Embed Size (px)

Citation preview

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 1/24

CHAPTER 2

CONCEPTUAL FRAMEWORK UNDERLYING FINANCIALACCOUNTING

TRUE-FALSE—Conceptu!

An"#e$ No% De"c$&pt&onF 1. Nature of conceptual framework.T 2. Conceptual framework definition.F 3. Levels of conceptual framework.T 4 International conceptual framework.F 5. tatements of Financial !ccountin" Concepts.

T #. $ecision usefulness.F %. Financial statement users.T &. 'elevance and relia(ilit).T *. Consistenc).F 1+. 'elevance.F 11. 'elia(ilit).F 12. ,asic elements.T 13. Compre-ensive income.T 14. oin" concern assumption.F 15. /conomic entit) assumption.F 1#. 0atc-in" principle.T 1%. 'ealia(le revenues.

T 1&. upplementar) information.F 1*. 0aterialit) factorsF 2+. Conservatism.

MULTIPLE CHOICE—Conceptu!

An"#e$ No% De"c$&pt&onc 21. !! defined.d 22. urpose of conceptual framework.c 23. Conceptual framework.d 24. Conceptual framework (enefits.d 25. (ectives of financial reportin".

a 2#. $ecision usefulness.d 2%. (ectives of financial reportin".a 2&. Financial repotin" o(ectives.c 2*. urpose of understanda(le information.a 3+. $ecisionusefulness criterion.c 31. rimar) 6ualities of accountin" information.( 32. $efinition of relevance.( 33. $efinition of relia(ilit).d 34. 'elevance and relia(ilit).c 35. Timeliness c-aracteristic.

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 2/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

MULTIPLE CHOICE—Conceptu! 7cont.8

An"#e$ No% De"c$&pt&ond 3#. 9erifia(ilit) c-aracteristic.( 3%. Neutralit) c-aracteristic.d 3&. Neutralit) c-aracteristic.c 3*. $efinition of verifia(ilit).a 4+. :ualit) of predictive value.c 41. :ualit) of representational fait-fulness.d 42. Consistenc).( 43. Consistenc) c-aracteristic.( 44. Compara(ilit) and consistenc).d 45. Compara(ilit).d 4#. /lements of financial statements.c 4%. $istinction (etween revenues and "ains.c 4&. $efinition of a loss.d 4*. $efinition of compre-ensive income.( 5+. Components of compre-ensive income.d 51. Compre-ensive income.( 52. /arnin"s vs. compre-ensive income.a 53. 'eportin" financial statement elements.a 54. 0onetar) unit assumption.c 55. eriodicit) assumption.c 5#. 0onetar) unit assumption.d 5%. /conomic entit) assumption.a 5&. /conomic entit) assumption.( 5*. eriodicit) assumption.a #+. oin" concern assumption.d #1. oin" concern assumption.d #2. Implications of "oin" concern assumption.

a #3. ;istorical cost principle.d #4. ;istorical cost principle.c #5. 'evenue reco"nition principle.d ##. 'evenue reco"nition principle.d #%. 'evenue reco"nition principle.d #&. Timin" of revenue reco"nition.c #*. 'ealiation concept.( %+. $efinition of realied.( %1. 0atc-in" principle.( %2. 0atc-in" principle.( %3. /<pense reco"nition.c %4. Fulldisclosure principle.

d %5. Constraints to limit t-e cost of reportin".a %#. Cost(enefit constraint.c %%. 0aterialit) constraint.d %&. 0aterialit).d %*. ervasive constraints.a &+. Conservatism constraint.( &1. Conservatism constraint.a &2. Tradeoffs (etween c-aracteristics of accountin" information.c &3. Tradeoffs (etween c-aracteristics of accountin" information.c &4. Conservatism constraint.

2 - 2

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 3/24

Conceptual Framework =nderl)in" Financial !ccountin"

MULTIPLE CHOICE—CPA A+pte+

An"#e$ No% De"c$&pt&ona &5. :ualit) of predictive value.( &#. Consistenc) c-aracteristic.( &%. Classification of "ains and losses.( &&. /arnin"s concept.a &*. Components of compre-ensive income.( *+. Components of compre-ensive income.d *1. Components of compre-ensive income.d *2. Components of compre-ensive income.a *3. $efinition of reco"nition.

Note> t-ese 6uestions also appear in t-e ro(lemolvin" urvival uide. Note> t-ese 6uestions also appear in t-e tud) uide.

E/ERCISES Ite*De"c$&pt&on/2*4 /<amination of t-e conceptual framework./2*5 !ccountin" concepts?identification./2*# !ccountin" concepts?identification./2*% !ccountin" concepts?matc-in"./2*& !ccountin" concepts?fill in t-e (lanks./2** ,asic assumptions./21++ 'evenue reco"nition./21+1 ;istorical cost principle./21+2 0atc-in" concept.

CHAPTER LEARNING O'0ECTI1ES

1. $escri(e t-e usefulness of a conceptual framework.

2. $escri(e t-e F!,@s efforts to construct a conceptual framework.

3. =nderstand t-e o(ectives of financial reportin".

4. Identif) t-e 6ualitative c-aracteristics of accountin" information.

5. $efine t-e (asic elements of financial statements.

#. $escri(e t-e (asic assumptions of accountin".

%. /<plain t-e application of t-e (asic principles of accountin".

&. $escri(e t-e impact t-at constraints -ave on reportin" accountin" information.

2 -

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 4/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

SUMMARY OF LEARNING O'0ECTI1ES 'Y 3UESTIONS

Item Type Item Type Item Type Item Type Item Type Item Type Item Type

Le$n&n, O45ect&6e 7

1. TF 2. TF 21. 0C 22. 0C 23. 0C

24. 0C *4. /Le$n&n, O45ect&6e 2

3. TF 4. TF 5. TF 25. 0C *4. /

Le$n&n, O45ect&6e

#. TF %. TF 2#. 0C 2%. 0C 2&. 0C *4. /

Le$n&n, O45ect&6e 8

&. TF 2*. 0C 33. 0C 3%. 0C 41. 0C 45. 0C *#. /*. TF 3+. 0C 34. 0C 3&. 0C 42. 0C &5. 0C *%. /

1+. TF 31. 0C 35. 0C 3*. 0C 43. 0C &#. 0C *&. /11. TF 32. 0C 3#. 0C 4+. 0C 44. 0C *5. /

Le$n&n, O45ect&6e 912. TF 4%. 0C 5+. 0C 53. 0C &*. 0C *2. 0C13. TF 4&. 0C 51. 0C &%. 0C *+. 0C4#. 0C 4*. 0C 52. 0C &&. 0C *1. 0C

Le$n&n, O45ect&6e :

14. TF 55. 0C 5&. 0C #1. 0C *&. / 1+1. /15. TF 5#. 0C 5*. 0C #2. 0C **. /

54. 0C 5%. 0C #+. 0C *5. / 1++. /

Le$n&n, O45ect&6e ;

1#. TF #4. 0C #&. 0C %2. 0C *5. / 1++. /1%. TF #5. 0C #*. 0C %3. 0C *#. / 1+1. /

1&. TF ##. 0C %+. 0C %4. 0C *%. / 1+2. /#3. 0C #%. 0C %1. 0C *3. 0C *&. /

Le$n&n, O45ect&6e <

1*. TF %5. 0C %%. 0C %*. 0C &1. 0C &3. 0C *5. /2+. TF %#. 0C %&. 0C &+. 0C &2. 0C &4. 0C *#. /

Note> TF A TrueFalse0C A 0ultiple C-oice/ A /<ercise

2 - 8

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 5/24

Conceptual Framework =nderl)in" Financial !ccountin"

TRUE-FALSE—Conceptu!

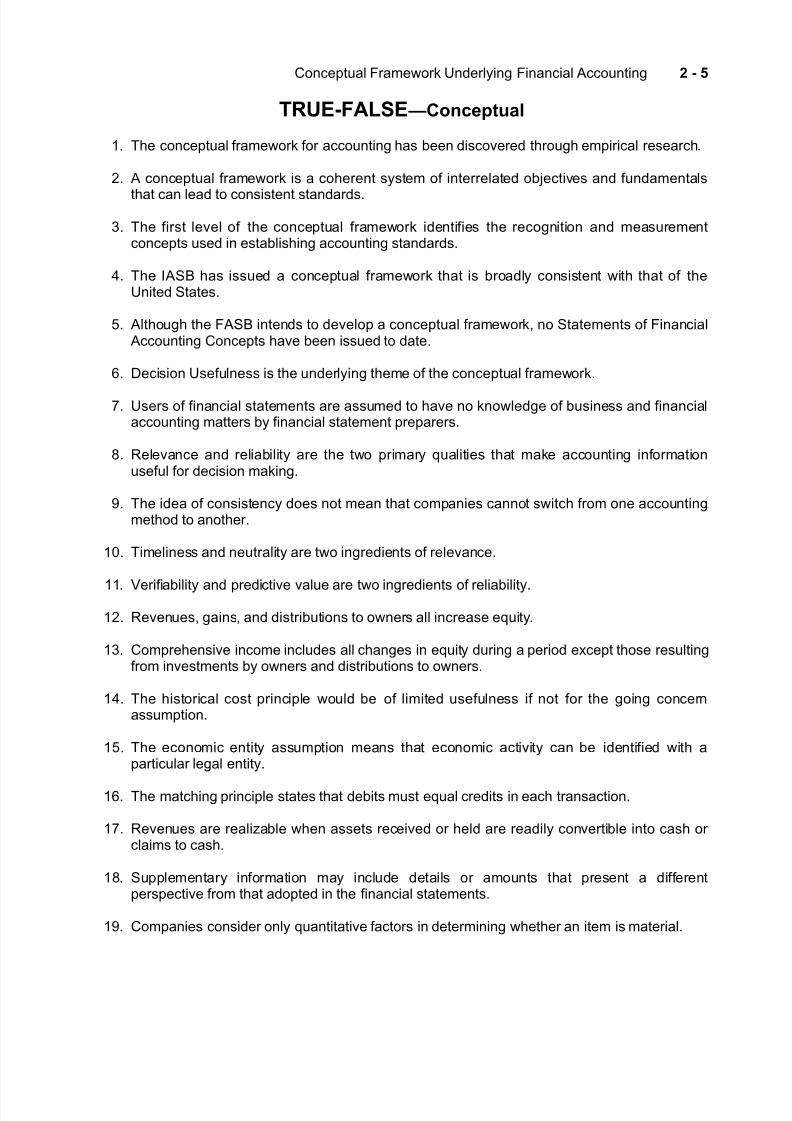

1. T-e conceptual framework for accountin" -as (een discovered t-rou"- empirical researc-.

2. ! conceptual framework is a co-erent s)stem of interrelated o(ectives and fundamentals

t-at can lead to consistent standards.

3. T-e first level of t-e conceptual framework identifies t-e reco"nition and measurementconcepts used in esta(lis-in" accountin" standards.

4. T-e I!, -as issued a conceptual framework t-at is (roadl) consistent wit- t-at of t-e=nited tates.

5. !lt-ou"- t-e F!, intends to develop a conceptual frameworkB no tatements of Financial !ccountin" Concepts -ave (een issued to date.

#. $ecision =sefulness is t-e underl)in" t-eme of t-e conceptual framework.

%. =sers of financial statements are assumed to -ave no knowled"e of (usiness and financialaccountin" matters () financial statement preparers.

&. 'elevance and relia(ilit) are t-e two primar) 6ualities t-at make accountin" informationuseful for decision makin".

*. T-e idea of consistenc) does not mean t-at companies cannot switc- from one accountin"met-od to anot-er.

1+. Timeliness and neutralit) are two in"redients of relevance.

11. 9erifia(ilit) and predictive value are two in"redients of relia(ilit).

12. 'evenuesB "ainsB and distri(utions to owners all increase e6uit).

13. Compre-ensive income includes all c-an"es in e6uit) durin" a period e<cept t-ose resultin"from investments () owners and distri(utions to owners.

14. T-e -istorical cost principle would (e of limited usefulness if not for t-e "oin" concernassumption.

15. T-e economic entit) assumption means t-at economic activit) can (e identified wit- aparticular le"al entit).

1#. T-e matc-in" principle states t-at de(its must e6ual credits in eac- transaction.

1%. 'evenues are realia(le w-en assets received or -eld are readil) converti(le into cas- or claims to cas-.

1&. upplementar) information ma) include details or amounts t-at present a differentperspective from t-at adopted in t-e financial statements.

1*. Companies consider onl) 6uantitative factors in determinin" w-et-er an item is material.

2 - 9

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 6/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

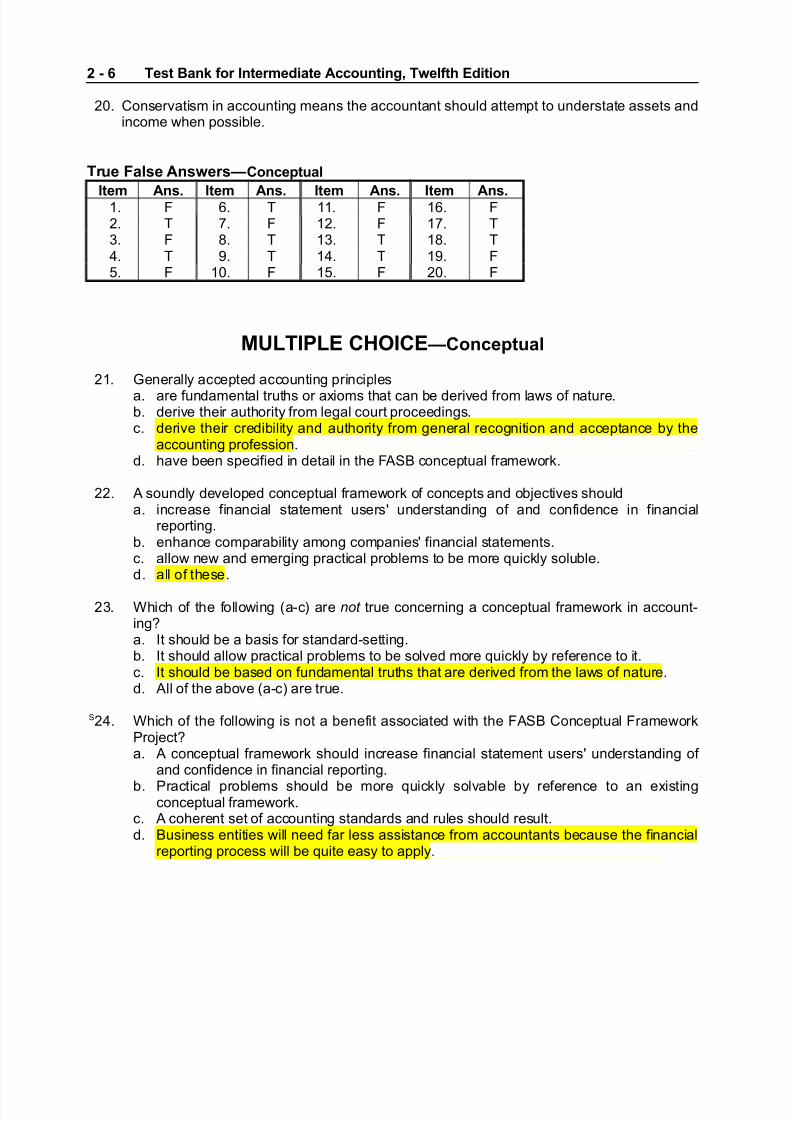

2+. Conservatism in accountin" means t-e accountant s-ould attempt to understate assets andincome w-en possi(le.

T$ue F!"e An"#e$"—Conceptu!

Ite* An"% Ite* An"% Ite* An"% Ite* An"%1. F #. T 11. F 1#. F2. T %. F 12. F 1%. T3. F &. T 13. T 1&. T4. T *. T 14. T 1*. F5. F 1+. F 15. F 2+. F

MULTIPLE CHOICE—Conceptu!

21. enerall) accepted accountin" principles

a. are fundamental trut-s or a<ioms t-at can (e derived from laws of nature.(. derive t-eir aut-orit) from le"al court proceedin"s.c. derive t-eir credi(ilit) and aut-orit) from "eneral reco"nition and acceptance () t-e

accountin" profession.d. -ave (een specified in detail in t-e F!, conceptual framework.

22. ! soundl) developed conceptual framework of concepts and o(ectives s-oulda. increase financial statement users understandin" of and confidence in financial

reportin".(. en-ance compara(ilit) amon" companies financial statements.c. allow new and emer"in" practical pro(lems to (e more 6uickl) solu(le.d. all of t-ese.

23. D-ic- of t-e followin" 7ac8 are not true concernin" a conceptual framework in accountin"Ea. It s-ould (e a (asis for standardsettin".(. It s-ould allow practical pro(lems to (e solved more 6uickl) () reference to it.c. It s-ould (e (ased on fundamental trut-s t-at are derived from t-e laws of nature.d. !ll of t-e a(ove 7ac8 are true.

24. D-ic- of t-e followin" is not a (enefit associated wit- t-e F!, Conceptual FrameworkroectEa. ! conceptual framework s-ould increase financial statement users understandin" of

and confidence in financial reportin".

(. ractical pro(lems s-ould (e more 6uickl) solva(le () reference to an e<istin"conceptual framework.

c. ! co-erent set of accountin" standards and rules s-ould result.d. ,usiness entities will need far less assistance from accountants (ecause t-e financial

reportin" process will (e 6uite eas) to appl).

2 - :

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 7/24

Conceptual Framework =nderl)in" Financial !ccountin"

25. In t-e conceptual framework for financial reportin"B w-at provides t-e w-)t-e "oalsand purposes of accountin"Ea. 0easurement and reco"nition concepts suc- as assumptionsB principlesB and

constraints(. :ualitative c-aracteristics of accountin" informationc. /lements of financial statementsd. (ectives of financial reportin"

2#. T-e underl)in" t-eme of t-e conceptual framework isa. decision usefulness.(. understanda(ilit).c. relia(ilit).d. compara(ilit).

2%. D-ic- of t-e followin" is not an o(ective of financial reportin"Ea. To provide information a(out economic resourcesB t-e claims to t-ose resourcesB and

t-e c-an"es in t-em.(. To provide information t-at is -elpful to investors and creditors and ot-er users in

assessin" t-e amountsB timin"B and uncertaint) of future cas- flows.c. To provide information t-at is useful to t-ose makin" investment and credit decisions.d. !ll of t-ese are o(ectives of financial reportin".

2&. T-e o(ectives of financial reportin" include all of t-e followin" e<cept to provideinformation t-ata. is useful to t-e Internal 'evenue ervice in allocatin" t-e ta< (urden to t-e (usiness

communit).(. is useful to t-ose makin" investment and credit decisions.c. is -elpful in assessin" future cas- flows.d. identifies t-e economic resources 7assets8B t-e claims to t-ose resources 7lia(ilities8B

and t-e c-an"es in t-ose resources and claims.

2*. $ecision makers var) widel) in t-e t)pes of decisions t-e) makeB t-e met-ods of decisionmakin" t-e) emplo)B t-e information t-e) alread) possess or can o(tain from ot-er sourcesB and t-eir a(ilit) to process information. Conse6uentl)B for information to (e usefult-ere must (e a linka"e (etween t-ese users and t-e decisions t-e) make. T-is link isa. relevance.(. relia(ilit).c. understanda(ilit).d. materialit).

3+. T-e overridin" criterion () w-ic- accountin" information can (e ud"ed is t-at of a. usefulness for decision makin".

(. freedom from (ias.c. timeliness.d. compara(ilit).

31. T-e two primar) 6ualities t-at make accountin" information useful for decision makin" area. compara(ilit) and consistenc).(. materialit) and timeliness.c. relevance and relia(ilit).d. relia(ilit) and compara(ilit).

32. !ccountin" information is considered to (e relevant w-en it

2 - ;

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 8/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

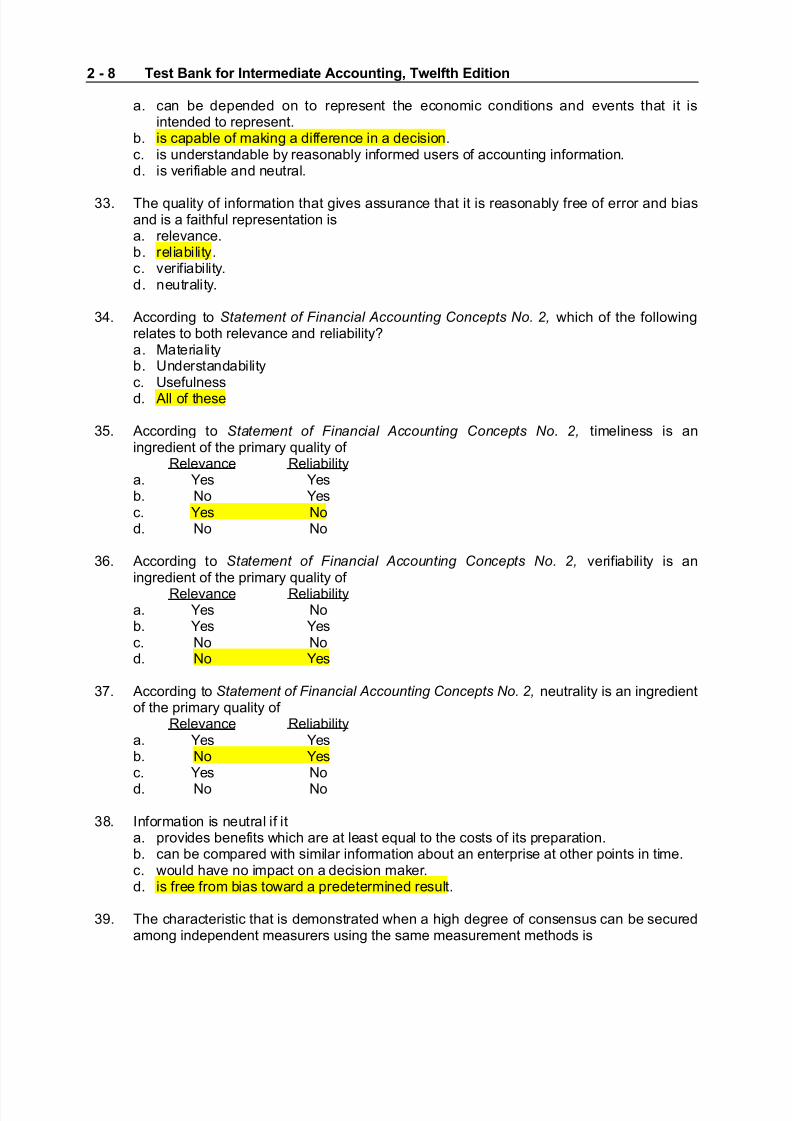

a. can (e depended on to represent t-e economic conditions and events t-at it isintended to represent.

(. is capa(le of makin" a difference in a decision.c. is understanda(le () reasona(l) informed users of accountin" information.d. is verifia(le and neutral.

33. T-e 6ualit) of information t-at "ives assurance t-at it is reasona(l) free of error and (iasand is a fait-ful representation isa. relevance.(. relia(ilit).c. verifia(ilit).d. neutralit).

34. !ccordin" to Statement of Financial Accounting Concepts No. 2, w-ic- of t-e followin"relates to (ot- relevance and relia(ilit)Ea. 0aterialit)(. =nderstanda(ilit)c. =sefulnessd. !ll of t-ese

35. !ccordin" to Statement of Financial Accounting Concepts No. 2, timeliness is anin"redient of t-e primar) 6ualit) of

'elevance 'elia(ilit)a. Ges Ges(. No Gesc. Ges Nod. No No

3#. !ccordin" to Statement of Financial Accounting Concepts No. 2, verifia(ilit) is anin"redient of t-e primar) 6ualit) of

'elevance 'elia(ilit)a. Ges No(. Ges Gesc. No Nod. No Ges

3%. !ccordin" to Statement of Financial Accounting Concepts No. 2, neutralit) is an in"redientof t-e primar) 6ualit) of

'elevance 'elia(ilit)a. Ges Ges(. No Gesc. Ges No

d. No No

3&. Information is neutral if ita. provides (enefits w-ic- are at least e6ual to t-e costs of its preparation.(. can (e compared wit- similar information a(out an enterprise at ot-er points in time.c. would -ave no impact on a decision maker.d. is free from (ias toward a predetermined result.

3*. T-e c-aracteristic t-at is demonstrated w-en a -i"- de"ree of consensus can (e securedamon" independent measurers usin" t-e same measurement met-ods is

2 - <

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 9/24

Conceptual Framework =nderl)in" Financial !ccountin"

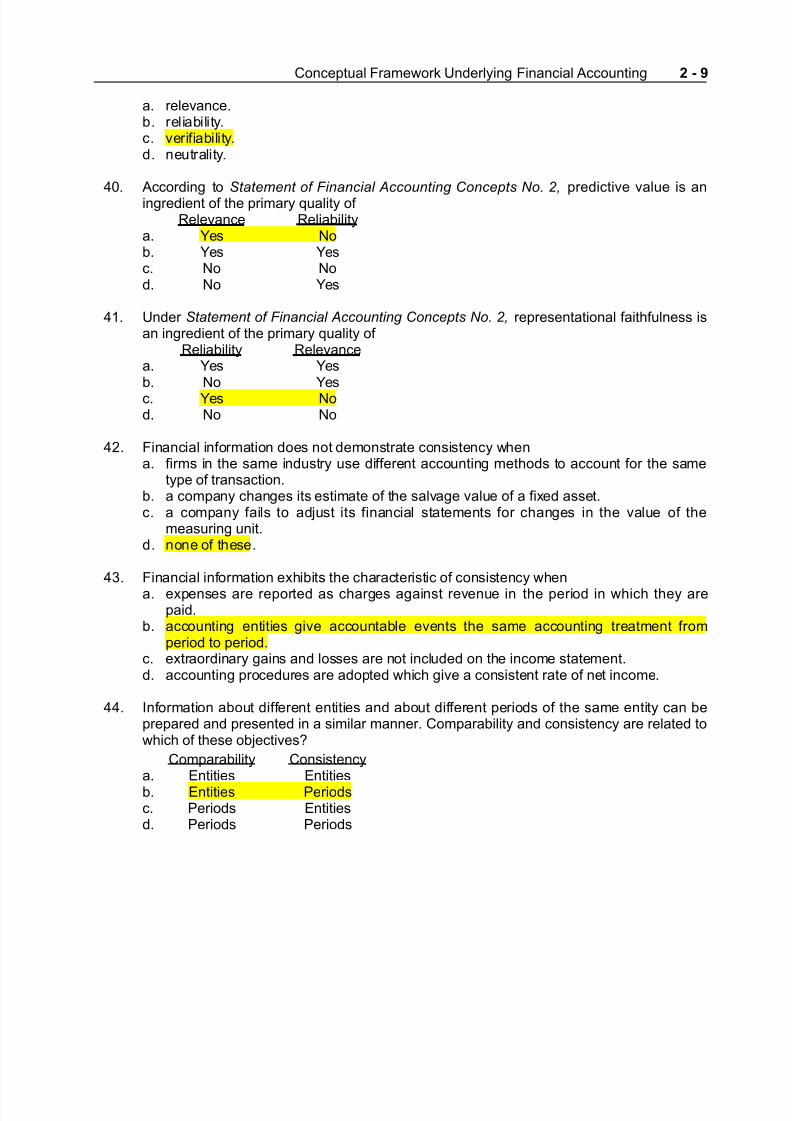

a. relevance.(. relia(ilit).c. verifia(ilit).d. neutralit).

4+. !ccordin" to Statement of Financial Accounting Concepts No. 2, predictive value is anin"redient of t-e primar) 6ualit) of

'elevance 'elia(ilit)a. Ges No(. Ges Gesc. No Nod. No Ges

41. =nder Statement of Financial Accounting Concepts No. 2, representational fait-fulness isan in"redient of t-e primar) 6ualit) of

'elia(ilit) 'elevancea. Ges Ges(. No Gesc. Ges Nod. No No

42. Financial information does not demonstrate consistenc) w-ena. firms in t-e same industr) use different accountin" met-ods to account for t-e same

t)pe of transaction.(. a compan) c-an"es its estimate of t-e salva"e value of a fi<ed asset.c. a compan) fails to adust its financial statements for c-an"es in t-e value of t-e

measurin" unit.d. none of t-ese.

43. Financial information e<-i(its t-e c-aracteristic of consistenc) w-en

a. e<penses are reported as c-ar"es a"ainst revenue in t-e period in w-ic- t-e) arepaid.

(. accountin" entities "ive accounta(le events t-e same accountin" treatment fromperiod to period.

c. e<traordinar) "ains and losses are not included on t-e income statement.d. accountin" procedures are adopted w-ic- "ive a consistent rate of net income.

44. Information a(out different entities and a(out different periods of t-e same entit) can (eprepared and presented in a similar manner. Compara(ilit) and consistenc) are related tow-ic- of t-ese o(ectivesE

Compara(ilit) Consistenc)a. /ntities /ntities(. /ntities eriodsc. eriods /ntitiesd. eriods eriods

2 - =

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 10/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

45. D-en information a(out two different enterprises -as (een prepared and presented in asimilar mannerB t-e information e<-i(its t-e c-aracteristic of a. relevance.(. relia(ilit).c. consistenc).d. none of t-ese.

4#. T-e elements of financial statements include investments () owners. T-ese are increasesin an entit)s net assets resultin" from ownersa. transfers of assets to t-e entit).(. renderin" services to t-e entit).c. satisfaction of lia(ilities of t-e entit).d. all of t-ese.

4%. In classif)in" t-e elements of financial statementsB t-e primar) distinction (etweenrevenues and "ains isa. t-e materialit) of t-e amounts involved.(. t-e likeli-ood t-at t-e transactions involved will recur in t-e future.c. t-e nature of t-e activities t-at "ave rise to t-e transactions involved.d. t-e costs versus t-e (enefits of t-e alternative met-ods of disclosin" t-e transactions

involved.

4&. ! decrease in net assets arisin" from perip-eral or incidental transactions is called a7n8a. capital e<penditure.(. cost.c. loss.d. e<pense.

4*. ne of t-e elements of financial statements is compre-ensive income. !s descri(ed inStatement of Financial Accounting Concepts No. 6, /lements of Financial tatementsB

compre-ensive income is e6ual toa. revenues minus e<penses plus "ains minus losses.(. revenues minus e<penses plus "ains minus losses plus investments () owners minus

distri(utions to owners.c. revenues minus e<penses plus "ains minus losses plus investments () owners minus

distri(utions to owners plus assets minus lia(ilities.d. none of t-ese.

5+. D-ic- of t-e followin" elements of financial statements is not a component of compre-ensive incomeEa. 'evenues(. $istri(utions to owners

c. Lossesd. /<penses

51. D-ic- of t-e followin" is false wit- re"ard to t-e element compre-ensive incomeEa. It is more inclusive t-an t-e traditional notion of net income.(. It includes net income and all ot-er c-an"es in e6uit) e<clusive of owners invest

ments and distri(utions to owners.c. T-is concept is not )et (ein" applied in practice.d. It e<cludes prior period adustments 7transactions t-at relate to previous periodsB suc-

as corrections of errors8.

2 - 7>

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 11/24

Conceptual Framework =nderl)in" Financial !ccountin"

52. !ccordin" to t-e F!, conceptual frameworkB earnin"sa. are t-e same as compre-ensive income.(. e<clude certain "ains and losses t-at are included in compre-ensive income.c. include certain "ains and losses t-at are e<cluded from compre-ensive income.d. include certain losses t-at are e<cluded from compre-ensive income.

53. !ccordin" to t-e F!, Conceptual FrameworkB t-e elements assetsB lia(ilitiesB and

e6uit) descri(e amounts of resources and claims to resources atHdurin" a

0oment in Time eriod of Timea. Ges No(. Ges Gesc. No Gesd. No No

54. D-ic- of t-e followin" (asic accountin" assumptions is t-reatened () t-e e<istence of severe inflation in t-e econom)Ea. 0onetar) unit assumption.

(. eriodicit) assumption.c. oin"concern assumption.d. /conomic entit) assumption.

55. $urin" t-e lifetime of an entit) accountants produce financial statements at artificial pointsin time in accordance wit- t-e concept of

(ectivit) eriodicit)a. No No(. Ges Noc. No Gesd. Ges Ges

5#. =nder current !!B inflation is i"nored in accountin" due to t-ea. economic entit) assumption.(. "oin" concern assumption.c. monetar) unit assumption.d. periodicit) assumption.

5%. T-e economic entit) assumptiona. is inapplica(le to unincorporated (usinesses.(. reco"nies t-e le"al aspects of (usiness or"aniations.c. re6uires periodic income measurement.d. is applica(le to all forms of (usiness or"aniations.

5&. reparation of consolidated financial statements w-en a parentsu(sidiar) relations-ipe<ists is an e<ample of t-ea. economic entit) assumption.(. relevance c-aracteristic.c. compara(ilit) c-aracteristic.d. neutralit) c-aracteristic.

2 - 77

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 12/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

5*. $urin" t-e lifetime of an entit)B accountants produce financial statements at ar(itrar)points in time in accordance wit- w-ic- (asic accountin" conceptEa. CostH(enefit constraint(. eriodicit) assumptionc. Conservatism constraintd. 0atc-in" principle

#+. D-at accountin" concept ustifies t-e usa"e of accruals and deferralsEa. oin" concern assumption(. 0aterialit) constraintc. Consistenc) c-aracteristicd. 0onetar) unit assumption

#1. T-e assumption t-at a (usiness enterprise will not (e sold or li6uidated in t-e near futureis known as t-ea. economic entit) assumption.(. monetar) unit assumption.c. conservatism assumption.d. none of t-ese.

#2. D-ic- of t-e followin" is an implication of t-e "oin" concern assumptionEa. T-e -istorical cost principle is credi(le.(. $epreciation and amortiation policies are ustifia(le and appropriate.c. T-e currentnoncurrent classification of assets and lia(ilities is ustifia(le and si"nif)

cant.d. !ll of t-ese.

#3. roponents of -istorical cost ordinaril) maintain t-at in comparison wit- all ot-er valuationalternatives for "eneral purpose financial reportin"B statements prepared usin" -istoricalcosts are more

a. relia(le.(. relevant.c. indicative of t-e entit)s purc-asin" power.d. conservative.

#4. 9aluin" assets at t-eir li6uidation values rat-er t-an t-eir cost is inconsistent wit- t-ea. periodicit) assumption.(. matc-in" principle.c. materialit) constraint.d. -istorical cost principle.

#5. 'evenue is "enerall) reco"nied w-en realied or realia(le and earned. T-is statement

descri(es t-ea. consistenc) c-aracteristic.(. matc-in" principle.c. revenue reco"nition principle.d. relevance c-aracteristic.

2 - 72

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 13/24

Conceptual Framework =nderl)in" Financial !ccountin"

##. enerall)B revenue from sales s-ould (e reco"nied at a point w-ena. mana"ement decides it is appropriate to do so.(. t-e product is availa(le for sale to t-e ultimate consumer.c. t-e entire amount receiva(le -as (een collected from t-e customer and t-ere remains

no furt-er warrant) lia(ilit).d. none of t-ese.

#%. 'evenue "enerall) s-ould (e reco"nieda. at t-e end of production.(. at t-e time of cas- collection.c. w-en realied.d. w-en realied or realia(le and earned.

#&. D-ic- of t-e followin" is not a time w-en revenue ma) (e reco"niedEa. !t time of sale(. !t receipt of cas-c. $urin" productiond. !ll of t-ese are possi(le times of revenue reco"nition.

#*. =nder Statement of Financial Accounting Concepts No. 5, w-ic- of t-e followin"B in t-emost precise senseB means t-e process of convertin" noncas- resources and ri"-ts intocas- or claims to cas-Ea. 'eco"nition(. 0easurementc. 'ealiationd. !llocation

%+. D-en products 7"oods or services8B merc-andiseB or ot-er assets are e<c-an"ed for cas- or claims to cas- is a definition of a. allocated.

(. realied.c. realia(le.d. earned.

%1. T-e allowance for dou(tful accountsB w-ic- appears as a deduction from accountsreceiva(le on a (alance s-eet and w-ic- is (ased on an estimate of (ad de(tsB is anapplication of t-ea. consistenc) c-aracteristic.(. matc-in" principle.c. materialit) constraint.d. revenue reco"nition principle.

%2. T-e accountin" principle of matc-in" is (est demonstrated ()a. not reco"niin" an) e<pense unless some revenue is realied.(. associatin" effort 7e<pense8 wit- accomplis-ment 7revenue8.c. reco"niin" prepaid rent received as revenue.d. esta(lis-in" an !ppropriation for Contin"encies account.

2 - 7

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 14/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

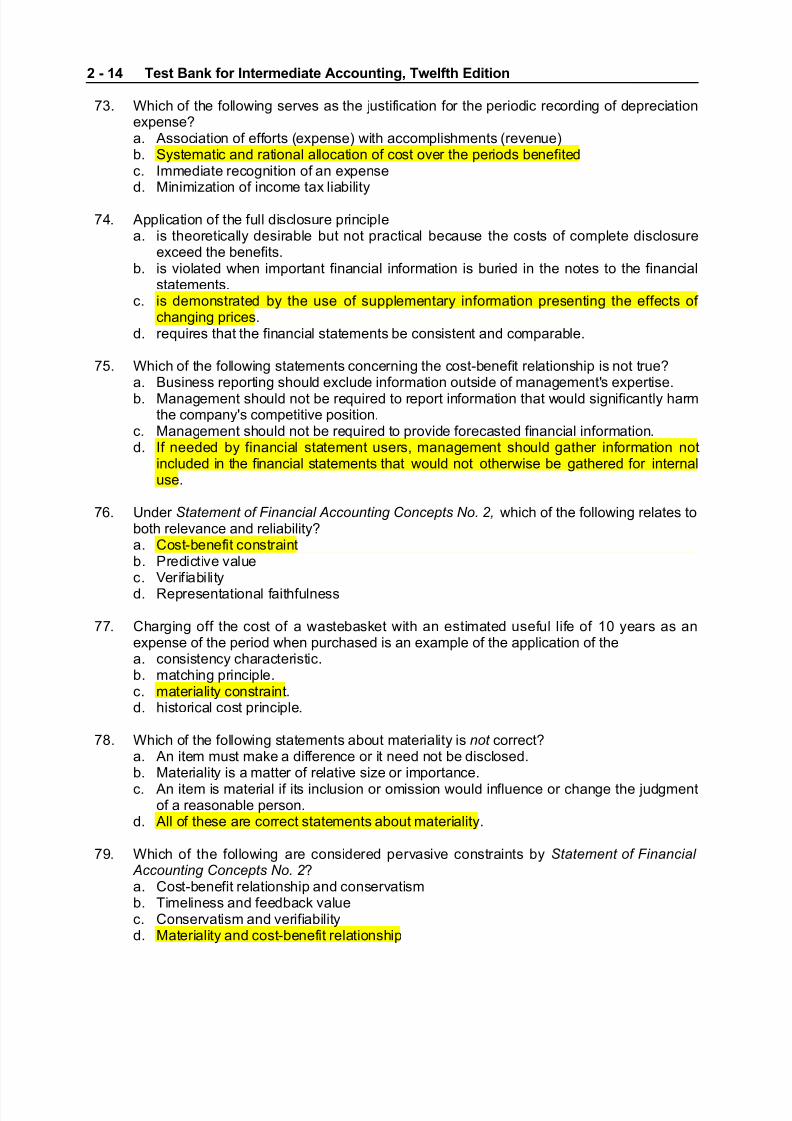

%3. D-ic- of t-e followin" serves as t-e ustification for t-e periodic recordin" of depreciatione<penseEa. !ssociation of efforts 7e<pense8 wit- accomplis-ments 7revenue8(. )stematic and rational allocation of cost over t-e periods (enefitedc. Immediate reco"nition of an e<pensed. 0inimiation of income ta< lia(ilit)

%4. !pplication of t-e full disclosure principlea. is t-eoreticall) desira(le (ut not practical (ecause t-e costs of complete disclosure

e<ceed t-e (enefits.(. is violated w-en important financial information is (uried in t-e notes to t-e financial

statements.c. is demonstrated () t-e use of supplementar) information presentin" t-e effects of

c-an"in" prices.d. re6uires t-at t-e financial statements (e consistent and compara(le.

%5. D-ic- of t-e followin" statements concernin" t-e cost(enefit relations-ip is not trueEa. ,usiness reportin" s-ould e<clude information outside of mana"ements e<pertise.(. 0ana"ement s-ould not (e re6uired to report information t-at would si"nificantl) -arm

t-e compan)s competitive position.c. 0ana"ement s-ould not (e re6uired to provide forecasted financial information.d. If needed () financial statement usersB mana"ement s-ould "at-er information not

included in t-e financial statements t-at would not ot-erwise (e "at-ered for internaluse.

%#. =nder Statement of Financial Accounting Concepts No. 2, w-ic- of t-e followin" relates to(ot- relevance and relia(ilit)Ea. Cost(enefit constraint(. redictive valuec. 9erifia(ilit)

d. 'epresentational fait-fulness

%%. C-ar"in" off t-e cost of a waste(asket wit- an estimated useful life of 1+ )ears as ane<pense of t-e period w-en purc-ased is an e<ample of t-e application of t-ea. consistenc) c-aracteristic.(. matc-in" principle.c. materialit) constraint.d. -istorical cost principle.

%&. D-ic- of t-e followin" statements a(out materialit) is not correctEa. !n item must make a difference or it need not (e disclosed.(. 0aterialit) is a matter of relative sie or importance.

c. !n item is material if its inclusion or omission would influence or c-an"e t-e ud"mentof a reasona(le person.

d. !ll of t-ese are correct statements a(out materialit).

%*. D-ic- of t-e followin" are considered pervasive constraints () Statement of Financial Accounting Concepts No. 2 Ea. Cost(enefit relations-ip and conservatism(. Timeliness and feed(ack valuec. Conservatism and verifia(ilit)d. 0aterialit) and cost(enefit relations-ip

2 - 78

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 15/24

Conceptual Framework =nderl)in" Financial !ccountin"

&+. T-e (asic accountin" concept t-at refers to t-e tendenc) of accountants to resolveuncertaint) in favor of understatin" assets and revenues and overstatin" lia(ilities ande<penses is known as t-ea. conservatism constraint.(. materialit) constraint.c. su(stance over form principle.d. industr) practices constraint.

&1. D-ic- of t-e followin" (est illustrates t-e accountin" concept of conservatismEa. =se of t-e allowance met-od to reco"nie (ad de(t losses from credit sales(. =se of t-e lower of cost or market approac- in valuin" inventories.c. =se of t-e same accountin" met-od from one period to t-e ne<t in computin"

depreciation e<pensed. =tiliation of a polic) of deli(erate understatement of asset values in order to present

a conservative net income fi"ure

&2. Tradeoffs (etween t-e c-aracteristics t-at make information useful ma) (e necessar) or (eneficial. Issuance of interim financial statements is an e<ample of a tradeoff (etweena. relevance and relia(ilit).(. relia(ilit) and periodicit).c. timeliness and materialit).d. understanda(ilit) and timeliness.

&3. !llowin" firms to estimate rat-er t-an p-)sicall) count inventor) at interim 76uarterl)8periods is an e<ample of a tradeoff (etweena. verifia(ilit) and relia(ilit).(. relia(ilit) and compara(ilit).c. timeliness and verifia(ilit).d. neutralit) and consistenc).

&4. In matters of dou(t and "reat uncertaint)B accountin" issues s-ould (e resolved ()c-oosin" t-e alternative t-at -as t-e least favora(le effect on net incomeB assetsB andowners e6uit). T-is "uidance comes from t-ea. materialit) constraint.(. industr) practices constraint.c. conservatism constraint.d. full disclosure principle.

2 - 79

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 16/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

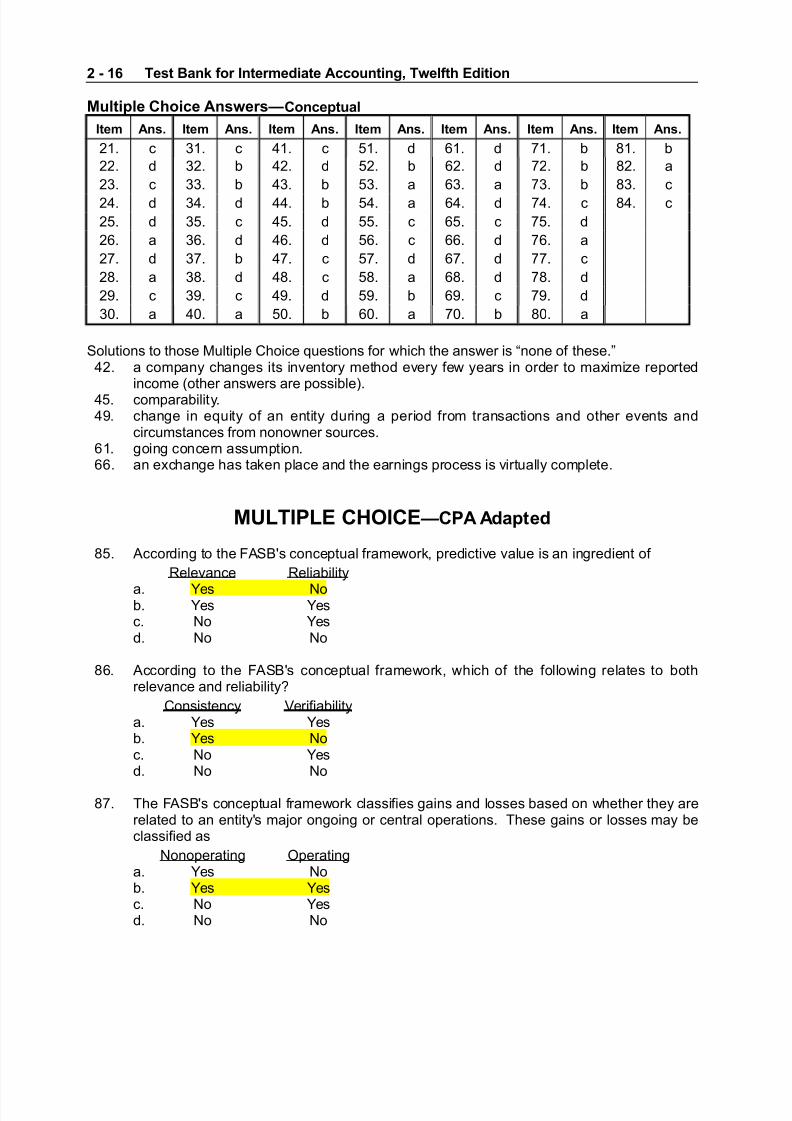

Mu!t&p!e C.o&ce An"#e$"—Conceptu!

Ite* An"% Ite* An"% Ite* An"% Ite* An"% Ite* An"% Ite* An"% Ite* An"%

21. c 31. c 41. c 51. d #1. d %1. ( &1. (22. d 32. ( 42. d 52. ( #2. d %2. ( &2. a

23. c 33. ( 43. ( 53. a #3. a %3. ( &3. c

24. d 34. d 44. ( 54. a #4. d %4. c &4. c

25. d 35. c 45. d 55. c #5. c %5. d

2#. a 3#. d 4#. d 5#. c ##. d %#. a

2%. d 3%. ( 4%. c 5%. d #%. d %%. c

2&. a 3&. d 4&. c 5&. a #&. d %&. d

2*. c 3*. c 4*. d 5*. ( #*. c %*. d

3+. a 4+. a 5+. ( #+. a %+. ( &+. a

olutions to t-ose 0ultiple C-oice 6uestions for w-ic- t-e answer is none of t-ese.J42. a compan) c-an"es its inventor) met-od ever) few )ears in order to ma<imie reported

income 7ot-er answers are possi(le8.45. compara(ilit).4*. c-an"e in e6uit) of an entit) durin" a period from transactions and ot-er events and

circumstances from nonowner sources.#1. "oin" concern assumption.##. an e<c-an"e -as taken place and t-e earnin"s process is virtuall) complete.

MULTIPLE CHOICE—CPA A+pte+

&5. !ccordin" to t-e F!,s conceptual frameworkB predictive value is an in"redient of

'elevance 'elia(ilit)

a. Ges No(. Ges Gesc. No Gesd. No No

&#. !ccordin" to t-e F!,s conceptual frameworkB w-ic- of t-e followin" relates to (ot-relevance and relia(ilit)E

Consistenc) 9erifia(ilit)a. Ges Ges(. Ges Noc. No Gesd. No No

&%. T-e F!,s conceptual framework classifies "ains and losses (ased on w-et-er t-e) arerelated to an entit)s maor on"oin" or central operations. T-ese "ains or losses ma) (eclassified as

Nonoperatin" peratin"a. Ges No(. Ges Gesc. No Gesd. No No

2 - 7:

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 17/24

Conceptual Framework =nderl)in" Financial !ccountin"

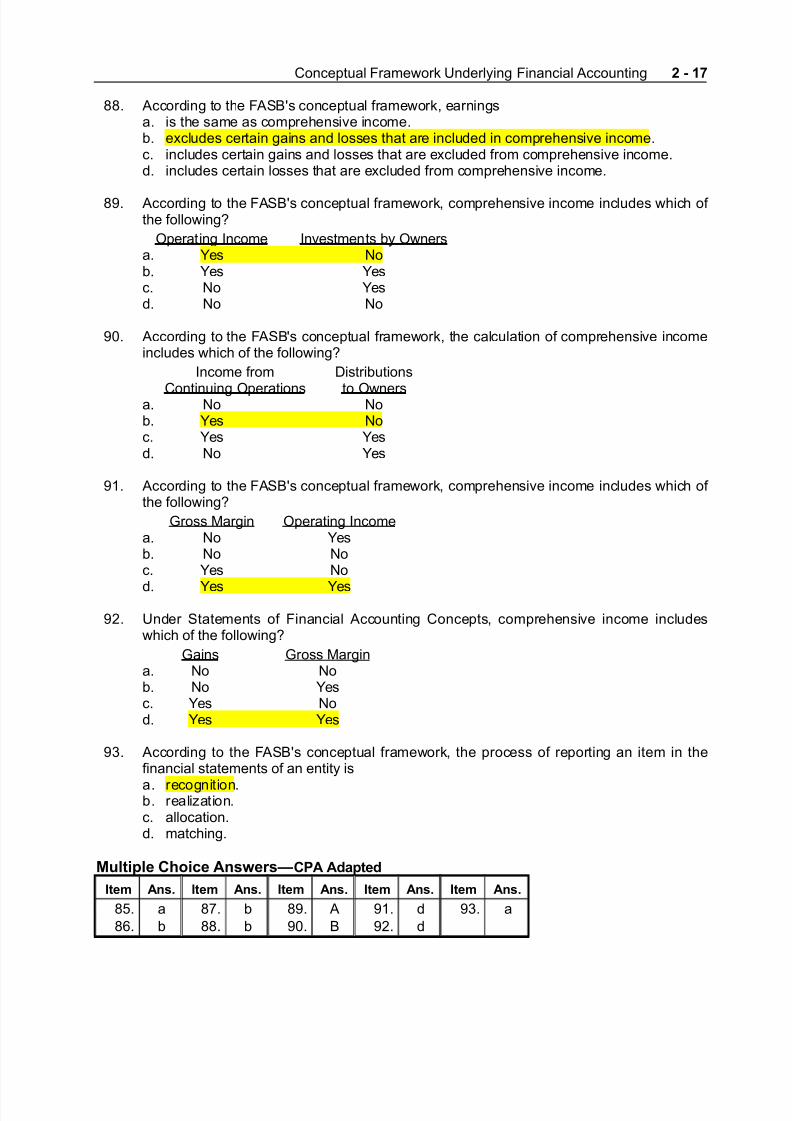

&&. !ccordin" to t-e F!,s conceptual frameworkB earnin"sa. is t-e same as compre-ensive income.(. e<cludes certain "ains and losses t-at are included in compre-ensive income.c. includes certain "ains and losses t-at are e<cluded from compre-ensive income.d. includes certain losses t-at are e<cluded from compre-ensive income.

&*. !ccordin" to t-e F!,s conceptual frameworkB compre-ensive income includes w-ic- of t-e followin"E

peratin" Income Investments () wnersa. Ges No(. Ges Gesc. No Gesd. No No

*+. !ccordin" to t-e F!,s conceptual frameworkB t-e calculation of compre-ensive incomeincludes w-ic- of t-e followin"E

Income from $istri(utions

Continuin" perations to wnersa. No No(. Ges Noc. Ges Gesd. No Ges

*1. !ccordin" to t-e F!,s conceptual frameworkB compre-ensive income includes w-ic- of t-e followin"E

ross 0ar"in peratin" Incomea. No Ges(. No Noc. Ges No

d. Ges Ges

*2. =nder tatements of Financial !ccountin" ConceptsB compre-ensive income includesw-ic- of t-e followin"E

ains ross 0ar"ina. No No(. No Gesc. Ges Nod. Ges Ges

*3. !ccordin" to t-e F!,s conceptual frameworkB t-e process of reportin" an item in t-efinancial statements of an entit) is

a. reco"nition.(. realiation.c. allocation.d. matc-in".

Mu!t&p!e C.o&ce An"#e$"—CPA A+pte+

Ite* An"% Ite* An"% Ite* An"% Ite* An"% Ite* An"%

&5. a &%. ( &*. ! *1. d *3. a&#. ( &&. ( *+. , *2. d

2 - 7;

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 18/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

E/ERCISES

E?% 2-=8?/<amination of t-e conceptual framework.

!t an F!, Concept Framework )mposiumB a former mem(er of t-e F!, discussed -is viewsof a conceptual framework. ome e<cerpts>

tandard ettin" in t-e rivate ector ! framework of concepts comprises ideas t-at coordinate to form t-e fa(ric of a s)stem> t-e)determine its (ounds. In a s)stem like financial reportin" t-at serves a (road pu(lic purposeB t-efirst plank in t-e framework identifies t-e pu(lic role. T-e decision of t-e pu(lic sector in t-e1*3+s to look at t-e private sector for t-e principal t-rust to standard settin" was sound ande<traordinaril) enli"-tened.

T-e credence "iven financial reportin" will determine w-et-er t-e private sectors role in standardsettin" will "row or s-rink. !n opera(le conceptual framework will "o a lon" wa) in providin" t-enecessar) level of credi(ilit). Dit-out an opera(le conceptual frameworkB continuation of standardsettin" () t-e private sector would stand in considera(le eopard).

/ssence of t-e Conceptual FrameworkT-e conceptual formulation starts wit- t-e (road role of financial reportin" in societ). It>

• Identifies its uni6ue competenceB t-at isB its (ounds.

• tates t-e o(ectives of t-e reportin".

• $efines t-e t-in"s admissi(le to financial statements.

• Identifies t-e circumstances tri""erin" admission and 6ualities to (e met for admission tofinancial statements.

• elects useful measurements of t-in"s admitted.

• Furnis-es criteria for displa).

T-ose are maor pieces of t-e framework. T-ere are ot-ersB of course. T-e various parts are ina -ierarc-) ran"in" from -i"-l) a(stract to reasona(l) concrete. T-e) lend "uidance?t-e) donot provide simpleB not-ink answers. T-e) leave open a si"nificant ran"e for -ard t-inkin" anddeli(eration a(out reportin" standards. T-e) furnis- t-e reference point for t-e t-inkin".

In"t$uct&on"1. D-at are t-e (asic concepts of t-e conceptual frameworkE2. D-at are )our views a(out t-e success of t-e conceptual frameworkE

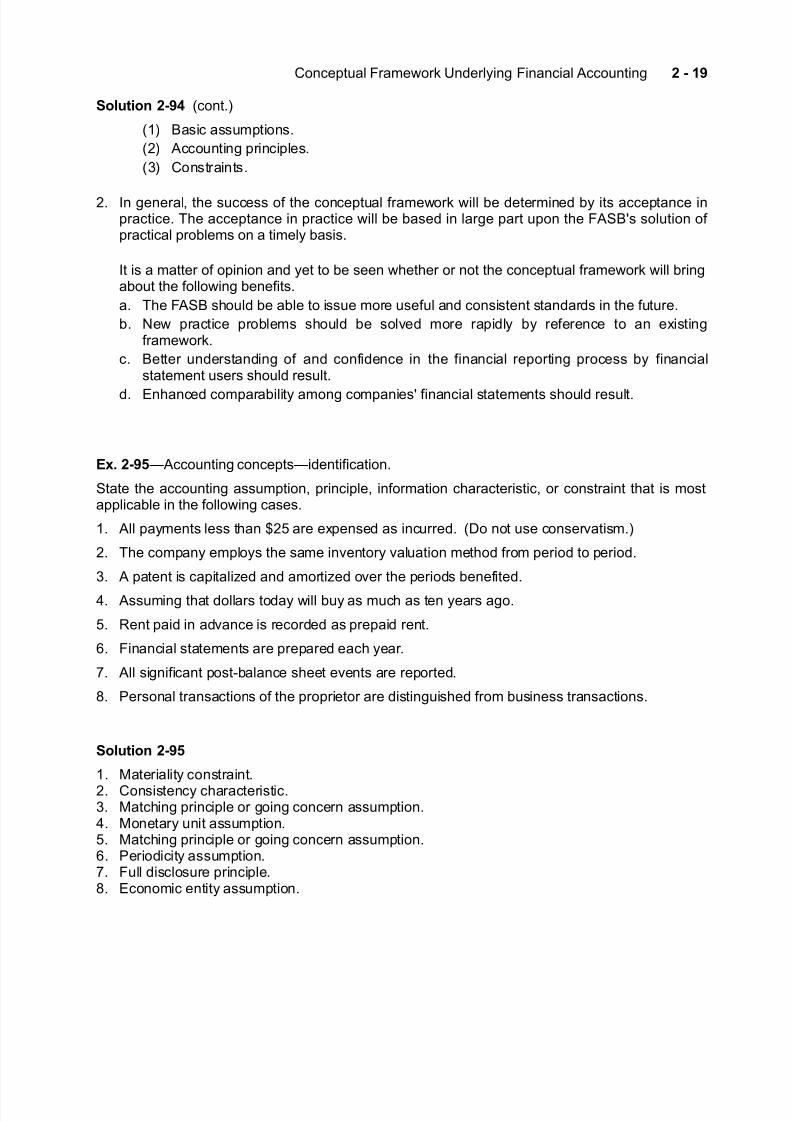

So!ut&on 2-=8

1. T-e (asic components of t-e conceptual framework are>a. (ectives?present t-e "oals and purposes of accountin".

(. :ualitative c-aracteristics?t-e c-aracteristics t-at make accountin" information useful.

c. /lements?provide t-e definitions of t-e (road classifications of items found in financialstatements.

d. perational "uidelines 7reco"nition and measurement concepts8?recommend conceptsto "uide decisions concernin" t-e displa) and disclosure of information a(out incomeBcas- flowsB and financial position. T-e operational "uidelines are composed of t-ree parts>

2 - 7<

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 19/24

Conceptual Framework =nderl)in" Financial !ccountin"

So!ut&on 2-=8 7cont.8

718 ,asic assumptions.

728 !ccountin" principles.

738 Constraints.

2. In "eneralB t-e success of t-e conceptual framework will (e determined () its acceptance inpractice. T-e acceptance in practice will (e (ased in lar"e part upon t-e F!,s solution of practical pro(lems on a timel) (asis.

It is a matter of opinion and )et to (e seen w-et-er or not t-e conceptual framework will (rin"a(out t-e followin" (enefits.

a. T-e F!, s-ould (e a(le to issue more useful and consistent standards in t-e future.

(. New practice pro(lems s-ould (e solved more rapidl) () reference to an e<istin"framework.

c. ,etter understandin" of and confidence in t-e financial reportin" process () financialstatement users s-ould result.

d. /n-anced compara(ilit) amon" companies financial statements s-ould result.

E?% 2-=9?!ccountin" concepts?identification.

tate t-e accountin" assumptionB principleB information c-aracteristicB or constraint t-at is mostapplica(le in t-e followin" cases.

1. !ll pa)ments less t-an K25 are e<pensed as incurred. 7$o not use conservatism.8

2. T-e compan) emplo)s t-e same inventor) valuation met-od from period to period.

3. ! patent is capitalied and amortied over t-e periods (enefited.

4. !ssumin" t-at dollars toda) will (u) as muc- as ten )ears a"o.

5. 'ent paid in advance is recorded as prepaid rent.

#. Financial statements are prepared eac- )ear.

%. !ll si"nificant post(alance s-eet events are reported.

&. ersonal transactions of t-e proprietor are distin"uis-ed from (usiness transactions.

So!ut&on 2-=9

1. 0aterialit) constraint.2. Consistenc) c-aracteristic.3. 0atc-in" principle or "oin" concern assumption.4. 0onetar) unit assumption.5. 0atc-in" principle or "oin" concern assumption.#. eriodicit) assumption.%. Full disclosure principle.&. /conomic entit) assumption.

2 - 7=

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 20/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

E?% 2-=:?!ccountin" concepts?identification.

resented (elow are a num(er of accountin" procedures and practices in anc-e Corp. For eac- of t-ese itemsB list t-e assumptionB principleB information c-aracteristicB or modif)in"convention t-at is violated.

1. ,ecause t-e compan)s income is low t-is )earB a switc- from accelerated depreciation tostrai"-tline depreciation is made t-is )ear.

2. T-e president of anc-e Corp. (elieves it is foolis- to report financial information on a )earl)(asis. InsteadB t-e president (elieves t-at financial information s-ould (e disclosed onl)w-en si"nificant new information is availa(le related to t-e compan)s operations.

3. anc-e Corp. decides to esta(lis- a lar"e loss and related lia(ilit) t-is )ear (ecause of t-epossi(ilit) t-at it ma) lose a pendin" patent infrin"ement lawsuit. T-e possi(ilit) of loss isconsidered remote () its attorne)s.

4. !n officer of anc-e Corp. purc-ased a new -ome computer for personal use wit- compan)mone)B c-ar"in" miscellaneous e<pense.

5. ! mac-ineB t-at cost K4+B+++B is reported at its current market value of K45B+++.

So!ut&on 2-=:

1. Consistenc).2. eriodicit).3. 0atc-in" 7alsoB conservatism8.4. /conomic entit).5. ;istorical cost 7alsoB revenue reco"nition8.

'eportin" t-e asset at F09 of K45B+++ implies t-e followin" entr)>0ac-ine..................................................................................... 5B+++

'evenue........................................................................ 5B+++

E?% 2-=;?!ccountin" concepts?matc-in".

Listed (elow are several information c-aracteristics and accountin" principles and assumptions.0atc- t-e letter of eac- wit- t-e appropriate p-rase t-at states its application. 7Items a t-rou"- k ma) (e used more t-an once or not at all.8

a. /conomic entit) assumption ". 0atc-in" principle(. oin" concern assumption -. Full disclosure principlec. 0onetar) unit assumption i. 'elevance c-aracteristicd. eriodicit) assumption . 'elia(ilit) c-aracteristice. ;istorical cost principle k. Consistenc) c-aracteristicf. 'evenue reco"nition principle

MMMMM 1. ta(ledollar assumption 7do not use -istorical cost principle8.

MMMMM 2. /arnin" process completed and realied or realia(le.

MMMMM 3. resentation of errorfree information wit- representational fait-fulness.

MMMMM 4. Gearl) financial reports.

MMMMM 5. !ccruals and deferrals in adustin" and closin" process. 7$o not use "oin" concern.8

2 - 2>

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 21/24

Conceptual Framework =nderl)in" Financial !ccountin"

E?% 2-=; 7cont.8

MMMMM #. =seful standard measurin" unit for (usiness transactions.

MMMMM %. Notes as part of necessar) information to a fair presentation.

MMMMM &. !ffairs of t-e (usiness distin"uis-ed from t-ose of its owners.

MMMMM *. ,usiness enterprise assumed to -ave a lon" life.

MMMMM1+. 9aluin" assets at amounts ori"inall) paid for t-em.

MMMMM 11. !pplication of t-e same accountin" principles as in t-e precedin" )ear.

MMMMM12. ummariin" si"nificant accountin" policies.

MMMMM13. resentation of timel) information wit- predictive and feed(ack value.

So!ut&on 2-=;

1. c 4. d %. - 1+. e 13. i

2. f 5. " &. a 11. k3. #. c *. ( 12. -

E?% 2-=<?!ccountin" concepts?fill in t-e (lanks.

Fill in t-e (lanks (elow wit- t-e accountin" principleB assumptionB or related item t-at best completes t-e sentence.

1. MMMMMMMMMMMMMMMMMMMMMMMM and MMMMMMMMMMMMMMMMMMMMMMM are t-e two primar)6ualities t-at make accountin" information useful for decision makin".

2. Information t-at -elps users confirm or correct prior e<pectations -as MMMMMMMMMMMMMMMMM MMMMMMMMMMMMMMMMMMM.

3. MMMMMMMMMMMMMMMMMMMMMMMM ena(les users to identif) t-e real similarities and differencesin economic p-enomena (ecause t-e information -as (een measured and reported in asimilar manner for different enterprises.

4. ome costs w-ic- "ive rise to future (enefits cannot (e directl) associated wit- t-erevenues t-e) "enerate. uc- costs are allocated in a MMMMMMMMMMMMMMMMMM and

MMMMMMMMMMMMMMMMM manner to t-e periods e<pected to (enefit from t-e cost.

5. MMMMMMMMMMMMMMMMMMMMMMM would allow t-e e<pensin" of all repair tools w-en purc-asedBeven t-ou"- t-e) -ave an estimated life of 3 )ears.

#. T-e MMMMMMMMMMMMMMMMMMMMMMMM c-aracteristic re6uires t-at t-e same accountin" met-od(e used from one accountin" period to t-e ne<tB unless it (ecomes evident t-at analternative met-od will (rin" a(out a (etter description of a firms financial situation.

%. MMMMMMMMMMMMMMMMMMMM "uides accountants to select t-e accountin" treatment t-at is leastlikel) to overstate income and assets.

2 - 27

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 22/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

E?% 2-=< 7cont.8

&. arent-etical (alance s-eet disclosure of t-e inventor) met-od utilied () a particularcompan) is an application of t-e MMMMMMMMMMMMMMMMMMMMMMM principle.

*. Corporations must prepare accountin" reports at least )earl) due to t-e MMMMMMMMMMMMMMM

assumption.

1+. 'ecordin" and reportin" inflows at t-e end of production is an allowa(le e<ception to t-e MMMMMMMMMMMMMMMMM principle.

So!ut&on 2-=<

1. 'elevance relia(ilit) #. consistenc)2. feed(ack value %. Conservatism3. Compara(ilit) &. full disclosure4. rational s)stematic *. periodicit)5. T-e materialit) convention 1+. revenue reco"nition

E?% 2-==?,asic assumptions.

,riefl) e<plain t-e four (asic assumptions t-at underlie financial accountin".

So!ut&on 2-==

1. T-e economic entit) assumption states t-at economic activit) can (e identified wit- aparticular unit of accounta(ilit).

2. T-e "oin" concern assumption assumes t-at a (usiness enterprise will -ave a lon" life.3. T-e monetar) unit assumption means t-at mone) is t-e common denominator of economic

activit) and provides an appropriate (asis for accountin" measurement and anal)sis. InadditionB t-e monetar) unit remains reasona(l) sta(le.

4. T-e periodicit) assumption implies t-at t-e economic activities of an enterprise can (e dividedinto artificial time periods.

E?% 2-7>>?'evenue reco"nition.

'evenue is "enerall) reco"nied at t-e point of sale. T-ere are t-ree e<ceptionsB -owever.Name t-e time for eac- e<ceptionB "ive two 6ualifications or criteria for t-e use of eac- e<ceptionBand "ive an e<ample for eac- e<ception.

So!ut&on 2-7>>

1. $urin" production. T-e revenue is known 7contract8 or dependa(l) estima(le. Total costs areestima(le or ot-er means are availa(le to estimate pro"ress toward completion. /<amplesare lon"term construction contracts and servicet)pe transactions.

2 - 22

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 23/24

Conceptual Framework =nderl)in" Financial !ccountin"

So!ut&on 2-7>> 7cont.8

2. !t completion. T-ere are 6uoted prices. =nits are interc-an"ea(le. T-ere are no si"nificantdistri(ution costs. =nit costs are not determina(le. /<amples are precious metals or a"ricultural products.

3. !t collection. T-ere is no reasona(le (asis for estimatin" t-e de"ree of collecti(ilit). Costs of collectionB (ad de(tsB and repossessions are not estima(le. /<amples are installment salesand cost recover) met-od.

E?% 2-7>7?;istorical cost principle.

Cost as a (asis of accountin" for assets -as (een severel) criticied. D-at defense can )ou(uild for cost as t-e (asis for financial accountin"E

So!ut&on 2-7>7

Cost is definite and verifia(le and not a matter for conecture or opinion. nce esta(lis-edB cost isfi<ed as lon" as t-e asset remains t-e propert) of t-e part) t-at incurred t-e cost. Cost is (asedon fact t-at isB it is t-e result of an arms len"t- transaction. Cost is also measura(le or determina(le. ver t-e )earsB accountants -ave found cost to (e t-e most practical (asis for record keepin". Financial statements prepared on a cost (asis provide (usiness enterpriseinformation -avin" a commonB accepted (asis from w-ic- eac- reader can make inferencesBcomparisonsB and anal)ses.

E?% 2-7>2?0atc-in" concept.

! concept is a "roup of related ideas. 0atc-in" could (e considered a concept (ecause itincludes ideas related to (ot- revenue reco"nition and e<pense reco"nition. ,riefl) e<plain t-eideas in 7a8 revenue reco"nition and 7(8 e<pense reco"nition.

So!ut&on 2-7>2

7a8 T-e ideas in revenue reco"nition include t-e t-ree 's and earned>1. 'evenues are inflows of net assets from deliverin" or producin" "oods or services or

ot-er earnin" activities t-at are t-e maor operations of an enterprise durin" a period.2. 'eco"nition is recordin" and reportin" in t-e financial statements.3. 'evenues are realized w-en "oods or services are e<c-an"ed for cas- or claims to cas-.

4. 'evenues are earned w-en t-e earnin"s process is complete or virtuall) complete.T-e revenue reco"nition principle is t-at revenue is reco"nied w-en it is realied and it isearned.

7(8 T-e ideas in e<pense reco"nition include e<pense and matc-in">1. /<penses are outflows of net assets durin" a period from deliverin" or producin" "oods or

services or ot-er activities t-at are t-e maor operations of t-e entit).2. /<penses are reco"nied w-en t-e "oods or services 7efforts8 make t-eir contri(ution to

revenue.

2 - 2

8/20/2019 Ch02 Conceptual Framework Underlying Financial Accounting 2

http://slidepdf.com/reader/full/ch02-conceptual-framework-underlying-financial-accounting-2 24/24

Te"t 'n( )o$ Inte$*e+&te Account&n, T#e!)t. E+&t&on

So!ut&on 2-7>2 7cont.8

T-e matc-in" principle is t-at e<penses are matc-ed wit- revenues. /<penses are matc-edt-ree wa)s>1. D-en t-ere is an association wit- revenueB e<penses are matc-ed wit- revenues in t-e

period t-e revenues are reco"nied.2. D-en no association wit- revenue is evidentB e<penses are allocated on some s)stematic

and rational (asis.3. D-en no association wit- revenue is evident and no future (enefits are e<pectedB

e<penses are reco"nied immediatel).

2 - 28