Embed Size (px)

Citation preview

Coca-Cola Hellenic (CCH) | Page 1

Coca-Cola Hellenic

(NYSE: CCH)

December 2012

Prepared by:

Broyhill Asset Management, LLC

800 Golfview Park

Lenoir, NC 28645

(828) 758 6100

www.broyhillasset.com

Subscribe At

Coca-Cola Hellenic (CCH) | Page 2

DISCLAIMER

The analyses and conclusions of Broyhill Asset Management (“Broyhill”) contained in this presentation are

based on publicly available information including SEC filings and numerous other public sources that we

believe to be reliable. We recognize that there may be confidential information in the possession of the

companies discussed in this presentation that could lead these companies to disagree with our conclusions. If

we have made any errors or if any readers have additional facts or corrections, we welcome hearing from you.

This presentation and the information contained herein is not a recommendation or solicitation to buy or sell

any securities.

This document contains general information that is not suitable for everyone. The information contained

herein should not be construed as personalized investment advice. The views expressed here are the current

opinions of the author and not necessarily those of Broyhill. The author’s opinions are subject to change

without notice. There is no guarantee that the views and opinions expressed in this document will come to

pass. Investing in the stock market involves gains and losses and may not be suitable for all investors.

Information presented herein is subject to change without notice and should not be considered as a

solicitation to buy or sell any security.

Our purpose is to disseminate publicly available information that we believe has not been made readily

available to the investing public but is critical to an evaluation of the company. The analyses provided may

include certain statements, estimates, and projections prepared with respect to the historical and anticipated

operating performance of the company. Such statements, estimates, and projections reflect various

assumptions by Broyhill concerning anticipated results that are inherently subject to significant economic,

competitive, and other uncertainties and contingencies and have been included solely for illustrative

purposes. No representations, expressed or implied, are made as to the accuracy or completeness of such

statements, estimates or projections, or with respect to any other materials herein.

Assets managed by Broyhill and its affiliates own shares of Coca-Cola Hellenic (“CCH”). Broyhill manages

accounts that are in the business of trading – buying and selling – securities and financial instruments. It is

possible that there will be developments in the future that cause Broyhill to change its position regarding

CCH. Broyhill may buy, sell, or otherwise change the form of its investment in CCH for any reason. Broyhill

hereby disclaims any duty to provide any updates or changes to the analyses contained here including, without

limitation, the manner or type of Broyhill investment.

Coca-Cola Hellenic (CCH) | Page 3

Executive Summary

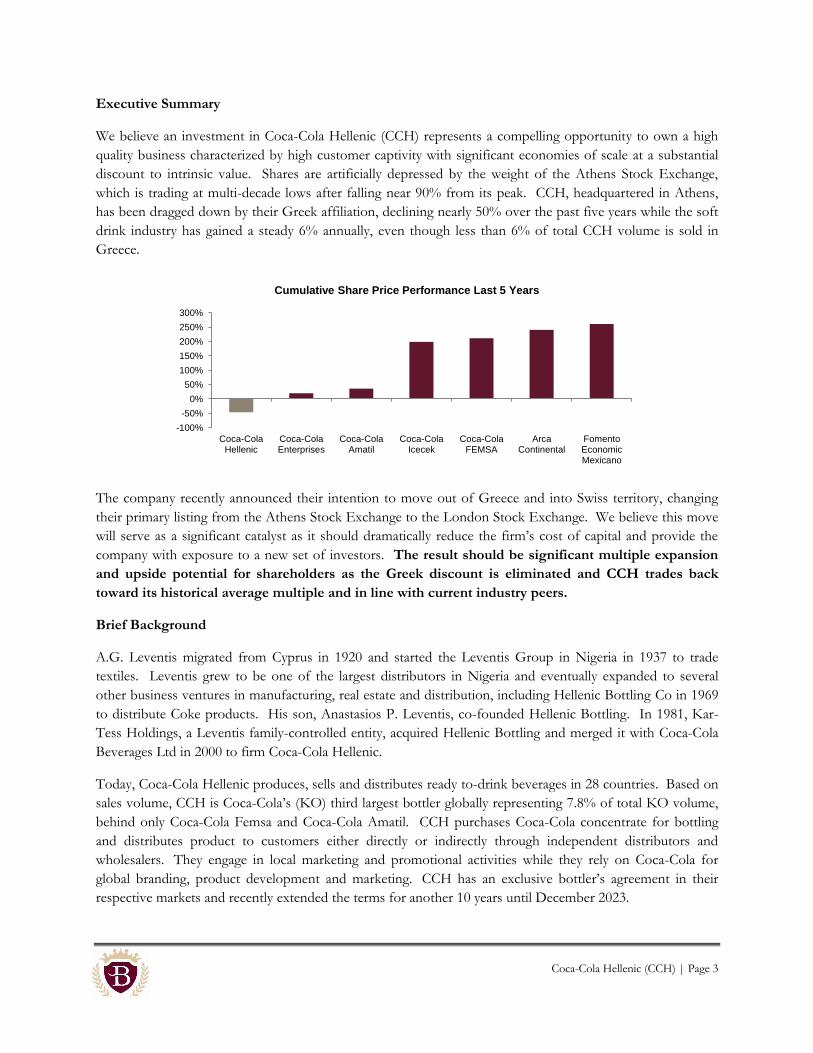

We believe an investment in Coca-Cola Hellenic (CCH) represents a compelling opportunity to own a high

quality business characterized by high customer captivity with significant economies of scale at a substantial

discount to intrinsic value. Shares are artificially depressed by the weight of the Athens Stock Exchange,

which is trading at multi-decade lows after falling near 90% from its peak. CCH, headquartered in Athens,

has been dragged down by their Greek affiliation, declining nearly 50% over the past five years while the soft

drink industry has gained a steady 6% annually, even though less than 6% of total CCH volume is sold in

Greece.

The company recently announced their intention to move out of Greece and into Swiss territory, changing

their primary listing from the Athens Stock Exchange to the London Stock Exchange. We believe this move

will serve as a significant catalyst as it should dramatically reduce the firm’s cost of capital and provide the

company with exposure to a new set of investors. The result should be significant multiple expansion

and upside potential for shareholders as the Greek discount is eliminated and CCH trades back

toward its historical average multiple and in line with current industry peers.

Brief Background

A.G. Leventis migrated from Cyprus in 1920 and started the Leventis Group in Nigeria in 1937 to trade

textiles. Leventis grew to be one of the largest distributors in Nigeria and eventually expanded to several

other business ventures in manufacturing, real estate and distribution, including Hellenic Bottling Co in 1969

to distribute Coke products. His son, Anastasios P. Leventis, co-founded Hellenic Bottling. In 1981, Kar-

Tess Holdings, a Leventis family-controlled entity, acquired Hellenic Bottling and merged it with Coca-Cola

Beverages Ltd in 2000 to firm Coca-Cola Hellenic.

Today, Coca-Cola Hellenic produces, sells and distributes ready to-drink beverages in 28 countries. Based on

sales volume, CCH is Coca-Cola’s (KO) third largest bottler globally representing 7.8% of total KO volume,

behind only Coca-Cola Femsa and Coca-Cola Amatil. CCH purchases Coca-Cola concentrate for bottling

and distributes product to customers either directly or indirectly through independent distributors and

wholesalers. They engage in local marketing and promotional activities while they rely on Coca-Cola for

global branding, product development and marketing. CCH has an exclusive bottler’s agreement in their

respective markets and recently extended the terms for another 10 years until December 2023.

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

Coca-ColaHellenic

Coca-ColaEnterprises

Coca-ColaAmatil

Coca-ColaIcecek

Coca-ColaFEMSA

ArcaContinental

FomentoEconomicMexicano

Cumulative Share Price Performance Last 5 Years

Coca-Cola Hellenic (CCH) | Page 4

George A. David, nephew of A.G. Leventis, serves as Chairman of the Board for CCH today. Anastassis G.

David serves as a non-executive director of the board. A.P. Leventis continues to serve on the board of

directors as Vice Chairman. Haralambos Leventis serves as non-executive director of the board. All four of

the above mentioned family members were nominated by Kar-Tess Holdings as part of the shareholder

agreement between Kar-Tess and The Coca-Cola Company. Of the five independent directors, KO has

appointed two board members. It is our understanding that the new board and the revised shareholder

agreement between Kar-Tess and KO will look similar to the existing structure once the move to a London

listing is complete.

Kar-Tess Holdings and Coca-Cola each own 23% of the company’s outstanding shares, with the remaining

54% floated in public markets. For this reason, the stock is pretty illiquid with average daily volume for the

ADR at 28,600 and roughly 7.2% of current outstanding shares floated in the US. But, as we discuss below,

that is set to change.

Industry & Competitive Dynamics

Bruce Greenwald and Judd Kahn offered up an excellent overview of the competitive dynamics governing

the soft drink industry in their 2005 book, Competition Demystified. This industry analysis remains as relevant

for the decade ahead as it did for the one just passed. The bottling industry is a rather boring business. It

demands high capital investment and generates limited returns on that capital, but what it offers in exchange

is a rather predictable and growing stream of cash flow. As discussed by Greenwald and Kahn:

The bottlers and distributors are joined to the soda companies at the hip. Many of them have been owned by the

companies at various times, others are franchises. The soda companies charge them for concentrate and syrup and have

raised prices at times on the promise of providing additional advertising and promotional support. Advertising has

generally been split between soda companies and bottlers, whereas promotional costs are borne by bottlers. Whatever the

divisions, these are allied campaigns. The soda companies cannot operate successfully unless their bottlers are distributors

are profitable and content. The bottlers are an integral part of the soft drink industry.

The bottling function is the part of the industry that demands the most capital investment. The high speed lines are

expensive and highly specialized. Cans don't work on lines designed for bottles, nor will twelve-ounce bottle move down

a line intended for quart containers. The demand for capital has been one of the reasons why the concentrate companies

have moved in and out of the bottler segment at various times, adding funds when necessary, then selling shares to the

public when possible.

Coca-Cola Hellenic (CCH) | Page 5

Both key indicators of the presence of barriers to entry and competitive advantage – stable market share and a high

return on capital – are present here. The existence of barriers to entry indicates that the incumbents enjoy competitive

advantages that potential entrants cannot match. In the soft drink world, the sources of these advantages are easy to

identify. First, on the demand side, there is the kind of customer loyalty that businesses dream about. People who drink

sodas drink them frequently, and they relish a consistency of experience that keeps them ordering the same brand, no

matter the circumstances. Second, there are large economies of scale in the soda business, both at the concentrate market

and bottler levels. The distribution of soda to the consumer benefits from regional scale economies. Concentrate supplied

by the soda company is sent to bottlers, who add water, bubbles and sweetener, close the containers, and send the drink

on to a variety of retail outlets. The water is heavy and thus expensive to haul over long distances. The more customers

in a region, the more economical the distribution.

The combination of captive customers and economies of scale creates a dominant competitive

advantage for Coca-Cola Hellenic. The company has 250 distribution centers and 86 warehouses, as well

as 295 filling lines within 76 plants for production. Further, these assets are guarded by significant barriers to

entry in the form of exclusive rights to produce and distribute the products of The Coca-Cola Company in

each of their territories.

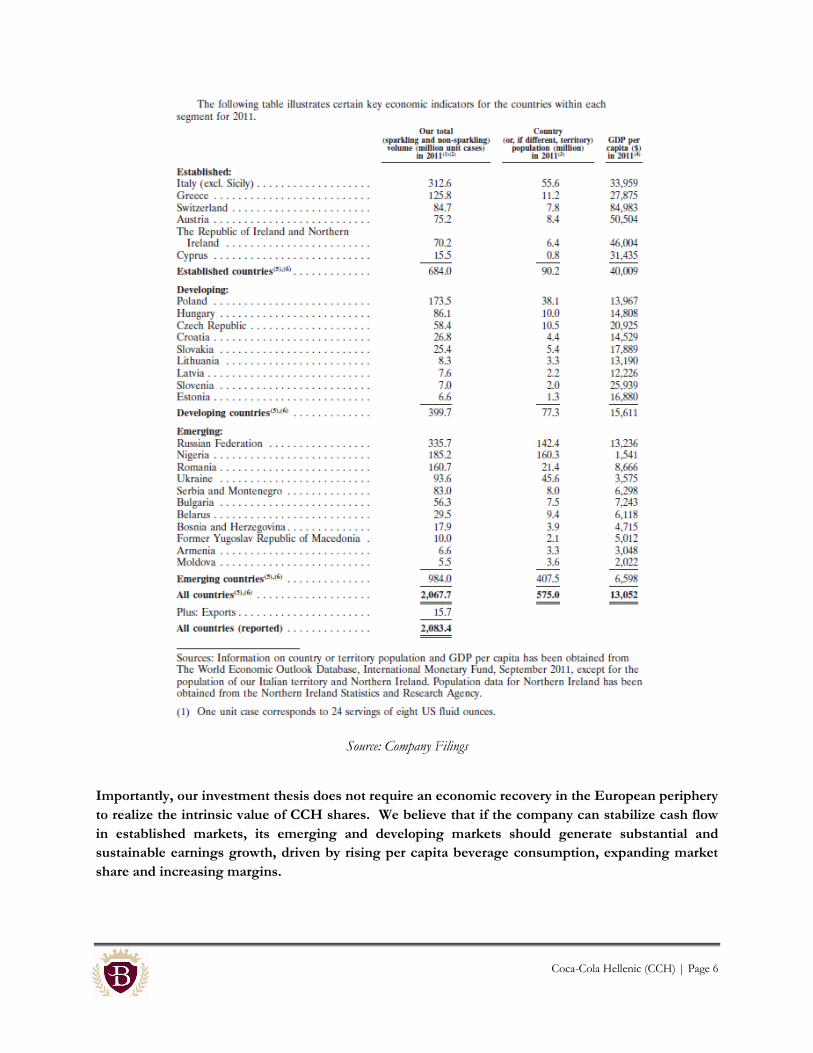

Regional Scale & Growth Potential

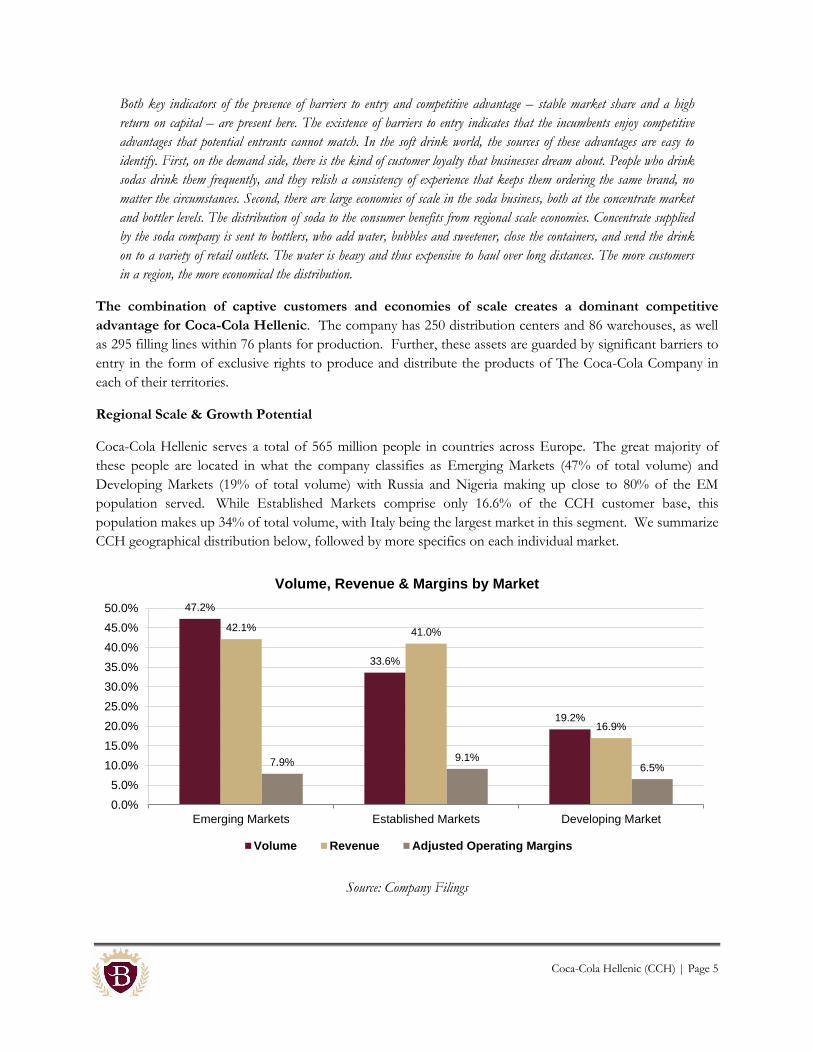

Coca-Cola Hellenic serves a total of 565 million people in countries across Europe. The great majority of

these people are located in what the company classifies as Emerging Markets (47% of total volume) and

Developing Markets (19% of total volume) with Russia and Nigeria making up close to 80% of the EM

population served. While Established Markets comprise only 16.6% of the CCH customer base, this

population makes up 34% of total volume, with Italy being the largest market in this segment. We summarize

CCH geographical distribution below, followed by more specifics on each individual market.

Source: Company Filings

47.2%

33.6%

19.2%

42.1% 41.0%

16.9%

7.9% 9.1% 6.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Emerging Markets Established Markets Developing Market

Volume, Revenue & Margins by Market

Volume Revenue Adjusted Operating Margins

Coca-Cola Hellenic (CCH) | Page 6

Source: Company Filings

Importantly, our investment thesis does not require an economic recovery in the European periphery

to realize the intrinsic value of CCH shares. We believe that if the company can stabilize cash flow

in established markets, its emerging and developing markets should generate substantial and

sustainable earnings growth, driven by rising per capita beverage consumption, expanding market

share and increasing margins.

Coca-Cola Hellenic (CCH) | Page 7

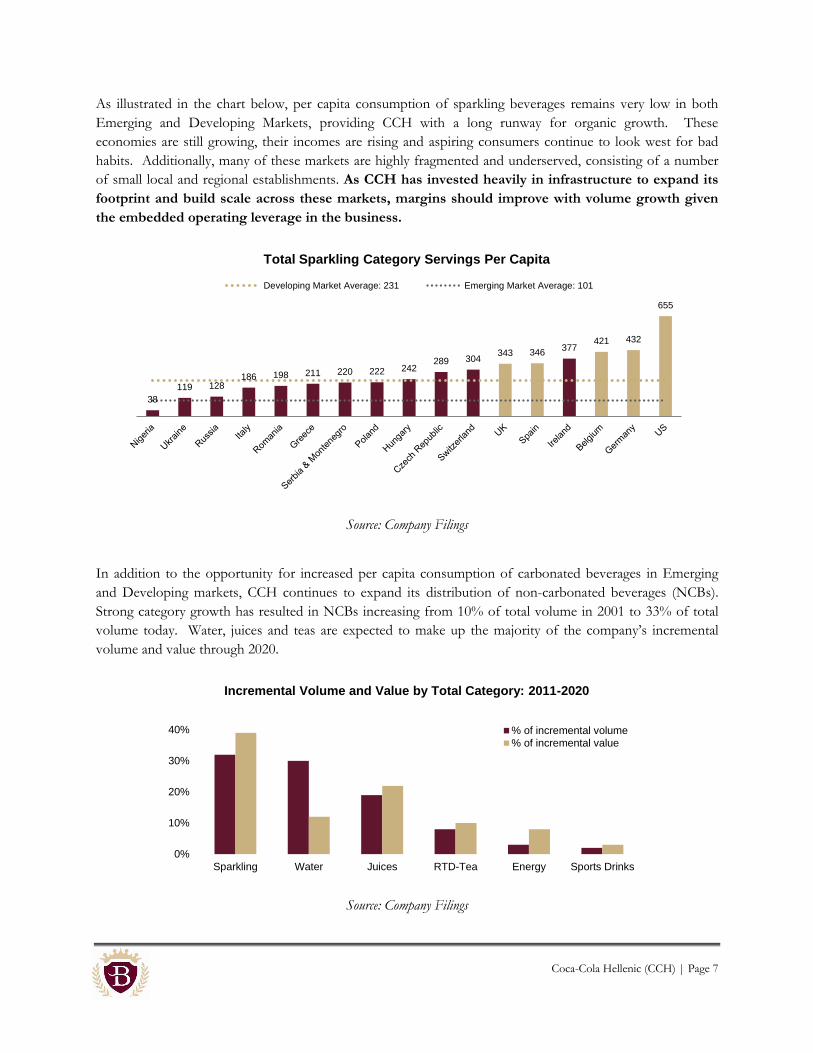

As illustrated in the chart below, per capita consumption of sparkling beverages remains very low in both

Emerging and Developing Markets, providing CCH with a long runway for organic growth. These

economies are still growing, their incomes are rising and aspiring consumers continue to look west for bad

habits. Additionally, many of these markets are highly fragmented and underserved, consisting of a number

of small local and regional establishments. As CCH has invested heavily in infrastructure to expand its

footprint and build scale across these markets, margins should improve with volume growth given

the embedded operating leverage in the business.

Source: Company Filings

In addition to the opportunity for increased per capita consumption of carbonated beverages in Emerging

and Developing markets, CCH continues to expand its distribution of non-carbonated beverages (NCBs).

Strong category growth has resulted in NCBs increasing from 10% of total volume in 2001 to 33% of total

volume today. Water, juices and teas are expected to make up the majority of the company’s incremental

volume and value through 2020.

Source: Company Filings

38

119 128 186 198 211 220 222 242

289 304 343 346

377 421 432

655

Total Sparkling Category Servings Per Capita

Developing Market Average: 231 Emerging Market Average: 101

0%

10%

20%

30%

40%

Sparkling Water Juices RTD-Tea Energy Sports Drinks

Incremental Volume and Value by Total Category: 2011-2020

% of incremental volume

% of incremental value

Coca-Cola Hellenic (CCH) | Page 8

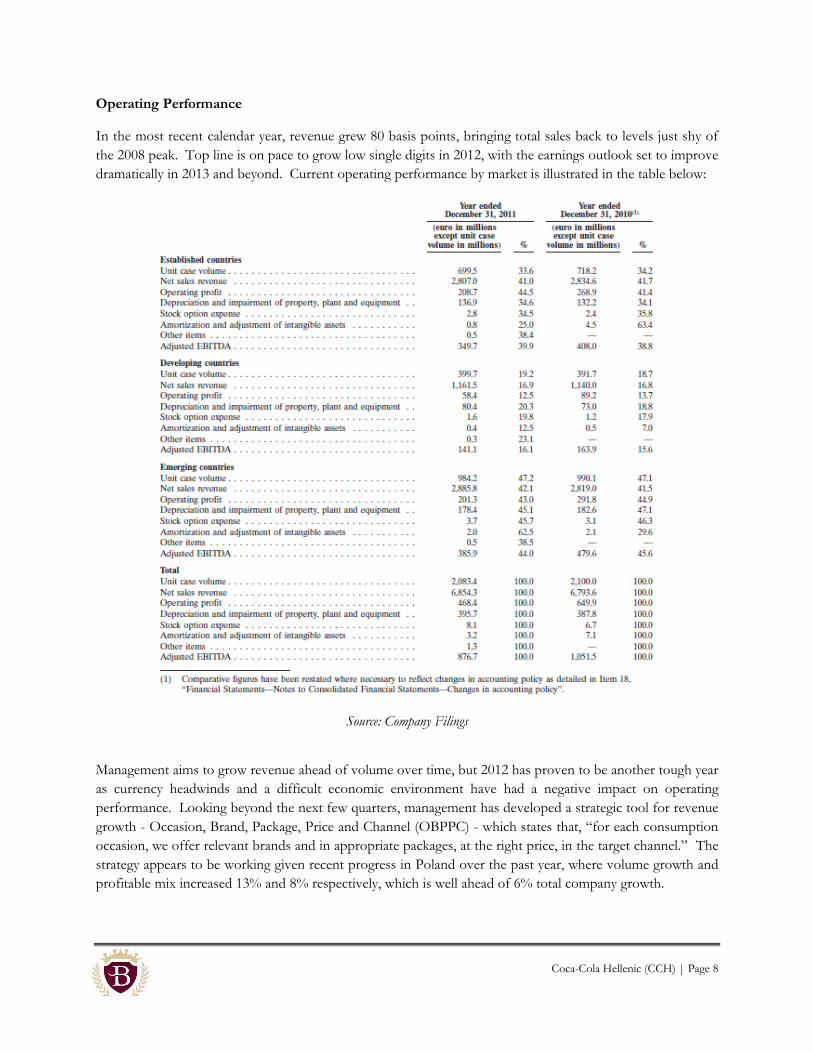

Operating Performance

In the most recent calendar year, revenue grew 80 basis points, bringing total sales back to levels just shy of

the 2008 peak. Top line is on pace to grow low single digits in 2012, with the earnings outlook set to improve

dramatically in 2013 and beyond. Current operating performance by market is illustrated in the table below:

Source: Company Filings

Management aims to grow revenue ahead of volume over time, but 2012 has proven to be another tough year

as currency headwinds and a difficult economic environment have had a negative impact on operating

performance. Looking beyond the next few quarters, management has developed a strategic tool for revenue

growth - Occasion, Brand, Package, Price and Channel (OBPPC) - which states that, “for each consumption

occasion, we offer relevant brands and in appropriate packages, at the right price, in the target channel.” The

strategy appears to be working given recent progress in Poland over the past year, where volume growth and

profitable mix increased 13% and 8% respectively, which is well ahead of 6% total company growth.

Coca-Cola Hellenic (CCH) | Page 9

In addition to the challenging demand outlook created by an ongoing European deleveraging process,

continued increases in the price of oil and corn have resulted in ongoing cost pressure in key inputs such as

artificial sweeteners, PET resin and fuel costs. While additional increases in the cost of commodities

represent a risk to the industry’s earnings potential, we believe this risk is sufficiently discounted in

CCH’s severely depressed valuation. Furthermore, any moderation in commodity cost pressure –

consistent with recent comments and guidance from major bottlers - would drive significant upside

in CCH given consensus expectations today.

CCH currently claims the absolute lowest margins among its peers in the industry. For perspective, consider

that EBITDA margins have averaged 15.4% over the past decade, more than 300 basis points higher than the

12.3% level reported today. Obviously there is substantial room for improvement relative to the company’s

own history as well as its peer group. Management has embarked on a plan to cut EUR 70 million of annual

costs out of the business by streamlining operations, consolidating and upgrading facilities, and implementing

shared services across the company’s operational footprint. The benefits of this strategy have already begun

to surprise on the upside. With most of the heavy lifting now complete, and the drag from input costs sets to

ease, we see no reason why margins shouldn’t mean revert over our forecast period.

Source: Bloomberg, Company Filings, Broyhill Asset Management Estimates

CCH is a consistent cash generator with an extremely high quality of earnings as free cash flow has

largely exceeded net income since 2002. Management is targeting zero working capital changes in 2015

and recently reiterated guidance of EUR 1.45 billion in free cash flow net of EUR 1.45 in cumulative capital

expenditures over the next two years. While guidance is skewed towards the back half of the period, it is

consistent with our outlook for improving revenue growth and normalizing margins.

As a result of this predictable cash flow, bottlers typically carry a significant amount of debt. CCH reports net

debt of EUR 1.6 billion, which equates to 1.9x EBITDA and an interest coverage ratio of 4.7x. Given the

new listing, we think the company has the capacity to further leverage the balance sheet, rewarding both

shareholders and family members with significant cash return. For example, CCE management targets 2.5x –

3.0x Net Debt to EBITDA. Assuming similar leverage ratios at CCH would imply that the company

could return an additional 8.8% to 16.0% of its current market capitalization to shareholders.

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM

EBITDA Margins

Coca Cola Hellenic Current Peer Group Average

Coca-Cola Hellenic (CCH) | Page 10

Valuation

Yogi Berra is credited a variety of luminous observations. One of my personal favorites is that, "In theory,

there is no difference between theory and practice. But in practice, there is." As a Yankee fan since childhood,

it is difficult for me to admit that this baseball hall of famer may have missed his calling. Yogi would have

made an excellent economist.

In theory, CCH should be “efficiently priced” by the market as a large liquid company with excellent

governance, operating in a global industry with numerous peers for comparative proposes. However, in

practice, CCH is trading at a substantial discount to the global bottling industry. This is likely attributable to a

single word - “Hellenic” – in the firm’s corporate title. Put simply, the potential investor base has been

drastically reduced by the Greek domicile.

While we think that “Emerging Market Coca Cola” or “Coca Cola Social Media Bottler” may resonate better

with more trendy investors while tacking on a few multiple turns, the company has opted for a less dramatic,

but still, highly effective change. In October, management announced a voluntary offer to acquire existing

Athens-listed shares and exchange them for new shares, listed on the London Stock Exchange. We believe

this shift has the potential to mark an important inflection point in the stock. Moving the

headquarters to Switzerland and listing the shares in the UK should translate into a much broader

investor base with significantly greater liquidity. The company’s current market cap would rank

CCH towards the middle of the FTSE 100 pack, with potential inclusion of new shares in the index

driving technical demand from index investors. Further, we would expect the new structure to have a

positive impact on the company’s credit, reducing CCH’s cost of capital and ultimately resulting in a

valuation more in line with global peers.

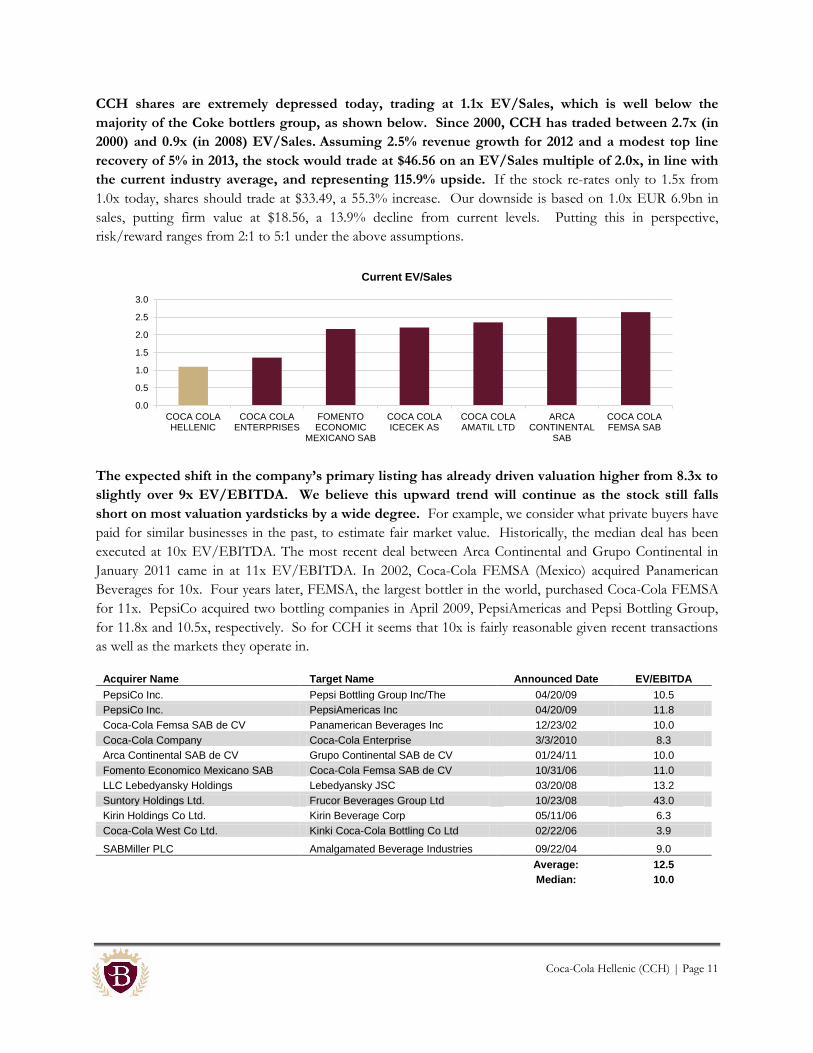

This valuation gap can best be seen in examining EV/Sales ratios across the bottling industry. Generally

speaking, companies that have historically generated attractive margins but currently trade at low EV/Sales

ratios may be discounted by the market because other investors assume the decline in profitability is

permanent. In this case, we believe EV/Sales to be a better tool than other valuation metrics. As a result, if

CCH can return to its former level of profitability, than the stock is quite cheap.

Coca-Cola Hellenic (CCH) | Page 11

CCH shares are extremely depressed today, trading at 1.1x EV/Sales, which is well below the

majority of the Coke bottlers group, as shown below. Since 2000, CCH has traded between 2.7x (in

2000) and 0.9x (in 2008) EV/Sales. Assuming 2.5% revenue growth for 2012 and a modest top line

recovery of 5% in 2013, the stock would trade at $46.56 on an EV/Sales multiple of 2.0x, in line with

the current industry average, and representing 115.9% upside. If the stock re-rates only to 1.5x from

1.0x today, shares should trade at $33.49, a 55.3% increase. Our downside is based on 1.0x EUR 6.9bn in

sales, putting firm value at $18.56, a 13.9% decline from current levels. Putting this in perspective,

risk/reward ranges from 2:1 to 5:1 under the above assumptions.

The expected shift in the company’s primary listing has already driven valuation higher from 8.3x to

slightly over 9x EV/EBITDA. We believe this upward trend will continue as the stock still falls

short on most valuation yardsticks by a wide degree. For example, we consider what private buyers have

paid for similar businesses in the past, to estimate fair market value. Historically, the median deal has been

executed at 10x EV/EBITDA. The most recent deal between Arca Continental and Grupo Continental in

January 2011 came in at 11x EV/EBITDA. In 2002, Coca-Cola FEMSA (Mexico) acquired Panamerican

Beverages for 10x. Four years later, FEMSA, the largest bottler in the world, purchased Coca-Cola FEMSA

for 11x. PepsiCo acquired two bottling companies in April 2009, PepsiAmericas and Pepsi Bottling Group,

for 11.8x and 10.5x, respectively. So for CCH it seems that 10x is fairly reasonable given recent transactions

as well as the markets they operate in.

Acquirer Name Target Name Announced Date EV/EBITDA

PepsiCo Inc. Pepsi Bottling Group Inc/The 04/20/09 10.5

PepsiCo Inc. PepsiAmericas Inc 04/20/09 11.8

Coca-Cola Femsa SAB de CV Panamerican Beverages Inc 12/23/02 10.0

Coca-Cola Company Coca-Cola Enterprise 3/3/2010 8.3

Arca Continental SAB de CV Grupo Continental SAB de CV 01/24/11 10.0

Fomento Economico Mexicano SAB Coca-Cola Femsa SAB de CV 10/31/06 11.0

LLC Lebedyansky Holdings Lebedyansky JSC 03/20/08 13.2

Suntory Holdings Ltd. Frucor Beverages Group Ltd 10/23/08 43.0

Kirin Holdings Co Ltd. Kirin Beverage Corp 05/11/06 6.3

Coca-Cola West Co Ltd. Kinki Coca-Cola Bottling Co Ltd 02/22/06 3.9

SABMiller PLC Amalgamated Beverage Industries 09/22/04 9.0

Average: 12.5

Median: 10.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

COCA COLAHELLENIC

COCA COLAENTERPRISES

FOMENTOECONOMIC

MEXICANO SAB

COCA COLAICECEK AS

COCA COLAAMATIL LTD

ARCACONTINENTAL

SAB

COCA COLAFEMSA SAB

Current EV/Sales

Coca-Cola Hellenic (CCH) | Page 12

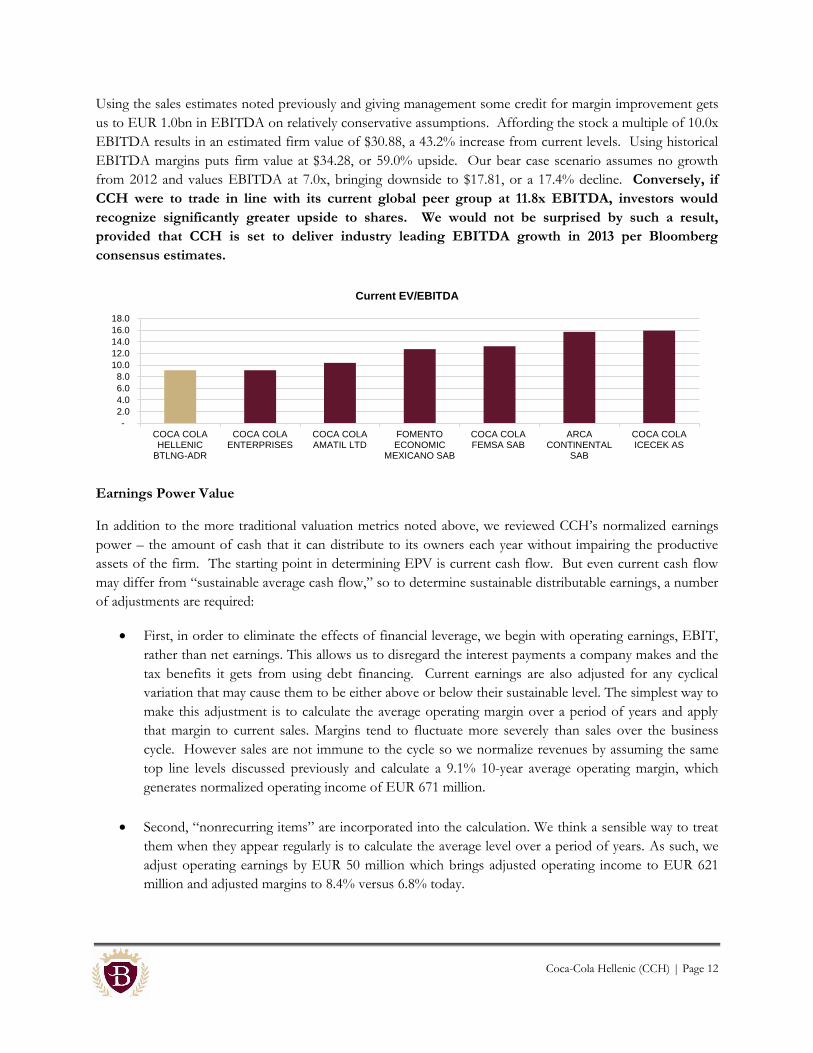

Using the sales estimates noted previously and giving management some credit for margin improvement gets

us to EUR 1.0bn in EBITDA on relatively conservative assumptions. Affording the stock a multiple of 10.0x

EBITDA results in an estimated firm value of $30.88, a 43.2% increase from current levels. Using historical

EBITDA margins puts firm value at $34.28, or 59.0% upside. Our bear case scenario assumes no growth

from 2012 and values EBITDA at 7.0x, bringing downside to $17.81, or a 17.4% decline. Conversely, if

CCH were to trade in line with its current global peer group at 11.8x EBITDA, investors would

recognize significantly greater upside to shares. We would not be surprised by such a result,

provided that CCH is set to deliver industry leading EBITDA growth in 2013 per Bloomberg

consensus estimates.

Earnings Power Value

In addition to the more traditional valuation metrics noted above, we reviewed CCH’s normalized earnings

power – the amount of cash that it can distribute to its owners each year without impairing the productive

assets of the firm. The starting point in determining EPV is current cash flow. But even current cash flow

may differ from “sustainable average cash flow,” so to determine sustainable distributable earnings, a number

of adjustments are required:

First, in order to eliminate the effects of financial leverage, we begin with operating earnings, EBIT,

rather than net earnings. This allows us to disregard the interest payments a company makes and the

tax benefits it gets from using debt financing. Current earnings are also adjusted for any cyclical

variation that may cause them to be either above or below their sustainable level. The simplest way to

make this adjustment is to calculate the average operating margin over a period of years and apply

that margin to current sales. Margins tend to fluctuate more severely than sales over the business

cycle. However sales are not immune to the cycle so we normalize revenues by assuming the same

top line levels discussed previously and calculate a 9.1% 10-year average operating margin, which

generates normalized operating income of EUR 671 million.

Second, “nonrecurring items” are incorporated into the calculation. We think a sensible way to treat

them when they appear regularly is to calculate the average level over a period of years. As such, we

adjust operating earnings by EUR 50 million which brings adjusted operating income to EUR 621

million and adjusted margins to 8.4% versus 6.8% today.

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

COCA COLAHELLENIC

BTLNG-ADR

COCA COLAENTERPRISES

COCA COLAAMATIL LTD

FOMENTOECONOMIC

MEXICANO SAB

COCA COLAFEMSA SAB

ARCACONTINENTAL

SAB

COCA COLAICECEK AS

Current EV/EBITDA

Coca-Cola Hellenic (CCH) | Page 13

Third, we note that accounting depreciation, as calculated for financial statements, may diverge

widely from true economic depreciation, which is best estimated by maintenance capital expense, and

omits capital expenditures for growth. Our discussions with management indicated that growth cap

ex is in line with peers – two-thirds growth and one-third maintenance. As such, we add back 75%

of growth capital expenditures.

Finally, taxes charged for accounting purposes may vary widely from year to year. Pretax operating

earnings should be converted to after-tax earnings using an average sustainable tax rate. After taking

out 25% in taxes, adjusted income is EUR 791 million, a 10.7% margin versus 4.6% currently.

Earnings power is an annual flow of funds. To convert it to an Earnings Power Value (EPV), the first step is

to divide earnings power by the cost of capital. The EPV calculated here is that of the firm as a whole. The

value of the equity is this total value less the value of the firm’s outstanding debt. Because growth has been

excluded from this valuation, and because it uses current cash flow, EPV is far less subject to error

than valuations dependent on estimating a terminal value many years into an uncertain future. Put

simply, this is the point in our analysis where we get very excited as we can explicitly demonstrate

the value unlocked by a relisting of shares from Athens to London. Let’s review a few different

scenarios:

The Greek Discount: The financing situation for both public and private companies is particularly

dire in Greece, with lending slowing to a trickle and funds deserting the market, resulting in a

punishingly high cost of capital for local companies. CCH has not gone unscathed as the company’s

current weighted average cost of capital (WACC) stands at a staggering 14.4%. Capitalizing our

adjusted income estimate above at the current WACC equates to a total enterprise value of EUR

5.5bn. Netting out debt and cash brings our total EPV to EUR 3.8 billion or $13.65 per diluted

share, a 36.7% decline from current prices. This is simply the penalty the company pays for listing in

Athens.

Peer Pressure: Global peers currently boast an average WACC of 8.5%, significantly below CCH’s

14.4% inflated cost of capital today. Assuming investors ultimately afford the company with a level

playing field, an 8.5% WACC would result in an EPV of EUR 9.3 billion, a firm value of EUR 7.6

billion, or $27.30 per diluted share – 26.6% upside from current levels.

De-Greeking Coke: We wrote extensively on Swiss interest rates earlier this year. To summarize,

they are low, very low. So low indeed, that it is worth considering the impact that a simple domicile

change may have on the cost of CCH capital and ultimately on the value of the shares. To fully

capture this premium, we recalculate CCH’s cost of capital by using the Swiss risk-free rate of 50 bps

and country premium of 10.0% - these simple changes reduce the firm’s cost of equity down from

19.0% to 9.8%, reducing their WACC to 7.4% (before the financial crisis, CCH’s WACC averaged

6.8%). The result is a firm value of EUR 10.7 billion or $32.25 per diluted share, or 49.6% upside

from current levels.

Coca-Cola Hellenic (CCH) | Page 14

In our view, the first scenario has largely been taken off the table with the move of CCH headquarters to

Switzerland. This leaves us with a base case of $27 and a bull case of $32 based upon current normalized

earnings power and assuming no growth in the future. This is even before we consider the following:

First, CCH is currently constrained by uncertain tax treatments on dividends in Greece. We can

assume that the new holding company structure and listing would permit a return to dividend

payouts and perhaps greater authority on future share repurchases. Considering the free cash flow

expected over the next few years, and assuming a targeted leverage ratio of 2.5x to 3.0x, management

would have nearly enough cash to take the company private at current levels.

And finally, assuming management is comfortable with such a targeted leverage ratio, the firm’s

WACC would drop to as low as 6.8%, resulting in additional upside to shares. Calculating firm value

using this reduced WACC results in a target value of $35.52 per share or roughly 64.7% upside from

current levels.

Bottom Line

Common wisdom today is that the really prime, risk free assets are the bonds of globally well-known, established corporate brands

that span borders of tax starved developed markets and risky often thugocracy emerging markets, capable of moving cash from one

country to another and protecting their cash flows and your investment in any market situation. Banks, high tech names, and

transportation companies don’t fit the bill as their assets are ephemeral, technology that is always moving on, or they are tied to

one place or another.

Names that seem to fit this elite bracket can be found in many countries. In the US, besides Coca-Cola there are Johnson &

Johnson, Microsoft, Exxon-Mobil, IBM, and McDonald’s and probably another five to ten names. In Europe there are

Unilever, Nestle, Siemens, Shell, British Petroleum, Bayer, and Daimler among a half dozen others. Japan has Toyota, Honda,

and Matsushita. There will always be some uncertainty as to who should be at the top of the mountain, but being ranked AAA

by S&P would be a good start. However, those that are really at the top never need to borrow any money so there aren’t any

bonds to buy. Although some compromises need to be made, these investments would seem to be far better at preserving value than

their host countries.

One company, Coca-Cola Hellenic, serves to highlight the dichotomy. The company, the second largest Coca-Cola bottler in the

world, having less than 5% of its sales in Greece with production in 27 other countries has moved its corporate headquarters to

Switzerland and its share trading to London, cutting the capitalization of the Athens equity market by about 25%. The

company’s CEO commented that the move made “clear business sense” as it would provide “flexibility to fund our future growth

on competitive terms.” What he is really saying is that his company can borrow much cheaper as a Swiss company than a Greek

one. Local companies are penalized by the credit worthiness of their sovereign, and borrowing below the sovereign rate has been

very unusual in the past. A major reason for this is that a rich company is often the best source of tax revenue for a government

desperate to find revenue. This certainly describes Greece and it is not surprising that the highest quality names in Greece,

assuming that their assets are not tied down, are leaving the country.

- John R. Taylor, Jr., Chief Investment Officer, FX Concepts

Coca-Cola Hellenic (CCH) | Page 15

We endorse Mr. Taylor’s assessment. Coca-Cola Hellenic is the highest quality name in Greece. We

believe an investment in CCH represents a compelling opportunity to own a high quality business

characterized by high customer captivity with significant economies of scale at a substantial

discount to intrinsic value. Shares have been dragged down by the weight of the Greek stock index at the

same time that revenues have suffered from volume declines in established markets, further compounded by

double-digit cost inflation which has proven to be detrimental to margins. Importantly, each of these factors

appears to be transitory. If we are right, we should get paid in two ways as both the earnings and the multiple

improve.

The coming shift in the company’s listing from Athens to London appears to have sparked a change

in investor sentiment. We expect this move to serve as an inflection point for the stock, driving

further multiple expansion over time. While current sales and future growth are largely driven by the

world’s emerging market population, investors have been unable to take their eyes off of the slow-motion

European train-wreck represented by CCH’s more mature market exposure - at least until now. We believe

the voluntary share exchange and the London listing should do the trick and properly refocus investor

attention on fundamentals.

Importantly, our investment thesis does not require an economic recovery in the European periphery to

realize the intrinsic value of CCH shares. We believe that if CCH can stabilize cash flow in established

markets, its emerging and developing markets should generate substantial and sustainable earnings

growth, driven by rising per capita beverage consumption, expanding market share and increasing

margins.

Furthermore, we believe input costs are more likely to present a tailwind than a headwind over our forecast

period. At the same time, CCH has been investing heavily in infrastructure to expand and build scale across

emerging markets, while streamlining operations across its geographical footprint. With most of the heavy

lifting now complete, and the drag from input costs sets to ease, margins should improve with

volume growth given the embedded operating leverage in the business.

Finally, given the new listing, we think the company has the capacity to further leverage the balance

sheet and the opportunity to reward shareholders with a significant return of capital. Considering the

free cash flow expected over the next few years, and assuming a targeted leverage ratio of 2.5x to 3.0x,

management would theoretically have enough cash to take the company private at prices well above recent

lows, providing investors with a comfortable floor for the shares.

Coca-Cola Hellenic (CCH) | Page 16

The Broyhill Global Thematic Portfolio is a

diversified, multi-asset class investment strategy.

Macroeconomic fundamentals and long term

investment themes drive the portfolio construction

process which is routed in a strict valuation discipline.

Embedded in our approach is a relentless focus on the

preservation of capital and the belief that risk

management begins with portfolio construction. The

objective is simply maximum total return,

commensurate with the given risk profile of global

capital markets and best suited for investors with a

long term time horizon.

The Broyhill Opportunistic Fixed Income

Portfolio is a separately-managed individual bond

portfolio focused on short duration, high-yielding

fixed income securities. The portfolio aims to

combine a high probability of the safe return of

principal with a current return superior to a portfolio

of US Treasury securities. A rigorous research process

drives the selection of only those securities that meet

our requirements based upon an independent

assessment of each issuer’s fundamental strength. The

result is a cash-generating portfolio focused only on

our highest conviction ideas.

The Broyhill High Quality Dividend Portfolio is a

concentrated equity strategy invested in a select group of

exceptional businesses judged to be competitively

entrenched market leaders, trading at reasonable prices.

Our research seeks to identify outstanding companies

with sustainable competitive advantages, rather than

speculate on mediocre businesses with uncertain futures.

The result is a portfolio of profitable businesses which

offer the potential for full participation in up markets

while mitigating the brunt of down markets, delivered to

investors in the form of attractive dividends and

consistent earnings growth.

For more information on our services, please contact:

To subscribe to our research, please click here:

Broyhill Asset Management, LLC

800 Golfview Park

Lenoir, NC 28645

(828) 758-6100

www.broyhillasset.com

www.viewfromtheblueridge.com

Broyhill Asset Management, LLC

Broyhill Asset Management is a private investment management boutique. We believe that capital preservation coupled

with consistent, compounded returns is the key to long term wealth generation. We are conservative investors for our

partners and for ourselves. Our objective is quite simple - superior risk-adjusted performance.

Since the sale of Broyhill Furniture in 1980, the Broyhill family wealth has been managed as a single family office. Today,

we are privileged to be able to offer the same level of expertise developed and refined over a quarter century within the

Broyhill Family Office, to additional families and investors. We have the highest respect for the trust our investment

partners have awarded us, and pledge to always treat non-family investments as if they were our own.

Our Services

The philosophies and strategies we endorse for our investors are only those we have developed and deployed for

ourselves. We currently offer investors three different investments, each of which is fundamentally driven by the same

objective – income generation and capital preservation. Each is consistent with our own goals and leverages our

expertise in asset allocation, in equity research and in credit analysis.

![The Research Proposal & Thesis Format [Draft] - Dec 2010](https://img.pdfslide.us/doc/110x75/577cd0a01a28ab9e7892b541/the-research-proposal-thesis-format-draft-dec-2010.jpg)