Embed Size (px)

Citation preview

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

a© 2017 Central Bank Of Swaziland

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

b © 2017 Central Bank Of Swaziland

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

i© 2017 Central Bank Of Swaziland

S DW NA AZIL

EMNTSHOLI

June 2017 Issue No. 1

FINANCIAL STABILITY REPORT

CeNtral BaNk Of SwazIlaNd

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

ii © 2017 Central Bank Of Swaziland

the mission of the Central Bank of Swaziland (the Bank) is to foster a stable financial sector that is conducive to economic development in Swaziland. One of the principal objectives of the Bank - as stipulated in the Central Bank of Swaziland Order, 1974 (as amended) - is to supervise banks, credit financial institutions and other financial institutions to the end of promoting a sound financial structure. In accordance with the Constitution of the Kingdom of Swaziland Act 2005, specifically sections 206 (2) (d) and (f), the Bank shall supervise the operations of financial institutions in the Kingdom, and promote monetary stability and a sound and stable financial

structure in Swaziland. Swaziland’s current financial stability framework is adopted from the Common Market for eastern and Southern Africa (COMESA)1 framework, which includes the responsibility to publish financial stability reports (FSRs).

The FSR 2017 is the first publication of its kind by the Bank. While FSRs are issued with the overarching objective of limiting financial instability by communicating key risks and vulnerabilities to relevant stakeholders, the Bank also views the FSR as a platform for enhancing and further contributing to overall financial system stability, increasing

1http://cmi.comesa.int/wp-content/uploads/2016/03/Shields-Manual-on-Financial-Stability-By-Gift-Chirozva.pdf

FOREWORD BY THE GOVERNOR AND CHAIRMAN OF THE FINANCIAL STABILITY COMMITTEE

MR MAJOZI V. SITHOLEGOVERNOR

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

iii© 2017 Central Bank Of Swaziland

accountability of the financial stability function and strengthening co-operation on financial stability among relevant authorities.

The report presents an assessment of the global, regional and domestic macro-financial developments encompassing the real economy, financial markets, financial institutions, financial system infrastructure, and the legal and policy frameworks. Recognizing the interlinkages between the macro economy and financial system, the FSR 2017 highlights emerging risks and vulnerabilities both in the international context more generally and from the Swaziland perspective specifically. The early detection of possible risks to the financial system is necessary to give policy makers sufficient lead-time to take pre-emptive action to avert a systemic crisis.

One of the most critical functions of the financial system is that it facilitates financial intermediation by connecting savers and investors, thereby channelling surplus funds to productive investments that will stimulate economic activity and — ultimately — economic growth. A sound, stable, safe, effective and efficient financial system pools surplus funds, transfers and minimises risks, while at the same time increasing liquidity and information sharing through financial innovations and technology. In this regard, the financial sector regulators contribute immensely to economic development through provision of a wide range of regulatory services that promote orderly and proportionate growth, development and functioning of financial institutions, financial markets and financial system infrastructure. Regulators continuously monitor and evaluate performance, soundness and stability of regulated financial institutions in order to detect, prevent and isolate system-wide risks.

Financial stability is more difficult to define than price stability, which simply relates to, among other indicators, a stable inflation environment and the internal and external value of the currency. One perspective is that financial

2Systemic risk is the risk that the default of one institution in the system can lead to the default of one or more otherwise sound institutions, thereby threatening the markets and the economy as a whole.

stability may antithetically be defined as the absence of systemic risk,2 while yet another is that financial stability may be defined in terms of what is necessary to achieve it, for example a sound regulatory environment, effective macro-prudential surveillance and public confidence in the financial system.

While Swaziland largely maintained a stable financial system and a resilient economy in 2016, the local currency was somewhat volatile against the United States (US) Dollar. On average, inflation remained stubbornly above the upper end of the Southern African Development Community (SADC) macroeconomic convergence target band of 3%-7%. This FSR highlights some policy interventions that could be taken in order to cushion the economy and financial system, in particular in mitigating any potential vulnerability.

In view of the above, the Central Bank of Swaziland defines financial stability as a condition in which the financial system comprising of financial intermediaries, markets and market infrastructures is capable of withstanding internal and external shocks such that participants have confidence in the system.

Overall, greater public awareness of financial system vulnerabilities in itself may serve to encourage financial institutions to curb activities that might exacerbate systemic risks and help to promote policy reforms to strengthen the resilience of the financial sector. The period covered by this report is from January 2016 to June 2017; however, as this report is also forward-looking, current data and forecasts have been used where appropriate. The Bank intends publishing a financial stability report annually in June.

Majozi V. SitholeGOVERNOR

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

iv © 2017 Central Bank Of Swaziland

CONTENTSGlossary ........................................................................................................................ 1

1. Introduction ............................................................................................................ 3

2. Swaziland Financial System Cobweb .............................................................................. 42.1 External Environment .......................................................................................... 52.2 Domestic Economy .............................................................................................. 52.3 Household Debt ................................................................................................. 62.4 Corporate Sector ................................................................................................ 62.5 Banking sector ................................................................................................... 62.6 Non-bank Financial Sector ..................................................................................... 72.7 Payments Systems Stability ................................................................................... 7

3. Financial stability developments and trends .................................................................... 83.1 Global Economic Growth and Outlook ....................................................................... 11

3.1.1 Government Fiscal Position ........................................................................ 173.2 Domestic Economic Outlook ................................................................................... 15

3.1.1 Government Debt .................................................................................... 20

4. Developments and Risk Analysis of the Banking System ...................................................... 204.1 Credit and Funding Concentration ........................................................................... 244.2 Banks’ Funding Structure ...................................................................................... 254.3 Liquidity Risk .................................................................................................... 26

5. Developments and Risk Analysis of Non-Bank Financial Institutions ........................................ 285.1 Capital Markets ................................................................................................. 285.2 Insurance Sector ................................................................................................ 295.3 Retirement Funds ............................................................................................... 325.4 Savings and Credit Cooperatives Societies ................................................................. 345.5 Credit Financial Institutions .................................................................................. 36

6. Payment infrastructure and regulatory developments ........................................................ 386.1 Card Transactions ............................................................................................... 396.2 MTN Mobile Phone Money Transfers ......................................................................... 40

7. Regulatory Developments to Improve The Robustness of the Domestic Financial Infrastructure .... 417.1 Review of the Financial Institutions Act, 2005 and Central Bank Order, 1974 ........................ 417.2 Drafting of Financial Stability Bill ........................................................................... 417.3 Policy Implementation: 2015-2016 ........................................................................... 41

7.3.1 National Payments System ......................................................................... 417.3.2 Bank Supervision ..................................................................................... 41

8. Stress-Testing The Swaziland Banking Sector ................................................................... 438.1 Credit risk ........................................................................................................ 43

8.1.1 Default by the largest borrowers ................................................................. 448.2 Liquidity Risk .................................................................................................... 44

8.2.1 Simulated Bank Run ................................................................................. 448.2.2 Sudden withdrawal by systemic largest depositor ............................................. 45

8.3 Scenario Analysis ................................................................................................ 458.4 Worst-case Scenario ............................................................................................ 45

9. Statistical Appendix ................................................................................................... 46

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

v© 2017 Central Bank Of Swaziland

FIGURESFigure 1: Financial System Cobweb ........................................................................ 4

Figure 2: Inflation and Economic Growth.................................................................. 11

Figure 3: Fiscal and Current Account Positions ........................................................... 12

Figure 4: Swaziland’s Fiscal Balance ....................................................................... 12

Figure 5: Debt-to-GDP Ratio ................................................................................. 14

Figure 6: Household Debt by Type of Institutions ........................................................ 16

Figure 7: Corporate Sector Assets .......................................................................... 18

Figure 8: Corporate Debt Composition .................................................................... 19

Figure 9: Banking Sector Assets ............................................................................. 20

Figure 10: Bank Credit Growth Rate ......................................................................... 22

Figure 11: Banks’ Non-Performing Loans .................................................................... 23

Figure 12: Sectorial Distribution of Loans .................................................................. 24

Figure 13: Banks’ Sources of Funding........................................................................ 25

Figure 14: Structure of Deposits ............................................................................. 26

Figure 15: Asset Allocation - Other Long-term Instruments .............................................. 28

Figure 16: Asset Allocation - Money Market ................................................................ 29

Figure 17: Short-term Insurance Asset Distribution as at 31 December 2016 ......................... 30

Figure 18: Premium Income Distribution as at 31 December 2016 ...................................... 30

Figure 19: Long-term Insurance Industry Year-On-Year Indicators ...................................... 31

Figure 20: Long-term Insurance Industry Asset Distribution as at 31 December 2016 ............... 32

Figure 21: Premium Income Distribution as at 31 December 2016 ...................................... 33

Figure 22: Retirement Funds Assets as at 31 December 2016 ........................................... 33

Figure 23: Local Asset Distribution as at 31 December 2016 ............................................ 34

Figure 24: Foreign Asset Distribution as at 31 December 2016 .......................................... 34

Figure 25: SACCOS’ Performance ............................................................................. 35

Figure 26: Total Credit Financial Institutions Loan Book: 2012-2016 ................................... 37

Figure 27: SAECH Cheques Volume and Value .............................................................. 38

Figure 28: SAECH EFT CR & DR Volume and Value ......................................................... 39

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

vi © 2017 Central Bank Of Swaziland

TABLESTable 1: Economic growth projections for selected countries/regions ............................9

Table 2: SADC Macroeconomic Convergence Indicators ..............................................13

Table 3: Composition of Government’s Domestic Debt by Maturity ................................15

Table 4: Composition of Government Securities by Ownership .....................................15

Table 5: Proportion of Bank Credit by type of Corporate ............................................ 17

Table 6: Selected Indicators for the Corporate Sector ............................................... 19

Table 7: Changes in Banks’ Assets........................................................................21

Table 8: Indicators of Banking Sector Profitability After-tax ........................................ 22

Table 9: Banks’ Credit Concentration Level ............................................................ 24

Table 10: Banks’ Funding Concentration Level ..........................................................25

Table 11: Banking Sector Maturity Analysis as at end December 2016 ..............................26

Table 12: Key Indicators of Bank Liquidity (percentage ratios)....................................... 27

Table 13: SACCOS’ Financial Position .....................................................................35

Table 14: SWIPSS Flows .....................................................................................38

Table 15: Paper Instrument (Cheques) Flows ............................................................39

Table 16: Other Payment Instruments Usage ............................................................ 40

Table 17: MTN Mobile Phone Money Transactions ....................................................... 40

Table 18: Summary of Stress Test Shocks and Breaking Points ........................................43

Table 19: Summary of Stress Test Results for Loans Migration ........................................43

Table 20: Default by the Largest Borrowers ............................................................. 44

Table 21: Summary of Stress Test Results for Bank Run ................................................ 44

Table 22: Sudden Withdrawal By Systemic Largest Depositor ........................................45

Table 23: Selected Quarterly Financial Soundness Indicators for Swaziland .......................46

Table 24: Commercial Banks’ Quarterly Financial Soundness Indicators ............................47

Table 25: Commercial Banks’ Quarterly Balance Sheet ................................................ 49

Table 26: Commercial Banks’ Quarterly Income Statement, year-on-year Figures ................51

BOXES:Box 1: Government Arears ..............................................................................13

Box 2: Calculating Household Disposable Income ................................................... 17

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

1© 2017 Central Bank Of Swaziland

GLOSSARY

ALSI All Shares Index

ATMs Automated Teller Machines

BCBS Basel Committee on Banking Supervision

BIS Bank for International Settlements

BOP Balance of Payments

CBR Central Bank rate

CBS Central Bank of Swaziland

CMA Common Monetary Area

CODAS Co-operative Data Analysis System

CSO Central Statistics Office

DIR Debt Service-to-Income Ratio

DSA Debt Sustainability Analysis

DTS Deposits Taking SACCOs

EMEs Emerging Market Economies

FDI Foreign Direct Investment

FSC Financial Stability Committee

FSI Financial Stability Indicators

FSR Financial Stability Report

FSRA Financial Services Regulatory Authority

FSTC Financial Stability Technical Committee

GDP Gross Domestic Product

IMF International Monetary Fund

IT Information Technology

JSE Johannesburg Stock Exchange

LCR Liquidity Coverage Ratio

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

2 © 2017 Central Bank Of Swaziland

LHS left Hand Side

MENA Middle East and North Africa

MTDS Medium Term Debt Strategy

NPLs Non-Performing Loans

NSFR Net Stable Funding Ratio

RHS Right Hand Side

ROA return on assets

ROE Return on Equity

SAECH Swaziland Automated Clearing House

SIPS Systemically Important Payment System

SMEs Small and Medium Enterprises

SSA Sub-Saharan Africa

SSX Swaziland Stock Exchange

SWIPSS Swaziland Interbank Payment and Settlement System

TRWA Total Risk-Weighted Assets

USA United States of America

USD United States Dollar

WEO World Economic Outlook

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

3© 2017 Central Bank Of Swaziland

This is the first issue of the Financial Stability Review, which focuses mainly on the eighteen-month period ended June 2017, comprises three main sections, namely (i) financial stability developments and trends, (ii) infrastructure and regulation, and (iii) stress testing of the banking system.

The first section starts with an overview of current international macrofinancial conditions. It contains a discussion of the major developments in the international, emerging-market, particularly South Africa, and regional environment that may influence financial stability in Swaziland. This section concludes with an analysis of the main developments in the Swaziland financial system, focusing specifically

on the sectors that have a significant bearing on the stability of the domestic financial system

The second section focuses on the financial system infrastructure and regulation, and starts with a review of the Financial Institutions Act (2005) and the Central Bank Order (1974). Furthermore, this section includes a note on the drafting of the Financial Stability Bill and the policy implementations for the national payment systems and the banking system.

Finally, the last section focuses on stress testing the banking sector of Swaziland under three scenarios to analyse the breaking point of the Swaziland banking system should these worst-case scenarios materialise.

INTRODUCTIONCHAPTER1

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

4 © 2017 Central Bank Of Swaziland

Figure 1: Financial System Cobweb

External Environment

Domestic Economy

Household debt

Corporate Sector HealthBanking Sector

Payments System Stability

Baseline Jun-17

NBFIs Sector

3See: http://www.riksbank.se/Documents/Rapporter/Ekonomiska_kommentarer/2012/rap_ek_kom_nr05_121128_eng.pdf

A cobweb3 is used to plot a summary of the assessment of financial stability. The assessment is largely based on the analysis of a range of quantitative indicators and variables. This applies to the assessment of the current situation as well as the assessment of the risks that might affect financial stability in the future. Risks are rated on a scale of 1 to 5, with 5 being the highest/worst risk rating. It is important to note that a large degree of judgement is used.

SWAZILAND FINANCIAL SYSTEM COBWEB

CHAPTER2The Bank has used seven categories for the cobweb to measure financial stability, namely:1. external environment;2. domestic economy;3. household debt;4. corporate sector health;5. banking sector;6. payments system stability; and7. non-bank financial sector.

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

5© 2017 Central Bank Of Swaziland

2.1 External EnvironmentSwaziland’s key trading partners (mainly South Africa) are likely to experience prolonged low economic growth, and this could lead to a concomitant slowdown in domestic economic growth. According to the April 2017 Global Financial Stability Report (GFSR)4 of the IMf, elevated political and policy uncertainty threaten global financial stability. The political climate in many countries is somewhat unsettled and low-income growth, among other factors, has given rise to more inward-looking protectionist policies. These developments expose economies and markets to shocks and increase the risk of economic and financial stagnation, potentially negating some of the benefits of decades of globalization. The IMF report further highlights that such challenges make it difficult for financial institutions to sustain healthy balance sheets, which in turn weaken economic growth and financial stability. On the back of exchange rate volatility, political uncertainty (particularly in South Africa),5 high interest rates and rising inflation, could undermine the support for economic growth by the financial sector. However, interest rates have decreased and inflation has somewhat subsided in South Africa6.

In April 2017, Fitch Ratings Agency (Fitch) downgraded South Africa’s sovereign credit

4http://www.imf.org/external/pubs/ft/gfsr/2016/02/ 5The anchor country for the Common Monetary Area (CMA)6https://www.resbank.co.za/Lists/News%20and%20Publications/Attachments/7396/MPC%20Statement%20July%202016.pdf7Import cover closed at 3.6 months at the end of December 2016. By the end of June 2017, it stood at 3.2 months, marginally higher than the international benchmark of 3 months.

rating one notch from investment standard (BBB-) to sub-investment standard (BB+). Corporates, banks and government are likely to pay a higher risk premium to attract foreign investors. In turn, the cost of finance will inevitably trickle down to consumers as corporates and government partially or fully pass costs on to consumers and taxpayers.

2.2 Domestic EconomyA combination of lowered Southern African Customs Union (SACU) receipts and exchange rate volatility of the Lilangeni resulted in lower reserves in 2016 when compared with 2015 and the reserves continue to be under pressure in 20177. Reserves stood at E8.3 billion at the end of January 2017, but have contracted to E6.9 billion in June 2017. The contraction in reserves was partly attributed to revaluation losses emanating from the strengthening of the Lilangeni against the US Dollar during the year. The Lilangeni started at its weakest at E16.06/USD at the end of January 2016 and was trading at its strongest at the end of December 2016 at E13.63/USD. As of June 2017, the Lilangeni was trading at E13.12/USD. SACU revenues were 13 percent lower in 2016 than in 2015 largely as a result of drought-induced lower agricultural production in the southern African region. The decline in SACU receipts was reflected in lower reserves, which fell by 9 percent in 2016.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

6 © 2017 Central Bank Of Swaziland

SACU revenues make up a significant portion of total government revenue (including grants). In 2016, SACU revenues amounted to 36.6 percent of total government revenue. The concentration of government revenue raises concerns from a financial stability viewpoint. Government has the largest workforce and largely supports small and medium enterprises (SMEs). In 2016, 34 percent of total government expenditure was projected to be spent on salaries and wages. Against a backdrop of highly indebted household and corporate sectors, adverse shocks to SACU revenues could have far-reaching effects across the economy transmitted through the financial sector.

Government has had trouble with servicing its obligations to domestic suppliers. Government arrears stood at e1.4 billion at the end of June 2017. At the cost of increasing domestic government debt, a supplier’s bond was issued in the last quarter of 2016 to support measures of reducing government arrears, prevent unsustainable drawdowns in reserves and ultimately support financial stability. Government arrears have since contracted to E434 million as at August 2017. However, the risk to financial stability remains as government expenditure growth outpaces the growth of government revenue. As a result, government’s budget deficit was projected to amount to 12.3 percent of GDP in the year 2016/17.

The outlook on government revenue is, however, positive as SACU receipts increased significantly to E7.2 billion in 2017 from the E5.2 billion received in 2016. Even though SACU receipts have increased, government expenditure and arrears remain, which could outweigh the benefits of the higher customs revenue.

2.3 Household DebtAt the end of 2016, credit extended to households by banks and non-bank financial institutions (NBFIs) amounted to 45.8 percent and 51 percent of total credit extension respectively. For the same period, 44.6 percent of household loans came from banks while 55.4 percent was from NBfIs. Households hold loans from both

banks and NBFIs at the same point in time as a result of information asymmetry between banks and non-banks. This situation poses a threat to financial stability since it is possible that when lending to the same household, neither creditor is aware of the true level of the particular household’s indebtedness. To this end, close monitoring of the household debt trend is required to enact policies that will support the Bank in its endeavours to maintain financial stability.

2.4 Corporate SectorThe corporate sector, especially the primary and secondary sub-sectors, experienced lowered production due to the drought experienced in 2016. Improved weather conditions as expected in 2017 have boosted production in the primary and secondary sector. Corporate sector profitability is threatened by the volatile exchange rate of the Lilangeni against major trading currencies. Corporate debt as a share of gross domestic product (GDP) is high, having hovered above 80 percent of GDP since 2013 before peaking at 90 percent in 2015. However, the risks arising from this situation depend on the corporate sector’s ability to reduce its indebtedness and debt management strategies. Failure to reduce corporate sector indebtedness could result in shrinking corporate sector profitability, which may translate to reduced private investments and consequently lower economic growth. The level of corporate sector indebtedness could also be an indication of other areas that macro and micro-prudential policies should focus on.

2.5 Banking SectorAlthough banks experienced growth during the period under review, maintaining their soundness and stability will remain a challenge. The levels of non-performing loans (NPLs) and banks’ cost-to-income ratios remain relatively high. Deteriorating asset quality and weakening profitability may further pose a challenge to the long-term health of the banking sector. This becomes even more crucial because of Swaziland’s highly concentrated banking sector, both from a funding as well as a

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

7© 2017 Central Bank Of Swaziland

8Out of 67 SACCOs

lending perspective. Therefore, banks need to continue paying close attention to credit risk management, ensuring that necessary controls are in place to protect themselves. In addition, the future economic outlook does not look particularly promising in terms of the operating environment for banks.

2.6 Non-bank Financial SectorThe non-banking financial sector continues to make progress in complying with the relevant legislation and capital adequacy requirements under the regulation and supervision of the Financial Services Regulatory Authority (FSRA). This promotes financial soundness of non-bank entities, thereby creating public confidence in the sector in order to protect the investing community. Full compliance with the recent legislated 50 percent local asset requirement may drive economic growth in the country even though it may take a while for investors to identify suitable local business partners.

Concentration risk is evident in the Savings and Credit Cooperatives (SACCOs) industry, with the top five8 which are government employee run SACCOs controlling 95 percent of the sector’s total assets, 66.3 percent of the industry’s loan book and 67.6 percent of the total deposits and savings. In effect, this means that should government experience cash flow challenges this sector may be under threat due to the high

levels of concentration as members rely on their salaries to make deposits/savings into the cooperatives and repay loans. Over-indebtedness to the credit financial institutions (CFIs) by individuals and households continues to be a precarious factor among these institutions. Total loans issued by credit institutions increase year after year, yet salary growth remains relatively low. The lack of an official credit bureau remains a challenge for the CFIs in assessing accurate and concise credit history information of borrowers. The country’s building society’s credit portfolio continues to deteriorate, with non-performing loans as a percentage of total loans increasing from 10.6 percent in 2014 to 12.5 percent in 2016. Tighter credit management practices have to be employed within the institution to reverse this trend.

2.7 Payments Systems StabilityThe national payment and settlement system operated smoothly throughout 2016, despite an overall increase in values and volumes transacted. The Swaziland Automated Electronic Clearing House (SEACH) and Swaziland Inter-Bank Payment and Settlement System (SWIPSS), which supports daily inter-bank dealings, are the two systemically important payment systems. Therefore, they remain one of the Bank’s main focus areas for the purposes of financial system stability assessment.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

8 © 2017 Central Bank Of Swaziland

3.1 Global Economic Growth and OutlookDuring 2017/18, global economic growth is projected to continue to improve on account of emerging markets’ and developing economies’ economic performance, particularly China’s, while advanced economies are expected to grow moderately. Global economic growth is expected to increase from 3.1 percent in 2016 to 3.5 percent in 2017 (Table 1)9. Emerging markets and developing economies (EMDEs) are projected to reach growth of 4.5 percent and 4.8 percent in 2017 and 2018, respectively. This growth forecast is largely attributed to China, whose economy is projected to expand by 6.5 percent in 2017, based on expectations of policy support. However, China’s reliance on policy stimulus measures, coupled with rapid growth in credit and slow progress in addressing substantial corporate debt levels and governance issues, poses a sharp downside risk to China’s long-term economic growth. According to April 2017 World Economic Outlook (WEO) Update, advanced economies are projected to grow moderately by 1.9 percent in 2017 and 2.0 percent in 2018, thus gradually converging to their long-term potential output growth.

Inflation in advanced economies and emerging markets is likely to increase in 2017, while inflation in EMDEs is projected to average 4.7 percent.10 Advanced economies, particularly the US, are registering important reductions in unemployment rates and a gradual recovery of output and income, with inflation rates gradually returning to within targeted levels.

9International Monetary Fund, World Economic Outlook Update, April 2017. http://www.imf.org/en/Publications/WEO/Issues/2017/04/04/world-economic-outlook-april-201710World Economic Outlook Database, April 2017.

Inflation rates in advanced economies and emerging markets may also increase following an expected significant uptick in oil prices as forecasted by the WEO.

The WEO Update views risks to global growth outlook as skewed to the downside. the report bases this observation on recent political developments in advanced economies that could threaten progress with cross-border economic integration, including calls for protectionist measures to be addressed. Increasing restrictions on global free trade and migration could affect productivity and income growth, as pressures around the implementation of inward-looking policies in advanced economies mount. As already noted, there are uncertainties about the lasting effectiveness of policy-induced growth in China against the background of structural weaknesses. Should these policies turn out unsuccessful, China could weigh down economic growth in EMDEs.

Growth in sub-Saharan Africa (SSA) has been declining in recent years, but it is projected to rebound somewhat in the period ahead. Regional growth is anticipated to reach 2.6 percent and 3.5 percent in 2017 and 2018, respectively; more than double the growth rate recorded in 2016 (Table 1). The more robust growth in SSA is expected to be driven by increases in commodity prices, and fuel and non-fuel commodity prices against the backdrop of stronger growth in global trade and GDP than in 2016.

GLOBAL ECONOMIC GROWTH AND OUTLOOK

CHAPTER3

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

9© 2017 Central Bank Of Swaziland

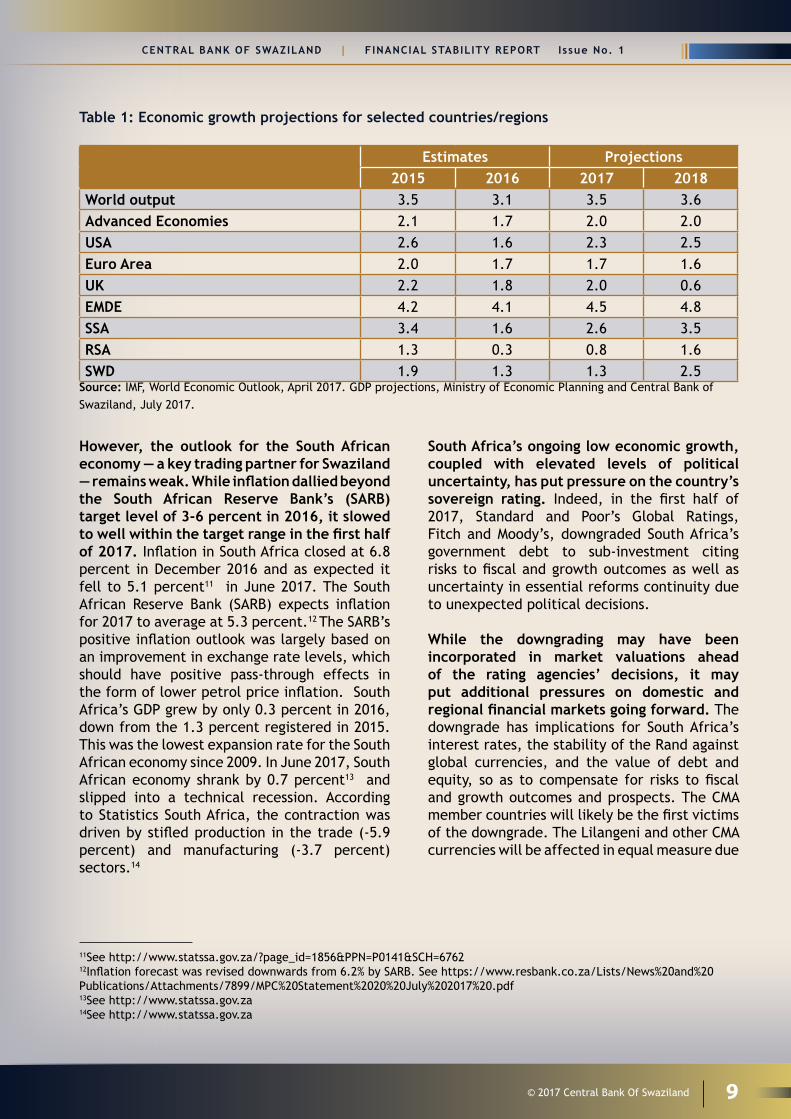

However, the outlook for the South African economy — a key trading partner for Swaziland — remains weak. While inflation dallied beyond the South African Reserve Bank’s (SARB) target level of 3-6 percent in 2016, it slowed to well within the target range in the first half of 2017. Inflation in South Africa closed at 6.8 percent in December 2016 and as expected it fell to 5.1 percent11 in June 2017. the South African Reserve Bank (SARB) expects inflation for 2017 to average at 5.3 percent.12 The SARB’s positive inflation outlook was largely based on an improvement in exchange rate levels, which should have positive pass-through effects in the form of lower petrol price inflation. South Africa’s GDP grew by only 0.3 percent in 2016, down from the 1.3 percent registered in 2015. This was the lowest expansion rate for the South African economy since 2009. In June 2017, South African economy shrank by 0.7 percent13 and slipped into a technical recession. According to Statistics South Africa, the contraction was driven by stifled production in the trade (-5.9 percent) and manufacturing (-3.7 percent) sectors.14

11See http://www.statssa.gov.za/?page_id=1856&PPN=P0141&SCH=676212Inflation forecast was revised downwards from 6.2% by SARB. See https://www.resbank.co.za/Lists/News%20and%20Publications/Attachments/7899/MPC%20Statement%2020%20July%202017%20.pdf13See http://www.statssa.gov.za14See http://www.statssa.gov.za

Table 1: Economic growth projections for selected countries/regions

Estimates Projections2015 2016 2017 2018

World output 3.5 3.1 3.5 3.6Advanced Economies 2.1 1.7 2.0 2.0USA 2.6 1.6 2.3 2.5Euro Area 2.0 1.7 1.7 1.6UK 2.2 1.8 2.0 0.6EMDE 4.2 4.1 4.5 4.8SSA 3.4 1.6 2.6 3.5RSA 1.3 0.3 0.8 1.6SWD 1.9 1.3 1.3 2.5

Source: IMF, World Economic Outlook, April 2017. GDP projections, Ministry of Economic Planning and Central Bank of Swaziland, July 2017.

South Africa’s ongoing low economic growth, coupled with elevated levels of political uncertainty, has put pressure on the country’s sovereign rating. Indeed, in the first half of 2017, Standard and Poor’s Global Ratings, Fitch and Moody’s, downgraded South Africa’s government debt to sub-investment citing risks to fiscal and growth outcomes as well as uncertainty in essential reforms continuity due to unexpected political decisions.

While the downgrading may have been incorporated in market valuations ahead of the rating agencies’ decisions, it may put additional pressures on domestic and regional financial markets going forward. the downgrade has implications for South Africa’s interest rates, the stability of the Rand against global currencies, and the value of debt and equity, so as to compensate for risks to fiscal and growth outcomes and prospects. The CMA member countries will likely be the first victims of the downgrade. The Lilangeni and other CMA currencies will be affected in equal measure due

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

10 © 2017 Central Bank Of Swaziland

to their peg to the rand. In addition, domestic credit institutions are unlikely to have a rating higher than the sovereign rating; hence the effects of the downgrade will be transmitted across the CMA through interlinkages in the financial system.

In April 2017, the effects of the developments in South Africa were evident in Swaziland’s bond market. A five-year E150 million bond was offered but bids to the value of only E78.25 million were received. The Auction Committee rejected all bids on the grounds that the tendered yields were deemed to be extraordinarily above market rates. Investor feedback revealed that the tendered yields reflected expectations based on the recent downgrade of South African debt.

The Swazi government’s dependence on SACU revenues is a contributor to government’s widening fiscal deficit. As a percentage of total government revenue, 36.6 percent was SACU receipts in 2016/17. The SACU receipts however, were projected to make up 42.1 percent of government’s revenue in 2017/18. The dependence on SACU has important spillover effects to the domestic economy which have manifested, in particular, in the accumulation of government payments arrears to its suppliers, as well as rising NPLs reported by banks. SACU revenue sharing amounts have been affected by South Africa’s lasting weak economic performance and have put pressure on SACU member

15Central Bank of Swaziland Quarterly Report, March 2017.16Financial Markets Data & Research Data, June 2017.17Central Bank of Swaziland Quarterly Report, December 2016

countries’ government finances, particularly Swaziland. The enduring weak performance of the South African economy, including droughts experienced in the Eastern and Southern Africa regions, has reduced SACU revenue inflows for other SACU member countries, as specified in the SACU revenue-sharing formula. In the case of Swaziland, SACU revenue declined from around 16.1 percent of GDP in 2013/14 to 12.2 percent of GDP in 2016/17.16

3.2 Domestic Economic Outlook A decline in economic growth and relatively high inflation were observed during 2016 in the Swazi economy. Swaziland’s economy is estimated to have grown by 1.3 percent in 2016 (Table 1), from a revised estimate of 1.9 percent17 growth in 2015. The drought affecting output in agriculture and agro-processing, as well as power generation and water supply, mainly contributed to the lower growth in 2016. Limited agricultural production was realized, in turn leading to relatively high food price inflation, which is likely to have significantly affected low-income families across the country. Partly to address the ensuing inflationary pressures, the Bank tightened monetary policy by raising the discount rate by a cumulative 100 basis points during 2016.

Inflation figures indicate a gradual decline in inflation in the second quarter of 2017: Inflation declined from 8.7 percent at the end of December 2016 to 6.9 percent at the end of June 2017 but it has remained sticky.

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

11© 2017 Central Bank Of Swaziland

Figure 2: Inflation and Economic Growth

2010 2011 2012

Average Inflation Economic Growth

2013 2014 2015 2016 Jun-2017*

109

8

7

6

5

4

3

2

1

0

Source: Central Bank of Swaziland Quarterly Review, March 2017. GDP Projections, Central Bank of Swaziland & Ministry of Economic Development and Economic Planning, August 2016. *Projection

18GDP Projections, Central Bank of Swaziland and Central Statistics Office, August 201619Ministry of Finance Budget Speech 2017, Presented 24 February 2017, Honourable Minister Martin Dlamini.

Going forward, a more benign combination of inflation and output growth is expected than in the recent past. Projections by the Ministry of Economic Planning and Development and the Bank depict a marginal rebound in economic activity supported by improved output from the agriculture and primary sectors in 201718. A firm monetary policy stance should also support a gradual reduction in the inflation rate in 2017. Downside risks to the projection, however, include a slower recovery of main trading partners than indicated above, as well as a slow rebound of the domestic secondary sector during the year. On the inflation front, there is still a delicate balance from an increased food supply that should put downward pressure on food prices and underlying threats of further droughts in particular areas of the country, which would counter a decline in the prices of main staples.

3.3.1 Government Fiscal Position19 Analysis of the county’s fiscal position reflects significant widening deficits from 2015/16 to 2016/17 (figure 3), including an increase in government’s payment arrears, which the government intends to address during the current fiscal year. The deficit for the 2016/17 financial year was estimated to be 12.3 percent of GDP, almost three times as high as the 2015/16 budget deficit . Increased government recurrent expenditure in the context of severely diminished SACU revenue largely explains the deterioration in the fiscal balance. The widening deficit poses risks to sound public debt management and government’s ability to meet its statutory obligations. Against this background, the government intends to reduce the fiscal deficit to 8.2 percent of GDP in 2017/18, by reigning in government expenditure and lowering reliance on SACU revenue.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

12 © 2017 Central Bank Of Swaziland

Figure 3: Fiscal and Current Account Positions

-4 000

-3 000

-2 000

-1 000

-

1 000

2 000

3 000

4 000

5 000

6 000

E'BI

LLIO

N

Fiscal A/C Surplus/Deficit Current A/C Surplus/Deficit

6,000

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16*

5,000

4,000

3,000

2,000

1,000

--1,000

-2,000

-3,000

-4,000

Fiscal A/C Surplus/Deficit Current A/C Surplus/Deficit

E’Bi

llion

Source: Central Bank of Swaziland Quarterly Review, December 2016

Figure 4: Swaziland’s Fiscal Balance

2009/10

SADC MECI Deficit/GDP

Surp

lus/

Defi

cit

as %

of

GD

P

Surplus/Deficit as % of GDP

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17**

6.05.04.03.02.01.00.0

-1.0-2.0-3.0-4.0-5.0-6.0-7.0-8.0-9.0

-10.0-11.0-12.0-13.0-14.0-15.0

Source: Central Bank of Swaziland Quarterly Review, December 2016*estimated Outturn**Budget

The deterioration in the government’s financial position has set back efforts towards nominal convergence within SADC. Figure 4 shows that the country was within the SADC Macroeconomic Convergence Indicators (MECI) target in 2014/15, when the fiscal deficit was 1.2 percent of GDP. However, since 2015/16,

the government’s budget deficit has widened significantly, thus moving away from the SADC recommended target. The Government of Swaziland is mindful of the SADC target for member states to achieve a fiscal deficit of less than 3 percent by 2018 (Table 2).

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

13© 2017 Central Bank Of Swaziland

Table 2: SADC Macroeconomic Convergence Indicators

2008 2012 2018Primary MECI Annual Inflation Rate <9.5% <5% <3%

Fiscal deficit/GDP <5% <3% <3%

Public debt/GDP <60% <60% <60%

Current account/GDP <9% <9% <3%

Secondary MECIEconomic growth (%) 7% 7% 7%

External reserves (import cover, months) 3 Months 6 Months 7 Months

Central Bank credit to government (% of Revenues) 10% 5% 5%

Domestic savings (% of GDP) 25% 30% 35%

Domestic investment (% of GDP) 30% 30% 30%Source: SADC Macroeconomic Surveillance and Performance Unit: Guidelines for preparation of country assessments and national macroeconomic convergence programs, 2013

Box 1 – Government ArrearsAn accumulation of government arrears indicates that government is behind on its payment obligations to its suppliers and creditors. The accumulation of government arrears could be caused by cash-flow problems, unrealistic budgets, inadequate provision for multi-year commitments, weak cash management perpetuated by inadequate monthly cash limits, corruption, selective payments and administrative delays.

Arrears increase the cost of service provision, as government suppliers protect themselves against delayed payments by raising their prices. These also reduce and interrupt public service delivery, as government is forced to reduce the amount of supplies purchased on the volume of public services provided. Government expenditure arrears may also perpetuate corruption, as rent-seeking behavior may increase. Chronic delays in payments may hike incentives for collusion between some government employees and suppliers, as the latter seek to accelerate payment by all means, including circumventing policies and procedures for public procurement and settlement of obligations.

Private sector confidence in government’s ability to pay could also be affected adversely. Consumers and investors may anticipate an increase in tax rates (as the government tries to arrest its difficult cash flow), higher inflation or a worsening of the government’s financial situation over the medium term. Due to the reach of government’s activities across the economy, arrear accumulation may spread to other sectors of the economy with severe consequences to financial stability and, therefore, prospects for economic growth.

Source: Adapted from Suzanne Flynn and Mario Pessoa, Prevention and Management of Government Expenditure Arrears (The Effects of Good Government on the City Life, Fresco, Palazo Pubblica, Sienna, Italy). Regional Course on Financial Programming and Policies, Pretoria South Africa (February 23-March 6, 2015), IMF Institute for Capacity Building

3.3.2 Government Debt

Over the years, government has refocused its source of debt finance from foreign to domestic debt. Government incurs foreign

debt primarily to finance large capital projects, while domestic debt is undertaken to meet government’s current domestic financial obligations. While the foreign debt-to-GDP ratio has increased at a slow rate since 2010, the

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

14 © 2017 Central Bank Of Swaziland

domestic-debt-to-GDP ratio has increased at a higher pace. The domestic-debt-to-GDP ratio increased from 3.7 percent at the end of 2010 to 10.6 percent at the end of June 2017. On the other hand, the foreign debt-to-GDP ratio increased at a slower rate, from 7.7 percent at the end of December 2010 to 9.2 percent at the end of June 2017. The shift of public debt to mostly domestic debt is explained by the continued issuance of government securities through the Bond Program, Suppliers Bond

Program, as well as the advance by the Bank to government in 2016.

Should such growth in domestic debt be maintained, it could pose a threat to financial stability. High growth in public debt could indicate that government is delaying tax efficiencies and diversification of sources of revenue, thus putting upward pressure on future interest rates, crowding out private sector credit, as well as posing risks related to debt maturity structure and debt roll-over.

Figure 5: Debt-to-GDP Ratio

-

5.0

10.0

15.0

20.0

2010 2011 2012 2013 2014 2015 2016 June-2017

DEB

T-TO

-GD

P RA

TIO

(%)

Foreign Debt to GDP Domestic Debt to GDP Total Debt to GDP

2010

Foreign Debt to GDP

Deb

t-to

-GD

P Ra

tio

(%)

Domestic Debt to GDP Total Debt to GDP

20.0

15.0

10.0

5.0

0.02011 2012 2013 2014 2015 2016 June-2017

Source: Central Bank of Swaziland Quarterly Review, March 2016. Financial Markets Department Data

Government arrears amounted to E1.4 billion at the end of June 2017. By end-February 2017, a total of E535 million had been raised through the bond programme. this amount has already been used to pay some suppliers. Government efforts towards eradicating the arrears aim to minimize the risk of suppliers’ default of their financial obligations with banks. The composition of government’s domestic debt since 2010 reflects an ongoing shift from short-term to longer-term debt financing that accelerated in late 2016 (Table 3). The hike in holdings of government bonds in 2016 was on account of debt issuances to tackle government payment arrears incurred during the year. This uptake was mainly noted in December 2016, when commercial banks and the building society increased their medium-term bond holdings through participation in the suppliers’ bond program, which comprised of short- to medium-

term notes with maturities that range between 12 months and 60 months. The program’s main objective was to reduce government’s payment arrears and address the concomitant negative spillover effects on the rest of the economy.

As a SADC member, Swaziland observes the regional convergence guidelines of a debt-to-GDP ratio that should not exceed 60 percent, although there may be hikes in Swaziland’s external debt ratios going forward. Swaziland’s public-debt-to-GDP stands below 20 percent, which is comfortably below the SADC recommended MECI level of below 60 percent even though a ratio below 60 percent or 20 percent in the case of Swaziland does not imply capacity to repay. The volatility of government debt-to-GDP ratio also looks contained as in 2003, government hedged the bulk of its foreign denominated debt maturing up to the

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

15© 2017 Central Bank Of Swaziland

year 2020. As at February 2017, government had hedged 28.2 percent of its total external debt. An emerging foreign exchange rate risk

may become evident as the old debt matures and as government takes up new unhedged foreign currency denominated debt.

Table 3: Composition of government’s domestic debt by maturity

Treasury Bills

(E’ 000)

Government bonds over 2 to 5 years

(E’ 000)

Government Bonds Over

5 to 10 years(E’ 000)

Total(E’ 000)

2010 772 250 219 1 2422011 720 817 146 1 6842012 1 101 767 146 2 0152013 1 906 814 200 2 9192014 1 752 747 451 2 9502015 1 649 749 725 3 1232016 1 675 2 069 670 4 414Jun-17 1 620 2 393 804 4 817

Source: Central Bank of Swaziland Quarterly Review, June 2017.

Table 4: Composition of government securities by ownership

Central Bank of Swaziland

(E’000)

Banks (E’000)

Non-bank financial institutions

(E’000)

Other (E’000)

2010 710 905 243 300 020 35 7312011 490 1 017 183 541 647 124 3092012 60 592 1 316 633 460 217 177 3772013 60 165 1 745 129 920 546 193 5082014 2 890 1 598 764 985 252 363 4842015 1 200 1 555 599 1 334 136 232 2852016 3 885 2 259 746 1 927 956 222 340 Jun-17 3 565 2 094 692 2 494 230 224 765

Source: Central Bank of Swaziland Quarterly Review, June 2017.

Banks and non-bank financial institutions (NBFIs) are the main holders of government debt (Table 4). As at March 2017, NBFIs held E2.5 billion in government bonds, while banks held E2.1 billion. Growth in holdings of medium-term government securities (2 to 5 years) has outpaced the growth in long-term government securities (5 to 10 years) as shown in Table 4. Market preference for government bonds is generally in the medium-term maturity ranges, where there is stronger bidding by banks than by

NBFIs that tend to favor longer-dated papers to match the long-term nature of their liabilities. The growth in medium-term bond holdings was boosted by the introduction of the suppliers’ bond program mentioned above.

Prudential holding requirements of domestic assets levied on NBFIs have boosted demand for government bonds to date and may raise issues of debt sustainability over the longer run. The holdings of government debt by the

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

16 © 2017 Central Bank Of Swaziland

financial sector could be attributed to NBFIs’ compliance with the statutory 30 percent local asset requirement as stated in schedule 3 of the Insurance Regulations 2008 and schedule 1A of the Retirement Fund Regulations 2008. Going forward, the financial sector is likely to increase their holdings of government debt following the enforcement of section 71(2) of the Securities Act 2010 by the NBFIs regulator, which requires fund managers to have at least 50 percent local asset holdings in their portfolios. Excessive exposure of the financial sector to government debt increases the risk of destabilizing the financial sector in the event government debt reaches unsustainable levels.

3.3.3 Household Sector The household sector is the largest sector served by commercial banks. As a percentage of total bank credit extended to the private sector as at December 2016, 44.6 percent was to households. Credit extension to households depicted year-on-year growth of 6.1 percent in 2016 when compared to December 2015. Despite holding a high portion of bank credit, households also hold a significant and increasing level of credit from NBFIs.21 Analysis of household credit revealed non-banks’ credit to households has grown from 45.8 percent in 2014 to 51 percent in 2016 (Figure 6).

21Data from NBFIs used is from the four biggest credit financial institutions, SACCOs and the Swaziland Building Society.22Measured as total household debt/gross disposable income.

Figure 6: Household debt by type of institutions

40.0

42.0

44.0

46.0

48.0

50.0

52.0

54.0

56.0

2014 2015 2016

Perc

ent

Banks & Building Society Credit Finance Institutions & SACCOs

Source: data from Central Bank of Swaziland and NBfIs

Household indebtedness22 accelerated from 128 percent in 2015 to 156 percent in 2016. The growth in interest rates has put downward pressure on gross disposable income as defined by the IMF Financial Stability Indicators (FSI) Compilation Guide 2006. The Bank rate is partly

informed by inflation and the base effects of the inflation rate from 2012 and 2013 have potentially distortionary effects on the actual current inflation rate, making it appear to be higher than it actually is. This should be factored in for future interest rate decisions.

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

17© 2017 Central Bank Of Swaziland

On the back of rising inflation and interest rates, household indebtedness should be closely monitored because changes in household behavior caused by a high debt burden can have a significant impact on both the real economy and the wider financial system. A highly indebted household sector is vulnerable to negative economic shocks which may impair households’ repayment capacity. Due diligence by credit providers is therefore encouraged to avoid an excessive burden being placed on disposable income caused by individuals being granted credit by multiple credit providers even after the statutory deductions to disposable income (per person) ratio has been exceeded.

Box 2 - Calculating household disposable income:

Income:Compensation to employeesCompensation by pension funds RemittancesSocial grants

(LESS)Expenses:Taxes= Gross disposable Income

Source: IMF FSI Compilation Manual 2006, paragraph 4.120

3.3.4 Corporate Sector According to the 2015 company survey23

conducted by the Central Bank of Swaziland in partnership with the Ministry for Finance, corporates find that domestic sources of finance are limited. Corporates in sectors such as real estate, utilities, agriculture and construction are primarily impeded by the low borrowing limits. Adding to this challenge are micro-prudential policies such as the single borrower limit that puts a cap on the amount of exposure that individual banks have to any single borrower. The average ratio of bank financing of corporates has been at around 10.5 percent of GDP during 2010-2016, with a marginal decline in the ratio being observed recently (see Table 5).

As can be seen from Table 5, corporate debt sourced from commercial banks is mostly skewed towards private non-financial corporates. As at June 2017, private sector corporates accounted for 82.5 percent of corporate debt in the banking sector. The proportion of bank credit extended to private non-financial corporates reflects a downward trend (Table 5). The share of bank credit to other financial corporates (non-bank private and public financial institutions) in total bank credit increased to 11.0 percent at the end of June 2017.

23Company Survey Summary Report 2015, Ministry for Finance and Central Bank of Swaziland, 2015. The survey focuses on significant entities in each sector of the economy.

Table 5: Proportion of bank credit by type of corporate

Other Financial Corporates

Public Non-Financial Corporates

Private Non-Financial Corporates

2010 13.2 3.9 82.92011 4.8 3.9 91.32012 4.5 2.9 92.62013 4.6 3.2 92.12014 7.5 3.1 89.42015 8.8 3.6 87.62016 12.5 3.9 83.6Jun-2017 11.0 6.4 82.5

Source: Central Bank of Swaziland Quarterly Review, June 2017.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

18 © 2017 Central Bank Of Swaziland

Total corporate sector assets grew from E55 billion in 2013 to E74.7 billion in 2016. this growth of 35.9 percent indicates a healthy corporate sector, as corporates are able to utilise growing assets to generate more sales and profits thereafter. As at 2016, corporate sector assets amounted to E74.7 billion — a

0.5 per cent decline from the previous year. As shown in figure 7, the largest three sectors are manufacturing, mining, quarrying, and industrial sector (39 percent), wholesale and retail trade, transportation and storage, accommodation and food service activities sector (19 percent), and the Real estate sector (12 percent).

Figure 7: Corporate Sector Assets

Agriculture, forestry and fishing Construction

Information and Communication

Manufacturing, Mining and Quarrying and Other Industrial

Other Service Activities

Professional, Scientific, Technical, Administrative and Support Service Activities

Public Administration and Defence, Education, Human Health and Social Work Activities

Real Estate Activities

Wholesale and Retail Trade, Transportation andStorage, Accommodation and Food Service Activities

10 4 3 39 3 8 2 12 19

1

2

3

4

5

6

7

8

9

19%10%

4%

3%

12%

2%

3%

8% 39%

Source: Swaziland Revenue Authority

Total corporate debt24 for non-financial and non-public corporates grew by 21 percent since 2013. However, it declined by 5 percent in 2016. In 2016, most corporates did not perform well and therefore relied more on credit to finance their operations. Total corporate debt amounted to E28.1 billion in 2016. Highly indebted corporates were mainly in the finance

and insurance sector, and the manufacturing and wholesale sector as at 2016 (Figure 8).

Corporate debt to GDP peaked at 56 percent in 2015 before declining to 51 percent in 2016. High corporate debt-to-GDP ratios were observed in the finance and insurance, and manufacturing and wholesale sectors.

24Corporate debt consists of long-term loans, director/ shareholder loans, associated company loans, trade payables, other payables, bank overdrafts, short-term loans and other loans.

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

19© 2017 Central Bank Of Swaziland

Figure 8: Corporate Debt Composition

Agriculture, forestry and fishing Construction

Information and Communication

Manufacturing, Mining and Quarrying and Other Industrial

Other Service Activities

Professional, Scientific, Technical, Administrative and Support Service Activities

Public Administration and Defence, Education, Human Health and Social Work Activities

Real Estate Activities

Wholesale and Retail Trade, Transportation andStorage, Accommodation and Food Service Activities

7 5 2 39 3 11 1 12 20

1

2

3

4

5

6

7

8

9

20%

7%5%

2%

12%

1%

3%

11%

39%

Source: Swaziland Revenue Authority

The high levels of corporate debt could be an indication that corporates have other sources of finance besides banks, for example, multi-national corporates are able to finance themselves through intra-company loans and local pension funds.

The overall performance of the corporate sector, measured by the return-on-equity (ROE) and return-on-assets (ROA) ratios, increased from 2015 to 2016 (Table 6). the agricultural sector - the worst performing sector in 2015 - improved in 2016 with ROE and ROA ratios of 9 percent and 5 percent respectively,

up from 2 percent and 1 percent respectively in 2015. At the end of 2016, the manufacturing sector outperformed the rest of the sectors, reporting ROE and ROA ratios of 47 percent and 20 percent respectively.

While credit extension is a driver of economic growth, close monitoring of credit extended to corporates is imperative to ensure that prudent lending is still practiced. Due diligence by banks should be exercised to minimize the risk of corporates defaulting on their contractual obligations.

Table 6: Selected indicators for the corporate sector

2013 2014 2015 2016Total debt to equity (%) 54 44 43 41Return on equity (ROE) (%) 37 29 27 28Profit after tax (E ‘billion) 4.6 5.0 5.8 5.5Return on assets (ROA) (%) 13 12 11 11Total assets (E ‘billion) 35.7 41.3 51.0 48.1Debt-To-GDP (%) 52 49 56 51

Source: Swaziland Revenue Authority

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

20 © 2017 Central Bank Of Swaziland

DEVELOPMENTS AND RISK ANALYSIS OF THE BANKING SYSTEM25

CHAPTER4The Swaziland banking sector, comprising four commercial banks (one of which is a government-owned bank), recorded strong annual growth during 2017. The increase reflected an expansion in almost all types of bank assets, particularly loans and overdrafts, investments and other securities, due from banks abroad, and holdings of government securities. Investments and other securities increased by 145.0 percent, while holdings with banks abroad increased by 48.8 percent. Holdings of securities, which increased by

13.3 percent, included banks’ participation in regular government Treasury bills (TBs) and bond auctions, as well as banks’ holdings of government paper under the supplier’s bond programme launched by the government from November, 2016 to March, 2017. During the year to June 2017, loans and overdrafts grew by 8.7 percent compared to 8.4 percent in June, 2016. On the liability side, the balance sheet’s expansion reflected the traditional increase in private sector deposits, mainly demand and term deposits.

Figure 9: Banking Sector Assets

Dec

-14

0.9

18.0

Loans & Overdrafts (Gross) due from Banks abroad

Investments and Other Securities due from Banks in Swaziland

Government Securities Asset Growth

20.0

10.0

16.0 15.0

8.0-

14.0 10.0

6.0(5.0)

2.0 (15.0)

12.05.0

4.0 (10.0)

- (20.0)

(5.0)

6.5

10.2

2.5

(1.5)

4.2 3.6

11.9

16.4

14.3

Mar

-15

E’Bi

llion

Perc

ent

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Source: Central Bank of Swaziland

25Also see the Note on “Stress-testing the Swaziland banking sector” in this publication

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

21© 2017 Central Bank Of Swaziland

Table 7: Changes in banks’ assets

Dec-14 Dec-15 Jun-16 Dec-16 Jun-17AssetsVolumes (E. Billion) 13.4 15.4 15.8 18.3 18.3

Annual growth (%) - 14.3 16.0 19.2 15.8

Loans and advancesVolumes (E. Billion) 9.3 9.7 9.9 10.7 10.7

Annual growth (%) - 3.6 4.1 10.5 8.7

Government SecuritiesVolumes (E. Billion) 1.5 1.6 1.8 2.1 2.1

Annual growth (%) - 9.3 25.6 28.9 13.3

due from banks abroad

Volumes (E. Billion) 1.3 2.1 1.9 2.7 2.8

Annual growth (%) - 57.7 46.2 26.3 48.8Source: Central Bank of Swaziland

Capital AdequacyBanks remained well capitalised during the period under review, with developments in 2017 resulting in increases in paid-up capital and reserves. all banks met the minimum capital adequacy requirements of 4.0 percent for tier 1 capital, 8.0 percent for total capital, and E15.0 million for minimum paid-up capital. The aggregate industry-wide regulatory tier 1 capital adequacy ratio and total capital adequacy ratios were at 21.0 percent and 23.5 percent respectively, thus showing the banks’ strong solvency positions. Total shareholder capital increased by 11.9 percent from E2.3 billion in June 2016 to E2.6 billion in June 2017, aided by growth in retained earnings. Banks also increased reserves appropriations, likely reflecting their precautionary stance in an uncertain economic environment.

The ratio of NPLs (net of specific provisions) to capital worsened from 20.7 percent reported in June, 2016 to 28.0 percent in

June 2017, showing increased credit risk and a future drain on capital. The leverage ratio,26 which is also an indicator of the adequacy of capital, increased marginally to 11.3 percent in June 2017 from 11.1 percent at the end of June 2016.

ProfitabilityBank profitability weakened somewhat in 2017 due to the on-going challenging economic environment. The average ROA and ROE ratios declined from 3.2 percent and 22.4 percent respectively at the end of June 2016, to 2.2 percent and 15.7 percent by June 2017 respectively. By international standards, however, the ROA and ROE ratios remained at relatively high levels. Year-on-year net after-tax earnings were E399.0 million, a decrease from E510.3 million in June 2016. The weakened profitability is as a result of the aforementioned increase in NPLs and the increased inflation, which hiked operating costs.

26The leverage ratio is the ratio of regulatory tier 1 capital to total assets, plus off-balance sheet items.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

22 © 2017 Central Bank Of Swaziland

Table 8: Indicators of banking sector profitability after-tax

Dec-14 Dec-15 Jun-16 Dec-16 Jun-17Net profit after tax (E. million) 359.4 485.9 510.3 458.0 399.0

ROA (%) 2.7 3.2 3.2 2.5 2.2

ROE (%) 19.8 23.1 22.4 18.4 15.7

Cost to income (%) 71.0 65.9 68.2 71.0 76.2Source: Central Bank of Swaziland

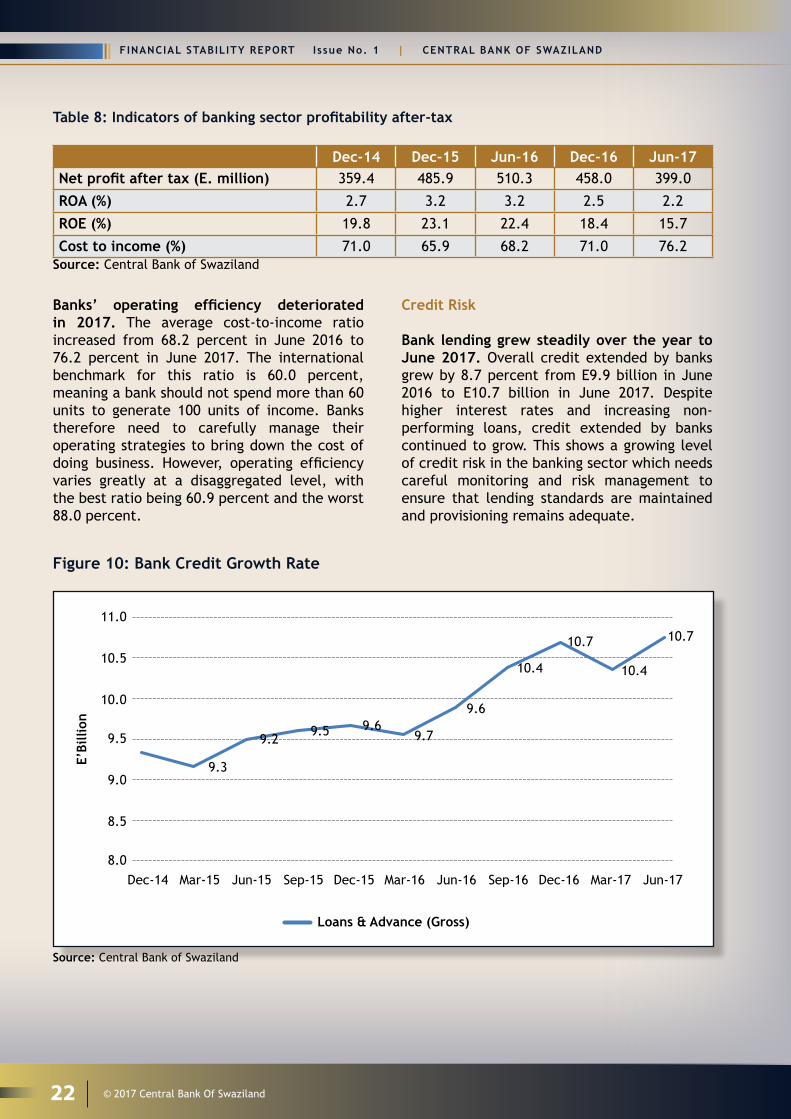

Banks’ operating efficiency deteriorated in 2017. The average cost-to-income ratio increased from 68.2 percent in June 2016 to 76.2 percent in June 2017. The international benchmark for this ratio is 60.0 percent, meaning a bank should not spend more than 60 units to generate 100 units of income. Banks therefore need to carefully manage their operating strategies to bring down the cost of doing business. However, operating efficiency varies greatly at a disaggregated level, with the best ratio being 60.9 percent and the worst 88.0 percent.

Credit Risk

Bank lending grew steadily over the year to June 2017. Overall credit extended by banks grew by 8.7 percent from E9.9 billion in June 2016 to E10.7 billion in June 2017. Despite higher interest rates and increasing non-performing loans, credit extended by banks continued to grow. This shows a growing level of credit risk in the banking sector which needs careful monitoring and risk management to ensure that lending standards are maintained and provisioning remains adequate.

Figure 10: Bank Credit Growth Rate

Dec-14

11.0

9.3

9.29.5 9.6

9.7

9.6

10.4

10.7

10.4

10.7

10.5

10.0

9.5

9.0

8.5

8.0Mar-15 Jun-15

Loans & Advance (Gross)

E’Bi

llion

Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17

Source: Central Bank of Swaziland

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

23© 2017 Central Bank Of Swaziland

Banks’ asset quality deteriorated during the year under review. The ratio of banks’ aggregate non-performing loans to total gross loans increased to 8.2 percent (E878.4 million) in June 2017 from 7.8 percent (E773.3 million) in June 2016. During 2016, Swaziland struggled with inflation triggered by both the drought and the falling exchange rate. The rise in inflation contributed to an increase in the lending rate,

which hampered customers’ repayment ability. The end result was an increase in the loan default rate as shown by the 13.6 percent hike in NPLs during 2017. Nevertheless, specific provisions to NPLs dropped by 20.2 percentage points from 39.1 percent to 18.9 percent over the same period, suggesting that banks are not providing sufficiently given the rate at which loan books are deteriorating.

Figure 11: Banks’ Non-performing Loans

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

E’M

illio

n

Perc

ent

1,200.0 12.0

10.0

8.0

6.0

4.0

2.0

0.0

4.3 4.43.8 3.7 3.7

3.64.6

6.47.6

7.89.1

9.2 9.9

8.2

1,000.0

800.0

600.0

Non-performing Loans NPLs to Total Gross Loans

400.0

200.0

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

170.0

Source: Central Bank of Swaziland

Lending for consumption and real estate-related purposes, as well as selected economic sectors, represents banks’ main business. The household sector accounted for the largest share of total banking sector loans at 42.6 percent, decreasing by 2.8 percentage points compared to June 2016. The financial wellbeing of households is therefore crucial for the future health of the banking sector. Unsecured household loans - usually a more expensive category of loans used mainly as a source for distressed lending - represented

12.3 percent of total banking sector loans and 28.8 percent of total household loans as at end June 2017. This suggests that households are significantly reliant on this type of credit. For households making use of this type of credit, an increase in interest rates could have serious implications. Distribution and tourism sector loans accounted for 12.5 percent of total loans followed by the real estate sector loans, which include both residential and commercial loans at 11.8 percent. The agriculture and forestry sector, which suffered as a result of the drought, accounted for 7.5 percent of total loans.

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

24 © 2017 Central Bank Of Swaziland

Figure 12: Sectorial Distribution of Loans

0.0

20.0

40.0

60.0

80.0

100.0

120.0 De

c-14

Mar

-15

Jun-

15

Sep-

15

Dec-

15

Mar

-16

Jun-

16

Sep-

16

Dec-

16

Mar

-17

Jun-

17

Perc

ent

Agriculture and forestry Mining and quarrying

Construction Distribution and tourism

Transport and communications Community social and personal services

Real estate Other businesses (not elsewhere included)

Personal and household loans Manufacturing

Other

Source: Central Bank of Swaziland

4.1 Credit and Funding ConcentrationConcentration risk remained relatively high for banks in Swaziland from both a funding and lending perspective.

Table 9: Banks’ Credit Concentration Level

Description Dec-14 Dec-15 Dec-16 Jun-17Average top 20 to Loans 46.7% 50.6% 44.6% 47.3%Average top 10 to Loans 39.2% 41.5% 36.2% 38.9%Average top 5 to Loans 31.0% 31.2% 25.8% 29.2%

Source: Central Bank of Swaziland

On average, the top 20 largest borrowers accounted for 47.3 percent of the loan book. These exposures should be carefully managed since a default by any of these borrowers could have dire consequences both for individual

banks and the banking sector as a whole. Also, 45.8 percent of total deposits are held by the top 20 largest depositors, which means that funding concentration is also fairly high.

CENTRAL BANK OF SWAZILAND | F INANCIAL STABILITY REPORT I ssue No. 1

25© 2017 Central Bank Of Swaziland

4.2 Banks’ Funding StructureCustomer deposits - the main source of funding for banks - grew by 23.9 percent in June 2017 compared to the year before, and represented 78.1 percent of total assets as at the end of June 2017. In absolute terms, total deposits

amounted to E14.3 billion. Total shareholders’ funds represented 14.0 percent of total assets and were the second largest source of funding. Funding from foreign financial institutions accounted for 1.5 percent of total assets as at June 2017.

Figure 13: Banks’ Sources of Funding

Due to Financial Institutions Abroad

Deposits

Total Shareholder’s Funds

Other

6.4 1.5 78.1 14

1

2

3

4

78.1%

14.0%6.4% 1.5%

Source: Central Bank of Swaziland

The increase in deposits was spread mainly between demand and term deposits. demand deposits grew by 35.4 percent to E5.0 billion while term deposits grew by 19.3 percent to E8.3 billion in June 2017. Savings deposits increased

by 10.9 percent to reach E917.9 million in June 2017. The interest paid on deposits increased from 2.5 percent to 3.0 percent in the year to June 2017.

Table 10: Banks’ Funding Concentration Level

Description Dec-14 Dec-15 Dec-16 Jun-17Average top 20 to total deposits 39.3% 36.6% 43.2% 45.8%Average top 10 to total deposits 29.1% 26.7% 34.0% 28.0%Average top 5 to total deposits 20.0% 17.8% 25.9% 19.7%

Source: Central Bank of Swaziland

FINANCIAL STABILITY REPORT I ssue No. 1 | CENTRAL BANK OF SWAZILAND

26 © 2017 Central Bank Of Swaziland

Figure 14: Structure of Deposits

-

1 000.0

2 000.0

3 000.0

4 000.0

5 000.0

6 000.0

7 000.0

8 000.0

9 000.0

-

1 000.0

2 000.0

3 000.0

4 000.0

5 000.0

6 000.0

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

E. Million

Demand Deposits Savings Deposits Time Deposits

Dec

-14

Dem

and

Dep

osit

s, E

’Bill

ion

Savi

ngs,

Tim

e

6.0 9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

-

5.0

4.0

3.0

2.0

Demand Deposits Savings Deposits Time Deposits

1.0

-

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar