Embed Size (px)

Citation preview

Tiger Alum Readies Hedge Fund Second Curve Capital, set up byformer Tiger Management stafferTom Brown, is planning to launch asmall and mid-cap fund in the comingmonths.

See story, page 2

In The NewsGoldman Hires JPMorgan

Structurer 2Asset Manager Eyes Fund 3BarCap Nabs UBS Marketer 3UBS Readies Peso Desk 3TD Credit Head Leaves 3NAB Lures Fx Sales Head 3Equity Trader Quits CDC 5UBS Pitches CDO of CDOs 5Commerz Lands Bear Stearns Head 5CAI Plans Credit Stripping Desks 5

User Strategies China Airlines Enters Swap 5Power Corp. Lights Up Swap 6ABN Sells Options In MTN 6

Departments Learning Curve: Close-Out

Netting & Set-Offs 7Markets 10

AUGUST 18, 2003VOL. XII, NO. 33

CDO STRUCTURERS EYE SINGLE-TRANCHEABS DEALS Collateralized debt obligation houses, including Bank of America and Deutsche Bank, arestarting to offer single-tranche deals referenced to asset-backed securities. “We are starting todo this; it’s a logical next step,” said Mitchell Braselton, managing director and Europeanhead of global structured products marketing for BofA in London.

Structurers began marketing single-tranche deals referenced to corporate debt last year,but were not able to offer products referenced to ABS because the deals were too illiquid. In

(continued on page 12)

KOREAN BANKING GIANT EYES CDO DEBUTSeoul-based Korea Exchange Bank, with over KRW61.4 trillion (USD51.9 billion) in assets,is considering investing in synthetic structured credit instruments, including collateralizeddebt obligations. “It’s an idea I have,” said Hee Dong Kim, head of the financial engineeringdepartment in Seoul. Kim said he is planning to speak with international derivatives housesto gain a further understanding of CDOs and credit baskets.

KEB has steered away from credit derivatives since experiencing losses in credit-linkedproducts in the Asian financial crisis, but is tempted to enter the market because of

(continued on page 12)

MERRILL DRAWS UP NOVEL CDO TOGRAB EXTRA BASIS POINTS Merrill Lynch is structuring several innovative syntheticsecuritizations to tweak extra basis points out of a creditmarket in which the arbitrage opportunities have all butdisappeared. Philippe Hatstadt, the firm’s newly installed headof structured credit derivatives trading in New York, saidinvestors are crying out for higher returns and the firm is looking

(continued on page 12)

UBS READIES MEXICAN PESO DERIVATIVES BOOKUBS is preparing to trade Mexican peso-denominated derivatives, including interest rate andcredit products by the end of the month as part of its expansion into emerging markets. “It’staken some time but we’re all set now,” said Joonkee Hong, global head of emerging marketderivatives in New York.

UBS will offer peso-denominated structured notes, interest rate and cross-currency swapsas well as credit derivatives. The Swiss bank has eyed the Mexican market since last year(DW, 12/15) but Hong noted that it has taken several months to establish systems that deal

(continued on page 12)

Check out www.derivativesweek.com for breaking news and updates—free to subscribers.

COPYRIGHT NOTICE: No part of this publication maybe copied, photocopied or duplicated in any form or byany means without Institutional Investor’s prior writtenconsent. Copying of this publication is in violation of theFederal Copyright Law (17 USC 101 et seq.). Violatorsmay be subject to criminal penalties as well as liabilityfor substantial monetary damages, including statutorydamages up to $100,000 per infringement, costs andattorney’s fees. Copyright 2003 Institutional Investor,Inc. All rights reserved.

For information regarding individual subscription rates,please contact Joe Mattiello at (212) 224-3457.

For information regarding group subscription rates and electronic licenses, please contact Dan Lalor at(212) 224-3045.

dw.08.18.03 8/16/03 4:08 PM Page 1

Stanfield Taps Head Of Risk Management

Stanfield Capital Partners, a New York-basedmoney manager that runs several hedge funds, has hired a headof risk management. Gordon Yeager was previously withsoftware vendor RiskMetrics Group, where he served as thehead of the alternative investments area responsible fordesigning and implementing risk management frameworks forclients. Yeager said he will join the firm later this month.Christie Kinney, v.p. of marketing and client services, notedthat Yeager’s position is newly created. Kinney declined tocomment further.

Stanfield manages roughly USD670 million in hedge fundstrategies, including high-yield and distressed debt. “Weappreciate the contribution [Yeager] made while working hereand we wish him luck,” said RiskMetrics spokesman MikeThompson. The firm has not yet determined whether to replaceYeager, added Thompson.

Muni Hedge Funds Take Profits AsSwap Spreads Blow OutFixed-income hedge funds have started unwinding swaps andoffloading municipal bonds to take profit after the recent surgein volatility. Ying Chen Li, director in the fixed income strategydivision at Merrill Lynch in New York, explained that manyhedge funds held short positions on LIBOR swaps as hedges fortheir portfolios. Under these trades they paid a fixed-rate basedon LIBOR and received floating. As interest-rates declined overthe last year the hedges had been losing money, however, recent

rocketing volatility has put the trades in profit. The 10-year swap spreads rocketed to 52 basis points last

Thursday, up from 40bps two weeks previous.

Tiger Alum Plans Hedge FundSecond Curve Capital, the financial sector hedge fund shopfounded by Tiger Management alumnus Tom Brown, isplanning to launch a small- and mid-cap fund in the fall. Thefirm is finalizing which prime broker it will hire for the newfund, said Stephen Krug, coo, declining to elaborate. SecondCurve, which manages USD275 million, uses ABN AMRO asthe prime broker for its flagship fund.

The firm has also hired Rick Biggs, as an analyst. Biggs said hewas previously an associate with Sanford C. Bernstein & Co.’sconsumer finance team. The hire brings the analyst team to five,Krug said. A Bernstein spokesman did not return a call. Brownwas unavailable for comment.

Goldman Lures JPMorgan Credit Structurer Goldman Sachs has hired Gilles Dellaert, credit derivativesstructurer at JPMorgan in New York, for a similar role. Dellaert,who declined comment, is reporting to Shlomi Raz, v.p. instructured credit marketing, according to an official familiar withthe move. Raz, who was traveling and could not be reached,joined the firm from JPMorgan earlier this summer (DW, 7/13).Bruce Corwin, spokesman in New York, did not return calls.Michael Dorfsman, spokesman at JPMorgan in New York,declined comment on Dellaert’s replacement.

Derivatives Week www.derivativesweek.com August 18, 2003

Copying prohibited without the permission of the publisher.2

EDITORIAL TOM LAMONT EditorSTEVE MURRAY Deputy EditorVICTOR KREMER Executive Editor (44-20) 7303-1748JEREMY CARTER Managing Editor [London] (44-20) 7303-1753KAREN BRETTELL Senior Reporter [New York] (212) 224-3269MATTHEW TREMBLAY Reporter [Hong Kong] (852) 2912-8097 CHARLOTTE MOORE Associate Reporter

[London] (44-20) 7303-1738STANLEY WILSON Washington Bureau Chief (202) 393-0728ROCHELLE BRETON Editorial AssistantJANA BRENNING, KIERON BLACK Sketch Artists

PRODUCTION DANY PEÑA DirectorLYNETTE STOCK, DEBORAH ZAKEN ManagersMICHELLE TOM, ILIJA MILADINOV,

MELISSA ENSMINGER, RAQUEL RODRIGUEZ AssociatesJENNY LO Senior Web Production DesignerTIMOTHY O’SHAUGHNESSY Web Production AssociateMARIA JODICE Advertising Production Manager

(212) 224-3267

PUBLISHINGGUY CROSSLEY Group PublisherELAYNE GLICK Director of Marketing & Circulation

(212) 224-3069RAMON MONTES Associate Marketing Manager (212) 224-3010

ADVERTISINGMICHAEL McCAFFERY Publisher, Director of Advertising

(212) 224-3534NAZNEEN KANGA Publisher, (212) 224-3005PAT BERTUCCI, MAGGIE DIAZ, KEVIN DOWNEY,

KRISTIN HEBERT, TAMARA WARD Associate PublishersUSHA BHATE Marketing Director JENNIFER FIGUEROA Media Kits (212) 224-3895

INDIVIDUAL SUBSCRIPTIONSJOE MATTIELLO Director of Sales (212) 224-3457KEN LERNER (212) 224-3043MATTHEW COLBECK (London) (44-20) 7779-8437ADI HELLER (Hong Kong) (852) 28426929,

Account Executives

GROUP SUBSCRIPTIONS/ELECTRONIC LICENSESDAN LALOR Director (212) 224-3045

REPRINTS AJANI MALIK Reprint Manager [New York] (212) 224-3205

[email protected] AND SUBSCRIBER SERVICES New York (212) 224-3800, London (44-20) 7779-8491,Hong Kong (852) 2842-6950CHRISTINE RAMIREZ Director

CHRISTOPHER BROWN Chief Executive OfficerSubscriptions: To subscribe call New York at (212) 224-3043,

London at (44-20) 7779-8437 or fax (212) 224-3491. One Year-$2,475 (in Canada add $30 postage, others outside U.S. add $75).

Derivatives Week is a general circulation newsweekly. No statement in this issue is to be construed as a recom-mendation to buy or sell securities or to provide investmentadvice.

Derivatives Week ©2003 Institutional Investor, Inc.Editorial Offices: Nestor House, London, EC4V 5EX, England. Circulation Offices: 225 Park Avenue South, New York,

NY 10003. Tel: (212) 224-3800. Fax: (212) 224-3491.For further information, please contact us at:[email protected]

At Press Time

dw.08.18.03 8/16/03 4:08 PM Page 2

August 18, 2003 www.derivativesweek.com Derivatives Week

Copying prohibited without the permission of the publisher. 3

Korean Investment House Readies FundKEB Commerz Investment Trust Management, withKRW2.7 trillion (USD2.3 billion) in assets, is gearing up across-asset class fund that will employ equity derivatives in thecoming months. Jae Hyun Lee, head of equities, said it willtrade such instruments as over-the-counter options, equity-linked notes and convertibles.

The fund, aimed at domestic institutional investors, has atarget launch size of KRW10 billion. He continued that thefund will be research-driven and primarily trade Korean bluechips.

Barclays Lures UBS Corporate Marketer Barclays Capital has hired Jonathan Shiff, director andmarketer in fixed income derivatives for U.S.-based corporatesat UBS, as a director in corporate derivatives marketing inNew York. Shiff reports to Ed Somekh, head of corporate riskmanagement and derivatives, according to Linda Wynns,spokeswoman in New York. Neither Shiff nor Somekhreturned calls.

At UBS Shiff reported to Suneel Kamlani, global head ofdebt capital markets in London, said Kris Kagel, spokesmanin Stamford, Conn. Kamlani was on vacation and could notbe reached.

Did Florida Hedge Fund Try To Pull A Fast One On Bear Stearns?Magnolia Capital Advisors, which was reportedly told toliquidate up to USD120 million in positions by Bear Stearns,its prime broker, may have tried to end-run the order byeffectively striking a repo agreement. Don Reinhard, ceo of theTallahassee-based hedge fund, did not reply to a series of phonecalls and e-mails seeking comment. Bear Stearns MBS chiefTom Marano declined to comment.

An individual involved with the trades says that Reinhardinitially complied with Bear Stearns’ order by selling the paperinto the marketplace and booking the trade as a sale. But thenMagnolia allegedly negotiated directly with WRH Mortgage ofSt. Petersburg, the money manager purchasing the bonds, toeffect a series of repurchase agreements for the approximatelyUSD120 million of CMOs.

WRH had no knowledge of Bear Stearns’ forced sale, theperson said. When the repurchase agreement trade ticket wassubmitted to Bear Stearns’ back office, it declined torecognize the trade, forcing WRH to take ownership of thebonds. It could not be learned what action, if any, Bear

Stearns is planning to take against Magnolia. WRH founderWilliam Hough was out of the office and unavailable forcomment, according to Joe Waechter, a portfolio manager atthe firm, who declined comment. WRH has reportedly madeno decision regarding any potential legal actions it mightpursue.

TD Securities U.S. Credit Trading Head DepartsAdrian Hyde, U.S. head of credit derivatives trading in NewYork, has quit TD Securities to set up an independentinvestment firm. Joe Hegener, vice chairman in New York,who Hyde reported into regionally, said Hyde quit because hewanted to set up his own project. Hyde and Hegener declinedcomment on the new venture.

Hyde has been replaced internally, according to Hegener,who declined to name the successor. On the product side,Hyde reported to John Gisborne, global head of creditderivatives trading in London.

Bank of China Eyes Sales, Trading PushBank of China International, the investment banking armof mainland giant Bank of China, is planning to bulk up itsfixed income and equity operation in Hong Kong. WarrenKwan, head of equity derivatives, said he is preparing to hirearound a total of five staff including marketers and traders.He is planning to wait until year end, however. “We’rewaiting until bonus season ends,” said Kwan. “We want tohire multi-talented people that can look at such asset classesas fixed income, fx, equity and credit,” he noted.

The current team of 11 handles such products as equityoptions, equity-linked notes and credit-linked notes.

NAB Grabs Fx Sales Head In U.S.National Australia Bank has hired Jacqui Steel, a foreignexchange professional at Westpac Banking Corp. in NewYork, as head of institutional foreign exchange sales, whichincludes over-the-counter options. Robert Cone, senior v.p.and head of the markets division for the Americas at NAB inNew York, said Steel has been hired as the Australian firmaims to pump up its U.S. fx sales coverage. Steel will start inOctober. She could not be reached for comment.

NAB anticipates making several additional hires in fx sales,particularly focusing the firm’s efforts toward hedge funds andreal money accounts, Cone said.

Officials at Westpac in New York did not return callsregarding Steel’s replacement.

dw.08.18.03 8/16/03 4:08 PM Page 3

present

20th November 2003London, Royal Garden Hotel

Register by 30th September 2003 and receive a £100 discountwww.euromoneyseminars.com/derivatives

Tel: USA TOLL FREE 1-800 437 9997 (free from within the USA) or UK+44 (0) 20 7779 8999

and

■ Learn about implementation of newcomplex accounting standards

■ Identify how to handle the transition period

■ Meet key industry players and gain newclients through targeted networking

The Inaugural

Mastering the complexities of IAS 32, 39 and SIC 12

Derivatives Accounting Summit 7/17/03 1:55 PM Page 1

August 18, 2003 www.derivativesweek.com Derivatives Week

Copying prohibited without the permission of the publisher. 5

Equity Trader Departs CDC In New YorkJason Megson, an equity derivatives trader at CDC IXISNorth America in New York, has left the firm. Megson, whocould not be reached, is not yet thought to have joined acompetitor. His departure follows Quincy Evans andChristophe Thomas, who co-headed the firm’s convertiblearbitrage effort (DW, 7/13). Janine Shagoury, spokeswomanin New York, declined comment.

Megson reported to Vuk Bulajic, head of equity derivatives atCDC in New York, who was on vacation and could not be reached.

UBS Markets CDO Of Senior CDOsUBS Securities is marketing a USD1 billion resecuritization ofoutstanding collateralized debt obligations that is expected tobe priced after Labor Day, according to investors and sell-sideanalysts. The firm is trying to gather investors for thetransaction, which will pool senior tranches of CDOs to createa CDO of CDOs, according to the officials. One marketparticipant said this is somewhat unusual, since most CDOsquareds are referenced to higher-yielding mezzanine tranchesto clip the higher coupons offered on junior tranches. Thesedeals also tend to be smaller, because there are feweroutstanding mezzanine pieces and they are smaller.

Jeff Herlyn, co-head of CDO banking, was on vacation lastweek and Mike Rosenberg, also co-head, was traveling and didnot return a call by press time.

Commerzbank Lands Ex-BearStearns Credit Trading Co-Chief Eric Langille, former co-head of credit derivatives trading atBear Stearns in New York, has joined Commerzbank as headof flow credit trading, which includes credit derivatives.George O’Dowd, head of New York credit trading, whoLangille reports into, said the hire caps off the German firm’sU.S. additions. Commerzbank is now “at full strength,” henoted. Langille, who declined comment, also reports toMichael Staveley, global head of credit trading in London.Staveley declined comment.

David Madon, former managing director and Americashead for credit markets and credit derivatives at CreditLyonnais Securities in New York, also recently came on boardas a senior structured derivatives marketer and productmanager (DW, 7/20).

Michele Agostinho, spokeswoman at Bear Stearns in NewYork, did not return calls regarding Langille’s replacement.

Crédit Agricole Eyes Bond Stripping Desks Crédit Agricole Indosuez is bulking up its convertible bondstripping group, with plans to expand in the U.S. and Asia and arecent addition in London. “The business is growing quite fast,”said Loic Fery, managing director and global head of creditderivatives and structures in London. Zouhair Bechchar,director and head of convertible asset swap trading in London,said that given the increase in client interest and growingissuance, the bank is looking to set up a New York-basedconvertible stripping desk by the middle of next year. “We’ll beputting a small desk there,” said Bechchar, noting that it willlook to bring in two staff for the effort, after the integrationwith Credit Lyonnais. He continued that CAI will hire anadditional convertible bond stripper for its Hong Kongoperation. Zouhair elaborated that the firm’s activity in theconvertibles stripping market has doubled in the last severalmonths, with volumes now exceeding USD3 billion per month.

For the London desk, CAI recently hired Jav Bose, convertibleasset swap trader at Merrill Lynch in London, for a similar role. “Wewant to become a global player,” said Bose, adding, “We’ve beenstrong in Europe and now we want to build up in the U.S. and Asia.”

At Merrill, Bose reported to David Page, director in equitiesin London. Page said that a replacement is intended for Bose,along with an impending restructuring of the group, butdeclined to elaborate.

China Airlines Executes SwapTaiwan’s China Airlines recently entered a five-year TWD1 billion(USD29 million) interest rate swap on its floating rate liabilityportfolio and plans to convert more into fixed rate debt in thecoming months. “It’s a good time to increase our liabilityportfolio hedging,” said Yang Yen, researcher in the financialdepartment in Taipei.

In the swap China Airlines pays a fixed rate and receives floatingto partially hedge its TWD26 billion floating-rate domesticportfolio. Yen continued that around 30% of its domestic portfolio,combined with its U.S. dollar-denominated USD1.4 billion indebt, is currently in fixed rate liabilities. She explained that givenprevailing low rates, China Airlines plans to increase its fixed ratehedging by 10% or greater in the coming months. “We’re justwaiting for the right price,” Yen added. “Flow-wise, a lot ofcorporates are interested in five-year swaps,” said Diamond Doong,manager of interest rate trading at Taishin International Bank inTaipei, the counterparty on the swap.

User Strategies

dw.08.18.03 8/16/03 4:08 PM Page 5

Derivatives Week www.derivativesweek.com August 18, 2003

U.S. Power Corp. Enters Swap, Locks In SavingsOil and gas producer Devon Energy has entered an interest-rate swap to convert a fixed-rate USD500 million note issueinto a synthetic floater. Brian Engel, spokesman in OklahomaCity, explained that the corporate is able to reduce its interestrate costs by 1.15% via the swap. This, in turn, creates savingsof USD5.75 million for the company.

In the swap, which mirrors the three-year maturity of thenotes, Devon receives the 1.75% coupon and pays LIBORminus 27 basis points, said Engel. UBS lead managed the notesale and is the counterparty on the swap.

ABN Structures Callable MTN With Digital OptionsABN AMRO is purchasing embedded digital options onforward dollar swap spreads to structure a 10-year callablemedium-term note. The note offers a 6.3% annualized couponevery day that the 30-year swap rate is above the two-year rate,which is a pick up of up to 130 basis points on 10-year Treasurybonds. Thomas Zieglmeyier, Swiss head of derivatives sales forfinancial markets in Zurich, said, “This note offers our clientsthe ability to take a view on the relative rather than absolutevalues of the 30-year and two-year dollar swap rates as well asoffering a higher yield.” The two-year rate normally trades belowthe 30-year rate, however, the market is expecting rates to rise

soon and as a result the yield curve is steep. Once the FederalReserve raises rates the curve is likely to flatten, but if the marketthen starts to price in fresh rate cuts the curve could invert.

ABN structures the note by buying a series of callableBermudan options, which gives it the right to call the note andcancel the options. It can call the note after six months andthen every quarter. Investors receive the principal and quarterlycoupons once the note is called.

Banque et Caisse d’Epargne de l’Etat issued the note. ABNdistributes it to its private clients.

Investec Sells Options For Structured Product Investec Financial Products is selling a structured note withembedded options to give investors capital protected exposureto Nova Alpha, a fund of hedge funds. Andrew Irvine, head ofstructured investment products in London, said it is launchingthe product because of demand for capital preservation andinterest in the hedge fund sector.

Bear Stearns structured the note by purchasing a zero-coupon bond, to guarantee investors 100% of their capital,and then call options to allow 80% participation in the upside.Both the note and option have a seven-year maturity.

Hedge Fund Research will manage the Nova Alpha fund offunds, which is made up of 10 different hedge fund strategiesincluding long/short equity, convertible arbitrage anddistressed securities and 26 different managers.

You

read

it here

first!We stay aheadof our competitionso you can stayahead of yours.

Merrill Forms New Structured-CreditArm, Derivatives Week SaysMerrill Lynch & Co. formed a structured-credit group in its principal finance unit,and named former head of creditderivatives Steve Padovano to run it,Derivatives Week said, citing anunidentified official. Among other banks with structured-credit group’s within principal finance,where bank buy bonds and repackagethem or keep them on their balancesheets, are Deutsche Bank AG andUBS AG, Derivatives Week said. Thepractice lets banks compete with

AUGUST 5, 2003

MERRILL SETS UP PRINCIPAL FINANCE

STRUCTURED CREDIT ARM

Merrill Lynch has set up a structured credit arm within

its principal finance operation and has appointed Steve

Padovano, former global head of credit derivatives in

New York, to spearhead the effort. The initiative comes

as more firms look toward principal finance as a means

of competing in an increasingly crowded marketplace.

Padovano declined comment. Michael DuVally,

spokesman in New York, declined to comment.

Other firms known to have structured credit divisions

within their principal finance businesses, through which

they invest in fixed-income securities and either

AUGUST 4, 2003

To Subscribe Call 212 224 3570 (USA), + 44 20 7779 8999 (UK), EMAIL: [email protected]

dw.08.18.03 8/16/03 4:08 PM Page 6

August 18, 2003 www.derivativesweek.com Derivatives Week

Copying prohibited without the permission of the publisher. 7

The huge role of U.S. banks in the derivativesindustry means counterparties must

understand the treatment of close-out netting and set-off foran insolvent bank by the Federal Deposit InsuranceCorporation (FDIC). Close-out netting and set-off, both ofwhich are typically provided under the ISDA MasterAgreement, provide the most effective and efficient way tominimize credit risk with respect to the insolvency of acounterparty.

Close-out Netting. The solvent party is concerned thatupon the insolvency of its counterparty, it will have to makepayments to the receiver or conservator, while remaining as ageneral creditor with respect to payments the insolvent bankowes to it. In such a scenario, the possibility of collecting theseamounts is minimal. Close-out netting, as provided under theISDA Master, eliminates much of that concern. First, itprovides that the solvent counterparty can terminate the ISDAAgreement upon the bank’s insolvency. As part of thetermination and close-out of an ISDA Agreement, eachincluded individual or included transaction is closed-out at itsmark-to-market value. The mark-to-market value is usuallyequal to the cost of replacing the individual terminatedtransaction.

Second, close-out netting provides that the solvent partycan then net the termination value of any transaction forwhich it is out-of-the-money with the termination value of anyTransaction for which it is in-the-money.

Set-off. Set-off rights are similar and generally are providedfor under the ISDA Agreement. The terms set-off or offsetrefer to the right of the solvent party to contractually set-off oroffset the net amount it owes to the insolvent party under theISDA Agreement, which occurs after close-out netting hasbeen applied, against any other amounts that the insolventparty owes to the solvent party, or vice versa. For example,assume that the solvent party owes the insolvent bank a netamount of USD20 under the ISDA Agreement, and theinsolvent bank owes the solvent party USD30 on a differenttransaction apart from the ISDA Agreement. The right of set-off under the ISDA Agreement would contractually permit thesolvent party to set-off the USD20 that it owes the insolventbank against the USD30 that the insolvent bank owes to thesolvent party, with the result being that the insolvent bank

owes the solvent party USD10. FDIA. Although the ISDA Agreement contractually

provides for both close-out netting and set-off, the concern isthat banking insolvency rules would prevent the solventcounterparty from exercising such rights. The insolvency of aninsured financial institution (i.e. a U.S. bank that acceptsFDIC insured deposits) is governed by Federal DepositInsurance Act as amended by FIRREA. In addition, theFederal Deposit Insurance Corporation Improvement Act of1991 (“FDICIA”) also must be considered. Parties are oftentempted to assume that the special insolvency rules withrespect to the treatment of derivatives for an insolvent U.S.bank under FDIA are completely parallel with the rules foundin the U.S. Federal bankruptcy code (the “Code”), the rulesthat govern the bankruptcy of most U.S. corporations.However, the mechanics and policy rationales behind FDIAare quite different from those under the Code.

Close-out Netting Under FDIA. Under FDIA, the generalrule is the FDIC may enforce a contract with a solventcounterparty if the sole reason for the termination of thecontract is the appointment of the FDIC as the receiver orconservator for the insolvent bank. There exists, however,important exceptions for contracts involving swap agreements.Swap agreements are defined under FDIA in a manner similarto that of the Code and includes a wide variety of the mostcommon over-the-counter derivative transactions.

Upon the appointment of the FDIC as a receiver or as aconservator, the FDIC initially has the power to transfer anISDA Agreement to another FDIC-insured bank. There is nosuch parallel power for the bankruptcy trustee of a debtor underthe Code. This means that a solvent party not only cannotinitially terminate the ISDA Agreement with an insolvent bank,but also may end up with a different counterparty altogether.Although such transfers, historically as a practical matter are rarethe power to do so is invested in the FDIC.

If the FDIC is a receiver, however, such transfer power mustbe exercised immediately. If the FDIC does not transfer an ISDAAgreement by close of business on the day following itsappointment as a receiver, the solvent counterparty may then goahead and terminate the ISDA Agreement. This closely resemblesa solvent creditor’s rights under the Code, although there is still aone day delay for terminating the ISDA Agreement that does not

L E A R N I N G C U R V E ®

Close-Out Netting & Set-Off Under U.S. Banking Insolvency Law

������������

Derivatives Week is now accepting submissions from industry professionals for the Learning Curve® section. For details and guidelines on writing a Learning Curve®,please call Jeremy Carter in London at 44-20-7303-1753, Karen Brettell in New York at 212 224 3269 or Matthew Tremblay in Hong Kong at 852-2912-8097.

dw.08.18.03 8/16/03 4:08 PM Page 7

Derivatives Week www.derivativesweek.com August 18, 2003

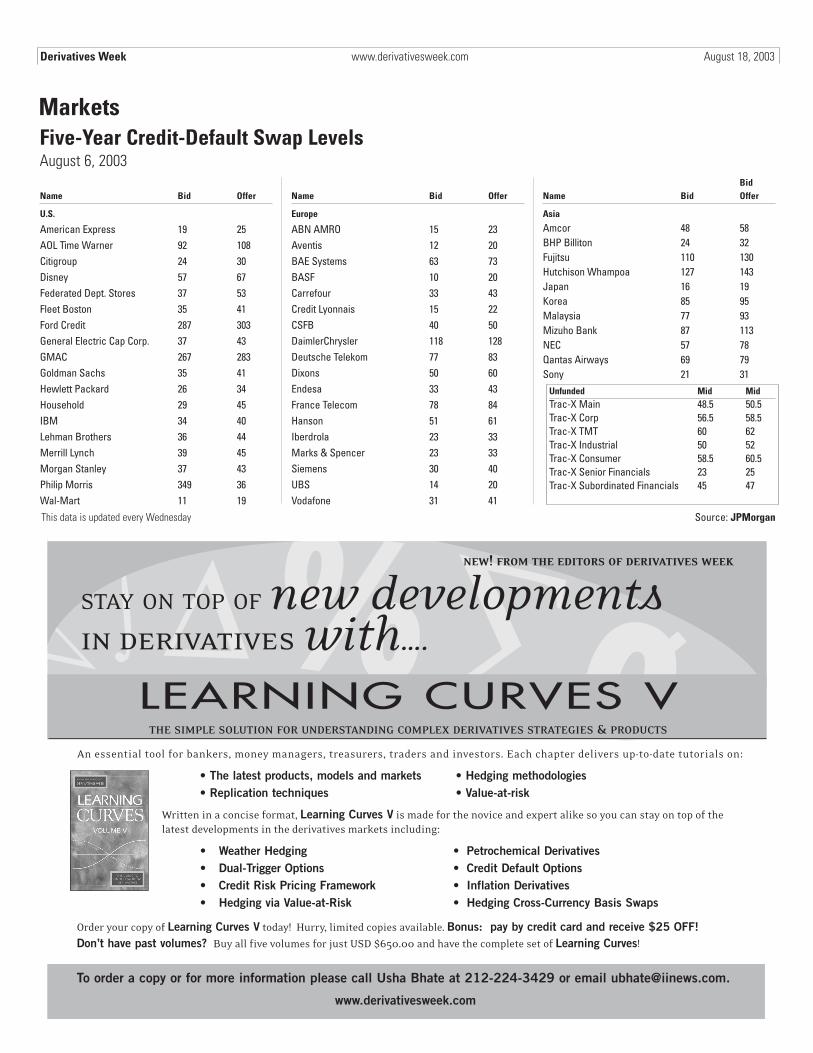

Markets

Name Bid Offer

U.S.

American Express 19 25AOL Time Warner 92 108Citigroup 24 30Disney 57 67Federated Dept. Stores 37 53Fleet Boston 35 41Ford Credit 287 303General Electric Cap Corp. 37 43GMAC 267 283Goldman Sachs 35 41Hewlett Packard 26 34Household 29 45IBM 34 40Lehman Brothers 36 44Merrill Lynch 39 45Morgan Stanley 37 43Philip Morris 349 36Wal-Mart 11 19

Name Bid Offer

Europe

ABN AMRO 15 23Aventis 12 20BAE Systems 63 73BASF 10 20Carrefour 33 43Credit Lyonnais 15 22CSFB 40 50DaimlerChrysler 118 128Deutsche Telekom 77 83Dixons 50 60Endesa 33 43France Telecom 78 84Hanson 51 61Iberdrola 23 33Marks & Spencer 23 33Siemens 30 40UBS 14 20Vodafone 31 41

BidName Bid Offer

Asia

Amcor 48 58BHP Billiton 24 32Fujitsu 110 130Hutchison Whampoa 127 143Japan 16 19Korea 85 95Malaysia 77 93Mizuho Bank 87 113NEC 57 78Qantas Airways 69 79Sony 21 31

Five-Year Credit-Default Swap LevelsAugust 6, 2003

This data is updated every Wednesday Source: JPMorgan

Unfunded Mid MidTrac-X Main 48.5 50.5Trac-X Corp 56.5 58.5Trac-X TMT 60 62Trac-X Industrial 50 52Trac-X Consumer 58.5 60.5Trac-X Senior Financials 23 25Trac-X Subordinated Financials 45 47

µ√

∫ ∆%∑øSTAY ON TOP OF new developmentsin derivatives with….

An essential tool for bankers, money managers, treasurers, traders and investors. Each chapter delivers up-to-date tutorials on:

• The latest products, models and markets • Hedging methodologies• Replication techniques • Value-at-risk

Written in a concise format, Learning Curves V is made for the novice and expert alike so you can stay on top of thelatest developments in the derivatives markets including:

• Weather Hedging • Petrochemical Derivatives• Dual-Trigger Options • Credit Default Options• Credit Risk Pricing Framework • Inflation Derivatives• Hedging via Value-at-Risk • Hedging Cross-Currency Basis Swaps

NEW! FROM THE EDITORS OF DERIVATIVES WEEK

LEARNING CURVES VTHE SIMPLE SOLUTION FOR UNDERSTANDING COMPLEX DERIVATIVES STRATEGIES & PRODUCTS

Order your copy of Learning Curves V today! Hurry, limited copies available. Bonus: pay by credit card and receive $25 OFF!Don’t have past volumes? Buy all five volumes for just USD $650.00 and have the complete set of Learning Curves!

To order a copy or for more information please call Usha Bhate at 212-224-3429 or email [email protected].

www.derivativesweek.com

dw.08.18.03 8/16/03 4:08 PM Page 8

August 18, 2003 www.derivativesweek.com Derivatives Week

Copying prohibited without the permission of the publisher. 9

occur under the Code.A solvent counterparty’s termination rights under the ISDA

Agreement are suspended if the FDIC is appointed as aconservator. Here, the FDIC as a conservator essentially stepsinto the shoes of the insolvent bank and assumes the rights andobligations of the insolvent bank. To terminate an ISDAAgreement after the appointment of the FDIC as aconservator, an event of default (other than an insolvency orinsolvency related event) or a termination event would have tooccur or the conservatorship would have to be replaced by areceivership. This is opposite from under the Code in whichthere is no stay on the solvent party from terminating theISDA Agreement.

As a practical matter, the vast majority of U.S. banks arenow put into receivership as opposed to conservatorship. It isunclear, however, how the FDIC would deal with theinsolvency of a large U.S. bank that was also acting as aderivatives dealer. By placing the dealer into a conservatorship,a solvent counterparty’s rights to terminate the ISDAAgreement may be indefinitely suspended.

Many believe a party’s close-out netting rights could still beenforced under certain circumstances under FDICIA, whichprovides that “notwithstanding any other provision of law”, aparty may enforce the close-out netting terms of a nettingcontract entered into between financial institutions. ISDA hasobtained legal memorandums that support such a reading ofthe statute. The FDIC, on the contrary, has taken the officialposition that FDICIA only enforces a party’s netting rights andnot the right to terminate an ISDA Agreement.

Cherrypicking. A concern for solvent parties with respect toclose-out netting, especially when the FDIC is appointed as aconservator, is cherrypicking. FDIA, however, has eliminatedthis risk. This is important because the solvent party’s creditanalysis is dependent upon close-out netting between all of thetransactions entered into with the bank.

FDIA defines a swap agreement as including both an ISDAAgreement as well as each of the underlying transactions. Eventhough there may be hundreds of transactions entered under asingle ISDA Agreement, FDIA treats it is as one agreement.Consistent with this definition, if the FDIC elects to transferan ISDA Agreement, it must also transfer all of the underlyingtransactions in the same ISDA Agreement to the sametransferee.

Set-off of a Qualified Financial Contract. Beyond close-outnetting, FDIA expressly provides for set-off of the earlytermination amount under the ISDA Agreement with amountsdue under other qualified financial contracts. FDIA definesqualified financial contracts as including a swap agreement, aqualified financial contract includes a securities contract,

commodity contract, a forward contract or a repurchaseagreement. A party entering into a swap agreement with a U.S.bank may also have entered other qualified financial contractswith that same bank that were not documented under thesame ISDA Agreement. The contractual set-off provisionfound in an ISDA Agreement should be sufficient to permit aparty, under FDIA, to set-off the amount owing under a swapagreement with amounts owing under any other qualifiedfinancial contracts entered into with the same party.

Set-off Against Other Amounts. After exercising its close-out netting rights and setting-off any net amounts that thesolvent party owes to the insolvent bank under qualifiedfinancial contracts, there may still be amounts owed by thesolvent party to the insolvent U.S. bank under the ISDA. Thesolvent party would want to set-off such amount against anyother amounts (apart from amounts under qualified financialcontracts) owed by the insolvent bank to it such as depositsthat the solvent party has with the U.S. bank.

Although the FDIC will generally recognize and will enforcea creditor’s right of set-off against an insolvent bank, suchrights may be severely limited because of application of thedepositor preference liquidation provisions of FDIA. TheFDIC would probably view these provisions as preemptingsuch a set-off right. Under the depositor preference liquidationprovisions, the FDIC as a receiver or conservator is required todistribute amounts collected from the liquidation or resolutionof the insolvent bank and then pay off any claims against thebank. Before the claims of general creditors are paid, theadministrative expenses of the FDIC and any domestic depositliabilities of the insolvent bank are paid off first.

If the solvent party were out of the money, the FDIC wouldrequire the party first to pay in any amounts that such a partyowed and would consider the solvent party to be a generalcreditor for any amounts owing to it by the insolvent bank.

Permitting the party to set-off any amounts owing to it bythe insolvent bank that were not of the same preference wouldappear to violate the depositor preference provision. This isbecause an insolvent bank’s obligation to a party with a lowpreference would be paid through application of the set-offprior to the other deposit liabilities with a higher preferencebeing paid off. Effectively, the only opportunity to exercise aset-off right would appear to be a situation in which thesolvent party that is out of the money under the ISDAAgreement had insured deposits with the insolvent bank thatwould be paid by the FDIC.

This week’s Learning Curve was written by Christian Johnson,associate professor at Loyola Law School in Chicago. He can becontacted at [email protected]

dw.08.18.03 8/16/03 4:08 PM Page 9

Stay Ahead of the Competition!Request your FREE no risk trial today and get exclusive breaking news

on some of the hottest topics in the financial industry!

Vendor Forum

401(k) Asset Slump

With 401(k) assets declining for the first

time in 20 years, some may wonder if

the defined contribution industry is still

attractive to money managers.

See Vendor Forum, page 9

Search Advisory

Computer Firm Selects Funds

3

Diamond Shops To Review Lineup3

Miss. Bank Taps Federated

4

Law Firm Considers Fund Search4

SUPERVALU Adds Funds

4

Vendors

T. Rowe Preps Wireless Product5

NYLB Names Prof. Services Head5

First Union Aligns With Berger5

Washington

Sen. Kennedy Introduces

Spousal Consent Bill

6

Departments

Profile

7

Search Directory

11

JULY 30, 2001

VOL. IX, NO. 16

MELLON EYES UNIFI NETWORK ACQUISITION

Mellon Financial

/Dreyfus Retirement Servi

cesis re

portedly intere

sted in buying

Pricewater

houseCooper’s

outsourcing unit, U

nifi Netw

ork. According to a so

urce fam

iliar

with Mellon’s plans, th

e vendor wants to

buy Unifi Netw

ork, which has roughly $64

billion in DC ass

ets under m

anagement, to broaden its

outsourcing exposure in

the

industry. Jo

seph Eck, senior v.p

. at Dreyfus, an

d Michael Stern

klar, head

of PwC’s

outsourcing business,

did not return rep

eated cal

ls by press

time. A

spokesman for U

nifi

Network said

that the PwC announced

last year

that it will b

e spinning off se

veral

(continued on page 1

1)

HELICOPTER TRANSPORTATION PLAN

SEARCHES FOR NEW PROVIDER

Petroleum Helic

optershas la

unched a search

for a new bundled provider f

or its $125

million 401(k) plan due to

poor service

from its curren

t provider, J.P. M

organ/ American

Century Plan Services,

said an offici

al at th

e plan. The official, w

ho wished to remain

anonymous, added that t

he 1,500-life plan has b

een unhappy with Americ

an Century’s

customer service

and some of its mutual fu

nds, decli

ning to provide specif

ics. “Their

funds have not being doing well f

or awhile,”

he said. A spokesw

oman at Americ

an

(continued on page 1

2)

Hewitt Study

AUTOMATIC ENROLLMENT COULD

WORK AGAINST SOME EMPLOYEES

Despite evidence t

hat automatic

enrollment ca

n increase 4

01(k) participant ra

tes, it ca

n

work against some em

ployees’ ass

et accu

mulation, aff

ecting their r

etirement in

come

security,

said Hewitt A

ssociates in

a study conducted

with researc

hers from Harva

rd

University

and the Univer

sity of Chicag

o. The study said

that although automatic

enrollment in

creases

participatio

n rates, p

articipants a

re more li

kely to remain at t

he

(continued on page 1

1)

Getting Personal

INVESMART TO ROLL OUT PROPRIETARY ADVICE

Invesmart

is working on plans to

offer perso

nalized fin

ancial advice

to its parti

cipants

through a call c

enter. Charli

e Kennedy, product d

evelopment v.p

., said it o

ffers fin

ancial

advice only to its

high-net-worth clie

nts but would begin to offer

advice to its

401(k)

clients b

y next year. Invesm

art curren

tly has an alli

ance with Morningstar

to offer advice

via the W

eb. Kennedy said it d

ecided to offer

the personaliz

ed advice based

on client

demand, adding that t

he financial

advice model is

part of its

overall st

rategy to provide

(continued on page 1

2)

COPYRIGHT NOTICE: No part of this publication may

be copied, photocopied or duplicated in any form or by

any means without Institutional Investor’s prior written

consent. Copying of this publication is in violation of the

Federal Copyright Law (17 USC 101 et seq.). Violators

may be subject to criminal penalties as well as liability

for substantial monetary damages, including statutory

damages up to $100,000 per infringement, costs and

attorney’s fees. Copyright 2001 Institutional Investor,

Inc. All rights reserved.

For information regarding group subscription rates

and electronic licenses, please contact Dan Lalor at

(212) 224-3045. Check www.dcnews.com during the week for breaking news and updates.

AICPA, SEC Draw Line

In The Sand

The American Institute of Certified

Public Accountants and Financial

Accounting Standards Board are

moving ahead with a vote on a block

discounting project, an effort which has

received sharp criticism from the

Securities and Exchange

Commission. See story, page 2

In The News

Investmart Plans Live Advice2

Fidelity Implements Customized

Statement Feature

3

Many Americans Unaware Of

Tax Relief, Study Says3

Smaller Managers Experiencing

Large Inflows This Year3

GE Creates Mid-Cap Growth Position 4

Citigroup Exec To Take Institutional

Approach

4

Technology

SEI To Integrate Advent, Vertical

Management Software7

Washington

Levitt Predicts Bright Future For Actively

Managed ETFs

7

Disclosure Watchdogs Call ICI

Dismissive

9

JULY 30, 2001

VOL. XII, NO. 30

A New Face

MORGAN INTEGRATING ALL STAFF,

UNITS OF FUND GROUPS

Morgan Stanley Dean Witter is creating two asset management brands, Morgan Stanley

Funds and Van Kampen Investments, and is integrating all staff and business units of Van

Kampen and Morgan Stanley Investment Management (MSIM). Michael Santo,

executive v.p. of operations and technology at Van Kampen, has been moved up to the new

position of chief operating officer and chairman of the management committee for Van

(continued on page 11)

BANK OF NEW YORK OPENING INVESTMENT

MANAGEMENT SERVICES CENTER IN ORLANDO

The Bank of New York Investment Management Services is opening a service center in

Orlando, Florida that will handle expansion of up to 330 fund accounting and technology

staffers and executives. Jeff Bieselin, senior v.p., said the expansion is a result of growth in

the financial companies services sector and the trend of investment management

companies, including mutual funds, looking to increasingly outsource fund accounting

and other back-office services.

(continued on page 12)

Nascent Market

BARCLAYS TO BE FIRST U.K. SPONSOR OF

MANAGED ACCOUNT PLATFORM

Barclays Stockbrokers is opening up the first separately

managed account platform in the

U.K. sponsored by a local player, and is set to launch technology to allow it to link with fund

managers around the globe. Nick May, product development manager at B

arclays, said the

firm is implementing CheckFree Investment Services’ APL Wrap system as the back-office

core of the product which will allow it to link with global money managers. Barclays has

(continued on page 11)

OPPENHEIMER, MFS MAKE BID FOR ZURICH

SCUDDER’S SEPARATE ACCOUNTS BIZ

OppenheimerFunds and MFS are among a number of firms making a bid to acquire

Zurich Scudder Investments’ separate accounts business. A recent report in The Wall Street

Journal indicated that Zurich Scudder was interested in some type of overhaul of its asset

management business, including a myriad of merger and acquisition possibilities, but the

report offered no specifics. According to an industry insider with knowledge of

Oppenheimer, Zurich is specifically accepting bids for its separate accounts business and in

(continued on page 11)

COPYRIGHT NOTICE: No part of this publication may

be copied, photocopied or duplicated in any form or by

any means without Institutional Investor’s prior written

consent. Copying of this publication is in violation of the

Federal Copyright Law (17 USC 101 et seq.). Violators

may be subject to criminal penalties as well as liability

for substantial monetary damages, including statutory

damages up to $100,000 per infringement, costs and

attorney’s fees. Copyright 2001 Institutional Investor,

Inc. All rights reserved.

For information regarding group subscription rates

and electronic licenses, please contact Dan Lalor at

(212) 224-3045.

Check www.fundaction.com during the week for breaking news and updates—free to subscribers.

DATAlynx Corners AdvisorsLast week advisor supermarket firm

DATAlynx held its annual conference in

Denver, Colo.

See conference coverage, pages 6-7

In The NewsMellon, Dreyfus Negotiate

With Citizens2

NY Life Hires Pru Official 2

Teachers’ VA Searching

For Managers2

Morgan Stanley Adding

Nasdaq Fund3

Investec Hires Head Wholesaler 3

Henderson Staffing Up 4

Marketing Strategies

Phoenix VA Company

Targets Affluent3

Aetna Playing Catch Up

With Fund Fees4

InternetMorgan Stanley Adding

Intranet Services4

DepartmentsProfiles Of New Funds 9

New Classes Of Shares 9

New Fund Filings10

JULY 30, 2001

VOL. VI, NO. 30

MORGAN STANLEY CREATES CLIENT GROUP,

MERGES FUND BRANDS

Morgan Stanley Investment Management has created a seven-unit client group that re-

organizes Morgan and Van Kampen Investments staff and resources around channels,

including mutual funds, 401(k)s and variable annuities, international and institutional.

Dick Powers, ceo of Van Kampen, will run the group in addition to his current role. In an

internal memo obtained by FMA sister publication Money Management Letter, Mitch

Merin, head of Morgan Stanley Investment Management, said, “The Client Group

(continued on page 12)

GE TO LAUNCH SEPARATE ACCOUNTS

FOR RETAIL INVESTORS

GE Asset Management is planning to slash its traditional multi-million dollar minimum

for institutional separate accounts and develop a series of managed accounts for retail

investors to be distributed through third-party intermediaries such as wirehouses. The

move represents GE’s first effort to bring its institutional services which typically require

$25 million minimum deposits down to a level where individual shareholders can

participate at $100,000 per account, according to an insider who is familiar with the

(continued on page 11)

Revolving Door

EQUITABLE DISTRIBUTORS’ CEO DEPARTS

Pat Miller, ceo of Equitable Distributors (EDI), has stepped down and will be officially

replaced at the end of next month by current president Alex MacGillivray, who will assume

the role of president and ceo. Miller, a founding member of EDI since its inception in

1996— the Equitable Life subsidiary which handles third-party mutual fund and variable

annuity distribution— had been in the position of ceo for 15 months after having been

promoted from the position of president of the wirehouse channel in April of last year. At

(continued on page 11)

NUVEEN CUSTOMIZES WEB SITES

FOR INTERNAL, EXTERNAL MARKETERS

Nuveen Investments has launched a new e-business initiative providing internal and

external marketers with personalized Web sites that serve as a portal for communicating

with financial professionals and delivering marketing materials previously stored in

wholesalers’ brief cases. Approximately 14 such sites have been created for Nuveen’s e-

Advisor Partners, a nascent group of marketers who guide intermediaries through virtual

sales and marketing resources and only spend about 30% of their time on the road in face-

(continued on page 11)

COPYRIGHT NOTICE: No part of this publication may

be copied, photocopied or duplicated in any form or by

any means without Institutional Investor’s prior written

consent. Copying of this publication is in violation of the

Federal Copyright Law (17 USC 101 et seq.). Violators

may be subject to criminal penalties as well as liability

for substantial monetary damages, including statutory

damages up to $100,000 per infringement, costs and

attorney’s fees. Copyright 2001 Institutional Investor,

Inc. All rights reserved.

For information regarding group subscription rates

and electronic licenses, please contact Dan Lalor at

(212) 224-3045.

Check www.fundmarketing.com during the week for breaking news and updates.

RAISING THE BAR: GOOD FAITH AIN’T WHAT IT USED TO BEBe careful what you wish for. That’s what some in the industry are thinking now

that the Securities and Exchange Commission has defined in greater detail what

constitutes “good faith” when directors oversee fair valuation procedures. After

clamoring for more information on what exactly the standard means, some industry

insiders don’t like what they hear. The April valuation letter penned by Douglas Scheidt, chief counsel of the

Division of Investment Management, states boards must discharge their duties(continued on page 8)

BOARDS SHOULD APPLY COST-BENEFITANALYSIS TO VALUATION CONTROLS

There’s a tendency to think more is always better, but this is clearly not the case

when it comes to valuation procedures. Having elaborate internal controls could

result in huge costs to funds, and hence, shareholders, noted Gene Gohlke,

associate director of the Office of Compliance Inspections and Examinations at the

Securities and Exchange Commission. Boards must apply a cost-benefit analysis

before signing off on the policies and procedures for fair-valuing securities, he

underscored.

(continued on page 7)

VOL. 10, NO. 7

JULY 2001

COPYRIGHT NOTICE: No part of this publication may be copied, photocopied or duplicated in any form or by any means without Institutional Investor’s prior written consent. Copying of this publication is in vio-

lation of the Federal Copyright Law (17 USC 101 et seq.). Violators may be subject to criminal penalties as well as liability for substantial monetary damages, including statutory damages up to $100,000 per

infringement, costs and attorney’s fees. Copyright 2001 Institutional Investor, Inc. All rights reserved.

For information regarding group subscription rates and electronic licenses, please contact Dan Lalor at (212) 224-3045.

Check www.funddirections.com during the week for breaking news and updates.

BOARDS SETCOMMITTEES Increasing stock market volatility.Rising foreign securities investments.Globalization of mutual funds. Theseare some of the reasons many boardshave stand-alone valuation committeesin place to monitor complicated pricingprocedures. While having a committeeisn’t required, most fund counsels andregulators agree it’s a good way toensure more accurate and consistentpricing of hard-to-value securities aswell as shield boards from potentialliability on pricing errors.More and more fund groups have

valuation committees because theyincreasingly invest in emerging markets,small-cap stocks, foreign securities andmunicipal bonds, explained PamelaWilson, a partner with Hale & Dorr.The Securities and ExchangeCommission doesn’t require funds to

have valuation committees because not allgroups need them. “If you’re a fund thatonly trades in large-cap, NYSE-listedU.S. stocks, you don’t really need apricing committee unless there’s anemergency,” Wilson pointed out.However, the trend seems to be that

IN THIS ISSUE

2 Morningstar’s Phillipsblasts fund managers, ICI

3 Industry mulls how boardsshould measure bestexecution for trades

4 ICI assembles task force onvaluation4 SEC official says funddirectors are getting tough

4 Industry news roundup

Fair-Value Triggers Concern Fund Counsels: see story, page 3

HOW BOARDS WORK

(continued on page 5)

Special Report: A Look At Valuation

Hong Kong Beckons Hedge FundsHedge funds are set to open for public

consumption in Hong Kong.See story, page 2

Brazilian Fund Marts Clip WingsBrazilian online brokers are shelving

expansion plans for their fund marts.See story, page 3In The NewsUBS Talks JV In China

2

New ProductsMerrill Moves Into Greece/Italy3

Marketing & DistributionMedusa Charms Canadians

4

Fidelity Rides With Toyota4

RegulationSaudi Arabia Creates Code7

Special Report: GermanyManagers Ready Pension Products 9

Wrap Accounts Take Off10

DepartmentsWeb Sightings

6

Regulatory Alert

7

Distributor Profile: Allianz Verm̈ogens-Bank AG 11

Search Directory

13

Distribution Directory

13

GERMAN BANKS ENTER THIRD-PARTY VENDING

Commercial banks and state-owned saving banks in Germany are rapidly opening up to

third-party distribution. Commerzbank and Hypovereinsbank have started, while

Dresdner Bank and Deutsche Bank are beginning to talk deals with providers. Even

the ultra conservative savings bank group, Deutsche Giro Zentrale (DGZ), is expected

soon to open doors to external fund managers following pressure from private investors,

who expect their banks to have the full range of products and competitors, said Eckard(continued on page 8)

JULY 23, 2001VOL. V, NO. 15

Distributors DivulgeHONG KONG VENDORS VOTE FIDELITY FUND

QUEENDistributors in Hong Kong place Fidelity Investments at the top of the heap when it

comes to brand name, access to fund managers, overall service, training and performance,

according to a survey by Expand Asia, a Hong Kong-based consulting group. INVESCO

Asset Management Asia was voted as having the best range of funds, while also tying

with Fidelity for giving its vendors the best access to fund managers. “Our strategy has(continued on page 16)

JP MORGAN REVAMPS MANAGEMENT

JP Morgan Fleming Asset Management has knocked the middle management layer,

regional heads, out of its Continental European structure and is considering a new

position for its head of European sales overseeing northern Europe, Martin Theisinger.

After JP Morgan Investment and Chase Fleming Asset Management merged, the firm

had decided to divide Europe into southern and northern regions, headed up by(continued on page 15)

Discrimination DecriedFEFSI FIGHTS FOR TAX HARMONISATION

ACROSS EUThe Fédération Européenne des Fonds et Sociétés d’investissement (FEFSI), the

European federation of fund managers, is lobbying the European Commission (EC)

and European Union member governments to rectify inequalities in taxation between

domestic and foreign funds. Discrimination against foreign funds in most European

Union countries is preventing the development of a real single market [for funds], said(continued on page 15)

COPYRIGHT NOTICE: No part of this publication may

be copied, photocopied or duplicated in any form or by

any means without Institutional Investor’s prior written

consent. Copying of this publication is in violation of the

Federal Copyright Law (17 USC 101 et seq.). Violators

may be subject to criminal penalties as well as liability

for substantial monetary damages, including statutory

damages up to $100,000 per infringement, costs and

attorney’s fees. Copyright 2001 Institutional Investor,

Inc. All rights reserved. For information regarding group subscription rates,

and electronic licenses, please contact Dan Lalor at

(212) 224-3045.

Check out www.globalfundnews.com for breaking news and updates—free to subscribers.

S P E C I A L R E P O R T : G E R M A N Y

www.globalfundnews.com

Mergers & Acquisitions • Technology •

New Markets/Products • Regulatory News

Technology News • Searches • Distribution

Directories • FundWorld • Personnel Moves

Plan Sponsor Profiles • Vendor Forums •

Washington • Special Reports • Surveys

FUND ACTION: www.fundaction.com• Covers important news and trends in the U.S. mutual fund industry and is regarded as

the "must-read" guide by all industry insiders.

FUND MARKETING ALERT: www.fundmarketing.com• Deals exclusively with mutual fund marketing, sales and distribution strategies. Covers the various

channels that fund companies use to sell their products.

FUND DIRECTIONS: www.funddirections.com• The only independent publication covering issues of concern to mutual fund boards. Analyzes the key

issues in mutual fund governance from an independent trustee's perspective.

GLOBAL FUND NEWS: www.globalfundnews.com• This newsletter delivers critical market intelligence on the international mutual fund industry.

DEFINED CONTRIBUTION NEWS: www.dcnews.com• Delivers exclusive intelligence on the burgeoning 401(k), 401(a), 457 and 403(b) plan markets.

❑YES! Send me my risk-free, no obligation 3 FREE trial issues (you may select up to two newsletters):

❑ Fund Action ❑ Fund Marketing Alert ❑ Global Fund News ❑ Defined Contribution News

For a trial to Fund Directions call Joe Mattiello at 1-212-224-3457

NAME TITLE FIRM

ADDRESS CITY/STATE POSTAL CODE/ZIP COUNTRY

TEL FAX E-MAIL TO2682

FAX: 1-212-224-3491 or CALL: 1-212-224-3457

5 NL promo ad 2/19/03 12:57 PM Page 1

August 18, 2003 www.derivativesweek.com Derivatives Week

Copying prohibited without the permission of the publisher. 11

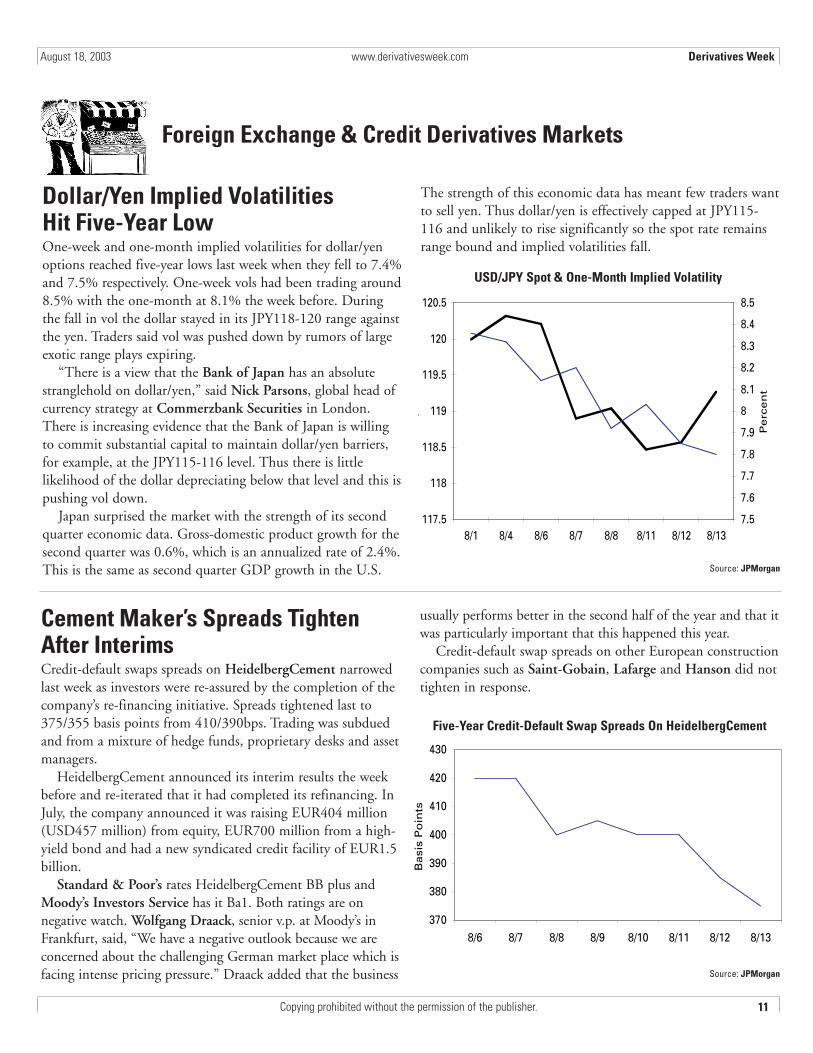

Dollar/Yen Implied Volatilities Hit Five-Year LowOne-week and one-month implied volatilities for dollar/yenoptions reached five-year lows last week when they fell to 7.4%and 7.5% respectively. One-week vols had been trading around8.5% with the one-month at 8.1% the week before. Duringthe fall in vol the dollar stayed in its JPY118-120 range againstthe yen. Traders said vol was pushed down by rumors of largeexotic range plays expiring.

“There is a view that the Bank of Japan has an absolutestranglehold on dollar/yen,” said Nick Parsons, global head ofcurrency strategy at Commerzbank Securities in London.There is increasing evidence that the Bank of Japan is willingto commit substantial capital to maintain dollar/yen barriers,for example, at the JPY115-116 level. Thus there is littlelikelihood of the dollar depreciating below that level and this ispushing vol down.

Japan surprised the market with the strength of its secondquarter economic data. Gross-domestic product growth for thesecond quarter was 0.6%, which is an annualized rate of 2.4%.This is the same as second quarter GDP growth in the U.S.

The strength of this economic data has meant few traders wantto sell yen. Thus dollar/yen is effectively capped at JPY115-116 and unlikely to rise significantly so the spot rate remainsrange bound and implied volatilities fall.

117.5

118

118.5

119

119.5

120

120.5

8/1 8/4 8/6 8/7 8/8 8/11 8/12 8/13

p

7.5

7.6

7.7

7.8

7.9

8

8.1

8.2

8.3

8.4

8.5

Pe

rce

nt

Source: JPMorgan

Foreign Exchange & Credit Derivatives Markets

Cement Maker’s Spreads TightenAfter InterimsCredit-default swaps spreads on HeidelbergCement narrowedlast week as investors were re-assured by the completion of thecompany’s re-financing initiative. Spreads tightened last to375/355 basis points from 410/390bps. Trading was subduedand from a mixture of hedge funds, proprietary desks and assetmanagers.

HeidelbergCement announced its interim results the weekbefore and re-iterated that it had completed its refinancing. InJuly, the company announced it was raising EUR404 million(USD457 million) from equity, EUR700 million from a high-yield bond and had a new syndicated credit facility of EUR1.5billion.

Standard & Poor’s rates HeidelbergCement BB plus andMoody’s Investors Service has it Ba1. Both ratings are onnegative watch. Wolfgang Draack, senior v.p. at Moody’s inFrankfurt, said, “We have a negative outlook because we areconcerned about the challenging German market place which isfacing intense pricing pressure.” Draack added that the business

usually performs better in the second half of the year and that itwas particularly important that this happened this year.

Credit-default swap spreads on other European constructioncompanies such as Saint-Gobain, Lafarge and Hanson did nottighten in response.

Source: JPMorgan

370

380

390

400

410

420

430

8/6 8/7 8/8 8/9 8/10 8/11 8/12 8/13

Basi

s P

oin

ts

Five-Year Credit-Default Swap Spreads On HeidelbergCement

USD/JPY Spot & One-Month Implied Volatility

dw.08.18.03 8/16/03 4:08 PM Page 11

Calendar• Information Management Network is running a Germanand Northern Europe securitization conference in Munich onSept. 15-16. To register, call (1 212) 768 2800.

• Derivatives Week is organizing a European derivativesaccounting summit about IAS32, 30 and SIC 12 in Londonon Nov. 20. To register, call 44 (0) 7779 8437.

Quote Of The Week“It’s an idea I have.”—Hee Dong Kim, head of the financialengineering department at Korea Exchange Bank in Seoul, talkingabout his plans for investing in synthetic collateralized debt obligations(see story, page 1).

One Year Ago In Derivatives WeekSynthetic collateralized debt obligations structurers were turningto novel innovations, including kickers to mezzanine tranches, asmeans of enticing increasingly reluctant buyers to participate inthe deals. [Enhancements, including reinvesting equity returnsinto securitized structures, are increasing popular and continueto feature in deals (see story, page 1).]

Derivatives Week www.derivativesweek.com August 18, 2003

Copying prohibited without the permission of the publisher.12

with the unique aspects of the Mexican market, such as its 28day interest rate cycle. “We have great expectations for Mexico,”said Hong, noting that the firm has a dedicated trader andmarketer for the effort, based in Stamford, Conn.

The bank established a specialized emerging markets grouplast year, spearheaded by Hong, who moved from the HongKong office (DW 2/3/02). UBS has already expanded intoEastern Europe, including Czech Republic, Hungary andPoland, and Hong says he plans further expansion, but declinedto be specific. —M.T

UBS READIES(continued from page 1)

at structural innovations and new asset pools to jack up yield. One of the deals in development is comprised of a synthetic

collateralized debt obligation that will reference a pool of credit-default swaps as well as options on default swaps, said Hatstadt.Merrill expects the extra leverage offered by the options will giveit a return of at least 110 basis points on the assets, which isaround 30bps higher than a plain-vanilla CDO—a level thecredit markets have not seen for six months. These exact returnswill depend on the volatility of asset spreads as well as whetherthe firm uses American or European-style options, he noted.

Spreads have tightened enormously over the last year andsome investors are looking at buying credit protection to prop uptheir CDO portfolios or profit from any future widening,according to buy and sell-side credit professionals. Merrill isresecuritizing a CDO of CDOs to allow structured creditinvestors to short credit risk. In the deal, Merrill structures asynthetic CDO of CDOs, referenced to 10-20 unfunded

mezzanine tranches, and then issues equity and mezzanine notescollateralized by the portfolio.

In addition, Merrill is planning to build on a series ofsynthetic CDOs it issued last year, dubbed MINT. The new dealswill reference static pools as an alternative to the managed poolsalready available. As with the previous issues, the new structureswill include features that reinvest a substantial part of the equityreturns into the structure, which allows mezzanine investorsgreater participation. —Karen Brettell

MERRILL DRAWS(continued from page 1)

improvements in liquidity and stability. These instruments wouldallow the bank to pick up additional yield over traditional bonds.Kim said it is too early to comment on the potential size ofinvestments.

“Asset-wise, they’re a big player,” said a credit marketer atJPMorgan, noting that he plans to speak with the bank.

In addition to an increasing number of domestic banks andinsurers including LG Insurance (DW, 7/6) eyeing CDOs,local securities houses are also looking to step into the marketlater this year, pending regulatory approval (DW, 7/27).

—Matt Tremblay

KOREAN BANKING(continued from page 1)

a single-tranche product the structurer sells one piece of the dealand then hedges the rest of the capital structure. This is onlypossible if there is a liquid underlying market or the firm candistribute highly correlated risk from other parts of the capitalstructure.

Investors have been turning their attention to CDOsreferenced to ABS in recent months because of their increasedstability in ratings and spreads compared to corporate deals.One European head of structured credit at a ratings agencyestimated that half of the CDOs in the pipeline are referencedto asset-backeds. A Deutsche Bank official said it is thisincreased deal volume that has triggered the interest from thesell-side in single-tranche deals. —Jeremy Carter

CDO STRUCTURERS(continued from page 1)

dw.08.18.03 8/16/03 4:08 PM Page 12