Embed Size (px)

DESCRIPTION

Analysis of the Mauritian tourism sector outlook for 2012.

Citation preview

Disclaimer: Information has been collected from sources believed to be reliable and in good faith by the company, but no representation or warranty, expressed or implied, is made as to their accuracy, completeness or correctness. Information contained therein does not represent the views of Credit Guarantee Insurance Co. Ltd or its executives. Credit Guarantee Insurance Co. Ltd disclaims all liability as regards to its content.

MARKET MONITOR

Tourism Authors:

Zayd Soobedar – Credit Risk Manager

Vibha Ramdhony – Trainee Underwriter

September 2012

2

OUTLOOK FOR DOMESTIC TOURISM SECTOR 2012

Dark clouds looming over the horizon…

The economic turmoil in Europe has taken its toll on tourist

arrivals. Statistics for the period of January-July 2012 are portraying

a gloomy outlook for the tourism sector for the current year.

Tourist arrivals rose marginally by only 0.1% yoy for the first 7

months of 2012 driven by the adverse outlook and slowdown in

our main source destinations and the Central Statistics Office has

reviewed its forecast of 980,000 tourist arrivals for the year 2012

to 960,000, representing a decrease of 0.5% over the figure of

964,642 in 2011. Our forecast for the year is close to the CSO

figure and stands around 959,000 tourists (representing a mild

drop of 0.6% yoy).

… mired with escalating downside risks…

The outlook for the domestic tourism sector 2012 is likely to be

adversely affected by the following downside risks:

Further economic slowdown in European economies and the

dependence of our domestic market on this region

The weakening of the Euro vis-à-vis the Mauritian rupee

implying lower revenues for the sector

Increased regional competition especially with Maldives,

Seychelles and Sri Lanka

Lower investment in the domestic tourism industry

Declining risk appetite of domestic

commercial banks regarding tourism-

sector related projects due to higher

credit risk

Sustainability of the high debt levels for

the main hotel groups

Excess room supply

… especially with a downturn in our

main markets…

More alarmingly, tourists from Europe (our

main market) have declined by 7.1% yoy to

316,213 for the period under review.

Further breakdown reveals that arrivals

from France, UK, Germany and Italy have

plummeted.

Arrivals from our leading source market

(France) experienced a sharp drop of 11.2%

yoy for the period of January to July 2012

and the same negative trend was present in

the number of tourists from Italy falling

from 30,379 for the same period in 2011 to

23,058 in the first 7 months of 2012. The

UK market, which already shrunk in recent

years, was faced with only a 3.8% yoy drop.

The outlook for European markets for the

year 2012 is bleak as the statistics are

clearly suggesting the persisting impact of

the recession in Europe. Another adverse

Table 1: Tourist Arrivals by Country of Residence, January - July of 2011 and

2012

Country Jan-July

% Growth yoy

2011 2012 2011/2012

EUROPE 340,227 316,213 -7.1

France 172,306 153,045 -11.2

United Kingdom 47,383 45,574 -3.8

Italy 30,379 23,058 -24.1

AFRICA 131,341 146,366 11.4

Reunion 68,826 80,574 17.1

South Africa 45,257 45,771 1.1

Malagasy Rep. 6,232 7,307 17.2

ASIA 53,094 60,559 14.1

India 33,954 34,199 0.7

P. Rep. of China 7,647 11,441 49.6

United Arab Emirates 1,918 2,696 40.6

OCEANIA 8,946 9,763 9.1

Australia 8,380 9,265 10.6

Other Oceanian 566 498 -12.0

AMERICA 8,295 10,049 21.1

USA 3,889 4,093 5.2

Canada 2,431 2,686 10.5

Other American 1,975 3,270 65.6

OTHER & N.STATED 735 369 -49.8

ALL COUNTRIES 542,638 543,319 0.1

THE BOX: Economic performance outlook for 2012 in our main tourist generating

countries

France: For the whole of 2011, GDP rose by 1.7% yoy. However, growth for 2012 is

expected to be only by 0.3 % yoy. Despite the fact that inflation is expected to remain contained for 2012, the rise in unemployment together with the tightening in budget policy and likely decrease in purchasing power, consumer confidence remains low. [Outlook: Fair]

United Kingdom: The UK economy expanded by only 0.7% yoy in 2011 and the growth for 2012 is forecasted to be even lower during 2012 at only 0.2% yoy. Economic activity has again contracted in the 1Q12 (-0.3% q/q) and the 2Q12 growth could be shrinking again.

Declining wages, worsening unemployment and heavy debt burden are not helping to build British household confidence. Inflationary pressures have nonetheless decreased to 3.2 % since January from the 5.2 % peak in September 2011. With bank lending being more and more restricted and

rising bankruptcies, the conditions remain gloomy. [Outlook: Gloomy]

India: Economic activity slowed down slightly in India with a hike of 7.1% yoy in 2011

and the trend is expected to linger during 2012 with estimated 2012 growth to be around 6.1%

yoy. Inflation is expected to remain high though its fundamentals remain strong such as high savings

and investment rates and moderate foreign debt. [Outlook: Good]

South Africa: The South African economy after a growth of 3.1% yoy in 2011 is

projected to experience milder expansion of 2.6% yoy this year. The general trend of low interest rates is driving consumption however its growth is being restricted by the high unemployment rate of 25% and slow growth in wages. The manufacturing sector of the country is being affected by the weak demand from the European Union. Its mining sector is also being affected due to a lack of

investment and strikes. Moreover, inflation has risen from 5% in 2011 to 6% in 2012. [Outlook: Fair]

Table 2: Economic outlook in main markets, 2010 to 2013

Country/Region 2010 2011 2012F 2013F Advanced Economies 3.2 1.6 1.4 1.9 US 3.0 1.7 2.0 2.3

Germany 3.6 3.1 1.0 1.4 France 1.7 1.7 0.3 0.8 UK 2.1 0.7 0.2 1.4 Sub Saharan Africa 5.3 5.2 5.4 5.3

South Africa 2.9 3.1 2.6 3.3 China 10.4 9.2 8.0 8.5 India 10.8 7.1 6.1 6.5

World Output 5.3 3.9 3.5 3.9

Source: IMF World Economic Outlook

3

OUTLOOK FOR DOMESTIC TOURISM SECTOR 2012

factor that could contribute to further decline in tourist arrivals from European countries is the reduction in the number of seats

by Air Mauritius (around 87,000 between 2006 and 2012) on European routes in an attempt to discontinue unprofitable routes

(cessation of flights to Vienna, Rome and Munich) which have led to higher travel costs to our destination.

... but offset by good performance of emerging markets…

Fortunately, the downturn in the European market was

offset by tourists from other regions with the number

of tourists from non-European countries soaring by

12.2% yoy for the period under review. A shift, though

marginal, from the Eurocentricity of the local tourism

industry can be noted with the good performance of

non-European regions (Figure 1). Africa and Asia, which

accounted for 27% and 11% of total tourist arrivals

respectively, displayed favourable results for January-

July 2012.

African tourists increased considerably by 11.2% yoy

reaching 146,666, driven by the excellent upsurge in the

number of tourists from Reunion Island (80,574 for the

period under review against 68,826 in 2011). The

South African market was less active with a mild

increment (+1.1% yoy) experienced in arrivals.

The Mauritius Tourism Promotion Authority’s (MTPA)

strategy to develop alternative markets like India and

China has yielded positive results so far but requires

further development. Tourist arrival from India rose

slightly by 0.7% yoy to hit 34,199 for the period. On the

other hand, Chinese tourists, albeit having a low

contribution to overall tourist arrivals for January-July

2012, grew significantly by 49.6% yoy to 11,441.

Other countries representing a small part of the market

have realised excellent results for the period explained

by the efforts from the government with its past

national budgets focussing on diversifying our client

base. Statistics show a significant boost in tourist arrivals

from Russia (+89.4% yoy), Kenya (+47.9% yoy) and

Hong Kong which has more than doubled in size

(+119%). Arrivals from the UAE were also on a rise

with a growth of 40.6% yoy. Despite their considerable

expansion, their current market share remains minor. However, these

emerging countries have potential for further growth in the long term

for the domestic tourism sector.

... yet overall occupancy rates stagnating…

The average room occupancy rate for “Large hotels” for 1H12 stagnated

at 64% in line with the figure achieved in the same period last year. A

similar trend was observed in bed occupancy rate which averaged 56%

during the first semester of 2012.

On the other hand, average occupancy rate for “All hotels” for the first

semester of 2012 (62%) was lower than the 2011 mid-year

performance of 65%. Bed occupancy rate was also inferior to 1H11 and

stood at 55% compared to 57% in the previous year. The presence of

non-hotel accommodation facilities are proving to be strong competitors causing hotels to gradually lose their market share

Table 3: Other hotel operational statistics, 2009 to 2012

Year Number as at end of period

Hotels Rooms Bedplaces

2009

Q1 102 11,444 23,148

Q2 97 10,486 21,362

Q3 100 11,102 22,530

Q4 102 11,456 23,235

2010

Q1 105 11,564 23,547

Q2 104 11,362 23,168

Q3 104 11,383 23,296

Q4 112 12,075 24,698

2011

Q1 112 12,082 24,664

Q2 111 11,999 24,493

Q3 109 11,816 24,018

Q4 109 11,925 24,242

2012 Q1 110 12,027 24,446

Q2 107 11,822 24,089

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

EUROPE AFRICA ASIA OCEANIA AMERICA

Num

ber

of

Touri

sts

Region

Figure 1: Tourist Arrivals, January to July 2011/12

Jan-July 2011 Jan-July 2012

0 10 20 30 40 50 60 70 80

2010

2011

2012

2010

2011

2012

All

hote

lsLarg

e h

ote

ls

Room occupancy rate (%)

Type

Figure 2: Room occupancy rate, Quarterly analysis 2010-2012

Q4

Q3

Q2

Q1

4

OUTLOOK FOR DOMESTIC TOURISM SECTOR 2012

(reflected by the decrease in occupancy rates). With an excess in room supply, hotels are implementing aggressive marketing

strategies by lowering prices and providing special packages to increase demand.

At the end of June 2012, there were 113 registered hotels of which 107 were in operation, with a total room capacity of 11,822

and 24,089 bedplaces. “Large hotels”, i.e. well-established beach hotels with more than 80 rooms, numbered 47 (44% of all

registered hotels in operation). These hotels had a combined room capacity of 8,613 with 17,667 bedplaces, representing 73% of

both total room capacity and total bedplaces respectively.

… leading to macroeconomic forecasts being revised downwards…

In June 2012, the CSO forecasted a growth of around 1.6% based on a forecast of 980,000 tourist arrivals in 2012 compared to

964,642 in 2011. However, factoring the revised tourist arrival figures and gloomy outlook in main markets, we project sectoral

growth of Hotels and Restaurants to be nil or negative.

The Bank of Mauritius has also revised its forecast for tourism receipts for the year 2012 to be around Rs 42,542 million (-0.4 %

yoy) compared to Rs 42,717 million in 2011.

…slowdown also impacting on the financial performance of main hotel groups…

The table below shoes the financial performance of listed hotel groups for 2011 and 2012. Apart from Lux Island Resorts Ltd,

the remaining groups are facing difficulties for a sustainable growth in net profit despite the general growth in revenue. By

considering issues regarding rupee strength, economic turmoil in Europe and shrinkage of air access capacity, our hotels are still

operating in unfavourable market conditions.

Table 4: Financial performance for main hotel groups in Mauritius

Hotel Group Revenue results (Rs Million) Net Profit results (Rs Million)

30th June 2011 30th June 2012 Growth yoy 30th June 2011 30th June 2012 Growth yoy

New Mauritius Hotels Ltd 5,961.2 6,445.2 8.1% 801.9 754.5 -5.9%

Sun Resorts Ltd 1,746.2 1,789.9 2.5% 56.5 3.7 -93.5%

Constance Hotel Services Ltd 1,011.6 1,032.4 2.1% (82.5) (81.6) 1.1%

Hotel Group 31st March

2011 31st March

2012 Growth yoy

31st March 2011

31st March 2012

Growth yoy

Lux Island Resorts Ltd 2,865.0 3,259.7 13.8% 303.9 382.7 25.9%

…contributing to higher credit risk associated with market players…

In general, the credit risk level associated with market players is escalating day-by-day and a radical change in the trend is not

expected soon especially with the gloomy outlook for the year. A large number of stakeholders have over recent years

(especially prior to the 2008 financial crisis)

contracted financing for expansion projects.

With drastic declines in profitability, interest-

bearing debt to equity ratio is on the high side

and is close to or greater than 1 time.

On average, this financial leverage ratio is

deteriorating for most businesses in this

industry causing the general Insolvency Risk of

this sector to be Moderate (previously Low).

Waning operating profit of these firms and

soaring debt-servicing pressures, have

contributed to fuel alarming drops in the

interest cover ratio for many tourism-related

businesses, thus causing upward pressures on the Insolvency Risk parameter. However, the high level of non-current assets

(especially land and buildings) provides some reasonable degree of comfort regarding this financial element.

On the other hand, lower revenues due to a weak Euro and slowdown in tourist arrivals have negatively impacted on the

general Default Risk of the domestic tourism sector actors. Many hotels and other tourism-based businesses like restaurants are

mired in a liquidity trap stemming from sharp drops in margins as well as high finance costs and reduced access to finance with

reduced risk appetite of banks/other financial institutions.

Very low

Low

Moderate

High

Very high

Default Risk

Very low

Low

Moderate

High

Very high

Insolvency Risk

5

OUTLOOK FOR DOMESTIC TOURISM SECTOR 2012

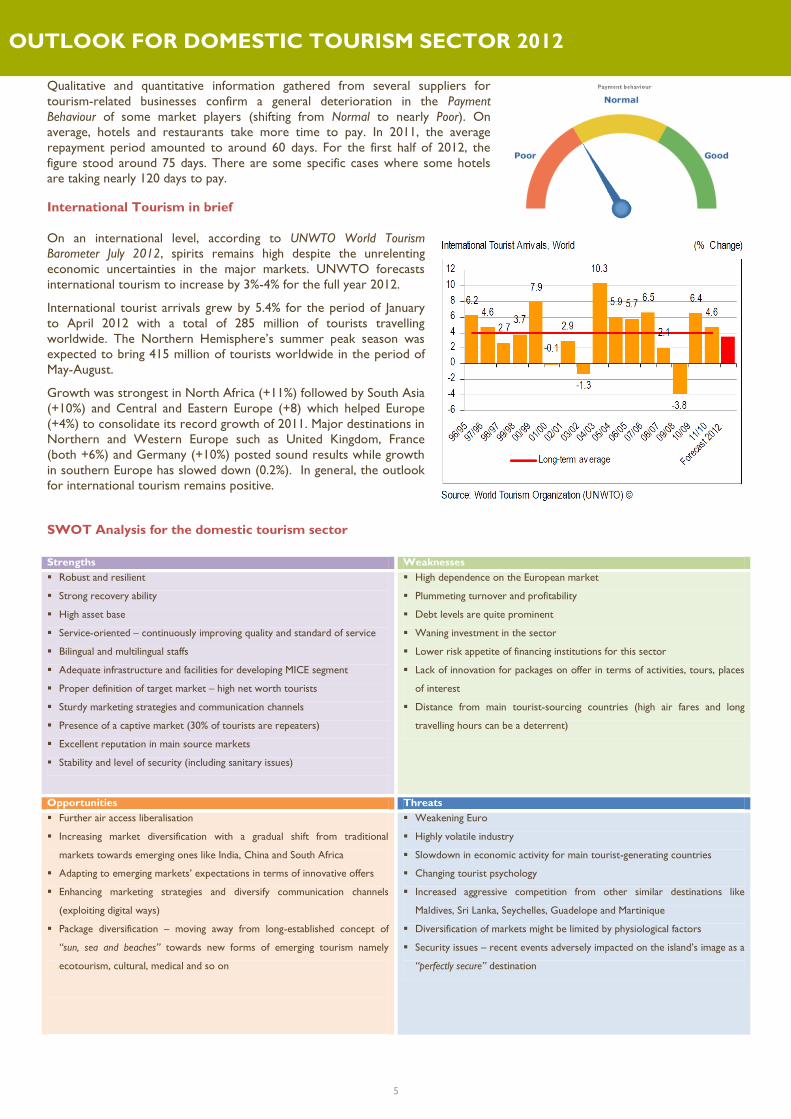

Qualitative and quantitative information gathered from several suppliers for

tourism-related businesses confirm a general deterioration in the Payment

Behaviour of some market players (shifting from Normal to nearly Poor). On

average, hotels and restaurants take more time to pay. In 2011, the average

repayment period amounted to around 60 days. For the first half of 2012, the

figure stood around 75 days. There are some specific cases where some hotels

are taking nearly 120 days to pay.

International Tourism in brief

On an international level, according to UNWTO World Tourism

Barometer July 2012, spirits remains high despite the unrelenting

economic uncertainties in the major markets. UNWTO forecasts

international tourism to increase by 3%-4% for the full year 2012.

International tourist arrivals grew by 5.4% for the period of January

to April 2012 with a total of 285 million of tourists travelling

worldwide. The Northern Hemisphere’s summer peak season was

expected to bring 415 million of tourists worldwide in the period of

May-August.

Growth was strongest in North Africa (+11%) followed by South Asia

(+10%) and Central and Eastern Europe (+8) which helped Europe

(+4%) to consolidate its record growth of 2011. Major destinations in

Northern and Western Europe such as United Kingdom, France

(both +6%) and Germany (+10%) posted sound results while growth

in southern Europe has slowed down (0.2%). In general, the outlook

for international tourism remains positive.

SWOT Analysis for the domestic tourism sector

Strengths Weaknesses

Robust and resilient

Strong recovery ability

High asset base

Service-oriented – continuously improving quality and standard of service

Bilingual and multilingual staffs

Adequate infrastructure and facilities for developing MICE segment

Proper definition of target market – high net worth tourists

Sturdy marketing strategies and communication channels

Presence of a captive market (30% of tourists are repeaters)

Excellent reputation in main source markets

Stability and level of security (including sanitary issues)

High dependence on the European market

Plummeting turnover and profitability

Debt levels are quite prominent

Waning investment in the sector

Lower risk appetite of financing institutions for this sector

Lack of innovation for packages on offer in terms of activities, tours, places

of interest

Distance from main tourist-sourcing countries (high air fares and long

travelling hours can be a deterrent)

Opportunities Threats

Further air access liberalisation

Increasing market diversification with a gradual shift from traditional

markets towards emerging ones like India, China and South Africa

Adapting to emerging markets’ expectations in terms of innovative offers

Enhancing marketing strategies and diversify communication channels

(exploiting digital ways)

Package diversification – moving away from long-established concept of

“sun, sea and beaches” towards new forms of emerging tourism namely

ecotourism, cultural, medical and so on

Weakening Euro

Highly volatile industry

Slowdown in economic activity for main tourist-generating countries

Changing tourist psychology

Increased aggressive competition from other similar destinations like

Maldives, Sri Lanka, Seychelles, Guadelope and Martinique

Diversification of markets might be limited by physiological factors

Security issues – recent events adversely impacted on the island’s image as a

“perfectly secure” destination

6

OUTLOOK FOR DOMESTIC TOURISM SECTOR 2012

Conclusion

The domestic tourism sector is currently facing daunting challenges especially with the downturn in our main source markets.

Other factors like eroding market share, weakening of the Euro, reduced risk appetite of banks to lend to tourism-based

businesses and changing consumer dynamics are hanging like the sword of Damocles over the industry. These market drivers are

pinning down even more the recovery scenario.

In addition, intrinsic growth parameters of market players are being hindered by toppling margins, debt-servicing burdens and

liquidity problems of our tourism-based businesses. These could jeopardise the existence of several hotels and restaurants in the

country, even though the sector is known to be robust and resilient. The credit risk associated with these businesses has

drastically deteriorated (low mid-2008 before the crisis and moderate to high in 2012). The long-term well-being of the industry

is also at stake with an astonishing deceleration of investment in the sector with very few new hotel projects and existing hotels’

renovation in the pipeline.

Solutions to these hardships are not readily available, but involve a proper soul-searching for all the stakeholders in the industry

with a lengthy timeframe for the necessary reforms to yield results. These changes would have to be across all levels ranging

from marketing strategies, communication channels, and air access to the quality of service and is the sine qua non condition for

changing the market dynamics. On a long-term perspective, the restructuring must be even carried at a higher echelon involving

strategic plans (e.g. mandatory learning of languages like Afrikaans, Mandarin, Hindi, etc in the curriculum of schools) to prepare

the new generation to cater for the needs of what might be our driving markets (mainly India, South Africa and China) in the

future. Of course, existing clients should not be neglected in the process (Europe accounts for 58% of arrivals and Reunion

Island 15% for the period January-July 2012).

Re-thinking the existing industry model (which has certainly generated positive results in the past, but alas gradually losing pace

and alarmingly starting to lose breath) would be the way for our flagship sector to navigate safely out of the storm!