Embed Size (px)

Citation preview

CEO Climate Change Task Force MeetingA Wall Street Perspective

Karl H. Pfeil III Managing DirectorPublic Power

December 3, 2007

www.fitchratings.com 2

The Credit Impact of Environmental Compliance

> Criteria – Managing Your Risks.

> Public Powers’ Environmental Credit Drivers

www.fitchratings.com 3

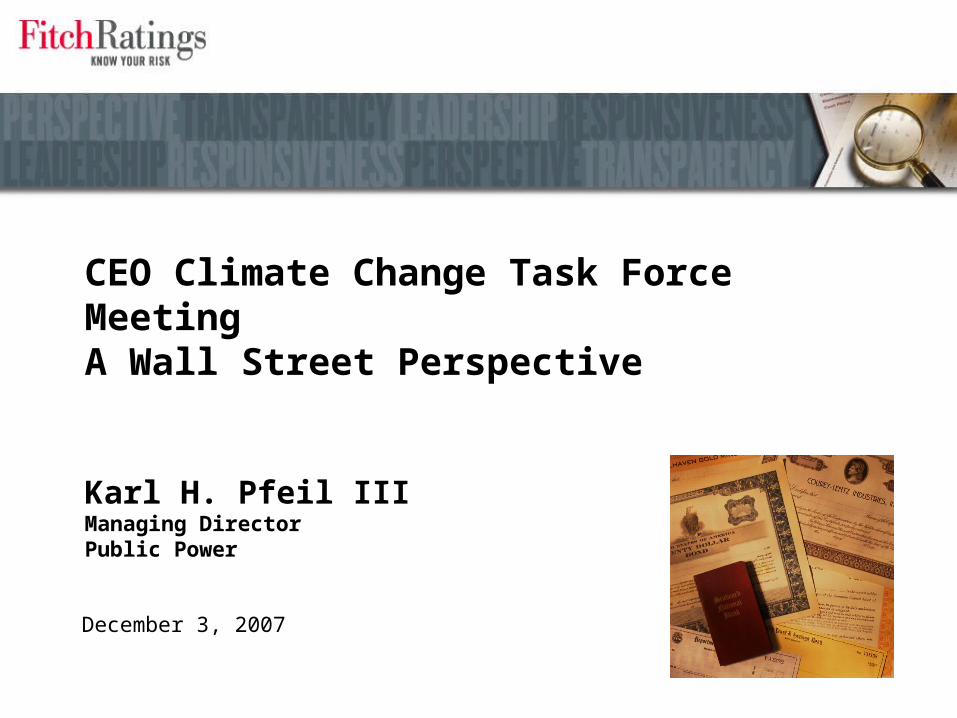

Primary Credit Factors

1. Mgmt

2. Customer Base

3. Risk Management

4. Power

Supply 5. Finances

6. Rates

7. Legal

Utility’sCredit

www.fitchratings.com 4

Location, Location, Location

> Each region has distinct

characteristics affecting the utilities’

credit profile:

— Fuel supply of wholesale market.

— Status of deregulated markets.

— Status of transmission

environment.

— Regional politics.

— Service territory characteristics.

— Environmental mandates.

—Ability to implement?

www.fitchratings.com 5

CO2 Regulation: Not if but when

> Fitch believes that there will be a carbon law at the federal level; however, it may

be a number of years off.

> Increasing number of state regulators are placing a cost on carbon in rate making

proceedings.

> More traditional Wall Street investors are now looking at carbon issues.

> Desire of industry participants to reduce regulatory risk by reducing uncertainty.

www.fitchratings.com 6

Current Industry Response to a Carbon Constrained Environment

> Build Clean Coal Plants

> Estimate and inform Investors as to Possible Costs

> Improved Efficiency

> Demand Side Management

www.fitchratings.com 7

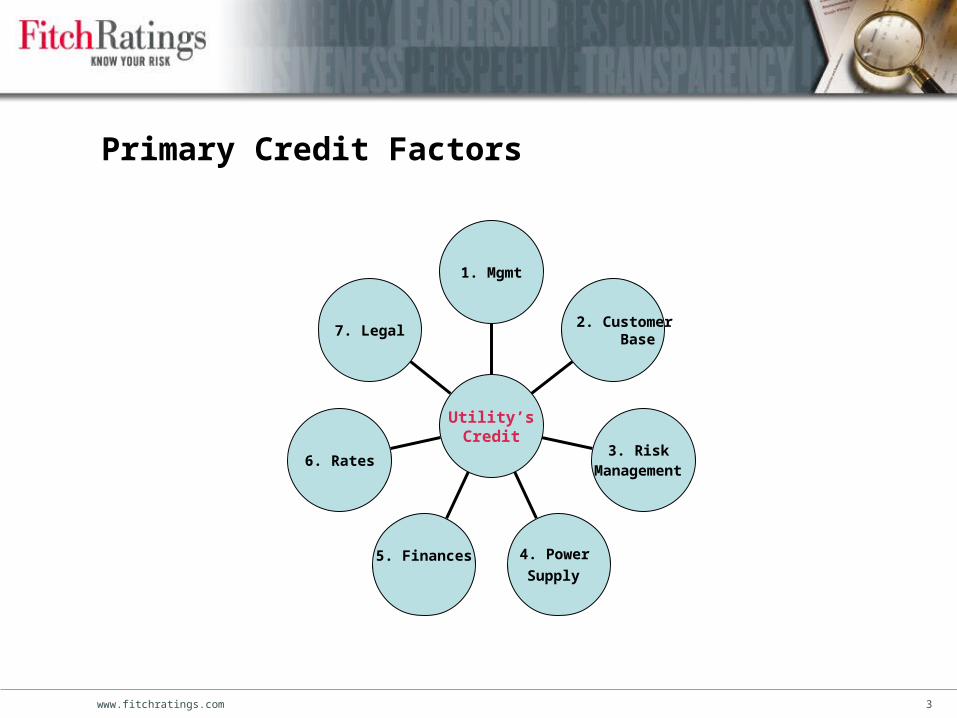

Challenges for CO2

> The power industry will need economically feasible CO2 emission control

technology

> The development of these devices will be challenged by:

– The time horizon for investors and developers

– The time horizon for electric power generators

– A realistic estimate for the price of “carbon” is challenged by the lack of US

regulation.

> Ultimate market size

> Uncertainty of

– Timing

– Regulatory framework

www.fitchratings.com 8

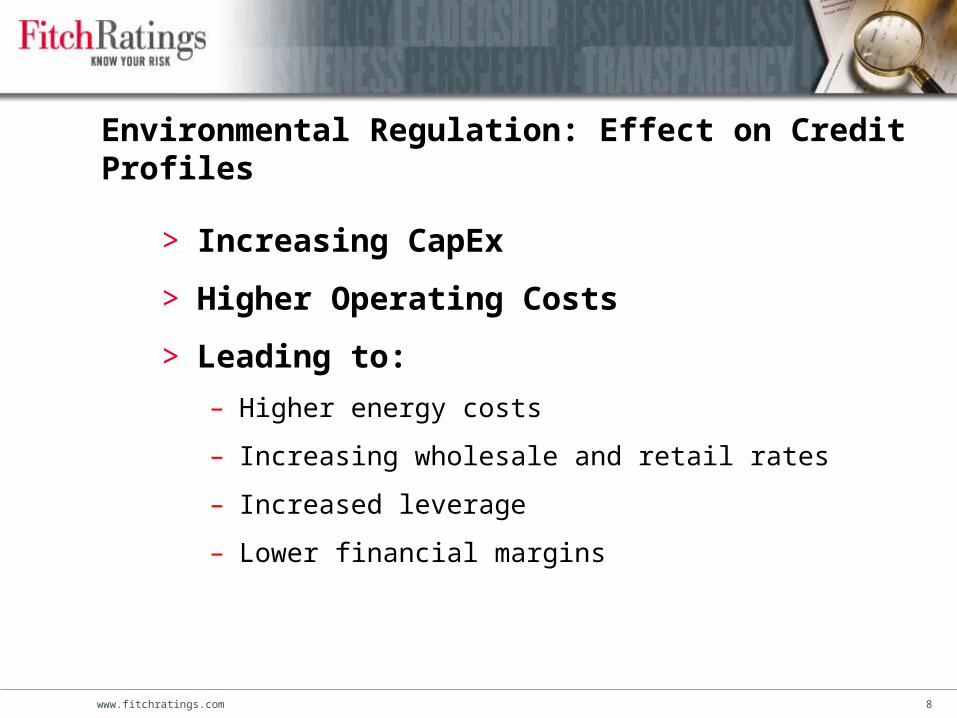

Environmental Regulation: Effect on Credit Profiles

> Increasing CapEx

> Higher Operating Costs

> Leading to:

– Higher energy costs

– Increasing wholesale and retail rates

– Increased leverage

– Lower financial margins

www.fitchratings.com 9

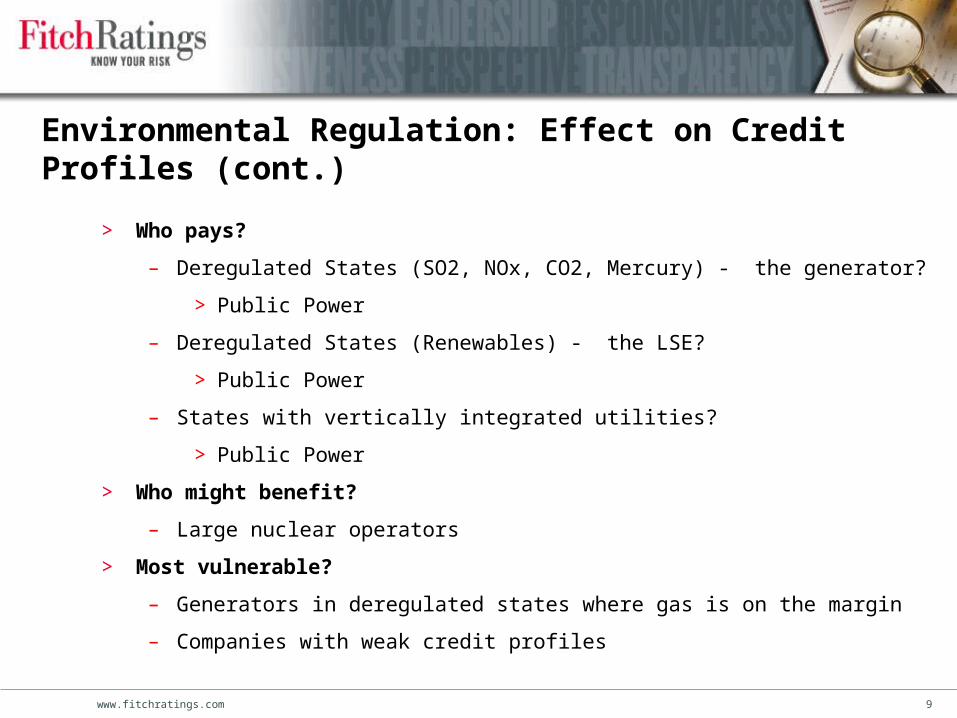

Environmental Regulation: Effect on Credit Profiles (cont.)

> Who pays?

– Deregulated States (SO2, NOx, CO2, Mercury) - the generator?

> Public Power

– Deregulated States (Renewables) - the LSE?

> Public Power

– States with vertically integrated utilities?

> Public Power

> Who might benefit?

– Large nuclear operators

> Most vulnerable?

– Generators in deregulated states where gas is on the margin

– Companies with weak credit profiles

www.fitchratings.com 10

Renewable Portfolio Standards (and Goals)

State Goal

☼ PA: 18%¹ by 2020

☼ NJ: 22.5% by 2021

CT: 23% by 2020

MA: 4% by 2009 + 1% annual increase

WI: requirement varies by utility; 10% by 2015 goal

IA: 105 MW

MN: 25% by 2025(Xcel: 30% by 2020)

TX: 5,880 MW by 2015

☼ AZ: 15% by 2025

CA: 20% by 2010

☼ *NV: 20% by 2015

ME: 30% by 200010% by 2017 - new RE

State RPSHI: 20% by 2020

RI: 16% by 2020

☼ CO: 20% by 2020 (IOUs)

*10% by 2020 (co-ops & large munis)

☼ DC: 11% by 2022

☼ NY: 24% by 2013

MT: 15% by 2015

IL: 25% by 2025

VT: RE meets load growth by 2012

Solar water heating eligible

*WA: 15% by 2020

☼ MD: 9.5% in 2022

☼ NH: 23.8% in 2025

*VA: 12% by 2022

MO: 11% by 2020

☼ *DE: 20% by 2019

☼ NM: 20% by 2020 (IOUs) 10% by 2020 (co-ops)

☼ NC: 12.5% by 2021 (IOUs)10% by 2018 (co-ops & munis)

ND: 10% by 2015

OR: 25% by 2025 (large utilities)5% - 10% by 2025 (smaller utilities)

☼ Minimum solar or customer-sited RE requirement* Increased credit for solar or customer-sited RE

¹PA: 8% Tier I / 10% Tier II (includes non-renewables)

Source: DSIRE (www.dsireusa.org), September 2007

www.fitchratings.com 11

“Renewable” Technologies (state specific)

Frequently on the list

> Wind

> Solar thermal electric

> Photovoltaic

> Landfill gas/methane

> Fuel cells

> Municipal solid waste

> Geothermal electric

> Biomass

> Tidal/wave/ocean thermal

Also included

> Geothermal heat pump

> Hydroelectric

> Small power generation

> Poultry litter

> Sustainably harvested biomass

> Resource recovery facilities

> Ethanol, methanol, biodiesel

> Anaerobic digestion

> Waste energy

> Coal bed methane

www.fitchratings.com 12

Where the Wind Blows

RIDGE CREST ESTIMATES (LOCAL RELIEF > 1000 FT)

1234567

WIND POWER WIND POWERW/m2

M / S MPH W/m2M / S MPH

0 0 0 0 0 0

100 4.4 9.8 200 5.5 12.5

150 5.1 11.5 300 6.4 14.3

200 6.7 12.5 400 7.0 15.7

250 7.0 13.4 500 7.5 16.8

300 6.4 14.3 600 8.0 17.9

400 7.0 15.7 800 8.8 19.7

1000 9.4 21.1 2000 11.9 26.6

WORLD

POWERCLASS

10m (33ft) 50M (164 FT)

SPEED SPEED

RIDGE CREST ESTIMATES (LOCAL RELIEF > 1000 FT)

1234567

WIND POWER WIND POWERW/m2

M / S MPH W/m2M / S MPH

0 0 0 0 0 0

100 4.4 9.8 200 5.5 12.5

150 5.1 11.5 300 6.4 14.3

200 6.7 12.5 400 7.0 15.7

250 7.0 13.4 500 7.5 16.8

300 6.4 14.3 600 8.0 17.9

400 7.0 15.7 800 8.8 19.7

1000 9.4 21.1 2000 11.9 26.6

WORLD

POWERCLASS

10m (33ft) 50M (164 FT)

SPEED SPEED

www.fitchratings.com 13

Where the Sun Shines

www.fitchratings.com 14

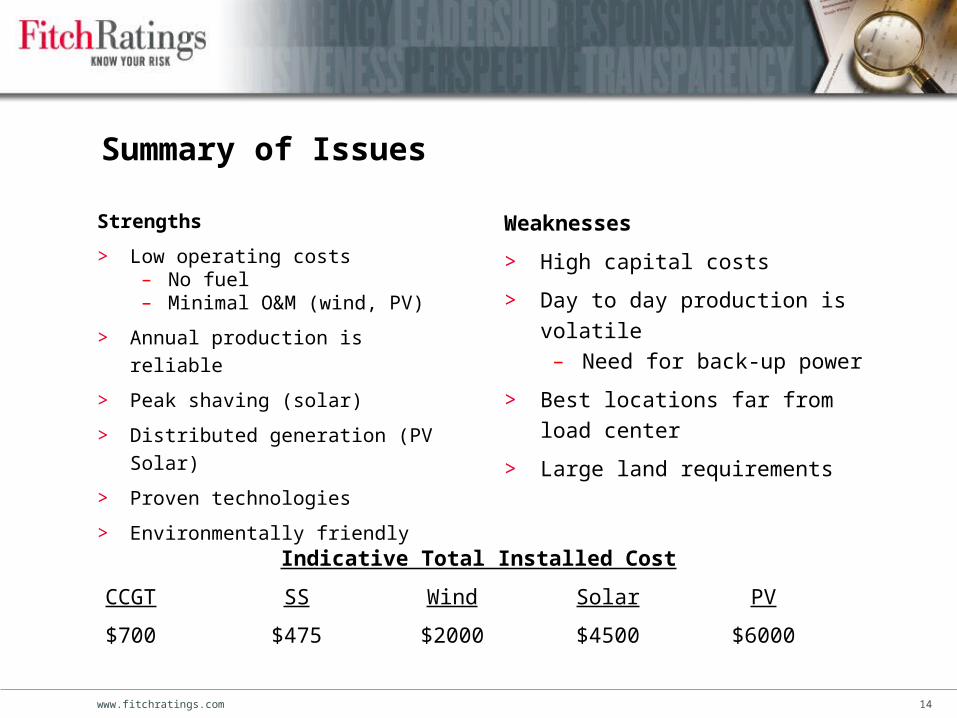

Summary of Issues

Strengths

> Low operating costs– No fuel– Minimal O&M (wind, PV)

> Annual production is reliable

> Peak shaving (solar)

> Distributed generation (PV Solar)

> Proven technologies

> Environmentally friendly

Weaknesses

> High capital costs

> Day to day production is volatile– Need for back-up power

> Best locations far from load center

> Large land requirements

Indicative Total Installed Cost

CCGT SS Wind Solar PV

$700 $475 $2000 $4500 $6000

www.fitchratings.com 15

RPS Compliance vs. Technology Issues

> Expect wind to be primary means of compliance.

– Requires additional investment for back-up capacity

– Increased ancillary services

> Prime locations for wind and solar are distant from load.

– Significant transmission

– Difficult to satisfy in-state production requirements

> Allow purchase of green credits (especially in Southeast)

> Encourage consumer involvement

– Financial incentives to conserve

– Financial incentives to self-generate (PV solar)

www.fitchratings.com 16

The Credit Impact

www.fitchratings.com 17

Many coal units will be replaced

US Coal-Fired Generating Plants

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

200520001995199019851980197519701965196019551950194519401935193019251920

Date Placed in Service

Tota

l Nam

epla

te C

apac

ity (M

W)

www.fitchratings.com 18

For a Stable Sector – The issues are very complex

Housing Declines

Housing Declines

Rates / Regulation

Rates / Regulation

Fuel Costs

Fuel Costs

EnvironmentalRegulation

EnvironmentalRegulation New GenerationNew Generation

Increasing Capital Costs

Increasing Capital Costs

www.fitchratings.com 19

Governance / Management

> Single most important credit factor

that affects all other areas of a utility.

– Organizational strategy.

– Working relationship between

Management and Board of

Directors (council).

– Ability to get things done (track

record).

– How will this impact your utility

compared to others in your

region?

– Know your risk – The more you

understand your risks the better you

can plan for them.

www.fitchratings.com 20

Fitch Public Power Credit Outlook for 2008

> Outlook for 2008 is Stable with the longer term Outlook reflecting increasing

Negative pressures.

> While our near-term outlook for the sector is stable, the public power industry

remains vulnerable to challenges that could pressure some credit ratings into the

future.

> Public power has historically proven itself to be a very solid investment despite past

complexities facing the industry such as deregulation, fuel price volatility, and the

corporate credit crisis.

> Q: Going forward how will public power address the new issues: growing power

resource needs, higher capital and labor costs, and uncertainties associated with

environmental policies and renewable portfolio standards, which have made it

harder to build new coal-fired generation and limits the options for new base-load

power resources?

– The answer rests with management!

Fitch Ratings

www.fitchratings.com

London

Eldon House

2 Eldon Street

London EC2M 7UA

UK

+44 207 417 4222

Singapore

7 Temasek Blvd.

Singapore 038987

+65 6336 6801

New York

One State Street Plaza

New York, NY 10004

+1 212 908 0500

+1 800 75 FITCH

The Fitch Group Fitch Ratings Algorithmics Fitch Training