Embed Size (px)

Citation preview

CEPR-RIETI Workshop

Presenter: Prof. Wouter DEN HAAN London School of Economics / CEPR

December 10, 2015

Handout

http://www.rieti.go.jp/en/index.html Research Institute of Economy, Trade and Industry (RIETI)

“Fiscal Sustainability”

1

Fiscal Sustainability and

Self-Fulfilling beliefs

2

Overview

• The basics• Sustainability of sovereign debt is something you can loose quickly

• Fundamental versus self-fulling problems• They are related

• The role of monetary policy• Solution or part of the problem

• Conventional monetary policy

• Unconventional monetary policy

3

The Basics

Dt+1 = (1+r) Dt - St+1

• D: nominal government debt

• S: the nominal primary surplus (revenues minus expenses before interest payments)

• r: nominal interest rate

4

The Basics

Dt+1 = (1+r) Dt - St+1

Divide through by GDP (Yt+1)

Dt+1 / Yt+1 = (1+r) Dt/ Yt+1 - St+1 / Yt+1

= (1+r)[Dt/ Yt][Yt / Yt+1] - St+1 / Yt+1

= [(1+r)/(1+g)] Dt/ Yt - St+1 / Yt+1

5

The Basics

dt+1 (1+r-g) dt - st+1With:

dt = Dt / Yt

st = St / Yt

Everything is in real terms now

6

The Basics

dt+1 (1+r-g) dt - st+1

• This formula is based on many simplifications, but

• There is an important lesson:

If g is low relative to r then debt is unsustainable

unless primary surplus is high enough

7

Debt Limits

Source: OECD (2015) & Fournier and Fall (2015)

8

Fundamental

versus

Self-fulfilling Problems

9

When Becomes Debt Unsustainable?

I: Fundamental problems

• Structural problems low g

• Low commitment to debt repayment high r

• Cyclical problems low s

• High initial debt high r

10

When Becomes Debt Unsustainable?

II: Self-fulfilling problems

• Market looses confidence high r

• Debt increases higher r

• Market looses confidence etc

Are these empirically relevant?

11

0

5

10

15

20

25

30

Jan-

1990

Oct

-199

0Ju

l-199

1A

pr-1

992

Jan-

1993

Oct

-199

3Ju

l-199

4A

pr-1

995

Jan-

1996

Oct

-199

6Ju

l-199

7A

pr-1

998

Jan-

1999

Oct

-199

9Ju

l-200

0A

pr-2

001

Jan-

2002

Oct

-200

2Ju

l-200

3A

pr-2

004

Jan-

2005

Oct

-200

5Ju

l-200

6A

pr-2

007

Jan-

2008

Oct

-200

8Ju

l-200

9A

pr-2

010

Jan-

2011

Oct

-201

1Ju

l-201

2A

pr-2

013

Jan-

2014

Oct

-201

4Ju

l-201

5

10 yr gov't bond yields (%)

Greece

Ireland

Italy

Spain

Portugal

Germany

Fundamental or Sustainable Problem?

12

Mario Draghi (2012)

“The assessment of the Governing Council is that we are in … a ‘bad equilibrium’, namely

an equilibrium where you may have self-fulfilling expectations that feed upon themselves and generate very adverse

scenarios. So, there is a case for intervening, in a sense, to ‘break’ these expectations …”

Do Self-fulfilling Equilibria exist?

ECB Press conference, transcript from the Q&A, September 6 2012

13

Self-Fulfilling Debt Crisis

Source: De Grauwe and Ji (2013)

14

Monetary Policy

15

De Grauwe (2011)

… the UK government is ensured that the liquidity is around to fund its debt. This means

that investors cannot precipitate a liquidity crisis in the UK that could force the UK

government into default. There is a superior force of last resort, the Bank of England”

Role of Monetary Policy & Unsustainable Debt

16

Gross Government Debt (%GDP)

17

10-year sovereign debt yield

18

Krugman (2011)

“Many people now accept the point … that … countries that have given up the ability to

print money become vulnerable to self-fulfilling panics in a way that countries with

their own currencies aren’t …”

Role of Monetary Policy & Unsustainable Debt

19

Role of Monetary Policy & Unsustainable Debt

• Traditionally Monetary Policy was thought to be the problem!

• Conventional Monetary Policy

• Unconventional Monetary Policy

20

Role of Monetary Policy & Unsustainable Debt

Key papers in the literature:

• Calvo (1988)

• Corsetti and Dedola (2014)

• Hall and Reis (2015)

21

Monetary PolicySolution or Source of Problem

Calvo (1988)

“… The possible empirical relevance of the non-uniqueness issue becomes apparent when

examining the role of interest-bearing government debt. … Will … debt be paid off in

full, will the government find it optimal to resort to higher inflation or currency

devaluation to diminish the burden of the debt, etc.?”

22

Monetary PolicySolution or Source of Problem

• Unpredictable monetary policy was believed to be important for risk premia and high interest rate

•

• Independent monetary policy can be source of unsustainable debt

23

0

5

10

15

20

25

30Ja

n-19

90O

ct-1

990

Jul-1

991

Apr

-199

2Ja

n-19

93O

ct-1

993

Jul-1

994

Apr

-199

5Ja

n-19

96O

ct-1

996

Jul-1

997

Apr

-199

8Ja

n-19

99O

ct-1

999

Jul-2

000

Apr

-200

1Ja

n-20

02O

ct-2

002

Jul-2

003

Apr

-200

4Ja

n-20

05O

ct-2

005

Jul-2

006

Apr

-200

7Ja

n-20

08O

ct-2

008

Jul-2

009

Apr

-201

0Ja

n-20

11O

ct-2

011

Jul-2

012

Apr

-201

3Ja

n-20

14O

ct-2

014

Jul-2

015

10 yr gov't bond yields (%)

Greece

Ireland

Italy

Spain

Portugal

Germany

Monetary Policy: Problem or Solution?

24

Calvo (1988)Easy to Get Self-fulling Crises

Setup:

• Simple two-period model

• No commitment: Government reoptimizes in period 2

• Rational investors

• Financing need government = B

• Interest Rate = R

25

Calvo (1988)No Default Equilibrium

26

Calvo (1988)No Default Equilibrium

27

Conventional

Monetary Policy

28

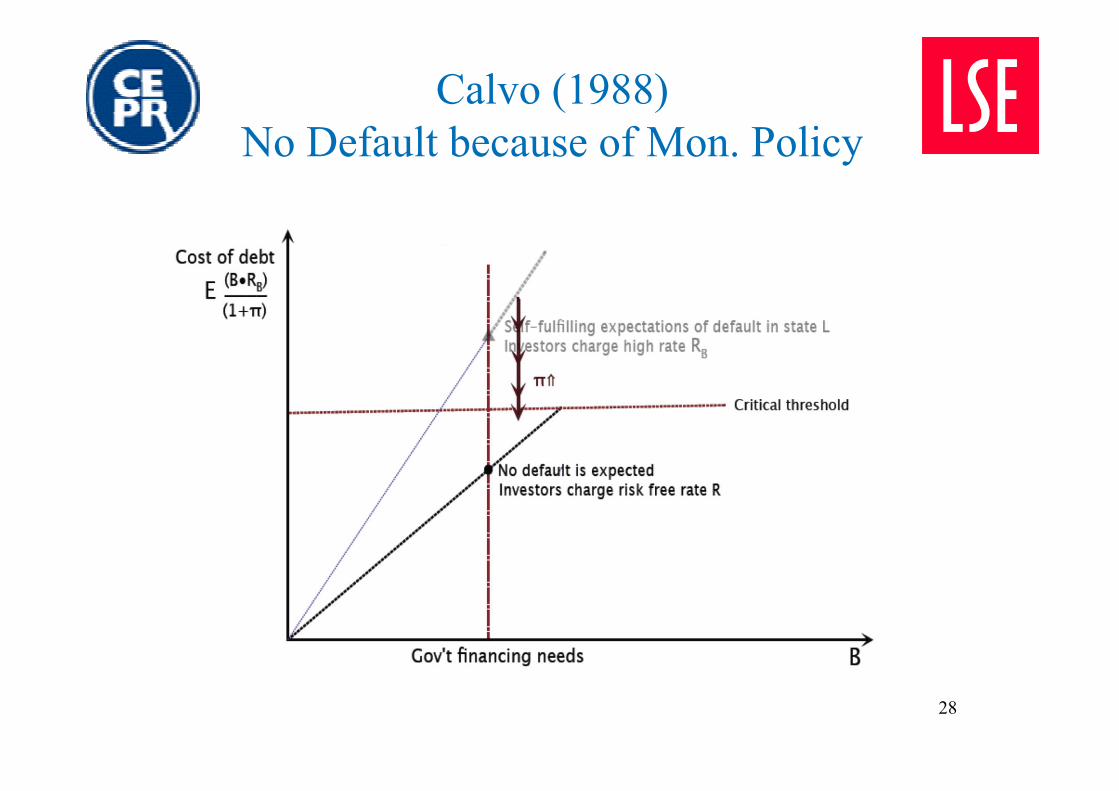

Calvo (1988)No Default because of Mon. Policy

29

Inflating Debt & Eliminating Self-fulfilling Panics

• Inflation must be unexpected• More likely if debt is long-term and issued during tranquil times

• The probability of government doing this (ever) must be low. If not, then investors would demand risk premium

30

Inflating Debt versus Regular (Partial) Default

• Even small partial default may have large fixed cost

• Small partial default through inflation probably not very costly

• Inflation means default on all debt, that is sovereign and private Inflation risk will increase yields on all debt

31

Monetary Policy & Eliminating Self-fulfilling Panics

Corsetti & Dedola (2014)

• Default because of self-fulfilling and fundamental reasons• 3 aggregate states:

• Expansion

• Recession

• Severe recession

• In period 2, government only reoptimizes with probability only self-fulfilling panic when fundamentals bad and/or government debt high

32

Corsetti and Dedola (2014)No Monetary Policy

33

Corsetti and Dedola (2014)Optimal Discretionary Monetary Policy

34

Monetary Policy & Eliminating Self-fulfilling Panics

Conclusion: Inflation possibility does not eliminate multiplicity

Why so little change?

• Agents are rational & inflation is costly

Why any change?

• Default and inflation are both distortionary, but there are advantages of smoothing these distortions

35

Unconventional

Monetary Policy

36

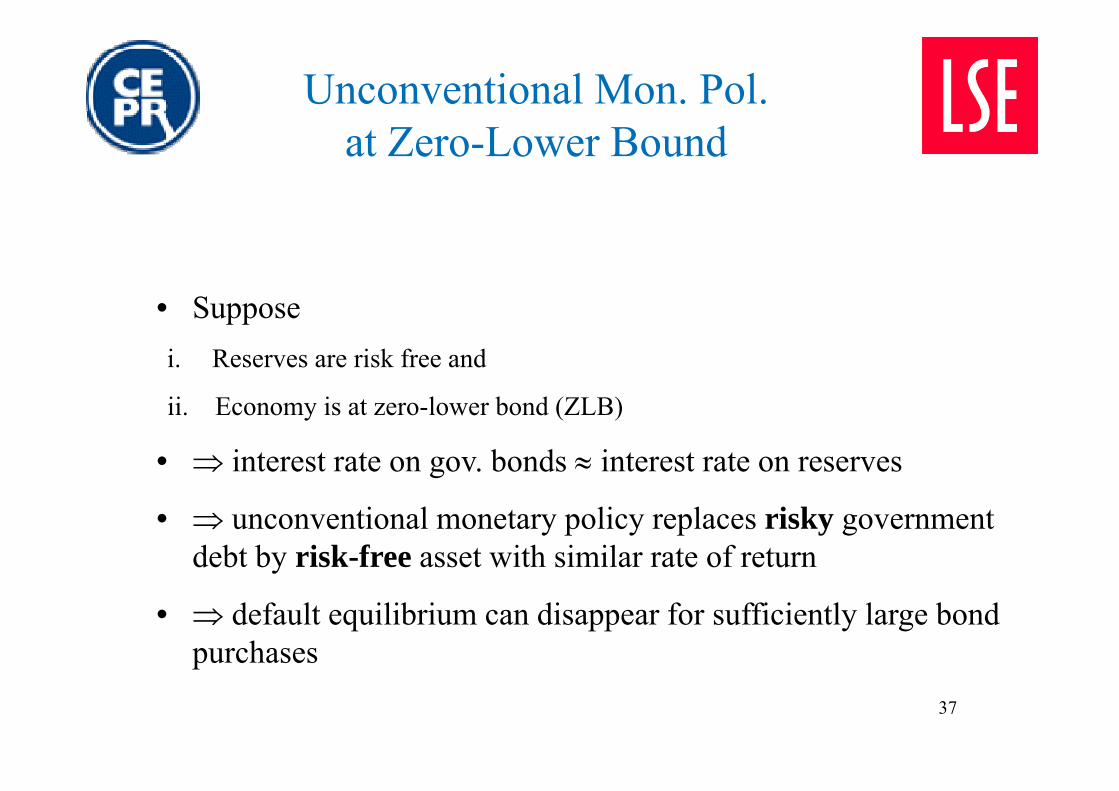

Unconventional Mon. Pol. Defined

Unconventional Monetary Policy Gov. Bond purchases

• Total liabilities of government (i.e. bonds + reserves) unchanged

• So why would this make any difference?

• Bonds ≠ reserves. Why?• Default risk different for bonds and reserves

• Interest rate could be different

37

Unconventional Mon. Pol. at Zero-Lower Bound

• Suppose i. Reserves are risk free and

ii. Economy is at zero-lower bond (ZLB)

• interest rate on gov. bonds interest rate on reserves

• unconventional monetary policy replaces risky government debt by risk-free asset with similar rate of return

• default equilibrium can disappear for sufficiently large bond purchases

38

Unconventional Mon. Pol. outside Zero-Lower Bound

• Suppose i. Reserves are risk free and

ii. Central bank pays interest on reserves

• interest rate on gov. Bonds (without default premium) interest rate on reserves

• unconventional monetary policy replaces risky government debt by risk-free asset with similar rate of return

• default equilibrium can disappear for sufficiently large bond purchases

39

Too Good to be True?

• If multiplicity can be broken by unconventional monetary policy

•

• Central banks should always engage in unconventional monetary policy

40

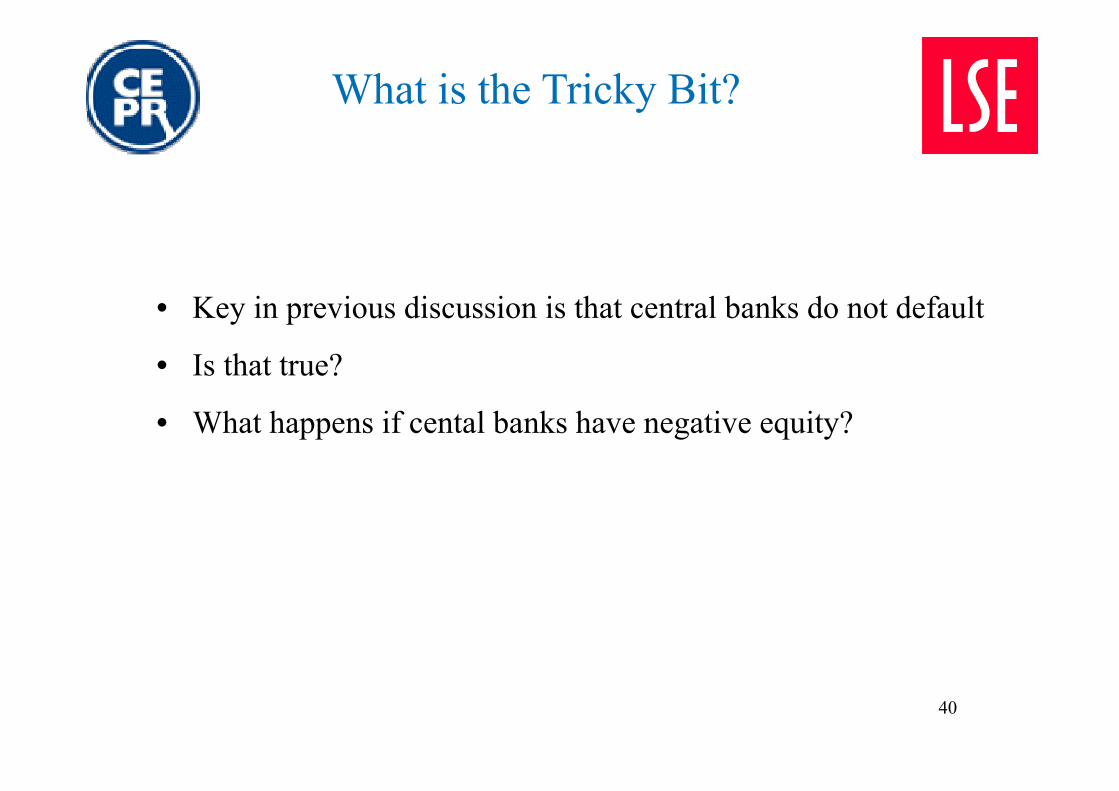

What is the Tricky Bit?

• Key in previous discussion is that central banks do not default

• Is that true?

• What happens if cental banks have negative equity?

41

Central Banks & Negative Equity

Two views

1. Central banks cannot have negative equity central bank may default or government recapitalizes central bank

2. Negative equity not a problem

Implied consequences

1. Default is not different unless this introduces a commitment mechanism for the government not to default

2. No default if central banks can have negative equity?

42

Central Banks & Negative Equity

Central bank balance sheet after default:

Assets Liabilities

Government Bonds 0 Reserves 1000Equity -1000

Is there a problem?

• Central banks can no longer reduce reserves in the usual way, that is by selling government bonds

•

• there could be default by inflation

• required reserves , which is similar to default

43

Central Banks & Negative Equity

Should we worry about central banks getting negative equity?

Hall and Reis (2015):

• FED (no default risk): There is risk for the FED losing the ability to stabilize prices given the historical volatility of interest rates and bond prices.

• ECB (with default risk): Little risk as long as default risk is priced into the bonds (that is, bonds can be bought cheaply).

• CBs with exchange risk: Here the situation is more problematic and it is important for such central banks to retain earnings during good times

44

References

Corsetti, G. And L. Dedola, 2014, The “Mystery of the Printing Press” Monetary Policy and Self-fulfilling Debt Crises, available at http://www.centreformacroeconomics.ac.uk/Discussion-Papers/2014/CFMDP2014-24-Paper.pdf.

De Grauwe, Paul, 2011, The Governance of a Fragile Eurozone, CEPS Working Document, No. 346, May 2011.

Fournier, Jean-Marc and Falilou Fall, 2015, Limits to Government Debt Sustainability, OECD Economics Department Working Paper No. 1229.

Hall, Robert E. And R. Reis, 2015, Maintaining Central-Bank Financial Stability under New-Style Central Banking, available at http://www.columbia.edu/~rr2572/papers/15-HallReis.pdf.

Krugman, P., 2011, Wonking Out About the Euro Crisis (Very Wonkish), available at http://krugman.blogs.nytimes.com/2011/08/08/wonking-out-about-the-euro-crisis-very-wonkish/

OECD, 2015, Achieving Prudent Debt Targets Using Fiscal Rules, OECD Economics Department Policy Notes, No. 28, July 2015.