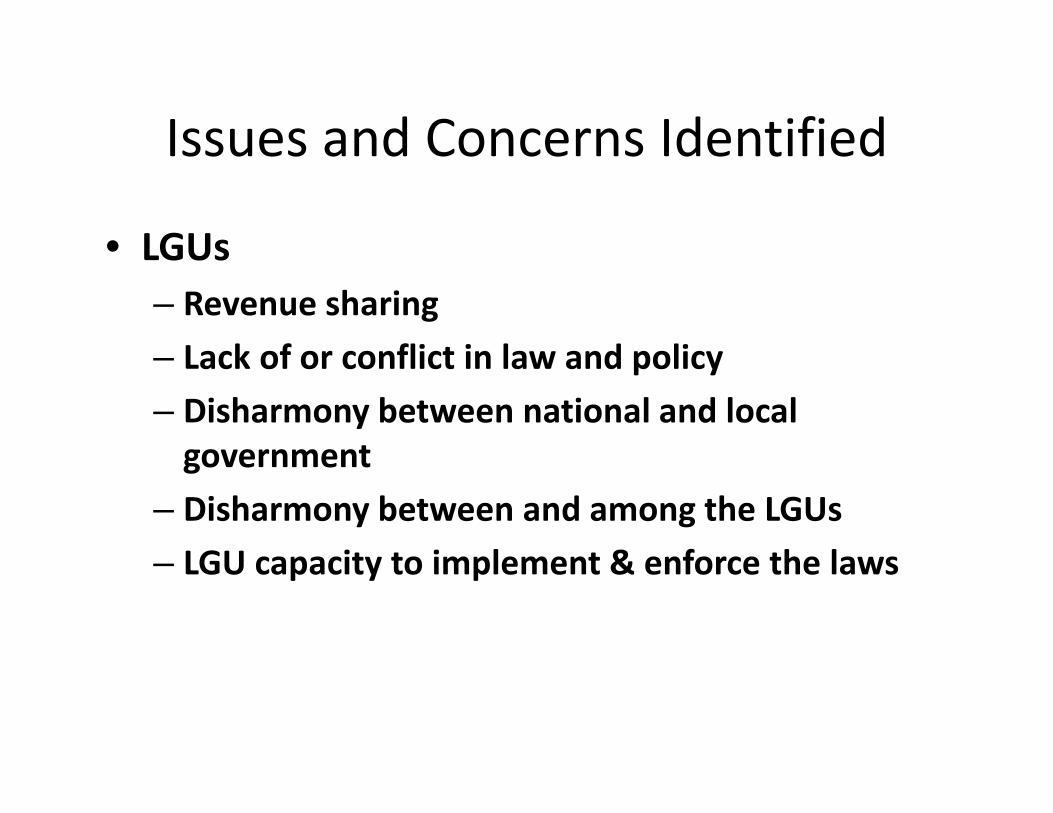

Issues and Concerns IdentifiedIssues and Concerns Identified

• LGUsLGUs– Revenue sharing Lack of or conflict in law and policy– Lack of or conflict in law and policy

– Disharmony between national and local governmentgovernment

– Disharmony between and among the LGUsLGU capacity to implement & enforce the laws– LGU capacity to implement & enforce the laws

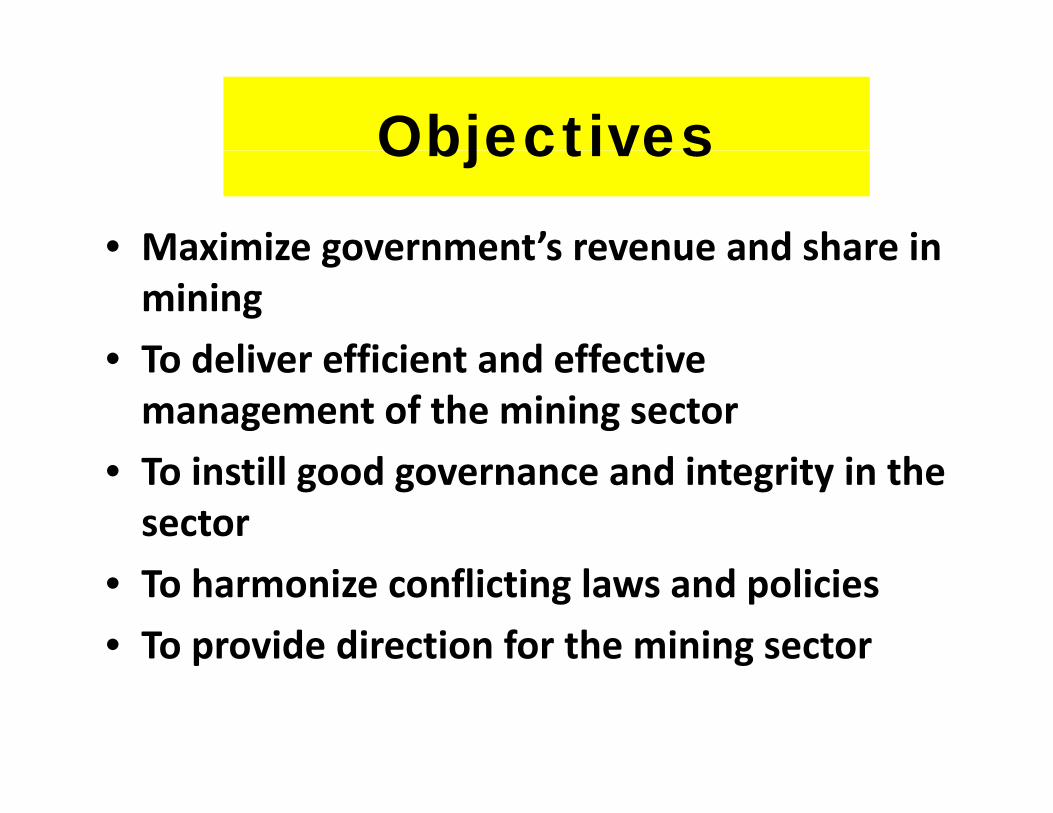

Objectives Objectives

• Maximize government’s revenue and share inMaximize government s revenue and share in mining

• To deliver efficient and effective• To deliver efficient and effective management of the mining sector T i ill d d i i i h• To instill good governance and integrity in the sector

• To harmonize conflicting laws and policies • To provide direction for the mining sector p g

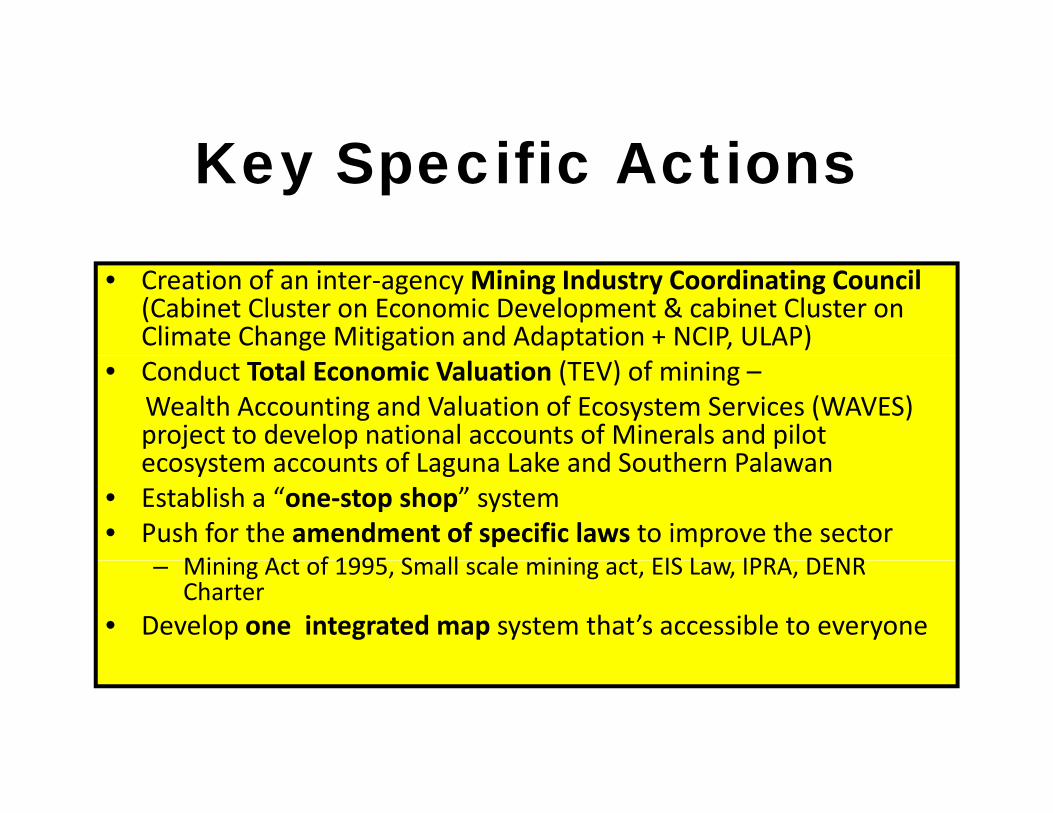

K S ifi A ti Key Specific Actions

• Creation of an inter‐agency Mining Industry Coordinating Council (Cabinet Cluster on Economic Development & cabinet Cluster on Climate Change Mitigation and Adaptation + NCIP, ULAP)

• Conduct Total Economic Valuation (TEV) of mining –Wealth Accounting and Valuation of Ecosystem Services (WAVES) project to develop national accounts of Minerals and pilot ecos stem acco nts of Lag na Lake and So thern Pala anecosystem accounts of Laguna Lake and Southern Palawan

• Establish a “one‐stop shop” system• Push for the amendment of specific laws to improve the sector

Mi i A t f 1995 S ll l i i t EIS L IPRA DENR– Mining Act of 1995, Small scale mining act, EIS Law, IPRA, DENR Charter

• Develop one integrated map system that’s accessible to everyone

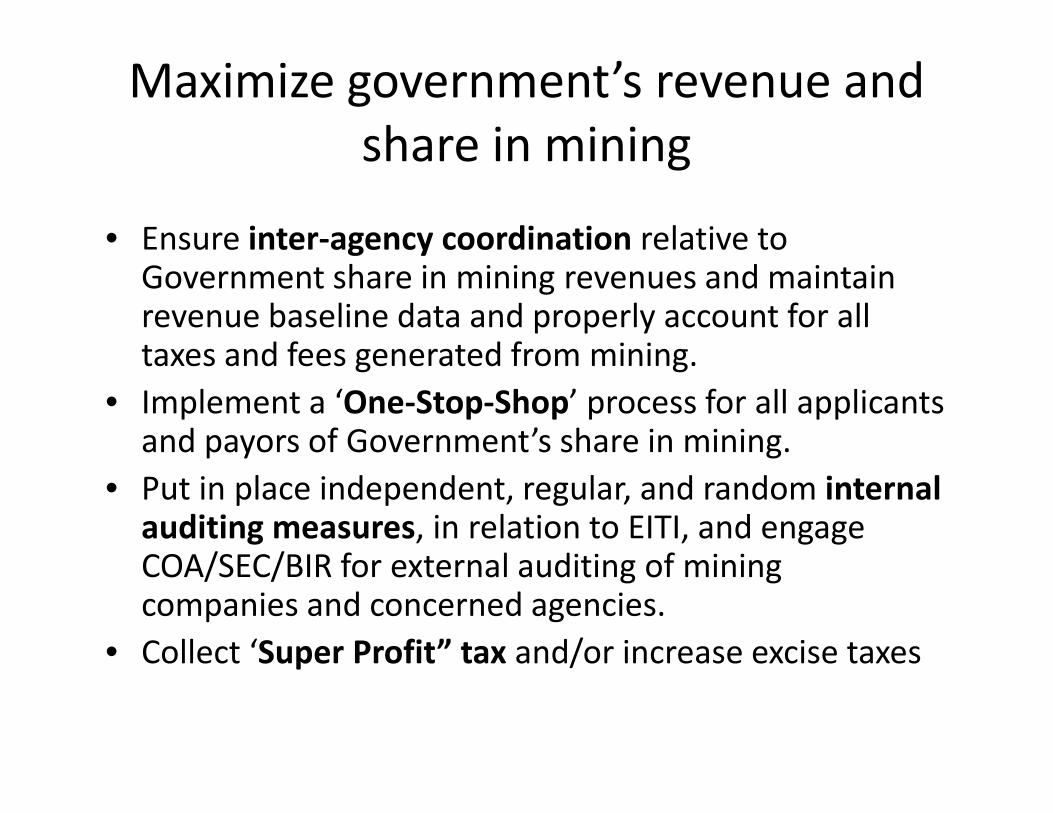

Maximize government’s revenue and share in miningshare in mining

• Ensure inter‐agency coordination relative to g yGovernment share in mining revenues and maintain revenue baseline data and properly account for all taxes and fees generated from miningtaxes and fees generated from mining.

• Implement a ‘One‐Stop‐Shop’ process for all applicants and payors of Government’s share in mining.p y g

• Put in place independent, regular, and random internal auditing measures, in relation to EITI, and engage COA/SEC/BIR for external auditing of miningCOA/SEC/BIR for external auditing of mining companies and concerned agencies.

• Collect ‘Super Profit” tax and/or increase excise taxesCollect Super Profit tax and/or increase excise taxes

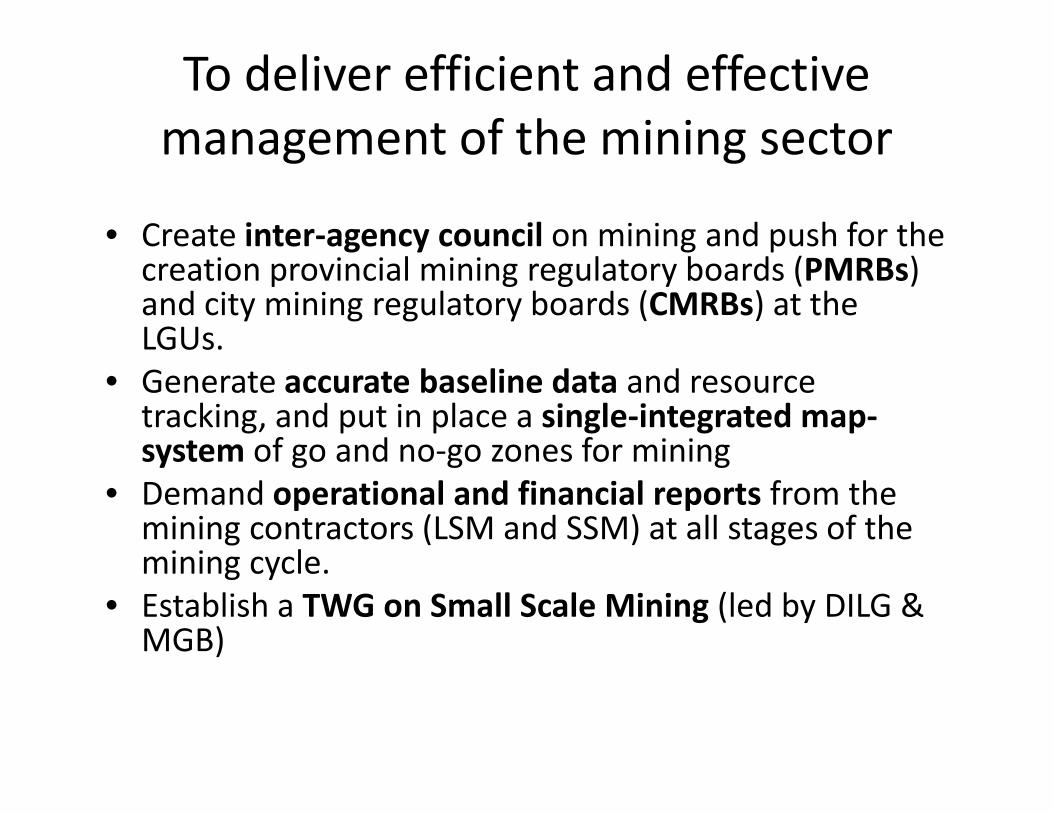

To deliver efficient and effective management of the mining sectormanagement of the mining sector

• Create inter‐agency council on mining and push for the creation provincial mining regulatory boards (PMRBs) and city mining regulatory boards (CMRBs) at the LGUs.

• Generate accurate baseline data and resource tracking, and put in place a single‐integrated map‐system of go and no‐go zones for miningsystem of go and no go zones for mining

• Demand operational and financial reports from the mining contractors (LSM and SSM) at all stages of the mining cyclemining cycle.

• Establish a TWG on Small Scale Mining (led by DILG & MGB)

To instill good governance and integrity in the sectorintegrity in the sector

• Ensure inter‐agency coordination towardsEnsure inter agency coordination towards good governance and integrity in the mining sector adopt the EITI (Extractive Industriessector, adopt the EITI (Extractive Industries Transparency Initiatives), and support the President’s call for reformsPresident s call for reforms.

• EITI ‐ TWG to operate under the MICC and the Cabinet Cluster on Good Governancethe Cabinet Cluster on Good Governance (Chaired by the President)

To harmonize conflicting laws and li ipolicies

• Ensure inter‐agency coordination towards the harmonization of conflicting laws and policies. Push for the amendment of laws such as RA 7942 and RA 7076 to remove gaps and conflict. g p

• Harmonize and resolve conflicts between IPRA and the mining law

• Harmonize mining with environmental laws by clearly• Harmonize mining with environmental laws by clearly identifying standards and criteria for responsible mining, allowable and no‐go areas, and evidence and data based decision to allow or not to allow mining indata‐based decision to allow or not to allow mining in certain areas

• Develop primers/manuals for a common d di f i i l d (l i )understanding of mining related terms (laymanize)

To provide direction for the mining sector EO 79 July 2012sector ‐ EO 79, July 2012

• Arrive at Government’s own unbiased, objective opinion of the effects of mining on the environment, society, and the economy through a Total Economicon the environment, society, and the economy through a Total Economic Valuation (TEV)/natural resource accounting ‐Wealth Accounting and Valuation of Ecosystem Services (WAVES) project with WB

• Created a Technical Working Group (TWG) on Mining and the Environment to develop and enforce strict guidelines on environmental safety, including:– Developed an integrated map for the country and determine “go” and “no‐

go” zones for mining based on areas reserved by law and executive issuances i i k l d i li h f ll i i– Requiring workplans and monitor accomplishments from all mining

contractors (large scale and small scale). This includes mine rehabilitation, post operation development, EPEPs, etc. Multi‐stakeholder bodies should be assembled to monitor compliance to these workplans. Non‐compliance p p pshould result to penalties and even termination of mining permits. Require the establishment of heritage funds by the mining contractors.

– Explore the possibility of requiring perpetual liability (study policies of other countries).

To provide direction for the mining tsector

• Create a TWG on Mining and Social Concerns to develop and enforce strict guidelines on social safety, including:– Conduct cultural mapping to identify Indigenous Peoples pp g y g p(IP) areas and address IP concerns relative to mining. (one map system)

– Conduct heritage/cultural sites mapping to identify g / pp g yheritage sites and areas and address heritage concerns relative to mining. (one map system)

– Conduct conflict mapping to identify conflict areas and address peace and order concerns relative to mining. Study the possibility of the Council and/or the TWG to sit in security cluster meetings.

To provide direction for the i i tmining sector

• Created a TWG on Economic Concerns to develop and enforce strict guidelines, including:– Reviewed the existing fiscal regime for mining and g g gpropose a new bill to be submitted to Congress;

– Prepare a road map for more value adding and the p p gdevelopment of downstream industries (copper, nickel, gold….)

– Complete the cleansing of mining permit applications before processing new ones (cleansing process should be clear and transparent)

Thank YouThank You