Embed Size (px)

Citation preview

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 1/13

CORPORATE FINANCE

CORPORATE FINANCE REPORT ON

Submitted to : Ms.Sandhya Prakash Submitted By:

Karan Gaur

PGP 09-11

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 2/13

CORPORATE FINANCE

Page 1

1 COMPANY BACKGROUND .......................... .......................... ........................... .................. 2

2 CORPORATE GOVERNANCE ANALYSIS ......................... ........................... ...................... 2

2.1 Corporate Governance at Reliance is based on following factor ..... .................................... 3

2.2 Balance of power between management and shareholder ............... .................................... 3

2.3 Management compensation ....................... ........................... ........................... .................. 3

2.4 Market Coverage ......................... ........................... ........................... ........................... .... 4

2.5 Social Responsibility ..................................... ........................... ........................... ............. 4

3 STOCK HOLDER ANALYSIS ........................ .......................... ........................... .................. 5

3.1. Shareholding Pattern ....................... ........................... ........................... ........................... 5

4 COST OF CAPITAL .......................... ........................... ........................... ........................... .... 6

4.1 Weighted average cost of capital ........................ ........................... ........................... ......... 6

5 RISK AND RETURN ANALYSIS ........................ .......................... ........................... ............. 7

6 RETURN ON INVESTMENT.............................. ........................... ........................... ............. 8

6.1 Typical Project.................................................................................................................. 9

6.2 Measuring Returns ....................... ........................... ........................... ........................... .... 9

7 CAPITAL STRUCTURE ........................ .......................... ........................... ..........................10

8 DIVIDEND POLICY ......................... ........................... ........................... ........................... ...11

9 CONCLUSION ......................................................................................................................11

8 REFRENCES .........................................................................................................................12

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 3/13

CORPORATE FINANCE

Page 2

1 COMPANY BACKGROUND

The Reliance Group, founded by Dhirubhai H. Ambani (1932-2002), is India's largest private sector enterprise, with businesses in the energy and materials value chain. Group'sannual revenues are in excess of US$ 44 billion. The flagship company, Reliance

Industries Limited, is a Fortune Global 500 company and is the largest private sector company in India.

Backward vertical integration has been the cornerstone of the evolution and growth of

Reliance. Starting with textiles in the late seventies, Reliance pursued a strategy of

backward vertical integration - in polyester, fiber intermediates, plastics, petrochemicals,

petroleum refining and oil and gas exploration and production - to be fully integrated

along the materials and energy value chain.

The Group's activities span exploration and production of oil and gas, petroleum refining

and marketing, petrochemicals (polyester, fiber intermediates, plastics and chemicals),textiles, retail and special economic zones.

Reliance enjoys global leadership in its businesses, being the largest polyester yarn and

fiber producer in the world and among the top five to ten producers in the world in major

petrochemical products.

Major Group Companies are Reliance Industries Limited (including main subsidiary

Reliance Retail Limited) and Reliance Industrial Infrastructure Limited

2 CORPORATE GOVERNANCE ANALYSIS

For Reliance, Corporate Governance revolves around earning the trust of allconstituencies in how Reliance conducts its business.

This translates into attaining the highest levels of transparency, accountability and equity,

in all facets of operations, and in all interactions with stakeholders, including

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 4/13

CORPORATE FINANCE

Page 3

shareholders, employees, government and lenders.

Reliance recognizes communication as a key element in the effective functioning of the

overall corporate governance framework, and emphasizes continuous, efficient and

relevant communication with all its external constituencies

2.1 Corporate Governance at Reliance is based on following factor

y Ensuring timely flow of information to the Board and its Committees to enable

them to discharge their functions effectively.

y Independent verification and safeguarding integrity of the Company¶s financial

reporting.

y A sound system of risk management and internal control.

y Timely and balanced disclosure of all material information concerning the

Company to all stakeholders.

y Transparency and accountability.y Compliance with all the applicable rules and regulations.

y Fair and equitable treatment of all its stakeholders including employees,

customers, shareholders and investors

2.2 Balance of power between management and shareholder

The Company¶s policy is to maintain optimum combination of Executive and NonExecutive Directors. The Board consists of 13 directors; out of which 7 are independentdirectors.RIL management maintains its power primarily through their boards of directors. The Company has designated Lead Independent Director with a defined role.

2.3 Management compensation

The remuneration policy of the company is directed towards rewarding performance,

based on review of achievements on a periodic basis. The remuneration policy is in

consonance of with the existing industry practice.

Remuneration paid to the chairman and managing director and the whole time director,

including stock options granted during 2009-2010.

(All values in Cr)

Name of

Director

Salary Perquisites

and

allowance

Retrial

benefits

Compensation

Payable

Total

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 5/13

CORPORATE FINANCE

Page 4

Mukesh D

Ambani

4.16 0.60 5.60 4.64 15.00

Nikhil R

Meswani

1.04 1.45 1.05 7.60 11.14

Hetal R

Meswani

1.04 1.45 0.95 7.70 11.14

Hardev

Singh kohli

0.43 0.76 0.13 - 1.32

P.M.S

Prasad

0.53 0.83 0.17 - 1.53

R

Ravimohan

0.22 0.48 0.07 - 0.77

2.4 Market Coverage Presently, the Company has around 3.5 million folios of shareholders holding

Equity Shares in the Company.

The Company¶s Equity Shares are under compulsory trading in demat form only.

Over 96% of the Company¶s Equity Shares are held in demat form. The Company¶s Equity Shares are freely transferable except as may be required

statutorily.

The Company¶s Equity Shares are listed on the National Stock Exchange of India

Limited (NSE) and the Bombay Stock Exchange Limited (BSE). The Global

Depository Receipts (GDRs) issued by the Company are listed on Luxembourg

Stock Exchange.

2.5 Social ResponsibilitySocial welfare and community development is at the core of RIL¶s CSR philosophy and this

continues to be a top priority for the Company. The CSR teams at the Company¶s manufacturing

divisions interact with the neighboring community on regular basis. RIL¶s contributions to the

community are in areas of health, education, infrastructure development (drinking water,

improving village infrastructure, construction of schools etc.), environment (effluent treatment,

tree plantation, treatment of hazardous waste etc.), relief and assistance in the event of a natural

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 6/13

CORPORATE FINANCE

Page 5

disaster and contributions to other social development organizations. RIL also supports and

partners with several NGOs in community development and health initiatives.

3 STOCK HOLDER ANALYSIS

The Company¶s Equity Shares are among the most liquid and actively traded shares onthe Indian Stock Exchanges. RIL shares consistently rank among the top few frequentlytraded shares, both in terms of the number of shares traded, as well as value. The highesttrading activity is witnessed on the BSE and NSE. Relevant data for the average dailyturnover for the financial year 2009-2010 is given below:

BSE NSE TOTAL

Shares (In Numbers) 11 35 840 43 76 797 55 12 637

Values (in Cr) 192.72 718.72 911.44

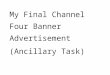

3.1. Shareholding Pattern

Share holding pattern of different groups of promoters is shown below.

Shareholding patternas on

31/12/2010 30/09/2010 30/06/2010

Face value 10.00 10.00 10.00

No of shares

% Holding No of shares

% holding No of shares

% holding

PROMOTERS HOLDINGIndian Promoter 1463923343 44.73 1463923343 44.74 1463923343 44.76

Sub Total 1463923343 44.73 1463923343 44.74 1463923343 44.76

Non promoter's holding Institutional investors

Banks fin institutionaland Insurance

264200752 8.07 266991969 8.16 260668783 7.97

FII¶s 576484887 17.62 549008002 16.78 562481618 17.20

Sub Total 915382856 27.97 882052146 26.96 908340551 27.77

Other Investors

Private corporateBodies

153584667 4.69 166770113 5.10 161838311 4.95

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 7/13

CORPORATE FINANCE

Page 6

NRI¶s/OCB¶s/ForeignOthers

24317948 0.74 24755648 0.76 24356714 0.74

Government 3428637 0.10 4967932 0.15 4967212 0.15

Others 174325490 5.33 302375382 9.24 122910567 3.76

Sub Total 355656742 10.87 498869075 15.25 314072804 9.60

General Public 411768012 12.58 426927899 13.05 412494014 12.61

Grand Total 3146730953 15 3271772463

100.00

3098830712 94.74

4 COST OF CAPITALThe project¶s cost of capital is the minimum required rate of return on funds committed to the

project, which depends on the riskiness of its cash flows. Since the investment projects

undertaken by firm may differ in risk, each one of them will have its own unique cost of capital.The firm represents the aggregate of investment projects undertaken by it. Therefore the firm¶s

cost of capital will be overall, on average, required rate of return on the aggregate of investment

project

4.1 Weighted average cost of capital

A firm obtains capital from various sources. As explained earlier, because of the risk differences

and the contractual agreements between the firm and investors, the cost of capital of each source

48%

9%

19%

10%

14%

Shareholding Pattern

Indian promoter banks financial institutional

FII's Other Investors

General public

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 8/13

CORPORATE FINANCE

Page 7

of capital differs. The cost of capital of each source of capital is known as component, or specific,

cost of capital. The overall is cost is also called the weighted average cost of capital.

COST OF DEBT=Interest rate (1-tax rate)

Interest rate=10%

Corporate tax=30%

Cost of debt=10 %*( 1-0.3)

Cost of debt=7%

COST OF EQUITY

P0=D/ (K e-growth)

K e= (D/p0) +G

Where D=dividend=7%

P0=current share price=996.00

Growth= (1-dividend payout rate)*(return on equity)

Dividend payout rate=17.52%

Return on equity=16.4%

Growth= (1-.1752)*(16.4)

Growth rate=13.52%

Cost of equity=13.52+ (7/996)

Cost of equity=14.22%

Apply the weighted average concept to calculate cost of capital

Weight (1) 2 1*2

Number of equity shares 3270.37 3270.37/65765=5 Costof

equity=14.22%

0.711

Number of debentures 62494.69 62494.69/65765=95 Cost of debt=7% 6.65

Total 65765.06 7.361%

5 RISK AND RETURN ANALYSIS

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 9/13

CORPORATE FINANCE

Page 8

It is important that one follows the Beta value as it tells us the volatility of a stock in

comparison with the prevailing index. The point is to note that Low-beta stocks make

Nifty less volatile and vice versa is also true. Beta=1 means that stock is moving in

correlation with the index and one can almost expect returns equivalent to the index

movement.

After taking values of Market and RIL stock of past three months from BSE INDIA SITE

(www.bseindia.com) and calculating the beta value by taking return on stock by market

return the value came out to be 1.085(approx) which indicates that the stock value of RIL

is more fluctuating viz-a-viz market value. i.e. The sensitivity of RIL is much more in

comparison to market movement. Hence we infer that since security has a beta value of

1.085, its return is more volatile than the return on the market portfolio. Eg: If the return

on market portfolio is expected to increase by 10 %, the return on the security with a beta

of 1.085 is expected to increase by 10.85 percent (1.085* 10 percent)

6 RETURN ON INVESTMENT

The ability of each firm to grow and create value for its stakeholders ultimately depends on its

management capability to indentify and undertake projects that generate returns exceeding the

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 10/13

CORPORATE FINANCE

Page 9

cost of capital employed. In this section we are going to evaluate return on capital (ROC) and

return on equity (ROQ) of company.

6.1 Typical Project Some of the major events of the year include the following:

KG D6 completed 365 days of 100% uptime and zero- incident production. Gas production from KG D6 has ramped up to 60 MMSCMD in a short span of 9 monthsfrom commencement. KG D6 has current production of about 60 MMSCMD. The designcapacity of the KG D6 deepwater gas production facilities were assessed and achieved aflow rate of 80 MMSCM.GSPAs have been executed in line with the Government of India¶s gas utilization policyfor over 69 MMSCMD in the fertilizers, power, and city gas distribution, steel, LPG,refinery and petrochemical sectors.

During the year, development of Panna-K (PK) area was completed.

The Company had made four new gas discoveries during the year, Dhirubhai-43 in Well AA1 in CB10 block Dhirubhai-44 in Well R1 in KGVD3 block Dhirubhai-45 in Well BF1 in CB10 block Dhirubhai-46 in Well AH1 in CB10 block

Subsequent to series of new discoveries in the southern and deeper areas of the KG D6 block, an optimized development plan has been submitted to DGH in December 2009.

6.2 Measuring Returns

Return on capital measures return generated on all capital, dept as well as equity invested

in all assets.

Return on equity focuses on just the equity component of the investment. It relates the

earnings left over for equity investors after dept services costs have been factored into the

equity invested in the asset.

We computed the return on equity (ROE) and return on capital (ROC) as follows.

ROE=

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 11/13

CORPORATE FINANCE

Page 10

Where:

NET INCOME=TOTAL INCOME-TOTAL EXPENSES

NET INCOME=200,399.79-166,070.69=34329.1

OPERATING INCOME=TOTAL INCOME-OPERATING EXPENES-DEPRICIATION

34329.1-10,496.53=23832.57

BVE=Book value of equity (current quarter) = 3,270.37

BVE=Book value of equity (previous quarter) = 1,573.53

BVD=Book value of debt (current quarter) = 62,494.69

BVD=Book value of debt (previous quarter) = 73,904.48

ROE=14.174

ROC=0.3374

7 CAPITAL STRUCTURE

Capital structure of reliance during 2009-2010 is shown below

FromYear

To year Class of share

Authorizedcapital

Issuedcapital

Paid upshare (num)

Paid upfacevalue

Paid upcapital

2009 2010 Equityshare

5000 3270.37 3270374360 10 3270.37

In year 2009-2010, the authorized capital was 5000 Cr however the capital which was

generated by floating of share was about 3270.37 Cr i.e. the paid up share were

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 12/13

CORPORATE FINANCE

Page 11

3270374360 with the face value of 10 Rs.The remaining capital i.e. 1729.63 (5000-

3270.37) was generated either from loan or from their own capital.

8 DIVIDEND POLICY

Directors have recommended a dividend of Rs. 7/- per Equity Share (last year Rs. 13/-

per Equity Share on pre bonus share capital) for the financial year ended March 31, 2010,

amounting to Rs. 2,430 crore (inclusive of tax of Rs. 346 crore) one of the highest ever

payout by any private sector domestic company. The dividend payout for the year under

review has been formulated in accordance with the Company¶s policy to pay sustainable

dividend linked to long term performance, keeping in view the Company¶s need for

Capital for its growth plans and the intent to finance such plans through internal accruals

to the maximum.

DIVIDEND DECLARED

Announcement date Effective date Dividend type Dividend Value%

26/04/2010 10/5/2010 Final 70%

7/10/2009 16/10/2009 Final 130

DIVIDEND YIELD

Dividend Yield = annual dividend per share / stock's price per share

Annual dividend = (70/100)*10=7 Rs

Stock Price/share=994 Rs

Dividend Yield=7/994=0.704%

9 CONCLUSION

Risk characteristic Cost of capital Investment

Performance

Dividend

yieldBeta value-1.08 7.361% ROC ROE 0.704%

0.3374 14.174

8/6/2019 CF_PROJECT Ekdum Final

http://slidepdf.com/reader/full/cfproject-ekdum-final 13/13

CORPORATE FINANCE

Page 12

The beta value of company came out to be 1.08 which shows that RIL stock fluctuates in

according to market portfolio. The risk is less in buying this share.

Cost of capital came out to be 7.361% which shows that business has enough amounts of

cash which it proposes to invest in a project.

8 REFRENCES

www.ril.com

www.moneycontrol.com

http://money.rediff.com/