Embed Size (px)

DESCRIPTION

mas

Citation preview

Managerial Accounting, 2eBraun/Tietz/Harrison

Test Item FileChapter 13: Statement of Cash Flows

13.1-1 The statement of cash flows reflects cash flows on a particular date.

Answer: False LO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: ReflectiveAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-2 The statement of cash flows reports why cash increased or decreased during the period.

Answer: True LO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: ReflectiveAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-3 Investors and management use the statement of cash flows to evaluate a firm's profitability.

Answer: False LO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: ReflectiveAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-4 For purposes of the statement of cash flows, "cash" includes cash on hand, cash in the bank and cash equivalents.

Answer: True LO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: ReflectiveAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 1

13.1-5 Cash equivalents include highly liquid investments that can be readily converted into cash.

Answer: True LO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: ReflectiveAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-6 Operating activities include activities that affect long-term liabilities and owners' equity.

Answer: False LO: 13-1Diff: 1EOC Ref: S13-2AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-7 The investing activities section of the statement of cash flows is the most important section.

Answer: False LO: 13-1Diff: 1EOC Ref: S13-2AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-8 The financing activities section of the statement of cash flows includes paying dividends and paying off loans.

Answer: True LO: 13-1Diff: 1EOC Ref: S13-2AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-9 Investing activities include activities that affect the long-term asset section of the balance sheet.

Answer: True LO: 13-1Diff: 1EOC Ref: S13-3AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 2

13.1-10 Financing activities include activities that affect current assets and liabilities on the balance sheet.

Answer: False LO: 13-1Diff: 1EOC Ref: S13-3AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-11 Which of the following is TRUE of the statement of cash flows? A) The statement of cash flows reports why cash increased or decreased during the period. B) The statement of cash flows covers a span of time and is dated "Year Ended Month Day, Year". C) The statement of cash flows shows where cash came from and how cash was spent. D) All of the above are true of the statement of cash flows.

Answer: D LO: 13-1Diff: 1EOC Ref: S13-4AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-12 A statement of cash flows is generated to show:A) the revenues the company has earned.B) the expenses the company incurred during the time period.C) the inflow and outflow of cash during the time period.D) how profits were generated.

Answer: CLO: 13-1Diff: 1EOC Ref: S13-1AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-13 For anything to be considered a “cash equivalent”, the investment must be:A) convertible to cash within 5 years.B) convertible to a known amount of cash.C) convertible to cash without loss of value.D) convertible to cash within 1 year.

Answer: BLO: 13-1Diff: 1EOC Ref: EOC Accounting VocabularyAASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 3

13.1-14 Which of the following financial statements reports an entity's cash receipts and cash payments during the period? A) The statement of cash flows B) The statement of retained earnings C) The balance sheet D) The income statement

Answer: A LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-15 Which of the following are created by operating activities? A) Revenues and expenses B) An increase in common stock C) An increase in long-term debt D) Both A and B

Answer: A LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-16 Which of the following statements about the information included on a statement of cash flows is TRUE? A) The statement of cash flows contains information about the business's ability to generate positive cash flows in future periods. B) The statement of cash flows contains information about stock splits and stock dividends distributed by the company. C) The statement of cash flows contains information about the business's percentage change in each item of revenue and expense. D) The statement of cash flows contains information about the differences between net income and additions to retained earnings.

Answer: A LO: 13-1Diff: 1EOC Ref: E13-15AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 4

13.1-17 Which of the following is TRUE about a statement of cash flows? A) The statement of cash flows is prepared at the option of management. B) The statement of cash flows is required by generally accepted accounting principles. C) The statement of cash flows may be combined with the income statement. D) The statement of cash flows does not have to be completed if an income statement is prepared.

Answer: B LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-18 Which of the following is a purpose for the statement of cash flows? A) To evaluate board of directors' decisions B) To help predict management's future decisions C) To determine the ability to pay dividends to stockholders and interest and principle to creditors D) To report the earnings per share

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-19 Which of the following is an acceptable basis for the preparation of the statement of cash flows? A) The sum of cash, inventory, and money market accounts B) The sum of cash and accounts receivableC) The sum of cash and cash equivalents D) Cash

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 5

13.1-20 Which of the following is included in the statement of cash flows? A) Total changes in retained earnings B) Total changes in total liabilities C) Total changes in cash from investing activities D) Total changes in stockholder's equity

Answer: C LO: 13-1Diff: 1EOC Ref: S13-1AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-21 Which of the following is TRUE if a corporation shows a net loss on its income statement? A) The company may still have a net increase in cash. B) The company will not be able to sell stock. C) The company will not be able to pay dividends. D) The company may still have an increase in retained earnings.

Answer: A LO: 13-1Diff: 1EOC Ref: S13-1AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-22 Which of the following descriptions DO apply to cash equivalents? A) Cash equivalents' values change because of interest rate changes. B) Cash equivalents are invested in fixed assets. C) Cash equivalents are long-term. D) Cash equivalents are highly liquid.

Answer: D LO: 13-1Diff: 1EOC Ref: S13-1AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 6

13.1-23 Which of the following is the correct order of the sections on a statement of cash flows? A) Operating, financing, investing B) Financing, investing, operating C) Investing, operating, financing D) Operating, investing, financing

Answer: D LO: 13-1Diff: 1EOC Ref: S13-2AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-24 Which of the following are the three major categories included on the statement of cash flows? A) Investing, operating and financing activities B) Investing, capital and financing activities C) Investing, operating and capital activities D) Financial, operating and capital activities

Answer: A LO: 13-1Diff: 1EOC Ref: S13-2AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-25 Which of the following are the activities that are included in the operating activities section of the statement of cash flows? A) Activities that obtain the cash needed to launch and sustain the business B) Activities that create revenue or expenses in the entity's major line of business C) Activities that increase or decrease long-term assets D) None of the above

Answer: B LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 7

13.1-26 Which of the following sections from the statement of cash flows includes activities that create revenue, expenses, gains and losses? A) Investing section B) Financing section C) Operating section D) None of the above

Answer: CLO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-27 Which of the following sections from the statement of cash flows includes activities that affect net income on the income statement? A) Financing section B) Operating section C) Investing section D) None of the above

Answer: B LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-28 Which of the following sections from the statement of cash flows includes activities that affect current assets and current liabilities on the balance sheet? A) Investing section B) Financing section C) Operating section D) None of the above

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 8

13.1-29 Which of the following sections from the statement of cash flows is the most important section because it reflects the day-to-day operations that determine the future of an organization? A) The financing section B) The operating section C) The investing section D) None of the above

Answer: B LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-30 Which of the following sections from the statement of cash flows includes activities that increase and decrease long-term assets? A) Financing section B) Operating section C) Investing section D) None of the above

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-31 Which of the following sections from the statement of cash flows includes purchases and sales of long-term assets? A) Financing section B) Operating section C) Investing section D) None of the above

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 9

13.1-32 Which of the following sections from the statement of cash flows includes activities that increase and decrease long-term liabilities and owners' equity? A) Financing section B) Operating section C) Investing section D) None of the above

Answer: A LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-33 Which of the following sections from the statement of cash flows includes the issuance of stock and the payment of dividends? A) Investing section B) Financing section C) Operating section. D) None of the above

Answer: B LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-34 Which of the following sections from the statement of cash flows includes the purchase and sale of treasury stock? A) Financing section B) Operating section C) Investing section D) None of the above

Answer: A LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 10

13.1-35 Which of the following sections from the statement of cash flows includes borrowing money and paying off loans? A) Investing section B) Operating section C) Financing section D) None of the above

Answer: C LO: 13-1Diff: 1EOC Ref: E13-16AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-36 Which of the following sections from the statement of cash flows would include the purchase of a building totally financed by a mortgage? A) Investing section B) Operating section C) Financing section D) None of the above

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-37 Which of the following sections from the statement of cash flows would include the acquisition of a building by issuing common stock? A) Investing section B) Financing section C) Operating section D) None of the above

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 11

13.1-38 Which of the following sections from the statement of cash flows includes loans to others and collections on loans? A) Financing section B) Investing section C) Operating section D) None of the above

Answer: B LO: 13-1Diff: 2EOC Ref: S13-7 AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-39 Which of the following sections from the statement of cash flows would include the payment of a note payable by issuing common stock? A) Investing section B) Financing section C) Operating section D) None of the above

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-40 Paying cash dividends would be:A) a cash outflow from financing.B) a cash outflow from operations.C) a cash outflow from investing.D) none of the above.

Answer: ALO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 12

13.1-41 Issuing preferred stock to stockholders would be a:A) cash inflow from investing.B) cash inflow from operations.C) cash inflow from financing.D) cash inflow from depreciation.

Answer: CLO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-42 Buying and selling property, plant and equipment would be considered in:A) the operating portion of the statement of cash flows.B) the investing portion of the statement of cash flows.C) the financing portion of the statement of cash flows.D) none of the above portions of the statement of cash flows.

Answer: BLO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-43 Of the following, which is NOT a cash outflow from an investing activity?A) Purchase of equity securitiesB) Loans made to another partyC) Purchase of treasury stockD) Purchase of commercial real estate

Answer: CLO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 13

13.1-44 Of the following, which is the primary source of cash over the life of a business?A) Operating activitiesB) Financing activitiesC) Investing activitiesD) None of the above

Answer: ALO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-45 Of the following, which is NOT a cash inflow from a financing activity?A) Additional owner investmentB) Issuance of stockC) Interest revenue on loansD) Mortgage proceeds

Answer: CLO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-46 An outflow of cash from an investing activity would be:A) purchasing treasury stock.B) issuing notes payable.C) paying cash dividends to stockholders.D) making loans to third parties.

Answer: DLO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 14

13.1-47 Money borrowed for a mortgage would be a(n) __________activity.A) operatingB) investingC) financing D) non-cash

Answer: CLO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-48 Which of the following is NOT a cash outflow from an operating activity?A) Payment of interest on a loanB) Payment for purchasing inventoryC) Owner withdrawal from the companyD) Payments to the government for taxes

Answer: CLO: 13-1Diff: 1EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-49 A payment of interest on a loan would be considered a:A) cash outflow from operating activities.B) cash outflow from investing activities.C) cash outflow from financing activities.D) cash outflow from depreciation.

Answer: ALO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 15

13.1-50 Cash received from selling merchandise would be considered a:A) cash inflow from investing activities.B) cash inflow from operating activities.C) cash inflow from financing activities.D) cash outflow from operating activities.

Answer: BLO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-51 Creditor and stockholder transactions are considered ___________ activities.A) planningB) financingC) operatingD) investing

Answer: B LO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-52 A loss of $35,000 from the sale of equipment would be included in which of the activities sections of the statement of cash flows?A) OperatingB) InvestingC) FinancingD) Would not be on the statement of cash flows

Answer: ALO: 13-1Diff: 2EOC Ref: S13-7AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 16

13.1-53 Which of the following are the activities that are included in the investing activities section of the statement of cash flows? A) Activities that increase or decrease long-term assets B) Activities that obtain the cash needed to launch and sustain the business C) Activities that create revenue or expenses in the entity's major line of business D) None of the above

Answer: A LO: 13-1Diff: 1EOC Ref: S 13-4AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-54 Which of the following sections from the statement of cash flows would include the issuance of a stock dividend? A) Operating section B) Financing section C) Investing section D) None of the above

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-55 Which of the following would be considered an operating activity on the statement of cash flows? A) Dividends paid to stockholders B) The sale of inventory C) Gain on sale of short-term investments D) The receipt of stock dividends from investment stock

Answer: BLO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 17

13.1-56 Which of the following items would be reported as an operating activity on the statement of cash flows? A) A purchase of treasury stock B) A payment of dividends C) An issuance of stock D) A payment of interest

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-57 Which of the following would be considered an investing activity on the statement of cash flows? A) A sale of land B) A purchase of treasury stock C) Depreciation of equipment D) A sale of inventory

Answer: A LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-58 Which of the following items would be reported in the financing activities section on the statement of cash flows? A) Cash paid for interest B) Cash received from customers C) Cash paid for operating expenses D) Cash received from a sale of treasury stock

Answer: D LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 18

13.1-59 Where are noncash investing and financing activities reported? A) The financing activities section of the statement of cash flows B) The investing activities section of the statement of cash flows C) A schedule accompanying the statement of cash flows D) In both A and B

Answer: C LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-60 Which of the following are the activities that are included in the financing activities section of the statement of cash flows? A) Activities that obtain the cash needed to launch and sustain the business B) Activities that increase or decrease long-term assets C) Activities that create revenue or expenses in the entity's major line of business D) None of the above

Answer: A LO: 13-1Diff: 2EOC Ref: S13-7 AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.1-61 List three ways that owners and investors use the statement of cash flows.

Answer: A. The statement of cash flows is used to predict future cash flows. B. The statement of cash flows is used to evaluate management decisions. C. The statement of cash flows is used to predict a company' ability to pay debts and dividends.

LO: 13-1Diff: 1EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 19

13.2-1 The indirect method of presenting the investing activities section of the statement of cash flow reconciles net income to net cash provided by investing activities.

Answer: False LO: 13-2Diff: 1EOC Ref: EOC Accounting VocabularyAACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-2 When a company uses the indirect method to present the statement of cash flows, depreciation expense must be added to net income to reconcile to net cash provided by operating activities.

Answer: True LO: 13-2Diff: 2EOC Ref: S13-7AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-3 When a company uses the indirect method to present the statement of cash flows, a gain on the sale of a long-term asset must be subtracted from net income to reconcile to net cash provided by operating activities.

Answer: True LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-4 When a company uses the indirect method to present the statement of cash flows, an increase in a current liability must be subtracted from net income to reconcile to net cash provided by operating activities.

Answer: False LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 20

13.2-5 When a company uses the indirect method to present the statement of cash flows, cash received from the sale of a long-term asset increases the amount of net cash provided by investing activities.

Answer: True LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-6 A company uses the indirect method to prepare the statement of cash flows. How will depreciation be presented on the statement? A) Depreciation expense will be added to net income in the financing activities section. B) Depreciation expense will be subtracted from net income in the operating section. C) Depreciation expense will be added to net income in the operating activities section. D) Depreciation expense will be added to net income in the investing activities section.

Answer: CLO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-7 A company uses the indirect method to prepare the statement of cash flows. How will a loss from the sale of equipment be presented on the statement? A) A loss from the sale of equipment will be an addition in the financing activities section. B) A loss from the sale of equipment will be added to net income in the operating activities section. C) A loss from the sale of equipment will be deducted from net income in the operating activities section. D) A loss from the sale of equipment will be an addition in the investing activities section.

Answer: B LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 21

13.2-8 A company uses the indirect method to prepare the statement of cash flows. Which of the following items would be added to net income in determining the net cash flow from operating activities? A) A decrease in accounts receivable would be added to net income. B) An increase in inventory would be added to net income. C) A decrease in accounts payable would be added to net income. D) An increase in preferred dividends payable would be added to net income.

Answer: A LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-9 A company uses the indirect method to prepare the statement of cash flows. Which of the following items would be subtracted from net income in determining the net cash flow from operating activities? A) Amortization of a premium on bonds payable would be subtracted from net income. B) An increase in dividends payable would be subtracted from net income. C) A loss on the sale of equipment would be subtracted from net income. D) Depreciation expense would be subtracted from net income.

Answer: A LO: 13-2Diff: 2EOC Ref: S13-5AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-10 A company uses the indirect method to prepare the statement of cash flows. How will the adjustment to reflect the amount of cash payments to employees be presented on the statement? A) The adjustment will be for the increase or decrease in accrued expenses for the period and will adjust net income in the operating activities section. B) The adjustment will be for the increase or decrease in accounts receivable for the period and will adjust net income in the operating activities section. C) The adjustment will be for the increase or decrease in inventory for the period and will adjust net income in the operating activities section. D) The adjustment will be for the increase or decrease in accounts payable for the period and will adjust net income in the operating activities section.

Answer: A LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 22

13.2-11 A company uses the indirect method to prepare the statement of cash flows. How will the adjustment to reflect the amount of cash paid for interest be presented on the statement? A) The adjustment will be for the increase or decrease in accounts receivable for the period and will adjust net income in the operating activities section. B) The adjustment will be for the increase or decrease in inventory for the period and will adjust net income in the operating activities section. C) The adjustment will be for the increase or decrease in accrued expenses for the period and will adjust net income in the operating activities section. D) The adjustment will be for the increase or decrease in accounts payable for the period and will adjust net income in the operating activities section.

Answer: C LO: 13-2Diff: 3EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-12 A company uses the indirect method to prepare the statement of cash flows. How will the adjustment to reflect the amount of cash payments to suppliers be presented on the statement? A) The adjustment will be for the increase or decrease in accounts payable for the period and will adjust net income in the operating activities section. B) The adjustment will be for the increase or decrease in inventory for the period and will adjust net income in the operating activities section. C) The adjustment will be for the increase or decrease in accrued expenses for the period and will adjust net income in the operating activities section. D) The adjustment will be for the increase or decrease in accounts receivable for the period and will adjust net income in the operating activities section.

Answer: ALO: 13-2Diff: 3EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 23

13.2-13 A company uses the indirect method to prepare the statement of cash flows. How will the adjustment to reflect the amount of cash received from customers be presented on the statement? A) The adjustment will be for the increase or decrease in accounts receivable for the period and will adjust net income in the operating activities section. B) The adjustment will be for the increase or decrease in accounts payable for the period and will adjust net income in the operating activities section. C) The adjustment will be for the increase or decrease in accrued expenses for the period and will adjust net income in the operating activities section. D) The adjustment will be for the increase or decrease in inventory for the period and will adjust net income in the operating activities section.

Answer: A LO: 13-2Diff: 3EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-14 The balance in the ___________ can be used to check the accuracy of the statement of cash flows.A) asset and liability accountsB) liability accountsC) asset accountsD) cash and cash equivalent accounts

Answer: DLO: 13-2Diff: 1EOC Ref: S13-8AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-15 Computing cash generated from operating activities is:A) the same for both the direct and indirect methods.B) different in that the direct method considers depreciation.C) different in that the indirect method considers depreciation.D) none of the above.

Answer: CLO: 13-2Diff: 1EOC Ref: S13-8AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 24

13.2-16 To prepare the statement of cash flows, you need the:A) accounts payable ledger.B) accounts receivable ledger.C) general journal.D) balance sheet from the beginning and ending of the period.

Answer: ALO: 13-2Diff: 2EOC Ref: E13-12AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-17 Operating activities resulting from the sales of goods and services relate to:A) retained earnings reported on the balance sheet.B) assets and liabilities reported on the balance sheet.C) net income on the retained earnings statement.D) the income statement.

Answer: DLO: 13-2Diff: 2EOC Ref: E13-12AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-18 Which of the following would NOT be done when calculating the change in cash from operating activities under the indirect method?A) Add an increase in accrued interest payableB) Deduct the purchase of equipmentC) Add a decrease in merchandise inventoryD) Deduct a decrease in accounts payable

Answer: BLO: 13-2Diff: 2EOC Ref: E13-12AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 25

13.2-19 Which is NOT reported as an operating activity on a cash flow statement?A) Proceeds from the sale of equipmentB) Interest revenueC) Interest expenseD) Dividend revenue

Answer: ALO: 13-2Diff: 2EOC Ref: E13-12AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-20 A company pays cash dividends on preferred stock. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The payment of cash dividends would be presented in the investing activities section as a cash payment under both methods. B) The payment of cash dividends would be presented in the financing activities section as a cash payment under both methods. C) The payment of cash dividends would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash payment under the direct method. D) The payment of cash dividends would be presented in the non-cash investing and financing activities section under both methods.

Answer: B LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-21 A company acquires its own stock to hold as treasury stock. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The acquisition of treasury stock would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash payment under the direct method. B) The acquisition of treasury stock would be presented in the financing activities section as a cash payment under both methods. C) The acquisition of treasury stock would be presented in the non-cash investing and financing activities section under both methods. D) The acquisition of treasury stock would be presented in the investing activities section as a cash payment under both methods.

Answer: B LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 26

13.2-22 A company sells treasury stock for an amount less than its acquisition cost. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The sale of treasury stock would be presented in the investing activities section as a cash receipt under the both methods. B) The sale of treasury stock would be presented in the financing activities section as a cash receipt under the both methods. C) The sale of treasury stock would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash receipt under the direct method. D) The sale of treasury stock would be presented in the non-cash investing and financing activities section under both methods.

Answer: B LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-23 A company purchases equipment for use in its business activities. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The purchase of equipment would be presented in the non-cash investing and financing activities section under both methods. B) The purchase of equipment would be presented in the financing activities section as a cash payment under both methods. C) The purchase of equipment would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash payment under the direct method. D) The purchase of equipment would be presented in the investing activities section as a cash payment under both methods.

Answer: D LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 27

13.2-24 A company sells equipment at a loss. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The sale of equipment at a loss would be presented in the investing activities section as a cash receipt under the both methods. B) The sale of equipment at a loss would be presented in the investing activities section as a cash payment under the both methods. C) The sale of equipment at a loss would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash receipt under the direct method. D) The sale of equipment at a loss would be presented in the financing activities section as a cash receipt under the both methods.

Answer: A LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-25 A company purchases land using its common stock. Where would this transaction appear if the company prepares the statement of cash flows using the indirect method or the direct method? A) The purchase of land would be presented in the financing activities section as a cash payment under both methods. B) The purchase of land would be presented in the investing activities section as a cash payment under both methods. C) The purchase of land would be presented in the non-cash investing and financing activities section under both methods. D) The purchase of land would be presented in the operating activities section as a reduction in net income under the indirect method and as a cash payment under the direct method.

Answer: C LO: 13-2Diff: 3EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-26 A company uses the indirect method to prepare the statement of cash flows. How will a gain from the sale of equipment be presented on the statement? A) A gain from the sale of equipment will be an addition in the investing activities section. B) A gain from the sale of equipment will be added to net income in the operating activities section. C) A gain from the sale of equipment will be deducted from net income in the operating activities section. D) A gain from the sale of equipment will be a deduction in the financing activities section.

Answer: C LO: 13-2Diff: 2EOC Ref: S13-5 AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 28

13.2-27 A company uses the indirect method to prepare the statement of cash flows. Which of the following items would be added to net income in determining the net cash flow from operating activities? A) An increase in accrued liabilities would be added to net income. B) An increase in dividends paid would be added to net income. C) A decrease in accounts payable would be added to net income. D) A gain on the sale of land would be added to net income.

Answer: ALO: 13-2Diff: 2EOC Ref: S13-12 AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-28 A company uses the indirect method to prepare the statement of cash flows. It sold a piece of equipment at a loss of $3,600. The equipment was purchased several years ago for $70,500 and had accumulated depreciation of $52,900. What is reported under the operating activities section on the statement of cash flows? A) Cash proceeds of $14,000 are subtracted from net income. B) Cash proceeds of $14,000 are added to net income. C) The loss of $3,600 is added to net income. D) The loss of $3,600 is subtracted from net income.

Answer: C LO: 13-2Diff: 3EOC Ref: S13-12AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 29

13.2-29 A company uses the indirect method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to accounts receivable? A) The increase of $10,000 will be subtracted from sales revenue. B) The increase of $10,000 will be added to net income. C) The increase of $10,000 will be added to sales revenue. D) The increase of $10,000 will be subtracted from net income

Answer: D LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-30 A cash flow statement shows $13,000 from operations, ($9,000) from investing, and $21,000 from financing. The cash balance must have increased or decreased by:A) $12,000.B) $25,000.C) $43,000.D) $34,000.

Answer: BLO: 13-2Diff: 2EOC Ref: S13-8AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 30

13.2-31 A company uses the indirect method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to accounts payable? A) The increase of $8,000 will be added to net income. B) The increase of $8,000 will be subtracted from net income. C) The increase of $8,000 will be subtracted from cost of goods sold. D) The increase of $8,000 will be added to cost of goods sold.

Answer: A LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 31

13.2-32 A company uses the indirect method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to inventory? A) The decrease of $19,000 will be subtracted from net income. B) The decrease of $19,000 will be subtracted from cost of goods sold. C) The decrease of $19,000 will be added to cost of goods sold. D) The decrease of $19,000 will be added to net income.

Answer: D LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 32

13.2-33 A company uses the indirect method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to salary payable? A) The increase of $3,000 will be added to net income. B) The increase of $3,000 will be added to cost of goods sold. C) The increase of $3,000 will be subtracted from cost of goods sold. D) The increase of $3,000 will be subtracted from net income

Answer: A LO: 13-2Diff: 2EOC Ref: S13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-34 A company reported beginning plant assets, net of depreciation, of $645,000 and an ending amount of $732,500. Depreciation expense of $48,300 and a loss on the sale of equipment of $5,600 were reported on the income statement. The company acquired $213,000 of plant assets during the year. How much will be reported as cash received from the sale of equipment in the investing activities section of the statement

of cash flows? A) The cash received upon the sale of the equipment was $71,600. B) The cash received upon the sale of the equipment was $77,200. C) The cash received upon the sale of the equipment was $82,800. D) The cash received upon the sale of the equipment was $119,900.

Answer: A LO: 13-2Diff: 2EOC Ref: E13-8AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 33

13.2-35 A company sold equipment with a book value of $9,000 at a gain of $2,500. How much will be reported in the investing activities section of the statement of cash flows as cash received upon the sale of the equipment? A) The cash received upon the sale of the equipment was $11,500. B) The cash received upon the sale of the equipment was $2,500. C) The cash received upon the sale of the equipment was $6,500. D) The cash received upon the sale of the equipment was $9,000.

Answer: A LO: 13-2Diff: 2EOC Ref: E13-15AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-36 The beginning and ending balances of long-term debt are $61,500 and $35,400, respectively, and cash payments for long-term debt during the year were $35,100. How much new long-term debt was issued during the year? A) New long-term debt issued during the year was $9,000. B) New long-term debt issued during the year was $300. C) New long-term debt issued during the year was $26,100. D) New long-term debt issued during the year was $61,200.

Answer: A LO: 13-2Diff: 3EOC Ref: E13-15AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 34

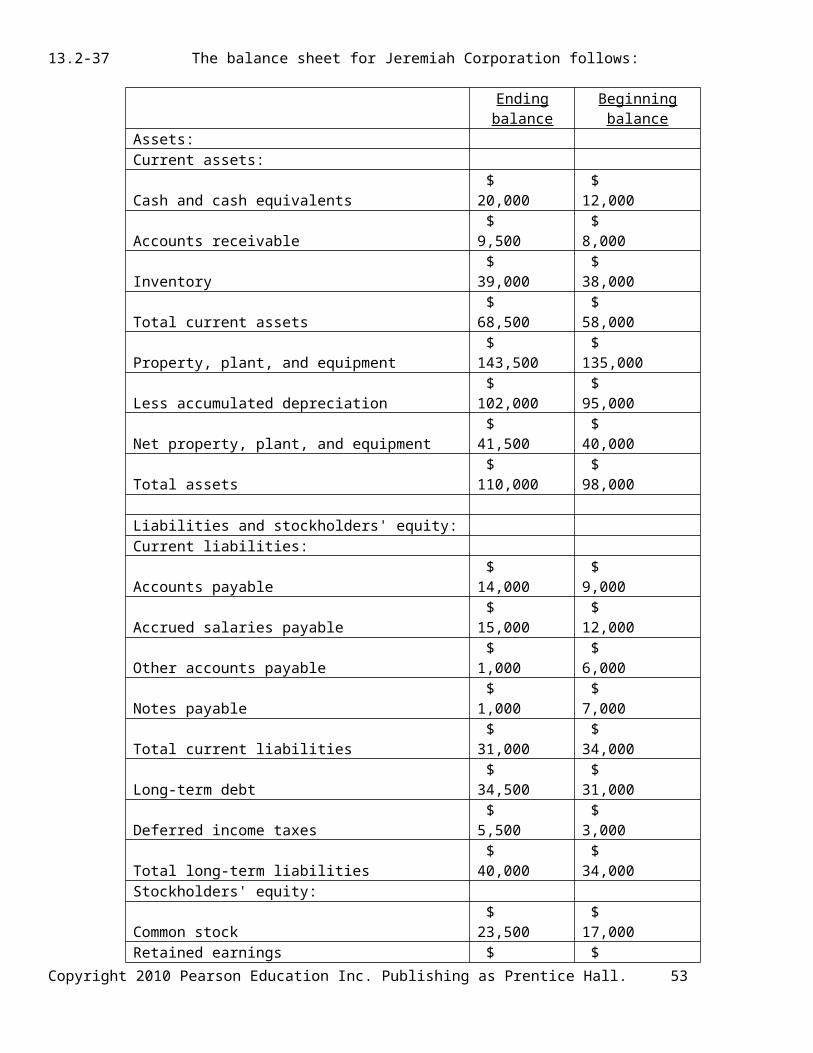

13.2-37 The balance sheet for Jeremiah Corporation follows:

Ending balance Beginning balance

Assets:Current assets:Cash and cash equivalents $ 20,000 $ 12,000 Accounts receivable $ 9,500 $ 8,000 Inventory $ 39,000 $ 38,000 Total current assets $ 68,500 $ 58,000 Property, plant, and equipment $ 143,500 $ 135,000 Less accumulated depreciation $ 102,000 $ 95,000 Net property, plant, and equipment $ 41,500 $ 40,000 Total assets $ 110,000 $ 98,000

Liabilities and stockholders' equity:Current liabilities:Accounts payable $ 14,000 $ 9,000 Accrued salaries payable $ 15,000 $ 12,000 Other accounts payable $ 1,000 $ 6,000 Notes payable $ 1,000 $ 7,000 Total current liabilities $ 31,000 $ 34,000 Long-term debt $ 34,500 $ 31,000 Deferred income taxes $ 5,500 $ 3,000 Total long-term liabilities $ 40,000 $ 34,000 Stockholders' equity:Common stock $ 23,500 $ 17,000 Retained earnings $ 15,500 $ 13,000 Total stockholders' equity $ 39,000 $ 30,000 Total liabilities and stockholders' equity $ 110,000 $ 98,000

Operating income for the period was $15,000, while cash dividends paid were $12,500. The overall total of the sources of cash for Jeremiah Corporation for the year was:A) $ 8,000.B) $12,500.C) $35,500.D) $42,500.

Answer: DLO: 13-2Diff: 2EOC Ref: E 13-15AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 35

13.2-38 The balance sheet for Jeremiah Corporation follows:

Ending balance Beginning balance

Assets:Current assets:Cash and cash equivalents $ 20,000 $ 12,000 Accounts receivable $ 9,500 $ 8,000 Inventory $ 39,000 $ 38,000 Total current assets $ 68,500 $ 58,000 Property, plant, and equipment $ 143,500 $ 135,000 Less accumulated depreciation $ 102,000 $ 95,000 Net property, plant, and equipment $ 41,500 $ 40,000 Total assets $ 110,000 $ 98,000

Liabilities and stockholders' equity:Current liabilities:Accounts payable $ 14,000 $ 9,000 Accrued salaries payable $ 15,000 $ 12,000 Other accounts payable $ 1,000 $ 6,000 Notes payable $ 1,000 $ 7,000 Total current liabilities $ 31,000 $ 34,000 Long-term debt $ 34,500 $ 31,000 Deferred income taxes $ 5,500 $ 3,000 Total long-term liabilities $ 40,000 $ 34,000 Stockholders' equity:Common stock $ 23,500 $ 17,000 Retained earnings $ 15,500 $ 13,000 Total stockholders' equity $ 39,000 $ 30,000 Total liabilities and stockholders' equity $ 110,000 $ 98,000

Operating income for the period was $15,000, while cash dividends paid were $12,500. The overall total of the uses of cash for Jeremiah Corporation for the year was:A) $ 8,000.B) $23,500.C) $34,500.D) $42,500.

Answer: CLO: 13-2Diff: 2EOC Ref: E13-15 AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 36

13.2-39 The balance sheet for Maleenah Corporation follows:

Ending balance Beginning balanceAssets:Current assets:Cash and cash equivalents $ 57,500 $ 44,000 Accounts receivable $ 19,600 $ 22,600 Inventory $ 50,000 $ 54,000 Total current assets $ 127,100 $ 120,600 Property, plant, and equipment $ 287,000 $ 275,000 Less accumulated depreciation $ 108,500 $ 101,500 Net property, plant, and equipment $ 178,500 $ 173,500 Total assets $ 305,600 $ 294,100

Liabilities and stockholders' equity:Current liabilities:Accounts payable $ 26,000 $ 29,500 Wages payable $ 41,500 $ 47,000 Other accounts payable $ 39,500 $ 33,000 Notes payable $ 24,000 $ 25,000 Total current liabilities $ 131,000 $ 134,500 Long-term debt $ 72,000 $ 78,000 Deferred income taxes $ 19,500 $ 17,000 Total liabilities $ 91,500 $ 95,000 Stockholders' equity:Common stock $ 54,000 $ 45,000 Retained earnings $ 29,100 $ 19,600 Total stockholders' equity $ 83,100 $ 64,600 Total liabilities and stockholders' equity $ 305,600 $ 294,100

Operating income for the period was $13,800, while cash dividends paid were $4,300. The overall total of the uses of cash for Maleenah Corporation for the year was:A) $ 2,000.B) $32,300.C) $34,500.D) $55,100.

Answer: BLO: 13-2Diff: 2EOC Ref: E13-15AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 37

13.2-40 The balance sheet for Maleenah Corporation follows:

Ending balance Beginning balanceAssets:Current assets:Cash and cash equivalents $ 57,500 $ 44,000 Accounts receivable $ 19,600 $ 22,600 Inventory $ 50,000 $ 54,000 Total current assets $ 127,100 $ 120,600 Property, plant, and equipment $ 287,000 $ 275,000 Less accumulated depreciation $ 108,500 $ 101,500 Net property, plant, and equipment $ 178,500 $ 173,500 Total assets $ 305,600 $ 294,100

Liabilities and stockholders' equity:Current liabilities:Accounts payable $ 26,000 $ 29,500 Wages payable $ 41,500 $ 47,000 Other accounts payable $ 39,500 $ 33,000 Notes payable $ 24,000 $ 25,000 Total current liabilities $ 131,000 $ 134,500 Long-term debt $ 72,000 $ 78,000 Deferred income taxes $ 19,500 $ 17,000 Total liabilities $ 91,500 $ 95,000 Stockholders' equity:Common stock $ 54,000 $ 45,000 Retained earnings $ 29,100 $ 19,600 Total stockholders' equity $ 83,100 $ 64,600 Total liabilities and stockholders' equity $ 305,600 $ 294,100

Operating income for the period was $13,800, while cash dividends paid were $4,300. The overall total of the uses of cash for Maleenah Corporation for the year was:A) $13,500.B) $32,300.C) $45,800.D) $38,800.

Answer: CLO: 13-2Diff: 2EOC Ref: E13-15AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 38

13.2-41 The following data relate to Wise Enterprises for last year:

Operating income $ 108,000 Net increase in all current assets except cash $ 12,000 Net increase in current liabilities $ 38,000 Cash dividends paid on common stock $ 15,000 Loss on sale of investments $ 4,000 Depreciation expense $ 6,000

What is the net cash provided by operating activities for last year on the statement of cash flows for Wise Enterprises?A) $121,000B) $124,000C) $144,000D) $151,000

Answer: CLO: 13-2Diff: 2EOC Ref: E13-15AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.2-42 The following data relate to Jackson Corporation for last year:

Operating income $ 225,000 Net increase in all current assets except cash $ 43,000 Net decrease in current liabilities $ 25,000 Cash dividends paid on common stock $ 32,000 Gain on sale of investments $ 10,000 Depreciation expense $ 12,000

What is the net cash provided by operating activities for last year on the statement of cash flows for Jackson Corporation?A) $127,000B) $159,000C) $155,000D) $113,000

Answer: BLO: 13-2Diff: 2EOC Ref: E13-15 AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 39

13.2-43 Rabin Corporation had the following selected balance sheet changes for the past year:

Assets and contra-assets Increase/(Decrease)Cash $ 37,000 Accounts receivable $ 12,000 Inventory $ 17,000 Prepaid expenses $ (5,000)Accumulated depreciation $ 9,000

Liabilities Increase/(Decrease)Accounts payable $ 18,000 Wages payable $ (9,000)Taxes payable $ 11,000

The company’s operating income for the year was $25,000. What is the net cash provided by operating activities for last year on the statement of cash flows for Rabin Corporation (using the indirect method)?A) $ 5,000B) $20,000C) $30,000D) $67,000

Answer: CLO: 13-2Diff: 2EOC Ref: E13-15AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 40

13.3-1 When a company uses the direct method to present the statement of cash flows, depreciation expense must be added to net income to reconcile to net cash provided by operating activities.

Answer: False LO: 13-3Diff: 2EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-2 The direct method of presenting the financing activities section of the statement of cash flow reconciles net income to net cash provided by financing activities.

Answer: False LO: 13-3Diff: 2EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-3 When a company uses the direct method to present the statement of cash flows, cash received from the sale of a long-term asset increases the amount of net cash provided by investing activities.

Answer: True LO: 13-3Diff: 2EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-4 When a company uses the direct method to present the statement of cash flows, cash received from the sale of treasury stock increases the amount of net cash provided by investing activities.

Answer: False LO: 13-3Diff: 2EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-5 When a company uses the direct method to present the statement of cash flows, the payment of cash dividends reduces the amount of net cash provided by operating activities.

Answer: False LO: 13-3Diff: 2EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 41

13.3-6 Which of the following would appear on a statement of cash flows prepared using the direct method? A) A loss of the sale of equipment would appear on the statement. B) Cash payments for salaries would appear on the statement. C) Amortization expenses would appear on the statement. D) Depreciation expenses would appear on the statement.

Answer: B LO: 13-3Diff: 2EOC Ref: E13-18AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-7 Which of the following would appear on a statement of cash flows prepared using the direct method? A) Interest received on a loan would appear on the statement. B) Collections from customers would appear on the statement. C) Cash payment of dividends would appear on the statement. D) All of the above would appear on the statement.

Answer: D LO: 13-3Diff: 2EOC Ref: E13-18AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-8 A company's income statement reports depreciation expenses of $25,000. How will the depreciation expense be reported on the statement of cash flows if the company uses the direct method to prepare the statement? A) Depreciation would not be reported on the statement of cash flows. B) Depreciation expense would be an addition under financing activities. C) Depreciation expense would be a deduction under operating activities. D) Depreciation expense would be an addition under investing activities.

Answer: A LO: 13-3Diff: 1EOC Ref: E13-18AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 42

13.3-9 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash payments to employees be computed? A) Cash payments to employees will be equal to salary expense plus the beginning balance in salary payable. B) Cash payments to employees will be equal to salary expense plus the ending balance in salary payable. C) Cash payments to employees will be equal to salary expense plus the increase in salary payable. D) Cash payments to employees will be equal to salary expense plus the decrease in salary payable.

Answer: D LO: 13-3Diff: 1EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-10 The only part that differs in a statement of cash flows using the direct method rather than the indirect method is:A) the financing activities section.B) the investing activities section.C) the operating activities section.D) none of the above.

Answer: CLO: 13-3Diff: 1EOC Ref: S13-9AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-11 Under the direct method of cash flow, which is NOT included in the cash flow statement?A) Changes in accounts receivableB) Changes in accounts payableC) Changes in depreciationD) Changes in interest expense

Answer: CLO: 13-3Diff: 1EOC Ref: S13-9AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 43

13.3-12 Which would NOT be included in the operating activities section of a direct method statement of cash flow?A) Changes in accounts payableB) Changes in accounts receivableC) Changes in inventoryD) Changes in depreciation

Answer: DLO: 13-3Diff: 1EOC Ref: S13-9AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-13 Under the direct method of preparing the statement of cash flows, a decrease in merchandise inventory would be:A) subtracted from operating expenses.B) added to cost of goods sold.C) added to operating expenses.D) subtracted from cost of goods sold.

Answer: DLO: 13-3Diff: 2EOC Ref: S13-9AASCB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-14 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash payments to suppliers be computed? A) The amount of cash payments to suppliers is computed as interest expense minus the decrease in accounts payable. B) The amount of cash payments to suppliers is computed as purchases minus the increase in accounts payable. C) The amount of cash payments to suppliers is computed as interest expense minus the decrease in merchandise inventory. D) The amount of cash payments to suppliers is computed as interest expense minus the increase in merchandise inventory.

Answer: B LO: 13-3Diff: 3EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 44

13.3-15 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash paid for interest be computed? A) The amount of cash paid for interest is computed as interest expense minus the increase in interest payable. B) The amount of cash paid for interest is computed as interest expense minus the increase in interest revenue. C) The amount of cash paid for interest is computed as interest expense minus the decrease in interest payable. D) The amount of cash paid for interest is computed as interest expense plus the increase in interest payable.

Answer: A LO: 13-3Diff: 3EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-16 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash purchases of inventory be computed? A) The amount of cash purchases of inventory is computed as cost of goods sold plus ending inventory. B) The amount of cash purchases of inventory is computed as cost of goods sold plus ending inventory plus beginning inventory. C) The amount of cash purchases of inventory is computed as cost of goods sold plus ending inventory minus beginning inventory. D) The amount of cash purchases of inventory is computed as beginning inventory minus ending inventory minus cost of goods sold.

Answer: C LO: 13-3Diff: 3EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 45

13.3-17 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash payments to employees be computed? A) The amount of cash payments to employees is computed as salary expense plus the decrease in salaries payable. B) The amount of cash payments to employees is computed as salary expense plus the ending balance salaries payable. C) The amount of cash payments to employees is computed as salary expense plus the increase in salaries payable. D) The amount of cash payments to employees is computed as salary expense plus the beginning balance in salaries payable.

Answer: A LO: 13-3Diff: 3EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-18 A company uses the direct method to prepare the statement of cash flows. How will the amount of cash received from customers be computed? A) The amount of cash received from customers is computed as sales revenue plus the decrease (or minus the increase) in accounts receivable. B) The amount of cash received from customers is computed as cost of goods sold minus ending inventory plus beginning inventory. C) The amount of cash received from customers is computed as cost of goods sold plus ending inventory minus beginning inventory. D) The amount of cash received from customers is computed as sales revenue minus the decrease (or plus the increase) in accounts receivable.

Answer: A LO: 13-3Diff: 3EOC Ref: S13-9AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-19 Which of the following would appear on a statement of cash flows prepared using the direct method? A) Amortization expense B) Loss on sale of equipment C) Net income D) Collections from customers

Answer: D LO: 13-3Diff: 2EOC Ref: S13-9 AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 46

13.3-20 A company uses the direct method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to accounts receivable? A) The increase of $10,000 will be subtracted from sales to determine cash received from customers. B) The increase of $10,000 will be subtracted from net income. C) The increase of $10,000 will be added to sales to determine cash received from customers. D) The increase of $10,000 will be added to net income.

Answer: A LO: 13-3Diff: 2EOC Ref: S13-10AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 47

13.3-21 A company uses the direct method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to accounts payable? A) The increase of $8,000 will be subtracted from purchases to determine payments to suppliers. B) The increase of $8,000 will be added to net income. C) The increase of $8,000 will be added to purchases to determine payments to suppliers. D) The increase of $8,000 will be subtracted from net income

Answer: A LO: 13-3Diff: 2EOC Ref: S13-10AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-22 A company uses the direct method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to inventory? A) The decrease of $19,000 will be subtracted from net income. B) The decrease of $19,000 will be added to net income. C) The decrease of $19,000 will be added to cost of goods sold to determine payments to suppliers. D) The decrease of $19,000 will be subtracted from cost of goods sold to determine payments to suppliers.

Answer: D LO: 13-3Diff: 2EOC Ref: S13-10AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 48

13.3-23 A company uses the direct method to prepare the statement of cash flows. It presents the following amounts on its financial statements.

End of this year End of prior yearAccounts receivable $110,000 $100,000Cost of goods sold 560,000Sales revenue 830,000Accounts payable* 75,000 67,000Inventory 86,000 105,000Salary payable 13,000 10,000Salary expense 49,000 45,000

*Relates solely to the acquisition of inventory

What will appear in the operating activities section related to salary payable? A) The increase of $3,000 will be subtracted from net income. B) The increase of $3,000 will be subtracted from salary expense to determine payments to employees. C) The increase of $3,000 will be added to salary expense to determine payments to employees. D) The increase of $3,000 will be added to net income.

Answer: B LO: 13-3Diff: 2EOC Ref: S13-10AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-24 A company's inventory account increased $26,800 and its accounts payable account decreased $18,240 during the year. The accounts payable relates only to the acquisition of inventory. Sales were $789,500 and cost of goods sold was $532,700. What was the amount of payments to supplier of inventory? A) $541,260 B) $834,540 C) $577,740 D) $550,940

Answer: C LO: 13-3Diff: 3EOC Ref: S13-10AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

Copyright 2010 Pearson Education Inc. Publishing as Prentice Hall. 49

13.3-25 A company uses the indirect method to prepare the statement of cash flows. The board of directorsdeclared dividends on common stock of $165,000 during the year. Dividends payable were $40,000 at thebeginning of the year and $45,000 at the end of the year.A. What was the amount of cash paid for dividends during the year?B. Where will this amount appear on the statement of cash flows?C. How would the amount appear if the company uses the direct method to prepare the statement?

Answer:A. $165,000 - 45,000 + 40,000 = $160,000B. The amount will be presented as a cash payment in the financing activities section.C. The presentation will be the same since it does not affect the operating activities section.

LO: 13-3Diff: 2EOC Ref: E13-13AACSB: Analytic SkillsAICPA Business Perspective Competencies: Strategic/Critical ThinkingAICPA Functional Competencies: Measurement, Reporting

13.3-26 The income statement and a partial balance sheet for Jefferson Company is presented below. Prepare theoperating activities section of the statement of cash flows using the direct method.

Jefferson CompanyIncome Statement

For the Current Year