Embed Size (px)

Citation preview

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 10-1LESSON 10-1

Notes Receivable

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

2

LESSON 10-1

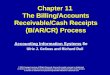

TERMS REVIEWTERMS REVIEW

notes receivable – promissory notes that business receives from customers

dishonored note – note that is not paid when due

page 296

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 10-1

ISSUING A NOTE RECEIVABLE FOR AN ISSUING A NOTE RECEIVABLE FOR AN ACCOUNT RECEIVABLEACCOUNT RECEIVABLE

April 3. Accepted a 30-day, 12% note from Duane Jansen for an extension of time on his account, $300.00. Note Receivable No. 11.

page 291

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 10-1

ISSUING A NOTE FOR A SALEISSUING A NOTE FOR A SALE

April 4. Accepted a 90-day, 12% note from Mark Carver for the sale of an appliance, $450.00. Note Receivable No. 12.

page 291

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

5

LESSON 10-1

1. Calculate interest income.

2. Record note.

3. Record interest income.

4. Enter total cash received.

RECEIVING CASH FOR A RECEIVING CASH FOR A NOTE RECEIVABLENOTE RECEIVABLE page 292

May 3. Received cash for the maturity value of Note Receivable No. 11: principal, $300.00, plus interest, $3.00; total, $303.00. Receipt No. 452.

PrincipalInterest

RateFraction of Year

= Interest× ×

$300.00 12%30

360 = $3.00× ×

4422

33

11

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 10-1

1. Calculate interest income.

2. Record the debit for the total amount receivable.

3. Record a credit for the note principal.

4. Record a credit for the interest income.

RECORDING A DISHONORED RECORDING A DISHONORED NOTE RECEIVABLENOTE RECEIVABLE page 293

June 1. Ruth Javinsky dishonored Note Receivable No. 8, a 30-day, 12% note, maturity value due today; principal, $250.00; interest, $2.50; total, $252.50. Memorandum No. 120.

Principal Interest Rate Fraction of Year = Interest× ×

$250.00 12%30360 = $2.50× ×

44

22

33

11

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 10-1

RECEIVING CASH FOR A DISHONORED RECEIVING CASH FOR A DISHONORED NOTE RECEIVABLENOTE RECEIVABLE page 294

MaturityValue

InterestRate

Fractionof Year

=AdditionalInterest

× ×

1. Calculate number of days from maturity date to date of payment.2. Calculate additional interest income.

Time Number of DaysJune 1 through 30 29 (30 – 1 = 29)July 31August 31 September 1 through 30 30Total number of days 121 days 11

$252.50 12%121360

= $10.18× × 22

September 30. Received cash from Ruth Javinsky for dishonored Note Receivable No. 8: maturity value, $252.50, plus additional interest, $10.18; total, $262.68. Receipt No. 201.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 10-1

3. Record payment of the account receivable.

4. Record additional interest income.

5. Enter total cash received.

RECEIVING CASH FOR A DISHONORED RECEIVING CASH FOR A DISHONORED NOTE RECEIVABLENOTE RECEIVABLE page 294

3344

55

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 10-2LESSON 10-2

Unearned and Accrued Revenue

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 10-2

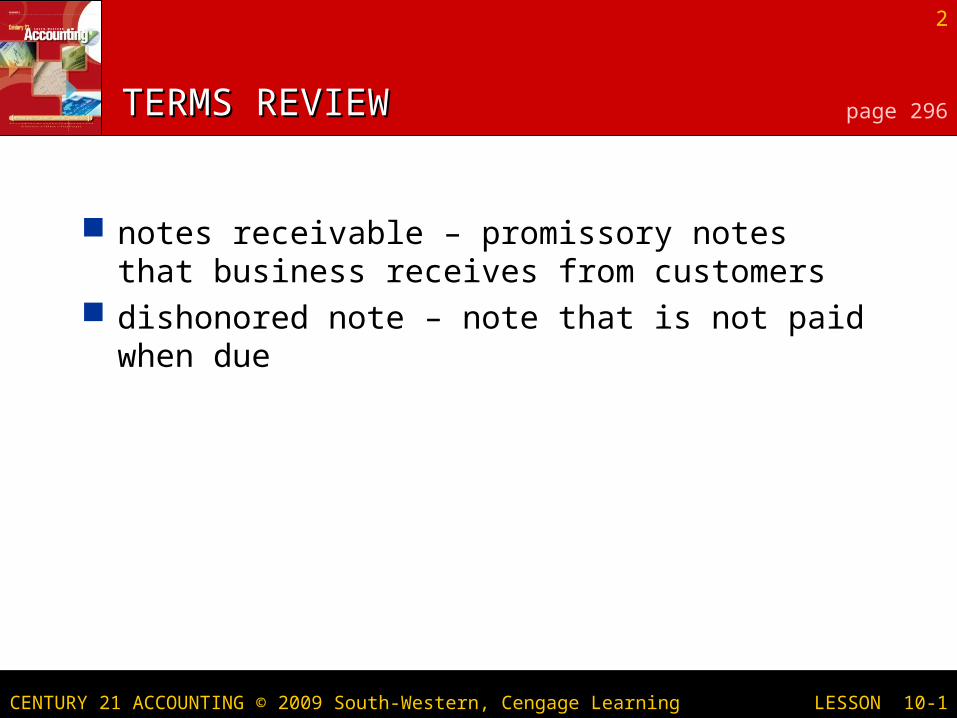

TERMS REVIEWTERMS REVIEW

unearned revenue – revenue that you’ve received in one fiscal period but won’t be earned until the next fiscal period For example – Prepaid Rental Income

accrued revenue – Revenue that you’ve earned but will not receive until a later fiscal period For example – Interest income on a note receivable

page 302

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 10-2

1. Debit the revenue account.

2. Credit the liability account.

ADJUSTING ENTRY FOR UNEARNED REVENUE ADJUSTING ENTRY FOR UNEARNED REVENUE INITIALLY RECORDED AS A REVENUEINITIALLY RECORDED AS A REVENUE

11

22

page 297

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 10-2

1. Debit the liability account.

2. Credit the revenue account.

REVERSING ENTRY FOR UNEARNED REVENUE REVERSING ENTRY FOR UNEARNED REVENUE INITIALLY RECORDED AS A REVENUEINITIALLY RECORDED AS A REVENUE

11

22

page 298

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

13

LESSON 10-2

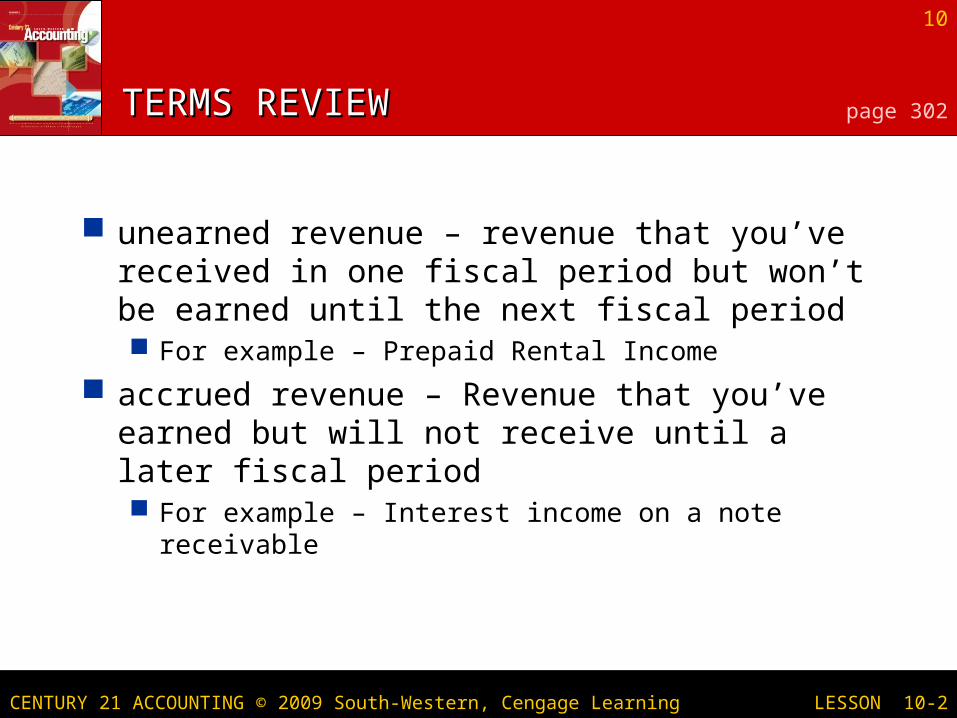

PrincipalInterest

RateFraction of Year

= Accrued Interest Income× ×Note

$500.00 10%30

360 = $4.17× ×12

$700.00 10%15

360 = 2.92× ×13

1. Calculate interest earned on the notes.

2. Record entry to accrue interest income.

ADJUSTING ENTRY FOR ACCRUED ADJUSTING ENTRY FOR ACCRUED INTEREST INCOMEINTEREST INCOME page 299

11

22

Total accrued interest income, December 31 . . . . $7.09

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

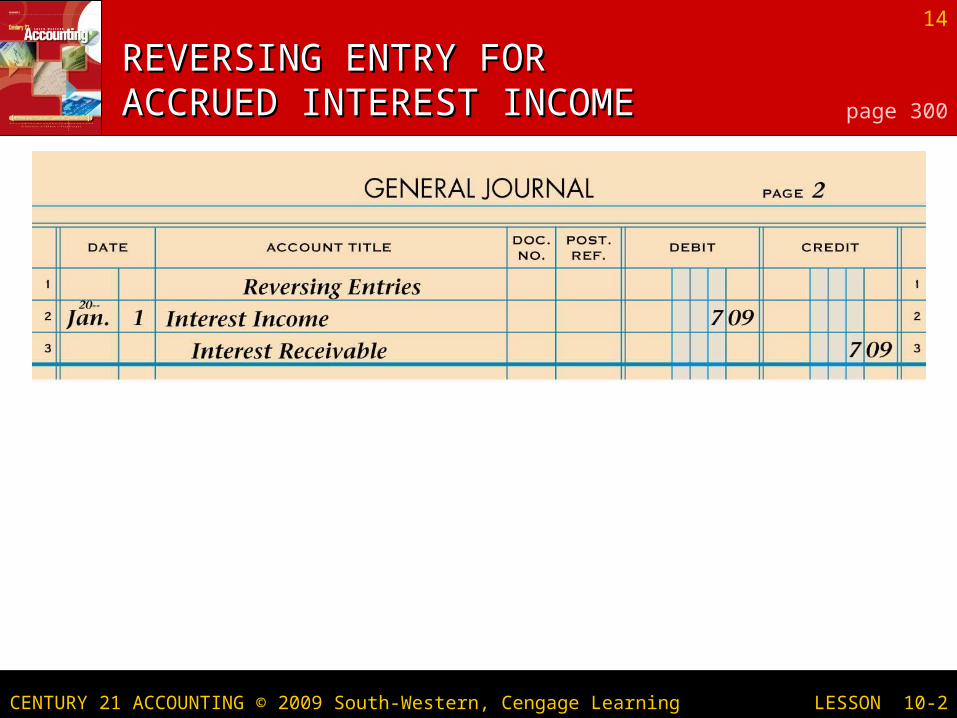

14

LESSON 10-2

REVERSING ENTRY FOR REVERSING ENTRY FOR ACCRUED INTEREST INCOMEACCRUED INTEREST INCOME page 300