Embed Size (px)

Citation preview

Challenges and Opportunities in Capital

Markets for Commercial Real Estate

ULI - Turkey

Istanbul, Turkey

June 22, 2015

Professor Tony Ciochetti

Elmo Burke Jr. Chair of Finance

Chairman, University of Texas, San Antonio

Program in Real Estate Finance and Development

Main Points

• Market overview

• Forms of capital

• Institutional perspective - why global?

• Real estate specific issues (4)

• Take-aways

Perspective

Tokyo

Beijing

Shanghai

Hong Kong

Stockholm

London

Paris

Berlin Frankfurt

Munich

San Francisco

Los Angeles

Chicago

New York D.C.

Istanbul

Bangalore

Mumbai

Delhi Seoul

Helsinki

Boston Portland

Phoenix Miami

Denver

Lisbon Athens

Chennai

Dubai

Abu Dhabi

Shenzhen

Chongqing Seattle

Las Vegas

Kuwait

Nairobi

Monterrey

Bogota

Sydney

Where is the Money Going?

Global Capital Flows Transaction Volumes Q2-2015 - Trailing 12 mo.

Source: RCA

Top 25 Markets - 2014

Source: RCA

Global Transactions - 2014

Source: RCA

Net Change, 2014 vs. 2013

Source: RCA

Cross Border Activity

Source: RCA

Pricing?

Source: RCA

Drivers of Pricing

Source: RCA

Forms of Commercial Real Estate Capital

2014

Debt

(39%)

$3.3 trillion

Equity

(61%)

$5.1 trillion

Private

(83%)

$7.0 trillion

$2.3 trillion $4.7 trillion

Public

(17%)

$1.4 trillion

$1.0 trillion $.91 trillion

Source: Federal Reserve Flow of Funds

The Four Quadrants of

US Commercial Real Estate Markets

Debt (39%)

$3.3 trillion

Equity (61%)

$5.1 trillion

Private

(83%)

$7.0 trillion

$4.7 trillion

Public

(17%)

$1.4 trillion

Source: Federal Reserve Flow of Funds

Direct Real Estate: $4.7 Trillion

• Private investors: 60% - $2.8 trillion

– High net worth investors (HNWI)

– Tax deferred investors (1031)

– Tenants in common (TIC)

– Other private partnerships

Direct Real Estate: $4.7 Trillion

• Institutional investment: ~ 20-25% - $1.0 trillion

– Pension funds - $750 billion

– Endowments, foundations - $250 billion

Direct Real Estate: $4.7 Trillion

• Foreign investment: ~ 7-10% - $329 billion

– Australian

– German

– UK

– Middle East

– Japanese

– Dutch

– Canada

– China

Direct US Foreign Investment

Source: RCA

Direct Real Estate: $4.7 Trillion

• Other investments : 11% - $517 billion

– Life insurance companies

– Commercial banks

– Other private financial institutions

(hedge/opportunity)

The Four Quadrants of

US Commercial Real Estate Markets, 2013

Debt (39%)

$3.3 trillion

Equity (61%)

$5.1 trillion

Private

(83%)

$7.0 trillion

$2.3 trillion

Public

(17%)

$1.4 trillion

Source: Federal Reserve Flow of Funds

Commercial Mortgages: $2.3

Trillion

• Commercial banks: 57% - $1.3 trillion

• Life insurance companies: 21% - $483 billion

• Savings/Thrifts: 12% - $276 billion

• Government agencies: 10% - $230 billion

2nd Mortgage

Lien

on Property

Traditional

Mortgage Second

Mortgage Loan

Mezzanine

Finance

Preferred

Equity

‘B’ Notes

Borrower

Equity

1st

Mortgage

1st

Mortgage

Lien on

borrower

equity

Capital

contribution to

borrower equity

A

Note

Borrower

Equity

Borrower

Equity Borrower

Equity

Borrower

Equity

B Note

Credit support for

A Note

1st

Mortgage

Mezzanine Finance: $115 - $225 Billion

1st

Mortgage

The Four Quadrants of

US Commercial Real Estate Markets

Debt (39%)

$3.3 trillion

Equity (61%)

$5.1 trillion

Private

(83%)

$7.0 trillion

Public

(17%)

$1.4 trillion

$0.91 trillion

Source: Federal Reserve Flow of Funds

REITs?

Debt, equity, hybrid

– 1971 – 34 - $1.4 bn (12 E, 12 D, 10 H)

– 2006 – 183 - $438 bn (138 E, 38 D, 7 H)

– 2008 – 136 - $191 bn (113 E, 20 D, 3 H)

– 2014 – 216 - $907 bn (177 E, 39 D, 0 H)

Company must be in the real estate business

– At least 90% of TI must be distributed annually to shareholders

– At least 75 percent of assets must be real property

– At least 75 percent of GI from rents – less than 30% GI from sales

held less than 4 years

208 companies trade on the NYSE

Players – 2014?

How Have REITs Done?

26

Continued Globalization of REIT Market

The Four Quadrants of

US Commercial Real Estate Markets, 2013

Debt (39%)

$3.3 trillion

Equity (61%)

$5.1 trillion

Private

(83%)

$7.0 trillion

Public

(17%)

$1.4 trillion

$600 billion CMBS

$400 billion REIT

Debt

Source: Federal Reserve Flow of Funds

LOANS

POOL OF

LOANS

SECURITIES/

BONDS

BACKED BY

POOL

HOUSE

CAR

AIRCRAFT

EQUIPMENT

Securitized Loans: Intuition

US CMBS Issuance

CMBS Concept

Impact of Losses on Bonds

14%

12%

9%

5%

3%

2%

0%

AAA

(86%)

AA

(2%)

A

(3%)

BBB

(4%)

BB

(2%)

B

(1%)

UR

(2%)

% Subordination

Average

Loss

Experience

Worst

Cohort Loss

Experience

(1986)

Source: Morgan Stanley, Author

4.9% 8.1%

13.9%

Asset Sale

CMBS Rollover Risk

Unsecured REIT Bonds: $400 bn

• Typical form of financing for REITs

• Similar to unsecured Corporate Debt

Institutional Perspective - Why

Real Estate?

• State Teachers Retirement System of Ohio

– ~ $80 bn

– Equities - 57%

– Cash – 1%

– Fixed – 18%

– Direct RE – 10% (9%) - ~ 55% core, 35% va, 7-10% opp :

$8bn RE

– Alt – 14% (PE/Opptnistic/Funds) : RE $575 mm funds

Attraction of Commercial Real Estate

Source: RCA

Rebound in US Commercial RE Prices

Source: RCA

‘Style’ Metrics for Real Estate Core Core Plus Value Added Opportunistic

General Strategies Equity Investments

in existing assets

with minimal lease-

up or redevelopment

and longer holding

periods.

Equity assets with

mainly "core"

properties taking

minimal leverage,

slight lease-up risk

and minimal

redevelopment risk.

Equity investments in

assets that require

fair redevelopment,

lease-up,

repositioning or

management

improvements.

Typically carries

more leverage than

core or core plus.

Highest risk vehicle

that are usually

structured as

partnerships. There is

often high latitude to

invest in nearly

anything - land,

significant

redevelopment,

vacant buildings,

sector bets or other

niches.

Risk Metric

Return expectations 6-8 (unlevered) 9-13% 12-18% 20%+

% from income 80-100% 60% 50% 20%

Leverage 0-30% 30-50% 50-60% 60-85%

Holding Periods 5-10 years 4-7 years 3-5 years 3-5 years

Why Global - Issues?

International Investors

Look For…

Access to

product Tax / Structures

Transparency

Political Stability

Low Currency

Risk Local

Partners

Availability Of

Finance

Occupier Market Covenant Strength

Exit

Strategy

Going Abroad – For Core Product?

Core Yields - 2015

Source: RCA

Turkey Office Performance – Q1-2015

Source: Cushman & Wakefield

Issues for Core Players

International Investors

Look For…

Access to

product Tax / Structures

Transparency

Political Stability

Low Currency

Risk Local

Partners

Availability Of

Finance

Occupier Market Covenant Strength

Exit

Strategy

For 50 – 100 bps?

What About Opportunistic Investors?

• Much smaller portion of overall portfolio (5-9%), unless

opportunity fund or P/E group

• Typical strategies:

– Conduit investing for one-off development deals (hands-

off)

– Hands on investment/management, one-off deals

– Entity level investment (P/E, opportunistic, hedge)

• 20%+, development risk, 3 – 5 year horizon

What About Opportunistic Investors?

• Challenges include:

– Entry structure

– Placing funds

– Oversight

– Exit

– Repatriation

Foreign Investing 5 Year Rolling Hold Period – USD/Host Country

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2006 2007 2008 2009 2010

Do

lla

r R

isk

Year of Investment

Turkey

India

China

Africa

Don’t Like FX Risk? Hedge

• Kenya – 950 – 1,100 bp/year

• India – 900 – 1,200 bp/year

• Turkey – 800 – 1,000 bp/year

• China? Why bother?

Issues for Opportunistic Players

International Investors

Look For…

Access to

product Tax / Structures

Transparency

Political Stability

Low Currency

Risk Local

Partners

Availability Of

Finance

Occupier Market Covenant Strength

Exit

Strategy

Un-hedged: 20%+ becomes negative (large) ?

Hedged: 20%+ becomes 10% -> ?

Real Estate Fund Activity

Real Estate Funds in 2014 (Core, VA, Opp, Dbt, Eq)

Source: Preqin

Private Equity Fundraising Activity $340 bn AUM - $85 bn ‘dry powder’

Historic Performance - Multiples

Source: Preqin

Net IRR’s

Source: Preqin

Value Add vs Opportunistic

Source: Preqin

Fund Strategies

Source: Preqin

Locational Preferences - 2015

Source: Preqin

Some Real Estate Specific Issues:

1. The ‘Emerging Market’ Story

India (China, Africa, ME, Turkey?)

• Speculators vs consumers

• 2.5% residential yield, no rent growth

• Indian sovereign debt yields: ~9%

Can You Make $ in Real Estate?

Source: Colliers 2014

Gurgaon, NCR

Gurgaon, NCR

• Project: 200 units, 2BHK, ~ 1,500 sq.ft.

– Golf Course Road Extension (GCRE)

• Land : 500 rs/sq.ft.

• Soft cost: 300 rs/sq.ft.

– Consultants, design, approvals

• Construction: 2,400 rs/sq.ft.

• Total development costs: 3,200 rs/sq.ft.

Gurgaon, NCR

• Market for 2 BHK:

– ~ 1,500 sq.ft. 7,500 – 9,000 rs/sq.ft.

• 3 year total development period

• Can we make $$ in development?

Total Development Costs

• Project: 200 units @ 1,500 sq.ft. 300,000 sq.ft.

• Land : 150 mm rs

• Soft cost: 60 mm rs (2 yr)

– Consultants, design, approvals

• Construction: 720 mm rs (1 yr)

• Total development costs: 930 mm rs (3 yr)

Option 1 – Developer Pays

Outflows:

• T0 – buy land for 150 mm rs

• ET1 – soft costs – 30 mm rs

• ET2 – soft costs – 30 mm rs

• T3 - construction – 720 mm rs

Time Frame - Outflows

150 mm 30 mm 30 mm 720mm

t0 t1 t2 t3

Option 1 – Developer Pays

Inflows:

• ET2 – pre-sales (post apprvl) – 50 units @7,500 rs/s.f.

@ 30%

– 168.8 mm rs (393.8 mm rs bal.)

• ET3 – sales – 150 units @ 9,000 rs/s.f.

– 2.025 bn rs + bal. of 393.8 mm from pre-sales

– = 2.42 bn rs

Time Frame - Inflows 2.42 bn rs

IRR= 131%

168.8 mm rs

150 mm 30 mm 30 mm 720mm

t0 t1 t2 t3

Want To Be a Developer?

Not Enough ‘Juice’ ? Let’s ‘Push’

the Deal !

Structure:

• Landowner becomes JV partner, contributes land:

– Option 1 – double your money (150mm->300mm)

– Option 2 – deferral for land (150mm + 15% of gross profits)

• ‘Soft sale’ ET1 – 9 units @ 7,500 rs/s.f. – 30% pmt

• Pre-sale ET2 – 8 units @ 8,000 rs/s.f. – 30% pmt

• Pre-sale BT3 – 50 units @8,250 rs/s.f. – 30% pmt

• Pre-sale MT3 – 50 units @ 8,500 rs/s.f. – 30% pmt

• Sale on completion ET3 (+6 mo) – 83 units @ 9,000 rs/s.f.

– + bal ET1 + bal ET2 + bal BT3 + bal MT3

Project – Cash Flows 1.45 bn

191 mm

185 mm

29 mm

30.4 mm

0 mm 30 mm 30 mm 720mm

t0 t1 t2 t3

Landowner Perspective

• Option 1 – contribute land – double price (300 mm rs)

– IRR = 26%

• Option 2 – contribute land – paid land price (150mm rs) and 15% of gross profits

– IRR = 39%

• Good deal for landowner?

• What about developer?

Project – Cash Flows 1.45 bn

IRR = ∞ %

191 mm

185 mm

29 mm

30.4 mm

0 mm 30 mm 30 mm 720mm

t0 t1 t2 t3

What Can Go Wrong?

• Approvals get held up

• Residents file law suit

• Developer starts F1 team

• Developer buys cricket team

• Developer buys more land

– Country Level Risk • Political, Legal, Economic Factors (FX)

– Market Level Risk • Institutional ( Property, Business Factors)

– Deal Level Risk • The deal itself (structure)

• Local markets, operator/developer

– Transparency, Regulation, Yield Compression Will Change the Game…

Emerging Market Risks

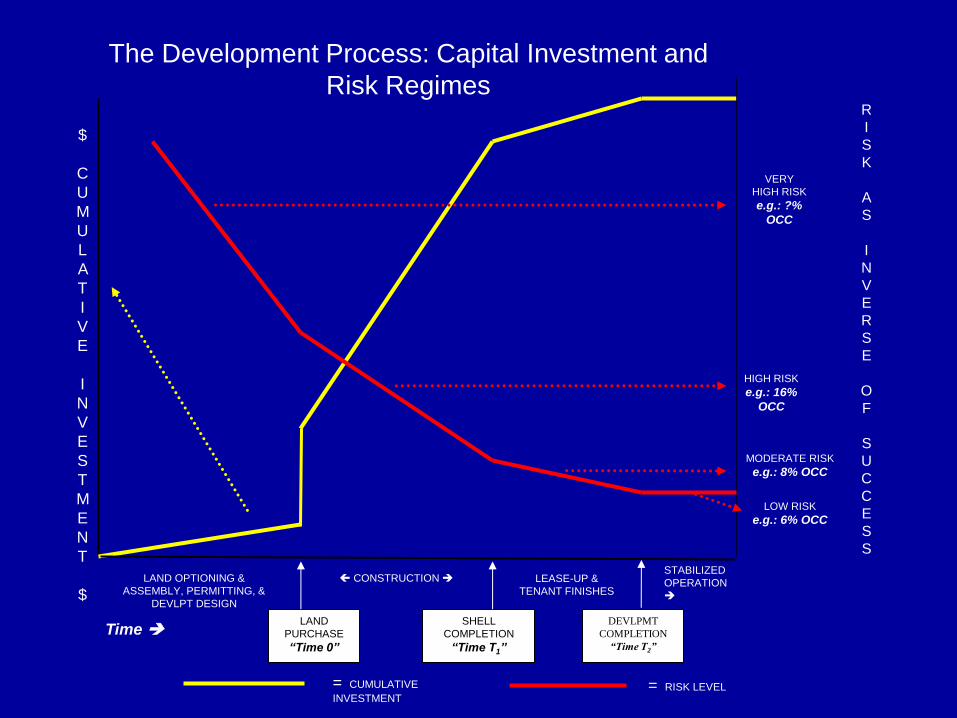

2. Risk Regimes in Real Estate Development

LAND OPTIONING &

ASSEMBLY, PERMITTING, &

DEVLPT DESIGN

CONSTRUCTION

LAND

PURCHASE

“Time 0”

SHELL

COMPLETION

“Time T1”

LEASE-UP &

TENANT FINISHES

STABILIZED

OPERATION

$

C

U

M

U

L

A

T

I

V

E

I

N

V

E

S

T

M

E

N

T

$

DEVLPMT

COMPLETION

“Time T2”

Time

R

I

S

K

A

S

I

N

V

E

R

S

E

O

F

S

U

C

C

E

S

S

VERY

HIGH RISK

e.g.: ?%

OCC

HIGH RISK

e.g.: 16%

OCC

MODERATE RISK

e.g.: 8% OCC

LOW RISK

e.g.: 6% OCC

The Development Process: Capital Investment and

Risk Regimes

= CUMULATIVE

INVESTMENT = RISK LEVEL

LAND OPTIONING &

ASSEMBLY, PERMITTING, &

DEVLPT DESIGN

CONSTRUCTION

LEASE-UP &

TENANT FINISHES

STABILIZED

OPERATION

$

C

U

M

U

L

A

T

I

V

E

I

N

V

E

S

T

M

E

N

T

$

Time

R

I

S

K

A

S

I

N

V

E

R

S

E

S

U

C

C

E

S

S

P

R

O

B

VERY HIGH

RISK =

60%

OCC

HIGH RISK

e.g.: 16%

OCC

MODERATE RISK

e.g.: 8% OCC

LOW RISK

e.g.: 6% OCC

Sell - at 6% OCC when stabilized - so 6% * 0% time weight = 0% time weighted IRR (Sum = 0%)

Lease up – 8% OCC, 25% of project time = 8% * 25% = 2% time weighted IRR (Sum = 2%)

Construction – 16% OCC, 50% of project time = 16% * 50% = 8% time weighted IRR (Sum = 10%)

Permitting, due diligence – X% OCC, 25% of project time = X% * 25% needs to equal 15% (25% overall – 10%

weighted total) = 15%/25% = X% OCC

= CUMULATIVE

INVESTMENT = RISK LEVEL

Overall Development Return = 25%

3. Real Estate Analytics – Sensitivity Analysis

How to Deal with Risk in RED?

• ‘Test’ our numbers (assumptions)

• How many of you do this?

• Construction issues….?

Dealing With Uncertainty…

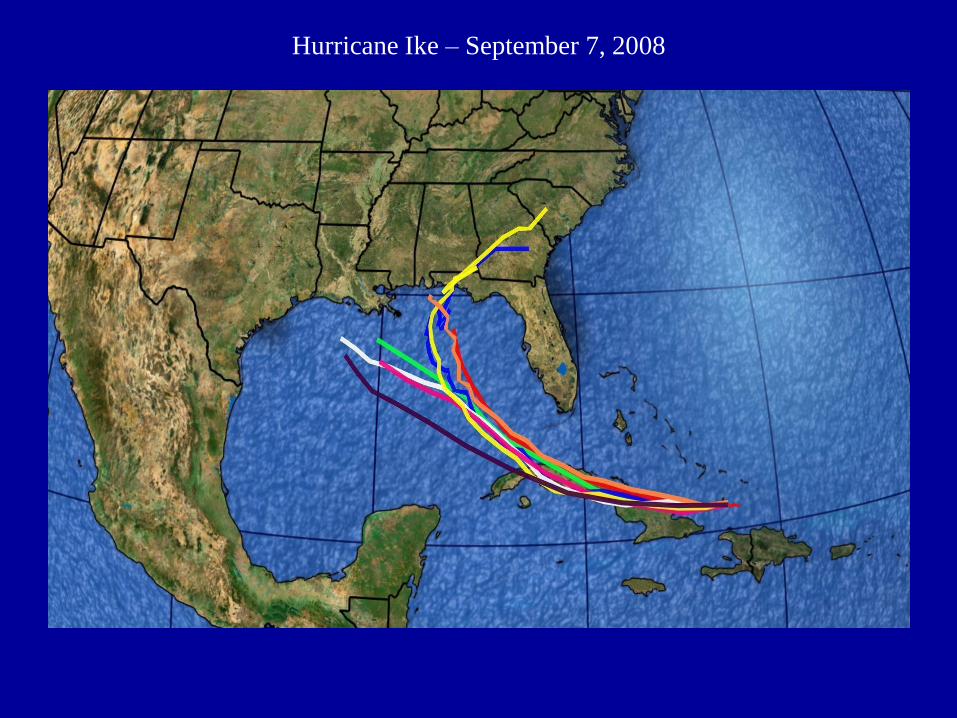

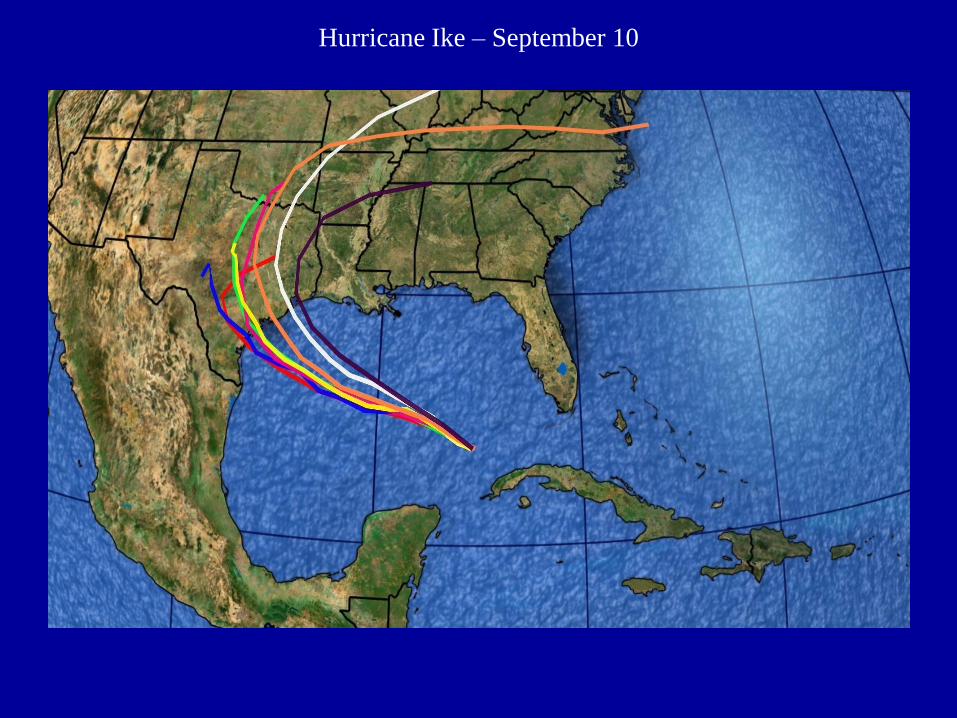

• What do hurricanes have to do with real

estate?

Hurricane Ike – September 7, 2008

Hurricane Ike – September 10

PE

RF

OR

MA

NC

E

TIME

Expectations – Market

PE

RF

OR

MA

NC

E

TIME

Expectations – Government Deal

Residential Rental Project

• Three Year Analysis

• Rents - $1,100 per unit/month

• Operating Expenses - $2.50 per square foot

• Going out Cap Rate – 9.5%

• How do we test our assumptions? • ‘Typical’ way – cut down trees

Discussion on Rents

$1,125

$1,075

$1,100

$1,050

LEVEL

L

I

K

E

L

I

H

O

O

D

Discussion on Operating Expenses

$2.50

$2.75

$2.30 $3.00

LEVEL

L

I

K

E

L

I

H

O

O

D

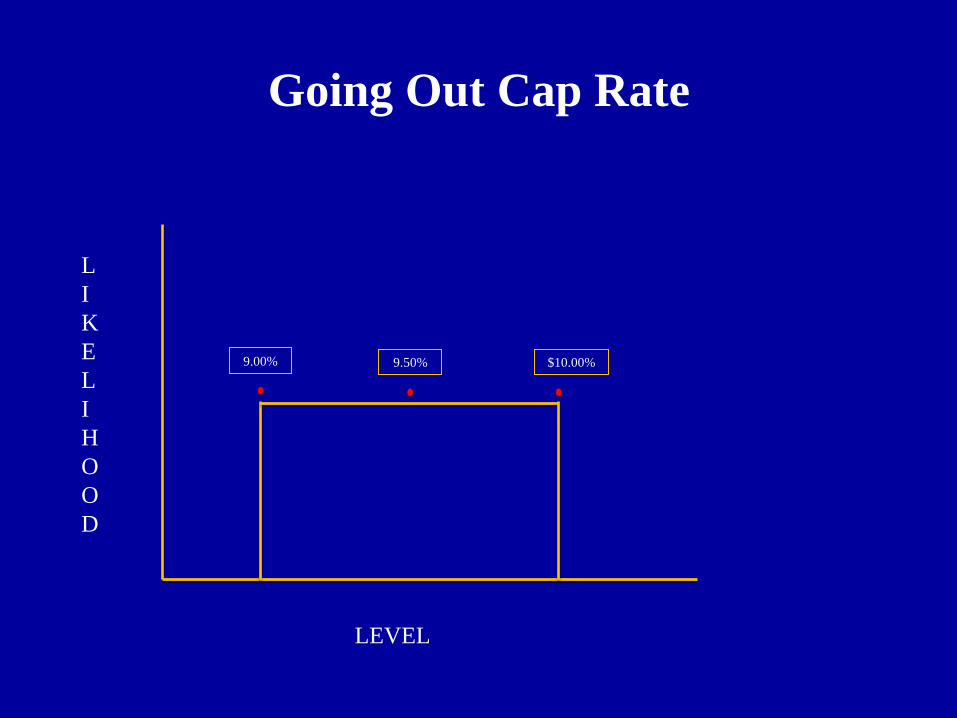

Going Out Cap Rate

9.50% $10.00% 9.00%

LEVEL

L

I

K

E

L

I

H

O

O

D

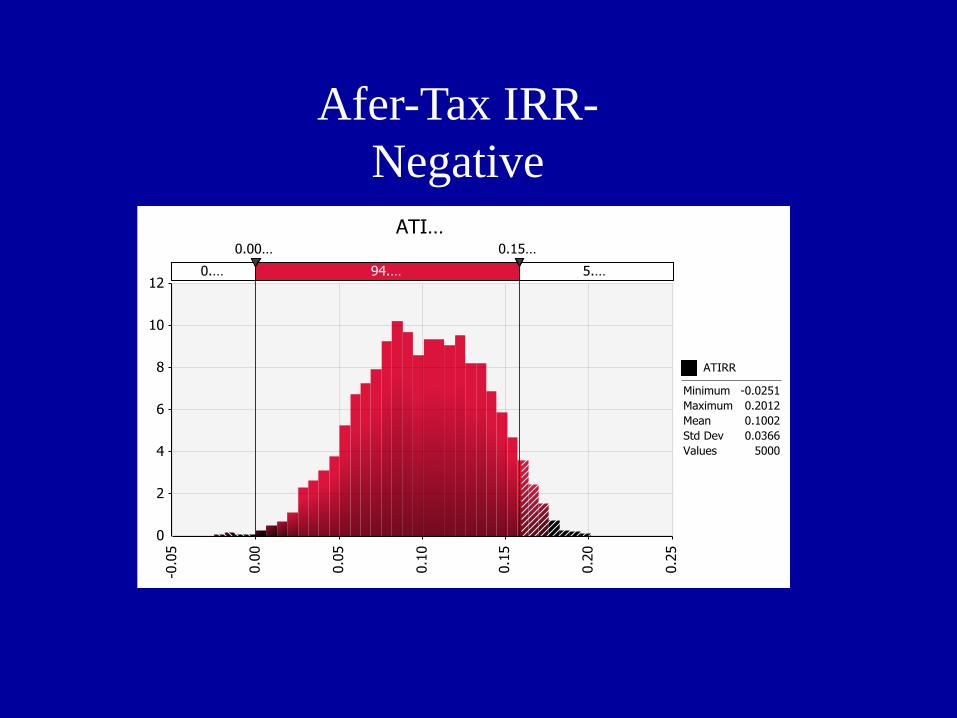

1 Simulation:

5,000 Iterations

Rents

Operating Expenses

Going-Out Cap Rate

Afer-Tax IRR

Afer-Tax IRR-

Negative

After-Tax IRR - Preferred

After-Tax IRR - Promote

• Allow us to articulate boundaries of outcomes

• Incorporates more information into model

• Outcomes are now in ‘ranges’, not single expectation

• Healthy discussion of ‘what matters’

Simulation in Real Estate

4. FOMC – Tightening on Horizon?

Impact of Rising Interest Rates on Short-

Term Development Deals

• Long-run 10 year Tsry: 5.1%

• Commercial real estate yield spread: ~ 500 bp

• Assume 10 year Tsry -> 4%

• Cap rates rise ~ 150 bp

• What will this mean?

A New World With Higher Yields

• The Deal:

– Value Added Apartment Deal (200+- units)

– $2,630,000 Equity ($4,540,000 PP)

– 8% preference

– Return of capital

– 75%/25% to an 18% ROI (non-cumulative)

– GP fee

– 50%/50% above

– 7% going out cap rate (today’s number)

Cash Flows

• T=0 ($2,630,000)

• T=1 $29,956

• T=2 $279,677

• T=3 cf $281,242

• T=3 resid 3,705,434

• Annual ROI: 22.9%

• IRR: 20.8%

• Good Deal….?

The New World - Cap Rates +150

• T=0 ($2,630,000)

• T=1 $29,956

• T=2 $279,677

• T=3 cf $281,242

• T=3 resid $2,670,455

• Annual ROI: 8.0%

• IRR: 7.57%

• ‘Opportunity’ becomes ‘Core’….?

Summary From Around the World

• Real Estate has ‘weathered the storm’… by and large

• Most players: concentrate on domestic markets

• Int’l -> specific markets and products

• Emerging markets are maturing – and noticing it….

• Increased capital flows from Asia … wealth is mobile (Latin America, Middle East)

• ‘Safe Haven’ cities continue to remain popular

• Mezzanine and new equity capital will be ‘fully priced’

How Does All of This Relate to Turkey?

• Challenges:

– Political risks

– RE market size

– Institutional stock

– From ‘5th’ gear to ‘3rd’ gear (PWC/ULI 7->20)

– JLL transparency – 31 (semi-transparent)

• Opportunities:

– Demographics, location, culture, re-generation, GDP growth

• Thank You

![Financial Markets in Africa: Opportunities & … Markets in Africa: Opportunities & Challenges Moremi Marwa [27th April 2015] 1 * Preface * Introduction * State of Financial Markets](https://img.pdfslide.us/doc/110x75/5ada6e6c7f8b9aee348cc85e/financial-markets-in-africa-opportunities-markets-in-africa-opportunities.jpg)