Embed Size (px)

Citation preview

CEE Real Estate Investment market| Mark Robinson February 2018

Colliers International 20175

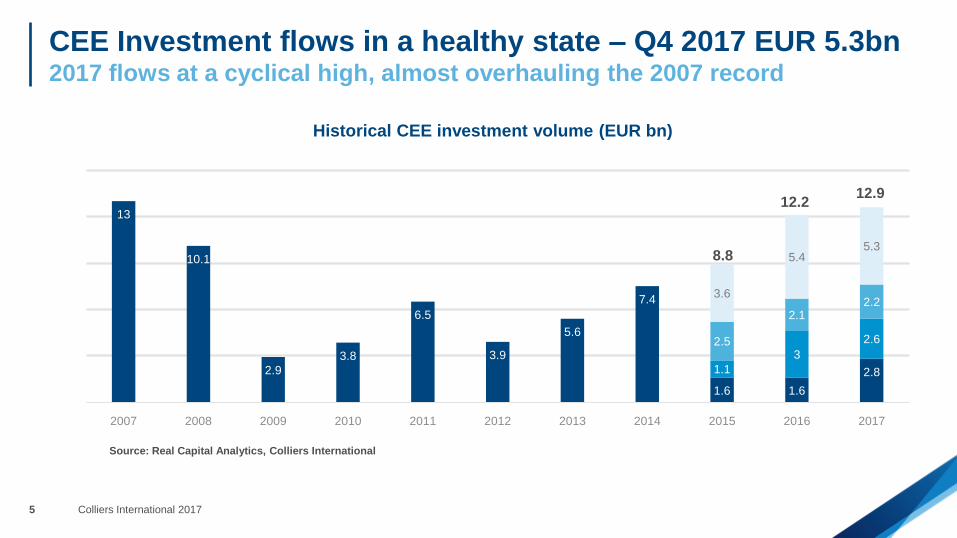

13

10.1

2.9

3.8

6.5

3.9

5.6

7.4

1.6 1.6

2.81.1

3

2.62.5

2.12.2

3.6

5.45.3

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

CEE Investment flows in a healthy state – Q4 2017 EUR 5.3bn2017 flows at a cyclical high, almost overhauling the 2007 record

Historical CEE investment volume (EUR bn)

Source: Real Capital Analytics, Colliers International

8.8

12.212.9

Colliers International 20176

Flows into retail and hotels grew fastest in 2017 Polish volumes made a strong comeback in H2 after a weak H1

Split of investment flows by destination

Source: Colliers International

Split of investment flows by sector

5,129

3,730

1,828

957

916 366

Poland

Czech R

Hungary

Bulgaria

Romania

Slovakia

EUR mn

3,549

2,280

5,015

988 1,096

Office

Industrial

Retail

Hotel

Other

EUR mn

Colliers International 20177

Can CEE-6 defy the downturn in EMEA volume?CEE’s momentum lagged EMEA in time historically – is it different this time?

EMEA and CEE investment volume (EUR bn)

Source: Real Capital Analytics, Colliers International

0

2

4

6

8

10

12

14

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EMEA flow (EURbn) CEE-6 flow (EURbn, right hand side scale)

Colliers International 20178

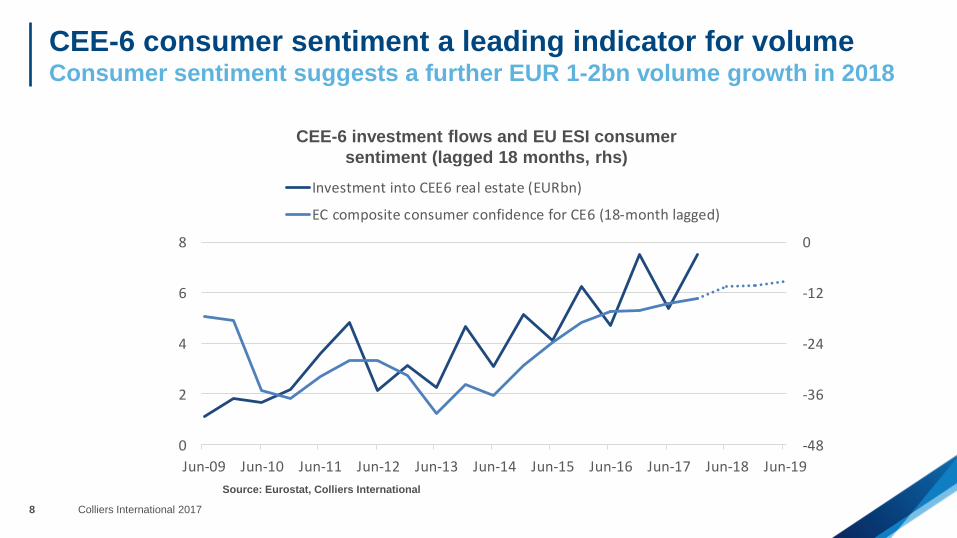

CEE-6 consumer sentiment a leading indicator for volumeConsumer sentiment suggests a further EUR 1-2bn volume growth in 2018

CEE-6 investment flows and EU ESI consumer

sentiment (lagged 18 months, rhs)

Source: Eurostat, Colliers International

-48

-36

-24

-12

0

0

2

4

6

8

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19

Investment into CEE6 real estate (EURbn)

EC composite consumer confidence for CE6 (18-month lagged)

Colliers International 20179

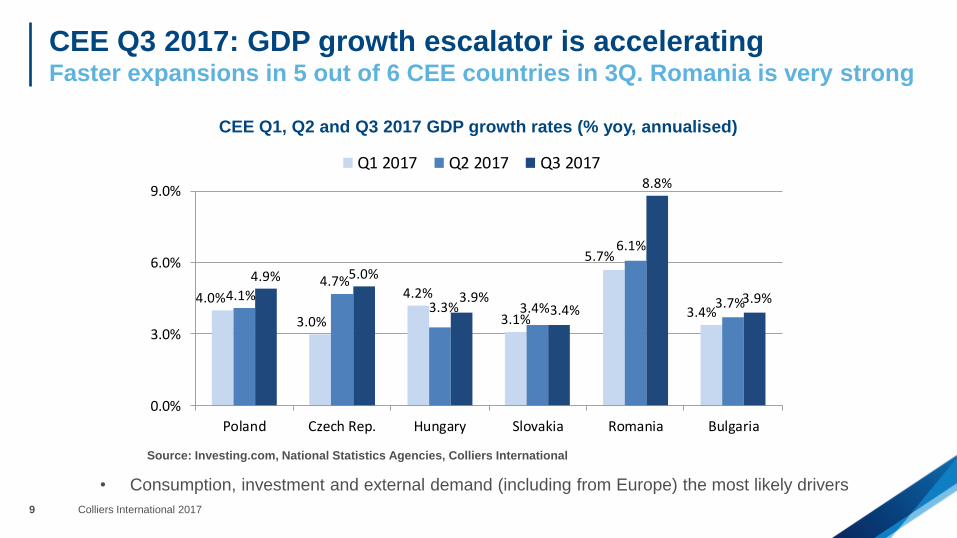

CEE Q3 2017: GDP growth escalator is accelerating Faster expansions in 5 out of 6 CEE countries in 3Q. Romania is very strong

CEE Q1, Q2 and Q3 2017 GDP growth rates (% yoy, annualised)

Source: Investing.com, National Statistics Agencies, Colliers International

• Consumption, investment and external demand (including from Europe) the most likely drivers

4.0%

3.0%

4.2%

3.1%

5.7%

3.4%4.1%

4.7%

3.3% 3.4%

6.1%

3.7%

4.9% 5.0%

3.9%3.4%

8.8%

3.9%

0.0%

3.0%

6.0%

9.0%

Poland Czech Rep. Hungary Slovakia Romania Bulgaria

Q1 2017 Q2 2017 Q3 2017

Colliers International 201710

Will CEE GDP growth drive rents? Example: Prime BUD office sector rents finally following GDP growth up

Hungary GDP growth (yoy) vs. Prime Budapest CBD office rent lagged 30 mths (per sqm, rhs)

Source: investing.com, Colliers International

• GDP growth predicts rent levels 30 months ahead. Will supply react?

17

18

19

20

21

22

23

24

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

GDP growth (yoy) Prime CBD office rent (EUR/sqm/mth, 30-month lag, rhs)

Colliers International 201711

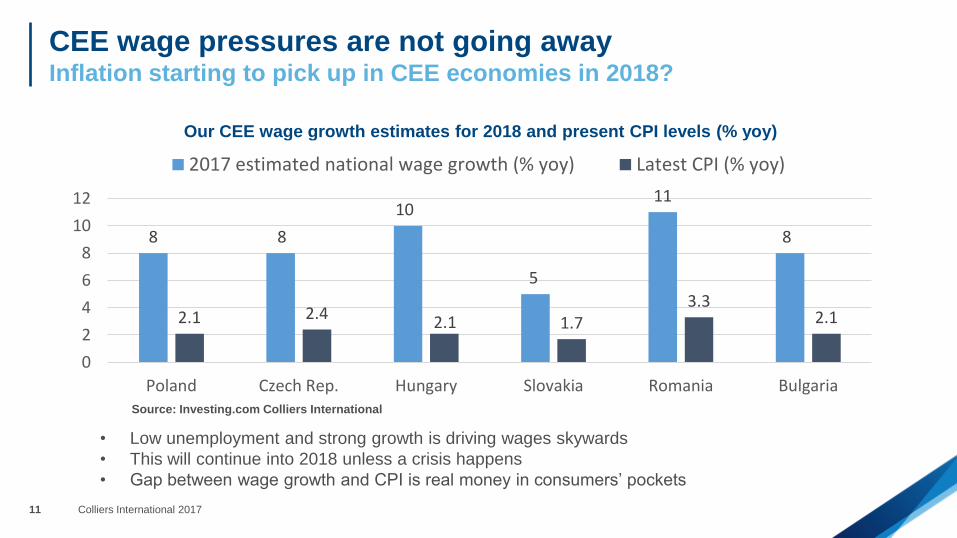

CEE wage pressures are not going awayInflation starting to pick up in CEE economies in 2018?

Our CEE wage growth estimates for 2018 and present CPI levels (% yoy)

Source: Investing.com Colliers International

• Low unemployment and strong growth is driving wages skywards

• This will continue into 2018 unless a crisis happens

• Gap between wage growth and CPI is real money in consumers’ pockets

8 8

10

5

11

8

2.1 2.4 2.1 1.73.3

2.1

0

2

4

6

8

10

12

Poland Czech Rep. Hungary Slovakia Romania Bulgaria

2017 estimated national wage growth (% yoy) Latest CPI (% yoy)

Colliers International 201712

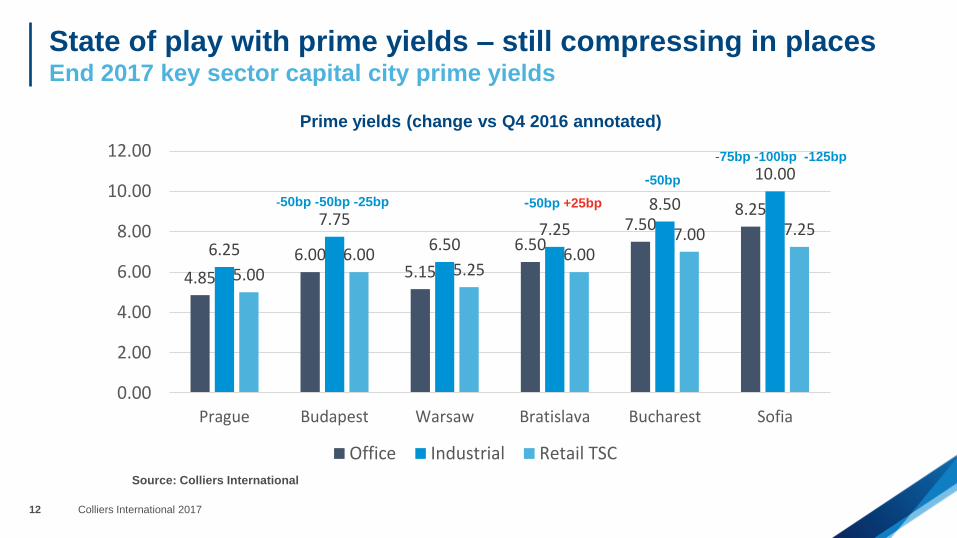

State of play with prime yields – still compressing in placesEnd 2017 key sector capital city prime yields

Prime yields (change vs Q4 2016 annotated)

4.85

6.005.15

6.507.50

8.25

6.25

7.75

6.507.25

8.50

10.00

5.006.00

5.256.00

7.00 7.25

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Prague Budapest Warsaw Bratislava Bucharest Sofia

Office Industrial Retail TSC

Source: Colliers International

-50bp +25bp

-75bp -100bp -125bp

-50bp -50bp -25bp

-50bp

Colliers International 201713

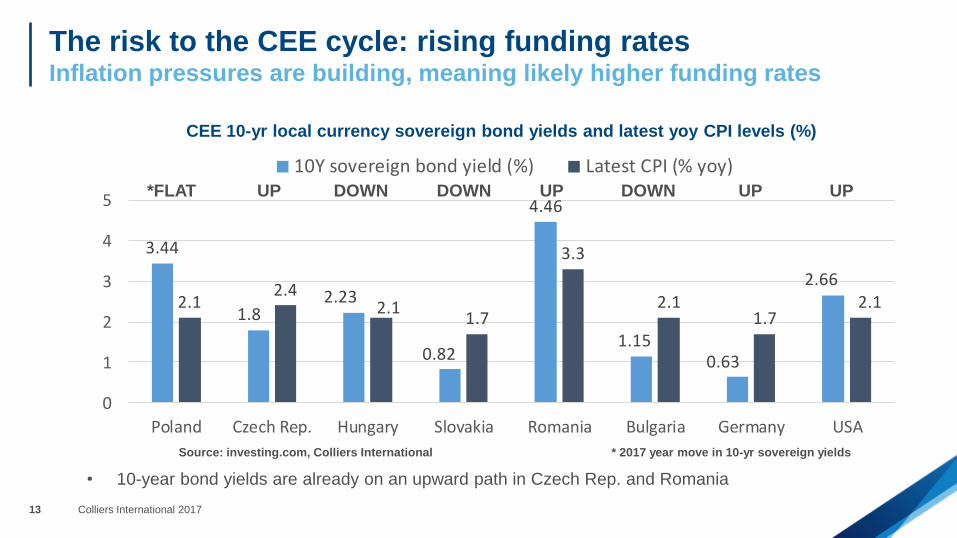

The risk to the CEE cycle: rising funding ratesInflation pressures are building, meaning likely higher funding rates

CEE 10-yr local currency sovereign bond yields and latest yoy CPI levels (%)

Source: investing.com, Colliers International * 2017 year move in 10-yr sovereign yields

• 10-year bond yields are already on an upward path in Czech Rep. and Romania

3.44

1.82.23

0.82

4.46

1.150.63

2.662.1

2.42.1

1.7

3.3

2.11.7

2.1

0

1

2

3

4

5

Poland Czech Rep. Hungary Slovakia Romania Bulgaria Germany USA

10Y sovereign bond yield (%) Latest CPI (% yoy)*FLAT UP DOWN DOWN UP DOWN UP UP

Colliers International 201714

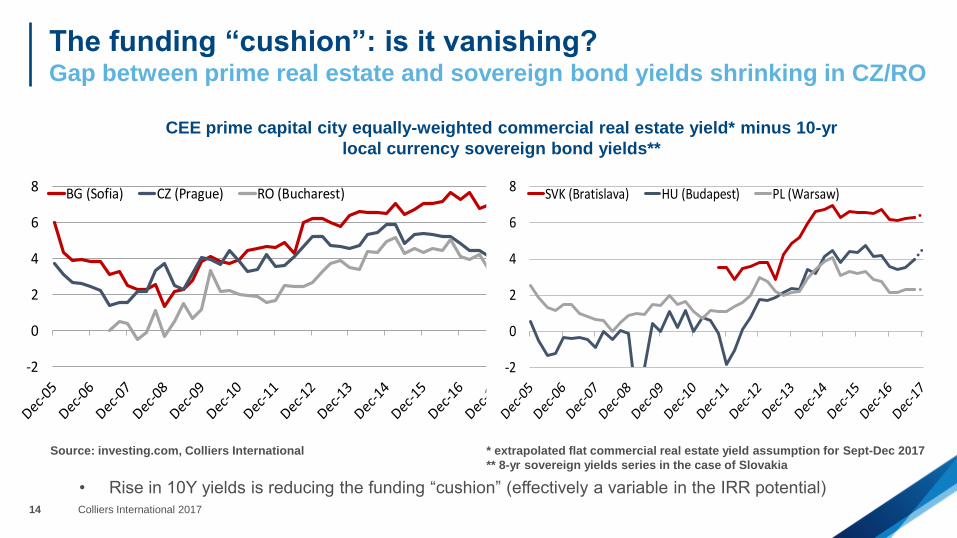

The funding “cushion”: is it vanishing?Gap between prime real estate and sovereign bond yields shrinking in CZ/RO

CEE prime capital city equally-weighted commercial real estate yield* minus 10-yr

local currency sovereign bond yields**

Source: investing.com, Colliers International * extrapolated flat commercial real estate yield assumption for Sept-Dec 2017

** 8-yr sovereign yields series in the case of Slovakia

• Rise in 10Y yields is reducing the funding “cushion” (effectively a variable in the IRR potential)

-2

0

2

4

6

8 BG (Sofia) CZ (Prague) RO (Bucharest)

-2

0

2

4

6

8 SVK (Bratislava) HU (Budapest) PL (Warsaw)

Colliers International 201715

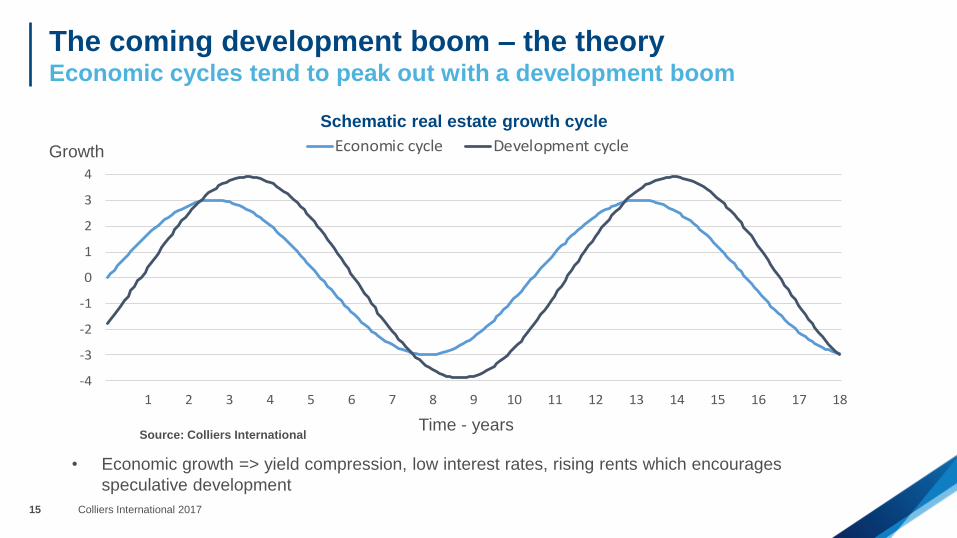

The coming development boom – the theoryEconomic cycles tend to peak out with a development boom

Source: Colliers International

• Economic growth => yield compression, low interest rates, rising rents which encourages

speculative development

Time - years

-4

-3

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Economic cycle Development cycleGrowth

Schematic real estate growth cycle

Colliers International 201716

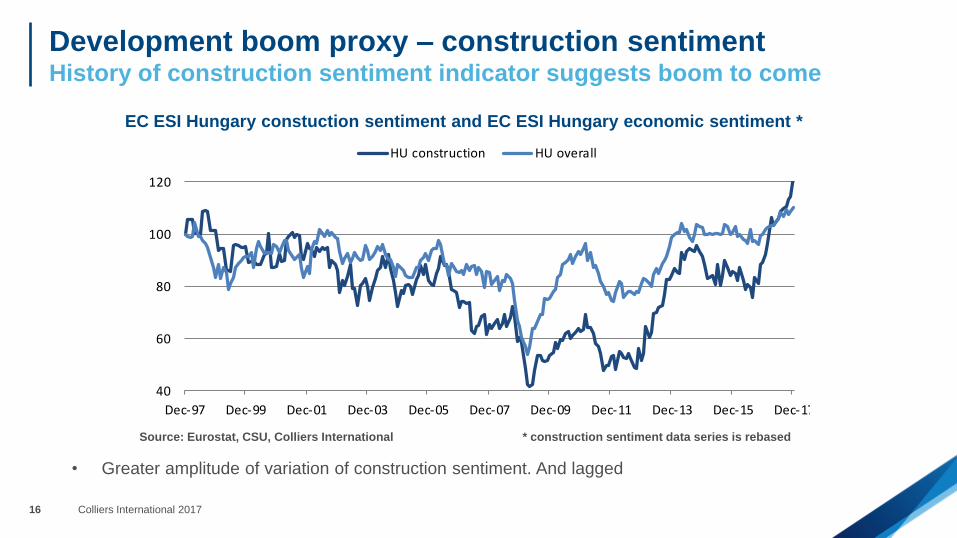

Development boom proxy – construction sentimentHistory of construction sentiment indicator suggests boom to come

EC ESI Hungary constuction sentiment and EC ESI Hungary economic sentiment *

Source: Eurostat, CSU, Colliers International * construction sentiment data series is rebased

• Greater amplitude of variation of construction sentiment. And lagged

40

60

80

100

120

Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

HU construction HU overall

Colliers International 201717

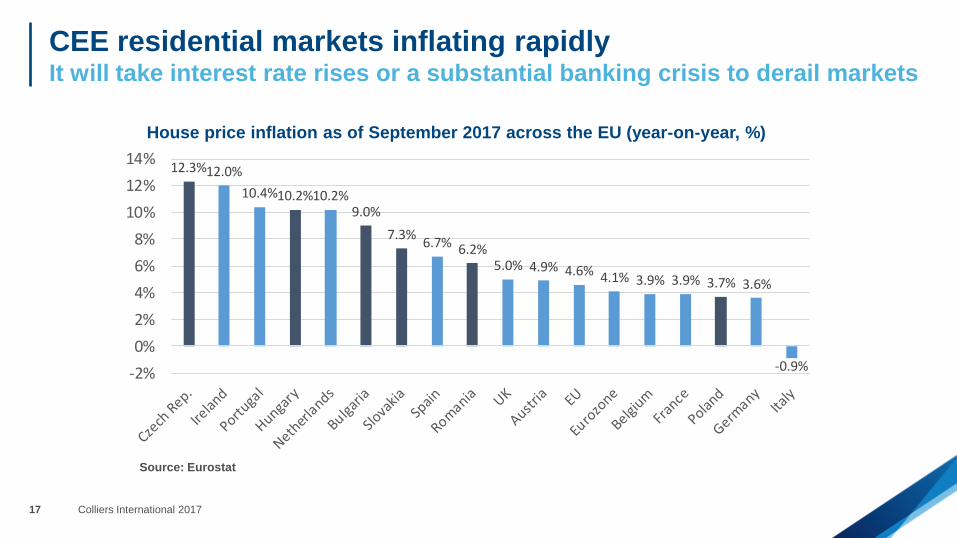

CEE residential markets inflating rapidlyIt will take interest rate rises or a substantial banking crisis to derail markets

House price inflation as of September 2017 across the EU (year-on-year, %)

Source: Eurostat

12.3%12.0%

10.4%10.2%10.2%9.0%

7.3%6.7% 6.2%

5.0% 4.9% 4.6% 4.1% 3.9% 3.9% 3.7% 3.6%

-0.9%-2%

0%

2%

4%

6%

8%

10%

12%

14%

Colliers International 201718

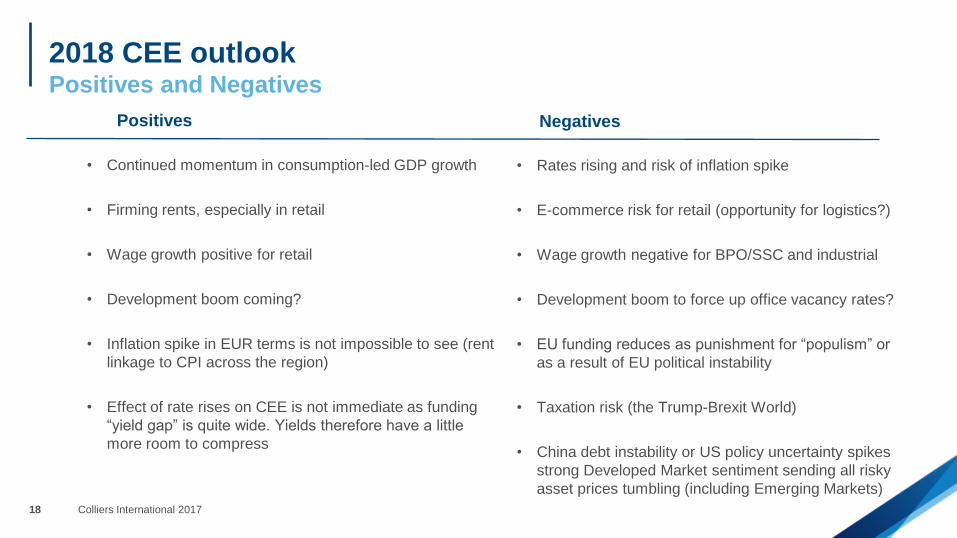

2018 CEE outlookPositives and Negatives

Negatives

• Continued momentum in consumption-led GDP growth

• Firming rents, especially in retail

• Wage growth positive for retail

• Development boom coming?

• Inflation spike in EUR terms is not impossible to see (rent

linkage to CPI across the region)

• Effect of rate rises on CEE is not immediate as funding

“yield gap” is quite wide. Yields therefore have a little

more room to compress

Positives

• Rates rising and risk of inflation spike

• E-commerce risk for retail (opportunity for logistics?)

• Wage growth negative for BPO/SSC and industrial

• Development boom to force up office vacancy rates?

• EU funding reduces as punishment for “populism” or

as a result of EU political instability

• Taxation risk (the Trump-Brexit World)

• China debt instability or US policy uncertainty spikes

strong Developed Market sentiment sending all risky

asset prices tumbling (including Emerging Markets)

Colliers International 201719

Colliers International | PragueSlovansky DumNa Prikope 859/22Prague 1 11000Czech Republic TEL +420 226 536 618

Mark Robinson

CEE Research Specialist | Prague

+420 226 537 646

1

9