Embed Size (px)

Citation preview

1

Centre for Finance Working Paper Series

Working paper 2009 008

Industry Effects of Recent Terrorist Attacks: Evidence From Singapore

Vikash Ramiah, Clara Wong Chia Hui and Sinclair Davidson

Abstract

In this paper, the impact of five recent terrorist attacks on equities listed on the

Singapore Stock Exchange is examined. We analyse how these events affect the

different sectors in Singapore, using the Global Industry Classification Standard.

Employing a variety of parametric and non-parametric tests, the relationship between

stock returns for equities listed in these sectors and terrorist attacks are analysed.

The empirical evidence shows significant short-term negative abnormal returns

around the September 11 attacks and, to a lesser extent, the Bali, London and

Mumbai bombings. Furthermore, some weak positive equity responses in the long

run were found in the Bali, London and Mumbai bombings, while no effect was found

from the Madrid attack on the Singaporean market. The results show that there is

evidence of a varied impact on the systematic risk of some of the sectors, for each of

the attacks.

2

I. Introduction

In a recent study by Ramiah, Maher, Ghafouri and Cam (2007), they find that the

terrorist attacks of September 11 had the most influence on the Australian equity

market, with the Pharmaceutical, Materials, Capital Goods, Real Estate and Group

Retailing Industries recording significantly negative abnormal returns. Conversely,

only the Water and Insurance sectors exhibit positive abnormal returns. In our paper,

we adopt a similar approach used by Ramiah, Maher, Ghafouri and Cam (2007), but

examine the impact of five recent terrorist attacks on the Singaporean equity market.

In an alternative study, Cam (2006), suggests that investors do not necessarily react

negatively to terrorist attacks. This is because equity holders tend to respond

negatively to such events, only if they perceive an increase in the expected costs of

terrorist activities. In this study, we argue that market participants may not react at

all if they do not perceive that the attack has an impact on expected returns. It is

possible that stock markets do not react negatively on days surrounding a major

terrorist attack. Through substitution effects, investors may move their investments

to neighbouring countries, and this can result in a positive externality for other

financial markets. As a result, investment paradise does not have to be

geographically remote from the country under attack, as neighbouring countries can

face different levels of terrorist risk. We believe that markets can respond differently

to the different attacks, and that the variability in risk and returns differs significantly

across different sectors within an economy.

The Singaporean Stock Exchange provides an ideal testing ground for several

reasons. First, Singapore has a dense urban setting with a high population density

(Singh, D., 2002). Such a populous nation with limited land suggests an eminent

3

likelihood for the presence of a high concentration of people within a specific location

at a point in time. With such a setting in place, it is very easy for terrorist groups to

achieve a significant number of casualties in the execution of a single operation.

Therefore, terrorist attacks can readily inflict death by the dozens, inflicting much fear

and instability in the hearts of people.

Second, Singh (2002) notes that Singapore has a relatively large Muslim community,

being in close proximity to other Islamic nations. The internal concentration of

Muslims, bolstered by the familiarity of similar counterparts in neighbouring countries,

suggests greater ease of coordinating and facilitating information between attacks.

Singh (2002) asserts that these terrorist groups are often made up of individuals with

strong Muslim influences, as indicated by the Jemmah Islamiah operations, which is

almost exclusively comprised of Muslims.

Finally, Singh (2002) shows that Singapore has many western establishments. This

is borne through Singapore’s historical ties with the British colony, and its current

western influences. This leaves Singapore vulnerable to attacks by terrorists that

have an agenda, set primarily to instigate mass destruction of infrastructures, largely

owned by these foreign counterparts.

In Singapore’s bid to express its strong support of the US anti-terror campaign, Singh

(2002) has identified the proactive steps which Singapore has adopted, the first of

which was the firm action taken against domestic extremists. Another involved

Singapore being one of the first country outside of North America to sign up for a US

Customs Container Security Initiative (CSI), which promises to safeguard US bound

containers issued from Singapore’s port. Therefore, it would be apparent from these

4

actions that Singapore has an ongoing strategic alignment with the US, which

inadvertently exposes Singapore as a prominent terrorist target, by virtue of its

alliance with the US. Tan (2003) reports that threats have been issued previously

towards Singapore, but were fortunately aborted, either because they were foiled by

security agencies or were not pursued for other reasons. Based on these findings, it is

evident that terrorist networks are indeed prevalent within Singapore, and could

possibly be currently sowing the seeds of terrorism, waiting to spring an attack.

Clearly, despite its close brush with terrorism, Singapore will continue to be

susceptible to future terrorist attacks.

Many global capital markets across the globe remained in operation on and after

September 11, with the information process realising statistically negative market

reactions. This result is supported by the findings of Chen and Siems (2004) and

Richman, Santos, and Barkoulas (2005), who showed that the Singaporean equity

market reacted negatively to the September 11 terrorist attacks. The evidence

provided by Cam (2006), Ramiah, Calabro, Maher, Ghafouri, and Cam (2007) and

Ramiah, Naughton, Hallahan and Anderson (2007a, 2007b) on industry effects of

terrorism in the United States, Australia, Japan and Malaysia respectively points

towards different countries react differently to terrorist activities. Furthermore the

existing literature argues that a market’s reaction also depends on where the terrorist

activities occurred.

To the best of our knowledge, there is no current study that looks specifically at the

short term impact of the September 11 attacks on the sectors within the Singaporean

equity market. The objective of this paper, therefore, is to fill this gap. Our

5

contributions are as follows. First, we identify which industries in Singapore were

affected. Second, we look at how subsequent attacks impacted on these industries.

Similar to the early literature on terrorism event studies, we have included firm specific

information, and thus report results which contain both the collective impact of terrorist

attacks, and other non terrorist components. Much of the extant literature may lead

one to conclude that terrorist attacks lead to an increase in terrorist risk, and therefore

reflect a negative sentiment. We argue that such generalizations and conclusions

should not be drawn until one considers the industry effects of terrorist attacks post

September 11. To support our hypothesis, we have adopted the approach used by

Ramiah, Maher, Ghafouri and Cam (2007) in exploring the impact of four subsequent

terrorist attacks that occurred in Bali, Madrid, London and Mumbai on the

Singaporean Stock Exchange. By observing the industry effects in Singapore, we

can determine how Singaporean investors’ reacted to the recent major terrorist

attacks. As such, this study is considered to be unique, in the sense that it is the first

study that looks at the short term effects of the five recent attacks on the different

Singaporean industries. The value that our research has created for investors is the

provision of a seemingly relevant guide to making an investment decision in

Singapore, in the event of another terrorist attack. Such analysis will be especially

beneficial to portfolio managers that use the top-down investment process. The

second stage of this process deals with the factors influencing the industry and we

contribute to this debate by adding the terrorist impact on the different industries. We

observe that more than one sector within the Singaporean equity market is sensitive

to international terrorist attacks, which manifests vital implications for Singapore’s

financial and economic security.

6

Our results are consistent with the prior literature, supporting the findings that the

events of September 11 indeed had a negative impact on the Singaporean equity

market. Furthermore, it is revealed that the market as a whole is fairly less sensitive

to the major terrorist attacks post September 11. Our contribution to this debate is

that while we show that the major terrorist attacks following September 11 did not

radically affect the Singaporean equity market as a whole, certain industries were

more severely affected. In Section II, we present the data and methods used in this

paper. Section III presents the empirical findings and Section IV provides some

concluding remarks.

II. Data and Methods

Data

We use daily stock return indexes, returns calculated from the Straits Times share

price index, and the 10-year bond rate, for the period August 1999 to February 2007,

obtained from Datastream. We have a total of 673 stocks in our sample. We construct

industry portfolios based on the Global Industry Classification Standards (GICS). One

of the practical issues that we face in this process is the small number of firms within

some industry sectors. To overcome this issue, we amalgamated some of the

industries described by GICS, and also introduce an extra sector known as ‘Others’,

which consists of industries that have a low firm count. Note that the 18 industries

include ‘Others’ which constitute 4 additional sectors, these being the

Pharmaceuticals, Utilities, Defence and Telecommunications sectors.

Table 1 reports the descriptive statistics for each of the different industries. The

average daily return for the Capital Goods, Consumer Durables and Apparels, Media,

7

Software and Services, Technology, Hardware and Equipment, and Healthcare

sectors are negative. The remaining sectors exhibit close to zero returns for the

period, with the exception of the Energy and Real Estate sectors which reveal

substantially positive returns. Furthermore, we fail to reject the null hypothesis that the

returns for the Healthcare, Consumer Durables and Apparels, Automobiles, Food and

Beverages, Transportation and Media sectors are normally distributed. Table 1 also

includes the standard deviation, skewness, excess kurtosis, range of returns, and the

number of firms in each of the industry sectors. Details of the five terrorist attacks that

occurred in the United States, Bali, Madrid, London and Mumbai, including the official

trading date after the event, are summarised in Table 2.

Methodology

We define daily return as:

=

−1

lnit

it

itSRI

SRIDR (1)

where DRit is the daily return for stock i, SRIit is the stock return index for stock i at

time t, and SRIit-1 is the stock return index for stock i at time t-1.

The ex-post abnormal returns (ARit) are calculated following Cam (2006), Ramiah,

Calabro, Maher, Ghafouri, and Cam (2007), Ramiah, Naughton, Hallahan and

Anderson (2007a, 2007b) and Brown and Warner (1985). These are calculated as the

difference between observed returns of firm i at event day t, and the expected return,

E(Rit):

( )ititit RERAR −= (2)

The daily expected return, E(Rit), is calculated as the average of the last 260 observed

daily returns:

8

( ) mtit RRE10

ββ += (3)

The abnormal return for industry i at time t, ARit, is obained by averaging the abnormal

return of each form within the industry:

∑=

=N

i

itit ARN

AR1

1 (4)

Parametric Tests

The parametric tests used in this study rely on the important assumption that the

industry abnormal returns and cumulative abnormal returns are normally distributed.

The standard t-statistic for the abnormal return is given by:

( )it

it

ARARSD

ARt

it= (5)

where SD(ARit) is an estimate of the standard deviation of the abnormal returns. By

cumulating the periodic abnormal return for each industry over five days, we obtain

the five day cumulative abnormal return, CARit:

∑=

=5

1

5t

itit ARCAR (6)

The t-statistic for the five day cumulative abnormal return is obtained by dividing

CAR5it by the standard deviation of the five day cumulative abnormal return,

SD(CAR5it):

( )it

it

CARCARSD

CARt

it 5

55

= (7)

Non-Parametric Tests

The literature dealing with abnormal returns shows that they are not normally

distributed. More specifically, the distribution of the abnormal returns tends to exhibit

9

fat tails and positive skewness. Under these circumstances, parametric tests tend to

reject the null too often when testing for positive abnormal performance and too

seldom when testing for negative abnormal returns. As a robustness test, we turn to

an alternative test developed by Corrado (1989). This non-parametric test is more

powerful at detecting the false null hypothesis of no abnormal returns.

We transform each firm’s abnormal returns, ARit into ranks, Ki, over the combined

period, Ti, of 260 days. This is denoted as:

( )iti ARrankK = (8)

Following Cam (2006), the period is broken up into the 244 days prior to the event, the

event day and 15 days after the event. The ranks in the event period for each firm are

then compared with the expected average rank,−

iK , under the null hypothesis of no

abnormal returns. This is given by:

25.0 i

i

TK +=

−

(9)

The non-parametric t-statistic, tnp, for the null hypothesis of no abnormal returns for

each industry is given by:

−

=∑

=

−

_

1

1

KSD

KKN

t

N

i

ii

np (10)

where

−

KSD is the standard deviation of the average rank, and is denoted by:

∑ ∑=

−−

−=

T

t

iit KKNT

KSD1

2

2

11 (11)

10

Regression Analysis

Using the CAPM, we then test if terrorist attacks have had an impact on the

systematic risk of Singaporean industries on the days of the attack. We include a

multiplicative dummy variable in the standard CAPM to test this possibility. The model

we estimate is therefore:

itftmtIftmtIIftIt Drrrrrr εββφ ~*]~~[]~~[~~ 21 +−+−+=− (12)

where Itr~ is industry I’s return at time t, ftr~ is risk free return at time t, mtr~ is return

on the market at time t and D is a dummy variable that takes the value of 1 on the day

of the event, and 0 otherwise. This variable is meant to capture the effect of terrorist

attacks on the systematic risk. The inclusion of an additive dummy variable in

equation (12), results in a near singular variance-covariance matrix. As a result, we

estimate a separate equation to test if the intercept was affected by the attacks:

itIftmtIIftIt Drrrr εααϕ ~]~~[~~ 21 ++−+=− (13)

We gathered the returns for each industry 244 days prior to the event, and 15 days

after the event. Standard tests and residual diagnostics revealed no major concerns

with the above two econometric models. We also test if these dummy variables were

redundant in the above equations using a Wald test for restrictions.

Further, we considered the long term impact of the terrorist events on the market. The

test determines whether the level of risk; specifically captured by structural changes,

was altered after the event day:

itIftmtIftmtIIit SDSDrrrrr εδδδϕ ~*]~~[]~~[~ 321 ++−+−+= (14)

11

where SD is a dummy variable that takes the value of 0 prior to the event, and 1 after

the day of the event. This variable is meant to capture the structural changes and

influence of terrorist attacks on the systematic risk, over a long term horizon.

III. Empirical Findings

This section reports the results of five different terrorist attacks on the Singapore

Stock Exchange. Using a variety of tests, we assess whether the returns and

systematic risk of 18 Singapore based industries were affected by these five events.

We confirm that there is a strong negative impact on returns for most of the industries,

and no change to the systematic risk in any of the sectors during the US attack.

Interestingly, we do not find similar significant evidence for the subsequent attacks.

Surprisingly, some of the subsequent attacks after September 11 recorded positive

long term effects in a number of the sectors. However, such an upside has been

outweighed by the occurrence of a greater number of negative effects, although

neither of the impacts claimed particularly staggering statistics.

United States- September 11

Table 3 and Table 4 summarise the parametric empirical results for September 11 for

the different sectors. Following Ramiah et al. (2007, 2007a, 2007b), we report the

abnormal return on the official trading day preceding the occurrence of each event,

the five day cumulative abnormal return, as well as their respective t-statistics for the

18 different industries. It should be noted that the Singaporean market was similar to

the Australian market, as both opened the day after the attack. In other words, we are

assessing the performance of the Singaporean stock market on the 12th of

September, 2001. The results reported in Table 3 and Table 4 show a relatively

12

consistent negative effect on equities listed in the Singaporean Stock Exchange

following the September 11 attack. Figure 1 supports this hypothesis, where all the

industries illustrate both a negative abnormal return and a negative five day

cumulative abnormal return, except for the Materials, Energy, Retail, Consumer

Durables and Apparels, Automobiles and ‘Others’ sectors. None of the sectors

obtained a statistically significant positive effect immediately after, or five days

preceding the occurrence of September 11.

Columns 2 and 3 of Table 3 report the abnormal returns and the parametric t-statistics

for the various sectors. Table 3 shows that the returns in the Transportation sector fell

by 7.85% after the September 11 attack, and the t-statistic shows that this value is

significantly statistically different from zero. In twelve out of the eighteen sectors were

notably affected by the event. The sector that was affected the most was the Software

and Services sector, which fell by a staggering 8.67%. Such a significant fall is not

unusual, given that Ramiah et al. (2007) reported a 39% fall in the returns of the

Utilities industry within the Australian equity market, after the September 11 attack in

the US. While the Australian industry classification used by Ramiah et al. (2007)

moderately differs from the GICS classification that we have used, some similarities

can be observed in the Real Estate, Capital Goods, Healthcare and Software and

Service industries. These four industries suffered considerably as a result of

September 11, in both Australia and Singapore, although the magnitude of the impact

is moderately higher in Singapore. We do not observe positive returns in any of the

sectors in Singapore. This result is consistent with Ramiah et al. (2007), which

showed only negative returns for all the sectors in the Australian equity market. A

direct comparison to the study of Ramiah et al. (2007) however, is not totally

appropriate because they have excluded firms with firm specific information

13

surrounding the events, which may account for the unexpected results in the returns

on the sectors. Conversely, we have not adopted this exclusion approach, due to the

existing limitations on the research data.

Although Cam (2006) US industry classification differs from that used by Ramiah et al.

(2007), and the GICS classification, the striking similarity of all three analyses is

epitomised within the Real Estate industry, which showed evidence of a statistical fall

in the United States, Australian and Singaporean equity markets. Thus, our findings

are consistent with both Cam (2006) and Ramiah et al. (2007) in this particular aspect.

Chen and Siems (2004) assess the short term effect of September 11 on the global

capital market. Using a major market index, they showed that the Singaporean equity

market fell by 4.96%. Using an international capital asset pricing model, Richman,

Santos, Barkoulas, (2005) reported a negative impact of about 5.78% on the Straits

Times Index. Our findings are thus consistent with Chen and Siems (2004) and

Richman et al. (2005), as we show a clear and consistent fall in the Singaporean

equity market of 5.38%. Figure 1 shows the ranking of the abnormal returns. From

Figure 1, we can observe that the Materials, Energy, Retail, Consumer Durables and

Apparels, Automobiles and ‘Others’ sectors, are the least adversely affected by the

September 11 terrorist attack.

However, the Materials, Retail and ‘Others’ sectors all exhibit a negative cumulative

abnormal return over the following five days. Note that our approach is consistent with

most studies, as this methodology supports the hypothesis of negative sentiment after

the September 11 attack. The second column of Table 4 shows that the Media sector

was the worst performing sector with an astounding -29.5% reported as the CAR over

14

the next five days (see Figure 1), supported by the t-statistic which implied that this is

very much statistically different from zero. All the other sectors within the Singapore

equity market also recorded statistically significant decline within the range of 11% to

30%, with exception of the Energy, Consumer Durables and Apparels, and

Automobiles sectors. Note that except for the Materials, Retail and the ‘Others’ sector,

all these other sectors also exhibited a statistically significant negative abnormal

return on the day following the attack which persisted into the following 5 days. It is

apparent from Figure 1 that the CAR5 is marginally higher than the event day AR for

most industries, implying that the market continued to plummet over the following five

days. Our findings are consistent with Chen and Siems (2004), who showed a

cumulative abnormal return of around -12.07%, six days after the event, and -16.00%

eleven days after the attack. However, this result is inconsistent with Cam (2006),

who found that the CAR over the following six days is lower than the abnormal return

for US firms.

As a robustness test, we consider the results of applying non-parametric tests, which

are reported in Table 5. The negative impact of the events of September 11 on

Singaporean based industries was also detected by the non-parametric tests. The

results in Table 5 show that except for the Energy, Automobiles and ‘Others’ sector,

all the other sectors have a significantly negative non-parametric t-statistic. For

instance, column 2 of Table 5 shows that the non-parametric t-statistic is -3.48902 for

the Diversified Financials sector. This reflects the negative abnormal returns identified

earlier in the parametric tests. Therefore, it is prudent to conclude that the general

results of the non-parametric tests support the results observed in the parametric

analysis.

15

Based on the above discussion, we can conclude that all the sectors except for the

Materials, Energy, Retail, Consumer Durables and Apparels, Automobiles and the

‘Others’ sectors were strongly negatively affected on the day following the September

11 attack. It is generally assumed that following a terrorist attack, returns of equities

fall as a result of an increase in systematic risk.

Our next objective will be to test if the industries negatively affected by the events of

September 11 experienced a general increase in their systematic risk. The

multiplicative regression analysis (see Equation 12) attempts to test this hypothesis.

Columns 2 to 4 of Table 6(a) report the results of the multiplicative dummy variable

model (equation 12). A positive (negative) coefficient of the multiplicative dummy

variable ( 2

Iβ ) reflects an increase (decrease) in systematic risk. The sign of the

coefficient ( 2

Iβ ) did not appear to be significantly positive or negative in any of the

industries identified, to be deemed as having been strongly affected on the day

following the September 11 attack. When the coefficient of the multiplicative dummy

variable is statistically different from zero, it implies a significant statistical change in

the systematic risk of the industry. The t-statistics results from column 4 of Table 6(a)

show that systematic risk had not statistically reduced or increased in any of the

sectors following the September 11 attack. A Wald test was conducted to test the

hypothesis that the dummy variable was a redundant variable. The results show that

the dummy variable is not a redundant variable for this sector. While the results of

this test are not reported, they are available from the author upon request

On the other hand, there is no statistical evidence of a change in systematic risk in the

twelve industries which were identified to have been strongly negatively affected on

the day following the September 11 attack. As such this indicates that terrorist attacks

16

do not necessarily lead to an increase in systematic risk, and that the risk of terrorist

attacks varies significantly across industries. However, this finding is not entirely

substantiated as none of the sectors was identified with this outcome. Therefore, this

result is not consistent with that obtained by Richman et al. (2005), who showed that

the Singaporean equity market experienced a general increase of -5.78% in the level

of short term systematic risk, on the first trading day (i.e. September 12).

Equation (13) shows the impact of September 11 on the intercept of the CAPM.

Columns 5 to 7 of Table 6(a) present the findings of the regression. As from Column

7, we can observe that the intercept had not been statistically significant in any of the

sectors.

Our final objective will be to test if the industries negatively affected by September 11

events experienced a general increase in their systematic risk in the long term. The

multiplicative regression analysis (see Equation 14) attempts to test this hypothesis.

Columns 1 to 4 of Table 7(a) report the results of the multiplicative dummy variable

model (equation 14). A positive (negative) coefficient of the multiplicative dummy

variable ( 2

Iδ ), which is the coefficient of the dummy variable SD, reflects an increase

(decrease) in systematic risk in the long term. The sign of the coefficient ( 2

Iδ )

appeared to be significantly positive in the Capital Goods, Energy, Media and

Transportation sectors. When the coefficient of the multiplicative dummy variable is

statistically different from zero, it implies a significant statistical change in the long

term systematic risk of the industry. Furthermore, a positive (negative) coefficient of

the multiplicative dummy variable ( 3

Iδ ), which the other coefficient of the dummy

variable SD, reflects an increase (decrease) in the intercept ( Iϕ ) of the regression

equation (E( Iϕ ) = 0), after the occurrence of the event. The t-statistics results from

17

column 4 of Table 7(a) show that this is not statistically significant in any of the sectors

following the September 11 attack. Therefore, there is no statistical evidence of a

change in the intercept ( Iϕ ) of the of the regression equation (E( Iϕ ) = 0), in any of the

twelve industries which were identified to have been strongly negatively affected on

the day following the September 11 events.

Bali

Among all the terrorist attacks studied in this paper, the Bali bombing is

geographically the closest to Singapore. The event occurred on Saturday, 12th of

October 2002, and the first day that the Singaporean market traded after the attack,

was on Monday, 14th of October, 2002. The results of the parametric test on sector

returns for this day are shown in Table 3 (Columns 4 and 5). Only the Automobiles

sector was significantly negatively affected on the first day that the market traded. The

robustness test also support the claim of a negative effect in the Automobiles sector

on the first day of trading. The third column of Table 5 shows the results on the

non-parametric test on the various Singapore industries. The non-parametric t-

statistic is negative and significant for the Automobiles industry. However,

interestingly, over the 5 day trading period, there was significant positive cumulative

returns recorded for the Banks and Insurance sector, as well as the Technology,

Hardware and Equipments sector of the market (see Table 4) for Bali bombing. These

positive effects appear to have occurred only after the first trading day following the

attack. This is because the negative effects which were present for these two sectors

on the first trading day disappeared after five days, where the CAR5 for the two

sectors became a significantly positive value. Interestingly, almost all of the sectors

appeared to have recovered over the 5 day period, generally recording positive values

18

for the CAR5, albeit not statistically significant. Therefore, although it is statistically

conclusive that only one of the sector, Automobiles was negatively affected

immediately after the Bali attack, the downturn was not enduring thereafter, as the

CAR5 reflected somewhat an improvement. From the results, it would deem apparent

that although the Banks and Insurance sector, as well as the Technology, Hardware

and Equipments sector had not reacted positively to the aftermath of the event, the

recovery was robustly evidenced over the 5 day trading period, where and a

statistically significant positive CAR5 was recorded. Unlike the five day CAR analysis,

the regression analysis shows no significant results. A Wald test was conducted to

test the hypothesis that the dummy variable was a redundant variable. The results

show that the dummy variable is not a redundant variable for this sector. While the

results of this test are not reported, they are available from the author upon request.

Based on the empirical results, we can further conclude that the Bali bombings did

have both a negative and positive effect on the Singaporean market, in both the short

run and long term. We may interpret the positive result as a substitution effect of

terrorist attacks. Our hypothesis is that investors move their investments from

countries directly under attack to the neighbouring country, in search of an investment

paradise. Unfortunately, our findings do not show a substantial evidence of

substitution effect, as only Banks and Insurance sector, and the Technology,

Hardware and Equipments sector noted statistically significant recovery over the 5

day period, both recording positive values for the CAR5.

It is generally assumed that following a terrorist attack, returns of equities fall as a

result of an increase in systematic risk. Our next objective will be to test if the

industries negatively affected by the Bali Bombings experienced a general increase in

19

their systematic risk. The multiplicative regression analysis (see Equation 12)

attempts to test this hypothesis. Columns 2 to 4 of Table 6(b) report the results of the

multiplicative dummy variable model (equation 12). A positive (negative) coefficient of

the multiplicative dummy variable ( 2

Iβ ) reflects an increase (decrease) in systematic

risk. The sign of the coefficient ( 2

Iβ ) did not appear to be significantly positive or

negative in any of the industries identified, to be deemed as having been strongly

affected on the day following the attacks in Bali. When the coefficient of the

multiplicative dummy variable is statistically different from zero, it implies a significant

statistical change in the systematic risk of the industry. The t-statistics results from

column 4 of Table 6(b) show that systematic risk had statistically reduced in the

Consumer Services and Technology, Hardware and Equipment sectors following the

Bali Bombings. A Wald test was conducted to test the hypothesis that the dummy

variable was a redundant variable. The results show that the dummy variable is not

a redundant variable for this sector. While the results of this test are not reported,

they are available from the author upon request. On the other hand, there is no

statistical evidence of a change in systematic risk in the Automobile sector, which was

identified to have been strongly negatively affected on the day following the Bali

Bombings. Therefore, it is difficult to conclude that terrorist attacks lead to a reduction

in systematic risk, and that the level of terrorist risk varies significantly across

industries.

On the other hand, equation (13) shows the impact of the Bali Bombings on the

intercept of the CAPM. Columns 5 to 7 of Table 6(b) present the findings of the

regression. As from Column 7, we can observe that the intercept had been statistically

significant in the Consumer Services and Technology, Hardware and Equipment

sectors.

20

Our final objective is to analyse if the industries negatively affected by the Bali

Bombings experienced a general increase in their systematic risk in the long term.

The multiplicative regression analysis (see Equation 14) attempts to test this

hypothesis. Columns 1 to 4 of Table 7(b) report the results of the multiplicative dummy

variable model (equation 14). A positive (negative) coefficient of the multiplicative

dummy variable ( 2

Iδ ), which is the coefficient of the dummy variable SD, reflects an

increase (decrease) in systematic risk in the long term. The sign of the coefficient

( 2

Iδ ) appeared to be significantly positive in only the Media sector. When the

coefficient of the multiplicative dummy variable is statistically different from zero, it

implies a significant statistical change in the long term systematic risk of the industry.

Furthermore, a positive (negative) coefficient of the multiplicative dummy variable

( 3

Iδ ), which the other coefficient of the dummy variable SD, reflects an increase

(decrease) in the intercept ( Iϕ ) of the regression equation (E( Iϕ ) = 0), after the

occurrence of the event. The t-statistics results from column 4 of Table 7(a) show that

this is only statistically significant in the Transportation sector following the Bali

Bombings. Therefore, there is only statistical evidence of a change in the intercept

( Iϕ ) of the of the regression equation (E( Iϕ ) = 0), in the Transportation sector, which

had not been identified to have been strongly negatively affected on the day following

the Bali Bombings.

Madrid

The bombings in Madrid occurred on Thursday, 11th of March 2004. We examine the

Singapore industry reactions both immediately, and five days following the event. The

results of the parametric test immediately after the attacks and five day after the

attacks are shown in columns 6 and 7 of Table 3 and Table 4 respectively. Based on

21

these two parametric tests, none of the sectors were significantly negatively affected.

The non-parametric test also failed to detect a statistical significant impact on the

event day on any of the sectors. Therefore, it is conclusive that all of the sectors were

immunized from the Madrid bombings. Of the five terrorist attacks analysed, Madrid

suffered the second highest injury and fatality rate. In spite of this, the results suggest

that this event had no negative impact on any of the sectors within the Singaporean

equity market.

As such, the Madrid evidence suggests that it is wrong to assume that terrorist attacks

will impact negatively on stock markets, implying that investment havens do exist

even under terrorist attacks.

It is generally assumed that following a terrorist attack, returns of equities fall as a

result of an increase in systematic risk. Our next objective will be to test if the

industries negatively affected by the Madrid Bombings experienced a general

increase in their systematic risk. The multiplicative regression analysis (see Equation

12) attempts to test this hypothesis. Columns 2 to 4 of Table 6(c) report the results of

the multiplicative dummy variable model (equation 12). The sign of the coefficient

( 2

Iβ ) did not appear to be significantly positive or negative in any of the industries

identified, to be deemed as having been strongly affected on the day following the

attacks in Madrid. When the coefficient of the multiplicative dummy variable is

statistically different from zero, it implies a significant statistical change in the

systematic risk of the industry. The t-statistics results from column 4 of Table 6(c)

show that systematic risk had statistically reduced in the Food and Beverages, Energy

and Media sectors following the Madrid Bombings. A Wald test was conducted to test

the hypothesis that the dummy variable was a redundant variable. The results show

22

that the dummy variable is not a redundant variable for this sector. While the results

of this test are not reported, they are available from the author upon request. On the

other hand, since none of the sectors had been identified to have been strongly

negatively affected on the day following the Madrid Bombings, there is therefore no

statistical evidence of a change in systematic risk.

On the other hand, the results of estimating equation (13) shows the impact of the

Madrid Bombings on the intercept of the CAPM. Once more we focus the industries

stated in the previous paragraph. Columns 5 to 7 of Table 6(c) present the findings of

the regression. As from Column 7, we can observe that the intercept had been

statistically significant in the Food and Beverages and Energy sectors.

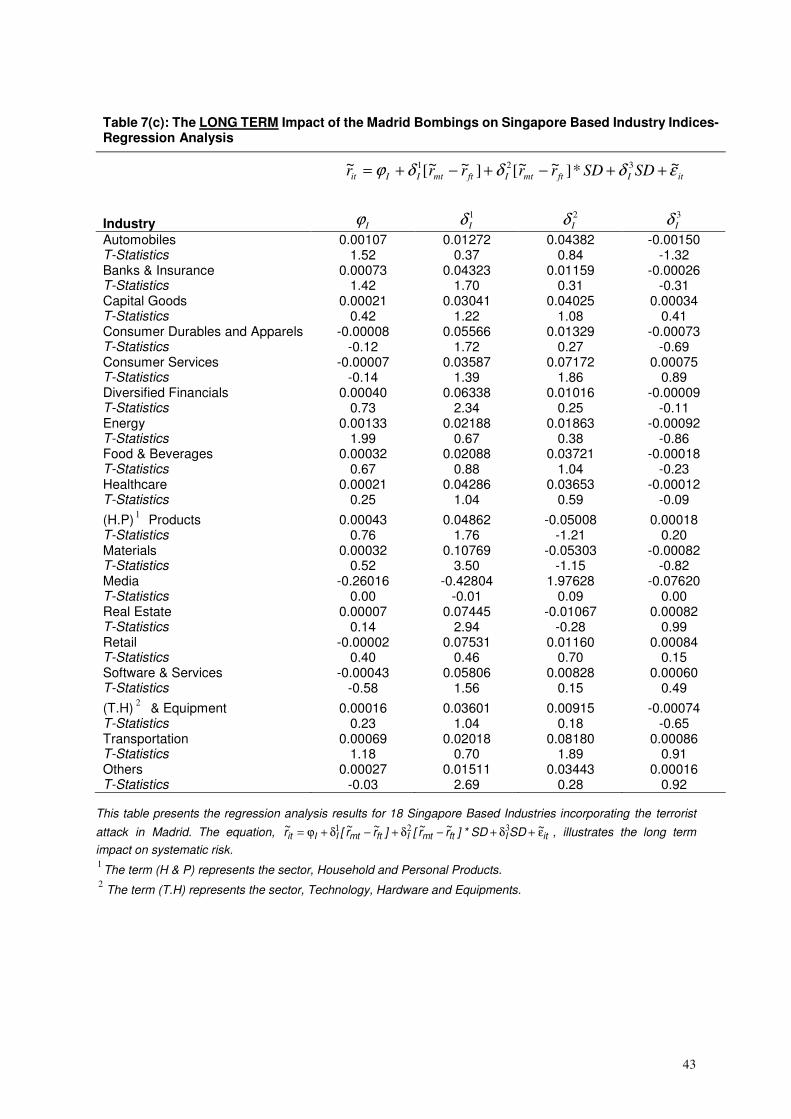

Our final objective is to analyse if the industries negatively affected by the Madrid

Bombings experienced a general increase in their systematic risk in the long term.

The multiplicative regression analysis (see Equation 14) attempts to test this

hypothesis. Columns 1 to 4 of Table 7(c) report the results of the multiplicative dummy

variable model (equation 14). The sign of the coefficient ( 2

Iδ ) is not significantly

positive in any of the sectors. The t-statistics results from column 4 of Table 7(c) again

show that this is not statistically significant in any of the sectors following the Madrid

Bombings. Therefore, there is no statistical evidence of a change in the intercept ( Iϕ )

of the of the regression equation (E( Iϕ ) = 0), in any of the sectors, and this is

consistent with earlier findings of an immunised effect arising from the Madrid

Bombings.

23

London

On Thursday, 7th of July 2005, London came under the wrath of terrorists. Intuitively,

because of Singapore’s close ties with the western world, one may envisage that a

substantial impact on the Singaporean equity market will materialise. True to this

belief, the Singaporean equity market’s response to the attack was noteworthy. The

trading day immediately after the attack saw both the Healthcare sector and the Food

and Beverage sector produce abnormal returns of -3.10% and -1.63% respectively

(see Table 3, Column 8). The non-parametric t-statistic however only supports the

statistically significant negative movement in the Healthcare sector, with an absence

of a similar support for the Food and Beverage sector. Instead, the non-parametric

t-statistic revealed that the Banks and Insurance sector experienced a significant

negative impact. However, the Household and Personal Products sector and ‘Others’

sector showed unusual positive cumulative abnormal returns of 4.83% and 4.93%

respectively over five days. Therefore, considering the London terrorist attack to be a

considerably major global event, it has affected more than one industry in the

Singaporean equity market on the day of the impact, and subsequently, more

industries in the days preceding the impact, although there is little consistency in the

extent the impact, and the sectors involved. Conclusively, it would deem that the

Healthcare and Food and Beverages sectors were negatively affect on the day of the

impact, but managed to gain recover thereafter in the following 5 days. In contrast, the

Household and Personal Products sector and ‘Others’ sectors also affirmed much

recovery after 5 days following the event, as significantly positive returns were noted

in these sectors.

Out of the five attacks studied in this analysis, a range of sectors have been

significantly affected by three of these events. Some of the sectors displayed

24

recurrent impacts in each of the events; one apparent sector being the Healthcare

sector which manifested negative impact in both the September 11 and the London

Bombings. In addition, there exist other sectors pertaining to each event which also

exhibited statistically significant returns, although the impact was not repeated in

subsequent attacks. These findings therefore conclusively demonstrate the

prevalence of extreme sensitivity around terrorist attacks.

It is generally assumed that following a terrorist attack, returns of equities fall as a

result of an increase in systematic risk. Our next objective will be to test if the

industries negatively affected by the London Bombings experienced a general

increase in their systematic risk. The multiplicative regression analysis (see Equation

12) attempts to test this hypothesis. Columns 2 to 4 of Table 6(d) report the results of

the multiplicative dummy variable model (equation 12). The sign of the coefficient

( 2

Iβ ) did not appear to be significantly positive or negative in any of the industries

identified, to be deemed as having been strongly affected on the day following the

attacks in London. The t-statistics results from column 4 of Table 6(d) show that

systematic risk had not statistically reduced or increased in any of the sectors

following the London Bombings. A Wald test was conducted to test the hypothesis

that the dummy variable was a redundant variable. The results show that the

dummy variable is not a redundant variable for this sector. While the results of this

test are not reported, they are available from the author upon request. On the other

hand, there is no statistical evidence of a change in systematic risk in the Healthcare,

and the Food and Beverage sectors, which were identified to have been strongly

negatively affected on the day following the September 11 attack. These results

suggest that major terrorist attacks do not necessary lead to an increase in systematic

risk, and that the level of terrorist risk varies significantly across industries.

25

The results obtained from estimating equation (13) shows the impact of the London

Bombings on the intercept of the CAPM. Columns 5 to 7 of Table 6(d) present the

findings of the regression. As can be seen from Column 7, the intercept was not

statistically significant in any of the sectors.

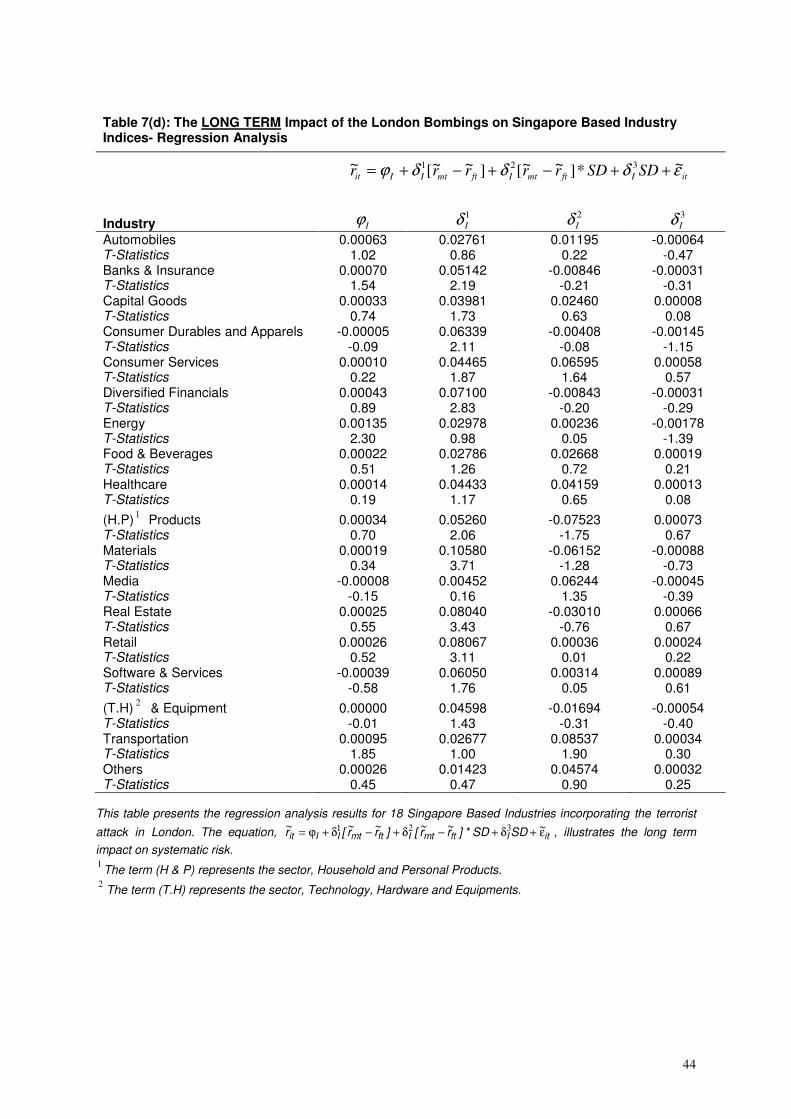

Our final objective is to analyse if the industries negatively affected by the London

Bombings experienced a general increase in their systematic risk in the long term.

The multiplicative regression analysis (see Equation 14) attempts to test this

hypothesis. Columns 1 to 4 of Table 7(d) report the results of the multiplicative dummy

variable model (equation 14). The sign of the coefficient ( 2

Iδ ) appeared to be

significantly positive in none of the sectors. The t-statistics results from column 4 of

Table 7(d) again show that this is not statistically significant in any of the sectors

following the London Bombings. Therefore, there is no statistical evidence of a

change in the intercept ( Iϕ ) of the of the regression equation (E( Iϕ ) = 0), in any of the

sectors, which following the London Bombings.

Mumbai

Although Mumbai’s terrorist attacks claimed 207 lives and injured 714 people, the

response on the Singaporean equity market was marginal. The impact of this attack

resulted in an abnormal performance for only the Media sector. The negative

abnormal return following the event was statistically significant. The effect was further

magnified 5 days after the occurrence of the event where the CAR5 had plunged by a

greater extend. The non-parametric t-statistic however does not support the

statistically significant negative movement.

26

It is generally assumed that following a terrorist attack, returns of equities fall as a

result of an increase in systematic risk. Our next objective will be to test if the

industries negatively affected by the Mumbai Bombings experienced a general

increase in their systematic risk. The multiplicative regression analysis (see Equation

12) attempts to test this hypothesis. Columns 2 to 4 of Table 6(e) report the results of

the multiplicative dummy variable model (equation 12). The sign of the coefficient

( 2

Iβ ) did not appear to be significantly positive or negative in any of the industries

identified, to be deemed as having been strongly affected on the day following the

attacks in Mumbai. The t-statistics results from column 4 of Table 6(e) show that

systematic risk had not statistically reduced or increased in any of the sectors

following the Mumbai Bombings. A Wald test was conducted to test the hypothesis

that the dummy variable was a redundant variable. The results show that the dummy

variable is not a redundant variable for this sector. While the results of this test are not

reported, they are available from the author upon request. On the other hand, there is

no statistical evidence of a change in systematic risk in the Media sector, which was

the only sector which was identified to have been strongly negatively affected on the

day following the September 11 attack.

Furthermore, the results of estimating equation (13) shows the impact of the Mumbai

Bombings on the intercept of the CAPM. Columns 5 to 7 of Table 6(e) present the

findings of the regression. As from Column 7, we can observe that the intercept had

not been statistically significant in any of the sectors.

Our final objective is to analyse if the industries negatively affected by the Mumbai

Bombings experienced a general increase in their systematic risk in the long term.

The multiplicative regression analysis (see Equation 14) attempts to test this

27

hypothesis. Columns 1 to 4 of Table 7(e) report the results of the multiplicative dummy

variable model (equation 14). The sign of the coefficient ( 2

Iδ ) appeared to be

significantly negative in the Household and Personal Products and Materials sectors.

The t-statistics results from column 4 of Table 7(e), again, show that this is not

statistically significant in any of the sectors, following the Mumbai Bombings.

Therefore, there is no statistical evidence of a change in the intercept ( Iϕ ) of the of

the regression equation (E( Iϕ ) = 0), in any of the sectors, following the Mumbai

Bombings.

IV. Conclusion

Studying the impact of the recent terrorist attacks on the Singaporean industries, we

are able to identify the various market effects. The events of September 11 had the

greatest effect on the Singaporean equity market. The majority of the industries were

down on the day of the event, and just over 60% of the industries remained negatively

affected 5 days after the event. None of the sectors showed a statistically significant

change in the level of systematic risk following the September 11 attacks. The London

bombings were next, revealing a negative impact on the Singaporean equity market,

and a positive effect five days after the event. Interestingly, the results obtained from

the Bali attacks were generally positive for Singapore. However, with only two sectors

demonstrating statistically significant effects 5 days after the event, there seems to be

only weak evidence for the occurrence of the substitution effect. Nevertheless, the

Bali Bombings show that terrorist attacks do not always nurture negative sentiment.

This poses advantages for the neighbouring country out of a substitution effect.

Another interesting finding was that the Madrid bombings had no major impact on the

Singaporean equity market. The evidence from the Madrid bombings suggest that

some capital markets may be insulated from certain terrorist attacks, and thus

28

investment havens may exist under such circumstances, even immediately after an

attack. Finally, it appears that more than one industry is sensitive to the terrorist

attacks. However, Singapore has not been radically affected by terrorist attacks post

September 11, indicating that investment havens do exist after those events.

Acknowledgements

We would like to acknowledge the invaluable research assistance of Liew Khar Wai,

Choo Wen Hoe, Wee Kuan Jin, Poh Chia Huei, Amrish Buroty, Neha Sandher and

Alias Adil in gathering the data and completing some of the empirical analysis. We

would also like to thank George tawadros, Mugwagwa Tafadzwa and Ashwin Madhou

for their ongoing assistance that contributed to the successful completion of this

paper. Any remaining errors, however, are our own.

29

References

Brown, S. J., and Warner, J.B., (1985), ‘Using daily stock returns: The case of event studies’,

Journal of Financial Economics, vol. 14, no. 1, 3-31.

Cam, M., (2006), ‘The impact of terrorism on United States Industry indexes’, School of

Economics, Finance and Marketing, Royal Melbourne Institute of Technology,

Melbourne.

Chen, A. H., and Siems, T. F., (2004), ‘The effects of terrorism on global capital markets’,

European Journal of Political Economy, vol. 20, 349-366.

Corrado, C. J., (1989), ‘A non parametric test for abnormal security price performance in

event studies’, Journal of Financial Economics, vol. 23, 385-395.

Hoa, T. V., (2004), ‘Economic and Financial Crisis Management in Asia: A Critical Analysis’,

University of Wollongong Economics Working Paper Series 2004.

Hon, M. T., , S. K., (2004), ‘Contagion in Financial Markets After September 11: Myth or

Reality?’, The Journal of Financial Research, vol. 27, no. 1, 95-114.

Ramiah, C., Maher, D., Ghafouri S., and Cam M. (2007). The Short Term Impact of the

Recent Terrorist Attacks on the Australian Equity Market. Economics, Finance and

Marketing. Melbourne, RMIT.

Ramiah, V., Naughton T., Hallahan T. and Anderson J. A. (2007a). ‘An Empirical

Investigation of the Short Term and Long Term Impact of the Recent International

Terrorist Attacks on the Japanese Equity Market.’, School of Economics, Finance and

Marketing, Royal Melbourne Institute if Technology, Melbourne.

Ramiah, V., Naughton T., Hallahan T. and Anderson J. A. (2007b). ‘An Empirical

Investigation of the Short Term and Long Term Impact of the Recent International

30

Terrorist Attacks on the Malaysian Equity Market.’, School of Economics, Finance and

Marketing, Royal Melbourne Institute if Technology, Melbourne.

Richman, V., Santos, M. R., and Barkoulas, J. T., (2005), ‘Short- and Long-Term effects of

the September 11 Event: The International Evidence’, International Journal of

Theoretical and Applied Finance, vol. 8, no. 7, 947-958.

Singh, D., (2002), ‘The Post-September 11 Geostrategic Landscape and Southeast Asian

Response to the Threat of Terrorism’, Institute of Southeast Asian Studies,

Singapore.

Tan, S. L., (2003), ‘The Threat of Terrorism and Singapore’s Legislative Response to

Terrorism Financing’, Journal of Money Laundering Control, vol. 7, no. 2, 139-144.

31

Table 1: Descriptive Statistics of daily Returns, for sectors in Singapore from August 1999 to February 2007.

MEAN STD DEV SKEWNESS KURTOSIS RANGE COUNT T-TEST STATS JB-STATS

Materials 0.044% 0.0358 -0.06 15.29 1.27 37 0.0123 360.58

Diversified Financials 0.039% 0.0288 0.14 45.67 9.19 28 0.0134 2433.49

Energy 0.144% 0.0337 -3.90 138.33 1.73 8 0.0427 6399.08

Real Estate 0.127% 0.0277 -0.20 36.91 3.77 48 0.0458 2725.31

Capital Goods -0.012% 0.0453 0.10 23.03 3.42 137 -0.0027 3027.18

Healthcare -0.005% 0.0330 0.55 9.27 1.58 15 -0.0016 54.44

Banks and Insurance 0.050% 0.0174 1.34 71.95 0.75 6 0.0286 1296.18

Retail 0.051% 0.0399 -0.28 33.46 1.63 26 0.0128 1213.16

Consumer Durables and Apparels -0.074% 0.0352 0.34 13.45 0.67 7 -0.0211 52.92

Automobiles 0.018% 0.0380 0.59 8.16 1.05 7 0.0047 19.81

Food and Beverages 0.053% 0.0364 0.42 13.75 1.71 52 0.0146 411.49

Transportation 0.056% 0.0293 0.23 11.72 1.36 26 0.0192 148.96

Media -0.020% 0.0396 0.26 9.38 1.15 9 -0.0051 33.10

Software and Services -0.001% 0.0503 -0.31 27.48 2.96 60 -0.0003 1888.58

Consumer Services 0.033% 0.0304 0.38 26.83 1.38 27 0.0109 810.59

Household and Personal Products 0.011% 0.0424 -0.34 30.14 1.68 45 0.0026 1704.10

Technology, Hardware and Equipment -0.047% 0.0435 -0.12 21.15 3.95 120 -0.0109 2235.84

Others1 0.024% 0.0305 1.78 46.36 1.46 15 0.0078 1351.19

The Market 0.051% 0.1174 0.06 79.88 9.19 673 0.0043 178924.33

1This category is comprised of the Pharmaceuticals, Utilities, Defence, and Telecommunications sectors.

32

Table 2: The Five Major Terrorist Attacks and Their Consequences.

Terrorist Attack Date Event Injuries Fatalities Official Trading (on

SGX) date after event

September 11, US 11/09/2001 Four commercial aircraft were hijacked. Two were deliberately crashed into the World Trade Centre, and another into the Pentagon. Passengers forced the crash of the other plane into Pennsylvania.

5,000 3,025 12/09/2001

Bali, Indonesia 12/10/2002 A car bomb exploded outside the crowded Sari Club and inside Padi’s Bar.

300 202 14/10/2002

Madrid, Spain 11/03/2004 Planted bombs detonated on commuter trains 1,800 191 11/03/2004

London, UK 7/07/2005 Suicide bombing of the London subway and bus system. 700 55 7/07/2005

Mumbai, India 11/07/2006 Explosive devices tore through several commuter trains. 714 207 12/07/2006

Source: Adapted From Ramiah et al. (2007).

33

Table 3: Abnormal Returns on Singapore Based Industry Indices Following Five Terrorist Attacks

September 11 Bali Madrid London Mumbai Industry

AR T-stats AR T-stats AR T-stats AR T-stats AR T-stats

Materials -0.03681 -1.94974 -0.01704 -1.21665 -0.00999 -0.77420 0.00187 0.22597 -0.00661 -0.58761

Diversified Financials -0.05331 -4.22608 -0.00115 -0.04937 -0.00883 -0.96650 0.00101 0.18629 -0.00068 -0.06114

Energy 0.01388 0.63588 0.01856 1.66880 -0.01039 -0.36228 -0.00087 -0.06671 -0.00840 -0.40017

Real Estate -0.03608 -3.05931 -0.00059 -0.05641 -0.00535 -0.47282 -0.00912 -1.24748 -0.00392 -0.38230

Capital Goods -0.05225 -3.96532 -0.01355 -1.48241 -0.01110 -0.79011 -0.00666 -0.93811 -0.00262 -0.27704

Healthcare -0.08450 -3.28418 -0.00120 -0.06580 -0.01010 -0.52314 -0.03096 -2.11739 -0.01338 -0.79694

Banks and Insurance -0.05259 -3.89846 -0.00018 -0.01643 -0.00492 -0.55556 -0.00924 -1.91051 -0.00246 -0.40217

Retail -0.02458 -1.94175 0.00444 0.39137 -0.01598 -1.49491 -0.00089 -0.10980 -0.00733 -0.68278

Consumer Durables and Apparels -0.04005 -1.84638 0.00697 0.44463 -0.00522 -0.42470 -0.00532 -0.44796 -0.01641 -0.92566

Automobiles 0.03443 1.57590 -0.05904 -2.15739 -0.03292 -1.27384 -0.00161 -0.09270 0.00910 0.41399

Food and Beverages -0.04598 -3.74802 0.00473 0.36926 -0.00541 -0.47862 -0.01631 -2.22531 -0.00205 -0.20314

Transportation -0.07850 -4.71659 -0.00560 -0.42688 -0.00654 -0.42155 0.00033 0.03885 0.01752 1.74297

Media -0.06682 -2.07278 0.00165 0.06946 0.00589 0.25039 -0.02847 -1.56176 -0.03706 -2.25961

Software and Services -0.08668 -5.17002 -0.00634 -0.36569 -0.00540 -0.27391 -0.01036 -1.02742 -0.00547 -0.43659

Consumer Services -0.03220 -2.56568 -0.00864 -0.76896 0.00462 0.39004 0.00888 1.05448 0.00479 0.51273

Household and Personal Products -0.05821 -3.37879 0.00862 0.61288 -0.00844 -0.57934 0.00070 0.05521 0.01152 0.83304

Technology, Hardware and Equipments

-0.07307 -3.96472 -0.00340 -0.19290 -0.01724 -0.95855 0.00464 0.49113 0.00517 0.48358

Others 1 -0.02318 -1.05926 -0.01448 -0.90689 0.00063 0.04439 -0.00237 -0.27495 -0.00071 -0.06422

This table presents abnormal returns and the parametric t-test results for 18 Singapore Based Industries after September 11, Bali, Madrid, London and Mumbai terrorist attacks 1 This category is comprised of the Pharmaceuticals, Utilities, Defence, and Telecommunications sectors.

34

Table 4: Cumulative Abnormal Returns on Singapore based Industry Indices Following Five Terrorist Attacks

September 11 Bali Madrid London Mumbai Industry

CAR5 T-stats CAR5 T-stats CAR5 T-stats CAR5 T-stats CAR5 T-stats

Materials -0.19970 -4.56914 0.02926 0.95281 -0.01273 -0.38489 0.01442 0.76612 -0.03748 -1.28408

Diversified Financials -0.18753 -5.43974 0.05468 1.00306 -0.03304 -1.48661 0.00429 0.42199 -0.04160 -1.89894

Energy -0.04057 -1.06937 0.05996 1.96380 0.06848 1.27111 0.03553 1.14945 -0.08811 -1.81030

Real Estate -0.11553 -3.80963 0.03910 1.62400 -0.01452 -0.48748 0.00201 0.13552 -0.03307 -1.22154

Capital Goods -0.20900 -5.67506 0.03572 1.43761 -0.01173 -0.30636 0.01852 1.07568 -0.04505 -1.87513

Healthcare -0.14890 -2.66696 0.04233 1.03083 -0.01566 -0.40563 0.04782 1.78915 -0.03922 -1.21624

Banks and Insurance -0.16593 -5.21018 0.05702 2.12593 -0.02116 -1.05271 0.00199 0.20715 -0.02382 -1.81194

Retail -0.14567 -4.56166 0.00069 0.02533 -0.02043 -0.72206 0.00888 0.55912 -0.02619 -1.17877

Consumer Durables and Apparels -0.09285 -1.92378 0.04232 1.22365 -0.01232 -0.50726 -0.02693 -1.19377 0.00167 0.04884

Automobiles -0.05066 -1.18793 -0.03485 -0.64075 -0.00664 -0.11188 0.04738 1.55731 -0.00565 -0.14284

Food and Beverages -0.16427 -5.19105 0.05629 1.91713 -0.00988 -0.35158 -0.00903 -0.67546 -0.03864 -1.79557

Transportation -0.20983 -5.51371 0.03606 1.15581 -0.00500 -0.12004 0.01040 0.56569 -0.02850 -1.17566

Media -0.29532 -3.97649 0.04196 0.88743 0.02007 0.43453 -0.02456 -0.86283 -0.10699 -3.10033

Software and Services -0.24668 -5.90360 0.07528 1.88274 0.00031 0.00633 0.00292 0.13107 -0.02590 -0.98494

Consumer Services -0.17676 -5.52968 0.02662 0.96575 0.00786 0.26637 -0.00193 -0.12415 -0.01276 -0.67704

Household and Personal Products -0.14797 -3.73544 0.03103 0.92024 -0.00413 -0.11662 0.04825 2.37551 -0.00411 -0.16671

Technology, Hardware and Equipments -0.27113 -5.38620 0.10512 2.21834 -0.01330 -0.28677 0.03219 1.31396 -0.03430 -1.20461

Others 1 -0.14936 -3.00760 0.03957 1.22012 -0.01299 -0.50496 0.04927 2.56357 -0.04747 -1.80204

This table presents five day cumulative abnormal returns and the parametric t-test results for 18 Singapore Based Industries after September 11, Bali, Madrid, London and Mumbai terrorist attacks 1 This category is comprised of the Pharmaceuticals, Utilities, Defence, and Telecommunications sectors.

35

Industry September 11 Bali Madrid London Mumbai

Materials -2.82882 -1.79039 -1.15519 -1.16119 -0.56059

Diversified Financials -3.48902 -0.39406 -1.54817 -0.78837 0.28511

Energy -0.41983 0.51110 -1.10190 0.26284 -0.61587

Real Estate -3.02680 -0.36181 -1.29868 -1.43775 -0.54371

Capital Goods -3.16321 -1.27246 -1.24354 -0.85178 -0.63549

Healthcare -2.47746 -0.61450 -1.71699 -2.01294 -1.46816

Banks and Insurance -2.59744 -0.27931 -1.13176 -2.02448 -0.09816

Retail -2.73689 -0.11871 -1.39821 -0.10146 -1.85337

Consumer Durables and Apparels -2.07927 0.61467 -0.89679 -0.43861 -0.65203

Automobiles 0.28541 -2.00035 -1.35813 -0.46765 -0.46629

Food and Beverages -3.36075 -0.34519 -1.42951 -0.90786 -0.77456

Transportation -3.38066 -0.37319 -0.80855 -0.76265 1.63282

Media -2.37199 -0.15372 -1.12748 -0.47646 -1.94055

Software and Services -3.04888 -0.76684 -1.19820 -1.45096 -0.95420

Consumer Services -3.26571 -1.05223 -1.09538 -0.92370 0.79061

Household and Personal Products -2.47512 0.23920 -1.68076 -0.15240 -0.55000

Technology, Hardware and Equipments -2.99985 -0.64480 -1.14041 -1.08230 -0.70051

Others 1 -1.42818 -0.70132 -0.74907 -0.67671 -0.98376

This table presents the non-parametric t-test results for 18 Singapore Based Industries after September 11, Bali, Madrid, London and Mumbai terrorist attacks.

1 This category is comprised of the Pharmaceuticals, Utilities, Defence, and Telecommunications sectors.

Table 5: The Impact of Five Terrorist Attacks on Singapore Based Industry Indices- Non-Parametric Results

36

Table 6(a): The Impact of September 11 Attack on Singapore Based Industry Indices- Regression Analysis

Industry

Automobiles -0.00071 0.00277 -0.06750 -0.00071 0.00277 0.00331 T-Statistics -0.68 0.05 -0.13 -0.68 0.05 0.13 Banks and Insurance 0.00080 0.03496 0.10433 0.00080 0.03496 -0.00512 T-Statistics 1.00 0.86 0.27 1.00 0.86 -0.27 Capital Goods -0.00078 -0.02441 -0.10363 -0.00078 -0.02441 0.00509 T-Statistics -1.06 -0.65 -0.29 -1.06 -0.65 0.29

(C.D)1 and Apparels -0.00081 0.07994 -0.40955 -0.00081 0.07994 0.02010

T-Statistics -0.76 1.47 -0.79 -0.76 1.47 0.79 Consumer Services -0.00076 0.01073 -0.03261 -0.00076 0.01073 0.00160 T-Statistics -1.01 0.28 -0.09 -1.01 0.28 0.09 Diversified Financials 0.00007 0.04387 0.04477 0.00007 0.04387 -0.00220 T-Statistics 0.07 0.88 0.09 0.07 0.88 -0.09 Energy 0.00100 0.03113 -0.54790 -0.00007 -0.06450 -0.01648 T-Statistics 1.91 1.27 -1.15 -0.07 -1.18 -0.64 Food and Beverages -0.00036 -0.01953 -0.09733 -0.00036 -0.01953 0.00478 T-Statistics -0.60 -0.63 -0.33 -0.60 -0.63 0.33 Healthcare -0.00055 -0.01926 0.40490 -0.00055 -0.01926 -0.01987 T-Statistics -0.31 -0.21 0.47 -0.31 -0.21 -0.47

(H.P)2

Products -0.00045 -0.01505 -0.25534 -0.00045 -0.01505 0.01253

T-Statistics -0.50 -0.33 -0.59 -0.50 -0.33 0.59 Materials -0.00068 0.11593 0.18935 -0.00068 0.11593 -0.00929 T-Statistics -0.70 2.34 0.40 -0.70 2.34 -0.40 Media -0.00097 -0.11943 0.29486 -0.00097 -0.11943 -0.01447 T-Statistics -0.98 -2.37 0.61 -0.98 -2.37 -0.61 Real Estate -0.00044 0.02476 -0.08396 -0.00044 0.02476 0.00412 T-Statistics -0.63 0.70 -0.25 -0.63 0.70 0.25 Retail -0.00116 0.07371 -0.56123 -0.00116 0.07371 0.02755 T-Statistics -1.38 1.73 -1.37 -1.38 1.73 1.37 Software and Services -0.00093 0.03715 0.32702 -0.00093 0.03715 -0.01605 T-Statistics -0.62 0.49 0.45 -0.62 0.49 -0.45

(T.H) 3and Equipment -0.00067 -0.01196 0.92011 -0.00067 -0.01196 -0.04516

T-Statistics -0.50 -0.18 1.43 -0.50 -0.18 -1.43 Transportation -0.00020 -0.01510 0.01293 -0.00020 -0.01510 -0.00064 T-Statistics -0.25 -0.37 0.03 -0.25 -0.37 -0.03 Others 0.00006 -0.05089 0.05199 0.00006 -0.05089 -0.00255 T-Statistics 0.05 -0.81 0.09 0.05 -0.81 -0.09

This table presents the regression analysis results for 18 Singapore Based Industries incorporating the terrorist attack in the United States. The first multiplicative dummy variable equation

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21 , illustrates the impact on systematic risk, and the second additive

dummy variable equation, ε+α+−α+ϕ=− 21 ~D]r~r~[r~r~ IftmtIIftIt , shows the impact on the intercept.

1The term (C.D) represents the sector, Consumer Durables.

2The term (H.P) represents the sector, Household and Personal Products.

3The term (T.H) represents the sector, Technology, Hardware and Equipment.

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21

itIftmtIIftIt~D]r~r~[r~r~ ε+α+−α+ϕ=− 21

1

Iβ 2

Iβ iϕ 1

Iα 2

Iαiφ

37

Table 6(b): The Impact of the Bali Bombings on Singapore Based Industry Indices- Regression Analysis

.

This table presents the regression analysis results for 18 Singapore Based Industries incorporating the terrorist attack in the United States. The first multiplicative dummy variable equation,

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21 , illustrates the impact on systematic risk, and the second additive

dummy variable equation, ε+α+−α+ϕ=− 21 ~D]r~r~[r~r~ IftmtIIftIt , shows the impact on the intercept.

1The term (C.D) represents the sector, Consumer Durables.

2The term (H. P) represents the sector, Household and Personal Products.

3The term (T.H) represents the sector, Technology, Hardware and Equipments.

Industry

Automobiles 0.00000 0.03154 -2.85004 0.00000 0.03154 0.04523 T-Statistics 0.01 0.64 -1.68 0.01 0.64 1.68 Banks & Insurance 0.00082 0.04275 -1.43561 0.00082 0.04275 0.02278 T-Statistics 1.29 1.27 -1.23 1.29 1.27 1.23 Capital Goods -0.00017 0.01348 -1.61568 -0.00017 0.01348 0.02564 T-Statistics -0.29 0.42 -1.46 -0.29 0.42 1.46

(C.D)1 and Apparels 0.00013 0.05734 0.34694 0.00013 0.05734 -0.00551

T-Statistics 0.15 1.29 0.22 0.15 1.29 -0.22 Consumer Services -0.00024 0.01444 -2.62257 -0.00024 0.01444 0.04162 T-Statistics -0.38 0.43 -2.27 -0.38 0.43 2.27 Diversified Financials 0.00023 0.05755 -1.06768 0.00023 0.05755 0.01694 T-Statistics 0.31 1.47 -0.79 0.31 1.47 0.79 Energy 0.00073 -0.01061 -1.25375 0.00073 -0.01061 0.01990 T-Statistics 0.88 -0.24 -0.82 0.88 -0.24 0.82 Food & Beverages 0.00002 -0.00034 -0.96021 0.00002 -0.00034 0.01524 T-Statistics 0.04 -0.01 -0.99 0.04 -0.01 0.99 Healthcare -0.00005 0.02858 -0.67677 -0.00005 0.02858 0.01074 T-Statistics -0.04 0.42 -0.29 -0.04 0.42 0.29

(H.P)2

Products 0.00029 0.01842 -1.07015 0.00029 0.01842 0.01698 T-Statistics 0.41 0.49 -0.83 0.41 0.49 0.83 Materials 0.00032 0.10641 0.07381 0.00032 0.10641 -0.00117 T-Statistics 0.42 2.64 0.05 0.42 2.64 -0.05 Media -0.31524 -1.19610 0.09371 -0.00025 -0.04942 -0.00213 T-Statistics 0.00 -0.05 0.13 -0.32 -1.20 -0.09 Real Estate -0.00023 0.05254 -0.86130 -0.00023 0.05254 0.01367 T-Statistics -0.39 1.72 -0.81 -0.39 1.72 0.81 Retail -0.00032 0.07670 -0.01802 -0.00032 0.07670 0.00029 T-Statistics -0.47 2.14 -0.01 -0.47 2.14 0.01 Software & Services -0.00108 0.02588 -2.94947 -0.00108 0.02588 0.04681 T-Statistics -0.96 0.44 -1.43 -0.96 0.44 1.43

(T.H)3 & Equipment -0.00015 0.02507 -4.16630 -0.00015 0.02507 0.06611

T-Statistics -0.15 0.46 -2.21 -0.15 0.46 2.21 Transportation -0.00011 0.01379 -1.51821 -0.00011 0.01379 0.02409 T-Statistics -0.17 0.39 -1.23 -0.17 0.39 1.23 Others 0.00046 -0.01683 -1.62630 0.00046 -0.01683 0.02581 T-Statistics 0.49 -0.34 -0.95 0.49 -0.34 0.95

1

Iβiφ 2

Iβ iϕ 1

Iα 2

Iα

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21

itIftmtIIftIt~D]r~r~[r~r~ ε+α+−α+ϕ=− 21

38

Table 6(c): The Impact of the Madrid Bombings on Singapore Based Industry Indices- Regression Analysis

Industry

Automobiles 0.00095 0.01321 -5.09932 0.00095 0.01321 0.05569 T-Statistics 1.17 0.33 -1.96 1.17 0.33 1.96 Banks & Insurance 0.00061 0.04468 -1.93898 0.00061 0.04468 0.02117 T-Statistics 1.06 1.56 -1.05 1.06 1.56 1.05 Capital Goods 0.00014 0.03102 -3.38903 0.00014 0.03102 0.03701 T-Statistics 0.24 1.12 -1.90 0.24 1.12 1.90

(C.D)1 and Apparels -0.00017 0.05698 -3.58233 -0.00017 0.05698 0.03912

T-Statistics -0.23 1.56 -1.52 -0.23 1.56 1.52 Consumer Services -0.00017 0.03688 -3.18672 -0.00017 0.03688 0.03480 T-Statistics -0.30 1.29 -1.72 -0.30 1.29 1.72 Diversified Financials 0.00029 0.06360 -3.41402 0.00029 0.06360 0.03728 T-Statistics 0.46 2.04 -1.69 0.46 2.04 1.69 Energy 0.00127 0.02366 -5.39832 0.00127 0.02366 0.05895 T-Statistics 1.74 0.66 -2.32 1.74 0.66 2.32 Food & Beverages 0.00020 0.02153 -3.40330 0.00020 0.02153 0.03716 T-Statistics 0.38 0.83 -2.03 0.38 0.83 2.03 Healthcare 0.00013 0.04204 -3.36362 0.00013 0.04204 0.03673 T-Statistics 0.14 0.86 -1.07 0.14 0.86 1.07

(H.P)2

Products 0.00032 0.04840 -3.27825 0.00032 0.04840 0.03580 T-Statistics 0.51 1.57 -1.64 0.51 1.57 1.64 Materials 0.00024 0.10614 -2.78928 0.00024 0.10614 0.03046 T-Statistics 0.35 3.14 -1.28 0.35 3.14 1.28 Media -0.34421 -0.31637 -1.72521 -0.00023 -0.01044 0.04024 T-Statistics 0.00 -0.01 -3.69 -0.34 -0.32 1.73 Real Estate -0.00004 0.07430 -2.82959 -0.00004 0.07430 0.03090 T-Statistics -0.07 2.73 -1.61 -0.07 2.73 1.61 Retail -0.00010 0.07263 -3.00439 -0.00010 0.07263 0.03281 T-Statistics 0.22 0.44 -1.34 -0.16 2.40 1.54 Software & Services -0.00050 0.05559 -3.62900 -0.00050 0.05559 0.03963 T-Statistics -0.56 1.27 -1.28 -0.56 1.27 1.28

(T.H)3 & Equipment 0.00009 0.03581 -4.75795 0.00009 0.03581 0.05196

T-Statistics 0.12 0.90 -1.84 0.12 0.90 1.84 Transportation 0.00066 0.02032 -3.59273 0.00066 0.02032 0.03923 T-Statistics 1.06 0.67 -1.82 1.06 0.67 1.82 Others 0.00017 0.01683 -3.31265 0.00017 0.01683 0.03617

This table presents the regression analysis results for 18 Singapore Based Industries incorporating the terrorist attack in the United States. The first multiplicative dummy variable

equation, itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21 , illustrates the impact on systematic risk, and the second

additive dummy variable equation, ε+α+−α+ϕ=− 21 ~D]r~r~[r~r~ IftmtIIftIt , shows the impact on the intercept.

1The term(C.D) represents the sector, Consumer Durables.

2The term (H.P) represents the sector, Household and Personal Products.

3The term (T.H) represents the sector, Technology, Hardware and Equipments.

itftmtIftmtIIftIt Drrrrrr εββφ ~*]~~[]~~[~~ 21 +−+−+=−itIftmtIIftIt Drrrr εααϕ ~]~~[~~ 21 ++−+=−

1

Iβiφ 2

Iβ iϕ 1

Iα 2

Iα

39

Table 6(d): The Impact of the London Bombings on Singapore Based Industry Indices- Regression Analysis

.

Industry

Automobiles 0.00065 0.02719 -0.75723 0.00065 0.02719 0.00187 T-Statistics 0.98 0.78 -0.07 0.98 0.78 0.07 Banks & Insurance 0.00072 0.05196 -3.27454 0.00072 0.05196 0.00809 T-Statistics 1.50 2.07 -0.42 1.50 2.07 0.42 Capital Goods 0.00037 0.03965 -3.33675 0.00037 0.03965 0.00825 T-Statistics 0.77 1.62 -0.44 0.77 1.62 0.44

(C.D)1 and Apparels -0.00005 0.06317 1.47512 -0.00005 0.06317 -0.00365

T-Statistics -0.09 1.99 0.15 -0.09 1.99 -0.15 Consumer Services 0.00013 0.04548 -1.63428 0.00013 0.04548 0.00404 T-Statistics 0.27 1.79 -0.21 0.27 1.79 0.21 Diversified Financials 0.00045 0.07102 -1.32665 0.00045 0.07102 0.00328 T-Statistics 0.86 2.62 -0.16 0.86 2.62 0.16 Energy 0.00137 0.02940 -1.72951 0.00137 0.02940 0.00428 T-Statistics 2.26 0.93 -0.18 2.26 0.93 0.18 Food & Beverages 0.00024 0.02753 -3.58312 0.00024 0.02753 0.00886 T-Statistics 0.53 1.19 -0.50 0.53 1.19 0.50 Healthcare 0.00019 0.04509 -10.25462 0.00019 0.04509 0.02535 T-Statistics 0.24 1.09 -0.81 0.24 1.09 0.81

(H.P)2

Products 0.00037 0.05223 -3.64771 0.00037 0.05223 0.00902 T-Statistics 0.71 1.94 -0.44 0.71 1.94 0.44 Materials 0.00020 0.10509 -0.64100 0.00020 0.10509 0.00158 T-Statistics 0.36 3.57 -0.07 0.36 3.57 0.07 Media -0.00007 0.00494 0.52084 -0.00007 0.00494 -0.00129 T-Statistics -0.13 0.17 0.06 -0.13 0.17 -0.06 Real Estate 0.00030 0.08098 -4.82460 0.00030 0.08098 -4.82460 T-Statistics 0.63 3.34 -0.65 0.46 0.43 0.32 Retail 0.00027 0.07993 -2.84591 0.00027 0.07993 0.00704 T-Statistics 0.51 2.96 -0.34 0.51 2.96 0.34 Software & Services -0.00037 0.06047 -3.17054 -0.00037 0.06047 0.00784 T-Statistics -0.51 1.62 -0.28 -0.51 1.62 0.28

(T.H)3 & Equipment -0.00002 0.04528 -8.35867 -0.00002 0.04528 0.02066

T-Statistics -0.03 1.31 -0.79 -0.03 1.31 0.79 Transportation 0.00102 0.02760 -9.07000 0.00102 0.02760 0.02242 T-Statistics 1.92 1.00 -1.07 1.92 1.00 1.07 Others 0.00029 0.01408 -3.19482 0.00029 0.01408 0.00790 T-Statistics 0.46 0.43 -0.32 0.46 0.43 0.32

This table presents the regression analysis results for 18 Singapore Based Industries incorporating the terrorist attack in the United States. The first multiplicative dummy variable equation,

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21 , illustrates the impact on systematic risk, and the second additive

dummy variable equation, ε+α+−α+ϕ=− 21 ~D]r~r~[r~r~ IftmtIIftIt , shows the impact on the intercept.

1The term (C.D) represents the sector Consumer Durable

2The term (H.P) represents the sector, Household and Personal Products.

3The term (T.H) represents the sector, Technology, Hardware and Equipments.

itftmtIftmtIIftIt Drrrrrr εββφ ~*]~~[]~~[~~ 21 +−+−+=−itIftmtIIftIt Drrrr εααϕ ~]~~[~~ 21 ++−+=−

1

Iβiφ 2

Iβ iϕ 1

Iα 2

Iα

40

Table 6(e): The Impact of the Mumbai Bombings on Singapore Based Industry Indices- Regression Analysis

.

Industry

Automobiles 0.00048 0.03650 -0.31125 0.00048 0.03650 -0.00271 T-Statistics 0.82 1.14 -0.11 0.82 1.14 -0.11 Banks & Insurance 0.00053 0.05811 0.35074 0.00053 0.05811 0.00305 T-Statistics 1.25 2.51 0.17 1.25 2.51 0.17 Capital Goods 0.00019 0.04706 0.21911 0.00019 0.04706 0.00191 T-Statistics 0.46 2.07 0.11 0.46 2.07 0.11

(C.D)1 and Apparels -0.00042 0.06125 1.63560 -0.00042 0.06125 0.01423

T-Statistics -0.78 2.07 0.61 -0.78 2.07 0.61 Consumer Services 0.00001 0.05174 0.31469 0.00001 0.05174 0.00274 T-Statistics 0.03 2.20 0.15 0.03 2.20 0.15 Diversified Financials 0.00026 0.07744 0.29454 0.00026 0.07744 0.00256 T-Statistics 0.57 3.12 0.13 0.57 3.12 0.13 Energy 0.00097 0.02875 0.86222 0.00097 0.02875 0.00750 T-Statistics 1.77 0.96 0.32 1.77 0.96 0.32 Food & Beverages 0.00015 0.03247 -0.83980 0.00015 0.03247 -0.00731 T-Statistics 0.36 1.49 -0.43 0.36 1.49 -0.43 Healthcare 0.00012 0.04625 0.59601 0.00012 0.04625 0.00519 T-Statistics 0.18 1.23 0.18 0.18 1.23 0.18

(H.P)2

Products 0.00029 0.05212 -1.00264 0.00029 0.05212 -0.00873 T-Statistics 0.62 2.08 -0.44 0.62 2.08 -0.44 Materials -0.00007 0.11647 -1.05012 -0.00007 0.11647 -0.00914 T-Statistics -0.13 4.14 -0.41 -0.13 4.14 -0.41 Media -0.00034 0.01487 -0.37953 -0.00034 0.01487 -0.00330 T-Statistics -0.68 0.55 -0.16 -0.68 0.55 -0.16 Real Estate 0.00018 0.08271 0.59588 0.00018 0.08271 0.00519 T-Statistics 0.42 3.62 0.29 0.42 3.62 0.29 Retail 0.00015 0.08764 0.23711 0.00015 0.08764 0.00206 T-Statistics 0.32 3.45 0.10 0.32 3.45 0.10 Software & Services -0.00036 0.06209 -0.59793 -0.00036 0.06209 -0.00520 T-Statistics -0.57 1.83 -0.19 -0.57 1.83 -0.19

(T.H)3 & Equipment -0.00029 0.04481 -1.32888 -0.00029 0.04481 -0.01156

T-Statistics -0.49 1.41 -0.46 -0.49 1.41 -0.46 Transportation 0.00085 0.03454 0.11799 0.00085 0.03454 0.00103 T-Statistics 1.76 1.32 0.05 1.76 1.32 0.05 Others 0.00026 0.01883 -0.35181 0.00026 0.01883 -0.00306 T-Statistics 0.48 0.63 -0.13 0.48 0.63 -0.13

This table presents the regression analysis results for 18 Singapore Based Industries incorporating the terrorist attack in the United States. The first multiplicative dummy variable equation,

itftmtIftmtIIftIt~D*]r~r~[]r~r~[r~r~ ε+−β+−β+φ=− 21 , illustrates the impact on systematic risk, and the second additive

dummy variable equation, ε+α+−α+ϕ=− 21 ~D]r~r~[r~r~ IftmtIIftIt , shows the impact on the intercept.

1The term(C.D) represents the sector Consumer Durable.

2The term (H & P) represents the sector, Household and Personal Products.

3The term (T.H) represents the sector, Technology, Hardware and Equipments.

itftmtIftmtIIftIt Drrrrrr εββφ ~*]~~[]~~[~~ 21 +−+−+=−itIftmtIIftIt Drrrr εααϕ ~]~~[~~ 21 ++−+=−

1

Iβiφ 2

Iβ iϕ 1

Iα 2

Iα

41

Table 7(a): The LONG TERM Impact of September 11 attack on Singapore Based Industry Indices- Regression Analysis

itIftmtIftmtIIit SDSDrrrrr εδδδϕ ~*]~~[]~~[~ 321 ++−+−+=

Industry Iϕ 1

Iδ 2

Iδ 3

Iδ