Embed Size (px)

Citation preview

CH. 5 By S. Khan

Chapter 5 CORPORATE SOCIAL RESPONSIBILITY

5.1 Introduction This section focuses on Corporate Social Responsibility and in so

doing builds on what was learnt in the previous section on Business Ethics. A company's corporate social responsibility initiatives to a large degree are underpinned by a company's code of ethics.

Corporate Social Responsibility will be addressed in this section through exploring the

following: • What is “social responsibility”? • Levels of social responsibility • Stakeholders to whom a business is responsible • Evaluating corporate social performance

5.2 What is “Social Responsibility”?

THINK POINT

Think about the corporate social responsibility initiatives which your company is

implementing. What are the key characteristics of these initiatives? How would you

define corporate social responsibility?

Comment on Think Point

Various definitions of “social responsibility” are provided below:

- “being socially responsible essentially means that a business tries to reconcile the Interests of its different stakeholders with each other.” (Cronje, Du Toit and Motlatla, 2000: 273)

- “social responsibility refers to a manager's duty or obligation to make decisions that promote the welfare and well-being of stakeholders and society as a whole” (Jones and George, 2003).

- Fulfilling an obligation to create a better social, ecological and aesthetic environment for the benefit of employees, their families and the greater community

social responsibility involves the managerial obligation to protect and improve the welfare of interest groups (stakeholders), society as a whole, and the interests of the business” (Nieman and Bennett, 2006: 328).

Nieman and Bennett (2006) expand on their definition and identify that social responsibility

includes:

- Improving the quality of life of employees

- Creating a social infrastructure which benefits the community, particularly in terms of development and educational opportunities.

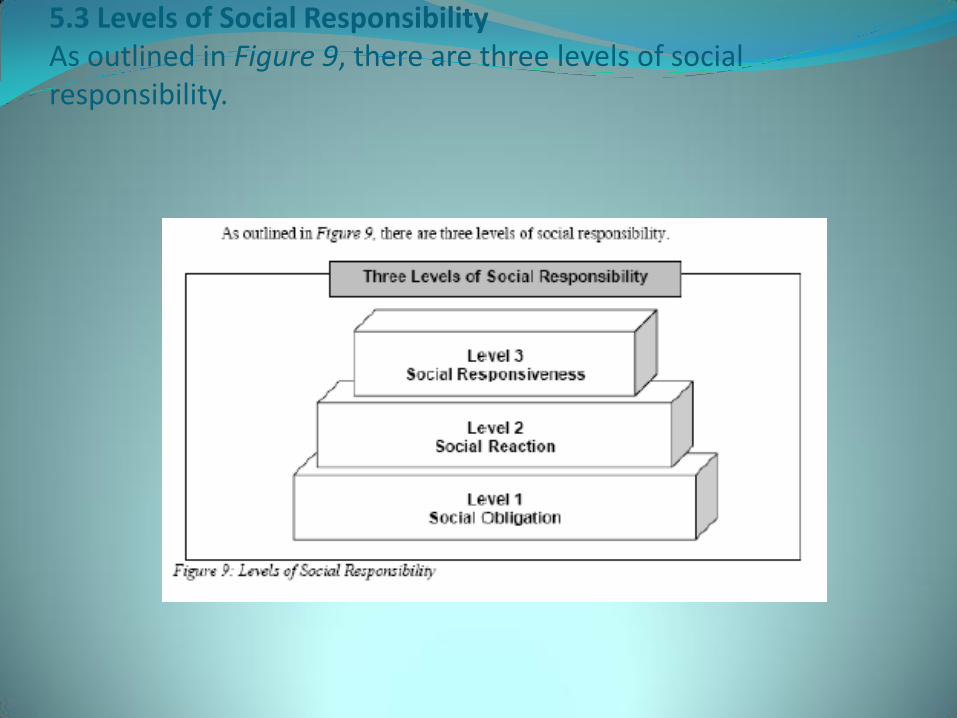

5.3 Levels of Social Responsibility As outlined in Figure 9, there are three levels of social responsibility.

5.3.1 Social Obligation At the level of social obligation it is argued that organisations,

in maximising their profits, are automatically being socially responsible as this provides for economic growth and has positive spin offs for the wider community (Smit and Cronje, 1997).

Social responsibility is seen to be limited to two responsibilities:

• Economic responsibility where the organisation is responsible for maximising profits and providing goods and services to the market at reasonable prices.

• Legal responsibility where the organisation is required to comply with the regulatory business framework and labour legislation (Smit and Cronje, 1997).

5.3.2 Social Reaction

At this level it is argued that an organisation's maximisation of profits and provision of goods and services does not amount to social responsibility. Rather, focus should be given to societal, environmental and ecological consequences of an organisation's actions. Socially responsible behaviour at this level therefore involves the organisation's voluntary participation in projects that assist in solving societal and environmental problems (Smit and Cronje, 1997).

5.3.3 Social Responsiveness At this level, social responsibility involves the organisation being proactive, and actively

seeking to prevent or find solutions to societal and environmental problems. At this level organizations also engage with the government about legislation and anticipated social and environmental problems (Smith and Cronje, 1997).

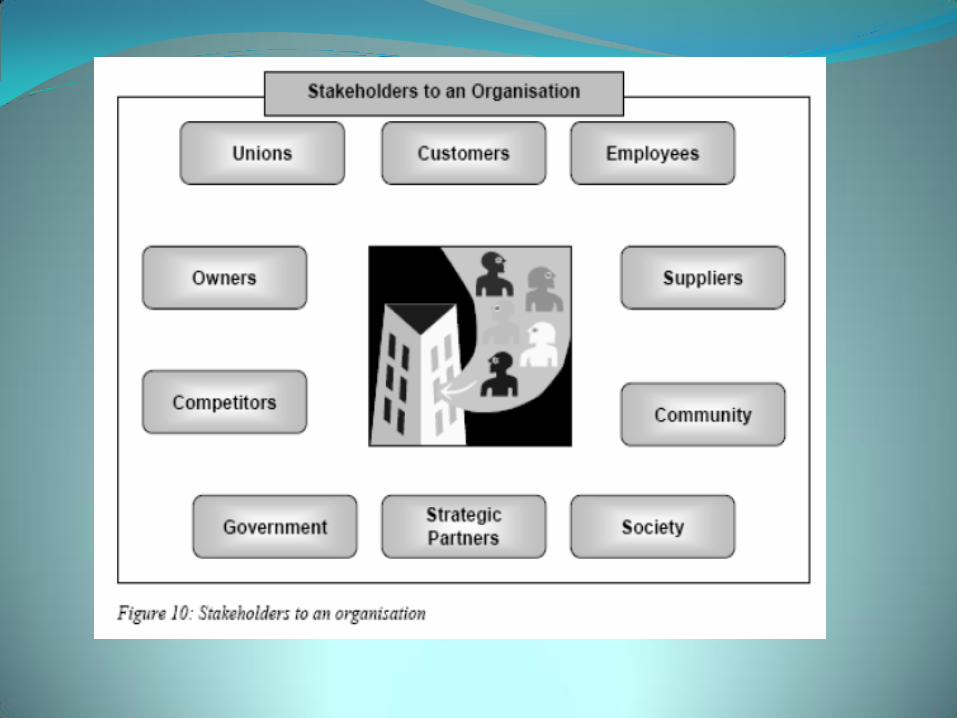

5.4 Stakeholders to Whom Business is Responsible The term stakeholders refers to “individuals or groups with interests and rights in, or

ownership of, an organisation and its activities” (Hellriegel, et al, 2004: 124). Stakeholders benefit, or are harmed, either directly or indirectly by the actions of an organisation. Similarly an organisation will suffer if a stakeholder group broke off the relationship (Hellriegel, et al, 2004). Certain stakeholders are regarded to be primary in that they are the most important, while others are secondary. Figure10 identifies some of the common stakeholders to an organisation.

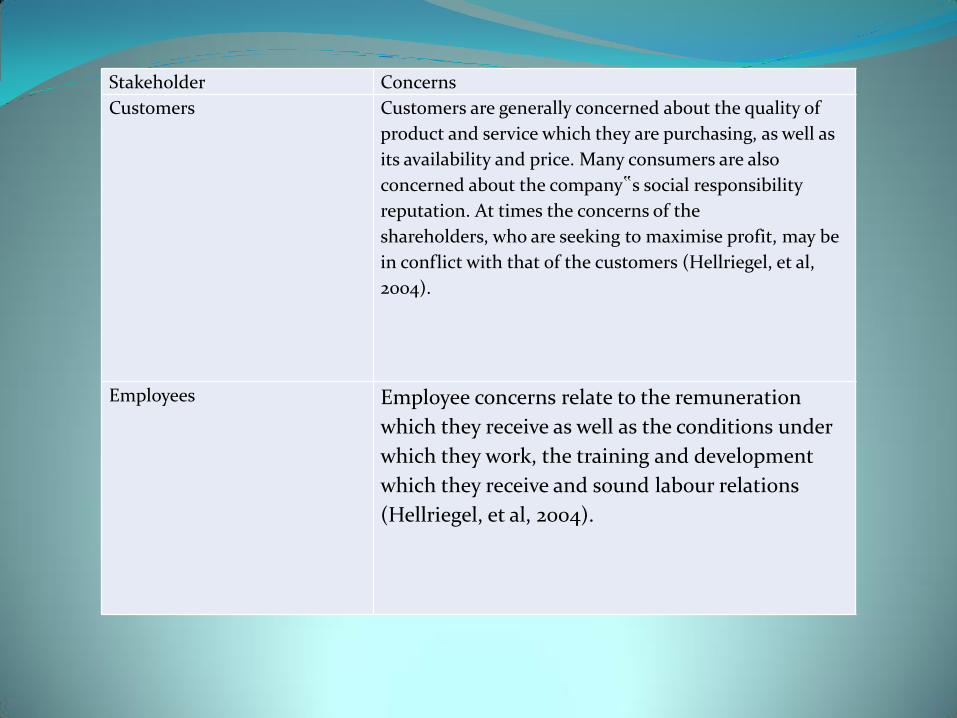

Stakeholder Concerns

Customers Customers are generally concerned about the quality of

product and service which they are purchasing, as well as

its availability and price. Many consumers are also

concerned about the company‟s social responsibility

reputation. At times the concerns of the

shareholders, who are seeking to maximise profit, may be

in conflict with that of the customers (Hellriegel, et al,

2004).

Employees Employee concerns relate to the remuneration

which they receive as well as the conditions under

which they work, the training and development

which they receive and sound labour relations

(Hellriegel, et al, 2004).

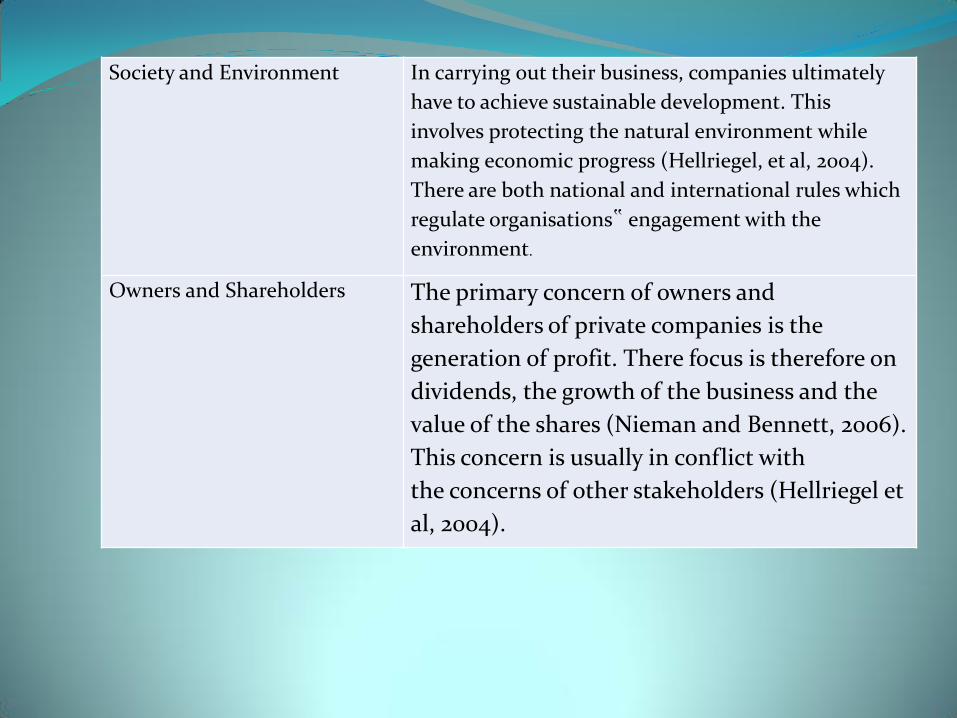

Society and Environment In carrying out their business, companies ultimately

have to achieve sustainable development. This

involves protecting the natural environment while

making economic progress (Hellriegel, et al, 2004).

There are both national and international rules which

regulate organisations‟ engagement with the

environment.

Owners and Shareholders The primary concern of owners and

shareholders of private companies is the

generation of profit. There focus is therefore on

dividends, the growth of the business and the

value of the shares (Nieman and Bennett, 2006).

This concern is usually in conflict with

the concerns of other stakeholders (Hellriegel et

al, 2004).

5.5 Evaluating Corporate Social Performance

Given the heightened public interest in corporate social performance, it would make good business sense for organisations to implement social responsibility initiatives at the level of social responsiveness. In this regard, the King II report emphasises the need for a move away from single accountability to triple bottom line accountability (Hellriegel, et al, 2004).

The “triple bottom line” involves “companies disclosing their social and environmental performance alongside their financial results.” (Hellriegel, et al, 2004: 128). Such an approach not only meets immediate organisational needs but also the needs of future generations.

Progress toward five broad obligations should be considered when evaluating an organisation's approach towards corporate social responsibility. These obligations are:

• Broad performance criteria: Companies need to broaden the focus of their organizational performance evaluation to include a focus on social and environmental initiatives.

• Ethical norms: Companies need to advocate ethical norms for the organisation, industry and business in general.

• Operating strategy: Organisations need to maintain and improve current standards of the physical and social environment. The potentially negative effects of an organisation's actions need to be investigated and addressed (Hellriegel, et al, 2004).

• Response to Social Pressure: Companies should participate actively in solving existing problems.

• Legislative and Political Activities: Organisations need to work with external bodies, such as the government to promote and facilitate the drafting of legislation and regulations regarding the protection of the natural and social environments in which they operate (Hellriegel, et al, 2006).

Companies that meet all five obligations are essentially at the level of “social responsiveness”, as discussed in section 5.3.

Summary

This section focused on Corporate Social Responsibility. The concept of “social responsibility‟was defined and the levels of social obligation, social reaction and social responsiveness were explored. The stakeholders to whom business is responsible and their respective concerns were also examined. In closing, the evaluation of corporate social performance was investigated.