Embed Size (px)

Citation preview

ATACAMA PACIFIC GOLD CORPORATION

Cerro Maricunga Oxide Gold Project

Trading Symbol – ATM:TSXV

January 2013

This presentation contains, or incorporates by reference, “forward-looking information and statements” within the meaning of applicable Canadian securities

legislation and within the meaning of the U.S. Securities Act of 1933 and the U.S. Securities Exchange Act of 1934. Forward-looking information may include,

but is not limited to, statements with respect to the future financial and operating performance of Atacama Pacific Gold Corporation and its subsidiaries, and

its mineral properties, the future price of gold and other metals, the estimation of mineral resources, results of exploration activities and studies, the

realization of mineral resource estimates, exploration expenditures, costs and timing of the development of new deposits, the acquisition of additional

mineral resources, the results of future exploration and drilling, timing of economic and scoping-level studies, costs and timing of future exploration of the

Projects, requirements for additional capital, management’s skill and knowledge with respect to the exploration and development of mining properties in

Chile in general and the relevance of that knowledge to the projects, government regulation of mining operations and exploration operations, timing and

receipt of approvals and licenses under mineral legislation, environmental risks and title disputes or claims and limitations of insurance coverage. In certain

cases, forward-looking statements can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”,

“forecasts”, “intends”, “anticipates” or “believes”, or variations (including negative variations) of such words and phrases, or state that certain actions, events

or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or

achievements of Atacama Pacific to be materially different from any future results, performance or achievements expressed or implied by the forward-looking

statements. Such factors include, among others, risks associated with the Company’s dependence on the Cerro Maricunga Project; the Company’s limited

operating history; general business, economic, competitive, political and social uncertainties; the actual results of current exploration activities; risks

associated with dependence on key members of management; conclusions of economic evaluations and studies; currency fluctuations (particularly in respect

of the Canadian dollar, the United States dollar and the Chilean peso and the rate at which each may be exchanged for the others); future prices of gold and

other metals; uncertainty in the estimation of mineral resources; exploration and development risks; infrastructure risks; inflation risks; defects and adverse

claims in the title to the projects; accidents, political instability, insurrection or war; labour and employment risks; changes in government regulations and

policies, including laws governing development, production, taxes, royalty payments, labour standards and occupational health, safety, toxic substances,

resource exploitation and other matters; delays in obtaining governmental approvals or financing or in the completion of development or construction

activities; insufficient insurance coverage; the risk that dividends may never be declared; liquidity and financing risks related to the global economic crisis, as

well as those factors discussed in the section entitled “Risk Factors” in the Company’s Prospectus dated October 29, 2010. Such forward-looking statements

are based on a number of material factors and assumptions, including: that contracted parties provide goods and/or services on the agreed timeframes; that

on-going contractual negotiations will be successful and progress and/or be completed in a timely manner; that no unusual geological or technical problems

occur; that plant and equipment work as anticipated and that there is no material adverse change in the price of gold. Although Atacama has attempted to

identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may

be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward-looking statements contained herein

are made as of the date of this presentation. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future

events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements

due to the inherent uncertainty therein.

x

Forward Looking Statement

2

ATACAMA PACIFIC GOLD CORPORATION

Focused on precious metals exploration and development in Chile

− A mining-friendly country with a long history of encouraging resource development

− Ranked No. 1 mining jurisdiction in Latin America and No. 8 in the world1

− Ranked No. 1 in the world for mining potential1

Atacama’s key property is the Cerro Maricunga Oxide Gold Project

− Located in the Maricunga Mineral Belt, an established gold mining region in Chile

Cerro Maricunga M&I resource2 is 2.67 M ounces of gold grading 0.51g/t Au

− Inferred resource of 1.81 M ounces at 0.47 g/t Au

Insiders own 32% of the shares of Atacama

− 42% beneficiary ownership

Well financed with $20 M in cash (Jan 2013)

3

1. Fraser Institute - 2010/2011 Survey of Mining Companies

2. National Instrument 43-101 Compliance: The Cerro Maricunga resource estimate was prepared under Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) Definition Standards (2005). Dr. Eduardo Magri, a mining engineer (Witwatersrand) and a Fellow of the Southern African Institute of Mining and Metallurgy with over 30 years of industry experience, is the independent qualified person, as defined by National Instrument 43-101 (“NI 43-101”), for the resource estimate.

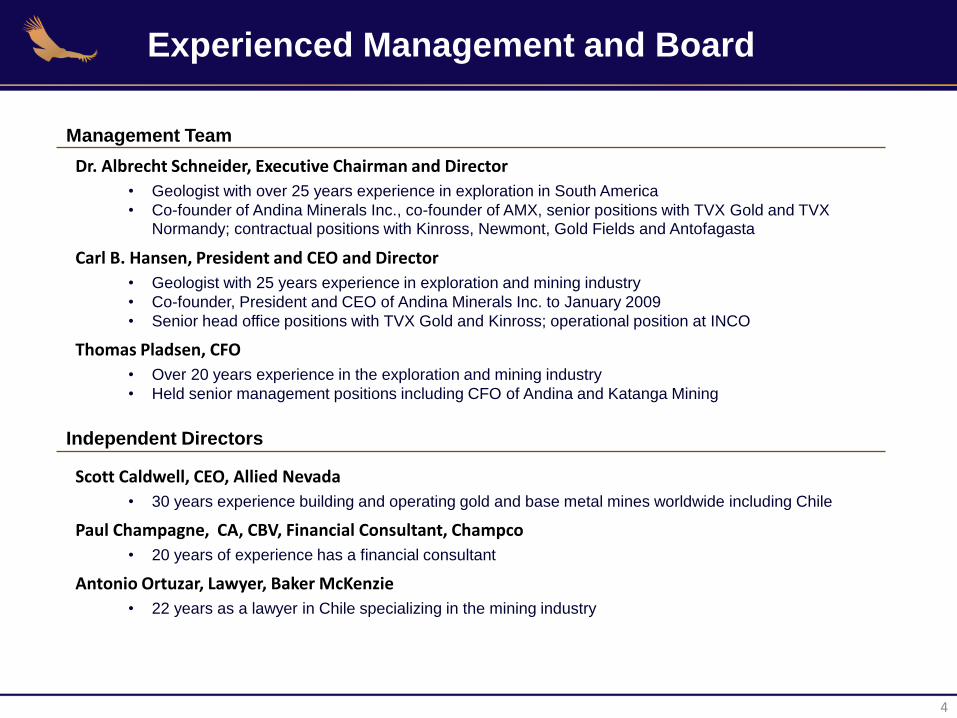

Experienced Management and Board

4

Management Team

Dr. Albrecht Schneider, Executive Chairman and Director

• Geologist with over 25 years experience in exploration in South America

• Co-founder of Andina Minerals Inc., co-founder of AMX, senior positions with TVX Gold and TVX Normandy; contractual positions with Kinross, Newmont, Gold Fields and Antofagasta

Carl B. Hansen, President and CEO and Director

• Geologist with 25 years experience in exploration and mining industry

• Co-founder, President and CEO of Andina Minerals Inc. to January 2009

• Senior head office positions with TVX Gold and Kinross; operational position at INCO

Thomas Pladsen, CFO

• Over 20 years experience in the exploration and mining industry

• Held senior management positions including CFO of Andina and Katanga Mining

Independent Directors

Scott Caldwell, CEO, Allied Nevada

• 30 years experience building and operating gold and base metal mines worldwide including Chile

Paul Champagne, CA, CBV, Financial Consultant, Champco

• 20 years of experience has a financial consultant

Antonio Ortuzar, Lawyer, Baker McKenzie

• 22 years as a lawyer in Chile specializing in the mining industry

Tightly Held Share Structure

5

Share Structure millions

Basic Shares Outstanding 50.94

Options 4.88

Fully Diluted Shares Outstanding 55.82

Basic Market Cap (at $3.00 per share) $153 M

Strong Shareholders Base

Insiders and Management (30%)

Investors Group

RBC Asset Management

Sentry Select

Salida

Sprott

Wellington

Insiders 30%

Funds* 40%

Others 30%

Shareholder Base

* Estimated from Bloomberg and direct sources

Cerro Maricunga Oxide Gold Project

6

Located In A Major Gold Mining Region

# Deposit Sulfide/ Oxide

Reserves & Resources Grade (g/t Au)

Historical Production

1 Esperanza (Laguna-100%)

N/A 1.2 M oz Au eq. 1.98 eq 0.83M oz Au eq

2 La Coipa / Puren (Kinross-100%)

Oxide 1.5 M oz Au, 45.5M oz Ag 2.2 eq 1 3.5M oz Au

3 Lobo – Marte (Kinross-100%)

Sulphide 9.8 M oz Au 0.98 >180K oz Au (1988-1992)

4 La Pepa (Yamana-100%)

Sulphide 3.4 M oz Au 0.56 148K oz Au (1980’s- 90’s)

5 Volcan (Andina-100%)

Sulphide 9.5 M oz Au 0.69 -

6 Pantanillo1

(Orosur-100%) Oxide/ Mixed

1.0 M oz Au 0.69 -

7 Maricunga (Kinross-100%)

Oxide/ Sulphide

9.4 M oz Au 0.68 2.1M oz Au

8 Caspiche (Exeter-100%)

Sulphide 24.3 M oz Au, 60.3 M oz Ag, 6.3 B lbs Cu

0.51 -

9 Cerro Casale (Barrick-75%, Kinross 25%)

Sulphide 31.0 M oz Au, 81.4 M oz Ag, 8.5 B lbs Cu

0.52 -

10 Cerro Maricunga (Atacama-100%)

Oxide 2.67 M oz Indicated @ 0.51 g/t Au* 1.81 M oz Inferred @ 0.47 g/t Au*

-

Maricunga Mineral Belt hosts over 90 million oz of gold resources

7

* M&I resources – 163.9 Mt @ 0.51 g/t Au & Inferred resources – 120.7 Mt @ 0.47 g/t Au. See page 8 for NI43-101 disclosure

September 2012 Resource Estimate

8

Cerro Maricunga Project – Oxide

Measured Indicated Measured and Indicated Inferred

Cut-off Tonnes Grade Tonnes Grade Tonnes Grade Oz Au Tonnes Grade Oz Au

(g/t Au) (millions) (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (OOO’s) (millions) (g/t Au) (OOO’S)

0.2 60.4 0.44 187.5 0.41 247.9 0.42 3,344 226.3 0.36 2,654

0.3 40.7 0.53 123.1 0.50 163.9 0.51 2,667 120.7 0.47 1,810

0.4 24.5 0.64 71.2 0.61 95.8 0.62 1,912 57.8 0.60 1,118

0.5 15.1 0.77 42.8 0.72 57.9 0.74 1,370 32.3 0.73 754

* National Instrument 43-101 Compliance The Cerro Maricunga resource estimate was prepared under Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) Definition Standards (2005). Dr. Eduardo Magri, a mining engineer (Witwatersrand) and a Fellow of the Southern African Institute of Mining and Metallurgy with over 30 years of industry experience, is the independent qualified person, as defined by National Instrument 43-101 (“NI 43-101”), for the resource estimate.

2.6

67

2.1

00

2.3

90

1.4

70

1.1

30

0.5

13

1.8

10

1.1

00

0.1

20

0.1

70

Cerro Maricunga,Atacama

Amulsar,Lydian

Shahuindo,Sulliden

Cerro Jumil,Esperanza

Pan,Midway Gold

Cerro Quema,Pershimco

Inferred (Moz Au) Indicated (Moz Au)

Cerro Maricunga – A Large Oxide Gold Deposit

The largest oxide gold deposit not owned by a gold producer

9

Updated from Stonecap Securities Aug 17, 2012 Atacama Report

10

2012 Resource Model

Lynx Zone 710 koz Au M&I 343 koz Au Inferred

Phoenix Zone 1,235 koz Au M&I 766 koz Au Inferred

Pollux Zone 162 koz Au M&I 409 koz Au Inferred

Crux Zone 560 koz Au M&I 292 koz Au Inferred

0 1000

metres

See page 8 for NI 43-101 disclosure

Measured Indicated Measured and Indicated Inferred

Cut-off Tonnes Grade Tonnes Grade Tonnes Grade Gold

Ounces Tonnes Grade

Gold

Ounces (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (000’s) (millions) (g/t Au) (000’s)

0.2 13.5 0.47 45.6 0.45 59.1 0.46 864 40.2 0.39 506

0.3 9.1 0.58 30.8 0.55 39.8 0.55 710 19.6 0.54 343

0.4 5.8 0.71 19.9 0.66 25.7 0.67 554 11.5 0.69 256

0.5 4.0 0.83 13.5 0.76 17.6 0.77 436 8.0 0.80 205

Lynx Zone Resource Estimate

11 * See page 8 for NI 43-101 disclosure

Phoenix Zone Resource Estimate

12 * See page 8 for NI 43-101 disclosure

Measured Indicated Measured and Indicated Inferred

Cut-off Tonnes Grade Tonnes Grade Tonnes Grade Gold

Ounces Tonnes Grade

Gold

Ounces

(g/t Au) (millions) (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (000’s) (millions) (g/t Au) (000’s)

0.2 29.8 0.42 86.5 0.41 116.3 0.41 1,547 85.5 0.37 1,029

0.3 20.1 0.50 57.6 0.49 77.7 0.49 1,235 52.8 0.45 766

0.4 12.0 0.61 33.5 0.60 45.5 0.60 877 22.6 0.60 434

0.5 7.1 0.73 19.5 0.70 26.5 0.71 606 12.4 0.72 288

Crux Zone Resource Estimate

13

* See page 8 for NI 43-101 disclosure

Measured Indicated Measured and Indicated Inferred

Cut-off Tonnes Grade Tonnes Grade Tonnes Grade Gold

Ounces Tonnes Grade

Gold

Ounces (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (000’s) (millions) (g/t Au) (000’s)

0.2 12.8 0.45 41.3 0.40 54.1 0.41 712 38.2 0.36 440

0.3 8.8 0.54 26.5 0.48 35.3 0.49 560 19.6 0.46 292

0.4 5.5 0.66 13.9 0.60 19.4 0.62 383 9.8 0.59 184

0.5 3.4 0.79 7.6 0.73 10.9 0.75 262 5.0 0.73 116

* See page 8 for NI 43-101 disclosure

Pollux Zone Resource Estimate

14

* See page 8 for NI 43-101 disclosure

Measured Indicated Measured and Indicated Inferred

Cut-off Tonnes Grade Tonnes Grade Tonnes Grade Gold

Ounces Tonnes Grade

Gold

Ounces

(g/t Au) (millions) (g/t Au) (millions) (g/t Au) (millions) (g/t Au) (000’s) (millions) (g/t Au) (000’s)

0.2 4.3 0.37 14.1 0.37 18.4 0.37 221 62.4 0.34 679

0.3 2.7 0.46 8.3 0.46 11.0 0.46 162 28.8 0.44 409

0.4 1.3 0.60 3.9 0.58 5.2 0.59 97 13.9 0.55 244

0.5 0.7 0.73 2.2 0.69 2.9 0.70 65 7.0 0.65 145

* See page 8 for NI 43-101 disclosure

15

80,000 m of Drilling Completed

Amenable to Heap Leach Processing

Note: Metallurgical testing managed by AMTEL, London, Canada. Tests conducted by Kappes Cassidy and Associated, Nevada.

16

• Column tests achieve gold recoveries of approximately 80% (19 mm)

− Potential to further optimize gold recoveries

• Gold deposit has low levels of deleterious elements

− Very low copper and silver levels

• Coarse crush (100 mm) column achieved gold recoveries of 77%

• Low grade columns (0.2 – 0.3 g/t Au) achieve outstanding recoveries of 78 to 82%

Composite

Sample

Crush

Size

Head

Grade

Gold

Recovery

Consumables Sample

Weight NaCN Lime Cement

(P80 - mm) (g/t Au) (%) (kg/t) (kg/t) (kg/t) (kg)

Comp. 7 19 0.22 78 0.57 4.0 1.0 39.9

Comp. 4 19 0.28 80 0.82 2.5 1.0 39.9

Comp. 4 19 0.28 82 0.52 2.5 1.0 39.8

Comp. 5 19 0.51 86 0.74 2.0 1.0 39.9

Comp. 5 19 0.51 84 0.97 2.0 1.0 39.4

Comp. 6 19 0.58 80 0.44 6.5 1.0 39.8

Comp. 6 50 0.58 78 0.10 6.7 1.0 210.9

Comp. 6 100 0.58 77 0.09 6.6 1.0 580.0

Rapid Gold Recoveries Achieved

17

Sample Grade

Comp. 7 0.22 g/t Au

Comp. 4 0.28 g/t Au

Comp. 5 0.51 g/t Au

Comp. 6 0.58 g/t Au

50 mm Crush – 78%

100 mm Crush – 77%

19 mm Crush – 80%

~85% of extractable gold recovered within the first 20 days at a 19 mm crush

Days

% G

old

Ext

ract

ion

Crush Size has Minimal Impact on Recoveries

Attractive Capital Costs for Heap Leach Ops

Heap leach operations typically have low capital costs per tonne of capacity built

• average $6.6k / tpd of built capacity for heap leach oxide

• average $19.2k / tpd of built capacity for milling operations

Considering processing rate for Cerro Maricunga in the range of 60,000 tpd to 80,000 tpd

18

Cerro Quema

Pan

Shahuido

La India

Camino Rojo

Cerro Jumil

Amulsar

Spanish Mountain

Toroparu

Haile

Magino

Esaase

Rainy River

Eagle

Rosia Montana

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

Cap

ital

Co

st /

tpd

Processing Rate (tpd)

Milling Projects

Heap Leach Projects

From Stonecap Securities Aug 17, 2012 Atacama Pacific Report

Mill

ing

Hea

p

Leac

h

Selected Oxide Gold Heap Leach Mines

*Indicated resources – 163.9 Mt @ 0.51 g/t Au &

*Inferred resources – 120.7 Mt @ 0.47 g/t Au.

See page 8 for NI 43-101 disclosure

19

Mines Gualcamayo1 La Arena El Castillo Maricunga1 Cerro Maricunga

Ownership Yamana Rio Alto Argonaut Kinross Atacama

Location Argentina Peru Mexico Chile Chile

Gold Oxide Reserves &

Resources (2011) 3.3 M oz Au (1.1 g/t Au) 1.5 M oz (0.46 g/t Au) 2.9 M oz (0.34 g/t Au) -

2.67 M oz Ind. (0.51 g/t Au)*

1.81 M oz Inf. (0.47 g/t Au)*

Sulphide Reserves 4.4 M oz (0.22 g/t Au)

4 B lb Cu (0.3 %) 1.5 M oz (0.30 g/t Au) 9.7 M oz (0.68 g/t Au) No Sulphide Mineralization

Grind Size 25 mm ROM ROM & 19 mm 12 mm 19 mm 100 mm

Gold Recovery 70% 80% 50% for ROM

70% for crushed 55%2 +81% 77%

Mining Rate (tpd ore) 29,000 24,000 30,000 40,000 projected 60,000 to 80,000

Strip Ratio (Waste:Ore) 3.4:1 (LOM) 1.47:1 2:1 0.9:1

PEA Study Underway

H1 2012 Gold Grade 0.88 g/t 1.21 g/t 0.38 g/t 0.66 g/t

Mining ($/t mined ) $1.22 $1.09

Mining ($t/ore mined) $5.86 $6.22 $2.54 $2.07

Processing ($/t processed) $2.47 $1.68 $2.60 $3.37

G&A ($/t processed) $1.00 $1.26 $0.23 $1.27

Total ($/t mined) $8.211 $9.16 $4.97 $6.711

Forecast 2012 Prod. 150,000 oz 200,000 oz 80,000 oz 250,000

H1 2012 Cash Cost (/oz) $491 $479 $635 $676

Note: Reserve / Resource figures from relevant Dec 2011 corporate documents. All technical / cost information, unless

otherwise noted, is from corporate Q2 2012 public disclosure.

1) Unit costs from most recent 43-101 Technical Report

2) 3 year average gold recovery calculated from Kinross reports

Value Creation Going Forward

• 20,000 m Phase IV drilling campaign has commenced

- Mainly focused on infill and geotechnical drilling

- 5,000 m dedicated to exploration

• Release Preliminary Economic Assessment in Jan 2013

- Defined process flow sheet

- Defined capital costs

• Further Optimize Gold Recovery

- Column test work continuing

- Will examine the potential for run of mine heap leach

• Outline Water Source

- Water exploration program as commenced

- Expand Exploration Activities

20

Atacama Pacific Gold Corporation 330 Bay Street, Suite 1210 Toronto, Ontario, M5H 2S8

Trading Symbol – ATM:TSXV

For further information visit www.atacamapacific.com

or email / call: Carl B. Hansen, President and CEO Email: [email protected] Phone: 416 861 8267