Embed Size (px)

Citation preview

1

CHAILEASE HOLDING COMPANY LIMITED

(“the Company”)

Minutes of 2013 Annual General Meeting

Time : May 30, 2013, 9:00 a.m.

Place : 2nd

Fl.,No. 399 Rueiguang Road, Taipei, Taiwan

11492

Present : 713,214,452shares(78.78% of issued shares)

Chairman: : Mr. Fong-Long (Albert) Chen

Minutes taken by : Ms. Jenny Wu

Quorum

As a quorum was present, the Chairman called the meeting to order.

A. Chairman’s Statement (omitted)

B. Matters to Report

Report No. 1

2012 Business Reports. (Please refer to Attachment 1)

Report No. 2

Audit Committee’s Review Report on the 2012 Financial Statements. (Please refer to Attachment 2)

Report No.3

To note the impact of the first-time adoption of IFRSs on the retained earnings and the appropriation

of special surplus reserve.

Explanation:

According to the mandate letters issued by the Financial Supervisory Commission on April

6, 2012, the Company needs to note the impact of the first-time adoption of IFRSs on the

retained earnings and the appropriation of special surplus reserve at the shareholders’

meeting.

1) The retained earnings of the Company decreased by NT$186,664 thousands for the

first-time adoption of IFRSs on January 1, 2012 and decreased by NT$541,551

thousands on January 1, 2013.

2) Due to the decrease in the retained earnings of the Company on the conversion date for

the first-time adoption of IFRSs, the Company doesn't need to appropriate special

surplus reserve for adoption of IFRSs on January 1, 2013 in accordance with the

foresaid mandate letters.

2

C. Matters for Adoption

Proposal 1:

To accept 2012 Business Report and Financial Statements. (Proposed by the Board)

Explanation:

Chailease Holding Company Limited’s Financial Statements, including the balance sheet,

income statement, statement of changes in shareholders’ equity, and statement of cash flows,

were audited by independent auditors, Ms. Lin Wan-Wan and Ms. Chen, Yi-Chun the

partners of KPMG, Taipei. Also Business Report and Financial Statements have been

approved by the Board and examined by the Audit Committee of Chailease Holding

Company Limited.

The 2012 Business Report, independent auditors’ audit report, and the above-mentioned

Financial Statements are attached as Attachment 1and Attachment 3.

Voting Results: 727,589,205 shares were represented at the time of voting;623,173,433shares voted

for the proposal ,representing 85.64% of the total represented shares present;

626shares voted against the proposal, representing 0.000086% of the total

represented shares present;104,415,146 votes were either invalidly cast or

abstained, representing 14.36% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

Proposal 2:

To approve the Proposal for Distribution of 2012 Profits. (Proposed by the Board)

Explanation:

The Company’s operating result of the year 2012 generated a net profit of

NT$4,141,047,030. The Company proposes the profit distribution proposal of 2012 as

follows:

1) To set aside the special surplus reserve of NT$64,864,800 as required by the Article 41

of the Securities and Exchange Act.

2) To pay a cash dividend per share of NT$2 totaling NT$1,810,600,756.

3) To pay a stock dividend per share of NT$ 1 totaling NT$905,300,370 by issuing

90,530,037 common share.

4) Distribution and Appropriation of retained earnings for the year 2012 is attached as

Attachment 4.

It is proposed to authorize the Board of Directors to determine the ex-dividend date and

ex-right date.

Voting Results: 727,589,205 shares were represented at the time of voting;624,634,433shares voted

for the proposal ,representing 85.84% of the total represented shares present;

626shares voted against the proposal, representing 0.000086% of the total

3

represented shares present;102,954,146 votes were either invalidly cast or

abstained, representing 14.16% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

D. Matters for Discussion

Proposal 1:

Proposal for a new share issue through capitalization of retained earnings. (Proposed by the Board)

Explanation:

For the needs of future business development, it is proposed to allot NTD 905,300,370 from

unappropriated retained earnings for capitalization and issue 90,530,037 new shares with

NTD10 par value as stock dividends;

The Company will pay a stock dividend of 100 shares to every 1,000 shares ("Dividend

Ratio") in proportion to the shareholdings shown on the shareholder register as of the

ex-right date, which will be issued at NTD10 par value. For fractional shares, the

shareholders may make an application with the Company's stock agent for aggregating their

fractional shares into one share within five days of the ex-right date; provided, however, that

if there are any fractional shares left, the Company will pay cash in NTD, rounded down to

NTD1, in lieu of stock dividends and the Chairman of the Board of Directors ("Chairman")

is authorized to allot such fractional shares for subscription by designated persons. The total

issued and outstanding common shares of the Company after the proposed capitalization

will be increased from 905,300,378 shares to 995,830,415 shares.

The shareholder’s rights and obligations of the new shares to be issued shall rank pari passu

in all respects with the issued and outstanding common shares of the Company.

Upon approvals of the Annual Shareholders’ Meeting and relevant competent authorities, it

is proposed to authorize the Board of Directors to determine the ex-right date.

It is proposed to authorize the Chairman to handle all matters relating to the proposed

capitalization depending on actual needs or accommodating the competent authority's

requirement to make any change thereto.

Voting Results: 727,589,205 shares were represented at the time of voting;625,974,736 shares

voted for the proposal ,representing 86.03% of the total represented shares present;

no votes were cast against the proposal;101,614,469 votes were either invalidly

cast or abstained, representing 13.97% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

Proposal 2:

To revise the “Rules and Procedures of Shareholders’ Meeting”. (Proposed by the Board)

Explanation:

To meet the latest sample template for the Rules of Procedure for Shareholders Meetings

4

“announced by TSE on February 27. 2013, it is proposed to amend the article 6, 7,9,12 and

13 of the Company’s “Rules and Procedures of Shareholders’ Meeting “.

Comparison Table for Amendments to the “Rules and Procedures of Shareholders’ Meeting”

is attached as Attachment 5.

Voting Results: 727,589,205 shares were represented at the time of voting;624,489,736 shares

voted for the proposal ,representing 85.82% of the total represented shares present;

16,000 shares voted against the proposal, representing 0.002% of the total

represented shares present;103,083,469 votes were either invalidly cast or

abstained, representing 14.17% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

Proposal 3:

To revise the “Processing Procedures for the Acquisition and Disposal of Assets”. (Proposed by the

Board)

Explanation:

The subject amendments are to comply with the regulatory requirements by Taiwan

competent authority and to accommodate the needs of business development.

The main amendments are summarized as follows:

1) Equipment purchased for rent and sales is included in the applicable scope. (revised)

2) To add an Article to define the specific terms used in the Procedure. (added)

3) To adopt the definition of IFRSs for related-party and the Subsidiary (added )

4) The authority delegated for the transaction of other fixed assets, membership,

intangible assets, and other assets are expressed by NTD instead of USD. ( revised )

5) To empower the Chairman to approve a single transaction for the acquisition or

disposal of business-use machinery and equipment between the Company and its

subsidiaries within NT$300 million. (added)

6) As required by the Article 41 of the Securities and Exchange Act, the Company shall

set aside a special surplus reserve for the real property transaction between the investee

under the equity method and the related party (added)

7) To set the principle of approval for the Audit Committee or the Board of Directors on

the material acquisition or disposal of assets transaction (added)

8) To reorder the Articles of the Procedure according to the Regulations issued by Taiwan

competent authority. (revised)

Comparison Table for Amendments to “Processing Procedures for the Acquisition and

Disposal of Assets” is attached as Attachment 6.

Voting Results: 727,589,205 shares were represented at the time of voting;624,505,736shares voted

for the proposal ,representing 85.83% of the total represented shares present; no

votes were cast against the proposal;103,083,469 votes were either invalidly cast

5

or abstained, representing 14.17% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

Proposal 4:

To amend the Company’s “Procedures for Engaging in Derivatives Trading”. (Proposed by the

Board)

Explanation:

The subject amendments are to comply with the regulatory requirements by Taiwan

competent authority and to accommodate the needs of business development.

The main amendments are summarized as follows:

1) To adopt the IFRSs accounting processing for the derivatives trading (Article 3)

2) To remove the loss limit of the non-hedging derivatives trading and to add the loss limit

of hedging derivatives trading. (Article 3)

3) To add the procedure for the Company to correct the announcement and the procedure

for the Subsidiaries to report the relevant announcement information. (Article 5 and

Article 12)

The revised “Procedures for Engaging in Derivatives Trading” thereof shall be submitted at

the Shareholders' Meeting for approval.

Comparison Table of Amendments to “Procedures for Engaging in Derivatives Trading” is

attached as Attachment 7.

Voting Results: 727,589,205 shares were represented at the time of voting;624,505,736shares voted

for the proposal ,representing 85.83% of the total represented shares present; no

votes were cast against the proposal;103,083,469 votes were either invalidly cast

or abstained, representing 14.17% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

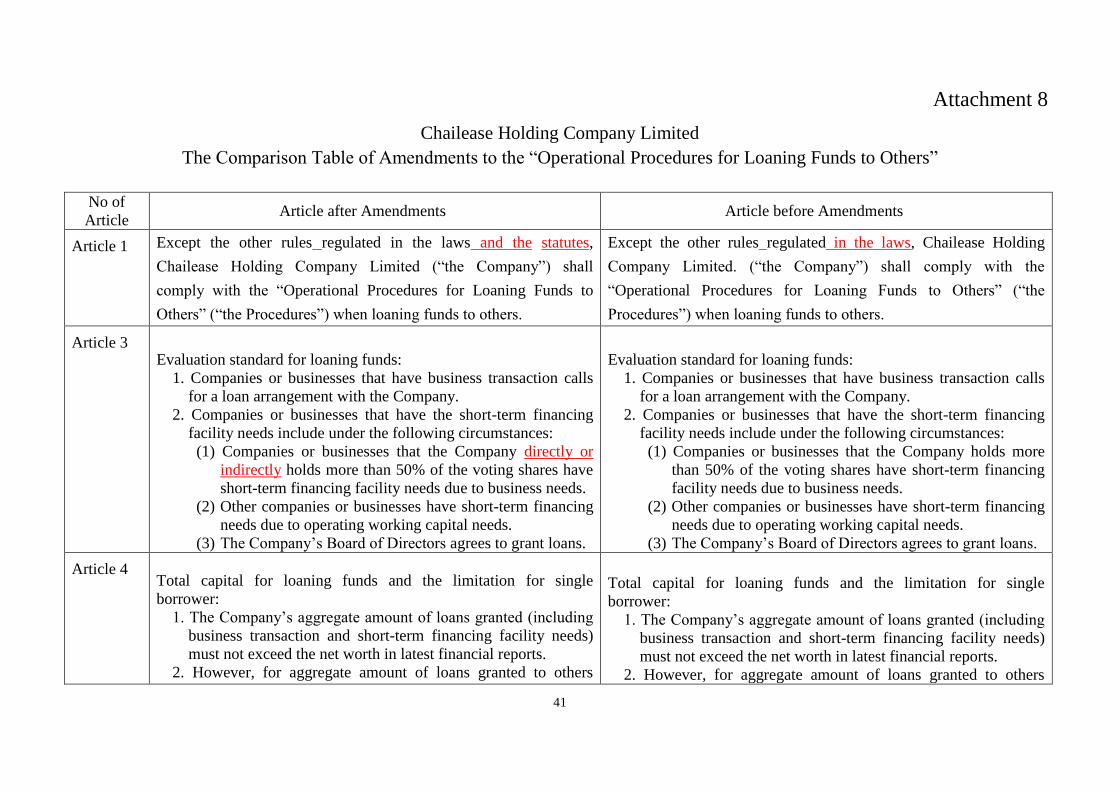

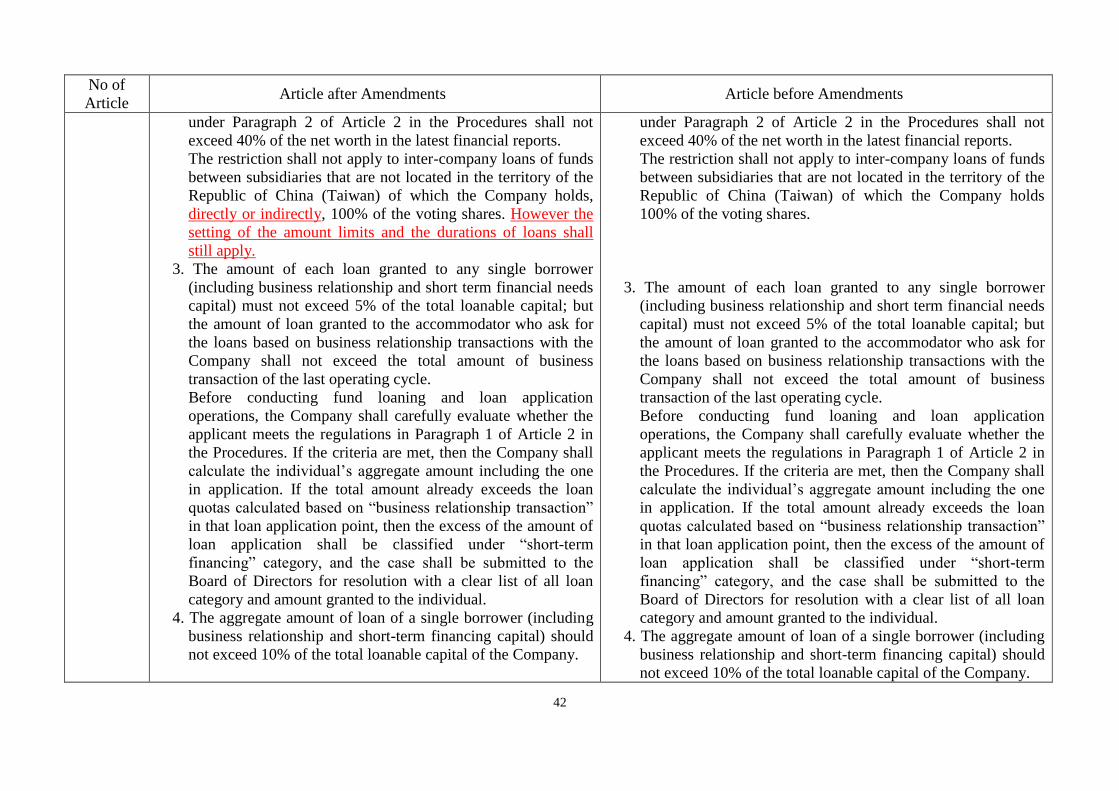

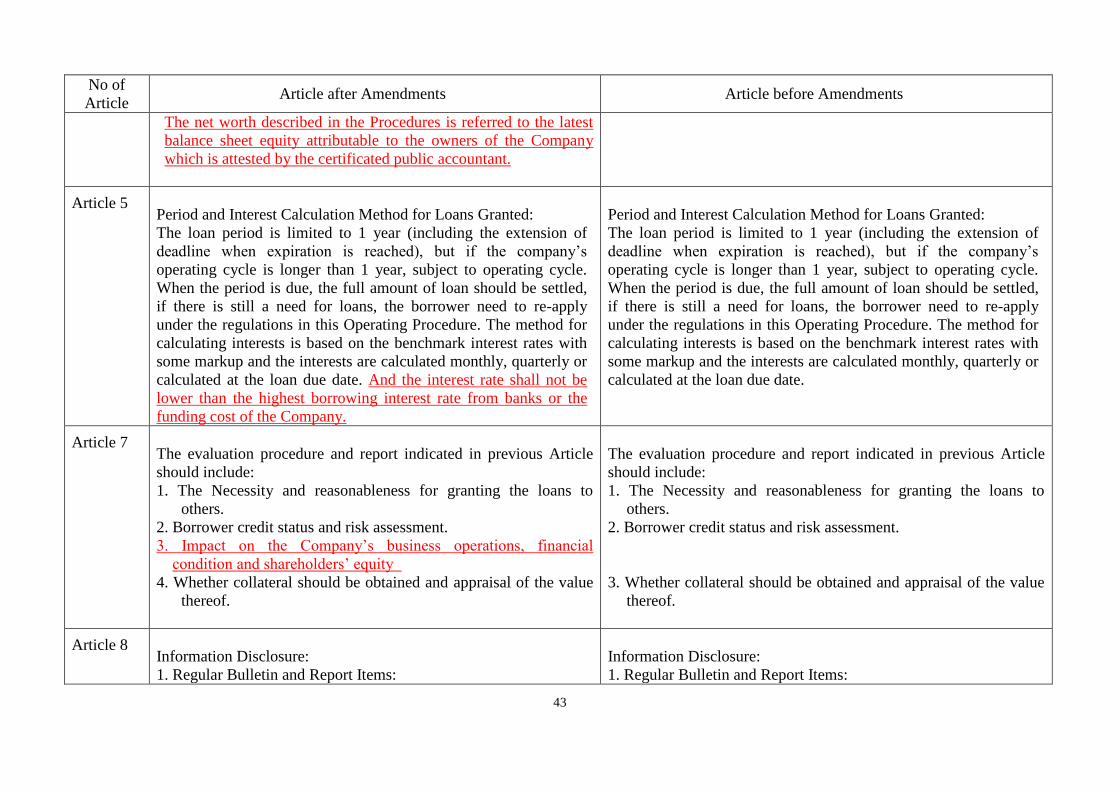

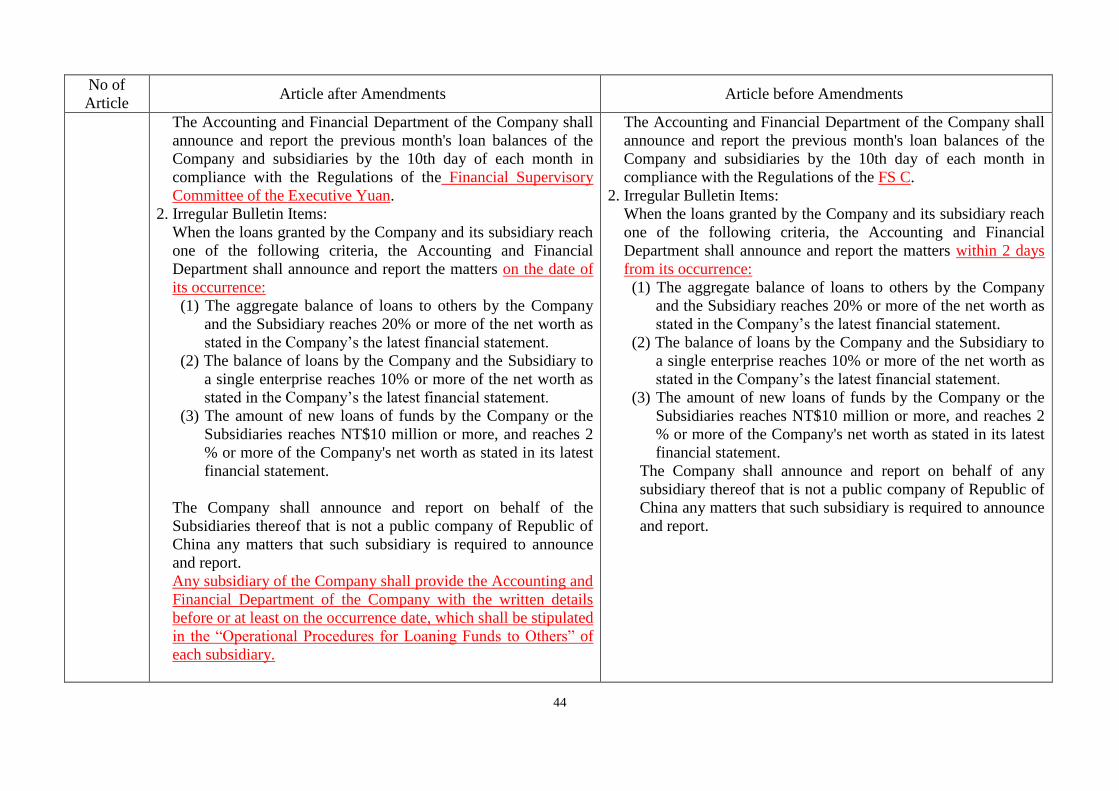

Proposal 5:

To revise the “Operational Procedures for Loaning Funds to Others”. (Proposed by the Board)

Explanation:

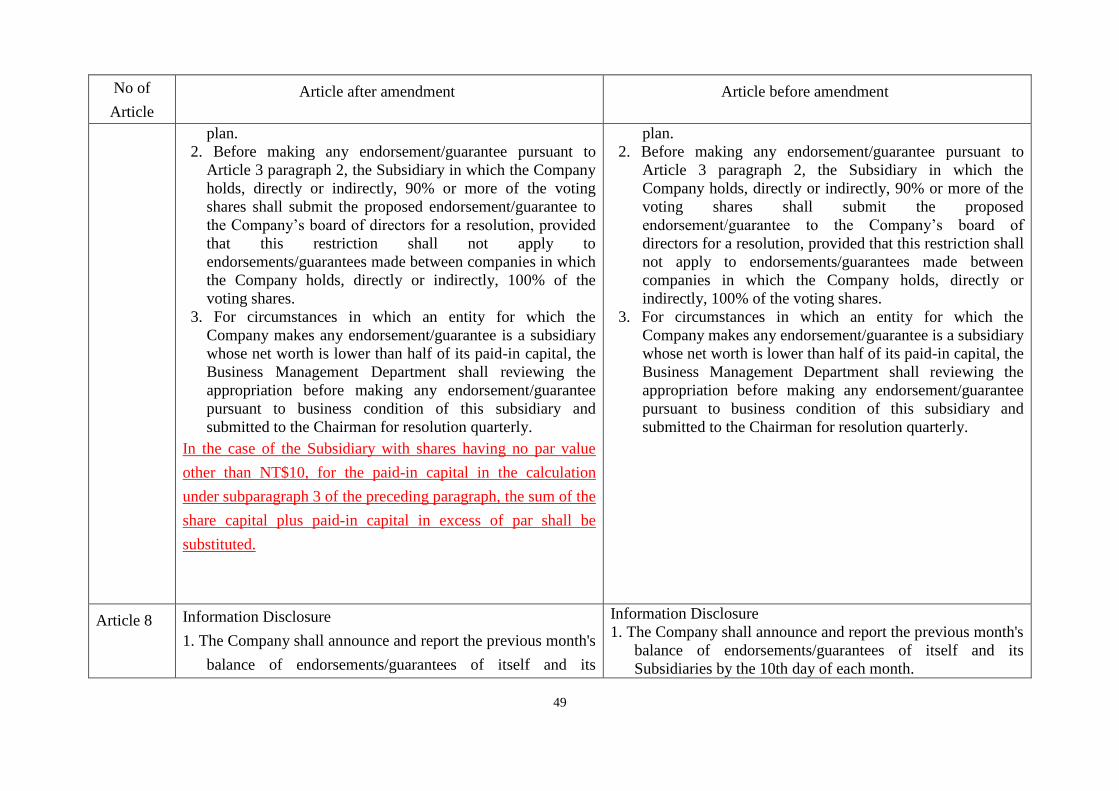

To comply with the latest “Regulations Governing Loaning of Funds and Making of

Endorsements/Guarantees by Public Companies” announced by Financial Supervisory

Commission, Executive Yuan (FSC) on 6 July 2012, the original “Operational Procedures

for Loaning Funds to Others” shall be revised or added.

The main amendments are summarized as follows:

1) To unify and redefine the terms of the Operational Procedures. (revised)

2) To formulate the amount limit and the duration term of Inter-company loans between

6

overseas Subsidiaries (added)

3) To set the principle of minimum lending rate (added)

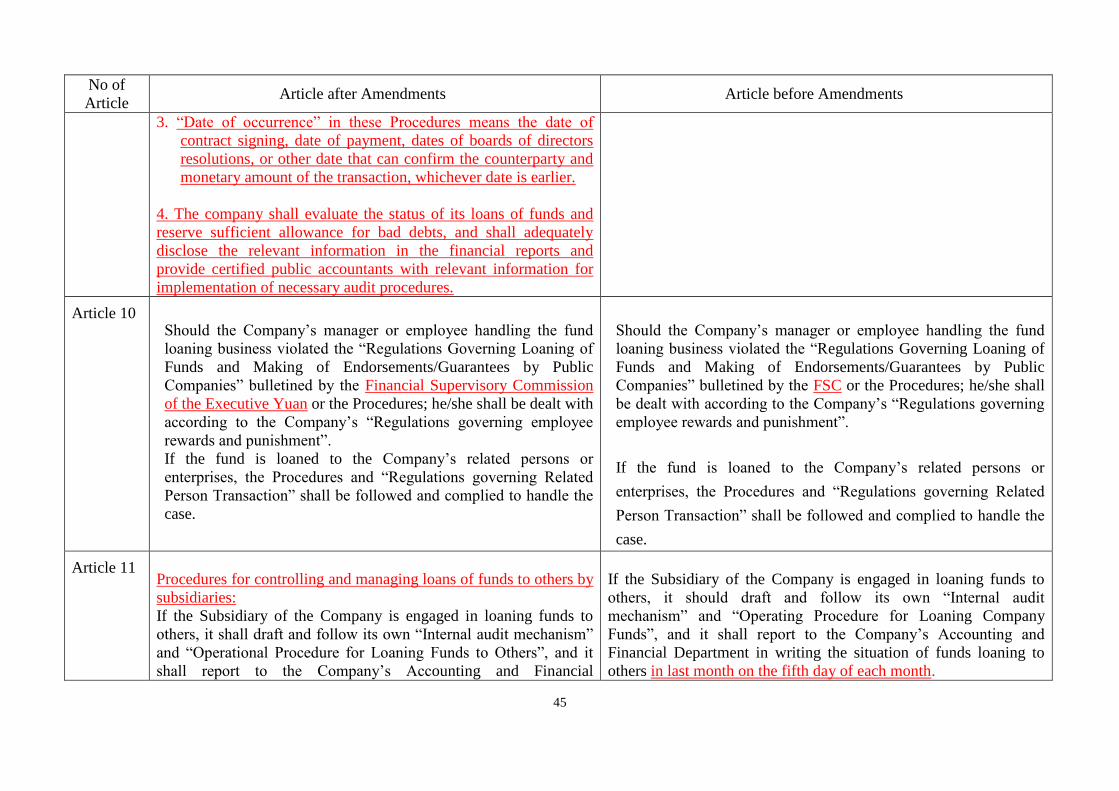

4) The Company shall evaluate the status of its loans of funds and reserve sufficient

allowance for bad debts, and shall adequately disclose the relevant information in the

financial reports, and provide certified public accountants with relevant information for

implementation of necessary audit procedures (added)

The revised “Operational Procedures for Loaning Funds to Others” thereof shall be

submitted at the Shareholders' Meeting for approval.

Comparisons Tables of Amendments to ”Operational Procedures for Loaning Funds to

Others” is attached as Attachment 8.

Voting Results: 727,589,205 shares were represented at the time of voting;624,505,736shares voted

for the proposal ,representing 85.83% of the total represented shares present; no

votes were cast against the proposal;103,083,469 votes were either invalidly cast

or abstained, representing 14.17% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

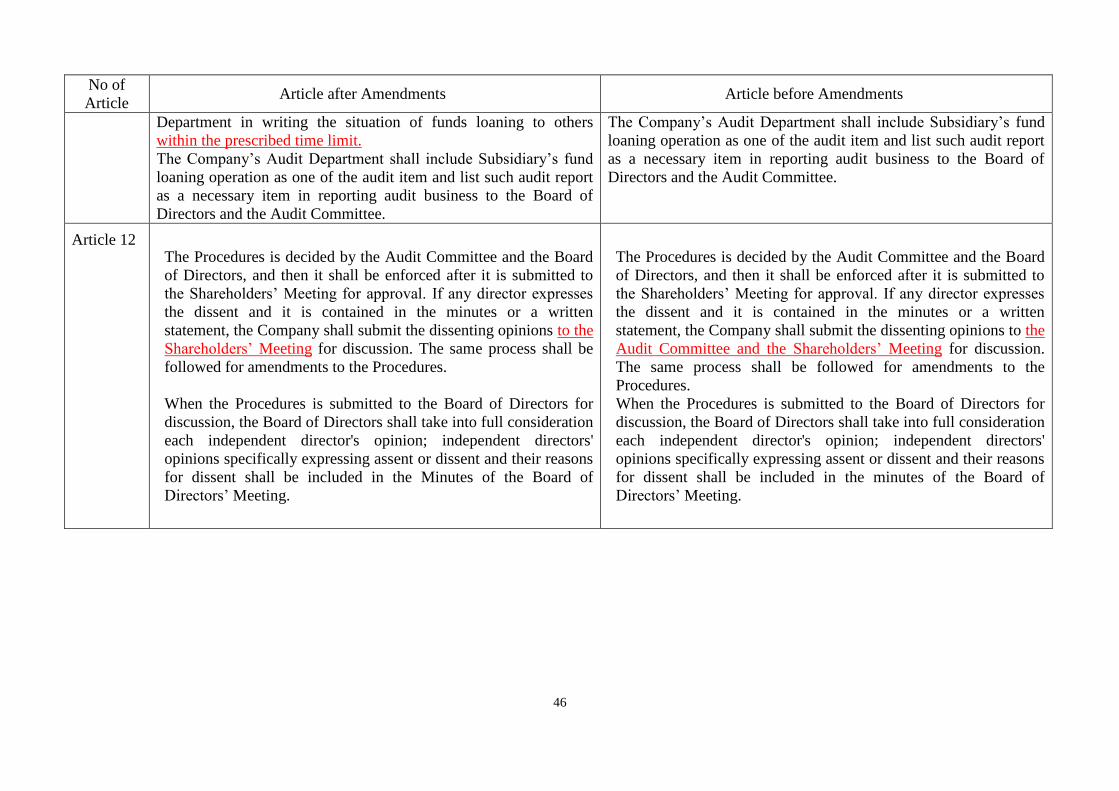

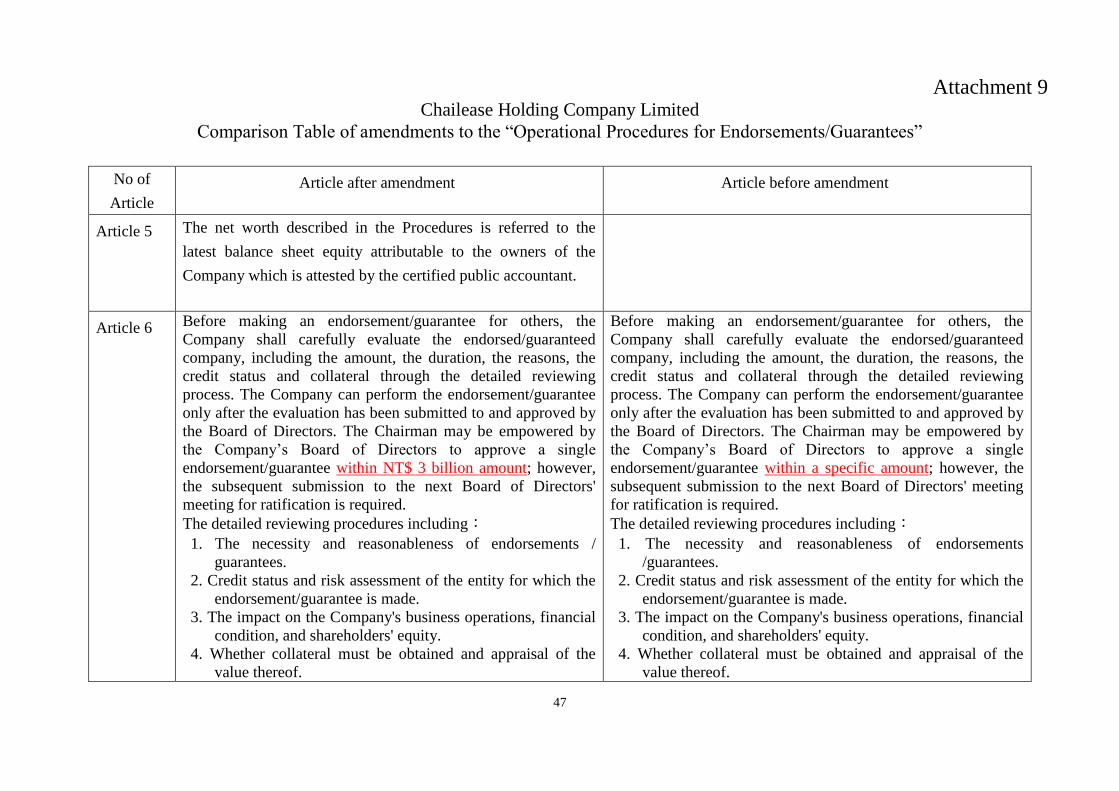

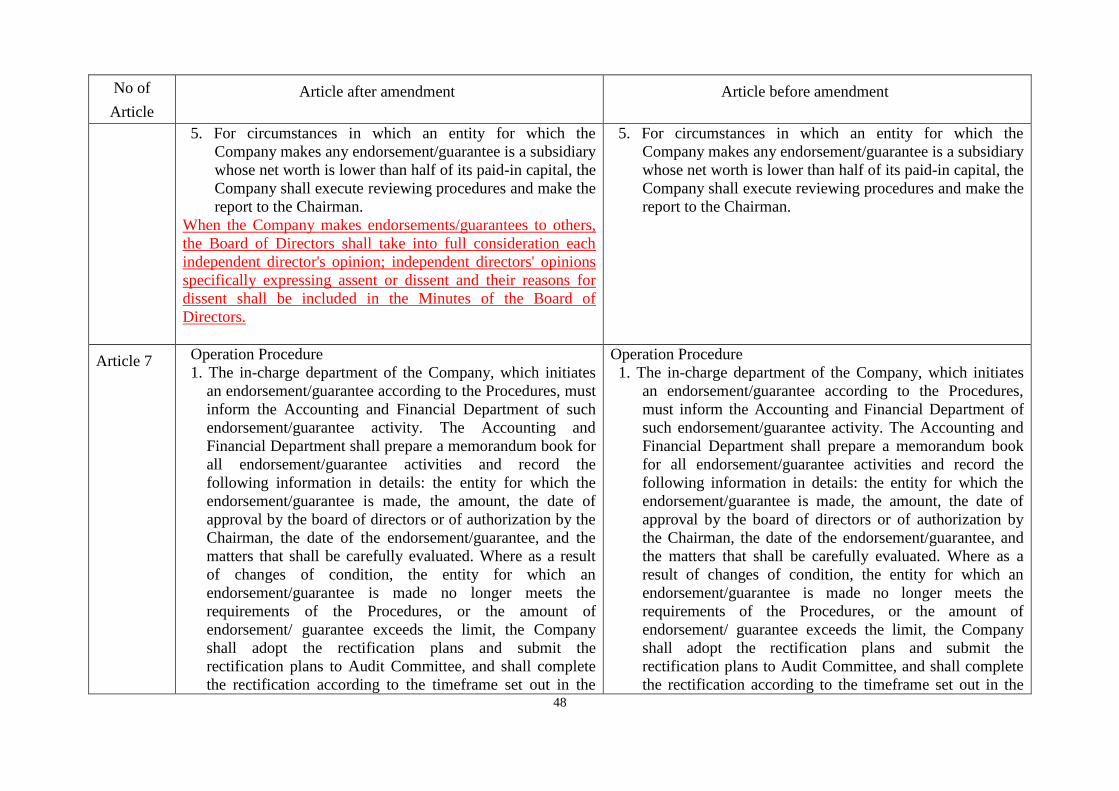

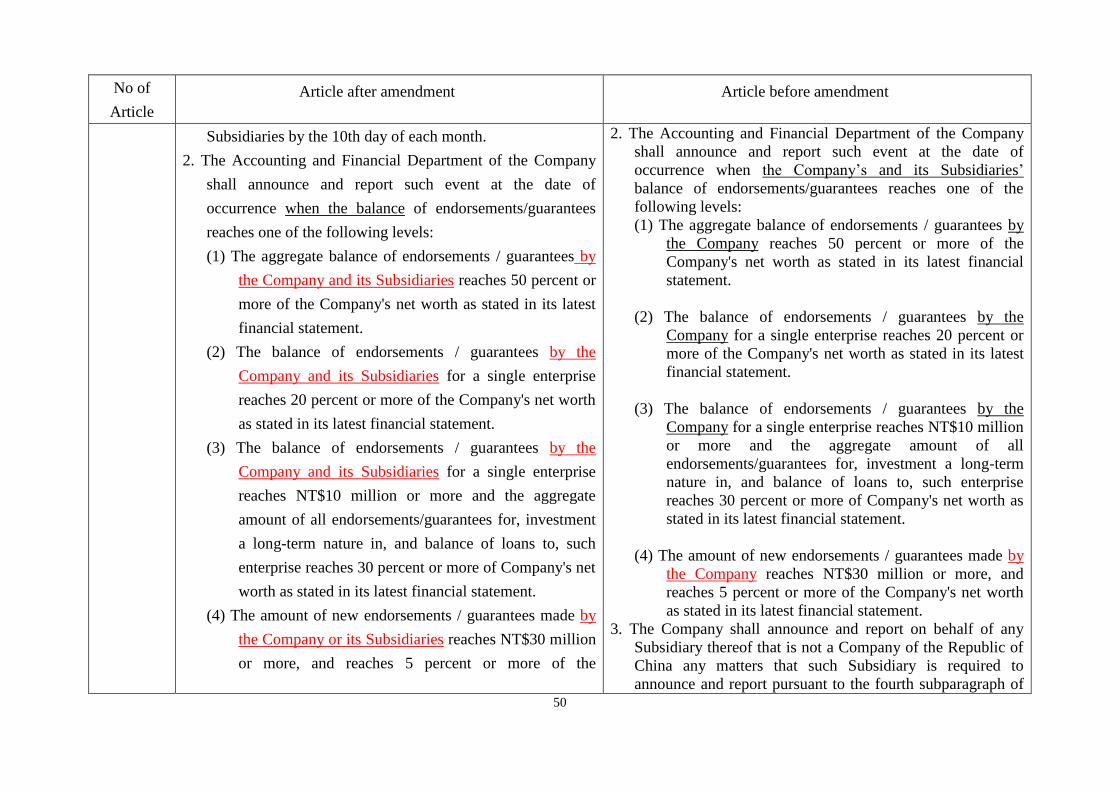

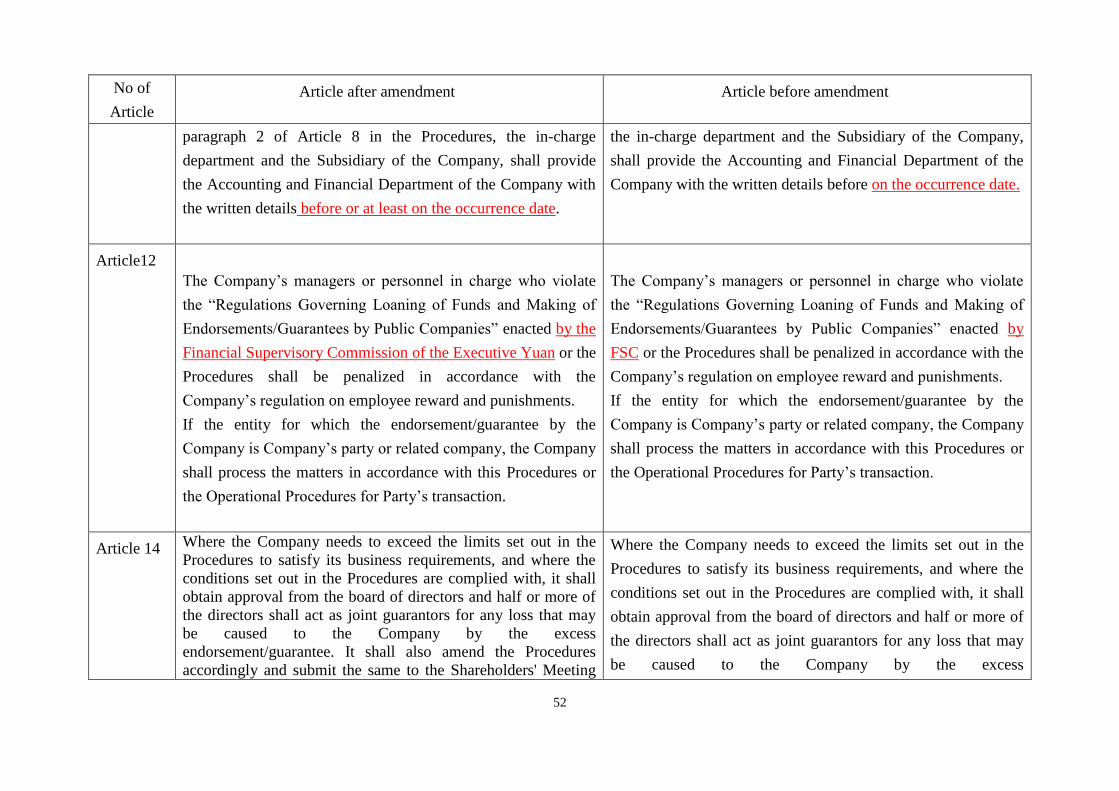

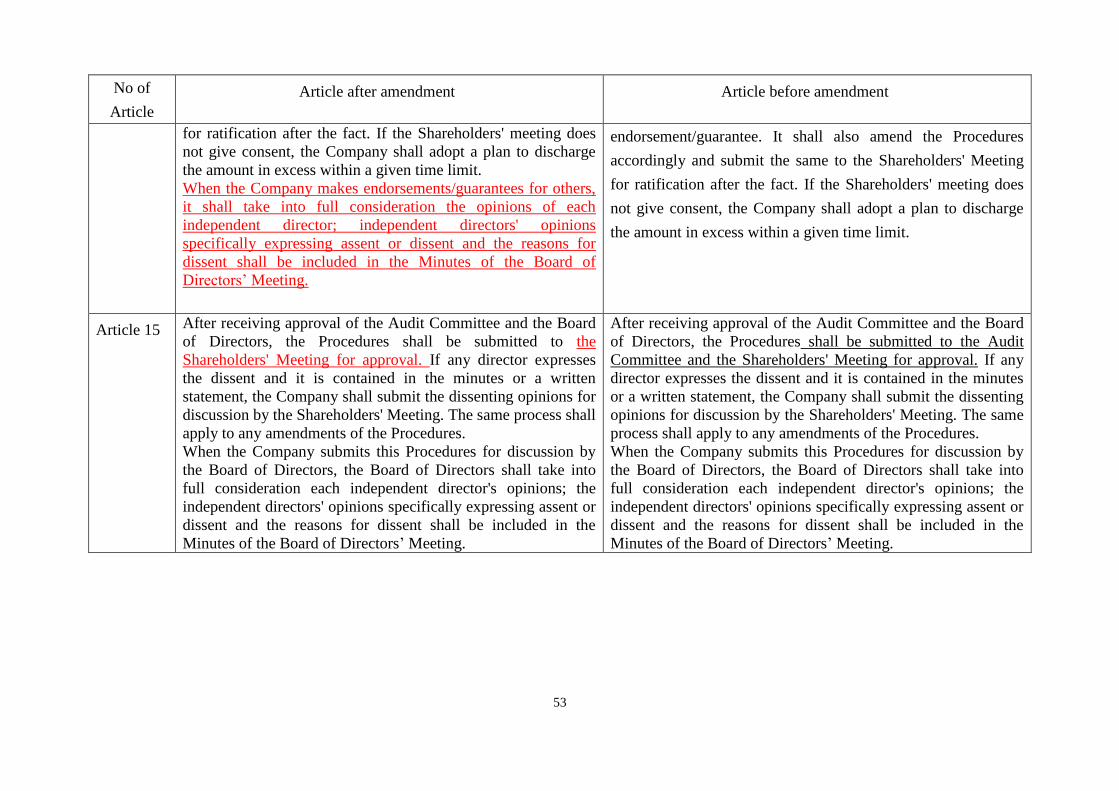

Proposal 6:

To amend the Company’s “Operational Procedures for Endorsements/Guarantees for Others".

(Proposed by the Board)

Explanation:

To comply with the latest “Regulations Governing Loaning of Funds and Making of

Endorsements/Guarantees by Public Companies” announced by Financial Supervisory

Commission, Executive Yuan(FSC) on 6 July 2012, the original “Operational Procedures for

Endorsements/Guarantees for Others” shall be revised or added

The main amendments are summarized as follows:

1) To unify and redefine the terms of the Operational Procedures. (revised)

2) To empower the Chairman to approve a single endorsement/ guarantee within NT$3

billion. (added)

3) When the Company makes an endorsement/ guarantee, the Company shall take into full

consideration each independent director’s opinion; and shall record the opinion in

Minutes of the Board of Directors’ Meeting. (added)

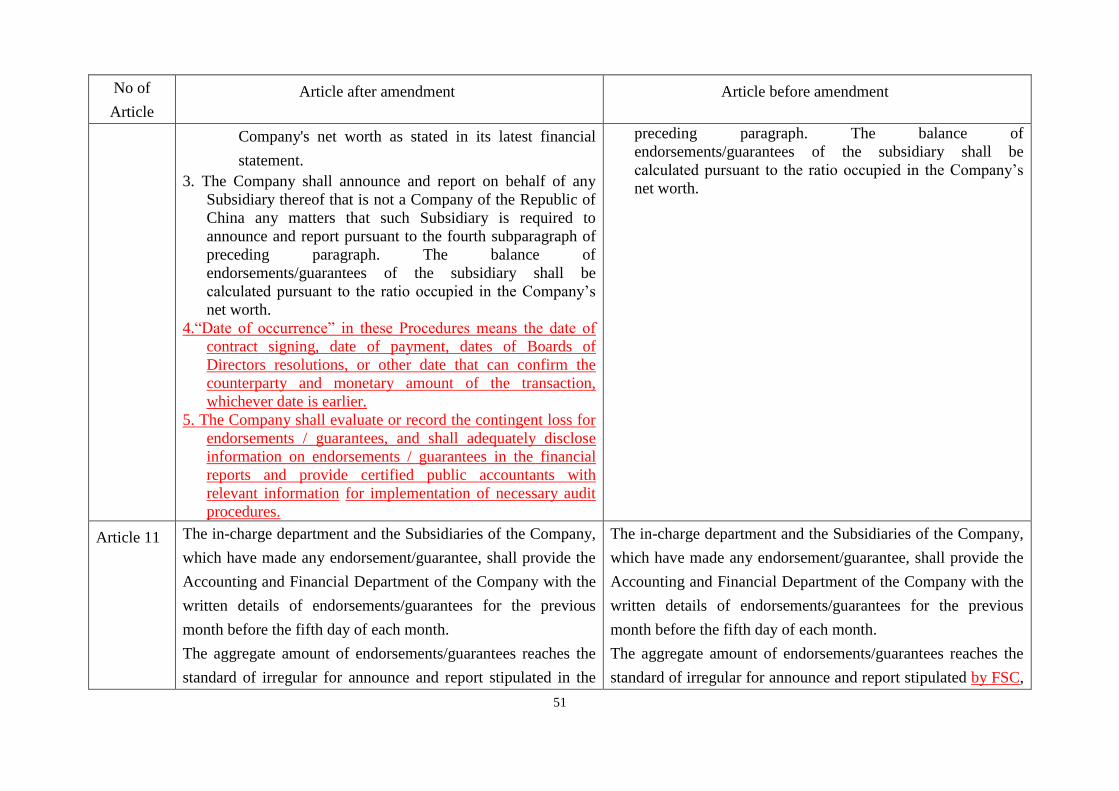

4) The Company shall evaluate or record the contingent loss for

endorsements/guarantees, and shall adequately disclose information on

endorsements/guarantees in the financial reports, and provide certified public

accountants with relevant information for implementation of necessary audit

procedures. (added)

The revised “Operational Procedures for Endorsements/Guarantees for Others” thereof

shall be submitted at the Shareholders' Meeting for approval.

Comparisons Table of Amendments to “Operational Procedures for

7

Endorsements/Guarantees for Others” is attached as Attachment 9.

Voting Results: 727,589,205 shares were represented at the time of voting;622,646,736 shares

voted for the proposal ,representing 85.57% of the total represented shares present;

1,000 shares voted against the proposal, representing 0.00013% of the total

represented shares present;104,941,469 votes were either invalidly cast or

abstained, representing 14.42% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

Proposal 7:

Proposal of release the prohibition on Directors and Independent Directors from participation in

competitive business. (Proposed by the Board)

Explanation:

This proposal is to comply with the Article 109 of the Articles of Association of the

Company which provides that “A director who does anything for himself or on behalf of

another person that is within the scope of the company’s business shall declare the essential

contents of such behavior to the general meeting and be approved by Supermajority

Resolution.”

The resolution to release the non-compete obligation of Directors (including Independent

Directors) has been adopted in the Company’s general meeting in 2012; however, some of

them conducted new business afterwards. It is hereby proposed pursuant to Article 109 of

the Articles of Association of the Company for approval by the Board of Directors that the

director (including the independent director) and its representative (in case of corporate

director) be released from non-compete obligation if he participates in operation of other

companies which are not the subsidiaries of the Company

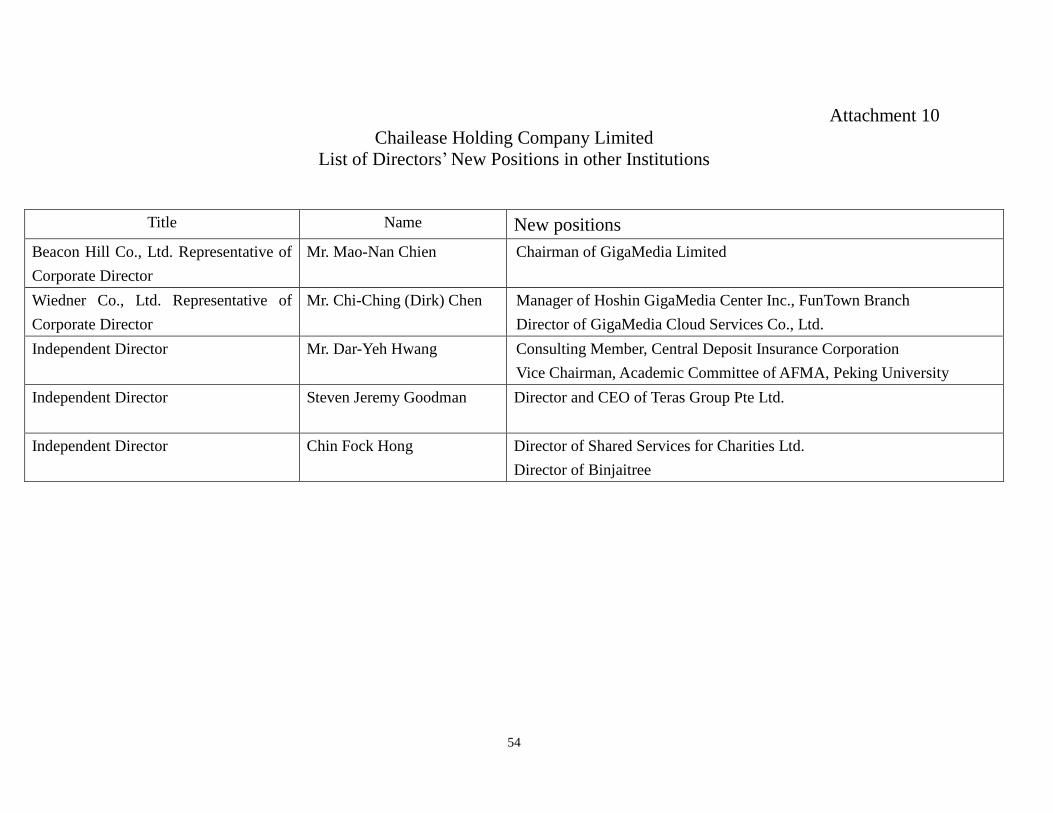

List of Directors’ New Positions is attached in this Handbook, Attachment 10.

Voting Results: 727,589,205 shares were represented at the time of voting;621,035,510 shares

voted for the proposal ,representing 85.35% of the total represented shares present;

1,613,226 shares voted against the proposal, representing 0.22% of the total

represented shares present;104,940,469 votes were either invalidly cast or

abstained, representing 14.43% of the total represented shares present。

RESOLVED, that the above proposal be and hereby was approved as proposed.

E. Any Other Special Motion for Discussion No other motion was proposed, and the Chairman declared the meeting closed.

8

Attachment

9

Attachment 1

2012 Business Report

Stronger and More Solid Growth for Chailease in 2013

2012 was a bumper year for Chailease Holding. Annual profits grew by 69.18%, compared to the

previous year and we had a strong finish to the year, with revenues in December 2012 achieving a

monthly historic high of NT$2.244 billion.

China

Most notable last year was Chailease’s performance in China. In 2012, the percentage of the total

Chailease group profits attributable to China continued to increase substantially.

The contribution of the Chinese market share is expected to continue to grow. For 2013, China

continues to maintain steady overall economic growth, as well as strong GDP and capital investment

growth. This favorable overall environment is expected to benefit Chailease and profits from China

for 2013 are projected to surpass those of 2012.

Chailease remains focused on a growth strategy in China to increase its points of presence in first

and second-tier cities. We have more than 6,500 clients in China, approximately 90% of which are

Chinese enterprises. In the future, we aim to increase our focus on a strategy of localization, in

addition to continuing an annual expansion of 3 to 5 new branches. Our entire China market will also

be divided into five main regions: East, North, Central, Southeast and Southwest, and in-depth

industrial district surveys will be performed in each region. At the same time, manpower will be

increased at branches which have already been established for at least 4 to 5 years in order to expand

the scope of the operations in China.

Chailease has already accumulated a strong first-mover advantage in China, and we are committed to

the continued expansion of our operational footprint, and lead the competition in terms of dedication

to our internal control system and localized manpower training. As the foundations are laid in China,

Chailease will strive to replicate the business model which has been so successful in Taiwan, i.e.

expanding the product line to include factoring (accounts receivable financing), insurance brokerage,

and corporate long-term car rental services, in addition to offering traditional services such as

industrial machinery and equipment financing.

Taiwan

10

Chailease was founded in Taiwan where it has thrived for thirty-six years and boasts numerous

branches offering innovative services. Since its inception, Chailease has provided services to its

SME customer base, which includes enterprises at varying stages of development with diverse

capital requirements. Chailease continues to launch a variety of innovative goods and services, and

now has more than 42% of the leasing market share in Taiwan. As the industry leader, Chailease

aims to strengthen brand competitiveness by offering more innovative, diversified and value-added

products, in addition to providing heartfelt, attentive service to clients.

Services and Products

Owing to Chailease’s extensive experience in providing services to SMEs, at times we can predict

what financing services clients will need before they even request it.

The best example of this is green financing, a tripartite combination of technical assessment,

manufacturing equipment, and energy-saving profit sharing, which assists enterprises in pursuing

sustainable development and simultaneously allows them to support the growing green energy

industry. After launching green financing, Chailease not only won wide praise, but also amassed

invaluable experience with suppliers from various fields.

This year, Chailease will launch its one-stop shopping “cloud platform,” which includes an

integration of hardware and software, communications, and data storage.

Due to Chailease’s impressive track record and unrivaled strategic vision, every new service we

introduce is marked with much fanfare. We are thus confident that the launch of our innovative new

products and services will be even more successful than ever before.

ASEAN Market

For 2013 and 2014, in addition to increasing profits in the Greater China market, we also aim to

make gains through the rapid rise of the ASEAN region. 2015 will be an especially important year

because ASEAN’s goal of regional economic integration will have been realized, allowing us to

accelerate our development in the region.

Chailease currently has four locations in Thailand and two in Vietnam. Thailand, in addition to being

ASEAN’s opinion leader, is also a world-class electronics and automobile manufacturer; moreover,

its government policies encourage investment. For these reasons, this year we plan to increase our

business base in Thailand to expand the size of our market share. We aim to accelerate the growth of

11

our total assets in Thailand, thereby enabling it to become one of the major future growth engines to

incrementally drive the comprehensive development of Chailease in the ASEAN region.

Corporate Social Responsibility and Sustainability

In recent years, Chailease has made countless social contributions. In 2004, we established a charity

foundation and a youth career counseling program. In 2011, we began organizing an SME forum

which brings together successful small business owners who make their vast knowledge and

expertise available to other SMEs. Additionally, to fulfill our environmental responsibilities as global

citizens, Chailease has successfully introduced technology and equipment to help clients save energy

and reduce carbon emissions, and in the future we will begin providing solar power financing

services.

Outlook for 2013

In 2012, Chailease exceeded performance expectations, and has already begun to attract the attention

of numerous global institutional investors. Positive reactions from our regional market segments

confirm the effectiveness of Chailease’s precise market positioning strategy.

This year, driven by the momentum of a multifaceted approach to growth, Chailease will continue

striving to outperform the GDP growth rate in each of its major markets. Thus, Chailease will

continue the expansion of existing products and services, in addition to increasing efforts to gain

widespread customer acceptance of new services, all toward the ultimate goal of meeting our 2013

growth objectives for shareholders.

Aided by the modest recovery of the global economy, I am confident that for 2013 this strong growth

momentum can be sustained to achieve even better results in our three major markets: China, Taiwan

and ASEAN.

12

Attachment 2

Chailease Holding Company Limited

Audit Committee’s Report

The Board of Directors has prepared the Company’s 2012 Business Report,

Financial Statements, and proposal for allocation of profits. The CPA, Ms. Wan

Wan Lin and Ms.Yi Chun, Chen of KPMG were retained to audit Chailease

Holding Company Limited’s Financial Statements and has issued an audit report

relating to the Financial Statement.

The Business Report, Financial Statements, and profit allocation proposal have

been reviewed and determined to be correct and accurate by the Audit committee

members of Chailease Holding Company Limited.

According to Article 14-4 of the Securities and Exchange Act, we hereby submit

this report.

Chailease Holding Company Limited

Chairman of the Audit Committee: Dar-Yeh Hwang

March 26, 2013

13

Attachment 3

(English Translation of Financial Report Originally Issued in Chinese)

INDEPENDENT ACCOUNTANTS’ AUDIT REPORT

The Board of Directors of

Chailease Holding Company Limited

We have audited the accompanying consolidated balance sheets of Chailease Holding Company

Limited (the “Company”) and its subsidiaries (“the Group”) as of December 31 , 2012 and 2011, and

the related consolidated statements of income, consolidated changes in stockholders’ equity, and

consolidated statements of cash flows for the years then ended. These consolidated financial

statements are the responsibility of the Group’s management. Our responsibility is to issue a report

on these consolidated financial statements based on our audits.

We conducted our audits in accordance with “Rules Governing Auditing and certification of

Financial Statements by Certified Public Accountants” and auditing standards generally accepted in

the Republic of China. Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the consolidated financial statements are free of material

misstatements. An audit includes examining, on a test basis, evidences supporting the amounts and

disclosures in the consolidated financial statements. An audit also includes assessing the accounting

principles used and significant estimates made by management, as well as evaluating the overall

consolidated financial statement presentation. We believe that our audits provide a reasonable basis

for our opinion.

In our opinion, based on our audit, the consolidated financial statements referred to the first

paragraph present fairly, in all material respects, the financial position of Chailease Holding

Company Limited and its subsidiaries as of December 31, 2012 and 2011, and the results of their

operations and their consolidated cash flows for the years then ended in conformity with the

Guidelines Governing the Preparation of Financial Reports by Securities Issuers and accounting

principles generally accepted in the Republic of China.

KPMG

CPA: Wan Wan, Lin

Yi Chun, Chen

Taipei, Taiwan, R.O.C.

March 26, 2013

Note to Readers

The accompanying consolidated financial statements are intended only to present the financial position, results of operations and cash flows in

accordance with the accounting principles and practices generally accepted in the Republic of China and not those of any other jurisdictions. The standards, procedures, and practices to audit such financial statements are those generally accepted and applied in the Republic of China.

The independent accountants’ report and the accompanying consolidated financial statements are the English translation of the Chinese version prepared and used in the Republic of China. If there is any conflict between, or any difference in the interpretation of, the English and Chinese language

independent accountants’ report and financial statements, the Chinese version shall prevail.

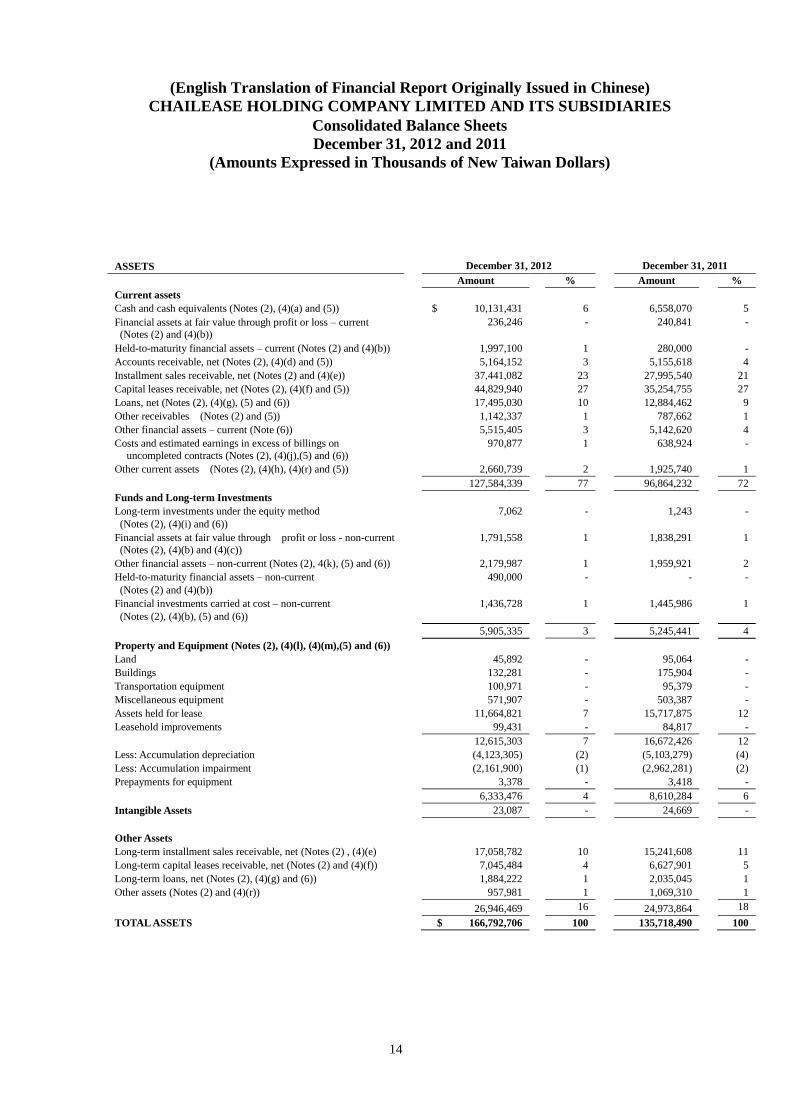

(English Translation of Financial Report Originally Issued in Chinese)

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Balance Sheets

December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars)

14

ASSETS December 31, 2012 December 31, 2011

Amount % Amount %

Current assets

Cash and cash equivalents (Notes (2), (4)(a) and (5)) $ 10,131,431 6 6,558,070 5

Financial assets at fair value through profit or loss – current (Notes (2) and (4)(b))

236,246 -

240,841 -

Held-to-maturity financial assets – current (Notes (2) and (4)(b)) 1,997,100 1 280,000 -

Accounts receivable, net (Notes (2), (4)(d) and (5)) 5,164,152 3 5,155,618 4

Installment sales receivable, net (Notes (2) and (4)(e)) 37,441,082 23 27,995,540 21

Capital leases receivable, net (Notes (2), (4)(f) and (5)) 44,829,940 27 35,254,755 27

Loans, net (Notes (2), (4)(g), (5) and (6)) 17,495,030 10 12,884,462 9

Other receivables (Notes (2) and (5)) 1,142,337 1 787,662 1

Other financial assets – current (Note (6)) 5,515,405 3 5,142,620 4

Costs and estimated earnings in excess of billings on

uncompleted contracts (Notes (2), (4)(j),(5) and (6))

970,877 1 638,924 -

Other current assets (Notes (2), (4)(h), (4)(r) and (5)) 2,660,739 2 1,925,740 1

127,584,339 77 96,864,232 72

Funds and Long-term Investments

Long-term investments under the equity method

(Notes (2), (4)(i) and (6))

7,062 - 1,243 -

Financial assets at fair value through profit or loss - non-current

(Notes (2), (4)(b) and (4)(c))

1,791,558 1 1,838,291 1

Other financial assets – non-current (Notes (2), 4(k), (5) and (6)) 2,179,987 1 1,959,921 2

Held-to-maturity financial assets – non-current

(Notes (2) and (4)(b))

490,000 - - -

Financial investments carried at cost – non-current

(Notes (2), (4)(b), (5) and (6))

1,436,728 1 1,445,986 1

5,905,335 3 5,245,441 4

Property and Equipment (Notes (2), (4)(l), (4)(m),(5) and (6))

Land 45,892 - 95,064 -

Buildings 132,281 - 175,904 -

Transportation equipment 100,971 - 95,379 -

Miscellaneous equipment 571,907 - 503,387 -

Assets held for lease 11,664,821 7 15,717,875 12

Leasehold improvements 99,431 - 84,817 -

12,615,303 7 16,672,426 12

Less: Accumulation depreciation (4,123,305) (2) (5,103,279) (4)

Less: Accumulation impairment (2,161,900) (1) (2,962,281) (2)

Prepayments for equipment 3,378 - 3,418 -

6,333,476 4 8,610,284 6

Intangible Assets 23,087 - 24,669 -

Other Assets

Long-term installment sales receivable, net (Notes (2) , (4)(e) 17,058,782 10 15,241,608 11

Long-term capital leases receivable, net (Notes (2) and (4)(f)) 7,045,484 4 6,627,901 5

Long-term loans, net (Notes (2), (4)(g) and (6)) 1,884,222 1 2,035,045 1

Other assets (Notes (2) and (4)(r)) 957,981 1 1,069,310 1

26,946,469 16 24,973,864 18

TOTAL ASSETS $ 166,792,706 100 135,718,490 100

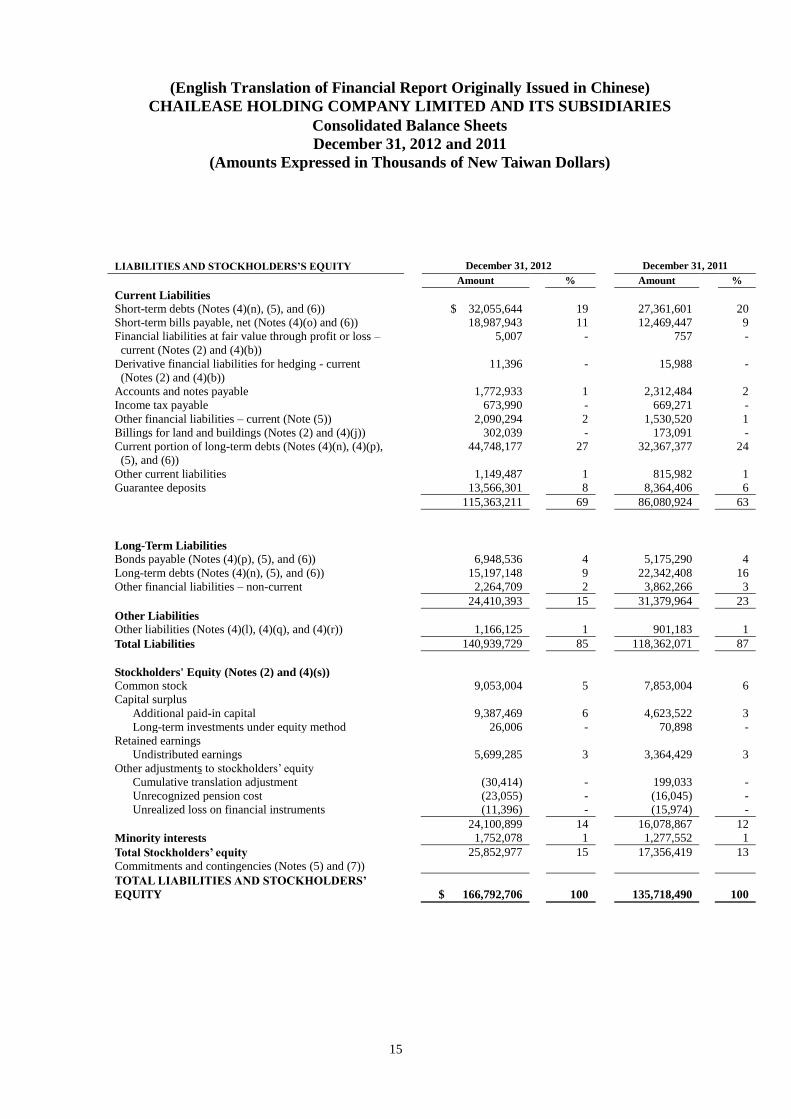

(English Translation of Financial Report Originally Issued in Chinese)

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Balance Sheets

December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars)

15

LIABILITIES AND STOCKHOLDERS’S EQUITY December 31, 2012 December 31, 2011

Amount % Amount %

Current Liabilities

Short-term debts (Notes (4)(n), (5), and (6)) $ 32,055,644 19 27,361,601 20

Short-term bills payable, net (Notes (4)(o) and (6)) 18,987,943 11 12,469,447 9

Financial liabilities at fair value through profit or loss –

current (Notes (2) and (4)(b))

5,007 - 757 -

Derivative financial liabilities for hedging - current

(Notes (2) and (4)(b))

11,396 - 15,988 -

Accounts and notes payable 1,772,933 1 2,312,484 2

Income tax payable 673,990 - 669,271 -

Other financial liabilities – current (Note (5)) 2,090,294 2 1,530,520 1

Billings for land and buildings (Notes (2) and (4)(j)) 302,039 - 173,091 -

Current portion of long-term debts (Notes (4)(n), (4)(p),

(5), and (6))

44,748,177 27 32,367,377 24

Other current liabilities 1,149,487 1 815,982 1

Guarantee deposits 13,566,301 8 8,364,406 6

115,363,211 69 86,080,924 63

Long-Term Liabilities

Bonds payable (Notes (4)(p), (5), and (6)) 6,948,536 4 5,175,290 4

Long-term debts (Notes (4)(n), (5), and (6)) 15,197,148 9 22,342,408 16

Other financial liabilities – non-current 2,264,709 2 3,862,266 3

24,410,393 15 31,379,964 23

Other Liabilities

Other liabilities (Notes (4)(l), (4)(q), and (4)(r)) 1,166,125 1 901,183 1

Total Liabilities 140,939,729 85 118,362,071 87

Stockholders' Equity (Notes (2) and (4)(s))

Common stock 9,053,004 5 7,853,004 6

Capital surplus

Additional paid-in capital 9,387,469 6 4,623,522 3

Long-term investments under equity method 26,006 - 70,898 -

Retained earnings

Undistributed earnings 5,699,285 3 3,364,429 3

Other adjustments to stockholders’ equity

Cumulative translation adjustment (30,414) - 199,033 -

Unrecognized pension cost (23,055) - (16,045) -

Unrealized loss on financial instruments (11,396) - (15,974) -

24,100,899 14 16,078,867 12

Minority interests 1,752,078 1 1,277,552 1

Total Stockholders’ equity 25,852,977 15 17,356,419 13

Commitments and contingencies (Notes (5) and (7))

TOTAL LIABILITIES AND STOCKHOLDERS’

EQUITY

$ 166,792,706

100

135,718,490

100

(English Translation of Financial Report Originally Issued in Chinese)

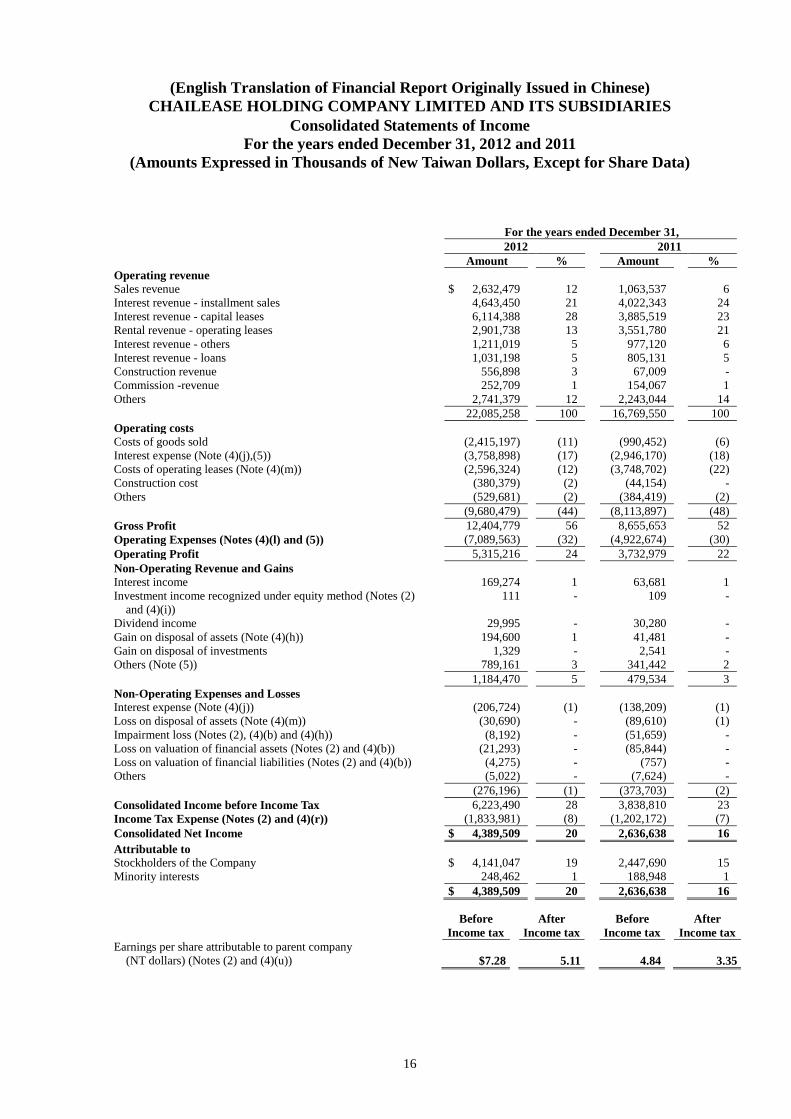

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Statements of Income

For the years ended December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars, Except for Share Data)

16

For the years ended December 31,

2012 2011

Amount % Amount %

Operating revenue

Sales revenue $ 2,632,479 12 1,063,537 6

Interest revenue - installment sales 4,643,450 21 4,022,343 24

Interest revenue - capital leases 6,114,388 28 3,885,519 23

Rental revenue - operating leases 2,901,738 13 3,551,780 21

Interest revenue - others 1,211,019 5 977,120 6

Interest revenue - loans 1,031,198 5 805,131 5

Construction revenue 556,898 3 67,009 -

Commission -revenue 252,709 1 154,067 1

Others 2,741,379 12 2,243,044 14

22,085,258 100 16,769,550 100

Operating costs

Costs of goods sold (2,415,197) (11) (990,452) (6)

Interest expense (Note (4)(j),(5)) (3,758,898) (17) (2,946,170) (18)

Costs of operating leases (Note (4)(m)) (2,596,324) (12) (3,748,702) (22)

Construction cost (380,379) (2) (44,154) -

Others (529,681) (2) (384,419) (2)

(9,680,479) (44) (8,113,897) (48)

Gross Profit 12,404,779 56 8,655,653 52

Operating Expenses (Notes (4)(l) and (5)) (7,089,563) (32) (4,922,674) (30)

Operating Profit 5,315,216 24 3,732,979 22

Non-Operating Revenue and Gains

Interest income 169,274 1 63,681 1

Investment income recognized under equity method (Notes (2)

and (4)(i))

111 - 109 -

Dividend income 29,995 - 30,280 -

Gain on disposal of assets (Note (4)(h)) 194,600 1 41,481 -

Gain on disposal of investments 1,329 - 2,541 -

Others (Note (5)) 789,161 3 341,442 2

1,184,470 5 479,534 3

Non-Operating Expenses and Losses

Interest expense (Note (4)(j)) (206,724) (1) (138,209) (1)

Loss on disposal of assets (Note (4)(m)) (30,690) - (89,610) (1)

Impairment loss (Notes (2), (4)(b) and (4)(h)) (8,192) - (51,659) -

Loss on valuation of financial assets (Notes (2) and (4)(b)) (21,293) - (85,844) -

Loss on valuation of financial liabilities (Notes (2) and (4)(b)) (4,275) - (757) -

Others (5,022) - (7,624) -

(276,196) (1) (373,703) (2)

Consolidated Income before Income Tax 6,223,490 28 3,838,810 23

Income Tax Expense (Notes (2) and (4)(r)) (1,833,981) (8) (1,202,172) (7)

Consolidated Net Income $ 4,389,509 20 2,636,638 16

Attributable to

Stockholders of the Company $ 4,141,047 19 2,447,690 15

Minority interests 248,462 1 188,948 1

$ 4,389,509 20 2,636,638 16

Before

Income tax

After

Income tax

Before

Income tax

After

Income tax

Earnings per share attributable to parent company

(NT dollars) (Notes (2) and (4)(u))

$7.28

5.11

4.84

3.35

(English Translation of Financial Report Originally Issued in Chinese)

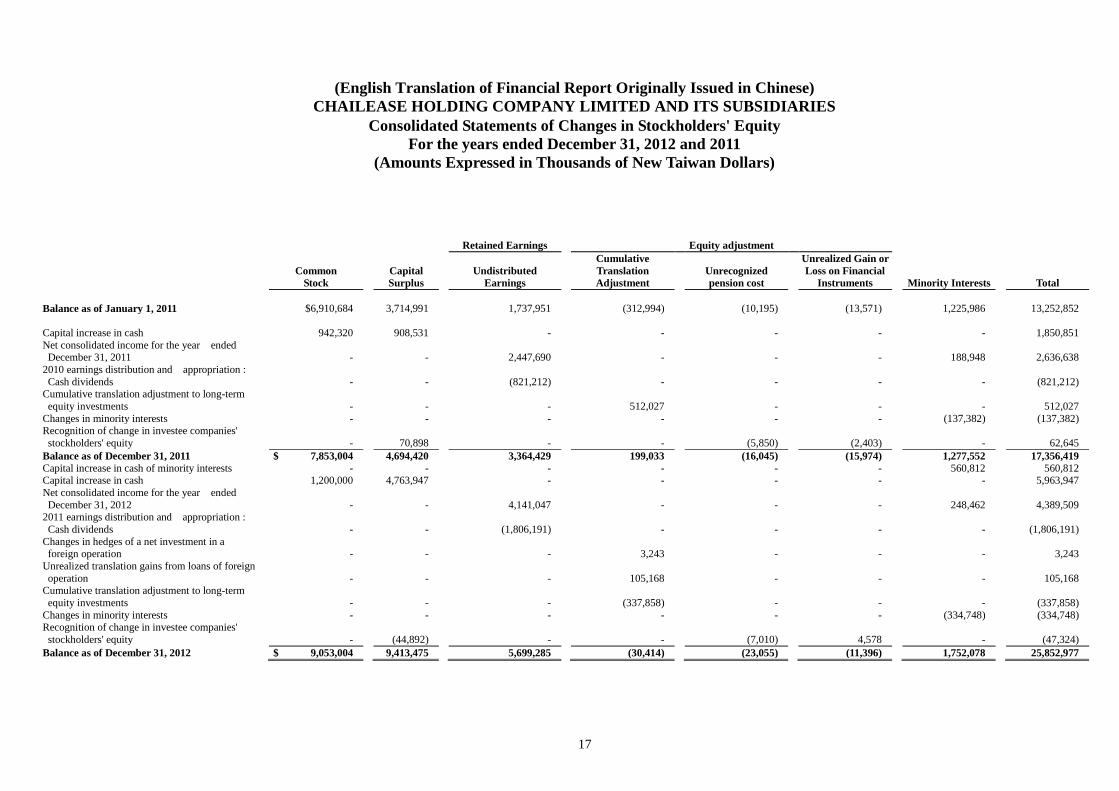

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Statements of Changes in Stockholders' Equity

For the years ended December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars)

17

Retained Earnings Equity adjustment

Common

Stock

Capital

Surplus

Undistributed

Earnings

Cumulative

Translation

Adjustment

Unrecognized

pension cost

Unrealized Gain or

Loss on Financial

Instruments Minority Interests Total

Balance as of January 1, 2011 $6,910,684 3,714,991 1,737,951 (312,994) (10,195) (13,571) 1,225,986 13,252,852

Capital increase in cash

942,320 908,531 - - - - - 1,850,851

Net consolidated income for the year ended December 31, 2011

- - 2,447,690 - - - 188,948 2,636,638

2010 earnings distribution and appropriation :

Cash dividends

- - (821,212) - - - - (821,212) Cumulative translation adjustment to long-term

equity investments

- - - 512,027 - - - 512,027

Changes in minority interests - - - - - - (137,382) (137,382) Recognition of change in investee companies'

stockholders' equity

- 70,898 - - (5,850) (2,403) - 62,645

Balance as of December 31, 2011 $ 7,853,004 4,694,420 3,364,429 199,033 (16,045) (15,974) 1,277,552 17,356,419

Capital increase in cash of minority interests - - - - - - 560,812 560,812 Capital increase in cash 1,200,000 4,763,947 - - - - - 5,963,947

Net consolidated income for the year ended

December 31, 2012

- - 4,141,047 - - - 248,462 4,389,509 2011 earnings distribution and appropriation :

Cash dividends

- - (1,806,191) - - - - (1,806,191)

Changes in hedges of a net investment in a foreign operation

- - - 3,243 - - - 3,243

Unrealized translation gains from loans of foreign

operation

- - - 105,168 - - - 105,168 Cumulative translation adjustment to long-term

equity investments

- - - (337,858) - - - (337,858)

Changes in minority interests - - - - - - (334,748) (334,748) Recognition of change in investee companies'

stockholders' equity

- (44,892) - - (7,010) 4,578 - (47,324)

Balance as of December 31, 2012 $ 9,053,004 9,413,475 5,699,285 (30,414) (23,055) (11,396) 1,752,078 25,852,977

(English Translation of Financial Report Originally Issued in Chinese)

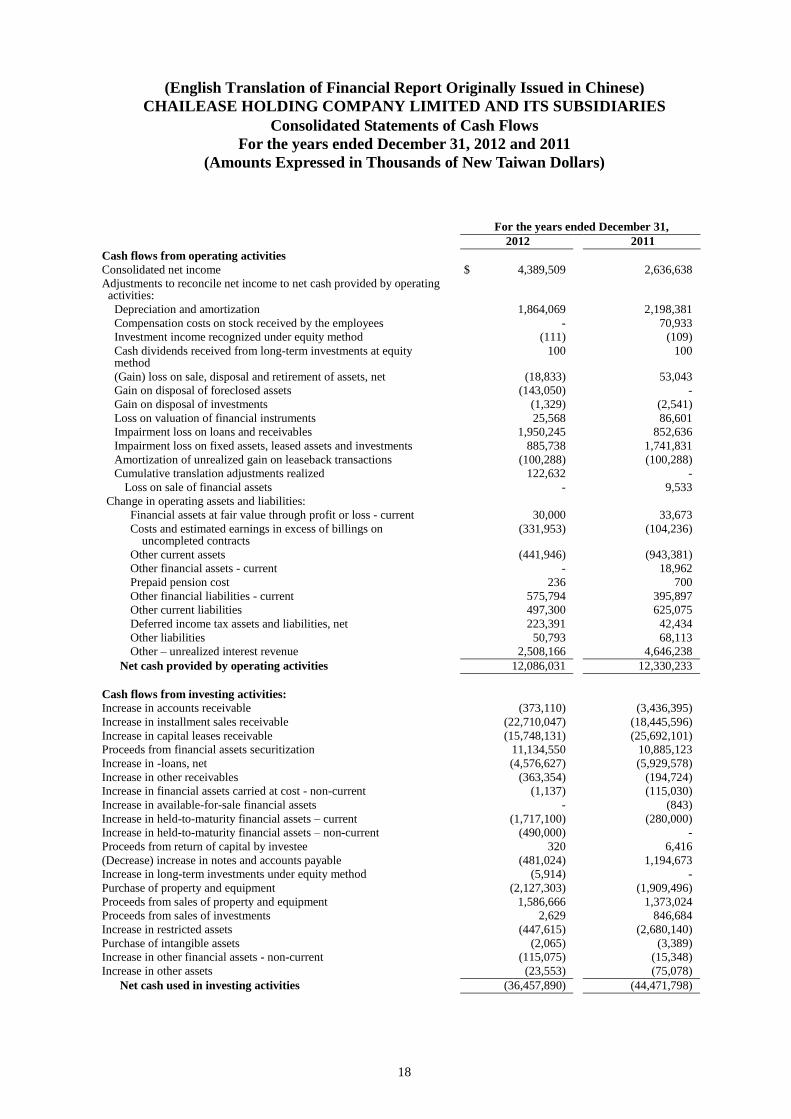

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Statements of Cash Flows

For the years ended December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars)

18

For the years ended December 31,

2012 2011

Cash flows from operating activities

Consolidated net income $ 4,389,509 2,636,638

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation and amortization 1,864,069 2,198,381

Compensation costs on stock received by the employees - 70,933

Investment income recognized under equity method (111) (109)

Cash dividends received from long-term investments at equity method

100 100

(Gain) loss on sale, disposal and retirement of assets, net (18,833) 53,043

Gain on disposal of foreclosed assets (143,050) -

Gain on disposal of investments (1,329) (2,541)

Loss on valuation of financial instruments 25,568 86,601

Impairment loss on loans and receivables 1,950,245 852,636

Impairment loss on fixed assets, leased assets and investments 885,738 1,741,831

Amortization of unrealized gain on leaseback transactions (100,288) (100,288)

Cumulative translation adjustments realized 122,632 -

Loss on sale of financial assets - 9,533

Change in operating assets and liabilities:

Financial assets at fair value through profit or loss - current 30,000 33,673

Costs and estimated earnings in excess of billings on uncompleted contracts

(331,953) (104,236)

Other current assets (441,946) (943,381)

Other financial assets - current - 18,962

Prepaid pension cost 236 700

Other financial liabilities - current 575,794 395,897

Other current liabilities 497,300 625,075

Deferred income tax assets and liabilities, net 223,391 42,434

Other liabilities 50,793 68,113

Other – unrealized interest revenue 2,508,166 4,646,238

Net cash provided by operating activities 12,086,031 12,330,233

Cash flows from investing activities:

Increase in accounts receivable (373,110) (3,436,395)

Increase in installment sales receivable (22,710,047) (18,445,596)

Increase in capital leases receivable (15,748,131) (25,692,101)

Proceeds from financial assets securitization 11,134,550 10,885,123

Increase in -loans, net (4,576,627) (5,929,578)

Increase in other receivables (363,354) (194,724)

Increase in financial assets carried at cost - non-current (1,137) (115,030)

Increase in available-for-sale financial assets - (843)

Increase in held-to-maturity financial assets – current (1,717,100) (280,000)

Increase in held-to-maturity financial assets – non-current (490,000) -

Proceeds from return of capital by investee 320 6,416

(Decrease) increase in notes and accounts payable (481,024) 1,194,673

Increase in long-term investments under equity method (5,914) -

Purchase of property and equipment (2,127,303) (1,909,496)

Proceeds from sales of property and equipment 1,586,666 1,373,024

Proceeds from sales of investments 2,629 846,684

Increase in restricted assets (447,615) (2,680,140)

Purchase of intangible assets (2,065) (3,389)

Increase in other financial assets - non-current (115,075) (15,348)

Increase in other assets (23,553) (75,078)

Net cash used in investing activities (36,457,890) (44,471,798)

(English Translation of Financial Report Originally Issued in Chinese)

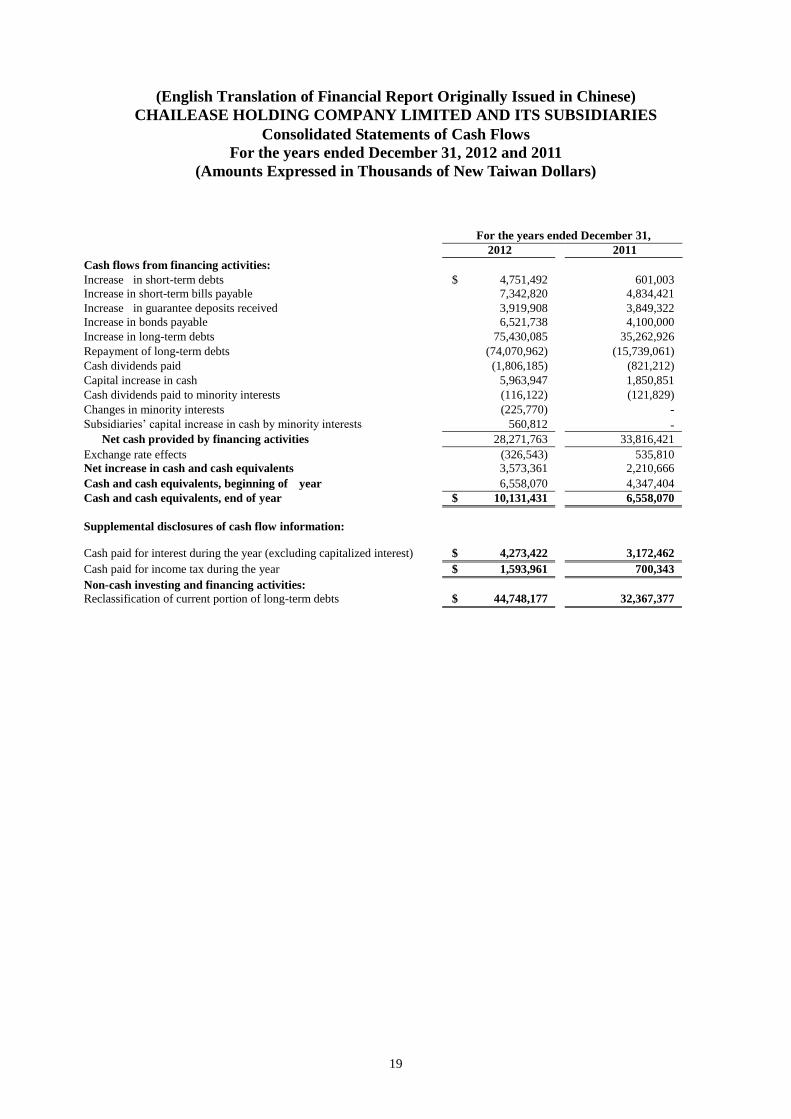

CHAILEASE HOLDING COMPANY LIMITED AND ITS SUBSIDIARIES

Consolidated Statements of Cash Flows

For the years ended December 31, 2012 and 2011

(Amounts Expressed in Thousands of New Taiwan Dollars)

19

For the years ended December 31,

2012 2011

Cash flows from financing activities:

Increase in short-term debts $ 4,751,492 601,003

Increase in short-term bills payable 7,342,820 4,834,421

Increase in guarantee deposits received 3,919,908 3,849,322

Increase in bonds payable 6,521,738 4,100,000

Increase in long-term debts 75,430,085 35,262,926

Repayment of long-term debts (74,070,962) (15,739,061)

Cash dividends paid (1,806,185) (821,212)

Capital increase in cash 5,963,947 1,850,851

Cash dividends paid to minority interests (116,122) (121,829)

Changes in minority interests (225,770) -

Subsidiaries’ capital increase in cash by minority interests 560,812 -

Net cash provided by financing activities 28,271,763 33,816,421

Exchange rate effects (326,543) 535,810

Net increase in cash and cash equivalents 3,573,361 2,210,666

Cash and cash equivalents, beginning of year 6,558,070 4,347,404

Cash and cash equivalents, end of year $ 10,131,431 6,558,070

Supplemental disclosures of cash flow information:

Cash paid for interest during the year (excluding capitalized interest)

$ 4,273,422

3,172,462

Cash paid for income tax during the year $ 1,593,961 700,343

Non-cash investing and financing activities:

Reclassification of current portion of long-term debts $ 44,748,177 32,367,377

20

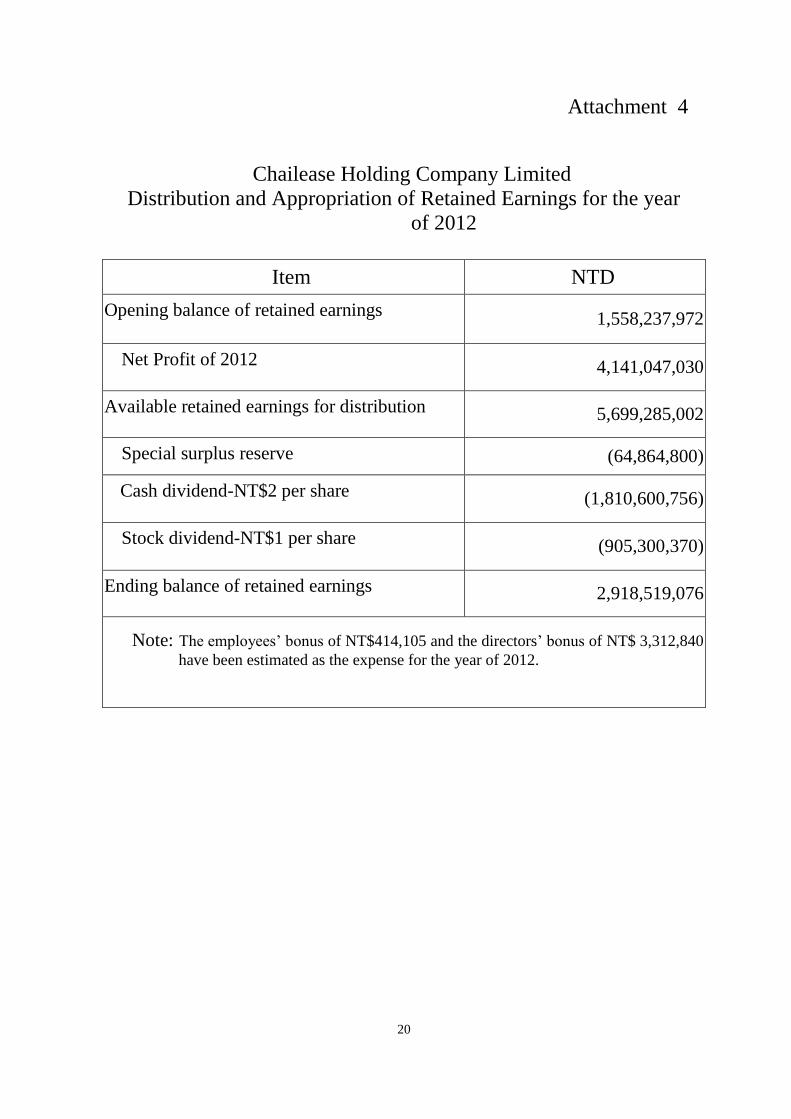

Attachment 4

Chailease Holding Company Limited

Distribution and Appropriation of Retained Earnings for the year

of 2012

Item NTD

Opening balance of retained earnings 1,558,237,972

Net Profit of 2012 4,141,047,030

Available retained earnings for distribution 5,699,285,002

Special surplus reserve (64,864,800)

Cash dividend-NT$2 per share (1,810,600,756)

Stock dividend-NT$1 per share (905,300,370)

Ending balance of retained earnings 2,918,519,076

Note: The employees’ bonus of NT$414,105 and the directors’ bonus of NT$ 3,312,840

have been estimated as the expense for the year of 2012.

21

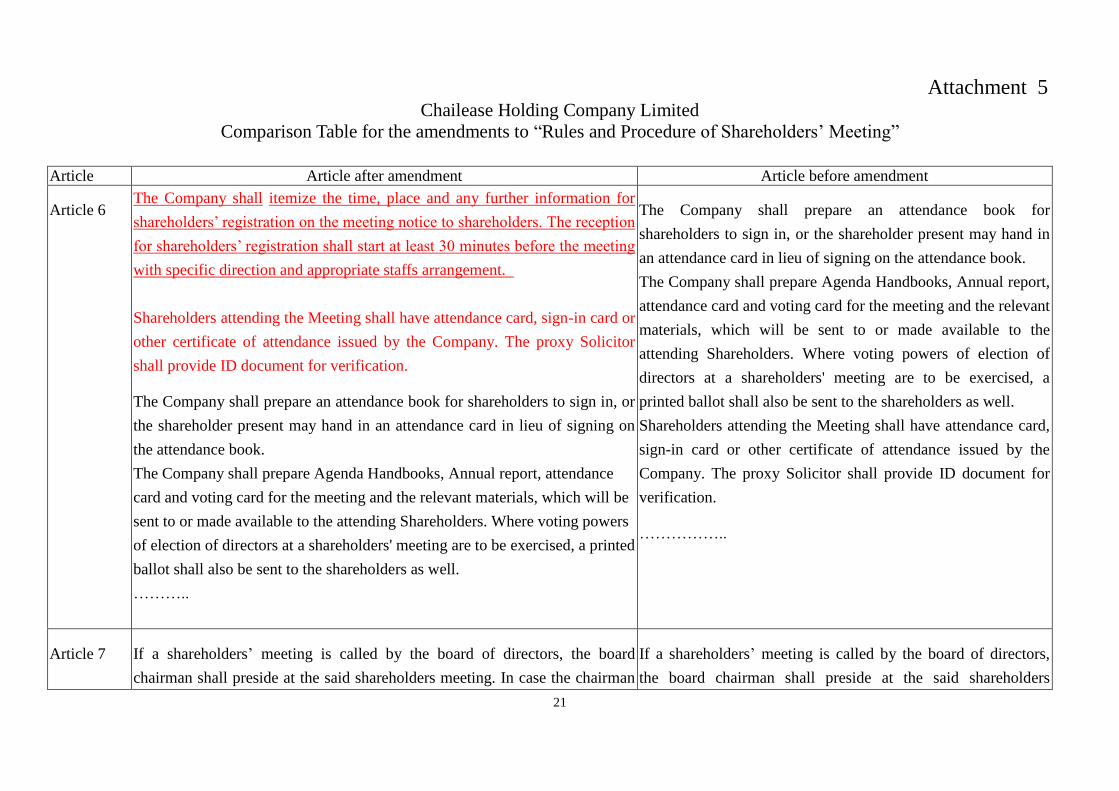

Attachment 5 Chailease Holding Company Limited

Comparison Table for the amendments to “Rules and Procedure of Shareholders’ Meeting”

Article Article after amendment Article before amendment

Article 6

The Company shall itemize the time, place and any further information for

shareholders’ registration on the meeting notice to shareholders. The reception

for shareholders’ registration shall start at least 30 minutes before the meeting

with specific direction and appropriate staffs arrangement.

Shareholders attending the Meeting shall have attendance card, sign-in card or

other certificate of attendance issued by the Company. The proxy Solicitor

shall provide ID document for verification.

The Company shall prepare an attendance book for shareholders to sign in, or

the shareholder present may hand in an attendance card in lieu of signing on

the attendance book.

The Company shall prepare Agenda Handbooks, Annual report, attendance

card and voting card for the meeting and the relevant materials, which will be

sent to or made available to the attending Shareholders. Where voting powers

of election of directors at a shareholders' meeting are to be exercised, a printed

ballot shall also be sent to the shareholders as well.

………..

The Company shall prepare an attendance book for

shareholders to sign in, or the shareholder present may hand in

an attendance card in lieu of signing on the attendance book.

The Company shall prepare Agenda Handbooks, Annual report,

attendance card and voting card for the meeting and the relevant

materials, which will be sent to or made available to the

attending Shareholders. Where voting powers of election of

directors at a shareholders' meeting are to be exercised, a

printed ballot shall also be sent to the shareholders as well.

Shareholders attending the Meeting shall have attendance card,

sign-in card or other certificate of attendance issued by the

Company. The proxy Solicitor shall provide ID document for

verification.

……………..

Article 7

If a shareholders’ meeting is called by the board of directors, the board

chairman shall preside at the said shareholders meeting. In case the chairman

If a shareholders’ meeting is called by the board of directors,

the board chairman shall preside at the said shareholders

22

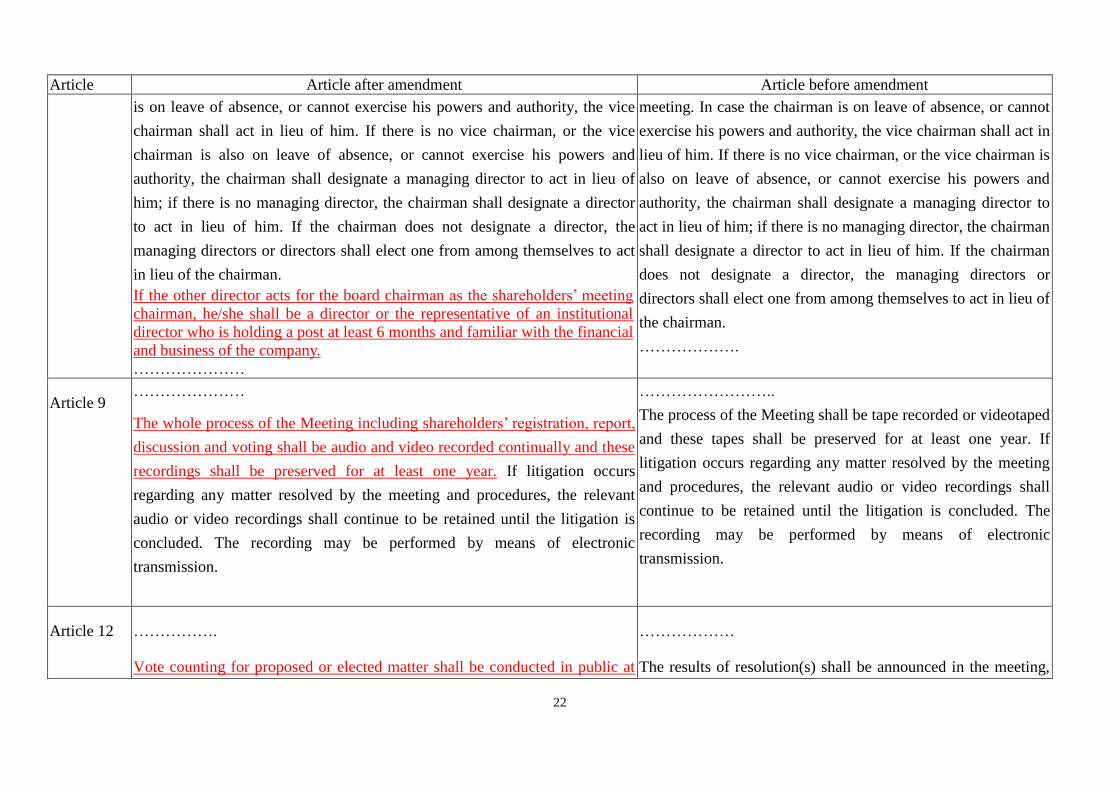

Article Article after amendment Article before amendment

is on leave of absence, or cannot exercise his powers and authority, the vice

chairman shall act in lieu of him. If there is no vice chairman, or the vice

chairman is also on leave of absence, or cannot exercise his powers and

authority, the chairman shall designate a managing director to act in lieu of

him; if there is no managing director, the chairman shall designate a director

to act in lieu of him. If the chairman does not designate a director, the

managing directors or directors shall elect one from among themselves to act

in lieu of the chairman.

If the other director acts for the board chairman as the shareholders’ meeting

chairman, he/she shall be a director or the representative of an institutional

director who is holding a post at least 6 months and familiar with the financial

and business of the company.

…………………

meeting. In case the chairman is on leave of absence, or cannot

exercise his powers and authority, the vice chairman shall act in

lieu of him. If there is no vice chairman, or the vice chairman is

also on leave of absence, or cannot exercise his powers and

authority, the chairman shall designate a managing director to

act in lieu of him; if there is no managing director, the chairman

shall designate a director to act in lieu of him. If the chairman

does not designate a director, the managing directors or

directors shall elect one from among themselves to act in lieu of

the chairman.

……………….

Article 9 …………………

The whole process of the Meeting including shareholders’ registration, report,

discussion and voting shall be audio and video recorded continually and these

recordings shall be preserved for at least one year. If litigation occurs

regarding any matter resolved by the meeting and procedures, the relevant

audio or video recordings shall continue to be retained until the litigation is

concluded. The recording may be performed by means of electronic

transmission.

……………………..

The process of the Meeting shall be tape recorded or videotaped

and these tapes shall be preserved for at least one year. If

litigation occurs regarding any matter resolved by the meeting

and procedures, the relevant audio or video recordings shall

continue to be retained until the litigation is concluded. The

recording may be performed by means of electronic

transmission.

Article 12 …………….

Vote counting for proposed or elected matter shall be conducted in public at

………………

The results of resolution(s) shall be announced in the meeting,

23

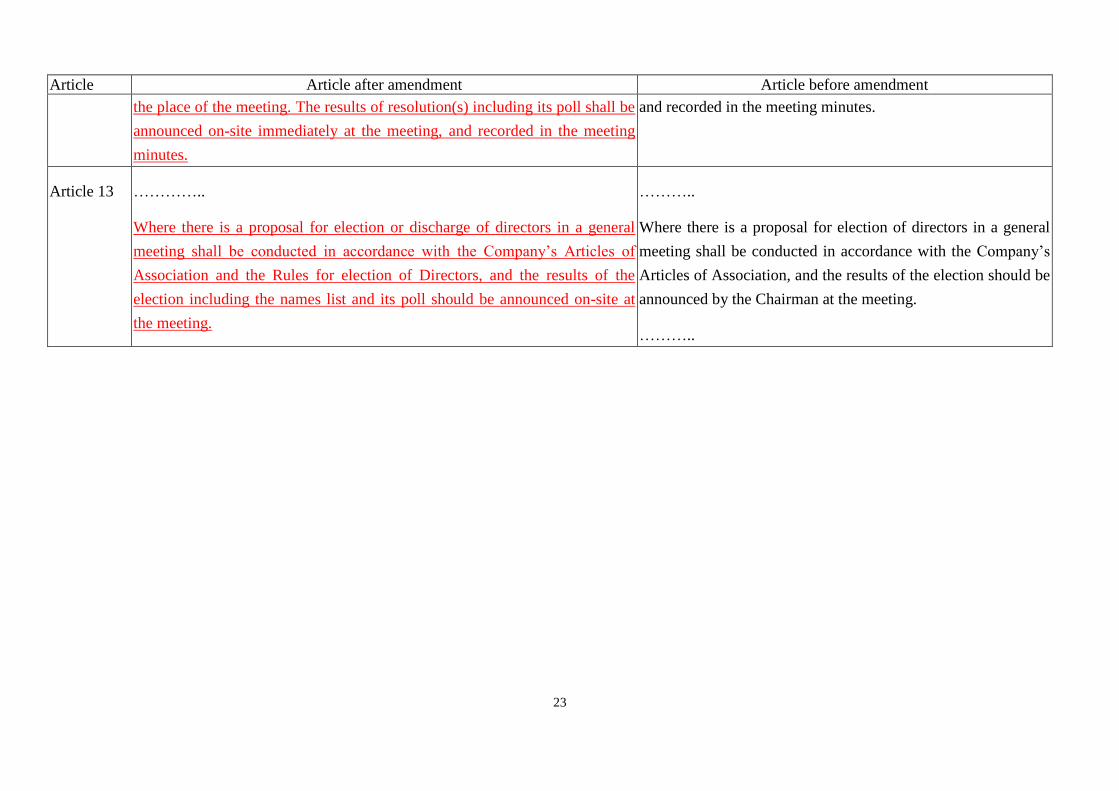

Article Article after amendment Article before amendment

the place of the meeting. The results of resolution(s) including its poll shall be

announced on-site immediately at the meeting, and recorded in the meeting

minutes.

and recorded in the meeting minutes.

Article 13 …………..

Where there is a proposal for election or discharge of directors in a general

meeting shall be conducted in accordance with the Company’s Articles of

Association and the Rules for election of Directors, and the results of the

election including the names list and its poll should be announced on-site at

the meeting.

………..

Where there is a proposal for election of directors in a general

meeting shall be conducted in accordance with the Company’s

Articles of Association, and the results of the election should be

announced by the Chairman at the meeting.

………..

24

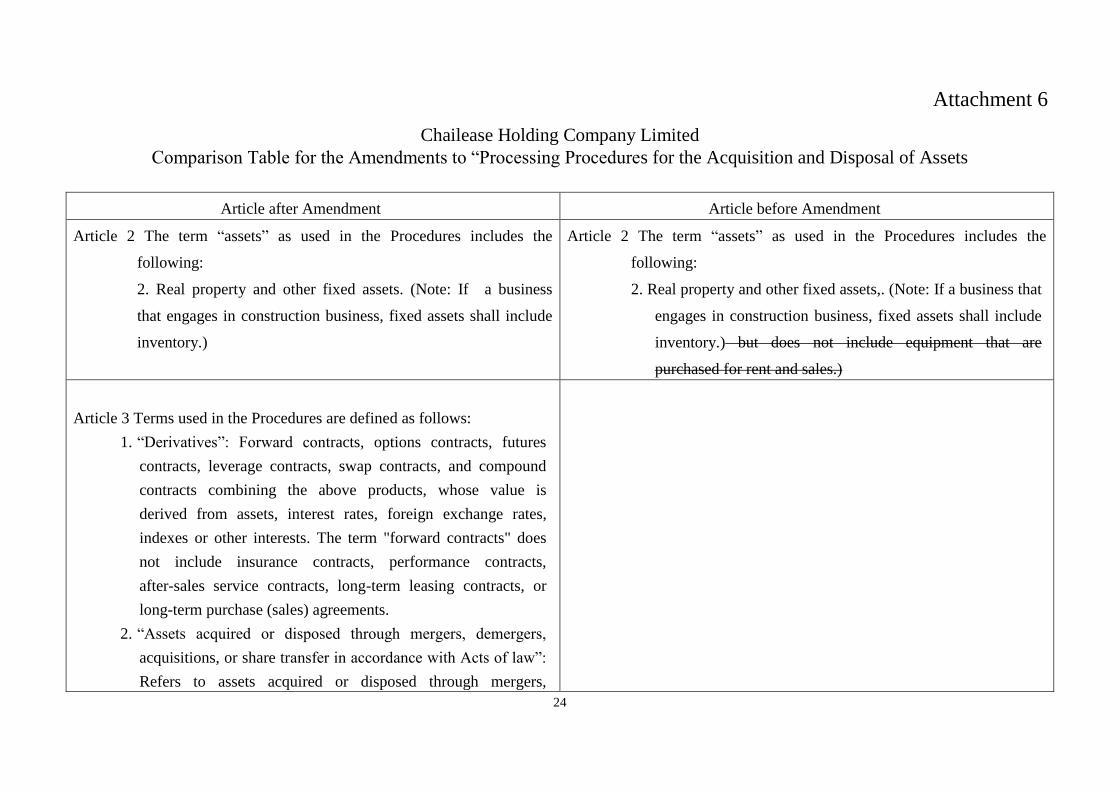

Attachment 6

Chailease Holding Company Limited

Comparison Table for the Amendments to “Processing Procedures for the Acquisition and Disposal of Assets

Article after Amendment Article before Amendment

Article 2 The term “assets” as used in the Procedures includes the

following:

2. Real property and other fixed assets. (Note: If a business

that engages in construction business, fixed assets shall include

inventory.)

Article 2 The term “assets” as used in the Procedures includes the

following:

2. Real property and other fixed assets,. (Note: If a business that

engages in construction business, fixed assets shall include

inventory.) but does not include equipment that are

purchased for rent and sales.)

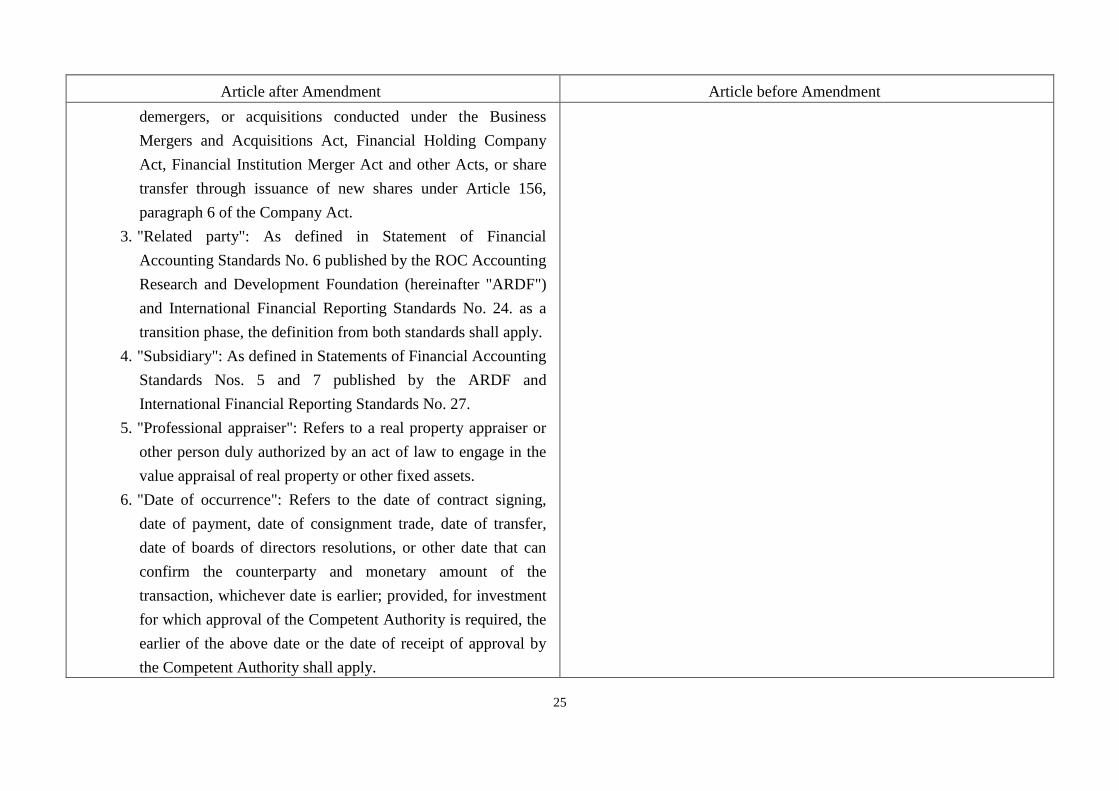

Article 3 Terms used in the Procedures are defined as follows:

1. “Derivatives”: Forward contracts, options contracts, futures

contracts, leverage contracts, swap contracts, and compound

contracts combining the above products, whose value is

derived from assets, interest rates, foreign exchange rates,

indexes or other interests. The term "forward contracts" does

not include insurance contracts, performance contracts,

after-sales service contracts, long-term leasing contracts, or

long-term purchase (sales) agreements.

2. “Assets acquired or disposed through mergers, demergers,

acquisitions, or share transfer in accordance with Acts of law”:

Refers to assets acquired or disposed through mergers,

25

Article after Amendment Article before Amendment

demergers, or acquisitions conducted under the Business

Mergers and Acquisitions Act, Financial Holding Company

Act, Financial Institution Merger Act and other Acts, or share

transfer through issuance of new shares under Article 156,

paragraph 6 of the Company Act.

3. "Related party": As defined in Statement of Financial

Accounting Standards No. 6 published by the ROC Accounting

Research and Development Foundation (hereinafter "ARDF")

and International Financial Reporting Standards No. 24. as a

transition phase, the definition from both standards shall apply.

4. "Subsidiary": As defined in Statements of Financial Accounting

Standards Nos. 5 and 7 published by the ARDF and

International Financial Reporting Standards No. 27.

5. "Professional appraiser": Refers to a real property appraiser or

other person duly authorized by an act of law to engage in the

value appraisal of real property or other fixed assets.

6. "Date of occurrence": Refers to the date of contract signing,

date of payment, date of consignment trade, date of transfer,

date of boards of directors resolutions, or other date that can

confirm the counterparty and monetary amount of the

transaction, whichever date is earlier; provided, for investment

for which approval of the Competent Authority is required, the

earlier of the above date or the date of receipt of approval by

the Competent Authority shall apply.

26

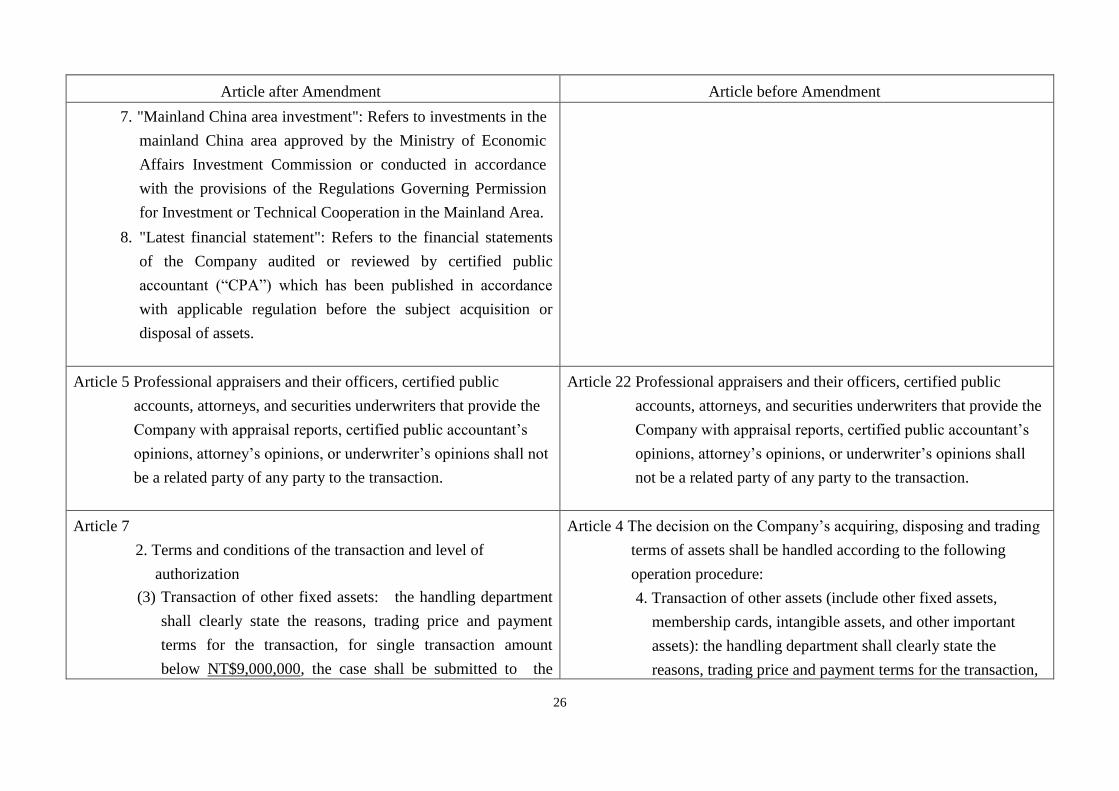

Article after Amendment Article before Amendment

7. "Mainland China area investment": Refers to investments in the

mainland China area approved by the Ministry of Economic

Affairs Investment Commission or conducted in accordance

with the provisions of the Regulations Governing Permission

for Investment or Technical Cooperation in the Mainland Area.

8. "Latest financial statement": Refers to the financial statements

of the Company audited or reviewed by certified public

accountant (“CPA”) which has been published in accordance

with applicable regulation before the subject acquisition or

disposal of assets.

Article 5 Professional appraisers and their officers, certified public

accounts, attorneys, and securities underwriters that provide the

Company with appraisal reports, certified public accountant’s

opinions, attorney’s opinions, or underwriter’s opinions shall not

be a related party of any party to the transaction.

Article 22 Professional appraisers and their officers, certified public

accounts, attorneys, and securities underwriters that provide the

Company with appraisal reports, certified public accountant’s

opinions, attorney’s opinions, or underwriter’s opinions shall

not be a related party of any party to the transaction.

Article 7

2. Terms and conditions of the transaction and level of

authorization

(3) Transaction of other fixed assets: the handling department

shall clearly state the reasons, trading price and payment

terms for the transaction, for single transaction amount

below NT$9,000,000, the case shall be submitted to the

Article 4 The decision on the Company’s acquiring, disposing and trading

terms of assets shall be handled according to the following

operation procedure:

4. Transaction of other assets (include other fixed assets,

membership cards, intangible assets, and other important

assets): the handling department shall clearly state the

reasons, trading price and payment terms for the transaction,

27

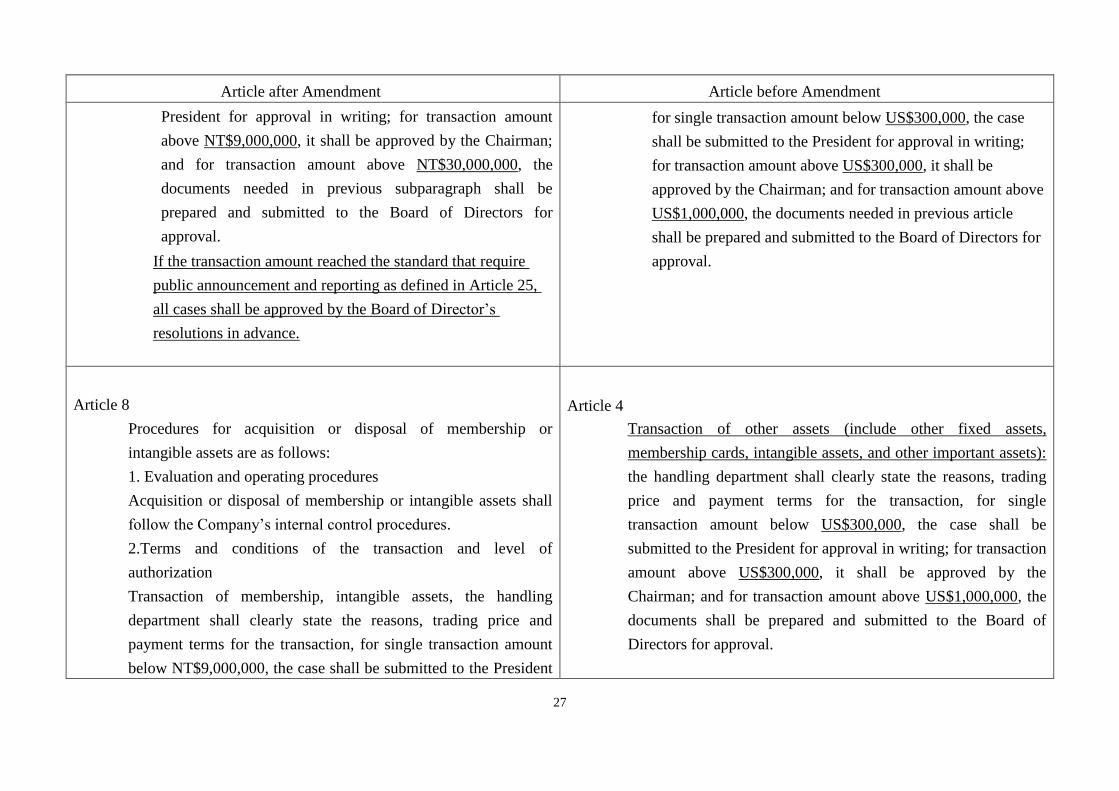

Article after Amendment Article before Amendment

President for approval in writing; for transaction amount

above NT$9,000,000, it shall be approved by the Chairman;

and for transaction amount above NT$30,000,000, the

documents needed in previous subparagraph shall be

prepared and submitted to the Board of Directors for

approval.

If the transaction amount reached the standard that require

public announcement and reporting as defined in Article 25,

all cases shall be approved by the Board of Director’s

resolutions in advance.

for single transaction amount below US$300,000, the case

shall be submitted to the President for approval in writing;

for transaction amount above US$300,000, it shall be

approved by the Chairman; and for transaction amount above

US$1,000,000, the documents needed in previous article

shall be prepared and submitted to the Board of Directors for

approval.

Article 8

Procedures for acquisition or disposal of membership or

intangible assets are as follows:

1. Evaluation and operating procedures

Acquisition or disposal of membership or intangible assets shall

follow the Company’s internal control procedures.

2.Terms and conditions of the transaction and level of

authorization

Transaction of membership, intangible assets, the handling

department shall clearly state the reasons, trading price and

payment terms for the transaction, for single transaction amount

below NT$9,000,000, the case shall be submitted to the President

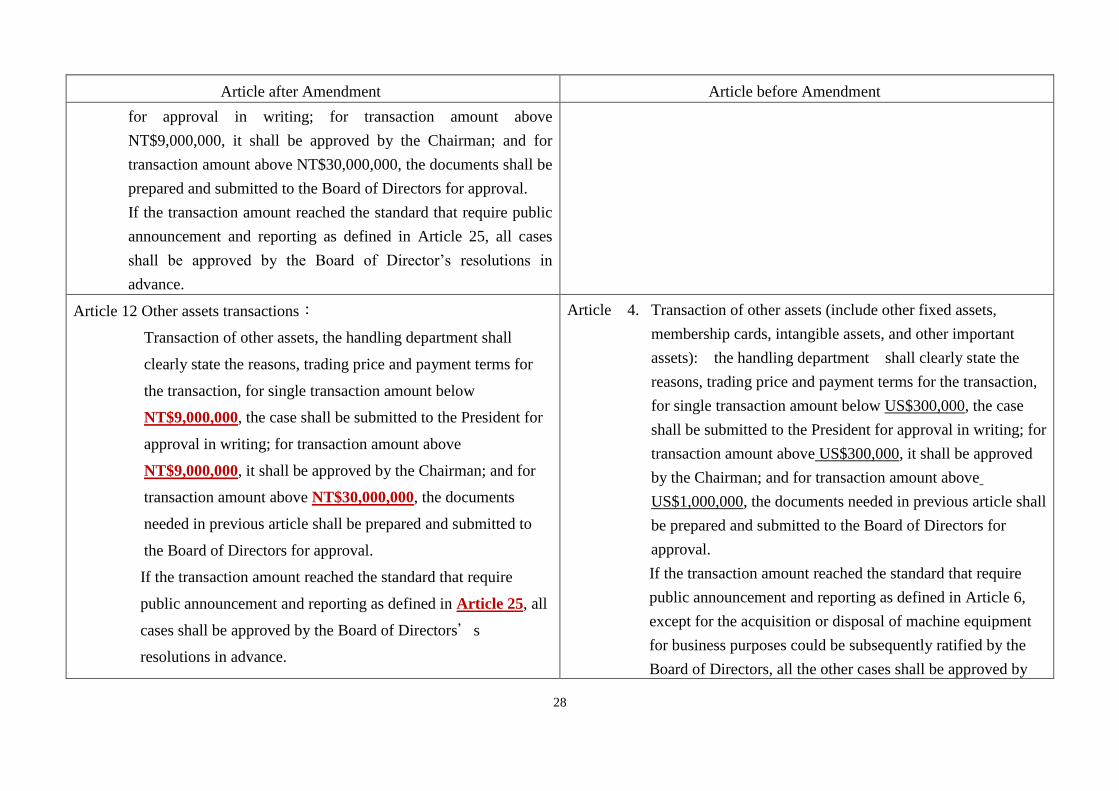

Article 4

Transaction of other assets (include other fixed assets,

membership cards, intangible assets, and other important assets):

the handling department shall clearly state the reasons, trading

price and payment terms for the transaction, for single

transaction amount below US$300,000, the case shall be

submitted to the President for approval in writing; for transaction

amount above US$300,000, it shall be approved by the

Chairman; and for transaction amount above US$1,000,000, the

documents shall be prepared and submitted to the Board of

Directors for approval.

28

Article after Amendment Article before Amendment

for approval in writing; for transaction amount above

NT$9,000,000, it shall be approved by the Chairman; and for

transaction amount above NT$30,000,000, the documents shall be

prepared and submitted to the Board of Directors for approval.

If the transaction amount reached the standard that require public

announcement and reporting as defined in Article 25, all cases

shall be approved by the Board of Director’s resolutions in

advance.

Article 12 Other assets transactions:

Transaction of other assets, the handling department shall

clearly state the reasons, trading price and payment terms for

the transaction, for single transaction amount below

NT$9,000,000, the case shall be submitted to the President for

approval in writing; for transaction amount above

NT$9,000,000, it shall be approved by the Chairman; and for

transaction amount above NT$30,000,000, the documents

needed in previous article shall be prepared and submitted to

the Board of Directors for approval.

If the transaction amount reached the standard that require

public announcement and reporting as defined in Article 25, all

cases shall be approved by the Board of Directors’s

resolutions in advance.

Article 4. Transaction of other assets (include other fixed assets,

membership cards, intangible assets, and other important

assets): the handling department shall clearly state the

reasons, trading price and payment terms for the transaction,

for single transaction amount below US$300,000, the case

shall be submitted to the President for approval in writing; for

transaction amount above US$300,000, it shall be approved

by the Chairman; and for transaction amount above

US$1,000,000, the documents needed in previous article shall

be prepared and submitted to the Board of Directors for

approval.

If the transaction amount reached the standard that require

public announcement and reporting as defined in Article 6,

except for the acquisition or disposal of machine equipment

for business purposes could be subsequently ratified by the

Board of Directors, all the other cases shall be approved by

29

Article after Amendment Article before Amendment

Board of Directors’ resolutions in advance

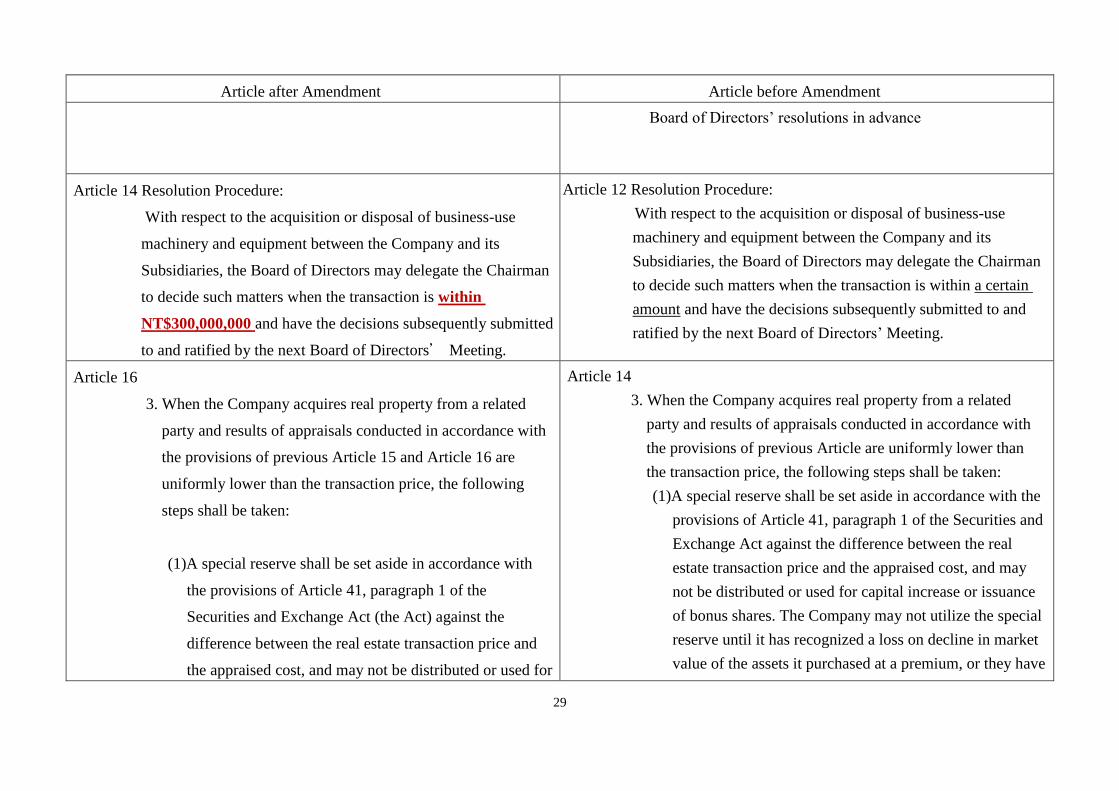

Article 14 Resolution Procedure:

With respect to the acquisition or disposal of business-use

machinery and equipment between the Company and its

Subsidiaries, the Board of Directors may delegate the Chairman

to decide such matters when the transaction is within

NT$300,000,000 and have the decisions subsequently submitted

to and ratified by the next Board of Directors’ Meeting.

Article 12 Resolution Procedure:

With respect to the acquisition or disposal of business-use

machinery and equipment between the Company and its

Subsidiaries, the Board of Directors may delegate the Chairman

to decide such matters when the transaction is within a certain

amount and have the decisions subsequently submitted to and

ratified by the next Board of Directors’ Meeting.

Article 16

3. When the Company acquires real property from a related

party and results of appraisals conducted in accordance with

the provisions of previous Article 15 and Article 16 are

uniformly lower than the transaction price, the following

steps shall be taken:

(1)A special reserve shall be set aside in accordance with

the provisions of Article 41, paragraph 1 of the

Securities and Exchange Act (the Act) against the

difference between the real estate transaction price and

the appraised cost, and may not be distributed or used for

Article 14

3. When the Company acquires real property from a related

party and results of appraisals conducted in accordance with

the provisions of previous Article are uniformly lower than

the transaction price, the following steps shall be taken:

(1)A special reserve shall be set aside in accordance with the

provisions of Article 41, paragraph 1 of the Securities and

Exchange Act against the difference between the real

estate transaction price and the appraised cost, and may

not be distributed or used for capital increase or issuance

of bonus shares. The Company may not utilize the special

reserve until it has recognized a loss on decline in market

value of the assets it purchased at a premium, or they have

30

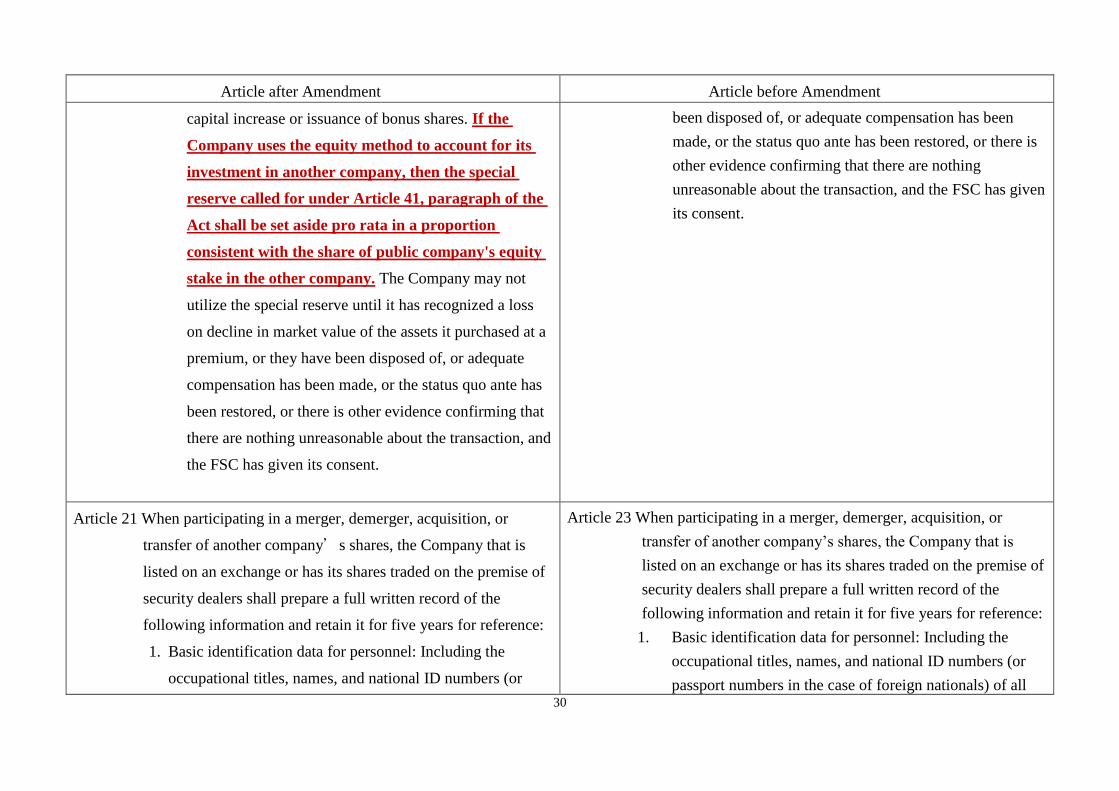

Article after Amendment Article before Amendment

capital increase or issuance of bonus shares. If the

Company uses the equity method to account for its

investment in another company, then the special

reserve called for under Article 41, paragraph of the

Act shall be set aside pro rata in a proportion

consistent with the share of public company's equity

stake in the other company. The Company may not

utilize the special reserve until it has recognized a loss

on decline in market value of the assets it purchased at a

premium, or they have been disposed of, or adequate

compensation has been made, or the status quo ante has

been restored, or there is other evidence confirming that

there are nothing unreasonable about the transaction, and

the FSC has given its consent.

been disposed of, or adequate compensation has been

made, or the status quo ante has been restored, or there is

other evidence confirming that there are nothing

unreasonable about the transaction, and the FSC has given

its consent.

Article 21 When participating in a merger, demerger, acquisition, or

transfer of another company’s shares, the Company that is

listed on an exchange or has its shares traded on the premise of

security dealers shall prepare a full written record of the

following information and retain it for five years for reference:

1. Basic identification data for personnel: Including the

occupational titles, names, and national ID numbers (or

Article 23 When participating in a merger, demerger, acquisition, or

transfer of another company’s shares, the Company that is

listed on an exchange or has its shares traded on the premise of

security dealers shall prepare a full written record of the

following information and retain it for five years for reference:

1. Basic identification data for personnel: Including the

occupational titles, names, and national ID numbers (or

passport numbers in the case of foreign nationals) of all

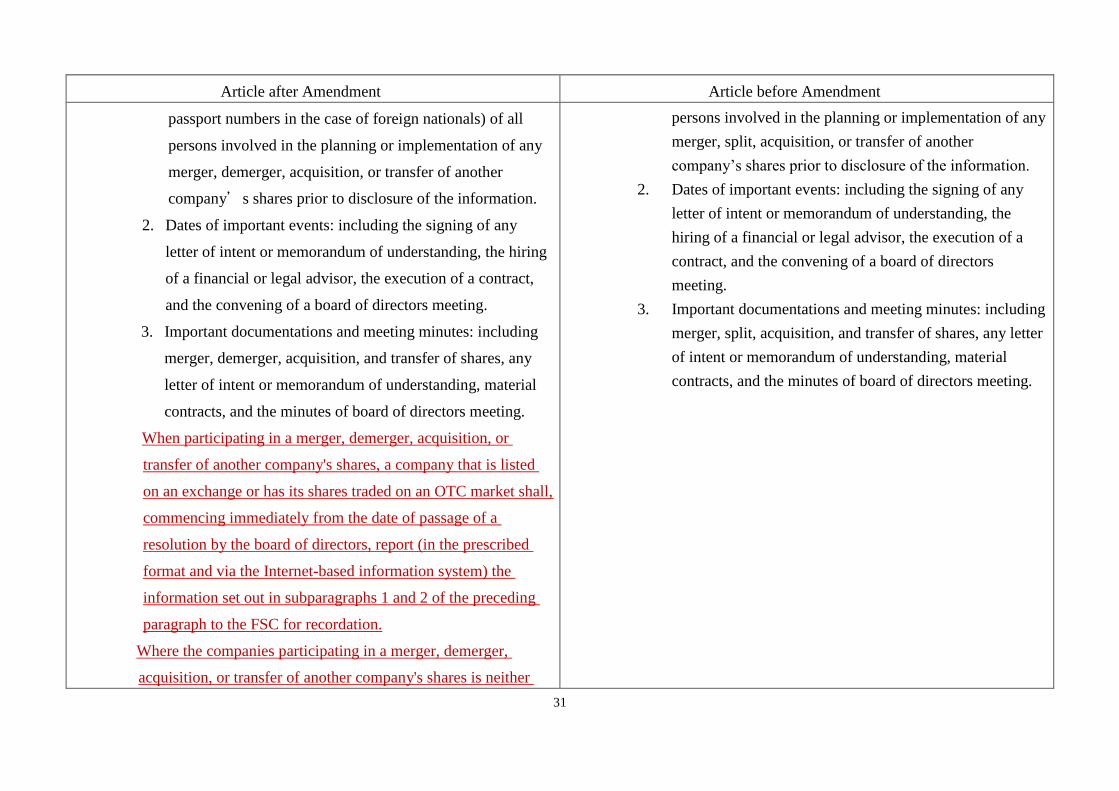

31

Article after Amendment Article before Amendment

passport numbers in the case of foreign nationals) of all

persons involved in the planning or implementation of any

merger, demerger, acquisition, or transfer of another

company’s shares prior to disclosure of the information.

2. Dates of important events: including the signing of any

letter of intent or memorandum of understanding, the hiring

of a financial or legal advisor, the execution of a contract,

and the convening of a board of directors meeting.

3. Important documentations and meeting minutes: including

merger, demerger, acquisition, and transfer of shares, any

letter of intent or memorandum of understanding, material

contracts, and the minutes of board of directors meeting.

When participating in a merger, demerger, acquisition, or

transfer of another company's shares, a company that is listed

on an exchange or has its shares traded on an OTC market shall,

commencing immediately from the date of passage of a

resolution by the board of directors, report (in the prescribed

format and via the Internet-based information system) the

information set out in subparagraphs 1 and 2 of the preceding

paragraph to the FSC for recordation.

Where the companies participating in a merger, demerger,

acquisition, or transfer of another company's shares is neither

persons involved in the planning or implementation of any

merger, split, acquisition, or transfer of another

company’s shares prior to disclosure of the information.

2. Dates of important events: including the signing of any

letter of intent or memorandum of understanding, the

hiring of a financial or legal advisor, the execution of a

contract, and the convening of a board of directors

meeting.

3. Important documentations and meeting minutes: including

merger, split, acquisition, and transfer of shares, any letter

of intent or memorandum of understanding, material

contracts, and the minutes of board of directors meeting.

32

Article after Amendment Article before Amendment

listed on an exchange nor has its shares traded on an OTC

market, the company(s) so listed or traded shall sign an

agreement with such company whereby the latter is required to

abide by the Article 20 and the provisions of paragraphs 1 and 2.

Article 25 Public announcement and reporting procedure:

1. Under any of following circumstances, the in-charging

department shall publicly announce and relevant information

on FSC’s designated website in the appropriate format as

prescribed by regulations on the day of the occurrence of the

fact:

(1). Acquisition or disposal of real property from or to a

related party, or acquisition or disposal of assets other

than real property from or to a related party where the

transaction amount reaches 20 percent or more of paid-in

capital, 10 percent or more of the company's total assets,

or NT$300 million or more; provided, this shall not apply

to trading of government bonds or bonds under

repurchase and resale agreements.

(2). Merger, demerger, acquisition, or transfer of shares.

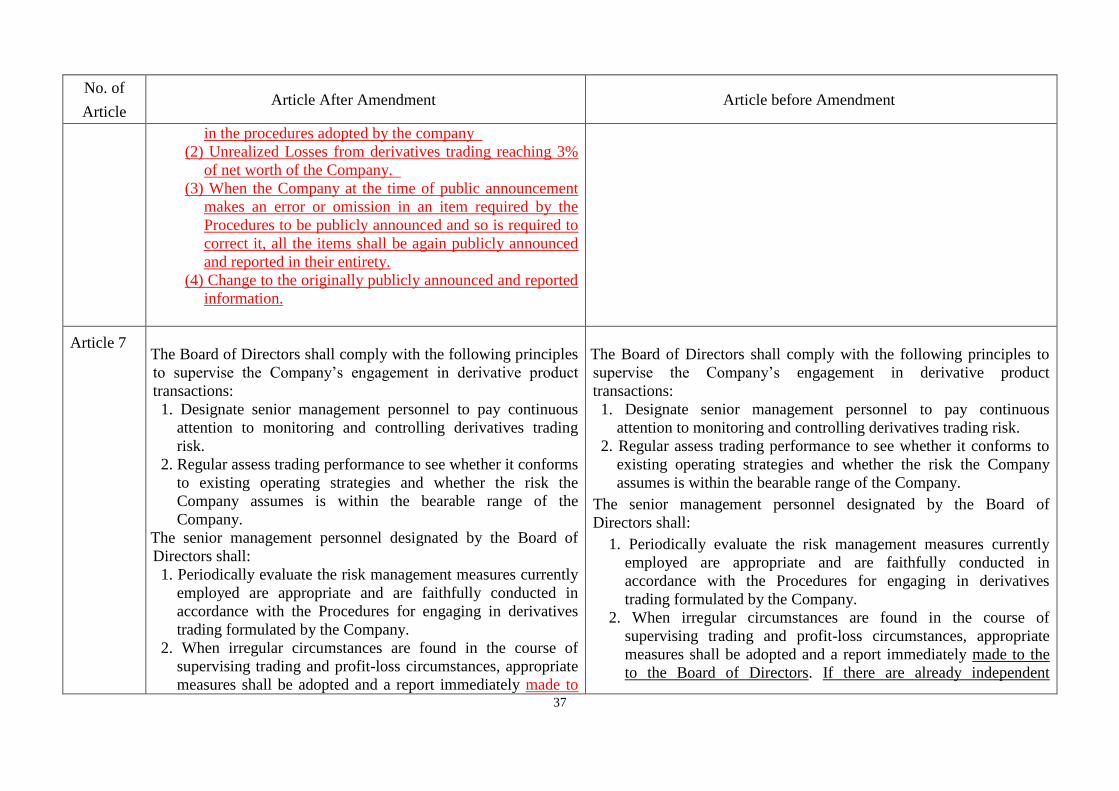

(3).Losses from derivatives trading reaching the limits on

aggregate losses or losses on individual contracts set out

in the procedures adopted by the company.

Article 6 Public announcement and reporting procedure:

1. Under any of following circumstances, the in-charging

department shall publicly announce and relevant information

on FSC’s designated website in the appropriate format as

prescribed by regulations on the day of the occurrence of the

fact:

(1) Acquisition or disposal of assets from related party where

the transaction amount reaches 20% or more of the

Company’s paid-in capital, 10% or more of the Company’s

total assets, or NT$ 300,000,000, provided, this shall not

apply to trading of government bonds or bonds under

repurchase and resale agreements.

(2) Conduct merger, split, acquisition or transfer of shares.

(3) Engage in derivative product transactions and the loss from

the engagement has reached loss ceiling for the full or

individual contract defined in “Handling Procedure for

derivative product transaction”.

(4) Engage in investment in mainland China and Asset

transaction except the four items indicated above, when

(a)single transaction amount

33

Article after Amendment Article before Amendment

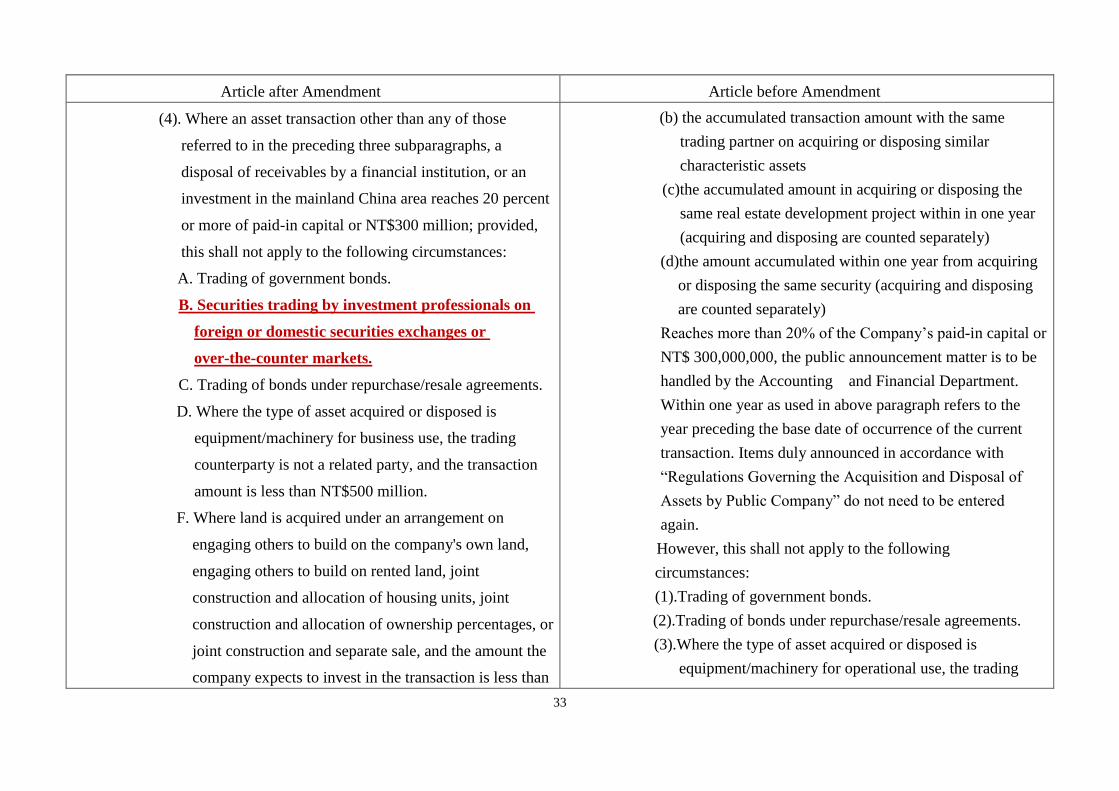

(4). Where an asset transaction other than any of those

referred to in the preceding three subparagraphs, a

disposal of receivables by a financial institution, or an

investment in the mainland China area reaches 20 percent

or more of paid-in capital or NT$300 million; provided,

this shall not apply to the following circumstances:

A. Trading of government bonds.

B. Securities trading by investment professionals on

foreign or domestic securities exchanges or

over-the-counter markets.

C. Trading of bonds under repurchase/resale agreements.

D. Where the type of asset acquired or disposed is

equipment/machinery for business use, the trading

counterparty is not a related party, and the transaction

amount is less than NT$500 million.

F. Where land is acquired under an arrangement on

engaging others to build on the company's own land,

engaging others to build on rented land, joint

construction and allocation of housing units, joint

construction and allocation of ownership percentages, or

joint construction and separate sale, and the amount the

company expects to invest in the transaction is less than

(b) the accumulated transaction amount with the same

trading partner on acquiring or disposing similar

characteristic assets

(c)the accumulated amount in acquiring or disposing the

same real estate development project within in one year

(acquiring and disposing are counted separately)

(d)the amount accumulated within one year from acquiring

or disposing the same security (acquiring and disposing

are counted separately)

Reaches more than 20% of the Company’s paid-in capital or

NT$ 300,000,000, the public announcement matter is to be

handled by the Accounting and Financial Department.

Within one year as used in above paragraph refers to the

year preceding the base date of occurrence of the current

transaction. Items duly announced in accordance with

“Regulations Governing the Acquisition and Disposal of

Assets by Public Company” do not need to be entered

again.

However, this shall not apply to the following

circumstances:

(1).Trading of government bonds.

(2).Trading of bonds under repurchase/resale agreements.

(3).Where the type of asset acquired or disposed is

equipment/machinery for operational use, the trading

34

Article after Amendment Article before Amendment

NT$500 million. counterparty is not a related party, and the transaction

amount is less than NT$ 500,000,000.

(4).Where land is acquired under an arrangement for

commissioned construction on self-owned land or

commissioned construction on rented land, joint

construction and allocation of housing units, joint

construction and allocation of ownership percentages, or

join construction and separate sale, and the amount the

company expects to invest in the transaction is less than

NT$ 500,000,000.

Article 29

With respect to the Company's acquisition or disposal of assets

that is subject to the approval of the Board of Directors under

the Procedures or other laws or regulations, the transaction shall

be approved by more than half of all Audit Committee Members

and submitted to the Board of Directors for a resolution.

If approval of more than half of all audit committee members as

required in the preceding paragraph is not obtained, the

transaction may be implemented if approved by more than

two-thirds of all directors, and the resolution of the Audit

Committee shall be recorded in the Minutes of the Board of

Directors’ Meeting.

35

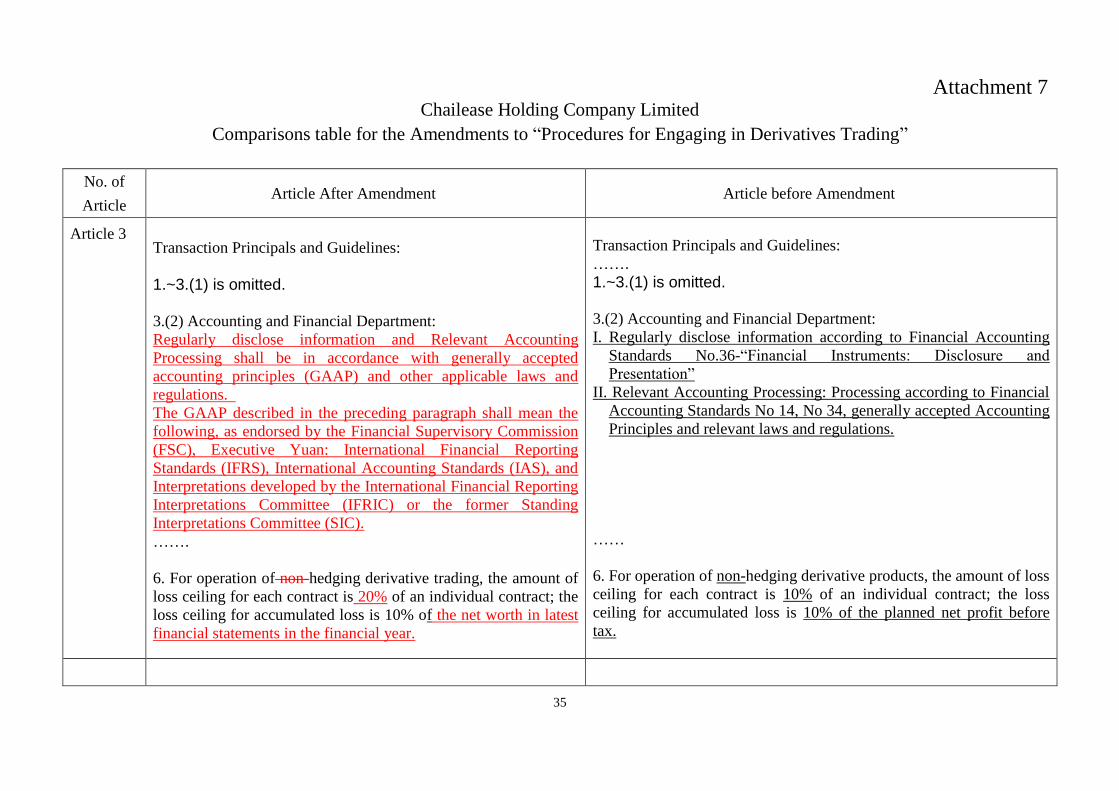

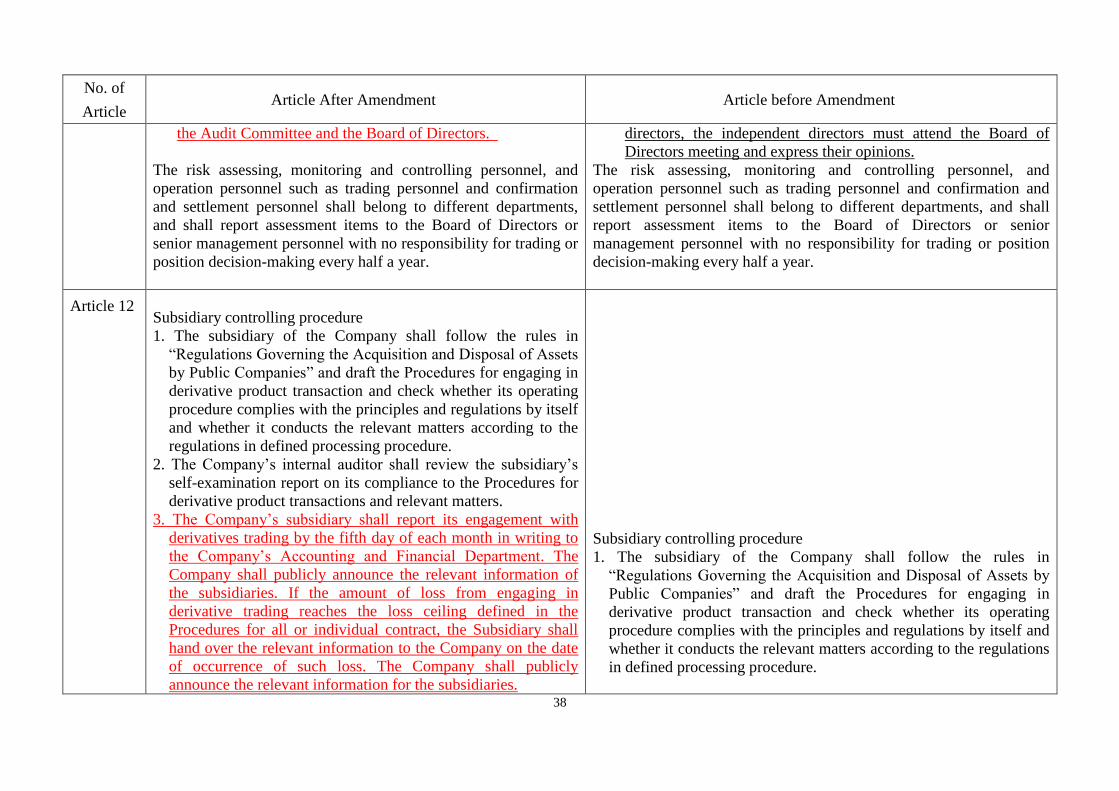

Attachment 7 Chailease Holding Company Limited

Comparisons table for the Amendments to “Procedures for Engaging in Derivatives Trading”

No. of

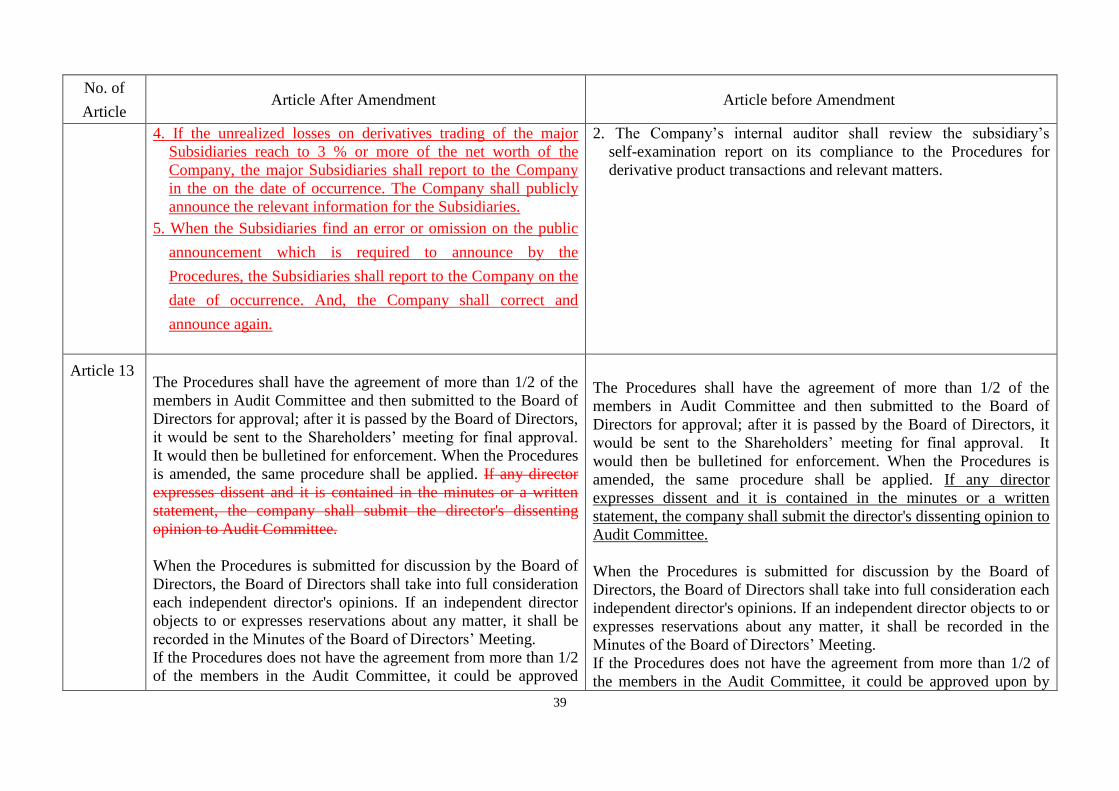

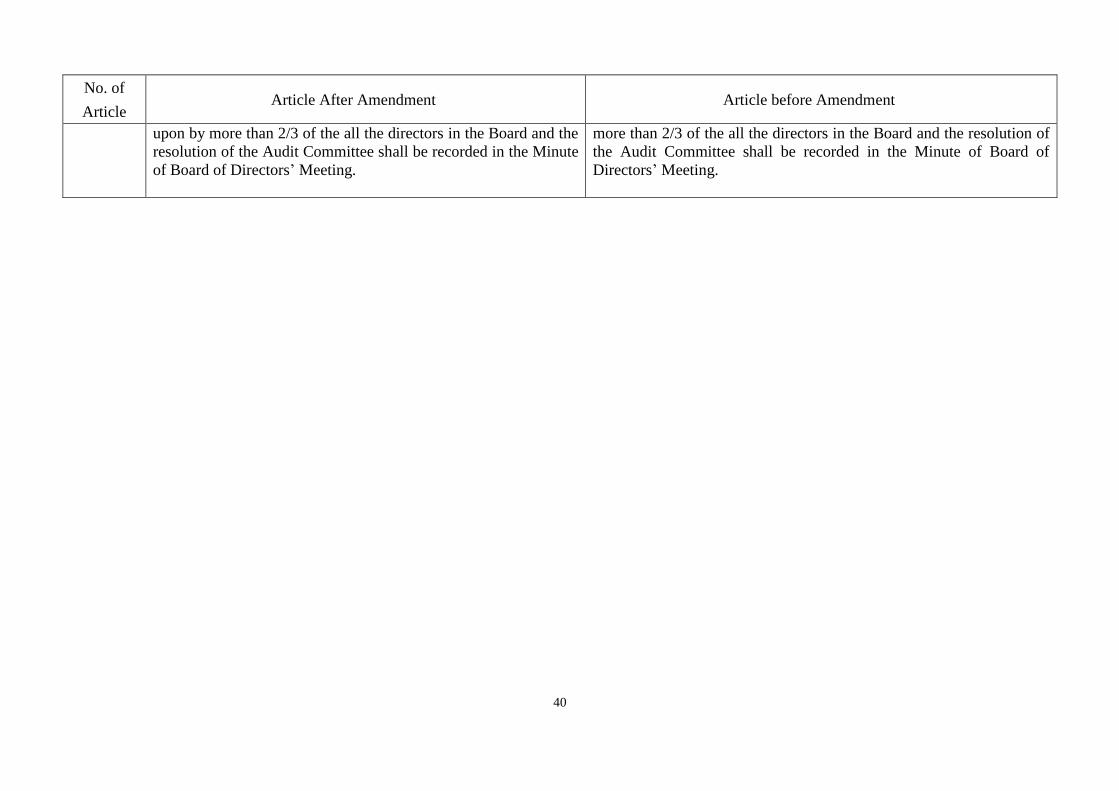

Article Article After Amendment Article before Amendment

Article 3

Transaction Principals and Guidelines: 1.~3.(1) is omitted.

3.(2) Accounting and Financial Department:

Regularly disclose information and Relevant Accounting

Processing shall be in accordance with generally accepted

accounting principles (GAAP) and other applicable laws and

regulations.

The GAAP described in the preceding paragraph shall mean the

following, as endorsed by the Financial Supervisory Commission

(FSC), Executive Yuan: International Financial Reporting

Standards (IFRS), International Accounting Standards (IAS), and

Interpretations developed by the International Financial Reporting

Interpretations Committee (IFRIC) or the former Standing

Interpretations Committee (SIC).

……. 6. For operation of non-hedging derivative trading, the amount of

loss ceiling for each contract is 20% of an individual contract; the

loss ceiling for accumulated loss is 10% of the net worth in latest

financial statements in the financial year.

Transaction Principals and Guidelines: ……. 1.~3.(1) is omitted.

3.(2) Accounting and Financial Department:

I. Regularly disclose information according to Financial Accounting

Standards No.36-“Financial Instruments: Disclosure and

Presentation”

II. Relevant Accounting Processing: Processing according to Financial

Accounting Standards No 14, No 34, generally accepted Accounting

Principles and relevant laws and regulations.

……

6. For operation of non-hedging derivative products, the amount of loss

ceiling for each contract is 10% of an individual contract; the loss

ceiling for accumulated loss is 10% of the planned net profit before

tax.

36

No. of

Article Article After Amendment Article before Amendment

…… (2). Exchange rate related products: If the exchange rate related

derivative product operation is for the needs of paying off the

foreign currency payment entrusted by the customers,

customer’s power of attorney must be submitted to sales

department head for approval and then the case should be

operated by Financial and Accounting Department; the

authorization level for other exchange rate products are as

follow:

…… (2). Exchange rate related products: If the exchange rate related

derivative product operation is for the needs of paying off the

foreign currency payment entrusted by the customers, customer’s

power of attorney must be submitted to sales department head for

approval and then the case should be operated by Financial and

Accounting Department; the authorization level for other

exchange rate products are as follow:

Article 5

Public Disclosure of information:

1. According to “Regulations Governing the Acquisition and

Disposal of Assets by Public Companies”, the Company

shall compile monthly reports on the status of derivatives

trading engaged in up to the end of the preceding month by

itself and any subsidiaries that are not domestic public

companies and enter the information in the prescribed

format into the information reporting website designated by

the FSC by the 10th day of each month.

2. Under any of the following circumstances, the Company

shall publicly announce and report the relevant information

on the FSC's designated website in the appropriate format as

prescribed by regulations on the date of occurrence of the

event:

(1) Losses from derivatives trading reaching the limits on

aggregate losses or losses on individual contracts set out

Public Disclosure of information:

1. According to “Regulations Governing the Acquisition and

Disposal of Assets by Public Companies”, the Company shall

compile monthly reports on the status of derivatives trading

engaged in up to the end of the preceding month by itself and

any subsidiaries that are not domestic public companies and

enter the information in the prescribed format into the

information reporting website designated by the FSC by the 10th

day of each month.