Embed Size (px)

Citation preview

August 2 Mr. DougDivision U.S. DepFederal S500 WesChicago,

Sent via e Re: R O Dear Mr. On AugusubmittedDepartmDecisioninappropAs a resuabout the

I. Imp Deliverinintent to containedCarl Barn

1 The DepaExhibit 1).

21, 2016

glas Parrott Director

partment of EStudent Aid,t Madison S, IL 60661

email to Dou

Request for ROPEIDs:

. Parrott:

ust 11, 2016d change ofent notified

n to CEHE, triate and unult, the mede Decision be

roper Poli

ng its Decisipoliticize th

d egregious, ney Living T

artment issued The Departm

Education School Part

Street

uglas.Parrot

Reconsiderat00367400 02110800 02594300 03120300

, 44 monthsf ownership CEHE of itsthe Departm

nsubstantiatedia, CEHE eefore CEHE

itical Mot

on to the mehe CEHE chunsubstanti

Trust (“Trust

a press release

ment did not sen

ticipation Te

tion concerni– Stevens H– California– CollegeA– CollegeA

s after the Ceapplications

s decision onment ambushed accusationmployees, it

E’s Chief Exe

tive and D

edia before phange of owated chargest”), denies C

e and redacted nd its decision

eam – Chicag

ing: Henager Colla College Samerica Denvmerica – Fla

enter for Exs for the coln the applica

hed CEHE bns, vilifying ts bank, busecutive Offic

enial of Fu

providing a cwnership pros against CE

CEHE fundam

copy of its decto CEHE until

go

lege an Diego ver agstaff

xcellence in lleges listedations (“Dec

by distributinCEHE and

siness associcer.

undament

copy to CEHocess. The a

EHE, the Colmental fairn

cision to medial 10:42am easte

Higher Edud above (the cision”). Pring a press rethe College

iates, and co

tal Fairne

HE1 reveals tadvance preslleges’ forme

ness and due

a outlets at 10:3ern (see Exhib

cation (“CE“Colleges”)

ior to sendinelease conta

es’ former owolleagues lea

ss and Jus

the Departmss release, wer owner, anprocess.

32am eastern (it 2).

EHE”) ), the

ng the aining wner. arned

stice

ment’s which nd the

(see

The orchadvancinevidencesenior exSecretarySecretary

message while haDepartmSecretaryallegationrights pu The Secr

want to cthe convclose.” IDepartmWhy? BeCEHE pColleges scholarshhave provparticipanhas helpebenefit. For the threateninagenda-d Even tho

2 See Exhib3 See Exhib

hestrated timng a political that this D

xecutives in y Ted Mitchy of Educati

to anyone wanging onto ent’s basis fy that CEHEn is false; a

ursuant to the

retary’s quo

convert to noersion is theIt is disturbent’s Decisiecause CEHEresented clebenefit the

hips and granvided 100% nts to take ted over 3,00

Departmentng claims) a

driven judgm

ough CEHE

bit 3 – letter frbit 4 – CEHE G

ming of thel agenda andecision was the Departm

hell, made aion King sta

who thinks cthe financia

for the DecisE’s change oand is intende Higher Edu

ote is follow

on-profit (sice owner of bing that thon contains E’s Collegesear evidencepublic2. Fonts to studenfree GED p

the GED ex00 people ea

t to issue aas the means

ment and effo

has operated

om Duane MoGrants and Sch

e press reled not on an

based uponment of Educalarming andated that “Th

converting toal benefits: sion. This staof ownershipded to intimucation Act o

wed by one

c) status neethe for-prof

he Under Seno facts, ev

s demonstrabe directly toor example, snts totaling opreparatory tuam) througharn their GE

a press reles of informinort to smear

d its College

rris attorney toholarships sinc

2

ease indicateunbiased ap

n a political cation, Secred unprecedehis [denial o

o non-profitdon’t waste

atement alsop was an attemidate otherof 1964, as a

from Under

ed to benefitfit school, thecretary wo

vidence, or sbly do benef

o Under Secsince Januarover $28 milutoring and h its Good NED for free!

ease such ang a collegeCEHE Colle

es as nonpro

o Under Secretae January 2013

es that thispplication of

agenda is tetary of Eduented direct of nonprofit

t (sic) statuse your time.”o includes a gempt to avoi

colleges froamended (“H

r Secretary T

t the public. hat doesn’t ould make support for sfit the publiccretary Mitcry 2013, CEHllion dollars3

instruction (Neighbor Ini

Such effor

as this (wite of a signifieges.

fit institution

tary Ted Mitch3.

s Decision wf law and regthe fact that ucation John

quotes in tt status] sho

s is a way to” This stategratuitous alid regulatoryom lawfullyHEA”).

Ted Mitche

If the primameet the basuch a statsuch an egrec. In fact, inchell demonHE’s Colleg3. Further, C(including paitiative. Thrts provide s

th false, inicant decisio

ns since Dec

hell.

was based gulation. Fu

two of the n King and Uthe press relould send a

o avoid overement revealllegation fromy oversight. y exercising

ll: “Schools

ary beneficiaar. It’s not ement whenegious allegan the fall of 2nstrating howges have awaCEHE’s Colaying the cois program substantial p

flammatory,on exemplifi

cember 31, 2

upon urther most

Under lease. clear

rsight ls the m the That their

s that

ary of even

n the ation. 2015, w the arded lleges ost for alone

public

, and ies an

2012,

the Depaprofit” foCEHE onDepartmthe basisall of ouDecisionregulatiounfounde The Depgovernmits principroprietaactivities(before iinfluence

II. The This Deccollege sdiscreditenow withalleged csudden dagainst pby filing 2015, Mrmany falnew regu After rel

4 See Exhib5 See Exhib

artment did or Title IV n March 15,ent implorin for the Dep

ur requests an is based o

ns, ignores ed surmise o

partment’s pment officials

ipals) simplary institutios. It is particinforming the members o

Ultimate

cision is bassector. Evided former Dh the Centurcollusion wideparture froproprietary c

a complaintr. Shireman lse allegationulations appl

lease of the

bit 5 – Robert bit 6 – NY Tim

not give CEregulatory p 2016. Sinc

ng the Deparpartment’s pand then amon a misappcontrolling

or conjecture

political age to impugn tly because tons. The Decularly immohe institutio

of the public

Aim of th

sed upon thdence show

Department ory Foundatioith short-sellom the Depaolleges that t against Keprovided in

ns, inventedlicable to for

New York

Shireman Back

mes Article

EHE any nopurposes untce then, CEHrtment to meosition. Ins

mbushed CEplication of Internal Rev

e contradicte

nda is not the characterthe nonprofiecision assigoral for the g

on and afforor seek to af

e Departm

he bias and s that the Dof Educationon, a self-prlers of publrtment of Edhad convertiser College

nformation tod a claim thar-profit colle

k Times arti

kground

3

otice of its til the Depa

HE has submeet with CEHstead of meeEHE with itsf law, disregvenue Servicd by objectiv

a proper bar and credibi

fit organizatigns maliciougovernment rding it an ffect judicial

ment’s Dec

animus of cDecision is dn Deputy Uroclaimed “plically tradedducation, Mrted to nonpre’s former owo the New Yat CEHE’s aeges5.

cle, a group

belief that artment sent

mitted at leasHE, in persoeting with CEs Decision. gards the pce (“IRS”) pve facts.

asis for thisility of a lawion acquired

us motives toto "poison topportunityl or regulato

cision

certain loud driven by a

Undersecretarprogressive”d proprietarr. Shireman

rofit corporawner, Dr. ArYork Times acquisition o

p of 21 legi

the Colleget a request fst eight urgeon or by teleEHE, the De As discu

plain languaprecedent, an

s Decision. wful nonprofd what had o perfectly mthe well" wi

y to respondory processes

critics of than agenda orry Robert S” think tank)ry colleges i, in 2014, la

ations. He inrthur Keiserfor an artic

of the Colleg

islators sent

s remained for documennt requests t

ephone, to reepartment dussed belowge of applind/or relies

It is wronfit institution

previously moral and laith a press red) – designes.

he private criginating w

Shireman (w). Followinin 20104 an

aunched an anitiated his ar. Then, in Mcle which, amges was to e

t a letter to

“for-nts to to the eview enied

w, the icable upon

ng for n (and

been awful elease ed to

career with a who is ng his nd his attack attack March mong evade

then

Secretarytransactiothis letterdemandscolleges.Covert FFoundatiinaccuracalmost coDepartmadvancingovernedDecision

III. C C

CEHE bemeasurabstudents.2-year purecent daaverage graduatiothan puboperates versus 16have an abetter). 15.9% fomeasures

6 See Exhib7 See Exhib8 See Exhib9 See Exhib

y of Educatons involvinr persuaded to discredi Mr. Shirem

For-Profit” iion contactecies that Mrompletely adent’s Decisi

ng a politicad solely by n without tak

CEHE’s MColleges

elieves it is bly better th On one imublic collegeata from thgraduation

on rate of 27lic 2-year coColleges.

6.2% for Araverage gradAnd CEHE

or Salt Lake s, such as tim

bit 7 – Democrbit 8 – Covert Fbit 9 – CEHE Rbit 10 – IPEDS

tion Arne Dng for-profitthe Departm

it and prohiman continuin October 2

ed CEHE for. Shireman dopted Mr. Sion. In doinal agenda.

existing laking into acco

Mission Ben

important fohan governm

mportant meaes in the stat

he Departmerate of 33

7.4%; CEHEolleges. SimCEHE’s Corizona commduation rate

E’s College iCity Comm

me-to-compl

rat Letter to DuFor-Profit RepResponse to CeS Graduation R

Duncan demt colleges be

ment to take wbit nonprofiued to advan20157. Prio

or comment.had planned

Shireman’s ang so, the De

This is legaws and regount any pol

nefits the P

or the Deparment 2-year asure, graduates where CEent’s IPEDS.5% and C

E’s Colleges,milar results olleges in Amunity colleof 33.3% vein Salt Lake

munity Collegletion, CEHE

uncan port entury Founda

Rate Data for C

4

manding thaeing mergedwhatever ac

fit corporationce his agen

or to publish. CEHE prd on includiagenda. Thaepartment hgally and mgulations anlitical agend

Public and

rtment to ackcommunity

ation rates, CEHE’s Colle

S system, CCalifornia’s , therefore, hhave been a

Arizona haveeges (159% ersus 28.2%e City, Utahge (81% bettE’s Colleges

tion Before “CCEHE Colleges

at the Depard into nonprction it couldons from conda by publhing this soromptly corring in his reat adoption inhas inapproprmorally wronnd the Depada.

d CEHE O

knowledge ty colleges. CEHE’s Coleges are loca

CEHE’s Collcommunity

have an averachieved in te an averagbetter). CE

% for Coloradh has a gradtter). On mas are superio

Covert” Report s and Commun

rtment rigorrofit corpora

d to appease ontrolling folishing a “st-called “studrected manyeport8. The ndicates the riately basedng. The Dartment mus

Operates G

that our ColOur Colleg

lleges perforated9. Accorleges in Ca

y colleges hrage graduatthe other stage graduatioEHE’s Colledo communiduation rate any other imr.

Published nity Colleges

rously scrutations6. Clethese legisla

ormer propritudy” titled dy”, the Cey falsehoods Departmentrue basis fo

d its DecisioDecision must reconside

Good

lleges’ resultges serve sirm better tharding to the

alifornia havhave an avte rate 22% bates where Con rate of 4eges in Coloity colleges of 28.8% v

mportant obje

tinize early, ators’ ietary “The

entury s and

nt has or the on on

ust be er the

ts are imilar an the most

ve an erage better

CEHE 41.9% orado (18%

versus ective

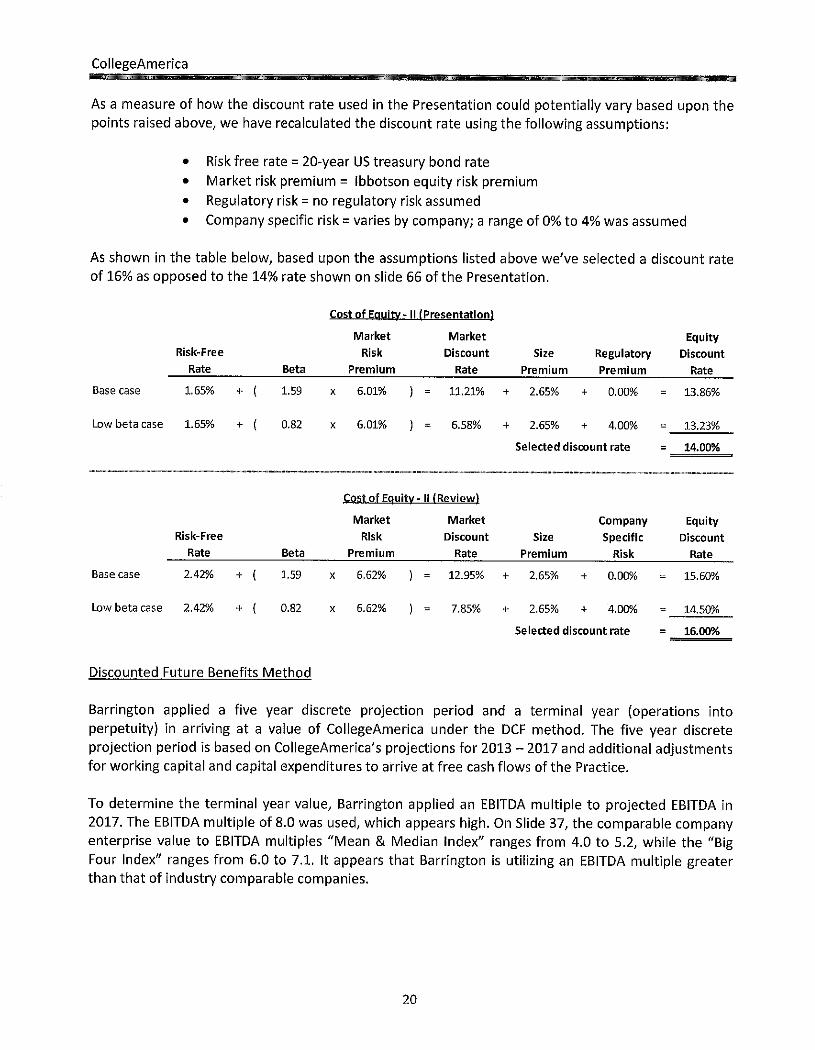

IV. B While threconsidelevied agputative regulatioattached The first (and his elementsowner hadebt paymin 34 C.inconsist

a. C 34 C.F.R

(1p

(i

(cR

CEHE’s §600.2. authorizeDepartm

10 See App11 See App

Basis for R

he Decisioneration10, CEgainst CEHEbasis for then. CEHE Appendix 2

charge is thalleged sign in 34 C.F.Rave inappropments and le.F.R. §600.2tent with the

CEHE’s Co

R. §600.2 def

1)(i) is owneart of the ne

(ii) is legallys physically

(iii) is determcontributionsRevenue Cod

Colleges saThe Colleg

ed to operateent does no

pendix 1 – Decipendix 2 – Misc

Reconsider

n contains EHE will fo

E, the College Decision. Baddresses o

11.

hat the Collenificant postR. §600.2. priately retaiease paymen2. As set law and pre

olleges Sati

fines a nonpr

ed and opert earnings of

y authorized located; and

mined by thes are tax-dede (26 U.S.C

atisfy all of tges are owne as a nonproot dispute th

ision Inaccuraccellaneous Det

ration

substantial ocus its reques’ former oBoth chargeother miscel

eges’ formert-transactionThe second

ined the bennts, which aforth below

ecedent.

sfy 34. C.F

rofit instituti

rated by onef which bene

to operate ad

e U.S. Interneductible in C. 501(c)(3).

the definitioned and opeofit organiza

his fact. And

cies and Misrepterminations in

5

misrepreseuest for recoowner, and thes are baselellaneous de

r owner’s con control) dod charge is tnefit of a conalso fail to cow, both of th

F.R § 600.2

ion as one th

e or more noefits any priv

as a nonprof

nal Revenueaccordance

nal elementserated by a ation in eachd, CEHE ha

presentations n the Decision

entations anonsiderationhe Trust. Th

ess and unsueterminations

ontinued partoes not confthat the Truntinued streonform to rehese determ

hat:

onprofit corpvate shareho

fit organizati

e Service to e with sectio

s for a nonpnonprofit co

h State whereas been dete

nd inaccuran on to two hese two cha

upported by es from the

ticipation inform to requust and the am of Title equired defin

minations are

porations orolder or indiv

ion by each

be an organon 501(c)(3

profit institutorporation. e it is physicrmined by t

acies warraprimary ch

arges serve aevidence, laDecision in

n the organizuired definitColleges’ foIV revenuenitional eleme inaccurate

r associationvidual;

State in wh

nization to w) of the Int

tion in 34 CCEHE is le

cally locatedthe IRS to b

anting harges as the aw, or n the

zation tional ormer s, via ments e and

ns, no

hich it

which ternal

C.F.R. egally d. The be an

organizatthe IRS C In the Deby a nonowner’s nonprofit

b. O

There is restricts, ownershi

“CE

an rol

The Depbecause contrary,Departm These tyreviewedthe collegapproval Universit The use arbitrarilythe Internowner bsomehow Over 40

tion to whicCode. The D

epartment’s nprofit corpoinvolvementt corporation

Operated b

nothing in or prohibits

ip or control

CEHE’s acqu

institution ile in the cont

artment claithe former , CEHE’s tent in its De

ypes of convd and approvges’ previou

of nonproty (2011), an

of the wory denying Cnal Revenueeing involv

w wrong, bad

years ago, t

ch contributiDepartment d

first charge,oration; ratht with CEHEn.

by a Nonp

the definitios, an institutil. The Depar

uisition of th

is acquired tinued opera

ims that the owner contitransaction ecision.

versions havved similar us owner remofit conversnd Remingto

rd “traditionCEHE’s chane Code. Furved with thed, or not “tra

the IRS publ

ions are tax does not disp

, the Departmher, the DepaE somehow

profit Corp

on for a nonion’s previourtment states

he colleges d

by a new owation of the i

subject traninues to mais in fact

ve been takconversions

mained involsions involvon College (2

nal” in this nge of staturthermore, the nonprofit

aditional” is

lished two re

6

deductiblepute this fact

ment does nartment’s demeans that

poration

nprofit institus owner fros that,

did not prese

wner and thinstitution.”

nsaction is naintain a role

more tradit

ing place foas part of c

lved followinving Ultima2011).

context is us without, ahe Departme

organizatiobaseless.

evenue rulin

in accordant.

not contest theterminationthe instituti

tution in 34om being inv

ent the trad

he former ow(emphasis a

not a “traditie in the nontional than

or decades. change of ong the transaate Medical

nothing moand in spite ent’s impliedon following

ngs, Revenu

nce with sec

hat the institn is that the ions are not

4 C.F.R. §60volved follow

ditional situa

wner no longadded)

ional” convenprofit corp

the one d

The Depawnership apaction. See tl Academy

ore than sleiof, controlli

d determinatg a change

ue Ruling 76

tion 501(c)(

tutions are oColleges fo“operated”

00.2 that defwing a chan

ation where

ger plays a

ersion transaporation. TOdescribed by

artment itselpplications wthe Departm (2015), K

ight of haning state lawtion that a foe to nonpro

6-91, 1976-1

(3) of

owned ormer

” by a

fines, nge of

action O the y the

lf has where

ment’s Keiser

d for w and ormer fit is

C.B.

15012, ana for-pro“Over onconsists osuch conthe Intern Similarlya for-proof the forschool. despite trevenue nonprofit The Dephis statussimply inmore thahave bee(Internal fact that The fact has explexemptioCEHE’s previouslfor-profit In this Dwell-estaIRS rule

12 See Exh13 See Exh14 See Exh

nd Revenue Rofit hospital ne-half of thof the stockh

ntrol, the nonnal revenue C

y, in Revenufit school’s r-profit schoAgain, the

the real proprulings dispt corporate b

artment’s pos as a substancorrect as an 70,000 noen founded a

Revenue Coa donor and

that CEHE licitly addreon, and the D

applicationly approved t to nonprofi

Decision, the ablished IRSd that an or

ibit 11 – Revenibit 12 - Revenibit 13 – Reven

Ruling 76-44formed a n

he board of holders [of t

nprofit corpoCode.

ue Ruling 76personal pro

ool. The forIRS ruled

perty lease pel the notibuyer follow

osition that tantial contrievidenced bonprofit organd funded bode) or statehis/her fami

is a public cessed the qDepartment ns. More

changes of it status with

Department precedent. rganization w

nue Ruling 76-nue Ruling 76-nue Ruling 66-

41, 1976-2 Cew nonprofidirectors of the selling fooration quali

6-441, Situatoperty and lermer ownersthat the noand post-saon that a f

wing a conver

the former obutor or due

by the Internanizations in

by a single de (Indiana) laily retain con

charity for taquestion of cannot denysignificantlyownership (

h circumstan

t is acting arFor exampl

would not b

-91 441 -219

7

C.B. 14713. fit corporatiof [the nonprofor profit hosfied for tax-

ion 1, the sueased the lans of the schonprofit corp

ale employmformer ownersion of statu

owner’s allee to his Trunal Revenuen the United

donor or famaw is not altentrol - even

ax purposes the relation

y controllingy, as indicaas recently a

nces similar t

rbitrarily in ie, in Revenu

be precluded

In Revenueon to purchaofit corporatspital].” Th-exempt statu

uccessor nonnd and buildool were theporation qua

ment relationer must havus transactio

eged control ust’s status ae Service’s d States tod

mily. Their nered or precif that contro

does not altnship of co

g IRS precedated above, as last year) to CEHE’s.

ignoring its ue Ruling 66d from estab

e Ruling 76-9ase and opetion purchas

he IRS still rus under sec

nprofit corpodings from then employedalified for tanship. Thesve no involvon regardless

over CEHEas a CEHE lpronouncem

day and the mnonprofit stacluded solelyol is perpetu

ter that concontrol to eldent that req

the Deparinvolving a

previous rec6-219, 1966-blishing its s

91, the ownerate the hossing the hosruled, that dection 501(c)(

oration purchhe former ow

d by the nonpax-exempt sse two publvement withs of its form.

E, whether dlender or bo

ments. Thermajority of

atus under fey by reason oual.

clusion. Theligibility fo

quires approvrtment itselfa conversion

cord of follo-2 C.B. 2081

section 501(

ers of spital. spital] espite (3) of

hased wners profit status lished h the .

due to oth, is re are them

ederal of the

e IRS r tax val of f has from

owing 14, the (c)(3)

status “mtrustee orCounsel control ointo the f

c. N The Depdefinitionwhen CEColleges The Depnonprofitinstitutio

“acorlaw

The privathe sameInternal R

Coopelitespoathanishaon othintecam

merely becaur merely becMemorandu

of a section foreseeable f

No Part of

partment’s snal elementsEHE makes ’ former own

artment’s tht found in tn as:

a school…orporations owfully inure,

ate inuremene language inRevenue Co

rporations, erated excluerary, or edorts competihletic facilitiimals, no paareholder or

propagandherwise proervene in (impaign on b

use the creatocause the orgum 33647 (O510(c)(3) orfuture, would

CEHE’s N

second chars in 34 C.F.debt paymener.

hree-part defhe Higher E

or institutioor associatio

to the benef

nt prohibitioncluded in thde:

and any cusively for rducational pition (but oies or equipart of the ner individual,da, or othevided in suincluding thbehalf of (or

or of the orgganization is Oct. 9, 1967rganization bd not preclud

Net Earni

rge is that R. §600.2 bents to the T

finition for aEducation A

on owned ons, no partfit of any pri

on containedhe definition

community religious, chpurposes, oronly if no ppment), or fet earnings no substan

erwise attemubsection (he publishingin oppositio

8

ganization (icontrolled b

7), the IRS by a founderde section 50

ngs Benef

CEHE’s inbecause the nTrust, and le

a nonprofit inAct (“HEA”)

and operatt of the net vate shareho

d in the HEAn of a nonpr

chest, fundharitable, scr to foster npart of its afor the preof which in

ntial part of mpting, to h)), and whg or distribun to) any can

if a trust) is by one indivOffice of Cr’s family, e01(c)(3) exe

fit a Privat

nstitutions dnet earningsease paymen

nstitution im). 20 U.S.C

ted by oneearnings of older or indi

A’s definitionrofit include

d, or foundcientific, tesnational or activities invevention of nures to the

the activitieinfluence l

hich does nuting of standidate for p

either the sovidual.” SimChief Counseeven when cemption.

te Individ

do not confs benefit a pnts to entiti

mplements thC. §1003 de

e or moref which inurividual.”

n of a nonprd in Section

dation, orgasting for pub

internationavolve the prcruelty to cbenefit of a

es of which legislation not participtements), anpublic office

ole or contromilarly, in Geel concludedcontrol is as

ual

form to reqprivate indives owned b

he definitionfines a nonp

e nonprofit res, or may

rofit is essenn 501(c)(3) o

anized and blic safety, al amateur rovision of children or any private is carrying (except as

pate in, or ny political e.

olling eneral d that sured

quired vidual y the

n of a profit

ntially of the

Indeed, binuremenestablishthat the imposed 501(c)(3) When th501(c)(3)purchaseoperation Federal negotiateregardlescontract gCir. 199regulatioincluding Treasurynot applyotherwiseand (vii).an indiviTreasuryother procontract tSee Treaincorporageneratedthe paymcash-flow Prior to accordan

before the Hnt under Seed meaning nonprofit hthe require

) by tracking

e HEA was ) to permit assets at fa

ns. Comm’r

courts haveed at arm’s ss of the regives a party9). The IRns pertain t

g a nonprofit

y Regulationy to fixed pe constitute . An initial cidual who w

y Regulationoperty specifthat is paid o

asury Regulaate an amoud by activitiment amounw based form

CEHE’s Dence with the

EA was adoection 501(c

of private iad to be a ement that g the particu

enacted, fedtax exempt

air market vv. Johnson,

e clarified tlength with lative bargay over the exRS formally to the receipt corporation

n 53.4958-4 ayments maan excess b

contract is dwas not an

n 53.4958-4(fied in an inor transferreation 53.495unt that depeies of the ornt or whethemula to deter

ecision, the e IRS’s int

opted in 1965c)(3) of the inurement pr501(c)(3) ta nonprofitlar language

deral courts t nonprofit value and to267 F. 2d 38

that this Tra person h

aining strengxempt entity

adopted thpt of privatn having tax

provides thaade pursuantbenefit transdefined as a b

insider imm(a)(3)(iii). Anitial contracd in exchang8-4(a)(3)(ii)

ends on futurganization) er payment rmine the am

Departmentterpretation

9

5, the IRS hInternal R

rohibition totax exempt t organizatioe of private b

had interprecorporations

o repay the 82 (1st Cir. 1

ransactional having no prgth of the p

y. Cancer Cohis position e benefits oexempt statu

at the privatt to an initiaaction. Seebinding writtmediately prAnd a fixedct or determge for the pr)(A). Regulure specified

if no persois made.

mount and tim

t has consisof private

had developeRevenue Codo control in

entity in 2on be able benefit in 50

eted the privs to borrowdebt with re1959) (“Tran

Exemption rior relationsparties or thouncil, Inc. v

in Treasuryor inuremenus under 50

te inuremenal contract, ee Treasury Rtten contract rior to enter

d payment mmined by a firovision of splations provid events or con exercisesThese regu

ming of paym

stently interpinurement

ed an interprde. Congrethe HEA.

20 U.S.C. §to satisfy

01(c)(3).

vate inuremew money froevenue fromnsactional E

applies to ship with thhe resultant v. Comr., 165y Regulation

nt from a ta1(c)(3).

nt prohibitioneven if such

Regulation 5between an ring into th

means an amixed formulapecified servide that a fixcontingencies discretion ulations permments.

rpreted 34 Cwhen rulin

retation of press intendedRather than § 1003, Con

requiremen

ent prohibitiom an insidm the tax exxemption”).

any transahe exempt e

control tha5 F. 3d 1173n 53.4958.

ax exempt e

n of 501(3) h payment w53.4958-4(a)

organizationhe contract. mount of caa specified ivices or propxed formulaes (e.g., revewhen calculmit the use

C.F.R. § 600ng on chang

rivate d this

state ngress nts of

on of der to xempt

action entity, at the 3 (7th The

entity,

does would )(3)(i) n and See

ash or in the perty. a may enues lating

of a

0.2 in ge in

ownershithe Depanet earniDepartmbalance (“GAAP VirtuallyUniversitdebt at thhad $1.5institutiorevenue Departma nonproheld by p(in CEHEdebt servSuch a po The DepCEHE’s debt is hpaymentsconsistenpayment definitionDepartminterpreta The Depa

“Inthe

15 See Exh16 See Exh

ip or controlartment, in Cings benefitient also ignsheets and i”) and Finan

y every nonpty, the alma he end of 20 billion dollns, like CEis paid to ent, for the f

ofit institutioprivate indivE’s Decisionvice and/or osition by th

partment canColleges, orheld by ones to one orntly and rout

of debt senal element ent must ration of the d

artment goes

n the acquise benefit of a

ibit 14 – Columibit 15 – Stanfo

l applicationCEHE Decising a privatenores the maincome statencial Accoun

profit collegmater of U.S

01215. Stanfolars of debt

EHE, fail theindividuals

first time, taon in 34 C.Fviduals or trun) would merent paymen

he Departme

nnot discrimr indeed, anye or more r more indivtinely (by itservice or reprohibiting treconsider idefinitional

s on to claim

sition here, ta continued s

mbia Universitford University

ns followingsion, to nowe individual anner in whements pursnting Standar

ge in the U.S. Secretary ord Universiat the end oe definition

or entitiesakes the posi.R. §600.2 i

usts. If consiean that events fails to mnt is untenab

minate and y one institutindividuals viduals is as actions andent to one the paymentits determinelements it h

m that:

the Transacstream of titl

ty Debt as of 20y Debt as of 20

10

g an institutiow conclude t

is contrary ich debt (losuant to Genrds Board (“

.S. has debtof Educatioty, the alma

of 201316. Iin 34 C.F.

who hold ition that an if the instituistently and

ery nonprofitmeet the deble.

selectively tion or groupis irrelevan

also irrelevad approvals)or more pr

t of net earnnation in Chas applied t

tion was strle IV revenue

012 13

on’s conversthat debt serto IRS rulin

oan and leasnerally Acc“FASB”) sta

t and incurson John Kinga mater of Us it the DepR. §600.2 bthe debt? institution f

ution uses pafairly appliet institution

efinitional el

interpret itsp of institutint. Whetheant. The D) establishedrivate indivinings benefitCEHE’s cato other nonp

ructured so es…”

sion to nonprvice and leangs. This cse payments)epted Accou

andards.

s lease expeg, had $1.28

Under Secretapartment’s pobecause par In CEHE

fails to meetart of its reved, the Depain the Unit

lement in 34

s regulationions. Whetheer an institu

Department hd that a nonpiduals doests to private ase and eqprofit institu

that the Tru

profit status.ase paymentconclusion b) is classifieunting Stan

enses. Colubillion dolla

ary Ted Mitcosition that

rt of their tuE’s Decisiont the definitivenue to payartment’s posed Sates tha4 C.F.R. §6

ns differentlyer an institutution makeshas, for decprofit institut not violateindividuals.

qually applyutions.

ust retained

. For ts are

by the ed on dards

umbia ars of chell, these

uition n, the ion of y debt sition at has 600.2.

y for tion’s s rent cades, tion’s e the The

y the

This is astatemencorporati

than a le The TrusprohibiteCode. Thif CEHEstate or fCEHE toDepartmwithout a The Depof principnot suppDepartmand otherepay loanotes is ainstitutio In realitymight deconcern aand insurbest inteschedule had availsame as phave no olength lo The Depcontrol o

an extreme mnt as the fouion under In

ender.

st has retaineed from doinhe Trust is n

E had obtainfederal law (o the Trust isent’s considany factual o

artment’s copal in amou

ported by eient is aware

er financial ans to the exalmost identns.

y, this constrefault on theas to whethere financial rest of the Cfor the repa

lable cash afprofits. Oncobligation toan is not the

artment furtof the Colleg

mischaracterundation for ndiana law a

ed no right, tng so under nothing moreed commercincluding th

s anything otderation of thor legal supp

onclusion thants equal to ither comme, the debt is institutions xtent of avaitical to the d

ruct for repaye notes. Theer CEHE woviability of Colleges (as

ayment of thfter satisfyince the debt io the Trust. e legal or fun

ther asserts tges. On the

rization of wa refusal to

and Title IV

title or interboth Indiana

e than a credcial financin

he Internal Rther than a bhe change o

port, is arbitr

at provisionsthe Excess

ercial lendinrequired, byreduce the ilable funds.definition of

yment of thee Colleges’ ould be able

the Colleges opposed toe principal.

ng all operatis paid in fuIn summary

nctional equi

that negativecontrary, the

11

what actuallyo recognize

regulations

rest in any paa law and se

ditor of CEHng. It is sig

Revenue Codbona fide indof ownershipary and capr

s in CEHE’sCash Flow,

ng norms oy applicable risk of non. The definif this term in

e notes was institutionalto pay its de

es after closio the Colleg Instead, CE

ional and caull (or refinany, the mandaivalent of a s

e covenants ese covenan

y occurred aCEHE’s sta. The Trus

articular streection 501(c

HE - just as a gnificant thatde) under whdebtedness fop applicationricious.

s debt, requiare distribu

or the facts law, to be on

npayment byition of “Exn the loan d

designed to l accreditor, ebt to the Truing, the partges’ former EHE was reqapital expendanced with a atory prepaymstream of inc

in the notesnts show that

and the Depatus as a bon

st is and wa

eam of revenc)(3) of the Ia commercialat the Decisihich indebtedfor all purposns). To con

iring mandatution of prof

of the trann market ter

y requiring txcess Cash Fdocuments o

mitigate anyACCSC, st

ust. To addrties determinowner) not

quired to payditure needsdifferent le

ment of princome to ben

s are evident the obligat

artment usena fide nonp

as nothing m

nue and is inInternal Revl lender wouion referencedness incurreses (includinnclude other

tory prepaymfits to the Trnsaction. Arms. Many bthe borrowe

Flow” in CEof major fina

y risk that Ctrongly exprress this conned it was it to have a y its debt wh. Cash is nonder) CEHE

ncipal of an aefit the Trus

nce of the Trions and deb

s this profit

more

ndeed venue uld be es no ed by

ng the rwise,

ments rust is

As the banks ers to

EHE’s ancial

CEHE essed

ncern, in the fixed hen it ot the E will arms’ st.

rust’s bt are

not, in anand the nnotes witwere reqindicia of Finally, faudited tbeing cocontinue never allCollegesDepartmactually cperspectiowner ev With restransactioCollegesconsidereCEHE BColleges CEHE’s owner agin long-tnegotiateindependperiods ohired an negotiati Congress

17 See Exh18 All of thDepartmen

ny way, a shnegative covth a major f

quired to be f the Trust h

for almost tthe transactimpleted, theto be invol

leged or con’ former owent should cost the Colive, the mergver entered in

spect to leaon, had som’ former owed a stream

Board of Direhad leases.

Colleges leagreed to do sterm leases e on the bedent manner,of rent abate

independenons with Mr

s was aware

ibit 16 – Accou

he information nt in CEHE’s r

haring of provenants in Cfinancial instreflected in

having contro

two years, thon itself ande IRS has nlved with thncluded that

wner or to thhave done) lleges’ formeger with CEHnto.

ses and leame exiting leawner. Howev

of “net earnectors asked. This requasing space so. Howeve

at favorablhalf of the , negotiatingement. The nt attorney ar. Juhlin.18

e that colleg

unting of Tranand evidence oesponses to the

ofits. NegatCEHE’s notetitution. CE

n the transacol of CEHE

he IRS has d CEHE’s F

not concludehe surviving

there is anye Trust. Thon this tran

er owner apHE was the

ase expensease obligatiover, as statednings” flowid the Collegeuest was solin buildingsr, before dole rates. MCEHE Boa

g long-term lformer ownand an inde

ges were con

saction for Carof independente Department’s

12

tive covenanes are muchEHE’s negatction. The nand the Coll

conducted aForm 990 taxed that the fo nonprofit oy inappropri

he IRS has onsaction, whproximatelyleast benefic

- it is trueons in proped above, CEHing to a prives’ former olely due to owned by ting so, the C

Mr. Eric Juhard of Direcleases that iner did not p

ependent rea

nverting to n

rl Barney t re-negotiations March and Ju

nts are custoh less restrictive covenannegative covleges.

audits of thix return. W

former owneorganizationiate benefit

obviously dohich shows

y $77 millioncial transact

e that the Certies owned HE’s paymevate individuowner to divthe fuss cri

the CollegesCEO and Bohlin, CEHEctors and dncluded reduparticipate inal estate bro

nonprofits u

ns of the Collegune 2016 docum

omary in comctive than tynts reflect mvenants are

is transactioWhile the auer, as a sole n. Furtherm

or inuremenone the arith

that the CEn dollars17. tion that the

Colleges, at by entities

ent of rent exual. Moreovest the real itics had be

s’ former owoard of CEHE’s CEO, wdid so in a uctions in renn the negotiaoker to cond

using seller

ges’ leases wasment requests.

mmercial lenypically foun

market normsnot, in any

on. The IRSudits are just

member, camore, the IRS

nt flowing thmetic (whicEHE mergeFrom a finaColleges’ fo

the time ocontrolled bxpense cann

over, in 2015estate wher

een raising awner. The foHE wanted towas authorize

professionalnt and signifations, but rduct arms-le

financing.

s provided to th

nding nd in s that way,

S has t now annot S has to the ch the r has

ancial ormer

of the by the not be 5, the re the about ormer o lock ed to l and ficant rather ength

They

he

were alsosolely tothem. In States SePensionscriticizednumerou20 U.S.Cinterpreta

V. CEH The Deptransactiothe philaand is bathe transinsure ththe benef The Depof the traDepartm

“TDewaoppinto

The Depa

“InMirev

o aware of th evade reguaddition to

enators to S’ report on

d these transus times sincC. § 1003. ation to deny

HE Board

partment alleon and that tnthropic mis

ased on a funsaction, and at the transafit of the Col

artment’s chansaction—ient to revers

The Transacecember 27, as based onposed to Mro the Merge

artment furth

ndeed, despinutes, the M

view.’”

he politicallyulation, and the public

Secretary Dun for profit sactions as bce these alleg

Accordingy CEHE’s ap

Actions P

eges that thethe sole purpssion of CEHndamental mthe due dil

action wouldlleges’ form

haracterizationdeed, so m

se its conclus

tion was ap2012. Altho ‘substantiar. Barney—cr Agreement

her asserts:

ite the stateMerger Agre

y-based claimthat proponeattack wage

uncan, the Shigher edu

being intendegations weregly, the Deppplication.

Prior to th

e CEHE boapose of the trHE. The De

misunderstanligence condd further the

mer owner.

ons of the famuch so that

sion. For exa

pproved byough the minal due diligconducted at.”

ement of ‘suements state

13

ms that soments were ased by Mr. SSenate Commucation publed to evade e made, andpartment ca

e Transac

ard (pre-tranransaction wepartment’s

nding of the ducted by C philanthrop

acts are fundthose errorsample, the D

y CEHE’s Bnutes of that

gence,’ thereany valuatio

ubstantial’ de that CEHE

me of the transking the D

Shireman anmittee on Hlished by thregulation. T

d Congress hannot arbitr

ction

nsaction) faiwas to benefi

conclusion nature of th

CEHE. In fpic mission o

damentally is alone proviDepartment s

Board… at t meeting ree is no evid

on of the Co

due diligencE performed

nsactions weDepartment tond the letter Health, Eduche committeThe HEA ha

has taken norarily impos

iled to propfit the Trust a

is riddled whe transactiofact, CEHE’of CEHE an

incorrect on ide sufficienstates:

a Board mecited that thdence that olleges befor

e in the CEd ‘limited du

ere being puro stop approfrom the Uation, Laboree in July as been ame

o action to amse an altern

erly evaluatand not to fu

with factual en, the purpo

’s board actnd not redou

critical elemnt grounds fo

meeting on he decision CEHE—as re entering

EHE Board ue diligence

rsued oving

United r and 2012

ended mend native

te the urther errors ose of ted to und to

ments or the

These cotransactio

to Mr. BAgreemeMercer19

CEHE atto ensureowner. The CEHCEHE boBlue & space, toreport is call and the Blue diligenceanalysis o As Attorcharacterthat “theDepartmclearly stdiligenceshould ta Althoughseems neperformediligence The Dep

19 See Exh20 See Exh21 See Exh

onclusions reons. Consid

Barney—conents.” This s, counsel fot that time, ae that the tr

HE board dioard demandCo. of India conduct an attached21. it was separ& Compan

e.” Thus, thof the compa

rney Mercerization of the Merger Agent has constates, “I have that I wouake in order t

h it is difficuecessary to eed a “limitede would be fo

partment clai

ibit 17 – Affidibit 18 – Statemibit 19 - Blue &

est on fundader first the

nducted anystatement is

or CEHE at an overridingransaction w

id not simpded an indepanapolis, IndindependenBlue & Co.rately review

ny report wahe Departmeany’s value

er’s affidavihe due diligegreements ststrued Merceve been requuld recommeto satisfy its

ult to undersexplain this fd due diligenor CEHE’s b

ims that the

avit of Jay Mement of Fred F& Co’s Report

mental errorstatement th

y valuation simply incthe time of g concern of

would not p

ply accept thpendent evaludiana, an ex

nt review and. presented iwed by counas conductednt’s claim thand review o

t makes cleence conducttate that CEHer’s statemenuested to proend” and the

minimum d

stand how thfurther: Mernce” reviewboard to sati

e CEHE boa

rcer Fransen

14

rs, misunderhat “…there

of the Colorrect. As the transact

f the CEHE provide any

he valuationuation of Baxperienced ad analysis ofits findings nsel for CEHd expressly “hat CEHE’sof Barringto

ear, the Deted by MercHE performnt to be exaovide the Boen lists mul

duties of due

he Departmercer was not; he was expsfy its duties

ard failed in

rstandings, a is no evide

lleges beforerecited in t

tion, and Freboard at theexcess ben

n conducted arrington’s aand leading f Barringtonto CEHE’s

HE. Contrary“for purposes board faileon’s appraisa

epartment her and the C

med ‘limited actly the oppoard with anltiple and ex diligence.

ent misundet characterizplaining whs with respec

n its duty to

and misrepreence that CE

e entering the attachededric Fransee time of theefit to the C

by Barringappraisal. Th

consulting n’s appraisalentire boardy to the Depes of the CEed to conducal is complet

has misrepreCEHE board

due diligencposite of whan outline of txtensive step

erstood this czing CEHE’sat the minimct to the tran

o conduct du

esentations oEHE—as opp

into the Md affidavit oen20, Presidee transactionColleges’ fo

gton. Insteadhe board retcompany in. Blue and

d in a conferpartment’s cEHE Board’ct an indepentely incorrec

esented Merwhen it conce review.”at it says. Mthe minimumps that the b

clear languas board as hamum level onsaction.

ue diligence

of the posed

Merger of Jay ent of n was ormer

d, the ained n this Co.’s rence

claim, s due ndent t.

rcer’s ntends

The Mercer m due board

age, it aving

of due

with

respect toMercer, transactiotransactioboard coconferensame issu At the bofiduciaryCollegespossibilitapprove tby confedetails, hthat the b Given thperiod cuconcludebe characconclusiois clearly The Depthe Colletransactiosupport ireason omembersopportunslightest As detailentering mission.

o the transaa distinguisons of this on was revieomplied withce call regarues that Mer

oard’s meetiny duties, res.” Moreovety of an excthe transacti

erence call whe provided board compli

he extensive ulminating ie that the boacterized as “on—that they not true.

partment’s aseges’ formeron, and smeit. The Dep

or desire to s of the boanity. The Deinterest in en

led in Fred into this mThere is no

ction. Not shed attorney

type. Mercewed, Merceh all due drding the varcer identifie

ng with Merponsibilities

er, he “strescess benefit ion.” Over twith and wa compreheied with the

effort, carein the closinard failed tolimited.” Th

e board failed

ssertion thatr owner misars the integpartment proenrich or o

ard had eveepartment idnriching or o

Fransen’s serger wouldt a single sh

true. First, y with extecer reportser devoted a

diligence reqaluation presed as the hea

rcer on Augus and liabilissed the ne

transactionthat same 6-ithout coun

ensive due dletter and th

e, and timeng of the trao perform adhe only concd to conduct

t CEHE’s pusconstrues thgrity and comovides basisotherwise ber even met

dentifies no motherwise be

statement, thd be the mohred of evide

15

as indicatednsive experthat over

approximatequirements, sentation. Tart of CEHE’

ust 27, 2012ities involveeed for a fan” and “also-month periosel present

diligence chehe spirit of it

spent by Cansaction, it dequate due crete assertiot independen

urpose in cohe transactiompetence ofs for why Cbenefit the Ct the Collegmotive for wenefiting the

he sole motiost effective ence to supp

d above, therience in cothe 6-monthly 150 hourincluding p

The Departm’s due dilige

, Mercer “exed in the prfair market o discussed od, the CEHto discuss t

ecklist for thts nonprofit m

CEHE and itdefies beliediligence; oon made by tnt analysis o

onducting thon, CEHE’s f CEHE’s boCEHE or itsColleges’ foges’ former

why the CEHColleges’ fo

ivation for tway to adv

port the Dep

e board retairporate law

th period durs to ensurinparticipating

ment now raince delibera

xplained to troposed tranvalue to guthe due dili

HE board metthe transacthe board to mission.

ts counsel oef that the Dor that its duthe Departmof the Barrin

his transactiopurpose in

oard withouts board wouormer owne

owner prioHE board woformer owner

the board wvance CEHEpartment’s bi

ined attorney, nonprofitsuring which

ng that the Cg in a 2 ½ ises preciselations.

the directorsnsaction withuard againsigence needt numerous ttion. As Mfollow to en

over the 6-mDepartment ce diligence c

ment to suppongton apprai

on was to beentering intt any eviden

uld have hader. None oor to the mould have har.

was its beliefE’s philanthizarre theory

y Jay , and h the

CEHE hour

ly the

s their h the

st the ded to times

Mercer nsure

month could could ort its isal—

enefit to the nce to d any of the

merger ad the

f that hropic y that

the CEHopposed The Depathe intentinferenceowner’s Accordinorganizatfinancial the transahistories organizatpursuing Departmformer ocontrollerelationshboard intfanciful c AccordinphilanthrtransactiCollegesgain mate The Depbetween scheme brecord unthe mergwith exte

22 See docu

E board hadto advancing

artment’s fat of benefitine that the Cself-enrichm

ng to Mr. tion since 2crisis, the b

action with tin the no

tions. CEHEits specific

ent’s failurewner, the Dd CEHE (anhip) sufficieto entering conclusion.

ng to Mr. Frropic missionion.” The ’ former owerially from

artment has CEHE and

by “shills” onequivocally

ger; the mergensive due d

uments CEHE

d any desire g CEHE’s ph

ilure to idenng the Colle

CEHE boardment.

Fransen’s 006. Follow

board was rethe Collegesonprofit sec

E had a multc mission a to provide e

Department an organizatiently to carrinto the me

ransen, if then of CEHE, members o

wner and, as the transact

fundamentad the Collegon the CEHEy demonstrager was condiligence wit

provided in re

or motive tohilanthropic

ntify any moteges’ formerd was compl

statement, wing a changeconstituted ts. All three octor as uni-year opera

and operatinevidence tha

also fails to ion with whry out an alerger. Certa

e former ow“there wou

of CEHE’s records preion.

ally misundeges. The DeE board to enates that CEHnducted to ath the advic

sponse to Depa

16

o benefit thec mission.

tive for the Cr owner, elimlicit in an a

CEHE funge of financto add the m

of CEHE’s pniversity proation record ang independeat CEHE hadevidence its

hich the Colllleged schem

ainly there i

wner’s intentld have beenboard had

viously prov

erstood and partment’s nrich the CoHE was an

advance CEHe of experie

artment reques

e Colleges’ f

CEHE boardminates any alleged sche

nctioned as cial supportemembers whopre-transactioofessors anas an indepeently of anyd any motivas theory thatleges’ formeme or to inds nothing in

t was anythin no purpos

no pre-exivided to the

mischaractecharacterizaolleges’ formindependent

HE’s philantenced legal c

sts from March

former owne

d to enter thesupport for t

eme of the C

an indepeers, in the wo were servion board me

nd employeendent nonpry third-partiation to bent the Collegeer owner haduce or oven the record

ing other thase for CEHEisting relati Departmen

erized the mation of the mer owner ist organizatiothropic misscounsel; and

h and June 201

er individual

e transactionthe DepartmColleges’ fo

endent nonpwake of the ing at the timembers havees of nonprofit organizies. As withefit the Colles’ former oad no preexierbear the Cd to support

an advancinE to engage iionship with

nt show22, di

merger transatransaction

s laughable. on at the timsion; it was d the Depart

6

lly as

n with ment’s ormer

profit 2008

me of e long profit zation h the leges’ owner isting

CEHE t this

ng the in the h the id not

action as a The

me of done

tment

has identthe indepenrichme The DepDepartmthe blatavaluation

VI. R The factsthat CEHincorrectand issurecognizinon-provof comptimefram Sincerely Eric S. JuChief Ex CC: S D C

tified no mopendent CEHent.

partment’s cent to accura

ant misstatemn, the Depart

Request fo

s, evidence, HE’s Collegt and politicae standard, ing their tru

visional partipliant opera

me is two yea

y,

uhlin xecutive Offi

teve GomboDr. Michale MCEHE Board

otive or theoHE board of

conclusions ately recognment that thtment should

r Reconsid

and precedeges fail to ally driven. non-provisi

ue status as nicipation agration under ars.

icer

os, Ritzert &McComis, A

d of Directors

ory as to howsubstantial a

amount to nize the due de board didd reconsider

deration

ent overwhelmeet the DCEHE there

ional, Progrnonprofit inreements bec

provisiona

& Leyton ACCSC s

17

w the Collegacademics to

unsupportediligence con

d not conducits Decision

lmingly demDepartment’sefore requestam Particip

nstitutions. Ccause the Coal participat

ges’ former o participate

ed nonsensenducted by tct its own dn.

monstrate thas regulatoryts the Depar

pation AgreeCEHE’s Coolleges havetion agreem

owner couldin an allege

e. Given ththe CEHE b

due diligence

at the Depary definition rtment to revements to Clleges are en

e already comments when

d have persued scheme of

he failure ooard, particue with respe

rtment’s Decfor nonpro

verse its DecCEHE’s Colntitled to rempleted 3½ n the custo

uaded f self-

of the ularly ect to

cision ofit is cision lleges eceive years

omary

1. T

thac

2. TCbyOapapsu

3. TPaT22

4. TchpAsun

TosuDwpRch

ToC

Inaccu

The Decisionhat occurrectually occu

The DecisionColleges") s

y NovembeOctober 22, pplications pplications ubmitted in

The DecisionParticipation

n initial onTemporary P

013 and ha016.

The Decisionhange of owaragraph 1)

Additionallyubmitted an

never submi

The Departmr ambiguityubmitted an

Department when it state

osition withRevenue Serharged with

The only appr not it wou

CEHE becom

uracies andAugust 1

n incorrectled as of Decurred on De

n incorrectlubmitted an

er 7, 2012 (C2012)” (paon the datein the fall o

n January 20

n incorrectln Agreemene month peProgram Pave been ext

n incorrectlwnership or). CEHE ney, in other cn applicatiotted an app

ment is comy of languagn applicatiohas no such

es near the eh respect torvice” (pageh determinin

plication CEuld issue neming the so

Ap

d Misrepr11, 2016 D

ly states thacember 27, ecember 31

ly states than electronicCalifornia Cage 1, parages specifiedof 2012. Th013.

ly states thants were effriod until J

articipation tended on a

ly states thar structure fever submittcorresponden for a “chalication for

mmitting a fage to mislean for a chanh applicatioend of its D

o CEHE’s ne 10, paragrng a corpor

EHE submiew Programole owner an

ppendix 1

resentationDecision (t

at, “This app2012…” (p, 2012.

at, “Each ofc applicatioCollege of S

graph 1). Thd. The Collehe actual ch

at, “Temporfective as ofJanuary 3 1,Agreement

a month-to-m

at CEHE sufor the abovted an appli

ences, the Dange of statr a change o

allacy of amad or misrepnge of strucons for colleDecision, “T

on-profit 50raph 5). Thration’s tax

itted was fom Participati

nd operator

ns in the Dthe “Decis

pplication repage 1, para

f the above on ("eapp") fSan Diego she Collegeseges submihange of ow

rary Provisif January 1, 2013” (pats were effemonth to ba

ubmitted, “…ve-named sication for c

Department tus for its coof status.

mbiguity bypresent the cture or chaeges. The DThe Departm01(c)(3) stahe IRS is thstatus.

or the Deparion Agreemr of the coll

Departmenion”)

esults from agraph 1). T

named schofor Change

submitted ths did not sutted pre-acq

wnership ap

ional Progr, 2013, and

age 1, paragective as of asis through

… an [applschools” (pachange of sclaims thatolleges”. C

y using a dotruth. CEH

ange of statuDepartmentment does natus with thhe only fede

rtment to dements to CEH

eges. CEH

nt’s

a transactiThe transac

ools ("the e in Ownersheir eapp o

ubmit quisition re

pplications w

ram d extended fgraph 1). ThJanuary 31h August 31

lication] forage 1, structure. t CEHE CEHE has

ouble meaniHE never us. The t recognizesnot take a e Internal eral entity

ecide whethHE followi

HE’s status a

ion ction

ship on

view were

for he , 1,

r a

ing

s this

her ng as a

nb T“inapT

5. T

DaanthC

6. T

re(pfoPothcoD

7. T

chC

8. T

coCC

9. T

cocl

10. T

non-profit coy the Depar

The DepartmThe Departnstitution thpply and ob

Title IV, HEA

The DecisionDepartment

dministratissistance pr

not petitionehat CEHE i

Colleges.

The Decisionequested appage 2, paraor the Depa

Participationperator of the Departmorporation

Department.

The Decisionhange of ow

CEHE never

The Decisiononsidered n

Colleges didCEHE as the

The Decisionontinued strlaims, title,

The Decision

orporation artment.

ment, later itment regulhat constitubtain approA program

n incorrectlto recognizon and overograms,”

ed the Depas a qualifie

n incorrectlpprovals foragraph 3). artment to dn Agreementhe colleges

ment to approand CEHE’.

n incorrectlwnership anr requested

n incorrectlnonprofit ind not apply te new owne

n incorrectlream of Tit or retentio

n incorrectl

and CEHE’

in its Decisilations idente a change

oval from th” (page 2, p

ly states thaze their conrsight of the(page 2, pa

artment for ad nonprofit

ly states thar the changThe only ap

decide whethnts to CEHEs. CEHE neove a chang’s sole own

ly states thand change tapproval fo

ly states thanstitutions…to be consider and opera

ly states thatle IV revenn of any str

ly states tha

2

’s sole owne

ion, acknowntify certaine of ownershhe Departmeparagraph 4

at, “The Conversion to neir particip

aragraph 1).any such ret corporatio

at this decisge of ownerspplication oher or not iE followingever requesge of status

nership of th

at, “… CEHto nonprofitor a change

at, "Because…” (page 3,

dered nonprator of the C

at, “… the Tues….” (paream of rev

at, “… Mr. B

ership of th

wledges exa covered trahip that reqent to conti

4).

olleges havenonprofit st

pation in Tit CEHE sen

ecognition. n and CEH

sion is in resship and chor request thit would issug CEHE bected or subm. CEHE’s s

he colleges

HE’s request status.” (p to nonprof

e the colleg, paragraph rofit, the CColleges.

Trust retainage 3, paragvenues from

Barney obt

he colleges i

actly what aransactions fquire the insinue particip

e petitioned tatus for thetle IV student no such p Again, it is

HE is the sol

sponse to, “hange to nonhat CEHE sue new Procoming the mitted an apstatus as a nis undisput

sted approvpage 2, parafit.

ges have apph 1). This isolleges app

ned the benegraph 3). T

m CEHE.

tained signif

is undispute

authority it for an stitution to ipating in th

d the e purposes

ent financiapetition ands undisputele owner of

“…CEHE’snprofit statusubmitted wogram

sole ownerpplication fonon-profit ted by the

vals for the agraph 3).

plied to be s false, the plied to have

efit of a The Trust ha

ificant contr

ed

has,

he

of l

d has ed f the

s us”

was

r and or

e

as no

rol

of3ap

11. TcoT

12. T

arco(pcow

13. T

loqCbpil

f CEHE an). Mr. Barnppointed as

The Decisionommissione

The Barringt

The Decisionre improperovenants sepage 5, paraovenants an

way illegal,

The Decisionoan agreemuarterly ma

CEHE, or 10usiness loanerformancellegal, wron

d by extensney did not s a member

n incorrectled by Mr. Bton valuatio

n incorrectlr, “… Mr. Bet forth in thagraph 3). nd restrictiowrong, or a

n incorrectlment or loan

andatory pr0% of CEHn or transac

e terms for tng, or a viol

sion, retaine“obtain” siof the corp

ly states thaBarney for uon was com

ly implies thBarney indehe NPA andVirtually ev

ons on the ba violation o

ly implies thterms are im

repayments HE’s total rection loan cthe borrowelation of any

3

ed control oignificant coporation pur

at, "The Baruse by the c

mmissioned,

hat restrictieed placed rd a subsequvery busineborrower. Tof any regu

hat loan termproper, "Sof the grea

evenues.” (pcontains cover. This is cy regulation

of the collegontrol; he wrsuant with

rrington evaompany…”, and paid f

ions or coverestrictions

uent Contingess loan or tThis is commulation.

rms, restrictSignificantlater of 75%page 6, paravenants, rescommon prn.

ges.” (pagewas duly anCEHE’s by

aluation wa” (page 5, pfor, by the C

enants in los on CEHE:gent Note Atransaction mon practic

tions, or covly, the notes

% of the exceagraph 1). strictions, anractice and

e 3, paragrapnd legally ylaws.

as paragraph 1)Colleges.

oan agreeme: by negativAgreement.”loan contaice and in no

venants in ts also requiess cash flowVirtually end specific in no way

ph

).

ents ve ” ins o

the ire w of very

The Depa

“Tdecthetra

This evenalmost thregardinghad no beis outside The basisthe transtam suit overly aDepartmaggressiv There is and efforbusiness heavy-hato close, price and Contraryevents cobenefit thparties crepresent

artment state

The Departmcided to procere would hansaction”

nt has no relhree years bg the purchaearing upon e the purview

s for a purchaction closeexisted or w

aggressive aent well knovely defende

no proof thrts to impugnoperations,

anded demanthe Colleges

d notes to sav

y to the asseonfirm the ohe Colleges’could not wtations had b

Miscell

es:

ment concludceed with thhave been a

levance whatbefore this evase price adjCEHE’s eli

w of the thre

hase price add. The Coll

would be fileassistant staows there is ed itself and

hat the Collen the reputatand caused

nd for an unrs had no alteve the institu

ertion that thopposite. C’ former owwait for a been breache

Ap

laneous C

des [from a Nhe Transactioa substantia

tsoever to thvent. This

djustment. Tigibility as a ee-part test u

djustment coleges and thed; nor couldate Attornean epidemicthe organiza

eges breachetion of the Ca decline in reasonable leernative but utions.

he CollegesEHE certainner in this rdeterminati

ed through t

ppendix 2

Conclusion

November 2on knowing al adjustme

he Departmeconclusion r

The purchasnonprofit in

used by the D

ould not havheir managemd the Collegy General

c of such suiation denies

ed any repreColleges and

revenue. Oetter of credto seek from

’ former ownly acted in regard. Dueion as to wthe court sys

ns in the D

2015 statemeabout the “

ent to the f

nt’s review relies upon e price (and

nstitution of Department i

ve been knowment could nges and their

would brinits against cothere is any

esentations oits former o

Out of necessdit while threm its lender a

wner acted imits College

e to the demwhether thestem. The s

ecision

ent] that if “material” infinancial ter

of a transactan after-the

d purchase phigher educ

in its Decisio

wn by either not have prer managemenng meritlesolleges of anbasis for suc

or warrantieowner have dsity, due to teatening to foan adjustmen

mproperly, s’ best inter

mand for a lee Colleges’ettlement al

CEHE had nformation, rms of the

tion that occe-fact supposprice adjustmcation. This on.

r party at theedicted that nt predict ths claims.

ny size. CEHch claims.

s. These acdamaged CEthe Departm

force the Colnt to the purc

these undisprests - and ntter of credi warrantieslowed the p

curred sition ment) issue

e time a qui

hat an The

HE is

ctions EHE’s ment’s lleges chase

puted not to it, the s and arties

to resolvColleges release C The Depdramaticsystemic or the Cothree yea

“Prev

No, it is establishexcess reStanford with exceinstitutiodebt alsoregulatiowith fair

“CTruori

CEHE dfinancial Decisionand descr

“Inthe

1 See Exhib

ve the mattenow satisfy

CEHE’s $43

partment knoally from 2attacks agai

olleges’ formars in the futu

Payments to venues over e

not the samed by GAAevenue overUniversity,

ess revenuesn without so fail the dns is arbitraapplication

CEHE did noust even thoiginal transa

did notify thstatements

n) on March ribes the deb

n either casee initial cons

bit 20 – Submi

er and meet y the financiamillion doll

ows the pol2012 to 201inst private

mer owner, cure is not cre

the Trust uexpenses - -

me! The DAP and FASB

r expenses and CEHE’

s over expensimultaneousdefinition. ary, capricioof its regula

ot notify the ough the CEaction was st

he Departmeto the Depa31, 20161.

bt restructuri

e, the significsideration of

ission of CEHE

the composal responsibars of escrow

itical enviro15. The prcareer colleg

could have foedible.

under the Nthe same wa

epartment’s B. Every cto service ts Colleges.

nses causes Csly concludi

Selective ious, and inaations.

DepartmentEHE’s appltill under rev

ent. CEHEartment (incl

Note 7 in Cing.

cant reductiof $431,000,0

E 2015 Audited

2

site score reility composw funds bein

onment and roblem arosges. For theoreseen or sh

Notes are esay as net inc

interpretatiocollege in ththeir debt. The Departm

CEHE’s Coling that all interpretatio

appropriate f

t of this signlication for view”

E provided aluding a copCEHE’s 201

on [in CEHE000 (and the

d Financials to

egulations. Nsite score, thng held by th

economics se from thee Departmenhould have f

ssentially bacome in a for

on runs couhe United St

This is trument cannotlleges to failexisting no

on and varyfor a federa

nificant debtthe change

a copy of ipy directly to

5 audited fi

E’s debt to te correspond

o DOE

Notwithstandhe Departmehe Departme

for career ce coordinatent to claim thforeseen suc

ased on ther-profit entity

unter to accotates that ha

ue for Columt conclude thl the definitinprofit colle

ying applicaal regulatory

t restructurine of ownersh

its fiscal yeo Mr. Parrotinancial repo

the Trust] suding indebte

ding the facent has refusent.

colleges chad campaignhat either CE

ch hostility tw

e excess of ty”

ounting pracas debt musmbia Univehat servicingion of a nonpeges that seation of exiy agency cha

ng with the hip for the

ear 2015 autt who signeort clearly d

uggests that edness) was

ct the sed to

anged n and EHE, wo to

ctices st use ersity, g debt profit ervice isting arged

udited ed the details

hig No, it wconclusioas of the years afttransactio

“TRelmorec

The DepdeterminAcceptedThe IRS under andebt musexpensesexpensesCEHE’s debt to anThis posidecisionsdistributi

“Aprount

The DepCEHE’s short-termimportancollege tr

ghly inflated

was not. Thon. Two sepdate of the

ter the transon was inapp

The Departmlated Contin

oney”, are esceived when

partment donation. The d Accountin

auditors hany definitionst do so wits. If an orgas, it cannot debt, the facnother entityition by the s. The Deions of profit

s an elemenoperties, Mrtil 2025 or 2

partment’s sColleges re

m businessence and valueransactions

”

he Departmeparate valuattransaction.

saction closepropriate. T

ent has detengent Notesssentially prit was the so

oes not havDepartmen

ng Principlesave certainly, profit distrth funds ava

anization doeservice deb

ct that the dey, it would sDepartmentpartment cat.

t of further br. Juhlin ren2026.”

statement is eceived subses or operae to higher eand if were

ent presentstions of the The Depared and pres

To do so is ill

rmined that s, which arrofit distributole sharehol

ve the authnt is not thes, and they y not made tributions. Eailable after es not generabt. Given ebt is to the

still have to st runs counteannot disreg

benefit to Mnegotiated m

void of anstantial beneations, and education into review th

3

s no evidenColleges wertment cannoent those evlogical.

the paymentre and weretions to the Tlder of the C

hority, the e IRS, they are not the this interpre

Every organithe organiz

ate more mothe arms-leColleges’ fo

service that er to well esgard, or ign

Mr. Barney inmost of the C

ny proof, evefits by renstability of

nstitutions. Those records

nce, basis, oere conducteot take evenvents as evi

ts under the e contingenTrust – subs

Companies.”

right, or tare not theFinancial A

etation. CEHization in thzation has soney than it nength transaformer ownedebt with ex

stablished lawnore the tru

n the form ofCollege leas

vidence, or negotiating if location aThe Departms it would s

or support foed; they estants that occuidence that

Term, Contnt on CEHEstantially the

the expertise promulgatAccounting SHE’s debt p

he United Staatisfied all oneeds to cov

action and mer is irrelevanxcess revenuws, rules, G

uth that deb

f enhanced vses to extend

support forits leases. and presencment has extsee that insti

for this profablished the vurred almost

an aspect o

tingent, and E “making e same as it

se to maketors of GeneStandards B

payments areates that serother operat

ver its operatmarket termnt. If CEHEue over expe

GAAP, and Fbt service is

value to the d the terms

r this allegaColleges are is of extensive recoritutions that

ffered value three

of the

e this erally

Board. e not, rvices tional tional

ms for E had enses. FASB s not

ation. e not treme rds of have

long-term CEHE pDepartmColleges paying) a

m leases in p

provided theent would rnegotiated

and received

place actually

e Departmenreview thosea significan

d 3-6 months

y command

nt with copie amendmenntly lower rs of rental ab

4

a higher valu

ies of all rents it will srental rate (batements.

uation in the

e-negotiatedsee that in v(from what

e marketplac

d lease amenvirtually evthe College

ce.

ndments. Iery instance

es were curr

If the e, the rently

From: U.S. Department of Education <[email protected]> Sent: Thursday, August 11, 2016 10:32 AM To: U.S. Department of Education Subject: EMBARGOED: Department Denies Request for Chain of For‐Profit Colleges to Convert to Non‐Profit Status

EMBARGOED UNTIL 11 A.M. ET ON THURSDAY, AUG. 11, 2016.

U.S. Department of Education Office of Communications & Outreach, Press Office 400 Maryland Ave., S.W. Washington, D.C. 20202 FOR IMMEDIATE RELEASE: Aug. 11, 2016 CONTACT: Press Office, (202) 401-1576 or [email protected]

Department Denies Request for Chain of For-Profit Colleges to Convert to Non-Profit

Status Center for Excellence in Higher Education campuses must continue to be accountable to

taxpayers, students through federal regulations The U.S. Department of Education today denied a request from the Center for Excellence in Higher Education (CEHE), a Utah-based chain of for-profit career colleges, to convert to non-profit status for purposes of federal financial student aid. The denial means that the colleges’ programs must continue to meet requirements under the federal Gainful Employment regulations[ed.gov]. “This should send a clear message to anyone who thinks converting to non-profit status is a way to avoid oversight while hanging onto the financial benefits: Don’t waste your time,” said U.S. Education Secretary John B. King Jr. This denial does not directly affect the approximately 12,000 students who attend the four institutions owned by CEHE - Stevens-Henager[stevenshenager.edu] in Utah and Idaho, CollegeAmerica Denver[collegeamerica.edu], CollegeAmerica Arizona[collegeamerica.edu], California College San Diego[cc‐sd.edu] and CollegeAmerica Services[collegeamerica.edu] - but it does mean that the Department will continue to limit the colleges to getting no more than 90 percent their revenue from Title IV federal student aid. It also means that the institutions must meet all federal regulations for for-profit colleges. CEHE first applied for non-profit status with the Department in the fall of 2012. In reviewing that request, the Department determined that CEHE, which had been a small educational non-profit that did not provide educational services, acquired four for-profit college companies

owned by the Carl Barney Living Trust. CEHE promised to pay the Trust more than $400 million dollars, and the colleges were merged into CEHE. When that happened, Mr. Barney became the board chairman of CEHE, and because of the way the transaction was structured, retained significant control of the colleges, despite the change in ownership to CEHE. While CEHE is recognized by the Internal Revenue Service as a non-profit company, the colleges’ tuition revenue continues to flow to Mr. Barney through the Trust to pay off the debt that CEHE owes from acquiring the colleges, and through the rent that some of Mr. Barney’s other companies receive as landlords for several of the college campuses. Under 34 C.F.R. § 600.2 of the Higher Education Act[www2.ed.gov] regulations, non-profit institutions must be owned and operated by a non-profit where no part of the net earnings benefit any private shareholder or individual. “Schools that want to convert to non-profit status need to benefit the public,” said U.S. Under Secretary of Education Ted Mitchell. “If the primary beneficiary of the conversion is the owner of the for-profit school, that doesn’t meet the bar. It's not even close.” Since 2012, the four institutions have continued participating in the Title IV financial aid programs on month-to-month agreements as for-profit institutions. In a letter to the company’s CEO, Eric Juhlin, the Department approved the change in ownership that CEHE requested but continues to recognize Mr. Barney as maintaining significant control of the institutions and the Title IV revenue they produce. During the review of the change in ownership request, the Department requested additional documentation from CEHE. The company provided information to the Department but marked much of it as confidential, and that information has been removed from copies of the letter made available for public review. Documents subject to CEHE’s confidentiality designation would have to be requested for public review under the Freedom of Information Act. During the time the applications were under review, risk factors identified in CEHE’s financial statements - including a lawsuit against one of the institutions filed by the Colorado Attorney General - led the Department to require CEHE to provide a $42.9 million surety, which is 30 percent of the annual federal student aid funding for 2013 for the four institutions. That surety remains in place but is subject to adjustment based on CEHE’s financial condition and other risks. To qualify for federal student aid, the law requires that most for-profit programs and certificate programs at private non-profit and public institutions prepare students for gainful employment in a recognized occupation.

###

1

Eric Juhlin

From: Parrott, Douglas <[email protected]>Sent: Thursday, August 11, 2016 8:42 AMTo: Eric JuhlinSubject: Decision on Change of Ownership for Stevens Henager College, OPE 003674,

CollegeAmerica Denver, OPE 025943, CollegeAmerica Arizona, OPE 031203, California College San Diego, OPE 021108

Attachments: image2016-08-11-093318.pdf

Mr. Juhlin, The Department’s Decision on Change of Ownership for Stevens Henager College, OPE 003674, CollegeAmerica Denver, OPE 025943, CollegeAmerica Arizona, OPE 031203, California College San Diego, OPE 021108 is attached to this message.

Campus2013

Jan-Dec2014

Jan-Dec2015

Jan-Dec2016

Jan-Jun TotalBoise 54,720 157,844 279,535 167,078 756,024

Cheyenne 1,800 63,507 64,446 37,249 172,991 ColoradoSprings 114,459 272,181 327,994 90,215 809,795Denver 135,641 202,405 278,345 114,554 788,472

Ft. Collins 66,904 66,855 168,964 55,689 399,636Flagstaff 51,102 189,636 151,903 58,831 498,592

International 0 3,750 57,750 37,500 99,000Idaho Falls 4,700 65,946 209,554 123,067 406,268

Layton 0 1,500 7,820 8,410 17,730Logan 93,312 123,312 160,220 124,328 619,431Nampa 39,354 81,855 248,357 89,769 491,872

NationalCity 79,282 154,138 248,694 162,014 655,128

IndependenceUniv. 2,246,334 3,385,612 4,368,002 2,446,178 12,811,203Ogden 105,978 150,325 178,807 114,493 655,416

Phoenix 124,867 558,277 785,316 389,911 1,908,374Provo 183,787 275,845 282,281 185,110 1,205,970