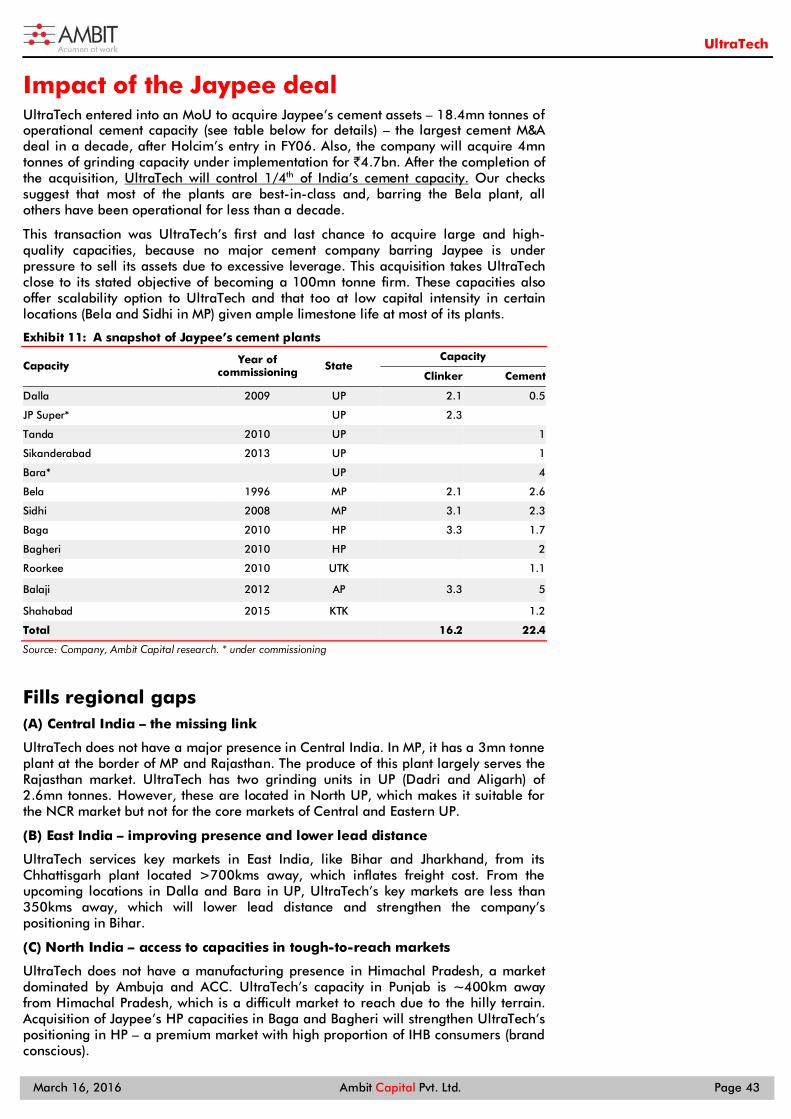

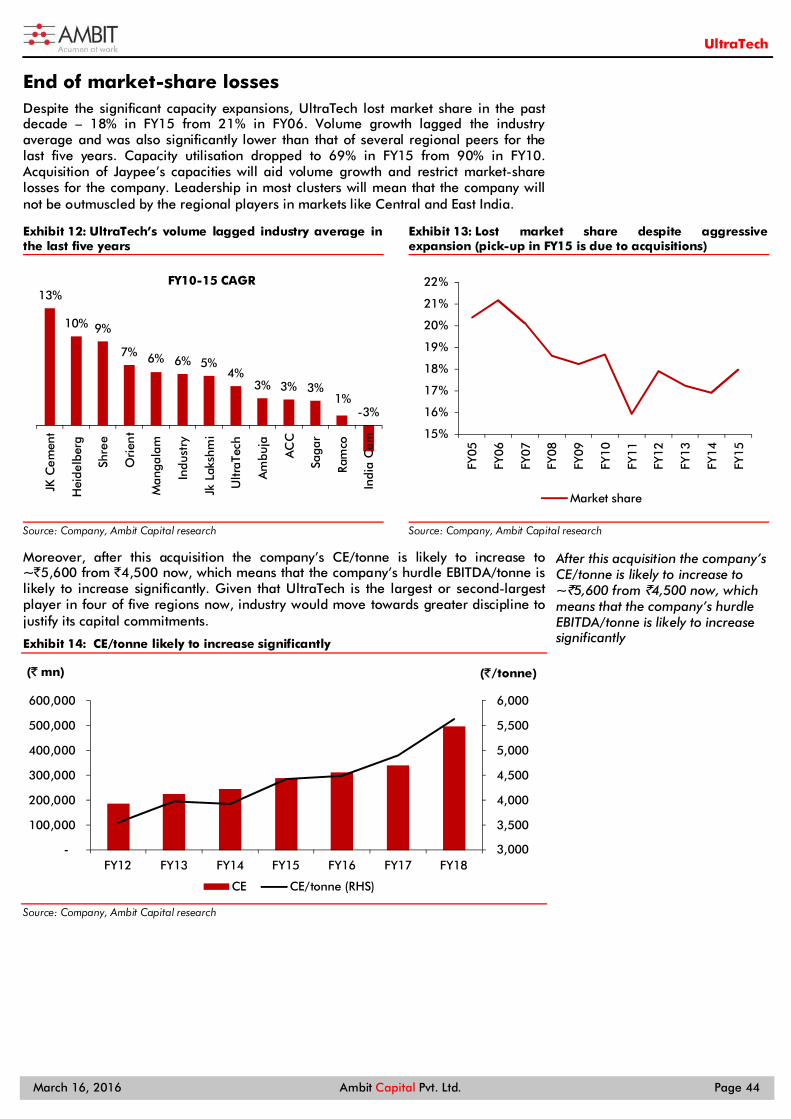

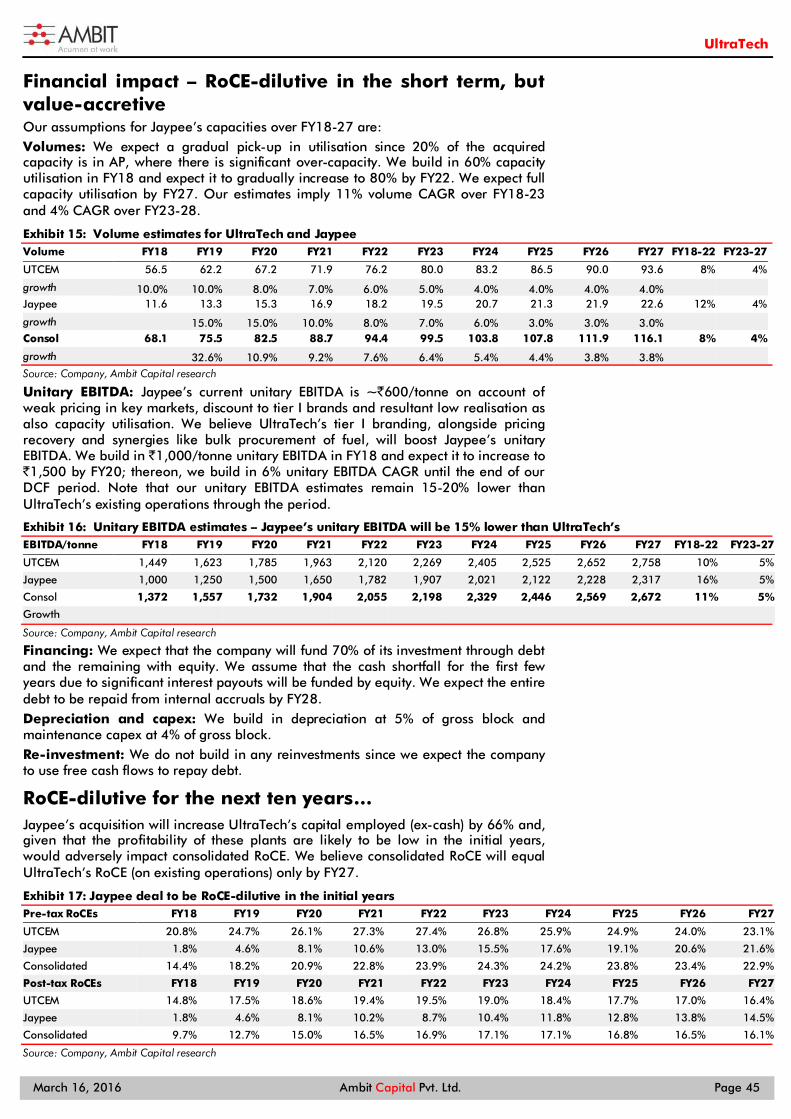

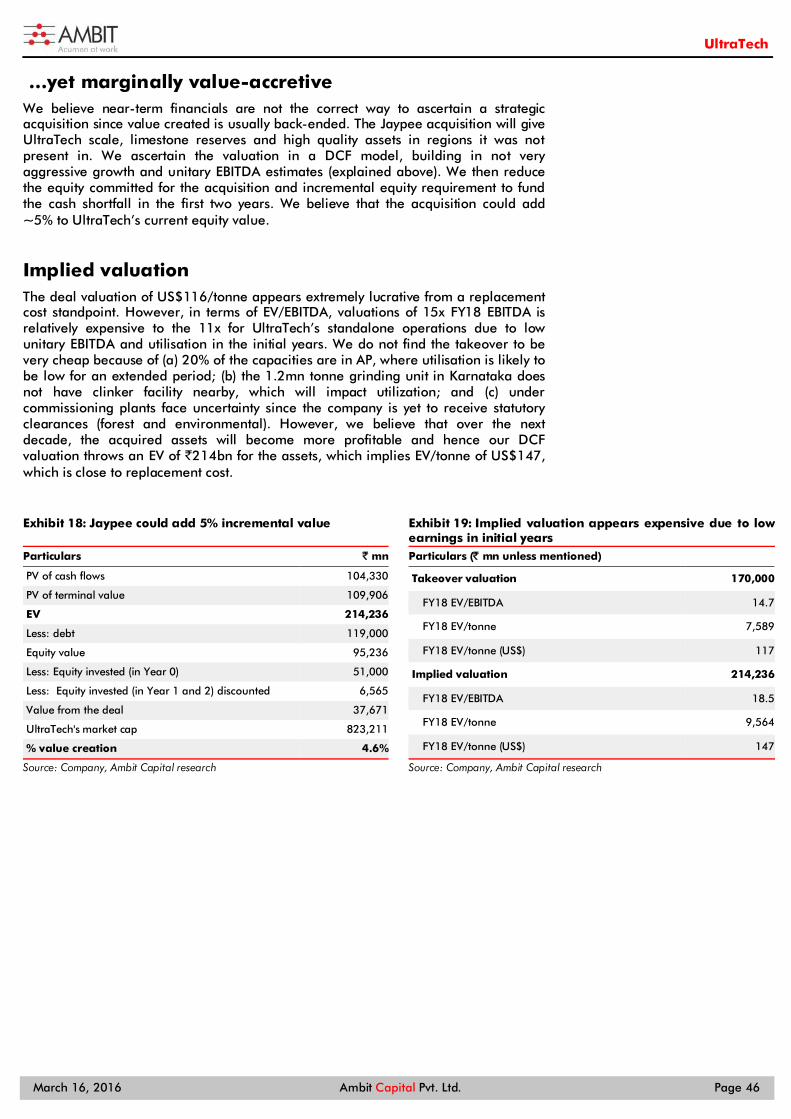

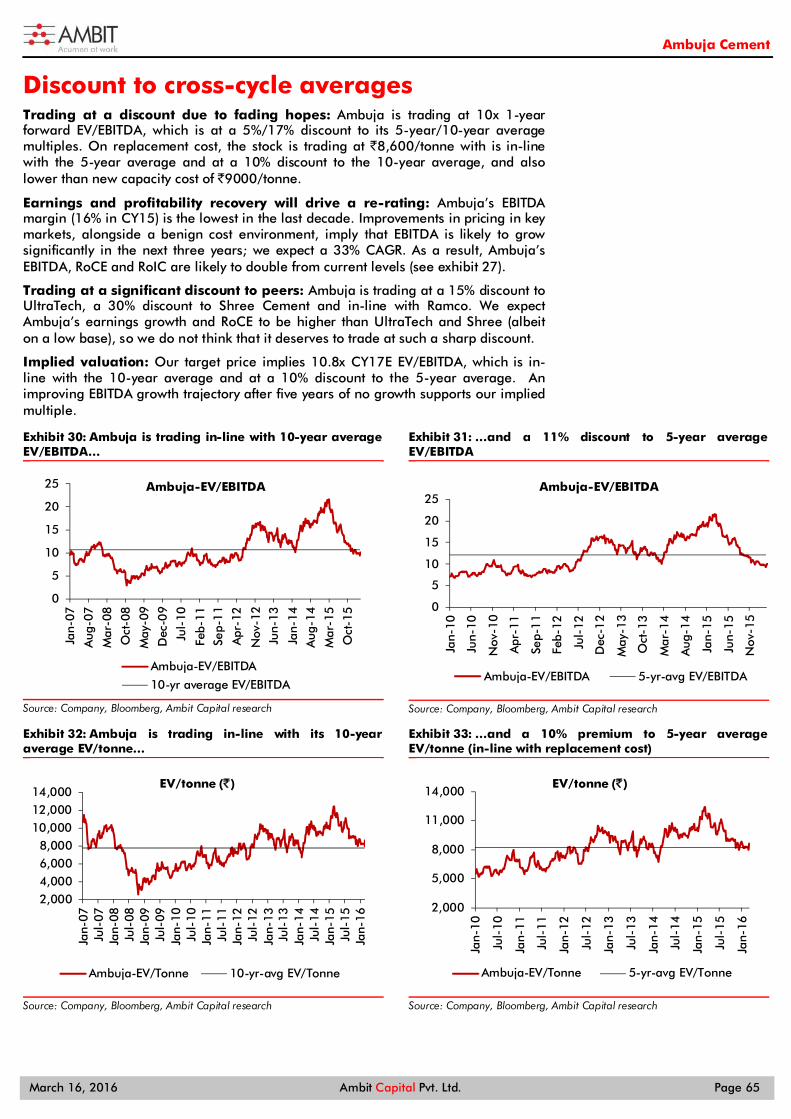

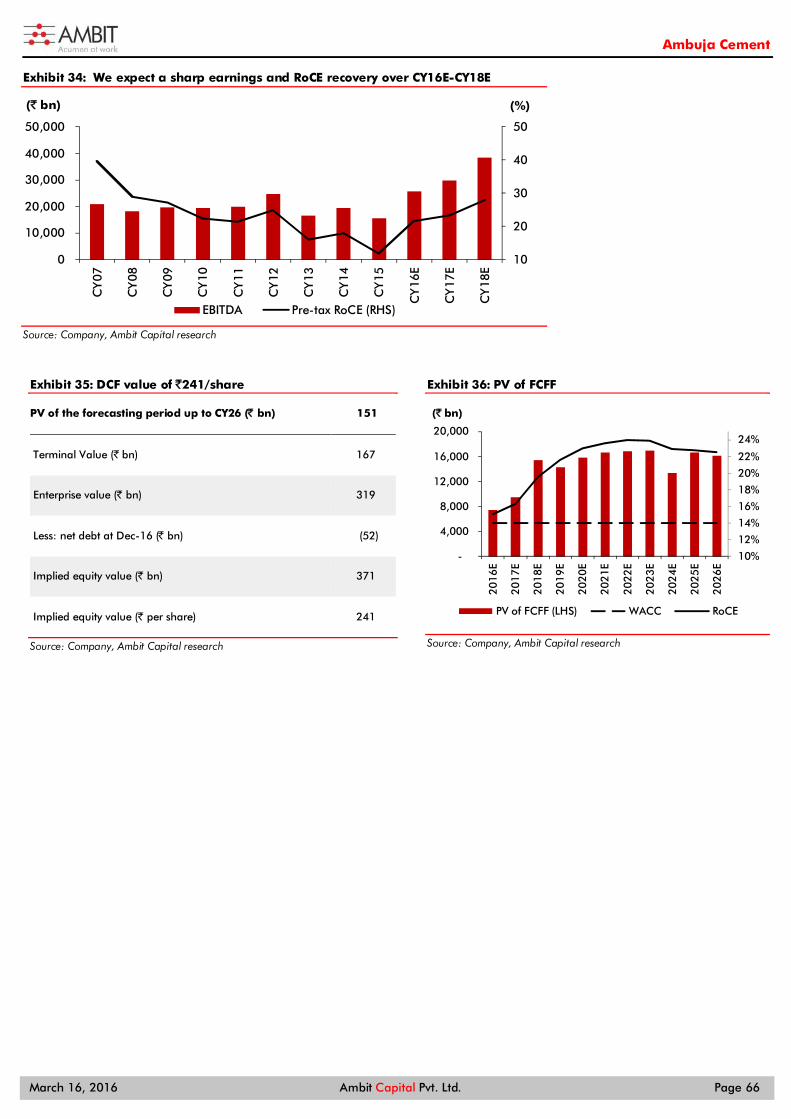

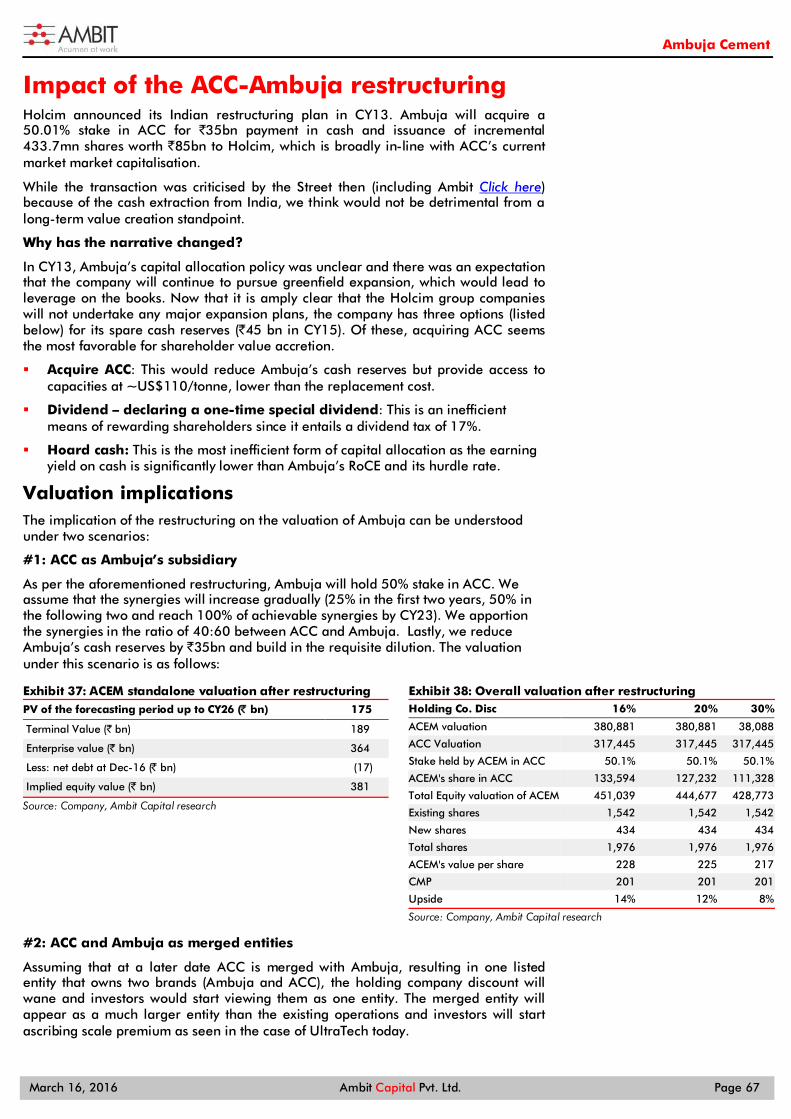

Embed Size (px)

Citation preview

CEMENT

Research Analysts:

End of the capex cycle!

Nitin [email protected]: +91 22 3043 3241

March 2016

Achint Bhagat, [email protected]: +91 22 3043 3178

Cement

March 17, 2016 Ambit Capital Pvt. Ltd. Page 2

CONTENTS

SECTOR

End of the capex!.…………………………………………………………………….. 3

Coverage summary …………………………………………………………………..4

Two decades of aggressive expansion …………………………………………….5

Understanding the last capex cycle ………………………………………………..6

How will the next 5year cycle be different? ……………………………………….9

Is the industry finally consolidating? ……………………………………………..13

Demand growth could retrace to 6-8% …………………………………………16

The retail consumer to the rescue 2.0 ……………………………………………18

Prices likely to recover from the lows …………………………………………….21

Costs – headwinds receding ……………………………………………………….22

End of the downgrade cycle ……………………………………………………….24

Ranking the cement peers …………………………………………………………30

Relative valuations …………………………………………………………………32

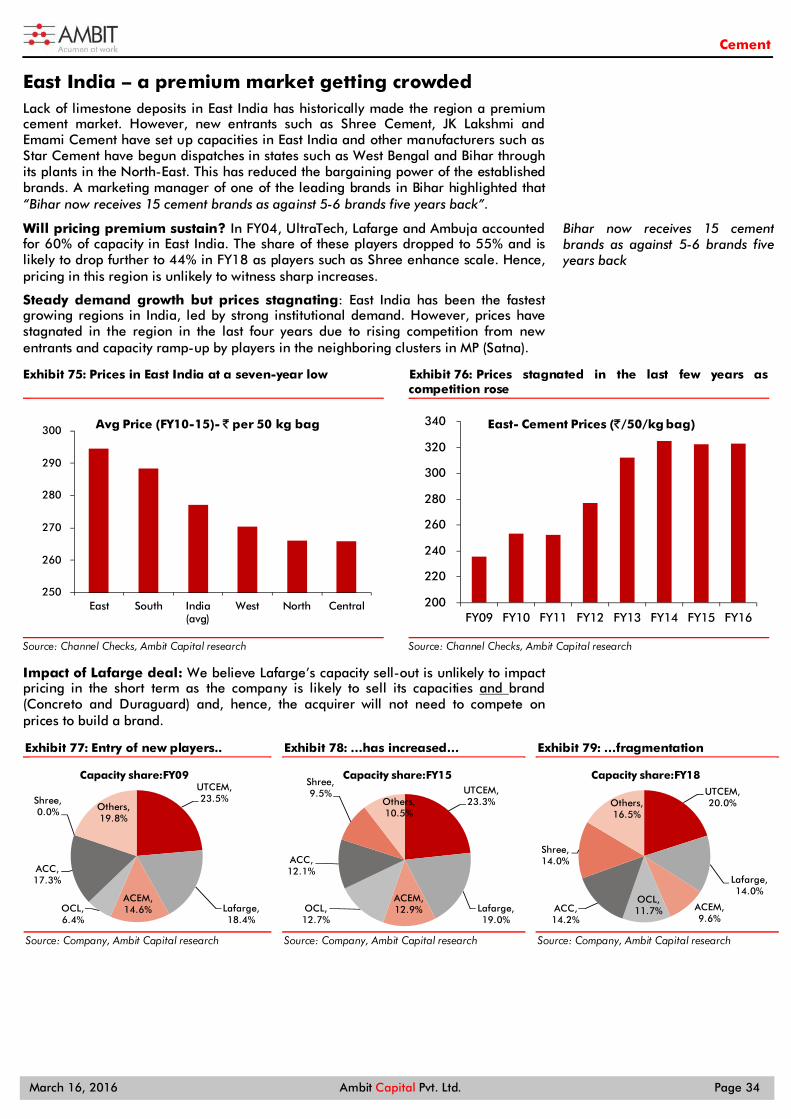

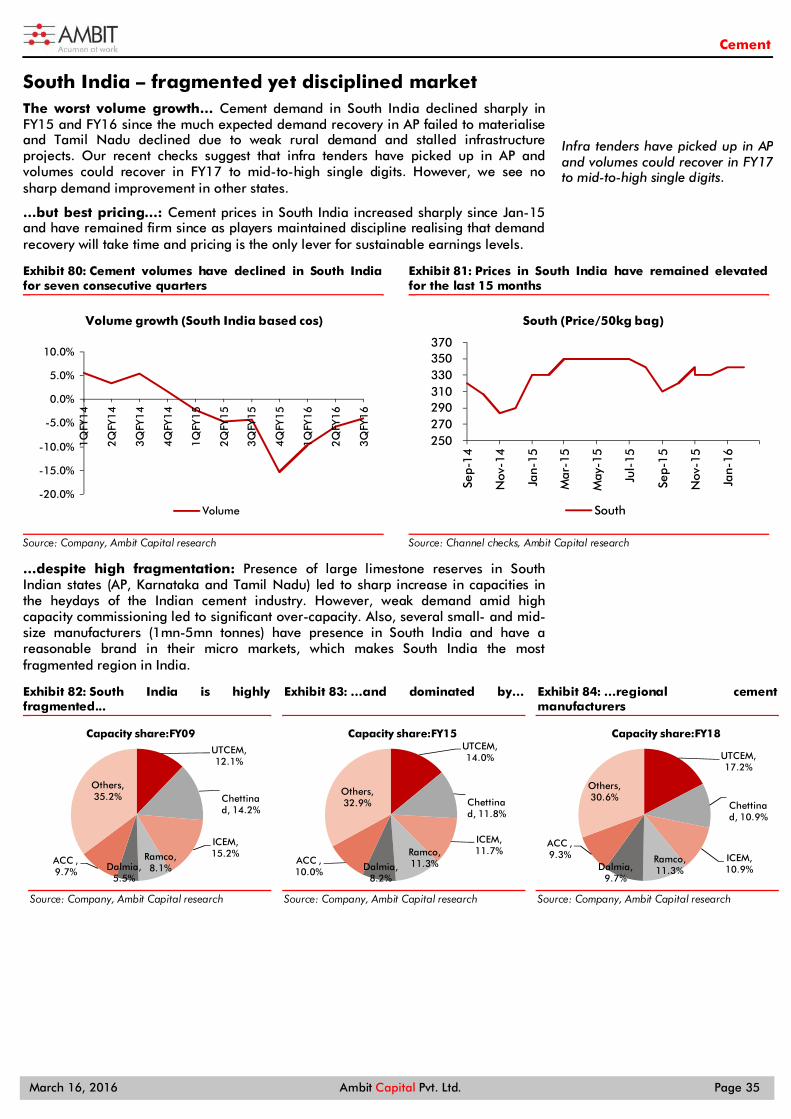

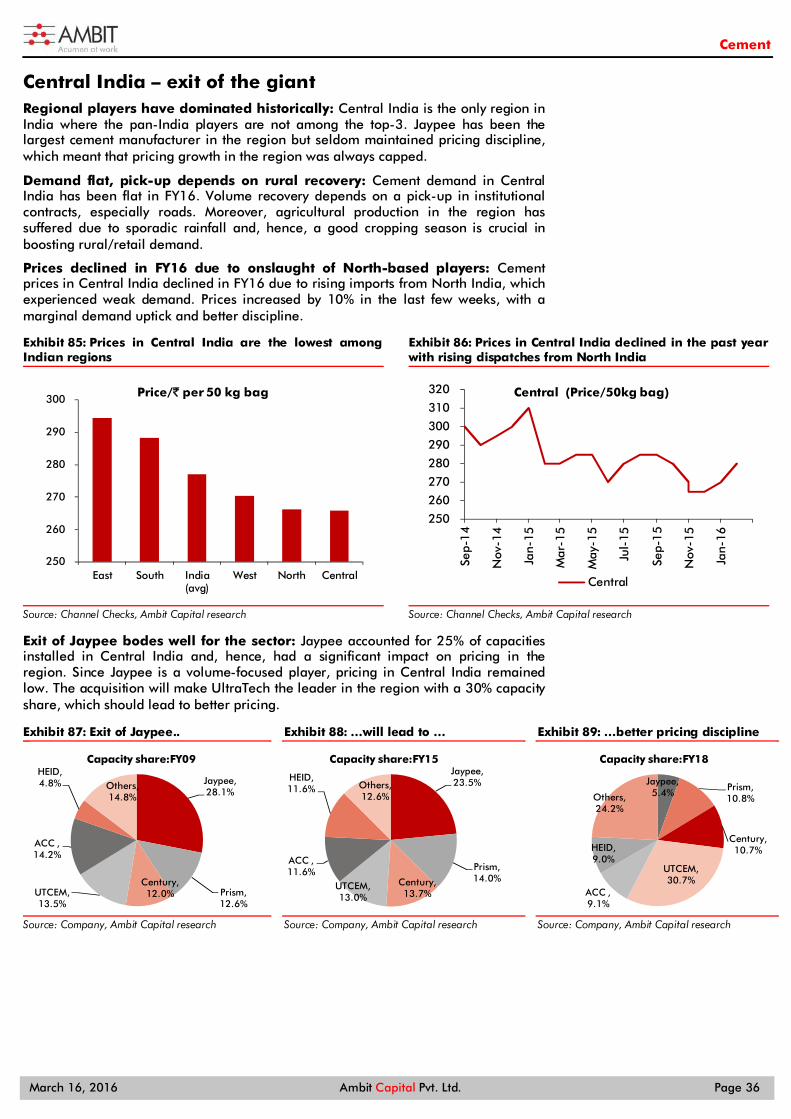

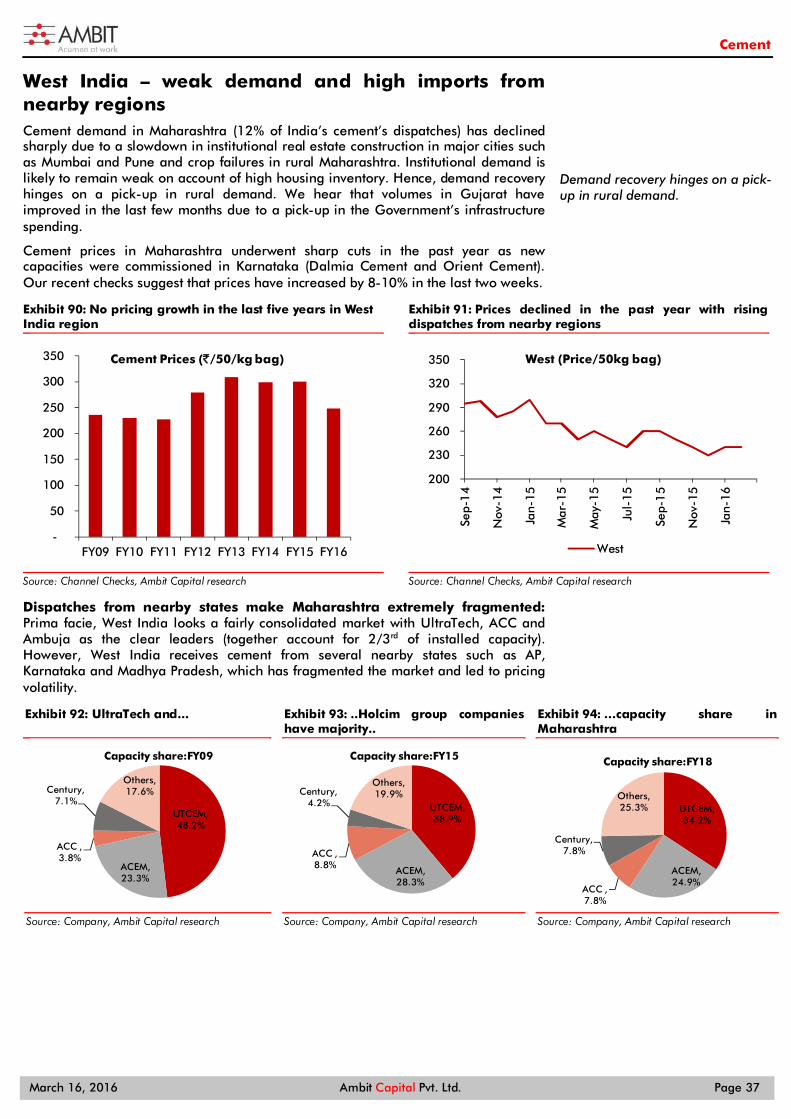

Regional dynamics ………………………………………………………………….33

COMPANIES

Ultratech Cement (BUY) ……………………………………………………………39

Ambuja Cement (BUY) ……………………………………………………………..55

ACC (BUY) ……………………………………………………………………………71

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

End of the capex cycle!

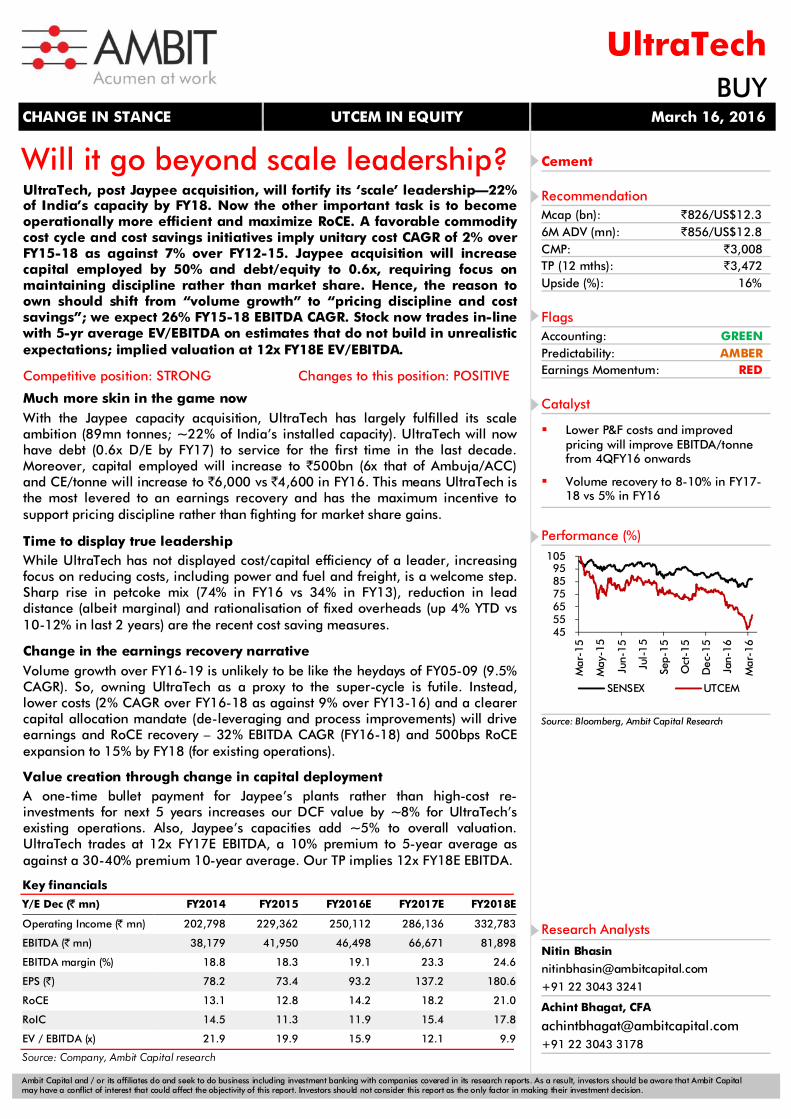

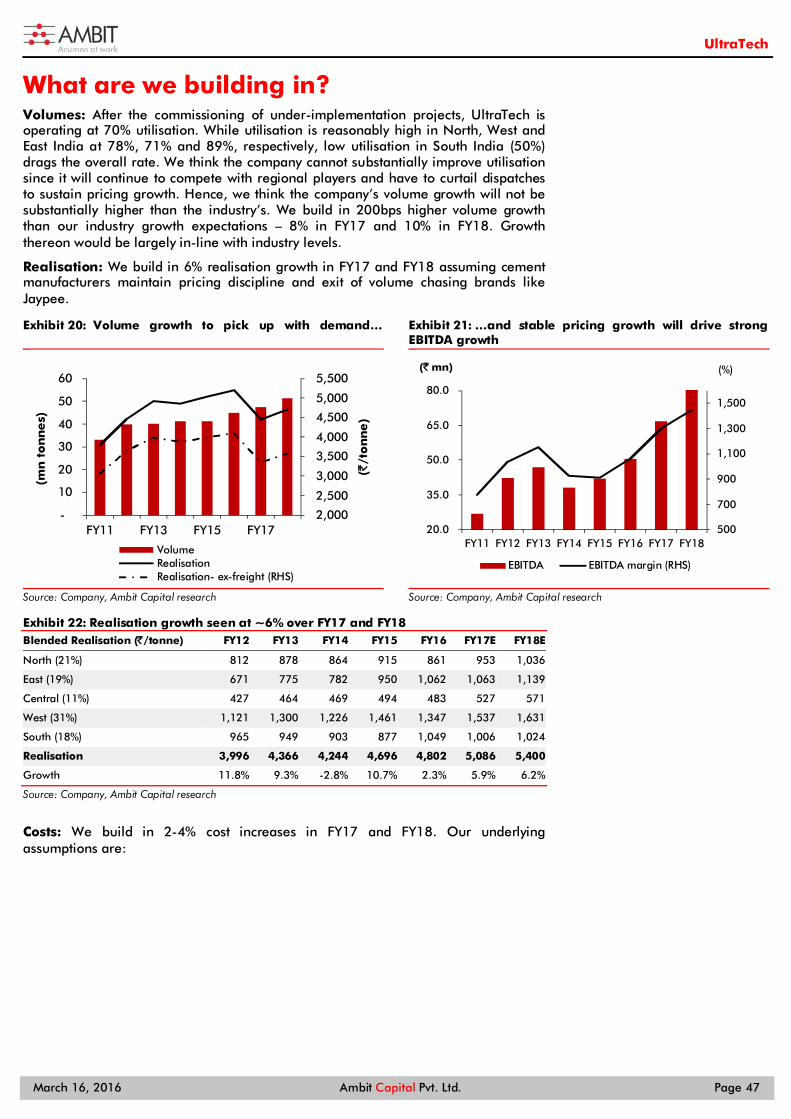

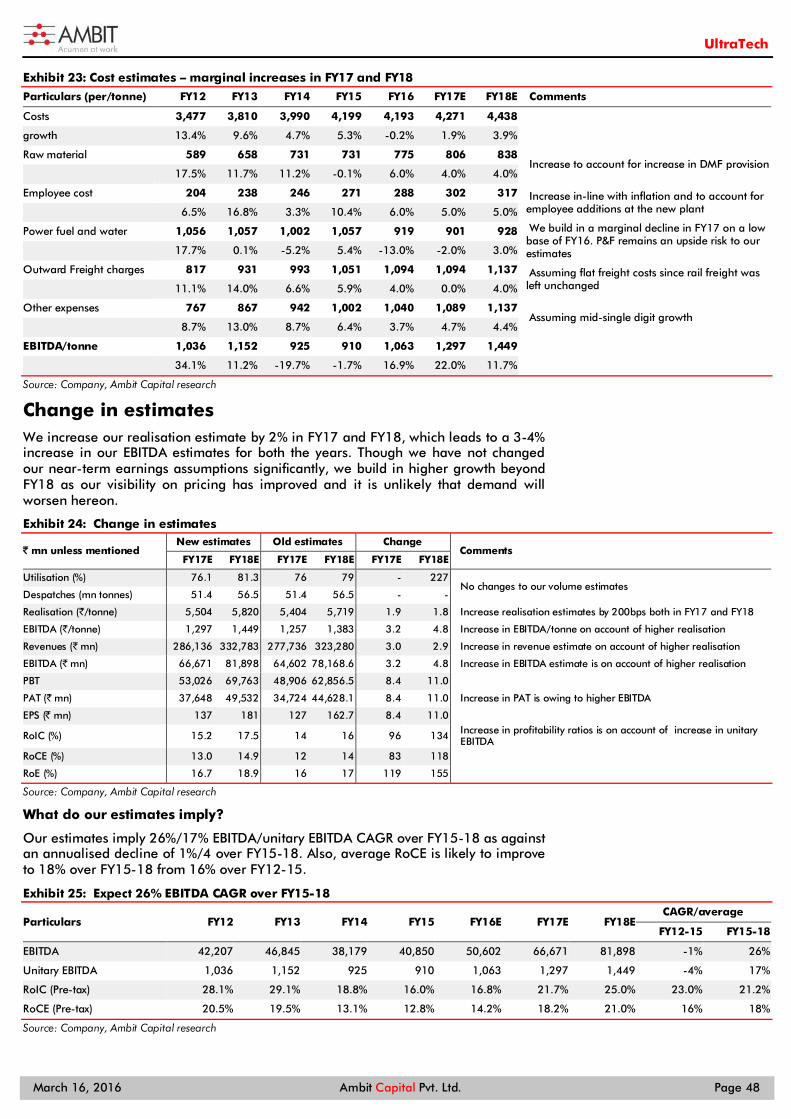

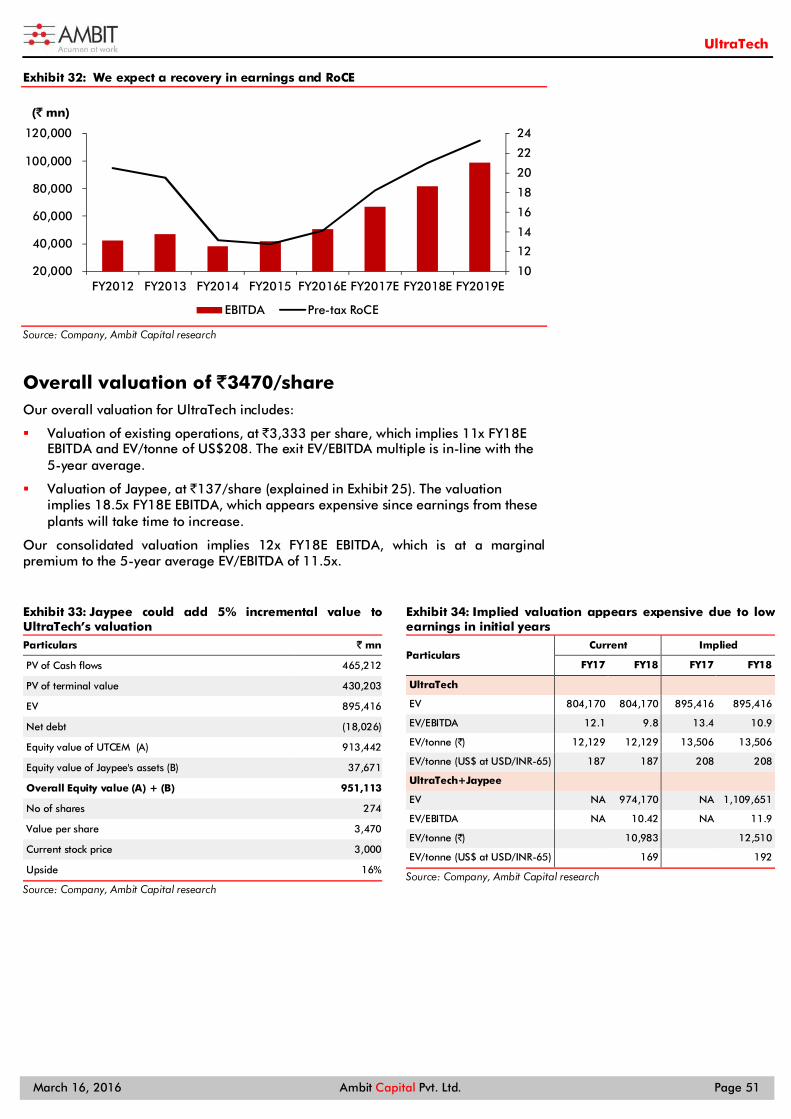

After 10 years of 100% CFO re-investment into capacity expansion, the Indian cement industry is likely to focus on a leaner balance sheet and ROCEs (at decadal lows in FY16) in the forthcoming years. Infrastructure-led super-cycle remains a distant dream and volume growth hinges on brand-conscious rural/retail consumers; government rural programmes to provide near-term impetus. UltraTech’s mega acquisition (5% of installed capacity) will reduce fragmentation/market share tussle that caused weak pricing in the past three years (1% CAGR over FY13-16). The less-favoured names – ACC and Ambuja – trade at relatively inexpensive valuations (10-10.5x CY16 EBITDA) and consensus estimates need upgrades to account for pricing and efficiency improvements. Narrative to own UltraTech should be increased focus on cost savings and clearer capital deployment road-map rather than a proxy play to the elusive demand super-cycle.

Changing priorities—RoCE for larger and deleveraging for smaller The last super-cycle (FY05-08) drove de-leveraging and strong FCF generation for the sector, followed by unbridled scale aspirations/capacity expansions (`120bn-140bn annual capex over FY07-15). The capex cycle is likely to end as the top-5 players (60% of capex over FY10-15) shift focus from scale to RoCE expansion and smaller players focus on FCF growth to reduce leverage. Sector RoCE/ EBITDA margins are 500/700bps lower than 15-year average. They should mean-revert by FY18 as capital employed stops increasing and margins expand due to efficiency initiatives (especially power and fuel and logistics) and discipline-led pricing improvement. One exit, multiple benefits Jaypee’s emergence as the third-largest cement group in India was a classic illustration of rising fragmentation – 10% capacity held by a volume-focused tier II brand gaining scale. Several small players added capacities and fought for market share, impacting pricing (1% CAGR over FY13-15, lowest in the past decade). UltraTech’s acquisition of Jaypee will not only reduce tier II competition in large markets of North, Central and East India but also reduce its greenfield capex (0.6X D/E). Rising challenges in securing limestone mines will fend off new competition and expansions by the smaller players. Will the wait end? Sector earnings to finally grow over FY16-18 After five years of no EBITDA growth (vs 36% CAGR over FY05-10), earnings of the sector should recover over FY16-18. While volume growth may hover at 6-8% (compared with hopes of 10-12%), pricing stability (6-7% CAGR) and lower costs (flat to 1-2% growth) will boost earnings growth. We expect 36% CAGR over FY16-18E for the six covered companies. Consensus estimates suffer from recency bias and display little predictive power; our FY17/FY18 EBITDA estimates are 10-25% higher than those of consensus.

Valuation – more rationality, less hopes Expensive valuations (30-50% premium over 5-year average) riding on high expectations were the reason for the sector’s underperformance (barring UTCEM/Shree) last year. Relatively inexpensive valuations (especially Ambuja and ACC; 0-15% premium to 5-year average EV/EBITDA), earnings/RoCE recovery from the trough, and lower expectations make cement a much better play now than in the past three years. Ambuja and ACC offer downside protection if status quo persists and significant upsides if earnings recover as per our expectations.

THEMATIC March 16, 2016

CementPOSITIVE

Key Recommendations

UltraTech BUY

Target Price: ̀ 3,473 Upside 16%

Ambuja Cement BUY

Target Price: ̀ 241 Upside: 18%

Shree Cement SELL

Target Price: ̀ 10,153 Downside: 10%

ACC BUY

Target Price: ̀ 1,515 Upside: 22%

Ramco Cement SELL

Target Price: `328 Downside: 16%

Orient Cement BUY

Target Price: ̀ 186 Upside: 39%

Rising consolidation after a decade

Source: Company, CMA, Ambit Capital research

57%

51%49% 55%

47%44% 38% 43%

30%35%40%45%50%55%60%

FY02

FY04

FY06

FY08

FY10

FY12

FY14

FY16E

Top-5 groups Top-3 groups

Research Analyst Details

Nitin Bhasin

+91 22 3043 3241

Achint Bhagat, CFA

+91 22 3043 3178

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 4

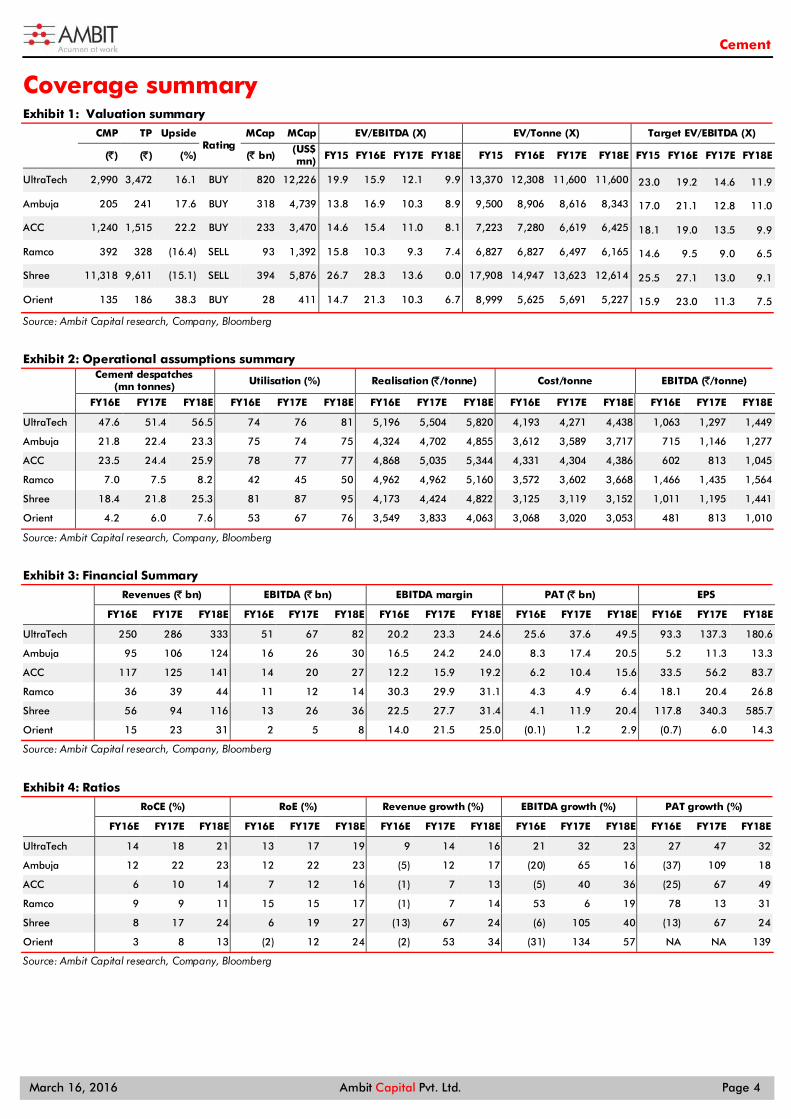

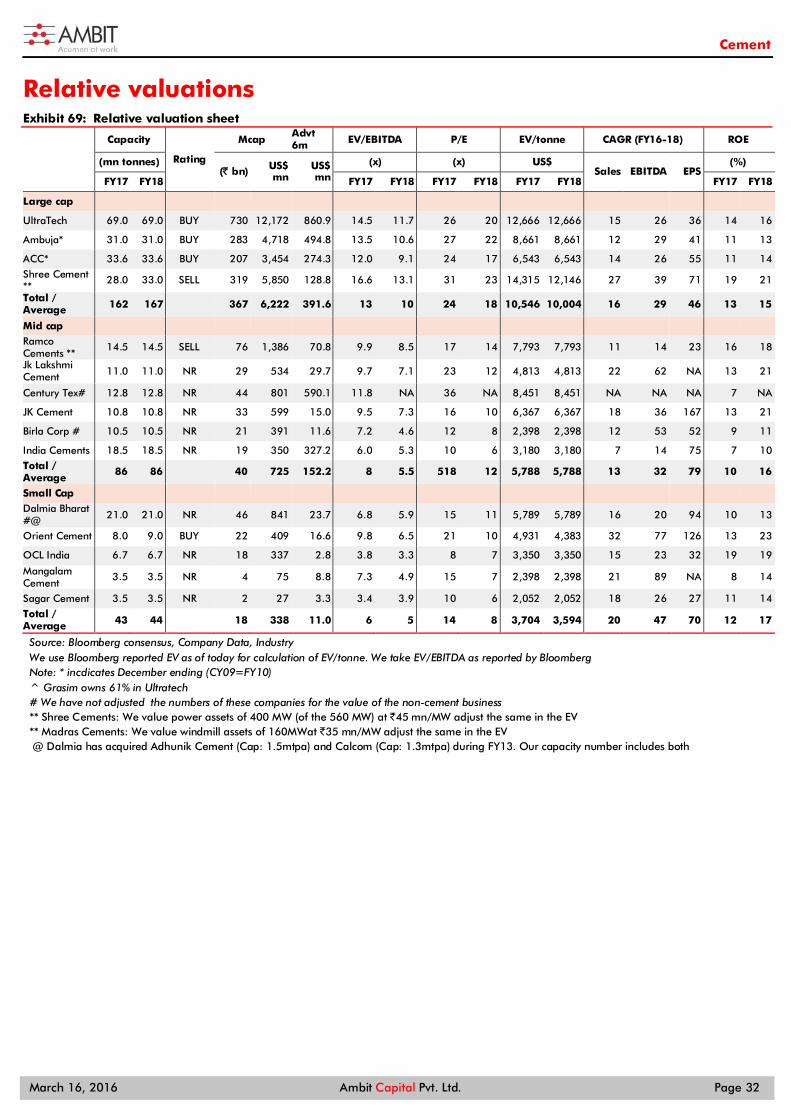

Coverage summary Valuation summary Exhibit 1:

CMP TP Upside Rating

MCap MCap EV/EBITDA (X) EV/Tonne (X) Target EV/EBITDA (X)

(`) (`) (%) (` bn) (US$ mn) FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

UltraTech 2,990 3,472 16.1 BUY 820 12,226 19.9 15.9 12.1 9.9 13,370 12,308 11,600 11,600 23.0 19.2 14.6 11.9

Ambuja 205 241 17.6 BUY 318 4,739 13.8 16.9 10.3 8.9 9,500 8,906 8,616 8,343 17.0 21.1 12.8 11.0

ACC 1,240 1,515 22.2 BUY 233 3,470 14.6 15.4 11.0 8.1 7,223 7,280 6,619 6,425 18.1 19.0 13.5 9.9

Ramco 392 328 (16.4) SELL 93 1,392 15.8 10.3 9.3 7.4 6,827 6,827 6,497 6,165 14.6 9.5 9.0 6.5

Shree 11,318 9,611 (15.1) SELL 394 5,876 26.7 28.3 13.6 0.0 17,908 14,947 13,623 12,614 25.5 27.1 13.0 9.1

Orient 135 186 38.3 BUY 28 411 14.7 21.3 10.3 6.7 8,999 5,625 5,691 5,227 15.9 23.0 11.3 7.5

Source: Ambit Capital research, Company, Bloomberg

Operational assumptions summary Exhibit 2:

Cement despatches (mn tonnes) Utilisation (%) Realisation (`/tonne) Cost/tonne EBITDA (`/tonne)

FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

UltraTech 47.6 51.4 56.5 74 76 81 5,196 5,504 5,820 4,193 4,271 4,438 1,063 1,297 1,449

Ambuja 21.8 22.4 23.3 75 74 75 4,324 4,702 4,855 3,612 3,589 3,717 715 1,146 1,277

ACC 23.5 24.4 25.9 78 77 77 4,868 5,035 5,344 4,331 4,304 4,386 602 813 1,045

Ramco 7.0 7.5 8.2 42 45 50 4,962 4,962 5,160 3,572 3,602 3,668 1,466 1,435 1,564

Shree 18.4 21.8 25.3 81 87 95 4,173 4,424 4,822 3,125 3,119 3,152 1,011 1,195 1,441

Orient 4.2 6.0 7.6 53 67 76 3,549 3,833 4,063 3,068 3,020 3,053 481 813 1,010

Source: Ambit Capital research, Company, Bloomberg

Financial Summary Exhibit 3:

Revenues (` bn) EBITDA (` bn) EBITDA margin PAT (` bn) EPS

FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

UltraTech 250 286 333 51 67 82 20.2 23.3 24.6 25.6 37.6 49.5 93.3 137.3 180.6

Ambuja 95 106 124 16 26 30 16.5 24.2 24.0 8.3 17.4 20.5 5.2 11.3 13.3

ACC 117 125 141 14 20 27 12.2 15.9 19.2 6.2 10.4 15.6 33.5 56.2 83.7

Ramco 36 39 44 11 12 14 30.3 29.9 31.1 4.3 4.9 6.4 18.1 20.4 26.8

Shree 56 94 116 13 26 36 22.5 27.7 31.4 4.1 11.9 20.4 117.8 340.3 585.7

Orient 15 23 31 2 5 8 14.0 21.5 25.0 (0.1) 1.2 2.9 (0.7) 6.0 14.3

Source: Ambit Capital research, Company, Bloomberg

Ratios Exhibit 4:

RoCE (%) RoE (%) Revenue growth (%) EBITDA growth (%) PAT growth (%)

FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

UltraTech 14 18 21 13 17 19 9 14 16 21 32 23 27 47 32

Ambuja 12 22 23 12 22 23 (5) 12 17 (20) 65 16 (37) 109 18

ACC 6 10 14 7 12 16 (1) 7 13 (5) 40 36 (25) 67 49

Ramco 9 9 11 15 15 17 (1) 7 14 53 6 19 78 13 31

Shree 8 17 24 6 19 27 (13) 67 24 (6) 105 40 (13) 67 24

Orient 3 8 13 (2) 12 24 (2) 53 34 (31) 134 57 NA NA 139

Source: Ambit Capital research, Company, Bloomberg

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 5

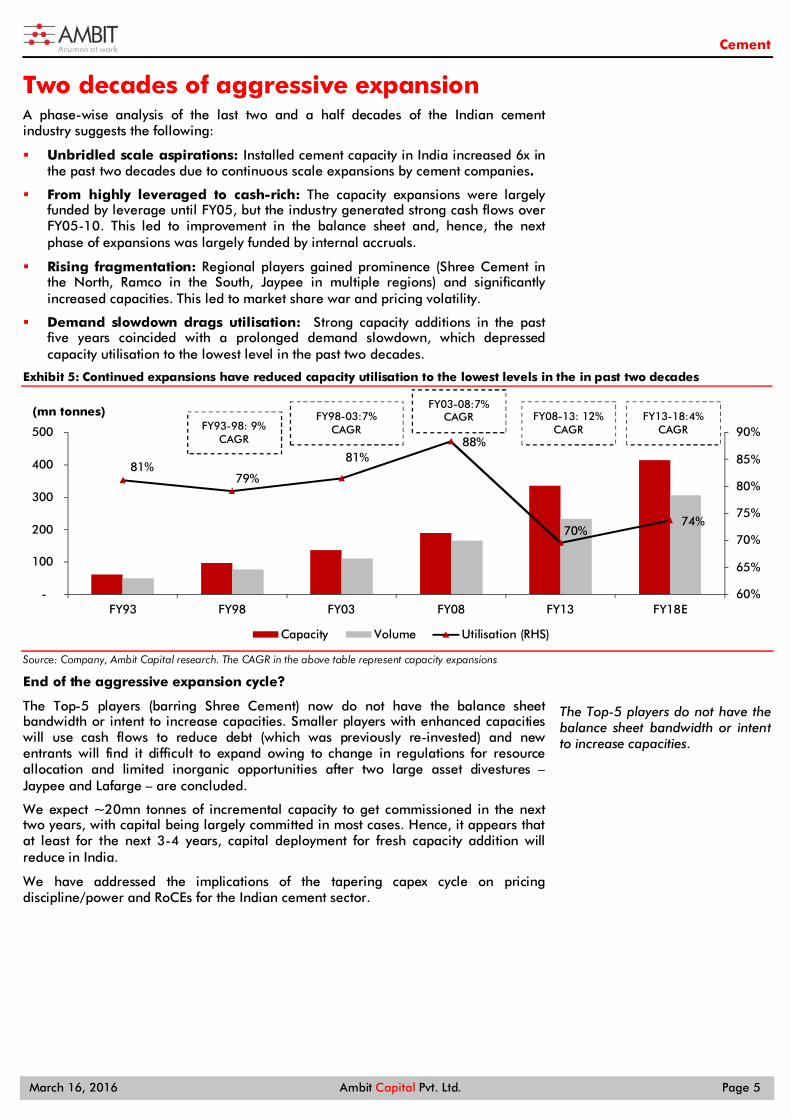

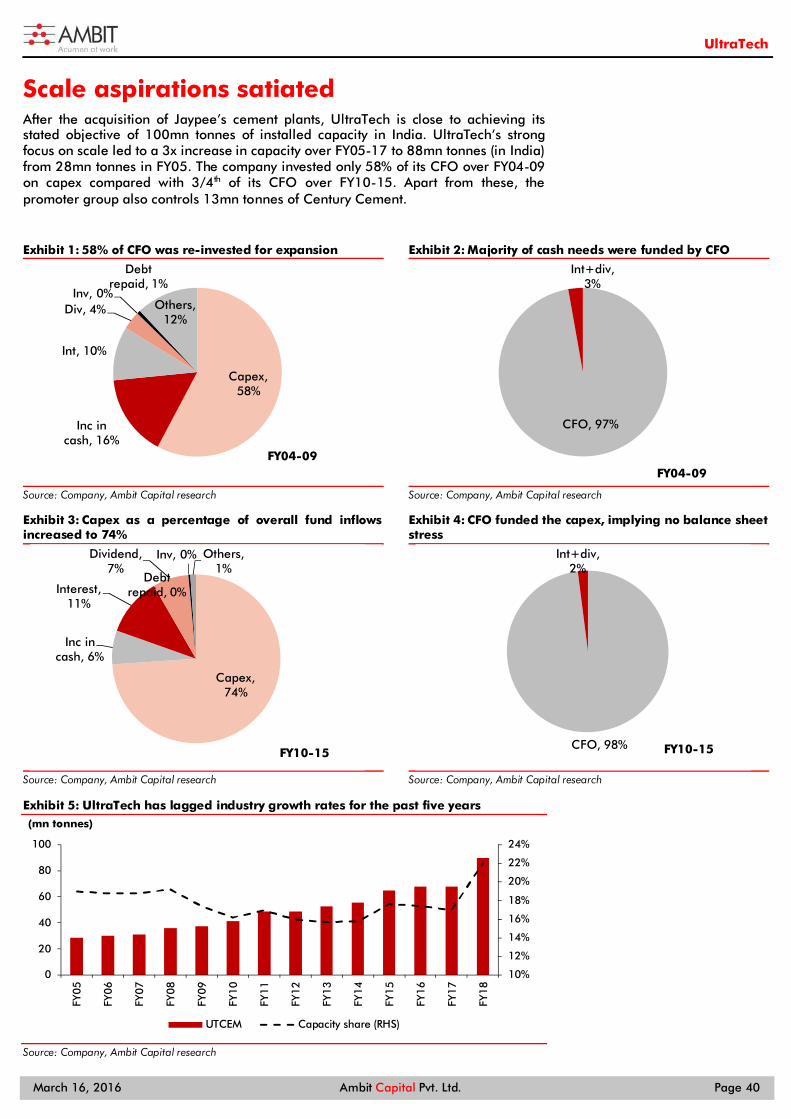

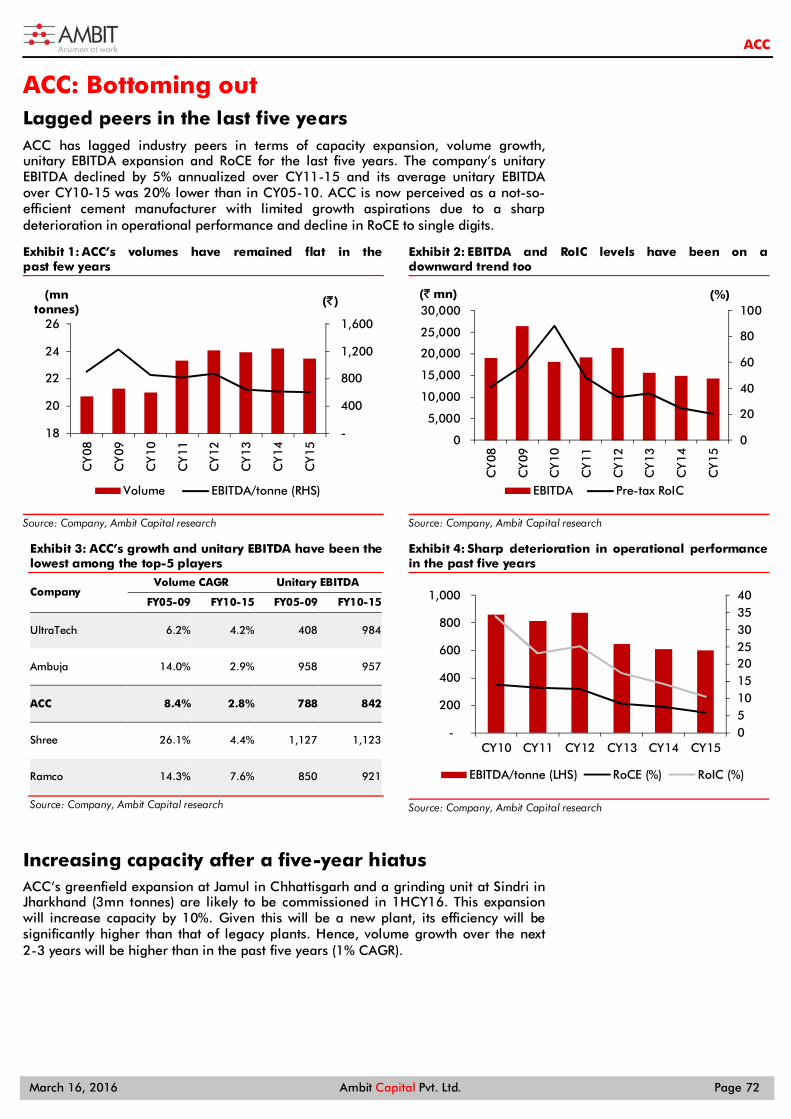

Two decades of aggressive expansion A phase-wise analysis of the last two and a half decades of the Indian cement industry suggests the following:

Unbridled scale aspirations: Installed cement capacity in India increased 6x in the past two decades due to continuous scale expansions by cement companies.

From highly leveraged to cash-rich: The capacity expansions were largely funded by leverage until FY05, but the industry generated strong cash flows over FY05-10. This led to improvement in the balance sheet and, hence, the next phase of expansions was largely funded by internal accruals.

Rising fragmentation: Regional players gained prominence (Shree Cement in the North, Ramco in the South, Jaypee in multiple regions) and significantly increased capacities. This led to market share war and pricing volatility.

Demand slowdown drags utilisation: Strong capacity additions in the past five years coincided with a prolonged demand slowdown, which depressed capacity utilisation to the lowest level in the past two decades.

Continued expansions have reduced capacity utilisation to the lowest levels in the in past two decades Exhibit 5:

Source: Company, Ambit Capital research. The CAGR in the above table represent capacity expansions

End of the aggressive expansion cycle?

The Top-5 players (barring Shree Cement) now do not have the balance sheet bandwidth or intent to increase capacities. Smaller players with enhanced capacities will use cash flows to reduce debt (which was previously re-invested) and new entrants will find it difficult to expand owing to change in regulations for resource allocation and limited inorganic opportunities after two large asset divestures – Jaypee and Lafarge – are concluded.

We expect ~20mn tonnes of incremental capacity to get commissioned in the next two years, with capital being largely committed in most cases. Hence, it appears that at least for the next 3-4 years, capital deployment for fresh capacity addition will reduce in India.

We have addressed the implications of the tapering capex cycle on pricing discipline/power and RoCEs for the Indian cement sector.

81%79%

81%88%

70%74%

60%

65%

70%

75%

80%

85%

90%

-

100

200

300

400

500

FY93 FY98 FY03 FY08 FY13 FY18E

(mn tonnes)

Capacity Volume Utilisation (RHS)

The Top-5 players do not have the balance sheet bandwidth or intent to increase capacities.

FY93-98: 9% CAGR

FY98-03:7% CAGR

FY03-08:7% CAGR FY08-13: 12%

CAGR FY13-18:4%

CAGR

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 6

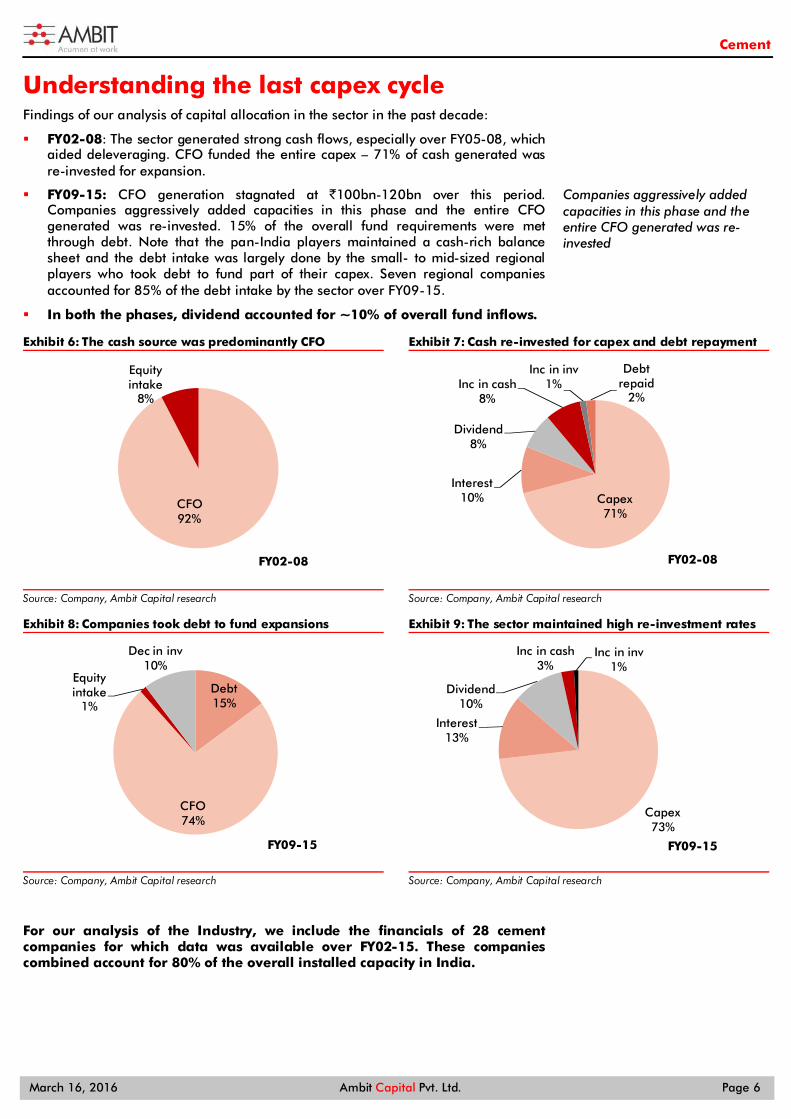

Understanding the last capex cycle Findings of our analysis of capital allocation in the sector in the past decade:

FY02-08: The sector generated strong cash flows, especially over FY05-08, which aided deleveraging. CFO funded the entire capex – 71% of cash generated was re-invested for expansion.

FY09-15: CFO generation stagnated at `100bn-120bn over this period. Companies aggressively added capacities in this phase and the entire CFO generated was re-invested. 15% of the overall fund requirements were met through debt. Note that the pan-India players maintained a cash-rich balance sheet and the debt intake was largely done by the small- to mid-sized regional players who took debt to fund part of their capex. Seven regional companies accounted for 85% of the debt intake by the sector over FY09-15.

In both the phases, dividend accounted for ~10% of overall fund inflows.

The cash source was predominantly CFO Exhibit 6:

Source: Company, Ambit Capital research

Cash re-invested for capex and debt repayment Exhibit 7:

Source: Company, Ambit Capital research

Companies took debt to fund expansions Exhibit 8:

Source: Company, Ambit Capital research

The sector maintained high re-investment rates Exhibit 9:

Source: Company, Ambit Capital research

For our analysis of the Industry, we include the financials of 28 cement companies for which data was available over FY02-15. These companies combined account for 80% of the overall installed capacity in India.

CFO92%

Equity intake

8%

FY02-08

Capex71%

Interest10%

Dividend8%

Inc in cash8%

Inc in inv1%

Debt repaid

2%

FY02-08

Debt15%

CFO74%

Equity intake

1%

Dec in inv10%

FY09-15

Capex73%

Interest13%

Dividend10%

Inc in cash3%

Inc in inv1%

FY09-15

Companies aggressively added capacities in this phase and the entire CFO generated was re-invested

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 7

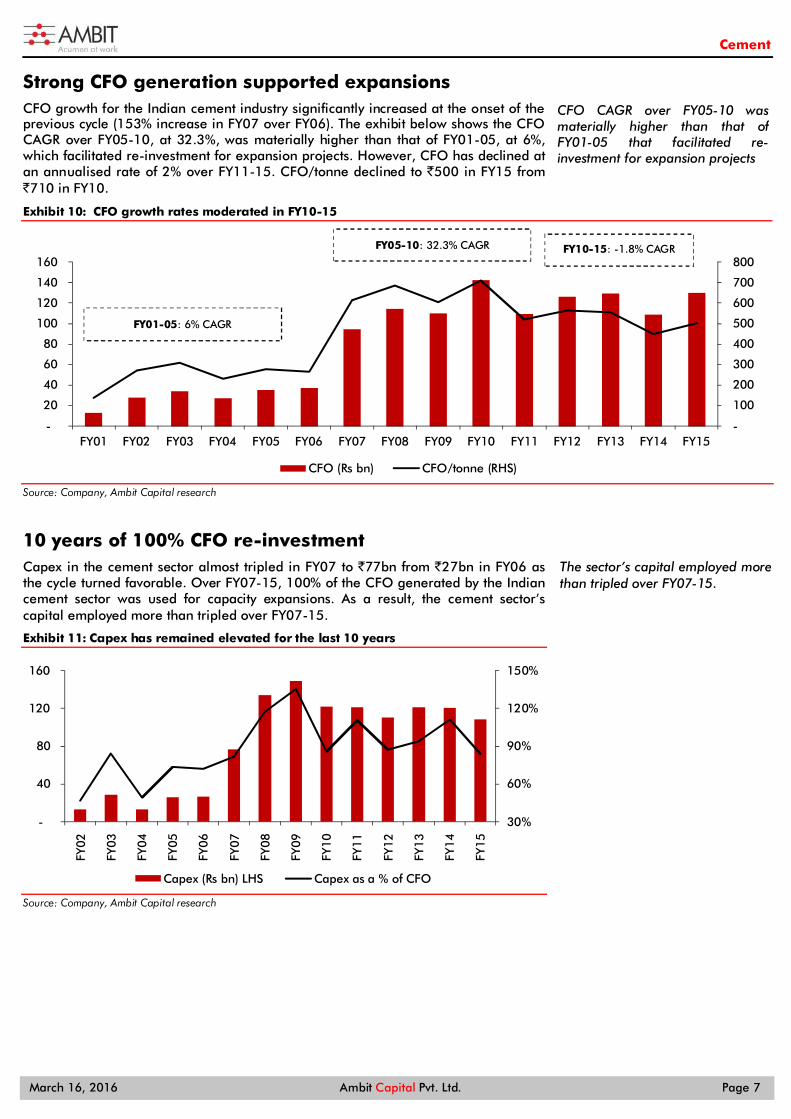

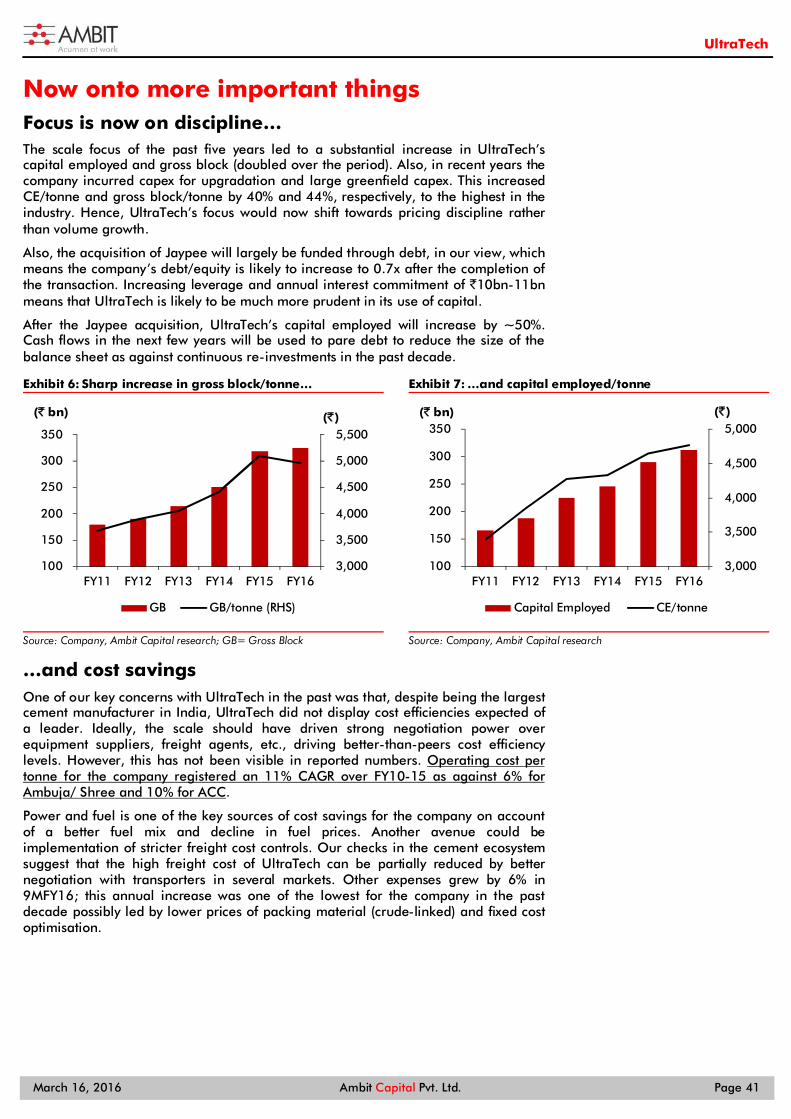

Strong CFO generation supported expansions CFO growth for the Indian cement industry significantly increased at the onset of the previous cycle (153% increase in FY07 over FY06). The exhibit below shows the CFO CAGR over FY05-10, at 32.3%, was materially higher than that of FY01-05, at 6%, which facilitated re-investment for expansion projects. However, CFO has declined at an annualised rate of 2% over FY11-15. CFO/tonne declined to `500 in FY15 from `710 in FY10.

CFO growth rates moderated in FY10-15 Exhibit 10:

Source: Company, Ambit Capital research

10 years of 100% CFO re-investment Capex in the cement sector almost tripled in FY07 to `77bn from `27bn in FY06 as the cycle turned favorable. Over FY07-15, 100% of the CFO generated by the Indian cement sector was used for capacity expansions. As a result, the cement sector’s capital employed more than tripled over FY07-15.

Capex has remained elevated for the last 10 years Exhibit 11:

Source: Company, Ambit Capital research

-

100

200

300

400

500

600

700

800

-

20

40

60

80

100

120

140

160

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

CFO (Rs bn) CFO/tonne (RHS)

30%

60%

90%

120%

150%

-

40

80

120

160

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

Capex (Rs bn) LHS Capex as a % of CFO

CFO CAGR over FY05-10 was materially higher than that of FY01-05 that facilitated re-investment for expansion projects

The sector’s capital employed more than tripled over FY07-15.

FY01-05: 6% CAGR

FY05-10: 32.3% CAGR FY10-15: -1.8% CAGR

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 8

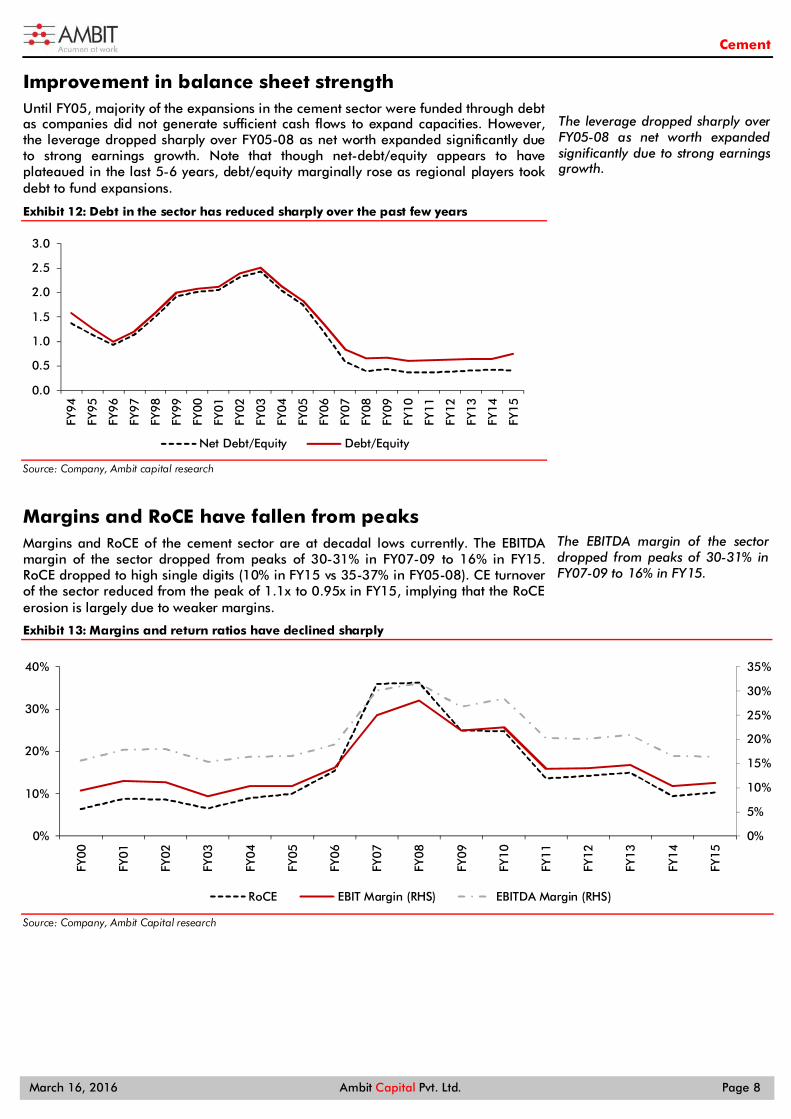

Improvement in balance sheet strength Until FY05, majority of the expansions in the cement sector were funded through debt as companies did not generate sufficient cash flows to expand capacities. However, the leverage dropped sharply over FY05-08 as net worth expanded significantly due to strong earnings growth. Note that though net-debt/equity appears to have plateaued in the last 5-6 years, debt/equity marginally rose as regional players took debt to fund expansions.

Debt in the sector has reduced sharply over the past few years Exhibit 12:

Source: Company, Ambit capital research

Margins and RoCE have fallen from peaks Margins and RoCE of the cement sector are at decadal lows currently. The EBITDA margin of the sector dropped from peaks of 30-31% in FY07-09 to 16% in FY15. RoCE dropped to high single digits (10% in FY15 vs 35-37% in FY05-08). CE turnover of the sector reduced from the peak of 1.1x to 0.95x in FY15, implying that the RoCE erosion is largely due to weaker margins.

Margins and return ratios have declined sharply Exhibit 13:

Source: Company, Ambit Capital research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Net Debt/Equity Debt/Equity

0%

5%

10%

15%

20%

25%

30%

35%

0%

10%

20%

30%

40%

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

RoCE EBIT Margin (RHS) EBITDA Margin (RHS)

The leverage dropped sharply over FY05-08 as net worth expanded significantly due to strong earnings growth.

The EBITDA margin of the sector dropped from peaks of 30-31% in FY07-09 to 16% in FY15.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 9

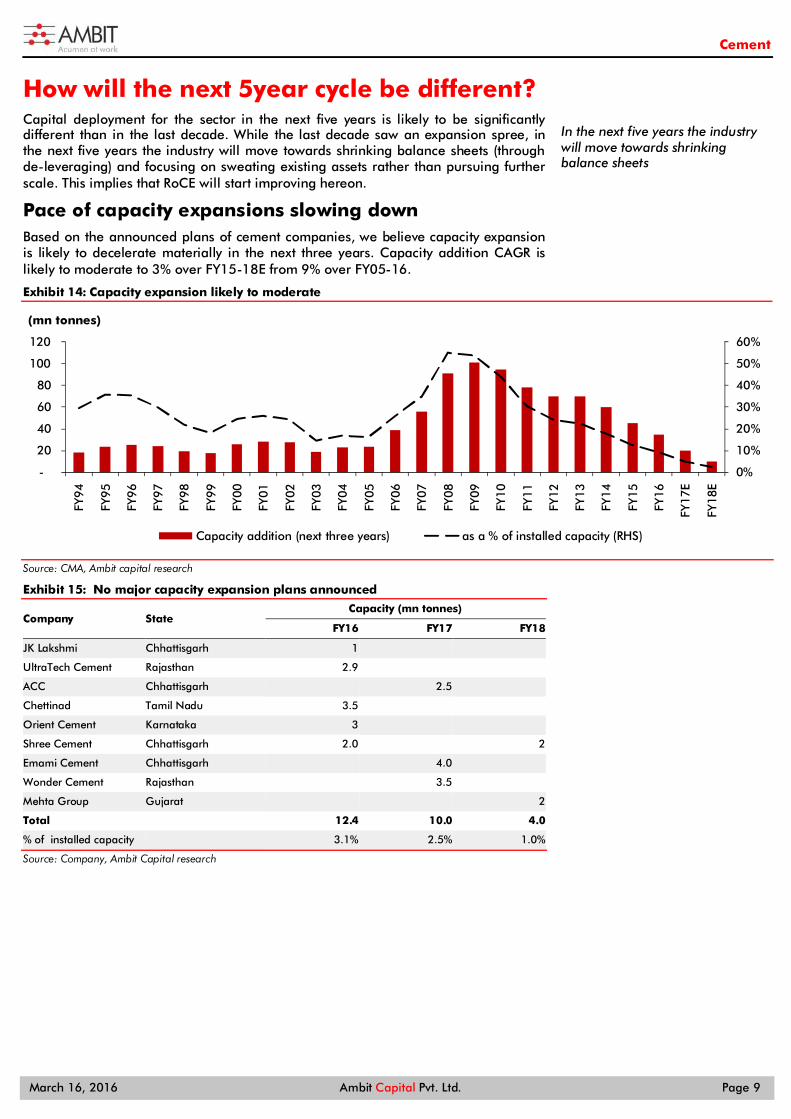

How will the next 5year cycle be different? Capital deployment for the sector in the next five years is likely to be significantly different than in the last decade. While the last decade saw an expansion spree, in the next five years the industry will move towards shrinking balance sheets (through de-leveraging) and focusing on sweating existing assets rather than pursuing further scale. This implies that RoCE will start improving hereon.

Pace of capacity expansions slowing down Based on the announced plans of cement companies, we believe capacity expansion is likely to decelerate materially in the next three years. Capacity addition CAGR is likely to moderate to 3% over FY15-18E from 9% over FY05-16.

Capacity expansion likely to moderate Exhibit 14:

Source: CMA, Ambit capital research

No major capacity expansion plans announced Exhibit 15:

Company State Capacity (mn tonnes)

FY16 FY17 FY18

JK Lakshmi Chhattisgarh 1 UltraTech Cement Rajasthan 2.9 ACC Chhattisgarh 2.5 Chettinad Tamil Nadu 3.5 Orient Cement Karnataka 3 Shree Cement Chhattisgarh 2.0 2

Emami Cement Chhattisgarh 4.0 Wonder Cement Rajasthan 3.5 Mehta Group Gujarat 2

Total 12.4 10.0 4.0

% of installed capacity 3.1% 2.5% 1.0%

Source: Company, Ambit Capital research

0%

10%

20%

30%

40%

50%

60%

-

20

40

60

80

100

120

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7E

FY1

8E

(mn tonnes)

Capacity addition (next three years) as a % of installed capacity (RHS)

In the next five years the industry will move towards shrinking balance sheets

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 10

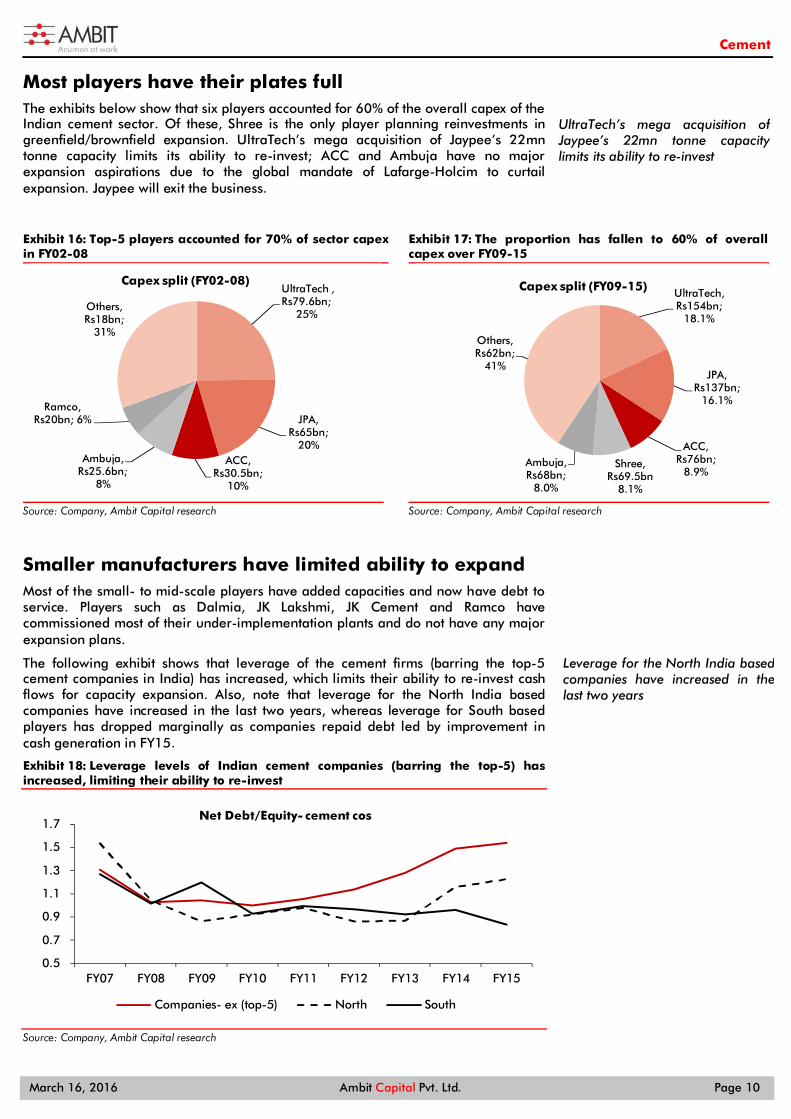

Most players have their plates full The exhibits below show that six players accounted for 60% of the overall capex of the Indian cement sector. Of these, Shree is the only player planning reinvestments in greenfield/brownfield expansion. UltraTech’s mega acquisition of Jaypee’s 22mn tonne capacity limits its ability to re-invest; ACC and Ambuja have no major expansion aspirations due to the global mandate of Lafarge-Holcim to curtail expansion. Jaypee will exit the business.

Top-5 players accounted for 70% of sector capex Exhibit 16:in FY02-08

Source: Company, Ambit Capital research

The proportion has fallen to 60% of overall Exhibit 17:capex over FY09-15

Source: Company, Ambit Capital research

Smaller manufacturers have limited ability to expand Most of the small- to mid-scale players have added capacities and now have debt to service. Players such as Dalmia, JK Lakshmi, JK Cement and Ramco have commissioned most of their under-implementation plants and do not have any major expansion plans.

The following exhibit shows that leverage of the cement firms (barring the top-5 cement companies in India) has increased, which limits their ability to re-invest cash flows for capacity expansion. Also, note that leverage for the North India based companies have increased in the last two years, whereas leverage for South based players has dropped marginally as companies repaid debt led by improvement in cash generation in FY15.

Leverage levels of Indian cement companies (barring the top-5) has Exhibit 18:increased, limiting their ability to re-invest

Source: Company, Ambit Capital research

UltraTech , Rs79.6bn;

25%

JPA, Rs65bn;

20%ACC,

Rs30.5bn; 10%

Ambuja, Rs25.6bn;

8%

Ramco, Rs20bn; 6%

Others, Rs18bn;

31%

Capex split (FY02-08)UltraTech, Rs154bn;

18.1%

JPA, Rs137bn;

16.1%

ACC, Rs76bn;

8.9%Shree,

Rs69.5bn 8.1%

Ambuja, Rs68bn;

8.0%

Others, Rs62bn;

41%

Capex split (FY09-15)

0.5

0.7

0.9

1.1

1.3

1.5

1.7

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Net Debt/Equity- cement cos

Companies- ex (top-5) North South

UltraTech’s mega acquisition of Jaypee’s 22mn tonne capacity limits its ability to re-invest

Leverage for the North India based companies have increased in the last two years

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 11

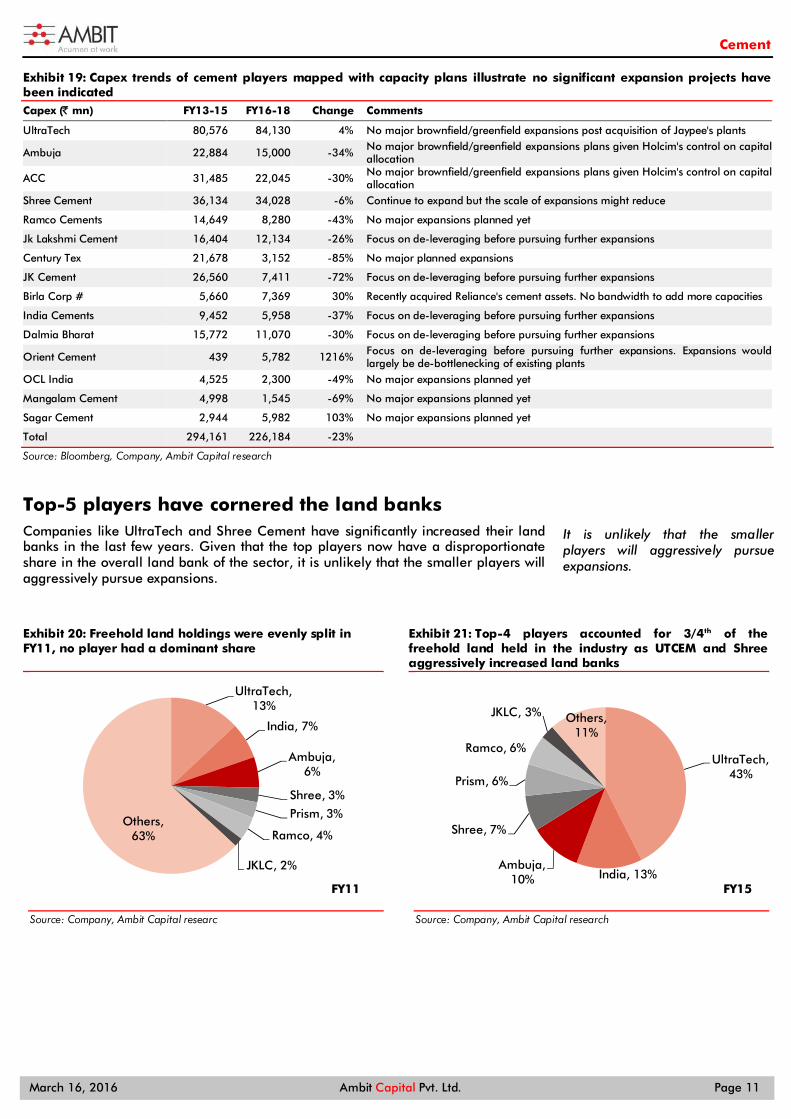

Capex trends of cement players mapped with capacity plans illustrate no significant expansion projects have Exhibit 19:been indicated Capex (̀ mn) FY13-15 FY16-18 Change Comments

UltraTech 80,576 84,130 4% No major brownfield/greenfield expansions post acquisition of Jaypee's plants

Ambuja 22,884 15,000 -34% No major brownfield/greenfield expansions plans given Holcim's control on capital allocation

ACC 31,485 22,045 -30% No major brownfield/greenfield expansions plans given Holcim's control on capital allocation

Shree Cement 36,134 34,028 -6% Continue to expand but the scale of expansions might reduce

Ramco Cements 14,649 8,280 -43% No major expansions planned yet

Jk Lakshmi Cement 16,404 12,134 -26% Focus on de-leveraging before pursuing further expansions

Century Tex 21,678 3,152 -85% No major planned expansions

JK Cement 26,560 7,411 -72% Focus on de-leveraging before pursuing further expansions

Birla Corp # 5,660 7,369 30% Recently acquired Reliance's cement assets. No bandwidth to add more capacities

India Cements 9,452 5,958 -37% Focus on de-leveraging before pursuing further expansions

Dalmia Bharat 15,772 11,070 -30% Focus on de-leveraging before pursuing further expansions

Orient Cement 439 5,782 1216% Focus on de-leveraging before pursuing further expansions. Expansions would largely be de-bottlenecking of existing plants

OCL India 4,525 2,300 -49% No major expansions planned yet

Mangalam Cement 4,998 1,545 -69% No major expansions planned yet

Sagar Cement 2,944 5,982 103% No major expansions planned yet

Total 294,161 226,184 -23% Source: Bloomberg, Company, Ambit Capital research

Top-5 players have cornered the land banks Companies like UltraTech and Shree Cement have significantly increased their land banks in the last few years. Given that the top players now have a disproportionate share in the overall land bank of the sector, it is unlikely that the smaller players will aggressively pursue expansions.

Freehold land holdings were evenly split in Exhibit 20:FY11, no player had a dominant share

Source: Company, Ambit Capital researc

Top-4 players accounted for 3/4th of the Exhibit 21:freehold land held in the industry as UTCEM and Shree aggressively increased land banks

Source: Company, Ambit Capital research

UltraTech, 13%

India, 7%

Ambuja, 6%

Shree, 3%

Prism, 3%

Ramco, 4%

JKLC, 2%

Others, 63%

FY11

UltraTech, 43%

India, 13%Ambuja,

10%

Shree, 7%

Prism, 6%

Ramco, 6%

JKLC, 3% Others, 11%

FY15

It is unlikely that the smaller players will aggressively pursue expansions.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 12

UltraTech and Shree have significantly increased their freehold land Exhibit 22:

Freehold land (̀ mn) FY11 FY12 FY13 FY14 FY15 CAGR

UltraTech 9,308 11,865 15,650 20,176 30,536 35%

India Cem 4,757 8,308 9,075 9,217 9,430 19%

Ambuja 4,113 5,167 5,828 7,010 7,495 16%

Shree 1,889 3,748 4,651 5,671 5,164 29%

Prism 2,072 2,354 2,856 3,933 4,515 22%

Ramco 3,107 3,193 3,423 3,972 4,295 8%

JK Lakshmi 1,190 1,190 1,826 1,925 2,012 14%

JK Cement 1,045 1,240 1,566 1,803 1,832 15%

ACC 1,928 2,493 2,829 1,044 1,189 -11%

Others 2,159 963 3,966 4,663 5,171 24%

Total 31,568 40,522 51,669 59,414 71,639 23%

Ex- UTCEM and Shree 20,371 24,909 31,368 33,567 35,939 15%

Source: Company, Ambit Capital research

Threat of new entrants receding Mandating limestone auctions creates an entry barrier that hitherto did not exist in the sector.

In the last five years, companies like Wonder Cement, Emami Cement, Nirma Cement and ABG Cement entered the industry with capacities ranging from 3mn-5mn tonnes. None had any background or expertise in cement; but they were allocated limestone mines given strong relationships with state governments and, hence, set up cement capacities.

The MMDR Act requires that limestone mines be auctioned from FY16; hence, companies will be required to competitively bid for limestone mines. This potentially reduces threat from non-core players.

Our checks with limestone consultants reveal that auctions in Rajasthan, Gujarat, Maharashtra and Odisha failed as high reserve price of limestone made bidding unviable. On the contrary, in Chhattisgarh, Shree Cement and Century Textiles won their bids at premium valuations of 58.5% and 10.5% of reserve price, respectively. This implies that companies are willing to pay a premium for strategic limestone assets.

Another possibility is that cash-rich companies are hoarding limestone reserves to fend off competition as the initial capital commitment for securing these reserves is not significant. Limestone is set to become a major strategic asset and companies which do not have sufficient reserves or capital to bid for limestone auctions will have no option but to moderate their expansion plans.

Implications of the end of the capex cycle Change in use of capital: The cement sector’s cash use will shift from capacity

addition to debt repayment and cleaning the balance sheet (especially for the smaller players). Hence, capital employed expansion should reduce hereon.

Reduced under-cutting: The regional players have expanded capacities and need to de-lever to improve their balance sheets. This implies that they would stop fighting for market share and focus on pricing.

Focus on efficiency: With capacity expansion behind, cement companies will invest time and some capital for enhancing efficiencies, either in terms of fuel usage or logistics. That, coupled with a benign commodity cycle, leads us to expect moderate expansion in unitary costs hereon.

RoCE recovery: Lack of major expansion in the capital employed base along with better pricing discipline will mean that pre-tax RoCEs will finally recover from the lows of the last five years to close to average levels of ~20%. See exhibit 53.

Companies were allocated limestone mines given strong relationships with state governments and, hence, set up cement capacities.

Auctions in Rajasthan, Gujarat, Maharashtra and Odisha failed as high reserve price of limestone made bidding unviable.

Limestone is set to become a major strategic asset

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 13

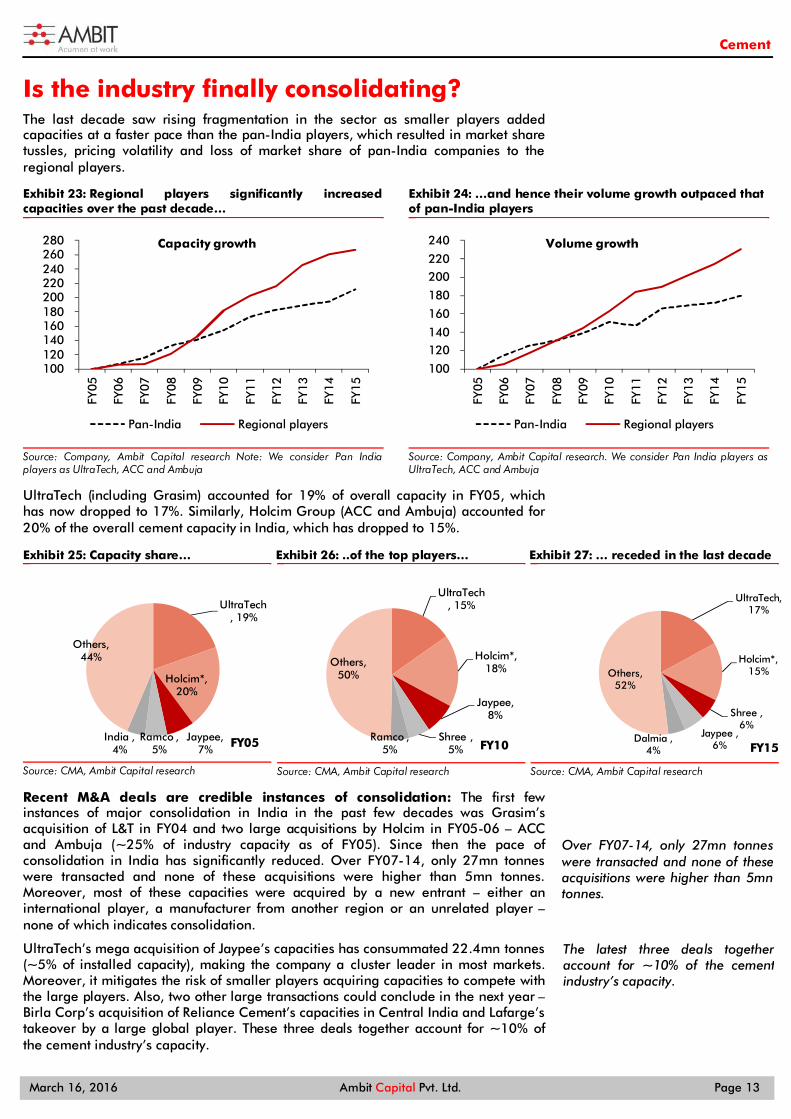

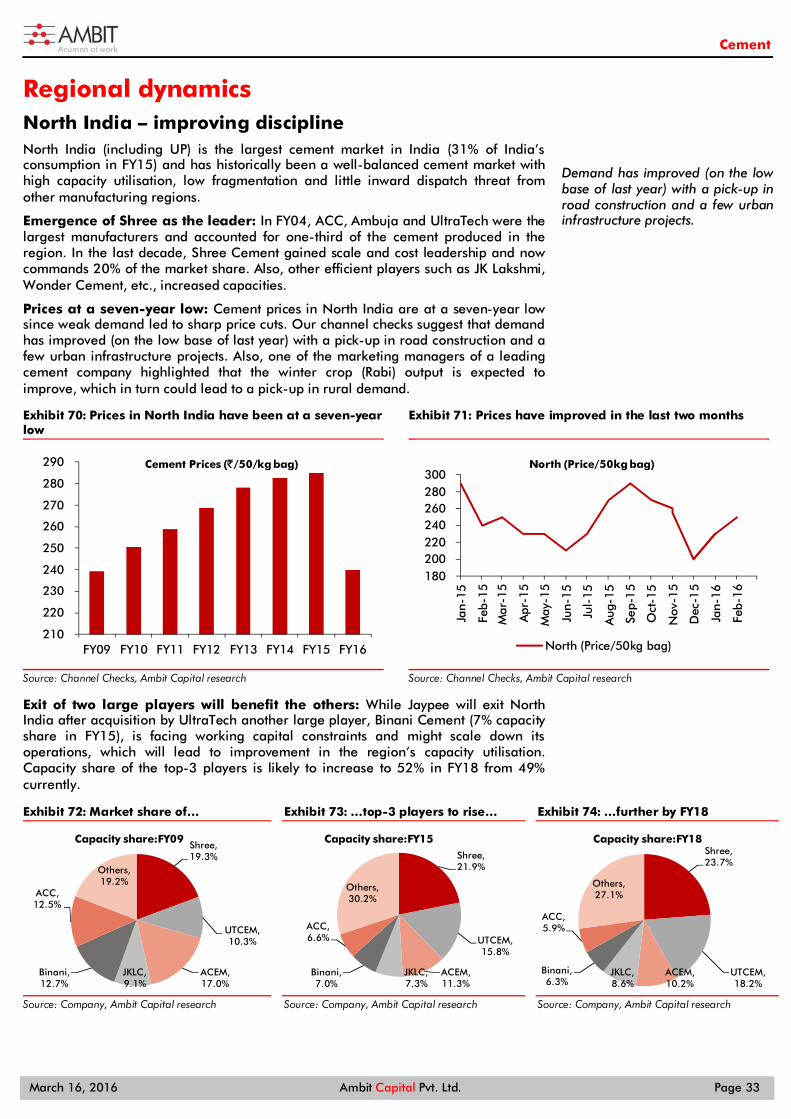

Is the industry finally consolidating? The last decade saw rising fragmentation in the sector as smaller players added capacities at a faster pace than the pan-India players, which resulted in market share tussles, pricing volatility and loss of market share of pan-India companies to the regional players.

Regional players significantly increased Exhibit 23:capacities over the past decade…

Source: Company, Ambit Capital research Note: We consider Pan India players as UltraTech, ACC and Ambuja

…and hence their volume growth outpaced that Exhibit 24:of pan-India players

Source: Company, Ambit Capital research. We consider Pan India players as UltraTech, ACC and Ambuja

UltraTech (including Grasim) accounted for 19% of overall capacity in FY05, which has now dropped to 17%. Similarly, Holcim Group (ACC and Ambuja) accounted for 20% of the overall cement capacity in India, which has dropped to 15%.

Capacity share… Exhibit 25:

Source: CMA, Ambit Capital research

..of the top players… Exhibit 26:

Source: CMA, Ambit Capital research

… receded in the last decade Exhibit 27:

Source: CMA, Ambit Capital research

Recent M&A deals are credible instances of consolidation: The first few instances of major consolidation in India in the past few decades was Grasim’s acquisition of L&T in FY04 and two large acquisitions by Holcim in FY05-06 – ACC and Ambuja (~25% of industry capacity as of FY05). Since then the pace of consolidation in India has significantly reduced. Over FY07-14, only 27mn tonnes were transacted and none of these acquisitions were higher than 5mn tonnes. Moreover, most of these capacities were acquired by a new entrant – either an international player, a manufacturer from another region or an unrelated player – none of which indicates consolidation.

UltraTech’s mega acquisition of Jaypee’s capacities has consummated 22.4mn tonnes (~5% of installed capacity), making the company a cluster leader in most markets. Moreover, it mitigates the risk of smaller players acquiring capacities to compete with the large players. Also, two other large transactions could conclude in the next year – Birla Corp’s acquisition of Reliance Cement’s capacities in Central India and Lafarge’s takeover by a large global player. These three deals together account for ~10% of the cement industry’s capacity.

100 120 140 160 180 200 220 240 260 280

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Capacity growth

Pan-India Regional players

100

120 140

160

180

200 220

240

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Volume growth

Pan-India Regional players

UltraTech, 19%

Holcim*, 20%

Jaypee, 7%

Ramco , 5%

India , 4%

Others, 44%

FY05

UltraTech, 15%

Holcim*, 18%

Jaypee, 8%

Shree , 5%

Ramco , 5%

Others, 50%

FY10

UltraTech, 17%

Holcim*, 15%

Shree , 6%

Jaypee , 6%

Dalmia , 4%

Others, 52%

FY15

Over FY07-14, only 27mn tonnes were transacted and none of these acquisitions were higher than 5mn tonnes.

The latest three deals together account for ~10% of the cement industry’s capacity.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 14

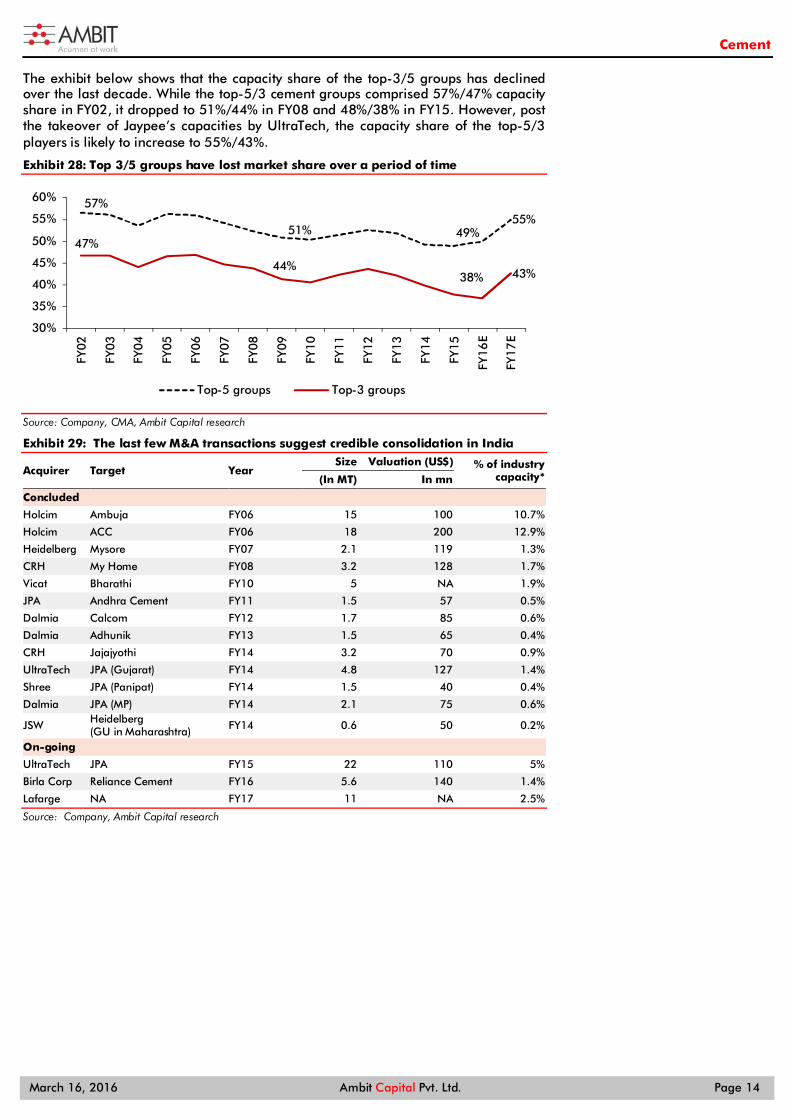

The exhibit below shows that the capacity share of the top-3/5 groups has declined over the last decade. While the top-5/3 cement groups comprised 57%/47% capacity share in FY02, it dropped to 51%/44% in FY08 and 48%/38% in FY15. However, post the takeover of Jaypee’s capacities by UltraTech, the capacity share of the top-5/3 players is likely to increase to 55%/43%.

Top 3/5 groups have lost market share over a period of time Exhibit 28:

Source: Company, CMA, Ambit Capital research

The last few M&A transactions suggest credible consolidation in India Exhibit 29:

Acquirer Target Year Size Valuation (US$) % of industry

capacity* (In MT) In mn

Concluded

Holcim Ambuja FY06 15 100 10.7%

Holcim ACC FY06 18 200 12.9%

Heidelberg Mysore FY07 2.1 119 1.3%

CRH My Home FY08 3.2 128 1.7%

Vicat Bharathi FY10 5 NA 1.9%

JPA Andhra Cement FY11 1.5 57 0.5%

Dalmia Calcom FY12 1.7 85 0.6%

Dalmia Adhunik FY13 1.5 65 0.4%

CRH Jajajyothi FY14 3.2 70 0.9%

UltraTech JPA (Gujarat) FY14 4.8 127 1.4%

Shree JPA (Panipat) FY14 1.5 40 0.4%

Dalmia JPA (MP) FY14 2.1 75 0.6%

JSW Heidelberg (GU in Maharashtra) FY14 0.6 50 0.2%

On-going

UltraTech JPA FY15 22 110 5%

Birla Corp Reliance Cement FY16 5.6 140 1.4%

Lafarge NA FY17 11 NA 2.5%

Source: Company, Ambit Capital research

57%

51% 49%55%

47%

44%38% 43%

30%

35%

40%

45%

50%

55%

60%

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

Top-5 groups Top-3 groups

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 15

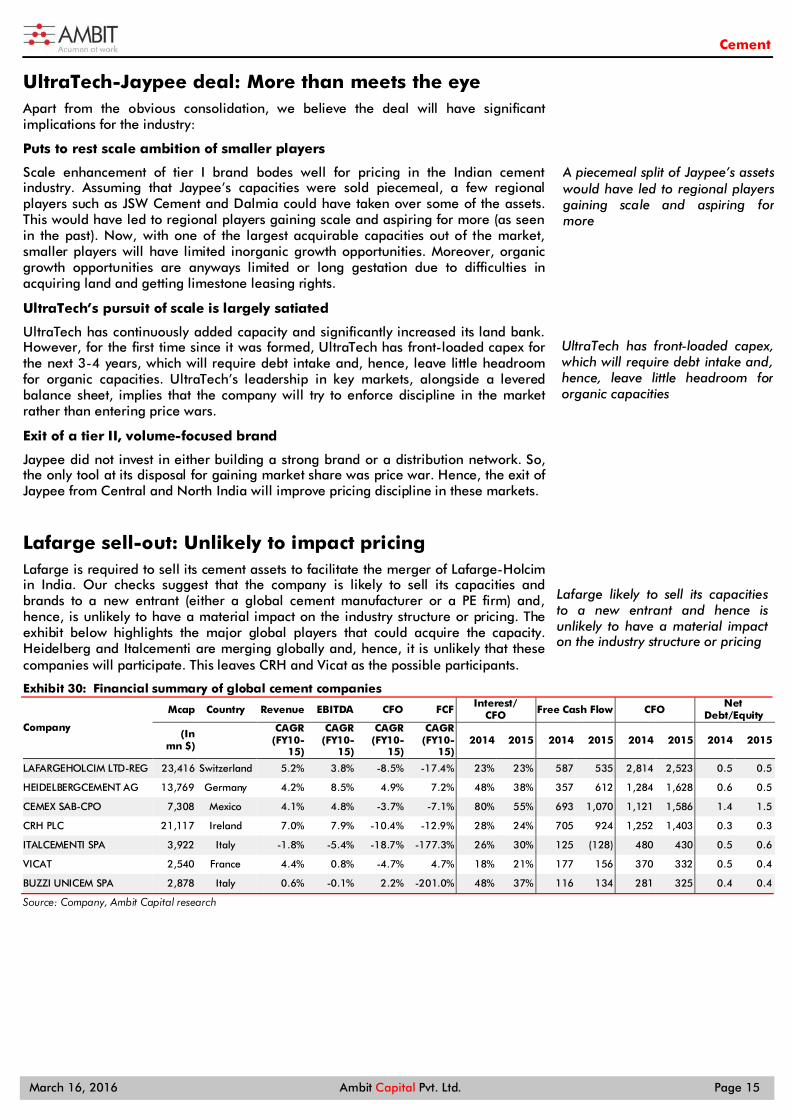

UltraTech-Jaypee deal: More than meets the eye Apart from the obvious consolidation, we believe the deal will have significant implications for the industry:

Puts to rest scale ambition of smaller players

Scale enhancement of tier I brand bodes well for pricing in the Indian cement industry. Assuming that Jaypee’s capacities were sold piecemeal, a few regional players such as JSW Cement and Dalmia could have taken over some of the assets. This would have led to regional players gaining scale and aspiring for more (as seen in the past). Now, with one of the largest acquirable capacities out of the market, smaller players will have limited inorganic growth opportunities. Moreover, organic growth opportunities are anyways limited or long gestation due to difficulties in acquiring land and getting limestone leasing rights.

UltraTech’s pursuit of scale is largely satiated

UltraTech has continuously added capacity and significantly increased its land bank. However, for the first time since it was formed, UltraTech has front-loaded capex for the next 3-4 years, which will require debt intake and, hence, leave little headroom for organic capacities. UltraTech’s leadership in key markets, alongside a levered balance sheet, implies that the company will try to enforce discipline in the market rather than entering price wars.

Exit of a tier II, volume-focused brand

Jaypee did not invest in either building a strong brand or a distribution network. So, the only tool at its disposal for gaining market share was price war. Hence, the exit of Jaypee from Central and North India will improve pricing discipline in these markets.

Lafarge sell-out: Unlikely to impact pricing Lafarge is required to sell its cement assets to facilitate the merger of Lafarge-Holcim in India. Our checks suggest that the company is likely to sell its capacities and brands to a new entrant (either a global cement manufacturer or a PE firm) and, hence, is unlikely to have a material impact on the industry structure or pricing. The exhibit below highlights the major global players that could acquire the capacity. Heidelberg and Italcementi are merging globally and, hence, it is unlikely that these companies will participate. This leaves CRH and Vicat as the possible participants.

Financial summary of global cement companies Exhibit 30:

Company

Mcap Country Revenue EBITDA CFO FCF Interest/

CFO Free Cash Flow CFO Net

Debt/Equity

(In mn $)

CAGR (FY10-

15)

CAGR (FY10-

15)

CAGR (FY10-

15)

CAGR (FY10-

15) 2014 2015 2014 2015 2014 2015 2014 2015

LAFARGEHOLCIM LTD-REG 23,416 Switzerland 5.2% 3.8% -8.5% -17.4% 23% 23% 587 535 2,814 2,523 0.5 0.5

HEIDELBERGCEMENT AG 13,769 Germany 4.2% 8.5% 4.9% 7.2% 48% 38% 357 612 1,284 1,628 0.6 0.5

CEMEX SAB-CPO 7,308 Mexico 4.1% 4.8% -3.7% -7.1% 80% 55% 693 1,070 1,121 1,586 1.4 1.5

CRH PLC 21,117 Ireland 7.0% 7.9% -10.4% -12.9% 28% 24% 705 924 1,252 1,403 0.3 0.3

ITALCEMENTI SPA 3,922 Italy -1.8% -5.4% -18.7% -177.3% 26% 30% 125 (128) 480 430 0.5 0.6

VICAT 2,540 France 4.4% 0.8% -4.7% 4.7% 18% 21% 177 156 370 332 0.5 0.4

BUZZI UNICEM SPA 2,878 Italy 0.6% -0.1% 2.2% -201.0% 48% 37% 116 134 281 325 0.4 0.4

Source: Company, Ambit Capital research

A piecemeal split of Jaypee’s assets would have led to regional players gaining scale and aspiring for more

UltraTech has front-loaded capex, which will require debt intake and, hence, leave little headroom for organic capacities

Lafarge likely to sell its capacities to a new entrant and hence is unlikely to have a material impact on the industry structure or pricing

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 16

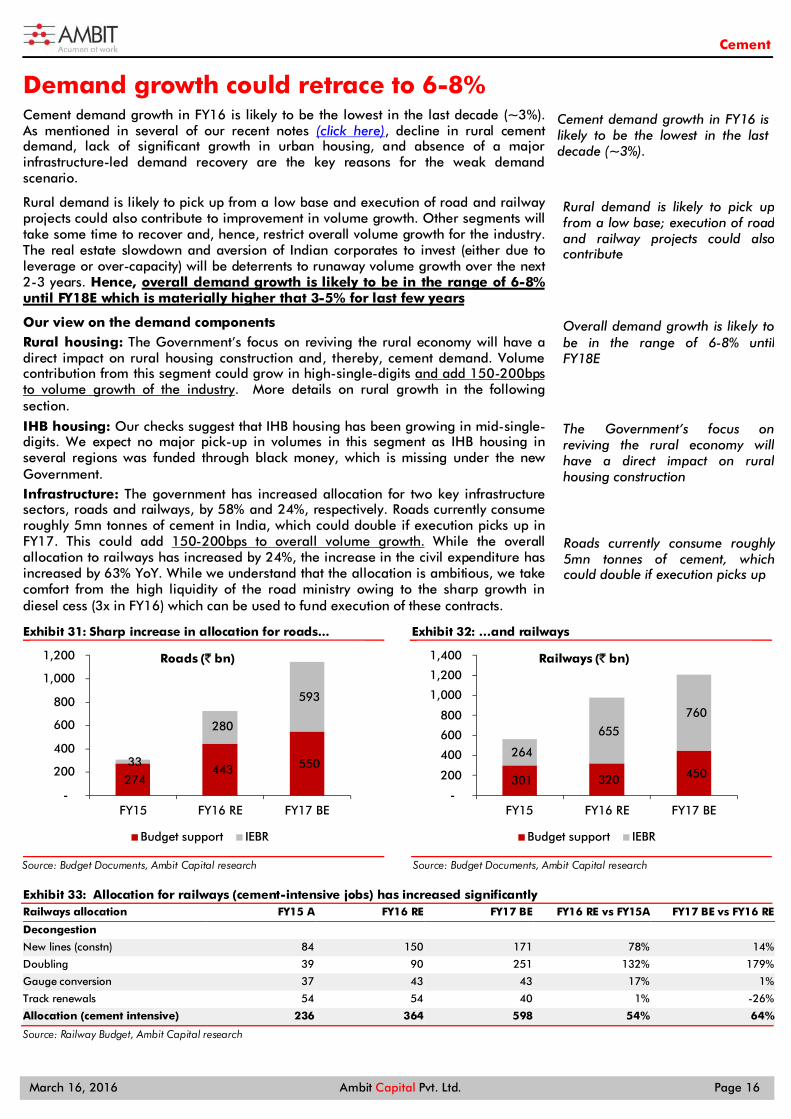

Demand growth could retrace to 6-8% Cement demand growth in FY16 is likely to be the lowest in the last decade (~3%). As mentioned in several of our recent notes (click here), decline in rural cement demand, lack of significant growth in urban housing, and absence of a major infrastructure-led demand recovery are the key reasons for the weak demand scenario.

Rural demand is likely to pick up from a low base and execution of road and railway projects could also contribute to improvement in volume growth. Other segments will take some time to recover and, hence, restrict overall volume growth for the industry. The real estate slowdown and aversion of Indian corporates to invest (either due to leverage or over-capacity) will be deterrents to runaway volume growth over the next 2-3 years. Hence, overall demand growth is likely to be in the range of 6-8% until FY18E which is materially higher that 3-5% for last few years

Our view on the demand components Rural housing: The Government’s focus on reviving the rural economy will have a direct impact on rural housing construction and, thereby, cement demand. Volume contribution from this segment could grow in high-single-digits and add 150-200bps to volume growth of the industry. More details on rural growth in the following section.

IHB housing: Our checks suggest that IHB housing has been growing in mid-single-digits. We expect no major pick-up in volumes in this segment as IHB housing in several regions was funded through black money, which is missing under the new Government. Infrastructure: The government has increased allocation for two key infrastructure sectors, roads and railways, by 58% and 24%, respectively. Roads currently consume roughly 5mn tonnes of cement in India, which could double if execution picks up in FY17. This could add 150-200bps to overall volume growth. While the overall allocation to railways has increased by 24%, the increase in the civil expenditure has increased by 63% YoY. While we understand that the allocation is ambitious, we take comfort from the high liquidity of the road ministry owing to the sharp growth in diesel cess (3x in FY16) which can be used to fund execution of these contracts.

Sharp increase in allocation for roads... Exhibit 31:

Source: Budget Documents, Ambit Capital research

…and railways Exhibit 32:

Source: Budget Documents, Ambit Capital research

Allocation for railways (cement-intensive jobs) has increased significantly Exhibit 33:Railways allocation FY15 A FY16 RE FY17 BE FY16 RE vs FY15A FY17 BE vs FY16 RE

Decongestion New lines (constn) 84 150 171 78% 14%

Doubling 39 90 251 132% 179%

Gauge conversion 37 43 43 17% 1%

Track renewals 54 54 40 1% -26%

Allocation (cement intensive) 236 364 598 54% 64%

Source: Railway Budget, Ambit Capital research

274 443 550 33

280

593

-

200

400

600

800

1,000

1,200

FY15 FY16 RE FY17 BE

Roads (` bn)

Budget support IEBR

301 320 450

264

655

760

-

200

400

600

800

1,000

1,200

1,400

FY15 FY16 RE FY17 BE

Railways (` bn)

Budget support IEBR

Cement demand growth in FY16 is likely to be the lowest in the last decade (~3%).

Rural demand is likely to pick up from a low base; execution of road and railway projects could also contribute

Overall demand growth is likely to be in the range of 6-8% until FY18E

The Government’s focus on reviving the rural economy will have a direct impact on rural housing construction

Roads currently consume roughly 5mn tonnes of cement, which could double if execution picks up

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 17

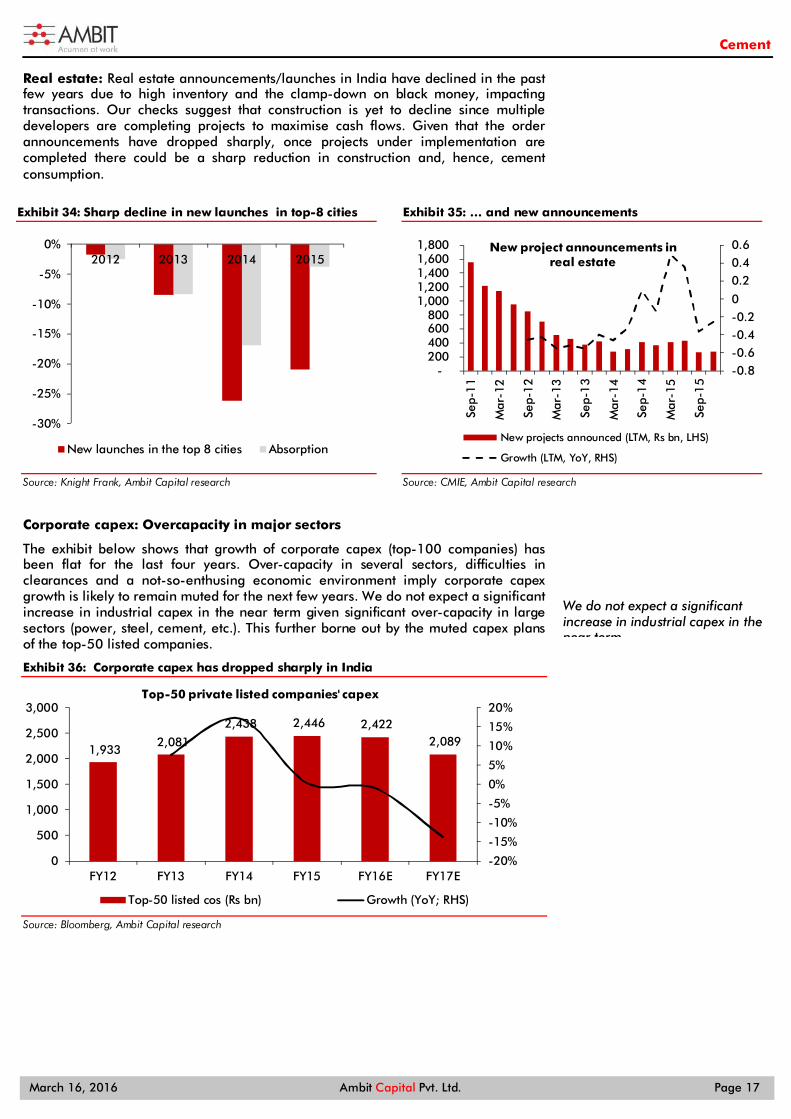

Real estate: Real estate announcements/launches in India have declined in the past few years due to high inventory and the clamp-down on black money, impacting transactions. Our checks suggest that construction is yet to decline since multiple developers are completing projects to maximise cash flows. Given that the order announcements have dropped sharply, once projects under implementation are completed there could be a sharp reduction in construction and, hence, cement consumption.

Corporate capex: Overcapacity in major sectors

The exhibit below shows that growth of corporate capex (top-100 companies) has been flat for the last four years. Over-capacity in several sectors, difficulties in clearances and a not-so-enthusing economic environment imply corporate capex growth is likely to remain muted for the next few years. We do not expect a significant increase in industrial capex in the near term given significant over-capacity in large sectors (power, steel, cement, etc.). This further borne out by the muted capex plans of the top-50 listed companies.

Corporate capex has dropped sharply in India Exhibit 36:

Source: Bloomberg, Ambit Capital research

1,933 2,081

2,438 2,446 2,422 2,089

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

500

1,000

1,500

2,000

2,500

3,000

FY12 FY13 FY14 FY15 FY16E FY17E

Top-50 private listed companies' capex

Top-50 listed cos (Rs bn) Growth (YoY; RHS)

Sharp decline in new launches in top-8 cities Exhibit 34:

Source: Knight Frank, Ambit Capital research

… and new announcements Exhibit 35:

Source: CMIE, Ambit Capital research

We do not expect a significant increase in industrial capex in the near term

-30%

-25%

-20%

-15%

-10%

-5%

0%2012 2013 2014 2015

New launches in the top 8 cities Absorption

-0.8-0.6-0.4-0.20

0.20.40.6

- 200 400 600 800

1,000 1,200 1,400 1,600 1,800

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

New project announcements in real estate

New projects announced (LTM, Rs bn, LHS)

Growth (LTM, YoY, RHS)

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 18

The retail consumer to the rescue 2.0 In our thematic note dated 19 Dec 2011, we highlighted that strong retail demand has a significant bearing on cement prices as the bargaining power of tier I brands strengthens over the regional players. Below is an excerpt from it:

“Low demand from bulk-buying-price-bargaining institutional clients and steady demand from the fragmented-low-bargaining-power brand-seeking Individual House Builder (IHB) is helping producers raise cement prices higher despite lower industry utilisation. Pricing power with the IHB consumer base will limit the drop in RoCEs and maintain strong cash flows for the larger players, thus supporting premium valuations and relative outperformance.”

From Ambit’s cement thematic

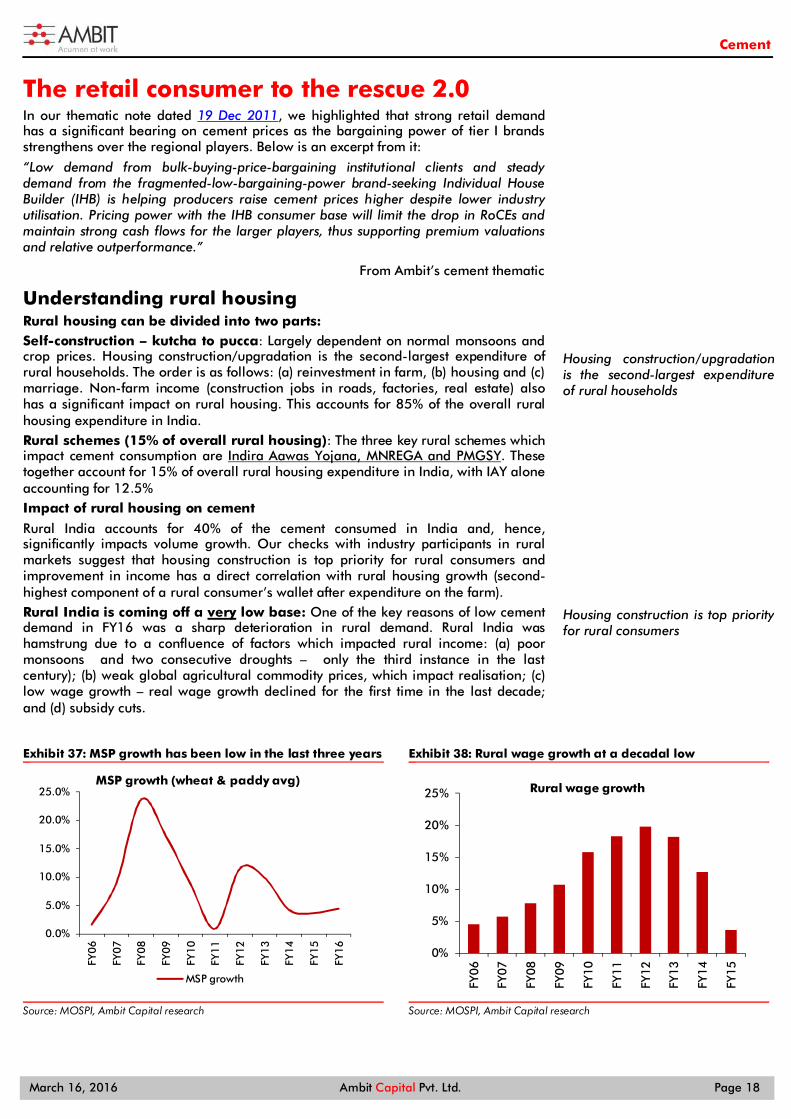

Understanding rural housing Rural housing can be divided into two parts: Self-construction – kutcha to pucca: Largely dependent on normal monsoons and crop prices. Housing construction/upgradation is the second-largest expenditure of rural households. The order is as follows: (a) reinvestment in farm, (b) housing and (c) marriage. Non-farm income (construction jobs in roads, factories, real estate) also has a significant impact on rural housing. This accounts for 85% of the overall rural housing expenditure in India. Rural schemes (15% of overall rural housing): The three key rural schemes which impact cement consumption are Indira Aawas Yojana, MNREGA and PMGSY. These together account for 15% of overall rural housing expenditure in India, with IAY alone accounting for 12.5% Impact of rural housing on cement

Rural India accounts for 40% of the cement consumed in India and, hence, significantly impacts volume growth. Our checks with industry participants in rural markets suggest that housing construction is top priority for rural consumers and improvement in income has a direct correlation with rural housing growth (second-highest component of a rural consumer’s wallet after expenditure on the farm). Rural India is coming off a very low base: One of the key reasons of low cement demand in FY16 was a sharp deterioration in rural demand. Rural India was hamstrung due to a confluence of factors which impacted rural income: (a) poor monsoons and two consecutive droughts – only the third instance in the last century); (b) weak global agricultural commodity prices, which impact realisation; (c) low wage growth – real wage growth declined for the first time in the last decade; and (d) subsidy cuts.

MSP growth has been low in the last three years Exhibit 37:

Source: MOSPI, Ambit Capital research

Rural wage growth at a decadal low Exhibit 38:

Source: MOSPI, Ambit Capital research

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

MSP growth (wheat & paddy avg)

MSP growth

0%

5%

10%

15%

20%

25%

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Rural wage growth

Housing construction/upgradation is the second-largest expenditure of rural households

Housing construction is top priority for rural consumers

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 19

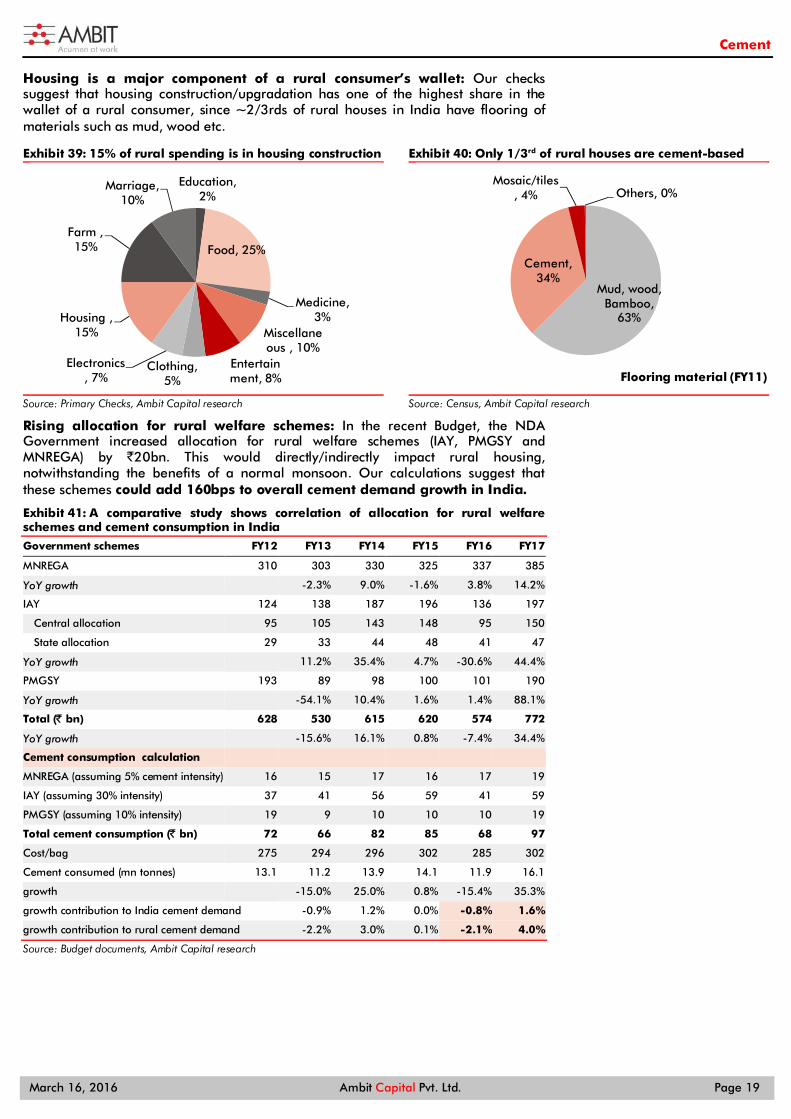

Housing is a major component of a rural consumer’s wallet: Our checks suggest that housing construction/upgradation has one of the highest share in the wallet of a rural consumer, since ~2/3rds of rural houses in India have flooring of materials such as mud, wood etc.

15% of rural spending is in housing construction Exhibit 39:

Source: Primary Checks, Ambit Capital research

Only 1/3rd of rural houses are cement-based Exhibit 40:

Source: Census, Ambit Capital research

Rising allocation for rural welfare schemes: In the recent Budget, the NDA Government increased allocation for rural welfare schemes (IAY, PMGSY and MNREGA) by `20bn. This would directly/indirectly impact rural housing, notwithstanding the benefits of a normal monsoon. Our calculations suggest that these schemes could add 160bps to overall cement demand growth in India.

A comparative study shows correlation of allocation for rural welfare Exhibit 41:schemes and cement consumption in India

Government schemes FY12 FY13 FY14 FY15 FY16 FY17

MNREGA 310 303 330 325 337 385

YoY growth -2.3% 9.0% -1.6% 3.8% 14.2%

IAY 124 138 187 196 136 197

Central allocation 95 105 143 148 95 150

State allocation 29 33 44 48 41 47

YoY growth 11.2% 35.4% 4.7% -30.6% 44.4%

PMGSY 193 89 98 100 101 190

YoY growth -54.1% 10.4% 1.6% 1.4% 88.1%

Total (̀ bn) 628 530 615 620 574 772

YoY growth -15.6% 16.1% 0.8% -7.4% 34.4%

Cement consumption calculation MNREGA (assuming 5% cement intensity) 16 15 17 16 17 19

IAY (assuming 30% intensity) 37 41 56 59 41 59

PMGSY (assuming 10% intensity) 19 9 10 10 10 19

Total cement consumption (̀ bn) 72 66 82 85 68 97

Cost/bag 275 294 296 302 285 302

Cement consumed (mn tonnes) 13.1 11.2 13.9 14.1 11.9 16.1

growth -15.0% 25.0% 0.8% -15.4% 35.3%

growth contribution to India cement demand -0.9% 1.2% 0.0% -0.8% 1.6%

growth contribution to rural cement demand -2.2% 3.0% 0.1% -2.1% 4.0%

Source: Budget documents, Ambit Capital research

Education, 2%

Food, 25%

Medicine, 3%

Miscellaneous , 10%

Entertainment, 8%

Clothing, 5%

Electronics, 7%

Housing , 15%

Farm , 15%

Marriage, 10%

Mud, wood, Bamboo,

63%

Cement, 34%

Mosaic/tiles, 4% Others, 0%

Flooring material (FY11)

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 20

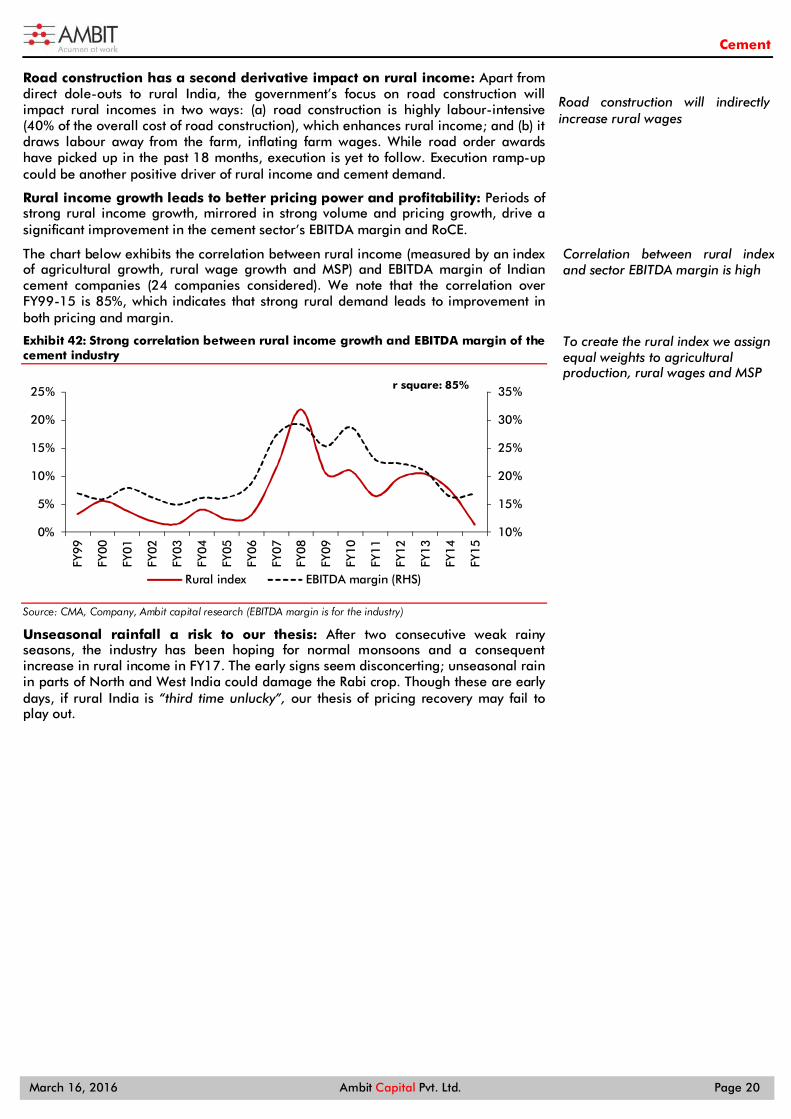

Road construction has a second derivative impact on rural income: Apart from direct dole-outs to rural India, the government’s focus on road construction will impact rural incomes in two ways: (a) road construction is highly labour-intensive (40% of the overall cost of road construction), which enhances rural income; and (b) it draws labour away from the farm, inflating farm wages. While road order awards have picked up in the past 18 months, execution is yet to follow. Execution ramp-up could be another positive driver of rural income and cement demand.

Rural income growth leads to better pricing power and profitability: Periods of strong rural income growth, mirrored in strong volume and pricing growth, drive a significant improvement in the cement sector’s EBITDA margin and RoCE.

The chart below exhibits the correlation between rural income (measured by an index of agricultural growth, rural wage growth and MSP) and EBITDA margin of Indian cement companies (24 companies considered). We note that the correlation over FY99-15 is 85%, which indicates that strong rural demand leads to improvement in both pricing and margin.

Strong correlation between rural income growth and EBITDA margin of the Exhibit 42:cement industry

Source: CMA, Company, Ambit capital research (EBITDA margin is for the industry)

Unseasonal rainfall a risk to our thesis: After two consecutive weak rainy seasons, the industry has been hoping for normal monsoons and a consequent increase in rural income in FY17. The early signs seem disconcerting; unseasonal rain in parts of North and West India could damage the Rabi crop. Though these are early days, if rural India is “third time unlucky”, our thesis of pricing recovery may fail to play out.

10%

15%

20%

25%

30%

35%

0%

5%

10%

15%

20%

25%

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

r square: 85%

Rural index EBITDA margin (RHS)

Road construction will indirectly increase rural wages

Correlation between rural index and sector EBITDA margin is high

To create the rural index we assign equal weights to agricultural production, rural wages and MSP

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 21

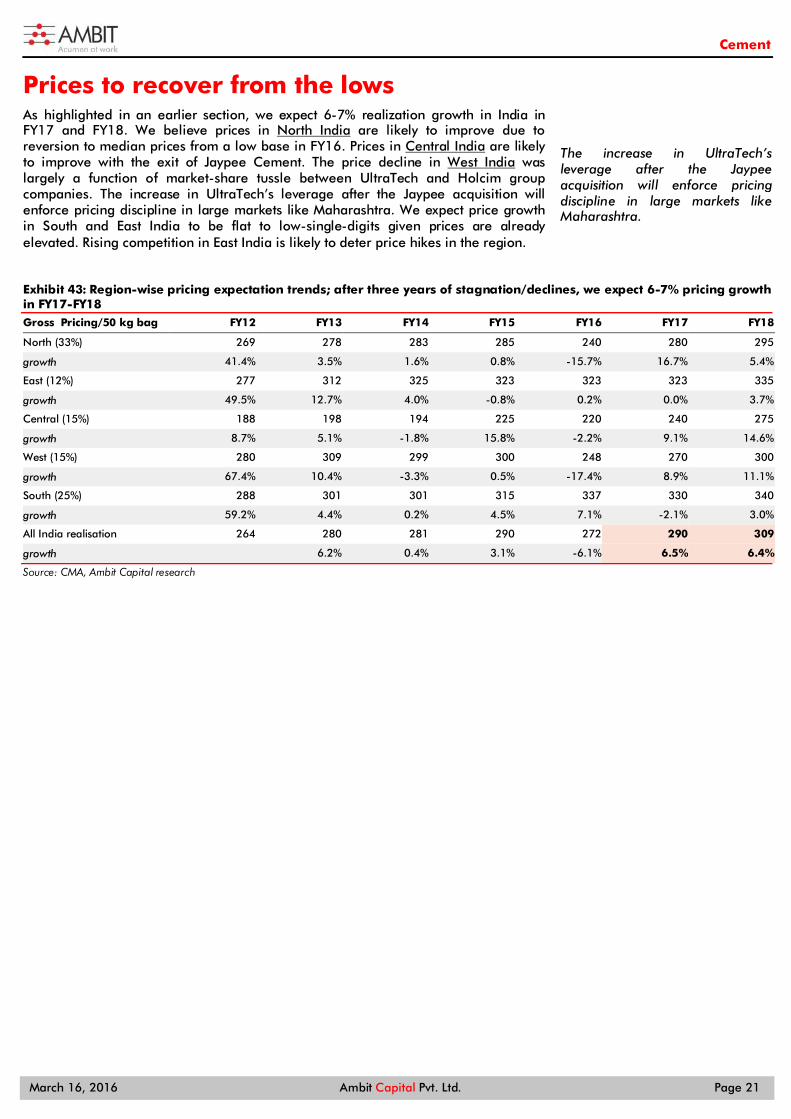

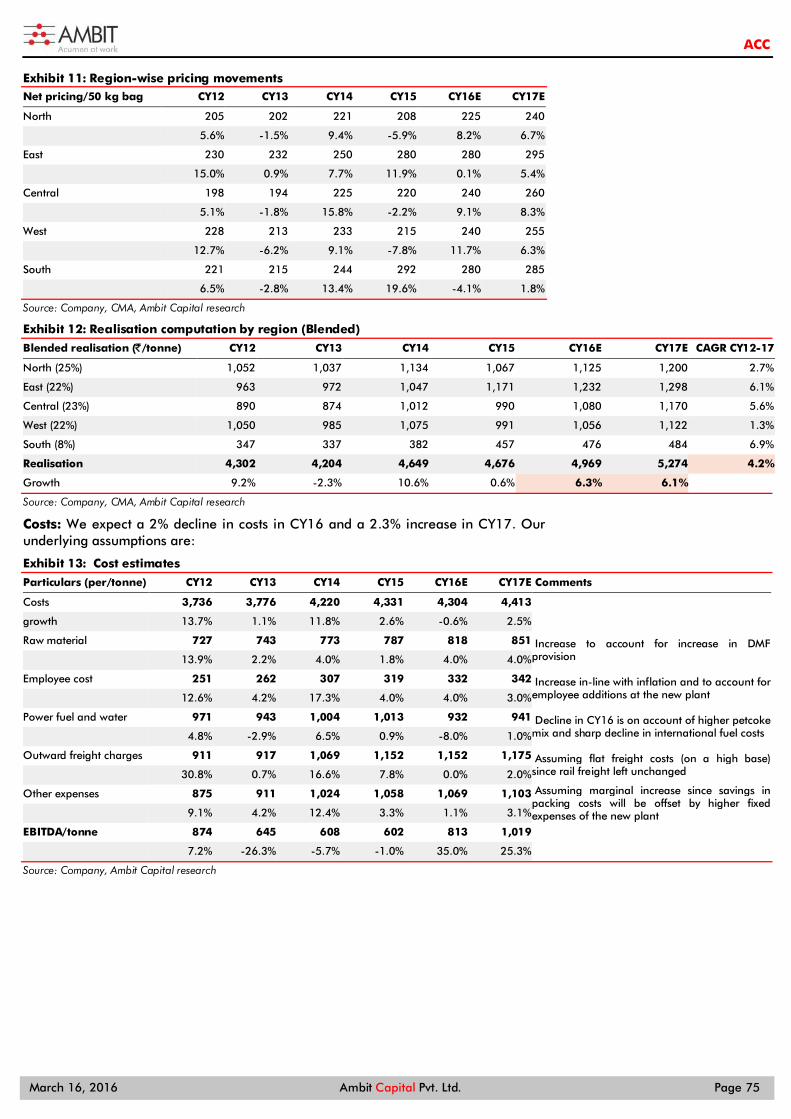

Prices to recover from the lows As highlighted in an earlier section, we expect 6-7% realization growth in India in FY17 and FY18. We believe prices in North India are likely to improve due to reversion to median prices from a low base in FY16. Prices in Central India are likely to improve with the exit of Jaypee Cement. The price decline in West India was largely a function of market-share tussle between UltraTech and Holcim group companies. The increase in UltraTech’s leverage after the Jaypee acquisition will enforce pricing discipline in large markets like Maharashtra. We expect price growth in South and East India to be flat to low-single-digits given prices are already elevated. Rising competition in East India is likely to deter price hikes in the region.

Region-wise pricing expectation trends; after three years of stagnation/declines, we expect 6-7% pricing growth Exhibit 43:in FY17-FY18 Gross Pricing/50 kg bag FY12 FY13 FY14 FY15 FY16 FY17 FY18

North (33%) 269 278 283 285 240 280 295

growth 41.4% 3.5% 1.6% 0.8% -15.7% 16.7% 5.4%

East (12%) 277 312 325 323 323 323 335

growth 49.5% 12.7% 4.0% -0.8% 0.2% 0.0% 3.7%

Central (15%) 188 198 194 225 220 240 275

growth 8.7% 5.1% -1.8% 15.8% -2.2% 9.1% 14.6%

West (15%) 280 309 299 300 248 270 300

growth 67.4% 10.4% -3.3% 0.5% -17.4% 8.9% 11.1%

South (25%) 288 301 301 315 337 330 340

growth 59.2% 4.4% 0.2% 4.5% 7.1% -2.1% 3.0%

All India realisation 264 280 281 290 272 290 309

growth 6.2% 0.4% 3.1% -6.1% 6.5% 6.4%

Source: CMA, Ambit Capital research

The increase in UltraTech’s leverage after the Jaypee acquisition will enforce pricing discipline in large markets like Maharashtra.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 22

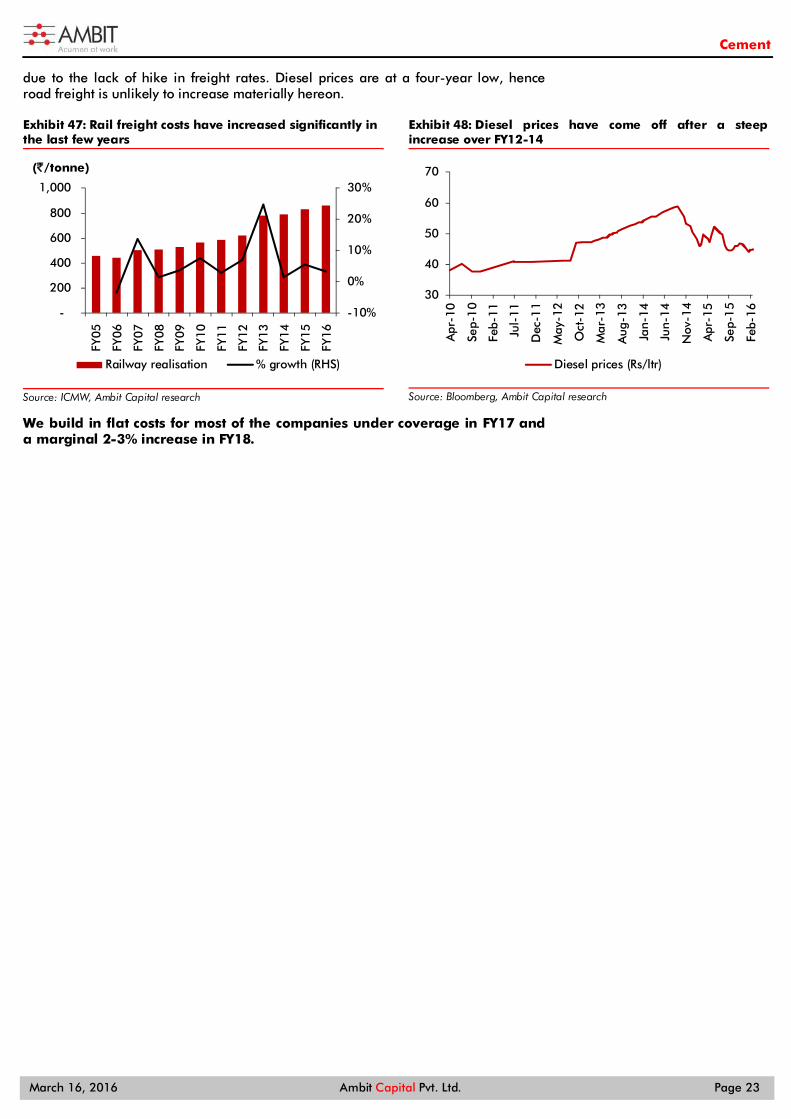

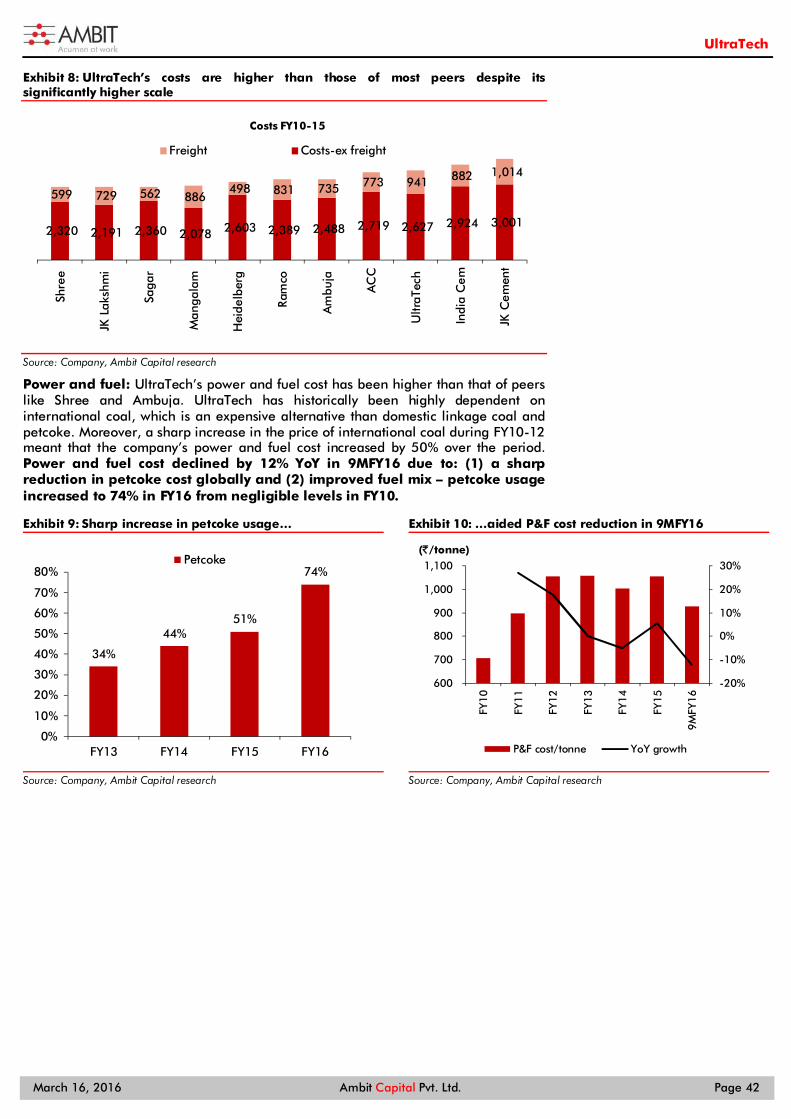

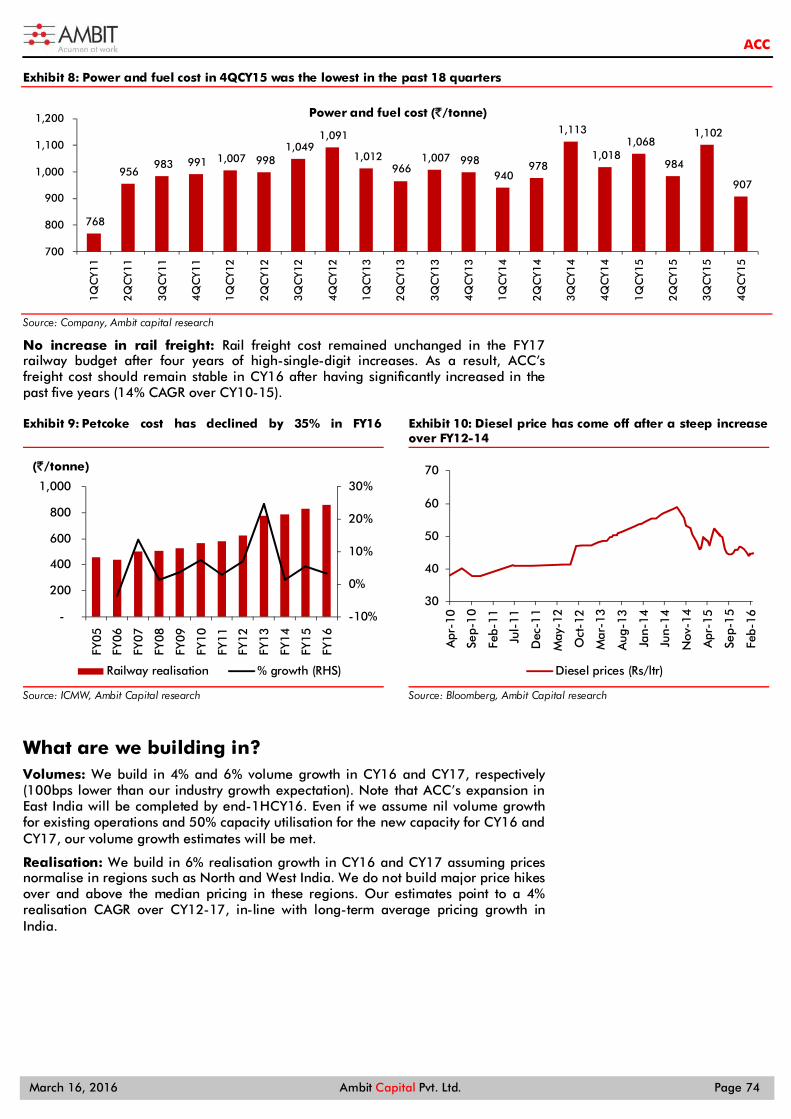

Costs – headwinds receding Operating costs for the Indian cement industry have increased materially in the past five years and especially over FY11-13 when a sharp rise in international coal costs inflated power and fuel costs.

The Indian government increased freight rates in each of the last five years, which inflated transportation costs for cement manufacturers, especially for players like ACC that are highly dependent on rail freight.

The chart below shows power & fuel (P&F) and freight costs, measured using an index of 11 companies, accounting for 60% of the industry’s capacities/volumes, registered 9% and 14% CAGR respectively over FY09-15. However, in 9MFY16, P&F costs fell by 15% while freight declined fell by 2%.

Sharp increase in key cost elements Exhibit 44:

Source: Company, Ambit Capital research. The above is an average of 11 cement companies - UltraTech,ACEM, ACC, Shree, JKLC, Mangalam, Ramco, ICEM, JKCE, Sagar, HEID

Power & fuel costs: The global commodity downcycle decreased international coal and petcoke costs significantly in the last two years. YTD, petcoke and international coal costs are down 35% and 10% respectively. Moreover, prices of domestic coal remains stable given Coal India’s agenda to increase production and lower demand from domestic power producers. In such a scenario, it is highly likely that fuel prices remain benign for the next 1- 2 years, which can support EBITDA/tonne expansion.

Petcoke costs declined by 35% in FY16 Exhibit 45:

Source: ICMW, Ambit Capital research

International coal prices down 10% YTD Exhibit 46:

Source: Bloomberg, Ambit Capital research

Freight costs: For the first time in last 10 years, the Government has kept rail freight rate unchanged in its budget. The exhibit below shows rail freight realisation of the Government clocked an 11% CAGR over FY10-13 due to significant hikes in those years. Realisations have been at 3% over FY13-FY16 and are likely to recede further

627 610 771 881 917 911 1,041 887

469 490 646

739 869 952 1,011

990

-

500

1,000

1,500

2,000

2,500

FY09 FY10 FY11 FY12 FY13 FY14 FY15 9MFY16

(`/tonne)

P&F Freight

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb-

16

1,500

1,800

2,100

2,400

2,700

3,000

3,300

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Mar

-16

Indonesian coal (`/tonne)

It is highly likely that fuel prices remain benign for the next 1- 2 years, which can support EBITDA/tonne expansion.

Diesel prices are at a four-year low, hence road freight is unlikely to increase materially hereon.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 23

due to the lack of hike in freight rates. Diesel prices are at a four-year low, hence road freight is unlikely to increase materially hereon.

Rail freight costs have increased significantly in Exhibit 47:the last few years

Source: ICMW, Ambit Capital research

Diesel prices have come off after a steep Exhibit 48:increase over FY12-14

Source: Bloomberg, Ambit Capital research

We build in flat costs for most of the companies under coverage in FY17 and a marginal 2-3% increase in FY18.

-10%

0%

10%

20%

30%

-

200

400

600

800

1,000

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

(`/tonne)

Railway realisation % growth (RHS)

30

40

50

60

70

Apr

-10

Sep-

10

Feb-

11

Jul-

11

Dec

-11

May

-12

Oct

-12

Mar

-13

Aug

-13

Jan-

14

Jun-

14

Nov

-14

Apr

-15

Sep-

15

Feb-

16

Diesel prices (Rs/ltr)

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 24

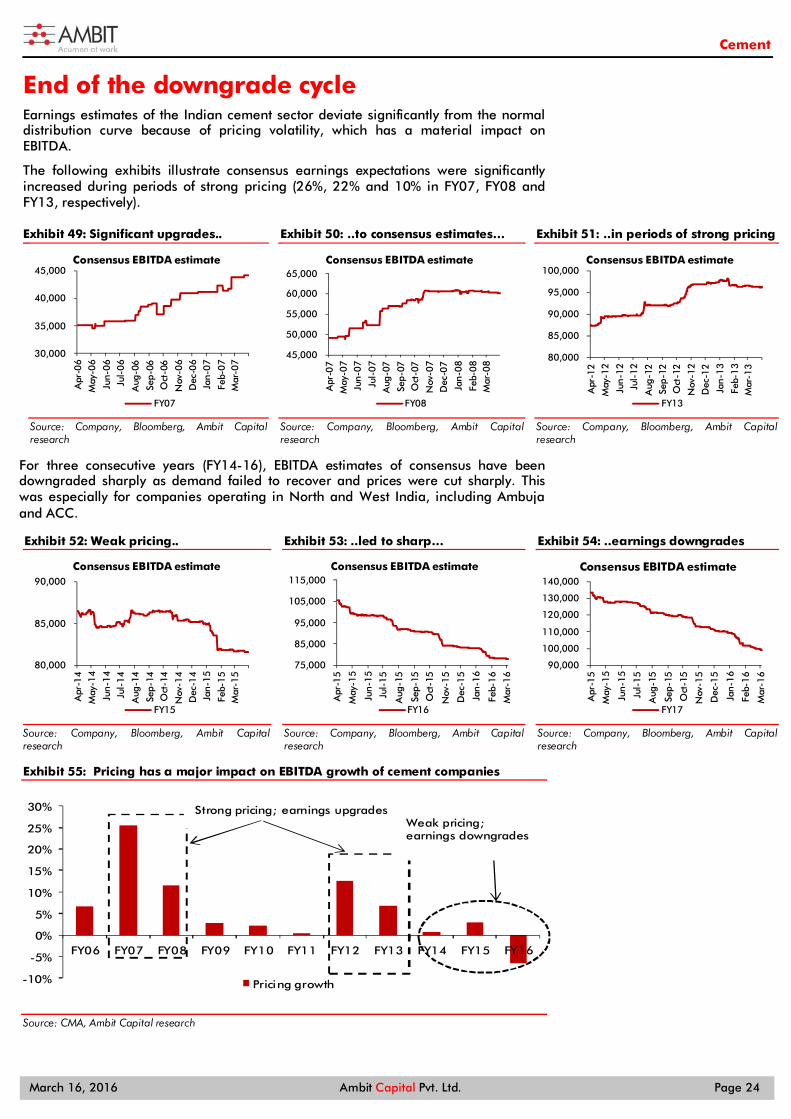

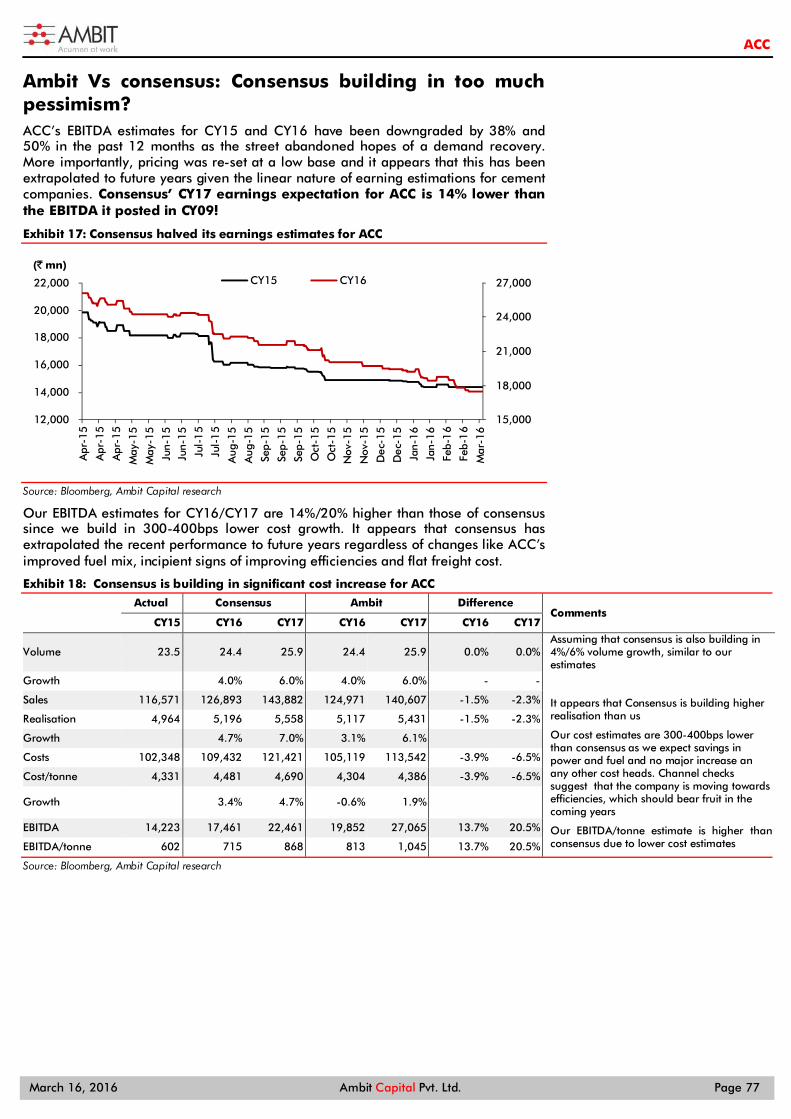

End of the downgrade cycle Earnings estimates of the Indian cement sector deviate significantly from the normal distribution curve because of pricing volatility, which has a material impact on EBITDA.

The following exhibits illustrate consensus earnings expectations were significantly increased during periods of strong pricing (26%, 22% and 10% in FY07, FY08 and FY13, respectively).

Significant upgrades.. Exhibit 49:

Source: Company, Bloomberg, Ambit Capital research

..to consensus estimates… Exhibit 50:

Source: Company, Bloomberg, Ambit Capital research

..in periods of strong pricing Exhibit 51:

Source: Company, Bloomberg, Ambit Capital research

For three consecutive years (FY14-16), EBITDA estimates of consensus have been downgraded sharply as demand failed to recover and prices were cut sharply. This was especially for companies operating in North and West India, including Ambuja and ACC.

Weak pricing.. Exhibit 52:

Source: Company, Bloomberg, Ambit Capital research

..led to sharp… Exhibit 53:

Source: Company, Bloomberg, Ambit Capital research

..earnings downgrades Exhibit 54:

Source: Company, Bloomberg, Ambit Capital research

Pricing has a major impact on EBITDA growth of cement companies Exhibit 55:

Source: CMA, Ambit Capital research

30,000

35,000

40,000

45,000

Apr

-06

May

-06

Jun-

06

Jul-

06

Aug

-06

Sep-

06O

ct-0

6

Nov

-06

Dec

-06

Jan-

07

Feb-

07

Mar

-07

Consensus EBITDA estimate

FY07

45,000

50,000

55,000

60,000

65,000

Apr

-07

May

-07

Jun-0

7

Jul-

07

Aug

-07

Sep-0

7O

ct-0

7

Nov

-07

Dec

-07

Jan-0

8

Feb-

08

Mar

-08

Consensus EBITDA estimate

FY08

80,000

85,000

90,000

95,000

100,000

Apr

-12

May

-12

Jun-

12

Jul-

12

Aug

-12

Sep-

12O

ct-1

2

Nov

-12

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Consensus EBITDA estimate

FY13

80,000

85,000

90,000

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

Sep-

14O

ct-1

4

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Consensus EBITDA estimate

FY15

75,000

85,000

95,000

105,000

115,000

Apr

-15

May

-15

Jun-

15

Jul-

15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Consensus EBITDA estimate

FY16

90,000

100,000

110,000

120,000

130,000

140,000A

pr-1

5

May

-15

Jun-

15

Jul-

15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Consensus EBITDA estimate

FY17

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Pricing growth

Strong pricing; earnings upgradesWeak pricing; earnings downgrades

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 25

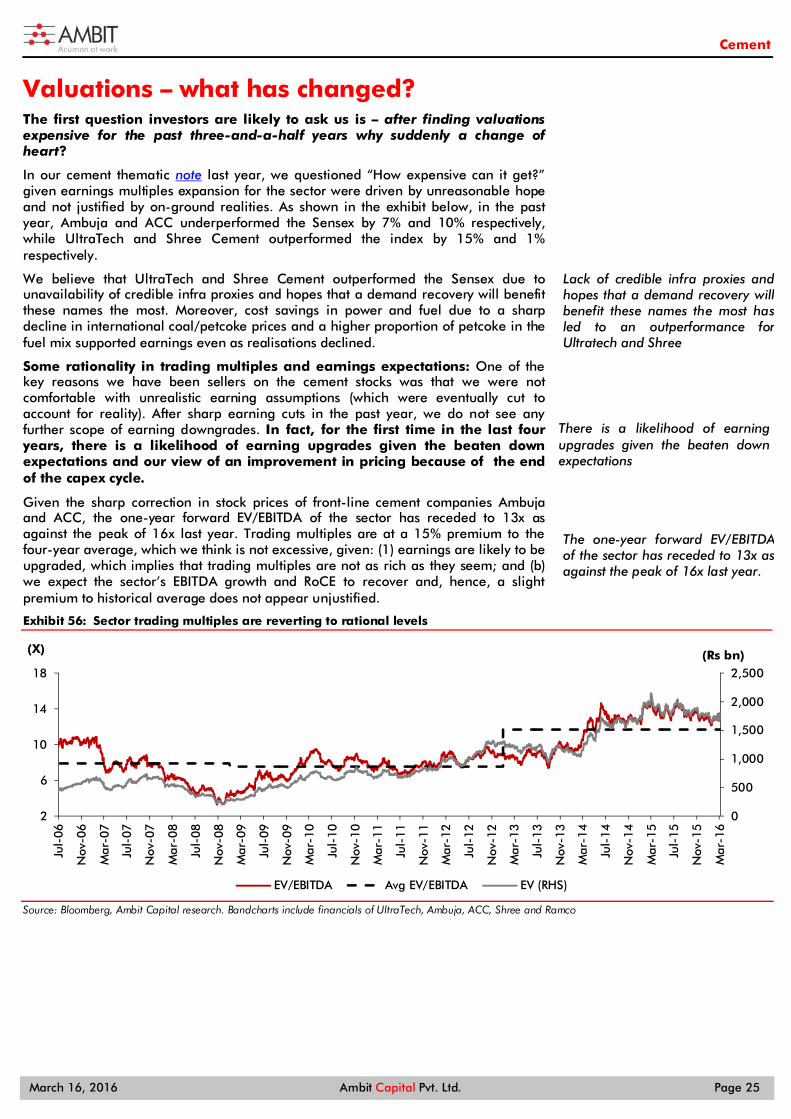

Valuations – what has changed? The first question investors are likely to ask us is – after finding valuations expensive for the past three-and-a-half years why suddenly a change of heart?

In our cement thematic note last year, we questioned “How expensive can it get?” given earnings multiples expansion for the sector were driven by unreasonable hope and not justified by on-ground realities. As shown in the exhibit below, in the past year, Ambuja and ACC underperformed the Sensex by 7% and 10% respectively, while UltraTech and Shree Cement outperformed the index by 15% and 1% respectively.

We believe that UltraTech and Shree Cement outperformed the Sensex due to unavailability of credible infra proxies and hopes that a demand recovery will benefit these names the most. Moreover, cost savings in power and fuel due to a sharp decline in international coal/petcoke prices and a higher proportion of petcoke in the fuel mix supported earnings even as realisations declined.

Some rationality in trading multiples and earnings expectations: One of the key reasons we have been sellers on the cement stocks was that we were not comfortable with unrealistic earning assumptions (which were eventually cut to account for reality). After sharp earning cuts in the past year, we do not see any further scope of earning downgrades. In fact, for the first time in the last four years, there is a likelihood of earning upgrades given the beaten down expectations and our view of an improvement in pricing because of the end of the capex cycle.

Given the sharp correction in stock prices of front-line cement companies Ambuja and ACC, the one-year forward EV/EBITDA of the sector has receded to 13x as against the peak of 16x last year. Trading multiples are at a 15% premium to the four-year average, which we think is not excessive, given: (1) earnings are likely to be upgraded, which implies that trading multiples are not as rich as they seem; and (b) we expect the sector’s EBITDA growth and RoCE to recover and, hence, a slight premium to historical average does not appear unjustified.

Sector trading multiples are reverting to rational levels Exhibit 56:

Source: Bloomberg, Ambit Capital research. Bandcharts include financials of UltraTech, Ambuja, ACC, Shree and Ramco

0

500

1,000

1,500

2,000

2,500

2

6

10

14

18

Jul-

06

Nov

-06

Mar

-07

Jul-

07

Nov

-07

Mar

-08

Jul-

08

Nov

-08

Mar

-09

Jul-

09

Nov

-09

Mar

-10

Jul-

10

Nov

-10

Mar

-11

Jul-

11

Nov

-11

Mar

-12

Jul-

12

Nov

-12

Mar

-13

Jul-

13

Nov

-13

Mar

-14

Jul-

14

Nov

-14

Mar

-15

Jul-

15

Nov

-15

Mar

-16

(Rs bn)(X)

EV/EBITDA Avg EV/EBITDA EV (RHS)

Lack of credible infra proxies and hopes that a demand recovery will benefit these names the most has led to an outperformance for Ultratech and Shree

There is a likelihood of earning upgrades given the beaten down expectations

The one-year forward EV/EBITDA of the sector has receded to 13x as against the peak of 16x last year.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 26

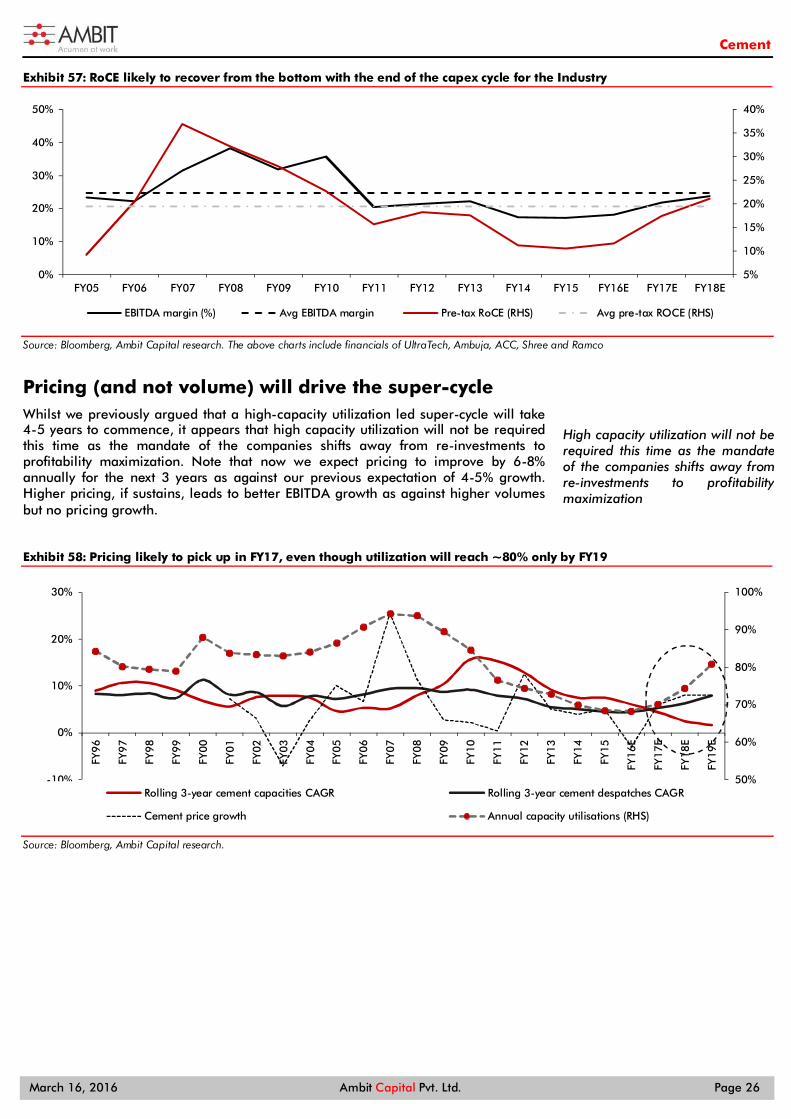

RoCE likely to recover from the bottom with the end of the capex cycle for the Industry Exhibit 57:

Source: Bloomberg, Ambit Capital research. The above charts include financials of UltraTech, Ambuja, ACC, Shree and Ramco

Pricing (and not volume) will drive the super-cycle Whilst we previously argued that a high-capacity utilization led super-cycle will take 4-5 years to commence, it appears that high capacity utilization will not be required this time as the mandate of the companies shifts away from re-investments to profitability maximization. Note that now we expect pricing to improve by 6-8% annually for the next 3 years as against our previous expectation of 4-5% growth. Higher pricing, if sustains, leads to better EBITDA growth as against higher volumes but no pricing growth.

Pricing likely to pick up in FY17, even though utilization will reach ~80% only by FY19 Exhibit 58:

Source: Bloomberg, Ambit Capital research.

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

EBITDA margin (%) Avg EBITDA margin Pre-tax RoCE (RHS) Avg pre-tax ROCE (RHS)

50%

60%

70%

80%

90%

100%

-10%

0%

10%

20%

30%

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

FY19

E

Rolling 3-year cement capacities CAGR Rolling 3-year cement despatches CAGR

Cement price growth Annual capacity utilisations (RHS)

High capacity utilization will not be required this time as the mandate of the companies shifts away from re-investments to profitability maximization

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 27

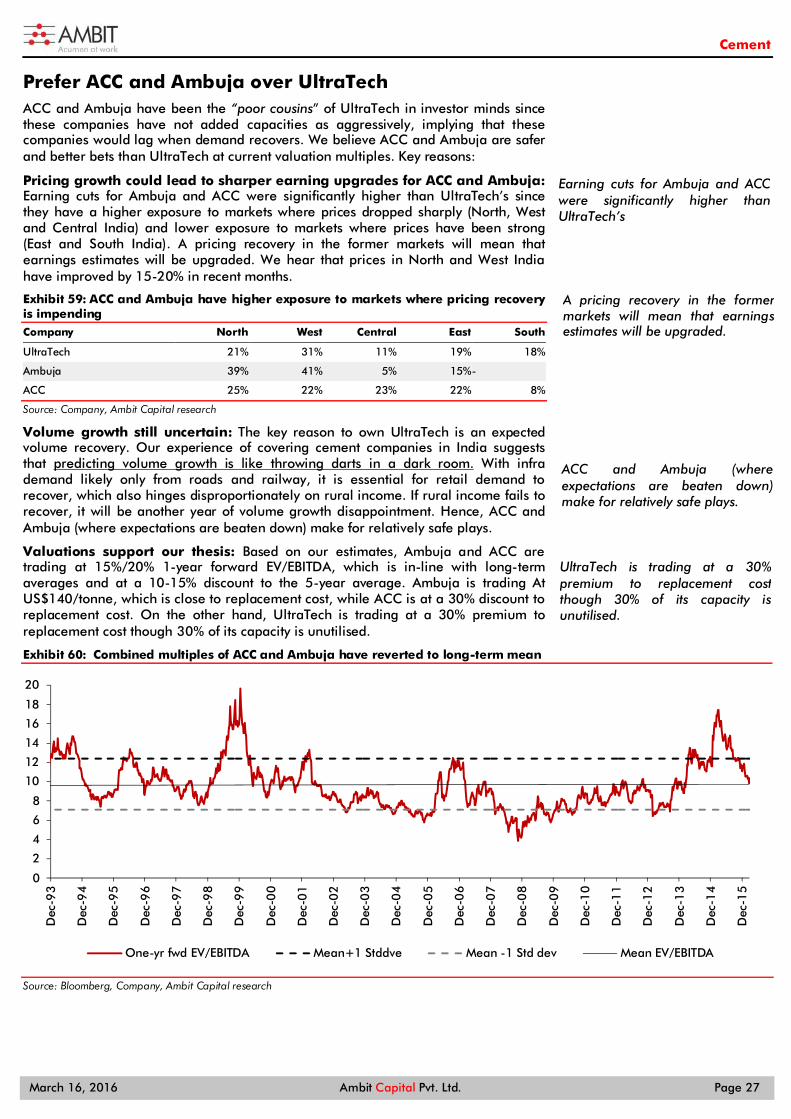

Prefer ACC and Ambuja over UltraTech ACC and Ambuja have been the “poor cousins” of UltraTech in investor minds since these companies have not added capacities as aggressively, implying that these companies would lag when demand recovers. We believe ACC and Ambuja are safer and better bets than UltraTech at current valuation multiples. Key reasons:

Pricing growth could lead to sharper earning upgrades for ACC and Ambuja: Earning cuts for Ambuja and ACC were significantly higher than UltraTech’s since they have a higher exposure to markets where prices dropped sharply (North, West and Central India) and lower exposure to markets where prices have been strong (East and South India). A pricing recovery in the former markets will mean that earnings estimates will be upgraded. We hear that prices in North and West India have improved by 15-20% in recent months.

ACC and Ambuja have higher exposure to markets where pricing recovery Exhibit 59:is impending Company North West Central East South

UltraTech 21% 31% 11% 19% 18%

Ambuja 39% 41% 5% 15% -

ACC 25% 22% 23% 22% 8%

Source: Company, Ambit Capital research

Volume growth still uncertain: The key reason to own UltraTech is an expected volume recovery. Our experience of covering cement companies in India suggests that predicting volume growth is like throwing darts in a dark room. With infra demand likely only from roads and railway, it is essential for retail demand to recover, which also hinges disproportionately on rural income. If rural income fails to recover, it will be another year of volume growth disappointment. Hence, ACC and Ambuja (where expectations are beaten down) make for relatively safe plays.

Valuations support our thesis: Based on our estimates, Ambuja and ACC are trading at 15%/20% 1-year forward EV/EBITDA, which is in-line with long-term averages and at a 10-15% discount to the 5-year average. Ambuja is trading At US$140/tonne, which is close to replacement cost, while ACC is at a 30% discount to replacement cost. On the other hand, UltraTech is trading at a 30% premium to replacement cost though 30% of its capacity is unutilised.

Combined multiples of ACC and Ambuja have reverted to long-term mean Exhibit 60:

Source: Bloomberg, Company, Ambit Capital research

0

2

4

6

8

10

12

14

16

18

20

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

One-yr fwd EV/EBITDA Mean+1 Stddve Mean -1 Std dev Mean EV/EBITDA

Earning cuts for Ambuja and ACC were significantly higher than UltraTech’s

A pricing recovery in the former markets will mean that earnings estimates will be upgraded.

ACC and Ambuja (where expectations are beaten down) make for relatively safe plays.

UltraTech is trading at a 30% premium to replacement cost though 30% of its capacity is unutilised.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 28

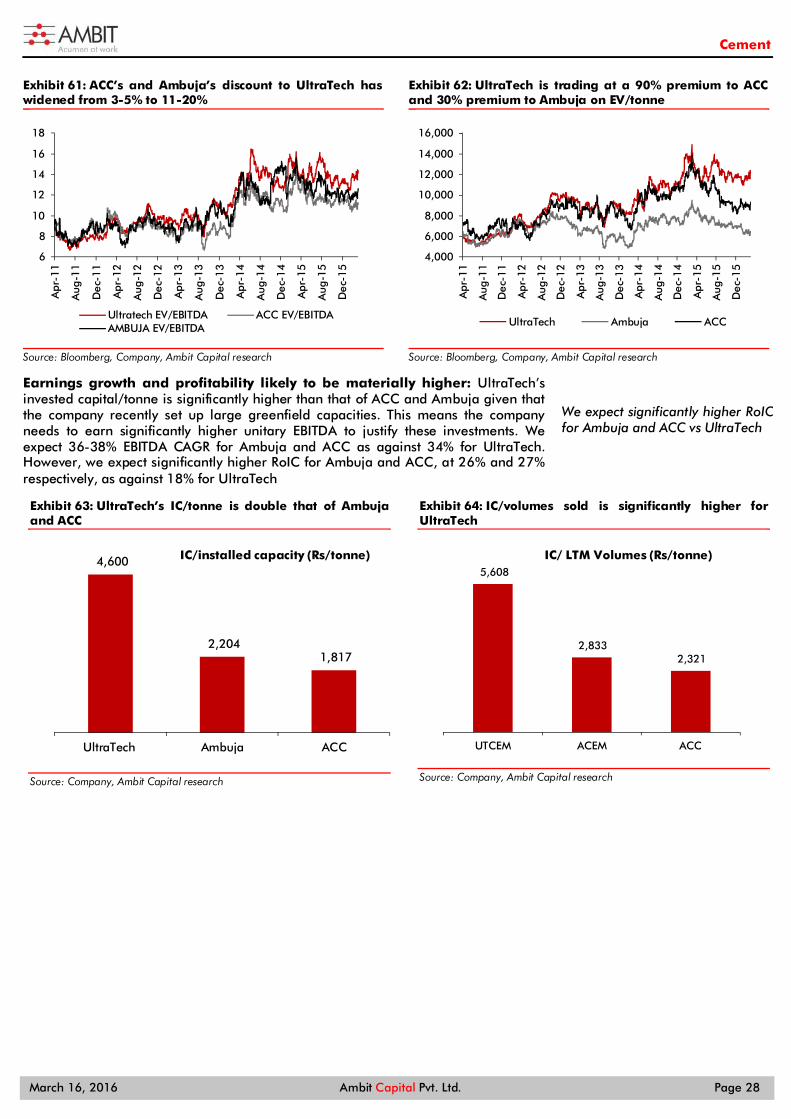

ACC’s and Ambuja’s discount to UltraTech has Exhibit 61:widened from 3-5% to 11-20%

Source: Bloomberg, Company, Ambit Capital research

UltraTech is trading at a 90% premium to ACC Exhibit 62:and 30% premium to Ambuja on EV/tonne

Source: Bloomberg, Company, Ambit Capital research

Earnings growth and profitability likely to be materially higher: UltraTech’s invested capital/tonne is significantly higher than that of ACC and Ambuja given that the company recently set up large greenfield capacities. This means the company needs to earn significantly higher unitary EBITDA to justify these investments. We expect 36-38% EBITDA CAGR for Ambuja and ACC as against 34% for UltraTech. However, we expect significantly higher RoIC for Ambuja and ACC, at 26% and 27% respectively, as against 18% for UltraTech

UltraTech’s IC/tonne is double that of Ambuja Exhibit 63:and ACC

Source: Company, Ambit Capital research

IC/volumes sold is significantly higher for Exhibit 64:UltraTech

Source: Company, Ambit Capital research

6

8

10

12

14

16

18

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Apr

-15

Aug

-15

Dec

-15

Ultratech EV/EBITDA ACC EV/EBITDAAMBUJA EV/EBITDA

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Apr

-15

Aug

-15

Dec

-15

UltraTech Ambuja ACC

4,600

2,204 1,817

UltraTech Ambuja ACC

IC/installed capacity (Rs/tonne)5,608

2,833 2,321

UTCEM ACEM ACC

IC/ LTM Volumes (Rs/tonne)

We expect significantly higher RoIC for Ambuja and ACC vs UltraTech

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 29

Regional peers likely to underperform We find the regional leaders, Shree and Ramco, expensive and, hence, less favorable plays currently. Though we have a BUY on Orient Cement, we believe the stock may underperform in the short term due to delayed utilisation ramp-up of the recently commissioned Karnataka plant.

Shree Cement – champion franchise but too expensive: No other Indian company has managed to build a leaner cost/capital employed cement firm. However, we believe current valuations of 17x FY17E and 13.5x FY18E EV/EBITDA adequately factor in the quality of the franchise, leaving little upside. If we were to change the pricing for Shree Cement as per our pricing for ACC/ Ambuja, our valuation rises to `12,000, implied valuation of 13x FY18 EBITDA; this also leaves ~4% upside

Ramco Cement – The company has surprised positively with significant cost savings and sustained pricing discipline, resulting in industry leading EBITDA/tonne. However, the stock trades at 10x FY17E and 9x FY18E EV/EBITDA, which are excessive for a company with a single region exposure and limited possibility of further price increases from already elevated levels.

Orient Cement – While we like the company for its low cost structure and efficient capital management, we remain concerned about weak demand in Andhra Pradesh and Maharashtra and low utilisation in its recently commissioned plant at Karnataka. We are likely to downgrade our estimates and do not expect outperformance in the short-to-mid term.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 30

Ranking the cement peers We rank the major cement companies on four key parameters such as (a) scale and brand, (b) cost efficiency, (c) capital efficiency and (d) Balance sheet strength. We segment the companies in two buckets – US$1bn and above market capitalization and others.

Ambuja stands as the best player amongst the cement majors due to strong cost and capital efficiency and cash-rich traits. OCL ranks #1 on our framework due to a reasonable brand in its region and strong capital discipline and Balance Sheet strength

Ambuja ranks as the best company on our ranking framework Exhibit 65:

Company Scale and Brand

Cost efficiency

Capital efficiency

B/S Strength

Overall Rank

Ambuja 2 3 1 2 1

ACC 3 5 3 1 2

Shree 5 1 2 4 3

UltraTech 1 4 6 3 4

Ramco 4 2 4 5 5

Dalmia 6 4 5 6 6

Source: Company, Ambit Capital research

Numbers behind our ranking Exhibit 66:

Parameters Avg. Realisation per tonne (FY13-

9MFY16)

Mkt share (FY13-

9MFY16)

Avg. Cost per tonne

(FY13-9MFY16)

Cost/tonne CAGR

(FY13-9MFY16)

Invested Capital

per tonne FY16

Average RoIC

(FY13-9MFY16)

Net Debt/ Equity (FY13-

9MFY16)

Int/EBITDA (FY13-

9MFY16)

Ambuja 4,405 8.7% 3,551 3% 1,787 28.1% -0.48 0.06

ACC 4,500 9.7% 4,075 5% 2,387 29.3% -0.15 0.04

Shree 3,914 5.7% 3,394 -3% 2,221 19.5% -0.01 0.06

UltraTech 4,349 17.3% 4,294 2% 3,722 11.1% 0.26 0.13

Ramco Cement 4,493 3.2% 3,569 1% 3,714 11.4% 0.68 0.17

Dalmia Bharat 4,400 3.1% 3,871 3% 3,690 10.9% 1.83 0.48

Source: Company, Ambit Capital research

OCL ranks as the best company on our ranking framework for non-major Exhibit 67:manufacturers

Company Scale and Brand

Cost efficiency

Capital efficiency

B/S Strength

Overall Rank

OCL 3 6 1 1 1

Sagar Cement 7 2 3 3 2

Jk Lakshmi Cement 4 1 4 6 3

India Cement 1 3 6 4 4

Mangalam Cement 5 5 2 5 5

Heidelberg Cement 6 4 6 2 6

JK Cement 2 7 7 7 7

Source: Company, Ambit Capital research

Numbers behind our ranking Exhibit 68:

Parameters Avg. Realisation per tonne (FY13-

9MFY16)

Market share (FY13-9MFY16)

Avg. Cost per tonne

(FY13-9MFY16)

Cost/tonne CAGR (FY13-9MFY16)

Invested Capital per tonne FY16

Average RoIC

(FY13-9MFY16)

Net Debt/Equity (FY13-9MFY16)

Int/EBITDA (FY13-9MFY16)

OCL 5,173 1.6% 4,255 1.1% 1,841 15.1% -0.02 0.30

Sagar Cement 3,561 0.6% 3,629 -5.7% 6,347 22.7% 1.15 0.29

Jk Lakshmi Cement 3,692 2.4% 3,182 2.8% 2,787 10.6% 1.16 0.77

India Cement 4,347 3.9% 3,872 -2.7% 3,029 6.6% 0.54 0.48

Mangalam Cement 3,607 0.9% 3,338 4.3% 2,332 12.2% 0.69 3.55

Heidelberg Cement 3,534 1.6% 3,324 4.1% 2,611 7.8% 0.81 0.47

JK Cement 4,963 2.5% 4,279 3.7% 3,423 13.0% 1.23 0.62

Source: Company, Ambit Capital research

Ambuja stands as the best player amongst the cement majors due to strong cost and capital efficiency and cash-rich traits.

Cement

March 16, 2016 Ambit Capital Pvt. Ltd. Page 31