Embed Size (px)

Citation preview

SPONSORED BY

C/C/C and You...Just what DOES

property damage liability cover

or not?

10/22/2012

1

C/C/C and you ...

just what DOES property damage liability cover or not

This program is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

With special thanks to the Insurance Services Office, Inc. for advance information, continued support, and permission to use their forms and information.

So …you’ve sold a policy that provide bodily injury and property damage ….

There shouldn’t be TOO much of an issue with what constitutes covered BI …

But …what constitutes covered PD …now THAT is a horse of a different color

10/22/2012

2

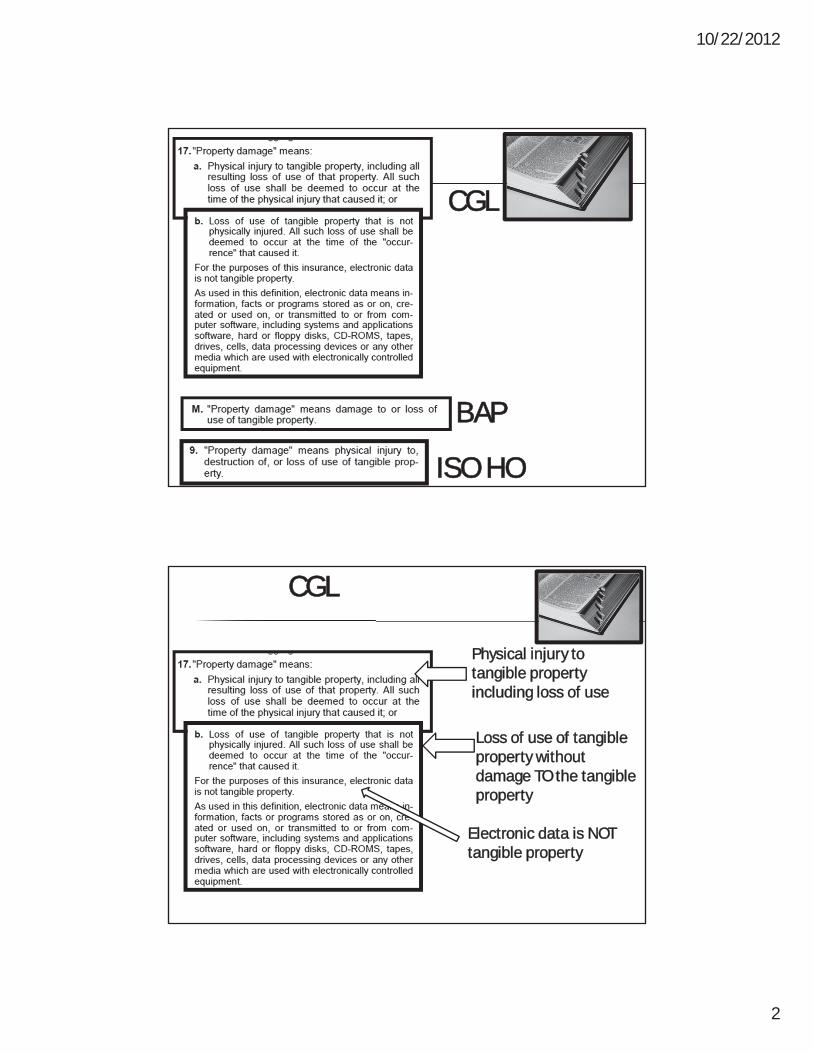

CGL

BAP

ISO HO

CGL

Physical injury to tangible property including loss of use

Loss of use of tangible property without damage TO the tangible property

Electronic data is NOT tangible property

10/22/2012

3

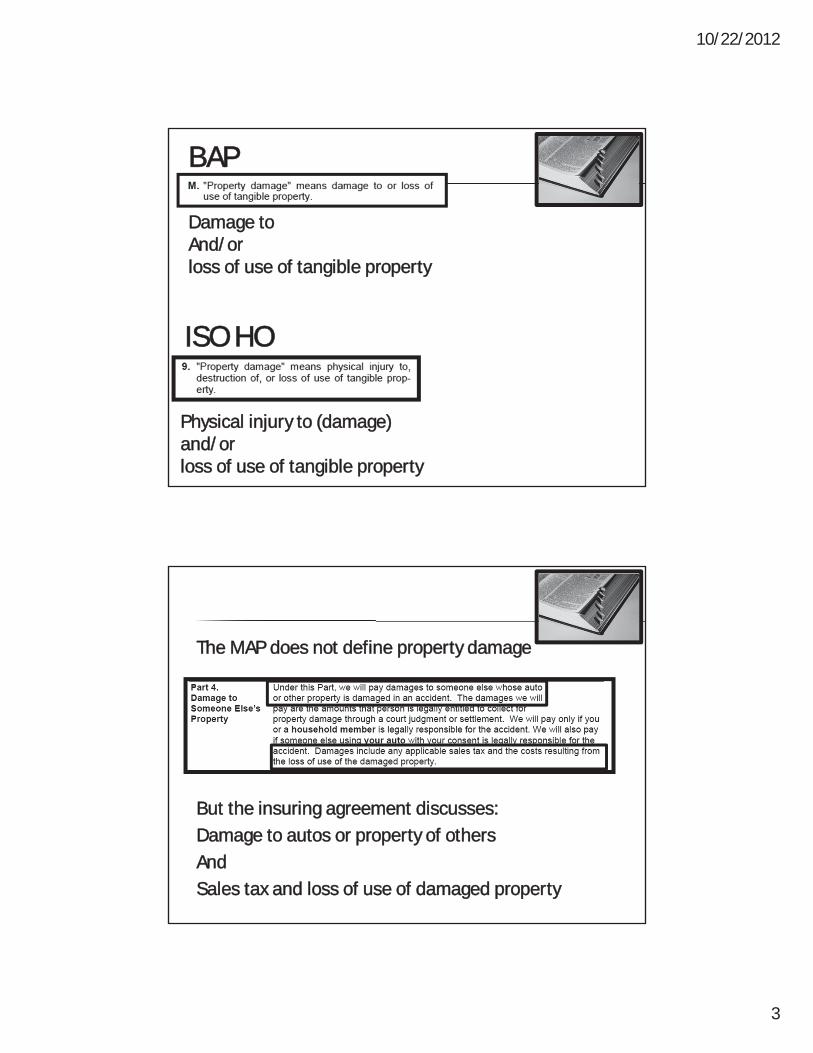

BAP

ISO HO

Damage to And/orloss of use of tangible property

Physical injury to (damage) and/orloss of use of tangible property

The MAP does not define property damage

But the insuring agreement discusses:Damage to autos or property of othersAndSales tax and loss of use of damaged property

10/22/2012

4

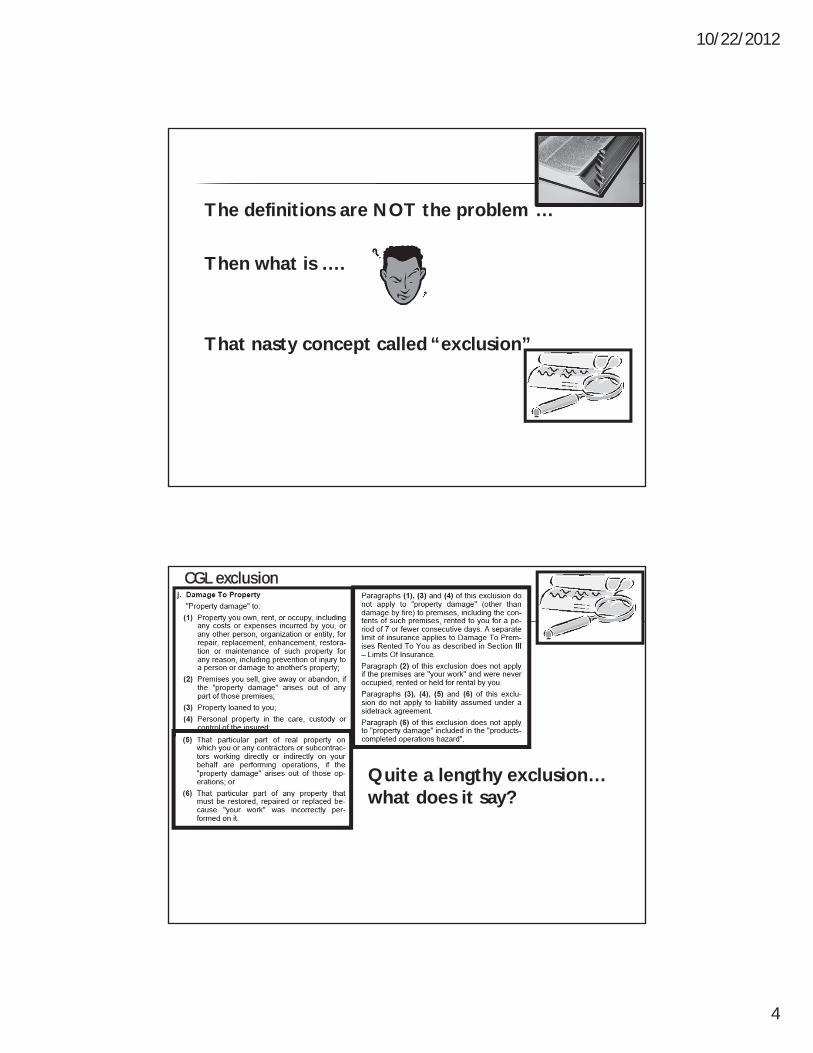

The definitions are NOT the problem …

Then what is ….

That nasty concept called “exclusion”

Quite a lengthy exclusion…what does it say?

CGL exclusion

10/22/2012

5

There is no PD to owned property…no kidding

There is no PD to real property rented or occupied by you….

So …what if your client is a tenant …would that be a problem?

CGL exclusion

Only get fire legal coverage to long term rental

CGL exclusion

10/22/2012

6

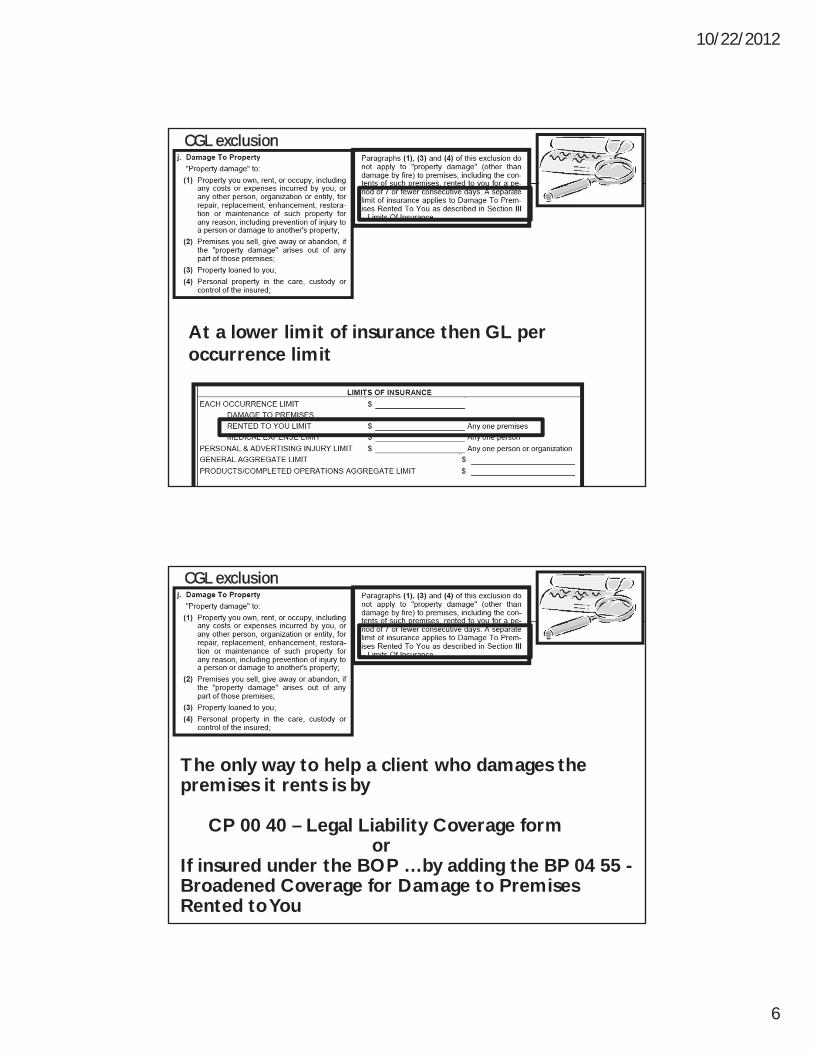

At a lower limit of insurance then GL per occurrence limit

CGL exclusion

The only way to help a client who damages thepremises it rents is by

CP 00 40 – Legal Liability Coverage formor

If insured under the BOP …by adding the BP 04 55 -Broadened Coverage for Damage to Premises Rented to You

CGL exclusion

10/22/2012

7

If employee smoking …cigarette causes fire then CGL or BOP liability would respond …for lower limit (usually start at $100,000)

If employee leaves window open and rain damages hardwood floors and walls …no coverage under CGL or unendorsed BOP

CGL exclusion

Property loaned to insured or in c/c/c of insured isNOT covered ….

Consider contractors borrowing mobile equipment

Insured who repairs or cleans or otherwise has other people’s personal property in its care

CGL exclusion

10/22/2012

8

These clients need inland marine coverage for damage to property of others …or company specific endorsement to CGL or BOP

CGL exclusion

Carpenter hired to remodel doorway and damage it during process

CGL exclusion

10/22/2012

9

Painter hired to buy and paint room “rust” …and paints it red….

CGL exclusion

If what your client built or repaired … damaged itself …or damage arose out of what wasdone …after work was complete …too bad

CGL exclusion - more

10/22/2012

10

After explaining the liability coverage to your client the contractor… he asks

What would happen if I built a deck for someone andit collapses 3 weeks after I finished it.

It collapses during a big party that the client is having … and people are injured as well as damage to the house and, of course, the deck.

CGL questions from an insured

The good news …CGLor BOP … CGL language:

BI and PD to others is covered if insured is legally obligated

And NO exclusions

CGL questions

10/22/2012

11

Injury to people when deck collapsed is covered as there are no exclusions

Damage to the house is covered as job was done

house not being occupied by client

Definition of property damage would apply

CGL questions

The damage to the deck will NOT becovered per the following exclusion

(and definition):

CGL questions

10/22/2012

12

Your client then questions …

What if he damages the house to which he is attaching the deck … while he is actually building the deck?

Will his CGL pay for that damage?

CGL questions

The house belonging to someone else WAS damaged … during the “operations” … but ….PD exclusion J(5) will be a problem

Since the part of the house that was having the deckattached to it was damaged … the exclusion for “particular part of REAL property” where you are performing your operations … will apply.

CGL questions

10/22/2012

13

He then asks …

What if he is remodeling a kitchen and while bringing the necessary lumber for the kitchen renovations from his pickup truck …up through the front door and through the living room ….he gouges the client’s living room walls. He must bring the materials in this way to get to the kitchen.

Will the damage to the living room walls be covered under his CGL?

CGL questions

Actually … no …

Damage done while unloading his truck by hand is excluded under the GL coverage …The following is language from the ISO CGL … but the ISO CGL hasthe same language…

CGL questions

10/22/2012

14

Both the BOP and the GL have the following definitions:

Your client has a F-250 pickup …which is definitely registered and definitely an “auto”

CGL questions

Unloading by hand or hand truck (dolly) is considered BAP … unloading by a non-attached mechanical device such as forklift or crane is considered CGL …

Since he was unloading by hand … the CGL considers this an “excluded” unloading situation of an excluded vehicle …

Coverage must be found elsewhere …not CGL

10/22/2012

15

GOOD NEWS … if he has a BAP …His BAP liability coverage states:

But ..it also has exclusions:

BAP questions

The BAP restriction for loading/unloadingfits the CGL/BOP liability like a “glove” …

BAP questions

10/22/2012

16

The BAP provides coverage for BI/PD arising out of the materials and supplies the second they are being loaded …if loaded by hand,

dolly

or

device attached to the truck

BAP questions

The BAP excludes unloading by a mechanical device that is NOT attached to the truck.

Since he unloaded by hand … the BAP will respond to the claim.

BAP questions

10/22/2012

17

What if he has a MAP class 30instead of a BAP…will MAP respond?

MAP has no definition of:

“property damage”“loading/unloading”

MAP questions

Good news …there is no exclusion

and certainly the insured IS legally responsible!

MAP questions

10/22/2012

18

Don’t listen to the …it’s not an auto claim … or too far from the truck …

MA common lawThe “complete operations” rule looks at the TOTALITY of the action … from beginning to end or when are you “done”.

In Busch & Company of Massachusetts, Inc v. Liberty Mutual 339 Mass 239 and F.W. Woolworth Company & Others) v. LumbermensMutual 355 Mass 211 (1969) the court invoked the “complete operation rule”

MAP questions

Your insured has another question …

What if the materials and supplies he bought for the job fall out of the back of the truck and are damaged …

will the MAP or BAP pay for damage to the materials and supplies?

Would it make a difference if the client had purchased them and the materials and supplies were not his?

MAP/BAP questions

10/22/2012

19

BAP

Excludes damage to property Owned OR transported by insured ….

Or otherwise in the insured’s C/C/C

MAP/BAP questions

MAP

Excludes damage to property Owned by insured ….

Or rented to Or in “care” of …an insured

MAP/BAP questions

10/22/2012

20

How do you cover this exposure???

One needs inland marine coverage …

Or if it is a PERSONAL issue …not business the HO policy could respond under Coverage C Personal property

MAP/BAP questions

Property damage … and the CGL …or not

A contractor was hired to power wash a house.

In doing so, the exterior of the house was damaged.

The commercial general liability carrier denied coverage because of the "your work" exclusions.

I don’t agree. I believe that the resulting damage to the house should be covered and only the cost of re-doing the power wash should be excluded.

Can you clarify this for me?

10/22/2012

21

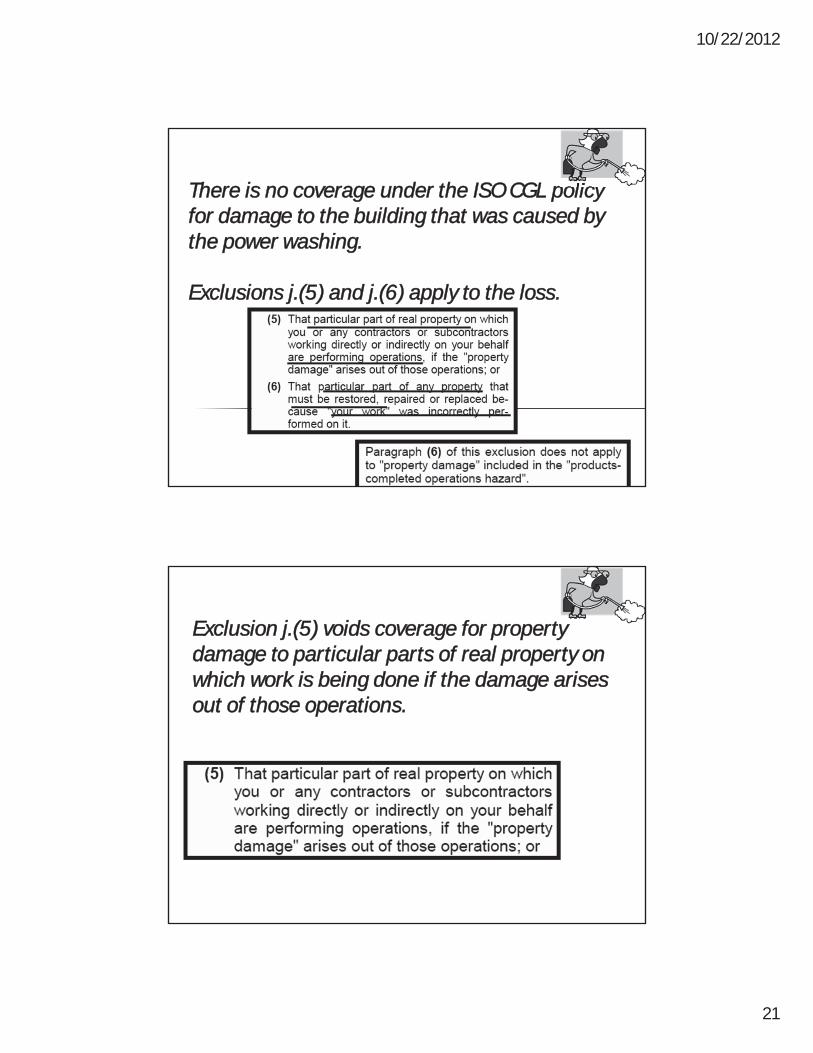

There is no coverage under the ISO CGL policy for damage to the building that was caused by the power washing.

Exclusions j.(5) and j.(6) apply to the loss.

Exclusion j.(5) voids coverage for property damage to particular parts of real property on which work is being done if the damage arises out of those operations.

10/22/2012

22

Exclusion j.(6) excludes coverage for the particular part of any property that must be restored, repaired, or replaced because "your work" was incorrectly performed on it.

The work (power washing) being performed damaged the building.

There is no separation between the damage and the power washing.

This appears to be a classic case of faulty workmanship, which the CGL is not designed to cover.

However, if the building were to collapse after the work had been completed and turned over to the owner,

exclusions j.(5) and (6) would not apply if, as they are OPERATIONS exclusions ….

10/22/2012

23

HO and c/c/c

Jack Sprat just signed a 12-month lease for a Back Bay apartment. After the year is up he will be on assignment in Saudi Arabia for 2 years. He has decided to lease apartment furniture for the next 12 months also.

The landlord had him sign a lease that “holds the landlord” harmless for all damages to the rented apartment

The lease he signed for the furniture leasing company requires that he return the furniture at the end of the lease in “similar condition” allowing only for minor wear and tear.

The furniture leasing company requires Jack to purchase insurance protecting the furniture

HO and c/c/c

10/22/2012

24

Can Jack insure leased contents ?

Yes

Coverage C applies to

HO and c/c/c

Owned and/or used property is covered

Leased property is property that you are “using”

Jack must be aware of Coverage C limitations and exclusions

HO and c/c/c

10/22/2012

25

We should recommend that he purchase the HO 04 90 Replacement cost endorsement (whether you sell the HO-91 or HO-2000/HO-2011 –contents is adjusted on an ACV basis)

Replacement cost will be paid for losses to covered property

Jack should read his lease to verify that replacement cost is acceptable –a lease agreement might also have “administration” fees if property is damaged and similar property can not be produced

HO and c/c/c

The HO-4 is a NAMED peril policy with only 16 perils. Jack is probably responsible for ALL loss to leased property.

HO-91 policy

1) “Open peril” special form tenants coverage is NOT available (at least according to ISO…company can

file anything it wants)

2) Warn Jack of the peril limitations in his policy

3) Again, we should make sure he is aware that he might be responsible for ALL damage to the leased property and only certain types of damage can be insured

HO and c/c/c

10/22/2012

26

ISO HO-2000/HO-2011 program has a Special Form Endorsement for the HO-4

1) HO 05 24 Special Personal Property Coverage Endorsement

2) Open peril coverage certain to exclusions as found in the HO-15 Special Personal Property Coverage Endorsement used with HO-3 or HO 17 31 Special Personal Property Coverage Endorsement used with the HO-6

3) Optional endorsement subject to carrier underwriting

HO and c/c/c

Jack is running the water in his bathtub for a nice long warm bath. The phone rings. His girlfriend’s car broke down on the highway and she needs him to come IMMEDIATELY.

He grabs his car keys and dashes out the door. Four hours later he returns home.

HO and c/c/c

10/22/2012

27

When he opens the door to his apartment he sees a layer of water all over the dining room hardwood floor and the living room rug. He runs into the bathroom to shut off the bathtub water.

It seems the face cloth he always leaves over the bath tub faucet acted like a stopper to the overflow outlet located right below the faucet.

HO and c/c/c

Water had been running for FOUR hours.

Shortly after entering his apartment the phone rang. It was the tenant below him screaming about water pouring through the ceiling. He had been using buckets to catch the water.

HO and c/c/c

10/22/2012

28

The landlord was informed and he reported to his insurance company. Theinsurance company paid the

claim and then sent a letter of subrogation to Jack. (Can the landlord’s insurance company require that Jack pay for the water damage?)

The damage to Jack’s apartment alone was $5,000. The damage to the apartment below was another $3,000.

What will Jack’s insurance carrier do?

HO and c/c/c

The lease that Jack signed did NOT have a waiver of subrogation clause.

Therefore, any damage caused by Jack’s negligence will ultimately be his responsibility

The Landlord’s insurance carrier has every right to go after the negligent party

HO and c/c/c

10/22/2012

29

WhatWillJack’sHO-4do?

HO and c/c/c

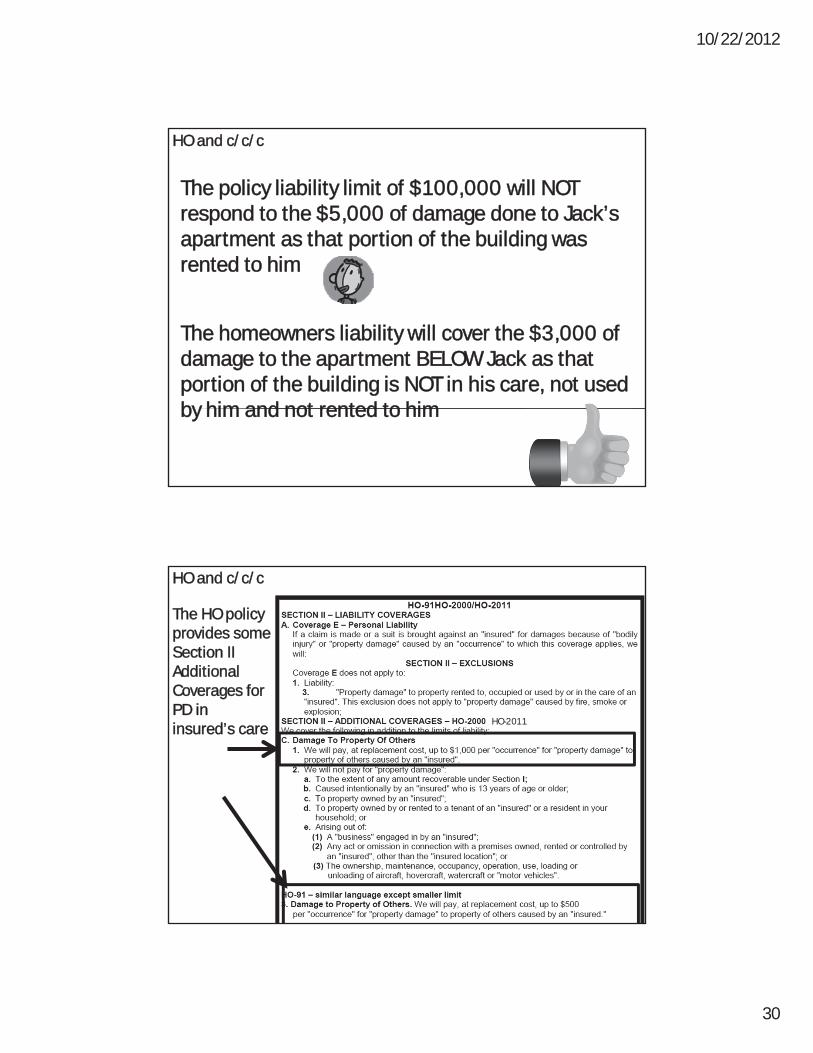

The HO policy PD liability coverage hasexclusion for PD to property in your care, rented or used by you unlessdamaged by fire, smoke or explosion

HO and c/c/c

10/22/2012

30

The policy liability limit of $100,000 will NOT respond to the $5,000 of damage done to Jack’s apartment as that portion of the building was rented to him

The homeowners liability will cover the $3,000 of damage to the apartment BELOW Jack as that portion of the building is NOT in his care, not used by him and not rented to him

HO and c/c/c

The HO policy provides some Section II Additional Coverages forPD in insured’s care

HO-2011

HO and c/c/c

10/22/2012

31

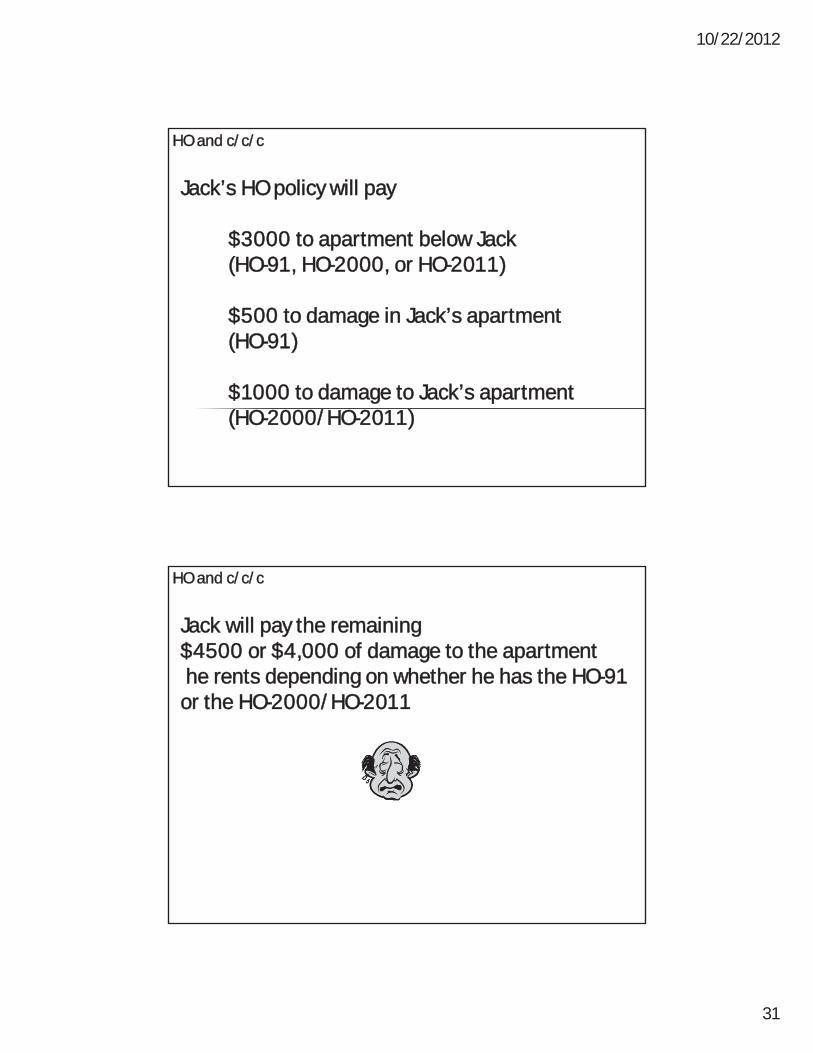

Jack’s HO policy will pay

$3000 to apartment below Jack (HO-91, HO-2000, or HO-2011)

$500 to damage in Jack’s apartment (HO-91)

$1000 to damage to Jack’s apartment (HO-2000/HO-2011)

HO and c/c/c

Jack will pay the remaining $4500 or $4,000 of damage to the apartmenthe rents depending on whether he has the HO-91

or the HO-2000/HO-2011

HO and c/c/c

10/22/2012

32

Legal Liability Coverage Form CP 00 40

1. This coverage form will allow Jack to buy coverage for damage to the apartment he rents

2. He can buy special form coverage for damage to the apartment due to Jack’s negligence.

Any special form peril type of damage that Jack was negligent in causing to the rented apartment will be covered

The policy will ONLY respond when Jack is negligent

HO and c/c/c

Reviewing leases and contracts

1. Would you sell a HO-6 to someone without reviewing the BYLAWS?

2. Selling insurance to our clients who sign leases and contracts WITHOUT reviewing these leases and contracts to identify the potential exposures is dangerous

HO and c/c/c